ACCAF知识点总结

acca f知识要点汇总(精简版)

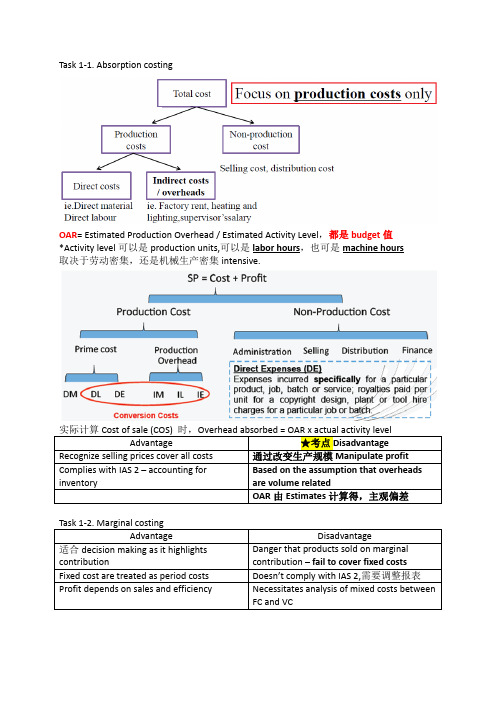

☆技巧 AC = MC + (Closing Inventory – Opening Inventory) x OAR *The absorption costing requires subjective judgments.预算估计主观判断太多 *There is often more than one way to allocate the overheads.制造成本分摊可操纵

Arbitrary apportionment 任意分配

★考点‐计算题(10.Dec.Q4)

Problems when implementing ABC:

‐ 耗时

‐ 需要上层支持,因为缺乏信息

‐ Project team 运作,成员来自各个部门

‐ IT 部门支持

‐ 了解成本结构

‐ Cost‐benefit analysis★成本效益分析

Maturity

Sales volume: Stable high volume

主要:

Initially profits keep increase as initial set‐up and fixed costs are recovered

材料人工等 Marketing and distribution economies are achieved

适合 decision making as it highlights contribution Fixed cost are treated as period costs Profit depends on sales and efficiency

Disadvantage Danger that products sold on marginal contribution – fail to cover fixed costs Doesn’t comply with IAS 2,需要调整报表 Necessitates analysis of mixed costs between FC and VC

ACCAF3考试知识点汇总

2015 年12 月ACCA F3考试知识点汇总☆Types of business entity A business can be organized in one of the several ways: ●Sole trader –a business owned and operated by one person.The simple form of business is the sole trader. This is owned and managed by one person, although there might be any number of employees. A sole trader is fully personall y liable for any losses that the business might make.●Partnership –a business owned and operated by two or more people.A partnership is a business owned jointly by a number of partners. The partners are jointly and severely liable for any losses that the business might make. (Traditionally the big accounting firms have been partnerships, although some are con verting their status to limited liability companies.)●Limited Liability Company –a business owned by many people and operated by m any ( though not necessarily the same) people. Companies are owned by shareholders. Sha reholders are also known as members. As a group, they elect the directors who run the b usiness. Companies are always limited companies.In summary, types of business entity should be differentiated in Ownership; Operation right and Liability for the business to undertake.For all three types of entity, the money put up by the individual, the partners or the shareholders, is referred to as the business capital. In the case of a company, this capital is divided into shares. ☆Business Transactions: Main types of business transactions for a business include:●Purchase of inventory for resale●Sales of goods●Purchase of non-current assets●Payment of expenses●Introduction of new capital to the business●Withdrawal of funds from the business by the owner☆Cash and credit transactions:Cash transactions: the buyer pays for the item immediately or possibly in advance. Credit transactions: the buyer does not have to pay for the item on receipt, but is all owed some time ( a credit period) before having to make the payment.☆Definition of accountingRecording : transactions must be recorded as they occur in order to provide up-to-dat e information for management.Summarizing: the transactions for a period are summarized in order to provide inform ation about the company to interested parties.☆Types of accountingFinancial accounting vs management accountingAccounting reports users include:●Management: Need information about the company’s financial situation as it is curre ntly and it is expected to be in the future. This is to enable them to manage the business efficiently and to make effective decisions.●Investors: The providers of risk, capital and their advisers are concerned with theris k inherent in, and return provided by, their investments. They need information to help th em determine whether they should buy, hold or sell.●Trade payables/ Suppliers: Suppliers and other trade payables. Suppliers and other tr ade payables are interested in information that enables them to determine whether amounts owing to them will be paid when due. Trade payables are likely to be interested in an enterprise over a shorter period than lenders unless they are dependent upon the continuanc e of an enterprise as a major customer.●Shareholders: Shareholders are also interested in market value of shares as well as information which enables them to assess the ability of the enterprise to pay dividends.●Lenders: Lenders are interested in information that enables them to determine wheth er their loans, and the interest attaching to them, will be paid when due.●Customers: Customers have an interest in information about the continuance of an e nterprise, especially when they have a long term involvement with or are dependent on, th e enterprise.●Government and their agencies: Governments are their agencies are interested in the allocation of resources and, therefore, the activities of enterprises. They also require infor mation in order to regulate the activities of enterprises, determine taxation policies and as the basis for national income and similar statistics.●Employees: Employees and their representative groups are interested in information a bout the stability and profitability of their employers. They are also interested in informati on which enables them to assess the ability of the enterprise to prove remuneration, retire ment benefits and employment opportunities.●General public: Enterprises affect members of the public in an variety of ways. For example, enterprises may make a substantial contribution to the local economy in many ways including the number of people they employ and their patronage of local suppliers. Financial statements may assist the public by providing information about the trends and recent developments in the prosperity of the enterprise and the range of its activities.☆The business entity conceptThe business entity concept●States that financial accounting information relates only to the activities of the busin ess entity and not to the activities of its owner.●The business entity is treated as separate from its owners.☆Financial Statements include:- a statement of financial position at the end of the period- a statement of comprehensive income for the period- a statement of changes in equity for the period- statement of cash flows for the period- notes, comprising a summary of accounting policies and other explanatory notes The statement of financial position:Statement of Financial Position: showing the financial position of a business at a poin t of time. The Vertical format of the SFP: (Statement of Financial Position as at31 December 2007)●The top half of the balance sheet shows the assets of the business.●The bottom half of the balance sheet shows the capital and liabilities of the busines s.A Statement of financial position at the end of the period (Balance Sheet): W Xang Balance Sheet as at December 31 20X6The horizontal format of the SFP: (Statement of Financial Position as at 31 Decembe r 2007)●The left half of the balance sheet shows the assets of the business.●The right half of the balance sheet shows the capital and liabilities of the business. W XangStatement of Financial Position as at 31 December 20x6☆The accounting equationFinancial accounting is based upon a very simple idea:The amount of resources supplied by the owner is called capital. The actual resources that are then in the business are called assets. Usually, people other than the owner have supplied some, of the assets, for example, a supplier supplies stock of goods on credit. The business is said to owe a liability towards these suppliers. The following accounting equation always holds true:The accounting equation:ASSETS = PROPRITOR’S CAPITAL + LIABILITIES- Any point in time, the assets of the business will be equal to its liabilities plus the capital of the business;- Assets less liabilities equal the capital of the business, which is known as netassets. - Each and every transaction that the business makes or enters into has two aspects to it and have a double effect on the business and the accounting equation. This is known as the duality concept.Duality concept: Each and every transaction that the business makes or enters into ha s two aspects to it and has a double effect on the business and the accounting equations. This is known as duality concept.if A=C+L=0 .......①C=A-L........②Illustration:1). Carl sets up in business by opening a coffee shop –Carl’s Coffee. He puts $5,00 0 into a business bank account.The opening accounting equation is:Assets (Cash in bank)= Capital + Liabilities($5,000) = ($5,000) + ($0)2). Carl buys furniture (chairs and tables) for the shop for $1,500, paying the supplie r out of the business bank account.The accounting equation after this transaction is:Assets Capital + Liabilties( Cash in bank $3,500) = ($5,000) ($0)(Furniture $ 1,500)3). Now Carl spends a further $2,000 to buy coffee-making equipment and $800 on crockery and cutlery, paying cash out of the business bank account.The accounting equation after this transaction is:Assets Capital + Liabilties(Cash in Bank $700) = ($5,000) ($0)(Equipment $2,000)(Fitting & Fixture $800)(Furniture $1,500)4). Carl persuades his bank to lend $1,000 to develop the business. The bank loan is accounted for as a liability of the business.The accounting equation is now as follows:Assets Capital + Liabilties(Cash in Bank $1,700) = ($5,000) ($1,000)(Equipment $2,000)( Fitting & Fixture $800)(Furniture $ 1,500)5). Carl now buys coffee, tea, milk, sugar, biscuits and cakes for $700, and pays in cash from the business bank account.The accounting equation is now as follows:Assets Capital + Liabilties(Inventory $700) = ($5,000) ($1,000)(Equipment $2,000)(Fitting & Fixture $800)(Furniture $1,500)(Cash in Bank $ 1,000)6). In his first day of trading, Carl uses up $650 of his inventory, and makes sales t otaling $1,050. All his sales are in cash.The accounting equation at the end of the day is as follows:Assets Capital + Liabilities(Inventory $50) = (Beginning $5,000) ($1,000)(Equipment $2,000) ( Profit $400)(Fitting & Fixture $800)(Furniture $1,500)( Cash in bank $2,050)☆Classification of Assets and LiabilitiesAssets: An asset is something owned or controlled by the business that will result in future economic benefits to the business. ( an inflow of cash or other assets.) Such as:Current assets:are assets owned by the business with the intention of turning them int o cash within one year (accounting period).This definition allows inventory or receivables to quality as current assets, e ven if the y may not be realized into cash within 12 months.Non-current asset: is an asset held for and used in operation(rather than for selling to customer), with a view to earning income or making profits from its use, for over more than one year ( accounting period).Liability: is something owed by the business to someone else.Current liability: These include the debts of the business that are repayable within the next 12 months.Non-current liabilities: are liabilities that do not need to be settled for at least one ye ar. (excluding the current portion of the debt)Capital: Capital is a type of liability. It represents the owner’s net investment in the business. Capital appears as a credit balance on the balance sheet.Assets –Liabilities = PROPRIETOR’S CAPITALNet Assets =( T otal )Assets –(T otal) LiabilitiesCapital (at SFP date) = Capital introduced + Profit –DrawingsDrawing: Drawings are any amounts taken out of the business by the owner for their own personal use. Drawings will reduce the capital balance reported on the balance sheet.Include:●Money taken out of the business●Goods taken for personal use●Personal expenses paid by the businessIncome statementIncome statement:Mr. W XangIncome statement for the year ended 31 December 20X6●Showing the financial performance of a business over a period of time.●Reports revenue and expenses for the period.●The sales revenue shows the income from goods sold in the year●The cost of buying the goods sold must be deducted from the revenue●The current year’s sales will include goods bought in the previous year, so this ope ning inventory must be added to the current year’s purchases.●Some of this year’s purchases will be unsold at 31/12/20x6 and this closing invento ry must be deducted from purchases to be set off against next year’s sales.●The first part gives gross profit. The second part gives net profit.The I.S. prepared following the accruals concept.Accrual concept:●Income and expenses are recorded in the I.S. as they are earned / incurred regardles s of whether cash has been received/ paid.(Sales revenue: income from goods sold in the year, regardless of whether those good s have been paid for.)☆Relationship between a statement of financial position and a statement of income●The balance sheets are not isolated statements, they are linked over time with the in come statement●As the business records a profit in the income statement, that profit is added to the capital section of the balance sheet, along with any capital introduced. Cash taken out of the business by the proprietor, called drawings, is deducted. Illustration –the accounting equation:The transactions:Day 1 Avon commences business introduction $1,000 cash.Day 2 Buys a motor car for $400 cash.Day 3 Buys inventory for $200 cash.Day 4 Sells all the goods bought on Day 3 for $300 cash.Day 5 Buys inventory for $400 on credit.SFP at the end of each day’s transactions:Solution:Day 1 Assets (Cash $1,000) = Capital ($1,000) + Liabilities ($0)Day 2 Assets (Motor $400) = Capital ($1,000) + Liabilities ($0)(Cash $600)Day 3 Assets ( Inventory $200) = Capital($1,000) + Liabilities ($0)(Motor $400)(Cash $400)Day 4 Assets ( Motor$ 400) = Capital + Liabilities ($0)(Cash $700) (Beginning$1,000)(Profit $100)Day 5 Assets (Inventory $ 400) = Capital + Liabilities( Motor$ 400) (Beginning$1,000)($400)(Cash $700) (Profit $100)Avon Statement of Financial Position as at end of Day 5Example: Continuing from the illustration above, prepare the SFP at the end of each day after accounting for the transactions below:Day 6 Sells half of the goods bought on Day 5 on credit for $250.Day 7 Pays $200 to his supplier.Day 8 Receives $100 from a customer.Day 9 Proprietor draws $75 in cash.Day 10 Pays rent of $40 in cash.Day 11 Receives a loan of $600 repayable in two years.Day 12 Pays cash of $30 for insurance.Your starting point is the SFP at the end of Day 5, from the illustration above. Prepare: SFP at the end of Day 12I.S. for the first 12 days of trading.Solution:Day 6 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400) (Beginning$1,000)($400)(Cash $700) (Profit $150)(A/Receivable$250)Day 7 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400) (Beginning$1,000)($200)(Cash $500) (Profit $150)(A/Receivable$250)Day 8 Assets (Inventory $ 200) = Capital + Liabilities ( Motor$ 400) (Beginning$1,000)($200)(Cash $600) (Profit $150)(A/Receivable$150)Day 9 Assets (Inventory $ 200) = Capital + Liabilities ( Motor$ 400) (Beginning$1,000)($200)(Cash $525) (Profit $150)(A/Receivable$150) (Drawing $75)Day 10 Assets (Inventory $ 200) = Capital + Liabilities ( Motor$ 400) (Beginning$1,000)($200)(Cash $485) (Profit $110)(A/Receivable$150) (Drawing $75)Day 11 Assets (Inventory $ 200) = Capital + Liabilities ( Motor$ 400) (Beginning$1,000)($200)(Cash $1,085) (Profit $110) ($600)(A/Receivable$150) (Drawing $75)Day 12 Assets (Inventory $ 200) = Capital + Liabilities (Motor$ 400) (Beginning$1,000)($200)(Cash $1,055) (Profit $80 ) ($600)(A/Receivable$150) (Drawing $75)AvonStatement of Financial Position as at end of Day 12AvonIncome statement for the period ended at Day 12Session 3 Double entry bookkeeping☆The duality concept and double entry bookkeepingDuality concept: each and every transaction has a double effect on the business and t he accounting equations.(A= C + L)Rules of double entry bookkeeping:●Each time a transaction is recorded, both effects must be taken into account.●These two effects are equal and opposite such that the accounting equation will al ways prove correct.Assets –Liabilities = Capital●Traditionally, one effect is referred to as the debit side ( Dr.) and the other as the credit side of the entry (Cr.)☆Ledger accounts, debits and creditsLedger account:●transactions are recorded in the relevant ledger accounts. There is a ledger account for each asset, liability, revenue and expenses’item, and for the owner’s capi tal.●Each account has two sides: the debit and credit sides.●The duality concept means that each transaction will affect two ledger accounts ●One account will be debited and the other credited●Whether an entry is to debit or credit side of an account depend on the types of account and the transaction.。

ACCA F 知识要点汇总 精简版

IAS8 IAS10

Accounting Policies, Changes in Accounting Estimates and Errors

Events after reporting period

IAS11 Construction Contract

* 流动资产一般自带减值

Take the higher of * Value in use (futher benefit through use 并折现)

* Fair Value less cost to sell

* Negative G/W,直接credit to P&L,从而credit to

COS从Loss倒推)

20)*75%=15.所以revenue=100*75%=75,

cost=80*75%=60, 分录:Cr CC 60,Dr GADFC 75, Dr COS 60,Cr

Revenue 75. 继上:Progress billing=70→Dr T/R 70, Cr GADFC

5种典型例子:

举例:100送20优

1) Commision ‐ 佣金 2) Deferred Income ‐ 3年学费1次支付 3) Sale & Return base ‐ 只有卖了不能退,才确认为销售(举

1) Dr Bank 5(or T/R),Cr T/P 4,Cr Revenue 1 2) Dr Bank 6, Cr deferred income 4,Cr Revenue 2 3) Dr Revenue 24, Cr T/R 24; Dr Inventory 18, Cr

举例:Total price=100, Cost todate=60, Further

ACCAF3考试重要知识点和考点梳理

ACCA F3考试重要知识点和考点梳理考察形式1.选择题:2’*35=70’。

包括文字题和计算题。

2.大题:15’*2=30’。

通常是编制两张报表,即SFP,P&L,CFS,CSFP,CP&L,四选二,但是,报表题目也可能以小题的形式出现在选择题,即考查编制报表时的各个working。

知识梳理及重要考点F3,financial accounting, 整本教材的编制顺序,遵照账务处理顺序,如下所示:Chapter1-4:介绍财务会计基础知识。

(1)会计做账主体为企业,即business。

(2)Sole trader, partnership和Limited liabilitycompany各自的特点。

(3)Financial accounting和management accounting的区别。

(4)Accounting equation(5)7种book of prime entry(6)会计5要素及做账原则,即借贷方表示增/减。

(7)Balancing and closing of T accountChapter5-13:常见账户的会计处理,即double entry。

(1) Chapter 5:Returns, discounts and sales tax。

本章主要考查trade discount和early settlement discount的会计处理及这两种折扣情况下如何计算sales tax,即均以折扣后的净值作为计税基础。

而sales revenue的金额,对于trade discount,以折扣后净值确认,对于early settlementdiscount则以折扣前的总数确认;sales tax liability的计算,即output tax减去input tax。

(2)Chapter 6:Inventory。

本章主要考查valuation of inventory,即lower of cost and NRV;adjustment of openingand closing inventory。

ACCAF4知识点总结

ACCAF4知识点总结Chapter11.民法(civil law)和刑法(criminal law)的划分Civil law: an form of private law,used by individuals to assert rights against other individualsCriminal law: an aspect of public law to regulate crimes and to punish offenders1.legislation(made by the Parliament)/secondary legislation( in exercise of law-making powers delegated by Parliament). [注:Necessity for delegated legislation/secondary legislation :more convenient ;can hand over the task of specifying the law in detailto experts]2.在case law中:common law普通法[created by judges through theapplication of the principle of judicial precedent. common lawdrew on customs/equity law衡平法:to resolve disputes where damages are not a suitable remedy and to introduce fairness intothe legal system.]2.不同法院管辖事件的类型Chapter2Chapter21.Doctrine of Precedence(遵循先例制度的一般规则): somedecisions made by a court are binding and similar subsequent legal cases should be decided on the basis of the law established in earlier cases.2.可以创立判例法规则: Supreme Court/Court of Appeal/HighCourt;不可以创立:Crown, Magistrates, County Courts cannot create precedent.3.Elements of judicial decision(影响法庭判决的因素):rationdecidendi判决理由[the reason for the decision]/Obiter dicta 附带说明[statement made by the way, not binding, but merely of persuasive authority]4.法官又可以因为那些理由拒绝先例(disregarding judicialprecedent): Overrule取代[the procedure whereby a court higher in the legal hierarchy sets aside a legal ruling established in a previous case]/Reverse推翻[a procedure whereby a court higher in the hierarchy reverses the decision of a lower court in the same case]/Distinguishing法官的自由裁决[a precedent is avoided by a judge demonstrating that the material facts of two cases are not the same]5.Rules of Statutory Interpretation(法的解释):①the literalapproach :the literal rule[means that words in the Act should be given their literal and grammatical meaning rather than what the judge thinks they mean./the golden rule :this rule is applied in circumstances where the application of the literal rule is likely to result in an obviously absurd result. ②the purposive approach :the judge should ,where necessary ,look beyond the words of statute to find out the reason/purpose for its enactment, and that meaning should be interpreted in the light of the purpose[Mischief rule :purposive approach的具体表现形式/where a statute is designed to remedy a weakness in the law, the correctinterpretation is the one which achieves it.]6.语言处理规则(法律没有追溯力 a statute does not haveretrospective effect)Chapter3 合同法(IMP)1.合同的概念a legally binding agreement enforceable in law2.从要约到承诺是否达成agreement [invitations to treat要约邀请--offer要约--acceptance承诺----agreement]3.Termination of an offer:express rejection/counter off反要约/lapse of time/revocation of an off/death/if the off is suject to a condition,it will lapse on failure of that condition4.Privity of Contract合同相对性原则: the common law doctrinethat only those are party to the contract---have rights or liabilities under the contract/ have the right to enforce the contract,contracts cannot give rights or obligations to others Chapter41.分类标准Express and lmplied terms:某个条款是否经过双方当事人协商同意(agreed by the parties)Condition,warranties and innominate terms 核心,从属和无名条款:根据条款重要性2.免责条款(三观概念)Any clause that attempts to exempt , or limit, the liability of one party for breach of contract or negligence3 test: correctly incorporated into the contract形式正确/wordedclearly to exclude the breach措辞清晰/reasonable per statute 内容合理Chapter51.type of breachRepudiatory breach根本性违约:refusal to perform拒绝履行/failure to perform an entire obligation不履行某项/incapacitation无力履行/breach of condition 违反核心条款/breach of an innominate term违反无名条款Anticipatory breach预期违约:未到合同履行时间,当事人提前说明无法履行;收到预期违约通知可立即追究违约责任,也可等到履行合同时间追究责任Lawful excuses for non-performance开脱责任:performance is impossible因不可预见的事情发生不可履行/尝试履行被拒绝/ the other party make it impossible for him to performance/contract is discharged through frustration情势变更/the party have been agreement permitted non-performance2.Remedies : when a breach occurs, the court has to decide what theappropriate remedy should be.3.Liquidated damage违约金:a genuine pre-estimate of the loss在订立合同前已经商定了,有利于解纠纷,如果违约金过高(远大于loss)判为惩罚性,则不可执行4.specific performance :the court directs a party to complete theircontractual obligations以下几种情况法官不会让合同继续履行:courts cannot supervise法官无力监督履行/personal service/minors involved Chapter6 Tort侵权法A wrongful act against an individual which gives rise to a civil claim.1.过失侵权的4个证明环节(概念标准内容)Negligence:It arises when one person suffers damage or injury though the negligent act(or omission to act)of another person.①Duty of care注意义务(三步走原则)1.Reasonable foreseeability合理预见原则2.Proximity关联性原则3.Justness and fairness of imposing a duty of care公平合理地强加注意义务②A breach of that duty违反注意义务1.general rule:The test for establishing breach of duty is an objective one:a breach of duty occurs if the defendant:”...fails to do something which a reasonable man...would do.”2.Special factors to considera.The probability of injuryb.The seriousness of the risk造成伤害的严重性c.Cost and practicability成本可行性mon practice证明是行业误差范围内e.Skilled persons/professionalsf.Social benefit③The breach of duty caused harm to the claimant违反义务是导致损失的原因1.The but for test2.No break in the chain of causation切断因果关系链的要素a.A natural eventb.Act of a third party 原侵权人不承担责任c.Act of the claimant④The loss ware not too remote主张的赔偿合理Reasonable foresight只赔偿违法者可以合理预见的部分2.抗辩事由①Contributory negligence共同过失(一般只是减少赔偿额,个别情况全部免除)②Volenti non fit injuria同意不生违法(彻底免除)Chapter7 劳动法1.身份判别①Control test :The amount of control that one person had over the other②Integration test不会外包给他人的,不可或缺的③Multiple test/Economic reality testa. The regularity and method of payment报酬支付频率,支付方式b. The ownership of tools and equipment是否提供工具c. The regularity of hours of work工作时间d. The ability to delegate all the work/to provide substitute 是否代理2.义务①Common Law Duties-Employers’ common law duties1)Duty of mutual trust and confidence2)To provide work for workers3)To pay wages/remuneration4)To indemnify employee against expenses and losses5)To provide for the care and safety of the employee6)No duty to provide reference when employees leave-Employees’ common law duties1) To obey reasonable and lawful orders2) To act faithfully/duty of faithful service/duty to account for all money and property3) To exercise reasonable skill and care in any activity in their role as an employee/reasonable competence to do his job4) Personal service亲自完成交付的责任②Statutory Duties1)Pay and equality不能低于国家平均2) Time off work3)Trade union officials工会组织罢工可以参加,还要给工资4) Every woman has a right to maternity leave and some are entitled to maternity pay5) Health and safety6)Working time:17week,not exceed 48 hours for each 7 days 除非员工书面同意多工作7) Flexible workingChapter81.解雇通知时间的计算1m-2Y: not less than 1 week2y-12y:1 week for each year≥12y: not less than 12 week劳动者离职要提前一周通知,合同期满不续则每工作一年折合一个月工资2.自动正当参加非法集合罢工unofficial industrial action/对国家安全有威胁自动不正当怀孕pregnancy/员工参加工会活动/收购并购时的解雇dismissal on transfer of an undertaking/工作存在安全问题/最低工作标准/作息时间/员工在周天拒绝工作3.用人单位解雇不当Chapter9 代理法1.代理关系建立方式Express agreement between the agent and principal达成委托代理协议合同,口头书面皆可Implied agreement默认没有代理协议但默认存在关系Ratification追任代理人先履行合同,事后委托人建立合同关系Without consent of principal 没有征得委托人同意就建立关系necessity/Estoppel2.代理权限(3)Express authority明示代理权限Implied authority默认代理权限Apparent/ostensible authority看起来有代理权限,实际上并没有Chapter10 合伙企业法1.合伙企业(概念):the relationships that subsists between personscarrying on a business in common with a view to profit. standard partnership is not s separate legal entity and its partners have full personal liability for the debts of partnership.2.Termination/dissolution合伙企业解散的债务处理:paying offexternal debts/repaying to the partners any loans or advances/repaying the partner’s capital contribution/anything left over is then repaid to the partners in the profit sharing ratio .3.Termination/dissolution合伙企业解散的条件:expiry of a fixedperiod stipulated in the partnership agreement/completion of the express purpose for which the partnership was formed/partner gives notice to leave/a new partner is admitted into the partnership/death or bankruptcy of partner/happeningof any event which makes company can’t carry on/on application by a partner the Court may decree a dissolution of the partnership4.Sole trade宏观特征:is not a separate legal entity, the person andbusiness are viewed as the same legal entity5.Authority合伙人的代理权限:express authority明示代理权限[from partnership agreement]/implied authority默示代理权限/apparent authority表面代理权限[已经退伙但其他人不知道]6. A partner’s liability usually extends to the period for which wereactually a partner of a firm. 合伙人只对担任合伙人期间合伙企业产生的债务有清偿责任7.Limited Partnership(LP)特征:the partnership must be registerwith the Company Registry/one or more of the partners must bear full,unlimited liability/partners with limited liability may not take part in management and cannot usually bind the business in contract/limited partner cannot withdraw their capital8.Limited Liability Partnership(LLP)特征:must be registered withthe the Registrar of Companies, with formation documents signed by at least two members/has a legal personality separate/ the name of partnership must end with LLP/partners are known as members, of which there must be at least two/LLPs must file annual returns and accounts/all members are agents of LLP/all members’ liability is limited/a designated member is responsible for administration and filing/LLP is not subject to corporation taxChapter121.设立pre-incorporation contacts谁来履行?Promoters发起人2.交什么文件①Memorandum of association公司章程(89年)②Application for registration注册申请书③A statement of capital and initial shareholdings关于公司资本坏人原始持有股份的状况说明④Statement of compliance遵从声明⑤A statement of company’s proposed officers拟任命谁为公司管理人员⑥A copy of any proposed articles of association自拟公司章程(06年)不是必须提交,没交使用默认模版3.2个证书的功能①Certificate of incorporation注册许可证Private company 只需要注册许可证,是形式审查②Trading certificate营业许可证Public company需要两个证,申领到注册许可证后一年内要申领到营业许可证,否则强制清算,是实质审查a.Allotted share capital is at least £50,000(允许股东分批缴纳)b.At least one quarter of the nominal value of the allotted share capital has been paid up(minimum £12,500)首次不低于票面的1/4,为确保一开始不会有资金困难c.Details of promoters’ expenses设立费用具体怎么产生d.A statement of compliance in respect of payment of nominal values and share premium4.章程修改的程序和内容-Contentsa. Directors’ powers and responsibilityb. Decisions making by directorsc. Appointment of directorsd. Organization and conduct of general meetingse. Issue and transference of sharesf. Payment of dividendsg. Exercise of mem bers’ rights-Alteringa. Passing a special resolution通过股东会的特别决定,3/4以上同意批准b. Providing the alteration has been made “bona fide in the interest of the company as a whole”内容符合全体股东的意愿5.各个公司名称缩写代表含义-Ltd:Limited-plc:public limited companyChapter131.capital的分类2. 普通股优先股的概念和差异3. Bonus issue 红利股发行The capitalization of the reserves if a company by the issue if additional shares to existing shareholders, in proportion to their holdings. Such shares are normally fully paid-up withno cashcalled for from the shareholders 4. Share premium概念shares may be issued at a price above their nominal value, the difference between the issue price and the nominal value is a share premium用途the issue of fully paid bonus share/writing off the preliminaryexpenses of company formation/writing off the discount onthe issueofdebentures/repurchase of debentures at a premiumChapter11 公司法The consequences of separate legal personality for the company are as follows:(1897年案例引出的规则)1: members' liability is limited.2: perpetual succession become possible as the company will need to be formally wounded-up.3: the company itself can own property.4 :the company can use, and be sued in its own name. Types of company (公司的分类)(此文档部分内容来源于网络,如有侵权请告知删除,文档可自行编辑修改内容,供参考,感谢您的配合和支持)编辑版word。

ACCA F1 大题知识点

1.what are the porter`s value chain?(Porter grouped the various activities of an organization into a value chain.)The value chain describes those activities of the organization that add value to purchased inputs.The porter`s value chain comprise support activities, primary activities and margin. Primary activities are directly related to production, sales, marketing. Deliver and service. Support activities provide purchased inputs, human resources, technology and infrastructural functions to support the primary activities. The margin is the excess the customer is prepared to pay over the cost to the firm of obtaining resource inputs and providing value activities.2.What are the five competitive forces?The competitive environment is structures by five forces.Barriers to entry; substitute products; the bargaining power of customers; the bargaining power of suppliers; competitive rivalry (行业竞争对手)3.What are the differences between internal and external audit?a.Reason. Internal audit is an activity designed to add value and improve an organization`s operations. External audit is anexercise to enable auditors to express an opinion on the financial statements.b.Reporting to. Internal audit reports to the board of directors, or other charged with governance. The external auditors reportto the shareholders or members of a company on the stewardship of the directors.c.Relating to. Internal audit`s work relates to the financial statements. (Concerned with the financial records that underliethese.)d.Relationship. With the company. Internal auditors are very often employees of the organization. External auditors areindependent of the company and its management. (They are appointed by the shareholders.)4.Introduce the fiscal policy and monetary policyFiscal policy provides an method of managing aggregate demand in the economy. Fiscal policy includes government policy on taxation, public, borrowing and public spending. Monetary policy uses money supply. Interest rates or credit controls to influence aggregate demand. Monetary policy: government policy on the money supply, the monetary system, interest rates, exchange rates and the availability of credit.5.What the situations of budget surplus and budget deficit happen?When government`s income exceeds its expenditure and there is a negative PSNCR or Public sector debt repayment (PSDR), we say that the government is running a budget surplus. This may be a deliberate policy to reduce the size of the money supply by taking money out of the economy. When a government`s expenditure exceeds its income, we say that the government is runninga budget deficit.6.Why does organization exist? (In brief, organizations enable people to be more productive.)Organizations can achieve results which individuals cannot achieve by themselves.a.Overcome people`s individual limitations, whether physical or intellectual.b.Enable people to specialize in what they do best.c.Save time. Because people can work together or do two aspects of a different task at the same time.d.Accumulate and share knowledge.e.Enable synergy: by bring together two individuals their combined output will exceed their output if they continued workingseparately.7.What the different between private companies and public limited companies?In the UK, limited companies come in two types: private limited companies and public limited companies. They differ as follows.a.Member of shareholders, most private companies are owned by only a small number of shareholders. Public companiesgenerally are owned by a wide proportion of the investing public.b.Transferability of shares. Share in public companies van be offered ti the general public. In practice this means that they canbe traded on a stock exchange. Shares in private companies, on the other hand, are rarely transferable without the consent of the shareholders.c.Directors as shareholders. The directors of a private limited company are more likely to hold a substantial portion of thecompany`s shares than the directors of a public company.8.In mintzberg`s view, what are the five component parts of an organization.According to mintzberg`s view, the five component parts include strategic apex, operating core, middle line, techno structure and support staff.9.Introduce the components of the shamrock organization and the Anthony hierarchy.Shamrock organization includes self employed, contingent, professional and consumers. Robert Anthony classified managerialactivity as follows: strategic management, tactical management and operational management.10.What are the types of committee?Committee can be classified according to the power they exercise.a.Executive committees have the power to govern or administer.b.Standing committees are formed for a particular purpose on a permanent basis. Their role is to deal with routine businessdelegated to them at weekly or monthly meetings.c.AD hoc committees are formed to complete a particular task.d.Sub-committee may be formed to co-ordinate the activities of two or more committees.e.Management committees in many businesses contain executives at a number of levels not all the decisions in a firm need tobe taken by the board.11.What are the qualities of good information?The qualities of good information include accurate, complete, cost- beneficial, user-targeted, relevant, authoritative, timely, easy to use.12.Introduce Handy`s 4 types of culturea.Power culture is shaped by one individual.b.Role culture is a bureaucratic culture shaped by rationality, rules and procedures.c.Rask culture is shaped by a focus on outputs and results.d.Existential or person culture is shaped by the interests of individuals.13.List the potential benefits of the informal organization.The potential benefits of the informal organization include Employee commitment, knowledge sharing, speed, responsiveness, co-operation.P75,P70,P53,P18,P11。

ACCA-F-知识点总结

ACCA考试F7知识点辅导I. The accounting problemBefore IAS37 provisions were recognized on the basis of prudence,little guidance was given on when a provision should be recognized and how it should be measured. This gave rise to inconsistencies,and also allowed profits to be manipulated.Some problems are noted below:(a) Provisions could be recognized on the basis of management intentions,rather than on any obligation to be entity;(b) Several items could be combined into one large provision. There were known as ‘big bath’ provisions;(c) A provision could be created for one purpose and then used for another;(d) Poor disclosure made it difficult to assess the effect of provisions on reported profits. In particular,provisions could be created when profits were high and released when profits were low in order to smooth profits.(1) DefinitionsIAS 37 views a provision as a liability.A provision is a liability of uncertainty timing or amount;A liability is an obligation of an enterprise to transfer economic benefits as a result of past transactions or events.Provision must be based on obligations,not management intentions.(2) Under IAS37, a provision should be recognized:a. When an enterprise has a present obligation;b. It is probable that a transfer of economic benefits will be required to settle it;c. A reliable estimate can be made of its amount; if a reasonable estimate cannot be made,then the nature of the provision and the uncertainties relating to the amount and timing of the cash flows should be disclosed.A provision is made for something which will probably happen. It should be recognizedwhen it is probable that a transfer of economic events will take place and when its amount can be estimated reliably.(3) Contingent liabilitiesDefinitionThe Standard defines a contingent liability as:(a) A possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the enterprise; or(b) A present obligation that arises from past events but is not recognized because:(i) It is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or(ii) The amount of the obligation cannot be measured with sufficient reliability.As a rule of thumb,probable means more than 50% likely. If an obligation is probable,it is not a contingent liability – instead,a provision is needed.Treatment of contingent liabilitiesContingent liabilities should not be recognized in financial statements but they should be disclosed. The required disclosures are:(a) A brief description of the nature of the contingent liability;(b) An estimate of its financial effect;(c) An indication of the uncertainties that exist;(d) The possibility of any reimbursement;(4) Contingent assetsDefinitionA possible asset that arises from the past events whose existence will be confirmed by the occurrence of one or more uncertain future events not wholly within the enterprise’s control.A contingent asset must not be recognized. Only when the realization of the relatedeconomic benefits is virtually certain should recognition take place. At that point,the asset is no longer a contingent asset.Disclosure:contingent assetsContingent assets must only be disclosed in the notes if they are probable. In that case a brief description of the contingent asset should be provided along with an estimate of its likely financial effect.II. Specific application1. Future operating lossesIn the past,provisions were recognized for future operating losses on the grounds of prudence. However these should not be provided for the following reasons.①They relate to future events;②There is no obligation to a third party. The loss-making business could be closed and the losses avoided.2. Onerous contractsAn onerous contract is a contract in which the unavoidable costs of meeting the contract exceed the economic benefits expected to be received under it.A common example of an onerous contract is a lease on a surplus factory. The leaseholder is legally obliged to carry on paying the rent on the factory,but they will not get any benefit from using the factory.The least net cost of an onerous contract should be recognized as a provision. The least net cost is the lower of the cost of fulfilling the contract or of terminating it and suffering any penalty payments.Some assets may have been bought specifically for the onerous contract. These should be reviewed for impairment before any separate provision is made for the contract itself.1DemoDroopers has recently bought all of the trade,assets and liabilities of Dolittle,an unincorporatd business. As part of the take-over all of the combined business’s activities have been relocated at Droopers main site. As a result Dolittle’s premises are now empty and surplus to requirements.However,just before the acquisition Dolittle had signed a three year lease for their premises at $6000 per calendar month. At 31 December 2003 this lease ad 32 months left to run and the landlord had refused to terminate the lease. A sub-tenant had taken over part of the premises for the rest of the lease at a rent of $2500 per calendar month.Required(a) Should Droopers recognized a provision for an onerous contract in respect of this lease?(b) Show how this information will be presented in the financial statements for 2003 and 2004. Ignore the time value of money.Solution:Droopers has a legal obligation to pay a further $192000 to the landlord,as a result of a lease signed before the year end. Therefore an onerous contract exists and must be provided for.There is also an amount recoverable form the sub-tenant of $80000(32×2500). This will be shown separately in the balance sheet as an asset.The $192000 payable and the $80000 recoverable can be netted off in the income statement.income statements20032004$$provision for onerous lease contract(net)112000 Dr.net rental payable on lease (72-30)-42000 Drrelease of provision42000 Cr112000 Dr.balance sheetsreceivalbesamounts recoverable from sub-tenants80000 Dr.50000 Drliabilitiesamounts payable on onerous contracts192000 Cr120000 Cr3. RestructuringA restructuring is a programme that is planned and controlled by management and has a material effect on:①The scope of a business undertaken by the reporting entity in terms of the products or services it provides; or②The manner in which a business undertaken by the reporting entity is conducted;Restructuring includes terminating a line of business,closure of business locations,changes in management structure,and refocu sing a business’s operations.Restructuring provisions have always been quite common,and have often been misused. IAS37 restricts the recognition of restructuring provisions to situations where an entity has a constructive obligation to restructure.A constructive obligation will only arise if:①There is a detailed formal plan for restructuring. This must identify the businesses,locations and employees affected; and②Those affected have a valid expectation that the restructuring will be carried out. This can be by starting to implement the plan or by announcing it to those affected.The constructive obligation must exist at the year-end.(Any obligation arising after the year end may require disclosure under IAS10)A board decision alone will not create a constructive obligation unless:①The plan is already being implemented. For example,assets are being sold,redundancy negotiations have begun; or②The plan has been announced to those affected by it. The plan must have a strict timeframe without unreasonable delays; or③The Board itself contains representatives of employees or other groups affected by the decision.(This is common in mainland Europe.)An announcement to sell an operation will not create a constructive obligation. An obligation will only arise when a purchaser is found and there is a binding sale agreement.A restructuring provision should only include the direct costs of restructuring. These must be both:(a) Necessarily entailed by the restructuring; and(b) Not associated with the ongoing activities of the entity;The following costs must not be provided for because they relate to future events:(a) Retaining or relocating staff;(b) Marketing;(c) Investment in new systems and distribution networks;(d) Future operating losses (unless arising from an onerous contract)(e) Profits on disposal of assets.cca f7真题对于acca f7的考试的重要性我相信各位acca考生都心知肚明了,首先我们先看一下acca f7科目的考试内容ACCA F7科目介绍:F7《财务报告》是F3《财务会计》的后续课程或说是升级课程。

acca f6知识点总结2023

ACCA F6知识点总结在2023年,ACCA F6考试将继续是很多学员的重要挑战。

F6考试侧重于税务方面的知识,涉及了许多复杂的税法和规定。

为了帮助考生更好地备战这一考试,下面将对ACCA F6的主要知识点进行总结和归纳。

一、纳税义务和居民身份1. 税务居民定义- 居住在国内的个人- 在国内有固定居所- 个人在国内居住180天以上的- 个人国内居住时间在2年以上的2. 纳税义务- 个人所得税- 营业税- 企业所得税- 增值税- 关税- 土地税二、个人所得税1. 个人所得税的计算- 确定税务居民身份- 计算应纳税所得额- 根据所得额确定纳税比例- 计算纳税金额- 申报纳税2. 税务减免- 公益捐赠- 教育支出- 医疗支出- 住房利息贷款三、公司税1. 企业所得税- 确定纳税所得额- 计算应纳税额- 申报纳税- 公司税务优惠政策2. 增值税- 税率和税基- 纳税申报- 增值税发票四、税务规划1. 个税规划- 个人所得税避税策略- 投资收益规划- 资产转移规划2. 公司税务规划- 利润转移- 投资资产安排- 跨国税务规划通过对以上知识点的总结和梳理,考生可以更清晰地了解ACCA F6考试所涉及的范围和重点。

在备战考试的过程中,考生需要特别关注每个知识点的细节和变化,同时也要结合实际情况进行深入理解和应用。

希望每一位考生都能够顺利通过ACCA F6考试,成为一名合格的财务税务专业人士。

祝各位考生取得优异的成绩,为自己的职业发展打下坚实的基础。

二、个人所得税3. 所得类别个人所得税的所得类别包括以下几种:- 工资薪金所得- 经营所得- 劳务报酬所得- 特许权使用费所得- 财产转让所得- 利息、股息、红利所得- 稿酬所得- 物业租赁所得- 财产保险所得- 税前抠除的养老金和退休金等4. 税前抠除在计算个人所得税时,个人可以享受税前抠除,降低应纳税所得额。

税前抠除主要包括以下项目:- 基本生活费、专项附加抠除和专项抠除- 子女教育、大病医疗等专项附加抠除- 购物商业健康保险的支出- 公积金、商业健康保险等社会保险的缴纳额。

ACCA考试知识点总结:F3易混词汇列举

ACCA考试知识点总结:F3易混词汇列举ACCA考试科目中,F3阶段的词汇是非常多的。

并且,有些词汇无论是意思还比较的相近。

为了重点区分这些词,中公财经小编在这里就给大家简单列举了以下;owed to vs owed fromowed to后面跟的是债主,是应该收钱的人;owed from后面跟的是欠钱的人;e.g.He owed money to many people;the number was probably in the thousands.Thousands of people were owed money from him.他欠了很多人的钱,他的债主可能有几千人。

due to vs due fromdue to后面跟的是债主,是应该收钱的人;due from后面跟的是欠钱的人;e.g.Have they been paid the money due to them?Have they been paid the money due from others?他们是否已经得到了别人欠他们的钱?F3中的due to还有“因为、由于”的意思,表示要寻找原因。

Du e to some errors,the total amount of the trial balance’s debit side was not equaled to the credit side.mark up on costvsmark up on sales pricee.g.1)A sold goods to B at a price of$10,000.The profit mark-up was 40%on the sales prices.mark up on sales price意味着sales=100%,profit=40%,cost=100%-40%=60%所以sales=10,000,profit=40%*10,000=4,000,cost=60%*10,000=6,0002)A sold goods to B at a price of$10,000.The profit mark-up was 40%on the cost.mark up on cost意味着cost=100%,profit=40%,sales=cost+profit=140%所以sales=10,000,cost=10,000*100%/140%=7143,profit=10,000*40%/140%=2857Invoice vs receiptsInvoice是发票,是卖方用来提醒买方所须付的金额;receipt是收据,也是卖方给买方的。

ACCA F4知识点:Criminal law and Civil law

ACCA F4知识点:Criminal law and Civil law今天给大家来说一说ACCA F4中关于Criminal law和Civil law,即刑法和民法。

首先我们先来看一下它们的定义。

Civil law sets out the rights and duties of persons as between themselves. The person whose rights have been infringed can claim a remedy from the wrongdoer. 民法主要关注的是人的权利和责任以及对其的补偿。

Criminal law is concerned with the conduct that is considered so undesirable that the State punishes persons who transgress. 刑法主要关注的是一个违法的人对其的违法行为的惩罚。

关于Burden of proof,即举证责任,有相似的部分。

The necessity of proof normally lies with the person who lays charges, i.e. the claimant. 举证责任由原告承担。

这两者之间的区别主要体现在四个方面。

(1)Aim. Civil law is aimed to provide compensation for an injured party, whereas criminal law is to regulate society by the threat of punishment.(2)Parties. In a civil action, the claimant sues the defendant, while in a criminal action, the State prosecutes the defendant.(3)Standard of proof. In Civil law, if the claimant can prove the wrong on the balance of probabilities, his litigation is successful and the defendant is held liable. 民法中,要保持可能性的平衡。

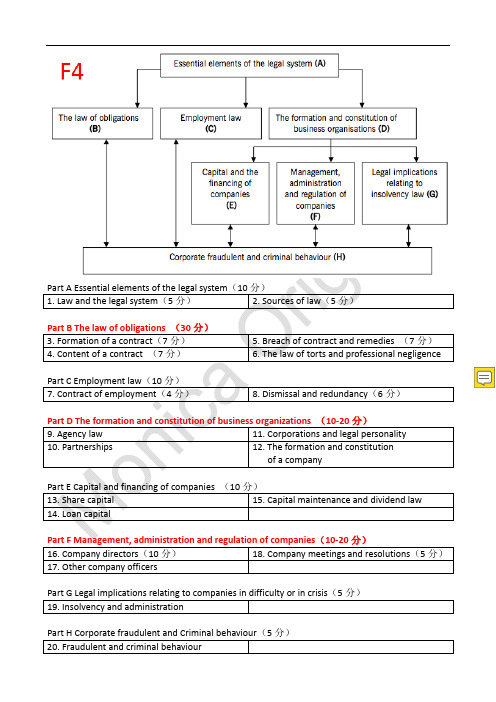

ACCA F4知识要点汇总(精简版)

b) T法 官 庭 : Trusts and mortgages, Revenue matters ,Bankruptcy (outside London ‐ County Court subject) ,Disputed

wills and administration of estates of deceased persons, Partnership and company matters 信托和抵押、收入、破产(London 外去郡法院)、遗 嘱纠纷、死者遗产管理、合伙和公司事宜

5. Breach of contract and remedies (7 分) 6. The law of torts and professional negligence

Part C Employment law(10 分) 7. Contract of employment(4 分)

8. Dismissal and redundancy(6 分)

Court of appeal 上诉法院

Supreme Court 最高法院

European Court of Justice (ECJ) 欧洲法院

a) 高院 3 个庭的上诉案件 b) 郡法院上诉 c) Employment Appeal Tribunal 上诉仲裁庭 上诉的程序:rehearing 重新审理 使用材料:transcript of the case 案件副本和 judge’s notes 法官记录 注意:不重新开庭,Witnesses not re‐examined & new evidence not permitted,只是案卷重审 a) 上诉法院的上诉 b) 非常偶然:高院的上诉 c) 使用材料:transcript of the case 案件副本和 judge’s notes 法官记录 注意:不重新开庭,Witnesses not re‐examined & new evidence not permitted,只是案卷重审 a) Interpreting European Treaty law 解释欧洲贸易法 b) 接受欧盟国家和机构间的案件 c) 欧盟个人利益受影响,ECJ 也受理

ACCAF知识要点汇总精简

ACCA-F知识要点汇总(精简版)————————————————————————————————作者:————————————————————————————————日期:1.抽样的概念●单纯随机抽样(simple random sampling)将调查总体全部观察单位编号,再用抽签法或随机数字表随机抽取部分观察单位组成样本.优点:操作简单,均数、率及相应的标准误计算简单.缺点:总体较大时,难以一一编号.●系统抽样(systematic sampling)又称机械抽样、等距抽样,即先将总体的观察单位按某一顺序号分成n个部分,再从第一部分随机抽取第k号观察单位,依次用相等间距,从每一部分各抽取一个观察单位组成样本.优点:易于理解、简便易行.缺点:总体有周期或增减趋势时,易产生偏性.●分层抽样(stratified sampling)先按对观察指标影响较大的某种特征,将总体分为若干个类别,再从每一层内随机抽取一定数量的观察单位,合起来组成样本.有按比例分配和最优分配两种方案.优点:样本代表性好,抽样误差减少.以上四种基本抽样方法都属单阶段抽样,实际应用中常根据实际情况将整个抽样过程分为若干阶段来进行,称为多阶段抽样.各种抽样方法的抽样误差一般是:整群抽样≥单纯随机抽样≥系统抽样≥分层抽样.●多级抽样(Multistage sampling)也叫多阶段抽样或阶段抽样,以二级抽样为例,二级抽样就是先将总分组,然后在第一级和第二中分别随机地抽取部分一级单位和部分二级单位。

例如:以全国性调查为例,当抽样单元为各级行政单位时,按社会发展水平分层后(或按经济发展水平,或按地理位置分层),从每层中先抽几个地区,再从抽中的地区抽市、县、村,最后再抽至户或个人。

优点:具体整体抽样的简单易行的优点,同时,在样本量相同的情况下又整群抽样的精度高。

缺点:计算复杂。

●整群抽样(cluster sampling)是先将调查总体分为群,然后从中抽取群,对被抽中群的全部单元进行调查。

ACCAF 知识点总结

Chapter11. 民法(civil law)和刑法(criminal law )的划分Civil law: an form of private law , used by individuals to assert rights against other individualsCriminal law: an aspect of public law to regulate1.primary legislation(made by theParliament)/secondary legislation( in exercise of law-making powers delegated by Parliament). [注:Necessity for delegatedlegislation/secondary legislation :moreconvenient ;can hand over the task of specifying the law in detail to experts] 2. 在case law 中:common law 普通法[created byjudges through the application of the principle of judicial precedent. common law drew oncustoms/equity law 衡平法:to resolve disputes where damages are not a suitable remedy and to introduce fairness into the legal system.] 2. 不同法院管辖事件的类型decided on the basis of the law established inearlier cases.2.可以创立判例法规则: Supreme Court/Court ofAppeal/High Court;不可以创立:Crown,Magistrates, County Courts cannot createprecedent.3.Elements of judicial decision(影响法庭判决的因素):ration decidendi判决理由[the reason for thedecision]/Obiter dicta附带说明[statement madeby the way, not binding, but merely of persuasive authority]4.法官又可以因为那些理由拒绝先例(disregardingjudicial precedent): Overrule取代[the procedurewhereby a court higher in the legal hierarchy sets aside a legal ruling established in a previouscase]/Reverse推翻[a procedure whereby a court higher in the hierarchy reverses the decision of a lower court in the same case]/Distinguishing法官的自由裁决[a precedent is avoided by a judgedemonstrating that the material facts of two cases are not the same] 5.Rules of Statutory Interpretation(法的解释):①theliteral approach :the literal rule[means that words in the Act should be given their literal andgrammatical meaning rather than what the judge thinks they mean./the golden rule :this rule isapplied in circumstances where the application of the literal rule is likely to result in an obviouslyabsurd result. ②the purposive approach :thejudge should ,where necessary ,look beyond thewords of statute to find out the reason/purposefor its enactment, and that meaning should beinterpreted in the light of the purpose[Mischiefrule :purposive approach的具体表现形式/wherea statute is designed to remedy a weakness inthe law, the correct interpretation is the one which achieves it.]6.语言处理规则(法律没有追溯力a statute doesnot have retrospective effect)Chapter3 合同法(IMP)1.合同的概念a legally binding agreement enforceablein law2.从要约到承诺是否达成agreement [invitations totreat要约邀请--offer要约--acceptance承诺----agreement]3.Termination of an offer:express rejection/counteroff反要约/lapse of time/revocation of anoff/death/if the off is suject to a condition,it willlapse on failure of that condition4.Privity of Contract合同相对性原则: the commonlaw doctrine that only those are party to thecontract---have rights or liabilities under thecontract/ have the right to enforce thecontract,contracts cannot give rights or obligationsto othersChapter41.分类标准Express and lmplied terms:某个条款是否经过双方当事人协商同意(agreed by the parties)Condition,warranties and innominate terms 核心,从属和无名条款:根据条款重要性2.免责条款(三观概念)Any clause that attempts to exempt , or limit, the liability of one party for breach of contract ornegligence3 test: correctly incorporated into the contract形式正确/worded clearly to exclude the breach措辞清晰/reasonable per statute内容合理Chapter5 1.type of breach⏹Repudiatory breach根本性违约:refusal toperform拒绝履行/failure to perform an entireobligation不履行某项/incapacitation无力履行/breach of condition 违反核心条款/breachof an innominate term违反无名条款⏹Anticipatory breach预期违约:未到合同履行时间,当事人提前说明无法履行;收到预期违约通知可立即追究违约责任,也可等到履行合同时间追究责任Lawful excuses for non-performance开脱责任:performance is impossible因不可预见的事情发生不可履行/尝试履行被拒绝/ the other party make it impossible for him to performance/contract is discharged through frustration情势变更/the party have been agreement permitted non-performance 2.Remedies : when a breach occurs, the court hasto decide what the appropriate remedy should be.3.Liquidated damage违约金:a genuinepre-estimate of the loss在订立合同前已经商定了,有利于解纠纷,如果违约金过高(远大于loss)判为惩罚性,则不可执行4.specific performance :the court directs a partyto complete their contractual obligations以下几种情况法官不会让合同继续履行:courtscannot supervise法官无力监督履行/personalservice/minors involvedChapter6 Tort侵权法A wrongful act against an individual which gives riseto a civil claim.1.过失侵权的4个证明环节(概念标准内容)Negligence:It arises when one person suffers damage or injury though the negligent act(or omission to act)of another person.注意义务(三步走原则)合理预见原则关联性原则公平合理地强加注意义务②A breach of that duty违反注意义务1.general rule:The test for establishing breach of duty is an objective one:a breach of duty occurs if the defendant:”...fails to do something which a reasonable man...would do.”2.Special factors to considera.The probability of injuryb.The seriousness of the risk造成伤害的严重性c.Cost and practicability成本可行性mon practice证明是行业误差范围内e.Skilled persons/professionalsf.Social benefit③The breach of duty caused harm to the claimant违反义务是导致损失的原因1.The but for test2.No break in the chain of causation切断因果关系链的要素a.A natural eventb.Act of a third party 原侵权人不承担责任c.Act of the claimant④The loss ware not too remote主张的赔偿合理Reasonable foresight只赔偿违法者可以合理预见的部分2.抗辩事由①Contributory negligence共同过失(一般只是减少赔偿额,个别情况全部免除)②Volenti non fit injuria同意不生违法(彻底免除)Chapter7 劳动法1.身份判别①Control test :The amount of control that one person had over the other②Integration test不会外包给他人的,不可或缺的③Multiple test/Economic reality testa. The regularity and method of payment报酬支付频率,支付方式b. The ownership of tools and equipment是否提供工具c. The regularity of hours of work工作时间d. The ability to delegate all the work/to provide substitute是否代理2.义务①Common Law Duties-Employers’ common law duties1)Duty of mutual trust and confidence2)To provide work for workers3)To pay wages/remuneration4)To indemnify employee against expenses and losses5)To provide for the care and safety of the employee6)No duty to provide reference when employees leave-Employees’ common law duties1) To obey reasonable and lawful orders2) To act faithfully/duty of faithful service/duty to account for all money and property3) To exercise reasonable skill and care in any activity in their role as an employee/reasonable competence to do his job4) Personal service亲自完成交付的责任②Statutory Duties1)Pay and equality不能低于国家平均2) Time off work3)Trade union officials工会组织罢工可以参加,还要给工资4) Every woman has a right to maternity leave and some are entitled to maternity pay5) Health and safety6)Working time:17week,not exceed 48 hours for each 7 days除非员工书面同意多工作7) Flexible workingChapter81.解雇通知时间的计算1m-2Y: not less than 1 week2y-12y:1 week for each year≥12y: not less than 12 week劳动者离职要提前一周通知,合同期满不续则每工作一年折合一个月工资2.自动正当参加非法集合罢工unofficial industrial action/对国家安全有威胁自动不正当怀孕pregnancy/员工参加工会活动/收购并购时的解雇dismissal on transfer of an undertaking/工作存在安全问题/最低工作标准/作息时间/员工在周天拒绝工作3.用人单位解雇不当Chapter9 代理法1.代理关系建立方式Express agreement between the agent andprincipal达成委托代理协议合同,口头书面皆可Implied agreement默认没有代理协议但默认存在关系Ratification追任代理人先履行合同,事后委托人建立合同关系Without consent of principal 没有征得委托人同意就建立关系necessity/Estoppel2.代理权限(3)Express authority明示代理权限Implied authority默认代理权限Apparent/ostensible authority看起来有代理权限,实际上并没有Chapter10 合伙企业法1.合伙企业(概念):the relationships that subsistsbetween persons carrying on a business incommon with a view to profit. standardpartnership is not s separate legal entity and itspartners have full personal liability for the debts of partnership.2.Termination/dissolution合伙企业解散的债务处理:paying off external debts/repaying to thepartners any loans or advances/repaying thepartner’s capital contribution/anything left over isthen repaid to the partners in the profit sharingratio .3.Termination/dissolution合伙企业解散的条件:expiry of a fixed period stipulated in thepartnership agreement/completion of the express purpose for which the partnership wasformed/partner gives notice to leave/a newpartner is admitted into the partnership/death orbankruptcy of partner/happening of any eventwhich makes company can’t carry on/onapplication by a partner the Court may decree adissolution of the partnership4.Sole trade宏观特征:is not a separate legal entity,the person and business are viewed as the same legal entity5.Authority合伙人的代理权限:express authority明示代理权限[from partnership agreement]/impliedauthority默示代理权限/apparent authority表面代理权限[已经退伙但其他人不知道]6. A partner’s liability usually extends to the periodfor which were actually a partner of a firm. 合伙人只对担任合伙人期间合伙企业产生的债务有清偿责任7.Limited Partnership(LP)特征:the partnership mustbe register with the Company Registry/one ormore of the partners must bear full,unlimitedliability/partners with limited liability may not take part in management and cannot usually bind thebusiness in contract/limited partner cannotwithdraw their capital8.Limited Liability Partnership(LLP)特征:must beregistered with the the Registrar of Companies,with formation documents signed by at least twomembers/has a legal personality separate/ thename of partnership must end with LLP/partnersare known as members, of which there must beat least two/LLPs must file annual returns andaccounts/all members are agents of LLP/allmembers’ liability is limited/a designated member is responsible for administration and filing/LLP is not subject to corporation taxChapter121.设立pre-incorporation contacts谁来履行?Promoters发起人2.交什么文件①Memorandum of association公司章程(89年)②Application for registration注册申请书③A statement of capital and initial shareholdings关于公司资本坏人原始持有股份的状况说明④Statement of compliance遵从声明⑤A statement of company’s proposed officers拟任命谁为公司管理人员⑥A copy of any proposed articles of association自拟公司章程(06年)不是必须提交,没交使用默认模版3.2个证书的功能①Certificate of incorporation注册许可证Private company 只需要注册许可证,是形式审查②Trading certificate营业许可证Public company需要两个证,申领到注册许可证后一年内要申领到营业许可证,否则强制清算,是实质审查a.Allotted share capital is at least £50,000(允许股东分批缴纳)b.At least one quarter of the nominal value of the allotted share capital has been paid up(minimum £12,500)首次不低于票面的1/4,为确保一开始不会有资金困难c.Details of promoters’ expenses设立费用具体怎么产生d.A statement of compliance in respect of payment of nominal values and share premium4.章程修改的程序和内容-Contentsa. Directors’ powers and responsibilityb. Decisions making by directorsc. Appointment of directorsd. Organization and conduct of general meetingse. Issue and transference of sharesf. Payment of dividendsg. Exercise of members’ rights-Alteringa. Passing a special resolution通过股东会的特别决定,3/4以上同意批准b. Providing the alteration has been made “bona2.普通股优先股的概念和差异1.概念shares may be issued at a price above their nominal value, the difference between the issueprice and the nominal value is a share premium用途the issue of fully paid bonus share/writing off the preliminary expenses of company formation/writing off the discount on the issue of debentures/repurchase of debentures at a premiumChapter11 公司法The consequences of separate legal personality for the company are as follows:(1897年案例引出的规则)1: members' liability is limited.2: perpetualsuccessionbecomepossible asthecompanywill need tobe formallywounded-up.3: the company itself can own property.4 :the company can use, and be sued in its own name.Types of company (公司的分类)。

ACCA必考知识点:F1第二部分知识点

ACCA F1阶段需要记忆的内容有很多,小编在上篇同文章中就给大家介绍过了。

多余的话不多说,中公财经小编就给大家继续整理F1阶段第二部分的考试必考知识点。

希望能够对大家的acca考前复习提供帮助;Informal organization: 非正式组织An informal organization is loosely structured (结构松散的) flexible (灵活的), and spontaneous (自发的). It exists alongside the formal one.非正式组织的定义不是我们的考点,但是你要知道它是什么,尤其是它定义中这几个放飞自我的形容词,暗示了它非规范化的特征~Span of control:控制跨度(重要!)It refers to the number of subordinates directly responsible to a superior.一个superior直接控制的下属的数量,两个重点:下属的数量,而不是其他的数量;一定要体现直接控制,如果没有directly responsible 的字眼,就要找最能体现直接控制的描述,这是定义热门考点,一定要通过习题感受!Scalar chain:权力链条The chain of command from the most senior to the most juniorDelayering & downsizing:去层级和规模缩减Delayering:Reduction the number of management levels from bottom top.去层级是指去掉某个层级,一般level 前会给出层级名称,如middle management level 等downsizing: large numbers of managers and staff have been made redundant (人数的缩减,可能同时发生在各个层级上)Tall and flat organization:(图形记忆法)将这几个组织架的概念串连在一起,就是:Tall organization 的scalar chain 较长,span of control 较窄,而flat organization 则相反,通过delayering “去层级”,tall organization 可以变成flat organization。

accafr章节知识点总结

accafr章节知识点总结1. Introduction to Financial ReportingFinancial reporting is the process of creating and presenting financial information about a company's performance and position to external stakeholders, such as investors, creditors, regulators, and the public. It involves preparing financial statements, including the balance sheet, income statement, cash flow statement, and statement of changes in equity. These financial statements provide a comprehensive view of the company's financial health and are essential for decision-making and performance evaluation.2. International Financial Reporting Standards (IFRS)IFRS are a set of accounting standards developed by the International Accounting Standards Board (IASB) that are used by companies across the world to prepare their financial statements. ACCA FR covers the principles and guidelines of IFRS and how they are applied in practice. It also includes the conceptual framework of IFRS, which sets out the underlying concepts and principles for financial reporting.3. Regulatory Framework for Financial ReportingIn addition to IFRS, companies are also required to comply with the regulatory frameworkof their respective jurisdictions. ACCA FR discusses the regulatory requirements for financial reporting, including the Companies Act, Securities and Exchange Commission (SEC) rules, and other relevant regulations. Understanding the regulatory framework is crucial for ensuring compliance and avoiding legal sanctions.4. Preparation of Financial StatementsThe preparation of financial statements is a fundamental aspect of financial reporting. ACCA FR covers the process of preparing the balance sheet, income statement, cash flow statement, and statement of changes in equity in accordance with IFRS. It also explores the accounting policies, estimates, and disclosures that are required to provide a true and fair view of the company's financial position and performance.5. Interpretation and Analysis of Financial StatementsOnce the financial statements are prepared, they need to be interpreted and analyzed to understand the company's financial performance and position. ACCA FR provides the knowledge and skills to analyze financial statements using ratio analysis, trend analysis, and other tools. It also covers the use of financial statements for decision-making, performance evaluation, and forecasting.6. Consolidated Financial StatementsFor companies with subsidiaries, the preparation of consolidated financial statements is essential to present the group's financial position and performance. ACCA FR delves into theprinciples of consolidations, including the treatment of non-controlling interests, intercompany transactions, and goodwill. It also explores the elimination of intra-group transactions and balances to avoid double counting and present a true and fair view of the group's financials.7. Accounting for Assets and LiabilitiesACCA FR includes detailed coverage of accounting for tangible and intangible assets, including property, plant, and equipment, investment property, and goodwill. It also covers the accounting treatment of financial instruments, inventories, and provisions. Furthermore, it addresses the recognition, measurement, and disclosure of liabilities, including leases, employee benefits, and provisions.8. Financial Reporting in Specialized IndustriesCertain industries, such as banking, insurance, and extractive industries, have specific accounting requirements due to their unique nature of operations and risks. ACCA FR provides an insight into the financial reporting standards and practices for these specialized industries, ensuring that candidates are equipped with the knowledge to address industry-specific challenges.9. Ethical and Professional Considerations in Financial ReportingEthical considerations are paramount in financial reporting to ensure the integrity and credibility of the financial information presented to stakeholders. ACCA FR emphasizes the ethical principles and professional conduct expected of accountants in their reporting responsibilities. It also explores the role of professional accountancy bodies and regulatory authorities in promoting ethical behavior and maintaining public trust.In conclusion, ACCA Financial Reporting is a comprehensive module that provides a deep understanding of the principles, standards, and practices of financial reporting. It equips candidates with the knowledge and skills to prepare, interpret, and analyze financial statements, ensuring compliance with IFRS and regulatory requirements. With a strong foundation in financial reporting, ACCA professionals are well-prepared to contribute to the transparency and accountability of the global business environment.。

ACCA F 知识要点汇总 上

Part 1. Audit 介绍*如图所示,审计是受股东委派,直接向股东报告。

External audits 关注财报For auditor to express their opinion and provide assurance to shareholders that the financial statements are prepared, in all material respects , in accordance with an applicable financial reporting framework. 即审计过程的最终目的.关键词:True and Fair, all Material respects, comply with IFRS● Materiality 重要性定义:Information is material if its omission or misstatement could influence theeconomic decisions of users taken on the basis of the financial statements.(相当于,低于多少金额,属于没有重大误报,报告是可接受的。

) Amount (quantity)一般5% ‐ 10% of profit before tax,属于重大Nature (quality)举例:未决诉讼,涉数金额较大;高管调查● Reasonable assurance 合理保证:任何100%保证的描述都是错误的,审计师给不了。

The highest level ofassurance given, as in the case of statutory audit , is described as 'reasonable assurance'. 非绝对的保证is not absolute assurance because there are 固有局限性inherent limitations of an audit which result in the auditor forming an opinion on evidence that is 有说服力的而不是结论性的persuasive rather than conclusive .原因:审计师不可能做到完全客观not objective 。

ACCAF3知识点:Depreciation

ACCA F3知识点:Depreciation今天给大家说一说ACCA F繁口识点,关于depreciation方面,即折旧。

Depreciation represents the systematic allocation of the depreciable amount (cost less residual value at the end of its useful life) of a fixed asset over its estimated useful life. Depreciation is consistent with the matching concept — the original cost of the non -current asset is spread across the accounting periods that are expected to benefit from its use.Depreciation has dual effects. Firstly, depreciation is charged as an expense in the statement of comprehensive income; secondly, the corresponding credit is accumulated in the provision for depreciation account in the statement of financial position to offset against the original cost of the non -current assets.The journal entry is:Dr Depreciation (SOCI) XXCr Provision for depreciation (SOFP) XX这里有两种折旧的方式,即straight-line method 和reducing balance method.Straight-line method (直线法) is spread evenly across the useful life of the non -current asset, resulting in same amount of depreciation charged every year.Straight line 计算方式:(Cost-Residual value)/useful lifeReducing balance method (余额递减法):A fixed depreciation rate (say 20% p.a.) is applied to the non -current asset' s net book value(cost less accumulated depreciation) every year. Since net book value diminishes yearly, the depreciation charge falls every year.Reducing balance method: X% x Net Book Value (NBV)Note: the residual value does not impact reducing balance calculation of depreciation.Policy is to charge depreciation at 20% per year on the straight line basis, with proportionate depreciation in the year of purchase and disposal (or ignore depreciation in the year of disposal or charge the full year in the year of acquisition).。

ACCAF知识点总结