Chapter_17Does Debt Policy Matter(公司理财原理,Brealey & Myers)

公司理财 习题库 Chap017

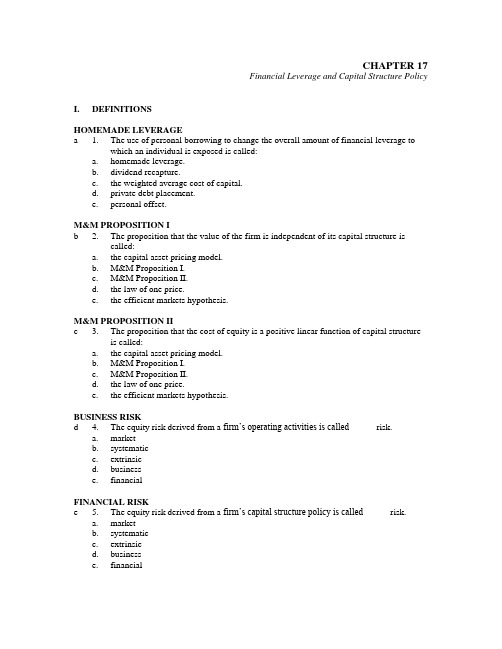

CHAPTER 17Financial Leverage and Capital Structure Policy I. DEFINITIONSHOMEMADE LEVERAGEa 1. The use of personal borrowing to change the overall amount of financial leverage towhich an individual is exposed is called:a. homemade leverage.b. dividend recapture.c. the weighted average cost of capital.d. private debt placement.e. personal offset.M&M PROPOSITION Ib 2. The proposition that the value of the firm is independent of its capital structure iscalled:a. the capital asset pricing model.b. M&M Proposition I.c. M&M Proposition II.d. the law of one price.e. the efficient markets hypothesis.M&M PROPOSITION IIc 3. The proposition that the cost of equity is a positive linear function of capital structureis called:a. the capital asset pricing model.b. M&M Proposition I.c. M&M Proposition II.d. the law of one price.e. the efficient markets hypothesis.BUSINESS RISKd 4. The equity risk derived from a firm’s operating activities is called _____ risk.a. marketb. systematicc. extrinsicd. businesse. financialFINANCIAL RISKe 5. The equity risk derived from a firm’s capital structure policy is called _____ risk.a. marketb. systematicc. extrinsicd. businesse. financialCHAPTER 17INTEREST TAX SHIELDa 6. The tax savings of the firm derived from the deductibility of interest expense is calledthe:a. interest tax shield.b. depreciable basis.c. financing umbrella.d. current yield.e. tax-loss carryforward savings.UNLEVERED COST OF CAPITALb 7. The unlevered cost of capital is:a. the cost of capital for a firm with no equity in its capital structure.b. the cost of capital for a firm with no debt in its capital structure.c. the interest tax shield times pretax net income.d. the cost of preferred stock for a firm with equal parts debt and common stock in itscapital structure.e. equal to the profit margin for a firm with some debt in its capital structure.DIRECT BANKRUPTCY COSTSc 8. The explicit costs, such as the legal expenses, associated with corporate default areclassified as _____ costs.a. flotationb. beta conversionc. direct bankruptcyd. indirect bankruptcye. unleveredINDIRECT BANKRUPTCY COSTSc 9. The costs of avoiding a bankruptcy filing by a financially distressed firm are classifiedas _____ costs.a. flotationb. direct bankruptcyc. indirect bankruptcyd. financial solvencye. capital structureFINANCIAL DISTRESS COSTSe 10. The explicit and implicit costs associated with corporate default are referred to as the_____ costs of a firm.a. flotationb. default betac. direct bankruptcyd. indirect bankruptcye. financial distressCHAPTER 17 STATIC THEORY OF CAPITAL STRUCTUREa 11. The proposition that a firm borrows up to the point where the marginal benefit of theinterest tax shield derived from increased debt is just equal to the marginal expense ofthe resulting increase in financial distress costs is called the:a. static theory of capital structure.b. M&M Proposition I.c. M&M Proposition II.d. capital asset pricing model.e. open markets theorem.BANKRUPTCYb 12. The legal proceeding for liquidating or reorganizing a firm operating in default iscalled a:a. tender offer.b. bankruptcy.c. merger.d. takeover.e. proxy fight.LIQUIDATIONc 13. The complete termination of a firm as a going business concern is called a:a. merger.b. repurchase program.c. liquidation.d. reorganization.e. divestiture.ACCOUNTING INSOLVENCYd 14. A firm that has negative net worth is said to be:a. experiencing a business failure.b. in legal bankruptcy.c. experiencing technical insolvency.d. experiencing accounting insolvency.e. in Chapter 11 bankruptcy reorganization.REORGANIZATIONd 15. An attempt to financially restructure a failing firm so that it can continue operating as agoing concern is called a:a. merger.b. repurchase program.c. liquidation.d. reorganization.e. divestiture.CHAPTER 17II. CONCEPTSCAPITAL STRUCTUREb 16. A firm should select the capital structure which:a. produces the highest cost of capital.b. maximizes the value of the firm.c. minimizes taxes.d. is fully unlevered.e. has no debt.CAPITAL STRUCTUREd 17. The value of a firm is maximized when the:a. cost of equity is maximized.b tax rate is zero.c. levered cost of capital is maximized.d. weighted average cost of capital is minimized.e. debt-equity ratio is minimized.CAPITAL STRUCTUREe 18. The optimal capital structure has been achieved when the:a. debt-equity ratio is equal to 1.b. weight of equity is equal to the weight of debt.c. cost of equity is maximized given a pre-tax cost of debt.d. debt-equity ratio is such that the cost of debt exceeds the cost of equity.e. debt-equity ratio selected results in the lowest possible weighed average cost ofcapital.BREAK-EVEN EBITd 19. ABC, Inc. is comparing two capital structures to determine how to best finance theirf irm’s operations. The first option consists of 100 percent equity financing. The secondoption is based on a debt-equity ratio of .40. What should ABC do if their expectedearnings before interest and taxes (EBIT) is less than the break-even level? Assumethere are no taxes.a. select the leverage option because the debt-equity ratio is less than .50b. select the leverage option since the expected EBIT is less than the break-even levelc. select the unlevered option since the debt-equity ratio is less than .50d. select the unlevered option since the expected EBIT is less than the break-even levele. cannot be determined from the information providedBREAK-EVEN EBITa 20. You have computed the break-even point between a capital structure that has no debtand one that has debt. Assume there are no taxes. At the break-even level, the:a. firm is just earning enough to pay for the cost of the debt.b. firm’s earnings before interest and taxes are equal to zero.c. earnings per share for the levered option are exactly double those of the unleveredoption.d. advantages of leverage exceed the disadvantages of leverage.e. firm has a debt-equity ratio of .50.CHAPTER 17 BREAK-EVEN EBITa 21. Which one of the following statements is correct concerning the relationship between acapital structure with debt and one without debt? Assume there are no taxes.a. When a firm is operating at a point where the actual earnings before interest and taxes(EBIT) exceed the break-even level, then adding debt to the capital structure willincrease the earnings per share (EPS).b. The earnings per share will equal zero when EBIT is zero for a levered firm.c. The advantages of leverage primarily occur when EBIT is just barely positive.d. The firm’s EPS will always be higher if the firm uses leverage.e. EPS are more sensitive to changes in EBIT when a firm is unlevered.HOMEMADE LEVERAGEd 22. Bryan invested in Bryco, Inc. stock when the firm was financed solely with equity. Thefirm is now utilizing debt in its capital structure. To unlever his position, Bryan needsto:a. borrow some money and purchase additional shares of Bryco stock.b. maintain his current position as the debt of the firm did not affect his personal leverageposition.c. sell some shares of Bryco stock and hold the proceeds in cash.d. s ell some shares of Bryco stock and loan it out such that he creates a personal debt-equity ratio equal to that of the firm.e. create a personal debt-equity ratio that is equal to exactly 50 percent of the debt-equityratio of the firm.HOMEMADE LEVERAGEe 23. The capital structure chosen by a firm doesn’t really matter because of:a. taxes.b. the interest tax shield.c. the relationship between dividends and earnings per share.d. the effects of leverage on the cost of equity.e. homemade leverage.M&M PROPOSITION I, NO TAXc 24. M&M Proposition I with no tax supports the argument that:a. business risk determines the return on assets.b. the cost of equity rises as leverage rises.c. it is completely irrelevant how a firm arranges its finances.d. a firm should borrow money to the point where the tax benefit from debt is equal to thecost of the increased probability of financial distress.e. financial risk is determined by the debt-equity ratio.M&M PROPOSITION I, NO TAXa 25. The proposition that the value of a levered firm is equal to the value of an unleveredfirm is known as:a. M&M Proposition I with no tax.b. M&M Proposition II with no tax.c. M&M Proposition I with tax.d. M&M Proposition II with tax.e. static theory proposition.CHAPTER 17M&M PROPOSITION I, NO TAXa 26. The concept of homemade leverage is most associated with:a. M&M Proposition I with no tax.b. M&M Proposition II with no tax.c. M&M Proposition I with tax.d. M&M Proposition II with tax.e. static theory proposition.M&M PROPOSITION II, NO TAXc 27. Which of the following statements are correct in relation to M&M Proposition II withno taxes?I. The return on assets is equal to the weighted average cost of capital.II. Financial risk is determined by the debt-equity ratio.III. Financial risk determines the return on assets.IV. The cost of equity declines when the amount of leverage used by a firm rises.a. I and III onlyb. II and IV onlyc. I and II onlyd. III and IV onlye. I and IV onlyM&M PROPOSITION I, WITH TAXa 28. M&M Proposition I with tax supports the theory that:a. there is a positive linear relationship between the amount of debt in a levered firm andits value.b. the value of a firm is inversely related to the amount of leverage used by the firm.c. t he value of an unlevered firm is equal to the value of a levered firm plus the value ofthe interest tax shield.d. a firm’s cost of capital is the same regardless of the mix of debt and equity used by thefirm.e. a firm’s weighted average cost of capital increases as the debt-equity ratio of the firmrises.M&M PROPOSITION I, WITH TAXd 29. M&M Proposition I with taxes is based on the concept that:a. the optimal capital structure is the one that is totally financed with equity.b. the capital structure of the firm does not matter because investors can use homemadeleverage.c. the firm is better off with debt based on the weighted average cost of capital.d. the value of the firm increases as total debt increases because of the interest tax shield.e. the cost of equity increases as the debt-equity ratio of a firm increases.CHAPTER 17 M&M PROPOSITION II, WITH TAXa 30. M&M Proposition II with taxes:a. has the same general implications as M&M Proposition II without taxes.b. reveals how the interest tax shield relates to the value of a firm.c. supports the argument that business risk is determined by the capital structureemployed by a firm.d. supports the argument that the cost of equity decreases as the debt-equity ratioincreases.e. reaches the final conclusion that the capital structure decision is irrelevant to the valueof a firm.M&M PROPOSITION IIc 31. M&M Proposition II is the proposition that:a. supports the argument that the capital structure of a firm is irrelevant to the value ofthe firm.b. the cost of equity depends on the return on debt, the debt-equity ratio and the taxrate.c. a firm’s cost of equity capital is a positive linear function of the firm’s capitalstructure.d. the cost of equity is equivalent to the required return on the total assets of a firm.e. supports the argument that the size of the pie does not depend on how the pie is sliced. BUSINESS RISKd 32. The business risk of a firm:a. depends on the level of unsystematic risk associated with the assets of the firm.b. is inversely related to the required return on the firm’s assets.c. is dependent upon the relative weights of the debt and equity used to finance the firm.d. has a positive relationship with the cost of equity for that firm.e. has no relationship with the required return on a firm’s assets according to M&MProposition II.FINANCIAL RISKd 33. Which of the following statements concerning financial risk are correct?I. Financial risk is the risk associated with the use of debt financing.II. As financial risk increases so too does the cost of equity.III. Financial risk is wholly dependent upon the financial policy of a firm.IV. Financial risk is the risk that is inherent in a firm’s operations.a. I and III onlyb. II and IV onlyc. II and III onlyd. I, II, and III onlye. I, II, III, and IVCHAPTER 17INTEREST TAX SHIELDe 34. The present value of the interest tax shield is expressed as:a. (T C⨯ D) ÷ R A.b. V U + (T C⨯D).c. [EBIT ⨯ (T C⨯ D)] ÷ R U.d. [EBIT ⨯ (T C⨯ D)] ÷ R A.e. T c⨯ D.INTEREST TAX SHIELDc 35. The interest tax shield has no value for a firm when:I. the tax rate is equal to zero.II. the debt-equity ratio is exactly equal to 1.III. the firm is unlevered.IV. a firm elects 100 percent equity as their capital structure.a. I and III onlyb. II and IV onlyc. I, III, and IV onlyd. II, III, and IV onlye. I, II, and IV onlyINTEREST TAX SHIELDc 36. The interest tax shield is a key reason why:a. the required rate of return on assets rises when debt is added to the capital structure.b. the value of an unlevered firm is equal to the value of a levered firm.c. the net cost of debt to a firm is generally less than the cost of equity.d. the cost of debt is equal to the cost of equity for a levered firm.e. firms prefer equity financing over debt financing.INTEREST TAX SHIELDd 37. Which of the following will tend to diminish the benefit of the interest tax shield givena progressive tax rate structure?I. a reduction in tax ratesII. a large tax loss carryforwardIII. a large depreciation tax deductionIV. a sizeable increase in taxable incomea. I and II onlyb. I and III onlyc. II and III onlyd. I, II, and III onlye. I, II, III, and IVCHAPTER 17 BANKRUPTCYe 38. Which one of the following statements concerning bankruptcy is correct?a. The administrative costs incurred in a bankruptcy are considered indirect bankruptcycosts.b. Bondholders have a greater incentive than stockholders to keep a firm from filing forbankruptcy.c. Bankruptcy is sometimes used as a means to increase payroll costs.d. The assets of a firm tend to increase in value when a firm is in financial distress.e. An implicit cost of bankruptcy is the loss of key employees.BANKRUPTCYe 39. Indirect bankruptcy costs:a. effectively limit the amount of equity a firm issues.b. serve as an incentive to increase the financial leverage of a firm.c. include direct costs such as legal and accounting fees.d. tend to increase as the debt-equity ratio decreases.e. include the costs incurred by a firm as it tries to avoid seeking bankruptcy protection. OPTIMAL CAPITAL STRUCTUREe 40. When a firm is operating with the optimal capital structure:I. the debt-equity ratio will also be optimal.II. the weighted average cost of capital will be at its minimal point.III. the required return on assets will be at its maximum point.IV. the increased benefit from additional debt is equal to the increased bankruptcy costs of that debt.a. I and IV onlyb. II and III onlyc. I and II onlyd. II, III, and IV onlye. I, II, and IV onlyOPTIMAL CAPITAL STRUCTUREd 41. The optimal capital structure will tend to include more debt for firms with:a. the highest depreciation deductions.b. the lowest marginal tax rate.c. substantial tax shields from other sources.d. lower probability of financial distress.e. less taxable income.OPTIMAL CAPITAL STRUCTUREc 42. The optimal capital structure of a firm _____ the marketed claims and _____ thenonmarketed claims against the cash flows of the firm.a. minimizes; minimizesb. minimizes; maximizesc. maximizes; minimizesd. maximizes; maximizese. equates; (leave blank)CHAPTER 17OPTIMAL CAPITAL STRUCTUREc 43. The optimal capital structure:a. will be the same for all firms in the same industry.b. will remain constant over time unless the firm does an acquisition.c. of a firm will vary over time as taxes and market conditions change.d. places more emphasis on the operations of a firm rather than the financing of a firm.e. is unaffected by changes in the financial markets.M&M THEORYb 44. The basic lesson of M&M Theory is that the value of a firm is dependent uponthe:a. capital structure of the firm.b. total cash flows of the firm.c. percentage of a firm to which the bondholders have a claim.d. tax claim placed on the firm by the government.e. size of the stockholders claims on the firm.OBSERVED CAPITAL STRUCTURESb 45. Corporations in the U.S. tend to:a. minimize taxes.b. underutilize debt.c. rely less on equity financing than they should.d. have extremely high debt-equity ratios.e. rely more heavily on bonds than stocks as the major source of financing. OBSERVED CAPITAL STRUCTURESe 46. In general, the capital structures used by U.S. firms:a. tend to overweigh debt in relation to equity.b. are easily explained in terms of earnings volatility.c. are easily explained by analyzing the types of assets owned by the various firms.d. tend to be those which maximize the use of the firm’s available tax shelters.e. vary significantly across industries.BANKRUPTCY PROCESSc 47. A firm is technically insolvent when:a. it has a negative net worth on its balance sheet.b. the value of the firm’s assets is less than the value of the firm’s liabilities.c. it is unable to meet its financial obligations.d. it files the legal forms petitioning for bankruptcy protection.e. the value of its stock declines by more than 50 percent.BANKRUPTCY PROCESSb 48. Which one of the following statements is correct concerning a Chapter 7 bankruptcy?a. A firm in Chapter 7 bankruptcy is reorganizing its operations such that is can return tobeing a viable concern.b. Under a Chapter 7 bankruptcy, a trustee will assume control of the firm’s assets untilthose assets can be liquidated.c. Chapter 7 bankruptcies are always involuntary on the part of the firm.d. Under a Chapter 7 bankruptcy, the claims of creditors are paid prior to theadministrative costs of the bankruptcy.e. Chapter 7 bankruptcy allows a firm to restructure its equity position such that newshares of stock are generally issued prior to the firm coming out of bankruptcy. BANKRUPTCY PROCESSe 49. Under a Chapter 7 bankruptcy, which one of the following is generallyconsidered to be the highest priority claim?a. consumer claimb. dividend payment to preferred shareholderc. company contribution to the employees’ retirement accountd. payment to an unsecured creditore. payment of employee wagesBANKRUPTCY PROCESSe 50. A firm may file for Chapter 11 bankruptcy:I. in an attempt to gain a competitive advantage.II. using a prepack.III. while allowing the current management to continue running the firm.IV. even though it is not insolvent.a. I and III onlyb. I, II, and IV onlyc. I and II onlyd. III and IV onlye. I, II, III, and IVSTATIC THEORY OF CAPITAL STRUCTUREa 51. The static theory of capital structure:a. assumes that the firm’s operations and assets are fixed.b. assumes that the firm’s o perations are fixed but that its assets are increasing.c. supports increasing the leverage employed by a firm when the probability of financialdistress becomes significant.d. equates the benefits of equity financing to the costs associated with the probability offinancial distress.e. states that a firm should operate at the point where the cost of capital is maximized.STATIC THEORY OF CAPITAL STRUCTUREc 52. The static theory of capital structure supports the theory that value-maximizingmanagers will:a. look to the asset side of the balance sheet to increase firm value since the mix of debtand equity selected is unlikely to affect firm value.b. not concern themselves with the capital structure of the firm as it is an irrelevant issue.c. select the capital structure for which the cost associated with the probability offinancial distress equals the benefit of the interest tax shield.d. select an all equity capital structure to ensure the value of the firm is maximized.e. select the capital structure which maximizes the interest tax shield.III. PROBLEMSBREAK-EVEN EBITe 53. Becker Industries is considering an all equity capital structure against one with bothdebt and equity. The all equity capital structure would consist of 25,000 shares of stock.The debt and equity option would consist of 15,000 shares of stock plus $250,000 ofdebt with an interest rate of 7 percent. What is the break-even level of earnings beforeinterest and taxes between these two options? Ignore taxes.a. $41,150b. $41,450c. $41,500d. $42,680e. $43,750BREAK-EVEN EBITa 54. Blackstone, Inc. is currently an all equity firm that has 65,000 shares of stockoutstanding at a market price of $22 a share. The firm has decided to leverage theiroperations by issuing $605,000 of debt at an interest rate of 6.5 percent. This new debtwill be used to repurchase shares of the outstanding stock. The restructuring isexpected to increase the earnings per share. What is the minimum level of earningsbefore interest and taxes that Blackstone is expecting? Ignore taxes.a. $92,950b. $94,700c. $95,250d. $95,400e. $96,150BREAK-EVEN EBITb 55. Martha White’s Fabrics is currently an all equity firm that has 15,000 shares of stockoutstanding at a market price of $12.50 a share. Company management has decided toissue $50,000 worth of debt and use the funds to repurchase shares of the outstandingstock. The interest rate on the debt will be 9 percent. What are the earnings per share atthe break-even level of earnings before interest and taxes? Ignore taxes.a. $1.005b. $1.125c. $1.175d. $1.200e. $1.250HOMEMADE LEVERAGEc 56. Martin & Sons (M&S) currently is an all equity firm with 40,000 shares of stockoutstanding at a market price of $25 a share. The company’s earnings before interestand taxes are $80,000. M&S has decided to add leverage to their financial operationsby issuing $500,000 of debt with a 7 percent interest rate. This $500,000 will be usedto repurchase shares of stock. You own 1,000 shares of M&S stock. You also loan outfunds at a 7 percent rate of interest. How many of your shares of stock in M&S mustyou sell to offset the leverage that the firm is assuming? Assume that you loan out allof the funds you receive from the sale of your stock.a. 400 sharesb. 450 sharesc. 500 sharesd. 550 sharese. 600 sharesHOMEMADE LEVERAGEd 57. You currently own 500 shares in K&S Stores. K&S is currently an all equity firm thathas 25,000 shares of stock outstanding at a market price of $10 a share. The company’searnings before interest and taxes is $20,000. K&S has decided to issue $150,000 ofdebt at a 6 percent rate of interest. This $150,000 will be used to repurchase shares ofstock. How many shares of K&S stock must you sell to unlever your position if youcan loan out funds at a 6 percent rate of interest?a. 150 sharesb. 200 sharesc. 250 sharesd. 300 sharese. 500 sharesHOMEMADE LEVERAGEd 58. R&F Enterprises is an all equity firm with 70,000 shares of stock outstanding at amarket price of $8 a share. The company has earnings before interest and taxes of$42,000. R&F decides to issue $200,000 of debt at a 7 percent rate of interest. The$200,000 will be used to repurchase shares of the outstanding stock. Currently, youown 1,500 shares of R&F stock. How many shares of this stock must you sell tounlever your position if you can loan out funds at a 7 percent rate of interest?a. 489 sharesb. 497 sharesc. 508 sharesd. 536 sharese. 541 sharesa 59. Thompson & Thomson is an all equity firm that has 500,000 shares of stockoutstanding. The company is in the process of borrowing $8 million at 9 percentinterest to repurchase 200,000 shares of the outstanding stock. What is the value of thisfirm if you ignore taxes?a. $20.0 millionb. $20.8 millionc. $21.0 milliond. $21.2 millione. $21.3 millionM&M PROPOSITION I, NO TAXc 60. Uptown Interior Designs is an all equity firm that has 40,000 shares of stockoutstanding. The company has decided to borrow $1 million to buy out the shares of adeceased stockholder who holds 2,500 shares. What is the total value of this firm ifyou ignore taxes?a. $15.5 millionb. $15.6 millionc. $16.0 milliond. $16.8 millione. $17.2 millionM&M PROPOSITION I, NO TAXe 61. You own 25 percent of Unique Vactions, Inc. You have decided to retire and want tosell your shares in this closely held, all equity firm. The other shareholders have agreedto have the firm borrow $1.5 million to purchase your 1,000 shares of stock. What isthe total value of this firm today if you ignore taxes?a. $4.8 millionb. $5.1 millionc. $5.4 milliond. $5.7 millione. $6.0 millionM&M PROPOSITION II, NO TAXd 62. Your firm has a debt-equity ratio of .75. Your pre-tax cost of debt is 8.5 percent andyour required return on assets is 15 percent. What is your cost of equity if you ignoretaxes?a. 11.25 percentb. 12.21 percentc. 16.67 percentd. 19.88 percente. 21.38 percentb 63. Bigelow, Inc. has a cost of equity of 13.56 percent and a pre-tax cost of debt of 7percent. The required return on the assets is 11 percent. What is the firm’s debt-equityratio based on M&M II with no taxes?a. .60b. .64c. .72d. .75e. .80M&M PROPOSITION II, NO TAXd 64. The Backwoods Lumber Co. has a debt-equity ratio of .80. The firm’s required returno n assets is 12 percent and its cost of equity is 15.68 percent. What is the pre-tax costof debt based on M&M II with no taxes?a. 6.76 percentb. 7.00 percentc. 7.25 percentd. 7.40 percente. 7.50 percentM&M PROPOSTION I, WITH TAXb 65. The Winter Wear Company has expected earnings before interest and taxes of $2,100,an unlevered cost of capital of 14 percent and a tax rate of 34 percent. The companyalso has $2,800 of debt that carries a 7 percent coupon. The debt is selling at par value.What is the value of this firm?a. $9,900b. $10,852c. $11,748d. $12,054e. $12,700M&M PROPOSITION I, WITH TAXb 66. Gail’s Dance Studio is currently an all equity firm that h as 80,000 shares of stockoutstanding with a market price of $42 a share. The current cost of equity is 12 percentand the tax rate is 34 percent. Gail is considering adding $1 million of debt with acoupon rate of 8 percent to her capital structure. The debt will be sold at par value.What is the levered value of the equity?a. $2.4 millionb. $2.7 millionc. $3.3 milliond. $3.7 millione. $3.9 million。

公司理财第二版答案英文版

Company Financial Management Second Edition Answer (EnglishVersion)IntroductionIn this document, we present the answers to the questions and exercises in the second edition of the Company Financial Management textbook. This comprehensive guide aims to provide a better understanding of financial management principles and practices for companies.Chapter 1: Introduction to Financial ManagementQuestion 1: Define financial management and explain its significance for businesses.Financial management refers to the process of planning, organizing, controlling, and monitoring a company’s financial resources to achieve its goals and objectives. It involves making strategic financial decisions that optimize the use of funds and contribute to the long-term success of the business. Financial management is essential for businesses as it allows them to:•Allocate resources efficiently•Minimize financial risks•Maximize profitability and shareholder value•Make informed investment decisions•Ensure regulatory complianceQuestion 2: Describe the three primary areas of financial management.The three primary areas of financial management are:1.Capital Budgeting: This involves evaluating andselecting the best long-term investment opportunities that align with the company’s goa ls. It includes analyzing thepotential returns, risks, and cash flows associated with each investment project.2.Capital Structure: Capital structure refers to themix of debt and equity used to finance a company’soperations. Financial managers need to determine theoptimal capital structure that balances the cost of capitaland the risk of the business. This decision affects thecompany’s ability to raise funds and its overall financialstability.3.Working Capital Management: Working capitalmanagement focu ses on managing the company’s short-term assets and liabilities to ensure smooth businessoperations. It includes managing cash flow, inventory,accounts receivable, and accounts payable effectively tomaintain a healthy liquidity position.Question 3: Explain the goal of financial management.The goal of financial management is to maximize shareholder wealth or value. Financial managers aim to make decisions that increase the market value of the company’sshares and generate higher returns for shareholders. This objective is accomplished by making sound financial decisions, such as investing in profitable projects, optimizing the capital structure, and efficiently managing working capital.Chapter 2: Financial Statements and AnalysisExercise 1: Analyzing Financial StatementsUsing the financial statements for Company XYZ provided below, answer the following questions:Income Statement:Year 1Year 2Revenue$500,000$600,000Expenses$300,000$350,000Net Income$200,000$250,000Balance Sheet:Year 1Year 2Assets$800,000$900,000Liabilities$200,000$250,000Equity$600,000$650,000a)Calculate the net profit margin for Year 1 and Year 2.Solution:Net Profit Margin (Year 1) = Net Income (Year 1) / Revenue (Year 1) * 100 = $200,000 / $500,000 * 100 = 40%Net Profit Margin (Year 2) = Net Income (Year 2) / Revenue (Year 2) * 100 = $250,000 / $600,000 * 100 = 41.67%b)Determine the return on equity (ROE) for Year 1 andYear 2.Solution:Return on Equity (Year 1) = Net Income (Year 1) / Equity (Year 1) * 100 = $200,000 / $600,000 * 100 = 33.33%Return on Equity (Year 2) = Net Income (Year 2) / Equity (Year 2) * 100 = $250,000 / $650,000 * 100 = 38.46%c)Calculate the current ratio for Year 1 and Year 2.Solution:Current Ratio (Year 1) = Assets (Year 1) / Liabilities (Year 1) = $800,000 / $200,000 = 4Current Ratio (Year 2) = Assets (Year 2) / Liabilities (Year 2) = $900,000 / $250,000 = 3.6ConclusionIn this document, we provided the answers to selected questions and exercises from the second edition of the Company Financial Management textbook. These answers should help readers enhance their understanding of financial management principles and practices for companies. It is important to note that this document covers only a fraction of the content presented in the textbook and can be used as a supplementary resource for further study.。

《公司理财》课后答案(英文版,第六版).doc

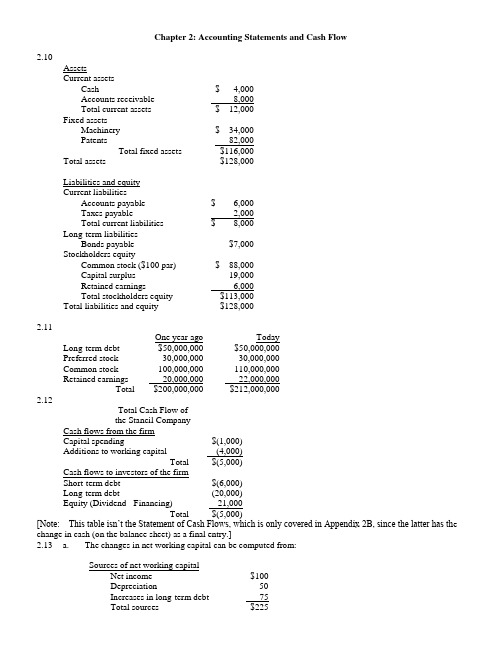

Chapter 2: Accounting Statements and Cash Flow2.10AssetsCurrent assetsCash $ 4,000Accounts receivable 8,000Total current assets $ 12,000Fixed assetsMachinery $ 34,000Patents 82,000Total fixed assets $116,000Total assets $128,000Liabilities and equityCurrent liabilitiesAccounts payable $ 6,000Taxes payable 2,000Total current liabilities $ 8,000Long-term liabilitiesBonds payable $7,000Stockholders equityCommon stock ($100 par) $ 88,000Capital surplus 19,000Retained earnings 6,000Total stockholders equity $113,000Total liabilities and equity $128,0002.11One year ago TodayLong-term debt $50,000,000 $50,000,000Preferred stock 30,000,000 30,000,000Common stock 100,000,000 110,000,000Retained earnings 20,000,000 22,000,000Total $200,000,000 $212,000,0002.12Total Cash Flow ofthe Stancil CompanyCash flows from the firmCapital spending $(1,000)Additions to working capital (4,000)Total $(5,000)Cash flows to investors of the firmShort-term debt $(6,000)Long-term debt (20,000)Equity (Dividend - Financing) 21,000Total $(5,000)[Note: This table isn’t the Statement of Cash Flows, which is only covered in Appendix 2B, since the latter has th e change in cash (on the balance sheet) as a final entry.]2.13 a. The changes in net working capital can be computed from:Sources of net working capitalNet income $100Depreciation 50Increases in long-term debt 75Total sources $225Uses of net working capitalDividends $50Increases in fixed assets* 150Total uses $200Additions to net working capital $25*Includes $50 of depreciation.b.Cash flow from the firmOperating cash flow $150Capital spending (150)Additions to net working capital (25)Total $(25)Cash flow to the investorsDebt $(75)Equity 50Total $(25)Chapter 3: Financial Markets and Net Present Value: First Principles of Finance (Advanced)3.14 $120,000 - ($150,000 - $100,000) (1.1) = $65,0003.15 $40,000 + ($50,000 - $20,000) (1.12) = $73,6003.16 a. ($7 million + $3 million) (1.10) = $11.0 millionb.i. They could spend $10 million by borrowing $5 million today.ii. They will have to spend $5.5 million [= $11 million - ($5 million x 1.1)] at t=1.Chapter 4: Net Present Valuea. $1,000 ⨯ 1.0510 = $1,628.89b. $1,000 ⨯ 1.0710 = $1,967.15c. $1,000 ⨯ 1.0520 = $2,653.30d. Interest compounds on the interest already earned. Therefore, the interest earned inSince this bond has no interim coupon payments, its present value is simply the present value of the $1,000 that will be received in 25 years. Note: As will be discussed in the next chapter, the present value of the payments associated with a bond is the price of that bond.PV = $1,000 /1.125 = $92.30PV = $1,500,000 / 1.0827 = $187,780.23a. At a discount rate of zero, the future value and present value are always the same. Remember, FV =PV (1 + r) t. If r = 0, then the formula reduces to FV = PV. Therefore, the values of the options are $10,000 and $20,000, respectively. You should choose the second option.b. Option one: $10,000 / 1.1 = $9,090.91Option two: $20,000 / 1.15 = $12,418.43Choose the second option.c. Option one: $10,000 / 1.2 = $8,333.33Option two: $20,000 / 1.25 = $8,037.55Choose the first option.d. You are indifferent at the rate that equates the PVs of the two alternatives. You know that rate mustfall between 10% and 20% because the option you would choose differs at these rates. Let r be thediscount rate that makes you indifferent between the options.$10,000 / (1 + r) = $20,000 / (1 + r)5(1 + r)4 = $20,000 / $10,000 = 21 + r = 1.18921r = 0.18921 = 18.921%The $1,000 that you place in the account at the end of the first year will earn interest for six years. The $1,000 that you place in the account at the end of the second year will earn interest for five years, etc. Thus, the account will have a balance of$1,000 (1.12)6 + $1,000 (1.12)5 + $1,000 (1.12)4 + $1,000 (1.12)3= $6,714.61PV = $5,000,000 / 1.1210 = $1,609,866.18a. $1.000 (1.08)3 = $1,259.71b. $1,000 [1 + (0.08 / 2)]2 ⨯ 3 = $1,000 (1.04)6 = $1,265.32c. $1,000 [1 + (0.08 / 12)]12 ⨯ 3 = $1,000 (1.00667)36 = $1,270.24d. $1,000 e0.08 ⨯ 3 = $1,271.25e. The future value increases because of the compounding. The account is earning interest on interest. Essentially, the interest is added to the account balance at the e nd of every compounding period. During the next period, the account earns interest on the new balance. When the compounding period shortens, the balance that earns interest is rising faster.The price of the consol bond is the present value of the coupon payments. Apply the perpetuity formula to find the present value. PV = $120 / 0.15 = $800a. $1,000 / 0.1 = $10,000b. $500 / 0.1 = $5,000 is the value one year from now of the perpetual stream. Thus, the value of theperpetuity is $5,000 / 1.1 = $4,545.45.c. $2,420 / 0.1 = $24,200 is the value two years from now of the perpetual stream. Thus, the value of the perpetuity is $24,200 / 1.12 = $20,000.pply the NPV technique. Since the inflows are an annuity you can use the present value of an annuity factor.ANPV = -$6,200 + $1,200 81.0= -$6,200 + $1,200 (5.3349)= $201.88Yes, you should buy the asset.Use an annuity factor to compute the value two years from today of the twenty payments. Remember, the annuity formula gives you the value of the stream one year before the first payment. Hence, the annuity factor will give you the value at the end of year two of the stream of payments.A= $2,000 (9.8181)Value at the end of year two = $2,000 20.008= $19,636.20The present value is simply that amount discounted back two years.PV = $19,636.20 / 1.082 = $16,834.88The easiest way to do this problem is to use the annuity factor. The annuity factor must be equal to $12,800 / $2,000 = 6.4; remember PV =C A T r. The annuity factors are in the appendix to the text. To use the factor table to solve this problem, scan across the row labeled 10 years until you find 6.4. It is close to the factor for 9%, 6.4177. Thus, the rate you will receive on this note is slightly more than 9%.You can find a more precise answer by interpolating between nine and ten percent.[ 10% ⎤[6.1446 ⎤a ⎡r ⎥bc ⎡6.4 ⎪ d⎣9%⎦⎣6.4177 ⎦By interpolating, you are presuming that the ratio of a to b is equal to the ratio of c to d.(9 - r ) / (9 - 10) = (6.4177 - 6.4 ) / (6.4177 - 6.1446)r = 9.0648%The exact value could be obtained by solving the annuity formula for the interest rate. Sophisticated calculators can compute the rate directly as 9.0626%.[Note: A standard financial calculator’s TVM keys can solve for this rate. With annuity flows, the IRR key on “advanced” financial c alculators is unnecessary.]a. The annuity amount can be computed by first calculating the PV of the $25,000 which youThat amount is $17,824.65 [= $25,000 / 1.075]. Next compute the annuity which has the same present value.A$17,824.65 = C 507.0$17,824.65 = C (4.1002)C = $4,347.26Thus, putting $4,347.26 into the 7% account each year will provide $25,000 five years from today.b. The lump sum payment must be the present value of the $25,000, i.e., $25,000 / 1.075 =$17,824.65The formula for future value of any annuity can be used to solve the problem (see footnote 11 of the text).Option one: This cash flow is an annuity due. To value it, you must use the after-tax amounts. Theafter-tax payment is $160,000 (1 - 0.28) = $115,200. Value all except the first payment using the standard annuity formula, then add back the first payment of $115,200 to obtain the value of this option.AValue = $115,200 + $115,200 30.010= $115,200 + $115,200 (9.4269)= $1,201,178.88Option two: This option is valued similarly. You are able to have $446,000 now; this is already on an after-tax basis. You will receive an annuity of $101,055 for each of the next thirty years. Those payments are taxable when you receive them, so your after-tax payment is $72,759.60 [= $101,055 (1 - 0.28)].AValue = $446,000 + $72,759.60 30.010= $446,000 + $72,759.60 (9.4269)= $1,131,897.47Since option one has a higher PV, you should choose it.et r be the rate of interest you must earn.$10,000(1 + r)12 = $80,000(1 + r)12= 8r = 0.18921 = 18.921%First compute the present value of all the payments you must make for your children’s educati on. The value as of one year before matriculation of one child’s education isA= $21,000 (2.8550) = $59,955.$21,000 415.0This is the value of the elder child’s education fourteen years from now. It is the value of the younger child’s education sixteen years from today. The present value of these isPV = $59,955 / 1.1514 + $59,955 / 1.1516= $14,880.44You want to make fifteen equal payments into an account that yields 15% so that the present value of the equal payments is $14,880.44.A= $14,880.44 / 5.8474 = $2,544.80Payment = $14,880.44 / 15.015This problem applies the growing annuity formula. The first payment is$50,000(1.04)2(0.02) = $1,081.60.PV = $1,081.60 [1 / (0.08 - 0.04) - {1 / (0.08 - 0.04)}{1.04 / 1.08}40]= $21,064.28This is the present value of the payments, so the value forty years from today is$21,064.28 (1.0840) = $457,611.46se the discount factors to discount the individual cash flows. Then compute the NPV of the project. NoticeYou can still use the factor tables to compute their PV. Essentially, they form cash flows that are a six year annuity less a two year annuity. Thus, the appropriate annuity factor to use with them is 2.6198 (= 4.3553 - 1.7355).Year Cash Flow Factor PV0.9091 $636.371$70020.8264 743.769003 1,000 ⎤4 1,000 ⎥ 2.6198 2,619.805 1,000 ⎥6 1,000 ⎦7 1,250 0.5132 641.508 1,375 0.4665 641.44Total $5,282.87NPV = -$5,000 + $5,282.87= $282.87Purchase the machine.Chapter 5: How to Value Bonds and StocksThe amount of the semi-annual interest payment is $40 (=$1,000 ⨯ 0.08 / 2). There are a total of 40 periods;i.e., two half years in each of the twenty years in the term to maturity. The annuity factor tables can be usedto price these bonds. The appropriate discount rate to use is the semi-annual rate. That rate is simply the annual rate divided by two. Thus, for part b the rate to be used is 5% and for part c is it 3%.A+F/(1+r)40PV=C Tra. $40 (19.7928) + $1,000 / 1.0440 = $1,000Notice that whenever the coupon rate and the market rate are the same, the bond is priced at par.b. $40 (17.1591) + $1,000 / 1.0540 = $828.41Notice that whenever the coupon rate is below the market rate, the bond is priced below par.c. $40 (23.1148) + $1,000 / 1.0340 = $1,231.15Notice that whenever the coupon rate is above the market rate, the bond is priced above par.a. The semi-annual interest rate is $60 / $1,000 = 0.06. Thus, the effective annual rate is 1.062 - 1 =0.1236 = 12.36%.A+ $1,000 / 1.0612b. Price = $30 12.006= $748.48A+ $1,000 / 1.0412c. Price = $30 1204.0= $906.15Note: In parts b and c we are implicitly assuming that the yield curve is flat. That is, the yield in year 5applies for year 6 as well.rice = $2 (0.72) / 1.15 + $4 (0.72) / 1.152 + $50 / 1.153= $36.31The number of shares you own = $100,000 / $36.31 = 2,754 sharesPrice = $1.15 (1.18) / 1.12 + $1.15 (1.182) / 1.122 + $1.152 (1.182) / 1.123+ {$1.152 (1.182)(1.06) / (0.12 - 0.06)} / 1.123= $26.95[Insert before last sentence of question: Assume that dividends are a fixed proportion of earnings.] Dividend one year from now = $5 (1 - 0.10) = $4.50Price = $5 + $4.50 / {0.14 - (-0.10)}= $23.75Since the current $5 dividend has not yet been paid, it is still included in the stock price.Chapter 6: Some Alternative Investment Rulesa. Payback period of Project A = 1 + ($7,500 - $4,000) / $3,500 = 2 yearsPayback period of Project B = 2 + ($5,000 - $2,500 -$1,200) / $3,000 = 2.43 yearsProject A should be chosen.b. NPV A = -$7,500 + $4,000 / 1.15 + $3,500 / 1.152 + $1,500 / 1.153 = -$388.96NPV B = -$5,000 + $2,500 / 1.15 + $1,200 / 1.152 + $3,000 / 1.153 = $53.83Project B should be chosen.a. Average Investment:($16,000 + $12,000 + $8,000 + $4,000 + 0) / 5 = $8,000Average accounting return:$4,500 / $8,000 = 0.5625 = 56.25%b. 1. AAR does not consider the timing of the cash flows, hence it does not consider the timevalue of money.2. AAR uses an arbitrary firm standard as the decision rule.3. AAR uses accounting data rather than net cash flows.aAverage Investment = (8000 + 4000 + 1500 + 0)/4 = 3375.00Average Net Income = 2000(1-0.75) = 1500=> AAR = 1500/3375=44.44%a. Solve x by trial and error:-$8,000 + $4,000 / (1 + x) + $3000 / (1 + x)2 + $2,000 / (1 + x)3 = 0x = 6.93%b. No, since the IRR (6.93%) is less than the discount rate of 8%.Alternatively, the NPV @ a discount rate of 0.08 = -$136.62.a. Solve r in the equation:$5,000 - $2,500 / (1 + r) - $2,000 / (1 + r)2 - $1,000 / (1 + r)3- $1,000 / (1 + r)4 = 0By trial and error,IRR = r = 13.99%b. Since this problem is the case of financing, accept the project if the IRR is less than the required rate of return.IRR = 13.99% > 10%Reject the offer.c. IRR = 13.99% < 20%Accept the offer.d. When r = 10%:NPV = $5,000 - $2,500 / 1.1 - $2,000 / 1.12 - $1,000 / 1.13 - $1,000 / 1.14When r = 20%:NPV = $5,000 - $2,500 / 1.2 - $2,000 / 1.22 - $1,000 / 1.23 - $1,000 / 1.24= $466.82Yes, they are consistent with the choices of the IRR rule since the signs of the cash flows change only once.A/ $160,000 = 1.04PI = $40,000 715.0Since the PI exceeds one accept the project.Chapter 7: Net Present Value and Capital BudgetingSince there is uncertainty surrounding the bonus payments, which McRae might receive, you must use the expected value of McRae’s bonuses in the computation of the PV of his contract. McRae’s salary plus the expected value of his bonuses in years one through three is$250,000 + 0.6 ⨯ $75,000 + 0.4 ⨯ $0 = $295,000.Thus the total PV of his three-year contract isPV = $400,000 + $295,000 [(1 - 1 / 1.12363) / 0.1236]+ {$125,000 / 1.12363} [(1 - 1 / 1.123610 / 0.1236]= $1,594,825.68EPS = $800,000 / 200,000 = $4NPVGO = (-$400,000 + $1,000,000) / 200,000 = $3Price = EPS / r + NPVGO= $4 / 0.12 + $3=$36.33Year 0 Year 1 Year 2 Year 3 Year 4 Year 51. Annual Salary$120,000 $120,000 $120,000 $120,000 $120,000 Savings2. Depreciation 100,000 160,000 96,000 57,600 57,6003. Taxable Income 20,000 -40,000 24,000 62,400 62,4004. Taxes 6,800 -13,600 8,160 21,216 21,2165. Operating Cash Flow113,200 133,600 111,840 98,784 98,784 (line 1-4)$100,000 -100,0006. ∆ Net workingcapital7. Investment $500,000 75,792*8. Total Cash Flow -$400,000 $113,200 $133,600 $111,840 $98,784 $74,576*75,792 = $100,000 - 0.34 ($100,000 - $28,800)NPV = -$400,000+ $113,200 / 1.12 + $133,600 / 1.122 + $111,840 / 1.123+ $98,784 / 1.124 + $74,576 / 1.125= -$7,722.52Real interest rate = (1.15 / 1.04) - 1 = 10.58%NPV A = -$40,000+ $20,000 / 1.1058 + $15,000 / 1.10582 + $15,000 / 1.10583= $1,446.76NPV B = -$50,000+ $10,000 / 1.15 + $20,000 / 1.152 + $40,000 / 1.153= $119.17Choose project A.PV = $120,000 / {0.11 - (-0.06)}t = 0 t = 1 t = 2 t = 3 t = 4 t = 5 t = 6 ...$12,000 $6,000 $6,000 $6,000$4,000$12,000 $6,000 $6,000 ...The present value of one cycle is:A+ $4,000 / 1.064PV = $12,000 + $6,000 306.0= $12,000 + $6,000 (2.6730) + $4,000 / 1.064= $31,206.37The cycle is four years long, so use a four year annuity factor to compute the equivalent annual cost (EAC).AEAC = $31,206.37 / 406.0= $31,206.37 / 3.4651= $9,006The present value of such a stream in perpetuity is$9,006 / 0.06 = $150,100o evaluate the word processors, compute their equivalent annual costs (EAC).BangAPV(costs) = (10 ⨯ $8,000) + (10 ⨯ $2,000) 414.0= $80,000 + $20,000 (2.9137)= $138,274EAC = $138,274 / 2.9137= $47,456IOUAPV(costs) = (11 ⨯ $5,000) + (11 ⨯ $2,500) 3.014- (11 ⨯ $500) / 1.143= $55,000 + $27,500 (2.3216) - $5,500 / 1.143= $115,132EAC = $115,132 / 2.3216= $49,592BYO should purchase the Bang word processors.Chapter 8: Strategy and Analysis in Using Net Present ValueThe accounting break-even= (120,000 + 20,000) / (1,500 - 1,100)= 350 units. The accounting break-even= 340,000 / (2.00 - 0.72)= 265,625 abalonesb. [($2.00 ⨯ 300,000) - (340,000 + 0.72 ⨯ 300,000)] (0.65)= $28,600This is the after tax profit.Chapter 9: Capital Market Theory: An Overviewa. Capital gains = $38 - $37 = $1 per shareb. Total dollar returns = Dividends + Capital Gains = $1,000 + ($1*500) = $1,500 On a per share basis, this calculation is $2 + $1 = $3 per sharec. On a per share basis, $3/$37 = 0.0811 = 8.11% On a total dollar basis, $1,500/(500*$37) = 0.0811 = 8.11%d. No, you do not need to sell the shares to include the capital gains in the computation of the returns. The capital gain is included whether or not you realize the gain. Since you could realize the gain if you choose, you should include it.The expected holding period return is:()[]%865.1515865.052$/52$75.54$50.5$==-+There appears to be a lack of clarity about the meaning of holding period returns. The method used in the answer to this question is the one used in Section 9.1. However, the correspondence is not exact, because in this question, unlike Section 9.1, there are cash flows within the holding period. The answer above ignores the dividend paid in the first year. Although the answer above technically conforms to the eqn at the bottom of Fig. 9.2, the presence of intermediate cash flows that aren’t accounted for renders th is measure questionable, at best. There is no similar example in the body of the text, and I have never seen holding period returns calculated in this way before.Although not discussed in this book, there are two generally accepted methods of computing holding period returns in the presence of intermediate cash flows. First, the time weighted return calculates averages (geometric or arithmetic) of returns between cash flows. Unfortunately, that method can’t be used here, because we are not given the va lue of the stock at the end of year one. Second, the dollar weighted measure calculates the internal rate of return over the entire holding period. Theoretically, that method can be applied here, as follows: 0 = -52 + 5.50/(1+r) + 60.25/(1+r)2 => r = 0.1306.This produces a two year holding period return of (1.1306)2 – 1 = 0.2782. Unfortunately, this book does not teach the dollar weighted method.In order to salvage this question in a financially meaningful way, you would need the value of the stock at the end of one year. Then an illustration of the correct use of the time-weighted return would be appropriate. A complicating factor is that, while Section 9.2 illustrates the holding period return using the geometric return for historical data, the arithmetic return is more appropriate for expected future returns.E(R) = T-Bill rate + Average Excess Return = 6.2% + (13.0% -3.8%) = 15.4%. Common Treasury Realized Stocks Bills Risk Premium -7 32.4% 11.2% 21.2%-6 -4.9 14.7 -19.6-5 21.4 10.5 10.9 -4 22.5 8.8 13.7 -3 6.3 9.9 -3.6 -2 32.2 7.7 24.5 Last 18.5 6.2 12.3 b. The average risk premium is 8.49%.49.873.125.246.37.139.106.192.21=++-++- c. Yes, it is possible for the observed risk premium to be negative. This can happen in any single year. The.b.Standard deviation = 03311.0001096.0=.b.Standard deviation = = 0.03137 = 3.137%.b.Chapter 10: Return and Risk: The Capital-Asset-Pricing Model (CAPM)a. = 0.1 (– 4.5%) + 0.2 (4.4%) + 0.5 (12.0%) + 0.2 (20.7%) = 10.57%b.σ2 = 0.1 (–0.045 – 0.1057)2 + 0.2 (0.044 – 0.1057)2 + 0.5 (0.12 – 0.1057)2+ 0.2 (0.207 – 0.1057)2 = 0.0052σ = (0.0052)1/2 = 0.072 = 7.20%Holdings of Atlas stock = 120 ⨯ $50 = $6,000 ⨯ $20 = $3,000Weight of Atlas stock = $6,000 / $9,000 = 2 / 3Weight of Babcock stock = $3,000 / $9,000 = 1 / 3a. = 0.3 (0.12) + 0.7 (0.18) = 0.162 = 16.2%σP 2= 0.32 (0.09)2 + 0.72 (0.25)2 + 2 (0.3) (0.7) (0.09) (0.25) (0.2)= 0.033244σP= (0.033244)1/2 = 0.1823 = 18.23%a.State Return on A Return on B Probability1 15% 35% 0.4 ⨯ 0.5 = 0.22 15% -5% 0.4 ⨯ 0.5 = 0.23 10% 35% 0.6 ⨯ 0.5 = 0.34 10% -5% 0.6 ⨯ 0.5 = 0.3b. = 0.2 [0.5 (0.15) + 0.5 (0.35)] + 0.2[0.5 (0.15) + 0.5 (-0.05)]+ 0.3 [0.5 (0.10) + 0.5 (0.35)] + 0.3 [0.5 (0.10) + 0.5 (-0.05)]= 0.135= 13.5%Note: The solution to this problem requires calculus.Specifically, the solution is found by minimizing a function subject to a constraint. Calculus ability is not necessary to understand the principles behind a minimum variance portfolio.Min { X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)}subject to X A + X B = 1Let X A = 1 - X B. Then,Min {(1 - X B)2σA2 + X B2σB2+ 2(1 - X B) X B Cov (R A, R B)}Take a derivative with respect to X B.d{∙} / dX B = (2 X B - 2) σA2+ 2 X B σB2 + 2 Cov(R A, R B) - 4 X B Cov(R A, R B)Set the derivative equal to zero, cancel the common 2 and solve for X B.X BσA2- σA2+ X B σB2 + Cov(R A, R B) - 2 X B Cov(R A, R B) = 0X B = {σA2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}andX A = {σB2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}Using the data from the problem yields,X A = 0.8125 andX B = 0.1875.a. Using the weights calculated above, the expected return on the minimum variance portfolio isE(R P) = 0.8125 E(R A) + 0.1875 E(R B)= 0.8125 (5%) + 0.1875 (10%)= 5.9375%b. Using the formula derived above, the weights areX A = 2 / 3 andX B = 1 / 3c. The variance of this portfolio is zero.σP 2= X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)= (4 / 9) (0.01) + (1 / 9) (0.04) + 2 (2 / 3) (1 / 3) (-0.02)= 0This demonstrates that assets can be combined to form a risk-free portfolio.14.2%= 3.7%+β(7.5%) ⇒β = 1.40.25 = R f + 1.4 [R M– R f] (I)0.14 = R f + 0.7 [R M– R f] (II)(I) – (II)=0.11 = 0.7 [R M– R f] (III)[R M– R f ]= 0.1571Put (III) into (I) 0.25 = R f + 1.4[0.1571]R f = 3%[R M– R f ]= 0.1571R M = 0.1571 + 0.03= 18.71%a. = 4.9% + βi (9.4%)βD= Cov(R D, R M) / σM 2 = 0.0635 / 0.04326 = 1.468= 4.9 + 1.468 (9.4) = 18.70%Weights:X A = 5 / 30 = 0.1667X B = 10 / 30 = 0.3333X C = 8 / 30 = 0.2667X D = 1 - X A - X B - X C = 0.2333Beta of portfolio= 0.1667 (0.75) + 0.3333 (1.10) + 0.2667 (1.36) + 0.2333 (1.88)= 1.293= 4 + 1.293 (15 - 4) = 18.22%a. (i) βA= ρA,MσA / σMρA,M= βA σM / σA= (0.9) (0.10) / 0.12= 0.75(ii) σB= βB σM / ρB,M= (1.10) (0.10) / 0.40= 0.275(iii) βC= ρC,MσC / σM= (0.75) (0.24) / 0.10= 1.80(iv) ρM,M= 1(v) βM= 1(vi) σf= 0(vii) ρf,M= 0(viii) βf= 0b. SML:E(R i) = R f + βi {E(R M) - R f}= 0.05 + (0.10) βiSecurity βi E(R i)A 0.13 0.90 0.14B 0.16 1.10 0.16C 0.25 1.80 0.23Security A performed worse than the market, while security C performed better than the market.Security B is fairly priced.c. According to the SML, security A is overpriced while security C is under-priced. Thus, you could invest in security C while sell security A (if you currently hold it).a. The typical risk-averse investor seeks high returns and low risks. To assess thetwo stocks, find theReturns:State of economy ProbabilityReturn on A*Recession 0.1 -0.20 Normal 0.8 0.10 Expansion0.10.20* Since security A pays no dividend, the return on A is simply (P 1 / P 0) - 1. = 0.1 (-0.20) + 0.8 (0.10) + 0.1 (0.20) = 0.08 = 0.09 This was given in the problem.Risk:R A - (R A -)2 P ⨯ (R A -)2 -0.28 0.0784 0.00784 0.02 0.0004 0.00032 0.12 0.0144 0.00144 Variance 0.00960Standard deviation (R A ) = 0.0980βA = {Corr(R A , R M ) σ(R A )} / σ(R M ) = 0.8 (0.0980) / 0.10= 0.784βB = {Corr(R B , R M ) σ(R B )} / σ(R M ) = 0.2 (0.12) / 0.10= 0.24The return on stock B is higher than the return on stock A. The risk of stock B, as measured by itsbeta, is lower than the risk of A. Thus, a typical risk-averse investor will prefer stock B.b. = (0.7) + (0.3) = (0.7) (0.8) + (0.3) (0.09) = 0.083σP 2= 0.72 σA 2 + 0.32 σB 2 + 2 (0.7) (0.3) Corr (R A , R B ) σA σB = (0.49) (0.0096) + (0.09) (0.0144) + (0.42) (0.6) (0.0980) (0.12) = 0.0089635 σP = = 0.0947 c. The beta of a portfolio is the weighted average of the betas of the components of the portfolio. βP = (0.7) βA + (0.3) βB = (0.7) (0.784) + (0.3) (0.240) = 0.621Chapter 11:An Alternative View of Risk and Return: The Arbitrage Pricing Theorya. Stock A:()()R R R R R A A A m m Am A=+-+=+-+βεε105%12142%...Stock B:()()R R R R R B B m m Bm B=+-+=+-+βεε130%098142%...Stock C:()R R R R R C C C m m Cm C=+-+=+-+βεε157%137142%)..(.b.()[]()[]()[]()()()()()()[]()()CB A m cB A m c m B m A m CB A P 25.045.030.0%2.14R 1435.1%925.1225.045.030.0%2.14R 37.125.098.045.02.130.0%7.1525.0%1345.0%5.1030.0%2.14R 37.1%7.1525.0%2.14R 98.0%0.1345.0%2.14R 2.1%5.1030.0R 25.0R 45.0R 30.0R ε+ε+ε+-+=ε+ε+ε+-+++++=ε+-++ε+-++ε+-+=++= c.i.()R R R A B C =+-==+-==+-=105%1215%142%)1113%09815%142%)137%157%13715%142%168%..(..46%.(......ii.R P =+-=12925%1143515%142%)138398%..(..To determine which investment investor would prefer, you must compute the variance of portfolios created bymany stocks from either market. Note, because you know that diversification is good, it is reasonable to assume that once an investor chose the market in which he or she will invest, he or she will buy many stocks in that market.Known:E EF ====001002 and and for all i.i σσεε..Assume: The weight of each stock is 1/N; that is, X N i =1/for all i.If a portfolio is composed of N stocks each forming 1/N proportion of the portfolio, the return on the portfolio is 1/N times the sum of the returns on the N stocks. Recall that the return on each stock is 0.1+βF+ε.()()()()()()[]()()()()()()()[]()[]()[]()()[]()()()()()j i 2j i 22j i i 2222222222P P P P iP ,0.04Corr 0.01,Cov s =isvariance the ,N as limit In the ,Cov 1/N 1s 1/N s )(1/N 1/N F 2F E 1/N F E 0.10.1/N F 0.1E R E R E R Var 0.101/N 00.1E 1/N F E 0.11/N F 0.1E R E 1/N F 0.1F 0.1(1/N)R 1/N R εε+β=εε+β∞⇒εε-+ε+β=ε∑+εβ+β=ε+β=-ε+β+=-==+β+=ε+β+=ε∑+β+=ε+β+=ε+β+==∑∑∑∑∑∑∑∑()()()()()()Thus,F R f E R E R Var R Corr Var R Corr ii ip P p i j PijR 1i =++=++===+=+010*********002250040002500412212111222.........,,εεεεεεa.()()()()Corr Corr Var R Var R i j i j p pεεεε112212000225000225,,..====Since Var ()()R p 1 Var R 2p 〉, a risk averse investor will prefer to invest in the second market.b. Corr ()()εεεε112090i j j ,.,== and Corr 2i()()Var R Var R pp120058500025==..。

[精选]罗斯《公司理财》(厦门大学沈艺峰老师)上

![[精选]罗斯《公司理财》(厦门大学沈艺峰老师)上](https://img.taocdn.com/s3/m/8392fa5d814d2b160b4e767f5acfa1c7aa0082ec.png)

第一章 导 论 Chapter 1 Introduction

《公司理财》的课程内容

可持续增长模型

公司理财 Corporate Finance

1

外部资金需要量

财务分析

如何才能顺利通过本门课程? How to survive?

• 案例(case) 20%Biblioteka • 期中测试20%

• 期末考试(final examination) 50%

• 做好各项财务收支的计划、控 制、核算、分析和考核工作

• 依法合理筹集资金

• 有效利用各项资产,努力提高 经济效益

第一章 导 论 Chapter 1 Introduction

公司理财的环境

• 金融环境 • 税收环境 • 法律环境 • 社会环境 • 政府

公司理财 Corporate Finance

公司理财 Corporate Finance

1

第四章 流动资金管理 Chapter 4 Working Capital Management

流动资金管理

• 流动资金(Working Capital)指占用在流动 资产上的资金。

• 流动资产指可在一年内 或一个营业周期内转换 成现金或运用的其他资 产。

Q* = 最优库存现金持有量

公司理财 Corporate Finance

1

第四章 流动资金管理 Chapter 4 Working Capital Management

米勒-俄尔(Miller-Orr)模型

3b 2

3

Z= 4i

h = 3Z

Z = 最优库存现金持有量 b = 变现成本

= 日净现金流量的方差

可持续增长模型-另一种思维

• 资产=负债 + 权益

公司理财第七版Chap017

17-18

Dividend Policy Irrelevance: Example 2

Case 2: In an attempt to increase share value, this same firm plans to instead pay annual dividends of $10 per share in perpetuity, and still shareholders expect an 8% rate of return. Assume 1,000,000 shares outstanding. What is the present value of each share?

Cash Dividend-Payment of cash by the firm to its

shareholders

Regular Dividend Special Dividend

Stock Dividend/Split

Distributions of additional shares to a firm’s stockholders

Stock Repurchase – When a firm buys back stock from its shareholders.

Four ways to implement:

1.

2.

Open-market repurchase

Tender offer Auction Direct negotiation

What is the effect of a change in dividend payout policy, given a firm’s current capital budgeting and borrowing decisions?

公司理财罗斯中文版15

Sniffles公司的目标债务权益率是0.90。它的WACC是13%,税率是35%。 a. 如果Sniffles公司的权益成本是18%,税前债务成本是多少? b. 如果你所知道的是税后债务成本为7.5%,那么权益成本是多少?

15. 求WACC

已知有关Dunhill电力公司的下列信息,假定公司的税率是35%,求WACC。 债券:3 000张票面利率为8%、面值为1 000美元的债券流通在外,20年后到期,以面值的103%出售;该债券每半年付 息一次。 普通股:90 000股流通在外,每股销售价格为45美元;贝塔系数是1.20。 优先股:13 000股股利率为7%的优先股流通在外,目前的销售价格是每股108美元。 市场:市场风险溢酬是8%,无风险利率是6%。

利用DCF模型来确定权益资本成本,有哪些优点?利用这个模型来求权益成本时,你需要哪些具体的信息?你可以通 过哪些方法来取得估计值?

6. 证券市场线(SML)权益成本估计

利用SML法来求权益资本成本,有哪些优点?有哪些缺点?利用这种方法时,你需要哪些具体的信息?这些变量都可 以通过观察得到,还是需要估计?你可以通过哪些方法来取得这些估计值呢?

15.3 因为Watta公司同时利用债务和权益来筹集经营所需的资金,我们首先必须计算加权平均发行成本。和15.2题一 样,权益筹资所占的百分比是2/3,因此加权平均发行成本是:

fA = (E/V)×fE + (D/V)×fD

第15章部资 本 成 本部部105

= 2/3×16% + 1/3×2% = 11.33%

10. 税负和WACC

Modigliani制造公司的目标债务权益率是0.75。它的权益成本是18%,债务成本是10%。如果税率是35%,Modigliani制 造公司的WACC是多少?

公司理财第17章

Chapter 17: Valuation and Capital Budgeting for the Levered Firm CONCEPT QUESTIONS - CHAPTER 1717.1∙How is the APV method applied?APV is equal to the NPV of the project (i.e. the value of the project for anunlevered firm) plus the NPV of financing side effects.∙What additional information beyond NPV does one need to calculate A|PV?NPV of financing side effects (NPVF)>17.2 ∙How is the FTE Method applied?FTE calls for the discounting of the cash flows of a project to the equity holder at the cost of equity capital.∙What information is needed to calculate FTE?Levered cash flow and the cost of equity capital.17.3∙How is the WACC method applied?WACC calls for the discounting of unlevered cash flows of a project (UCF) at the weighted average cost of capital, WACC.17.4∙What is the main difference between AAPV and WACC?WACC is based upon a target debt rate and APV is based upon the level of debt.∙What is the main difference between the FTE approach and the two other approaches?FTE uses levered cash flow and other methods use unlevered cash flow.∙When should the APV method be used?When the level of debt is known in each future period.∙When should the FTE and WACC approaches be used?When the target debt ratio is known.Answers to End-of-Chapter Problems17.1 a. The maximum price that Hertz should be willing to pay for a fleet of cars with allequity funding is the price that makes the NPV of the fleet zero. Let I be the cost ofthe fleet. Then the NPV is simply the outflows (-I) plus the PV of the after-taxearnings plus the PV of the depreciation tax shield.⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡-+⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡--+-==0.06(1.06)11)(0.34)(I/50.10(1.10)11,000)0.34)($100(1I 0NPV 55I = $350,625.29b. APV = Base-case (B/C) NPV + NPV of the LoanBase-case NPV:There are two ways to determine the B/C NPV. One way is to compute it directly using the formula in part a and substituting $325,000 for I.Alternatively,NPV = 50.150.06$66,000A ](0.34/5)A I[1+-- Since, I = $325,000, NPV = $18,285.17NPV of the Loan:There are two ways to compute the NPV of the loan. You can compute the actual NPV of the loan, or you can compute the PV of the interest tax shield.Method One:NPV(Loan) = Amount borrowed - PV of the after-tax interest payment - PV of theprincipal1.08$200,0000.08(1.08)11))($200,0000.34)(0.08(1$200,000=55-⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡--- = $21,720.34Method Two:PV(Tax Shield) = $21,720.340.08(1.08)110)8)($200,00(0.34)(0.05=⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡- Therefore, the APV is:APV = $18,285.17 + $21,720.34 = $40,005.51c. Use of the subsidized loan will increase the NPV of the loan. Thus, it will allow Honda to charge more for the fleet of cars. To compute the maximum price Hertzwill pay, set the APV equal to zero.403,222.85$I (1.08)$200,0000.08(1.08)11))($200,0000.34)(0.05(1$200,0000.061.0611)(0.34)(I/50.101.1011,000)0.34)($100(1I 0APV 5555=-⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡---+⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡-+⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡--+-==Note: When a subsidy exists on a loan, you cannot use the PV (Tax Shield) methodto compute the NPV of the loan. This is true because even with an interest rate subsidy, the appropriate rate by which to discount the after-tax interest payments is the market rate of interest. The PV (Tax Shield) method presumes the interest rate and the discount rate are the same.17.2 a. APV= Base-case (B/C) NPV - Floatation costs + NPV of the LoanBase-case NPV:Base-case NPV= Outflows + Present value of the depreciation tax shield + Presentvalue of the after-tax cash revenues less expenses4$168,875.50.181.18110,000)0.3)($9,00(10.061.0611,000)(0.3)($700$2,100,00033-=⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡--+⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡-+-=Flotation Costs:Net proceeds are $2.1 million and flotation costs are 1% of gross. Gross proceeds = $2,100,000/(1-0.01)=$2,121,212.12 Flotation costs = $21,212.12Annual tax deduction = $21,212.12/3 = $7,070.71 Annual tax shield = $7,070.71 x 0.30 = $2,121.21 Net cost = Flotation cost - NPV (tax shield)= $21,212.12 - ($2,121.21)(2.6730) = $15,542.12NPV of the Loan:There are two ways to compute the NPV of the loan. You can compute the actual NPV of the loan, or you can compute the PV of the interest tax shield.Method One:NPV (Loan) = Amount Borrowed - PV of the after-tax interest payments - PVof the principal1$189,425.1(1.125).12$2,121,2120.125(1.125)1112.12))($2,121,20.3)(0.125(1.12$2,121,212NPV(Loan)33=-⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡---=Method Two:1$189,425.10.125(1.125)1112.12))($2,121,20.3)(0.125(shield)(Tax PV 3=⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡-= Therefore, the APV is:APV = -$168,875.54 - $15,542.12 + $189,425.11= $5,007.45Peatco should undertake the project!b. Using the City Council’s loan , the only numbers that will change are those in the NPV of the loan. Now the interest payments are $212,121.21 (=0.10 x$2,121,212.12) rather than $265,151.51 (= 0.125 x $2,121,212.12).$227,823.5(1.125).12$2,121,2120.125(1.125)112.12)($2,121,210.3)(0.10)(1.12$2,121,212NPV(Loan)33=-⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡---=Therefore, the APV is:APV = -$168,875.54 - $15,542.12 + $277,823.50= $93,405.84Peatco should accept the City Council’s offer and begin the project.Note: When a subsidy exists on a loan, you cannot use the PV (Tax Shield) method to compute the NPV of the loan. This is true because even with an interest rate subsidy, the appropriate rate by which to discount the after-tax interest payments is the market rate of interest. The PV (Tax Shield) method presumes the interest rate and the discount rate are the same.17.3 The calculation of the APV allows us to judge the attractiveness of the new project. Thefirst step is to calculate the all-equity (base-case) NPV. The unlevered cash flows are given, but we must infer the required return on assets from:0.10)0.4)(r 0.25(1r 0.18or),r )(r T (1SBr r 00B 0C 0S --+=--+= This relation implies that r 0 is approximately equal to 17.0%. Using the asset cash flows, the all-equity NPV is:1.37(1.170)10(1.170)8(1.170)515equity)-NPV(all 32=+++-=The additional value provided by the debt issue can be computed as:0.41(1.1).4(.1)2(1.1).4(.1)4(1.1).4(.1)6=)r (1Br T )r (1B r T )r (1B r T =PVTS =issue)NPV(debt 323B 2BC 2B 1B C B 0B C =+++++++The APV of the expansion is therefore 1.37 + 0.41 = 1.78. Since this is positive, MEO should go through with the capacity increase. 17.4million1.99$8974(.25)x3.8694x.79726(.75)x7.4690110(.75)x1.20(20/5).25A )12.1/(.25)A 6(1.25)A 10(120NPV Case Base 50.092200.1220.12-=++--=+-+---=million$4.232)10](27457.0)0607.8)(05.0)(75.0(1[10/(1.09).25)(.05)A (11010loan government subsidized of NPV 15150.09=--=---= Total NPV of the project = 4.232 - 1.99 = $2.242 million 17.5Annual cash flow from each store:Sales1,000,000 -Cost of goods sold-400,000 -General administrative costs -300,000-Interest-900,000 (30%) (9.5%)Income before tax 274,350-Tax-274,350 (40%) Net income 164,610 (annual cash flow)r r BS(1T )(r r )S 0C 0B =+--=+--=15%30%(140%)(15%95%)1599%..V equity value of each store =164,610 / 15.99% = $1,029,455.91 V each store = $1,029,455.91 + $270,000 = $1,299,455.91 V milano pizza club =3 V each store = $3,898,367.7317.6 a.You must apply the CAPM to determine the cost of equity for Wild Widgets. Toapply the CAPM to equity, you need the equity beta.βS = β0 [1 + (1-T C )(B/S)] where, βS = Equity betaβ0 = Overall firm betaTherefore, βS = .9 [ 1 + (0.66) (0.5)] = 1.197 Applying CAPM you getr S = 0.08 + 1.197 (0.16 - 0.08) = 0.17576 = 17.576% b. r B = $1070 / $972.72 -1 = 10%Therefore, the after-tax cost of debt is 6.6% (=10% x 0.66)c. To compute the WACC you need the debt-to-value and equity-to-value ratios. Since the debt-to-equity ratio is 1/2 (=D/E) and the value of the firm is the sum of the debt and equity (=D+E), the debt-to-value ratio D/(D+E) is 1 / (1+2) = 1/3. Theequity-to-value ratio is 2/3.WACC = (1/3)(6.6%) + (2/3)(17.576%) = 13.917%17.7 This firm has a capital structure which has three parts. As a capital structure becomes morecomplex, the WACC simply adds additional terms. a. Book value:WACC = ($5/$20)(0.08)(1-0.34) + ($5/$20)(0.10)(1-0.34) + ($10/$20)(0.15)= 0.1047Market value:WACC = ($5/$20)(0.08)(1-0.34) + ($2/$20)(0.10)(1-0.34) + ($13/$20)(0.15)= 0.1173Target value: The firm wants the market values of long and short term debt to be equal. Let x be the amount of long-term debt. Then total debt equals 2x. Since the firm also wants its debt-equity ratio to be 100% (or 1), the amount of equity must also be 2x. The value of the firm will be the sum of these terms which is 4x. Thus, the long-term-debt-value ratio is x/4x = 1/4. The short-term-debt-value ratio is the same, and the equity-value ratio is 1/2 (=2x / 4x). These weights should be used to compute the target WACC.WACC = (1/4)(0.08)(1-0.34) + (1/4)(0.10)(1-0.34) + (1/2)(0.15) = 0.1047b. The differences in the WACCs are due to the weights. The WACC using marketweights is the firm’s current WACC. The WACC computed using the target weights is the WACC used for project evaluation. It should be used when the project is financed in such a way that the debt-to-equity ratio of the firm isunchanged by the project. Since we assume firms fund projects at their company’s WACC, target weights are the correct weights to use in the WACC.17.8 The capital budgeting decision requires the calculation of the NPV of the equipment. TheNPV calculation requires the WACC. Cost of Equity: βS = 0.031/0.162 = 1.21r S = 7% + 1.21 (8.5%) = 17.293%After-tax cost of debt: 11% (1-0.34) = 7.26% Value of the firm: V = B + S= $24,000,000 + ($15)(4,000,000) = $84,000,000WACC = ($24,000,000 / $84,000,000) (7.26%) + ($60,000,000 / $84,000,000) (17.293%) = 14.426%The new machinery provides earnings that are an annuity for five years. The net present value of the additional equipment ision $3.084mill 0.14426(1.14426)11$9$27.5NPV 5=⎥⎥⎥⎥⎦⎤⎢⎢⎢⎢⎣⎡-+-=Yes, Baber should purchase the additional equipment.17.9 a. NEC’s debt -equity ratio is 2. That means that for every dollar of equity the firm has,it has two dollars in debt. The debt-to-value ratio of the firm is B / (B + S), so it is equal to 2/(2+1) = 2/3. The equity-to-value ratio is 1/3. Thus, the WACC is WACC = (2/3)(0.10)(1-0.34) + (1/3)(0.20) = 0.1107 Thus,NPV = -$20,000,000 + $8,000,000 / 0.1107 = $52,267,389.34 Yes, NEC should accept the project.b. Mr. Edison’s conclusion is incorrect. Even though the issuing costs of debt are farlower than those of equity, the firm must try to maintain its optimal capital structure. Recall, if a firm’s objective is to maximize shareholder wealth, it should maintain its optimal capital structure. Thus, anytime all-debt financing is used, the firm will have to issue more equity in the future to bring the capital structure back to the optimal.17.10 Baber’s WACC does not change if the firm chooses to fund the project entirely with debt.Thus, the WACC for Baber is still 14.426%. The use of target weights is based upon the assumption that the current capital structure is optimal. Indeed, if the fir m’s objective is to maximize shareholder wealth, it should always use its target weights in the computation of WACC. All debt funding for this project simply implies that the firm will have to use more equity in the future to bring the capital structure back to optimal.17.11 The all-equity value of the firm is given by:V U = 30 (1-0.34) / 0.18 = $110 millionThe share price before the recap is therefore $110 / share. Because there are no personal taxes or costs of financial distress, the value of the leverage per se is T C B = 0.34 (50) = $17 million. The value of the firm after the recap is therefore 110 + 17 = $127 million, which implies a share price of $127. At this price, the $50 million proceeds from the debt issue enables the firm to repurchase 50,000,000 / 127 = 393,700 shares. Thus, about 606,300 shares will remain outstanding. Earning per share will be:EPS = [30 million - 0.10 (50 million)] (1-0.34) / 606,300 =$27.21 / shareThe required return on equity will be:%43.21%)10%18%)(341(77/50%18)r )(r T (1SB r r B 0C 0LS =--+=--+= These values together verify the stock price by the FTE approach, since 27.21 / 0.2143 = $127.17.12 a. The unlevered free cash flows for the Kinedyne division can be calculated asSales $19,740 Variable costs 11,844 Depreciation 1,800 Taxable income $6,096 Taxes 2,438 After-tax income $3,658 Depreciation 1,800 Investment 1,800 UCF $3,658In all-equity form, the division is therefore worth 3,658 / 0.16 = $22.86 MM.b. If the division were leveraged as the parent, its weighted average cost of capitalwould be:()1344.0)]4.0(4.01[16.0V BT 1r r C 0WACC =-=-⨯= Using this rate to discount the unlevered free cash flows, the levered division value would be 3,658 / 1.344 = $27.21 MM.c. At this capital structure, the shareholders would require the return:%4.18%)10%16%)(401)(6/4(%16)r )(r T (1SBr r B 0C 0S =--+=--+=d. We need to show that the cash flow to the shareholders, discounted at the 18.4%required return, implies the value of the equity outstanding, which is .60 x V L = 0.60 ($27.21 MM) = $16.33 MM. To see this, note that the shareholders have a claim on the unlevered cash flow less the after-tax interest payment. This amount is(1T )r B C B -= .6 (.1) 10.89 MM = 0.65 MM, where the debt level is 40% of V L above. Deducting this after-tax interest payment from the unlevered cash flow implies a flow to equity (FTE) of (3.66 - 0.65) = 3.01 MM, which, when divided by the equity return of 18.4%, yields the value for shares outstanding of $16.33 MM.17.13 APV:V U = UCF / r 0 = $151.52(1– 34%)/ 0.2 = $500.016 APV = V U + T C B = $500 + (34%) ($500) = $670WACC:r S = r 0 + B/S (1– T C )(r 0 – r B ) , where S = V L – B = $670 – $500 = $170 = 0.2 + 500/170 (0.66)(0.2-0.1)=0.3941 = 39.41%r wacc = B S S +r S + BS +Br B (1– T C )=170/670 (39.41%) + 500/670 (10%)(1 – 34%) =14.92%V L = WACC r UCF = %92.14%)341(52.151- = $670FTE:LCF = (EBIT – r B B)(1 – T C )= ($151.52 – $50)(1– 34%) = $67.0032 V L = PV = ($67.0032 / 39.41%) – (– $500) =$170 + $500 = $67017.14 For the benchmark:r S = r f + β (R M – r f ) = 9% + 1.5 ( 17% – 9%) = 21% r wacc benchmark = r wacc project21% (1/1.3) + 10% (0.3/1/3) (1– 40%) = r S project (1/1.35) + 10% (0.35/1.35) (1– 40%) r S project = 21.58%16.968,288$90.615,11626.352,1726t 21.58%)(15%)55,000(1%)58.211(%)51(000,55...%)58.211(%)51(000,55%58.211000,55project the of PV t 4542=+=∑∞=+++++++++++=As PV of the project is less than the initial investment of $325,000, Schwartz & Brothers Inc. should give up the project.17.15 Flotation Cost = 4,250,000 / (1– 1.25%) – 4,250,000 = $53,797NPV of the loan = (Proceeds net of flotation cost) – (After tax present value of interest and principal payment) +(flotation costs tax shield).39$1,045,472 6.30622,1520.4072]4,303,7976.3062[232,4054,250,000A 10)53,797(40%](1.094)/4,303,79740%)A (9%)(1[4,303,7974,250,000=109.4%10109.4%=⨯+⨯+⨯-=++--17.16 a. βn = [1+(1-35%) x 1,000,000 / 1,500,000] x 1.2 = 1.72βs = [1+(1-35%) x 1,500,000 / 1,000,000] x 1.2 = 2.37b.R sn = r f + βn (R M– r f) = 4.25% + 1.72(12.75% – 4.25%) = 18.87%R ss = r f + βn (R M– r f) = 4.25% + 2.37 (12.75% – 4.25%) = 24.40%c. Although the two firms have the same risk level in case of all equity financing, thelevered β for South Pole Fishing Equipment Corp. is higher as a result of its higherleverage. Consequently, the required rate of return on the levered equity is higherfor South Pole Fishing Equipment too.Answers to End-of-Chapter Problems B-173。

公司理财笔记

公司理财读书笔记目录Chapter1. Foundations (2)1.1 foundation of firm (2)1.2 foundation of corporate finance (2)Chapter2. The Objective (4)Investment Decision (8)Chapter3. The Basics of risk (8)Chapter4. Risk measurement and Hurdle Rates (11)4.1 CAPM (11)4.1.1. Risk free Rate (12)4.1.2 risk premium (13)4.1.3 Beta (15)4.1.4 Estimating the cost of equity (19)4.2 APM (20)4.3 From Cost of Equity to Cost of Capital (20)4.3.1 Borrowing Risk Measurement (20)4.3.2 Computing W ACC (21)4.3.3 Choosing the Right Hurdle Rate (22)Chapter5. Measuring Returns on Investments (23)Chapter6. Project interactions, side costs and benefits (29)Financing Decision (33)Chapter7. An Overview of the Financing Decisions (33)Chapter8. Capital Structure: Model and Applications (40)8.1 Operating income Approach (40)8.2 Cost of capital Approach (40)8.3 APV Approach (42)8.4 Comparative Analysis Approach (43)Chapter9. Adjusting to optimal structure (45)Dividend Decision (51)Chapter10. The Determinants of Dividend Policy (51)Chapter11. A Framework for Analyzing Dividend Policy (57)11.1 Choices of returning cash to stockholders (57)1.2 Dividend policy analysis (58)Chapter1. Foundations本章介绍了公司理财的三个基本原则,即the investment principle、the financing principle and the dividend principle,这三个原则围绕着最大化企业价值的目标。

公司理财((美国)斯蒂芬·A·罗斯 StephenA.Ross (美国)布拉德福德·D·乔丹 BradfordD.Jordan))第八版答案

1.在所有权形式的公司中,股东是公司的所有者。

股东选举公司的董事会,董事会任命该公司的管理层。

企业的所有权和控制权分离的组织形式是导致的代理关系存在的主要原因。

管理者可能追求自身或别人的利益最大化,而不是股东的利益最大化。

在这种环境下,他们可能因为目标不一致而存在代理问题。

2.非营利公司经常追求社会或政治任务等各种目标。

非营利公司财务管理的目标是获取并有效使用资金以最大限度地实现组织的社会使命。

3.这句话是不正确的。

管理者实施财务管理的目标就是最大化现有股票的每股价值,当前的股票价值反映了短期和长期的风险、时间以及未来现金流量。

4.有两种结论。

一种极端,在市场经济中所有的东西都被定价。

因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。

另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。

一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30美元万。

然而,该公司认为提高产品的安全性只会节省20美元万。

请问公司应该怎么做呢?”5.财务管理的目标都是相同的,但实现目标的最好方式可能是不同的,因为不同的国家有不同的社会、政治环境和经济制度。

6.管理层的目标是最大化股东现有股票的每股价值。

如果管理层认为能提高公司利润,使股价超过35美元,那么他们应该展开对恶意收购的斗争。

如果管理层认为该投标人或其它未知的投标人将支付超过每股35美元的价格收购公司,那么他们也应该展开斗争。

然而,如果管理层不能增加企业的价值,并且没有其他更高的投标价格,那么管理层不是在为股东的最大化权益行事。

现在的管理层经常在公司面临这些恶意收购的情况时迷失自己的方向。

7.其他国家的代理问题并不严重,主要取决于其他国家的私人投资者占比重较小。

较少的私人投资者能减少不同的企业目标。

高比重的机构所有权导致高学历的股东和管理层讨论决策风险项目。

此外,机构投资者比私人投资者可以根据自己的资源和经验更好地对管理层实施有效的监督机制。

(公司理财)英文版罗斯公司理财习题答案C