商业银行 Commercial Banks

商业银行CommercialBanks商业银行概述商

2024/10/13

31

表外业务与中间业务比较

一、联系

两者都是独立于资产负债业务之外、以收取手续费为目 的的业务,而且都是以接受委托的方式开展业务活动。

二、区别 1、中间人的身份不同 中间业务:银行以第三者身份接受委托,扮演中间人的角色

贴现利息=票面金额×贴现率×(未到期天数/360)

贴现金额=票面金额-贴现利息

(四)证券投资业务Security Investments

证券投资:商业银行在金融市场上运用其资金购买有价证 券的活动。

谋取收益(利息收入和证券增值的收益)

目 资产多样化,以分散风险 的

提高资产的流动性(商业银行的第二准备)

(1)依靠吸收存款作为其发放贷款的主要来源

(2)创造存款货币(信用创造)

资产业务

(3)经营业务范围极其广泛

2024/10/13

2

2、现代商业银行的产生主要通过两条途径 旧的高利贷性质的银行 根据股份制原则,以股份公司的形式创建

1694年,第一个股份制银行——英格兰银行(Bank of England)成立,标志着现代商业银行的产生。

遏制金融资本垄断 优 点 易于管理费用低

银行与地方关系密切,为发展地方经济服务

与经济的外向发展存在矛盾,削弱了竞争力 缺 点 经营成本较高

业务相对集中,风险较大

2024/10/13

9

2、分支行制 分支银行制又称总分行制,法律允许在总行之下,普遍设

立分支机构,分支银行的各项业务统一遵照总行的指示办理。

欧洲货币(Eurocurrency) :指存放在货币发行国境外 其他国家银行中的各国货币。(欧洲美元、欧洲日元、欧洲 英镑)

商业银行英语怎么说

商业银行英语怎么说商业银行是一个以营利为目的,以多种金融负债筹集资金,多种金融资产为经营对象,具有信用创造功能的金融机构。

主要业务范围包括吸收公众、企业及机构的存款、发放贷款、票据贴现及中间业务等。

那么你知道商业银行用英语怎么说吗?接下来跟着店铺来学习一下吧。

商业银行的英语说法1:bank of commerce商业银行的英语说法2:commercial bank商业银行的相关短语:南洋商业银行 Nanyang Commercial Bank北京市商业银行 Beijing City Commercial Bank国有独资商业银行 wholly state-owned commercial banks商业银行法 Law of Commercial Banks商业银行实务 Practice of Business Bank商业银行管理 Commercial Banking Management商业银行的英语例句:1. Mexico and the Philippines have both concluded agreements with their commercial bank creditors.墨西哥和菲律宾均已与商业银行债权人达成了协议。

2. The merchant banks raise capital for industry. They don't actually put it up themselves.商业银行为产业界募集资金。

事实上他们自己并不出资。

3. The merchant bank is being weighed down by a £1.3 billion book of bad debts.这家商业银行因13亿英镑的呆账而忧心忡忡。

4. The main function of the merchant banks is to raise capital for industry.商业银行的主要职能是为产业融资。

新编金融英语教程ChapterCommercialBanks

Supervision and Regulations of Commercial Banks

Trust business

Manage assets and handle affairs on behalf of clients, and charge a certain handling fee.

Agency business

Handling various financial services on behalf of clients, such as agency collection and payment, agency insurance, etc.

Credit risk: refers to the possibility that the borrower or debtor, due to various reasons, fails to fulfill their obligations as stipulated in the contract, resulting in losses for creditors or investors.

Operational risk refers to the risk caused by internal processes, personnel, systems, and other issues, such as internal fraud, errors, process defects, etc.

Credit intermediary: absorbs deposits, issues loans, and plays a role in transferring risks and financing funds.

financial intermediaries种类

financial intermediaries种类Financial intermediaries refer to institutions or individuals that act as a middleman between the lenders and borrowers in the financial market. These intermediaries play a crucial role in the economy by facilitating the flow of funds to different sectors. There are several types of financial intermediaries, each serving a specific purpose in the financial system. In this article, we will explore and discuss the main categories of financial intermediaries.1. Commercial Banks:One of the most well-known types of financial intermediaries is commercial banks. Commercial banks are authorized institutions that accept deposits from the public and provide loans to individuals and businesses. They offer various services such as current and savings accounts, lending facilities, and trade finance. Commercial banks play a pivotal role in channeling funds from surplus economic units to deficit economic units.2. Investment Banks:Investment banks are financial institutions that specialize in providing services related to capital market activities such as underwriting securities, assisting with mergers and acquisitions,and facilitating the issuance of new securities. Unlike commercial banks, investment banks do not accept deposits from individuals. Instead, they operate mainly through trading activities and offering advisory services to their clients.3. Mutual Funds:Mutual funds are investment vehicles that pool money from multiple investors to invest in a diversified portfolio of securities. They are managed by professional fund managers who make investment decisions on behalf of the investors. Mutual funds offer individuals with limited capital the opportunity to access a wide range of investment options and benefit from professional management. They are an effective tool for diversification and risk management.4. Insurance Companies:Insurance companies are financial intermediaries that provide coverage against potential risks and uncertainties. They collect premiums from policyholders and use the funds to compensate them in case of a covered event. Insurance companies help individuals and businesses manage risks by spreading them across a large pool of policyholders. They offer various types of insurance,such as life, health, property, and casualty insurance.5. Pension Funds:Pension funds are intermediaries that collect contributions from individuals and employers to provide a steady income after retirement. Pension funds pool the contributions and invest them in various financial instruments such as stocks, bonds, and real estate. The funds are managed professionally to ensure growth and sustainability. Pension funds play a crucial role in ensuring individuals have a secure financial future after they retire.6. Finance Companies:Finance companies, also known as consumer finance companies or non-bank financial institutions, provide loans and credit facilities to individuals and businesses. They specialize in lending to high-risk borrowers who may not qualify for loans from traditional banks. Finance companies fund their lending activities through borrowing from banks and other financial institutions.7. Stockbrokers:Stockbrokers are intermediaries that facilitate the buying and selling of securities on behalf of their clients. They are licensedprofessionals who provide investment advice, execute trades, and manage portfolios for individual and institutional investors. Stockbrokers play a crucial role in the functioning of stock exchanges and ensuring efficient trading in the capital market.8. Venture Capital and Private Equity Firms:Venture capital (VC) and private equity (PE) firms are intermediaries that provide funding to startups and small businesses in exchange for an equity stake. They specialize in providing capital tohigh-growth potential companies that may have difficulty accessing traditional sources of financing. VC and PE firms contribute to the development and growth of innovative businesses and often provide strategic guidance and expertise in addition to financial support.In conclusion, financial intermediaries are essential players in the economy, connecting lenders and borrowers, and facilitating the flow of funds. The various types of financial intermediaries, such as commercial banks, investment banks, mutual funds, insurance companies, pension funds, finance companies, stockbrokers, and venture capital/private equity firms, each serve a specific functionin the financial system. By understanding these intermediaries and their roles, individuals and businesses can make informed decisions regarding their financial needs and goals.。

unit 4 commercial banks

Unit 4Commercial Banks in the Financial System of U.S.AThe importance of the nation’s banking system to the processes of a modern industrial economy can hardly be exaggerated. The banking system is an integral part of the monetary system, accumulating and lending idle funds, facilitating the transfer of money, and providing for its safekeeping. The banking system also provides part of the long-term financing required by industry, by commerce, and by agriculture. It plays an important part, too, in financing the construction of the nation’s millions of homes; and it is an important source for personal loans.Although the various depository institutions of the nation, namely commercial banks, savings and loan associations, credit unions, and mutual savings banks, display a trend toward providing similar services, there remains enough of the unique character of each to distinguish easily among them. Further, it is through the commercial banking system that the principal influence of fiscal and monetary policy is carried out. It is for this reason that special emphasis is placed on commercial banking in any discussion of a nation’s financial system.In the United States, a commercial bank can be chartered either by the state (state-chartered banks) or by the federal government (national banks). Of all the commercial banks, more than half were state-chartered. All national banks must be members of the Federal Reserve System and must be insured by the Bank Insurance Fund (BIF), which is administered by the Federal Deposit Insurance Corporation. BIF was created early in 1989 by the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA).State-chartered banks may elect to join the Federal Reserve System. Their deposits must be insured by BIF. In spite of the large number of banks that elect not to be members of the Federal Reserve System, banks that are members hold more than 70% of all deposits in the United States. Moreover, with the passage of the Depository Institutions Deregulation and Monetary Control Act of 1980 (DIDMCA), the reserve requirements that apply to members of the Federal Reserve System apply also to state-chartered banks.Bank ServicesCommercial banks provide numerous services in the U.S. financial system. The services can be broadly classified as follows: (1) individual banking,( 2)institutional banking, and (3) global banking. Of course, different banks are more active in certain of these activities than others. For example, money center banks (defined later) are more active in global banking.Individual banking encompasses consumer lending, residential mortgage lending, consumer installment loans, credit card financing, automobile and boat financing, brokerage services, student loans, and individual-oriented financial investment services such as personal trust andinvestment services. Interest and fee income are generated from mortgage lending and credit card financing. Mortgage lending is often referred to as "mortgage banking" Fee income is generated from brokerage services and financial investment services.Loans to nonfinancial corporations, financial corporations (such as life insurance companies), and government entities (state and local governments in the U.S. and foreign governments) fall into the category of institutional banking. Also included in this category are commercial real estate financing, leasing activities, and factoring. In the case of leasing, a bank may be involved in leasing equipment either as lessors, as lenders to lessors, or as purchasers of leases. Loans and leasing generate interest income, and other services that banks offer institutional customers generate fee income. These services include management of the assets of private and public pension funds, fiduciary and custodial services, and cash management services such as account maintenance, check clearing, and electronic transfers.It is in the area of global banking that banks have begun to compete head-to-head with another financial institution--investment banking firms. Global banking covers a broad range of activities involving corporate financing and capital market and foreign exchange products and services. Most global banking activities generate fee income rather than interest income.Corporate financing involves two components. First is the procuring of funds for a bank's customers. This can go beyond traditional bank loans to involve the underwriting of securities, though the Glass-Steagall Act limits bank activities in this area. In assisting its customers in obtaining funds, banks also provide bankers' acceptances, letters of credit, and other types of guarantees for their customers. That is, if a customer has borrowed funds backed by a letter of credit or other guarantee, its lenders can look to the customer's bank to fulfill the obligation. The second area of corporate financing involves advice on such matters as strategies for obtaining funds, corporate restructuring, divestitures, and acquisitions.Capital market and foreign exchange products and services involve transactions where the bank may act as a dealer or broker in a service. Some banks, for example, are dealers in U.S. government or other securities. Customers who wish to transact in these securities can do so through the government desk of the bank. Similarly, some banks maintain a foreign-exchange operation, where foreign currency is bought and sold. Bank customers in need of foreign exchange can use the services of the bank.In their role as dealers, banks can generate income in three ways: (1) the bid-ask spread, (2) capital gains on the securities or foreign currency used in transactions, and (3) in the case of securities, the spread between interest income earned by holding the security and the cost of funding the purchase of that security.The financial products that banks have developed to manage risk also yield income. These products include interest rate swaps, interest rate agreements, currency swaps, forward contracts, and interest rate options. Banks can generate either commission income (that is, brokerage fees) or spread income from selling such products.Bank FundingIn describing the nature of the banking business, we have focused so far on how a bank can generate income. We will have a look at how a bank can raise funds. There are three sources of funds for banks: (1) deposits, (2) nondeposit borrowing, and (3) common stock and retained earnings. Banks are highly leveraged financial institutions, which means that most of their fundscome from borrowing--the first two sources we refer to. Included in nondeposit borrowing are borrowing from the Federal Reserves through the discount window facility, borrowing reserves in the federal funds market, and borrowing by the issuance of instruments in the money and bond markets.Deposits--There are several types of deposit accounts. Demand deposits (checking accounts) pay no interest and can be withdrawn upon demand. Savings deposits pay interest (typically below market interest rates), do not have a specific maturity, and usually can be withdrawn upon demand.Time deposits, also called certificates of deposit, have a fixed maturity date and pay either a fixed or floating interest rate. Some certificates of deposit can be sold in the open market prior to their maturity if the depositor needs funds. Other certificates of deposits cannot be sold. If a depositor elects to withdraw the funds from the bank prior to the maturity date, a withdrawal penalty is imposed. A money-market demand account is one that pays interest based on short-term interest rates. The market for short-term debt obligations is called the money market, which is how these deposits get their name.Borrowing at the Fed discount window--The Federal Reserve Bank is the banker’s bank --or, to put it another way, the bank of last resort. Banks temporarily short of funds can borrow from the Federal at its discount window. Collateral is necessary to borrow, but not just any collateral will do. The Fed establishes (and periodically changes) the type of collateral that is eligible. Currently it includes:( l) Treasury securities, federal agency securities, and municipal securities, all with a maturity of less than six months, and ( 2) commercial and industrial loans with 90 days or less to maturity.The interest rate that the Fed charges to borrow funds at the discount window is called the discount rate. The Fed changes this rate periodically in order to implement monetary policy. Bank borrowing at the Fed to meet required reserves is quite limited in amount, despite the fact that the discount rate generally is set below the cost of other sources of short-term funding available to a bank. This is because the Fed views borrowing at the discount window as a privilege to be used to meet short-term liquidity needs, and not a device to increase earnings.Continual borrowing for long periods and in large amounts is thereby viewed as a sign of a bank's financial weakness or as exploitation of the interest differential for profit. If a bank appears to be going to the Fed frequently to borrow, relative to its previous borrowing pattern, the Fed will make an “informational” call to ask for an explanation for the borrowing. If there is no subse quent improvement in the bank's borrowing pattern, the Fed then makes an “administrative counseling" call in which it tells the bank that it must stop its borrowing practice.Other nondeposit borrowing--Most deposits have short maturities. Bank borrowing in the federal funds market and at the discount window of the Fed is short-term. Other nondeposit borrowing can be short-term in the form of issuing obligations in the money market, or intermediate to long-term in the form of issuing securities in the bond market. An example of the former is the repurchase agreement (of "repo") market, example of intermediate—or long-term borrowing is floating-rate notes and bonds.Bank assetsThe principal assets of a commercial bank are cash, securities, and loans.Cash. Cash includes funds in the bank’s vaults, in a federal reserve bank, and in correspondentbanks. A bank must keep a certain minimum of vault cash to meet the day-to-day currency requirements of the bank’s customers. The amount of such cash requi rements may be small relative to the total of a bank’s resources for the simple reason that the typical day’s operation will result in approximately the same amount of cash deposits as cash withdrawals. A margin of safety, however, is required to take care of those periods when for one reason or another withdrawals exceed deposits.The appropriate amount of cash that a bank should carry depends largely upon the character of its banking operations and on the distance of the bank from its depository for legal reserves. For example, a bank that has a few very large accounts might be expected to have a larger volume of unanticipated withdrawals than a bank that has only small individual accounts. An erratic volume of day-to-day withdrawals requires, of course, a larger cash reserve. A bank that is located a great distance from its depository for legal reserves also must maintain larger cash reserves than a bank that can in a matter of minutes or hours draw on such reserves.The second cash item, designated “in Federal Reserve Bank,” is considerably greater than vault cash. Members of the Federal Reserve System are required to keep a percentage of their deposits as minimum reserves either with the federal reserve banks of their districts or in the form of vault cash. As withdrawals are made and total deposit balances decrease, the amount of the required reserves also decreases. These reserves that have been freed may be used by the bank to help meet withdrawal demands.Cash “in correspondent banks” refers to the com mon practice of keeping substantial deposits with other banks, particularly banks in large cities. Such correspondent relations with other banks facilitate the clearing of drafts and other credit instruments, and provide an immediate access to information regarding the money markets of the large cities.Securities. Securities comprise the second major group of bank assets. These securities held by the bank include those of the United States government, those of state governments, and of municipalities. Also included are other bonds and capital stock of the Federal Reserve Bank. The bonds owned by this bank are held as investments. The capital stock of the Federal Reserve Bank owned by the bank is a requirement for all member banks of the Federal Reserve System. Loans. The third group of asset items includes several classifications of loans: first, those loans that are payable on demand and which are secured; second, those secured loans that have definite maturities; third, and by far the most important, unsecured loans and discounts with definite maturities; and finally, real estate loans on first mortgage.Other Bank Assets. The remaining assets are of less importance than the foregoing groups. They include interest accrued on bonds and notes earned but not yet received, bank buildings and furniture, and prepaid expenses such as insurance premiums paid in advance.Capital requirements for commercial banksThe capital structure of banks, like that of all corporations, consists of equity and debt (i.e., borrowed funds). Commercial banks, like some other depository institutions and like investment banks, are highly leveraged institutions. That is, the ratio of equity capital to total assets is low, typically less than 8% in the case of banks. This gives rise to regulatory concern about potential insolvency resulting from the low level of capital provided by the owners. An additional concern is that the amount of equity capital is even less adequate because of potential liabilities that do not appear on the bank's balance sheet. These so-called “off-balance sheet” obligations includecommitments such as letters of credit and obligations on customized interest rate agreements (such as swaps, caps, and floors).Prior to 1989, capital requirements for a bank were based solely on its total assets. No consideration was given to the types of assets. In January 1989, the Federal Reserve adopted guidelines for capital adequacy based on the credit risk of the assets held by the bank These guidelines are referred to as risk-based capital requirements The guidelines are based on a framework adopted in July 1988 by the Basel Committee on Banking Regulations and Supervisory Practices, which consists of the central banks and supervisory authorities of the G-10 countries.Termscommercial bank商业银行national banks国家银行state-chartered banks洲级银行idle funds闲散资金individual banking个人银行业务institutional banking机构银行业务global banking国际(全球)银行业务deposit存款equity capital权益资本consumer spending消费支出residential mortgage lending住房抵押贷款consumer installment loans分期消费贷款student loans 助学贷款personal trust个人信托leasing activities租赁业务factoring保理业务pension funds养老金check clearing支票清算electronic transfer电汇corporate restructuring公司重组divestiture撤资secured loans 抵押/担保贷款discount贴现floating interest rate浮动利率bid-ask spread买卖差价ExercisesI.Answer the following questions.1. What is individual banking? Give an example in your daily life.2. What is the major source of commercial banks’ funds?3. Why are commercial banks called leveraged institution?4. What is the function of the Federal Deposit Insurance Corporation?5. What are the major forms of banks’ pro fits?6. What is included in the global banking?7. How do the governments try to control the risks of banks?8. What is included in banks’ assets?9. Why are commercial banks relatively safer than other types of financial institutions?II. Translate the following passages.Banks are susceptible to many forms of risk which have triggered occasional systemic crises. These include liquidity risk (where many depositors may request withdrawals beyond available funds), credit risk (the chance that those who owe money to the bank will not repay it), and interest rate risk (the possibility that the bank will become unprofitable, if rising interest rates force it to pay relatively more on its deposits than it receives on its loans).Banking crises have developed many times throughout history, when one or more risks have materialized for a banking sector as a whole. Prominent examples include the bank run that occurred during the Great Depression, the U.S. Savings and Loan crisis in the 1980s and early 1990s, the Japanese banking crisis during the 1990s, and the subprime mortgage crisis in the 2000s.。

bank的用法总结精选集锦

bank的用法总结精选集锦bank是银行的意思,下面我把bank的学问点做了一个总结,此时此刻共享给大家。

释义bankn. 银行;岸;浅滩;储库vt. 将…存入银行;倾斜转弯vi. 积累;倾斜转弯n. (Bank)人名;(英、德、俄)班克;(法、匈)邦克[ 复数banks 过去式banked 过去分词banked 此时此刻分词banking 第三人称单数banks ]词组短语central bank [经]中心银行commercial bank 商业银行bank of china 中国银行world bank n. 世界银行bank account 银行存款;银行往来帐户peoples bank of china 中国人民银行investment bank 投资银行development bank 开发银行construction bank 建立银行west bank 约旦河西岸bank credit 银行信贷;银行信用状bank loan 银行贷款agricultural bank 农业银行industrial and commercial bank 工商银行issuing bank 开证银行;发行钞票的银行river bank 河岸;河堤china construction bank 中国建立银行in bank 存入银行bank on 希望;依靠bank of america n. 美国银行词语辨析shore, bank, seaside, beach, coast这组词都有“岸”的意思,其区分是:shore 指紧靠大湖泊或海洋的陆地边缘或靠海的养息地。

bank 多指有必须坡度的河岸、湖岸或堤岸。

seaside 尤指疗养地、巡游地区的海边。

beach 指倾斜度小,被海、湖或河水冲刷而有沙或卵石积存的地方。

bank用法bank可以用作名词bank的根本意思是“银行”,引申可作储存东西的“库”。

金融英语quiz答案(展示版)

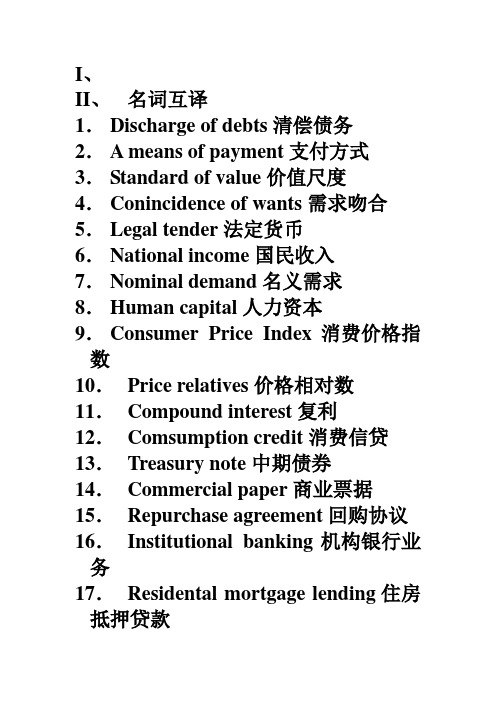

I、II、名词互译1.Discharge of debts清偿债务2.A means of payment支付方式3.Standard of value价值尺度4.Conincidence of wants需求吻合5.Legal tender法定货币6.National income国民收入7.Nominal demand名义需求8.Human capital人力资本9.Consumer Price Index消费价格指数10.Price relatives价格相对数11.Compound interest复利12.Comsumption credit消费信贷13.Treasury note中期债券14.Commercial paper商业票据15.Repurchase agreement回购协议16.Institutional banking机构银行业务17.Residental mortgage lending住房抵押贷款18.Consumer installment loan分期消费贷款19.Corporate restructuring公司重组20.Secured loan抵押贷款21.Open market operation公开市场操作22.Reserve requirement法定存款准备金率23.Target rate目标利率24.Floating interest rate浮动利率25.Bid-ask spread买卖差价1.支票清算check clearing2.撤资divestiture3.助学贷款student loan4.消费支出consumer spending5.商业银行commercial bank6.政策目标policy goal7.中央银行central bank8.不兑现纸币fiat money9.货币基数monetary base10.个人银行业务individual banking11.金融市场financial market12.直接融资direct financing13.长期信贷long-term credit14.银行承兑banker’s acceptance15.规模经济scale economy16.国民总产出national output17.实物资本physical capital18.工业产品指数Producer Price Index19.复利compound interest20.收入分配distribution of income21.交换媒介medium of exchange22.银行存款bank deposits23.延迟支付deferred payment24.专业化分工specialization25.物物交换barterIII、请简要回答下列问题(仅供参考) 1.what are the major functions of money? Give some examples to show the each function of money.Answer: Standard of value, medium ofexchange, store of value and standard of deferred payments.2.what are the effects of inflation and deflation on business?Answer: The effects of inflation: Profit illusion at initial stage and loss later and maybe recession or depression coming next.The effects of deflation: Less profit immediately.3.how will the change in money’s value redistribute people’s income and wealth?Answer: In the situation of inflation, creditors suffer, in the situation of deflation, debtors suffer.4.what are the attributes of credit instruments?Answer: Yield, liquidity and safety.5.what is the relationship between yield and safety of credit instruments? Answer: The higher yield means thelower the safety.6.what is included in banks’ assets? Answer: Cash; Securities: Loans7.why are commercial banks relatively safer than other types of financial institutions?Answer:8.what is individual banking? Give an example in your daily life?Answer:Individual banking encompasses consumer lending, residential mortgage lending, consumer installment loans, credit card financing and so on.9.what are the major functions of central banks?Answer:Issuing a common currency, clearing payments, regulating banks and acting as a “lender of last resort” for banks in financial trouble.10.what challenge is faced by centralbanks in the future?Answer:To balance three policy goals,to balance financial innovations and financial stability and so on .IV、翻译1.Deposit accounts, together with sav ings accounts, represent the simplest form of bank account. The customer deposits f unds and withdraws them as required. No chequebook is issued on this type of acco unt. 存款账户,和储蓄账户一起,是银行账户的基本形式,客户按规定存、取款。

高级商务英语

Key Vocabulary

The banking sector (银行业)in the United Kingdom is made up of a variety of institutions supervised by the country‘s central bank(中央银行). The Bank of England. This bank looks after the government’s finance and monetary policy (货币政策)and acts as banker(贷款人) to other banks. However, for the general public and many businesses(企业), banking services are provided by commercial banks(商业银行), or clearing banks, which have branches throughout the country.

4 Which of the items would you use if you needed to 1 check how much money you had in your bank account several weeks ago? 2 take money with you for a visit to a foreign country? 3 see how much you have to pay for the electricity you used last month? 4 send payment by post? 5 take money out of your account on a Sunday?

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

有利于银行开展全面的业务但加大银行的经营风险

《金融服务现代化法案》

2020/2/12

10

(四)商业银行的组织结构 1、单一银行制

银行业务由各自独立的商业银行经营,不设立任何分支机构

遏制金融资本垄断 优 点 易于管理费用低

银行与地方关系密切,为发展地方经济服务

保资不抵债 损失贷款:本息无法收回(呆帐/坏帐)

工商业贷款 4、贷款对象 农业贷款

消费贷款

2020/2/12

25

(三)贴现业务Discount 1、贴现对象:银行持有的政府债券 2、贴现方式:转贴现、再贴现

(四)证券投资业务Security Investments

证券投资:商业银行在金融市场上运用其资金购买有价证

银行以中间人的身份为客户办理各类金融服务,

从中赚取手续费或佣金。

2020/2/12

28

1、结算业务 Settlement

(1)结算工具:本票、支票、汇票、信用证 (2)结算方式

同城结算:支票结算、转帐、票据交换所自动转帐系统

异地结算

2020/2/12

汇款结算 Remittance 托收业务 Collection 信用证业务 Letter of Credit 电子资金划拨系统(环球银行金融电讯协会

表外业务:可能成为交易的直接当事人(银行保函)

2020/2/12

34

2、业务风险不同 中间业务:其较少动用或不动用自己的资金。风险较小

表外业务:可能以某种形式垫付资金,从而形成银行与客户之 间的债权债务关系,其风险度较大。( 贷款承诺) 2019年英国巴林银行破产案

3、发展的时间长短不同 表外业务是近20多年才发展起来的,与国际业务的发展、

经营性租赁: 出租人将自己的设备反复出租的租赁业务。

6、信息咨询业务

2020/2/12

31

(二)表外业务(Off-Balance Sheet Activities,OBS)

商业银行按照通行的会计准则,不列入资产负债表内,不影 响其资产负债总额,但能影响银行当期损益的经营活动。

1、担保类业务:商业银行为客户债务清偿能力提供担保,

1、商业银行:以经营存款、贷款、办理转帐结算为主

要业务,以盈利为主要经营目标的金融企业。 (1)依靠吸收存款作为其发放贷款的主要来源 资产业务

(2)创造存款货币(派生存款)

(3)经营业务范围广泛

2020/2/12

2

2、现代商业银行的产生主要通过两条途径

旧的高利贷性质的银行 根据股份制原则,以股份公司的形式创建

承担客户违约风险的业务。

履约保函

银行保函(bank’s Letter of Guarantee,L/G) 投标保函 贷款保函

备用信用证(Standby Letter of Credit)

2020/2/12

32

2、承诺类业务是指商业银行在未来某一日期按照事先约 定的条件向客户提供约定的信用业务,包括贷款承诺等。

闲散 资金 存款 供 给者 (负债业务)

银行

贷款 资金需求者

资产业务

2、支付中介 通过客户 活期存款帐户 资金的转移为客户办理货币结算、

收付、兑换和存款转移等业务活动 节约流通费用/降低银行的筹资成本,扩大银行的资金来源

2020/2/12

6

3、信用创造 信用创造:商业银行通过吸收活期存款、发放贷款,从 而

市场

交易者B 美

2020/2/12

交易地A 日 交易货币 美元

交易者 c 英

18

4、回购协议交易 商业银行在通过出售证券等金融资产取得资金的同时,

约定在一定期限后按约定价格赎回所卖证券,以获取即时可 用资金的交易方式。

5、发行金融债券

资本性金融债券:弥补银行资本不足

一般性金融债券:筹集长期贷款、投资等业务所需资金

2020/2/12

19

二、商业银行的资产业务 商业银行的资产业务:资金运用业务,是指商业银行将通

过负债业务所积聚的货币资金加以运用获取收益的业务。

现金资产

贷款业务

贴现业务

2020/2/12

证券投资业务

20

(一)现金资产 1、库存现金:应付存款户提取现金和日常开支所需 2、准备金存款 法定存款准备金:商业银行从其吸收的存款中按法定存款准

国际金融市场及现代通讯技术的发展紧密相关。

2020/2/12

35

第三节 商业银行的经营管理

(一)安全性 安全性:银行在运营过程中资产免遭损失的可靠程度。

市场风险 违约风险

安全性对贷款来说是按期收回,证券资产则是随时足值收回

2020/2/12

36

(二)流动性 流动性:商业银行能够随时应付 客户提现 和满足 客户借贷

用权分离

(3)中央银行实施货币政策的最重要的基础和途径

(4)高负债比例

2020/2/12

4

3、与其他金融机构的区别 吸收活期存款、创造和收缩存款货币

商业银行是以追求最大利润为目标,以金融资产和 金融负债为经营对象,向客户提供多功能、综合性 服务的金融企业。

2020/2/12

5

(二)商业银行的职能 1、信用中介(最基本)

行取得贷款。

2020/2/12

17

2、银行同业拆入

商业银行之间或与其他金融机构相互进行的资金融通

弥补商业银行在中央银行存款账户上的准备金不足

3、向国际金融市场借款

欧洲货币(Eurocurrency) :指存放在货币发行国境外 其他国家银行中的各国货币。(欧洲美元、欧洲日元、欧洲 英镑)

欧洲货币市场:在货币发行国境外存储和贷放该国货币的

3、金融衍生交易类业务是指商业银行为满足客户保值或 自身头寸管理等需要而进行的货币和利率的远期、掉期、期 权等衍生交易业务。

2020/2/12

33

(三)表外业务与中间业务比较

独立于资产负债业务之外、以收取手续费为目的的业务, 而且都是以接受委托的方式开展业务活动。

1、身份不同 中间业务:银行以第三者身份接受委托,扮演中间人的角色

增银行资本。

4、20未20/2分/12 配利润

16

(二)存款业务

活期存款(可签发支票) 定期存款:商业银行稳定的资金来源 储蓄存款:主要针对居民个人

(三)借款业务

1、向中央银行借款

缓解流动性不足

再贴现:把贴现买进的尚未到期的商业票据出售给 中央银行

再贷款:开出本票或借据,以信用方式,通过抵押直接从央

增加银行的资金来源、扩大社会货币供应量。

前提:支票流通和转账结算

原始存款、法定存款准备金率、现金漏损率

2020/2/12

7

例:法定存款准备金率10%,假定A存入100元 100元的存款会一分为二哦

法定存款准备金10元

可贷款金额90元

假定银行向B贷款90元,B把钱存入其银行账户 B存款账户增加90元

1694年,英格兰银行(Bank of England)的成立,标志 着现代商业银行的产生。

2020/2/12

3

二、商业银行的性质与职能

(一)商业银行的性质 1、具有一般企业的特征: 利润最大化目标、自负盈亏、自求发展

2、自身的特点

(1)经营对象:货币资本

(2)经营方式:货币资本有条件的暂时让渡,所有权与使

备金率提取 的,并存放在中央银行的资金。

超额准备金:商业银行在中央银行的存款中超过法定准备金

的存款。

2020/2/12

21

3、银行同业存款 商业银行存放在其他商业银行的资金。 方便清算业务

4、托收未达款:商业银行应收的清算款项

现金资产是非盈利资产(或低息),是商业银行的第一准 备,用来满足商业银行的流动性(支付)需要的。

委托人--- > 代理人(商业银行)

代理融通(Factoring ):由商业银行代顾客收取应收账

款202并0/2/向12 顾客提供资金融通的一种业务

30

4、银行卡业务

贷记卡:先消费后还款 信用卡

借记卡:先存款后使用

5、租赁业务 Leasing

商业银行

金融租赁(融资性租赁): 出租人出资购买承租人选定的设 备,按协议出租

第六章 商业银行 Commercial Banks

•了解商业银行的基本概念、性质与职能 •理解商业银行的类型和组织结构 •掌握商业银行的各项业务及其构成 •掌握商业银行经营管理的基本理论和基本原则

2020/2/12

docin/sundae_meng

1

第一节 商业银行概述 一、商业银行的概念

负债业务

与经济的外向发展存在矛盾,削弱了竞争力 缺 点 经营成本较高

业务相对集中,风险较大

2020/2/12

11

2、分支行制

分支银行制又称总分行制,法律允许在总行之下,普遍 设立分支机构,分支银行的各项业务统一遵照总行的指示办理。

总行制:总行除了领导和管理分支行处,本身也对外营业

总管理处制:总行只负责管理和控制分支行除,本身不对外营 业,在总行所在地另设分支行或营业部开展业务活动。

2020/2/12

12

3、银行持股公司制

由一个企业集团成立控股公司,再由该公司控制或者收 购若干银行的组织形式。

扩大银行资本总量,增强抵御风险和竞争的能力, 弥补单一制的不足。

4、连锁银行制

由个人或某一集体通过购买若干家独立银行的多数股票, 或以其他法律允许的方式取得对这些银行的控制权力的一种组 织形式。

2020/2/12

13

第二节 商业银行的业务

资产=负债+所有者权益

负债业务Liability Business