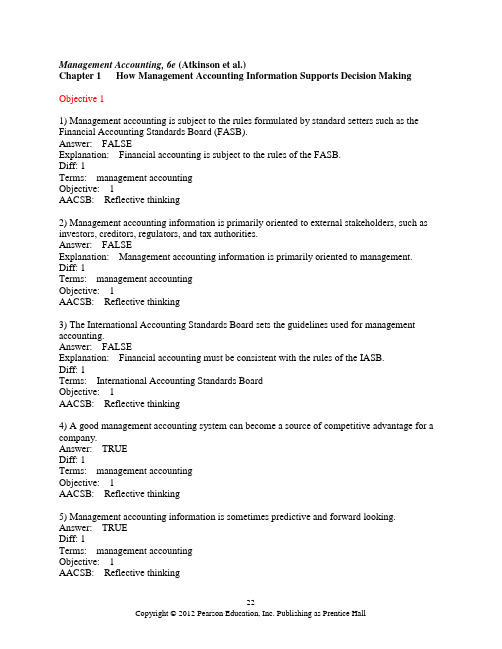

管理会计示范性双语课件习题01

管理会计示范性双语课件习题07

管理会计示范性双语课件习题07CHAPTER 7MANAGEMENT ACCOUNTING AND CONTROLSYSTEMS: ASSESSING PERFORMANCE OVER THEVALUE CHAINTRUE/FALSE1. A system is in control if it is on the path to achieving its strategicobjectives.a. Trueb. False2. For the process of control to have meaning, the organization must beable to identify and correct out-of-control situations.a. Trueb. False3. The same basic control process applies to all industries.a. Trueb. False4. One key difference in the control process lies in determining the mostappropriate types of performance measures for each company.a. Trueb. False5. The control function in management accounting focuses on discipliningemployees who do not meet targeted production levels.a. Trueb. False6. The scope of a well-designed management accounting and controlsystem should be on manufacturing rather than on the entire value chain.a. Trueb. False7. A well-designed management accounting and control system shouldprovide a consistent framework across the organization and yet allow flexibility to accommodate the local needs of each division.a. Trueb. False8. Total-life-cycle costing manages costs along the entire value chain.a. Trueb. False9. Deciding how to allocate organizational resources over the life cycle isprimarily determined during the manufacturing stage.a. Trueb. False10. The proportion of costs incurred during each stage of the product lifecycle varies by industry.a. Trueb. False11. Deciding how to allocate resources over the life cycle is usuallydecided once at the beginning of the design phase.a. Trueb. False12. To be profitable, a company must generate revenues to cover costsincurred throughout the entire value chain.a. Trueb. False13. By some estimates, 10-15% of product’s total life costs are committedduring the research, development, and engineering cycle.a. Trueb. False14. Spending more on the design phase of a new product usually reducessubsequent product-related costs.a. Trueb. False15. One goal of target costing is to design costs out of products during theresearch, development, and engineering stage of the product life cycle.a. Trueb. False16. Target costing starts by estimating expected product costs.a. Trueb. False17. Suppliers play a key role in the success of target costing.a. True18. Supply chain management may result in buyers and suppliers sharinginformation about each other’s companies.a. Trueb. False19. Guiding the target costing process is a cross-functional team made upof individuals from within and from outside the organization.a. Trueb. False20. One concern of target costing is that even though the target cost mightbe met, increased development time may cause the product to come late to market.a. Trueb. False21. Target costing uses the total-life-cycle concept by making it a key goalto minimize the cost of ownership.a. Trueb. False22. Target costing is a comprehensive approach to profit planning and costmanagement.a. Trueb. False23. Kaizen costing offers more opportunity to affect change than targetcosting.b. False24. Employee burnout is a problem for Kaizen costing but not for targetcosting.a. Trueb. False25. The goal of target costing is to reduce costs through small, incrementalchanges.a. Trueb. False26. Kaizen costing assumes engineers and managers possess the bestknowledge to improve processes and reduce costs.a. Trueb. False27. Kaizen costing requires relevant financial results to be shared withfront-line employees.a. Trueb. False28. Environmental costing computes the cost effects an organization hason the environment.a. Trueb. False29. Benchmarking partners should be within the same industry.a. TrueMULTIPLE CHOICE30. Which BEST describes the control function in a managementaccounting and control system?a. MACS seeks out areas that are out-of-control for correctiveaction.b. MACS achieves cost reduction targets that are continuallyadjusted downward.c. MACS guides and motivates employees to achieve organizationalobjectives.d. MACS ensures performance standard goals are being met.31. For the process of control to have meaning and credibility, the BESTresponse is:a. the organization must have the ability to correct situations that itidentifies as out-of-controlb. a consistent framework must be applied globally across theorganizationc. reports need to be generated that are both timely and accurated. information must be gathered about the best practices of others32. Which of the following is NOT true regarding a control system?a. A control system includes developing organizational objectivesand executing a plan for implementation.b. A control system includes monitoring the current level ofperformance and comparing it to the planned level of performance.c. The same performance measures apply to all organizations.d. The basic control process applies to all organizations.33. The process of keeping an organization in control consists of thefollowing five stages:a. research and development, design, manufacturing, marketing, andserviceb. research and development, design, manufacturing, distribution,and disposalc. planning, design, manufacturing, marketing, and benchmarkingd. planning, execution, monitoring, evaluation, and correcting34. A management accounting and control system is in control if it is onthe path:a. to achieving its strategic objectivesb. to implementing a planc. to developing objectivesd. to measuring performance35. Which BEST describes the purpose of a management accounting andcontrol system (MACS)?a. A MACS defines the value chain and identifies nonvalue-activities for a business.b. A MACS helps decision makers determine whether strategies andobjectives are being met.c. A MACS offers a system of controls to ensure employees aremeeting predetermined standards.d. A MACS provides a signal for management attention whenareas are out-of-control.36. A well-designed management accounting and control system assessesperformance:a. primarily in the actual production processb. primarily in the research, development, and engineering cyclec. primarily in the post-sales service and disposal cycled. over the entire value chain of activities37. The two major categories of technical considerations for amanagement accounting and control system are:a. design and accuracyb. relevance and scopec. service and timely informationd. development and flexibility38. Relevance of information includes providing all of the followingEXCEPT:a. the most accurate information possibleb. a global framework that can be applied uniquely to eachor unitc. feedback on performance measures in a timely fashiond. different costing methods for each division39. The scope of management accounting and control system technicalconsiderations should include:a. the performance of suppliersb. design activitiesc. the actual production processd. All of the above are correct.40. Information is relevant if:a. it can be applied in a flexible mannerb. it is inaccuratec. it is inconsistentd. it is late41. By some estimates, 80% to 85% of a product’s total life costs arecommitted by decisions made during the __________ cycle.a. research, development, and engineeringb. manufacturingc. post-sale service and disposald. operating42. The characteristic of a management accounting and control system thatallows employees to customize applications for local decisions isreferred to as being:a. timelyb. flexiblec. accurated. in control43. The characteristic of a management accounting and control system thatmeans the language used and the technical methods applied do notconflict within various parts of the organization is referred to as being:a. in controlb. accuratec. consistentd. Kaizen44. For most products, the majority of costs are incurred during the:a. research, development, and engineering cycleb. manufacturing cyclec. post-sale service and disposal cycled. operating cycle45. Facilities layout and just-in-time manufacturing help reduce costsincurred during the:a. research, development, and engineering cycleb. manufacturing cyclec. post-sale service and disposal cycled. operating cycle46. Total-life-cycle costing is the name given to:a. a method of cost planning to reduce manufacturing costs totargeted levelsb. the process of examining each component of a product todetermine whether its cost can be reducedc. the process of managing all costs along the value chaind. a system that focuses on reducing costs during the manufacturingcycle47. Deciding how to allocate resources over the life cycle usually is:a. decided once at the beginning of the design phaseb. not known until the beginning of the manufacturing cyclec. part of product developmentd. an iterative process over the life of the product48. Total-life-cycle costing is the process of managing costs within:a. research, development, and engineering, manufacturing, andpost-sale service and disposalb. market research, product design, and product developmentc. planning, monitoring, and correctingd. timeliness, consistency, and flexibility49. The service cycle consists of the following stages:a. market research, product design, and product developmentb. research, development, and engineering, manufacturing, and post-sale service and disposalc. selling price, target profit, and target costd. rapid growth, transition, and maturity50. An understanding of total-life-cycle costs can lead to:a. additional costs during the manufacturing cycleb. less need for the evaluation of opportunity costsc. cost effective product designs that are easier to serviced. mutually beneficial relationships between buyers and sellers51. Emerging customer needs are assessed and ideas generated for newproducts during the __________ stage of research, development, and engineering.a. market researchb. product designc. product developmentd. service52. Total-life-cycle costing is particularly important when:a. the development period for research, development, andengineering is short and inexpensiveb. there are significant nonproduction costsc. most costs are locked in during productiond. a low percentage of costs are incurred before any revenues arereceived53. The best chance of incorporating engineering flexibility is during the:a. research, development, and engineering cycleb. manufacturing cyclec. post-sale service and disposal cycled. operating cycle54. One goal of __________ is to design costs out of products in theresearch, development, and engineering stage.a. cost-plus pricingb. target costingc. Kaizen costingd. traditional costing55. __________ starts with estimated product costs and next determinesthe estimated selling price.a. Standard costingb. Target costingc. Kaizen costingd. Traditional costing56. __________ starts with estimated product costs and next adds theexpected profit margin.a. Cost-plus pricingb. Target costingc. Kaizen costingd. Standard costing57. All of the following are true regarding target costing EXCEPT that:a. improvements are implemented in small, incremental amountsb. customer input is collected continually throughout the targetcosting processc. input is requested from suppliers and distributorsd. a key goal is to minimize costs over the product’s useful life58. All of the following are associated with target costing EXCEPT:a. value engineeringb. target reduction ratesc. supply-chain managementd. cross-functional teams59. Concerns about target costing include all EXCEPT that:a. attention may be diverted away from other company goalsb. excessive pressure is put on suppliersc. development time may decreased. burnout of design engineers occurs60. Target costing differs from traditional costing in all of the followingways EXCEPT:a. target costing collects market research continually throughout thetarget costing process rather than as a single eventb. target costing uses the total-life-cycle concept to minimizeownership costsc. traditional costing spends less time on product specification anddesignd. traditional costing uses cross-functional teams to guide theprocess61. Target costing is:a. used for short-term pricing decisionsb. one form of cost-plus pricingc. where the selling price estimate is based on the customers’perceived value of the productd. where the relevant costs are all variable costs62. Relevant costs for target pricing include:a. variable manufacturing costsb. variable manufacturing and variable nonmanufacturing costsc. all fixed costsd. all future costs, both variable and fixed63. Place the following steps for the implementation of target costing inorder:A = Derive a target costB = Develop a target selling priceC = Perform value engineeringD = Determine target profit margina. B D A Cb. B A D Cc. A D B Cd. A B C D64. Value engineering may result in all of the following EXCEPT:a. improved product designb. changes in materials specificationsc. increases in the quantity of nonvalue-added cost driversd. the evaluation of all business functions within the value chain65. To design costs out of products is a goal of:a. cost-plus pricingb. target costingc. kaizen costingd. peak-load costing66. The product strategy in which companies first determine the price atwhich they can sell a new product and then design a productthat can be produced at a low enough cost to provide adequate operating income is referred to as:a. cost-plus pricingb. target costingc. kaizen costingd. full costingTHROUGH 70.After conducting a market research study, Schultz Manufacturing decided to produce a new interior door to complement its exterior door line. It is estimated that the new interior door can be sold at a target price of $60. The annual target sales volume for interior doors is 20,000. Schultz has a 20% expected return on sales target.67. What are target sales revenues?a. $960,000b. $2,000,000c. $1,200,000d. None of the above is correct.68. What is the target profit margin?a. $240,000b. $300,000c. $192,000d. $180,00069. What is the target cost?a. $900,000b. $960,000c. $1,260,000d. $1,008,00070. What is the target cost for each interior door?a. $48b. $58c. $60d. $45THROUGH 73.Dennis’ TV currently sells small televisions for $180. It has costs of $140.A competitor is bringing a new small television to market that will sell for $150. Management believes it must lower the price to $150 to compete in the market for small televisions. Marketing believes that the new price will cause sales to increase by 10%, even with a new competitor in the ma rket. Dennis’ sales are currently 100,000 televisions per year.71. What is the change in profit margin if Marketing is correct and onlythe sales price is changed?a. $1,100,000b. $300,000c. $(1,100,000)d. $(2,900,000)72. What is the new target cost if profit margin is 25% of sales?a. $37.50b. $45.00c. $112.50d. $135.0073. What is the target cost if the company wants to maintain its sameprofit margin and Marketing is correct?a. $112.50b. $113.64c. $123.34d. $140.0074. __________ focuses on reducing costs during the manufacturingstage.a. Cost-plus pricingb. Target costingc. Kaizen costingd. Traditional costing75. All below are true regarding Kaizen costing EXCEPT that:a. cost-variance analysis compares target Kaizen costs with actualcost reduction amountsb. cost reductions apply to all variable costsc. workers are assumed to have the best knowledge to improveprocesses and reduce costsd. cost reduction targets are set and applied on an annual basis76. Concerns about Kaizen costing include:a. radical process improvementsb. excessive pressures are put on employeesc. focus is on the overall systemd. grace periods may be granted77. All of the following are associated with Kaizen costing EXCEPT:a. target reduction rateb. supply-chain managementc. cost reductions during manufacturingd. small monthly cost reductionsTHE FOLLOWING INFORMATION APPLIES TO QUESTIONS 78AND 79.Dan and Donna Enterprises are using the Kaizen approach to budgeting for 2005. The budgeted income statement for January 2005 is as follows: Sales (84,000 units) $500,000Less: Cost of goods sold 300,000Gross margin 200,000Operating expenses (includes $50,000 of fixed costs) 150,000 Operating income $ 50,000Under the Kaizen approach, cost of goods sold and variable operating expenses are budgeted to decline by 1% per month.78. What is budgeted cost of goods sold for March 2005?a. $294,030b. $294,000c. $300,000d. $297,00079. What is budgeted gross margin for March 2005?a. $196,020b. $198,000c. $204,020d. $205,97080. Environmental costing includes all below EXCEPT:a. target reduction ratesb. selecting suppliers with matching environmental philosophiesc. disposing of waste productsd. addressing post-sale disposal issues81. Benchmarking partners:a. have to be of equal sizeb. are most likely to be industry leadersc. have to be within the same industryd. have to trust each other。

(完整版)管理会计课后习题学习指导书习题答案(第一章)

第一章课后习题一、思考题1.从管理会计定义的历史研究中你有哪些思考和想法?答:从管理会计定义的历史研究中我发现,管理会计的概念是随着历史的发展不断完善的,因为在历史进程中,人们会发现原有概念的不足,进而不断去修改完善,这才有了现在的管理会计。

这也启发了我们,要善于发现问题,去思考,解决问题。

2.经济理论对管理会计的产生和发展有哪些重要影响?你从中得到了什么启示?答:社会经济的发展和经济理论的丰富,使得管理会计的理论体系逐渐完善,内容更加丰富,逐步形成了预测、决策、预算、控制、考核、评价的管理会计体系。

由于市场竞争的日趋激烈,人们认识到对外部环境的准确决策就是不可能的,企业的计划必须以外部环境的变化为基础,更加留心市场变化的动态,更加密切关注竞争对手。

与此相适应,战略管理的理论有了长足的发展。

这启示了我们,要细心观察,因地制宜,适应变化莫测的外部环境,进行自身调整。

同时,实践出真知,只有经过了实践考验理论才是好理论。

3.科学管理理论对现代管理会计有哪些重要影响?这些影响在管理会计的不同发展阶段是如何表现的?答:现代管理科学为管理会计的形成奠定了一定的基础。

在以成本控制为基本特征的管理会计阶段,古典组织理论特别是科学管理理论的出现促使现代会计分化为财务会计和管理会计,现代会计的管理职能得以表现出来。

该阶段,管理会计以成本控制为基本特征,以提高企业的生产效率和工作效率为目的,其主要内容包括标准成本、预算控制、差异分析。

在以预测、决策为基本特征的管理会计阶段,以标准成本制度为主要内容的管理控制继续得到了强化并有了新的发展。

责任会计将行为科学的理论与管理控制的理论结合起来,不仅进一步加强了对企业经营的全面控制(不仅仅是成本控制),而且将责任者的责、权、利结合起来,考核、评价责任者的工作业绩,从而极大地激发了经营者的积极性和主动性。

社会经济的发展和经济理论的丰富,使得管理会计的理论体系逐渐完善。

4.什么是价值链分析?价值链分析的目的是什么?答:价值链分析是指将一个企业的经营活动分解为若干战略性相关的价值活动,每一种价值活动都会对企业的相对成本产生影响,进而成为企业采取差异化战略的基础。

{财务管理财务会计}管理会计示范性双语讲义习题

{财务管理财务会计}管理会计示范性双语讲义习题CHAPTER1MANAGEMENTACCOUNTING:INFORMATIONTHATCREATESVALUE TRUE/FALSE1.Managementaccountinggathersshort-term,long-term,financial,andnonfinancialinformation.a.Trueb.False2.Managementaccountinginformationgenerallyreportsontheorganizationas awhole.a.Trueb.Falsepanieshavetofollowstrictguidelineswhendesigningamanagementacco untingsystem.a.Trueb.False4.Agoodmanagementaccountingsystemisintendedtomeetspecificdecision-makingneedsatalllevelsintheorganization.a.Trueb.False5.Duringthehistoryofmanagementaccounting,innovationsweredevelopedto addressthedecision-makingneedsofmanagers.a.Trueb.False6.Akeyelementinanyorganization’sstrategyistoidentifyitstargetcustomersandtodeliverwhatthosetargetcustomerswant.a.Trueb.False7.Thevaluepropositionhasonlytwoelements:costandquality.a.Trueb.False8.Qualityisthedegreeofconformancebetweenwhatthecustomerispromisedan dwhatthecustomerreceives.a.Trueb.False9.Recently,thedemandforimprovedmanagementaccountingandcontrolinfor mationwithinmanufacturingfirmshasalsooccurredinserviceorganizations.a.Trueb.False10.Recently,thepetitiveenvironmentforbothmanufacturingandservicepanies hasbeefarmorechallenginganddemanding.a.Trueb.False11.Servicepaniesareverysimilartomanufacturingpaniesinmayways,includingt hefactthatmanyemployeeshavedirectcontactwithcustomers.a.Trueb.False12.Sensitivitytotimelinessandqualityofserviceisespeciallyimportanttoservice organizations.b.Falseernmentandnonprofitorganizations,aswellasprofit-seekingenterprises,arefeelingthepressuresforimprovedperformance.a.Trueb.False14.Managementaccountinginformationallowsmanagerstopareactualandpla nnedcostsandtoidentifyareasandopportunitiesforprocessimprovement.a.Trueb.False15.Managementaccountingcanprovideinformationoncustomersatisfaction.a.Trueb.False16.ROI(returnoninvestment)binestwoprofitabilitymeasurestoproduceasingle measureofdepartmentalordivisionalperformance.a.Trueb.False17.Around1920,centralizedcontrolofdecentralizedoperationswasacplishedb yhavingcorporatemanagersreceivefinancialreportsaboutdivisionaloperation sandprofitability.a.Trueb.False18.Inthelate1990s,littleinterestorattentionwaspaidtoevaluatingmanagement ’sappropriategovernanceandstrategychoices.b.False19.Financialinformationidentifiesandexplainstheunderlyingproblems.a.Trueb.False20.Managementaccountingmeasurescanprovideadvancewarningsofproble ms.a.Trueb.False21.Customersatisfactionisanexampleoffinancialinformation.a.Trueb.False22.Operatingprofitisanexampleofnonfinancialinformation.a.Trueb.Falseanizationalleadershipplaysacriticalroleinfosteringanorganization’s c ultureofhighethicalstandards.a.Trueb.Falsermationisneverneutral;justtheactofmeasuringandreportinginformatio naffectstheindividualsinvolved.a.Trueb.False25.Boundarysystemsarealwaysstatedinpositivetermsthatoutlinemaximumsta ndardsofbehavior.a.Trueb.FalseMULTIPLECHOICE26.Managementaccountinghelpsapanyachieve:a.itsstrategicobjectivesb.itsoperationalobjectivesc.controlandalsosupportsperformanceevaluationd.Alloftheabovearecorrect.27.Whichofthefollowingtypesofinformationareusedinmanagementaccounti ng?a.financialinformationb.nonfinancialinformationrmationfocusedonthelongtermd.Alloftheabovearecorrect.28.Managementaccounting:a.focusesonestimatingfuturerevenues,costs,andothermeasurestoforecastacti vitiesandtheirresultsb.providesinformationaboutthepanyasawholec.reportsinformationthathasoccurredinthepastthatisverifiableandreliabled.providesinformationthatisgenerallyavailableonlyonaquarterlyorannualbasi s29.Whichofthefollowingdescriptorsrefertomanagementaccountinginformati on?a.Itisverifiableandreliable.b.Itisdrivenbyrules.c.Itispreparedforshareholders.d.Itprovidesreasonableandtimelyestimates.30.Whichofthefollowingstatementsreferstomanagementaccountinginformat ion?a.Therearenoregulationsgoverningthereports.b.Thereportsaregenerallydelayedandhistorical.c.Theaudiencetendstobestockholders,creditors,andtaxauthorities.d.Thescopetendstobehighlyaggregate.31.Managementaccountinginformationincludes:a.tabulatedresultsofcustomersatisfactionsurveysb.thecostofproducingaproductc.thepercentageofunitsproducedthatisdefectived.Alloftheabovearecorrect.32.ManagementaccountingreportsMOSTlikelyincludeinformationabout:a.customerplaintsinefortheyearc.totalassetsd.Alloftheabovearecorrect.33.ThepersonMOSTlikelytousemanagementaccountinginformationisa(n):a.bankerevaluatingacreditapplicationb.shareholderevaluatingastockinvestmenternmentaltaxingauthorityd.assemblydepartmentsupervisor34.WhichofthefollowingisNOTafunctionofamanagementaccountingsystem?a.strategicplanningb.financialreportingc.operationalcontrold.productcosting35.FinancialaccountingprovidesthePRIMARYsourceofinformationfor:a.decisionmakinginthefinishingdepartmentb.improvingcustomerservicec.preparingtheinestatementforshareholdersd.planningnextyear’soperatingbudget36.Financialaccounting:a.focusesonthefutureandincludesactivitiessuchaspreparingnextyear'soperati ngbudgetb.mustplywithGAAP(generallyacceptedaccountingprinciples)c.reportsincludedetailedinformationonthevariousoperatingsegmentsoftheb usinesssuchasproductlinesordepartmentsd.ispreparedfortheuseofdepartmentheadsandotheremployees37.ThepersonMOSTlikelytouseONLYfinancialaccountinginformationisa:a.factoryshiftsupervisorb.vicepresidentofoperationsc.currentshareholderd.departmentmanager38.Theaccountingprocessisconstrainedbymandatedreportingrequirementsb yallofthefollowingorganizationsEXCEPTthe:a.InternalRevenueService(IRS)b.InstituteofManagementAccountants(IMA)c.FinancialAccountingStandardsBoard(FASB)d.SecuritiesandExchangeCommission(SEC)forpaniesthatarepubliclytraded39.Historically:a.inthebeginningofthe20th century,theGuildskeptdetailedrecordsofrawmateri alsandlaborcostsasevidenceofproductqualityb.inmedievalEngland,thebasicsofmodernmanagementaccountingemergedw ithstandardsformaterialuse,employeeproductivity,andbudgetsc.inthelate19th century,railroadmanagersimplementedlargeandplexcostingsy stemstoputethecostofdifferenttypesoffreightd.from1400-1600,largeandintegratedpaniessuchasDuPontandGeneralMotors,developed waystomeasurereturnoninvestment40.Ingeneral,itwasnotuntilthe1970sthatmanagementaccountingsystems:a.wereimprovedbecauseofdemandsbytheFASBandtheSECb.stagnatedandprovedinadequatec.startedtodevelopinnovationsincostingandperformance-measurementsystemsduetointensepressurefromoverseaspetitorsd.startedtoaddressthedecision-makingneedsofmanagers41.Allsuccessfulorganizationsmustidentifyandunderstandtheir:a.weaknessesb.petitionc.strategyd.definitionofquality42.Akeyelementofanyorganization’sstrategyisidentifying:a.itspotentialshareholdersb.itstargetcustomersc.petitor’sproductsd.employeeneeds43.Whatanorganizationtriestodelivertocustomersiscalleditsvalueproposition ,whichincludestheelementsof:a.costandqualityb.cost,quality,andfunctionalityandfeaturesc.cost,quality,functionalityandfeatures,andserviced.cost,quality,functionalityandfeatures,service,andindustrystandards44.Thepricepaidbythecustomer,giventheproductfeaturesandpetitor’sprices ,isreferredtoasthe__________elementofthevalueproposition.a.costb.industrystandardsc.qualityd.service45.Thedegreeofconformancebetweenwhatthecustomerispromisedandwhatt hecustomerreceivesisreferredtoasthe__________elementofthevaluepropositio n.a.costb.industrystandardsc.qualityd.service46.Theperformanceoftheproduct,forexample,amealinarestaurantprovidesth edinerwiththelevelofsatisfactionexpectedforthepricepaid,isreferredtoasthe__ ________elementofthevalueproposition.a.functionalityandfeaturesb.industrystandardsc.qualityd.service47.Howthecustomeristreatedatthetimeofthepurchaseisanexampleofthe_____ _____elementofthevalueproposition.a.functionalityandfeaturesb.industrystandardsc.qualityd.service48.Managementaccountingprovides:rmationontheefficiencyoffactorylaborrmationonthecostofservicingmercialcustomersrmationontheperformanceofanoperatingdivisiond.Alloftheabovearecorrect.49.WhichofthefollowinggroupswouldbeLEASTlikelytoreceivedetailedmanag ementaccountingreports?a.stockholdersb.customerservicerepresentativesc.productionsupervisord.vicepresidentofoperations50.Topexecutivesofamulti-plantfirmareLEASTlikelytousemanagementaccountinginformation:a.tosupportdecisionsthatresultinlong-termconsequencesb.toevaluatetheperformanceofindividualplantsc.forstrategicplanningd.foroperationalcontrol51.ManagersofservicedepartmentsneedallofthefollowinginformationEXCEPT:a.efficiencydataonworkperformanceb.qualitydataonworkperformancec.profitabilitydataofthewholepanyd.profitabilitydataoftheservicedepartmentrmationMOSTus efultothe employeewhoassembles thefurnitureincludes:a.adailyreportparingtheactualtimeittooktoassembleapieceoffurnituretothest andardtimeallowedb.amonthlyreportontheportionoffurniturepiecesassembledwithdefectsc.thenumberoffurniturepiecessoldthismonthd.revenueperemployeermationMOSTus efultothe topexecutive includes:a.individualjobsummariesofmaterialsusedb.monthlyfinancialreportsonthepany’sprofitabilitybyproductlinec.timereportssubmittedbyeachemployeed.scheduleddowntimeforroutinemaintenanceonmachines54.AquarterlyreportdisclosingdecliningmarketshareinformationisMOSTusef ulto:a.afront-lineemployeeb.themanagerofoperationsc.thechiefexecutiveofficerd.theaccountingdepartment55.Aweeklyreportparingmachinetimeusedtoavailablemachinetimeisinformat ionMOSTusefulto:a.afront-lineemployeeb.themanagerofoperationsc.thechiefexecutiveofficerd.theaccountingdepartment56.Adailyreportonthenumberofqualityunitsassembledbyeachemployeeisinf ormationMOSTusefulto:a.afront-lineassemblyworkerb.theaccountingdepartmentc.thechiefexecutiveofficerd.thepersonneldepartment57.WhichofthefollowingwouldbeLEASThelpfulforatopmanagerofapany?a.profitabilityreportofthepanyrmationtomonitorhourlyanddailyoperationsc.numberofcustomerplaintsd.operatingexpensesummaryreportedbydepartment58.Recently,increaseddemandformanagementaccountinginformationhasbeen:a.primarilyfrommanufacturingfirmsb.primarilyfromserviceorganizationsc.fromboththemanufacturingandtheserviceindustriesd.anillusion;infact,thedemandformanagementaccountinghaschangedverylitt le59.Managementaccountingcanplayacriticalroleintheserviceindustrybecause ofallthefollowingreasonsEXCEPT:a.firmsmustbeespeciallysensitivetothetimelinessandqualityofcustomerservic eb.manyemployeeshaveverylittlecontactwithcustomersc.customersimmediatelynoticedefectsandadelayinserviced.dissatisfiedcustomersmayneverreturn60.Historically,theNEGLECTofmanagementaccountingintheserviceindustryw asaresultof:a.nonpetitiveenvironmentsb.globalcustomerdemandsc.theswitchtofreemarketeconomiesd.aninfluxofhigher-qualityandlower-pricedproductsfromoverseas61.Currently,managementaccountinginformationwithingovernmentandnon profitorganizationsisingreaterdemandbecause:a.publicandprivatedonorsaredemandingaccountabilityb.citizensarerequestingresponsiveandefficientperformancefromtheirgoverni ngunitsc.morenonprofitorganizationsarepetingforlimitedfundsd.Alloftheabovearecorrect.62.Currently,pressuresforimprovedcostandperformancemeasurementsarebe ingfeltby:a.nonprofitorganizationsernmentalagenciesc.profit-seekingenterprisesd.Alloftheabovearecorrect.63.Financialaccountinginformation:a.providesasignalthatsomethingiswrongb.identifieswhatiswrongc.explainswhatiswrongd.simplysummarizesinformationbutgivesnoindicationthatanythingiswrong64.Decentralizedresponsibilityreferstoallowinglower-levelmanagerstodoallofthefollowingEXCEPT:a.makedecisionswithoutseekinghigherapprovalb.takeadvantageoflocalopportunitiesc.makeperiodicfinancialreportstoupper-managementd.pursueindividualobjectiveseventhoughtheymaynotcontributetotheentirepany65.Thereturnoninvestment(ROI)performancemeasureuses__________toevalua tetheperformanceofoperatingdivisions.a.asinglenumberb.fournumbersc.fivenumbersd.tennumbers66.Thereturnoninvestment(ROI)performancemeasurebines__________toprod uceameasureofdepartmentalperformance.a.twoprofitabilitymeasuresb.twocapitalutilizationmeasuresc.oneprofitabilitymeasureandonecapitalintensitymeasured.twoprofitabilitymeasuresandtwocapitalintensitymeasures67.Allofthefollowingaretrueregardingthereturnoninvestment(ROI)formulade velopedatDupontEXCEPTthat:a.itisthesolemeasuretop-managementutilizestoevaluatewhichdivisionshouldreceiveadditionalcapitalb.itallowspaniestohavecentralizedcontrolwithdecentralizedresponsibilityc.itproducesameasureofdivisionalperformanced.itequals(Operatingine/Sales)x(Sales/Investment) THEFOLLOWINGINFORMATIONAPPLIESTOQUESTIONS68AND69. Thefollowinginformationpertainstothreedivisions: FlowersShrubsTreesSales$15,000$28,000$120,000Operatingine$2,000$2,000$6,000Investment$22,000$40,000$100,00068.WhatisthereturnoninvestmentfortheShrubDivision?a.2.00%b.5.00%c.7.14%d.70.00%69.WhichdivisionismoreprofitablebasedonROI?a.Flowersb.Shrubsc.Treesd.BothFlowersandShrubsareequallymoreprofitablethanTrees.70.Tohelpevaluatemanagement’sappropriategovernanceandstrategicchoic es,organizationshavecalledonmanagementaccountantstodevelop:a.internalcontrolsystemstoprotectassetsfromtheftb.measurestomonitorpliancewithbehaviorthatisconsistentwiththeorganizati on’sbesti nterestsc.systemstoevaluateprofitabilityd.reportstohighlightvariancesfromamountsplanned71.ManagementaccountinginformationisBESTdescribedas:a.providingasignalthatsomethingiswrongb.identifyingandhelpingtoexplainwhatiswrongc.simplysummarizinginformation,butgivingnoindicationthatanythingiswron gd.measuringoverallorganizationalperformance72.Forimprovingoperationalefficienciesandcustomersatisfaction,nonfinancia linformationis:a.criticalb.helpfulc.infrequentlyusedd.unnecessary73.Nonfinancialinformationmightbeusedto:a.improvequalityb.reducecycletimesc.satisfycustomerneedsd.Alloftheabovearecorrect.74.Theactofsimplymeasuringandreportinginformation:a.focusestheattentionofemployeesonthoseprocessesb.divertstheemployee’sattentiontootheractivitiesc.disprovesthesaying“Whatgetsmeasuredgetsmanaged.”d.hasnoeffectonemployeebehavior75.WhichstatementbelowisFALSE?a.“Whatgetsmeasuredgetsmanaged.”b.Peoplereacttomeasurements.c.Employeesspendmoreattentiononthosevariablesthatarenotgettingmeasur ed.d.“IfIcan’tmeasureit,Ican’tmanageit.”76.Whenachangeisintroduced,employeestendto:a.embracethechangeb.beindifferenttothechangec.exhibitnochangeinbehaviord.resistthechange77.TheintroductionofanewmanagementsystemisMOSTlikelytomotivateUNW ANTEDemployeebehaviorwhenitisusedfor:a.evaluationb.planningc.decisionmakingd.coordinatingindividualefforts78.ManagementaccountantsareMOSTlikelytofeeloutsidepressuretofavorabl yinfluencethenumbersfavorablywhentheinformationisusedfor:a.budgetingb.pensationandpromotionsc.continuousimprovementd.productcosting79.FosteringacultureofhighethicalstandardsincludesallofthefollowingEXCEP T:a.followingthegoodexamplesetbyseniormanagementb.municatingtoemployeesabeliefsystemthatinspiresandpromotesmitmentto theorganization’scorevaluesc.followingthegeneralexamplessetbyfront-lineemployeesd.municatingtoallemployeesaboundarysystemthatstateswhatactionswillnot betolerated80.TheInstituteofManagementAccountants(IMA):a.isaprofessionalorganizationofmanagementaccountantsb.isaprofessionalorganizationoffinancialaccountantsc.issuesstandardsformanagementaccountingd.issuesstandardsforfinancialaccountingCRITICALTHINKING/ESSAY81.Describemanagementaccountingandfinancialaccounting.82.Whatisthepurposeofmanagementaccounting?83.Brieflydescribehowmanagersmakeuseofmanagementaccountinginformat ion.84.Describethevaluepropositionandtheelementsthatpriseit.85.Isfinancialaccountingormanagementaccountingmoreusefultoanoperatio nsmanager?Why?86.Whatrolehastheincreasinglypetitivebusinessenvironmentplayedinthedev elopmentofmanagementaccounting?87.Describereturnoninvestment(ROI).Whywasitdeveloped?Whenwasitdevel oped?88.Givetwoexamplesoffinancialinformationandnonfinancialinformation.89.Discussthepotentialbehaviorimplicationsofperformanceevaluation.CHAPTER1SOLUTIONSMANAGEMENTACCOUNTING:INFORMATIONTHATCREATESVALUETRUE/FALSE LO11.aLO12.bLO13.bLO14.aLO15.aLO26.aLO27.bLO28.aLO39.aLO310.aLO311.bLO312.aLO313.aLO314.aLO315.aLO416.bLO417.aLO518.aLO519.bLO520.aLO521.b LO522.bLO623.aLO624.aLO625.bMULTIPLECHOICELO126.dLO127.dLO128.aLO129.dLO130.aLO131.dLO132.aLO133.dLO134.bLO135.cLO136.bLO137.cLO138.bLO139.cLO140.cLO241.cLO242.bLO243.cLO244.aLO245.cLO246.aLO247.dLO348.d LO349.a LO350.d LO351.c LO352.a LO353.b LO354.c LO355.b LO356.aLO357.bLO358.cLO359.bLO360.aLO361.dLO362.dLO463.aLO464.dLO465.aLO466.cLO467.aLO468.bLO469.aLO570.bLO571.bLO572.aLO573.dLO674.aLO675.cLO676.dLO677.aLO678.bLO679.cLO680.aMULTIPLECHOICE68.$2,000/$40,000=5.00%69.$2,000/$22,000=9.09%;$2,000/$40,000=5.00%;$6,000/$100,000=6.00%CRITICALTHINKING/ESSAYLO181.Describemanagementaccountingandfinancialaccounting.Solution:Managementaccountingprovidesinformationtointernaldecisionma kersofthebusinesssuchastopexecutives.Itspurposeistohelpmanagerspredicta ndevaluatefutureresults.Reportsaregeneratedoftenandareusuallybrokendo wnintosmallerreportingdivisionssuchasdepartmentorproductline.Therearen orulestobepliedwithsincethesereportsareforinternaluseonly. Financialaccountingprovidesinformationtoexternaldecisionmakerssuchasinv estorsandcreditors.Itspurposeistopresentafairpictureofthefinancialcondition ofthepany.Reportsaregeneratedquarterlyorannuallyandreportonthepanyasa whole.ThefinancialstatementsmustplywithGAAP(generallyacceptedaccounti ngprinciples).ACPAaudits,orverifies,thattheGAAParebeingfollowed.LO182.Whatisthepurposeofmanagementaccounting?Solution:Managementaccountinggathersshort-termandlong-termfinancialandnonfinancialinformationtoplan,coordinate,motivate,improv e,control,andevaluatesuccessfactorsofanorganization.Managementaccounti ngconvertsdataintousableinformationthatsupportsstrategic,operational,and controldecisionmaking.LO183.Brieflydescribehowmanagersmakeuseofmanagementaccountinginformat ion.Solution:Managersuseaccountinginformationforthreebroadpurposes.ONE:Toplanbusinessoperationsthatincludespreparingstrategiesandbudgets anddeterminingthepricesandcostsofproductsandservices.Apanymustknowt hecostofeachproductandservicetodecidewhichproductstoofferandwhethert oexpandordiscontinueproductlines.TWO:Tocontrolbusinessoperationsthatincludesparingactualresultstothebud getedresultsandtakingcorrectiveactionwhenneeded.THREE:Toevaluateperformance.LO284.Describethevaluepropositionandtheelementsthatpriseit.Solution:Thevaluepropositioniswhatanorganizationtriestodelivertoitstargetc ustomers–itdefinestheorganizationalstrategy. Thefourelementsarecost,quality,functionalityandfeatures,andservice. •Cost isthepricepaidbythecustomer,giventheproductfeaturesandpetitor’s prices.•Quality isthedegreeofconformancebetweenwhatthecustomerispromiseda ndwhatthecustomerreceives.•Functionalityandfeatures referstotheperformanceoftheproduct.Forexamp le:Amealinarestaurantprovidesthedinerwiththelevelofsatisfactionexpectedfo rthepricepaid.•Service isalloftheotherelementsoftheproduct.Forexample:Howthecustom eristreatedatthetimeofthepurchase.LO385.Isfinancialaccountingormanagementaccountingmoreusefultoanoperatio nsmanager?Why?Solution:Managementaccountingismoreusefultoanoperationsmanagerbeca usemanagementaccountingreportsoperatingresultsbydepartmentorunitrath erthanforthepanyasawhole,itincludesfinancialaswellasnonfinancialdatasuch ason-timedeliveriesandcycletimes,anditincludesquantitativeaswellasqualitativedat asuchasthetypeofreworkthatwasneededondefectiveunits.LO386.Whatrolehastheincreasinglypetitivebusinessenvironmentplayedinthedev elopmentofmanagementaccounting?Solution:Thepetitiveenvironmenthaschangeddramatically.Therehasbeenade regulationmovementinNorthAmericaandEuropeduringthe1970sand1980sth atchangedthegroundrulesunderwhichservicepaniesoperated.Inaddition,org anizationsencounteredseverepetitionfromoverseaspaniesthatofferedhigh-qualityproductsatlowprices.Therehasbeenanimprovementofoperationalcont rolsystemssuchthatinformationismorecurrentandprovidedmorefrequently.T henatureofworkhaschangedfromcontrollingtoinforming.Firmsareconcerned aboutcontinuousimprovement,employeeempowerment,andtotalquality.No nfinancialinformationhasbeeacriticalfeedbackmeasure.Finally,thefocusofma nyfirmsisnowonmeasuringandmanagingactivities.LO487.Describereturnoninvestment(ROI).Whywasitdeveloped?Whenwasitdevel oped?Solution:ROI=(operatingine/sales)x(sales/investment) TheROImeasurebinesaprofitabilitymeasure(operatingine/sales)withacapitali ntensitymeasure(sales/investment)toprovideasinglemeasureofdepartmental anddivisionalperformance. ROIwasdevelopedintheearlydecadesofthe1900ssothatseniormanagersatmul ti-divisionaldiversifiedcorporations,suchasDuPontandGeneralMotors,couldeva luatetheoperatingperformanceoftheirdecentralizeddivisions.LO588.Givetwoexamplesoffinancialinformationandnonfinancialinformation. Solution:Financialinformationincludesamountsthatcanbeexpressedindollara mountssuchassales,netine,andtotalassets.Italsoincludesratiospreparedusing financialinformationsuchasincreaseinsales,return-on-sales,andreturn-on-investment. Nonfinancialinformationincludesmeasuresthatarenotexpressedindollaramo unts.Forexample,nonfinancialmeasuresofcustomersatisfactionincludethenu mberofrepeatcustomersorrankedestimatesofsatisfactionlevels.Nonfinancial measuresofproductionqualityincludepercentofon-timedeliveries,thenumberofdefects,productionyield,andcycletimes.LO689.Discussthepotentialbehaviorimplicationsofperformanceevaluation.Solution:Asmeasurementsaremadeonoperationsand,especially,onindividual sandgroups,thebehavioroftheindividualsandgroupsareaffected.Peoplereactt othemeasurementsbeingmade.Theywillfocusonthosevariablesorthebehavior beingmeasuredandspendlessattentiononvariablesandbehaviorthatarenotm easured.Inaddition,ifmanagersattempttointroduceorredesigncostandperfor mancemeasurementsystems,peoplefamiliarwiththeprevioussystemwillresist. Managementaccountantsmustunderstandandanticipatethereactionsofindivi dualstoinformationandmeasurements.Thedesignandintroductionofnewmea surementsandsystemsmustbeacpaniedwithananalysisofthelikelyreactionstot heinnovations.感谢阅读多年企业管理咨询经验,专注为企业和个人提供精品管理方案,企业诊断方案,制度参考模板等欢迎您下载,均可自由编辑。

管理会计示范性双语课件习题02

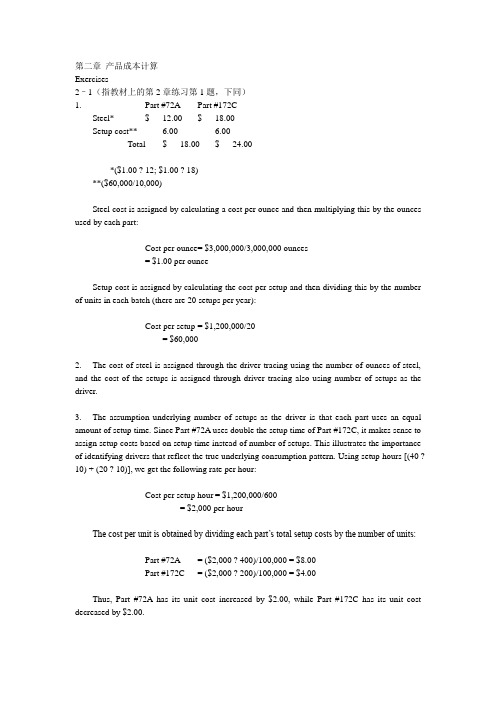

CHAPTER 2COST MANAGEMENT CONCEPTS AND COST BEHAVIOR TRUE/FALSE1. There is no single definition of cost.a. Trueb. False2. The role of the management accountant is to tailor the cost calculation to fit the currentdecision situation.a. Trueb. False3. A cost that is useful for one decision may not be useful information for another decision.a. Trueb. False4. In most organizations, managing nonmanufacturing costs as well as manufacturing costs isimportant for financial success.a. Trueb. False5. The cost of a customized machine only used in the production of a single product would beclassified as a direct cost.a. Trueb. False6. The wages of a plant supervisor would be classified as a period cost.a. Trueb. False7. The classification of product and period costs is particularly valuable in managementaccounting.a. Trueb. False8. For external reporting, generally accepted accounting principles require that costs beclassified as either flexible or capacity-related costs.a. Trueb. False9. Knowing whether a cost is a period or a product cost helps to estimate total cost at a newlevel of activity.a. Trueb. False10. Flexible costs are always direct costs.a. Trueb. False11. Capacity-related costs vary with the level of production or sales volume.a. Trueb. False12. Currently, most personnel costs are classified as capacity-related costs.a. Trueb. False13. Some capacity-related costs might be classified as direct manufacturing costs.a. Trueb. False14. Capacity-related costs depend on the resources used, not the resources acquired.a. Trueb. False15. Break-even point is NOT an important concept since the goal of business is to make aprofit.a. Trueb. False16. To perform cost-volume-profit analysis, a company must be able to separate costs intocapacity-related and flexible components.a. Trueb. False17. Cost-volume-profit analysis may be used for single-product and multiproduct analysis.a. Trueb. False18. Selling price per unit is $30, flexible cost per unit is $15, and capacity-related cost per unitis $10. When this company operates above the break-even point, the sale of one more unit will increase net income by $5.a. Trueb. False19. A company with sales of $100,000, flexible costs of $70,000, and capacity-related costs of$50,000 will reach its break-even point if sales are increased by $20,000.a. Trueb. False20. In multiproduct situations when the sales mix shifts toward the product with the lowestcontribution margin, the break-even quantity will decrease.a. Trueb. False21. The opportunity cost of a resource is zero if there is excess capacity of that resource.a. Trueb. False22. When a firm maximizes profits it will simultaneously minimize opportunity costs.a. Trueb. False23. Even when the only constraint limiting production is machine time, a company should bemost concerned with maximizing contribution margin per unit.a. Trueb. False24. The time over which a decision maker can adjust capacity is referred to as the short run.a. Trueb. False25. For general customers, the price charged for a product must cover its long-run cost to theorganization.a. Trueb. False26. In recent years, capacity-related costs have increased as a proportion of total manufacturingcosts.a. Trueb. False27. Machine setup costs are usually classified as a business-sustaining activity.a. Trueb. False28. The benefits of classifying activities using the broader framework of unit-related, batch-related, product-sustaining, customer-sustaining, and business-sustaining activities are there are generally more costs that are directly traceable to cost objects.a. Trueb. False29. Product life-cycle costing helps organizations decide whether a new product should belaunched.a. Trueb. FalseMULTIPLE CHOICE30. An example of a cost object is:a. a productb. a customerc. a departmentd. All of the above are correct.31. Manufacturing costs include:a. machinery used inside of the factoryb. research and development costsc. costs of dealing with customers after the saled. general and administrative costs32. Manufacturing costs include all of the following EXCEPT:a. costs incurred inside the factoryb. both direct and indirect costsc. both flexible and capacity-related costsd. both product and period costs33. Nonmanufacturing costs:a. include only capacity-related costsb. seldom influence financial success or failurec. include the cost of selling, distribution, and after-sales costs for customersd. are considered by GAAP to be an element of product costs34. Product costs:a. include administrative and marketing costsb. are particularly useful in financial accountingc. are expensed in the accounting period manufacturedd. are also referred to as nonmanufacturing costs35. For external reporting:a. costs are classified as either product or period costsb. costs reflect current valuesc. there are no prescribed rules since no one is exactly sure how the investors andcreditors will use these numbersd. expenses include amounts that reflect current and future benefits36. Product costs are expensed on the income statement when:a. raw materials for the product are purchasedb. raw materials are requisitioned for the productc. the product completes the manufacturing processd. the product is sold37. Depreciation of plant facilities is classified as a(n):a. direct material costb. direct labor costc. indirect manufacturing costd. general and administrative cost38. The cost of inventory reported on the balance sheet may include the cost of all thefollowing EXCEPT:a. advertisingb. wages of the plant supervisorc. depreciation of the factory equipmentd. parts used in the manufacturing process39. A plant manufactures several different products. The wages of the plant supervisor can beclassified as a:a. direct costb. product costc. flexible costd. nonmanufacturing cost40. Period costs:a. are treated as expenses in the period they are incurredb. are directly traceable to productsc. include direct labord. are also referred to as indirect manufacturing costs41. Which of the following is NOT a period cost?a. marketing costsb. general and administrative costsc. research and development costsd. manufacturing costs42. Advertising is an example of a _________ cost expensed on the income statement in theaccounting period incurred.a. directb. manufacturingc. periodd. product43. (CMA adapted, June 1992) The terms "direct cost" and "indirect cost" are commonlyused in cost accounting. Classifying a cost as either direct or indirect depends upon:a. the behavior of the cost in response to volume changesb. whether the cost is expended in the period in which it is incurredc. whether the cost can be related readily to resources consumed for a cost objectd. whether an expenditure is unavoidable because it cannot be changed regardless of anyaction taken44. Indirect manufacturing costs:a. can be traced to the product that created the costsb. may have a cause-and-effect relationship with capacity rather than with individualunits of productionc. generally include the cost of material and the cost of labord. are included in period costs45. A manufacturing plant produces two product lines: football equipment and hockeyequipment. An indirect cost for the hockey equipment line is the:a. material used to make the hockey sticksb. labor to bind the shaft to the blade of the hockey stickc. shift supervisor for the hockey lined. plant supervisor46. A manufacturing plant produces two product lines: football equipment and hockeyequipment. Direct costs for the football equipment line are the:a. beverages provided daily in the plant break roomb. monthly lease payments for a specialized piece of equipment needed to manufacturethe football helmetc. salaries of the clerical staff that work in the company administrative officesd. utilities paid for the manufacturing plantTHE FOLLOWING INFORMATION APPLIES TO QUESTIONS 47 THROUGH 53.The Bowley Company manufactures several different products. Unit costs associated with product ICT101 are as follows:Direct materials $ 60Direct labor 10Flexible manufacturing support costs 18Capacity-related manufacturing support costs 32Sales commissions (2% of sales) 4Administrative salaries 16Total $14047. Total product costs associated with product ICT101 are:a. $ 50b. $ 88c. $120d. $14048. Total period costs associated with product ICT101 are:a. $ 4b. $16c. $20d. $5249. Total flexible costs associated with product ICT101 are:a. $18b. $22c. $88d. $9250. Total capacity-related costs associated with product ICT101 are:a. $16b. $32c. $48d. $5251. Total nonmanufacturing costs associated with product ICT101 are:a. $ 4b. $16c. $20d. $5252. Total manufacturing costs associated with product ICT101 are:a. $70b. $88c. $120d. $14053. Direct manufacturing costs associated with product ICT101 are:a. $70b. $88c. $92d. $10854. Cost behavior refers to:a. how costs react to a change in the level of activityb. whether a cost is incurred in a manufacturing, merchandising, or service companyc. classifying costs as either product or period costsd. whether a particular expense has been ethically incurred55. Which statement is FALSE?a. All flexible costs are direct costs.b. Because of a cost-benefit tradeoff, some direct costs may be treated as indirect costs.c. All capacity-related costs are indirect costs.d. Direct costs may be flexible or capacity-related.56. An understanding of the underlying behavior of costs helps in all of the followingEXCEPT:a. sales volume can be better estimatedb. costs can be better estimated as volume expands and contractsc. true costs of processes can be better evaluatedd. process inefficiencies can be better identified and, as a result, improved57. Capacity-related costs:a. may be either direct or indirect costsb. vary with production or sales volumec. include parts and materials used to manufacture a productd. can be adjusted in the short run to meet actual demands58. Capacity-related costs depend on:a. the amount of resources usedb. the amount of resources acquiredc. the volume of productiond. the volume of sales59. Currently, most companies consider annual labor costs as:a. a capacity-related costb. a flexible costc. an opportunity costd. a period cost60. Which of the following does NOT describe a flexible cost?a. Flexible cost are always indirect costs.b. Flexible costs increase in total when the actual level of activity increases.c. Flexible costs include most personnel costs and depreciation on machinery.d. Flexible costs can always be traced directly to the cost object.61. Cost-volume-profit analysis is used PRIMARILY by management:a. as a planning toolb. for control purposesc. to establish a target net income for next yeard. to attain extremely accurate financial results62. Contribution margin equals revenues minus:a. product costsb. period costsc. flexible costsd. capacity-related costs63. The break-even point is the level at which revenues:a. equal capacity-related costsb. equal flexible costsc. equal capacity-related costs minus flexible costsd. equal flexible costs plus capacity-related costs64. The break-even point is:a. total costs divided by flexible costs per unitb. contribution margin per unit divided by revenue per unitc. capacity-related costs divided by contribution margin per unitd. (capacity-related costs plus flexible costs) divided by contribution margin per unit65. Cost-volume-profit analysis assumes all of the following EXCEPT:a. all costs are purely flexible or capacity relatedb. units manufactured equal units soldc. total flexible costs remain the same over the relevant ranged. total capacity-related costs remain the same over the relevant range66. All of the following are assumed in a cost-volume-profit analysis EXCEPT:a. a constant product mixb. capacity-related costs increase when activity increasesc. revenue per unit does not change as volume changesd. all costs can be classified as either capacity-related or flexible67. In multiproduct situations, when sales mix shifts toward the product with the highestcontribution margin, then:a. total revenues will decreaseb. breakeven quantity will increasec. total contribution margin will decreased. operating income will increaseTHE FOLLOWING INFORMATION APPLIES TO QUESTIONS 68 THROUGH 71. Karen’s Kraft Korner, Inc., sells a single product. This year, 7,000 units were sold resulting in $70,000 of sales revenue, $28,000 of flexible costs, and $12,000 of capacity-related costs.68. Contribution margin per unit is:a. $4.00b. $4.29c. $6.00d. None of the above is correct.69. Break-even point in units is:a. 2,000 unitsb. 3,000 unitsc. 5,000 unitsd. None of the above is correct.70. The number of units that must be sold to achieve $60,000 of profits is:a. 10,000 unitsb. 11,666 unitsc. 12,000 unitsd. None of the above is correct.71. If sales increase by $25,000, profits will increase by:a. $10,000b. $15,000c. $22,200d. an unknown amountTHE FOLLOWING INFORMATION APPLIES TO QUESTIONS 72 THROUGH 74.Mr. Paul’s Company sells several products for an average price of $20 per unit and the average flexible costs per unit are as follows:Direct material $4.00Direct labor $1.60Indirect manufacturing costs $0.40Selling commissions $2.00Mr. Paul’s annual capacity-related costs total $96,000.72. The contribution margin per unit is:a. $6b. $8c. $12d. $1473. The number of units that Mr. Paul’s must sell each year to break even is:a. 8,000 unitsb. 12,000 unitsc. 16,000 unitsd. an unknown amount74. The number of units that Mr. Paul’s must sell annually to make a profit of $144,000 is:a. 12,000 unitsb. 18,000 unitsc. 20,000 unitsd. 30,000 unitsTHE FOLLOWING INFORMATION APPLIES TO QUESTIONS 75 THROUGH 79.The following information is for Barnett Corporation:Product X Product YRevenue per unit: $10.00 $15.00Flexible cost per unit: $ 2.50 $ 5.00Total capacity-related costs: $50,00075. If the sales mix consists of two units of Product X and one unit of Product Y, what is therevenue per unit of average product?a. $10.00b. $11.66c. $13.33d. $15.0076. If the sales mix consists of two units of Product X and one unit of Product Y, what is thebreak-even point?a. 1,000 units of Y and 2,000 units of Xb. 1012.5 units of Y and 2,025 units of Xc. 2012.5 units of Y and 4,025 units of Xd. 2,000 units of Y and 4,000 units of X77. What is the operating income, assuming actual sales total 150,000 units, and the sales mixis two units of Product X and one unit of Product Y?a. $1,200,000b. $1,250,000c. $1,750,000d. None of the above is correct.78. If the sales mix shifts to one unit of Product X and two units of Product Y, then theweighted-average contribution margin will:a. increase per unitb. stay the samec. decrease per unitd. be undeterminable79. If the sales mix shifts to one unit of Product X and two units of Product Y, then the break-even point will:a. increaseb. stay the samec. decreased. be undeterminable80. Opportunity cost(s):a. of a resource with excess capacity is zerob. should be maximized by organizationsc. are recorded as an expense in the accounting recordsd. are most important to financial accountants81. A recent college graduate has the choice of buying a new auto for $20,000 or to invest themoney for four years with a 12% expected rate of return. If the graduate decides to purchase the auto, the BEST estimate of the opportunity cost of that decision is:a. $2,400b. $11,740c. $20,000d. There is no opportunity cost for this decision.THE FOLLOWING INFORMATION APPLIES TO QUESTIONS 82 THROUGH 86. Brenda’s Brakes manufactures three different product lines, Model X, Model Y, and Model Z. Considerable market demand exists for all models. The following per unit data apply:Model X Model Y Model Z Selling price $50 $60 $70Direct materials 6 6 6Direct labor ($12 per hour) 12 12 24Flexible support costs ($4 per machine hour) 4 8 8Capacity-related costs 10 10 1082. Which model has the greatest contribution per unit?a. Model Xb. Model Yc. Model Zd. both Models X and Y83. Which model has the greatest contribution per machine hour?a. Model Xb. Model Yc. Model Zd. both Models Y and Z84. If there is excess capacity, which model is the most profitable to produce?a. Model Xb. Model Yc. Model Zd. both Models X and Y85. If there is a machine breakdown, which model is the most profitable to produce?a. Model Xb. Model Yc. Model Zd. both Models Y and Z86. How can Brenda encourage her salespeople to promote the more profitable model?a. Put all sales persons on salary.b. Provide higher sales commissions for higher priced items.c. Provide higher sales commissions for items with the greatest contribution margin perconstrained resource.d. Both (b) and (c) are correct.87. Which statement is FALSE? Short run costs:a. are actually flexible costsb. affect long-run capacityc. are included in the calculation of long-run costsd. increase when one more unit is produced or served88. To sustain the profitability of a product, the list price of a product must cover its:a. flexible costsb. capacity-related costsc. indirect costsd. long-run costs89. Compared to the early 1900s, __________ costs now comprise a much higher share of totalproduct costs.a. direct laborb. direct materialsc. flexibled. capacity-related90. In recent years, the manufacturing cost structure has changed as a result of:a. greater automationb. better customer servicec. the proliferation of multiple productsd. All of the above are correct.91. Cost distortion is common in conventional costing systems because:a. of the recent change in cost structureb. the number of products being manufactured is increasingc. capacity-related costs are allocated using a volume measured. capacity-related costs create higher risks for a company92. Costs that must be allocated to products for external reporting purposes include:a. selling and marketing costsb. direct material and direct labor costsc. the cost of equipment used to manufacture several different productsd. All of the above are correct.93. The benefits of classifying activities using the broader framework of unit, batch, product,customer, and business-sustaining activities are that there are generally more costs:a. directly traceable to cost objectsb. treated as indirect costsc. arbitrarily allocated to cost objectsd. There is no major difference regarding costs.94. For budgeting purposes, product-sustaining activity costs should be:a. allocated to individual unitsb. allocated to individual customersc. assigned directly to individual product linesd. assigned directly to individual batches95. Which of the following activities is a unit-related activity?a. preparing and filing the annual tax return for the organizationb. machine setups for each production runc. quality inspections of 2% of the items producedd. obtaining patents and regulatory approval for each product produced96. Which of the following activities is a batch-related activity?a. preparing and filing the annual tax return for the organizationb. machine setups for each production runc. quality inspections of 2% of the items producedd. obtaining patents and regulatory approval for each product produced97. Which of the following activities is a product-sustaining activity?a. preparing and filing the annual tax return for the organizationb. machine setups for each production runc. quality inspections of 2% of the items producedd. obtaining patents and regulatory approval for each product produced98. Which of the following activities is a business-sustaining activity?a. preparing and filing the annual tax return for the organizationb. machine setups for each production runc. making sales callsd. obtaining patents and regulatory approval for each product produced99. Which of the following activities is a customer-sustaining activity?a. preparing and filing the annual tax return for the organizationb. machine setups for each production runc. making sales callsd. obtaining patents and regulatory approval for each product produced100. Product life-cycle costing:a. is useful for external reportingb. is primarily a planning toolc. includes manufacturing costs but not the cost of research and developmentd. assumes product related costs are incurred evenly over the product’s lifetime101. Companies want to ensure that product revenues cover the product’s:a. manufacturing costsb. manufacturing and distribution costsc. developing, supporting, and abandoning costsd. manufacturing, distribution, developing, supporting, and abandoning costs102. More attention is being devoted to the product development and planning phase because:a. abandonment includes significant costsb. of the need to better understand the relevant costsc. during this phase of the product-life cycle, revenues finally begin to cover long-runcostsd. during this phase of the product-life cycle, price competition becomes intense 103. One of the primary motivations for considering costs other than manufacturing and distribution costs is so that:a. these costs can be amortized over the life of the productb. costs can be more evenly distributed over the pr oduct’s life cyclec. planners can develop reasonable estimates of the costs associated with new productsd. if price competition becomes intense the selling price can be rationalizedEXERCISE/PROBLEM104. Winfield Manufacturing Company produces several different products. Classify each of their following costs as direct materials, direct labor, indirect manufacturing costs, or nonmanufacturing costs.a. Production supervisory salaries.b. Controller's office supplies.c. Executive office heat and air conditioning.d. Executive office security personnel.e. Factory heat and air conditioning.f. Supplies used in small quantities, such as glue, to complete assembly work.g. Power to operate factory equipment.h. Parts used in assembly.i. Wages of the assembly-line workers.j. Property taxes on office buildings for sales staff.k. Depreciation on furniture for sales staff.l. Salaries of top executives in the company.m. Wages of the finishing department workers.n. Sales commissions.o. Sales personnel office rental.105. Stephanie’s Stuffed Animals reported the following:Revenues $1,000Flexible manufacturing costs $ 200Flexible nonmanufacturing costs $ 230Capacity-related manufacturing costs $ 150Capacity-related nonmanufacturing costs $ 140Required:a. Compute contribution margin.b. Compute gross margin.c. Compute operating income.106. In 2005, Grant Company has sales of $800,000, flexible costs of $200,000, and capacity-related costs of $300,000. In 2006, Grant Company expects annual property taxes todecrease by $15,000.Required:a. Calculate operating income and the break even point for 2005.b. Calculate the break even point for 2006.107. Sunshine, Inc., sells a single product. The company's most recent income statement is given below.Sales (4,000 units) $120,000Less flexible expenses (68,000)Contribution margin 52,000Less capacity-related expenses (40,000)Net income $ 12,000Required:a. Contribution margin per unit is $ _______________ per unitb. If sales are doubled to $240,000,total flexible costs will equal $ _______________c. If sales are doubled to $240,000,total capacity-related costs will equal $ _______________d. If 10 more units are sold, profits will increase by $ _______________e. Compute how many units must be sold to break even. # _______________f. Compute how many units must be soldto achieve a profit of $20,000. # _______________ 108. Jeffrey’s, Inc., sells a single product. The company's most recent income statement is given below.Sales $200,000Less flexible expenses (120,000)Contribution margin 80,000Less capacity-related expenses (50,000)Net income $ 30,000Required:a. Contribution margin ratio is __________ %b. Break-even point in total sales dollars is $ _______________c. To achieve $40,000 in net income, sales must total $ _______________d. If sales increase by $50,000, net income will increase by $ _______________109. Yurus Manufacturing Company produces two products, X and Y. The following information is presented for both products:X YSelling price per unit $36 $24Flexible cost per unit 28 12Total capacity-related costs $234,000 Required:Assume the sales mix is 3 units of X for every unit of Y:a. What is the revenue per unit of average product, the weighted average flexible cost,and the contribution margin per unit of average product?b. What is the break-even point in units of both X and Y?110. Bob’s Te xtile Company sells shirts for men and boys. The average selling price and flexible cost for each product are as follows:Men’s BoysSelling price $28.80 $24.00Flexible cost $20.42 $16.80Total capacity-related costs $38,400Required:Assume t he sales mix is 2 men’s shirts for each boy’s shirt:a. What is the revenue per unit of average product, the weighted average flexible cost,and the contribution margin per unit of average product?b. What is the break-even point in units for each type of shirt?c. What is the operating income, assuming sales total 9,000 shirts?111. Charlie’s Chairs manufactures two models, Standard and Premium. Weekly demand is estimated to be 120 units of the Standard Model and 70 units of the Premium Model. Only 420 machine hours are available per week. The following per unit data apply:Standard PremiumContribution margin per unit $12 $15Number of machine hours required 2 3Required:a. For each model, compute the contribution per machine hour.b. To maximize weekly production profits, how many machine hours would yourecommend of each model? How many units of each model?c. If there are 500 machine hours available per week (instead of only 420 machine hoursper week), how many chairs of each model shoul d Charlie’s produce to maximizeprofits?。

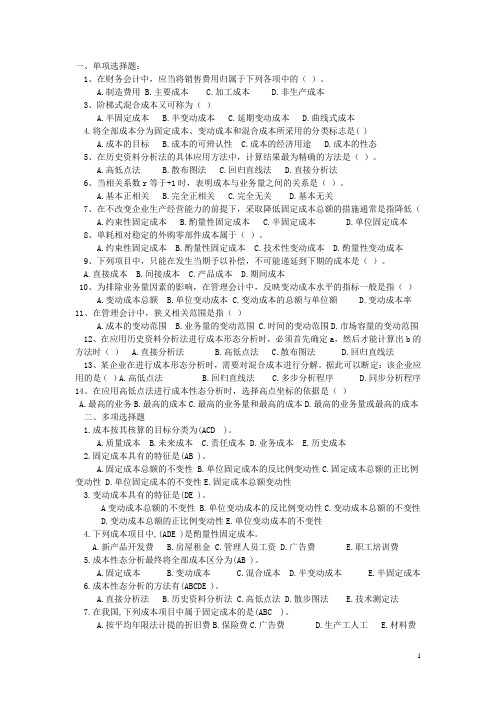

管理会计双语练习题