CORPORATE PBOC CREDIT REPORT - ENGLISH

美国反舞弊性财务报告委员会发起组织的报告【外文翻译】

本科毕业论文(设计)外文翻译外文题目Committee of sponsoring organizationsof the treadway Commission 外文出处Enterprise risk management外文作者Committee of sponsoring organizations 原文:Committee of sponsoring organizations of the treadway commission Organizational overviewCOSO was formed in 1985 to sponsor the National Commission on Fraudulent Financial Reporting (the Treadway Commission). The Treadway Commission was originally jointly sponsored and funded by five main professional accounting associations and institutes headquartered in the United States: the American Institute of Certified Public Accountants (AICPA), American Accounting Association (AAA), Financial Executives International (FEI), Institute of Internal Auditors (IIA) and the Institute of Management Accountants(IMA). The Treadway Commission recommended that the organizations sponsoring the Commission work together to develop integrated guidance on internal control. These five organizations formed what is now called the Committee of Sponsoring Organizations of the Treadway Commission.The original chairman of the Treadway Commission was James C. Treadway, Jr., Executive Vice President and General Counsel, Paine Webber Incorporated and a former Commissioner of the U.S. Securities and Exchange Commission. Hence, the popular name "Treadway Commission". Currently, David L. Landsittel replaced Larry E. Rittenberg as the COSO Chairman.HistoryDue to questionable corporate political campaign finance practices and foreigncorrupt practices in the mid -1970s, the U.S. Securities and Exchange Commission (SEC) and the U.S. Congress enacted campaign finance law reforms and the 1977 Foreign Corrupt Practices Act(FCPA) which criminalized transnational bribery and required companies to implement internal control programs. In response, the Treadway Commission, a private-sector initiative, was formed in 1985 to inspect, analyze, and make recommendations on fraudulent corporate financial reporting.The Treadway Commission studied the financial information reporting system over the period from October 1985 to September 1987 and issued a report of findings and recommendations in October 1987 titled Report of the National Commission on Fraudulent Financial Reporting. As a result of this initial report, the Committee of Sponsoring Organizations (COSO) was formed and it retained Coopers & Lybrand, a major CPA firm, to study the issues and author a report regarding an integrated framework of internal control.In September 1992, the four volume report entitled Internal Control— Integrated Framework was released by COSO and later re-published with minor amendments in 1994. This report presented a common definition of internal control and provided a framework against which internal control systems may be assessed and improved. This report is one standard that U.S. companies use to evaluate their compliance with FCPA. According to a poll by CFO Magazine released in 2006, 82% of respondents claimed t hey used COSO’s framework for internal controls. Other frameworks used by respondents included COBIT, AS2 (Auditing Standard No. 2, PCAOB), and SAS 55/78 (AICPA).Internal control - integrated frameworkKey concepts of the COSO frameworkThe COSO framework involves several key concepts:∙Internal control is a process. It is a means to an end, not an end in itself.∙Internal control is affected by people. It’s not merely policy, manuals, and forms, but people at every level of an organization.∙Internal control can be expected to provide only reasonable assurance, not absolute assurance, to an entity’s management and board.Internal control is geared to the achievement of objectives in one or more separate but overlapping categories.Use of the capability maturity modelThe capabilities of an organization in relation to the COSO model could be assessed based on universal states or plateaus that organizations typically target. The descriptions are incremental.The capability descriptions are based on evolution toward generally recognized best practices. Each organization determines which level of "maturity" would be the most appropriate in support of its business needs, priorities and availability of resources. A rating system of “0” to “5” is used. A rating of “5” does not necessarily mean “goodness”, but rather, maturity of capability. The ideal maturity rating for any area is dependent on the needs of the organization. The different and progressive plateaus are: 0 Non-existent when:The organization lacks procedures to monitor the effectiveness of internal controls. Management internal control reporting methods are absent. There is a general unawareness of IT operational security and internal control assurance. Management and employees have an overall lack of awareness of internal controls.1 Initial/Ad Hoc when:Management recognizes the need for regular IT management and control assurance. Individual expertise in assessing internal control adequacy is applied on an ad hoc basis. IT management has not formally assigned responsibility for monitoring the effectiveness of internal controls. IT internal control assessments are conducted as part of traditional financial audits, with methodologies and skill sets that do not reflect the needs of the information services function.2 Repeatable but Intuitive when:The organization uses informal control reports to initiate corrective action initiatives. Internal control assessment is dependent on the skill sets of key individuals. The organization has an increased awareness of internal control monitoring. Information service management performs monitoring over the effectiveness of what it believes are critical internal controls on a regular basis. Methodologies and tools formonitoring internal controls are starting to be used, but not based on a plan. Risk factors specific to the IT environment are identified based on the skills of individuals.3 Defined when:Management supports and institutes internal control monitoring. Policies and procedures are developed for assessing and reporting on internal control monitoring activities. An education and training program for internal control monitoring is defined. A process is defined for self-assessments and internal control assurance reviews, with roles for responsible business and IT managers. Tools are being utilized but are not necessarily integrated into all processes. IT process risk assessment policies are being used within control frameworks developed specifically for the IT organization. Process-specific risks and mitigation policies are defined.4 Managed and Measurable when:Management implements a framework for IT internal control monitoring. The organization establishes tolerance levels for the internal control monitoring process. Tools are implemented to standardize assessments and automatically detect control exceptions. A formal IT internal control function is established, with specialized and certified professionals utilizing a formal control framework endorsed by senior management. Skilled IT staff members are routinely participating in internal control assessments. A metrics knowledge base for historical information on internal control monitoring is established. Peer reviews for internal control monitoring are established.5 Optimized when:Management establishes an organization wide continuous improvement program that takes into account lessons learned and industry best practices for internal control monitoring and reporting. The organization uses integrated and updated tools, where appropriate, that allow effective assessment of critical IT controls and rapid detection of IT control monitoring incidents. Knowledge sharing specific to the information services function is formally implemented. Benchmarking against industry standards and good practices is formalized.Definition of internal control and framework objectivesThe COSO framework defines internal control as a process, effected by an entity’sboard of directors, management and other personnel, designed to provide "reasonable assurance" regarding the achievement of objectives in the following categories: ∙Effectiveness and efficiency of operations∙Reliability of financial reporting∙Compliance with applicable laws and regulationsThe five framework componentsThe COSO internal control framework consists of five interrelated components derived from the way management runs a business. According to COSO, these components provide an effective framework for describing and analyzing the internal control system implemented in an organization as required by financial regulations (see Securities Exchange Act of 1934, Section 240 15d-15). The five components are the following:Control environment:The control environment sets the tone of an organization, influencing the control consciousness of its people. It is the foundation for all other components of internal control, providing discipline and structure. Control environment factors include the integrity, ethical values, management's operating style, delegation of authority systems, as well as the processes for managing and developing people in the organization.Risk assessment:Every entity faces a variety of risks from external and internal sources that must be assessed. A precondition to risk assessment is establishment of objectives and thus risk assessment is the identification and analysis of relevant risks to the achievement of assigned objectives. Risk assessment is a prerequisite for determining how the risks should be managed.Control activities: Control activities are the policies and procedures that help ensure management directives are carried out. They help ensure that necessary actions are taken to address the risks that may hinder the achievement of the entity's objectives. Control activities occur throughout the organization, at all levels and in all functions. They include a range of activities as diverse as approvals, authorizations, verifications, reconciliations, reviews of operating performance, security of assets and segregation of duties.Information and communication:Information systems play a key role in internal control systems as they produce reports, including operational, financial and compliance-related information, that make it possible to run and control the business. In a broader sense, effective communication must ensure information flows down, across and up the organization. For example, formalized procedures exist for people to report suspected fraud. Effective communication should also be ensured with external parties, such as customers, suppliers, regulators and shareholders about related policy positions.Monitoring: Internal control systems need to be monitored—a process that assesses the quality of the system's performance over time. This is accomplished through ongoing monitoring activities or separate evaluations. Internal control deficiencies detected through these monitoring activities should be reported upstream and corrective actions should be taken to ensure continuous improvement of the system. LimitationsInternal control involves human action, which introduces the possibility of errors in processing or judgment. Internal control can also be overridden by collusion among employees (see separation of duties) or coercion by top management.CFO magazine reported that companies are struggling to apply the complex model provided by COSO. “One of the biggest problems: limiting internal audits to one of the three key objectives of the framework. In the COSO model, those objectives are applied to five key components (monitoring, information and communication, control activities, risk assessment, and control environment). Given the number of possible matrices, it's not surprising that the number of audits can get out of hand.” CFO magazine continued by stating, that many organization are creating their own risk-and-control matrix by taking the COSO model and altering it to focus on the components that relate directly to Section 404 of the Sarbanes-Oxley Act.Source:Enterprise risk management,2004.译文:美国反舞弊性财务报告委员会发起组织的报告组织概述COSO是成立于1985年的美国反虚假财务报告委员会(特雷德韦委员会)的发起组织委员会。

银监会英语考试银行英语词汇

银监会英语考试银行英语词汇Banking English Vocabulary for the China Banking Regulatory Commission English ExamIntroduction:Banking industry professionals in China need a strong command of English to communicate effectively in a globalized financial environment. The China Banking Regulatory Commission (CBRC) requires its employees to possess English language skills, including a good understanding of banking-specific vocabulary. This article provides a comprehensive overview of essential banking English vocabulary that will help CBRC candidates excel in the English proficiency test.1. Banking Basics1.1 Deposit Accounts- Savings Account- Current Account/Checking Account- Fixed Deposit Account- Time Deposit Account- Certificate of Deposit (CD)1.2 Lending and Borrowing - Loan- Mortgage- Personal Loan- Business Loan- Credit Card1.3 Investments- Stocks- Bonds- Mutual Funds- Portfolio- Risk Management2. Financial Institutions 2.1 Commercial Banks- Retail Banks- Commercial Lending- Corporate Banking- Investment Banking2.2 Central Banks- Monetary Policy- Interest Rates- Money Supply- Open Market Operations2.3 Investment Banks- Mergers and Acquisitions- Underwriting- Initial Public Offering (IPO)- Securities Trading3. Regulatory Bodies3.1 China Banking Regulatory Commission (CBRC) - Banking Regulations- Supervision and Examination- Enforcement Actions- Consumer Protection3.2 Financial Stability Board (FSB)- International Banking Regulations- Basel III- Systemically Important Financial Institutions (SIFI) 3.3 International Monetary Fund (IMF)- Economic Surveillance- Financial Assistance- Exchange Rate Policies- Global Financial Stability Report4. Financial Concepts4.1 Interest- Simple Interest- Compound Interest- Annual Percentage Rate (APR)- Prime Rate4.2 Risk- Credit Risk- Market Risk- Liquidity Risk- Operational Risk4.3 Financial Statements- Balance Sheet- Income Statement- Cash Flow Statement- Statement of Retained Earnings5. Business Correspondence5.1 Emails and Memos- Formal Greetings and Closings - Clear and Concise Content- Actionable Language5.2 Reports and Presentations- Executive Summaries- Visual Aids- Data Analysis and Interpretation6. Customer Service6.1 Opening an Account- Account Application- Identification Documentation- Account Terms and Conditions6.2 Handling Inquiries- Account Balance- Transaction History- Interest Rates and Fees6.3 Resolving Complaints- Active Listening- Empathy and Understanding- Prompt and Effective SolutionsConclusion:Mastering banking English vocabulary is crucial for success in the CBRC English exam. This article has provided a comprehensive overview of key banking terms and concepts that will help candidatesprepare effectively. By incorporating this vocabulary into their study plan, CBRC candidates will increase their chances of achieving excellent results and advancing their career in the banking industry.。

企业年度报告证明英文

企业年度报告证明英文*Introduction*In this annual report, we aim to provide a comprehensive overview and assessment of our company's performance during the past year. Our company has strived to remain competitive in an ever-evolving market, and this report serves as evidence of our success and dedication.*Financial Performance*Our company has achieved remarkable growth in terms of revenue and profitability. The total revenue for the year has increased by 20% compared to the previous year, reaching an all-time high of 100 million. This growth can be attributed to our efforts in expanding our customer base, improving customer satisfaction, and introducing innovative products.Notably, our profit margin has also witnessed a significant improvement, increasing by 15% compared to the previous year. This improvement can be attributed to cost management strategies and increased productivity. Cash flow management has been another key focus for our company. We have successfully increased our operating cash flow by streamlining our operations and implementing effective accounting practices. This has allowed us to invest in research and development, expand our production capacity, and fund strategic acquisitions in line with our long-term growth plans.*Market Analysis*Our company operates in a highly competitive market where constant innovation and adaptation are essential. Despite these challenges, we have successfully maintained our market share and even gained new ones, thanks to the implementation of effective marketing strategies.In terms of market growth, our company has consistently outperformed the industry average. This can be attributed to our ability to identify emerging market trends and respond swiftly with appropriate products and services. Additionally, our strong brand reputation has allowed us to attract new customers and retain existing ones.*Corporate Social Responsibility*As a responsible corporate citizen, our company is committed to making a positive impact on society and the environment. In the past year, we have actively participated in various social and environmental initiatives. We have implemented sustainable practices throughout our supply chain, reducing our carbon footprint and waste production. We have also supported local communities by volunteering our time and resources in education and healthcare projects.*Future Outlook*Looking ahead, we are confident in our ability to sustain and build upon our success. With a solid financial foundation, a strong market presence, and a dedicated workforce, our company is well-positioned for futuregrowth.To further drive growth, we will continue to invest in research and development to bring innovative and advanced products to the market. Additionally, we will focus on expanding our global reach by exploring new market opportunities and building strategic partnerships.*Conclusion*In conclusion, this annual report provides a comprehensive overview of our company's performance and achievements for the past year. Our strong financial performance, market growth, and commitment to corporate social responsibility are evidence of our dedication to success. We look forward to another year of growth and continued success.。

征信报告 英文模板

征信报告英文模板Personal InformationName: [Full Name]Date of Birth: [Date of Birth]Social Security Number: [SSN]Address: [Current Address]Phone Number: [Phone Number]Credit SummaryThe credit report provides a comprehensive overview of the individual’s credit history, including credit accounts, payment history, and public records. This report is generated based on data obtained from credit bureaus and other financial institutions. The information presented in this report is accurate as of [Date]. Summary of AccountsThe individual possesses a total of [Number of Accounts] credit accounts, including credit cards, loans, and mortgages. The following is a summary of the various accounts:1. Credit Card Accounts:- [Credit Card Company]: [Account Number]- [Credit Card Company]: [Account Number]2. Loan Accounts:- [Lending Institution]: [Loan Type]- [Lending Institution]: [Loan Type]3. Mortgage Accounts:- [Mortgage Lender]: [Mortgage Type]- [Mortgage Lender]: [Mortgage Type]Payment HistoryThe individual’s payment history reflects their ability to manage debt responsibly and make timely payments. A positive payment history contributes to a higher credit score. The following is an overview of the payment history:1. Credit Card Accounts:- [Credit Card Company]: [Account Number]- Date of Last Payment Made: [Date]- Payment Status: [Current/Overdue]- Amount of Credit Utilized: [Credit Utilization Rate]- Payment History: [Number of On-Time Payments]2. Loan Accounts:- [Lending Institution]: [Loan Type]- Date of Last Payment Made: [Date]- Payment Status: [Current/Overdue]- Outstanding Balance: [Amount]- Payment History: [Number of On-Time Payments]3. Mortgage Accounts:- [Mortgage Lender]: [Mortgage Type]- Date of Last Payment Made: [Date]- Payment Status: [Current/Overdue]- Outstanding Balance: [Amount]- Payment History: [Number of On-Time Payments]Public RecordsPublic records include legal actions, such as bankruptcies, tax liens, and judgments, which may negatively impact an individual's creditworthiness. The following information denotes any public records associated with the individual:1. Bankruptcies: [Number of Bankruptcies]- [Details of Bankruptcy Case]2. Tax Liens: [Number of Tax Liens]- [Details of Tax Liens]3. Judgments: [Number of Judgments]- [Details of Judgments]Credit ScoreBased on the information provided in this report, the individual's credit score is [Credit Score]. The credit score is a numerical representation of an individual's creditworthiness and is used by lenders to assess the risk associated with extending credit.A higher credit score indicates a lower credit risk. ConclusionThis credit report serves as a detailed summary of the individual's credit history, encompassing the various credit accounts, payment history, and any public records. It is essential to review this report periodically to ensure accuracy and to identify any potential discrepancies that require attention.Please note that this report is for informational purposes only and does not constitute financial advice. It is important to consult with a financial professional regarding specific credit decisions.If you have any further questions or require additional information, please contact [Contact Information].*Please keep this report confidential and secured.*。

述职报告英文版

述职报告英文版英文回答:Performance Evaluation Report。

Executive Summary。

As the esteemed [Insert your position], I am honored to present my performance evaluation report for the period [Insert time period]. During this time, I have consistently exceeded expectations in my role and made significant contributions to the success of the organization. My unwavering commitment to excellence, coupled with my proactive approach and ability to deliver exceptional results, has been instrumental in driving growth and achieving our strategic objectives.Key Accomplishments。

1. Spearheaded the implementation of a new CRM system,resulting in a 20% increase in sales conversion rates and a 15% reduction in customer service response times.2. Led the development of a comprehensive marketing campaign, which generated a 30% increase in website traffic and a 25% increase in qualified leads.3. Successfully negotiated a major contract, securing a 10% increase in revenue and expanding our market share in a key industry sector.4. Mentored and developed a team of high-performing individuals, who have consistently exceeded their targets and contributed to the overall success of the organization.5. Actively participated in industry events and conferences, sharing our expertise and establishing the company as a thought leader in our field.Skill Development and Training。

公司年度财务报告(中英文对照)模板(2023范文免修改)

公司年度财务报告(中英文对照)模板摘要本文档为公司年度财务报告的模板,包含中英文对照的版本,旨在为公司提供一个方便、清晰的财务报告撰写参考。

目录1. [公司概述](公司概述)2. [财务指标](财务指标)3. [利润表](利润表)4. [资产负债表](资产负债表)5. [现金流量表](现金流量表)6. [附注](附注)1. 公司概述本部分提供公司的背景信息和概述,包括公司名称、注册地、主要业务领域、经营范围等内容。

1.1 公司名称公司名称:[公司名称]1.2 注册地公司注册地:[注册地]1.3 主要业务领域公司主要从事的业务领域:[主要业务领域]1.4 经营范围公司经营范围:[经营范围]2. 财务指标本部分列出公司在过去年度的财务指标,包括营业收入、净利润、资产总额等。

财务指标 201X年 201X年 -营业收入 [金额] [金额] -净利润 [金额] [金额] -资产总额 [金额] [金额] -3. 利润表本部分提供公司在过去年度的利润表,包括营业收入、销售成本、营业利润等。

项目 201X年 201X年 --营业收入 [金额] [金额] -销售成本 [金额] [金额] -营业利润 [金额] [金额] -净利润 [金额] [金额] -4. 资产负债表本部分提供公司在过去年度的资产负债表,包括资产总额、负债总额、所有者权益等。

项目 201X年 201X年 ---资产总额 [金额] [金额] -负债总额 [金额] [金额] -所有者权益 [金额] [金额] -5. 现金流量表本部分提供公司在过去年度的现金流量表,包括经营活动现金流量、投资活动现金流量、筹资活动现金流量等。

项目 201X年 201X年 --经营活动现金流量 [金额] [金额] -投资活动现金流量 [金额] [金额] -筹资活动现金流量 [金额] [金额] -净现金流量 [金额] [金额] -6. 附注本部分提供公司年度财务报告的附注说明,包括重要会计政策、关联交易、风险和挑战等。

商业银行英文作文

商业银行英文作文英文:As a commercial bank, our main goal is to provide financial services to our customers. We offer a wide range of products and services, including checking and savings accounts, loans, credit cards, and investment options.One of the most important services we offer is lending. We provide loans to individuals and businesses for various purposes, such as buying a house or starting a business. We analyze the creditworthiness of the borrower and determine the interest rate and terms of the loan. It is importantfor us to manage the risks associated with lending, so we carefully evaluate each loan application.Another important service we offer is deposit-taking. We accept deposits from individuals and businesses and pay interest on those deposits. This allows us to use the funds to provide loans and other services to our customers. Wealso offer various types of accounts, such as checking accounts, savings accounts, and certificates of deposit.In addition to these services, we also offer credit cards to our customers. Our credit cards come with various benefits, such as cashback rewards and travel perks. We also offer investment options, such as mutual funds and retirement accounts, to help our customers grow their wealth.Overall, our goal is to provide our customers with the financial services they need to achieve their goals. We strive to offer competitive rates, excellent customer service, and innovative products and services.中文:作为一家商业银行,我们的主要目标是为客户提供金融服务。

国外上市公司资产评估报告英文版

国外上市公司资产评估报告英文版1. IntroductionWhen it comes to investing in foreign companies, it is essential to have access to comprehensive and reliable information about their assets, including their valuation reports. In this article, we will explore the importance of having access to English-language asset evaluation reports for foreign public companies and the impact it can have on investment decisions.2. The Importance of Access to English-language Asset Evaluation Reports2.1 Understanding the Asset Valuation ProcessIn order to make informed investment decisions, it is crucial to have a clear understanding of how the assets of a company are evaluated. Access to English-language asset evaluation reports provides investors with the necessary information to assess the value of a company's assets and make informed decisions.2.2 Transparency and AccountabilityEnglish-language asset evaluation reports contribute to the transparency and accountability of foreign public companies. By providing access to these reports, companies demonstrate theircommitment to providing investors with clear and reliable information, which in turn can build trust and confidence among potential investors.2.3 Facilitating Due DiligenceFor investors conducting due diligence on foreign companies, access to English-language asset evaluation reports is crucial. These reports provide detailed information about the company's assets, allowing investors to assess the company's financial health and make informed investment decisions.3. The Impact of English-language Asset Evaluation Reports on Investment Decisions3.1 Informed Decision MakingBy having access to English-language asset evaluation reports, investors are able to make more informed investment decisions. These reports provide valuable insights into the value of a company's assets, allowing investors to assess the company's financial position and potential for growth.3.2 Risk ManagementEnglish-language asset evaluation reports also play a key role in risk management for investors. By gaining a better understanding of a company's assets, investors are better equipped to assess the risks associated with their investmentand take the necessary precautions.3.3 Market ConfidenceAccess to English-language asset evaluation reports can also contribute to market confidence. When investors have access to comprehensive and reliable information about a company's assets, they are more likely to have confidence in the company's financial stability and potential for growth, which can have a positive impact on the company's stock performance.4. Personal Perspective and UnderstandingAs a writer who regularly helps clients evaluate and understand asset valuation reports for foreign public companies, I have seen first-hand the impact that access to English-language reports can have on investment decisions. The ability to access clear and reliable information about a company's assets is invaluable for investors, and can significantly impact their confidence and decision-making process.5. ConclusionIn conclusion, access to English-language asset evaluation reports for foreign public companies is crucial for investors seeking to make informed and strategic investment decisions. These reports provide valuable insights into the value of acompany's assets, contributing to transparency, accountability, and market confidence. As a writer, I have witnessed the impact that access to these reports can have on my clients' understanding and decision-making process, and I believe that they are an essential tool for any investor considering foreign investments.In summary, the accessibility of English-language asset evaluation reports for foreign public companies is crucial for investors interested in buying into foreign stocks. These reports are indispensable as they provide valuable insights into the value of a company's assets, contributing to transparency, accountability, and market confidence. As a writer, it is clear to me that access to these reports is an essential tool for any investor considering foreign investments.。

企业社会责任报告 英文

企业社会责任报告英文IntroductionIn today's rapidly evolving business landscape, corporate social responsibility (CSR) has become an essential part of an organization's success. CSR refers to a company's commitment to operating in an economically, socially, and environmentally sustainable manner. This report aims to provide an overview of our company's CSR activities and initiatives undertaken during the fiscal year.Economic ResponsibilityAs a responsible corporate citizen, we understand the importance of economic responsibility. We strive to create economic value for our shareholders, employees, and the communities we operate in. In the past year, we have focused on strengthening our supply chain management, enhancing cost efficiency, and optimizing revenue generation strategies. By doing so, we have achieved a 10% increase in net profit, benefitting our stakeholders and contributing to economic growth.Social ResponsibilityOur commitment to social responsibility is deeply ingrained in our corporate culture. We believe in conducting business in a manner that respects human rights, promotes diversity and inclusiveness, and supports the communities we operate in. We have implemented various initiatives such as employee training programs, equal opportunitypolicies, and community engagement projects. We are proud to have achieved a 20% increase in employee satisfaction and to have contributed to the welfare of the communities through our philanthropic endeavors.Environmental ResponsibilityPreserving the environment and minimizing our ecological footprint is crucial for a sustainable future. As part of our environmental responsibility, we have adopted green practices throughout our operations. We have implemented energy-efficient technologies, reduced our carbon emissions by 15%, and actively promoted waste reduction and recycling initiatives. Furthermore, we have partnered with environmental NGOs to support reforestation projects, resulting in the planting of over 10,000 trees in deforested areas.Stakeholder EngagementWe believe that effective stakeholder engagement is vital for the success of our CSR initiatives. We have engaged with our stakeholders through various channels, including regular communication, surveys, and feedback sessions. Through these interactions, we have gained valuable insights into their expectations and concerns. These engagements have helped us establish stronger relationships and improve our CSR practices further.Future GoalsLooking ahead, we are committed to continuously enhancing our CSR efforts. Our future goals include:1. Increasing our investment in renewable energy sources to reduce our carbon footprint.2. Expanding our employee training programs to promote professional development and inclusivity.3. Strengthening our partnerships with local communities to support economic growth and social development.4. Improving transparency in our reporting and communication to ensure accountability and build trust with our stakeholders. ConclusionOur CSR initiatives have been integral to our success as a responsible corporate citizen. We remain dedicated to creating sustainable value for our stakeholders, while addressing the social and environmental challenges we face. By embracing our economic, social, and environmental responsibilities, we are confident in contributing to a better world for future generations.。

企业财务报告条例 英文

企业财务报告条例英文IntroductionCorporate financial reporting is a critical aspect of business operations. It involves the preparation and presentation of financial statements, which provide a comprehensive view of a company's financial performance and position. To ensure consistency and transparency in reporting, many countries have put in place regulations that govern corporate financial reporting. This article aims to explore the key aspects of these regulations and their importance in the business world.Objectives of the RegulationsThe primary objectives of corporate financial reporting regulations are as follows:1. Transparency: Regulations aim to promote transparency and ensure that accurate and reliable financial information is made available to stakeholders. By establishing guidelines for financial reporting, regulations minimize the risk of misleading or fraudulent practices.2. Standardization: Regulations provide a standard framework for financial reporting, ensuring that all companies follow consistent accounting principles and methods. This allows for meaningful comparisons between different businesses and facilitates decision making for investors, creditors, and other stakeholders.3. Accountability: Financial reporting regulations hold companiesaccountable for their financial activities and performance. By requiring the disclosure of financial information, regulations provide a level of assurance to stakeholders that the company is operating ethically and responsibly.4. Investor Confidence: Regulations help build investor confidence by providing a level playing field for all players in the financial markets. Investors can rely on the information provided in financial statements to make informed investment decisions, thereby increasing market efficiency.Key Components of Financial Reporting RegulationsFinancial reporting regulations typically encompass several key components, including:1. Generally Accepted Accounting Principles (GAAP)GAAP is a set of accounting standards and principles that provide guidance on how financial statements should be prepared and presented. These principles aim to ensure consistency, comparability, and transparency in financial reporting. Examples of widely recognized GAAP standards include the International Financial Reporting Standards (IFRS) and the Generally Accepted Accounting Principles (GAAP) in the United States.2. Disclosure RequirementsRegulations require companies to disclose certain information in theirfinancial statements. This includes information about the company's accounting policies, significant accounting estimates, related party transactions, and contingent liabilities. Disclosure requirements aim to provide stakeholders with a comprehensive understanding of the company's financial position and performance.3. Auditing and AssuranceFinancial reporting regulations often mandate independent audits of financial statements by certified public accountants (CPAs). This ensures that financial statements are prepared in accordance with the applicable accounting standards and are free from material misstatement. Auditing provides an additional level of assurance to stakeholders regarding the reliability of the financial information reported by the company. Importance of Financial Reporting RegulationsFinancial reporting regulations play a crucial role in maintaining trust and facilitating economic growth. Here are some key reasons why these regulations are important:1. Investor ProtectionBy promoting transparency and standardization in financial reporting, regulations protect investors from fraudulent practices and misleading financial information. Investors can rely on the accuracy and reliability of financial statements to make informed investment decisions.2. Efficient Capital AllocationFinancial reporting regulations help ensure efficient allocation of capital by enabling investors to compare the financial performance and health of different companies. This promotes fair competition and allows investors to allocate capital to the most deserving businesses.3. Stakeholder TrustAccurate and transparent financial reporting builds trust among stakeholders, including shareholders, creditors, and employees. By disclosing relevant financial information, companies demonstrate their commitment to accountability and ethical business practices.4. Economic StabilityFinancial reporting regulations contribute to overall economic stability by reducing information asymmetry and facilitating better risk assessment. Investors and creditors can make informed decisions based on reliable financial information, thereby minimizing the likelihood of financial crises.ConclusionCorporate financial reporting regulations ensure transparency, standardization, and accountability in financial reporting. By setting guidelines for companies, these regulations promote investor confidence, protect stakeholders, and facilitate economic growth. Compliance with financial reporting regulations is an essential responsibility for everybusiness, as it not only informs decision making but also builds trust and credibility in the marketplace.。

关于企业信用的英语作文

关于企业信用的英语作文Enterprise credit is crucial for the success of a business. It reflects the trustworthiness and reliability of a company in its financial transactions and business operations. A good credit score can open up opportunities for a company to access loans, secure partnerships, and attract investors.Maintaining a strong credit profile requires consistent and responsible financial management. This includes paying bills on time, managing debt levels, and keeping accurate financial records. A company with a solid credit history demonstrates its ability to meet its financial obligations and manage its resources effectively.In today's competitive business environment, a positive credit rating can give a company a competitive edge. It can provide assurance to suppliers, customers, and other stakeholders that the company is financially stable and capable of delivering on its promises. This can lead tobetter terms on contracts, lower interest rates on loans, and improved relationships with business partners.On the other hand, a poor credit score can limit a company's growth and success. It can make it difficult to obtain financing, attract new customers, and expand into new markets. A negative credit history can also damage a company's reputation and credibility, making it harder to build trust and secure business opportunities.In conclusion, enterprise credit is a key factor in the overall health and success of a business. It is essential for building trust, attracting investment, and accessing the resources needed for growth. By maintaining a strong credit profile, a company can position itself for long-term success and sustainability in the marketplace.。

征信专业词汇讲解

征信专业词汇一、机构名称Consumer Credit-Reporting Agencies 个人征信机构Credit Reference Agency 征信机构Credit Bureau信用局/征信机构(私营征信机构,一般也做征信机构返称)Credit Registry 信贷登记机构(公共)Commercial Credit Reporting Agency企业征信机构Credit Reporting Service Providers (Crsp)征信服务提供机构(国际金融公司征信知识指南用语)Experian 益百利Equifax 艾可飞Transunion 环联CRIF 科锐富(意大利)Veda Advantage 澳大利亚征信机构威达优势公司Schufa 夏华(德国)Teikouku Data Bank,TDB 帝国数据银行(日本)Tokyo Shoko Research,TSR 东京工商调查公司(日本)National Credit Bureau of Thailand 泰国国家征信局CIBIL 印度信用信息有限公司Creditinfo冰岛征信机构科瑞迪福FICO费埃哲D&B 邓白氏BIIA 亚太-中东征信协会(商业信用信息行业协会)ACCIS 欧洲征信协会European Credit Research Institute,ECRI 欧洲信贷研究所Centre for European Policy Studies,CEPS 欧洲政策研究中心The European Financial Management Association, EFMA 欧洲金融管理协会ESMA欧洲证券和市场管理局EACRA欧洲信用评级组织联合会Consumer Financial Protection Bureau, CFPB 美国消费者金融保护局The Federal Trade Commission(FTC)联邦贸易委员会Ponemon Institute波耐蒙研究所,是美国一家专门对隐私、数据保护和信息安全政策进行独立研究的机构二、信息采集Rules of Reciprocity 互惠原则Voluntary Contribution of Information 自愿报送信息Comprehensive / Full-File Credit Reporting 全面征信Positive Data 正面数据Negative Data 负面数据Thin-File Individuals薄信用报告者(缺少传统信用信息的人)Nontraditional Credit Data 非传统信用数据Individual-Level Information 个人信息Consumer Credit Information 个人信用信息Firm-Level Information 企业信息Reference Data 参考信息/个人基本信息(用来进行借款申请人的身份验证)Header Information 信用报告报告头数据(当前和历史住址、年龄、职业等信息)Public Information 公共信息Electoral Rolls 选民名册Identity Records 身份信息Court Judgments 法院判决信息Company Registration Records 企业工商注册信息Trade Lines Data/Credit Account Information / Payment Behavior Information正面还款数据或信用账户数据(一般包括借款额、还款额、账户状态、透支等按月更新的账户还款数据)Inquiry Database 查询数据库Proven Fraud File 已确定为欺诈的信息Application Form Information申请表信息Historical Data 历史数据Defaults on Previous Credit Transactions 信用交易违约信息Previous Searches/Inquiries 历史查询信息Outstanding Accounts 透支账户Credit Limits 信用额度Overdue Amount 逾期未还额Past Due 逾期Exposure to Credit 信贷敞口Overall Indebtedness 总负债额Ability and Willingness to Pay 还款能力和还款意愿Loan/Account Type 贷款账户类型Lending Institution 放贷机构Borrower’s Assets and Liabilities 借款人资产负债情况Debt Maturity 债务期限情况Installment Amount 分期还款额Current Balance 当前透支余额On-Time Payments 按时还款Pattern of Repayments 还款方式Default Rate 违约率Insolvencies无力偿还Borrowing Propensity借款倾向Remaining Balance未偿还额Probability of Payment 还款概率Collateral and Guarantee Data 抵押和担保数据Revolving Balances 循环透支Raw Data 原始数据Derived Variables 衍生变量Upload the Data 加载数据Data Aggregation 数据整合Cross-Referencing 交叉核对Cross Check 交叉核验信息Nonbank Creditors 非银行信贷机构Microfinance Lenders/Institutions 微型金融机构Rent And Utility Payments Information房租和公用事业支付信息Microfinance Institutions 微型金融机构Real-Time Data Governance 实时数据治理Data Breaches 数据外泄Flagging 添加标识Credit Profile 信用档案Big Data 大数据Corporate Linkage 企业关联Statement of Account会计报表Account Current往来帐目Current Accout 往来帐户Joint Account共同账户Outstanding Account透支/未决帐项Credit Account/Creditor Account贷方帐项Debit Account/Debtor Account借方帐项Account Payable应付帐款Account Receivable应收帐款New Account新交易/新帐户Old Account未决帐户Cash Account现金帐户Overdue Account/Pastdue Account逾期账户Bad Account呆帐Title of Account会计项目Account-Book会计薄/帐薄Discount 贴现Discount Rate/Bank Rate 贴现率三、数据库运营Data Storage/ Storing 数据存储Receiving, Checking and Loading Data数据接收、检验和加载Interface Software接口软件Operating Software 运营软件Application Software 应用软件Upgrading Frequency 更新频度Data Management Processes 数据管理流程DMP 数据管理平台Data Processing 数据处理Data Distributing数据提供Encrypt Data 对数据加密Data Cleansing 数据清理Data Migration数据迁移Data Volume 数据量Data Accuracy 数据准确性Credit-Granting Decisions 授信决策Field 字段Data Element 数据项Financially Stressed Consumers 财务紧张的消费者Origination System 信贷发起系统Credit Issuance 信贷发放Data Sets数据集Audit Trail Information (有关数据库操作的)审计跟踪记录信息Relational Database 关系型数据库Mainframe Database 大型主机数据库Collateral Register担保物权登记部门Access to And Exchange of Credit Data 数据获取与交换Pre-Processing Data 数据预处理Data Retrieval 数据检索Check Sum 校验总合/总校验码Fuzzy Matching 模糊匹配Back-Out Data 返还数据(当报数出现错误时)Backups and Mirroring of Database 数据库备份System Maintenance and Upgrades 系统维护和升级VPN 虚拟专用网System Capacity 系统容量Failover System 灾备系统(主系统发生故障时的临时服务系统) Data Disclosure 数据披露Data Security 数据安全Data Redress Mechanism 数据修复机制四、信用报告与增值服务Mapping & Planning of Credit Reporting Products 征信产品布局和规划Value-Added Services (Vas) 增值服务Customer Life Cycle 客户信贷生命周期Prospecting and Marketing 潜在客户筛选和市场营销Customer Profiling 客户特征分析Demographics 人口信息(年龄、职业、婚姻状态等个人特征信息等)Geo-Demographic Data 地理人口统计信息(在某个地理区域层级上汇总的人口信息)Prospect Lists 潜在客户名单Mail Screening 邮递筛选New Customer Acquisition 新客户获取Credit Scoring信用评分Expansion Score For Thin File Population 面向薄报告人群(缺少信用信息)的扩展评分ID Verification 身份认证Fraud Detection Service欺诈检测服务File Cross-Referencing文档交叉核对Fraud Scoring欺诈评分Payment Fraud 支付欺诈Application Fraud 申请欺诈E-Payments Fraud 电子支付欺诈Identity Theft Protection 防身份盗窃Credit Capacity Indicator 信贷能力指数Application Fraud Prevention 申请欺诈防范Fraud Shield 欺诈防范Misuse of Facility 账户滥用Alert Service (about Potentially Distressed Consumers) 对发生财务压力的借款人向贷款机构发出预警Fisk Triggers 风险触发器Credit Application Processing System 信贷申请处理系统Customer Relationship Management System客户关系管理系统Portfolio Monitoring 信贷组合监控Cross Sell/Up Sell交叉销售/追加销售Customized Value-Adding Tools 个性化(定制)增值产品Behavioral Scoring System 行为评分系统Data Mining数据挖掘Data Modeling数据建模Fine Tune 微调(指根据数据的变化对模型进行的调整)In-House Outreach Training 内部推广培训Bureau Score 局评分Statistical Model统计模型Mathematical Algorithm 数学算法Risk-Based Pricing Rules 基于风险的定价规则Retrospective Data Processing and Analysis 数据回溯与分析服务Score Monitoring, Validation 评分模型监测、验证Model Risk Governance Service模型风险治理服务Portfolio Risk Segmentation 信贷组合风险分类In-House Custom Scores 内部定制评分Batch Screening 批量筛选Ad-Hoc Inquiry 单笔查询Stress Testing压力测试Credit Officer 信贷员Automated Decision-Making Systems自动决策系统Cut-Offs (对好坏客户的)筛选规则Softeware Applications 应用软件Credit Underwriting Process 信贷审批流程Credit Decisioning 信贷决策流程Consumer Information Solutions 消费者信息解决方案(面向机构的征信或其他信息服务)Collections贷款催收Tracing/Skip Tracing Services 逃废债人追踪Personal Solutions 个人解决方案(面向个人的征信服务)Interactive (征信机构面向个人的)互动式服务五、法律监管框架与国际标准Access to Finance 获取融资Micro, Small and Medium Enterprises (Msmes) 小微企业Data Providers /Furnishers报数机构/数据提供者Credit Grantors授信机构Debt Collectors 债务催收机构Users 用户Data Subjects 数据主体Authorities /Regulators/ Supervisors 当局监管机构Consumer Credit Reporting Database个人征信系统Enterprise Credit Reporting Database企业征信系统Regulation on Credit Reporting Industry征信管理条例Consumer Protection Law 消费者保护法Data Protection Law 数据保护法Credit Reporting Activities 征信活动Consumer Right 消费者权益Financial Infrastructure 金融基础设施Regulatory Environment 监管环境Personal Screening and Due Diligence 手工筛选和尽职调查Overindebtedness 过度负债Complaints / Disputes /Contestation Settlement 异议处理Dispute Rate 异议率On- Site Inspection现场检查Administrative Sanctions 行政处罚Written Warning 书面警告Punitive Fines 罚款License (征信机构运营)许可Revocation of Business License 吊销运营许可PSI Directive 欧盟公共信息再利用指令Trade Payment Data 商业付款数据The General Principles for Credit Reporting 征信通用原则Doing Business Annual Report世界银行全球营商环境报告Responsible Lending负责任放贷Fair Trading and Financial Services Authority 美国公平交易和金融服务监管机构Treating Customers Fairly Requirements 监管机构关于“公平对待消费者”的要求Fair Credit Granting 公平授信Privacy And Data Protection 隐私和数据保护Citizens' Privacy 公民隐私权Consent (个人)授权Data Retention Periods 数据保存期限Fcra Resolution Process 公平信用报告法异议解决流程Disputants 异议提出人Modifications 更改Consumer Education and Outreach消费者教育与宣传Cross-Border Data Flows 跨境数据流动Fair and Accurate Credit Transaction Act 公平准确信用交易法案(美国,2003)Fair Credit Report Act 公平信用报告法(美国,1971)Equal Credit Opportunity Act 平等信用机会法(美国,1974)The Privacy Act 隐私权法(美国,1974)Children's Online Privacy Protection Act,Coppa 儿童在线隐私保护规则(美国,2000)Electronic Communications Privacy Act,Ecpa电子通信隐私法(美国,1986)Directives on Data Protection欧盟数据保护指令(欧盟,1995)共同体机构个人数据处理和流动保护规定(欧盟,2000)Public Sector Information Directive 公共部门信息指令(欧盟,2003)German Federal Data Protection Act 联邦数据保护法(德国,1977)The Law on Protection of Personal Information of Korea个人信息保护法(韩国,2011)Guidelines on The Protection of Privacy and Transborder Flows of Personal Data个人数据跨境流动和隐私保护指南(经合组织,1980)Data Protection Act数据保护法案(英国,1998)Guide to Credit Scoring信用评分指南(英国,2000)Identity Cards Act 身份证法(英国,2006)Credit Bureau Law 信用局法(墨西哥,2002)Transparency and Access Law 信息公开和使用法(墨西哥,2002)六、其他IRB巴塞尔银行内部评级法Portfolio Mapping贷款组合分级管理Predictable Variables可预测变量Segmentation Variables 局部变量Structured Finance结构性融资Movable Registry System动产登记系统Receivable Registry应收账款质押登记系统Financial Leasing Registry System融资租赁登记系统E-Oscar (Automated Dispute System)美国互联网信用报告异议处理系统Equifax Financial Stability Exchange 艾可飞个人收入信息验证数据库Mortgage Providers 住房抵押贷款机构Peer-to-Peer Lenders 人人贷Building Societies 住房金融互助会社Motor Finance Companies 汽车金融公司Cloud Computing 云计算Web-Crawler Technology网页爬行技术Social Networks 社交网络Payday Lenders 发薪日贷款机构Social Media Data 社交媒体数据No Claims Discount (Ncd) Database 无理赔数据库Experian/Moody’s Analytics Small Business Credit Index 益百利/穆迪小企业信用指数Credit Information Index (全球营商环境报告)信用信息指数。

给董事会的书面报告英语作文

给董事会的书面报告英语作文Quarterly Report to the Board of Directors.Introduction.Esteemed members of the Board of Directors,。

I am honored to present this quarterly report, which provides a comprehensive overview of the company's performance and strategic initiatives during the past three months. This report highlights key achievements, financial metrics, operational updates, and a forward-looking perspective on our business trajectory.Financial Performance.The company has experienced consistent financial growth during the reporting period. Revenue reached $12.5 million, representing an increase of 15% compared to the previous quarter. This growth was primarily driven by strong demandfor our flagship products and the expansion of our customer base.Net income for the quarter was $2.8 million, a 20% increase over the corresponding period last year. This improved profitability was achieved through effective cost management and strategic investments in sales and marketing initiatives.Operational Highlights.Product Development:Successfully launched our new product, "Apex," which has received overwhelmingly positive reviews from customers.Initiated development of a groundbreaking innovationin our core product line, scheduled for release in the next quarter.Sales and Marketing:Expanded our geographic footprint by entering three new international markets.Implemented a comprehensive digital marketing campaign that generated a significant increase in website traffic and lead conversion.Operations:Streamlined production processes to optimizeefficiency and reduce production costs.Implemented a state-of-the-art inventory management system to ensure optimal stock levels and minimize waste.Human Capital.We continue to invest in our most valuable asset our employees. During the quarter, we:Hired 15 new employees across various departments, bringing our total workforce to 120.Launched a comprehensive training and development program to enhance employee skills and knowledge.Promoted a culture of innovation and collaboration through regular team-building exercises.Strategic Initiatives.Market Expansion:Explored strategic partnerships with industry leaders to expand our reach into untapped markets.Identified several emerging markets with high growth potential for our products.Technology Investments:Invested in advanced analytics software to optimize decision-making and enhance customer insights.Developed a mobile application to improve customer engagement and streamline service delivery.Sustainability:Implemented sustainable practices throughout our operations, reducing our environmental footprint.Partnered with non-profit organizations to promote social responsibility initiatives.Risk Management.We have implemented a robust risk management framework to proactively identify and mitigate potential threats. During the quarter, we:Conducted a comprehensive risk assessment to evaluate potential risks and their impact on the company.Developed mitigation plans to address key risks and ensure business continuity.Outlook.The company is well-positioned for continued growth and success in the coming months. Our strong financial performance, innovative product pipeline, and strategic initiatives provide a solid foundation for future expansion.We anticipate continued revenue growth driven by the launch of new products and the expansion of ourinternational presence. We are committed to maintaining efficient operations, investing in technology, andfostering a collaborative and innovative work environment.We are confident that the company is on track toachieve its long-term goals of becoming a global leader in our industry.Conclusion.Esteemed Board members, I am proud to report that the company has made significant progress in the past quarter.Our financial performance, operational efficiency, and strategic initiatives have positioned us well for future growth.I would like to express my sincere gratitude to the entire team for their hard work and dedication, and to you, the Board, for your unwavering support and guidance.We look forward to continuing to drive innovation, expand our market share, and deliver value to our stakeholders.Thank you.。

企业信用修复英语

企业信用修复英语In the fast-paced world of commerce, where trust is the lifeblood of business relationships, the concept of corporate credit repair emerges as a vital strategy for companies striving to regain their financial integrity and market reputation. Imagine a scenario where a company, once a beacon of reliability, finds itself mired in a quagmire of financial missteps and tarnished credibility. The journey to redemption begins with a comprehensive approach to corporate credit repair, a process that not only involves rectifying past errors but also fortifying the foundation for future success.The first step in this journey is acknowledging the damage and understanding the root causes. It's about transparency and accountability, where companies must be willing to face the music and take responsibility for their past actions. This honesty sets the stage for rebuildingtrust with stakeholders, including investors, customers, and the public at large.Next comes the strategic planning phase, where a detailed roadmap is crafted to address the specific issues at hand. This includes financial restructuring, debt management, and the implementation of robust internal controls to prevent future lapses. It's about weaving a safety net of best practices that ensure compliance with regulatory standards and ethical business conduct.The execution of this plan requires a blend of expertise and agility. Engaging with financial advisors, legal counsel, and industry experts can provide the necessary guidance and support. It's also crucial to communicate the company's commitment to change, both internally and externally, through press releases, investor updates, and public statements.As the company makes tangible progress, the focus shifts to rebuilding the brand's image. This involves proactive engagement with the media, participation in industry events, and showcasing the company's new initiatives and successes. Social responsibility initiatives can also play a pivotalrole in demonstrating the company's commitment to making a positive impact on society.Finally, the ongoing monitoring and assessment of the credit repair process are essential. Regular audits, feedback loops, and performance metrics help ensure that the company remains on track and continues to build on its progress. It's a continuous cycle of improvement, where learning from past experiences becomes the driving force for a stronger, more resilient corporate entity.In essence, corporate credit repair is not just about mending the past; it's about laying the groundwork for a more sustainable and trustworthy future. It's a testament to the resilience of businesses that, despite the setbacks, are determined to rise above and forge ahead with renewed vigor and integrity.。

CORPORATE PBOC CREDIT REPORT - ENGLISH

报告编号Report Code: B-201208834902概况信息(简单版)General Information (Simple Version)借款人中文名称 Borrower's Chinese Name 借款人外文名称 Borrower's Foreign Name 组织机构代码 Code of Organization国税登记证号码 National Tax Registration No.地税登记号码 Local Tax Registration No.贷款卡编码 Code of the Loan Card 贷款卡状态 Status of the Loan Card 所属行业 Business Industry借款人注册地址 Borrower's Registration Address 借款人联系电话 Borrwoer's Contact Tel. No.职务 Position 姓名Name 法定代表人 Regal Representative James Lee 财务负责人 Financial Principal Wang Li出资方名称贷款卡编号Lin Su Wang Yue Liang Wei业务种类(明细)Business Category(Detail)贷款Loan保函Guarantee 保函Guarantee 保函GuaranteeContract No. /Borrower's Property Has No Data!Profit and Profit Distribution Has No Data!信贷信息 Cr未结清信款信息(详细版)Outstanding Loan Inforamtion (Specific Version)Borrower's Liability Has No Data!对外投资信息(简单版)External InExternal Investment Information Has No Data!贷款人财务信息(简单版)Borrower'sBorrower's Asset Has No Data!企业基本信用信息报告Corporate报告时间Report ti基本状况Ba信用报告Credit Report中国人民银行THE P高管人员信息(简单版)High L资本构成信息(简单版)Capital st注册资金 单位:万元:承兑汇票Acceptances 承兑汇票Acceptances业务种类(汇总)Business Category(Total)贷款Loan保函Guarantee承兑汇票Acceptances业务种类(汇总)Business Category(Total)贷款Loan保函Guarantee承兑汇票Acceptances保证合同编号(明细)Guarantee Contract Code (detail)保证合同有效状态(明细)Guarantee Contract ValidStatus(det ail)1210_2012_0083是Yes保证合同笔数合计(汇总)Guarantee Contract Quantity in Total (Total)保证担保合同金额本外币合计(汇总) 单位:元 Guarantee Contract of All Curr Unit: Yuan本担保人保证担保金额本外币合计(汇总) 单位:元 This Guarantor Guaranteed of All Currencies in Total Unit: Yuan保证合同笔数合计(汇总)Guarantee Contract Quantity in Total (Total)Current External Guarantee -Current External Guarantee 被担保信息 (简单版)Guarant 未结清不良信贷信息(简单版)Outstanding NoOutstanding Non-performing Loan Information Has No Data!已结清不良信贷信息(简单版)Cleared Non-Cleared Non-performing Loan Information Has No Data!Interest Delinquency Has No Data!当前对外担保信息(详细版)Current Exte币种(汇总)RMB 欠信信息(简单版)InteresRMB RMB 已结清贷款信息(简单版)Cleare币种(汇总)RMB RMB RMB保证担保合同金额本外币合计(汇总) 单位:元 Guarantee Contract of All Curr Unit: Yuan抵押合同笔数合计(汇总)Mortgage Contract Quantity in Total (Total)保证担保合同金额本外币合计(汇总) 单位:元 Mortgage Contract of All Curr Unit: YuanGuaranteed Information -垫款信息 (简单版)AdvanceAdvances infor公开授信信息(简单版)Open CrOpen Credit I资产剥离信息(简单版)AssAsset Strip不良信贷资产处置(简单版)Credit DisposalCredit Disposal of Non-per集团信息(简单版)GroupGroup Inform股票信息(简单版)StockStock诉讼信息(简单版)LitigatiLitigatio大事记信息(简单版)Memorabi大事记信息记录流水号 Record No.20202020社保信息(简单版)Social Secu 参保信息Insured InformationInsured Infor 应参保未参保信息Insurable Uninsured InformationInsurable Uninsured公积金信息(简单版)ProvidentProvident Fund In法院信息CoCourt Information证监会信息(行政处罚)(简单版)Securities RegulaSecurities Regulatory Commission Infor税务信息Tax Infor 纳税基本信息Tax Basic InformationTax Basic Info 纳税明细信息Tax Particular InformationTax Particular In 处罚信息Penalty InformationPenalty Infor表彰奖励信息Award InformationAward Inform奖励信息(简单版)AwardAward Inform行政处罚信息(简单版)AdministratiAdministrative penalt许可信息(简单版)PermissiPermission Info资质信息(简单版)QualificatQualification In认证信息(简单版)AuthenticaAuthentication In质检通关及企业进出品监管信息(简单版)The QC clearance and entThe QC clearance and enterprises import a出入境检验检疫绿色通道信息Entry-exit inspection and quarantine gree-channeEntry-exit inspection and quaranti进出口商品免验信息Import and export merchandise exempted from inspection IImport and export merchandise exempte进出品商品检验分类监管信息Import and export commodity inspection and classImport and export commodity inspection and cla公用事业缴费信息(简单版)Utilitie电信缴费信息Telecommunications payment InformationTelecommunications paym电费缴纳信息Electricity bill payment InformationElectricity bill payme水费缴纳信息Water bill payment InformationWater bill payment燃气费缴纳信息Gas bill InformationGas bill Infor有线电视收视缴纳信息Cable TV bill InformationCable TV bill In其他公用事业缴纳信息Other Utilities bill payment InformationOther Utilities bill pay借款人声明Bor异议标注O本信用报告应由定购者以机密文件方式处理,并不得作为政府机关或法庭往来文件。

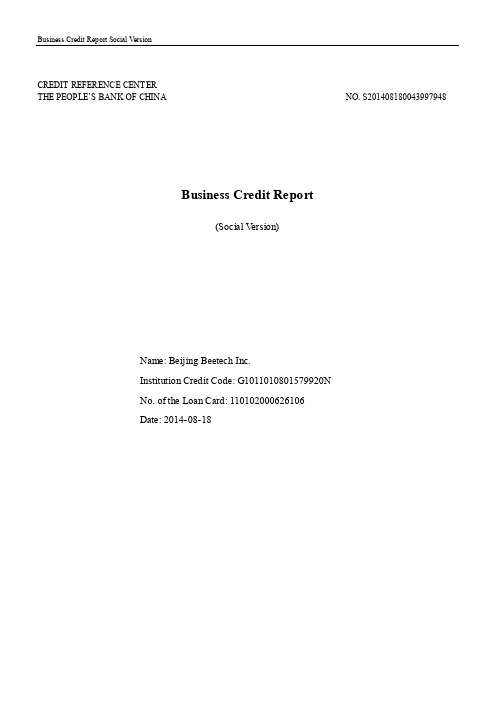

企业信用报告英文版.

CREDIT REFERENCE CENTERTHE PEOPLE’S BANK OF CHINA NO. S201408180043997948Business Credit Report(Social V ersion)Name: Beijing Beetech Inc.Institution Credit Code: G1011010801579920NNo. of the Loan Card: 110102*********Date: 2014-08-18Instructions to the Report1. This report is issued by Credit Reference Center of the People’s Bank of China, and is produced from the information recorded in the business credit systems as of the date the report issued. Except for the notes from the Credit Reference Center, all the information in the report is provided by the relevant data presentation institutions and the main body for the information, the Credit Reference Center will not guarantee its truth and accuracy, but promises to keep objective, neutral position during the whole process of information integration, summary and presentation.2. The identity information, information of the main contributors and executives is from the relevant material provided by the main body to the sub-branches of the People’s Bank of China.3. Should there are no special notes, the unit for the amount data in this report is ten thousand Y uan.4. Should there are no special notes on currency, the summarized amount data in this report is calculated in RMB. The conversion of foreign currency to RMB shall be calculated in accordance with the conversion rate sheet for other currencies to USD announced by State Administration of Foreign Exchange in the current month.5. Notes of the data presentation institution are all the supplementary ones to the information in the report or to the main body.6. Notes of the Credit Reference Center are the all ones made to the information record in the report or to the main body;7. Statement from the main body is the brief one made to the information record provided by the data presentation institution;8. Please use this report following the agreements made with the main body and keep it properly. Credit Reference Center will not assume any responsibility to any dispute arising from improper use of this report.Basic InformationIdentity InformationInformation of the Main ContributorsThe registered capital is equivalent RMB 3,505 ten thousand Y uan in totalInformation of ExecutivesInformation AbstractThe information main body had the first credit relationship with the financial institution in 2009. Within the period of the report, it has processed credit business in one financial institution in total, and currently its business in the one financial institution has not been settled.Abstract of unsettled credit informationAbstract of settled credit information* Exchange rate (USD converted to RMB): 6.17 V alid to: 2014-08。

英语征信作文

Writing a credit report in English requires a clear and concise presentation of an individuals or a companys credit history.Here are some key points to consider when composing a credit report:1.Introduction:Begin with a brief introduction of the subject of the report,whether it is an individual or a business,and the purpose of the report.2.Personal or Business Information:Provide basic information such as the full name, address,social security number for individuals,or the business registration number and date of incorporation for businesses.3.Credit History:Detail the credit history,including the types of credit accounts held, such as credit cards,loans,mortgages,and any other forms of credit.Include the dates when these accounts were opened and the current status active,closed,or in default.4.Payment History:Describe the payment patterns,noting any late payments,defaults,or e a scale if appropriate,such as Excellent,Good,Fair,Poor,or Bad.5.Credit Score:If available,include the credit score,which is a numerical representation of creditworthiness.Explain what the score indicates about the subjects credit risk.6.Current Debts and Obligations:List current debts,including the outstanding balance, monthly payments,and the creditors name.7.Public Records:Mention any public records that may affect creditworthiness,such as liens,judgments,or foreclosures.8.Inquiries:Record any recent inquiries made by lenders or creditors,which can indicate recent attempts to obtain credit.9.Employment and Income:For individuals,include employment history and current income,as this can affect the ability to repay debts.10.Summary and Recommendations:Conclude with a summary of the credit reports findings and any recommendations for improving credit health or managing existing credit responsibly.11.Contact Information:Provide contact details for the credit reporting agency or any other relevant parties.Remember to maintain confidentiality and privacy when handling credit reports,as they contain sensitive e formal language and avoid any personal opinions or judgments.Heres a brief example of how a credit report might begin:Credit Report for Name of Individual/BusinessIntroduction:This credit report provides a comprehensive overview of the credit history and financial standing of Name of Individual/Business.Personal/Business Information:Name:Full Name or Business NameAddress:Mailing AddressSocial Security Number/Business Registration Number:As applicableCredit History:The subject has maintained Number credit accounts,including Types of Credit Accounts. The oldest account was opened on Date,and the most recent on Date.Payment History:The payment history indicates a pattern of Payment Pattern Description.There have been Number instances of late payments within the last Time Period.This is just a starting point,and the rest of the report should follow a similar structured and detailed approach.。

信贷基本词汇英汉对照