Presentation onTax Deduction at Source

税收词汇

farmlandoccupationtax

土地增值税

land appreciation tax

印花税

stamp duty

个人所得税

personal income tax (PIT)

企业所得税

corporate/enterprise income tax (CIT/EIT)

车辆购置税

vehicle acquisition tax

(Losses/credits) be carried forward without limitation

股息/利息预提税

DIRR

股息、利息、特许权使用费、租金

gift tax

赠与税

estate tax

遗产税(总遗产税)

inheritance tax

继承税(分遗产税)

earnings before/after taxes

税前/后收益

earned/active income

积极所得(包括经营所得operating income和劳务所得service income)

经合组织/联合国税收协定范本

permanent establishment

常设机构

business presence

营业存在

可比非受控价格法

comparable uncontrolled price method (CUP)

再销售价格法

resale price method (RPM)

成本加成法

cost-plus method

契税

deed tax

燃油税

fuel tax

证券交易税

securities transaction tax

纳税申报英语

纳税申报英语一、单词1. tax [tæks]- 释义:n. 税;税款;v. 对…征税- 用法:作名词时,可用于表达各种类型的税,如ie tax(所得税);作动词时,常用于被动语态be taxed,表示被征税。

- 例句:The government plans to raise taxes on luxury goods.(政府计划提高对奢侈品的征税。

)2. declaration [ˌdekləˈreɪʃn]- 释义:n. 申报;宣布;宣言- 用法:在纳税语境中,常指纳税申报,如tax declaration(纳税申报)。

- 例句:You need to submit your tax declaration before the deadline.(你需要在截止日期前提交你的纳税申报。

)3. filer [ˈfaɪlə(r)]- 释义:n. 申报者;档案管理员(在纳税申报中主要指申报者)- 用法:直接表示进行纳税申报的人。

- 例句:The tax filer should provide accurate information.(纳税申报者应该提供准确的信息。

)4. deduction [dɪˈdʌkʃn]- 释义:n. 扣除;减除;推论- 用法:在纳税中,指可以从应纳税所得额中扣除的项目,如tax deductions(税收扣除项目)。

- 例句:Mortgage interest is amon tax deduction for homeowners.(房屋贷款利息是房主常见的税收扣除项目。

)5. exemption [ɪɡˈzempʃn]- 释义:n. 免除;豁免- 用法:表示某些情况或项目在纳税时被免除,如tax exemption (免税)。

- 例句:Some charities enjoy tax exemption.(一些慈善机构享受免税待遇。

)6. revenue [ˈrevənjuː]- 释义:n. 税收;收入;收益- 用法:指政府通过征税等方式获得的财政收入。

国际税收课后习题答案

1.what is International Tax?What does it mainly address(探讨)?International Tax is a science focusing on a serious tax issues resulting from different and conflicting tax rules made by particular countries ,jurisdictions and resolutions(决议).International tax in a board sence covers not only income but also turnover taxes,etc.2.Talk about differences between China and USA on taxation system1)The USA is a country with income taxes as a major tax while in China we have turn over taxes as our important taxes.2)The federal government,state government and local government of the USA have pretty rights to collect taxes,while the rights to collect taxes are mostly controlled in central government.3)The USA use comprehensive income tax system and deduct fees refers to different situation.China use itemized income tax system.4)In the respect of estate tax, real estate tax is the mainly object to be taxed .3.On differences among Macau,China Continent and HongKong for the purpose of tax features according to table 11)The corporate income tax rates in China Continent is the highest in these three ,to 25%.The tax base of China Continent Is worldwide while the others are territorial.2)In China Continent we have taxes for interest,royalties,technical fees,management fees (all of them are 10% for non-resident,20%for resident ),while the others don’t have them.3)China Continent have value-added tax ,while the others don’t have them.4.On differences among UK,China Continent and Spain for the purpose of Corporate income tax according to table 21)Spain has the highest corporate tax rate to 32.5%.2)UK doesn’t tax for many income which China Continent or Spain will tax such as Capital gains ,branch profits,dividends, technical fees and management fees.5.On differences among China Continent and foreign jurisdictions for the purpose of withholding taxes according to table 31)For branch profits, interest ,technical fees and management fees most jurisdictions don’t collect tax except Ireland(collect for interest) and China Continent.2)Except Switzerland federal tax rates of dividends and interest are 35% and higher than China Continent ,other jurisdictions’ withholding tax rates are mostly lower or equal to China Continent.International Income Taxation1.How does a country generally design its income taxation system?(book page50)1)territorial(领土模式):tax only income earned within their borders.eg.HongKong.2)Residency(属人模式):tax on the worldwide income of residents, and impose tax on the income of nonresidents from certain sources within the country. eg.the USA.3)Exclusion(例外):specific inclusion or exclusion of certain amounts,classes,or items of income in/from the base of taxation.4)Hybrid(混合模式):some governments have chosen for all or only certain classes of taxpayers, to adopt systems that are a combination of territorial, residency, or exclusionary.2.Why is it important to make clear source of income?To make clear source of income is important because it decidides that whether a individual or corporation should pay tax in a country and what credits can it enjoy.3.Term explanation:Thin Capitalization;Foreign tax Credit;Withholding tax; International tax treaty; Deferral system; International transfer pricingThin Capitalization:Thin capitalization is a method that taxpayers borrow too much money from oversea related party and pay much interest, so that they can enjoy much deduction before tax.By this way,they transfer profits from high tax burden countries to low tax burden countries or jurisdictions.Foreign tax Credit(外国税收抵免):If you paid or accrued foreign taxes to a foreign country on foreign source income and are subject to resident country tax on the same income, you may be able to take a credit for those taxes. Taken as a credit, foreign income taxes reduce your own country tax liability.Withholding tax:Withholding tax is tax withheld by the country when a corporation making a payment to its resident country , in which the full amount owed to that corporation is reduced by the tax withheld.International tax treaty:International tax treaty is a treaty a country (or jurisdiction) signed with other countries (or jurisdiction) for affairs about taxation.Deferral system:Deferral system is a tax incentive (激励措施)to encourage domestic tax residence to make investment broad.But it may cause international tax avoidance.(缺点:可能造成国际避税)International transfer pricing:International transfer pricing is a very important way for multinational company to avoid international tax.Transfer pricing refers to a kind of non-market pricing action taken by related corporations to shift profits form high tax rate countries or jurisdictions to low tax rete regions.Tax Residence1.What is the main difference between a tax resident and a non-tax resident for tax liability purpose? In general, a tax resident bears infinite tax liability ,should pay tax for all of its income.A non-tax resident bears limited tax liability, should pay tax for income sourced from the country.2.Can you name some tests in determining whether a person is a resident?for corporation:place-of-incorporation test,place-of-management test,residence of the shareholders testfor individiual:a fact-and-circumstances test ;abode test; number of day test(in China:1~5year – temporary resident,>5year - long-term resident)3.Take an example to prove how different countries apply differing tests to judge a person's residence?For example ,China for individual:domicile test,number of days(a full year);for corporation:place-of-incorporation test or place-of-management testireland for individual:number of days test(183 days),domicile testfor corporation:place-of-incorporation test or place-of-management test4.Term explanation:Tax residence;dual resident;domicile test;Tax residence:If an individual or a corporation is a tax residence ,it bears infinite tax liabilitis to its own country.Domicile is, in common law jurisdictions.dual resident:dual resident means an individual or a corporation is resident taxpayer in two countries at the same time.It often occurs when two use different standard for tax residence.domicile test:If an individual or a corporation has its domicile in a country ,it is the country's tax residence.It is a common tax jurisdiciton.Income Source Jurisdiction and Rules1.What is source jurisdiction?Source jurisdiction is one important form of income tax jurisdiction.It is the most important tax jurisdiction.(收入来源地管辖权是一种重要的,并且是最重要的税收管辖权)All country and jurisdiction adopt source jurisdiction(所有的国家和地区都使用来源地管辖权) So called source jurisdiction refers to that as long as an tiem of income is sourced within the territory, the government of the territory has rights to lavy income tax on it .(一笔所得只要来源于本国,就可以对其征税)2.How to determine the source of employment and personal services income?If the income derived from personal services performed by an employee, it is source of employment.If the income is performed by an independent contractor or a professional ,it is source of personal service income.3.How to determine the source location of business Income?What is PE?If the income is attributable to a PE(permanent establishment) in the country(ues 1.attribution rule 归属原则2.attraction rule引力规则), it is the country’s source income.PE: permanent establishment,based on substance or people.(场所:辅助性、准备性不算;人:必须是非独立代理人,经常为公司签订合同的等)4.How to determine the source of investment income?Dividend and interest income.If the income is derived from ownership of equity ,it is the source of investment income.5.How about US source rules?6.What are China's source rules?An RE(resident enterprise)must pay enterprise income tax to the Chinese government on all its income,regardless of whether such income is generated within or outside of China.The defult tax rate for an RE ,prior to any special tax treatment, is 25 percent.An NRE(nonresident enterprise) that has any Operational Establishment in China is required to pay enterprise income tax only on its income sourced from China.The tax rate is 10 percent.International Double Taxation and Relief1.What is International double taxation?International double taxation is that the same item of asset is taxed twice or more than twice in a tax year.2.What is the main difference between legal International double taxation and economic International double taxation?Legal International double taxation is for the same taxpayers ,who are often branch companys, using direct credits.Economic International double taxation is for different taxpayers,who are often subside companys,using indirect credits.3.Take an example to prove International double taxation arising from the same tax jurisdiction and relief.4.What approaches are used to solve International double taxation resulting from residence-source conflicts?Unilateral,bilateral and multilateral approaches.Deduction method,exemption method,credit method and so on.5.What is the main difference between deduction method and credit method?Deduction:reduce all kinds of fees from taxable income.Credit:reduce credit from tax due.6.Which specific relief methods does international community agree to?The OECD and UN models only authorize the credit and exemption method,not the deduction method.7.Termexplanation:fullexemption;partialexemption;limitation on credit;full exemption:only levy tax on income from resident company's own country.partial exemption:give resident company a part of tax exemption for overseas income.limitation on credit:the tax rate of resident company's own country multiply by the income in the country.If the taxpayer paied a amount of tax less than the limitation,it should pay tax in arrears.International Tax Avoidance and Tax Haven1.What is tax haven?Tax haven is a country or jurisdiction which has low tax rate or no tax so that people choose to live or register company there to avoid the high tax burden in their own country or jurisdiction.Another definition:A tax haven is a country or territory where taxes are lavied at a low rate or not at all.(in the book)2.How many types of tax havens are there in the world?There.1)Nil-Tax Havens(零税率):do not have any of the three main direct taxes:No income tax or corporation tax;No capital gains tax,and No inheritance tax.2)Foreign Source Exempt Havens(外国来源豁免):They only tax you on lacally derived income.3)Low-Tax Havens(低税率):Have special concessions or double tax treaties. some non-tax features of a tax haven?Generally,a tax haven have these features:1)Small territory2)Privacy3)Ease of residence4)Political stability5)Political stability6)Relaible communications7)Good life factors.4.How does an international taxpayer make use of a tax haven?(in book P104)methodology1)Change personal residency.(改变居民身份)Relocate themselves in low-tax jurisdiction.2)Asset holding.(资产持有)Utilize a trust or a company which will be formed in tax haven.3)Trading and other business activity.(生产经营)Set up many businesses which do not requirea specific geographical location or extensive labor in tax havens to minimimze tax exposure.4)Financial intermediaries.(通过财务金融中介公司)Use funds,banking,life insurance and pensions.Deposit with the intermediary in the low-tax jurisdiction.5.Does China have anti-tax-haven rules?Yes.In CFC rules.6.What are the advantages of being a tax haven?Being a tax haven ,a jurisdiction can1) have divisions of multinational locating there and employ some of the local population;2)transfer needed skills to the local population;3)go a long way to attracting foreign companies.7.What are the reasons for some jurisdictions desiring to be tax havens?The same as question6.Chapter 7International Transfer Pricing and Rules1.What is International transfer pricing?Transfer pricing refers to a kind of non-market pricing action taken by related corporations to shift profits form high tax rate countries or jurisdictions to low tax rete regions.The main purposes are reduce tax burden and a series of non-tax purposes like 1)occupy market 2)change the subsidiary’s image in order to gain other interest 3)avoid currency control 4)minimize the expose to import duty 5)earn excess profit …2.Take an example to prove that International transfer pricing can be used to avoid international tax ?For example,A has a product can be sold at 1000 dollars, but A sold it to B at 100 dollars.Then B will sell it at 1000, 900 profit was shift to B’s countries or jurisdictions,andB was setup in tax haven,the group don’t have to pay much tax.3.Whatare the main contents of International transfer pricing rules?International transfer pricing rules are a series of tax manage rules made by countries or governments in order to prevent corporations particularly multinational corporations utilize International transfer pricing to avoid tax ,which cause government’s tax run off.4.Termexplanation:comparable uncontrolled price;costplus;resaleprice;transactional net margin method;profit split method;comparabilityanalysisChapter8Controlled Foreign Corporation and Rules1.How does a multinational firm use a CFC to avoid tax?In most cases,Chinese firms tend to not distribute or just distribute a little profit from CFC to its parent firm.While, foreign firms usually let the profit stay in the CFC.2.What is CFC?CFC refers to firms controlled by resident firms and theyare often set in low tax rate or no tax reigions.3.What is the relationship between deferral system(延迟缴纳) and CFC rules?The law of many countries does not tax a shareholder of a corporation on the corporation’s income until the income is distributed as a dividend.This dividend could be avoided indefinitely by loaning the earnings to the shareholder without actually declaring a dividend.The CFC rules were intended to cause current taxation to the shareholder where income was of a sort that could be artificially shifted or was made available to the shareholder.At the same time, such rule were designed to interfere with normal commercial practices.4.What arethe main contents of a country’s CFC rules?The main contents of a country’s CFCrules are to prevent residents (including individuals and firms) using controlled foreign corporation to avoid tax burden.5.When were China’s CFC rules established?Year 2009.6.Can you name any differences between China and foreign jurisdictions for purposes of CFC rules?7.Must a foreign corporation which is established in a tax haven and controlled by our residents bea CFC for our tax purpose?Why?No.If the foreign corporation is1)a small corporation(the total profit a year is less than 5 millions);2)the main income was get from positive operating activities, it won’t be a CFC for our tax purpose.Thin Capitalization and Rules1.What is thin capitalization?Thin capitalization is a method that taxpayers borrow too much money from oversea related party and pay much interest, so that they can enjoy much deduction before tax.By this way,they transfer profits from high tax burden countries to low tax burden countries or jurisdictions.2.Give an example to prove that thin capitalization can be used to avoid tax.暂无3.What are the main contents of thin capitalization rules?1)The relationship between borrower and lender.2)Thedetermination of excessive interest.3)Treatment of excessive interest: deemed dividend and withholding tax is lavied.4)4.What are the main features of the USA thin capitalization rules?5.Talk about thin capitalization rules in ChinaChina use ALP(arm’s lenth principle)/fixed Debt-to-Equity Ratio /Earnings stripping(收益剥离法)。

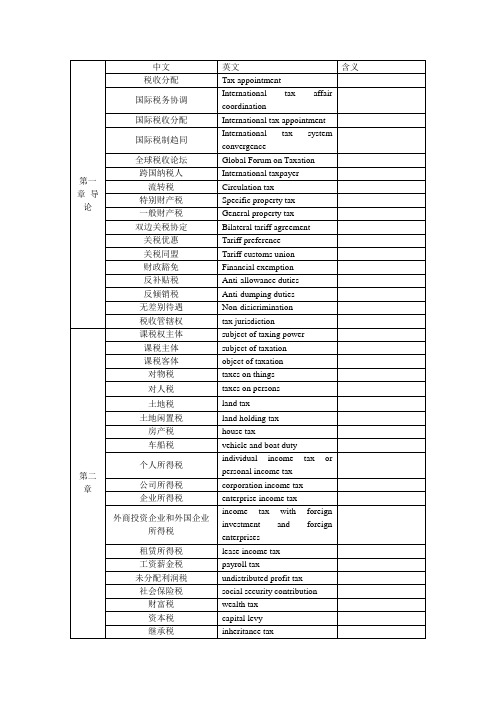

国际税收英文词汇

国际税收英文词汇经合组织:OECD联合国:UN入境交易:Inbound transactions出境交易:Outbound transactions营业税:Business tax消费税:Excise tax财产税:Property tax死亡税:Death duty技术贸易壁垒:TBT居民管辖权:Domiciliary tax jurisdiction地域管辖权:Regional tax jurisdiction住所:Domicile居所:Residence居民纳税人:Resident tax payer税收流亡者:Tax refuges法律住所:Legal domicile财政住所:Fiscal domicile管理机构所在地:Place of effective management总机构所在地:Place of head office营业利润:Business profit子公司:Subsidiary company常设机构:Permanent establishment实际所得原则:Attribution principle引力原则:Force of attraction principle(非)独立劳务所得:Income from(in)dependent personal services 股息:Dividend专利权:Patent right专有技术:Know-how有(无)线纳税义务:(Un)limited tax liability推迟课税:Tax deferral法律性重复征税:Juridical double taxation经济性重复征税:Economic double taxation长期性住所:Permanent home重要利益中心:Center of vital interests习惯性住所:Habitual abode国籍:Nationality扣除法:Deduction method免税法:Exemption method全部免税法:Full exemption累进免税法:Exemption with progression抵免法:Credit method全额抵免:Full credit普通抵免:ordinary credit抵免限额:Ceiling in credit分国抵免:Tax credit on a country by country basis分项抵免:Tax credit on an item by item basis分国分项抵免:Tax credit on a source by source basis 分国不分项抵免:Overall credit on a per-country basis 分项不分国抵免:Overall credit on a per-item basis综合抵免:Overall credit直(间)接抵免:(in)Direct tax credit归属抵免制:Imputation system汇率:Exchange rate税收饶让抵免:Tax sparing credit避税(偷税):Tax evasion跨境:Cross abroad滥用国际税收协定:Treaty shopping国际避税地:Tax heavens美国国内收入署:Internal Revenue Service(IRS)离岸中心:Offshore center自由港:Free port基地公司:Base company转让定价:Transfer pricing转让价格:Transfer price滥用转让定价:Transfer pricing abuse信托:Trust内部保险公司:Captive insurance company资本弱化:Thin capitalization公平交易原则:the arm’s length可比非受控价格法:Compared uncontrolled price method 工业制成品:Manufactured goods再销售价格法:Resell price method成本加成法:Cost plus method净(总)利润率:Net(Gross)profit margin预约定价协议:Advance pricing agreements(APA)反避税地法规:Anti-tax haven legislation受控外国公司法规:CFC legislation消极投资所得:Passive income税收情报交换方式:a.根据要求交换:Exchange on requestb.自动交换:automatic exchangec.自发交换:Spontaneous exchanged.同时检查:Simultaneous examination条约:Convention股息收益人:Beneficial owner of the dividends。

国际税收协定中英对照

international income from pensions

跨国政府服务所得

international income from governmental services

跨国董事费所得

international income from directors fees

跨国表演家和运动员所得

第四章

跨国权益所得

international income from legal right

跨国独立劳动所得

international income from independentpersonallabour

跨国非独立劳动所得

international income from dependent personal labour

第二章

课税权主体

subject of taxing power

课税主体

subject of taxation

课税客体

object of taxation

对物税

taxes on things

对人税

taxes on persons

土地税

land tax

土地闲置税

land holding tax

房产税

house tax

跨国一般静态财产价值

international general propertyvalue on stationary

第三章

税制性重复征税

tax systematic double taxation

法律性重复征税

juridical or legal double taxation

经济性重复征税

economic double taxation

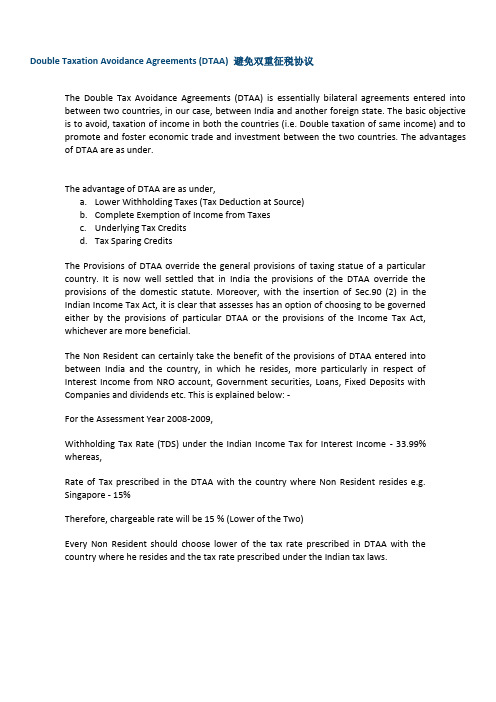

Double Taxation Avoidance Agreements (DTAA) 避免双重征税协议

Double Taxation Avoidance Agreements (DTAA) 避免双重征税协议The Double Tax Avoidance Agreements (DTAA) is essentially bilateral agreements entered into between two countries, in our case, between India and another foreign state. The basic objective is to avoid, taxation of income in both the countries (i.e. Double taxation of same income) and to promote and foster economic trade and investment between the two countries. The advantages of DTAA are as under.The advantage of DTAA are as under,a.Lower Withholding Taxes (Tax Deduction at Source)plete Exemption of Income from Taxesc.Underlying Tax Creditsd.Tax Sparing CreditsThe Provisions of DTAA override the general provisions of taxing statue of a particularcountry. It is now well settled that in India the provisions of the DTAA override theprovisions of the domestic statute. Moreover, with the insertion of Sec.90 (2) in theIndian Income Tax Act, it is clear that assesses has an option of choosing to be governedeither by the provisions of particular DTAA or the provisions of the Income Tax Act,whichever are more beneficial.The Non Resident can certainly take the benefit of the provisions of DTAA entered intobetween India and the country, in which he resides, more particularly in respect ofInterest Income from NRO account, Government securities, Loans, Fixed Deposits withCompanies and dividends etc. This is explained below: -For the Assessment Year 2008-2009,Withholding Tax Rate (TDS) under the Indian Income Tax for Interest Income - 33.99%whereas,Rate of Tax prescribed in the DTAA with the country where Non Resident resides e.g.Singapore - 15%Therefore, chargeable rate will be 15 % (Lower of the Two)Every Non Resident should choose lower of the tax rate prescribed in DTAA with thecountry where he resides and the tax rate prescribed under the Indian tax laws.Double taxation is the systematic imposition of two or more taxes on the same income (in the case of income taxes), asset (in the case of capital taxes), or financial transaction (in the case of sales taxes). It refers to taxation by two or more countries of the same income, asset or transaction, for example income paid by an entity of one country to a resident of a different country. The double liability is often mitigated by tax treaties between countries.The term 'double taxation' is additionally used, particularly in the USA, to refer to the fact that corporate profits are taxed and the shareholders of the corporation are (usually) subject to further personal taxation when they receive dividends or distributions of those profits.International double taxation agreementsEuropean Union savings taxationIn the European Union, member states have concluded a multilateral agreement on information exchange. This means that they will each report (to their counterparts in each other jurisdiction) a list of those savers who have claimed exemption from local taxation on grounds of not being a resident of the state where the income arises. These savers should have declared that foreign income in their own country of residence, so any difference suggests tax evasion.(For a transition period, some states have a separate arrangement. They may offer each non-resident account holder the choice of taxation arrangements: either (a) disclosure of information as above, or (b) deduction of local tax on savings interest at source as is the case for residents).Cyprus double tax treatiesCyprus has concluded 34 double tax treaties which apply to 40 countries. The main purpose of these treaties is the avoidance of double taxation on income earned in any of these countries. Under these agreements, a credit is usually allowed against the tax levied by the country in which the taxpayer resides for taxes levied in the other treaty country and as a result the tax payer pays no more than the higher of the two rates. Further, some treaties provide for tax sparing credits whereby the tax credit allowed is not only with respect to tax actually paid in the other treaty country but also from tax which would have been otherwise payable had it not been for incentive measures in that other country which result in exemption or reduction of tax.German taxation avoidanceIf a foreign citizen is in Germany for less than a relevant 183-day period (approximately six months) and is tax resident (i.e., and paying taxes on his or her salary and benefits) elsewhere, then it may be possible to claim tax relief under a particular Double Tax Treaty. The relevant 183 day period is either 183 days in a calendar year or in any period of 12 months, depending upon the particular treaty involved.So, for example, the Double Tax Treaty with the UK looks at a period of 183 days in the German tax year (which is the same as the calendar year); thus, a citizen of the UK could work in Germany from 1 September through the following 31 May (9 months) and then claim to be exempt from German tax (whilst still paying the UK tax).IndiaIndia has comprehensive Double Taxation Avoidance Agreements (DTAA) with 79 countries. This means that there are agreed rates of tax and jurisdiction on specified types of income arising in a country to a tax resident of another country. Under the Income Tax Act 1961 of India, there are two provisions, Section 90 and Section 91, which provide specific relief to taxpayers to save them from double taxation. Section 90 is for taxpayers who have paid the tax to a country with which India has signed DTAA, while Section 91 provides relief to tax payers who have paid tax to a country with which India has not signed a DTAA. Thus, India gives relief to both kinds of taxpayers.A large number of foreign institutional investors who trade on the Indian stock markets operate from Mauritius. According to the tax treaty between India and Mauritius, capital gains arising from the sale of shares are taxable in the country of residence of the shareholder and not in the country of residence of the company whose shares have been sold. Therefore, a company resident in Mauritius selling shares of an Indian company will not pay tax in India. Since there is no capital gains tax in Mauritius, the gain will escape tax altogether.The Indian and Cypriot tax treaty is the only other such Indian treaty to provide for the same beneficial treatment of capital gains.It must be noted that India has and is making attempts to revise both the Mauritius and Cyprus tax treaties to eliminate this favorable treatment of capital gains tax. The Indian governments periodically check for its DTAA with many countries and come up with amendments.United StatesU.S. citizens and resident aliens abroadThe U.S. requires its citizens to file tax returns reporting their earnings wherever they reside. However, there are some measures designed to reduce the international double taxation that results from this requirement.First, an individual who is a bona fide resident of a foreign country or is physically outside the United States for an extended time is entitled to an exclusion (exemption) of part or all of their earned income (i.e. personal service income, as distinguished from income from capital or investments.) That exemption is $91,400 for 2009, pro-rated. (See IRS form 2555.)Second, the United States allows a foreign tax credit by which income taxes paid to foreign countries can be offset against U.S. income tax liability attributable to foreign income. This can be a complex issue that often requires the services of a tax advisor. The foreign tax credit is not allowed for taxes paid on earned income that is excluded underthe rules described in the preceding paragraph (i.e. no double dipping).[edit] Double taxation within the United StatesDouble taxation can also happen within a single country. This typically happens when sub national jurisdictions have taxation powers, and jurisdictions have competing claims. In the United States a person may legally have only a single domicile. However, when a person dies different states may each claim that the person was domiciled in that state. Intangible personal property may then be taxed by each state making a claim. In the absence of specific laws prohibiting multiple taxation, and as long as the total of taxes does not exceed 100% of the value of the tangible personal property, the courts will allow such multiple taxation.[Taxation of corporate dividendsIn the United States, the term "double taxation" is also used by critics to describe dividend taxation.参考资料:/wiki/Double_taxation/tax_dbl.htm/v7428666.htm#/n8136506/n8136593/n8137537/n8687294/index.html /n1057/n3873/n3918/n323624.files/n442040.ppt。

酒类、食物类翻译

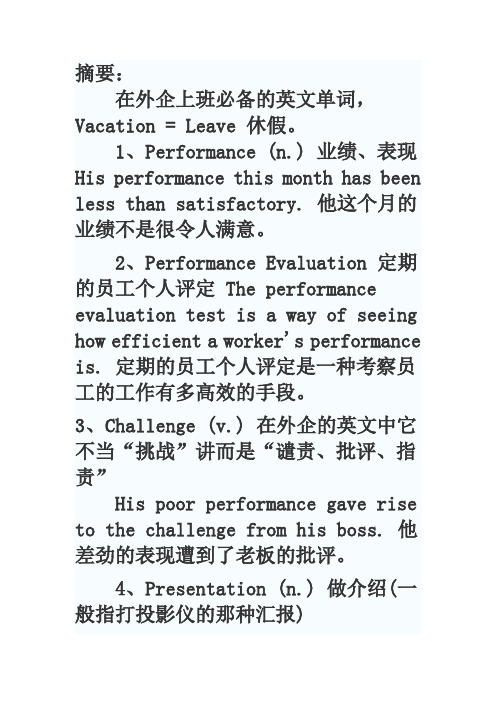

摘要:在外企上班必备的英文单词,Vacation = Leave 休假。

1、Performance (n.) 业绩、表现His performance this month has been less than satisfactory. 他这个月的业绩不是很令人满意。

2、Performance Evaluation 定期的员工个人评定 The performance evaluation test is a way of seeing how efficient a worker's performance is. 定期的员工个人评定是一种考察员工的工作有多高效的手段。

3、Challenge (v.) 在外企的英文中它不当“挑战”讲而是“谴责、批评、指责”His poor performance gave rise to the challenge from his boss. 他差劲的表现遭到了老板的批评。

4、Presentation (n.) 做介绍(一般指打投影仪的那种汇报)His presentation on the Earth Summit proves that we really need to pay more attention to the global environment.他在地球峰会上的报告证实了我们的确要更加关注全球的环境。

5、Quota (n.) 员工的(一年或半年的)任务量 Have you reached your predicted quota for this quarter? 你达到了本季度预期的任务量了吗?6、Solid (n.) 可靠的、稳妥的Their partnership is solid as a rock. 他们的伙伴关系像岩石一样坚不可摧。

7、Complicated (adj.) 复杂的English grammar is very complicated. 英语语法非常复杂。

确认专税流程英语

确认专税流程英语English:The confirmation of the specialized tax process involves a series of steps to ensure compliance and accuracy. Firstly, it starts with gathering all relevant financial information and documents, including income statements, expense receipts, and asset records. This step is crucial as it provides a comprehensive overview of the company's financial activities. Once the information is collected, the next step is to analyze and classify the data according to the tax regulations and guidelines. This process requires careful attention to detail and knowledge of the specific tax laws applicable to the company's industry.After categorizing the financial data, the next step is to calculate the taxable income. This involves reviewing the income and expenses to determine the appropriate deductions, exemptions, and credits that can be claimed. It is important to ensure accuracy in the calculations to avoid any potential penalties or audits in the future. The taxable income calculation also involves considering any tax incentives orbenefits that the company may be eligible for, such as research and development credits or investment tax credits.Once the taxable income is determined, the next step is to prepare the tax return. This involves filling out the necessary forms and schedules, ensuring that all required information is included and accurate. It is essential to adhere to the specific formatting and reporting requirements specified by the tax authorities to avoid any processing delays or rejections. The tax return must include all applicable income, deductions, and credits, along with supporting documentation.After the tax return is prepared, it needs to be reviewed and verified for accuracy. This step involves a thorough examination of the return by a tax professional or accountant to identify any errors or discrepancies. It is crucial to ensure that all calculations are correct, and there are no omissions or inaccuracies that could raise red flags during an audit or inspection by the tax authorities.Finally, once the tax return is reviewed and verified, it is ready for submission to the tax authorities. This includes filing the returnelectronically or via mail, depending on the local tax regulations. It is important to meet all filing deadlines and comply with any payment requirements to avoid late fees or other penalties. The submission of the tax return marks the completion of the specialized tax process, with the assurance of compliance and accuracy.中文翻译:确认专税流程涉及一系列步骤,以确保合规性和准确性。

英国个人所得税研究

英国个人所得税英国个人所得税对居民就其来源于国内外的一切所得征税;对非居民仅就其来源于英国的所得征税。

英国个人所得税的计税依据是应税所得。

应税所得是指所得税分类表规定的各种源泉所得,各自扣除允许扣除的很必要费用后,加以汇总,再统一扣除生计费用后的余额。

英国居民个人就英国以外来源所得在英国以外缴纳的税 ( 限于直接的海外税 ) ,按照避免双重征税的协定或英国法律的单边规定给予税收抵免。

英国个人所得税以分类所得为基础采用对综合所得计税的办法。

应税所得分为六类,即①经营土地、建筑物等不动产所取得的租赁费、租赁佣金及类似支付的所得;②森林土地所得;③在英国境内支付的英国与外国公债利息所得;④工薪所得;⑤英国居民公司支付的股息红利所得;⑥经营及专业开业所得、外国的经营与财产所得,未经源泉扣缴的利息、养老金、特许权使用费所得、外国有价证券利息以及其他类型所得。

其纳税人分为常住居民、非常住居民、非居民三种。

居民指:①在英国征税年度内停留6个月以上;②连续5年中每年有3个月以上居住在英国;③在英国有住所,并在英国居住,不论其停留时间长短。

但自己全部时间在国外从事经营、其他职业或受雇佣者等除外。

④居民一般要按其在世界范围的所得纳税,居民如果具有英国国籍法规定的英国人资格,可在计算应税所得时享受基本生活扣除待遇。

非居民则仅就其在英国的源泉所得征税,一般不享有基本生活扣除待遇。

但是有英国人资格者可按其英国所得占其在世界所得的比例给予基本生活扣除。

纳税人应税所得的计算是将各类所得分别扣除其法定扣除项目(如经营所得的合格经营费用),求得各类所得(包括已从源泉征税的所得)的综合所得,再扣除生计费用后,即为实际应税所得。

允许扣除的生计费用包括:基础扣除、抚养扣除、劳动所得扣除、老年人扣除、病残者扣除、寡妇 ( 鳏夫 ) 扣除和捐款扣除等。

这些扣除项目的金额,按法律规定,每年随物价指数进行调整。

各类所得合并为综合所得时,允许依法冲抵盈亏(如经营亏损可以用总所得冲抵),然后依分级差额累进税率计征。

税收及会计报表英语词汇

税收报表英语词汇Accession Tax 财产增值税、财产增益税Additional Tax 附加税Admission Tax 入场税Allowable Tax Credit 税款可抵免税;准予扣除税额Amended Tax Return 修正后税款申报书Animal Slaughter Tax 动物屠宰税Annual Income Tax Return 年度所得税申报表Assessed Tax. 估定税额Assessment of Tax 税捐估定Asset Tax 资产税Back Tax 欠缴税款;未缴税额Business Tax (工商)营业税;工商税Capital Tax 资本税:<美>按资本额稽征;<英>指资本利得税和资本转让税(=[缩]CTT)<英>资本转让税Capital Transfer Tax 资本转移税;资本过户税Company Income Tax / Company Tax 公司所得税Corporate Profit Tax / Corporation Profit Tax 公司利润税;公司利得税Corporate Profits After Taxes <美>公司税后利润(额);公司税后收益(额)Corporate Profits Before Taxes <美>公司税前利润(额);公司税前收益(额)Corporation Tax Act <美>公司税法Corporation Tax Rate 公司税税率Deferred Income Tax 递延所得税Deferred Income Tax Liability 递延所得税负债Deferred Tax 递延税额;递延税额Development Tax 开发税;发展税Direct Tax 直接税Dividend Tax 股利税;股息税Earnings After Tax (=[缩]EAT)(纳)税后盈利;(纳)税后收益(额)Earnings Before Interest and Tax (=[缩]EBIT)缴付息税前收益额;息税前利润Effective Tax Rate 实际税率Employment Tax 就业税;职业税;雇用税Entertainment Tax 娱乐税;筵席捐Estate Tax 遗产税Estimated Income Tax Payable 估计应付所得税;预估应付所得税Estimated Tax 估计税金Exchange Tax 外汇税Excise Tax ①[国内]税;[国内]货物税②营业税;执照税Export Tax 出口税Export Tax Relief 出口税额减免Factory Payroll Taxes 工厂工薪税Factory Tax [产品]出厂税Fine for Tax Overdue 税款滞纳金Fine on Tax Makeup 补税罚款Franchise Tax 特许经营税;专营税Free of Income Tax (=[缩]f.i.t.)<美>免付所得税Import Tax 进口税Income Before Interest and Tax 利息前和税前收益Income After Taxes 税后收益;税后利润Income Tax ([缩]=IT)所得税Income Tax Benefit 所得税可退税款Income Tax Credit 所得税税额抵免Income Tax Deductions 所得税扣款;所得税减除额Income Tax Exemption 所得税免除额Income Tax Expense 所得税费用Income Tax Law 所得税法Income Tax Liability 所得税负债Income Tax on Enterprises 企业所得税Income Tax Payable 应付所得税Income Tax Prepaid 预交所得税Income Tax Rate 所得税率Income Tax Return 所得税申报表Income Tax Surcharge 所得附加税Income Tax Withholding 所得税代扣Increment Tax;Tax on Value Added 增值税Individual Income Tax Return 个人所得税申报表Individual Tax 个人税Inheritance Tax <美>继承税;遗产税;遗产继承税Investment Tax Credit (=[缩]ITC/I.T.C.)<美>投资税款减除额;投资税款宽减额;投资减税额Liability for Payroll Taxes 应付工薪税Local Tax / Rates 地方税Luxury Tax 奢侈(品)税Marginal Tax Rate 边际税率Notice of Tax Payment 缴税通知;纳税通知书Nuisance Tax <美>繁杂捐税;小额消费品税Payroll Tax 工薪税;工资税;<美>工薪税Payroll Tax Expense 工薪税支出;工资税支出Payroll Tax Return 工薪所得税申报书;工资所得税申报书Personal Income Tax 个人所得税Personal Income Tax Exemption 个人所得税免除Personal Tax 对人税;个人税;直接税Prepaid Tax 预付税捐Pretax Earnings 税前收益;税前盈余;税前盈利Pretax Income 税前收入;税前收益;税前所得Pretax Profit 税前利润Product Tax 产品税Production Tax 产品税;生产税Profit Tax 利得税;利润税Progressive Income Tax 累进所得税;累退所得税Progressive Income Tax rate 累进所得税率Progressive Tax 累进税Progressive Tax Rate 累进税率Property Tax 财产税Property Tax Payable 应付财产税Property Transfer Tax 财产转让税Rate of Taxation;Tax Rate 税率Reserve for Taxes 税捐准备(金)纳税准备(金)Retail Taxes 零售税Sales Tax 销售税;营业税Tax Accountant 税务会计师Tax Accounting 税务会计Tax Accrual Workpaper 应计税金计算表Tax Accruals 应计税金;应计税款Tax Accrued / Accrued Taxes 应计税收Tax Administration 税务管理Tax Audit 税务审计;税务稽核Tax Authority 税务当局Tax Benefit <美>纳税利益Tax Benefit Deferred 递延税款抵免Tax Bracket 税(收等)级;税别;税阶;税档Tax Collector 收税员Tax Credits <美>税款扣除数;税款减除数Tax Deductible Expense 税收可减费用Tax Deductions <美>课税所得额扣除数Tax Due (到期)应付税款Tax Evasion 逃税;漏税;偷税Tax Exemption / Exemption of Tax/ Tax Free 免税(额)Tax Law 税法Tax Liability 纳税义务Tax Loss 纳税损失;税损Tax on Capital Profit 资本利得税;资本利润税Tax on Dividends 股息税;红利税Tax Payment 支付税款;纳税Tax Penalty 税务罚款Tax Rate Reduction 降低税率Tax Rebate (出口)退税Tax Refund 退还税款Tax Return 税款申报书;纳税申报表Tax Savings 税金节约额Tax Withheld 扣缴税款;已预扣税款Tax Year 课税年度;纳税年度Taxable 可征税的;应纳税的Taxable Earnings 应税收入Taxable Income (=[缩]TI)可征税收入(额);应(课)税所得(额);应(课)税收益(额)Taxable Profit 应(课)税利润Taxation Guideline 税务方针;税务指南Taxes Payable 应缴税金,应付税款Tax-exempt Income 免税收入;免税收益;免税所得Tax-free Profit 免税利润Taxpayer 纳税人Transaction Tax 交易税;流通税Transfer Tax ①转让税;过户税②交易税Turnover Tax 周转税;交易税Undistributed Taxable Income 未分配课税所得;未分配应税收益Untaxed Income 未纳税所得;未上税收益Use Tax 使用税Value Added Tax (=[缩]VAT)增值税Wage Bracket Withholding Table 工新阶层扣税表Withholding Income Tax <美>预扣所得税;代扣所得税Withholding of Tax at Source 从源扣缴税款Withholding Statement 扣款清单;扣缴凭单Withholding Tax 预扣税款Withholding Tax Form (代扣所得税表)English Language Word or Term Chinese Language Word or TermINDIVIDUAL INCOME TAX WITHHOLDING RETURN 扣缴个人所得税报告表Withholding agent's file number 扣缴义务人编码Date of filing 填表日期Day 日Month 月Year 年Monetary Unit 金额单位RMB Yuan 人民币元This return is designed in accordance with the provisions of Article 9 of INDIVIDUAL INCOME TAX LAW OF THE PEOPLE'S REPUBLIC OF CHINA. The withholding agents should turn the tax withheld over to the State Treasury and file the return with the local tax authorities within seven days after the end of the taxable month.根据《中华人民共和国个人所得税法》第九条的规定,制定本表,扣缴义务人应将本月扣缴的税款在次月七日内缴入国库,并向当地税务机关报送本表。

VAT

Regressive Vs Progressive taxes

• Progressive tax – the more you earn the higher the tax rate – eg income tax • Regressive tax – the less you earn the higher the tax rate – eg VAT • Moral issues raised – should everyone pay the same? Who should bear tax? • What kind of tax do you think could be seen to be a disincentive to labour? How far do you think this is the case?

VAT

VAT

• • • • Theory of indirect and direct taxes Who bears VAT? What is VAT charged on? Who must register for VAT?

Direct vs. indirect taxes

• Direct taxes – charged on income, capital or gains • Deducted at source or paid directly to tax authorities • Indirect Taxes – taxes on spending – paid to vendor • Vendor’s responsibility to account for the tax

VAT

• VAT is an indirect tax charged on supplies • Supplies can be: • Zero rated • Exempt • Standard rated

税务英语文章

税务英语文章以下是一篇关于税务英语的文章,供参考:Taxation is a critical component of any country's financial system. It provides the government with the funds necessary to operate and provide essential services to its citizens. Tax laws and regulations are complex and can be difficult to understand, particularly for non-native speakers of English. For this reason, it is important for tax professionals to have a strong understanding of English tax terminology and concepts.One of the key concepts in taxation is the tax base. This refers to the value or amount of income, property, goods, or services that are subject to taxation. The tax base is used to calculate the amount of tax owed by an individual or organization. Different types of taxes may have different tax bases. For example, income tax is typically based on a person's taxable income, while sales tax is based on the price of goods or services sold.Another important concept is tax credits. These are deductions from the amount of tax owed, and they can be applied for a variety of reasons. For example, a tax credit may be available for education expenses, charitable donations, or energy-efficient home improvements. Tax credits can help reduce the amount of tax owed and can be particularly valuable for low-income taxpayers.Tax evasion is a serious crime in many countries, and tax authorities use a variety of methods to detect potential tax fraud. One of the mostcommon methods is through audits, which involve a review of an individual or organization's financial records to ensure that all income and deductions have been reported accurately. Tax authorities may also use computer algorithms to detect potential fraud.Taxation is a complex and ever-changing field, and it is important for tax professionals to stay up-to-date with the latest laws and regulations. English-language tax resources, such as tax journals and online databases, can be valuable tools for keeping informed about changes in the tax landscape.In conclusion, a strong understanding of tax terminology and concepts is essential for tax professionals working in an English-speaking context. With the right training and resources, tax professionals can navigate the complex world of taxation and ensure that their clients are in compliance with tax laws and regulations.以下是另一篇关于税务英语的文章,供参考:As businesses expand globally, tax professionals must navigate the complexities of international tax laws and regulations. English plays a critical role in this field, as it is the primary language used in many international tax agreements and treaties.One of the key concepts in international taxation is transfer pricing. This refers to the practice of pricing goods and services between affiliated companies in different countries. Transfer pricing can be used to shiftprofits to countries with lower tax rates, and as a result, it has become a major area of concern for tax authorities around the world. Transfer pricing rules are complex and can vary by country, so it is important for tax professionals to have a strong understanding of the relevant terminology and concepts in English.Another important concept in international taxation is the permanent establishment. This refers to a fixed place of business in a foreign country, such as a branch office or factory. When a business has a permanent establishment in a foreign country, it may be subject to taxes in that country. The rules for determining whether a permanent establishment exists can be complicated, so tax professionals must be familiar with the relevant English-language tax treaties and laws.Tax treaties are a critical component of international taxation, as they provide a framework for avoiding double taxation and resolving disputes between countries. Many tax treaties are written in English, so it is important for tax professionals to have a strong understanding of the relevant terminology and concepts. Some common terms that appear in tax treaties include "taxable presence," "dividends," and "withholding tax."In addition to tax treaties, there are also international tax organizations that play a key role in shaping tax policy around the world. These organizations, such as the Organization for Economic Cooperationand Development (OECD), publish guidelines and recommendations for countries to follow in order to ensure consistency and fairness in international taxation.In conclusion, international taxation is a complex and rapidly-changing field. Tax professionals must have a strong understanding of English tax terminology and concepts in order to navigate the complex web of tax laws and regulations. With the right training and resources, tax professionals can stay up-to-date with the latest developments in international taxation and provide valuable advice to their clients.。

财税英语专用词汇

财税英语--税收专用词汇State Administration for Taxation 国家税务总局Local Taxation bureau 地方税务局Nationwide Taxation Departments 全国税务系统State Council 国务院Ministry of Finance 财政部Business Tax 营业税Individual Income Tax 个人所得税Income Tax for Enterprises企业所得税Income Tax for Enterprises with Foreign Investment and Foreign Enterprises外商投资企业和外国企业所得税deed tax 契税stamp tax 印花税tax returns filing 纳税申报taxes payable 应交税金the assessable period for tax payment 纳税期限the timing of tax liability arising 纳税义务发生时间consolidate reporting 合并申报the local competent tax authority 当地主管税务机关the outbound business activity 外出经营活动Tax Inspection Report 纳税检查报告tax avoidance 避税tax evasion 逃税tax base 税基refund after collection 先征后退withhold and remit tax 代扣代缴collect and remit tax 代收代缴income from authors remuneration 稿酬所得income from remuneration for personal service 劳务报酬所得income from lease of property 财产租赁所得income from transfer of property 财产转让所得contingent income 偶然所得resident 居民non-resident 非居民tax year 纳税年度temporary trips out of 临时离境flat rate 比例税率withholding income tax 预提税withholding at source 源泉扣缴State Treasury 国库tax preference 税收优惠the first profit-making year 第一个获利年度refund of the income tax paid on the reinvested amount 再投资退税export-oriented enterprise 出口型企业technologically advanced enterprise 先进技术企业Special Economic Zone 经济特区tax transparency 税收透明度registration duties 注册税subscription tax 认购税foreign investment and foreign enterprises 外商投资和外国企业pre-tax deduction 税前扣除tax payment for loan repayment 以税还贷rational tax burden 合理税负proactive fiscal policy 积极财政政策rural tax for fee reform 农村税费改革。

税收专业英文选读

税收专业英文选读Taxation: A Modern PerspectiveTaxation is a topic that has been prevalent in the public discourse of modern society. It’s a crucial piece of fiscal policy that helps fund many important social programs, but also can be controversial due to its effects on businesses and individuals. As such, taxation is a complex issue with myriad facets and outcomes, making it an important subjectfor students and professionals alike.This compilation of readings presents an overview of taxation from multiple perspectives, including historical, economic, and sociological. It offers a comprehensive introduction to the history, goals, and challenges oftaxation as well as insights into the various approaches taken by governments and individuals to manage its implications.The readings begin with a brief overview of the history of taxation, tracing the development of the practice from ancient times to the present. The discussion then focuses on taxation fundamentals, explaining important concepts and terms, such as tax brackets and escalations. From there, readers are introduced to modern methodologies forcalculating tax liabilities and the various forms of tax relief available.In addition, the collection covers the diverse approaches countries around the world have taken to taxation, from progressive income taxes to flat taxes. Other topics discussed include deductions, exemptions, capital gains, andconsumption taxes. Finally, it looks at tax compliance, including strategies used to reduce avoidance and evasion, and the role of technology in moving towards more efficient tax systems.This compilation of readings provides an invaluable resource to those wishing to gain a better understanding of taxation and its implications. With its comprehensive coverage, insightful explanations, and clear presentation of the complexities of this important field, it is an essential resource for students and professionals alike.。

会计学(第21版)课件:Income Taxes, Unusual Income Tax Items

3. Revenues or gains are taxed before they are reported on the income statement.

corner of the screen. You can point and click anywhere on the screen.

Objectives

1. Journalize the entries for corporate income taxAefste,rinsctuluddying tdheisferred income taxes. chapter, you should

21 000 00 21 000 00

Corporate Income Taxes

Ratio of Reported Income Tax Expense to Earnings

Before Taxes for Selected Industries

Automobiles

33%

Banking

35

Computers

4. Expenses or losses are deducted in determining taxable income before they are reported in the income statement.

Temporary Differences

✓ Differences in tax law and GAAP create some temporary differences that reverse in later years.

WithholdingVATorVATDeductionatSource(VDS)

Withholding Services

1. S002.00 – Decorators & Caterers (15%) 2. S003.10 – Motor Garage & workshop (7.5%) 3. S003.20 – Dockyard (7.5%) 4. S004.00 – Construction Firm (5.5%) 5. S007.00 – Advertising Firm (15%) 6. S008.10 – Printing Press (15%) 7. S009.00 – Auctioneer (15%) 8. S010.10 – Land Developer (3%) 9. S010.10 – Building Developer (3%) 10. S014.00 – Indenting Firm (15%) 11. S020.00 – Survey Firm (15%) 12. S021.00 – Plant & Capital Machinery renting firm (15%)

Use proper Economic Code 1/1133/0000/0311 Third 4-digits is the code of concern VAT

Commissionerate where the WE located. The Co issio erate’s ode are: 1 Khul a - 0001, (2)

6

Withholding Services

13. S024.00 – Furniture Sales Center Manufacturing - 6% Trading – 4% (if invoice of manufacturing is there)

用英语介绍自己对税收的认识

Knowledge about tax I knowI am a lively girl come from Henan province, whose name is Xiao Lina. Even though obedient as I am in the eyes of elder member of my family, actually, I usually behave naughty, especially along with my close friends. Because friendship is a vital part of my life, and I believe that as long as I treat others sincerely, can we get along even share joys and sorrows with each other. Now, I study in Jiangxi University of Finance and Economics, majoring in tax. As a professional tax stu dent, today I will introduce some basics of tax that I learn in schonol.Tax is a way of that the state in order to meet social public needs, relying on public power, according to the standard stipulated in the laws and procedures, participate in national income allocation, and get financial revenue by force.Because of the differences of attribution归属, collection收集and management in accordance 协调with the tax revenue, Chinese tax system can be divided into two different sections: national tax and local tax. The former is distinct necessary to maintain national rights. The latter is mainly responsible for the appropriate local taxes in order to increase the local finance income.Tax refers to the transactions事项、事物、交易that relate to tax. General tax include: the concept of the tax law, the essence of tax, the origin of tax and the functions of tax. LFirst, the concept of the tax law is files which the departments of state power and administrative行政的agency adjust the relationship about tax. Its core content is the allocation分配of tax benefits.Second, the nature of the tax is a form of a country to allocate the social products according to political power and public power. The most important effect of allocation of tax is to meet social public needs, through its three obvious characteristics: not directly to repay, mandatory强制性and solid无偿性.Third, tax is along with the produce of the country. First of all, enough social products lay a good material foundation. Additionally, the whole social have independent economic interest and tax can meet kinds of public needs. Most importantly, public power provides the upper conditions for the appearance of tax revenue. Of course, Chinese tax revenue has a long and rich history. Since 594 BC in thespring and autumn period the earliest tax was established with the private ownership of land.Forth, tax function refers to the inner influence. Under certain conditions, the functions of tax are mainly manifested表现in the following aspects:Tax is the main source of revenue, so organization becomes the basic function of tax revenue. Owing to tax’s three characteristics of gratuitous,无偿性mandatory and solid that raising finance income becomes stable and reliable, while making it the world's governments the basic form of organizing financial revenue. For instance, our country tax revenue accounts for more than 90% of the national financial revenue.Tax is an important means of regulating and controlling economic operation. Namely is, tax and economic interact each other closely. This not only reflects the economy is the source of tax revenue, but also reflects the tax's regulatory role of the economy. Taxation as an economic lever, by raising or reducing taxes to affect the economic interests of the members of the community, such as guidance to the enterprises企事业单位and individual economic behavior, impact on resource allocation and social economydevelopment, so as to achieve the purpose of the regulation of economic operation. The government makes good use of tax means, both can adjust the macro economy, also can adjust the economic structure.Tax is an important tool to adjust income distribution. From over all, as a country’s significant method to participate in the national tax income distribution in the form of the main and the most standard, to standardize the relationship between the government, enterprises and individuals, different tax plays a different role in the field of distribution. Such as extra progressive累进tax rate is appropriate for the individual income tax, high earners high taxes and low earners low taxes, thus, to promote social justice.Besides, tax also has the function to control economic activities, involving in social production’s distribution and consumption fields, to reflect the quality and efficiency of national economy. On the one hand, through tax revenue increase or decrease and the change of tax sources, we can timely grasp the trend of the development of the macro economy. On the other hand, we can understand the status of the microeconomic in tax collection and administration activities, with the aim of finding and correcting the problems existing in theproduction operation and financial management, so as to promote the sustainable and healthy development of national economy.Tax is everywhere and every citizen has the duty to pay taxes legally, in fact, we have been doing it virtually. Only all the Chinese people join together observing law and discipline, can we make our country more thriving and powerful.。

银行业务英语词汇

银行业务英语词汇会计账目用语会计报表statement of account往来帐目account current此刻往来帐||存款额current accout销货帐account sales共同计算帐项joint account未决帐项outstanding account贷方帐项credit account||creditor account借方帐项debit account||debtor account应付帐||应付未付帐account payable应收帐||应收未收帐account receivable新交易||新帐new account未决帐||老帐old account现金帐cash account流水帐running account呆帐bad account会计工程title of account借贷细帐||交验帐account rendered继续记帐to keep account与... 有交易to have an account with清算||清理债务to make up an account清洁帐目||与... 遏制交易to close one's account with结帐to close an account结清差额to balance the account with查抄帐目to examine an account转入A的帐户to charge the amount to A's account以计帐方式付款to pay on account代办署理某人||为某人on one's account||on account of one 为本身计算||独立帐目on one's own account支票用语支票薄cheque book支票陈票人cheque drawer持票人cheque holder不记名支票cheque to bearer||bearer cheque记名支票||认人支票cheque to order到期支票antedated cheque未到期支票postdated cheque保付支票certified cheque未获兑现支票,退票returned cheque空白支票blank cheque掉效支票,过期支票stale cheque普通支票open cheque支票换现金||兑现to cash a cheque清理票款to clear a cheque包管兑现to certify a cheque支票退票to dishonour a cheque拒付支票to refuse a cheque拒付支票to stop payment of a cheque提示要求付款to present for payment支付指定人payable to order已过期||无效out of date||stale请给出票人R/D||refer to drawer存款缺乏N/S||N.S.F.||not sufficient funds||I/F||insufficient funds 文字与数字不一致words and figures differ更改处应加盖印章alterations require initials交换时间已过effects not cleared遏制付款payment stopped支票毁损cheque mutilated汇款用语汇款||寄钱to remit||to send money寄票供取款||支票支付to send a cheque for payment寄款人a remitter收款人a remittee汇票汇单用语国外汇票foreign Bill国内汇票inland Bill跟单汇票documentary bill空头汇票accommodation bill原始汇票original bill改写||换新单据renewed bill电汇telegraphic transfer (T.T)担保书trust receipt||letter of indemnity承兑||认付acceptance单张承兑general acceptance有条件承兑qualified acceptance附条件认付conditional acceptance局部认付partial acceptance拒付||退票dishonour由于存款缺乏而退票dihonour by non-payment提交presentation期满||到期maturity托收collection外汇行情exchange quotation现汇汇率spot rate持久汇率long rate私人汇票折扣率rate on a private bill远期汇票兑换率forward rate付款汇率pence rate当日汇率||成交价currency rate套汇||套价||公断交易率arbitrage收到汇款to receive remittance填写收据to make out a receipt付款用语付款方法mode of payment现金付款payment by cash||cash payment||payment by ready cash 以支票支付payment by cheque以汇票支付payment by bill以物品支付payment in kind付清||支付全部货款payment in full||full payment按期付款payment on term年分期付款annual payment预付货||先付payment in advance||prepayment延付货款deferred payment当即付款prompt payment||immediate payment暂付款suspense payment延期付款delay in payment||extension of payment结帐||清算||支付settlement分期付款instalment滞付||拖欠||尾数款未付arrears特许迟延付款日days of grace包管付款del credere付款to pay||to make payment||to make effect payment结帐to settle||to make settlement||to make effect settlement||to square||to balance支出||付款to defray||to disburse结清to clear off||to pya off迟延付款to defer payment||to delay payment付款被迟延to be in arrears with payment还债to discharge迅速付款to pay promptly付款颇为恶劣to pay very badly||to never pay unless forced拒绝付款to refuse payment||to refuse to pay||to dishonour a bill惠请付款kindly pay the amount||please forward payment||please forward a cheque.索取利息to charge interest附上利息to draw interest||to bear interest||to allow interest生息to yield interest生息3% to yield 3%存款to deposit in a bank||to put in a bank||to place on deposit||to make deposit在银行存款to have money in a bank||to have a bank account||to have money on deposit 向银行提款to withdraw one's deposit from a bank换取现金to convert into money||to turn into cash||to realize打折扣购置to buy at a discount打折扣出售to sell at a discount打折扣-让价to reduce||to make a reduction减价to deduct||to make a deduction回扣to rebate现金折扣cash discount货到付款||现金提货cash on deliver (C.O.D.)货到付现款cash on arrival即时付款prompt cash净价||最低价格付现net cash现金付款ready cash即期付款spot cash||cash down||cash on the nail笔据据付现款cash against documents凭提单付现款cash against bills of lading承兑交单documents against acceptance (D/A)付款交单documents against payment (D/P)信用证用语追加信用证additional credit||additional L/C信用证金额amount of credit赊帐金额credit balance可裁撤信用证revocable L/C不成裁撤信用证irrevocable L/C保兑信用证confirmed L/C不保兑信用证unconfirmed L/C可转让信用证assignable L/C||transferable L/C无条件信用证open credit||free credit普通信用证general letter of credit旅行信用证circular letter of credit出格信用证special letter of credit信用证底帐letter of credit ledger信用证发行帐letter of credit issued account信用证金额amount of creditWhat kind of account did you have in your mind 你想开哪种帐户?Do you like to open a current account你想开一个活期存款帐户吗?A deposit or current account按期还是活期?Please tell me how you would like to deposit your money.请告诉我你想存何种户头?There's a service charge for the checking account but no charge for the savings. 支票户头要收效劳费,现金户头不收。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

….Few Examples

Q. Difference if licensed in CD or downloaded from internet?

Q.

What if upgraded versions are provided?

Slide 12

Clear distinction between right to use copyright vs. copyrighted material (upheld by ITAT in Lucent / Samsung cases)

Slide 9 PricewaterhouseCoopers

…. Royalty Definition

Slide 8

PricewaterhouseCoopers

…. Royalty Definition

What are copyright? Right to make copies of computer program for purposes of distribution to the public by sale or other transfer of ownership, or by rental, lease or lending; Right to prepare derivative computer programs based upon the copyrighted computer program; Right to make public performance of the computer program; or Right to publicly display the computer program

Slide 4 PricewaterhouseCoopers

….Section 195

Scope of Word Paid – “Material date: Art. 12 fails to settle the question as to the point of time at which royalties may be taxed. However, restrictions that the DTC imposes on taxation must be observed even in cases where domestic law provides for taxation during an assessment period that is earlier or later than that during which the ‘payment’ was made (= received)” Deduction required at the time of making provision itself, actual payment not a pre-requisite. [Flakt (India) Ltd. (2004) 267 ITR 727 (AAR)].

Pricew

Example 2 Facts Readymade software Right to use for limited period - not perpetual To return software on completion of period To destroy copies after completion of period Analysis No copyright right transferred Case of right to use copyrighted article Q. What if program gets deactivated automatically after the completion of period?

What is use of secret formula or process? Imparting information about ideas and principles underlying the program viz. logic, algorithms or programming language or techniques may be characterized as right to ‘use secret formula’ [OECD Commentary] What is industrial, commercial or scientific experience? Imparting of information concerning technical, industrial, commercial or scientific knowledge, experience or skill alludes the concept of making available know-how.

Slide 5

PricewaterhouseCoopers

TDS on Software Payments

PricewaterhouseCoopers

Royalty Definition

Payment for right to use copyright of a literary, artistic or scientific work right to use secret formula or process information concerning industrial, commercial or scientific experience [OECD Model] What is ‘right to use’? Royalty in respect of license ‘to use’ ….is income to recipient from letting [OECD Commentary] Phrase interpreted to mean a “leasing transaction” [Memorandum explaining Finance Act 2001] Letting/leasing would envisage separation of ownership of an asset and its possession [Madras H.C. (133 ITR 922)]

Slide 3 PricewaterhouseCoopers

….Section 195

TDS at the time of credit or payment CJ International Hotels Ltd. (Delhi ITAT) Shree Sajjan Mills Ltd. (SC) Can TDS obligation arise only at the time of payment? Treaty requires taxation in relation to royalties / FTS arising in source State and paid to resident of the other State “Royalties and fees for technical services arising in a Contracting State and paid to resident of the other Contracting State may be taxed in that other State Notwithstanding the provisions of Paragraph (1), such royalties and fees for technical services may also be taxed in the Contracting State in which they arise, ……”

Presentation on Tax Deduction at Source

By Rajiv Anand Associate Director

September 9, 2005

Presentation Outline

• TDS on payments to non residents for

(a) Software (b) Satellite Connectivity

• Other TDS issues

• Implications of non-compliance of TDS

provisions

Slide 2

PricewaterhouseCoopers

Section 195

Applies only when following conditions are fulfilled: Payment is in nature of income in the hands of non-resident; Such income is taxable in India; and At the time of credit or payment Payment must be in the nature of “Income” Ericsson Communications Ltd. (Delhi ITAT) Transmission Corporation of AP Ltd. (SC) Payment must be “Taxable in India” Option to choose between DTA and ITA, 1961 Two Case Studies • Software Payments • Satellite Connectivity Payments

Slide 10

PricewaterhouseCoopers

Few Examples

Example 1 Facts Readymade software Perpetual license Transferee received right to use for business purposes Right to make copy for utilization of software Right to sell the software to third party after destroying other copies Same conditions imposed on third party Analysis No copyright rights transferred to transferee Case of sale of copyrighted article