管理会计双语教学

成本与管理会计课程双语教学问题研究

葛。 模式,在教学目标涉及的外语水平上与完全运用外语进行的教

教学 中可将它们进行适 当的分类 , 教学 内容条理 分明, 使 如在介

重J 是有 学还 所不同的。 对于国际 性的 来说, 本与管 专业 成 理会计课 绍成本会计课涉及的间接成本差异分析内容时 ,将 细分 的计 算 主 教学目 标可在 过渡型 教学目 标上有所提高, 使学生基本上能够 预算变动制造费用分配率 、 变动制造费用差异 、 固定 制造 费 计算

吾f 的特征 ,完全或基本上使用汉语或使用英语教学都不应算是严

r 蹩 ~ E

.

_

.

.

.

.

.

. 经济论

一

—

—

二 趔 Em 些

翻

论期刊数 宇化发展对痂辑的要 求

口 但 丹 吴 瑕 军 事 经 济 学 院襄 阳士 官 学 校

摘

要 : 了适 应期 刊数 字化 对 编 辑 带 来 的 影 响 , 文 试 从 三 个 方 面 论 述 了期 刊 数 字 化 发展 对 编 辑 的要 求 , 思 想 素 质 、 辑 能 为 该 即 编

目标 是 通 过 教 学 使 学 生 对 成 本 会 计 和 管 理 会 计 的基 本 理 论 、 基

本 知识 和方 法有 全 面 和 系统 的 了解 , 以及 培 养 学 生 应 用 所 学 理 论 、 识 和 方 法 解 决相 关 问题 和 创 新 的 能力 。 样 的 目标 是 解 决 知 这

掌握 专 业 理 论 、 识 和 方 法 放 在 重要 的位 置 上 。 因 此 , 教 学 过 知 在

程 中 , 师 在 认 为 有 必 要 让 学 生 更 清 楚 了 解某 些专 业 内 容 时 , 教 可 以适 当运 用 中文 进 行 表述 。 如 , 管 理 会 计 的 经 营利 润 的战 略 例 对 分 析方 法 的介 绍 ,可 采 用 我 国教 学 中通 常 采 用 的差 额 计 算 法 和 中文 进行 总差 异 和 具 体 分 析 的描 述 ,并 与 国外 有 关 教 材 的分 别 就成 长 、 价格 补 偿 和 生 产 率 三 个 方 面 差 异 进 行 的英 文 描 述 进 行 比较 。教 学 实 践 证 明 , 教 学 中 适 当 运 用 一些 中 文 描 述 , 学 生 在 对

本科管理会计学双语教学初探

有关 能够适 应 WT O发展 的专 业课 程 的

双语开课率要达到所开课 程的 5 ~ % 1%。 此 , 管 理 会计 学 实 行 双语 教 学 , 0 因 对 使 学 生 能 够 真 正 地 掌 握 管 理 会 计 学 应 该

用了原版 的英 文教材 ,可 以使 学生体会

到 国外最前沿 的理 论信息 , 领略 “ 原汁原

双 语 教 学 是 指 对 中 文 、外 文 两 种 语 言进 行 有 机 结 合 同时 对 专 业 课 程 进 行 两

随着全球化经济 的发展 ,世界 各地

的文 化 互 相 传 播 、 收 , 新 速 度 的 不 断 吸 更

对 于已经习惯 了国内中文教材风格 的学 生来说 , 需要一个逐渐适应 的过程 。

的 详 细 分析 . 出 了我 国 实行 双 语教 学 的 , O 性 以及 阻碍 双 语教 学 过 程 有 效 实施 的相 关 问题 , 根 据 双语 教 学 过 程 中 自身 积 累的 找 z r - 并

一

些相 关经 验 . 于 目前 管理 会 计 学所 存 在 的 一 些 问题 提 出 了有 效 对 策 。 对 关键词 : 管理 会 计 学 ; 语 教 学 ; 学过 程 双 教

增 强 自身 的 学 习 能 力 和创 新 能 力 ,从 而

管 理 会 计 学 科 涉 及 的 领 域 广 ,在 培 养 国 际化 人 才 目标 的趋 势 下 ,管 理 会 计

提高 自身 的国际竞争力 。通过对学生实 施管理会计 学的双语教学 ,能够使学 生

际趋势发展 的必然选择。因此 , 国各 高 全 校也不 断对 双语 教学进行 深入的推广 与

式 的 教 学 现 象 还 是 存 在 ,无 法 发 挥 学 生 的 主 动性 与积 极 性 。

《管理会计》课件全英文Acct_ch1_ManAcct_(Feb_25)

1. Externally focused 2. Must follow externally imposed rules 3. Objective financial information

1 -23

Types of Information

For management accounting, the The restrictions imposed on financial accounting tend to financial or nonfinancial produce objectivebe much more information may and verifiable financial information. subjective in nature.

Continued

1 -3

Objectives

5. Describe the role of management accountants in an organization. 6. Explain the importance of ethical behavior for managers and management accountants. 7. List three forms of certification available to management accountants.

1 -12

Management Process

The Management Process is defined by the following activities: Planning Controlling Decision Making

Decision making is the process of choosing among competing alternatives.

管理会计双语第5章

Sales level at which operating income is zero Sales above breakeven result in a profit Sales below breakeven result in a loss Two methods: Income statement approach Contribution margin approach

Units produced Direct materials cost per unit Total direct materials cost

100 200 300

$120 $60 $40

12,000 12,000 12,000

400

500

$30

$24

12,000

12,000

Committed fixed costs represent investments with a

Contribution margin is used first to cover fixed expenses.

Any remaining contribution margin contributes to net operating income.

Sales revenue per unit

Fixed costs Contribution margin ratio

Breakeven point in sales dollars

$20,000 $15,000

Dollars

$10,000 $5,000 $0 0 500

•

Revenues

1,000

1,500

Volume of Units

(完整版)管理会计示范性双语课件习题09

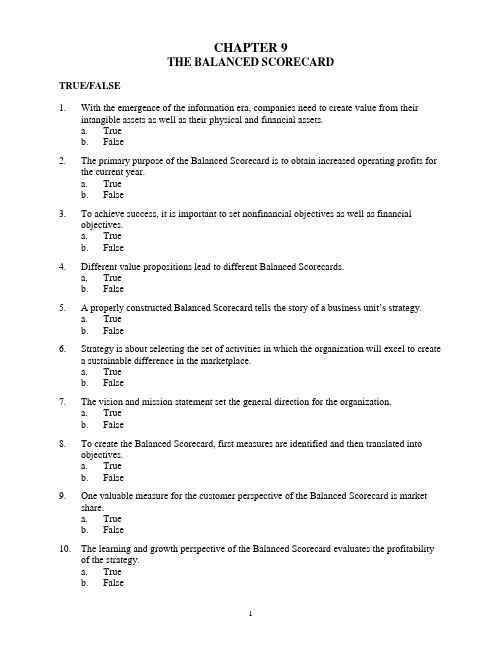

CHAPTER 9THE BALANCED SCORECARDTRUE/FALSE1. With the emergence of the information era, companies need to create value from theirintangible assets as well as their physical and financial assets.a. Trueb. False2. The primary purpose of the Balanced Scorecard is to obtain increased operating profits forthe current year.a. Trueb. False3. To achieve success, it is important to set nonfinancial objectives as well as financialobjectives.a. Trueb. False4. Different value propositions lead to different Balanced Scorecards.a. Trueb. False5. A properly constructed Balanced Scorecard tells the story of a business unit’s strategy.a. Trueb. False6. Strategy is about selecting the set of activities in which the organization will excel to createa sustainable difference in the marketplace.a. Trueb. False7. The vision and mission statement set the general direction for the organization.a. Trueb. False8. To create the Balanced Scorecard, first measures are identified and then translated intoobjectives.a. Trueb. False9. One valuable measure for the customer perspective of the Balanced Scorecard is marketshare.a. Trueb. False10. The learning and growth perspective of the Balanced Scorecard evaluates the profitabilityof the strategy.a. Trueb. False11. Employee satisfaction is a measure of the internal business perspective of the BalancedScorecard.a. Trueb. False12. Success in the customer perspective of the Balanced Scorecard should lead to improvementin the financial perspective.a. Trueb. False13. Key performance indicator scorecards that don’t reflect a company’s strategy can be just aseffective as the Balanced Scorecard.a. Trueb. False14. Key performance indicator cards will lead to local but not to global or strategicimprovements.a. Trueb. False15. Nonprofit and government organizations cannot use the Balanced Scorecard since financialperformance is not their primary measurement.a. Trueb. False16. Mission, rather than the financial perspective, drives the strategy of nonprofit andgovernment organizations.a. Trueb. False17. Balanced Scorecard measurements create focus for the future.a. Trueb. False18. CEOs and senior leadership can effectively implement strategy by themselves.a. Trueb. False19. Poor scorecard design, rather than a poor organizational process, is the biggest threat tosuccessful Balanced Scorecard implementation.a. Trueb. False20. If a Balanced Scorecard implementation team is really committed, they can initiallydevelop the perfect scorecard.a. Trueb. FalseMULTIPLE CHOICE21. Moving from the industrial age to the information age, companies need to:a. focus on the management of financial assets and liabilitiesb. make prudent investment in physical assetsc. create value from their intangible assets as well as their physical and financial assetsd. present an expanded section of intangible assets on their balance sheets22. Many intangible assets:a. do not appear on the balance sheet since it is difficult to place a reliable financialvalue on themb. should be evaluated with ROI and other performance measuresc. can be measured and managed with current financial control systemsd. are unimportant because they have no physical substance23. Intangible assets that are currently reported on the balance sheet include:a. loyal and profitable customer relationsb. innovative products and servicesc. employee skills and motivationd. the cost of a patent giving exclusive rights to a process24. The saying “what gets measured gets done” refers to measuring performance:a. so that appropriate disciplinary actions can be takenb. to ensure that employees perform equally in all dimensions of their jobsc. so that essential tasks get accomplishedd. to ensure that the ethical code of conduct is also being enforced25. The use of multiple-performance measures would be expected to lead to all of thefollowing EXCEPT:a. more extensive use of financial measures such as cost and profitb. employees recognizing the various dimensions of their workc. the use of new performance measures such as customer satisfaction and employeemoraled. group-level performance measures26. Balanced Scorecard objectives are in balance when:a. debits equal creditsb. financial performance measurements are less than the majority of measurementsc. the measurements are faird. the measurements reflect an improvement over the previous year27. The Balanced Scorecard is said to be “balanced” because it measures:a. short-term and long-term objectivesb. financial and nonfinancial objectivesc. internal and external objectivesd. All of the above are correct.28. __________ translate(s) an organization’s mission, vision, and strategy int o acomprehensive set of performance measures that provide the framework for implementing its strategy.a. Critical success factorsb. The value propositionc. Objectivesd. The Balanced Scorecard29. Which of the following statements is NOT true of a good Balanced Scorecard?a. It tells the story of a company’s strategy by articulating a sequence of cause-and-effect relationships.b. It helps to communicate corporate strategy to all members of the organization.c. It identifies all measures, whether significant or small, that help to implement strategy.d. It uses nonfinancial measures to serve as leading indicators of future financialperformance.30. Which of the following statements is NOT true of the Balanced Scorecard?a. Different strategies call for different scorecards.b. Successful implementation requires commitment and leadership from topmanagement.c. Only objective financial measures should be used, and subjective nonfinancialmeasures should be avoided.d. Cause-and-effect linkages may not be precise and should evolve over time.31. A strategy map provides direct cause-and-effect linkages between the:a. financial perspective and the learning and growth perspectiveb. financial perspective and the internal perspectivec. customer perspective and the internal perspectived. customer perspective and the learning and growth perspective32. A chain of cause-and-effect relationships that appropriately link the four balancedscorecard perspectives is:a. a high return on investment causes customer loyalty that results in skilled productionworkers that improve process qualityb. skilled production workers help to produce process quality that results in customerloyalty that helps to increase return on investmentc. customer loyalty results in a high return on investment that results in the ability toattract skilled production workers that improve process qualityd. improved process quality results in a high return on investment that causes customerloyalty that results in the ability to attract skilled production workers33. If a financial measure were growing revenues, then a driver from the customer perspectivewould MOST likely be:a. cross-selling other company productsb. trained employeesc. reduced cycle timesd. innovative processes34. If a customer measure were customer loyalty, then a driver from the internal perspectivewould MOST likely be:a. implementing cutting-edge technologyb. repeat salesc. high-quality production processesd. increased profits35. If an internal measure were shorter cycle times, then a driver from the learning and growthperspective would MOST likely be to:a. lower cost of acquiring materialsb. achieve just-in-time supplier capabilityc. offer a complete product lined. expand product offerings36. Which of the following statements is true?a. Vision and mission set the general direction for the organization.b. Strategy is a concise, internally-focused statement of how the organization expects tocomplete and deliver value to customers.c. Mission is a concise, externally-focused statement that expresses how theorganization wants to be perceived by the external world.d. Vision is about selecting the set of activities to create a sustainable difference in themarketplace.37. The purpose of the Balanced Scorecard is BEST described as helping an organization:a. develop customer relationsb. mobilize employee skills for continuous improvements in processing capabilities,quality, and response timesc. introduce innovative products and services desired by target customersd. translate an organization’s mission, vision, and strategy into a set of performancemeasures that help to implement the strategy38. The FIRST step to successful Balanced Scorecard implementation is clarifying:a. the organization’s mission, vision, and strategyb. who is the target customerc. the owner’s expectations about the return on investmentd. the objectives of all four balanced scorecard measurement perspectivesTHE FOLLOWING INFORMATION APPLIES TO QUESTIONS 39 AND 40.Stewart Corporation plans to grow by offering a sound system, the SS3000, which is superior and unique from the competition. Stewart believes that putting additional resources into R&D and staying ahead of the competition with technological innovations is critical to implementing its strategy.39. Stewart’s value proposition is:a. product innovation and leadershipb. best total costc. complete customer solutionsd. employees recognizing customer needs40. To further company strategy, measures on the Balanced Scorecard would MOST likelyinclude:a. shorter cycle timesb. manufacturing qualityc. yieldd. lowest cost supplierTHE FOLLOWING INFORMATION APPLIES TO QUESTIONS 41 AND 42.Riter Corporation manufactures water toys. It plans to grow by producing high-quality water toys at a low cost that are delivered in a timely manner. There are a number of other manufacturers who produce similar water toys. Riter believes that continuously improving its manufacturing processes and having satisfied employees are critical to implementing its strategy.41. Riter’s value proposition is:a. product innovation and leadershipb. complete customer solutionsc. employees recognizing customer needsd. best total cost42. To further company strategy, measures on the balanced scorecard would MOST likelyinclude:a. number of process improvementsb. first to marketc. longer cycle timesd. number of new products43. __________ are (is) best stated as action phrases that articulate what the organization hopesto accomplish.a. Measuresb. The value propositionc. Objectivesd. The balanced scorecard44. __________ describe(s) specifically how success in achieving objectives is determined.a. Measuresb. The value propositionc. Targetsd. The Balanced Scorecard45. __________ establish the level of performance or rate of improvement required for ameasure.a. Critical success factorsb. The value propositionc. The Balanced Scorecardd. Targets46. Identi fy the BEST description below of the Balanced Scorecard’s financial perspective. Toachieve our firm’s vision and strategy:a. How can we obtain greater profits for the current year?b. How should we appear to our shareholders?c. How will we obtain continuous improvements?d. How can we secure greater customer satisfaction?47. Identify the BEST description of the Balanced Scorecard’s internal perspective. To achieveour firm’s vision and strategy:a. How do we lower costs?b. How do we motivate employees?c. How can we obtain greater profits?d. What must we excel at to satisfy our customers and shareholders?48. All of the following questions relate to the Balanced Scorecard’s learning and growthperspective EXCEPT:a. How do we achieve greater employee satisfaction?b. How do we increase profits and return on capital?c. How do we provide information systems with updated technology?d. How will we sustain our ability to change and improve?49. Identify the BEST description of the Balanced Scorecard’s customer perspective. Toachieve our firm’s vision and strategy:a. How do we obtain a greater market share?b. What do our noncustomers consider to be most important?c. What new processes do our customers value?d. How do we obtain outcomes that meet or exceed customer expectations?50. The return-on-investment ratio is an example of a Balanced Scorecard measure of the:a. internal perspectiveb. customer perspectivec. learning and growth perspectived. financial perspective51. The number of complaints about a product is an example of a Balanced Scorecard measureof the:a. internal perspectiveb. customer perspectivec. learning and growth perspectived. financial perspective52. Manufacturing cycle efficiency is an example of a Balanced Scorecard measure of the:a. internal perspectiveb. customer perspectivec. learning and growth perspectived. financial perspective53. Surveys of employee satisfaction is an example of a Balanced Scorecard measure of the:a. internal perspectiveb. customer perspectivec. learning and growth perspectived. financial perspective54. Measures of the Balanced Scorecard’s customer perspective include:a. market shareb. number of on-time deliveriesc. number of process improvementsd. revenue growth55. The following statements are true regarding the financial perspective EXCEPT:a. Financial performance can be improved through two basic approaches – revenuegrowth and productivity.b. Financial objectives typically relate to profitability.c. A financial measure might be net income.d. A financial objective might be to offer low prices to satisfy and retain price-sensitivecustomers.56. The following statements are true regarding the customer perspective EXCEPT:a. Customer satisfaction leads to customer retentionb. A customer target might be to reduce cash expenses by 3%.c. Customer retention generally leads to increased customer profitabilityd. Success in the customer perspective should lead to improvement in the financialperspective.57. It is useful to think of the internal business processes perspective of the Balanced Scorecardwithin four groupings that include all of the following EXCEPT:a. operating processesb. customer satisfaction processesc. innovation processesd. regulatory and social processes58. Managers for the learning and growth perspective of the Balanced Scorecard must invest inall of the following EXCEPT:a. reducing development cycle timesb. improving the skills of their employeesc. enhancing information technology and systemsd. aligning people to the company’s objectives59. Key performance indicator cards are scorecards that are developed:a. with only a single measure for each of the Balanced Scorecard perspectivesb. without working from organizational strategyc. to be more effective than the balanced scorecardd. to define the compensation system for executives60. Key performance indicator cards:a. lead to local but not global or strategic improvementsb. include only financial measuresc. are organized into ten perspectivesd. measure only a single Balanced Scorecard perspective61. Nonprofit and government organizations:a. cannot use the Balanced Scorecard because they have no customersb. cannot use the Balanced Scorecard because they have no financial objectivec. may use the Balanced Scorecard by adding a social impact perspective to the top ofthe strategy mapd. may use the Balanced Scorecard by not linking it to mission and strategy62. Success for nonprofit and government organizations is measured primarily by:a. their financial performanceb. their effectiveness in providing benefits to constituentsc. whether they can raise moneyd. whether they can balance their budgets63. To effectively use the Balanced Scorecard, nonprofit and government organizations:a. must identify a clear strategy with outcomes and initiatives identifiedb. must identify an extended list of planned programsc. must shift thinking to what it plans to do, not what it plans to accomplishd. These organizations cannot effectively use the Balanced Scorecard.64. Nonprofit and government organizations:a. may identify the customer as the funder (taxpayer/donor) or the recipient of theservicesb. use the Balanced Scorecard to communicate mission and strategy more clearly toemployeesc. use the mission rather than shareholder objectives to drive strategyd. All of the above are correct.65. Measurement for the Balanced Scorecard:a. creates focus for the futureb. communicates an important message to all employeesc. focuses the entire organization on strategic implementationd. All of the above are correct.66. Translating the strategy to operational terms:a. is an analytical exerciseb. results in the benefit of having the end product of the scorecardc. often results in team building and commitment to the new strategyd. All of the above are correct.67. Which of the following statements regarding aligning the organization to strategy is true?a. Measures of individual business units must add up to the corporate measure, just likeaggregating financial measures.b. Support functions and shared units are exempt from the Balanced Scorecard processsince they have no external customer.c. High-level strategic objectives on the corporate scorecard guide the development ofBalanced Scorecards for the decentralized operating units.d. All of the above are correct.68. Which of the following statements regarding strategy is correct?a. All employees are challenged to develop team or individual objectives that supportcorporate objectives.b. CEOs and senior leadership can implement strategy by themselves.c. It is safe to assume that the workforce is incapable of understanding these conceptsand ideas.d. All of the above are correct.69. To become a strategy-focused organization:a. monthly management meetings should focus on variances between performance andwhat was plannedb. the budgeting process must protect long-term initiatives from the pressures to delivershort-term performancec. scorecards and priorities should be updated annually when preparing next year’sbudgetd. All of the above are correct.70. To mobilize change, leadership should:a. actively involve the executive teamb. continually focus on the change initiativesc. use teamwork to coordinate changesd. All of the above are correct.71. The greatest threat to successful Balanced Scorecard implementation is:a. poor scorecard designb. a poor organizational process for development and implementationc. too few scorecard measuresd. too many financial perspective measures72. Senior management, rather than middle management, must be actively involved in theBalanced Scorecard project because:a. middle management lacks understanding of the strategy for the entire organizationb. middle management lacks authorization to make decisionsc. senior management needs to build an emotional commitment to the strategyd. All of the above are correct.73. Successful implementation of the Balanced Scorecard:a. may be completed by one important member of the senior management team, such asthe chief financial officerb. involves everyone in the organization knowing and understanding the strategyc. should not begin until data are collected for all scorecard measuresd. starts with a process to acquire a new data collection systemEXERCISE/PROBLEM74. Draw a strategy map that identifies the cause-and-effect linkages of the followingobjectives:Process qualityCustomer loyaltySkilled production workersReturn on investment75. Draw a strategy map that identifies the cause-and-effect linkages of the followingobjectives:Market shareStrategic technology availabilityGrow revenuesDesign and develop new products76. Buck Corporation plans to grow by offering a computer monitor, the CM3000, which issuperior and unique from the competition. Buck believes that putting additional resources into R&D and staying ahead of the competition with technological innovations are critical to implementing its strategy.Required:a. Is Buck’s strategy one of product innovation and leadership, best total cost, orcomplete customer solutions? Briefly explain.Identify at least one key element that you would expect to see included in the BalancedScorecard:b. for the financial perspective;c. for the customer perspective;d. for the internal perspective; ande. for the learning and growth perspective.77. Maloney Corporation manufactures plastic water bottles. It plans to grow by producinghigh-quality water bottles at a low cost that are delivered in a timely manner. There are a number of other manufacturers who produce similar water bottles. Maloney believes that continuously improving its manufacturing processes and having satisfied employees are critical to implementing its strategy.Required:a. Is Maloney’s strategy one of product innovation and leadership, best total cost, orcomplete customer solutions? Briefly explain.Identify at least one key element that you would expect to see included in the Balanced Scorecard:b. for the financial perspective;c. for the customer perspective;d. for the internal perspective; ande. for the learning and growth perspective.CRITICAL THINKING/ESSAY78. Give at least two examples of knowledge-based intangible assets. Are knowledge-basedintangible assets critical for success? Explain.79. What are the four key perspectives in the Balanced Scorecard? In a strategy map, what arethe cause-and effect linkages among these four perspectives?80. What is the primary purpose of the Balanced Scorecard?81. What is a key performance indicator scorecard and how does it differ from the BalancedScorecard? Which is more effective?82. How does a Balanced Scorecard for nonprofit and government agencies differ from a for-profit scorecard?83. Describe at least two of the five principles that assist in making the transition to a strategy-focused organization.84. What is the key ingredient to successful Balanced Scorecard implementation? Explain.CHAPTER 9THE BALANCED SCORECARDTRUE/FALSELO1 1. a LO2 2. b LO2 3. a LO2 4. a LO3 5. aLO3 6. a LO3 7. a LO4 8. b LO4 9. a LO4 10. b LO4 11. b LO4 12. a LO5 13. b LO5 14. a LO6 15. b LO6 16. a LO7 17. a LO7 18. b LO8 19. b LO8 20. b MULTIPLE CHOICELO1 21. cLO1 22. aLO1 23. dLO1 24. cLO1 25. aLO2 26. bLO2 27. dLO2 28. dLO2 29. cLO2 30. cLO2 31. cLO2 32. bLO2 33. aLO2 34. cLO2 35. bLO3 36. aLO3 37. dLO3 38. aLO3 39. aLO3 40. bLO3 41. dLO3 42. aLO4 43. cLO4 44. aLO4 45. dLO4 46. bLO4 47. dLO4 48. bLO4 49. dLO4 50. dLO4 51. bLO4 52. aLO4 53. cLO4 54. aLO4 55. dLO4 56. bLO4 57. bLO4 58. aLO5 59. bLO5 60. aLO6 61. cLO6 62. bLO6 63. aLO6 64. dLO7 65. dLO7 66. dLO7 67. cLO7 68. aLO7 69. bLO7 70. dLO8 71. bLO8 72. dLO8 73. bEXERCISE/PROBLEMLO274. Skilled production workers → Process quality → Customer loyalty → Return oninvestmentLO275. Strategic technology availability → Design and develop new products → Market share →Grow revenuesLO2,3,476. Solution:a. Buck’s strategy is one of product innovation and leadership because the companyplans to offer a product that is superior and unique from the competition.The company’s Balanced Scorecard should describe the product innovation and leadership strategy. Key elements should include:b. operating income growth from charging higher margins for CM3000 for the financialperspective;c. market share in the high-end monitor market, customer satisfaction, and newcustomers for the customer perspective;d. manufacturing quality, new product features added, and order delivery time for theinternal business perspective; ande. development time for new features, improvements in manufacturing technologies,employee education and skill levels, and employee satisfaction for the learning andgrowth perspective.LO2,3,477. Solution:a. Maloney’s strategy is one of best total cost because there are a number of othermanufacturers who produce similar water bottles. To succeed, Maloney will have toachieve lower costs relative to competitors through productivity and efficiencyimprovements, elimination of waste, and tight cost controls.The company’s Balanced Scorecard should describe the best total cost strategy. Keyelements should include:b. operating income growth from productivity gains and growth for the financialperspective;c. growth in market share, new customers, customer responsiveness, and customersatisfaction for the customer perspective;d. yield, time to complete customer jobs, and order delivery time for the internalbusiness perspective; ande. number of process improvements, hours of employee training, and employeesatisfaction for the learning and growth perspective.CRITICAL THINKING/ESSAYLO178. Give at least two examples of knowledge-based intangible assets. Are knowledge-basedintangible assets critical for success? Explain.Solution: Yes, business has moved from the industrial age into the information age where knowledge-based intangible assets create value and are critical for success. Examplesinclude loyal and profitable customer relations, high-quality processes, innovative products and services, employee skills and motivation, and database and information systems.LO279. What are the four key perspectives in the Balanced Scorecard? In a strategy map, what arethe cause-and effect linkages among these four perspectives?Solution: The four key perspectives in the Balanced Scorecard are:a. the financial perspective;b. the customer perspective;c. the internal perspective; andd. the learning and growth perspective.In a strategy map, the learning and growth perspective causes improvement in the internal business processes perspective, which causes improvement in the customer perspective, which helps to attain the objectives of the financial perspective.Learning and growth → Internal → Customer → Financial perspectivesLO380. What is the primary purpose of the Balanced Scorecard?Solution: The primary purpose of the Balanced Scorecard is to translate an organization’s vision, mission, and strategy into a set of performance measures that put that strategy into action with clearly-stated objectives, measures, targets, and initiatives.LO581. What is a key performance indicator scorecard and how does it differ from the BalancedScorecard? Which is more effective?Solution: The Balanced Scorecard translates an organization’s strategy into a set ofperformance measures that put that strategy into action with clearly-stated objectives,whereas the key performance indicator scorecard does not link the performance indicators to a strategy. The Balanced Scorecard is more effective because it links objectives tostrategy.。

会计专业双语教学的SWOT分析

科技经济市场界发生的物理过程既看不见又摸不着也是瞬间即失,如果采用动画慢放的方式,这些就一目了然了。

人造地球卫星的发射、运转、接收过程是相当漫长的且无法进行实验观察,采用挂图进行讲解是定态的,采用动画快放的方式进行,学生就有一种身临其境的真实感。

当然选择和使用教学媒体的目的,是为了促进学生的学习,实现一定的教学目标,所选的媒体要能有效实现相应的教学事件和教学目标。

否则媒体选择和使用只是“作秀”,毫无实用价值,不能促进学生的思维,反而会影响教学效果。

参考文献:[1]加涅(美).皮连生等译.教学设计原理———当代心理科学名著译丛[M].华东师范大出版社,2004.[2]王嘉毅.课程与教学设计[M].高等教育出版社,2007.[3]朱美健,张军朋.谈物理课堂教学设计[J].物理教学探讨,2007,15(8):35-38.[4]Kenneth D,Moore.中学教学方法[M].中国轻工业出版社,2005.[5]吴剑藩.创新性物理教学设计[J].浙江教育学院学报,2001,3(2):106-108.SWOT分别代表strengths(优势)、weaknesses(劣势)、opport-unities(机会)、threats(威胁)。

SWOT分析通过对优势、劣势、机会和威胁加以综合评估与分析得出结论,然后再调整企业资源及企业策略,来达成企业的目标。

本文借助SWOT分析会计专业双语教学,大力发挥有利于会计双语教学发展的因素,去除或尽量减少不利因素的影响,抓住机遇迎接挑战,促进会计专业双语教学不断提高与完善,适应我国经济化发展的需求。

1会计专业双语教学面临的机遇和威胁进入21世纪的今天,经济、社会、科技等诸多方面的迅速发展,我国社会的国际化程度越来越高。

世界经济一体化进程的加快,国际间的交往日益频繁,企业所处的环境更为开放和动荡,对人才的期许越来越高,对国际化的人才需求越来越迫切。

会计工作作为企业管理的重要组成部分,更是需要既懂专业外语能力又强的人才。

《管理会计》双语案例教学实例分析

总额 因业务量 的变动而成正 比例变动 ,但单位变动成本

( 单位业务量负担的变动成本) 不变。 ③混合成本。 混合成本

就是“ 混合” 了固定成本和变动成本两种不 同性质的成本 。 方面 , 它们要随业务量 的变化而变化 ; 另一方面, 它们的 变化又不能与业务量 的变化保持着纯粹 的正比例关系。 混

程展示给所有的学生 , 把其中出现的问题带到学生的思考中

去解决 。 例如在 教学角 的度量 时 , 利用投 影把量角器放 大 , 学 生结合 自己手 中的量角器一起认识各部分的功能, 更具有影

响力。 教学角的量法, 教师可以在投影仪下操作 , 学生一边听 着操作过程 , 一边看着教师操作, 把头脑 中听到的影像与实 际操作结合起来 , 更真切的体会了测量的过程。 之后的练习, 学生也可以借助投影仪把 自己的操作过程展示给全体学生 , 这其中出现的一些问题 , 在学生中就解决了。现代化的教学 硬件设施把学生的眼睛擦的更亮了, 把学生大的思维擦的更 敏捷了, 把知识展现的更全面具体了。 除了硬件的应用 , 软件 的音像教材 , 如教学幻灯片、 投

中图分 类号 : G 6 4 2 . 0 文献标 志码 : A 文章编 号 : 1 6 7 4 — 9 3 2 4 ( 2 O 1 3 ) 2 4 - 0 0 5 0 — 0 3

案例教学法是一种启发学生研究实际问题 , 注重学生 智力开发及能力培养的现代教学方法 , 它有着传统教学方 法所不具备的特殊功能。《 管理会计》 课程实践性强 , 采用 案 例教 学 模 式 , 给予 学 生积 极 思 考 、 用英 语 踊 跃 发 言 的 自 我表现机会 , 加深学生对学科基础知识在实践中运用的理 解, 通过用英语讨论 , 使得学生专业知识和英语语言均得 到 提高 , 同时使 学 生对 实 际工作 中出现 的问题 获得 较 正 确 和透彻 的理解。 本文拟 以《 管理会计》 中成本性态 的知识介 绍案例教学方法如何在双语教学 中组织和开展的。

《管理会计(双语)》教学大纲

《管理会计(双语)》课程教学大纲课程编码:12120203k206课程性质:专业必修课学分:3课时:48开课学期:第五学期适用专业:会计学一、课程简介《管理会计(双语》是会计学专业(本科)的一门必修课程。

是以现代企业所处的社会经济环境为背景,明确阐明以企业为主体,密切联系现代会计的预测、决策、规划、控制、考核评价等职能,系统地介绍了现代管理会计的基本理论、基本方法和实用操作技术。

课程分为三部分,第一部分主要交代了管理会计的基本原理和传统管理会计的基本方法;第二部分主要分别讨论管理会计各项职能在实践中的应用程序与具体操作方法。

第三部分集中介绍管理会计发展的新领域。

管理会计是一门理论性较强、计算内容较多的课程。

通过该门课程的学习,使学生领会管理会计的精髓,掌握管理会计的基本理论和基本方法,学会各种分析方法的应用技能和技巧,不断提高学生分析问题和解决问题的能力。

二、教学目标课程总体目标:通过本课程教学,掌握管理会计的基本理论和基本分析方法,结合相应的实践教学,培养学生能独立开展各项管理会计工作的能力。

具体入下:1.了解管理会计的产生与发展,明确管理会计的特点、职能、内容和任务;2.掌握成本习性与变动成本法、本量利分析等管理会计基础分析方法,并了解方法的一般原理;3.掌握短期经营决策分析、长期投资决策分析、全面预算、标准成本控制、责任会计等内容的基本理论与方法。

三、教学内容(一)Chapter 1 Managerial Accounting Concepts and PrinciplesThe main content: Chapter 1 introduces students to managerial accounting and the manufacturing process. Students will learn how managerial accounting is used in the management decision process. They will also be exposed to the terminology used to describe costs related to manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe managerial accounting and the role of managerial accounting in a business.2. Define and illustrate the following costs: 1. direct and indirect costs, 2. direct materials,direct labor, and factory overhead costs, 3. product and period costs.3. Describe and illustrate the following statements for a manufacturing business: 1.balance sheet, 2. statement of cost of goods manufactured, 3. income statement.4. Describe the uses of managerial accounting information.Some key points: direct and indirect costs, direct materials, direct labor, factory overhead costs, product and period costs; cost of goods manufactured.Teaching methods: use of multimedia tools. We ad opt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(二)Chapter 2Job Order CostingThe main content:Chapter 2 introduces students to managerial job order cost systems. Students will be exposed to the terminology used to describe costs related to manufacturing. The first of two basic manufacturing accounting systems, job order, is described in this chapter. Students learn how costs flow through a manufacturing system and the basis for determining product costs under job order costing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe cost accounting systems used by manufacturing businesses.2. Describe and illustrate a job order cost accounting system.3. Describe the use of job order cost information for decision making.4. Describe the flow of costs for a service business that uses a job order cost accountingsystem.Some key points: Job Order Cost System; Overapplied Factory Overhead; Underapplied Factory Overhead; predetermined overhead rate;Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is suppl emented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(三)Chapter 3Process Cost SystemsThe main content:Chapter 3 completes the coverage of manufacturing accounting by introducing process costing. The text demonstrates process costing under the FIFO method.The average cost method is presented in th e chapter’s appendix. Chapter 3 also discusses the impact of just-in-time systems on manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe process cost systems.2. Prepare a cost of production report.3. Journalize entries for transactions using a process cost system.4. Describe and illustrate the use of cost of production reports for decision making.5. Compare just-in-time processing with traditional manufacturing processing.Some key points: Process Cost System; First-in, First-out (FIFO) Method; Cost of Production Report; Just-in-Time (JIT) Processing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(四)Chapter 4 Cost Behavior and Cost-Volume-Profit AnalysisThe main content: In Chapter 4, students learn how to conduct cost-volume-profit analysis. In preparation for this activity, the chapter discusses variable, fixed, and mixed costs.Learning Objectives:After studying the chapter, your students should be able to:1. Classify costs as variable costs, fixed costs, or mixed costs.2. Compute the contribution margin, the contribution margin ratio, and the unitcontribution margin.3. Determine the break-even point and sales necessary to achieve a target profit.4. Using a cost-volume-profit chart and a profit-volume chart, determine the break-evenpoint and sales necessary to achieve a target profit.5. Compute the break-even point for a company selling more than one product, theoperating leverage, and the margin of safety.Some key points:variable costs; fixed costs; mixed costs; High-Low Method; Contribution Margin; Cost-Volume-Profit Analysis; Contribution Margin Ratio; Unit Contribution Margin.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(五)Chapter 5 BudgetingThe main content: Chapter 5 emphasizes accounting activities that help managers plan, direct, and control the operations of a business. Budgeting is used to establish business goals in the planning function. Budgets help guide managers’ operational decisions. Budgets are also used to control operations as actual results are compared to the budgeted results.Learning Objectives:After studying the chapter, your students should be able to:1. Describe budgeting, its objectives, and its impact on human behavior.2. Describe the basic elements of the budget process, the two major types of budgeting,and the use of computers in budgeting.3. Describe the master budget for a manufacturing company.4. Prepare the basic income statement budgets for a manufacturing company.5. Prepare balance sheet budgets for a manufacturing company.Some key points: Goal Conflict;Budgetary Slack;Continuous Budgeting;Static Budget;Flexible Budget;Zero-Based Budgeting;Capital Expenditures Budget.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(六)Chapter 6 Performance Evaluation Using Variances from Standard Costs The main content: Standard cost systems set budgets for the materials, labor, and factory overhead used by a manufacturer to produce its product. Deviations from these standards are reported as variances.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the types of standards and how they are established.2. Describe and illustrate how standards are used in budgeting.3. Compute and interpret direct materials and direct labor variances.4. Compute and interpret factory overhead controllable and volume variances.5. Journalize the entries for recording standards in the accounts and prepare an incomestatement that includes variances from standard.6. Describe and provide examples of nonfinancial performance measures.Some key points: Direct Labor Rate Variance ;Direct Materials Price Variance;Direct Labor Time Variance;Direct Materials Quantity Variance;Budgeted Variable Factory Overhead;Factory Overhead Cost Variance Report;Controllable Variance;Volume Variance.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(七)Chapter 7 Performance Evaluation for Decentralized Operations The main content: Chapter 7 applies responsibility accounting to cost, profit, and investment centers. The chapter demonstrates the responsibility accounting reports that are used to evaluate department or division performance. This provides an excellent opportunity to remind your students that managers are judged, at least in part, using accounting data.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the advantages and disadvantages of decentralized operations.2. Prepare a responsibility accounting report for a cost center.3. Prepare responsibility accounting reports for a profit center.4. Compute and interpret the rate of return on investment, the residual income, and thebalanced scorecard for an investment center.5. Describe and illustrate how the market price, negotiated price, and cost priceapproaches to transfer pricing may be used by decentralized segments of a business.Some key points:Responsibility Accounting;Balanced Scorecard;Profit Margin;DuPont Formula;Rate of Return on Investment (ROI);Investment Center ;Residual Income;Investment TurnoverTeaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(八)Chapter 8 Differential Analysis, Product Pricing, and Activity-Based Costing The main content: This chapter covers (1) differential analysis, (2) methods of determining the selling price of a product using a cost-plus markup approach, (3) the effects of production bottlenecks, and (4) activity-based costing. The cost-plus approach of product cost is described in Objective 2; total cost and variable cost methods are presented in thechapter appendix. All topics in this chapter are able to stand alone. Therefore, the instructor is free to cover only one or two of the topics if class time is a limited resource as the term draws to a close.Learning Objectives:After studying the chapter, your students should be able to:1. Prepare differential analysis reports for a variety of managerial decisions.2. Determine the selling price of a product, using the product cost concept.3. Compute the relative profitability of products in bottleneck production processes.4. Allocate product costs using activity-based costing.Some key points:Product Cost Concept ; Target Costing; Production Bottleneck; Theory of Constraints (TOC); Activity-Based Costing (ABC).Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(九)Chapter 9 Capital Investment AnalysisThe main content: Capital investment analysis is a topic that usually receives detailed coverage in introductory finance courses and/or intermediate accounting. The purpose of this chapter is to give students a brief introduction to the basics of capital investment analysis using the following methods: average rate of return, cash payback, net present value, and internal rate of return.Learning Objectives:After studying the chapter, your students should be able to:1. Explain the nature and importance of capital investment analysis.2. Evaluate capital investment proposals using the average rate of return and cashpayback methods.3. Evaluate capital investment proposals using the net present value and internal rate ofreturn methods.4. List and describe factors that complicate capital investment analysis.5. Diagram the capital rationing process.Some key points: Capital Investment Analysis;Time Value of Money Concept;Average Rate of Return;Cash Payback Period;Internal Rate of Return (IRR) Method;Capital Rationing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.四、整体课时分配五、实验教学1. 实验项目与课时分配3.实验报告The basic requirements of the experiment report, including: name of the experiment, purpose of the experiment, case data, case analysis, conclusions and enlightenment.六、课程考核与成绩评定1.考核方式:考查;笔试;闭卷。

管理会计双语版总结

Static budget Flexible budget Static budget variance

Sales volume variance Flexible budget variance

Favorable variance and unfavorable variance Management by exception

16

Types of Problems

A. Equipment Replacement

Sunk Costs & Depreciation

B. Special Order

Fixed Cost & Opportunity Costs

C. Outsourcing: Make or Buy Decision

Comparison of traditional and ABC overhead allocation

6

Major Points of Cost Allocation

1 2 3

4

Why allocate? How much to allocate?

Allocate to whom? How to allocate?

7

Chapter 5 : Cost Behavior

Common cost behavior patterns

Fixed costs : think as total Variable costs : think on a per-unit basis Relevant range

Mixed costs and its separation

2

Chapter 2 :Classifying Costs

管理会计第十二版 全英课件 appendix A

Price elasticity of demand

McGraw-Hill/Irwin

Copyright 2008, The McGraw-Hill Companies, Inc.

A-8

Price Elasticity of Demand

Suppose the managers of Nature's Garden believe that every 10 percent increase in the selling price of its applealmond shampoo will result in a 15 percent decrease in the number of bottles of shampoo sold. Let's calculate the price elasticity of demand. For its strawberry glycerin soap, managers of Nature's Garden believe that the company will experience a 20 percent decrease in unit sales if its price is increased by 10 percent. percent

McGraw-Hill/Irwin Copyright 2008, The McGraw-Hill Companies, Inc.

A-6

Price Elasticity of Demand

As a manager, you should set higher (lower markups over cost when lower) demand is inelastic (elastic elastic)

管理会计 双语课件 Management accounting

03 作业

High-Tech

Globalization

Economic Transition

03 作业 Need for innovation and relevant produces: – Activity-based management • ABC Improves accuracy of assigning costs

– Customer orientation

• Strategic positioning to maintain competitive advantage

• Value chain framework to focus on customer value

– Total quality management emphasized continuous improvement

1950-1980 1980-

Most of the product-costing and internal accounting procedures used in the last century were developed.

Emphasis of accounting information for internal management . Management accounting practices developed, including: Flexible budgeting, Standard costs, Variance analysis, transfer prices et al.

03 管理会计的定义

1 、国外会计学界的定义 1 )狭义管理会计 管理会计知识为企业内部管理者提供规划和控制所需信息的内部会计。 • 为企业管理当局的管理目标服务。

《管理会计(双语)》课程 (5)

Time-Driven ABC

Use parameter estimates to assign indirect costs: Cost of using resource i by product j =

Capacity cost rate of resource i x Quantity of capacity of resource i used

Time-driven activity-based costing systems (TDABC or Time-Driven ABC) estimate two parameters and then assign indirect costs similar to the way direct costs are assigned

by product j

8

TDABC Profitability Report

Refer to Madison Dairy’s report, Exhibit 5-5 The results from the time-driven activity-based

costing system were quite different from the results based on the traditional cost system

Committed costs become variable via a two-st resources change either because of changes in the quantity of activities performed or because of changes in the efficiency of performing activities

高级管理会计双语课程大纲

高级管理会计双语课程大纲课程名称:高级管理会计(双语)/Advanced Management Accounting (Bilingual)课程编号:241075课程属性:专业教育选修课授课对象:会计学专业本科生总学时/学分:48/3开课学期:第7学期执笔人:先修课程:中级财务会计(上)、编写日期:中级财务会计(下)、管理会计一、课程概述本课程主要讲述管理会计领域中更深层次的内容,其所涉及到的内容包括:管理会计和管理决策之间的关系、决策实务框架内容、决策过程中所涉及的各种深层次问题、当前管理会计最新使用的实务方法、作业本钱法和作业管理内容、管理会计所涉及的代理理论、转移价格的制定及对业绩的影响、管理会计中深层次的道德内容,以及管理会计各种知识内容的整合。

通过本课程学习,学生将在更深的层次上理解管理会计相关理论和实践内容。

This course focuses on the field of deeper content of management accounting.The contents include the relationship between management accounting and management decision-making, decision-making practice frame content, a variety of deep-seated problems involved in the decision-making process, current methods of management accounting practices, activity-based costing method, agency theory in management accounting,transfer pricing and its influence on performance, deep moral content of management accounting, as well as a variety of integrated management accounting knowledge content. Through this course, students will understand the theory and practice of management accounting-related content on a deeper level.二、课程目标1.掌握开展管理会计中所涉及的决策过程相关问题的处理和当前最新的管理会计实务方法;2.熟悉管理会计中决策的作用、实务工作中完成决策工作的必要环节和框架结构、作业本钱法和作业管理的机理和操作、绩效管理中转移价格政策所造成的影响、管理会计实践过程中的道德问题;3.学会当前最新管理会计实务方法的应用、作业本钱法和作业管理的实施以及转移价格的制定;4. 了解管理会计所涉及的深层次的理论,如:代理理论,管理会计实践过程中的道德问题形成的机理等内容。

高校双语教学实践研究——基于“管理会计”双语教学的思考

高 校 双 语 教 学 实 践 研 究

基于“ 管理会计” 双语教学 的思考

上 海 立信 会 计 学院 立信 会 计研 究院 李 颖琦

【 要 】 目前 , 国各 高校都在 从培 养 “ 个面 向” 才 的战略 高度 来 不断推 进 双语 教学 实践 本文对 “ 摘 我 三 人 管理 会 计” 双语 教 学

二、 管理会 计” 双 语教 学的 实施 及 “

相关 问题 的探讨

专 业 教 学 ,获 取 学 科 知 识 是 双语 教 学 致使课前预习没有实际效果而最终放弃 , 的核 心 和 重点 。

学习效率较低。 这就需要教师在进行双语 教学前要合理评价授课水平与学生素质,

明 确双语 教 学的基 本条 件 与学生 的 可接 受性 ,并以此为基 础充分 准备教 学资料 , 指导学生 进行课前预 习。 这些教学 资料应

业知识和技能 , 力培养学生的国际意 着 识、国际交往能力和国际竞争能 力, 并 为今后 进入 的专业研究打下 良好的基 础 。“ 管理会计 ”作为会计专业的核心

国际化会计专业人 才的需求不断增长 , 这对我国高校的会计教育提出了更高的

要 求 。 同时 , 育 部 2 0 年 颁 布 《 自教 01 关

( ) 语教 材的 选 用 一 双

要 进行 高质 量的 双语 教 学 ,必须 选 该包括全英文的教材、 教学大纲、 授课专

于加强高等学校本科教学工作 提高教 择恰当的双语教材 ,教师要兼顾教材内

其要 补充 难 度适 中的 阅读材 料 ,以扩展 专 题主要 内容 ,列 出关键 词并 加以解释 , 学生 的知识 面 , 学生 的 求知 欲 。 培养 ( ) 二 双语教 学 准备 与实 践 通过例 题讲解加 深对理论 的理解 , 根据时 间提 出一些小 问题让学生 解答 , 引导 着重

关于《管理会计》双语本科教学的思考

i f o tn s be t , n o ne t u jc” 直译 的含义是“ g c 能

在学校 里使用第二语言或 外语进行各 门学

科的教 学” 。

就 目前我 国高等 教 育的现 状来 看 , 双 语教 学主要 指用汉语和英语课 堂讲授英 文

维普资讯

【 摘要 】 笔者通过 对 管理会计》 双语教

学 的 经 验 和 体 会 , 阐述 了对 双语 教 学 的 认

0 乏 60s 也 乜 §e60 e§邑 s s 0

0 ‰

识+ 探讨 了双语教学师资的培 养厦教材的选

择、 中英 文授课语 言的比例 、 与学互动和 教 突出启发式教学、 情景教学方法等 问题

一

: 专家型” , 应是“ 人才 具有 次才是具备 良 好英语素 管理会计发展至今 , 其学 哦和方法 , 双语教学首先 能够通晓管理 会计的发 通 畅的信息交流, 使得这 容易达到。 目 管理会 前《 : 问题仍然是语言。 教学任务 的教 师,学校 训计划。 者认 为, 笔 近年

关于《 管理会计》 §

署本科教学的思考

京财经 大学会计 学院 郭春 明 中亚楠 / 稿 撰

∽

构建国际化 的会计教育 。 是会计专业双 语教学 的切八点 。 管理会计作为-1边缘学 -" 7 科,自 2 世纪初产生以来得到了迅速的发 0 展, 在会计 中具有越来越重要 的地位 。许 多 财经类院校都对该课程实施了双语教学 , 一 方面可 以使 学生更好 地 了解 和理 解管理会 计的理论 及前沿 ; 另一方面对我国管理会计 理论和实务的发展也有好处。 笔者在两个学 期《 管理会计》 双语教学中遇 到不少 问题 , 现

高校会计专业开展双语教学的几点思考

间 的衔 接 ; 一方 面 可 以 交 流 教 学 信 息 , 如 聘 请 外 另 比

高等教育 要根据社 会 的需要 , 教学 内容 、 程 籍教师 、 对 课 留学 国 外 多 年 的华 裔 教 师 、 内 其 他 高 校 的 国 体 制 、 学方 法 和 教 学 手 段 进 行 不 断 改 革 。高 教 改 革 名 师 为 客 座 教 授 ,讲 授 会 计 专 业课 或 开 设 专 题 讲 座 教 的重 要 举 措 之 一 就 是 双 语 教 学 , 成 为全 国各 个 高校 等 , 强 外 语 学 习 的氛 尉 , 系统 化 、 范 化 地 开 展 会 它 增 并 规

、

开 展会 计 双 语 教 学 的意 义

( ) 计 双 语 教 学是 全 球 化 经 济 的 必 然 选 择 , 已 成 为 限 制 会 计 双 语 教 学 提 高 层 次 和 扩 大 发 展 的 一 会 是培养创新人才的需要

在 国 际化 、 息 化 、 球 化 的 大 背 景 下 , 想 提 高 业 教 师 朝 双 语 方 向发 展 , 台切 实 可行 的 会 计 双 语 师 信 全 要 出 综合国力 , 关键 在 于 科 技 创 新 , 才创 新 。 了培 养能 资 培 养 计 划 , 括 确 定 培 养 对 象 、 定实 施 培 养 方 案 、 人 为 包 制

管理会计 学研 究。

[ 中图分类号】 G4. 620

【 文献标识码】 A 【 文章编号】 10— 17 20 )70— 11O 24 ( 06 0/8 05一2 0 0

2 o ̄ o 1 -8月 1 7日教 育 部 颁 发 了 《 于加 强 高 等 的高 素 质 人 才 有重 要 意 义 。 关 学 校 本 科 教 学 工 作 提 高 教 学 质 量 的 若 干 意 见 》 的通

管理会计第十三版英文影印版教学设计

Managerial Accounting 13th Edition English PhotocopyTeaching DesignIntroductionManagerial accounting is a critical component of any business operation as it ds in decision-making, provides financial informationfor internal use, and helps management in controlling costs andfinancial risks. As such, it is essential that students of accounting and business have a clear understanding of managerial accounting and its practical applications.The 13th edition of Managerial Accounting, an English photocopy version, provides in-depth coverage of the subject matter and helps students develop a strong foundation of knowledge for their future careers. The purpose of this teaching design is to provide an outline of the topics and teaching methods for the 13th edition of Managerial Accounting.Course OverviewCourse TitleManagerial AccountingCourse DescriptionThe course is designed for students who have a basic knowledge of financial accounting and wish to gn a deeper understanding of managerial accounting concepts. The course covers topics such as cost behavior,cost-volume-profit analysis, budgeting, responsibility accounting, and capital budgeting.Course GoalsThe primary goal of the course is to enable students to understand the fundamental principles of managerial accounting and how they can be applied in real-world situations. Specifically, the course ms to: •Develop students’ understanding of cost behavior and how to use it to make business decisions•Provide students with the skills to analyze and interpret financial information for internal use•Help students understand the various types of budgets and how they are used in managerial accounting•Develop students’ understanding of responsibility accounting and how it can be used to monitor performance•Help students understand the process of capital budgeting and how to evaluate investment projectsCourse Requirements•Attend lectures and participate in class discussions•Complete assigned readings and homework•Take quizzes and examsTeaching MethodologyLecturesThe course will be delivered through a series of lectures. In these lectures, the instructor will use a combination of PowerPointpresentations, case studies, and group discussions to illustrate key concepts and reinforce understanding. Lectures are designed to provide students with a comprehensive understanding of each topic covered in the course.Case StudiesCase studies are an important element of the course as they help students apply what they have learned in real-world situations. Students will be assigned case studies that require them to analyze financial data, interpret budgets, and make business decisions based on the information provided.Group DiscussionsGroup discussions will enable students to share their experiencesand perspectives on various managerial accounting concepts. They will be encouraged to provide insight on how the concepts can be applied intheir future careers and to generate ideas for resolving business issues.Quizzes and ExamsQuizzes and exams are designed to evaluate stude nts’ comprehensionof the course materials. Students will be tested on their understanding of key managerial accounting concepts and their ability to analyze financial data, interpret budgets, and make business decisions based on the information provided.AssessmentAssessment of student learning will be based on the following: •Quizzes (25%)•Midterm Exam (35%)•Final Exam (40%)ConclusionThe 13th edition of Managerial Accounting provides students with a comprehensive understanding of managerial accounting concepts and their practical applications. Through the use of lectures, case studies, and group discussions, students will be able to apply what they have learned in real-world situations and develop a strong foundation of knowledge that will serve them well in their future careers.。

全英文教学模式下关于管理会计的教学方法研究

全英文教学模式下关于管理会计的教学方法研究近年来,全球范围内的英语教育模式逐渐普及,全英文教学模式在大学教育中也越来越受到重视。

在商学院的管理会计教学中,采用全英文教学模式是否能够有效提高学生的学习效果是一个备受关注的问题。

本文旨在探讨全英文教学模式下关于管理会计的教学方法,并提出一些可行的建议。

为了更好地探讨全英文教学模式下的管理会计教学方法,首先需要明确全英文教学模式的意义和意义。

全英文教学模式即是指在课堂上使用英文作为主要的授课语言,包括讲义、教学资料、教学互动等都以英文进行。

在当今全球化的背景下,英语作为国际商务交流的主要语言之一,掌握英语已经成为现代商业人士的基本素养。

在商学院的管理会计课程中引入全英文教学模式,不仅可以帮助学生提高英语水平,更能够更好地理解和应用管理会计知识。

在管理会计的教学中,全英文教学模式下的教学方法需要灵活多样。

教师在选择教学内容和讲解时要尽量简洁明了,避免使用过多复杂的语言和术语。

教学过程中应加强与学生的互动,鼓励学生积极参与讨论和提问,以促进学生的思维深度和广度。

还可以采用案例教学的方式,让学生在实际案例中运用英语进行分析和讨论,从而更好地理解和掌握管理会计的知识和技能。

在全英文教学模式下,学生也需要做好相应的准备工作。

学生需要提前预习相关的英文资料,熟悉相关的英语单词和句型,以便更好地理解和接受教师的授课。

学生需要加强英语口语和写作的练习,提高自己的英语表达能力和沟通能力。

学生还要能够积极参与课堂的讨论和互动,提出自己的见解和观点,与教师和同学们共同探讨问题,从而更好地提高自己的学习效果。

在实际的教学中,全英文教学模式下的管理会计教学可以采用以下的教学方法:教师可以结合具体的案例和企业实践,让学生在实际案例中了解和分析各种管理会计方法和工具,同时学生也需要用英语进行相关的讨论和解答,从而锻炼自己的英语表达能力。

教师可以利用多媒体和互动课件进行教学,通过图片、图表、视频等形式生动直观地呈现管理会计知识,同时也可以与学生进行互动讨论,激发学生的学习兴趣和积极性。

《管理会计(双语)》课程 (9)

MACS should incorporate the principles of an organization’s code of ethical conduct

Empowering employees to be involved in decision making and MACS design

Developing an appropriate incentive system to reward performance

3

Impact of MACS on Behavior

Ethical considerations listed in descending order of authority:

– Legal rules – Societal norms – Professional memberships – Organizational/group norms – Personal norms

One step is to maintain a hierarchy of authority

14

Role of Senior Management

A critical variable that can reduce ethical conflicts is the way that the chief executive and other senior managers behave and conduct business

6

Central Assumptions of HRMM

Employees have a great deal of knowledge and information about their jobs, the application of which will improve the way they perform tasks and benefit the organization as a whole

基于雨课堂和网络教学平台的《管理会计》双语教学实践

基于雨课堂和网络教学平台的《管理会计》双语教学实践近年来,随着互联网技术和移动互联网的飞速发展,网络教学平台在高校教育中扮演了越来越重要的角色。

雨课堂是一款以视频直播和互动教学为核心的在线教育平台,为教育行业提供了全新的教学方式和教学资源。

在这样一个背景下,本文将探讨基于雨课堂和网络教学平台的《管理会计》双语教学实践的相关内容。

一、教学平台的选择网络教学平台的选择对于双语教学的开展非常重要。

在本次实践中,我们选择了雨课堂作为主要的教学平台。

雨课堂是一款集直播、录播、互动、资源管理等多种功能于一身的在线教育平台,能够为双语教学提供良好的技术支持和教学环境。

通过雨课堂,学生可以在家通过网络直播收听中文讲课,同时也可以在课堂上通过摄像头和麦克风和老师进行双语互动交流,这样就能够真正地实现全球范围内的双语教学。

二、教学内容的设计在双语教学中,教学内容的设计是至关重要的。

在《管理会计》这门课程中,我们需要做到既注重理论知识的讲解,同时也要注重实践案例和应用技能的培养。

在教学内容的设计上,我们采取了理论与实践相结合的方式,通过中文讲授基础知识,然后通过案例分析和讨论,引导学生深入理解和应用知识。

双语教学有着自己独特的教学方法。

在《管理会计》的双语教学实践中,我们采取了多种灵活的教学方法。

在中文讲授环节,老师会以清晰、流畅的中文讲授基础理论知识,让学生在听讲的过程中积累知识。

在案例分析和讨论环节,老师会以中英文双语进行交流,引导学生深入理解和应用知识。

通过实践操作和作业等方式,巩固学生所学的知识。

四、教学实践的效果通过基于雨课堂和网络教学平台的《管理会计》双语教学实践,我们取得了一定的成效。

学生在听讲和讨论中逐渐掌握了管理会计的基本理论和知识。

在案例分析和实践操作中,学生能够运用所学知识解决实际问题,培养了实战能力。

通过线上线下相结合的教学方式,学生对双语教学产生了浓厚的兴趣,积极参与到教学活动中去。

学生的学习成绩得到了一定的提升,提高了学生的学习积极性和主动性。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

管理会计双语教学

当前世界经济的一个显著特点是经济全球化,越来越多的公司正超越

国与国的界限,演变为全球性公司,采用全球化架构、全球化战略。

双语教学是适应国际趋势需要的选择,可以培养受教育者形成“双语、双文、双能”的素养。

就会计专业而言,经济环境的变迁要求会计类

人才不仅具有专业知识,也要具有先进的国际思维和先进的理念。

一、管理会计双语教学的意义

管理会计是21世纪较为前沿的学科之一。

管理会计直接源于西方,

且西方理论与实务水平均远远高于国内发展水平。

对管理会计开展双

语教学,一方面可以使学生更好地理解管理会计的理论及前沿知识;

另一方面对我国国内管理会计理论与实务的发展也非常有益处。

管理

会计双语教学不仅可以拓展学生的英语知识,而且可以促进学生用英

语思考企业管理中遇到的问题,培养学生用国际思维逻辑解决问题的

能力。

双语教学的一个重要特点是通常采用原版教材。

教材是双语教学开展

的必要物质载体。

国内的中文版教材更多倾向于理论的阐述,而缺少

现实的案例分析。

这样,学习国内教材的学生可能会对理论较为熟悉,而在将这些理论运用到实际中解决现实问题时则会力不从心。

而实行

双语教学,运用原版教材可以使学生学习到国际先进的教学模式,能

够比较多的接触到国外最新的发展情况,使教与学及时跟踪学科发展

的脚步,从而能够研究和借鉴国际上先进的管理思想、方法和国际案例,形成运用全球性思维思考问题的习惯。

另外,原版教材一般翔实

生动,而且在不同章节均安排了具体的案例分析,这些案例有假设的,也有实际的,如阿特金森、卡普兰等所著教材《managementaccounting》中就列举了安然公司、华尔街时报、迈罗

银行等不同企业的情况,而且将管理会计的理念扩展到政府和非盈利

组织,列举了军队和政府部门对于平衡计分卡的运用。

采用案例教学

能够激起学生的学习兴趣和积极性,培养学生的思维能力和实际解决

问题的能力,使学生在不同性质的单位工作时都能够较为灵活地运用

相关管理会计的理念。

二、我国管理会计双语教学的现状分析

管理会计双语教学具有重大的积极意义。

但是,从我国高校双语教学

的现状来看,当前的师资力量、学生综合素质、教学方法、教学模式

等方面均无法保证双语教学的顺利开展,也影响了双语教学效果的充

分体现。

在师资力量上,教师双语教学的能力和方式有待进一步提升。

在目前

的双语教学中,师资是限制各高校提升层次和扩大发展的“瓶颈”。

进行双语教学的教师不仅要具有专业知识,还需要过硬的外语水平,

包括掌握准确的专业词汇、标准的发音等,还需要掌握外语授课的技巧,能够用简单的外语把问题解释清楚,同时还要求能够引导学生用

西方的思维方式对所讲授的内容进行分析。

目前在大多数院校,能够

有效驾驭语言能力和专业知识,并且又有丰富教学经验的双语教师还

为数不多。

另外,我国双语教学开展时间相对较短,与国外高校专门

针对教学方面的交流机制还没有形成,教学方式上还不能将教学内容

和教学语言完全有效融合起来,现实中比较普遍地存有着英文教材、

英文内容与用汉语授课的中英文分离现象。

作为教学对象和主要目标的学生,其英语水平、专业知识基础、社会

实践精力、学习兴趣动机和态度等都决定或影响双语教学的成效。

作

者对本校学习双语管理会计的学生作了简单统计:对于会计专业的学生,30%的能够理解上课所讲知识点,并能够独立完成练习题;40%的

学生能够基本了解所学知识点,练习题独立完成有难度,在小组讨论

的情况下可以完成。

在原因上,主要有:一方面因为英语水平参差不齐,心理上还存有“畏难”心理,对英语教材和板书无从下手,不知

如何预习和复(论文网)习;另一方面因为对管理会计原版教材的逻辑

顺序存有一个适应和接受的过程,所以,通常在刚开课的一段时间里,还不能积极主动地运用原版教材的思维进行思考,导致教学效果不很

理想。

另外,现实教学中存有着教学策略比较单

一、教学方式比较单调的情况,缺少教师与学生“教”与“学”的充

分互动,没有让学生充分融入到课程的学习中。

管理会计原版教材内

容非常丰富,但是,受到有限课时的限制,同时也受传统授课方式的

影响,“讲课+考试”仍构成了大多数教师教学活动的主体,双语教学

方式比较单一,授课存有以译代讲的现象,小组进行案例讨论的机会

很少,没有充分调动学生的主动性。

三、改进管理会计双语教学的相关对策

管理会计双语教学是适应时代发展的应时之举,不过国内真正意义上

的管理会计双语教学模式尚未形成,需经过一定的经验积累,在实践

中持续探索,才能逐渐成熟,达到预期目标。

双语教学不但是教学内容、教学方法、教材及课程设置、师资培养等方面的改革与调整,而

且涉及到人才培养目标与规格等深层次的问题,可谓牵一发而动全身。

规范管理会计教学模式,保证双语教学效果,不是单从某个方面可以

做到的,需要从师资、学生、教学方式等方面进行全方位的考虑。

(一)教师培训和教学定位方面

双语教学要求双语教师既要具备较高的英语水平,又要具备丰富的学

科教学经验。

学校应该分析本学校双语教学中师资方面需要改进的地方,并因地制宜地增强师资培训。

学校可以走自我培养和引进相结合

的道路。

自我培养方面,可以选派有一定英语基础的专业教师到外语

院校或双语教学比较成功的院校进行观摩教学、单科进修或作访问学者;有条件的学校可以组织双语教师到英语母语国进行短期进修。

引

进方面,学校可以引进相关专业的外籍教师或者国外大学的老师作为

名誉老师或特聘教授等进行授课。

管理会计双语教师必须将教学定位在引导和启发而不是机械的灌输,

因此,双语教师可以采用启发式教学和情景教学相结合的方式,将学

生的可接受水准以及可能接受的情况用活泼的情景方式将专业知识通

过英语的方式传授给学生。

(二)教学内容和教学方式

教师应该帮助学生熟悉西方教材的风格,在整个学习过程中帮助他们

整理思路,梳理知识点。

中文教材通常逻辑性较强,受篇幅所限,内

容上有很大的浓缩。

原版教材中案例、佐证、背景阐述比较多,内容

之间条块分明,知识点显得比较散乱。

因为大多数学生更为习惯国内

教材的风格,所以教师在进行双语教学的时候,可以不必拘泥于原版

教材的体系编排,可以国内教材的内容体系编排为主线,调整穿插原

版教材内容,这样容易使学生通过中文教材与英文教材对照进行预习

和复习,把握管理会计的主要知识与脉络。

教学内容要有适应性,即适应现代社会发展的需要、适应科学技术发

展的需要、适应人才就业的需要。

在教学内容的安排上,可以将狭窄

的知识面拓展为复合的知识体;将知识量的增加转变为知识结构的优化,注重对学生能力的培养。

另外,应考虑学生的未来工作趋向,适

当调整重点或补充相关内容。

进行双语教学的目的之一就是给学生提

供一个氛围,培养一种意识,了解一部分专业知识的英语表达方法。

在课堂上英语和母语各占多少百分比,都没有一个固定的标准,应以

实际学习效果作为核心,视学生的实际能力及课堂信息量而定。

考虑

到学生综合素质的不同,双语教学应坚持“因材施教”的教育方式,

根据学生的英语水平和专业能力制定相对应的教学计划,采用分阶段

分层次的教育策略。

(三)学生综合素质的提升和学习兴趣的培养

学校要增强双语教学氛围的整体设计和对双语教学的激励,学校可以

在考试制度、学分评价体系等方面进行相对应的改革,在学分、评优、奖学金等方面适当向参加双语教学的学生倾斜,激发学生的积极性和

兴趣,引导学生积极主动地接受双语教学。

为了培养学生对于双语教

学的认可度和兴趣,可以通过请著名企业家特别是国外知名企业的经

济或管理类人士来学校作相关的报告,让学生从现实中体会到双语学

习的重要性和现实意义。

(四)学校应建立对于双语教学的交流机制和评价、考核机制

学校作为双语教学的平台,应激励教师和学生积极参与到双语教学中去,应该创造条件积极支持教师开展课程建设、教学研究、教学经验

交流及组织教师间的教学观摩,并研究制定专门的课程质量评估体系。

学校应鼓励教师结合原版教材的特点,努力学习和掌握国外先进的教

学思想和理念,积极寻找教与学的最佳结合点,持续探索运用现代教

学方法来变革传统的教学方式,增强师生的双向互动,避免和克服教

师的单向讲授,努力营造学生积极参与课堂教学的氛围。

在此基础上,学校可以建立、健全双语教学的质量监控与评价体系,根据双语教学

的特点建立不同于传统教学且能够有效激发教师积极性的评价、考核

机制,从而保证双语教学健康稳步发展。

管理会计双语教学。