管理会计双语

财管专业——《管理会计(双语)》

《管理会计(双语)》课程教学大纲课程编码:12120204211课程性质:专业必修课学分:3课时:48开课学期:5适用专业:财务管理一、课程简介《管理会计(双语)是财务管理专业(本科)的一门必修课程。

是以现代企业所处的社会经济环境为背景,明确阐明以企业为主体,密切联系现代会计的预测、决策、规划、控制、考核评价等职能,系统地介绍了现代管理会计的基本理论、基本方法和实用操作技术。

课程分为三部分,第一部分主要交代了管理会计的基本原理和传统管理会计的基本方法;第二部分主要分别讨论管理会计各项职能在实践中的应用程序与具体操作方法。

第三部分集中介绍管理会计发展的新领域。

管理会计是一门理论性较强、计算内容较多的课程。

通过该门课程的学习,使学生领会管理会计的精髓,掌握管理会计的基本理论和基本方法,学会各种分析方法的应用技能和技巧,不断提高学生分析问题和解决问题的能力。

二、教学目标课程总体目标:通过本课程教学,掌握管理会计的基本理论和基本分析方法,结合相应的实践教学,培养学生能独立开展各项管理会计工作的能力。

(一)知识要求:1.了解管理会计的产生与发展,明确管理会计的特点、职能、内容和任务;2.掌握成本习性与变动成本法、本量利分析等管理会计基础分析方法,并了解方法的一般原理;3.掌握短期经营决策分析、长期投资决策分析、全面预算、标准成本控制、责任会计等内容的基本理论与方法。

(二)能力要求:1、具有热爱管理会计工作,爱岗敬业的道德观念;2、具有胜任管理会计工作的良好业务素质和身体素质;3、具有预测、决策、规划、控制的实务能力;4、具有管理会计工作的职业判断、分析和思维能力三、教学内容(一)Chapter 1 Managerial Accounting Concepts and PrinciplesThe main content: Chapter 1 introduces students to managerial accounting and the manufacturing process. Students will learn how managerial accounting is used in the management decision process. They will also be exposed to the terminology used to describe costs related to manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe managerial accounting and the role of managerial accounting in a business.2. Define and illustrate the following costs: 1. direct and indirect costs, 2. direct materials,direct labor, and factory overhead costs, 3. product and period costs.3. Describe and illustrate the following statements for a manufacturing business: 1.balance sheet, 2. statement of cost of goods manufactured, 3. income statement.4. Describe the uses of managerial accounting information.Some key points: direct and indirect costs, direct materials, direct labor, factory overhead costs, product and period costs; cost of goods manufactured.Teaching methods: use of multimedia tools. We ad opt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(二)Chapter 2Job Order CostingThe main content:Chapter 2 introduces students to managerial job order cost systems. Students will be exposed to the terminology used to describe costs related to manufacturing. The first of two basic manufacturing accounting systems, job order, is described in this chapter. Students learn how costs flow through a manufacturing system and the basis for determining product costs under job order costing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe cost accounting systems used by manufacturing businesses.2. Describe and illustrate a job order cost accounting system.3. Describe the use of job order cost information for decision making.4. Describe the flow of costs for a service business that uses a job order cost accountingsystem.Some key points: Job Order Cost System; Overapplied Factory Overhead; Underapplied Factory Overhead; predetermined overhead rate;Teaching methods: use of multimedia tools. We adopt Classroom-based teaching,which is suppl emented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(三)Chapter 3Process Cost SystemsThe main content:Chapter 3 completes the coverage of manufacturing accounting by introducing process costing. The text demonstrates process costing under the FIFO method. The average cost method is presented in th e chapter’s appendix. Chapter 3 also discusses the impact of just-in-time systems on manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe process cost systems.2. Prepare a cost of production report.3. Journalize entries for transactions using a process cost system.4. Describe and illustrate the use of cost of production reports for decision making.5. Compare just-in-time processing with traditional manufacturing processing.Some key points: Process Cost System; First-in, First-out (FIFO) Method; Cost of Production Report; Just-in-Time (JIT) Processing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(四)Chapter 4 Cost Behavior and Cost-Volume-Profit AnalysisThe main content: In Chapter 4, students learn how to conduct cost-volume-profit analysis. In preparation for this activity, the chapter discusses variable, fixed, and mixed costs.Learning Objectives:After studying the chapter, your students should be able to:1. Classify costs as variable costs, fixed costs, or mixed costs.2. Compute the contribution margin, the contribution margin ratio, and the unitcontribution margin.3. Determine the break-even point and sales necessary to achieve a target profit.4. Using a cost-volume-profit chart and a profit-volume chart, determine the break-evenpoint and sales necessary to achieve a target profit.5. Compute the break-even point for a company selling more than one product, theoperating leverage, and the margin of safety.Some key points:variable costs; fixed costs; mixed costs; High-Low Method; Contribution Margin; Cost-Volume-Profit Analysis; Contribution Margin Ratio; Unit Contribution Margin.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(五)Chapter 5 BudgetingThe main content: Chapter 5 emphasizes accounting activities that help managers plan, direct, and control the operations of a business. Budgeting is used to establish business goals in the planning function. Budgets help guide managers’ operational decisions. Budgets are also used to control operations as actual results are compared to the budgeted results.Learning Objectives:After studying the chapter, your students should be able to:1. Describe budgeting, its objectives, and its impact on human behavior.2. Describe the basic elements of the budget process, the two major types of budgeting,and the use of computers in budgeting.3. Describe the master budget for a manufacturing company.4. Prepare the basic income statement budgets for a manufacturing company.5. Prepare balance sheet budgets for a manufacturing company.Some key points: Goal Conflict;Budgetary Slack;Continuous Budgeting;Static Budget;Flexible Budget;Zero-Based Budgeting;Capital Expenditures Budget.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(六)Chapter 6 Performance Evaluation Using Variances from Standard Costs The main content: Standard cost systems set budgets for the materials, labor, and factory overhead used by a manufacturer to produce its product. Deviations from these standards are reported as variances.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the types of standards and how they are established.2. Describe and illustrate how standards are used in budgeting.3. Compute and interpret direct materials and direct labor variances.4. Compute and interpret factory overhead controllable and volume variances.5. Journalize the entries for recording standards in the accounts and prepare an incomestatement that includes variances from standard.6. Describe and provide examples of nonfinancial performance measures.Some key points: Direct Labor Rate Variance ;Direct Materials Price Variance;Direct Labor Time Variance;Direct Materials Quantity Variance;Budgeted Variable Factory Overhead;Factory Overhead Cost Variance Report;Controllable Variance;Volume Variance.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(七)Chapter 7 Performance Evaluation for Decentralized Operations The main content: Chapter 7 applies responsibility accounting to cost, profit, and investment centers. The chapter demonstrates the responsibility accounting reports that are used to evaluate department or division performance. This provides an excellent opportunity to remind your students that managers are judged, at least in part, using accounting data.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the advantages and disadvantages of decentralized operations.2. Prepare a responsibility accounting report for a cost center.3. Prepare responsibility accounting reports for a profit center.4. Compute and interpret the rate of return on investment, the residual income, and thebalanced scorecard for an investment center.5. Describe and illustrate how the market price, negotiated price, and cost priceapproaches to transfer pricing may be used by decentralized segments of a business.Some key points:Responsibility Accounting;Balanced Scorecard;Profit Margin;DuPont Formula;Rate of Return on Investment (ROI);Investment Center ;Residual Income;Investment TurnoverTeaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(八)Chapter 8 Differential Analysis, Product Pricing, and Activity-Based CostingThe main content: This chapter covers (1) differential analysis, (2) methods of determining the selling price of a product using a cost-plus markup approach, (3) the effects of production bottlenecks, and (4) activity-based costing. The cost-plus approach of product cost is described in Objective 2; total cost and variable cost methods are presented in the chapter appendix. All topics in this chapter are able to stand alone. Therefore, the instructor is free to cover only one or two of the topics if class time is a limited resource as the term draws to a close.Learning Objectives:After studying the chapter, your students should be able to:1. Prepare differential analysis reports for a variety of managerial decisions.2. Determine the selling price of a product, using the product cost concept.3. Compute the relative profitability of products in bottleneck production processes.4. Allocate product costs using activity-based costing.Some key points:Product Cost Concept ; Target Costing; Production Bottleneck; Theory of Constraints (TOC); Activity-Based Costing (ABC).Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(九)Chapter 9 Capital Investment AnalysisThe main content: Capital investment analysis is a topic that usually receives detailed coverage in introductory finance courses and/or intermediate accounting. The purpose of this chapter is to give students a brief introduction to the basics of capital investment analysis using the following methods: average rate of return, cash payback, net present value, and internal rate of return.Learning Objectives:After studying the chapter, your students should be able to:1. Explain the nature and importance of capital investment analysis.2. Evaluate capital investment proposals using the average rate of return and cashpayback methods.3. Evaluate capital investment proposals using the net present value and internal rate ofreturn methods.4. List and describe factors that complicate capital investment analysis.5. Diagram the capital rationing process.Some key points: Capital Investment Analysis;Time Value of Money Concept;Average Rate of Return;Cash Payback Period;Internal Rate of Return (IRR) Method;Capital Rationing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.四、整体课时分配五、课程考核与成绩评定1.考核方式:考查;笔试;闭卷。

管理会计双语版总结

8

Chapter 6 : Business Decisions using Cost Behavior

Cost-volume-profit analysis

Actual cost system vs. normal cost system

Over-apply vs. under-apply

Process costing

Equivalent units and ost of ending work-in-process

Contribution margin

total vs. per unit Contribution margin ratio

Break-even (in units and in dollars) Target profit (in units and in dollars)

Three formulas (page 136)

4

Chapter 3 :Determining Costs of Products

Job order costing

Direct material : trace

Direct labor : trace

Manufacturing overhead : allocate

Cost pool and allocation base

Cost of completed units

5

Chapter 4 : Activity Based Costing

ABC

Cost driver : causes the cost to occur Steps to employ ABC

推行管理会计双语教学实践研究

推行管理会计双语教学实践研究一、管理会计双语教学的概念管理会计双语教学是指在管理会计教学中,借助双语教学手段,将英语作为第二语言,从而提高学生的英语水平以及管理会计知识的学习效果。

它是全球化背景下的一种教学创新模式,通过将英语与管理会计相结合,使学生能够更好地理解管理会计知识,提高自身的跨文化交流能力和竞争力。

二、管理会计双语教学的意义1.促进学生的语言能力提升管理会计双语教学能够有效提升学生的英语水平,使他们在学习过程中不仅仅掌握了管理会计的理论知识,同时也提高了语言沟通能力和跨文化交流能力。

2.增强学生的国际化视野通过管理会计双语教学,学生将更容易接触到国外的管理会计理论和实践经验,培养国际化背景下的管理会计人才,以适应全球化时代的挑战。

3.提高管理会计实践能力管理会计双语教学能够帮助学生更好地理解国际管理会计的前沿知识和技术,加深对管理会计实践的理解,为将来的职业发展打下坚实的基础。

三、管理会计双语教学的实践研究近年来,国内外对管理会计双语教学的实践研究逐渐展开。

在国际上,一些知名的大学和学术机构开始探索在管理会计教学中引入英语教学的新模式,取得了一定的成果。

在国内,也有一些高校开始尝试管理会计双语教学,但由于条件和观念的不同,实践过程中也遇到了一些困难和挑战。

就国内而言,管理会计双语教学的实践研究还处于起步阶段。

通过对一些高校的案例分析,可以发现学生对这种教学模式的接受度较高,但教师对于教学内容和教学方法的调整还存在一定的困难。

学生在语言水平和专业知识上的双重压力也需要得到重视和解决。

四、管理会计双语教学的发展前景管理会计双语教学的发展前景是值得期待的。

随着经济全球化和国际贸易的不断深入,管理会计双语教学将成为国内高校管理会计教学的一种趋势。

学生对于这种教学模式的接受度很高,他们对于未来的国际化就业也具有了更多的优势。

不断完善教学体系和培养教师团队,也将是管理会计双语教学发展的重要保障。

《管理会计(双语)》课程 (4)

12

Predetermined Overhead Rates

Because the total indirect costs for the year are not known until after the year end, organizations allocate indirect costs to production during the year based on predetermined indirect cost rates

Manufacturing costs are classified into three groups:

– Direct Materials – Direct Labor – Manufacturing Overhead

Materials are withdrawn from raw materials inventory as production begins

depreciation and salaries paid to administrative employees

Direct Cost—a cost that is uniquely and unequivocally attributable to a single cost object

– Almost all variable costs are direct costs

Manufacturing, retail, and service organizations have different patterns of cost flows resulting in different management accounting priorities

《管理会计(双语)》课程 (1)

9

Behavioral Implications

As measurements are made on operations and especially on individuals and groups their behavior changes

When the measurements are used not only for information, planning, and decision-making, but also for control, evaluation, and reward, employees and managers place great pressure on the measurements themselves

– People react when they are being measured, and they react to the measurements

– They focus on the variables and behavior being measured and spend less attention on those not measured

Early 20th century – DuPont and General Motors expanded the focus to planning and control

1970’s – Japanese manufacturers developed new tools to report on quality, service, customer, and employee performance

《管理会计》双语案例教学实例分析

总额 因业务量 的变动而成正 比例变动 ,但单位变动成本

( 单位业务量负担的变动成本) 不变。 ③混合成本。 混合成本

就是“ 混合” 了固定成本和变动成本两种不 同性质的成本 。 方面 , 它们要随业务量 的变化而变化 ; 另一方面, 它们的 变化又不能与业务量 的变化保持着纯粹 的正比例关系。 混

程展示给所有的学生 , 把其中出现的问题带到学生的思考中

去解决 。 例如在 教学角 的度量 时 , 利用投 影把量角器放 大 , 学 生结合 自己手 中的量角器一起认识各部分的功能, 更具有影

响力。 教学角的量法, 教师可以在投影仪下操作 , 学生一边听 着操作过程 , 一边看着教师操作, 把头脑 中听到的影像与实 际操作结合起来 , 更真切的体会了测量的过程。 之后的练习, 学生也可以借助投影仪把 自己的操作过程展示给全体学生 , 这其中出现的一些问题 , 在学生中就解决了。现代化的教学 硬件设施把学生的眼睛擦的更亮了, 把学生大的思维擦的更 敏捷了, 把知识展现的更全面具体了。 除了硬件的应用 , 软件 的音像教材 , 如教学幻灯片、 投

中图分 类号 : G 6 4 2 . 0 文献标 志码 : A 文章编 号 : 1 6 7 4 — 9 3 2 4 ( 2 O 1 3 ) 2 4 - 0 0 5 0 — 0 3

案例教学法是一种启发学生研究实际问题 , 注重学生 智力开发及能力培养的现代教学方法 , 它有着传统教学方 法所不具备的特殊功能。《 管理会计》 课程实践性强 , 采用 案 例教 学 模 式 , 给予 学 生积 极 思 考 、 用英 语 踊 跃 发 言 的 自 我表现机会 , 加深学生对学科基础知识在实践中运用的理 解, 通过用英语讨论 , 使得学生专业知识和英语语言均得 到 提高 , 同时使 学 生对 实 际工作 中出现 的问题 获得 较 正 确 和透彻 的理解。 本文拟 以《 管理会计》 中成本性态 的知识介 绍案例教学方法如何在双语教学 中组织和开展的。

管理会计(双语)教学大纲

《管理会计》(双语)教学大纲课程名称:《管理会计》(双语)课程编码:B0421004适用专业及层次:会计学专业本科层次课程总学时:48学时课程总学分:3学分理论学时:48学时实践学时:0学时先修课程:会计学原理、成本会计等一、课程的性质、目的与任务管理会计是会计、财管专业的专业基础课。

通过本课程的教学,使学生了解现代管理会计学在会计学科体系中的地位和作用,掌握管理会计的基本内容和基本理论,学会如何在社会主义市场经济条件下和现代企业制度环境中,进一步加工和运用企业内部财务信息,预测经济前景、参与经营决策、规划经营方针、控制经营过程和考评责任业绩的基本程序、操作技能和基本方法。

二、教学内容、教学要求及教学重难点CHAPTER 1 The Role, History, and Direction of Management Accounting【教学内容】Chapter 1 provides an overview of management accounting. This chapter also is anopportunity to discuss ethical behavior.【教学要求】1. Learning the role of management accountants in an organization, and could provide a briefhistorical description of management accounting;2. Mastering the differences between management accounting and financial accounting;3. Understanding the current focus of management accounting,and the importance of ethicalbehavior for managers and management accountants【教学重难点】1. Mastering the differences between management accounting and financial accounting;2. Understanding the current focus of management accounting.CHAPTER 2 Basic Management Accounting Concepts【教学内容】This chapter introduces basic terminology that is used throughout the text. Accounting issometimes called the language of business. Learning the accounting terminology in Chapter 2 is similar to learning a foreign language. Understanding the accounting terminology in Chapter 2 is crucial to students understanding topics covered later.【教学要求】1. Learning tangible and intangible products and explain why there are different product costdefinitions;2. Mastering could prepare income statements for manufacturing and service organizations;3. Understanding the cost assignment process, and the differences between functional-based andactivity-based management accounting systems.【教学重难点】1. Mastering could prepare income statements for manufacturing and service organizations;2. Learning tangible and intangible products and explain why there are different product costdefinitions;CHAPTER 3 Activity Cost Behavior【教学内容】This chapter expands the discussion of cost behavior in Chapter 2; more specifically, it focuses on activity cost behavior. In addition, the resource usage model is presented. This chapter is an important foundation for the activity-based costing system discussed in the next chapter. In addition, several methods to estimate and evaluate the cost equation are discussed.【教学要求】1. Learning cost behavior for fixed, variable, and mixed costs , and the role of multipleregression in assessing cost behavior ;2.Mastering how to separate mixed costs into their fixed and variable components using thehigh-low method, the scatter plot method, and the method of least squares ;3. Understanding the role of the resource usage model in understanding cost behavior, and theuse of managerial judgment in determining cost behavior.【教学重难点】1. Mastering how to separate mixed costs into their fixed and variable components using thehigh-low method, the scatter plot method, and the method of least squares ;2. Understanding the role of the resource usage model in understanding cost behavior, and theuse of managerial judgment in determining cost behavior.CHAPTER 4 Activity-Based Costing【教学内容】Technological changes in manufacturing have made the traditional costing method obsolete in many firms. Unit-based cost systems often are no longer adequate in measuring product costs because overhead costs have increased while direct labor costs have decreased. This chapter introduces an approach that can improve product costing in many firms.【教学要求】1. Learning the importance of unit costs, a detailed description of how activities can be grouped intohomogeneous sets to reduce the number of activity rates2. Mastering how an activity-based costing system works, activity-based customer and suppliercosting;3. Understanding functional-based costing approaches, and why functional-based costingapproaches may produce distorted costs.【教学重难点】1. Mastering how an activity-based costing system works, activity-based customer and suppliercosting;2. Understanding functional-based costing approaches, and why functional-based costingapproaches may produce distorted costs.CHAPTER 5 Job-Order Costing【教学内容】Product costing plays a critical role in the new manufacturing environment and has become a significant factor in the service industries with the impact of deregulation. Nonaccounting majors should realize that understanding the basics of product costing is an important topic covered in the course. This chapter introduces students to the important topic of job-order costing.【教学要求】1. Mastering the differences between job-order costing and process costing, and identify the types offirms that would use each method, and the cost flows associated with job-order costing;2. Understanding how to identify and set up the source documents used in job-order costing.【教学重难点】Mastering the differences between job-order costing and process costing, and identify the typesof firms that would use each method, and the cost flows associated with job-order costing; CHAPTER 6 Process Costing【教学内容】If time permits, coverage of process costing is recommended. It exposes students to a different method of determining costs for products and provides useful insights in later chapters. The material in this chapter is generally difficult for the students because of the amount of detail. If you wish to cover this lightly, I suggest you focus on the weighted average approach.【教学要求】1. Learning the basic characteristics and cost flows associated with process manufacturing, and equivalent units and explain their role in process costing2. Mastering the differences between the weighted average method and the FIFO method ofaccounting for process costs, and prepare a departmental production report using the weighted average method;3. Understanding how to how process costing is affected by nonuniform application of manufacturinginputs and the existence of multiple processing departments.【教学重难点】1. Mastering the differences between the weighted average method and the FIFO method ofaccounting for process costs, and prepare a departmental production report using the weightedaverage method;2. Understanding how to how process costing is affected by nonuniform application of manufacturinginputs and the existence of multiple processing departments.CHAPTER 7 Support Department Cost Allocation【教学内容】Allocation of support-department costs is an important topic for product costing. In recent years the issue of accurate product costing has assumed considerable importance, and managers need to be fully aware of how products are costed and the limitations associated with those assignments. The introductory scenario discusses a copying department in a large regional public accounting firm.【教学要求】1. Mastering how to calculate single charging rates for a support department, and allocatesupport-department costs to producing departments using the direct, sequential, and reciprocalmethods, and calculate departmental overhead rate;2. Understanding the difference between support departments and producing departments..【教学重难点】1. Mastering how to calculate single charging rates for a support department, and allocatesupport-department costs to producing departments using the direct, sequential, and reciprocalmethods, and calculate departmental overhead rate;CHAPTER 8 Functional and Activity-Based Budgeting【教学内容】Budgeting is one topic that most students can relate to since they are involved with their own personal budgets. Students may benefit by reading the scenario at the beginning of the chapter.【教学要求】1. Learning budgeting and discuss its role in planning, control, and decision making;2. Mastering the master budget, identify its major components, and explain the interrelationships of thevarious components, and flexible budgeting and identify the features that a budgetary system should have to encourage managers to engage in goal-congruent behavior.3. Understanding activity-based budgeting.【教学重难点】1.Mastering the master budget, identify its major components, and explain the interrelationships of the various components, and flexible budgeting and identify the features that a budgetary system should have to encourage managers to engage in goal-congruent behavior.2. Understanding activity-based budgeting.CHAPTER 9 Standard Costing: A Managerial Control Tool【教学内容】This chapter covers standard costing and variances.【教学要求】1. Learning how unit standards are set and why standard cost systems are adopted, and the purpose of a standard cost sheet.2. Mastering how to compute the materials and labor variances and explain how they are used forcontrol, and the variable and fixed overhead variances and explain their meanings;3. Understanding the basic concepts underlying variance analysis and explain when variances should beInvestigated.【教学重难点】1. Mastering how to compute the materials and labor variances and explain how they are used forcontrol, and the variable and fixed overhead variances and explain their meanings;2. Understanding the basic concepts underlying variance analysis and explain when variances should beInvestigated.CHAPTER 10 Activity- and Strategic-Based Responsibility Accounting【教学内容】Activity-based management is a fairly new topic in management accounting textbooks. This chapter is important in order to understand the new environment in management accounting. The scenario to Chap- ter 10 is a good place for students to start. In addition, students should be comfortable with the topics from Chapters 3 and 4.【教学要求】1. Learning the difference among functional-based, activity-based, and strategic-based responsibilityaccounting systems.2. Mastering the basic features of the Balanced Scorecard;3. Understanding process value analysis and activity performance measurement.【教学重难点】1. Mastering the basic features of the Balanced Scorecard;2. Understanding process value analysis and activity performance measurement.CHAPTER 11 Quality Costs and Productivity: Measurement, Reporting, and Control【教学内容】This chapter focuses on the measurement and control of quality costs, and does a good job of discussing a topic that is not presented in most first-level management accounting textbooks. It provides an excellent bridge to understanding the new manufacturing environment of a world-class manufacturer. The opening scenario provides an interesting discussion of quality issues.【教学要求】1. Learning the four types of quality costs;2. Mastering how to prepare a quality cost report and explain the difference between the conventionalview of acceptable quality level and the view espoused by total quality control and why quality cost information is needed and how it is used;3. Understanding what productivity is and calculate the impact of productivity changes on profits.【教学重难点】1.Mastering how to prepare a quality cost report and explain the difference between theconventional view of acceptable quality level and the view espoused by total quality control and why quality cost information is needed and how it is used;2. Understanding what productivity is and calculate the impact of productivity changes on profits. CHAPTER 12 Environmental Cost Management【教学内容】In this chapter, Hansen and Mowen discuss environmental and life-cycle costs. These issues are presented in the scenario at the beginning of the chapter.【教学要求】1. Learning the importance of measuring environmental costs;2. Mastering how environmental costs are assigned to products and processes;3. Understanding the life-cycle cost assessment model, and activity- and strategic-based environmentalcontrol.【教学重难点】1. Mastering how environmental costs are assigned to products and processes;2. Understanding the life-cycle cost assessment model, and activity- and strategic-based environmentalcontrol.CHAPTER 13 Performance Evaluation in the Decentralized Firm【教学内容】The scenario in this chapter illustrates some of the issues faced by firms selling abroad. This chapter is relevant because of global competition faced by many firms.【教学要求】1. Learning responsibility accounting and four types of responsibility centers;2. Mastering how to compute and explain return on investment (ROI) and economic value added(EVA);3. Understanding why firms choose to decentralize, and methods of evaluating and rewarding managerial performance, the role of transfer pricing in a decentralized firm.【教学重难点】Mastering how to compute and explain return on investment (ROI) and economic value added(EVA);CHAPTER 14 International Issues in Management Accounting【教学内容】The scenario in this chapter illustrates some of the issues faced by firms selling abroad. This chapter is relevant because of global competition faced by many firms.【教学要求】1. Learning the role of the management accountant in the international environment, and the varying levels of involvement that firms can undertake in international trade;2. Mastering the ways management accountants can manage foreign currency risk,3. Understanding why multinational firms choose to decentralize, and how environmental factors can affect performance evaluation in the multinational firm, and the role of transfer pricing in the multinational firm.【教学重难点】1. Mastering the ways management accountants can manage foreign currency risk;2. Understanding why multinational firms choose to decentralize, and how environmental factors canaffect performance evaluation in the multinational firm, and the role of transfer pricing in themultinational firm.CHAPTER 15 Segmented Reporting and Performance Evaluation【教学内容】Coverage of this chapter expands on material outlined briefly in Chapter 2. Here we use thevariable-costing income statement as a way to organize information on cost behavior. A variety of management decision-making applications are presented.【教学要求】1. Learning the differences between variable and absorption costing;2. Mastering how variable costing is useful in evaluating the performance of managers, and how to prepare a segmented income statement based on a variable-costing approach and explain how this format can be used with activity-based costing to assess customer profitability.3. Understanding why multinational firms choose to decentralize, and how environmental factors can affect performance evaluation in the multinational firm, and the role of transfer pricing in the multinational firm.【教学重难点】1. Mastering how variable costing is useful in evaluating the performance of managers, and how to prepare a segmented income statement based on a variable-costing approach and explain how this format can be used with activity-based costing to assess customer profitability.2. Understanding why multinational firms choose to decentralize, and how environmental factors can affect performance evaluation in the multinational firm, and the role of transfer pricing in the multinational firm.CHAPTER 16 Cost-Volume-Profit Analysis: A Managerial Planning Tool【教学内容】Cost-volume-profit (CVP) analysis can be used to illustrate how managers use accounting data for planning and decision making. Students who enjoy solving puzzles will probably enjoy the discussion of CVP. A more complete analysis of the subject material can be taught by using simple algebra.【教学要求】1. Learning the impact of activity-based costing on cost-volume-profit analysis;2. Mastering the number of units that must be sold to break even or to earn a targeted profit., the amount of revenue required to break even or to earn a targeted profit, and apply cost-volume-profit analysis in a multiple-product setting;3.Understanding a profit-volume graph and a cost-volume-profit graph and explain themeaning of each, and the impact of risk, uncertainty, and changing variables on cost-volume-profit analysis.【教学重难点】Mastering the number of units that must be sold to break even or to earn a targeted profit., theamount of revenue required to break even or to earn a targeted profit, and apply cost-volume-profit analysis in a multiple-product setting;CHAPTER 17 Tactical Decision Making【教学内容】This chapter deals with relevant information and how it is used in short-run decisions.【教学要求】1. Learning the tactical decision-making model;2. Mastering how the activity resource usage model is used in assessing relevancy, and how to apply the tactical decision-making concepts in a variety of business situations.3.Understanding the impact of cost on pricing decisions.【教学重难点】Mastering how the activity resource usage model is used in assessing relevancy, and how to apply the tactical decision-making concepts in a variety of business situations.CHAPTER 18 Capital Investment Decisions【教学内容】This chapter covers the basic capital budgeting models. Taxes are considered later in the chapter. The focus of the chapter is on learning how to apply the models.【教学要求】1. Learning what a capital investment decision is and distinguish between independent and mutually exclusive capital investment decisions;2. Mastering how to compute the payback period and accounting rate of return for a proposed investment and explain their roles in capital investment decisions, and use net present value analysis for capital investment decisions involving independent projects, and use the internal rate of return to assess the acceptability of independent projects.3. Understanding the role and value of postaudits, and why NPV is better than IRR for capitalinvestment decisions involving mutually exclusive projects.【教学重难点】Mastering how to compute the payback period and accounting rate of return for a proposed investmentand explain their roles in capital investment decisions, and use net present value analysis for capital investment decisions involving independent projects, and use the internal rate of return to assess the acceptability of independent projects.CHAPTER 19 Inventory Management【教学内容】The material in this chapter tends to be more quantitative than in previous chapters. While thematerial is very important to many management accountants, the discussion of these topics is often delayed until the second managerial/cost accounting class.【教学要求】1. Learning the traditional inventory management model, and the theory of constraints and explain how it can be used to manage inventory.2. Understanding JIT inventory management, and long-term contracts, continuous replenishment, electronic data interchange, and JIT II.【教学重难点】Understanding JIT inventory management, and long-term contracts, continuous replenishment, electronic data interchange, and JIT II.三、教学章节及学时分配(一)总体学时分配四、教学方法与教学手段说明教学方法式是以普通理论课堂教学和案例教学为主要形式,注重培养学生活学活用的能力。

《管理会计(双语)》课程 (6)

Managing Customer Profitability

High-profit customers appear in the left section of the profitability whale curve

– These customers should be protected – They could be vulnerable to competitive inroads – Managers should be prepared to offer discounts,

Both financial and nonfinancial metrics are needed to manage performance with customers

To balance the pressure to meet and exceed customer expectations, companies should also measure the cost to sfits generated

15

Salesperson Incentives

A typical salesperson’s compensation plan sets minimum quotas and provides incentive commissions based on sales revenue

There may be special rewards such as vacation trips for achieving sales revenues above a stretch goal

– Strive to reduce costs of setup and order handling – Encourage customers to place orders electronically

《管理会计(双语)》教学大纲

《管理会计(双语)》课程教学大纲课程编码:12120203k206课程性质:专业必修课学分:3课时:48开课学期:第五学期适用专业:会计学一、课程简介《管理会计(双语》是会计学专业(本科)的一门必修课程。

是以现代企业所处的社会经济环境为背景,明确阐明以企业为主体,密切联系现代会计的预测、决策、规划、控制、考核评价等职能,系统地介绍了现代管理会计的基本理论、基本方法和实用操作技术。

课程分为三部分,第一部分主要交代了管理会计的基本原理和传统管理会计的基本方法;第二部分主要分别讨论管理会计各项职能在实践中的应用程序与具体操作方法。

第三部分集中介绍管理会计发展的新领域。

管理会计是一门理论性较强、计算内容较多的课程。

通过该门课程的学习,使学生领会管理会计的精髓,掌握管理会计的基本理论和基本方法,学会各种分析方法的应用技能和技巧,不断提高学生分析问题和解决问题的能力。

二、教学目标课程总体目标:通过本课程教学,掌握管理会计的基本理论和基本分析方法,结合相应的实践教学,培养学生能独立开展各项管理会计工作的能力。

具体入下:1.了解管理会计的产生与发展,明确管理会计的特点、职能、内容和任务;2.掌握成本习性与变动成本法、本量利分析等管理会计基础分析方法,并了解方法的一般原理;3.掌握短期经营决策分析、长期投资决策分析、全面预算、标准成本控制、责任会计等内容的基本理论与方法。

三、教学内容(一)Chapter 1 Managerial Accounting Concepts and PrinciplesThe main content: Chapter 1 introduces students to managerial accounting and the manufacturing process. Students will learn how managerial accounting is used in the management decision process. They will also be exposed to the terminology used to describe costs related to manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe managerial accounting and the role of managerial accounting in a business.2. Define and illustrate the following costs: 1. direct and indirect costs, 2. direct materials,direct labor, and factory overhead costs, 3. product and period costs.3. Describe and illustrate the following statements for a manufacturing business: 1.balance sheet, 2. statement of cost of goods manufactured, 3. income statement.4. Describe the uses of managerial accounting information.Some key points: direct and indirect costs, direct materials, direct labor, factory overhead costs, product and period costs; cost of goods manufactured.Teaching methods: use of multimedia tools. We ad opt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(二)Chapter 2Job Order CostingThe main content:Chapter 2 introduces students to managerial job order cost systems. Students will be exposed to the terminology used to describe costs related to manufacturing. The first of two basic manufacturing accounting systems, job order, is described in this chapter. Students learn how costs flow through a manufacturing system and the basis for determining product costs under job order costing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe cost accounting systems used by manufacturing businesses.2. Describe and illustrate a job order cost accounting system.3. Describe the use of job order cost information for decision making.4. Describe the flow of costs for a service business that uses a job order cost accountingsystem.Some key points: Job Order Cost System; Overapplied Factory Overhead; Underapplied Factory Overhead; predetermined overhead rate;Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is suppl emented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(三)Chapter 3Process Cost SystemsThe main content:Chapter 3 completes the coverage of manufacturing accounting by introducing process costing. The text demonstrates process costing under the FIFO method.The average cost method is presented in th e chapter’s appendix. Chapter 3 also discusses the impact of just-in-time systems on manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe process cost systems.2. Prepare a cost of production report.3. Journalize entries for transactions using a process cost system.4. Describe and illustrate the use of cost of production reports for decision making.5. Compare just-in-time processing with traditional manufacturing processing.Some key points: Process Cost System; First-in, First-out (FIFO) Method; Cost of Production Report; Just-in-Time (JIT) Processing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(四)Chapter 4 Cost Behavior and Cost-Volume-Profit AnalysisThe main content: In Chapter 4, students learn how to conduct cost-volume-profit analysis. In preparation for this activity, the chapter discusses variable, fixed, and mixed costs.Learning Objectives:After studying the chapter, your students should be able to:1. Classify costs as variable costs, fixed costs, or mixed costs.2. Compute the contribution margin, the contribution margin ratio, and the unitcontribution margin.3. Determine the break-even point and sales necessary to achieve a target profit.4. Using a cost-volume-profit chart and a profit-volume chart, determine the break-evenpoint and sales necessary to achieve a target profit.5. Compute the break-even point for a company selling more than one product, theoperating leverage, and the margin of safety.Some key points:variable costs; fixed costs; mixed costs; High-Low Method; Contribution Margin; Cost-Volume-Profit Analysis; Contribution Margin Ratio; Unit Contribution Margin.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(五)Chapter 5 BudgetingThe main content: Chapter 5 emphasizes accounting activities that help managers plan, direct, and control the operations of a business. Budgeting is used to establish business goals in the planning function. Budgets help guide managers’ operational decisions. Budgets are also used to control operations as actual results are compared to the budgeted results.Learning Objectives:After studying the chapter, your students should be able to:1. Describe budgeting, its objectives, and its impact on human behavior.2. Describe the basic elements of the budget process, the two major types of budgeting,and the use of computers in budgeting.3. Describe the master budget for a manufacturing company.4. Prepare the basic income statement budgets for a manufacturing company.5. Prepare balance sheet budgets for a manufacturing company.Some key points: Goal Conflict;Budgetary Slack;Continuous Budgeting;Static Budget;Flexible Budget;Zero-Based Budgeting;Capital Expenditures Budget.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(六)Chapter 6 Performance Evaluation Using Variances from Standard Costs The main content: Standard cost systems set budgets for the materials, labor, and factory overhead used by a manufacturer to produce its product. Deviations from these standards are reported as variances.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the types of standards and how they are established.2. Describe and illustrate how standards are used in budgeting.3. Compute and interpret direct materials and direct labor variances.4. Compute and interpret factory overhead controllable and volume variances.5. Journalize the entries for recording standards in the accounts and prepare an incomestatement that includes variances from standard.6. Describe and provide examples of nonfinancial performance measures.Some key points: Direct Labor Rate Variance ;Direct Materials Price Variance;Direct Labor Time Variance;Direct Materials Quantity Variance;Budgeted Variable Factory Overhead;Factory Overhead Cost Variance Report;Controllable Variance;Volume Variance.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(七)Chapter 7 Performance Evaluation for Decentralized Operations The main content: Chapter 7 applies responsibility accounting to cost, profit, and investment centers. The chapter demonstrates the responsibility accounting reports that are used to evaluate department or division performance. This provides an excellent opportunity to remind your students that managers are judged, at least in part, using accounting data.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the advantages and disadvantages of decentralized operations.2. Prepare a responsibility accounting report for a cost center.3. Prepare responsibility accounting reports for a profit center.4. Compute and interpret the rate of return on investment, the residual income, and thebalanced scorecard for an investment center.5. Describe and illustrate how the market price, negotiated price, and cost priceapproaches to transfer pricing may be used by decentralized segments of a business.Some key points:Responsibility Accounting;Balanced Scorecard;Profit Margin;DuPont Formula;Rate of Return on Investment (ROI);Investment Center ;Residual Income;Investment TurnoverTeaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(八)Chapter 8 Differential Analysis, Product Pricing, and Activity-Based Costing The main content: This chapter covers (1) differential analysis, (2) methods of determining the selling price of a product using a cost-plus markup approach, (3) the effects of production bottlenecks, and (4) activity-based costing. The cost-plus approach of product cost is described in Objective 2; total cost and variable cost methods are presented in thechapter appendix. All topics in this chapter are able to stand alone. Therefore, the instructor is free to cover only one or two of the topics if class time is a limited resource as the term draws to a close.Learning Objectives:After studying the chapter, your students should be able to:1. Prepare differential analysis reports for a variety of managerial decisions.2. Determine the selling price of a product, using the product cost concept.3. Compute the relative profitability of products in bottleneck production processes.4. Allocate product costs using activity-based costing.Some key points:Product Cost Concept ; Target Costing; Production Bottleneck; Theory of Constraints (TOC); Activity-Based Costing (ABC).Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(九)Chapter 9 Capital Investment AnalysisThe main content: Capital investment analysis is a topic that usually receives detailed coverage in introductory finance courses and/or intermediate accounting. The purpose of this chapter is to give students a brief introduction to the basics of capital investment analysis using the following methods: average rate of return, cash payback, net present value, and internal rate of return.Learning Objectives:After studying the chapter, your students should be able to:1. Explain the nature and importance of capital investment analysis.2. Evaluate capital investment proposals using the average rate of return and cashpayback methods.3. Evaluate capital investment proposals using the net present value and internal rate ofreturn methods.4. List and describe factors that complicate capital investment analysis.5. Diagram the capital rationing process.Some key points: Capital Investment Analysis;Time Value of Money Concept;Average Rate of Return;Cash Payback Period;Internal Rate of Return (IRR) Method;Capital Rationing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.四、整体课时分配五、实验教学1. 实验项目与课时分配3.实验报告The basic requirements of the experiment report, including: name of the experiment, purpose of the experiment, case data, case analysis, conclusions and enlightenment.六、课程考核与成绩评定1.考核方式:考查;笔试;闭卷。

《管理会计(双语)》atkinson6e REVISED (4)

In service organizations, the focus is on determining the cost of a project or service

The primary focus in retail operations is the profitability of product lines or epartments

© 2012 Pearson Prentice Hall. All rights reserved.

5

Service Organizations

– This is often called a fixed cost

– Examples include equipment and building depreciation and salaries paid to administrative employees

Direct Cost—a cost that is uniquely and unequivocally attributable to a single cost object

Stores incur various overhead costs such as depreciation, lighting, labor, and heating

Once the sale is made, the costs transfer to cost of goods sold

Accumulating and Assigning Costs to Products

Chapter 4

《管理会计(双语)》章节 (1)

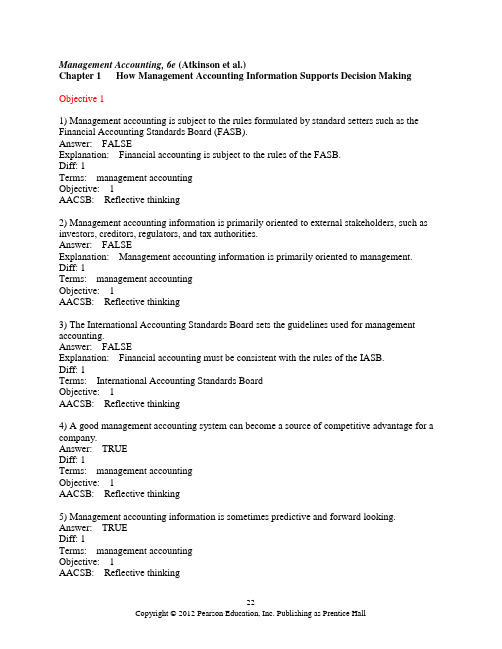

Management Accounting, 6e (Atkinson et al.)Chapter 1 How Management Accounting Information Supports Decision Making Objective 11) Management accounting is subject to the rules formulated by standard setters such as the Financial Accounting Standards Board (FASB).Answer: FALSEExplanation: Financial accounting is subject to the rules of the FASB.Diff: 1Terms: management accountingObjective: 1AACSB: Reflective thinking2) Management accounting information is primarily oriented to external stakeholders, such as investors, creditors, regulators, and tax authorities.Answer: FALSEExplanation: Management accounting information is primarily oriented to management. Diff: 1Terms: management accountingObjective: 1AACSB: Reflective thinking3) The International Accounting Standards Board sets the guidelines used for management accounting.Answer: FALSEExplanation: Financial accounting must be consistent with the rules of the IASB.Diff: 1Terms: International Accounting Standards BoardObjective: 1AACSB: Reflective thinking4) A good management accounting system can become a source of competitive advantage for a company.Answer: TRUEDiff: 1Terms: management accountingObjective: 1AACSB: Reflective thinking5) Management accounting information is sometimes predictive and forward looking. Answer: TRUEDiff: 1Terms: management accountingObjective: 1AACSB: Reflective thinking6) Management accounting has no prescribed rules about its content, how the content is to be developed, and how the content is to be presented.Answer: TRUEDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking7) The Federal Accounting Standards Advisory Board sets cost accounting standards for all federal government activities.Answer: TRUEDiff: 2Terms: Government Accounting Standards BoardObjective: 1AACSB: Reflective thinking8) Management accounting measures can provide advance warnings of problems. Answer: TRUEDiff: 1Terms: management accountingObjective: 1AACSB: Reflective thinking9) Information about customer satisfaction is an example of financial information. Answer: FALSEExplanation: Information about customer satisfaction is an example of nonfinancial information.Diff: 1Terms: nonfinancial informationObjective: 1AACSB: Reflective thinking10) Management accounting information can be used for all of the following EXCEPT:A) calculate the cost of a product or service.B) evaluate the performance of a company.C) project materials needs.D) evaluate the market price of the stock.Answer: DDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking11) Which of the following types of information are used in management accounting?A) financial informationB) nonfinancial informationC) information focused on the long termD) All of the above are correct.Answer: DDiff: 1Terms: management accountingObjective: 1AACSB: Reflective thinking12) Management accounting:A) is both retrospective, providing feedback about past operations, and also prospective, incorporating forecasts and estimates about future events.B) is primarily oriented to external stakeholders.C) must be consistent with rules formulated by the Financial Accounting Standards Board (FASB).D) provides information that is generally available only on a quarterly or annual basis. Answer: ADiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking13) Which of the following descriptors refer to management accounting information?A) It is only retrospective, reporting and summarizing in financial terms the results of past decisions and transactions.B) It is driven by rules.C) It is prepared for shareholders.D) It is oriented to meeting the decision making needs of employees and managers inside the organization.Answer: DDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking14) Which of the following would be considered management accounting information?A) Budgeted production for the year 2011.B) Budgeted Balance Sheet.C) Analysis of trend in stock prices.D) Both budgeted production for the year of 2011, and the budgeted balance sheet. Answer: DDiff: 1Terms: management accountingObjective: 1AACSB: Reflective thinking15) Management accounting information includes all of the following EXCEPT:A) tabulated results of customer satisfaction surveys.B) the cost of producing a product.C) the percentage of units produced that is defective.D) market price of the stock.Answer: DDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking16) Management accounting reports might include information about:A) customer complaints.B) net income for the year on budgeted income statement.C) total assets on budgeted balance sheet.D) All of the above are correct.Answer: DDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking17) The person MOST likely to use management accounting information is a(n):A) banker evaluating a credit application.B) shareholder evaluating a stock investment.C) governmental taxing authority.D) assembly department supervisor.Answer: DDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking18) Which of the following is NOT a function of a management accounting system?A) strategic developmentB) financial reportingC) controlD) product costingAnswer: BDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking19) Financial accounting:A) focuses on the future and includes activities such as preparing next year's operating budget.B) does not need to comply with GAAP (generally accepted accounting principles).C) is primarily oriented to external stakeholders, such as investors, creditors, regulators and tax authorities.D) is prepared for the use of department heads and other employees.Answer: CDiff: 1Terms: financial accountingObjective: 1AACSB: Reflective thinking20) The person MOST likely to use ONLY financial accounting information is a:A) factory shift supervisor.B) vice president of operations.C) current shareholder.D) department manager.Answer: CDiff: 2Terms: financial accountingObjective: 1AACSB: Reflective thinking21) Historically, management accounting innovations have been developed by:A) the International Accounting Standards Board.B) the Cost Accounting Standards Board.C) Academic accountants.D) Managers.Answer: DDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking22) In general, it was not until the 1970s that management accounting systems:A) were improved because of demands by the FASB and the SEC.B) stagnated and proved inadequate.C) started to develop innovations in costing and performance-measurement systems due to intense pressure from overseas competitors.D) started to address the decision-making needs of managers.Answer: CDiff: 2Terms: management accountingObjective: 1AACSB: Reflective thinking23) Financial accounting information:A) provides a signal that something is wrong.B) identifies what is wrong.C) explains what is wrong.D) simply summarizes information but gives no indication that anything is wrong. Answer: ADiff: 2Terms: financial accountingObjective: 1AACSB: Reflective thinking24) The regulatory authority responsible for formulating rules of United States GAAP is:A) the Financial Accounting Standards Board.B) the Cost Accounting Standards Board.C) the Federal Accounting Standards Advisory Board.D) the International Accounting Standards Board.Answer: ADiff: 1Terms: financial accounting, FASBObjective: 1AACSB: Reflective thinking25) Management accounting information is BEST described as:A) providing a signal that something is wrong.B) identifying and helping to explain what is wrong.C) simply summarizing information, but giving no indication that anything is wrong.D) measuring overall organizational performance.Answer: BDiff: 1Terms: management accountingObjective: 1AACSB: Reflective thinking26) Compare and contrast the users and uses of management accounting and financial accounting.Answer: Management accounting provides information to internal decision makers of the business such as line supervisors, division managers and top executives. Its purpose is to help managers plan, organize, control and make operating decisions by predicting future results and evaluating performance.Financial accounting provides information to external decision makers such as investors and creditors. Its purpose is to present a fair picture of the financial condition of the company for use by these parties in making investing and credit decisions.Diff: 2Terms: management accounting, financial accountingObjective: 1AACSB: Reflective thinkingMAL: This question is not available in MyAccountingLab.27) What is the purpose of management accounting?Answer: Management accounting gathers short-term and long-term financial and nonfinancial information to plan, coordinate, motivate, improve, control, and evaluate success factors of an organization. Management accounting converts data into usable information that supports planning, organizing, and control decision making.Diff: 2Terms: management accountingObjective: 1AACSB: Reflective thinkingMAL: This question is not available in MyAccountingLab.Objective 21) During the history of management accounting, innovations were developed to address the decision-making needs of managers.Answer: TRUEDiff: 2Terms: management accountingObjective: 2AACSB: Reflective thinking2) A key element in any organization's strategy is to identify its target customers and to deliver what those target customers want.Answer: TRUEDiff: 1Terms: strategyObjective: 2AACSB: Reflective thinking3) Management accounting innovations are usually developed by academics.Answer: FALSEExplanation: Management accounting innovations are usually developed by management accountants in the field.Diff: 2Terms: management accountingObjective: 2AACSB: Reflective thinking4) The first modern industry to develop and use large quantities of financial statistics to assess and monitor organizational performance was:A) steel companies.B) lumber companies.C) the railroads.D) automobile companies.Answer: CDiff: 2Terms: financial informationObjective: 2AACSB: Reflective thinking5) Which of the following companies is a service company?A) Lands' EndB) Schwinn BicyclesC) Orkin Pest ControlD) British PetroleumAnswer: CDiff: 1Terms: service companiesObjective: 2AACSB: Reflective thinking6) Historically, service companies have:A) operated in less competitive environments than manufacturing companies.B) enjoyed global customer demand.C) used management accounting information in much the same way as manufacturing companies.D) competed by managing costs to provide the best service at the lowest price.Answer: ADiff: 2Terms: service companiesObjective: 2AACSB: Reflective thinking7) The Hawthorne study revealed that:A) individuals alter their behavior when they know they are being studied.B) groups alter their behavior when they know they are being studied.C) People react when they are being measured.D) All of the above are correct.Answer: DDiff: 2Terms: nonfinancial information, Hawthorne studyObjective: 2AACSB: Reflective thinking8) _______ helped develop the Plan-Do-Check-Act (PDCA) cycle.A) HawthorneB) Deming.C) CarnegieD) FordAnswer: DDiff: 2Terms: plan-do-check-act cycleObjective: 2AACSB: Reflective thinking9) Describe the steps in the PDCA cycle.Answer: The Plan step of the PCDA cycle defines the organization's purpose and selects the focus and scope of its strategy. The Do step of the PDCA cycle involves the implementation of a chosen course of action. In this setting, management accounting information gets communicated to front-line and support employees to inform their daily decisions and work activities. The check step in the PDCA cycle includes two components — measuring and monitoring ongoing performance and taking short-term actions based on the measured performance. In the Act step of the PDCA cycle, managers take actions to lower costs, change resource allocations, improve the quality, cycle time and flexibility of processes, modify the product mix, change customer relationships, and redesign and introduce new products.Diff: 3Terms: plan-do-check-act cycleObjective: 2AACSB: Reflective thinkingMAL: This question is not available in MyAccountingLab.10) What role has the increasingly competitive business environment played in the development of management accounting?Answer: The competitive environment has changed dramatically. There has been a deregulation movement in North America and Europe during the 1970s and 1980s that changed the ground rules under which service companies operate.In addition, organizations encountered severe competition from overseas companies that offered high-quality products at low prices. There has been an improvement of operational control systems such that information is more current and provided more frequently. Employees need better management accounting information and accurate and timely information to improve the activities they perform and to make decisions. Employees also want innovations in management accounting information. Nonfinancial information has become a critical feedback measure. Finally, the focus of many firms is now on measuring and managing activities.Diff: 3Terms: financial accounting, management accountingObjective: 2AACSB: Reflective thinkingMAL: This question is not available in MyAccountingLab.Objective 31) At the highest level strategic planning involves choosing a strategy that provides the best fit between the organization's environment and its internal resources in order to achieve the organization's objectives.Answer: TRUEDiff: 2Terms: strategyObjective: 3AACSB: Reflective thinking2) Quality is the degree of conformance between what the customer is promised and what the customer receives.Answer: TRUEDiff: 1Terms: qualityObjective: 3AACSB: Reflective thinking3) Government and nonprofit organizations, as well as profit-seeking enterprises, are feeling the pressures for improved performance.Answer: TRUEDiff: 1Terms: government and nonprofit organizationsObjective: 3AACSB: Reflective thinking4) Management accounting information allows managers to compare actual and planned costs and to identify areas and opportunities for process improvement.Answer: TRUEDiff: 1Terms: management accountingObjective: 3AACSB: Reflective thinking5) Management accounting can provide information on customer satisfaction.Answer: TRUEDiff: 2Terms: management accountingObjective: 3AACSB: Reflective thinking6) Planning activities include all of the following EXCEPT:A) estimate the cost and profit consequences from a course of action.B) evaluating the quality of the service provided.C) projecting labor requirements.D) budgeting.Answer: BDiff: 2Terms: plan-do-check-act cycleObjective: 3AACSB: Reflective thinking7) The most important factor in successful organizations is:A) weaknesses.B) competition.C) strategy.D) definition of quality.Answer: CDiff: 2Terms: strategyObjective: 3AACSB: Reflective thinking8) A key element of any organization's strategy is identifying:A) its potential shareholders.B) its target customers.C) competitor's products.D) employee needs.Answer: BDiff: 3Terms: strategyObjective: 3AACSB: Reflective thinking9) Explain the role of management accounting in helping an enterprise develop and implement its strategy.Answer: The organization needs management accounting information to help implement the strategy, allocate resources for the strategy, communicate the strategy, and link employees and operational processes to achieve the strategy. As the strategy gets executed, management accounting information provides feedback about where it is working and where it is not, and guides actions to improve the performance from the strategy..Diff: 2Terms: management accounting, strategyObjective: 3AACSB: Reflective thinkingMAL: This question is not available in MyAccountingLab.Objective 41) Quality expert, W. Edwards Deming, helped develop and disseminate the plan-do-check-act (PDCA) cycle.Answer: TRUEDiff: 2Terms: plan-do-act cycleObjective: 4AACSB: Reflective thinking2) Many organizations start the planning stage by re-affirming or updating its mission statement. Answer: TRUEDiff: 2Terms: plan-do-check-act cycleObjective: 4AACSB: Reflective thinking3) Operating profit is an example of nonfinancial information.Answer: FALSEExplanation: Operating profit is an example of financial information.Diff: 1Terms: financial informationObjective: 4AACSB: Reflective thinking4) The check step in the PDCA cycle includes two components — measuring and monitoring ongoing performance and taking short-term actions based on the measured performance. Answer: TRUEDiff: 2Terms: plan-do-check-act cycleObjective: 4AACSB: Reflective thinking5) Which of the following best represents the Plan step in the Plan-Do-Check-Act (PDCA) cycle?A) Take actions to lower costs, change resource allocations, improve the quality, cycle time and flexibility of processes, modify the product mix, change customer relationships, and redesign and introduce new products..B) Measure and monitor ongoing performance and take short-term actions based on the measured performance.C) Define the organization's purpose and select the focus and scope of its strategy. .D) Implement the chosen course of action.Answer: CDiff: 2Terms: plan-do-check-act cycleObjective: 4AACSB: Reflective thinking6) Which of the following best represents the Do step in the Plan-Do-Check-Act (PDCA) cycle?.A) Take actions to lower costs, change resource allocations, improve the quality, cycle time and flexibility of processes, modify the product mix, change customer relationships, and redesign and introduce new products.B) Measure and monitor ongoing performance and take short-term actions based on the measured performance.C) Define the organization's purpose and select the focus and scope of its strategy.D) Implement the chosen course of action.Answer: DDiff: 2Terms: plan-do-check-act cycleObjective: 4AACSB: Reflective thinking7) Which of the following best represents the Check step in the Plan-Do-Check-Act (PDCA) cycle?A) Take actions to lower costs, change resource allocations, improve the quality, cycle time and flexibility of processes, modify the product mix, change customer relationships, and redesign and introduce new products.B) Measure and monitor ongoing performance and take short-term actions based on the measured performance.C) Define the organization's purpose and select the focus and scope of its strategy.D) Implement the chosen course of action.Answer: CDiff: 2Terms: plan-do-check-act cycleObjective: 4AACSB: Reflective thinking8) Which of the following best represents the Act step in the Plan-Do-Check-Act (PDCA) cycle?A) Take actions to lower costs, change resource allocations, improve the quality, cycle time and flexibility of processes, modify the product mix, change customer relationships, and redesign and introduce new products.B) Measure and monitor ongoing performance and take short-term actions based on the measured performance.C) Define the organization's purpose and select the focus and scope of its strategy.D) Implement the chosen course of action.Answer: ADiff: 2Terms: plan-do-check-act cycleObjective: 4AACSB: Reflective thinking9) How the customer is treated at the time of the purchase is an example of the __________ element of the value proposition.A) functionality and featuresB) industry standardsC) qualityD) serviceAnswer: DDiff: 2Terms: nonfinancial informationObjective: 4AACSB: Reflective thinking10) Managers of service departments need all of the following information EXCEPT:A) efficiency data on work performance.B) quality data on work performance.C) profitability data of the whole company.D) profitability data of the service department.Answer: CDiff: 2Terms: financial information, nonfinancial informationObjective: 4AACSB: Reflective thinking11) A national company manufactures a line of modern furniture. Information MOST useful to the employee who assembles the furniture includes:A) a daily report comparing the actual time it took to assemble a piece of furniture to the standard time allowed.B) a monthly report on the proportion of furniture pieces assembled with defects.C) the number of furniture pieces sold this month.D) revenue per employee.Answer: ADiff: 2Terms: financial information, nonfinancial informationObjective: 4AACSB: Reflective thinking12) A national company manufactures a line of modern furniture. Information MOST useful to the top executive includes:A) individual job summaries of materials used.B) monthly financial reports on the company's profitability by product line.C) time reports submitted by each employee.D) scheduled downtime for routine maintenance on machines.Answer: BDiff: 2Terms: financial information, nonfinancial informationObjective: 4AACSB: Reflective thinking13) A quarterly report disclosing declining market share information is MOST useful to:A) a front-line employee.B) the manager of operations.C) the chief executive officer.D) the accounting department.Answer: CDiff: 2Terms: financial informationObjective: 4AACSB: Reflective thinking14) A weekly report comparing machine time used to available machine time is information LEAST useful to:A) a front-line employee.B) the manager of operations.C) the chief executive officer.D) the accounting department.Answer: CDiff: 1Terms: financial information, nonfinancial informationObjective: 4AACSB: Reflective thinking15) A daily report on the number of quality units assembled by each employee is information MOST useful to:A) a front-line assembly worker.B) the accounting department.C) the chief executive officer.D) the personnel department.Answer: ADiff: 2Terms: nonfinancial informationObjective: 4AACSB: Reflective thinking16) Which of the following would be MOST helpful for a top manager of a company?A) profitability report of the companyB) information to monitor hourly and daily operationsC) number of customer complaintsD) operating expense summary reported by departmentAnswer: ADiff: 2Terms: financial information, nonfinancial informationObjective: 4AACSB: Reflective thinking17) A law firm would use management accounting information for all of the following decisions EXCEPT:A) staffing needs.B) performance evaluation of staff.C) budgeted purchases of supplies.D) location of annual holiday party.Answer: DDiff: 2Terms: financial information, nonfinancial informationObjective: 4AACSB: Reflective thinking18) Management accounting can play a critical role in the service industry because of all the following reasons EXCEPT:A) firms must be especially sensitive to the timeliness and quality of customer service.B) many employees have very little contact with customers.C) customers immediately notice defects and a delay in service.D) dissatisfied customers may never return.Answer: BDiff: 2Terms: management accountingObjective: 4AACSB: Reflective thinkingThe following information pertains to three divisions of Marine Industrial Coatings, Inc. (amounts in millions):19) What is the return on investment for the Chemical Division?A) 1.25%B) 2.25%C) 25.0%D) 50.00%Answer: ADiff: 2Terms: return on investmentObjective: 4AACSB: Analytical skills20) Which division is more profitable based on ROI?A) ChemicalB) Retail paintC) IndustrialD) Both Chemical and Retail paint are more profitable than Industrial.Answer: CDiff: 3Terms: return on investmentObjective: 4AACSB: Analytical skills21) What is the Return on Sales for the Retail paint division?A) 2%B) 4.5%C) 20%D) 45%Answer: CDiff: 2Terms: return on salesObjective: 4AACSB: Analytical skills22) For improving operational efficiencies and customer satisfaction, nonfinancial information is:A) critical.B) moderate.C) infrequently used.D) unnecessary.Answer: ADiff: 2Terms: nonfinancial informationObjective: 4AACSB: Reflective thinking23) Nonfinancial information might be used for all of the following EXCEPT:A) improve product quality.B) reduce cycle times.C) satisfy customers' needs.D) All of the above are used.Answer: DDiff: 2Terms: nonfinancial informationObjective: 4AACSB: Reflective thinking24) Is financial accounting or management accounting more useful to an operations manager? Why?Answer: Management accounting is more useful to an operations manager because management accounting reports operating results by department or unit rather than for the company as a whole, it includes financial as well as nonfinancial data such as the number or percent of on-time deliveries and cycle times, and it includes quantitative as well as qualitative data such as the type of rework that was needed on defective units. It also provides information to control operations; it measures and evaluates existing systems to identify problems.Diff: 3Terms: financial accounting, management accountingObjective: 4AACSB: Reflective thinkingMAL: This question is not available in MyAccountingLab.25) Give two examples of financial information and nonfinancial information.Answer: Financial information includes amounts that can be expressed in dollar amounts such as sales, net income, and total assets. It also includes ratios prepared using financial information such as the percentage increase in sales, return-on-sales, and return-on-investment. Nonfinancial information includes measures that are not expressed in dollar amounts. For example, nonfinancial measures of customer satisfaction include the number of repeat customers or ranked estimates of satisfaction levels. Nonfinancial measures of production quality include percent of on-time deliveries, the number of defects, and production yield.Diff: 3Terms: financial information, nonfinancial informationObjective: 4AACSB: Reflective thinkingMAL: This question is not available in MyAccountingLab.Objective 51) The design and introduction of new measurements and systems must be accompanied by an analysis of the behavioral and organizational reactions to the measurements.Answer: TRUEDiff: 2Terms: nonfinancial informationObjective: 5AACSB: Reflective thinking2) People react when they are being measured, and they react to the measurements..Answer: TRUEDiff: 2Terms: measurementsObjective: 5AACSB: Reflective thinking3) Information is never neutral; just the act of measuring and reporting information affects the individuals involved.Answer: TRUEDiff: 2Terms: financial information, nonfinancial informationObjective: 5AACSB: Reflective thinking。

管理会计(双语)课后答案answer-chapter 23

CHAPTER 23PERFORMANCE MEASUREMENT, COMPENSATION, ANDMULTINATIONAL CONSIDERATIONS1.An example of a performance measure based on external financial information would bea.market share.b.stock prices.c.innovation measures.d.defect rates.2.Which of the following does not describe the three steps in designing anaccounting-based performance measure?a.The issues in each step are interdependent.b.The decision maker will often proceed through the steps several times beforedeciding on one or more performance measure(s).c.The answers to the questions raised at each step depend on top management’sbeliefs about the organization.d.The steps must be done in sequence.The following data apply to questions 3 through 7.Information pertaining to Piney River Division of MO Corporation for 2004:Revenues $950,000Variable costs 575,000Traceable fixed costs 336,500Average invested capital 350,000Imputed interest rate 10%3.The return on investment (ROI) wasa. 4 percent.b. 10 percent.c. 11 percent.d. 37 percent.4.The return on sales (ROS), a component of the DuPont method of profitability analysis,was (rounded to the nearest percent)a. 11 percent.b. 40 percent.c. 1 percent.d.4 percent.5.The residual income wasa. $3,500.b. $35,000.c. $38,500.d. $0.6.If top management at MO Corporation adopts a 15 percent target ROI for the Piney RiverDivision, which combination (while holding other factors constant) will yield this targetROI?a. A 1 percent increase in sales volumeb. A 5 percent decrease in average invested assetsc. A 2 percent increase in sales pricesd. A 3 percent decrease in fixed costs7.Which of the following factors would not be needed to calculate EVA from the giveninformation for Piney River Division of MO Corporation?a.Income tax rateb.Weighted-average cost of capitalc.Current liabilitiesd.Current assets8.When managers set and measure target levels of performancea.historical-cost-based accounting measures are usually adequate for evaluatingeconomic returns on new investments.b.historical-cost ROIs cannot be used to evaluate current performance.c.the timing of feedback is not dependent on the sophistication of theorganization’s information technology.d.the timing of feedback depends on the specific level of management receiving thefeedback.9.James Jessmore is a manager at a local bank. James’s management style is best describedas entrepreneurial—he is risk neutral. Wynetta George is a customer servicerepresentative who reports to James. Wynetta is risk averse. In designing a compensationpackage for James and Wynetta, which type of compensation arrangement should beemphasized more?James Jessmore Wynetta Georgea. Performance-based Performance-basedb. Performance-based Straight salaryc. Straight salary Performance-basedd. Straight salary Straight salary10.Moral hazard is best described in contexts in whicha.division managers cite enormous top management pressures “to make the budget”as excuses for not adhering to ethical accounting policies and procedures.b.the numbers that subunit managers report should be uncontaminated by “cookingthe books.”c.an employee prefers to exert less effort than desired by the owner because theeffort cannot be accurately monitored and enforced.d.socially responsible companies set aggressive environmental goals and measureand report their performance against them.SOLUTIONS1. b2. d3. c4. d5. a6. c7. d8. d9. b10. cQuestion Calculations3. Revenues $950,000Variable costs (575,000)Traceable fixed costs (336,500)Operating income $ 38,50038,500/350,000 = 11%4. 38,500/950,000 = 4.1% or rounded to 4%5. Operating income $38.500350,000 ⨯ 10% 35,000Residual income 3,5006. a. 950,000 ⨯ 101% $959,500575,000 ⨯ 101% (580,750)(336,500)Operating income 42,50042,500/350,000 = 12.1%b. 350,000 ⨯ .95 = 332,500 38,500/332,500 = 11.6%c. 950,000 ⨯ 102% $969,000(575,000)(336,500)Operating income $ 57,50057,500/350,000 = 16.4%d. $950,000(575,000) 336,500 .97 = (326,405)Operating Income 48,59548,595/350,000 = 13.9%。

《管理会计(双语)》课程 (5)

Time-Driven ABC

Use parameter estimates to assign indirect costs: Cost of using resource i by product j =

Capacity cost rate of resource i x Quantity of capacity of resource i used

Time-driven activity-based costing systems (TDABC or Time-Driven ABC) estimate two parameters and then assign indirect costs similar to the way direct costs are assigned

by product j

8

TDABC Profitability Report