非居民企业所得税核定征收管理办法-中英文版

非居民企业所得税核定征收管理办法

非居民企业所得税核定征收管理办法在中国,非居民企业所得税是指依照税法规定,在中国境外没有住所、场所、管理机构,或者在中国境外有住所、场所、管理机构但与所取得的所得无实质性关联的企业,在境内取得的所得支付给中国税务机关征收的税款。

为了规范非居民企业所得税的核定征收管理行为,中国税务机关颁布了《非居民企业所得税核定征收管理办法》。

一、纳税义务的确认根据《非居民企业所得税核定征收管理办法》,境内扣除义务人应履行纳税义务。

境内扣除义务人是指支付所得给非居民企业的机构、团体、个人等。

非居民企业所得税必须在取得所得后15天内在缴税地办理纳税义务登记,并按月或按季进行纳税申报、税款缴纳。

二、所得计算和税款缴纳管理非居民企业所得税的计算方法是按照境内扣除义务人支付给非居民企业的所得额计算,并按照适用税率计算税款。

非居民企业所得包括利息、股息、特许权使用费、财产租赁费、财产转让所得等。

为了规范非居民企业所得税的计算和税款缴纳管理,税务机关要求境内扣除义务人在支付所得给非居民企业时,应当在扣除所得的总额后,按规定的税率计算并缴纳非居民企业所得税。

三、信息报告义务《非居民企业所得税核定征收管理办法》规定,境内扣除义务人在支付所得给非居民企业时,应当向税务机关报告相关信息。

这些信息包括非居民企业的基本情况、所得的性质、金额,以及纳税义务的履行情况等。

境内扣除义务人应当按照规定的格式填报和报送相关信息,并保证信息的真实、准确、完整。

同时,税务机关有权要求境内扣除义务人提供相关的书面材料、账务凭证等。

四、税务检查和纳税信用管理为确保非居民企业所得税的核定征收工作的有效进行,《非居民企业所得税核定征收管理办法》还明确了税务机关对境内扣除义务人的税务检查和纳税信用管理。

税务机关有权对境内扣除义务人进行税务检查,核实其纳税义务的履行情况。

同时,税务机关还对境内扣除义务人的纳税信用进行评价,并根据评价结果采取相应的奖惩措施。

信用评价结果将涵盖纳税诚信情况、履行纳税义务的情况、事前咨询和纳税申报义务等。

中华人民共和国税收征收管理法实施细则_英文版_国务院令[2002]第362号_2002-10-15生效

![中华人民共和国税收征收管理法实施细则_英文版_国务院令[2002]第362号_2002-10-15生效](https://img.taocdn.com/s3/m/309d8cec5ef7ba0d4a733b14.png)

plans and implementation methods formulated by the State Administration of Taxation.The local People's Governments at various levels should positively support the tax information system construction and organize to realize information sharing between the relevant departments.Article 5 The secrecy that the tax authorities shall keep for the taxpayers and withholding agents as mentioned in Article 8 of the Tax Administration Law refers to the commercial secrecy and privacy of the taxpayers and withholding agents. The tax offences of the taxpayers and the withholding agents are not within the scope of the secrecy keeping.Article 6 The State Administration of Taxation should set out the criteria and standards for the behaviour and services of the tax staff.When discovering offences of the tax authorities at lower levels, the upper level tax authorities should timely rectify them. The lower tax authorities should make timely corrections in accordance with the decision of the tax authorities above.When discovering tax offences of tax authorities at a higher level, the tax authorities finding that offences should report to the tax authorities above or the relevant departments.Article 7 The tax authorities shall prize the informants upon their contribution. The fund for the prize shall be included in the annual budget of the tax department for separate accounting. The specific method and standards for the prize shall be made by the State Administration of Taxation together with the Ministry of Finance.Article 8 When assessing the tax payable, adjusting the pre-assumptive tax amount, conducting tax inspection, imposing tax penalty and/or handling tax administrative review, the tax staff should refrain from the case when having one of the following relations with the taxpayers, withholding agents or their legal representatives, directly responsible persons:(1) Husband and wife.(2) Direct blood relatives.(3) Indirect blood relatives within three generations.(4) Close relatives through marriage.(5) Other relations that may influence the impartial execution of laws.Article 9 The tax organizations to be set up and made public as ruled by the State Council as mentioned in Article 14 of the Tax Administration Law refer to the tax investigation bureaus at and below provincial level. The tax investigation bureaus are exclusively in charge of the investigation and dealing of tax evasion, tax arrears, cheating of tax and tax refusal cases.The State Administration of Taxation should make clear the duties of the tax offices and the tax investigation bureaus to avoid overlapping of duties.Chapter 2 Tax RegistrationArticle 10 The SAT offices and the local tax bureaus should adopt the same code for the same taxpayer and share the information.The specific method for tax registration shall be formulated by the State Administration of Taxation.Article 11 The Industrial and Commercial Administration Departments at various levels should regularly inform the SAT offices and the local tax bureaus at the same level of the registration of opening business, changes, de-registration and suspension and cancellation of business licenses.The specific methods of informing shall be made jointly by the State Administration of Taxation and the State Industrial and Commercial Administration.Article 12 The taxpayers engaged in production or business operations should file a written application for tax registration with the competent tax authorities at the location of production and business operation or where the tax obligation arises within 30 days after obtaining the business license. The taxpayers should truthfully fill in the tax registration form and provide the relevant documents, materials as required by the tax authorities.The taxpayers rather than the above, except for the State organs and individuals, should, within 30 days after the date of tax obligation arising, bring the relevant documents to the local competent tax authorities for tax registration.The method for Individual Income Tax registration shall be formulated by the State Council separately.The pattern of the tax registration certificate shall be produced by the State Administration of Taxation.Article 13 The withholding agents should, within 30 days after the date of withholding obligation arising, go to the local competent tax authorities for withholding registration, and obtain the withholding registration certificate. For the withholding agents who have already finished tax registration, the tax authorities may simply record the tax withholding items in the tax registration certificate and shall not issue the withholding registration certificate.Article 14 Where a change occurs in the contents of tax registration, the taxpayer concerned shall, within 30 days after the date of completing the formalities for such change of registration with the Administration for Industry and Commerce or other departments, report to and complete the formalities for change of tax registration with the original tax authorities by presenting the relevant supporting documents.Where taxpayer's tax registration contents change but there is no need to change the registration with the Administration for Industry and Commerce or other departments, the taxpayer shall, within 30 days after the change, present the relevant documents to the original tax authorities to apply to change the tax registration.Article 15 If a taxpayer is involved in dissolution, bankruptcy, cancellation or other circumstances, thus terminating its tax payment obligations pursuant to the law, the taxpayer shall, before cancelling its registration with the Administration for Industry and Commerce or other departments, present the relevant documents to the original tax authorities to apply for cancellation of its tax registration. If, in accordance with regulations, the taxpayer is not required to cancel its registration with the Administration for Industry and Commerce or other departments, the taxpayer shall, within 15 days after the relevant organ approving or announcing the termination, present the relevant documents to the original tax authorities to apply for cancellation of its tax registration.If a change in a taxpayer's address of residence or address of business operations necessities an alteration of the tax authorities for its tax registration, the taxpayer shall, before applying to theAdministration for Industry and Commerce or other departments to amend or cancel its registration and before changing its address of residence or address of business operations, present the relevant documents to the original tax authorities to apply for cancellation of its tax registration and shall carry out tax registration procedures with relevant tax authorities in the new region within 30 days.A taxpayer whose business license is revoked by the Administration for Industry and Commerce or whose registration is cancelled by other departments shall, within 15 days of the revoking of the business license or cancellation of the registration, apply to the original tax authorities for cancellation of its tax registration.Article 16 Before carrying out procedures to cancel its tax registration, a taxpayer shall settle all taxes payable, late payment penalties and other fines and shall turn over invoices, tax registration certificates and other tax documents to the tax authorities.Article 17 Taxpayers engaged in production, business operation should report to the competent tax authorities in written form all of their account numbers within 15 days after opening the basic deposit accounts or other deposit accounts. In case of change, the taxpayers should report in written to the competent tax authorities about the change within 15 days after the change.Article 18 Except in cases where a tax registration certificate is not required in accordance with regulations, a taxpayer must present a tax registration certificate when carrying out the following matters:(1) Opening bank accounts.(2) Applying for a tax reduction, exemption or refund.(3) Applying for a deferred tax report or tax payment.(4) Purchasing invoices.(5) Applying for a certificate of tax administration for business operations in other areas.(6) Handling business termination or business close.(7) Other relevant tax matters.Article 19 The tax authorities shall implement a regular certificate inspection and replacement system for tax registration certificates. A taxpayer shall present the relevant documents to the competent tax authorities within the prescribed time limit to undergo certificate inspection or replacement procedures.Article 20 Taxpayers should openly hang the tax registration certificates at the premises of their production, business operation or offices for the inspection of the tax authorities.In case of losing the tax registration certificate, the taxpayer should report in written to the competent tax authorities and announce in paper the invalidity of the certificate.Article 21 A taxpayer engaged in production or business operations who wants to temporarily undertake production or business activities in another country (town) must present the duplicate of the tax registration certificate and the certificate for tax administration of outside operations issued by the local tax authorities to the tax authorities in the new place of operations for inspection and registration and shall be subject to its administration.The taxpayers who undertake production, business operation for more than 180 days accumulatively in the same other area should go through the tax registration formalities at the place of the business operation.Chapter 3 Administration of Accounting Books and Supporting VouchersArticle 22 A taxpayer engaged in production or business operations shall, in accordance with the relevant rules of the State, establish accounting books within 15 days after the date of obtaining its business license or after the day of tax obligation arises.The term "accounting books" as stated in the previous paragraph shall refer to general ledgers, detailed accounts, journals and other auxiliary accounting books. General ledgers and journals should be in a bound form.Article 23 The taxpayers engaged in industry and commerce with only a small production or business operation which genuinely lacks the ability to keep accounting books may hire the professional organizations approved for engagement in accounting agents or the accounting personnel recognized by the tax authorities to keep its books and handle accounting matters. Should there be real difficulty in hiring the above organizations or personnel, the party may, with approval by tax authorities at country or higher level, keep a book for pasting in all receipt and expenditure vouchers, a goods purchase and sale registry or use tax control system in accordance with the rules by the tax authorities.Article 24 Within 15 days of receipt of its tax registration certificate, a taxpayer engaged in production or business operations shall submit details of its financial and accounting systems or methods to the competent tax authorities for records.In case of making accounting records by computers, the taxpayers should, before use of that, report the accounting software, instructions for use and the relevant materials of the electronic accounting system to the competent tax authorities for records.The electronic accounting system set up by the taxpayers should satisfy the relevant rules of the State and be able to correctly, completely account the revenue or income of the taxpayers.Article 25 Within 10 days from the start of its tax withholding obligations as prescribed by the tax laws and administrative regulations, a withholding agent shall establish a tax withholding and remitting or collecting and remitting book pursuant to the categories of tax to be withheld or collected.Article 26 Where the accounting system of the taxpayers, withholding agents is complete and is able to correctly, completely compute the revenue and income or the tax withholding, the print-out of the complete paper accounting records may be taken in place of the accounting books.Where the accounting system of the taxpayers, withholding agents is not complete and can not be able to correctly, completely compute the revenue and income or the tax withholding, the taxpayers should set up the general accounting records and the other accounting books relevant to tax payment or tax withholding.Article 27 Accounting books, supporting vouchers and statements shall be kept in Chinese. In a national minority autonomous region, the local minority language script in common use throughout the region may be used simultaneously. Enterprises with foreign investment and foreign enterprises may use a foreign language script simultaneously.Article 28 Taxpayers should install and use tax control equipment as required by the tax authorities and report the relevant data and materials according to the rules of the tax authorities.The administrative method for usage and application of tax control equipment shall be formulated by the State Administration of Taxation separately and shall be implemented after approval by the State Council.Article 29 The accounting books, supporting vouchers, statements, tax payment receipts, invoices, documents for exportation and other tax relevant materials should be legal, truthful and complete.The accounting books, supporting vouchers, statements, tax payment receipts, invoices, documents for exportation and other tax relevant materials should be kept for at least 10 years, except otherwise ruled by laws, administrative regulations and rules.Chapter 4 Filing Tax ReturnsArticle 30 The tax authorities should set up and improve the self-assessment system. Upon approval by the tax authorities, taxpayers and withholding agents may file tax returns or submit the withholding reports by mail or electronic data forms.The electronic data forms refer to the forms of telephone voice, electronic data exchange and network transmission confirmed by the tax authorities.Article 31 In filing tax returns by mail, the taxpayers should use the uniform tax filing envelope and take the receipt of the post department as the evidential documents for tax report. The date of the post stamp shall be the actual reporting date for return filing by mail.In filing returns by electronic form, the taxpayers should keep the relevant materials within the time limit ruled by the tax authorities and should regularly submit to the tax authorities in written form.Article 32 Where taxpayers have no tax payable in the tax period, the taxpayers should go through the tax reporting as well.During the tax reduction and tax exemption period, the taxpayers enjoying tax reduction and/or tax exemption should deal with the tax reporting by the relevant rules.Article 33 The tax return or reporting schedule on taxes withheld and remitted or collected and remitted which is submitted by a taxpayer or withholding agent accordingly shall include the following items: tax category, taxable items, taxable projects or projects on which tax should be withheld and remitted or collected and remitted, basis for tax calculations, deductible items and standards, applicable tax rate or tax amount per unit, tax items refundable and amount of tax, tax reduction and exemption items and amount of tax, amount of tax payable or the amount of tax due to be withheld and remitted or collected and remitted, the applicable tax period, deferred tax payment, tax arrears and late payment interest.Article 34 A taxpayer submitting a tax return shall complete the tax return accurately and, depending on the circumstances, shall submit the following relevant documents and materials accordingly:(1) Financial and accounting statements and related explanatory materials.(2) Contracts and letters of agreement relevant to tax payment and documents.(3) Electronic tax reporting materials.(4) Tax administration certificates for business operations in other areas and tax completion certificates of other areas.(5) Relevant documents issued by notary bodies within and without China.(6) Other relevant documents and materials required by tax authorities in accordance with regulations.Article 35 A withholding agent filing a reporting schedule on taxes withheld and remitted or collected and remitted shall complete the form accurately and submit legal certificates related to its tax withholding and remitting or collecting and remitting obligations, as well as other relevant documents and materials required by the tax authorities.Article 36 The taxpayers paying tax on a regular and fixed basis may adopt the tax reporting in a simplified way, by putting together the tax payment periods.Article 37 If a taxpayer or withholding agent has genuine difficulty in submitting a tax return or a reporting schedule on taxes withheld and remitted or collected and remitted within the prescribed time limit and requires an extension, a written application for an extension shall be submitted to the tax authorities within the prescribed time limit and, upon examination and approval of application by the tax authorities, procedures shall be completed within the approved extension period.If a taxpayer or withholding agent is unable to submit a tax return or a reporting schedule on taxes withheld and remitted or collected and remitted within the prescribed time limit due to force majeure, the period may be extended, but a report must be submitted to the tax authorities immediately after the force majeure conditions have abated. The tax authorities shall grant approval after verifying the facts.Chapter 5 Tax CollectionArticle 38 The tax authorities should strengthen the tax collection and administration, and set up and perfect the responsibility system.The tax authorities should determine the mode of tax collection in line with the principle of ensuring the timely payment of tax in full amount to the Treasury, providing convenience to the taxpayers and lowering the tax costs.The tax authorities should strengthen the administration over the taxpayer's export tax refund. The specific method for the administration shall be formulated by the State Administration of Taxation together with the relevant departments of the State Council.Article 39 The tax authorities should timely hand in the taxes, late payment interest and fines to the State Treasury based on the budgetary levels and items as ruled by the State. The tax authorities should not occupy, take away or take part of them for other use and should not put them into any account other than those tax accounts of the State or the Treasury.Any unit and individual should not arbitrarily change the budgetary item and level for the taxes, late payment interest and fines already paid into the State Treasury.Article 40 The tax authorities should encourage the use of checks, bank credit cards and electronic settlement in payment of taxes based on the principle of convenience, quickness and safety.Article 41 One of the following cases belongs to the case of difficulty as mentioned in Article 30 of the Tax Administration Law:(1) The taxpayers have suffered from large losses due to force majeure and thus the normal production and business operation is affected seriously.(2) The balance of the current monetary funds after deduction of wages payable and social security contribution is not enough to pay the taxes.The SAT offices and the local tax bureaus of the specially listed cities may examine and approve the deferral of tax payment in reference to paragraph 2 of Article 30 of the Tax Administration Law.Article 42 In case of needing to defer the payment of taxes, the taxpayers should put forward the application before the expiration of the time limit for tax payment and hand in the following materials: the application report for the deferral of tax payment, current monetary fund balance statement and all bank reconciliation statements, balance sheets, the budget of wages payable and social security contribution as required by the tax authorities.The tax authorities should work out the agreement or disagreement within 20 days after receiving the application report for the deferral of tax payment. In case of disagreement, late payment interest shall be collected starting from the date of expiration of the time limit for the tax payment.Article 43 The taxpayers eligible for tax exemptions or reductions as regulated by laws and administrative regulations or as approved by the statutory approving departments should bring the relevant documents to the competent tax authorities for going through the tax exemptions and reductions formalities. At the expiration of the tax reductions and exemptions, the taxpayers should resume tax payment starting from the day following the expiration day.When the conditions for the tax reductions and exemptions change, the taxpayers enjoying the tax exemptions and reductions should report to the tax authorities within 15 days after the change. Those not satisfying the conditions for the reductions and exemptions should perform the tax payment obligation by law. Where the taxpayers do not pay the tax by law, the tax authorities shall pursue that.Article 44 The tax authorities may, based on the principle of being favorable to tax administration and control, convenient for the taxpayers' tax payment and in accordance with relevant State regulations, entrust related entities and individuals to collect small, decentralized, nuisance tax payments and the payment in different places and shall issue them a certificate of an entrusted tax collector. The entrusted entities and individuals shall collect taxes lawfully in the name of the tax authorities pursuant to the conditions prescribed in the certificate of the entrusted tax collectors and the taxpayers should not refuse. In case of refusal by the taxpayers, the entrusted entities and individuals should timely report to the tax authorities.Article 45 The term "tax payment receipts" as stated in Article 34 of the Tax Administration Law shall refer to the various types of tax payment certificates, tax memos, tax stamps, withholding or collecting certificates and other tax payment documents.Without designation of the tax authorities, any unit and individual shall not be allowed to print tax payment receipts. The tax payment receipts should not be lent, sold, forged or changed.The format of a tax payment receipt and the method for its management shall be formulated by the State Administration of Taxation.Article 46 After receiving the tax payment, the tax authorities should issue the tax payment receipts to the taxpayers. The taxpayers shall pay the tax through the banks. The tax authorities may entrust the banks to issue the tax payment receipts.Article 47 In the case of a taxpayer in one of the circumstances stated in Article 35 or 37 of the Tax Administration Law, the tax authorities shall have the right to use any one of the following methods to assess the amount of tax payable:(1) Assess the tax payable in reference to the tax burden level of the taxpayers of similar business size and revenue level of the same sector or similar sector in the same place.(2) Assess the amount of tax payable according to the business revenue or cost plus reasonable amounts of expenses and profits.(3) Assess the amount of tax payable according to a calculation or assessment of the amount of raw materials, fuels, power, and that consumed.(4) Assess the amount of tax payable according to other reasonable methods.If using one of the above-mentioned methods is insufficient to accurately assess the amount of tax payable, two or more methods may be used simultaneously.Where the taxpayers have objections to the assessment of the tax authorities by using one of the above methods, the taxpayers should provide the relevant evidences and the tax authorities shall make adjustment to the tax payable after verifying the evidences.Article 48 The tax authorities shall be responsible for the evaluation of the reputation level of the taxpayers. The method for the evaluation shall be formulated by the State Administration of Taxation.Article 49 Where the subcontractors or lessees have independent production and business operation rights and are independent in accounting and regularly pay the contract makers or lessors the contract commissions or rentals, the subcontractors or lessees should pay income tax on the revenue and income from their production and business operation and accept the tax administration, except otherwise regulated by laws and administrative regulations.Within 30 days after contract or lease making, the contract makers or the lessors should report to the competent tax authorities about the subcontractors and lessees. Should the contract makers or the lessors fail to report that, they shall bear the associated responsibility with the subcontractors or the lessors.Article 50 In case of disbanding, cancellation or bankruptcy, the taxpayers should, before liquidation, report to the competent tax authorities. For those not settling the tax payment, the competent tax authorities shall participate in the liquidation.Article 51 The term "associated enterprises" as stated in Article 36 of the Tax Administration Law shall refer to companies, enterprises or other economic entities which have one of the following relationships:(1) Direct or indirect ownership or control in relation to such areas as capital, business operations and purchases and sales.(2) Direct or indirect ownership or control by a third party.(3) Other mutually beneficial associations.A taxpayer shall be obliged to provide to its local tax authorities with details of price, expense standards, etc., with regard to its business transactions with associated enterprises. The specific method shall be formulated by the State Administration of Taxation.Article 52 The "business transactions between independent enterprises" as stated in Article 36 of the Tax Administration Law shall refer to business dealings between enterprises with no associated relationship which are conducted pursuant to fair transaction prices and common business practices.Article 53 The taxpayers may put forward the pricing principle and computation method for the business transactions with their associated enterprises. After examination and approval, the competent tax authorities shall conclude an agreement on the pricing matters with the taxpayers in advance and monitor the execution of the taxpayers.Article 54 The tax authorities may adjust the tax payable of the taxpayers if the business transactions of the taxpayers with the associated enterprises have one of the following conditions:(1) The purchasing and sales transactions are not priced in line with the arm's length principle.(2) The amount of interest paid or received on the loan between them exceeds or is less than the amount that would be agreeable between non-associated parties or exceeds or is less than the normal interest rates of similar loan services.(3) The provision of labour service is not charged or paid in line with the arm's length principle.(4) The transfer of property, provision of the use right of property is not priced or charged or paid at arm's length.(5) Other cases are not priced at arm's length.Article 55 In one of the cases as described in Article 54 of these detailed rules, the tax authorities may adjust the taxable revenue or income by the following methods:(1) According to pricing for the same or similar business transactions between independent enterprises.(2) According to the profit margin obtainable if reselling the goods to a non-associated third party.(3) According to the cost plus reasonable expenses and profits.(4) According to other appropriate methods.Article 56 Where the taxpayers fail to make payment, pay expenses for the business transactions with their associated enterprises at arm's length, the tax authorities shall make adjustments within 3 years after the tax year when the transactions occurred. In special cases, the adjustment may be made within 10 years after the occurrence of the transactions.Article 57 The taxpayers failing to go through the tax registration for production and business operation as ruled in Article 37 of the Tax Administration Law include those doing business in another country (city) without reporting to the local tax authorities for registration.Article 58 Where the tax authorities impound commodities or goods pursuant to the provisions of。

非居民企业所得税核定征收管理办法(中英文)

Measures for Administration of the Levy of Income Tax on Non-tax-resident Enterprises by Assessment非居民企业所得税核定征收管理办法Issue: June 2010CLP Reference: 3230/10.02.20PRC Reference:国税发 [2010] 19号Promulgated: 20 February 2010Effective: 20 February 2010(Issued by the State Administration of Taxation on, and effective as of, February 20 2010.)Guo Shui Fa [2010] No.19Article 1:These Measures have been formulated pursuant to the PRC Enterprise Income Tax Law (the Enterprise Income Tax Law) and its Implementing Regulations and the PRC Law on the Administration of the Levy and Collection of Taxes (the Tax Collection Law) in order to regulate the assessment and levy of enterprise income tax on non-tax-resident enterprises.(国家税务总局于二零一零年二月二十日发布施行。

)国税发 [2010] 19号第一条为了规范非居民企业所得税核定征收工作,根据《中华人民共和国企业所得税法》(以下简称企业所得税法)及其实施条例和《中华人民共和国税收征收管理法》(以下简称税收征管法)及其实施细则,制定本办法。

企业所得税法中英对照

企业所得税法中英对照中文:企业所得税法英文:Enterprise Income Tax Law中文:第一章总则英文:Chapter I General Provisions中文:第一条为了贯彻税收法律,加强税收管理,维护国家税收秩序,制定本法。

英文:Article 1 This Law is enacted for the purpose of implementing tax laws, strengthening tax administration, maintaining the order of national tax revenue, and regulating income tax for enterprises.中文:第二条对中华人民共和国内地、独立关税区、保税区和其他划归国家的经济特区(以下统称为中国境内)内的所有企业及其他组织,按照本法规定征收企业所得税。

英文:Article 2 Enterprise income tax shall be levied according to the provisions of this Law on all enterprises and other organizations within the territory of the People's Republic of China, including the mainland, independent customs zones, bonded areas, and other economic special zones (hereinafter referred to collectively as "China's territory").中文:第三条企业所得税的税源是企业在依法确认的各种收入中取得的所得。

英文:Article 3 The sources of enterprise income tax are the income obtained by enterprises from various legally confirmed revenue sources.中文:第四条享受优惠税率和从事特定业务或投资特定项目税收优惠的企业,在法律、行政法规和其它规范性文件中,另有规定的,适用其规定。

企业所得税法英文版

The Law of the People’s Republic of China on Enterprise Income Tax中华人民共和国企业所得税法Order of the President [2007] No.6316 March, 2007(Adopted at the 5th Session of the 10th National People’s Congress on 16 March 2007, promulgated by Order No. 63 of the President of the People’s Republic of China and effective as of 1 January 2008)Table of ContentChapter One: General ProvisionsChapter Two: Taxable IncomeChapter Three: Payable TaxChapter Four: Preferential Tax TreatmentChapter Five: Tax Withheld at SourceChapter Six: Special Tax Payment AdjustmentChapter Seven: Administration of Tax Levying and CollectionChapter Eight: Supplementary ProvisionsChapter One: General ProvisionsArticle 1: Taxpayers of enterprise income tax shall be enterprises and other organizations that obtain income within the People’s Republic of China (hereinafter referred to as “Enterprises”) and shall pay enterprise income tax in accordance with the provisions of this Law.This Law shall not apply to wholly individually-owned enterprises and partnership enterprises.Article 2: Enterprises are divided into resident enterprises and non-resident enterprises.For the purposes of this Law, the term “resident enterprises” shall refer to Enterprises that are set up in China in accordance with the law, or that are set up in accordance with the law of the foreign country (region) whose actual administration institution is in China.For the purposes of this Law, the term “non-resident enterprises” shall refer to Enterprises that are se t up in accordance with the law of the foreign country (region) whose actual administration institution is outside China, but they have set up institutions or establishments in China or they have income originating from China without setting up institutions or establishments in China.Article 3: Resident enterprises shall pay enterprise income tax originating both within and outside China. Non-resident enterprises that have set up institutions or premises in China shall pay enterprise income tax in relation to the income originating from China obtained by their institutions or establishments, and the income incurred outside China but there is an actual relationship with the institutions or establishments set up by such enterprises.Where non-resident enterprises that have not set up institutions or establishments in China, or where institutions or establishments are set up but there is no actual relationship with the income obtained by theinstitutions or establishments set up by such enterprises, they shall pay enterprise income tax in relation to the income originating from China.Article 4: The rate of enterprise income tax shall be 25%.Non-resident enterprises that have obtained income in accordance with the provisions of Paragraph Three of Article 3 hereof, the applicable tax rate shall be 20%.Chapter Two: Taxable IncomeArticle 5: The balance derived from the total income in each taxable year of Enterprises, after deduction of the non-taxable income, tax exempted income, other deductions and the making up of losses of previous years shall be the taxable income.Article 6: Income obtained by Enterprises from various sources in monetary and non-monetary terms shall be the total income, including:1.income from sale of goods;2.income from provision of labour services;3.income from transfer of property;4.income from equity investment such as dividend and bonus;5.interest income;6.rental income;7.income from royalties;8.income from donations; and9.other income.Article 7: The following income from the total income shall not be taxable:1.financial funding;2.administrative fees and government funds obtained and included in financial management in accordance with the law; and3.other non-taxable income prescribed by the State Council.Article 8: Reasonable expenses that are relevant to the income actually incurred and obtained by Enterprises, including costs, fees, tax payments, losses and other fees may be deducted from the taxable income.Article 9: In relation to the expenses from charitable donations incurred by Enterprises, the portion within 12% of the total annual profit may be deducted from the taxable income.Article 10: The following expenses may not be deducted from the taxable income:1.income from equity investment paid to investors such as dividend and bonus;2.payment of enterprise income tax;te payment fines;4.penalties; fines and losses from confiscated property;5.expenses from donations other than those prescribed in Article 9 hereof;6.sponsorship fees;7.expenses for non-verified provisions; and8.other expenses irrelevant to the income obtained.Article 11: Where Enterprises compute the taxable income, the depreciation of fixed assets calculated in accordance with provisions may be deducted.No depreciation may be deducted for the following fixed assets:1.fixed assets other than premises and buildings that have not yet been used;2.fixed assets leased from other parties by means of business lease;3.fixed assets leased to other parties by means of lease financing;4.fixed assets that have been depreciated in full but are still in use;5.fixed assets that are irrelevant to business activities;nd credited as fixed assets after independent price valuation;7.other fixed assets whose depreciation may not be calculated.Article 12: In Enterprises compute the taxable income, the amortization of intangible assets calculated in accordance with provisions may be deducted.The amortization of the following intangible assets may not be deducted:1.the fees for self development of intangible assets that have been deducted from the taxable income;2.self-created goodwill;3.intangible assets that are irrelevant to business activities; and4.other intangible assets whose amortization fee may not be calculated.Article 13: Where Enterprises calculate taxable income, the following expenses incurred by Enterprises as long-term fees to be amortized and that are amortized in accordance with provisions may be deducted:1.reconstruction expenses for fixed assets that have been depreciated in full;2.reconstruction expenses for fixed assets leased from other parties;3.heavy repair expenses of fixed assets; and4.other expenses that shall be treated as long-term amortization fees.Article 14: During the period when Enterprises invest outside the territory, the cost of investment in assets may not be deducted from the taxable income.Article 15: The inventory used or sold by Enterprises whose cost is calculated in accordance with provisions may be deducted from the taxable income.Article 16: Where Enterprises transfer assets, the net value thereof may be deducted from the taxable income.Article 17: Where Enterprises compute the consolidated enterprise income tax, the losses of business institutions outside the territory may not be offset by the profits of business institutions inside the territory.Article 18: Where there is a loss in a taxable year of Enterprises, it may be brought forward to thesucceeding years and made up by the income of succeeding years, but the limit of bringing forward may not exceed five years.Article 19: Where non-resident enterprises obtain income provided in Paragraph Three of Article 3 hereof, the taxable income shall be calculated in accordance with the following methods:1.income from equity investment such as dividend and bonus and interest income, rental income and royalties, the total income shall be the taxable income;2.income from property transfer, the balance derived from the deduction of net asset value from the total income shall be the taxable income;3.other income whose taxable income shall be calculated with reference to the previous two methods.Article 20: The income, specific scope and standard of deduction and the specific method of taxation treatment of assets prescribed in this Chapter shall be provided by the departments in charge of finance and taxation under the State Council.Article 21: In computing the taxable income, where financial and accounting treatment methods of Enterprises are inconsistent with tax laws and administrative regulations, such taxable income shall be computed in accordance with tax laws and administrative regulations.Chapter Three: Payable TaxArticle 22: The taxable income of Enterprises shall be the balance derived from the taxable income of Enterprises multiplies the applicable rate and minus the tax amount of tax reduction and exemption pursuant to the preferential tax treatment hereof.Article 23: The income tax that has been paid outside the territory for the following income obtained by Enterprises may be offset from the payable tax of the current period. The offset limit is the payable tax calculated in accordance with provisions hereof in respect of the income of such item, the portion in excess of the offset limit may be made up by the balance of the offset amount of the current year out of the annual offset limit within the next five years:1.The taxable income originating outside China by resident enterprises;2.The taxable income incurred outside China that is obtained by institutions or establishments of non-resident enterprises set up in China with an actual relationship with such institution or establishment.Article 24: Where income from equity investment such as dividend and bonus originating outside the territory of China is shared by foreign enterprises directly or indirectly controlled by resident enterprises, the portion undertaken by foreign enterprises in the actual income tax actually paid outside the territory by foreign enterprises may be offset in the offset limit prescribed in Article 23 hereof as the income tax that may be offset outside the territory by such resident enterprises.Chapter Four: Preferential Tax TreatmentArticle 25: The industries and projects with key support and under encouraged development by the State may be given preferential enterprise income tax treatment.Article 26: The following income of Enterprises shall be tax-exempted income:1.income from interests on government bonds;2.income from equity investment income such as dividend and bonus between qualified resident enterprises;3.income from equity investment such as dividend and bonus obtained from resident enterprises by non-resident enterprises that have set up institutions or establishments in China with an actual relationship with such institutions or establishments;4.income of qualified non-profit organizations.Article 27: The following income may be subject to exempted or reduced enterprise income tax:1.income from engaging in projects of agriculture, forestry, animal husbandry and fisheries by Enterprises;2.income from investment and operation of infrastructure projects with key state support such as habour, pier, airport, railway, highway, electricity and hydroelectricity by Enterprises;3.income from engaging in qualified projects of environmental protection and energy and water conservation;4.income from qualified transfer of technology by Enterprises; and5.income prescribed by Paragraph Three of Article 3 hereof.Article 28: Small-scale Enterprises with minimal profits that are qualified are subject to the applicable enterprise income tax rate with a reduction of 20%.High and new technology Enterprises that require key state support are subject to the applicable enterprise income tax rate with a reduction of 15%.Article 29: The autonomous authority of ethnic autonomous locality may decide on the reduction or exemption of the portion of enterprise income tax shared by the locality that shall be paid by Enterprises of the ethnic autonomous locality. Where an autonomous prefecture or autonomous county decides on the reduction or exemption, they must report to the people’s government of province, autonomous region or municipality directly under the central government for approval.Article 30: Weighted deduction may be computed in taxable income for the following expenses of Enterprises:1.research and development fees incurred by Enterprises in the development of new technology, new products and new skills; and2.the wages paid by Enterprises for job placement of the disabled and of other personnel encouraged by the State.Article 31: Venture investment enterprises that engage in venture investment requiring key state support and encouragement may offset the taxable income at a certain ratio of the investment amount.Article 32: Where the fixed assets of Enterprises actually require accelerated depreciation due to technology advancement, the years of depreciation may be shortened or the accelerated depreciationmethod may be adopted.Article 33: The income obtained by Enterprises from the production of products in line with state industrial policies through comprehensive use of resources may be deducted from the taxable income.Article 34: The investment by Enterprises on procurement of special facilities for environmental protection, energy and water conservation and safe production may be subject to an offset tax amount at a certain ratio.Article 35: The specific measures of preferential tax treatment prescribed by this Law shall be formulated by the State Council.Article 36: Where there is a significant impact on the business activities of Enterprises pursuant to the needs of national economy and social development, or due to unexpected public incidents, the State Council may formulate the special preferential policy of enterprise income tax and report to the Standing Committee of the National People’s Congress for the record.Chapter Five: Tax Withheld at SourceArticle 37: The payable income tax from income obtained by non-resident enterprises in accordance with Paragraph Three of Article 3 hereof shall be subject to tax withheld at source, with the payer as the withholding agent. The tax payment shall be withheld from the amount paid or the payable amount due from each tax payment and payable amount of the withholding agent.Article 38: In respect of the payable income tax from income obtained by non-resident enterprises from project works and labour services in China, the tax authority may designate the payer of project price or labour fee as withholding agent.Article 39: In respect of the income tax that shall be withheld in accordance with Articles 37 and 38 hereof, where the withholding agent has not withheld or fails to perform the withholding obligation in accordance with the law, the taxpayer shall pay in the place where the tax is incurred. Where the taxpayer does not pay in accordance with the law, the tax authority may pursue the payable tax amount of such taxpayer from the amount payable by the payer of other income projects in China of such taxpayer.Article 40: The withholding agent shall turn the tax payment withheld to the treasury within 7 days from the day of withholding, and submit a statement of withholding enterprise income tax to the tax authority of the place where it is located.Chapter Six: Special Tax Payment AdjustmentArticle 41: The business transactions between Enterprises and their affiliates that reduce the taxable income or income of such Enterprises and their affiliates not in compliance with independent transaction principle, the taxation authority has the right to make an adjustment in accordance with reasonablemethods.The cost incurred in joint development and transfer of intangible assets, or joint provision and acceptance of labour services by Enterprises and their affiliates shall be shared under the independent transaction principle in computing the taxable income.Article 42: Enterprises may report to the tax authority the pricing principle and calculation method of the transactions between their affiliates. Upon negotiation and confirmation with the Enterprises, the tax authority may reach the advance pricing arrangement.Article 43: Where Enterprises submit to the tax authority the annual enterprise income tax return, they shall enclose a statement of the annual business transactions between affiliates in respect of the business transactions of the Enterprises and their affiliates.Where the tax authority conducts affiliated business investigation, Enterprises and their affiliates, and other enterprises relevant to the affiliated business investigation shall provide the relevant information in accordance with provisions.Article 44: Where Enterprises fail to provide the information of business transactions of affiliates, or provide false and incomplete information that cannot faithfully reflect the actual affiliated business transaction, the tax authority has the right to verify its taxable income.Article 45: Where Enterprises controlled by resident enterprises or resident enterprises and Chinese residents in the country (region) where the actual tax burden is obviously lower than the tax rate prescribed by Paragraph One of Article 4 hereof, and profits are not distributed or distributed at a reduced rate due to reasons other than reasonable business needs, the portion of the above profits belonged to such resident enterprises shall be included in the income of such resident enterprises of the current period.Article 46: The interest fee incurred in excess of the prescribed standard obtained by Enterprises from the loan investment and equity investment of their affiliates may not be deducted from the taxable income.Article 47: Where Enterprises implement other arrangement without reasonable business objectives to reduce the payable income or income, the tax authority has the right to adjust in accordance with reasonable methods.Article 48: Where tax payment requires to be levied additionally by tax authority in respect of the tax payment adjustment made in accordance with the provisions of this Chapter, such tax payment shall be levied additionally and interest shall be levied in accordance with the provisions of the State Council.Chapter Seven: Administration of Tax Levying and CollectionArticle 49: The administration of levy and collection of enterprise income tax shall follow the provisions hereof in addition to the Law of the People’s Republic of China on the Administration of Levying and Collection of Tax.Article 50: Unless otherwise specified by tax laws and administrative regulations, resident enterprises whose place of tax payment is the place of registration of the Enterprise but the place of registration is outside the territory, the place of tax payment shall be the place where the actual administration institution is located.Where resident enterprises establish business institutions in China without legal person qualification, it shall consolidate the calculation and payment of enterprise income tax.Article 51: In respect of non-resident enterprises that obtain the income prescribed in Paragraph Two of Article 3 hereof, the place of tax payment shall be the place where the institution or the establishment is located. Non-resident enterprises that set up two or more institutions or establishments in China may, upon the examination and approval of the tax authority, select its main institution or establishment to pay the consolidated enterprise income tax.Where non-resident enterprises obtain the income prescribed in Paragraph Three of Article 3 hereof, the place of tax payment shall be the place where the withholding agent is located.Article 52: Enterprises may not pay consolidated enterprise income tax unless otherwise prescribed by the State Council.Article 53: Enterprise income tax shall be calculated in accordance with the taxable year which starts from 1 January to 31 December of a calendar year.If an Enterprise commences business or terminates its business activities during the taxable year and the actual business period of such taxable year is less than 12 months, the actual business period shall be treated as a taxable year.Where the Enterprise is liquidated in accordance with the law, the liquidation period shall be a taxable year.Article 54: Enterprise income tax shall be prepaid on a monthly or quarterly basis.Enterprises shall submit a prepaid enterprise income tax return to the tax authority within 15 days of the completion of the month or the quarter to make tax prepayment.Enterprises shall submit an annual enterprise income tax return to the tax authority within five months of the completion of the year and make the settlement of the payable and refundable tax payment. Enterprises that submit the enterprise income tax return shall enclose a financial report and other relevant information in accordance with provisions.Article 55: Where Enterprises terminate business activities in the interim of the year, they shall handle with the tax authority the settlement and payment of enterprise income tax of the current period within 60 days from the actual termination of business.Enterprises shall, prior to handling registration cancellation, file a return of the income settled and pay enterprise income tax in accordance with the law.Article 56: Enterprise income tax paid in accordance with this Law shall be calculated in Renminbi. Where the income is calculated in a currency other than Renminbi, it shall be converted into Renminbi for tax payment.Chapter Eight: Supplementary ProvisionsArticle 57: Enterprises set up with approval prior to the promulgation of this Law that enjoy low preferential tax rate in accordance with the tax laws and administrative regulations at the current period may, pursuant to the provisions of the State Council, gradually transit to the tax rate provided herein within five years of the implementation of this Law. Where such enterprises enjoy regular tax exemption and reduction, the treatment continues to apply until expiry after the implementation of this Law. However, those that fail to be entitled to this treatment by reason of not making any profits, the preferential period shall be calculated from the year this Law is implemented.High and new technology enterprises that are set up in a specific zone in accordance with the law for the purpose of external economic cooperation and technology exchange and that are newly set up and require key state support in the region of special policy of such region specified by the State Council may eligible for transitional treatment and the specific measures shall be provided by the State Council.Other enterprises under the encouraged category confirmed by the state may eligible for tax exemption and reduction in accordance with the provisions of the State Council.Article 58: Where agreements on taxation concluded by the People’s Republic of China and foreign governments contain different provisions, such agreements shall prevail.Article 59: The implementing regulations shall be formulated by the State Council on the basis of this Law.Article 60: This Law shall come into effect as of 1 January 2008. The Law of the People’s Republic of China on the Enterprise Income Tax of Foreign-invested Enterprises and Foreign Enterprises adopted at the 4th session of the 7th National People’s Congress on 9 April 1991 and the Tentative Regulations of the People’s Republic of China on Enterprise Income Tax promulgated by the State Council on 13 December 1993 shall be repealed simultaneously.。

非居民个人所得税指南 英文版

非居民个人所得税指南英文版Here's a guide to non-resident individual income tax in English, following the requirements you've mentioned:When it comes to non-resident individual income tax, things can get a bit tricky. But don't worry, we've got you covered. Basically, if you're not a resident of a country but earn income there, you might have to pay taxes. It's important to know the rules and rates so you don't get caught off guard.Let's talk about exemptions first. Some income sources for non-residents are tax-free, like dividends from foreign companies or interest on foreign bank accounts. But always check with a tax advisor to be sure.Now, let's dive into the tax rates. They vary depending on the country and your income level. Some countries have progressive tax rates, meaning the more you earn, the higher the tax rate. Others have flat rates, so it's allthe same percentage no matter how much you make.Filing taxes as a non-resident can be a bit of a challenge. You might need to hire a local tax preparer or use an online service to make sure you're doing it correctly.。

企业所得税法 双语

企业所得税法双语企业所得税法(英文: Enterprise Income Tax Law)是一项为规范企业所得税政策、确保税收公平和提高税收征管效率而颁布的法律。

该法律依据国家税收政策和经济发展需要,通过界定纳税主体、确定应纳税所得额、规定减免和优惠政策、规范税务管理等内容,对企业所得税的课税对象、税率、纳税义务等方面进行详细规定。

下面将对企业所得税法的相关内容进行详细解析。

企业所得税法规定了应纳税的企业所得税税率,并对纳税主体进行了明确的规定。

在中国,纳税主体主要包括了企业、个体工商户和其它组织。

企业按照其所得的来源和性质分为内资企业和外资企业。

据法律规定,企业应当依法申报纳税,并按照规定的税率和应纳税所得额缴纳企业所得税。

企业所得税法对企业的所得计算和所得调整等方面也作出了明确的规定。

税法规定了企业所得的计算方法和计税基础,包括利润、投资收益、财产转让收益等所得项目的计算及调整。

税法还对企业在发生亏损等情况下的处理方式做出了具体规定,从而保障了企业税收的公平性和稳定性。

企业所得税法还规定了一系列的减免和优惠政策,以鼓励和促进企业发展。

这些减免和优惠政策包括了对特定行业、区域和项目的税收优惠政策,以及对企业技术创新、环保投入等方面的支持政策。

这些政策的出台,不仅有利于提高企业的生产经营效率,还可以有效促进经济的发展和转型升级。

在税务管理方面,企业所得税法要求企业依法履行纳税申报、纳税缴款等义务,同时规定了税务机关的监督管理和税收征管措施。

税法还规定了企业所得税税务处理的程序和程序限期,以确保税收征管的及时性和有效性。

企业所得税法是对企业所得税政策的具体规定,涉及了纳税主体、税率、所得计算、减免和优惠政策、税务管理等方面的内容。

企业应当遵守企业所得税法的相关规定,认真履行纳税义务,促进企业健康发展,同时也为国家财政的稳定和发展贡献应有的税收收入。

国家税务总局关于印发《非居民企业所得税汇算清缴工作规程》的通知

国家税务总局关于印发《非居民企业所得税汇算清缴工作规程》的通知文章属性•【制定机关】国家税务总局•【公布日期】2009.02.09•【文号】国税发[2009]11号•【施行日期】2009.02.09•【效力等级】部门规范性文件•【时效性】失效•【主题分类】企业所得税正文国家税务总局关于印发《非居民企业所得税汇算清缴工作规程》的通知(国税发〔2009〕11号)各省、自治区、直辖市和计划单列市国家税务局,广东省和深圳市地方税务局:现将《非居民企业所得税汇算清缴工作规程》印发给你们,请遵照执行。

执行中发现的问题请及时反馈到税务总局(国际税务司)。

附件:1.非居民企业汇总申报纳税事项协查函2.非居民企业汇总申报纳税事项处理联络函3.非居民企业所得税汇算清缴汇总表(据实申报企业适用)4.非居民企业所得税汇算清缴汇总表(核定征收企业适用)5.非居民企业所得税汇算清缴指标分析表(据实申报企业适用)国家税务总局二○○九年二月九日非居民企业所得税汇算清缴工作规程为贯彻落实《国家税务总局关于印发〈非居民企业所得税汇算清缴管理办法〉的通知》(国税发〔2009〕6号,以下简称《办法》),规范税务机关对非居民企业所得税的汇算清缴工作,提高汇算清缴工作质量,制定本规程。

一、汇算清缴工作内容非居民企业所得税汇算清缴包括两方面内容:一是非居民企业(以下简称企业)应首先按照《办法》的规定,自行调整、计算本纳税年度的实际应纳税所得额、实际应纳所得税额,自核本纳税年度应补(退)所得税税款并缴纳应补税款;二是主管税务机关对企业报送的申报表及其他有关资料进行审核,下发汇缴事项通知书,办理年度所得税多退少补工作,并进行资料汇总、情况分析和工作总结。

二、汇算清缴工作程序企业所得税汇算清缴工作分为准备、实施、总结三个阶段,各阶段工作的主要内容及时间要求安排如下:(一)准备阶段。

主管税务机关应在年度终了之日起三个月内做好以下准备工作:1.宣传辅导。

非居民企业所得税核定征收管理办法

非居民企业所得税核定征收管理办法第一章总则第一条为了规范非居民企业所得税的征收管理,保障国家税收收入,维护纳税人合法权益,根据《中华人民共和国企业所得税法》及其实施细则,制定本办法。

第二条本办法适用于在中华人民共和国境内未设立机构、场所,或者虽设立机构、场所但取得的所得与其所设机构、场所没有实际联系的非居民企业。

第三条国家税务总局及其地方税务局负责非居民企业所得税的核定征收管理工作。

第二章纳税义务人第四条非居民企业在中国境内取得的股息、利息、租金、特许权使用费等所得,应当依法缴纳企业所得税。

第五条非居民企业在中国境内取得的转让财产所得,包括转让中国境内不动产、土地使用权、企业股权等,应当依法缴纳企业所得税。

第三章税款核定第六条非居民企业所得税的应纳税所得额,由税务机关根据实际情况进行核定。

第七条税务机关在核定应纳税所得额时,可以采用下列方法之一:(一)按固定比例核定;(二)按实际收入核定;(三)按成本加成核定;(四)税务机关认为合理的其他方法。

第八条非居民企业应当按照税务机关的要求,提供与核定应纳税所得额相关的财务会计报告、合同、协议等资料。

第四章税款征收第九条非居民企业所得税的征收,可以采用源泉扣缴或者指定扣缴义务人的方式进行。

第十条源泉扣缴义务人应当按照规定的税率,从支付给非居民企业的款项中扣缴企业所得税,并及时解缴国库。

第十一条指定扣缴义务人应当按照税务机关的要求,从支付给非居民企业的款项中扣缴企业所得税,并及时解缴国库。

第五章税收优惠第十二条非居民企业在中国境内取得的所得,可以按照中国法律及中国与其他国家签订的税收协定或者协议,享受税收优惠。

第六章法律责任第十三条非居民企业未按照本办法规定缴纳企业所得税的,税务机关有权追缴税款,并依法加收滞纳金。

第十四条源泉扣缴义务人或者指定扣缴义务人未按照本办法规定扣缴税款的,税务机关有权追缴税款,并依法加收滞纳金。

第七章附则第十五条本办法自发布之日起施行。

企业所得税法中英对照

企业所得税法中英对照企业所得税法实施条例第一章总则第一条为了规范企业所得税的征收和管理,加强税收征管,维护纳税人的合法权益,根据《中华人民共和国企业所得税法》(以下简称企业所得税法)制定本条例。

第二条本条例所称企业应纳税所得额,是指企业在一个纳税年度的应纳税所得额。

企业所得税负责税务机关按规定对企业税务信息进行审查、核对后确定的纳税义务。

第三条本条例所称企业所得税负责人,是指企业依照企业所得税法规定的职责,负有支付企业所得税的主体,可以是企业法定代表人、负责财务承办的主要负责人或者其他负责支付企业所得税的负责人。

第四条纳税人依法自行提出附注企业所得税年度纳税申报表,或者在导致其应纳税所得额发生增减变化的情况下,应当在规定的期限内补充或者修改已报送的企业所得税年度纳税申报表。

税务机关应当在规定的期限内对补充或者修改的企业所得税年度纳税申报表进行审查。

第五条本条例所称中小企业,是指依法设立,经营状况良好,具有独立承担民事责任能力的各类企业,以其所得税法规定的条件为界限划分的中型企业和小型企业。

第二章纳税申报第六条纳税人应当于每年1月1日至2月28日,向主管税务机关自行提出企业所得税年度纳税申报表。

按年报纳税的,纳税人可以根据具体情形自行提出每月、季度预报企业所得税预缴申报表。

税务机关应当自收到企业所得税年度纳税申报表之日起15日内予以登记备案。

第七条纳税人在各项损益科目实际发生的基础上,按照企业所得税法规定的会计制度和核算制度自行提出企业所得税年度纳税申报表。

纳税人应当在企业所得税年度纳税申报表上公示利润总额与净利润的账面和实际余额,以及税务机关对其上月末的财务状况与财务收支等情况。

企业在向税务机关提出企业所得税预缴申报表时,应当提交企业所得税费明细表。

第八条对采取现代技术手段会计核算的纳税人可以最大限度地利用现代技术,自行申报企业所得税核定和课税情况。

税务机关应当在规定时间内抽查企业所得税年度纳税申报表和企业所得税预缴申报表,并在规定时间内向纳税人发送审核结果。

关于印发《非居民企业所得税核定征收管理办法》的通知……

关于印发《非居民企业所得税核定征收管理办法》的通知……作者:来源:《财会学习》2010年第04期国家税务总局关于印发《非居民企业所得税核定征收管理办法》的通知◎政策背景根据企业所得税法第三条第二款,非居民企业在中国境内设立机构、场所的,应当就其所设机构、场所取得的来源于中国境内的所得,以及发生在中国境外但与其所设机构、场所有实际联系的所得,缴纳企业所得税。

为了规范非居民企业在中国境内设立机构、场所(不包括常驻代表机构)的企业所得税管理,国家税务总局在2月20日发布了《非居民企业所得税核定征收管理办法》(国税发[2010]19号)。

19号文提高了非居民企业的核定利润率,并且重申明确了某些执行问题。

◎明确了非居民企业的所得税征收方式1.据实征收非居民企业应当按照税收征管法及有关法律法规设置账簿,根据合法、有效凭证记账,进行核算,并应按照其实际履行的功能与承担的风险相匹配的原则,准确计算应纳税所得额,据实申报缴纳企业所得税。

2.核定征收非居民企业因会计账簿不健全,资料残缺难以查账,或者其他原因不能准确计算并据实申报其应纳税所得额的,税务机关有权采取以下方法核定其应纳税所得额。

(1)按收入总额核定应纳税所得额:适用于能够正确核算收入或通过合理方法推定收入总额,但不能正确核算成本费用的非居民企业。

计算公式如下:应纳税所得额=收入总额×经税务机关核定的利润率(2)按成本费用核定应纳税所得额:适用于能够正确核算成本费用,但不能正确核算收入总额的非居民企业。

计算公式如下:应纳税所得额=成本费用总额/(1-经税务机关核定的利润率)×经税务机关核定的利润率(3)按经费支出换算收入核定应纳税所得额:适用于能够正确核算经费支出总额,但不能正确核算收入总额和成本费用的非居民企业。

计算公式:应纳税所得额=经费支出总额/(1-经税务机关核定的利润率-营业税税率)×经税务机关核定的利润率◎核定征收的利润率提高19号文发布之前的核定利润率一般为10%~40%,19号文重新规定了核定征收下的非居民企业的利润率标准:(1)从事承包工程作业、设计和咨询劳务的,利润率为15%~30%;(2)从事管理服务的刑润率为30%~50%;(3)从事其他劳务或劳务以外经营活动的,利润率不低于15%。

企业所得税法中英对照

企业所得税法中英对照企业所得税法对国内外企业在中国境内取得的所得进行征税,是中国税法体系中的重要组成部分。

以下是企业所得税法中英对照的文章,旨在为读者提供生动、全面、有指导意义的解读。

IntroductionEnterprise Income Tax (EIT) Law is an essential component of China's tax system, aiming to tax domestic and foreign enterprises' income generated within the country's borders. This article provides a comprehensive and informative interpretation of the EIT Law, emphasizing its significance and offering practical guidance.Scope of Taxation企业所得税法的征税范围是企业所得。

按照该法,“企业所得”包括居民企业的所得和非居民企业的所得。

The scope of taxation under the EIT Law includes enterprise income, encompassing the income of resident enterprises and non-resident enterprises.Resident Enterprises居民企业是指依照中国税法规定在中国境内注册设立并具有住所或者实际经营机构的企业。

Resident enterprises are those registered and established within China's territory with a domicile or actual operating premises, in accordance with Chinese tax laws.Non-resident Enterprises非居民企业是指未在中国境内注册设立的企业,或在中国境内注册设立,却没有住所或者实际经营机构的企业。

非居民企业所得税相关规定有哪些

⾮居民企业所得税相关规定有哪些⼀、企业所得税纳税⼈规定(⼀)居民企业(1)依法在中国境内成⽴的企业;(所得税法第⼆条第⼆款)(2)依照外国(地区)法律成⽴但实际管理机构在中国境内的企业;(所得税法第⼆条第⼆款)企业所得税法第⼆条所称依照外国(地区)法律成⽴的企业,包括依照外国(地区)法律成⽴的企业和其他取得收⼊的组织。

(条例第三条第⼆款)企业所得税法第⼆条所称实际管理机构,是指对企业的⽣产经营、⼈员、账务、财产等实施实质性全⾯管理和控制的机构。

(条例第四条)相关⽂件参阅《国家税务总局关于境外注册中资控股企业依据实际管理机构标准认定为居民企业有关问题的通知》(国税发[2009]82号),需要注意此⽂件的适⽤范围和⽂件制定的背景,主要是为解决红筹上市国企分配股息的免税问题及返程投资框架下重复交税问题。

(⼆)⾮居民企业(1)依照外国(地区)法律成⽴且实际管理机构不在中国境内,但在中国境内设⽴机构、场所的企业。

(所得税法第⼆条第三款)纳税义务:应当就其所设机构、场所取得的来源于中国境内的所得,以及发⽣在中国境外但与其所设机构、场所有实际联系的所得,缴纳企业所得税。

(所得税法第三条第⼆款)企业所得税法第⼆条第三款所称机构、场所,是指在中国境内从事⽣产经营活动的机构、场所,包括:(⼀)管理机构、营业机构、办事机构;(⼆)⼯⼚、农场、开采⾃然资源的场所;(三)提供劳务的场所;(四)从事建筑、安装、装配、修理、勘探等⼯程作业的场所;(五)其他从事⽣产经营活动的机构、场所。

(条例第五条)⾮居民企业委托营业代理⼈在中国境内从事⽣产经营活动的,包括委托单位或者个⼈经常代其签订合同,或者储存、交付货物等,该营业代理⼈视为⾮居民企业在中国境内设⽴的机构、场所。

(条例第五条)企业所得税法第三条所称实际联系,是指⾮居民企业在中国境内设⽴的机构、场所拥有据以取得所得的股权、债权,以及拥有、管理、控制据以取得所得的财产等。

(条例第⼋条)(2)依照外国(地区)法律成⽴且实际管理机构不在中国境内,在中国境内未设⽴机构、场所,但有来源于中国境内所得的企业。

非居民企业所得税征收方式鉴定表(新)

合同号行次

主管税务机关审核意见1

2

3

4

5

6

核定征

收方式

成本费用核算情况纳税申报情况中文名称:

纳税人识别号:

英文名称:

项目纳税人自报情况账簿设置情况收入核算情况非居民企业所得税征收方式鉴定表

编号:青税18所非鉴( )- □按收入总额 □按成本费用 □按经费支出换算收入从事的行业

及适用的利润率

□承包工程作业、设计和咨询劳务,核定利润率( )

□管理服务,核定利润率( )

□其他劳务或劳务以外经营活动,核定利润率( )

履行纳税义务情况其他情况注:1、本表由非居民企业填写并报送主管税务机关;一式一份。

2、在符合情形的□内打“√”,在核定利润率“()”中填写具体的利润率。

负责人签章:

年 月 日负责人签章:税务机关受理意见:经办人:

(受理章) 年 月 日纳税人对征收方式的意见:经办人:申请采用企业所得税核定征收。

国税发〔2009〕6号 关于印发《非居民企业所得税汇算清缴管理办法》的通知_

国家税务总局关于印发《非居民企业所得税汇算清缴管理办法》的通知国税发〔2009〕6号各省、自治区、直辖市和计划单列市国家税务局,广东省和深圳市地方税务局:为贯彻实施《中华人民共和国企业所得税法》及其实施条例,规范非居民企业所得税汇算清缴工作,税务总局制定了《非居民企业所得税汇算清缴管理办法》,现印发给你们,请遵照执行。

执行中发现的问题请及时反馈税务总局(国际税务司)。

附件:1.非居民企业所得税汇算清缴涉税事宜通知书(据实申报企业适用)2.非居民企业所得税汇算清缴涉税事宜通知书(核定征收企业适用)3.非居民企业汇总申报企业所得税证明4.非居民企业所得税应纳税款核定通知书国家税务总局二○○九年一月二十二日非居民企业所得税汇算清缴管理办法为规范非居民企业所得税汇算清缴工作,根据《中华人民共和国企业所得税法》(以下简称企业所得税法)及其实施条例和《中华人民共和国税收征收管理法》(以下简称税收征管法)及其实施细则的有关规定,制定本办法。

一、汇算清缴对象(一)依照外国(地区)法律成立且实际管理机构不在中国境内,但在中国境内设立机构、场所的非居民企业(以下称为企业),无论盈利或者亏损,均应按照企业所得税法及本办法规定参加所得税汇算清缴。

(二)企业具有下列情形之一的,可不参加当年度的所得税汇算清缴:1.临时来华承包工程和提供劳务不足1年,在年度中间终止经营活动,且已经结清税款;2.汇算清缴期内已办理注销;3.其他经主管税务机关批准可不参加当年度所得税汇算清缴。

二、汇算清缴时限(一)企业应当自年度终了之日起5个月内,向税务机关报送年度企业所得税纳税申报表,并汇算清缴,结清应缴应退税款。

(二)企业在年度中间终止经营活动的,应当自实际经营终止之日起60日内,向税务机关办理当期企业所得税汇算清缴。

三、申报纳税(一)企业办理所得税年度申报时,应当如实填写和报送下列报表、资料:1.年度企业所得税纳税申报表及其附表;2.年度财务会计报告;3.税务机关规定应当报送的其他有关资料。

国税发[2010]19号文

![国税发[2010]19号文](https://img.taocdn.com/s3/m/7f563b47e45c3b3567ec8b42.png)

国家税务总局关于印发《非居民企业所得税核定征收管理办法》的通知国税发[2010]19号各省、自治区、直辖市和计划单列市国家税务局、地方税务局:为规范非居民企业所得税核定征收工作,税务总局制定了《非居民企业所得税核定征收管理办法》,现印发给你们,请遵照执行。

执行中发现的问题请及时反馈税务总局(国际税务司)。

非居民企业所得税核定征收管理办法第一条为了规范非居民企业所得税核定征收工作,根据《中华人民共和国企业所得税法》(以下简称企业所得税法)及其实施条例和《中华人民共和国税收征收管理法》(以下简称税收征管法)及其实施细则,制定本办法。

第二条本办法适用于企业所得税法第三条第二款规定的非居民企业,外国企业常驻代表机构企业所得税核定办法按照有关规定办理。

第三条非居民企业应当按照税收征管法及有关法律法规设置账簿,根据合法、有效凭证记账,进行核算,并应按照其实际履行的功能与承担的风险相匹配的原则,准确计算应纳税所得额,据实申报缴纳企业所得税。

第四条非居民企业因会计账簿不健全,资料残缺难以查账,或者其他原因不能准确计算并据实申报其应纳税所得额的,税务机关有权采取以下方法核定其应纳税所得额。

(一)按收入总额核定应纳税所得额:适用于能够正确核算收入或通过合理方法推定收入总额,但不能正确核算成本费用的非居民企业。

计算公式如下:应纳税所得额=收入总额×经税务机关核定的利润率(二)按成本费用核定应纳税所得额:适用于能够正确核算成本费用,但不能正确核算收入总额的非居民企业。

计算公式如下:应纳税所得额=成本费用总额/(1-经税务机关核定的利润率)×经税务机关核定的利润率(三)按经费支出换算收入核定应纳税所得额:适用于能够正确核算经费支出总额,但不能正确核算收入总额和成本费用的非居民企业。

计算公式:应纳税所得额=经费支出总额/(1-经税务机关核定的利润率-营业税税率)×经税务机关核定的利润率第五条税务机关可按照以下标准确定非居民企业的利润率:(一)从事承包工程作业、设计和咨询劳务的,利润率为15%-30%;(二)从事管理服务的,利润率为30%-50%;(三)从事其他劳务或劳务以外经营活动的,利润率不低于15%。

企业所得税法中英对照

企业所得税法中英对照企业所得税法是中国的一部重要税法,对企业的纳税义务和纳税方式进行了规定。

下面是企业所得税法的中英对照:第一条为了规范企业所得税的征收管理,调节国民经济的结构,促进经济发展和社会进步,根据中华人民共和国宪法,制定本法。

Article 1: In order to regulate the collection and administration of corporate income tax, adjust the structure of the national economy, promote economic development and social progress, this law is formulated in accordance with the Constitution of the People's Republic of China.第二条本法所称企业所得税缴纳义务人,包括居民企业经营者和非居民企业经营者。

Article 2: The persons liable to pay corporate income tax referred to in this law include resident enterprise operators and non-resident enterprise operators.第三条企业所得税法调整政策适用期限由国务院规定。

Article 3: The adjustment period for corporate income tax laws and policies shall be determined by the State Council.第四条企业所得税的税款以以下应纳税所得额为计税依据:(一)所有权人取得的赢利;(二)其他经济利益,依照国务院税务主管机关的规定计征。

Article 4: The taxable income of corporate income tax is based on the following taxable income:(1) Profits obtained by owners;(2) Other economic benefits, as assessed according to the regulations of the tax authorities under the State Council.第五条企业所得税的税率为25%。

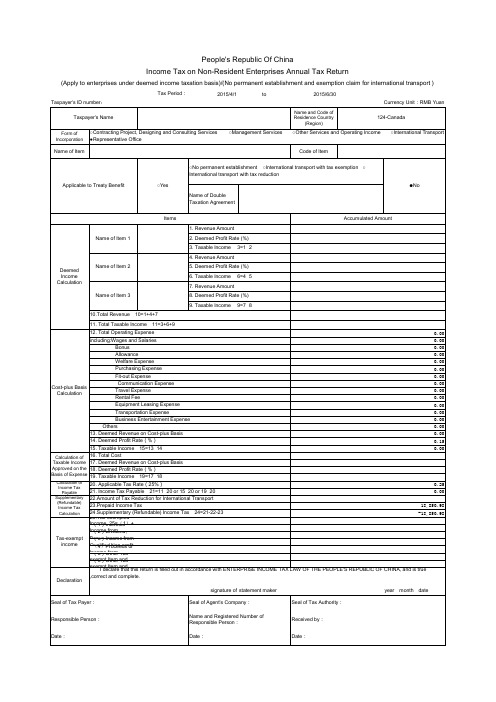

非居民企业所得税季度和年度纳税申报表中英文版

10.Total Revenue 10=1+4+7 11. Total Taxable Income 11=3+6+9 12. Total Operating Expense 0.00 including:Wages and Salaries 0.00 Bonus 0.00 Allowance 0.00 Welfare Expense 0.00 Purchasing Expense 0.00 Fit-out Expense 0.00 Communication Expense 0.00 Travel Expense 0.00 Rental Fee 0.00 Equipment Leasing Expense 0.00 Transportation Expense 0.00 Business Entertainment Expense 0.00 Others 0.00 13. Deemed Revenue on Cost-plus Basis 0.00 14. Deemed Profit Rate(%) 0.15 15. Taxable Income 15=13×14 0.00 16. Total Cost 17. Deemed Revenue on Cost-plus Basis 18. Deemed Profit Rate(%) 19. Taxable Income 19=17×18 20. Applicable Tax Rate(25%) 0.25 21. Income Tax Payable 21=11×20 or 15×20 or 19×20 0.00 22.Amount of Tax Reduction for International Transport 23.Prepaid Income Tax 18,850.98 24.Supplementary (Refundable) Income Tax 24=21-22-23 -18,850.98 25.Tax-exempted Income 25= (1)+(2)+(3)+(4)+(5)+(6) (1)Interests Income from Government Bond (2)Dividend, Bonus Income from Resident Enterprises (3)Income from Qualified Non-profit Organizations (4)Proceeds or Income from Acquisition of Local Government Bond Interest (5)Other Tax-exempt Item and Code (6)Other Tax-exempt Item and Code I declare that this return is filled out in accordance with ENTERPRISE INCOME TAX LAW OF THE PEOPLE'S REPUBLIC OF CHINA, and is true ,correct and complete. signature of statement maker Seal of Tax Payer: Responsible Person: Date: Seal of Agent's Company: Name and Registered Number of Responsible Person: Date: Seal of Tax Authority: Received by: Date: year month date

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Measures for Administration of the Levy of Income Tax on Non-tax-resident Enterprises by Assessment非居民企业所得税核定征收管理办法Issue: June 2010CLP Reference: 3230/10.02.20PRC Reference:国税发 [2010] 19号Promulgated: 20 February 2010Effective: 20 February 2010(Issued by the State Administration of Taxation on, and effective as of, February 20 2010.)Guo Shui Fa [2010] No.19Article 1:These Measures have been formulated pursuant to the PRC Enterprise Income Tax Law (the Enterprise Income Tax Law) and its Implementing Regulations and the PRC Law on the Administration of the Levy and Collection of Taxes (the Tax Collection Law) in order to regulate the assessment and levy of enterprise income tax on non-tax-resident enterprises.(国家税务总局于二零一零年二月二十日发布施行。

)国税发 [2010] 19号第一条为了规范非居民企业所得税核定征收工作,根据《中华人民共和国企业所得税法》(以下简称企业所得税法)及其实施条例和《中华人民共和国税收征收管理法》(以下简称税收征管法)及其实施细则,制定本办法。

Article 2:These Measures apply to the non-tax-resident enterprises specified in the second paragraph of Article 3 of the Enterprise Income Tax Law. The means for assessing the enterprise income tax of the resident representative offices of foreign enterprises shall be handled in accordance with relevant provisions.第二条本办法适用于企业所得税法第三条第二款规定的非居民企业,外国企业常驻代表机构企业所得税核定办法按照有关规定办理。

Article 3:A non-tax-resident enterprise shall keep account books in accordance with the Tax Collection Law and relevant laws and regulations, keep its accounts and do its accounting based on lawful and valid documents, accurately calculate its taxable income based on the principle of the matching of the functions it actually performs and the risks that it bears, and truthfully file and pay enterprise income tax.第三条非居民企业应当按照税收征管法及有关法律法规设置账簿,根据合法、有效凭证记账,进行核算,并应按照其实际履行的功能与承担的风险相匹配的原则,准确计算应纳税所得额,据实申报缴纳企业所得税。

Article 4:If a non-tax-resident enterprise has incomplete account books, there are gaps in its documentation that make the checking of its accounts impossible or the accurate calculation and truthful filing of its taxable income is not possible due to another reason, the tax authority shall have the authority to assess its taxable income by one of the following methods.第四条非居民企业因会计账簿不健全,资料残缺难以查账,或者其他原因不能准确计算并据实申报其应纳税所得额的,税务机关有权采取以下方法核定其应纳税所得额。

(1) Assessment of taxable income based on total revenue: applicable to non-tax-resident enterprises that can accurately calculate their income or deduce their total revenue by reasonable means but cannot accurately calculate their costs and expenses. The formula therefor is as follows:(一)按收入总额核定应纳税所得额:适用于能够正确核算收入或通过合理方法推定收入总额,但不能正确核算成本费用的非居民企业。

计算公式如下:taxable income = total revenue × profit rate determined by the tax authority.应纳税所得额=收入总额×经税务机关核定的利润率(2) Assessment of taxable income based on costs and expenses: applicable to non-tax-resident enterprises that can accurately calculate their costs and expenses but cannot accurately calculate their total revenue. The formula therefor is as follows:(二)按成本费用核定应纳税所得额:适用于能够正确核算成本费用,但不能正确核算收入总额的非居民企业。

计算公式如下:taxable income = total of costs and expenses ÷ (1 – profit rate determined by the tax authority) × profit rate determined by the tax authority.应纳税所得额=成本费用总额/(1-经税务机关核定的利润率)×经税务机关核定的利润率(3) Assessment of taxable income based on revenue converted from operational expenditures: applicable to non-tax-resident enterprises that can accurately calculate their operational expenditures but cannot accurately calculate their total revenue and their costs and expenses. The formula therefor is as follows:(三)按经费支出换算收入核定应纳税所得额:适用于能够正确核算经费支出总额,但不能正确核算收入总额和成本费用的非居民企业。

计算公式:taxable income = total of operational expenditures ÷ (1 – profit rate determined by the tax authority – business tax rate) × profit rate determined by the tax authority.应纳税所得额=经费支出总额/(1-经税务机关核定的利润率-营业税税率)×经税务机关核定的利润率Article 5:A tax authority may assess a non-tax-resident enterprise’s profit rate based on the following rates:第五条税务机关可按照以下标准确定非居民企业的利润率:(1) for enterprises engaging in project contracting, design and consulting services, a profit rate of 15% to 30%;(一)从事承包工程作业、设计和咨询劳务的,利润率为15%-30%;(2) for enterprises providing management services, a profit rate of 30% to 50%; and(二)从事管理服务的,利润率为30%-50%;(3) for enterprises providing other services or engaging in business activities other than the provision of services, a profit rate of not less than 15%.(三)从事其他劳务或劳务以外经营活动的,利润率不低于15%。

If the tax authority has evidence to believe that a non-tax-resident enterprise’s actual profit rate is markedly higher than the foregoing rates, it may assess its taxable income based on a profit rate higher than the foregoing rates.税务机关有根据认为非居民企业的实际利润率明显高于上述标准的,可以按照比上述标准更高的利润率核定其应纳税所得额。