FinancialAccounting2th财务会计ReviewCases全套复习案例

Financial Accounting第二章

Equity

Debit / Dr. Credit / Cr.

N o r m a l B a la n c e

Normal Balance

C h a p te r 3 -2 4

Chapter 3-25

2-7

Debits and Credits

If Debit amounts are greater than Credit amounts, the account will have a debit balance.

2-19

Debit/Credit Rules Question

Debits: a. increase both assets and liabilities. b. decrease both assets and liabilities. c. increase assets and decrease liabilities. d. decrease assets and increase liabilities.

A ssets

D e b it / D r . C r e d it / C r .

N o r m a l B a la n c e

C h a p te r 3 -2 3

2-6

The Account

Debit and credit procedure

L ia b ilit ie s

D e b it / D r . C r e d it / C r .

Formal recording system “Double-entry accounting system”

“We are going to record (register) transactions in books” (=Bookeeping)

ch12Financial Accounting 2th财务会计

received FMarket i n t e r e s t rate

Transparency 12-17

Market Value of Bonds

There are two cash inflows associated with bonds:

Transparency 12-15

Price of Bond

Bond prices f o r both new issues and existing bonds are quoted as a percentage of the face value of the bond, which i s usually $1,000.

Unsecured notes – Financial instruments t h a t r e l y on the bor r ower ’ s general c r e d i t worthiness for their repayment.

Transparency 12-14

Rights of Borrower and Lender in Default

Normal Rights of Borrower and Lender

Callable bonds are subjected t o retirement a t a s t a t e d d o l l a r amount p r i o r t o maturity a t the option of the issuer (i.e.,borrower).

《财务会计英语》课件

Definition of Financial Accounting

Summary: Financial Accounting is a process of recording, categorizing, and summarizing financial transactions and events in a systematic manager to provide information about the financial position, performance, and changes in the financial position of an entity to interested parties

Cost calculation and expense allocation

Summary: Formulation of cost sharing standards Detailed description: Develop reasonable cost allocation standards and allocate indirect expenses to specific cost objects. The formulation of cost sharing standards should consider relevant factors, such as direct labor, machine hours, etc., to ensure the rationality and accuracy of cost sharing. At the same time, the allocation standards should be regularly evaluated and adjusted to reflect changes in the company's business and the actual occurrence of expenses.

财务会计英语unit2

Section 1 Accounting for Cash

Financial Accounting English (Second Edition)

LOGO

Unit 2

Assets

Financial Accounting English (Second Edition)

Contents

Section 1 Accounting for Cash

Section 2 T Accounting for Receivables

Section 3 Inventory Accounting Section 4 Accounting for Non-current Assets

Financial Accounting English (Second Edition)

Section 1 Accounting for Cash

A second cash control practice is to require that all cash receipts be deposited daily in bank accounts. A third cash control practice is to require that all cash expenditures (except those paid out of petty cash) be made with pre-numbered checks and filed in sequence.

Example 2.3 In the next month, on February6tobe exact, Mr. Lott borrowed$400 for an investigation travel. And a week later, on February 14, he returned and settled his traveling expense. His actual expenditure was $300, the remaining $100 was returned. The entries on the different date would be:

财务会计(英文版·原书第5版)ch02

See notes page for discussion

Chapter 2-12

SO 2 Define debits and credits and explain their use in recording business transactions.

Assets and Liabilities

Each transaction must affect two or more accounts to keep the basic accounting equation in balance. Recording done by debiting at least one account and crediting another. DEBITS must equal CREDITS.

Assets

Debit / Dr.

Credit / Cr.

Normal Balance

Chapter 3-23

Liabilities

Debit / Dr.

Credit / Cr.

Chapter 3-24

Chapter 2-13

Normal Balance

Assets - Debits should exceed credits. Liabilities – Credits should exceed debits. The normal balance is on the increase side.

Debit / Dr.

Credit / Cr.

Chapter 3-26

Normal Balance

Expense

Debit / Dr.

Credit / Cr.

Normal Balance

财务会计英语词汇 (financial accounting terms)

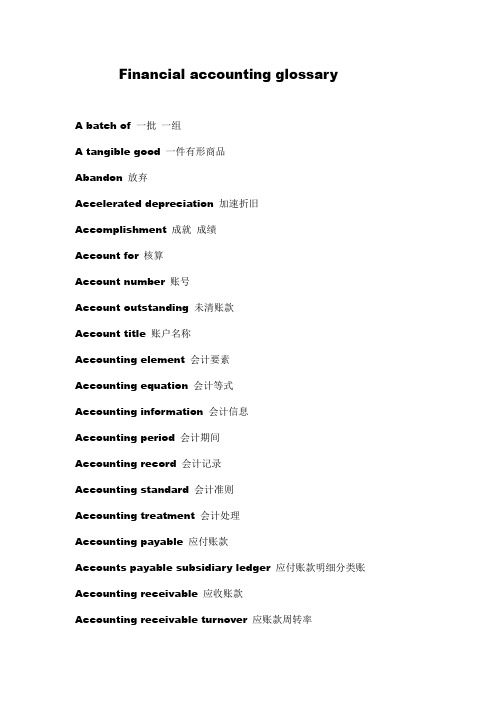

Financial accounting glossaryA batch of 一批一组A tangible good 一件有形商品Abandon 放弃Accelerated depreciation 加速折旧Accomplishment 成就成绩Account for 核算Account number 账号Account outstanding 未清账款Account title 账户名称Accounting element 会计要素Accounting equation 会计等式Accounting information 会计信息Accounting period 会计期间Accounting record 会计记录Accounting standard 会计准则Accounting treatment 会计处理Accounting payable 应付账款Accounts payable subsidiary ledger 应付账款明细分类账Accounting receivable 应收账款Accounting receivable turnover 应账款周转率Accrual accounting 权责发生制会计Accrual basis of accounting 权责发生制会计制度Accrue 应计增值Accrued expense 应计费用Accrued liability 应计负债Accrued revenue 应计收入Accumulated 积累的Accumulated depreciation 累计折旧Accumulated earnings 累计收益Acid-test ratio 酸性测试比率,速动比率Acquisition 取得Additional paid-in capital溢缴资本Adjust 调节调账Adjusting entry 调账分录Administrative expense 管理费用行政费用办公费用Administrative salary expense 行政管理工资费用Admission and withdrawal of partners 合伙人的入伙及撤伙Admission by contribution of assets 通过捐缴资产的方式入伙Admission by purchase of interest 通过购买权益的方式入伙Admission of a new partner 新合伙人的入伙Admit 允许进入接受Advance payment 预付款Advertising expense 广告费用Agent 代理,代理人Aging method 账龄法Allocation of the cost 成本的分配Allowance for bad debts 坏账准备Allowance method 备抵法American express 美国运通卡Amortization 摊销摊提分期偿还Amortization expense 摊销费用Amortize 摊销摊提Amount to(在数量上) 达——Analysis period 报告期分析期Analytical tool 分析工具Anticipate 期望Apparent 明显的Apparent 明显的Applicable 实际的适用的Applicable expense 使用费用Appraisal 估价鉴定Arise from 产生于,因—-而造成Arrive at 得出As of 在或直到(某一时间)Aspect 方面Assess 评估,评价Asset acquisition 资产的取得Asset 资产Auditor 审计师Authorized stock 核定股份Available-for-sale securities 可供出售的债权Average 平均的使平均Average days inventory on hand 平均库存天数Average days sale uncollected 应收销售款平均收现天数bad debt 坏账呆账bad debt expense 坏账费用呆账费用balance 平衡余额balance 使平衡balance sheet 资产负债表bank deposit 银行存款bank reconciliation 银行往来调节银行往来对账bank service charge 银行手续费银行服务费bank statement 银行对账单bankrupt 破产的bankruptcy 破产倒闭bargain price 廉价处理价;交易价格成交价格base amount 基数base period 基期basket purchase 一揽子购买bear no connection with 与——没有联系beauty parlor 美容院beginning balance 期初余额beginning inventory 期初存货,期初库存benefit from 从——受益bill账单billing 开单出具账单board of directors 董事会bond discount z债券折价bonds payable 应付债券bonus 红利补贴津贴bonus to partner 补贴合伙人book 账簿账册book 接受——的预定、订购book value 账面价值bookkeeper 簿记员book-to-tax difference 财税之差business 企业business enterprise 商业企业企业机构business entity 企业实体商号business operation 企业机构商业企业business performance 经营活动营业活动by note 签发票据calculate 计算call for 要求call privilege 赎回权利callable bond 可通赎回债券可赎回债券cancelled check 已注销支票付讫支票capital 资本capital acquisition 资本取得capital balance 资本余额capital balance ratio 资本额比例capital contribution 资本摊缴capital expenditure 资本支出基本建设支出capital lease 资本租赁capital stock 股本capital structure 资本结构capitalize 使资本化变为资本caption 标题carry on 经营cash 现金cash basis accounting 现金收付制会计cash disbursement 现金支出cash discount 付现折扣cash dividend 现金股利现金股息cash equivalent 现金等价物cash expenditure 现金支出cash inflow 现金流入cash outflow 现金流出cash payment 现金支付现金支出cash receipt 现金收入现金所得cash receipt journal 现金收入日记账cash sale 现金销售现销cashier 出纳员categorize 分类category 类别(n)center on 以——为中心围绕certificate 凭证证明书certificate of deposit 存折存款单challenging 挑战性的changing hands 易手转手chart of accounts 会计科目表chronological record 序时记录clarify 使清楚易懂澄清classification 分类classified income statement 分类损益表closing entry 结账分录collect 收账收款collection 收款收账commission 佣金commission expense 佣金费用commitment 承付款项承诺付款数common equivalents 普通股等价物,相当于普通股的股票common stock 普通股票common-size analysis 统一度量式分析,百分比分析,共同比例分析总体结构分析common-size balance sheet 统一度量式(只用百分比,不用金额)资产负债表,通用型资产负债表,总体结构资产负债表,共同比例资产负债表,百分比资产负债表,共同量资产负债表common-size comparative balance sheet 统一度量式比较资产负债表,百分比比较资产负债表common-size comparative income statement 统一度量式比较损益表,百分比比较损益表common-size financial statement统一度量式报表,总体结构报表,共同比报表common-size statement 统一度量式报表comparative balance sheet 比较资产负债表comparative financial statement 比较财务报表complete 完成使完整complex 复杂的complicated 复杂的component 成分构成组成部分computerized accounting statement 电算化会计制度connote 含有——意义consent 同意conservation concept 保守概念consignee 承销人代售人consignee payable 应付承销人账款应付代售人账款consignment 寄售consignor 寄售人consignor payable 应付寄售人账款constitute 构成组成construction in program 在建工程consumption 消费context 上下文背景环境contingency 或有事项continuous existence 持续经营contra account 对销账户,抵消账户contractor 承包人承包商conversion privilege 兑换特权convert 改变成convertible 可转换的convertible bond 可转换债券co-owner 共有者,共同所有者co-ownership of property 共有财产copyright 版权著作权corporate (a)公司的(v)组建股份公司corporate accounting 公司会计corporate tax 公司所得税企业所得税corporation 股份公司cost accounting 成本会计cost available for sale 可销成本cost measurement 成本核定费用计量cost of goods available for sale 可销成本cost of goods manufactured 产品成本,制成成本cost of goods purchased 进货成本采购成本cost of goods sale 销售成本cost of installment sales 分期付款销货成本cost-to-cost method 成本比例法,完工百分比法count 数,盘点coupon bond 付息票(公司)债券credit 贷方贷记credit 信贷贷款credit balance 贷方余额credit card sales 信用卡销售credit card service expense 信用卡服务费credit purchase 赊购credit sales 赊销credit term 信用条件creditor 债权人criteria 标准尺度critical 关键的,至关重要的cross-reference 交叉检索current agreed value 现行的意见一致的价值current asset 流动资产current debt 流动负债current financial operation 本期财务运转current liability 流动负债current obligation 本期债务current period 当期,本期current portion of a long-term debt 一年内到期的长期负债current ratio 流动比率customer ratio 用户收费率,顾客运费率cut-off 盘存debenture 信用债券debit 借方借记debit balance 借方余额debit entry 借方分录debt ratio 负债比率debt securities 债务证券declare 通告(分红)deduct 扣除deduction (扣除)defective goods 次品deferred gross profit 递延毛利deferred income tax 递延所得税delivery expense 运费交货费用delivery wages expense 交货工资费用delivery trucks 运输车辆deposit in transit 在途存单deposit slip 存款单存款收据depositor’s books 储户的账册depreciation 折旧depreciation expense 折旧费用detect 察觉查出difference 差差额direct cost 直接成本direct labor cost 直接人工成本direct matching 直接配比direct material 直接材料直接原料direct method 直接法direct write-off method 直接冲销法director 董事disburse 支付disbursement 支出支付discount 贴息折价折扣discount on bound 债券折价discount period 折扣期间贴现期间discount sale 折价销售display 展示disposal 处理清理dissolution (n)散伙解散dissolve (v)散伙解散distinguish 区别divergent 不同的divide into 分成——divide——by——(用——除以——)dividend 红利股息股利dividend revenue 股息收入红利收益dividend payable 应付股息应付股利division of labor分工dollar amount 金额dollar change 金额变化double-entry system 复式会计制度drawing 个人提取(账户)due (票据等)到期的duration 期限earnings per share 每股收益effective interest method 实际利息(计算)法efficiency 效率efficiency ratio 效能比率效率比率efforts-expended method 已付努力法elaborate 详尽阐述elaboration 详尽说明electricity bill 电费账单employee training program 员工培训计划endanger 危及ending balance 期末余额ending capital 期末资本ending inventory 期末存货end-user 最终用户最终消费者enter into 签订entitle to 给——权利给——资格entry 分录equity accounting 权益会计equity ratio 业主权益比率equity securities 权益证券establish 建立evaluate 评估估价exceed 超过excessive 过分的excise tax 消费税exclusive right 专营权专有权executive 行政管理人员expenditure 开支expense 费用计入费用的账户expense recognition 费用的确定external 外部的(internal内部的)extraordinary gain 非常收益extraordinary item (收入或费用)非常项目,特殊项目extraordinary loss 非常损失意外损失face interest rate 票面利率face value 面值factor 系数率fair market value 公允市价公平市价fair presentation 公允表达FASB(financial accounting standard board)财务会计准则委员会Feasible 可行的Federal income tax 联邦所得税Fee 手续费服务费酬金Fees income tax 联邦所得税FICA(federal insurance contribution act)联邦社会保险法FIFO(first in first out)先进先出法Financial ability 财力资金Financial accounting 财务会计Financial analyst 财务分析家Financial condition 财务状况Financial expense 财务费用Financial institution 金融机构Financial management 财务管理Financial position 财务状况Financial report 财务报告Financial statement 财务报表Financial statement analysis 财务报表分析Financial activity 筹资活动Finished goods inventory 产成品库存制成品库存Finished product 制成品产成品Fit in 适于——Fixed assets 固定资产Fluctuate 浮动Foreign currency translation adjustment 外币换算调整Format 形式Formation partnership 合伙企业的组成Formula 公式Formulate 订立Forward 转递转交Franchise 专营权特许经营权Fraud 欺骗欺诈Frequently 频繁的Full cost 全部成本Funding by bond 债券筹资Funding by stock 股票筹资GAAP(generally accepted accounting principles)公认会计原则Gain on sale of land 销售土地所得Gain or loss of sale asset 资产变卖损益Garment factory 服装厂General and administrative cost 总务及管理成本General and administrative expense 总务及管理费用General expense 管理费用General journal 普通日记账General ledger 总账Generate 产生Goods in process 在产品在制品Goodwill 商誉Government securities 政府债券Gravel deposit 砾石矿Grocery store 杂货店Gross 总的毛的Gross amount 总计总额毛计Gross margin 毛利Gross profit 毛利总利润Guideline 标准准则Hardware store 五金商店Have something to do with 与——有关Held-to-maturity securities 持至到期的债券Historical cost 历史成本Hold back 阻挡Horizontal analysis 水平分析横向分析Hours of labor 工时人工小时Human resource management 人力资源管理Identical 同样的Identifiable 可辨认的可识别的Identify 认出确认Idle cash 闲置现金游资Idle fund 闲置资金游资Imprecise 不精确的不准确的In desperate need 急需In monetary term 用货币术语来说In proportion to 按比例In regard to 关于In that 由于因为Income before tax 税前收入Income from main operations 主营业务收入Income from other operations 其他业务收入Income statement 损益表Income summary 汇总账户损益汇总账户Income tax 所得税Income tax accounting 所得税会计Income tax effect 所得税税收效应Income tax law 所得税法Income taxes expense 所得税费用Income taxes on operations 营业所得税Incompetent 不称职的不能胜任的Incorporation 组成公司组建公司Incredible 难以置信的Incur 招致遭受Incurrence of a cost 成本的发生Indirect cost 间接成本Indirect method 间接成本法Indirect production cost 间接生产成本Industry 行业Inevitable 不可避免的Inflationary 通货膨胀Inflow流入Initial investment 起初投资Input measure 投入测算法投入核算法、Inspector 检验员检察员Installment 分期付款分期收款Installment accounts receivable 应收分期账款Installment sales 分期付款销售Insurance expense 保险费Insurance premium 保险费Intangible asset 无形资产Intangible service 无形的服务Intend as (为——而)准备,打算使——成为Intended meaning 原来的意思原有目的Interest basis 利息法按利息分配损益的方法Interest cost 利息成本Interest payable 应付利息Interest period 计息期Interest rate 利率Interest-bearing note 附息票据Interest-free 无息的Internal 内部的Interpretation 解释Intuition 直觉,直觉行为Inventory 存货库存Inventory accounting 存货核算存货会计Inventory cost flow 库存成本流转Inventory cut-off 存货盘存存货盘点Inventory on consignment 寄销存货Inventory purchase 采购存货Inventory shrinkage 存货损耗Inventory taking 盘存盘点存货Inventory turnover 存货周转率Investing activity 投资活动Investing revenue 投资收益Invoice 发票Issuance 发行Issue bond and notes 发行债券及票据Issue debt 放债Issued stock 已发行股份Janitor 看门人Journal entry 日记账分录Journal 日记账Journalizing 登陆日记账Junk bond 地基债券Label 标记归类Labor dollar 工资Labor hour 工时Labor negotiation 劳动谈判劳资谈判Law firm 律师事务所Layer 层面Lease 租赁Lease obligation 租赁债务Lease payment 租赁付款Lease term 租赁期Lessee 承租人Leaser 出租人Leger 总账Legal formality 法律手续法律形式Lending and collecting loans 放贷及收贷Less 减去Liability 负债License 执照LIFO(last in first out) 后进先出法Limited liability 有限责任Limited life 有限的经营期限Liquid 流动的易转换成现款的Liquidation 清算清偿(企业的)资产清理Liquidity 流动性Liquidity ratio 流动性比率List price 零售价目录价格List sale price 目录销售价Long-lived asset 长期资产Long-run 长期的Long-standing 长期的Long-term asset 长期资产Long-term construction contract 长期建筑合同Long-term investment 长期投资Long-term liability 长期负债Long-term obligation 长期债务Loss on write-down of inventory 存货减记损失Lower of cost or market rule 成本与市场孰低法Lubricating oil 润滑油Lump-sum payment 一次总算支付Major operation 主营业务Make clear 澄清阐述Make loans to other entities 向其他实体放贷Make out 得出完成Manipulated 易受操控的Manufacturing business 制造业制造型企业Manufacturing company 制造公司Manufacturing cost 制造成本生产成本Manufacturing overhead (间接)制造费用Market interest rate 市场利率Market price 市场价格市值Marketable 适合市场销售的销售好的可市场买卖的Marketable securities 有价证券可转售证券适销证券MasterCard 万事达卡Matching concept 配合概念配比概念Matching principle 配比原则Matching rule 配比规则Material handler 材料员Material inventory 物资库存(原)材料盘存Mathematical 数学Maturity value 到期值Merchandise 商品Merchandising business 商业企业流通业Merchandising inventory 商品存货库存商品商品盘存Merchandiser 商人商业企业Merit 优点长处Mileage 英里数里程数Mineral deposit 矿藏Minus 减减去Miscellaneous expense 杂项费用,其他费用,杂项开支Modifier 修饰语,修饰成分Money order 汇款单Monitor 监视监控Monthly statement 月结单Mortgage agreement 抵押协议Mortgage bond 抵押债券Mortgage payable 应付抵押账款Multiple 倍倍数Multiply——by (用——乘以)Negative amount 负值Negative figure 负数负值Negatively 负面的Net asset 净资产Net cash flow 现金净流量Net change 变动净额Net effect 净效果Net income 净收入Net profit after income taxes 税后净利润Net purchase 购入净值进货净额Noncash asset 非现金资产Noncurrent 非流动的Nonoperating gains and losses 非营业性利得和损失Nonproduction cost 非生产性成本No-par stock 无面值股票Notion 观念概念NSF(nonsufficient fund)check 存款不足的支票Number of share 股数Number of shares of stock outstanding 在外股票的股数Objectively 客观的Obligation 债务义务责任Office salaries expense 办公室工资费用Office supplies expense 办公室材料费用Offset against 抵消Oil well 油井On account 赊销赊购赊账On credit 赊账One decimal place 一位小数小数点后一位Operating activity 经营活动Operating asset 营业资产Operating cycle 营业循环营业周期经营周期Operating expense 营业费用Operating income 营业收入营业收益营业所的Operating lease 营业租赁Order 订单Other accounts receivable 其他应收账款Other than (除了——除非——)Outflow 流出Output measure 产量测算法产量核算法Outstanding check 未兑现的支票Outstanding stock 流通在外的股票Over the long run 从长远的观点来看长期的Overall 综合的全部的包括一切的Overhaul 彻底检修大修Overhead cost 制造成本间接成本管理费用Overstate 多计Overstatement 过多的陈述多计多报Over-the-counter 柜台上的Overtime coffee 加班咖啡加班餐饮费Owner’s equity 所有者权益Owner’s interest 所有者权益P.R(posting reference)过账证明Packing material 包装材料Par 面值Participation参与Partnership 合伙企业Partnership accounting 合伙会计Partnership agreement 合伙契约Part-time help 非全日助手Par-value stock 有面值的股票Past-due 过期的逾期的Patent 专利Payment of dividends 支付股利Payroll 工资表工资单工资额Percent change 百分比变化Percentage-of-completion accounting 完工百分比核算法Performance 绩效业绩成果Period cost 期间成本Periodic inventory method 实地盘存法Periodic payment 定期付款定期支付Perpetual inventory method 永续盘存法Pertain to 属于Petty cash 零用钱小额现金Petty cash fund 领用基金Physical quantity 实物数量Pocket 据为己有Polling 集资向共同基金提供资金Positive amount 正值Posting 过账Precede 在——前面加上在——前面先说Preference 偏爱Preferred dividend 优先股股息Preferred stock 优先股Premium 溢价Pre-numbered check 有序列号的支票Prepaid expense 预付费用Prepaid insurance 预付保险费Prepaid rent 预付房租Prepare 编制(报表等)Present 提交展示Pretax book income 税前账面收入未扣税账面所得Previous 先前的以前的Price 定价Primary income statement 基本损益表Principle 本金Principle collection 收回本金Prior 优先的Proceeds 进款收入Product cost 成品成本Product selling business 销售产品的企业Product unit cost 单位产品成本Productive 富有成效的得益的Profit 利润Profit and lost distribution 损益分配Profit margin 净利比率Profit reporting procedure 利润报告程序Profitability 获利能力盈利能力Profitability ratio 盈利率Profitable operation 获取利润的经营Progress billing 进度账单阶段账单Progress billing on construction contract 建筑合同阶段账单Promissory note 期票本票Prompt payment 立即付款Property tax 财产税Property tax payable 应付财产税Proprietorship 独资企业Prospect 前景Provisions 条款规定Prudent 谨慎的Public utilities 公用事业股份公司Purchase 进货采购Purchase return 购货退回进货退回Purchase journal 进货日记账Purchase on account 赊购Pursue 追求Quick assets 速动资产Quick ratio 速动比率、R&D(research and development) 研发实验室Ratio analysis 比率分析Raw material 原料Real estate 不动产房地产Realizable 可实现的Realization concept 收益实现概念Realization of expense 费用的确定Reconcile 调节使协调使一致Redeem 赎回买回Redeemable preferred stock 可赎回优先股Reflect 折射反射反应Regardless of 不管不顾Registered bond 记名债券Regulate 管理控制Regulator 政府管理者Reimbursable 可收回的可补偿的Reimbursement 偿还偿付付还Relevant 相关的Rely on 依靠依赖Render 提供Rent expense 房租费用租赁费用Rent revenue 租赁收入Repairs and maintenance expense 维护费用Repay 偿还Repetitive 重复的Research and development cost 研发成本Restrictive 限制性的约束性的Result from (因——而)产生发生Retail 零售Retail store 零售店Retained earning 留存盈余Retained earnings statement 留存盈余表Return on total assets 总资产收益率Revenue 收入收益Revenue recognition 收入的确定营业收入的确定Revenue-producing operating 获取总收入的经营Review 回顾Round 把——四舍五入Sacrifice 牺牲Safeguard 保护保障Salaries payable 应付薪金应付工资Salary basis 工资法Salary-interest basis 工资利息法Sales contract 销售合同Sales discount 销售折扣Sales on account 赊销Sales returns and allowance 销货退回及折让Sales salaries expense 销售工资费用Sales tax 销售税营业税Salvage value 残值Secured bond 有保(公司)债券Self-manufactured semi-finished product 自制半成品Selling and administrative expense 销售及管理费用Selling cost 销售成本Selling expense 销售成本Semiannual 半年,每半年的Serial bond 分期偿还(公司)债券,序列(公司)债券Service business 服务业Service enterprise 服务型企业Service firm 服务性企业Settle 结算Share 股票Shareholder investment 股东投资Shares outstanding 流通在外的股票,发行在外的股票Shipping expense 运费Shipping supplies expense 运输材料费Short-term asset 短期资产Short-term investment 短期投资Showroom 样品间展厅Skepticism 怀疑态度Slippery 把握不准的不稳定的不明确的Solvency analysis 偿付能力分析Solvency ratio 偿付比率Special delivery service 特快专递服务Special journal 特种日记账Special identification method 个别辨认法Specify 明确说明详细的说明Spice 香料调味料Stated ratio 设定比例固定比例Statement of cash flow 现金流量表Sticker price 卷标价格Stock 股票Stock certificate 股权证Stock issuance 股票的发行Stockholder 股东,股票持有者Stockholders’ equity 股东权益Stock-option 认股权购股选择权Stockroom personal 仓库管理人员库管Straight-line amortization 直线摊销Straight-line depreciation method 直线折旧法Straight-line method 直线法Subscriber 订阅者Subscription 订阅订购Subsequent payment 分期缴付Subtotal 小计Subtract 减去Successive 连续的Sufficient 足够的Suit 一套衣服Summarize 汇总Sundry 杂的多项的Supervisor 检察员监察员Supplement 补充Supplier 供货商Supplies 材料Synonym 同义词T account 丁字账户Take inventory 盘存Take preference over 对——具有优先权Tangible asset 有形资产Tax benefit 纳税利益Tax effect 课税效果税收效应Tax exemption 免税Tax rate 税率Taxable income 应纳税收入需纳税的收入Taxi fare 搭乘出租车费用Taxing authorities 税务部门Temporary account 临时账户Term bond 定期(公司)债券Term of consignment 寄售条款寄售条件The converse 相反的事物Timber tract 伐木道路Time deposit 定期存款Time-consuming 耗时的Title of account 账户名称To date 到现在为止到目前为止至今Total assets turnover 总资产周转率Trace 追溯查出找到Trade discount 商业折扣Transaction 会计事项Transfer 转账Transfer of ownership 所有权转让Traveling expense 差旅费Treasury bill 短期国国库券Treasury note (美)国库券Treasury stock 库存股票Uncertainty 不确定的事物Uncollectible (a)无法收回的(b)无法收回的账项Uncollectible account 坏账呆账Uncover 揭开——的盖子,暴露Understate 少计Understatement 不完全陈述不充分陈述少计少报Unearned revenue 预收收入递延收入Unexpected 意外的Uniform Partnership Act 《统一合伙条例》Unincorporated business 非股份制企业Union 工会Union dues 工会会费Unique 无比的独一无二的不寻常的Units-of-production depreciation method 产量单位折旧法Unlimited liability 无限责任Unregistered bond 无记名债券Unsecured bond 无担保债券Utility expense 公用事业费Utilities payable 应付公用事业费Utmost 最大的极度的Van 面包车微型车Vendor 卖主出卖人叫卖商Verification 核实验证Vertical analysis 垂直分析纵向分析VISA 维萨卡Void 作废的Voluntary association 自愿的联盟Weighted-average method 加权平均法Well-offness 好的境遇繁荣昌盛生意兴隆Withdraw (v)撤回撤资撤Withdrawal (n) 撤回撤资撤伙Withdrawal account 提取账户Withhold 预扣Withholding tax 预扣税款Work in process inventory 在制品盘存在产品存货Working capital 运营资本,流动资金Working capital ratio 运营资本比率Workmanship 工艺技艺做工Write-down 减记化减Zero-interest bond 无息债券。

大学财务会计专业英语教材

大学财务会计专业英语教材In recent years, the field of accounting has witnessed significant advancements and developments, necessitating comprehensive and up-to-date academic resources to meet the demands of students studying finance and accounting. With the increasing globalization of business and finance, proficiency in English is an essential skill for accounting professionals, particularly those specializing in financial accounting. Therefore, the creation of a specialized English textbook for university-level finance and accounting students is of great importance.Chapter 1: Introduction to Financial Accounting1.1 The Role and Importance of Financial Accounting1.2 Basic Concepts and Principles in Financial AccountingChapter 2: Preparation of Financial Statements2.1 The Accounting Equation2.2 Recording Transactions: The Double-Entry System2.3 The Chart of Accounts2.4 Journalizing and Posting Transactions2.5 Trial BalanceChapter 3: Income Statement and Statement of Financial Position3.1 Understanding Income Statement3.2 Income Statement Components3.3 Statement of Financial Position: Assets, Liabilities, and EquityChapter 4: Revenue Recognition and Measurement4.1 Revenue Recognition Principles4.2 Measurement of Revenue: Sales, Services, and Other IncomeChapter 5: Expense Recognition and Measurement5.1 Expense Recognition Principles5.2 Measurement of Expenses: Cost of Goods Sold, Operating Expenses, and OthersChapter 6: Cash Flow Statements6.1 Importance and Purpose of Cash Flow Statements6.2 Operating, Investing, and Financing Activities6.3 Preparing a Cash Flow StatementChapter 7: Analysis and Interpretation of Financial Statements7.1 Financial Ratios and Metrics7.2 Horizontal and Vertical Analysis7.3 Limitations and Adjustments in Financial StatementsChapter 8: International Financial Reporting Standards (IFRS)8.1 Overview of IFRS8.2 IFRS Framework and Key Concepts8.3 Differences between IFRS and Generally Accepted Accounting Principles (GAAP)Chapter 9: Corporate Financial Reporting9.1 Financial Reporting for Corporations9.2 Disclosure Requirements and Auditors’ Opinions9.3 Regulatory Framework for Corporate Financial ReportingChapter 10: Accounting for Business Combinations10.1 Mergers and Acquisitions10.2 Consolidation Methods and Procedures10.3 Accounting for Non-controlling InterestsChapter 11: Financial Statement Analysis and Valuation11.1 Valuation of Assets and Liabilities11.2 Valuation Techniques: Cost Approach, Market Approach, and Income Approach11.3 Interpreting Financial Statement Analysis for Investment and Decision MakingBy providing a systematic overview of the principles, concepts, and techniques in financial accounting, this specialized English textbook addresses the needs of university students studying finance and accounting. It equips them with the necessary knowledge and skills to understand and apply financial accounting practices in an international context. With itscomprehensive content and clear explanations, this textbook serves as an indispensable resource for students pursuing a career in finance and accounting.。

financial statement名词解释

Financial statement(财务报表)是会计学中的一个重要概念,它是指企业为了向外界展示其财务状况、经营成果和现金流量而编制的正式文件。

财务报表通常包括以下几个部分:

1. 资产负债表(Balance Sheet):资产负债表反映了企业在特定日期的财务状况,包括企业的资产、负债和所有者权益。

它分为流动资产、非流动资产、流动负债、非流动负债和所有者权益等部分。

2. 收益表(Income Statement,又称损益表):收益表展示了企业在一定会计期间的经营成果,包括企业的收入、成本、费用和利润等。

它反映了企业的盈利能力和经营效率。

3. 现金流量表(Cash Flow Statement):现金流量表记录了企业在一定会计期间的现金流入和流出情况,包括经营活动、投资活动和筹资活动产生的现金流量。

它反映了企业的现金流动性和财务健康状况。

4. 所有者权益变动表(Statement of Changes in Equity):所有者权益变动表展示了会计期间内所有者权益的变动情况,包括资本注入、利润分配等对所有者权益的影响。

财务报表是企业管理层、投资者、债权人以及其他利益相关方做出决策的重要依据。

通过对财务报表的分析,可以评估企业的财务状况、经营绩效和未来的发展潜力。

大学财务会计英语教材

大学财务会计英语教材IntroductionFinancial accounting plays a crucial role in the field of business and finance. As globalization continues to impact the corporate world, the demand for professionals proficient in the language of finance is ever-increasing. This article explores the importance of the financial accounting English textbook for university students, highlighting its benefits, structure, and key topics covered.Importance of the Financial Accounting English Textbook1. Enhancing Language Skills: The financial accounting English textbook serves as a valuable resource for students to improve their language proficiency, particularly within the context of finance and accounting. It provides students with the necessary vocabulary, terminologies, and grammatical structures related to financial accounting.2. Bridging the Gap between Theory and Practice: The textbook aids in bridging the gap between theoretical concepts and their practical application. It introduces students to real-world scenarios and case studies, enabling them to understand how financial accounting principles are implemented in various business settings.3. Global Perspective: With increasing globalization, it is crucial for students to gain exposure to international accounting standards and practices. The financial accounting English textbook helps students develop a global perspective by incorporating examples and illustrations from different countries and regions.Structure of the Financial Accounting English Textbook1. Introduction to Financial Accounting: The textbook begins with an introduction to the basic principles and concepts of financial accounting. This section familiarizes students with the fundamental accounting equation, the double-entry system, and the preparation of financial statements.2. Financial Statement Analysis: This section focuses on the analysis and interpretation of financial statements. It covers topics such as ratio analysis, vertical and horizontal analysis, and the assessment of a company's financial performance and stability.3. Revenue Recognition and Expense Measurement: Students gain an understanding of revenue recognition principles and the measurement of expenses according to generally accepted accounting principles (GAAP). This section also delves into specific topics such as revenue recognition for long-term contracts and the capitalization of development costs.4. Accounting for Assets and Liabilities: The textbook extensively covers the accounting treatment of various assets and liabilities. Topics include the recognition and measurement of current and non-current assets, depreciation and amortization, impairments, as well as the recognition and measurement of different types of liabilities.5. Equity and Shareholders' Equity: This section explores the accounting for equity transactions, including the issuance and repurchase of shares, dividends, and stock splits. It also covers the various components of shareholders' equity, such as retained earnings and comprehensive income.Key Topics Covered in the Financial Accounting English Textbook1. International Financial Reporting Standards (IFRS): The textbook emphasizes the importance of understanding IFRS, which is widely adopted in many countries around the world. Students learn the key concepts and principles of IFRS and their implications for financial reporting.2. Financial Analysis and Interpretation: The textbook focuses on equipping students with the necessary skills to analyze and interpret financial statements. It covers ratio analysis, trend analysis, and benchmarking techniques to evaluate a company's financial performance and make informed decisions.3. Ethics and Professionalism: Recognizing the significance of ethics in the field of financial accounting, the textbook dedicates a section to ethical considerations and professional conduct. Students learn about the ethical responsibilities of accountants, the importance of confidentiality, and the consequences of unethical behavior.ConclusionThe financial accounting English textbook serves as an essential tool for university students studying finance and accounting. Its comprehensive structure, diverse topics, and global perspective aid students in developing a strong foundation in financial accounting principles and practices. By improving their language skills and bridging the gap between theory and practice, students are better equipped for success in the demanding and ever-changing field of financial accounting.。

Chapter 1 overview of financial accounting 会计英语 第一章 财务会计总论

Cash balance and accrual accounting profit

Using the following information for Dawn’s Diving Trips , calculate: 1. The cash in bank as at the end of 2007 2. The 2007 accrual accounting profit.

12 430

1 000

68 990

850

1 480

36 910

Payable to suppliers as at the end of 2007(paid in 2008)

Depreciation on diving equipment during 2007 Cash used by Dawn for personal purposes during 2007

1.3

What are the basic assumptions? Explain them clearly. 会计责任,问责

Identify which basic assumption of accounting is best described in each item below.

(a)The economic activities of FedEx Corporation are divided into 12-month periods for the purpose of issuing annual reports. Periodicity (b) Solectron Corporation, Inc. does not adjust amounts in its financial statements Monetary for the effects of inflation. (c) Walgreen Co. reports current and noncurrent classifications in its balance sheet. Going

财务会计英语词汇 (financial accounting terms)

Financial accounting glossaryA batch of 一批一组A tangible good 一件有形商品Abandon 放弃Accelerated depreciation 加速折旧Accomplishment 成就成绩Account for 核算Account number 账号Account outstanding 未清账款Account title 账户名称Accounting element 会计要素Accounting equation 会计等式Accounting information 会计信息Accounting period 会计期间Accounting record 会计记录Accounting standard 会计准则Accounting treatment 会计处理Accounting payable 应付账款Accounts payable subsidiary ledger 应付账款明细分类账Accounting receivable 应收账款Accounting receivable turnover 应账款周转率Accrual accounting 权责发生制会计Accrual basis of accounting 权责发生制会计制度Accrue 应计增值Accrued expense 应计费用Accrued liability 应计负债Accrued revenue 应计收入Accumulated 积累的Accumulated depreciation 累计折旧Accumulated earnings 累计收益Acid-test ratio 酸性测试比率,速动比率Acquisition 取得Additional paid-in capital溢缴资本Adjust 调节调账Adjusting entry 调账分录Administrative expense 管理费用行政费用办公费用Administrative salary expense 行政管理工资费用Admission and withdrawal of partners 合伙人的入伙及撤伙Admission by contribution of assets 通过捐缴资产的方式入伙Admission by purchase of interest 通过购买权益的方式入伙Admission of a new partner 新合伙人的入伙Admit 允许进入接受Advance payment 预付款Advertising expense 广告费用Agent 代理,代理人Aging method 账龄法Allocation of the cost 成本的分配Allowance for bad debts 坏账准备Allowance method 备抵法American express 美国运通卡Amortization 摊销摊提分期偿还Amortization expense 摊销费用Amortize 摊销摊提Amount to(在数量上) 达——Analysis period 报告期分析期Analytical tool 分析工具Anticipate 期望Apparent 明显的Apparent 明显的Applicable 实际的适用的Applicable expense 使用费用Appraisal 估价鉴定Arise from 产生于,因—-而造成Arrive at 得出As of 在或直到(某一时间)Aspect 方面Assess 评估,评价Asset acquisition 资产的取得Asset 资产Auditor 审计师Authorized stock 核定股份Available-for-sale securities 可供出售的债权Average 平均的使平均Average days inventory on hand 平均库存天数Average days sale uncollected 应收销售款平均收现天数bad debt 坏账呆账bad debt expense 坏账费用呆账费用balance 平衡余额balance 使平衡balance sheet 资产负债表bank deposit 银行存款bank reconciliation 银行往来调节银行往来对账bank service charge 银行手续费银行服务费bank statement 银行对账单bankrupt 破产的bankruptcy 破产倒闭bargain price 廉价处理价;交易价格成交价格base amount 基数base period 基期basket purchase 一揽子购买bear no connection with 与——没有联系beauty parlor 美容院beginning balance 期初余额beginning inventory 期初存货,期初库存benefit from 从——受益bill账单billing 开单出具账单board of directors 董事会bond discount z债券折价bonds payable 应付债券bonus 红利补贴津贴bonus to partner 补贴合伙人book 账簿账册book 接受——的预定、订购book value 账面价值bookkeeper 簿记员book-to-tax difference 财税之差business 企业business enterprise 商业企业企业机构business entity 企业实体商号business operation 企业机构商业企业business performance 经营活动营业活动by note 签发票据calculate 计算call for 要求call privilege 赎回权利callable bond 可通赎回债券可赎回债券cancelled check 已注销支票付讫支票capital 资本capital acquisition 资本取得capital balance 资本余额capital balance ratio 资本额比例capital contribution 资本摊缴capital expenditure 资本支出基本建设支出capital lease 资本租赁capital stock 股本capital structure 资本结构capitalize 使资本化变为资本caption 标题carry on 经营cash 现金cash basis accounting 现金收付制会计cash disbursement 现金支出cash discount 付现折扣cash dividend 现金股利现金股息cash equivalent 现金等价物cash expenditure 现金支出cash inflow 现金流入cash outflow 现金流出cash payment 现金支付现金支出cash receipt 现金收入现金所得cash receipt journal 现金收入日记账cash sale 现金销售现销cashier 出纳员categorize 分类category 类别(n)center on 以——为中心围绕certificate 凭证证明书certificate of deposit 存折存款单challenging 挑战性的changing hands 易手转手chart of accounts 会计科目表chronological record 序时记录clarify 使清楚易懂澄清classification 分类classified income statement 分类损益表closing entry 结账分录collect 收账收款collection 收款收账commission 佣金commission expense 佣金费用commitment 承付款项承诺付款数common equivalents 普通股等价物,相当于普通股的股票common stock 普通股票common-size analysis 统一度量式分析,百分比分析,共同比例分析总体结构分析common-size balance sheet 统一度量式(只用百分比,不用金额)资产负债表,通用型资产负债表,总体结构资产负债表,共同比例资产负债表,百分比资产负债表,共同量资产负债表common-size comparative balance sheet 统一度量式比较资产负债表,百分比比较资产负债表common-size comparative income statement 统一度量式比较损益表,百分比比较损益表common-size financial statement统一度量式报表,总体结构报表,共同比报表common-size statement 统一度量式报表comparative balance sheet 比较资产负债表comparative financial statement 比较财务报表complete 完成使完整complex 复杂的complicated 复杂的component 成分构成组成部分computerized accounting statement 电算化会计制度connote 含有——意义consent 同意conservation concept 保守概念consignee 承销人代售人consignee payable 应付承销人账款应付代售人账款consignment 寄售consignor 寄售人consignor payable 应付寄售人账款constitute 构成组成construction in program 在建工程consumption 消费context 上下文背景环境contingency 或有事项continuous existence 持续经营contra account 对销账户,抵消账户contractor 承包人承包商conversion privilege 兑换特权convert 改变成convertible 可转换的convertible bond 可转换债券co-owner 共有者,共同所有者co-ownership of property 共有财产copyright 版权著作权corporate (a)公司的(v)组建股份公司corporate accounting 公司会计corporate tax 公司所得税企业所得税corporation 股份公司cost accounting 成本会计cost available for sale 可销成本cost measurement 成本核定费用计量cost of goods available for sale 可销成本cost of goods manufactured 产品成本,制成成本cost of goods purchased 进货成本采购成本cost of goods sale 销售成本cost of installment sales 分期付款销货成本cost-to-cost method 成本比例法,完工百分比法count 数,盘点coupon bond 付息票(公司)债券credit 贷方贷记credit 信贷贷款credit balance 贷方余额credit card sales 信用卡销售credit card service expense 信用卡服务费credit purchase 赊购credit sales 赊销credit term 信用条件creditor 债权人criteria 标准尺度critical 关键的,至关重要的cross-reference 交叉检索current agreed value 现行的意见一致的价值current asset 流动资产current debt 流动负债current financial operation 本期财务运转current liability 流动负债current obligation 本期债务current period 当期,本期current portion of a long-term debt 一年内到期的长期负债current ratio 流动比率customer ratio 用户收费率,顾客运费率cut-off 盘存debenture 信用债券debit 借方借记debit balance 借方余额debit entry 借方分录debt ratio 负债比率debt securities 债务证券declare 通告(分红)deduct 扣除deduction (扣除)defective goods 次品deferred gross profit 递延毛利deferred income tax 递延所得税delivery expense 运费交货费用delivery wages expense 交货工资费用delivery trucks 运输车辆deposit in transit 在途存单deposit slip 存款单存款收据depositor’s books 储户的账册depreciation 折旧depreciation expense 折旧费用detect 察觉查出difference 差差额direct cost 直接成本direct labor cost 直接人工成本direct matching 直接配比direct material 直接材料直接原料direct method 直接法direct write-off method 直接冲销法director 董事disburse 支付disbursement 支出支付discount 贴息折价折扣discount on bound 债券折价discount period 折扣期间贴现期间discount sale 折价销售display 展示disposal 处理清理dissolution (n)散伙解散dissolve (v)散伙解散distinguish 区别divergent 不同的divide into 分成——divide——by——(用——除以——)dividend 红利股息股利dividend revenue 股息收入红利收益dividend payable 应付股息应付股利division of labor分工dollar amount 金额dollar change 金额变化double-entry system 复式会计制度drawing 个人提取(账户)due (票据等)到期的duration 期限earnings per share 每股收益effective interest method 实际利息(计算)法efficiency 效率efficiency ratio 效能比率效率比率efforts-expended method 已付努力法elaborate 详尽阐述elaboration 详尽说明electricity bill 电费账单employee training program 员工培训计划endanger 危及ending balance 期末余额ending capital 期末资本ending inventory 期末存货end-user 最终用户最终消费者enter into 签订entitle to 给——权利给——资格entry 分录equity accounting 权益会计equity ratio 业主权益比率equity securities 权益证券establish 建立evaluate 评估估价exceed 超过excessive 过分的excise tax 消费税exclusive right 专营权专有权executive 行政管理人员expenditure 开支expense 费用计入费用的账户expense recognition 费用的确定external 外部的(internal内部的)extraordinary gain 非常收益extraordinary item (收入或费用)非常项目,特殊项目extraordinary loss 非常损失意外损失face interest rate 票面利率face value 面值factor 系数率fair market value 公允市价公平市价fair presentation 公允表达FASB(financial accounting standard board)财务会计准则委员会Feasible 可行的Federal income tax 联邦所得税Fee 手续费服务费酬金Fees income tax 联邦所得税FICA(federal insurance contribution act)联邦社会保险法FIFO(first in first out)先进先出法Financial ability 财力资金Financial accounting 财务会计Financial analyst 财务分析家Financial condition 财务状况Financial expense 财务费用Financial institution 金融机构Financial management 财务管理Financial position 财务状况Financial report 财务报告Financial statement 财务报表Financial statement analysis 财务报表分析Financial activity 筹资活动Finished goods inventory 产成品库存制成品库存Finished product 制成品产成品Fit in 适于——Fixed assets 固定资产Fluctuate 浮动Foreign currency translation adjustment 外币换算调整Format 形式Formation partnership 合伙企业的组成Formula 公式Formulate 订立Forward 转递转交Franchise 专营权特许经营权Fraud 欺骗欺诈Frequently 频繁的Full cost 全部成本Funding by bond 债券筹资Funding by stock 股票筹资GAAP(generally accepted accounting principles)公认会计原则Gain on sale of land 销售土地所得Gain or loss of sale asset 资产变卖损益Garment factory 服装厂General and administrative cost 总务及管理成本General and administrative expense 总务及管理费用General expense 管理费用General journal 普通日记账General ledger 总账Generate 产生Goods in process 在产品在制品Goodwill 商誉Government securities 政府债券Gravel deposit 砾石矿Grocery store 杂货店Gross 总的毛的Gross amount 总计总额毛计Gross margin 毛利Gross profit 毛利总利润Guideline 标准准则Hardware store 五金商店Have something to do with 与——有关Held-to-maturity securities 持至到期的债券Historical cost 历史成本Hold back 阻挡Horizontal analysis 水平分析横向分析Hours of labor 工时人工小时Human resource management 人力资源管理Identical 同样的Identifiable 可辨认的可识别的Identify 认出确认Idle cash 闲置现金游资Idle fund 闲置资金游资Imprecise 不精确的不准确的In desperate need 急需In monetary term 用货币术语来说In proportion to 按比例In regard to 关于In that 由于因为Income before tax 税前收入Income from main operations 主营业务收入Income from other operations 其他业务收入Income statement 损益表Income summary 汇总账户损益汇总账户Income tax 所得税Income tax accounting 所得税会计Income tax effect 所得税税收效应Income tax law 所得税法Income taxes expense 所得税费用Income taxes on operations 营业所得税Incompetent 不称职的不能胜任的Incorporation 组成公司组建公司Incredible 难以置信的Incur 招致遭受Incurrence of a cost 成本的发生Indirect cost 间接成本Indirect method 间接成本法Indirect production cost 间接生产成本Industry 行业Inevitable 不可避免的Inflationary 通货膨胀Inflow流入Initial investment 起初投资Input measure 投入测算法投入核算法、Inspector 检验员检察员Installment 分期付款分期收款Installment accounts receivable 应收分期账款Installment sales 分期付款销售Insurance expense 保险费Insurance premium 保险费Intangible asset 无形资产Intangible service 无形的服务Intend as (为——而)准备,打算使——成为Intended meaning 原来的意思原有目的Interest basis 利息法按利息分配损益的方法Interest cost 利息成本Interest payable 应付利息Interest period 计息期Interest rate 利率Interest-bearing note 附息票据Interest-free 无息的Internal 内部的Interpretation 解释Intuition 直觉,直觉行为Inventory 存货库存Inventory accounting 存货核算存货会计Inventory cost flow 库存成本流转Inventory cut-off 存货盘存存货盘点Inventory on consignment 寄销存货Inventory purchase 采购存货Inventory shrinkage 存货损耗Inventory taking 盘存盘点存货Inventory turnover 存货周转率Investing activity 投资活动Investing revenue 投资收益Invoice 发票Issuance 发行Issue bond and notes 发行债券及票据Issue debt 放债Issued stock 已发行股份Janitor 看门人Journal entry 日记账分录Journal 日记账Journalizing 登陆日记账Junk bond 地基债券Label 标记归类Labor dollar 工资Labor hour 工时Labor negotiation 劳动谈判劳资谈判Law firm 律师事务所Layer 层面Lease 租赁Lease obligation 租赁债务Lease payment 租赁付款Lease term 租赁期Lessee 承租人Leaser 出租人Leger 总账Legal formality 法律手续法律形式Lending and collecting loans 放贷及收贷Less 减去Liability 负债License 执照LIFO(last in first out) 后进先出法Limited liability 有限责任Limited life 有限的经营期限Liquid 流动的易转换成现款的Liquidation 清算清偿(企业的)资产清理Liquidity 流动性Liquidity ratio 流动性比率List price 零售价目录价格List sale price 目录销售价Long-lived asset 长期资产Long-run 长期的Long-standing 长期的Long-term asset 长期资产Long-term construction contract 长期建筑合同Long-term investment 长期投资Long-term liability 长期负债Long-term obligation 长期债务Loss on write-down of inventory 存货减记损失Lower of cost or market rule 成本与市场孰低法Lubricating oil 润滑油Lump-sum payment 一次总算支付Major operation 主营业务Make clear 澄清阐述Make loans to other entities 向其他实体放贷Make out 得出完成Manipulated 易受操控的Manufacturing business 制造业制造型企业Manufacturing company 制造公司Manufacturing cost 制造成本生产成本Manufacturing overhead (间接)制造费用Market interest rate 市场利率Market price 市场价格市值Marketable 适合市场销售的销售好的可市场买卖的Marketable securities 有价证券可转售证券适销证券MasterCard 万事达卡Matching concept 配合概念配比概念Matching principle 配比原则Matching rule 配比规则Material handler 材料员Material inventory 物资库存(原)材料盘存Mathematical 数学Maturity value 到期值Merchandise 商品Merchandising business 商业企业流通业Merchandising inventory 商品存货库存商品商品盘存Merchandiser 商人商业企业Merit 优点长处Mileage 英里数里程数Mineral deposit 矿藏Minus 减减去Miscellaneous expense 杂项费用,其他费用,杂项开支Modifier 修饰语,修饰成分Money order 汇款单Monitor 监视监控Monthly statement 月结单Mortgage agreement 抵押协议Mortgage bond 抵押债券Mortgage payable 应付抵押账款Multiple 倍倍数Multiply——by (用——乘以)Negative amount 负值Negative figure 负数负值Negatively 负面的Net asset 净资产Net cash flow 现金净流量Net change 变动净额Net effect 净效果Net income 净收入Net profit after income taxes 税后净利润Net purchase 购入净值进货净额Noncash asset 非现金资产Noncurrent 非流动的Nonoperating gains and losses 非营业性利得和损失Nonproduction cost 非生产性成本No-par stock 无面值股票Notion 观念概念NSF(nonsufficient fund)check 存款不足的支票Number of share 股数Number of shares of stock outstanding 在外股票的股数Objectively 客观的Obligation 债务义务责任Office salaries expense 办公室工资费用Office supplies expense 办公室材料费用Offset against 抵消Oil well 油井On account 赊销赊购赊账On credit 赊账One decimal place 一位小数小数点后一位Operating activity 经营活动Operating asset 营业资产Operating cycle 营业循环营业周期经营周期Operating expense 营业费用Operating income 营业收入营业收益营业所的Operating lease 营业租赁Order 订单Other accounts receivable 其他应收账款Other than (除了——除非——)Outflow 流出Output measure 产量测算法产量核算法Outstanding check 未兑现的支票Outstanding stock 流通在外的股票Over the long run 从长远的观点来看长期的Overall 综合的全部的包括一切的Overhaul 彻底检修大修Overhead cost 制造成本间接成本管理费用Overstate 多计Overstatement 过多的陈述多计多报Over-the-counter 柜台上的Overtime coffee 加班咖啡加班餐饮费Owner’s equity 所有者权益Owner’s interest 所有者权益P.R(posting reference)过账证明Packing material 包装材料Par 面值Participation参与Partnership 合伙企业Partnership accounting 合伙会计Partnership agreement 合伙契约Part-time help 非全日助手Par-value stock 有面值的股票Past-due 过期的逾期的Patent 专利Payment of dividends 支付股利Payroll 工资表工资单工资额Percent change 百分比变化Percentage-of-completion accounting 完工百分比核算法Performance 绩效业绩成果Period cost 期间成本Periodic inventory method 实地盘存法Periodic payment 定期付款定期支付Perpetual inventory method 永续盘存法Pertain to 属于Petty cash 零用钱小额现金Petty cash fund 领用基金Physical quantity 实物数量Pocket 据为己有Polling 集资向共同基金提供资金Positive amount 正值Posting 过账Precede 在——前面加上在——前面先说Preference 偏爱Preferred dividend 优先股股息Preferred stock 优先股Premium 溢价Pre-numbered check 有序列号的支票Prepaid expense 预付费用Prepaid insurance 预付保险费Prepaid rent 预付房租Prepare 编制(报表等)Present 提交展示Pretax book income 税前账面收入未扣税账面所得Previous 先前的以前的Price 定价Primary income statement 基本损益表Principle 本金Principle collection 收回本金Prior 优先的Proceeds 进款收入Product cost 成品成本Product selling business 销售产品的企业Product unit cost 单位产品成本Productive 富有成效的得益的Profit 利润Profit and lost distribution 损益分配Profit margin 净利比率Profit reporting procedure 利润报告程序Profitability 获利能力盈利能力Profitability ratio 盈利率Profitable operation 获取利润的经营Progress billing 进度账单阶段账单Progress billing on construction contract 建筑合同阶段账单Promissory note 期票本票Prompt payment 立即付款Property tax 财产税Property tax payable 应付财产税Proprietorship 独资企业Prospect 前景Provisions 条款规定Prudent 谨慎的Public utilities 公用事业股份公司Purchase 进货采购Purchase return 购货退回进货退回Purchase journal 进货日记账Purchase on account 赊购Pursue 追求Quick assets 速动资产Quick ratio 速动比率、R&D(research and development) 研发实验室Ratio analysis 比率分析Raw material 原料Real estate 不动产房地产Realizable 可实现的Realization concept 收益实现概念Realization of expense 费用的确定Reconcile 调节使协调使一致Redeem 赎回买回Redeemable preferred stock 可赎回优先股Reflect 折射反射反应Regardless of 不管不顾Registered bond 记名债券Regulate 管理控制Regulator 政府管理者Reimbursable 可收回的可补偿的Reimbursement 偿还偿付付还Relevant 相关的Rely on 依靠依赖Render 提供Rent expense 房租费用租赁费用Rent revenue 租赁收入Repairs and maintenance expense 维护费用Repay 偿还Repetitive 重复的Research and development cost 研发成本Restrictive 限制性的约束性的Result from (因——而)产生发生Retail 零售Retail store 零售店Retained earning 留存盈余Retained earnings statement 留存盈余表Return on total assets 总资产收益率Revenue 收入收益Revenue recognition 收入的确定营业收入的确定Revenue-producing operating 获取总收入的经营Review 回顾Round 把——四舍五入Sacrifice 牺牲Safeguard 保护保障Salaries payable 应付薪金应付工资Salary basis 工资法Salary-interest basis 工资利息法Sales contract 销售合同Sales discount 销售折扣Sales on account 赊销Sales returns and allowance 销货退回及折让Sales salaries expense 销售工资费用Sales tax 销售税营业税Salvage value 残值Secured bond 有保(公司)债券Self-manufactured semi-finished product 自制半成品Selling and administrative expense 销售及管理费用Selling cost 销售成本Selling expense 销售成本Semiannual 半年,每半年的Serial bond 分期偿还(公司)债券,序列(公司)债券Service business 服务业Service enterprise 服务型企业Service firm 服务性企业Settle 结算Share 股票Shareholder investment 股东投资Shares outstanding 流通在外的股票,发行在外的股票Shipping expense 运费Shipping supplies expense 运输材料费Short-term asset 短期资产Short-term investment 短期投资Showroom 样品间展厅Skepticism 怀疑态度Slippery 把握不准的不稳定的不明确的Solvency analysis 偿付能力分析Solvency ratio 偿付比率Special delivery service 特快专递服务Special journal 特种日记账Special identification method 个别辨认法Specify 明确说明详细的说明Spice 香料调味料Stated ratio 设定比例固定比例Statement of cash flow 现金流量表Sticker price 卷标价格Stock 股票Stock certificate 股权证Stock issuance 股票的发行Stockholder 股东,股票持有者Stockholders’ equity 股东权益Stock-option 认股权购股选择权Stockroom personal 仓库管理人员库管Straight-line amortization 直线摊销Straight-line depreciation method 直线折旧法Straight-line method 直线法Subscriber 订阅者Subscription 订阅订购Subsequent payment 分期缴付Subtotal 小计Subtract 减去Successive 连续的Sufficient 足够的Suit 一套衣服Summarize 汇总Sundry 杂的多项的Supervisor 检察员监察员Supplement 补充Supplier 供货商Supplies 材料Synonym 同义词T account 丁字账户Take inventory 盘存Take preference over 对——具有优先权Tangible asset 有形资产Tax benefit 纳税利益Tax effect 课税效果税收效应Tax exemption 免税Tax rate 税率Taxable income 应纳税收入需纳税的收入Taxi fare 搭乘出租车费用Taxing authorities 税务部门Temporary account 临时账户Term bond 定期(公司)债券Term of consignment 寄售条款寄售条件The converse 相反的事物Timber tract 伐木道路Time deposit 定期存款Time-consuming 耗时的Title of account 账户名称To date 到现在为止到目前为止至今Total assets turnover 总资产周转率Trace 追溯查出找到Trade discount 商业折扣Transaction 会计事项Transfer 转账Transfer of ownership 所有权转让Traveling expense 差旅费Treasury bill 短期国国库券Treasury note (美)国库券Treasury stock 库存股票Uncertainty 不确定的事物Uncollectible (a)无法收回的(b)无法收回的账项Uncollectible account 坏账呆账Uncover 揭开——的盖子,暴露Understate 少计Understatement 不完全陈述不充分陈述少计少报Unearned revenue 预收收入递延收入Unexpected 意外的Uniform Partnership Act 《统一合伙条例》Unincorporated business 非股份制企业Union 工会Union dues 工会会费Unique 无比的独一无二的不寻常的Units-of-production depreciation method 产量单位折旧法Unlimited liability 无限责任Unregistered bond 无记名债券Unsecured bond 无担保债券Utility expense 公用事业费Utilities payable 应付公用事业费Utmost 最大的极度的Van 面包车微型车Vendor 卖主出卖人叫卖商Verification 核实验证Vertical analysis 垂直分析纵向分析VISA 维萨卡Void 作废的Voluntary association 自愿的联盟Weighted-average method 加权平均法Well-offness 好的境遇繁荣昌盛生意兴隆Withdraw (v)撤回撤资撤Withdrawal (n) 撤回撤资撤伙Withdrawal account 提取账户Withhold 预扣Withholding tax 预扣税款Work in process inventory 在制品盘存在产品存货Working capital 运营资本,流动资金Working capital ratio 运营资本比率Workmanship 工艺技艺做工Write-down 减记化减Zero-interest bond 无息债券。

财务会计中英文.

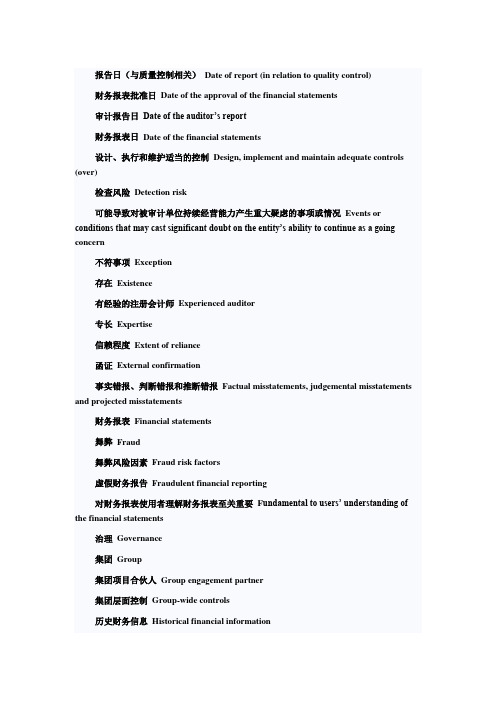

报告日(与质量控制相关)Date of report (in relation to quality control)财务报表批准日Date of the approval of the financial statements审计报告日Date of the auditor’s report财务报表日Date of the financial statements设计、执行和维护适当的控制Design, implement and maintain adequate controls (over)检查风险Detection risk可能导致对被审计单位持续经营能力产生重大疑虑的事项或情况Events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern不符事项Exception存在Existence有经验的注册会计师Experienced auditor专长Expertise信赖程度Extent of reliance函证External confirmation事实错报、判断错报和推断错报Factual misstatements, judgemental misstatements and projected misstatements财务报表Financial statements舞弊Fraud舞弊风险因素Fraud risk factors虚假财务报告Fraudulent financial reporting对财务报表使用者理解财务报表至关重要F undamental to users’ understanding of the financial statements治理Governance集团Group集团项目合伙人Group engagement partner集团层面控制Group-wide controls历史财务信息Historical financial information识别、评估和应对重大错报风险Identify, assess and respond to risk of material misstatement无法获取充分、适当的审计证据Inability to obtain sufficient appropriate audit evidence后任注册会计师Incoming auditor不一致Inconsistency独立性Independence与财务报告相关的信息系统Information system relevant to financial reporting 审计的固有限制Inherent limitation of audit固有风险Inherent risk首次审计业务Initial audit engagement生成、记录、处理和报告交易Initiate, record, process and report transactions 询问Inquiry检查Inspection中期财务信息或报表Interim financial information or statements内部审计师Internal auditors内部控制Internal control内部控制缺陷Internal control deficiency国际财务报告准则International Financial Reporting Standards调查Investigate财务报表报出日Issuance date of the financial statements信息技术应用控制IT application controls信息技术环境IT environment会计分录和其他调整Journal entries and other adjustments会计分录Journal entry/entries严重程度Level of significance上市公司实体Listed entity管理层Management管理层偏向Management bias管理层凌驾于控制之上Management override of controls管理当局声明书Management representation letter管理层对其自身责任的认可与理解Management’s acknowledgement and understanding of its responsibilities管理层的专家Management’s expert重大类别的交易、账户余额和披露Material classes of transactions, account balances and disclosure重大不确定性Material uncertainty财务报表整体的重要性Materiality for the financial statements as a whole侵占资产Misappropriation of assets错报Misstatement对事实的错报Misstatement of fact非标准审计报告Modified audit report非无保留意见Modified opinion监控Monitoring对控制的监督Monitoring of controls审计程序的性质、时间安排和范围Nature, timing and extent of audit procedures 消极式函证Negative confirmation网络事务所Network firm违反法律法规Non-compliance未回函Non-response非抽样风险Non-sampling risk观察Observation发生Occurrence期初余额Opening balances内部控制的运行有效性Operating effectiveness of internal control其他信息Other information其他事项段Other matter paragraph会计估计的结果Outcome of an accounting estimate超出正常经营过程Outside the normal course of business总体审计方案Overall audit approach总体审计策略Overall audit strategy总体结论Overall conclusion总体应对措施Overall responses合伙人Partner实际执行的重要性Performance materiality人员Personnel广泛性Pervasive计划活动Planning activities总体Population/Overall积极式函证Positive confirmation执业人员Practitioner前任注册会计师Predecessor auditor初步业务活动Preliminary engagement activities与管理层和治理层(如适用)责任相关的执行审计工作的前提Premise, relating to the responsibilities of management and, where appropriate, those charged with governance, on which an audit is conducted编制和列报财务报表Prepare and present the financial statements列报与披露Presentation and disclosure收入确认存在舞弊风险的假定Presumed fraud risks in revenue recognition防止或发现并纠正重大错报Prevent or detect and correct material misstatement专业胜任能力Professional competence职业判断Professional judgment职业怀疑态度Professional skepticism业务执行Provision of service/Delivery of service通常对决定财务报表中的重大金额和披露有直接影响的法律法规的规定Provisions of laws and regulations generally recognized to have a direct effect on the determination of material amounts and disclosures in the financial statements具有适当资格的外部人员Qualified external person保留意见Qualified opinion量化财务影响Quantification of the financial impacts合理保证(针对审计业务和质量控制)Reasonable assurance (in the context of audit engagements, and in quality control)合理性测试Reasonableness test重新计算Re-calculation连续审计业务Recurring audit engagements将认定层次的审计风险降至可接受的低水平Reduce audit risk at the assertion level to an acceptably low level关联方Related parties具有支配性影响的关联方Related parties with dominant influence管理层以前未识别或未向注册会计师披露的关联方关系或关联方交易Related party relationships or transactions that management has not identified or disclosed to the auditor 按照等同于公平交易中通行的条款执行的关联方交易Related party transactions conducted on terms equivalent to those prevailing in an arm’s length transaction (审计证据的)相关性和可靠性Relevance and reliability (of audit evidence)相关职业道德要求Relevant ethical requirements剩余期间Remaining period重新执行Re-performance管理层施加的限制Restrictions imposed by management复核(与质量控制相关) Review (in relation to quality control)权利与义务Rights and obligations风险评估程序Risk assessment procedures重大错报风险Risk of material misstatement财务报表层次和认定层次的重大错报风险Risk of material misstatement at financial statement level and at assertion level样本量Sample size抽样Sampling抽样风险Sampling risk抽样单元Sampling unit选择和运用会计政策Selection and application of accounting policies选取测试项目Selection of items for testing重要组成部分Significant component值得关注的内部控制缺陷Significant deficiencies in internal control重大事项Significant matters特别风险Significant risk重大非常规交易Significant unusual transactions特定的审计程序Specified audit procedures员工Staff统计抽样Statistical sampling存货盘点Stocktake分层Stratification期后事项Subsequent events实质性分析程序Substantive analytical procedures实质性程序Substantive procedure(审计证据的)充分性Sufficiency (of audit evidence)补充信息Supplementary information测试Test控制测试Test of controls细节测试Test of details特定类别的交易、账户余额或披露的一个或多个重要性水平The materiality level or levels for particular classes of transactions, account balances or disclosures 治理层Those charged with governance错报的临界值Threshold for misstatements可容忍错报Tolerable misstatement可容忍偏差率Tolerable rate of deviation趋势分析法、比率分析法、合理性测试法和回归分析法Trend analysis, ratio analysis, reasonableness test, and regression analysis不确定性Uncertainty未更正错报Uncorrected misstatements标准审计报告Unmodified audit report无保留意见Unqualified opinion计价与分摊Valuation and allocation/amortization穿行测试Walk-through test解除业务约定Withdraw from the engagement书面声明Written representation职业道德可接受的水平Acceptable level广告Advertising过度推介Advocacy承担管理层职责Assume management responsibilities鉴证客户Assurance client鉴证业务Assurance engagement鉴证业务项目组Assurance team审计客户Audit client审计业务Audit engagement审计项目组Audit team近亲属Close family密切私人关系Close personal relationship保密Confidentiality利益冲突Conflicts of interest或有收费Contingent fee冷却期Cooling off period现任会计师Current accountant/auditor直接经济利益Direct financial interest董事或高级管理人员Director or senior officer/senior management应有的关注Due care消除或降低不利影响Eliminate or reduce threats项目合伙人Engagement partner项目质量控制复核Engagement quality control review项目组Engagement team外部专家External expert密切关系Familiarity经济利益Financial interests历史财务信息Historical financial information直系亲属/ 主要近亲属Immediate family独立性Independence从实质上和形式上保持独立性Independence of mind, Independence in appearance 间接经济利益Indirect financial interest诚信Integrity外在压力Intimidation/Pressure关键审计合伙人Key audit partner上市实体Listed entity长期存在业务关系Long association (with an audit client)严重虚假或误导性的陈述Materially false or misleading statement非鉴证服务Non-assurance services客观和公正性Objectivity专业服务Professional services拟接受的客户Prospective client公众利益实体Public interest entity关联实体Related entity审阅客户Review client审阅业务Review engagement审阅项目组Review team轮换Rotation防范措施Safeguards自身利益Self-interest自我评价Self-review重要且密切的商业关系Significant and close business relationship 特殊目的财务报表Special purpose financial statements鉴证业务的对象Subject matter of assurance engagement不利影响、威胁Threats税法兼营Also engaged in应计税款Accrued tax从价税Ad valorem tax加计扣除Additional deduction附加税Additional tax/Surcharge所得额调整Adjustment of income税后所得After-tax income准予扣除数Allowable deductions税收可抵免额Allowable tax credit从量定额Amount based on quantity增值额Amount of appreciation/Value added销售额Amount of sales抵免税额Amount of tax credit应纳税所得额Amount of taxable income扣除项目金额Amount of the deductions适用税额Applicable tax amount适用税率Applicable tax rates计税成本Assessable cost核定所得额Assessable income平均成本利润率Average cost-plus margin rate平均销售价格Average sales price营业税Business tax偶然所得Casual income所得项目Category of income组成计税价格Composite taxable price本纳税年度Current tax year所得税申报Declaration of income tax扣除项目Deductible items免税项目扣除Deduction of the tax exemption item契税Deed tax视同销售Deemed sales/sales equivalent免除纳税义务Discharge of tax obligation应税商品Dutiable goods纳税义务Duty of tax payment权益性投资收益Earning from equity investments雇员福利,职工福利Employee benefit企业所得税Enterprise income tax国外所得收入Foreign earned income一般纳税人General taxpayer特许权使用费所得Income from franchise royalty利息、股息、红利所得Income from interests, dividends and bonuses 劳务所得Income from labor service财产租赁所得Income from leasing of property生产经营所得Income from production and business operation转让财产所得Income from property transfer工资薪金所得Income from wages, salaries财产转让收入Income from property transfer所得税抵免Income tax credit申报缴纳所得税Income tax declaration应纳所得税Income tax payable接受捐赠所得Income from donation个人所得税Individual income tax增值税进项税额Input value added tax非正常损失Irregular loss滞纳金Late fee清算所得税Liquidation income tax最低应纳税所得额Minimum taxable income增值税起征点Minimum threshold of value-added Tax混合销售行为Mixed sales activities所得税前净所得Net income before income tax税后净利润Net profit after tax非货币资产Non-monetary asset不征税收入Non-taxable income不计入征税范围Not included in the scope of taxable activities 财产原值Original value of the property/ Cost of property当期销项税额Output tax for the period增值税销项税额Output value added tax滞纳税款/欠税Overdue tax应补缴税款Payment of tax in arrears累进税率Progressive tax rate比例税率Proportional tax rate公益性捐赠Public welfare donations房产税Real estate tax居民纳税人Resident taxpayer资源税Resource tax含税销售额Sales amount including tax所得税征收范围Scope of income tax/Subject to income tax 小规模纳税人Small-scale taxpayer源泉扣缴Source withholding纳税特别扣除项目Special deductible items特殊性税务处理Special tax treatment印花税Stamp tax应征税额Tax accrued税额Tax amounts税基/计税依据Tax base税种Tax category消费税税率Tax computation税收抵免Tax credit抵免限额Tax credit quota纳税期限Tax deadline税前可扣除项目Tax deductible items税收减免Tax deduction or exemption计税差异Tax differences到期应纳税款Tax due漏税/逃税Tax evasion免税Tax exemption纳税申报Tax filing本期税额Tax for the period/year已纳税额Tax paid应纳税额Tax payable纳税期限Tax payment deadline税率Tax rate减税Tax reduction退税Tax refund税收附加Tax surcharge起征点Tax threshold计税价格Tax value/Taxable price减免税额Tax amount deducted应税所得Taxable income应税项目Taxable item纳税期间Taxable period对股息征税Taxation of dividends免税收入Tax-exempt income免税税目Tax-exempt item免税利润Tax-exempt profit含税价格Tax-included price纳税人Taxpayer土地使用税Urban land-use tax增值税Value added tax(VAT)土地增值税Value-added tax on land/Land appreciation tax 增值税减免VAT exemption or reduction车船税Vehicle and vessel tax车辆购置税Vehicle purchase tax扣缴义务人Withholding agent代扣代缴税款Withholding and remitting tax预提所得税Withholding income tax零税率Zero tax rate财务成本管理应收账款周转次数Accounts receivable turnover应收账款周转天数Accounts receivable turnover days取得成本Acquisition cost实际增长率Actual growth rate实际利率Actual interest rate配股后每股价格After-allotment price per share配股权价值Allotment option value配股价格Allotment price预付年金(即付年金、期初年金)Annuity due会计报酬率法Accounting rate of return(ARR)平均交货时间Average delivery time贝塔(β)系数Beta coefficient债券评级Bond rating债券估价Bond valuation每股净资产Book value per share(BPS)盈亏临界点Break-even point保险储备(安全存量)Buffer inventory资本支出Capital expenditure持有成本Carrying cost现金预算Cash budget现金股利Cash dividend现金流量利息保障倍数Cash flow interest coverage ratio 经营活动现金流量Cash flows from operational activities 混合租赁Combination lease佣金Commission普通股Common stock补偿性余额Compensating balance复利Compound interest全面预算Comprehensive budget企业价值评估Corporate valuation成本性态Cost behavior成本中心Cost centre成本的归集和分配Cost collection and allocation资本成本Cost of capital税后债务成本Cost of debt after tax成本差异Cost variance平息债券Coupon bond债券票面利率Coupon interest rate流动资产周转次数Current assets turnover流动资产周转天数Current assets turnover days流动比率Current ratio本期收入乘数Current sales multiplier债务市场Debt market/Bond market资产负债率Debt-to-asset ratio产权比率Debt-to-equity ratio股利宣告日Declaration date财务杠杆系数Degree of financial leverage(DFL)直接租赁Direct leasing折现率Discount rate纯贴现债券(零息债券)Discounted bond (Zero coupon bond)股利支付率Dividend payout ratio经营杠杆系数Degree of operating leverage(DOL)股价下行乘数Downstream price multiplier总杠杆系数Degree of total leverage (DTL)息前税前利润Earnings before interests and taxes(EBIT)经济订货量Economic order quantity(EOQ)每股盈余稀释EPS dilution每股盈余无差别点法EPS indifferent point method(EBIT-EPS break even analysis)每股盈余最大化EPS maximization每股盈余Earnings per share(EPS)权益乘数Equity multiplier股权价值Equity value经济增加值Economic value added(EVA)除息日Ex-dividend date执行价格Exercise price/Strike price外部融资销售增长比External financing needed to sales growth ratio 融资租赁Financial lease/Capital lease财务估价Financial valuation完工产品Finished goods固定预算Fixed budget弹性预算Flexible budget浮动利率Floating interest rate浮动优惠利率Floating prime interest rate债务现金流量Free cash flows of creditors股权现金流量Free cash flows of equity实体现金流量Free cash flows of firm复利终值系数FV interest factor预付年金终值系数FV interest factor of annuity due终值Future value(FV)管理费用General and administrative expense持续经营价值Going concern value毛租赁Gross lease营业现金毛流量Gross operating cash flows套期保值原理Hedging principle间接成本Indirect cost通货膨胀率Inflation rate利息保障倍数Interest coverage ratio税后利息率Interest rate after tax内含增长率Internal growth rate内部转移价格Internal transfer price内在市销率Intrinsic sales multiplier内在价值Intrinsic value存货周转次数Inventory turnover存货周转天数Inventory turnover days投资中心Investment center内含报酬率法Internal rate of return(IRR) 非相关成本Irrelevant cost发行价格Issuance price租赁期Lease term租赁资产Leasehold property承租人Lessee出租人Lessor杠杆贡献率Leverage contributing ratio杠杆租赁Leverage lease清算价值Liquidation value短期偿债能力比率Liquidity ratios长期债券Long-term bond制造费用预算Manufacturing overhead budget边际贡献率Marginal contribution ratio市场组合Market portfolio市场价格Market price市价稀释Market price dilution市场风险溢价Market risk premium债券到期日Maturity date市场增加值Market value added(MAV)最大最小法Maximin method企业价值最大化Maximization of firm’s value股东财富最大化Maximization of shareholders’ wealth混合成本Mixed cost互斥项目Mutually exclusive projects/events流通债券Negotiable bond净财务杠杆Net financial leverage净租赁Net lease营业现金净流量Net operating cash flows销售净利率Net profit margin净现值法NPV method净现值Net present value(NPV)经营租赁Operating lease经营杠杆Operating leverage机会成本Opportunity cost期权价值Option value订货提前期Order lead time订货成本Ordering cost普通年金(后付年金)Ordinary annuity债券面值Par value/Face value回收期法Payback period method股利支付日Payment date经营资产销售百分比Percentage of operating assets to sales经营负债销售百分比Percentage of operating liabilities to sales 销售百分比法Percentage-of-sales method期间成本Period cost定期预算Periodic budget永久债券Perpetual bond永续年金Perpetuity优先股Preferred stock现值指数Present value index产品成本预算Product cost budget生产预算Production budget生产成本Production cost制造费用Production overhead利润中心Profit center利润最大化Profit maximization项目特有风险Project-specific risk公开增发Public offering复利现值系数PV interest factor预付年金现值系数PV interest factor of annuity due现值Present value(PV)速动比率Quick ratio股权登记日Record date共同年限法Replacement chain (common life) approach 必要报酬率Required rate of return剩余股利政策Residual dividend policy剩余权益收益Residual equity income剩余净金融支出Residual net financial expenditure剩余经营收益Residual operating income责任中心Responsibility center利润留存率Retention ratio权益净利率Return on equity投资报酬率Return on investment收入中心Revenue center无风险利率Risk-free interest rate无风险报酬率Risk-free rate of return安全边际率Safety margin ratio销售预算Sales budget销售费用Sales expense销售预测Sales forecast销售增长率Sales growth rate代销Sales on commission销售数量Sales volume股东权益增长率Shareholders’ equity g rowth ratio短缺成本Shortage cost证券市场线Security market line(SML)标准成本Standard cost股票股利Stock dividend股价最大化Stock price maximization股票回购Stock repurchase股票分割Stock split储存成本Storage cost沉没成本Sunk cost可持续增长率Sustainable growth rate系统风险(市场风险、不可分散风险)Systematic risk (Market risk/Non-diversifiable risk)目标资本结构Target capital structure时间溢价Time premium货币的时间价值Time value of money固定成本总额Total fixed cost标的资产Underlying assets包销Underwrite单位销售价格Unit sales price单位变动成本Unit variable costs股价上行乘数Upstream price multiplier变动成本率Variable cost ratio加权平均资本成本Weighted average cost of capital(WACC)营运资本投资Working capital investment在产品Work-in-progress到期收益率法Yield-to-maturity method(YTM method)公司战略与风险管理低增长—强竞争地位的―现金牛‖业务―Cash cow‖ position : slow growth - high competitiveness低增长—弱竞争地位的―瘦狗‖业务―Dog‖ position : slow growth - low competitiveness 高增长—低竞争地位的―问题‖业务―Question mark‖ position : high growth - low competitiveness高增长—强竞争地位的―明星‖业务―Star‖ position : high growth - high competitiveness放弃战略Abandon strategy竞争环境分析Analysis of competitive environment竞争对手分析Analysis of competitors企业能力分析Analysis of corporate competencies and capabilities企业资源分析Analysis of corporate resources宏观环境分析Analysis of macro-environment市场需求分析Analysis of market demand分析型战略Analytical strategy审计委员会Audit committee平衡计分卡Balanced scorecard基准分析Benchmarking analysis蓝海战略Blue Ocean strategy波士顿矩阵Boston matrix业务单位战略(竞争战略)Business (Competitive) strategy经营目标Business objectives运营风险Business risk业务单元Business unit事业部制组织结构Business unit organization structure战略变革Change management in strategy内部信息传递Communication of internal information全面风险管理Comprehensive risk management收缩战略Contraction strategy控制活动Control activities控制环境Control environment公司治理Corporate governance总体战略Corporate strategy成本领先战略Cost leadership strategy惩治成本Cost of punishment损失成本Cost of total loss风险管理成本与效益Costs and benefits of risk management信用风险Credit risk文化与绩效Culture and performance客户细分或市场细分事业部制结构Customer segmentation/Market segmentation business structure消费动机Customer’s motivation负债和杠杆作用Debt and gearing扁平型结构Decentralized structure决策支持系统Decision support system防御型战略Defensive strategy制定风险管理策略Development of risk management strategy 发展战略Development strategy钻石模型Diamond model差异化战略Differentiation strategy直接投资Direct investment多元化并购Diversified merger and acquisition多种经营战略Diversified strategy垄断优势理论Dominance advantage theory每股盈余或市净率Earnings per share or price to book ratio 效率Efficiency生产要素Elements in production内部控制的要素Elements of internal control创业型组织结构Entrepreneurial organization structure自然环境风险Environment risk股权投资Equity investment评估成本Evaluation cost事项识别Event identification处置成本Execution cost实地查验Field inspection财务风险与经营风险的搭配Financial risk and business risk 内部控制的五大要素Five elements in internal control产业五种竞争力Five forces in the competitive approach集中化战略Focus strategy紧缩与集中战略Focused strategy职能制组织结构Functional organization structure职能战略Functional strategy资金活动Fund-related activities全球化战略Globalization strategy毛利率与净利润率Gross profit margin and net profit margin增长型战略Growth strategy开拓型战略Growth strategy担保业务Guarantee businessH型结构(控股企业/控股集团组织结构) H type organization structure (Holding company/Group organization structure)高经营风险与高财务风险搭配High business risk, high financial risk高经营风险与低财务风险搭配High business risk, low financial risk高长型结构High growth structure横向并购Horizontal merger and acquisition增量预算Incremental budgeting产品生命周期Industry life cycle产业风险Industry risk信息与沟通Information and communication一体化战略Integrated strategy后向一体化战略Integrated strategy - Backward前向一体化战略Integrated strategy - Forward横向一体化战略Integrated strategy - Horizontal纵向一体化战略Integrated strategy - Vertical产业内现有企业的竞争Intensity of industry rivalry密集型战略Intensive strategy内部控制Internal control多国本土化战略International subsidiaries strategy国际战略Internationalization strategy资源的不可替代性Irreplaceable resources合资经营Joint investment business准时生产系统Just-in-time system(JIT)杠杆收购Leveraged buy-out法律风险Litigation risk长期目标Long-term objective维持成本Maintenance cost管理信息系统Management information system市场开发——现有产品和新市场Market development - existing product and new market市场渗透——现有产品和现有市场Market penetration - existing product and existing market重要缺陷Material deficiency矩阵制组织结构Matrix organization structure风险度量Measurement of risk公司战略的现代概念Modern concept of corporate strategy监督Monitoring风险管理的监督与改进Monitoring and improvement of risk managementM型企业组织结构(多部门结构) Multi-divisional organization structure非杠杆收购Non leveraged buy-out内部控制的目标Objectives of internal control风险管理的目标Objectives of risk management现场检查On-site inspection运行缺陷Operating deficiency操作风险Operational risk期权合约Options contracts组织管理能力Organization management ability组织资源Organization resources组织架构Organization structure业务外包Outsourcing信息系统外包Out-sourcing of information system人员导向性People-driven绩效评估Performance evaluation资源的持久性Persistence of the resources ownedPEST分析PEST analysis政治风险Political risk供应者、购买者讨价还价的能力Power of buyers or suppliers预防成本Prevention cost基本活动(又称主体活动)Primary activities内部控制的原则Principles of internal control风险管理基本流程Process of risk management采购业务Procurement activities产品开发——新产品和现有市场Product development - new product and existing market产品/品牌事业部制结构Product/Brand business structure生产流程计划Production process planning生产运营Production and operation生产管理能力Production management ability产能计划Production plan盈利能力和回报率指标Profitability and rate of return measurement质量管理Quality management反应型战略Reactive strategy相关多元化Related diversification研究与开发Research and development研发能力Research and development ability已动用资本报酬率(投资回报率或净资产回报率)Return of capitalemployed(ROCE)/Return of investment(ROI)/Return of net assets(RONA) 转向战略Reverse strategy激励和奖励机制Reward and incentive system风险承担Risk acceptance风险偏好Risk appetite风险评估Risk assessment风险规避Risk avoidance风险补偿Risk compensation风险控制Risk control风险转换Risk conversion风险转移Risk transfer角色导向型Role-driven证券投资Securities investment重大缺陷Significant deficiency稳定战略Stable strategy利益相关者stakeholders企业战略联盟Strategic alliances战略分析Strategic analysis外部环境分析Strategic analysis – External environment战略业务单位组织结构Strategic business unit organization structure(SBU)战略控制系统Strategic control system战略群组Strategic group战略目标Strategic objective国际化经营的战略类型Strategic options for international business业绩计量Strategic performance evaluation战略风险Strategic risk内部环境分析Strategy analysis - Internal environment发展战略Strategy development战略实施Strategy implementation战略管理过程Strategy management process战略选择Strategy selection继任计划Succession planning技术风险Technology risk潜在进入者的进入威胁Threat of new entrants 替代品的替代威胁Threat of substitutes跨国战略Transnational strategy非相关多元化Unrelated diversification战略失效Unsuccessful strategy价值链分析Value chain analysis纵向并购Vertical merger and acquisition零基预算Zero-based budgeting经济法承诺Acceptance收购人Acquirer要约收购Acquisition by offer上市公司收购Acquisition of a listed company 资产收购Acquisition of assets实际出资人Actual capital contributor实际控制Actual control实际控制人Actual controller临时报告Ad hoc report管理人Administrator入伙Admission to a partnership代理/受托人Agent协议转让Agree to transfer合同变更Alter of contract年度报告Annual report关联交易Associated transaction公司章程Association of articles破产财产Bankrupt property破产债权Bankruptcy creditor破产费用Bankruptcy expenses破产法Bankruptcy Law基准日Base date大宗交易Block trading董事会Board of directors监事会Board of supervisors民事行为能力Capacity for civil conducts 董事长Chairperson of the board民事权利能力Civil rights集体所有权Collective ownership公司分立Company demergers公司法Company Law股份有限公司Company limited公司合并Company mergers经营者集中Concentration of operators 一致行动Consistent act合同法Contract Law承揽人/承包人Contractor委托合同Contracts for commission承揽合同Contracts for work控股股东Controlling shareholders可转换公司债券Convertible bond协同行为Coordinated behavior公司债券Corporate bond信用评级Credit rating债权人委员会Creditors’ committee债权人会议Creditors’ meeting违约金Damages for breach of contract债务人财产Debtor’s property破产宣告Declaration of bankruptcy减资Decrease of capital故意Deliberate intention标的物Delivery of the object定金Deposits注销登记Deregistration董事Directors清偿Discharge持股权益披露Disclosure of shareholders’ interest 任意公积金Discretionary reserve fund合同的解除Dismissal of contract处分权Disposal right解散Dissolution新设分立Division by new establishment赠与Donation提存Drawing选举权Election rights发包人Employer股权收购Equities acquisition合同成立Establishment of a contract核准Examination and approval免责条款Exclusion clauses执行董事Executive directors除名Expel临时股东大会Extraordinary general meeting不可抗力Force majeure欺诈Fraud无偿划拨Free allotment股东大会General meeting of shareholders普通合伙人General partners普通合伙企业General partnership enterprises政府债券Government bond重大过失Gross fault保证人Guarantor担保Guaranty担保合同Guaranty contracts保证期间Guaranty period不动产Immovable property/Real estate独立董事Independent directors间接收购Indirect takeover首次公开发行Initial public offering(IPO)内幕交易Insider trading资不抵债Insolvency胁迫Intimidation无效行为Invalid activities出资义务Investment obligation非公开发行Issuance in a non-public manner连带责任保证Joint and several liability guarantee 共同共有Joint co-ownership正当理由Justified reasons土地承包经营权Land contractual operating rights 租赁物Leased property法人财产权Legal person property rights法定代理人Legal representatives违约责任Liability for breach of contract诉讼时效Limitation of action有限责任公司Limited liability company有限合伙人Limited partner有限合伙企业Limited partnership enterprise 限定交易Limited trading清算组Liquidation committee清算义务人Liquidation obligor上市公司Listed company管理层收购Management buyout强制要约Mandatory offer操纵市场行为Market rigging市场份额Market share重大资产重组Material assets reorganization 吸收合并Merger by absorption新设合并Merger by consolidation少数股东权益Minority shareholder rights垄断行为Monopolistic practices垄断Monopoly抵押权Mortgage动产Movable property名义股东Nominee shareholder非货币财产出资Non-monetary contribution 不可替代物Non-substitute善意取得Obtain in good faith要约Offer抵销Offset经营者Operators所有权Ownership有偿出让Paid transfer履行Perform重整期间Period of reorganization定期报告Periodic report配股Placing质权Pledge rights优先清偿Preferential repayment委托人Principal私人所有权Private ownership破产和解程序Procedure of settlement for bankruptcy加工Processing利润分配Profit distribution发起人Promoter发起设立Promotion招股说明书Prospectus公积金Provident fund物权法Real Rights Law注册资本Registered capital重整Reorganization收购报告书Report of acquisition要约收购报告书Reports of acquisition by offer股东会决议Resolution of shareholders’ meeting可撤销合同Revocable contract知情权Right to know提议权Right to propose破产撤销权Right to rescind bankruptcy优先受偿权Right to seek preferential payments of compensation 证券法Securities Law。

财务管理基础课件:Review of Accounting

– It is purely a voluntary act on the part of the company

Байду номын сангаас2-20

Limitations of the Balance Sheet (cont’d)

• Indicates what the firm owns and how these assets are financed in the form of liabilities or ownership interest

– Delineates the firm’s holdings and obligations – A picture of the firm at a point in time – Items are stated on an original cost basis

Review of Accounting

Chapter Outline

• Income Statement • Price-earnings Ratio • Balance Sheet • Statement of Cash Flows • Tax-free Investments (Depreciation)

• Accumulated depreciation: Sum of past and present depreciation charges on currently owned assets

2-15

Balance Sheet Items (cont’d)

– Total assets: Financed through liabilities or stockholders’ equity

财务会计文献评述范文

财务会计文献评述范文英文回答:Financial Accounting Literature Review.Introduction.Financial accounting literature provides insights into the principles, practices, and theories underlying the preparation and interpretation of financial statements. This literature review aims to explore key themes and advancements in financial accounting research, offering a comprehensive overview of the field and its implications for financial reporting.Historical Evolution.The foundations of financial accounting can be traced back to the development of double-entry bookkeeping in the 14th century. However, the modern era of financialaccounting emerged in the 19th century with the rise of industrialization and the need for standardized reporting.Conceptual Framework.The International Accounting Standards Board (IASB) has established a conceptual framework that provides the theoretical underpinnings for financial reporting. This framework outlines the objectives of financial statements, the qualitative characteristics of useful financial information, and the elements of financial statements.Balance Sheet.The balance sheet presents a snapshot of a company's financial position at a specific point in time. It lists assets, liabilities, and equity, providing insights into the company's financial health and liquidity.Income Statement.The income statement reports a company's financialperformance over a period of time. It measures revenues, expenses, and net income, indicating the company's profitability and earning power.Statement of Cash Flows.The statement of cash flows provides information about the sources and uses of cash over a period of time. It classifies cash flows into operating, investing, and financing activities, revealing the company's cash generation and utilization.Financial Statement Analysis.Financial statement analysis involves using various techniques to assess a company's financial performance and position. Ratio analysis, horizontal analysis, and vertical analysis are common methods used to identify trends, compare performance, and evaluate financial health.Current Issues.Contemporary financial accounting research is addressing emerging issues such as:The impact of technology on financial reporting.Sustainability and social responsibility accounting.The role of artificial intelligence in financial analysis.Data quality and data analytics.Conclusion.Financial accounting literature provides a valuable resource for practitioners, researchers, and policymakers in understanding the principles and practices of financial reporting. By reviewing key themes and advancements in the field, this literature review contributes to the ongoing development and improvement of financial accounting standards and practices.中文回答:财务会计文献评述。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。