国际投资学教程课后题答案 完整版

国际投资(杜奇华)课后思考题答案(精整版)

国际投资(杜奇华)课后思考题答案(精整版)国际投资课后思考题第⼀章:国际投资导论⼀、国际投资的特征有哪些?1、国际投资的领域呈现不完全竞争性2、国际投资的⽬的呈现多样性3、国际投资的主体呈现双重性4、国际投资所使⽤的货币呈现多元化5、国际投资的环境呈现差异性6、国际投资的运⾏呈现曲折性7、国际投资的过程呈现更⼤的风险性⼆、国际投资的主体和客体包括哪些?(⼀)、国际投资的主体●跨国公司●国际⾦融机构●官⽅与半官⽅机构●个⼈投资者(⼆)、国际投资的客体1.货币性资产(Monetary Assets)●现⾦●银⾏存款●应收账款●国际债券●国际股票2.实物资产(Real Assets)●⼟地●建筑物●机器设备●零部件和原材料3.⽆形资产(Intangible Assets)●⽣产诀窍●管理技术●商标●商誉●技术专利三、国际投资历经了哪⼏个发展时期?1、起步阶段(18世纪末~1914年)●英、法、德、美、荷从事国际投资●国际投资主要流向⾃然资源丰富的地区2、低迷徘徊阶段(1914年~1945年)●国际投资的总额下降●国际投资⽅式仍然以国际间接投资为主3、恢复增长阶段(1946年~1979年)●国际投资的规模迅速扩⼤●国际投资的⽅式转变为国际直接投资为主4、逐渐发展阶段(20世纪80年代)●国际直接投资的规模迅速扩⼤●国际投资的流动转向以发达国家为主。

5、⾼速增长阶段(20世纪90年代)●国际直接投资总额⼤幅上升●国际直接投资产业分布的转化●国际投资主体向多元化发展●新兴的发展中国家成为国际投资的热点五、国际投资学的研究⽅法有哪些?●总量分析与个量分析相结合●静态分析与动态分析相结合●定性分析与定量分析相结合●历史分析与逻辑分析相结合●抽象分析与实证分析相结合●理论总结与实践操作相结合六、国际投资的最新发展趋势有哪些?●全球外国直接投资增速下降●⼤型跨国公司主宰全球经济●外国直接投资流量继续集中在欧、⽇、美●政府加速开放外国直接投资政策●签订了更多的双边协定和投资协议●中国将成为全球最具活⼒的外商投资地区第⼆章国际直接投资理论⼆、垄断优势理论与内部化理论的主要区别是什么?⾸先,垄断优势理论是以市场不完全作为跨国经营的前提内部化理论的⽬的是消除市场的不完全性;其次,垄断优势理论中由于市场不完全导致垄断排斥竞争内部化理论中由于市场不完全导致市场失灵再次,垄断优势理论注重技术垄断优势,是跨国经营的重要意义内部化理论中交易成本最⼩,注重保证跨国经营的优势最后,垄断优势理论适⽤于发达国家内部化理论既适⽤于发达国家,也适⽤于发展中国家,即可适⽤于国内,也可适⽤于国外。

国际投资学教程课后题答案(完整版) (2)(word文档良心出品)

第一章1.名词解释:国际投资:是指以资本增值和生产力提高为目标的国际资本流动,是投资者将其资本投入国外进行的一阴历为目的的经济活动。

国际公共(官方)投资: 是指一国政府或国际经济组织为了社会公共利益而进行的投资,一般带有国际援助的性质。

国际私人投资:是指私人或私人企业以营利为目的而进行的投资。

短期投资:按国际收支统计分类,一年以内的债权被称为短期投资。

长期投资:一年以上的债权、股票以及实物资产被称为长期投资。

产业安全:可以分为宏观和中观两个层次。

宏观层次的产业安全,是指一国制度安排能够导致较合理的市场结构及市场行为,经济保持活力,在开放竞争中本国重要产业具有竞争力,多数产业能够沈村冰持续发展。

中观层次上的产业安全,是指本国国民所控制的企业达到生存规模,具有持续发展的能力及较大的产业影响力,在开放竞争中具有一定优势。

资本形成规模:是指一个经济落后的国家或地区如何筹集足够的、实现经济起飞和现代化的初始资本。

2、简述20世纪70年代以来国际投资的发展出现了哪些新特点?(一)投资规模,国际投资这这一阶段蓬勃发展,成为世纪经济舞台最为活跃的角色。

国际直接投资成为了国际经济联系中更主要的载体。

(二)投资格局,1.“大三角”国家对外投资集聚化 2.发达国家之间的相互投资不断增加 3.发展中国家在吸引外资的同时,也走上了对外投资的舞台(三)投资方式,国际投资的发展出现了直接投资与间接投资齐头并进的发展局面。

(四)投资行业,第二次世界大战后,国际直接投资的行业重点进一步转向第二产业。

3.如何看待麦克杜格尔模型的基本理念?麦克杜格尔模型是麦克杜格尔在1960年提出来,后经肯普发展,用于分析国际资本流动的一般理论模型,其分析的是国际资本流动对资本输出国、资本输入国及整个世界生产和国民收入分配的影响。

麦克杜格尔和肯普认为,国际间不存在限制资本流动的因素,资本可以自由地从资本要素丰富的国家流向资本要素短缺的国家。

资本流动的原因在于前者的资本价格低于后者。

国际投资第二章课后习题答案

Chapter 2Foreign Exchange Parity Relations1. Because the interest rate in A is greater than the interest rate in B, α is expected to depreciate relativeto β, and should trade with a forward discount. Accordingly, the correct answer is (c).2. Because the exchange rate is given in €:$ terms, the appropriate expression for the interest rate parity relation is€+=+$11r F S r (r $ is a part of the numerator and r € is a part of the denominator).a. The one-year €:$ forward rate is given by €:==1.05$ 1.1795 1.19081.04b. The one-month €:$ forward rate is given by€:+==+1(0.04/12$ 1.1795 1.18051(0.03/12)Of course, these are central rates, and bid-ask rates could also be determined on the basis of bid-askrates for the spot exchange and interest rates.3. a. bid €:¥ = (bid $:¥) × (bid €:$) = 108.10 × 1.1865 = 128.2607.ask €:¥ = (ask $:¥) × (ask €:$) = 108.20 × 1.1870 = 128.4334.b. Because the exchange rate is in €:$ terms, the appropriate expression for the interest rate parityrelation is F /S = (1 + r $)/(1 + r €).€€€++==++=$1(ask )1(0.0525/4):$3-month ask (spot ask :$)1.18701(bid )1(0.0325/4)1.1929r rThus, the €:$3-month forward ask exchange rate is: 1.1929.c. bid $:€ = 1/ask €:$ = 1 / 1.1929 = 0.8383.Thus, the 3-month forward bid exchange rate is $:€ = 0.8383.Chapter 2 Foreign Exchange Parity Relations 7d. Because the exchange rate is in $:¥ terms, the appropriate expression for the interest rate parityrelation is F /S = (1 + r ¥ )/1 + r $.$++===+¥1(bid )1(0.0125/4)$:¥3-month bid (spot ask $:¥)108.10107.031(ask )(0.0325/4)r r $++===+¥1(ask )1(0.0150/4)$:¥3-month ask (spot ask $:¥)108.20107.261(bid )(0.0500/4)r rThus, the $:¥ 3-month forward exchange rate is: 107.03 – 107.26. Note : The interest rates one uses in all such computations are those that result in a lower forwardbid (so, bid interest rates in the numerator and ask rates in the denominator) and a higher forward ask (so, ask interest rates in the numerator and bid rates in the denominator).4. a. For six months, r SFr = 1.50% and r $ = 1.75%. Because the exchange rate is in $:SFr terms, the appropriate expression for the interest rate parity relation isSFr $SFr $1,or (1)(1)1r F F r r S r S+=+=++ The left side of this expression is$ 1.6558(1)(10.0175) 1.01331.6627F r S+=+= The right side of the expression is: 1 + r SFr = 1.0150. Because the left and right sides are not equal, IRP is not holding.b. Because IRP is not holding, there is an arbitrage possibility: Because 1.0133 < 1.0150, we cansay that the SFr interest rate quote is more than what it should be as per the quotes for the otherthree variables. Equivalently, we can also say that the $ interest rate quote is less than what itshould be as per the quotes for the other three variables. Therefore, the arbitrage strategy shouldbe based on borrowing in the $ market and lending in the SFr market. The steps would be asfollows:• Borrow $1,000,000 for six months at 3.5% per year. Need to pay back $1,000,000 ×(1 + 0.0175) = $1,017,500 six months later.• Convert $1,000,000 to SFr at the spot rate to get SFr 1,662,700.• Lend SFr 1,662,700 for six months at 3% per year. Will get back SFr 1,662,700 ×(1 + 0.0150) = SFr 1,687,641 six months later.• Sell SFr 1,687,641 six months forward. The transaction will be contracted as of the current date but delivery and settlement will only take place six months later. So, six months later,exchange SFr 1,687,641 for SFr 1,687,641/SFr 1.6558/$ = $1,019,230.The arbitrage profit six months later is 1,019,230 – 1,017,500 = $1,730.5. a. For three months, r $ = 1.30% and r ¥ = 0.30%. Because the exchange rate is in $:¥ terms, the appropriate expression for the interest rate parity relation is¥$¥$1,or (1)(1)1r F F r r S r S+=+=++8 Solnik/McLeavey • Global Investments, Sixth EditionThe left side of this expression is$107.30(1)(10.0130) 1.0064.108.00F r S+=+= The right side of this expression is: 1 + r ¥ = 1.0030. Because the left and right sides are not equal, IRP is not holding.b. Because IRP is not holding, there is an arbitrage possibility. Because 1.0064 > 1.0030, we cansay that the $ interest rate quote is more than what it should be as per the quotes for the otherthree variables. Equivalently, we can also say that the ¥ interest rate quote is less than what itshould be as per the quotes for the other three variables. Therefore, the arbitrage strategy shouldbe based on lending in the $ market and borrowing in the ¥ market. The steps would be asfollows:• Borrow the yen equivalent of $1,000,000. Because the spot rate is ¥108 per $, borrow$1,000,000 × ¥108/$ = ¥108,000,000. Need to pay back ¥108,000,000 × (1 + 0.0030) =¥108,324,000 three months later.• Exchange ¥108,000,000 for $1,000,000 at the spot exchange rate.• Lend $1,000,000 for three months at 5.20% per year. Will get back $1,000,000 ×(1 + 0.0130) = $1,013,000 three months later.• Buy ¥108,324,000 three months forward. The transaction will be contracted as of the current date, but delivery and settlement will only take place three months later. So, three monthslater, get ¥108,324,000 for ¥108,324,000 / (¥107.30 per $) = $1,009,543.The arbitrage profit three months later is 1,013,000 – 1,009,543 = $3,457.6. At the given exchange rate of 5 pesos/$, the cost in Mexico in dollar terms is $16 for shoes, $36 forwatches, and $120 for electric motors. Thus, compared with the United States, shoes and watches are cheaper in Mexico, and electric motors are more expensive in Mexico. Therefore, Mexico will import electric motors from the United States, and the United States will import shoes and watches from Mexico. Accordingly, the correct answer is (d).7. Consider two countries, A and B. Based on relative PPP,+=+1011A BS I S I where S 1 and S 0 are the expected and the current exchange rates between the currencies of A and B, and I A and I B are the inflation rates in A and B. If A and B belong to the group of countries thatintroduces the same currency, then one could think of both S 1 and S 0 being one. Then, I A and I B should both be equal for relative PPP to hold. Thus, introduction of a common currency by a group ofcountries would result in the convergence of the inflation rates among these countries. A similarargument could be applied to inflation among the various states of the United States.8. Based on relative PPP,+=+Switzerland 10US11I S S IChapter 2 Foreign Exchange Parity Relations 9where S 1 is the expected $:SFr exchange rate one year from now, S 0 is the current $:SFr exchange rate, and I Switzerland and I US are the expected annual inflation rates in Switzerland and the United States, respectively. So,1110.02and 1.60(1.02/1.05)SFr 1.55/$.1.6010.05S S +===+ 9. a. A Japanese consumption basket consists of two-thirds sake and one-third TV sets. The price ofsake in yen is rising at a rate of 10% per year. The price of TV sets is constant. The Japanese consumer price index inflation is therefore equal to+=21(10%)(0%) 6.67%33b. Relative PPP states thatFC 10DC1.1I S S I +=+ Because the exchange rate is given to be constant, we have S 0 = S 1, which implies S 1/S 0 = 1. As a result, in our example, PPP would hold if 1 + I FC = 1 + I DC (i.e., I FC = I DC ). Because the Japanese inflation rate is 6.67% and the American inflation rate is 0%, we do not have I FC = I DC , and PPP does not hold.10. a. i. The law of one price is that, assuming competitive markets and no transportation costs ortariffs, the same goods should have the same real prices in all countries after convertingprices to a common currency.ii. Absolute PPP, focusing on baskets of goods and services, states that the same basket ofgoods should have the same price in all countries after conversion to a common currency.Under absolute PPP, the equilibrium exchange rate between two currencies would be the ratethat equalizes the prices of a basket of goods between the two countries. This rate wouldcorrespond to the ratio of average price levels in the countries. Absolute PPP assumes noimpediments to trade and identical price indexes that do not create measurement problems.iii. Relative PPP holds that exchange rate movements reflect differences in price changes(inflation rates) between countries. A country with a relatively high inflation rate willexperience a proportionate depreciation of its currency’s value vis-à-vis that of a countrywith a lower rate of inflation. Movements in currencies provide a means for maintainingequivalent purchasing power levels among currencies in the presence of differing inflationrates.Relative PPP assumes that prices adjust quickly and price indexes properly measure inflationrates. Because relative PPP focuses on changes and not absolute levels, relative PPP is morelikely to be satisfied than the law of one price or absolute PPP.b. i. Relative PPP is not consistently useful in the short run because of the following:(1) Relationships between month-to-month movements in market exchange rates and PPPare not consistently strong, according to empirical research. Deviations between the ratescan persist for extended periods. (2) Exchange rates fluctuate minute by minute becausethey are set in the financial markets. Price levels, in contrast, are sticky and adjust slowly.(3) Many other factors can influence exchange rate movements rather than just inflation.ii. Research suggests that over the long term, a tendency exists for market and PPP rates tomove together, with market rates eventually moving toward levels implied by PPP.10 Solnik/McLeavey • Global Investments, Sixth Edition11. a. If the treasurer is worried that the franc might appreciate in the next three months, she couldhedge her foreign exchange exposure by trading this risk against the premium included in theforward exchange rate. She could buy 10 million Swiss francs on the three-month forward market at the rate of SFr 1.5320 per €. The transaction will be contracted as of the current date, butdelivery and settlement will only take place three months later.b. Three months later, the company received the 10 million Swiss francs at the forward rate ofSFr 1.5320 per € agreed on earlier. Thus, the company needed (SFr 10,000,000)/(SFr 1.5320per €), or €6,527,415. If the company had not entered into a forward contract, the companywould have received the 10 million Swiss francs at the spot rate of SFr 1.5101 per €. Thus, thecompany would have needed (SFr 10,000,000) / (SFr 1.5101 per €), or €6,622,078. Therefore,the company benefited by the treasurer’s action, because €6,622,078 – €6,527,415 = €94,663were saved.12. The nominal interest rate is approximately the sum of the real interest rate and the expected inflationrate over the term of the interest rate. Even if the international Fisher relation holds, and the realinterest rates are equal among countries, the expected inflation can be very different from one country to another. Therefore, there is no reason why nominal interest rates should be equal among countries.13. Because the Australian dollar is expected to depreciate relative to the dollar, we know from thecombination of international Fisher relation and relative PPP that the nominal interest rate inAustralia is greater than the nominal interest rate in the United States. Further, the nominal interest rate in the United States is greater than that in Switzerland. Thus, the nominal interest rate inAustralia has to be greater than the nominal interest rate in Switzerland. Therefore, we can say from the combination of international Fisher relation and relative PPP that the Australian dollar is expected to depreciate relative to the Swiss franc.14. According to the approximate version of the international Fisher relation, r Sweden − r US = I Sweden − I US . So, 8 − 7 = 6 − I US , which means that I US = 5%.According to the approximate version of relative PPP,−=−10Sweden US 0S S I I S where, S 1 and S 0 are in $:SKr terms. I Sweden − I U S = 6 − 5 = 1%, or 0.01. So, (6 − S 0)/S 0 = 0.01. Solving for S 0, we get S 0 = SKr 5.94 per $.According to the approximate version of IRP,−=−0Sweden US 0F S r r S where, F and S 0 are in $:SKr terms. r Sweden − r US = 8 − 7 = 1%, or 0.01. So, (F − 5.94)/5.94 = 0.01. Solving for F , we get F = SKr 6 per $.Because we are given the expected exchange rate, we could also have arrived at this answer by usingthe foreign exchange expectations relation.Chapter 2 Foreign Exchange Parity Relations 1115. According to the international Fisher relation,++=++Switzerland Switzerland UK UK1111r I r I So,++=++Switzerland 110.0410.1210.10r therefore, r Switzerland = 0.0589, or 5.89%.According to relative PPP,+=+Switzerland 10UK11I S S I where, S 1 and S 0 are in £:SFr terms.So,110.04.310.10S +=+ Solving for S 1 we get S 1 = SFr 2.8364 per £.According to IRP,+=+Switzerland 0UK11r F S r where, F and S 0 are in £:SFr terms.So,10.0589.310.12F +=+ Solving for F , we get F = SFr 2.8363 per £. This is the same as the expected exchange rate in oneyear, with the slight difference due to rounding.16. During the 1991–1996 period, the cumulative inflation rates were about 25 percent in Malaysia,61 percent in the Philippines, and 18 percent in the United States. Over this period, based on relative PPP, one would have expected the Malaysian ringgit to depreciate by about 7 percent relative to the United States dollar (the inflation differential). In reality, the Malaysian ringgit appreciated by about 8 percent. Similarly, in view of the very high inflation differential between the Philippines and the United States, one would have expected the Philippine peso to depreciate considerably relative to the dollar. But it did not. Thus, according to PPP, both currencies had become strongly overvalued.12 Solnik/McLeavey • Global Investments, Sixth Edition17. a. According to PPP, the current exchange rate should bePif Pif 1010$$10//PI PI S S PI PI == where subscript 1 refers to the value now, subscript 0 refers to the value 20 years ago, PI refers toprice index, and S is the $:pif exchange rate. Thus, the current exchange rate based on PPP should be1200/1002pif 1 per $.400/100S ⎛⎞==⎜⎟⎝⎠b. As per PPP, the pif is overvalued at the prevailing exchange rate of pif 0.9 per $.18. Exports equal 10 million pifs and imports equal $7 million (6.3 million pifs). Accordingly, the tradebalance is 10 − 6.3 = 3.7 million pifs.• Balance of services includes the $0.5 million spent by tourists (0.45 million pifs).• Net income includes $0.1 million or 0.09 million pifs received by Paf investors as dividends,minus 1 million pifs paid out by Paf as interest on Paf bonds (− 0.91 million pifs).• Unrequited transfers include $0.3 million (0.27 million pifs) received by Paf as foreign aid.• Portfolio investment includes the $3 million or 2.7 million pifs spent by Paf investors to buyforeign firms. So, portfolio investment = −2.7 million pifs.Based on the preceding,• Current account = 3.24 (= 3.70 + 0.45 − 0.91)• Capital account = 0.27• Financial account = −2.7The sum of current account, capital account, and financial account is 0.81. By definition of balance ofpayments, the sum of the current account, the capital account, the financial account, and the change in official reserves must be equal to zero. Therefore, official reserve account = −0.81.The following summarizes the effect of the transactions on the balance of payments.Current account 3.24Trade balance 3.70Balance of services 0.45Net income – 0.91Capital account 0.27Unrequited transfers 0.27Financial account – 2.70Portfolio investment – 2.70Official reserve account – 0.8119. a. A traditional flow market approach would suggest that the home currency should depreciatebecause of increased inflation. An increase in domestic consumption could also lead to increased imports and a deficit in the balance of trade. This deficit should lead to a weakening of the homecurrency in the short run.b. The asset market approach claims that this scenario is good for the home currency. Foreigncapital investment is attracted by the high returns caused by economic growth and high interestrates. This capital inflow leads to an appreciation of the home currency.Chapter 2 Foreign Exchange Parity Relations 13 20. a. i. The immediate effect of reducing the budget deficit is to reduce the demand for loanablefunds because the government needs to borrow less to bridge the gap between spending andtaxes.ii. The reduced public-sector demand for loanable funds has the direct effect of lowering nominal interest rates, because lower demand leads to lower cost of borrowing, iii. The direct effect of the budget deficit reduction is a depreciation of the domestic currency and the exchange rate. As investors sell lower yielding Country M securities to buy thesecurities of other countries, Country M’s currency will come under pressure andCountry M’s currency will depreciate.b. i. In the case of a credible, sustainable, and large reduction in the budget deficit, reducedinflationary expectations are likely because the central bank is less likely to monetize thedebt by increasing the money supply. Purchasing power parity and international Fisherrelationships suggest that a currency should strengthen against other currencies whenexpected inflation declines.ii. A reduction in government spending would tend to shift resources into private-sector investments, in which productivity is higher. The effect would be to increase the expectedreturn on domestic securities.。

国际投资学第三章国际投资环境课后习题答案(个人总结)

国际投资学第三章国际投资环境课后习题答案(个人总结)第一篇:国际投资学第三章国际投资环境课后习题答案(个人总结) 第三章国际投资环境1.名词解释国际投资环境:影响国际投资的各种自然因素、经济因素、政治因素、社会因素和法律因素相互依赖、相互完善、相互制约所形成的的矛盾统一体。

硬环境:能影响投资的外部物质条件。

软环境:能影响国际直接投资的各种非物质形态的因素。

冷热比较分析法:从政治稳定性、市场机会、经济发展与成就、文化一元化等“热”因素和法令障碍、实质障碍、地理与文化差异等冷因素共7各方面对各国投资环境进行综合比较分析。

2.简述国际直接投资环境的重要性及其决定因素重要性:国际直接投资环境的优劣直接决定了一国对外资吸引力的大小。

决定因素:经济环境是最直接、最基本的因素。

3.试总结各种国际投资环境评估方法的基本思路和共性基本思路和共性是将总投资环境分解为若干具体指标,然后再综合评判。

4.案例分析分别运用等级尺度法和要素评价分类法对英国的投资环境进行计分和评价等级尺度法:1.货币稳定性(4-20分)2.近五年通货膨胀率(2-14分)3.资本外调(0-12分)4.外商股权(0-12分)5.外国企业与本地企业之间的差别待遇和控制(0-12分)6.政治稳定性(0-12分)7.当地资本供应能力(0-10分)8.给予关税保护的态度(2-8分)要素评价法:I=AE/CF(B+D+G+H)+x 投资环境激励系数(A)城市规划完善度因子(B)利税因子(C)劳动生产率因子(D)地区基础因子(E)效率因子(F)市场因子(G)管理权因子(H)5.试结合本章专栏3-1和专栏3-3,分析我国改善投资环境的重点和具体措施。

改善投资环境的重点是改善软环境和社会因素中的价值观念、教育水平、社会心理与习惯。

具体措施是降低贸易壁垒、提高私有财产保护程度、降低企业运行障碍、提高政府清廉程度、提高经济自由程度和提高法律完善程度。

本章小结国际投资环境是指影响国际投资的各种因素相互依赖、相互完善、相互制约所形成的矛盾统一体,国际直接投资环境的优劣直接决定了一国对外资吸引力的大小。

国际投资第三章课后习题答案

Chapter 3Foreign Exchange Determination andForecasting1. Applying expansionary macroeconomic policy, which results in higher goods prices and lower realinterest rates, will not reduce the balance of payments deficit. Higher prices will make the country’s goods less competitive internationally, and lower interest rates will discourage foreign capital. Thus, the balance of payments deficit will worsen instead of improve. On the other hand, (a), (b), and (d) will help in remedying the balance of payments deficit. Accordingly, the answer is (c).2. a. One advantage of a wider band is “emotional.” France could claim that it did not devalue itscurrency. Another advantage is flexibility. If there were no long-term fundamental reasons(inflation, balance of payments deficit, etc.) for a devaluation, the temporary pressure on thefranc could ease and the franc could later revert to its previous level. The disadvantage of a wider band is exchange rate uncertainty for all firms. A “credible” small band is preferable for firmsconducting international trade,b. A wider band makes speculation less attractive, because there is no guarantee that a central bankwill defend its currency until the wide fluctuation margin is reached.3. a. The American investor has paid a 25 percent premium over the price paid by a domestic investor.Yet, he receives the same dividends as the domestic investor. Therefore, his investment bears asmaller yield than it would for a domestic investor.b. Lifting of the exchange controls would be bad news to an existing foreign investor in Paf, sinceher asset could only be repatriated at the normal pif rate (1.00), while she had bought it at thefinancial rate (1.25).c. Lifting of the exchange controls would be good news to foreign investors planning to invest inPaf in the future, because they would no longer have to pay the 25 percent premium when buying assets in Paf.4. Remember that the Eurozone is made up of those countries in the EU that have adopted the euro ascommon currency. Statements I and III are clearly correct. Statement II is clearly not correct, because there is a possibility that more countries may join the Eurozone in future. For example, the British are debating whether to join the Eurozone.5. The statement is true. Because of riskless arbitrage, interest rate parity between two currencies wouldhold if the markets for both are free and deregulated. Developed financial markets tend to be more free and deregulated. A developing country is more likely to impose various forms of capital controls and taxes that impede arbitrage. A developing country is economically not as well integrated with the world financial markets as the developed markets are. Also, some smaller currencies can only be borrowed and lent domestically, and the domestic money markets of developing countries are more likely to be subjected to political risk.Chapter 3 Foreign Exchange Determination and Forecasting 156. a. Using the first-order approximation of PPP relationship, the variation in rupee to dollar exchangerate should equal the inflation differential between rupee and dollar. So, the rupee to dollarexchange rate should increase by 6 − 2.5 = 3.5%. That is, the rupee should depreciate by 3.5%relative to the dollar.b. The nominal dollar return for the U.S. institutional investor is approximately 12 − 5 = 7%. Thereal return for the U.S. investor is approximately 7 − 2.5 = 4.5%. The real return for the Indianinvestor is approximately 12 − 6 = 6%. Thus, the U.S. investor has a lower real return than theIndian investor. This is so because the rupee depreciated with respect to the dollar by more thanwhat the PPP relationship would indicate. Indeed, the difference between the real returns is6 − 4.5 = 1.5%, which is the same as the difference between the actual depreciation of the rupeeand the depreciation that should have occurred as per PPP (5 − 3.5 = 1.5%).7. If a country’s currency is undervalued, it means that the real prices of assets in this country are lowcompared with other countries. Also, the wages are lower in real terms than in other countries. Thus, investors from other countries would invest in this country to take advantage of low prices andwages. This action would help in the appreciation of the undervalued currency and restoration of the PPP in the long run. In terms of foreign trade, an undervalued currency implies that exports from this country would get a boost while imports would become less attractive. This would also help in the appreciation of the undervalued currency and restoration of the PPP in the long run.8. In risk-neutral efficient foreign exchange markets, the forward rate is the expected value of the futurespot rate. The forward rate can be computed using the interest rate parity relation. Because the exchange rate is given in $:SFr terms, the appropriate expression for the interest rate parity relation isSFr $11r F Sr +=+ (that is, r SFr is a part of the numerator and r $ is a part of the denominator). Accordingly, the three-month forward rate is10.00951.4723 1.460010.0180F +==+ thus, the implied market prediction for the three-month ahead exchange rate is SFr1.4600 per $.9. As per the model, one € would be worth $0.9781 six months later. Based on the forward rate, one €would be worth $0.9976 six months later. Therefore, the market participants, who believe that the model is quite good, would buy the dollar in the forward market (sell euros). Consequently, the price of the euro forward would decrease (the dollar forward would increase) and the forward rate would become equal to $0.9781 per €. The spot exchange rate and the dollar and euro interest rates would change so as to be consistent with this forward rate. A look at the interest rate parity relationship— written in the form€$11r F S r+=+ as F and S are in €:$ terms—suggests that with the decrease in forward rate from $0.9976 per € to$0.9781 per €, the spot rate and interest rate in dollars are likely to go down and interest rate in euros is likely to go up.16 Solnik/McLeavey • Global Investments, Sixth Edition10. a. The forward rate can be computed using the interest rate parity relation. Because the exchange rate is given in £:$ terms, the appropriate expression for the interest rate parity relation is$£11r F S r +=+ (that is, r $ is a part of the numerator, and r £ is a part of the denominator). Accordingly, the one-year forward rate is1.02001.5620$1.5283 per £1.0425F .== b. Based on the forward rate, one pound would be worth $1.5283 one year later. The model predictsthat one pound would be worth $1.5315 one year later. Thus, as per the model, the pound isunderpriced in the forward market. Accordingly, Dustin Green would buy pounds forward at$1.5283/£.c. If everyone were to buy pounds forward, the price of pounds forward would increase and becomeequal to $1.5315 per £. The spot exchange rate and the dollar and pound interest rates wouldchange so as to be consistent with this forward rate. A look at the interest rate parity relationship suggests that the spot rate and the interest rate in dollars are likely to go up and the interest rate in pounds is likely to go down, to be consistent with the increase in the forward rate.11. a. If the market participants are risk-neutral, the expected future spot exchange rate would be thesame as the current forward rate. The forward rate is determined based on the current spotexchange rate and the interest rate differential between the two currencies. Thus, the expectedfuture spot exchange rate would depend on the current spot exchange rate and the interest ratedifferential.b. If the market participants are risk-averse, the forward rate would differ from the expected futurespot exchange rate by the risk premium. The risk premium, based on the extent of risk aversionof the market participants, could be positive or negative. So, the expected future spot exchangerate is the forward rate less the risk premium. Since the forward rate is based on the current spot exchange rate and the interest rate differential between the two currencies, the expected futurespot exchange rate would depend on the current spot exchange rate, the interest rate differential, and the risk premium.12. There is some evidence of positive serial correlation in exchange rate movements (real and nominal).Hence, when a currency is going up, a reasonable forecast is that it will continue going up. Similarly, when a currency is going down, a reasonable forecast is that it will continue going down. However, at some point in time, the trend would reverse, and the problem is that a trend-based forecasting model cannot forecast when this turning point would occur. Although these turning points may be infrequent, they can be the occasion of a huge swing. The Mexican peso is a good example. For a few years until the end of 1994, the real value of the peso appreciated steadily. So, forecasters using trendmodels for the real exchange rates were quite successful for many months. However, in December 1994, the peso suddenly crashed and lost around half of its value.13. Statements (a), (c), and (d) are true. Statement (b) is not true, because the objective of central bankactivity in the foreign exchange market is not to profit from trading activities, but to implementmonetary policy and exchange rate targets.Chapter 3 Foreign Exchange Determination and Forecasting 17 14. A mean-reverting time series is one that may diverge from its fundamental value in the short run butreverts to its fundamental value in the long run. Empirical evidence suggests that exchange rates are mean reverting. The real exchange rates (observed exchange rate minus inflation) do deviate from the fundamental value implied by PPP in the short run, but tend to revert to the fundamental value in the long run.15. Most econometric models are unsuitable for short-term exchange rate forecasts, as they model long-term structural economic relationships. For long-term exchange rate forecasts, the use of econometric models has some problems. First, most of them rely on predictions for certain key variables, such as money supply and interest rates. It is not easy to forecast these variables. Second, the structuralcorrelation estimated by the parameters of the equation can change over time, so that even if allcausative variables are correctly forecasted, the model can still yield poor exchange rate predictions.In periods when structural changes are rapid compared with the amount of time-series data required to estimate parameters, econometric models are of little help.16. Technical analysis is more likely to be used for short-term exchange rate movements, while theeconometric approach is more likely to be used for long-term exchange rate movements. The manager of a currency hedge fund and currency traders change their foreign exchange positions quite quickly, and are interested in short-term changes in exchange rates. On the other hand, the manager of an international stock portfolio is unlikely to change his foreign exchange positions quickly, because the transaction costs of buying and selling stocks are quite high. Therefore, the manager of aninternational stock portfolio is more interested in the long-term movements in exchange rates.Similarly, the long-term strategic planner of a corporation is interested in the long-term movements.Accordingly, the answers are:a. Technical analysisb. Econometric approachc. Technical analysisd. Econometric approach17. a. The absolute values of prediction errors are as follows: Forward rate: 1.440 − 1.308 = 0.132;Analyst A: 1.410 − 1.308 = 0.102; and Analyst B: 1.580 − 1.308 = 0.272. Thus, the forecast byAnalyst A was the most accurate.b. The forward rate and Analyst B erroneously predicted that the SFr to $ exchange rate would goup from the then-spot rate of SFr 1.420 per $; that is, the SFr would depreciate. Only Analyst Acorrectly predicted that the Swiss franc would appreciate.18. a. The absolute values of forecast errors are as follows: Forward rate: 148.148 − 144.697 = 3.451;Commerzbank: 148.148 − 142 = 6.148; and Harris Bank: 156 − 148.148 = 7.852. Thus, theforecast as per the forward rate was the most accurate, followed by Commerzbank, and then byHarris Bank.b. Although the forward rate and Commerzbank were more accurate than Harris Bank, both of themerroneously predicted that the yen would appreciate relative to the dollar. Only Harris Bankcorrectly predicted that the yen would depreciate.18 Solnik/McLeavey • Global Investments, Sixth Editionc. Commerzbank’s forecast was ¥142 per $, which was less than the forward rate. Therefore, DavidBrock bought yen forward (sold dollars) at the rate of ¥144.697 per $. Because the actual rateturned out to be ¥148.148 per $, buying yen forward did not turn out to be the right strategy. On the other hand, Harris Bank’s forecast was ¥156 per $, which was more than the forward rate.Therefore, Brian Lee sold yen forward (bought dollars) at the rate of ¥144.697 per $. Because the actual rate turned out to be ¥148.148 per $, selling yen forward turned out to be the right strategy. d. Commerzbank’s forecast had a lower forecast error than Harris Bank’s in Part (a). However, inPart (c), it was right to buy and sell based on Harris Bank’s forecast and not Commerzbank’s.The reason is that Harris Bank’s forecast turned out to be on the right side of the forward rate,while Commerzbank’s did not.19. Let the forecasts made by the Industrial Bank of Japan at the beginning of period t for the beginningof period t + 1 be E (S t + 1|φt ). Let the forward rates quoted at the beginning of period t for thebeginning of period t + 1 be F t , and the actual spot rates at the beginning of periods t and t + 1 be S t and S t +1, respectively. The percentage forecast errors (∈and e ) for each forecast made by the Industrial Bank of Japan and the forward rate are computed as εt +1 = [S t +1 − E (S t +1|φt )]/S t and e t +1 = [S t +1 − F t ]/S t , respectively. The following table details the computations.Pd. S t F t E (S t +1|φt ) S t +1 εt +1e t +1 ε2t +1 e 2t +1 1 143.164 142.511 140 144.3000.03000.01250.0009 0.0002 2 144.300 143.968 141 152.7500.08140.06090.0066 0.0037 3 152.750 153.600 151 149.400−0.0105−0.02750.0001 0.0008 4 149.400 149.400 143 129.600−0.0897−0.13250.0080 0.0176 5 129.600 129.700 130 129.500−0.0039−0.00150.0000 0.0000 6 129.500 129.800 131 139.2500.06370.07300.0041 0.0053 MSE0.0033 0.0046RMSE 0.0573 0.0678 The RMSE for the Industrial Bank of Japan is lower than that for the forward rate. Thus, as per thelimited data set in this problem, the Industrial Bank outperformed the forward rate in terms ofaccuracy of the forecasts, as measured by the RMSE. We have not tested whether the difference in forecast performances is statistically significant.。

国际投资学 国际投资理论课本精炼知识点 含课后习题答案

第二章国际投资理论第一节国际直接投资理论一、西方主流投资理论(一)垄断优势论:市场不完全性是企业获得垄断优势的根源,垄断优势是企业开展对外直接投资的动因。

市场不完全:由于各种因素的影响而引起的偏离完全竞争的一种市场结构。

市场的不完全包括:1.产品市场不完全2..要素市场不完全3.规模经济和外部经济的市场不完全4.政策引致的市场不完全。

跨国公司具有的垄断优势:1.信誉与商标优势2.资金优势3.技术优势4.规模经济优势(内部和外部)5.信息与管理优势。

跨国公司的垄断优势主要来源于其对知识资产的控制。

垄断优势认为不完全市场竞争是导致国际直接投资的根本原因。

(二)产品生命周期论:产品在市场销售中的兴与衰。

(三)内部化理论:把外部市场建立在公司内部的过程。

(纵向一体化,目的在于以内部市场取代原来的外部市场,从而降低外部市场交易成本并取得市场内部化的额外收益。

)(1)内部化理论的基本假设:1.经营的目的是追求利润最大化2.企业可能以内部市场取代外部市场3.内部化跨越了国界就产生了国际直接投资。

(2)市场内部化的影响因素:1.产业因素(最重要)2.国家因素3.地区因素4.企业因素(最重要)(3)市场内部化的收益:来源于消除外部市场不完全所带来的经济效益,包括1.统一协调相互依赖的企业各项业务,消除“时滞”所带来的经济效益。

2.制定有效的差别价格和转移价格所带来的经济效益。

3.消除国际市场不完全所带来的经济效益。

4.防止技术优势扩散和丧失所带来的经济效益。

市场内部化的成本:1.资源成本(企业可能在低于最优化经济规模的水平上从事生产,造成资源浪费)2.通信联络成本3.国家风险成本4.管理成本当市场内部化的收益大于大于外部市场交易成本和为实现内部化而付出的成本时,跨国企业才会进行市场内部化,当企业的内部化行为超越国界时,就产生对外直接投资。

(四)国际生产折衷理论:决定跨国公司行为和对外直接投资的最基本因素有所有权优势、内部化优势和区位优势,即“三优势范式”。

国际投资(杜奇华)课后思考题答案(精整版)

国际投资课后思考题第一章:国际投资导论一、国际投资的特征有哪些?1、国际投资的领域呈现不完全竞争性2、国际投资的目的呈现多样性3、国际投资的主体呈现双重性4、国际投资所使用的货币呈现多元化5、国际投资的环境呈现差异性6、国际投资的运行呈现曲折性7、国际投资的过程呈现更大的风险性二、国际投资的主体和客体包括哪些?(一)、国际投资的主体●跨国公司●国际金融机构●官方与半官方机构●个人投资者(二)、国际投资的客体1.货币性资产(Monetary Assets)●现金●银行存款●应收账款●国际债券●国际股票2.实物资产(Real Assets)●土地●建筑物●机器设备●零部件和原材料3.无形资产(Intangible Assets)●生产诀窍●管理技术●商标●商誉●技术专利三、国际投资历经了哪几个发展时期?1、起步阶段(18世纪末~1914年)●英、法、德、美、荷从事国际投资●国际投资主要流向自然资源丰富的地区2、低迷徘徊阶段(1914年~1945年)●国际投资的总额下降●国际投资方式仍然以国际间接投资为主3、恢复增长阶段(1946年~1979年)●国际投资的规模迅速扩大●国际投资的方式转变为国际直接投资为主4、逐渐发展阶段(20世纪80年代)●国际直接投资的规模迅速扩大●国际投资的流动转向以发达国家为主。

5、高速增长阶段(20世纪90年代)●国际直接投资总额大幅上升●国际直接投资产业分布的转化●国际投资主体向多元化发展●新兴的发展中国家成为国际投资的热点五、国际投资学的研究方法有哪些?●总量分析与个量分析相结合●静态分析与动态分析相结合●定性分析与定量分析相结合●历史分析与逻辑分析相结合●抽象分析与实证分析相结合●理论总结与实践操作相结合六、国际投资的最新发展趋势有哪些?●全球外国直接投资增速下降●大型跨国公司主宰全球经济●外国直接投资流量继续集中在欧、日、美●政府加速开放外国直接投资政策●签订了更多的双边协定和投资协议●中国将成为全球最具活力的外商投资地区第二章国际直接投资理论二、垄断优势理论与内部化理论的主要区别是什么?首先,垄断优势理论是以市场不完全作为跨国经营的前提内部化理论的目的是消除市场的不完全性;其次,垄断优势理论中由于市场不完全导致垄断排斥竞争内部化理论中由于市场不完全导致市场失灵再次,垄断优势理论注重技术垄断优势,是跨国经营的重要意义内部化理论中交易成本最小,注重保证跨国经营的优势最后,垄断优势理论适用于发达国家内部化理论既适用于发达国家,也适用于发展中国家,即可适用于国内,也可适用于国外。

《国际投资》各章练习题答案33页PPT

56、极端的法规,就是极端的不公。 ——西 塞罗 57、法律一旦成为人们的需要,人们 就不再 配享受 自由了 。—— 毕达哥 拉斯 58、法律规定的惩罚不是为了私人的 利益, 而是为 了公共 的利益 ;一部 分靠有 害的强 制,一 部分靠 榜样的 效力。 ——格 老秀斯 59、假如没有法律他们会更快乐的话 ,那么 法律作 为一件 无用之 物自己 就会消 灭。— —洛克

60、人民的幸福是的人,才不会再掉进坑里。——黑格尔 32、希望的灯一旦熄灭,生活刹那间变成了一片黑暗。——普列姆昌德 33、希望是人生的乳母。——科策布 34、形成天才的决定因素应该是勤奋。——郭沫若 35、学到很多东西的诀窍,就是一下子不要学很多。——洛克

国际投资学教程课后题答案(完整版)

第一章1.名词解释:国际投资:是指以资本增值和生产力提高为目标的国际资本流动,是投资者将其资本投入国外进行的一阴历为目的的经济活动。

国际公共(官方)投资: 是指一国政府或国际经济组织为了社会公共利益而进行的投资,一般带有国际援助的性质。

国际私人投资:是指私人或私人企业以营利为目的而进行的投资。

短期投资:按国际收支统计分类,一年以内的债权被称为短期投资。

长期投资:一年以上的债权、股票以及实物资产被称为长期投资。

产业安全:可以分为宏观和中观两个层次。

宏观层次的产业安全,是指一国制度安排能够导致较合理的市场结构及市场行为,经济保持活力,在开放竞争中本国重要产业具有竞争力,多数产业能够沈村冰持续发展。

中观层次上的产业安全,是指本国国民所控制的企业达到生存规模,具有持续发展的能力及较大的产业影响力,在开放竞争中具有一定优势。

资本形成规模:是指一个经济落后的国家或地区如何筹集足够的、实现经济起飞和现代化的初始资本。

2、简述20世纪70年代以来国际投资的发展出现了哪些新特点?(一)投资规模,国际投资这这一阶段蓬勃发展,成为世纪经济舞台最为活跃的角色。

国际直接投资成为了国际经济联系中更主要的载体。

(二)投资格局,1.“大三角”国家对外投资集聚化 2.发达国家之间的相互投资不断增加 3.发展中国家在吸引外资的同时,也走上了对外投资的舞台(三)投资方式,国际投资的发展出现了直接投资与间接投资齐头并进的发展局面。

(四)投资行业,第二次世界大战后,国际直接投资的行业重点进一步转向第二产业。

3.如何看待麦克杜格尔模型的基本理念?麦克杜格尔模型是麦克杜格尔在1960年提出来,后经肯普发展,用于分析国际资本流动的一般理论模型,其分析的是国际资本流动对资本输出国、资本输入国及整个世界生产和国民收入分配的影响。

麦克杜格尔和肯普认为,国际间不存在限制资本流动的因素,资本可以自由地从资本要素丰富的国家流向资本要素短缺的国家。

资本流动的原因在于前者的资本价格低于后者。

国际投资学教程课后练习答案

第一章1.名词解释:国际投资:是指以资本增值和生产力提高为目标的国际资本流动,是投资者将其资本投入国外进行的一阴历为目的的经济活动。

国际公共(官方)投资: 是指一国政府或国际经济组织为了社会公共利益而进行的投资,一般带有国际援助的性质。

国际私人投资:是指私人或私人企业以营利为目的而进行的投资。

短期投资:按国际收支统计分类,一年以内的债权被称为短期投资。

长期投资:一年以上的债权、股票以及实物资产被称为长期投资。

产业安全:可以分为宏观和中观两个层次。

宏观层次的产业安全,是指一国制度安排能够导致较合理的市场结构及市场行为,经济保持活力,在开放竞争中本国重要产业具有竞争力,多数产业能够沈村冰持续发展。

中观层次上的产业安全,是指本国国民所控制的企业达到生存规模,具有持续发展的能力及较大的产业影响力,在开放竞争中具有一定优势。

资本形成规模:是指一个经济落后的国家或地区如何筹集足够的、实现经济起飞和现代化的初始资本。

2、简述20世纪70年代以来国际投资的发展出现了哪些新特点?(一)投资规模,国际投资这这一阶段蓬勃发展,成为世纪经济舞台最为活跃的角色。

国际直接投资成为了国际经济联系中更主要的载体。

(二)投资格局,1.“大三角”国家对外投资集聚化2.发达国家之间的相互投资不断增加 3.发展中国家在吸引外资的同时,也走上了对外投资的舞台(三)投资方式,国际投资的发展出现了直接投资与间接投资齐头并进的发展局面。

(四)投资行业,第二次世界大战后,国际直接投资的行业重点进一步转向第二产业。

3.如何看待麦克杜格尔模型的基本理念?麦克杜格尔模型是麦克杜格尔在1960年提出来,后经肯普发展,用于分析国际资本流动的一般理论模型,其分析的是国际资本流动对资本输出国、资本输入国及整个世界生产和国民收入分配的影响。

麦克杜格尔和肯普认为,国际间不存在限制资本流动的因素,资本可以自由地从资本要素丰富的国家流向资本要素短缺的国家。

资本流动的原因在于前者的资本价格低于后者。

《国际投资》第六版作业课后练习答案

第一章15/16/20第二章4/6/9/15/16/19/20第三章3/5/9/16/18第四章8/13/15/16/17第五章2/7/10/15/17第六章6/8/10/12/13文本:人参淫家Fish 汉化:fish&MonkEy协力排版:MonkEy 校对:无时间:无后期:无本汉化由马骝鱼汉化组制作,本作品来源于互联网供学习爱好者使用禁止用于商业盈利行为若因私自散布造成法律纠纷汉化组概不负责第一章15.问:假设在某一时点,巴克莱银行每英镑的美元标价为英镑对美元=1.4570。

兴业银行每美元的目标价位为美元对日元=128.17,米德银行每英镑的日元的套算汇率的标价为英镑对日元=183.a.不考虑买卖价差,此处是否存在套利机会b.加入存在套利机会,你要通过哪些步骤以获得套利利润?如果你有100万美元,你可以获利多少?解:a.根据题目可以求得美元对日元的汇率:£:¥= $:¥⨯ £:$ = 128.17 ⨯ 1.4570 = 186.74。

然而,米德银行的标价为£:¥=1:183,因此存在套利机会b.在存在£:¥=186.74的同时,米德银行汇率标价为£:¥=1:183,即英镑对日元价值在米德银行被相对低估,因此,你的套利步骤应建立为使用日元从米德银行购买英镑,有100万美元情况下,具体步骤如下:a. 在兴业银行售出美元以取得日元: 售出$1,000,000 以取得$1,000,000 ⨯ ¥128.17 / $ =¥128,170,000.b. 在米德银行出售日元以购买英镑:售出l ¥128,170,000 以购买¥128,170,000/(¥183 / £) =£700,382.51.c. 在巴克莱银行将英镑兑换为美元: 卖出£700,382.51 ,得到£700,382.51 ⨯ ($1.4570 /k, £) =$1,020,457.32.因此,获利为:$1,020,457.32 - $1,000,000 = $20,457.3216.吉姆擅长与套算汇率套利,在某一个时点,他注意到如下标价:以瑞士法郎标价的美元价值= 1.5971 瑞士法郎/美元以澳大利亚元标价的美元价值=1.8215 澳大利亚/美元以澳大利亚元标价的瑞士法郎价值=1.1450 澳大利亚元/瑞士法郎不考虑交易成本,基于这些标价,吉姆有套利机会吗?他应该怎样做来获取套利利润?他用100万美元可以套利多少?解:由题可知,澳元跟瑞士法郎之间的隐形汇率为SFr:A$ = $:A$ ⨯ SFr:$ = ($:A$) ÷ ($:SFr) = 1.8215/1.5971 = 1.1405。

国际投资学教程(第四版)綦建红 答案

《国际投资学教程》(第四版)习题参考答案第一章 国际投资概述1.名词解释国际投资:是指以资本增值和生产力提高为目标的国际资本流动,是投资者将其资本投入国外进行的以盈利为目的的经济活动。

公共投资VS 私人投资:前者是指一国政府或国际经济组织为了社会公共利益而进行的投资,一般带有国际援助的性质;后者是指私人或私人企业以盈利为目的而进行的投资。

二者区分的关键点在于投资主体和投资目的。

长期投资VS 短期投资:二者区分的关键点在于时间,前者一年以上,后者一年之内。

产业安全:所谓产业安全,可以分为宏观和中观两个层次。

宏观层次的产业安全,是指一国制度安排能够导致较合理的市场结构及市场行为,经济保持活力,在开放竞争中本国重要产业具有竞争力,多数产业能够生存并持续发展。

中观层次上的产业安全,是指本国国民所控制的企业达到生存规模,具有持续发展的能力及较大的产业影响力,在开放竞争中具有一定优势。

资本形成规模:是指海外直接投资的进入通常会引致东道国资本存量的增加,并被认为是国际投资对东道国(尤其是发展中东道国)经济增长的重大贡献。

2.简述20世纪70年代以来国际投资的发展出现了哪些新特点?(1)投资规模:国际直接投资的增长率大大超过了同期世界总产值和世界出口的增长率,成为国际经济联系中更主要的载体。

(2)投资格局,三个要点:其一,“大三角”国家对外投资集聚化,即美国、日本和西欧三足鼎立的“大三角”国际投资格局得以形成。

不仅如此,“大三角”国家和发展中国家相比,在对外投资领域显示出绝对主导地位。

其二,发达国家之间的相互投资不断增加。

不仅在国际资本流动中占据2/3的比重,成为国际投资的主体,而且在全球直接投资中占有更加重要的地位,形成了明显的以德国为中心的欧盟圈、以美国为中心的北美圈和以日本为中心的亚洲圈,占据了发达国家之间资本输入的绝大部分。

其三,发展中国家在吸引外资的同时,也走上了对外投资的舞台。

(3)投资方式:20世纪80年代以来,国际投资的发展出现了直接投资与间接投资齐头并进的发展局面。

国际投资第二章课后习题答案

Chapter 2Foreign Exchange Parity Relations1. Because the interest rate in A is greater than the interest rate in B, α is expected to depreciate relativeto β, and should trade with a forward discount. Accordingly, the correct answer is (c).2. Because the exchange rate is given in €:$ terms, the appropriate expression for the interest rate parity relation is€+=+$11r F S r (r $ is a part of the numerator and r € is a part of the denominator).a. The one-year €:$ forward rate is given by €:==1.05$ 1.1795 1.19081.04b. The one-month €:$ forward rate is given by€:+==+1(0.04/12$ 1.1795 1.18051(0.03/12)Of course, these are central rates, and bid-ask rates could also be determined on the basis of bid-askrates for the spot exchange and interest rates.3. a. bid €:¥ = (bid $:¥) × (bid €:$) = 108.10 × 1.1865 = 128.2607.ask €:¥ = (ask $:¥) × (ask €:$) = 108.20 × 1.1870 = 128.4334.b. Because the exchange rate is in €:$ terms, the appropriate expression for the interest rate parityrelation is F /S = (1 + r $)/(1 + r €).€€€++==++=$1(ask )1(0.0525/4):$3-month ask (spot ask :$)1.18701(bid )1(0.0325/4)1.1929r rThus, the €:$3-month forward ask exchange rate is: 1.1929.c. bid $:€ = 1/ask €:$ = 1 / 1.1929 = 0.8383.Thus, the 3-month forward bid exchange rate is $:€ = 0.8383.Chapter 2 Foreign Exchange Parity Relations 7d. Because the exchange rate is in $:¥ terms, the appropriate expression for the interest rate parityrelation is F /S = (1 + r ¥ )/1 + r $.$++===+¥1(bid )1(0.0125/4)$:¥3-month bid (spot ask $:¥)108.10107.031(ask )(0.0325/4)r r $++===+¥1(ask )1(0.0150/4)$:¥3-month ask (spot ask $:¥)108.20107.261(bid )(0.0500/4)r rThus, the $:¥ 3-month forward exchange rate is: 107.03 – 107.26. Note : The interest rates one uses in all such computations are those that result in a lower forwardbid (so, bid interest rates in the numerator and ask rates in the denominator) and a higher forward ask (so, ask interest rates in the numerator and bid rates in the denominator).4. a. For six months, r SFr = 1.50% and r $ = 1.75%. Because the exchange rate is in $:SFr terms, the appropriate expression for the interest rate parity relation isSFr $SFr $1,or (1)(1)1r F F r r S r S+=+=++ The left side of this expression is$ 1.6558(1)(10.0175) 1.01331.6627F r S+=+= The right side of the expression is: 1 + r SFr = 1.0150. Because the left and right sides are not equal, IRP is not holding.b. Because IRP is not holding, there is an arbitrage possibility: Because 1.0133 < 1.0150, we cansay that the SFr interest rate quote is more than what it should be as per the quotes for the otherthree variables. Equivalently, we can also say that the $ interest rate quote is less than what itshould be as per the quotes for the other three variables. Therefore, the arbitrage strategy shouldbe based on borrowing in the $ market and lending in the SFr market. The steps would be asfollows:• Borrow $1,000,000 for six months at 3.5% per year. Need to pay back $1,000,000 ×(1 + 0.0175) = $1,017,500 six months later.• Convert $1,000,000 to SFr at the spot rate to get SFr 1,662,700.• Lend SFr 1,662,700 for six months at 3% per year. Will get back SFr 1,662,700 ×(1 + 0.0150) = SFr 1,687,641 six months later.• Sell SFr 1,687,641 six months forward. The transaction will be contracted as of the current date but delivery and settlement will only take place six months later. So, six months later,exchange SFr 1,687,641 for SFr 1,687,641/SFr 1.6558/$ = $1,019,230.The arbitrage profit six months later is 1,019,230 – 1,017,500 = $1,730.5. a. For three months, r $ = 1.30% and r ¥ = 0.30%. Because the exchange rate is in $:¥ terms, the appropriate expression for the interest rate parity relation is¥$¥$1,or (1)(1)1r F F r r S r S+=+=++8 Solnik/McLeavey • Global Investments, Sixth EditionThe left side of this expression is$107.30(1)(10.0130) 1.0064.108.00F r S+=+= The right side of this expression is: 1 + r ¥ = 1.0030. Because the left and right sides are not equal, IRP is not holding.b. Because IRP is not holding, there is an arbitrage possibility. Because 1.0064 > 1.0030, we cansay that the $ interest rate quote is more than what it should be as per the quotes for the otherthree variables. Equivalently, we can also say that the ¥ interest rate quote is less than what itshould be as per the quotes for the other three variables. Therefore, the arbitrage strategy shouldbe based on lending in the $ market and borrowing in the ¥ market. The steps would be asfollows:• Borrow the yen equivalent of $1,000,000. Because the spot rate is ¥108 per $, borrow$1,000,000 × ¥108/$ = ¥108,000,000. Need to pay back ¥108,000,000 × (1 + 0.0030) =¥108,324,000 three months later.• Exchange ¥108,000,000 for $1,000,000 at the spot exchange rate.• Lend $1,000,000 for three months at 5.20% per year. Will get back $1,000,000 ×(1 + 0.0130) = $1,013,000 three months later.• Buy ¥108,324,000 three months forward. The transaction will be contracted as of the current date, but delivery and settlement will only take place three months later. So, three monthslater, get ¥108,324,000 for ¥108,324,000 / (¥107.30 per $) = $1,009,543.The arbitrage profit three months later is 1,013,000 – 1,009,543 = $3,457.6. At the given exchange rate of 5 pesos/$, the cost in Mexico in dollar terms is $16 for shoes, $36 forwatches, and $120 for electric motors. Thus, compared with the United States, shoes and watches are cheaper in Mexico, and electric motors are more expensive in Mexico. Therefore, Mexico will import electric motors from the United States, and the United States will import shoes and watches from Mexico. Accordingly, the correct answer is (d).7. Consider two countries, A and B. Based on relative PPP,+=+1011A BS I S I where S 1 and S 0 are the expected and the current exchange rates between the currencies of A and B, and I A and I B are the inflation rates in A and B. If A and B belong to the group of countries thatintroduces the same currency, then one could think of both S 1 and S 0 being one. Then, I A and I B should both be equal for relative PPP to hold. Thus, introduction of a common currency by a group ofcountries would result in the convergence of the inflation rates among these countries. A similarargument could be applied to inflation among the various states of the United States.8. Based on relative PPP,+=+Switzerland 10US11I S S IChapter 2 Foreign Exchange Parity Relations 9where S 1 is the expected $:SFr exchange rate one year from now, S 0 is the current $:SFr exchange rate, and I Switzerland and I US are the expected annual inflation rates in Switzerland and the United States, respectively. So,1110.02and 1.60(1.02/1.05)SFr 1.55/$.1.6010.05S S +===+ 9. a. A Japanese consumption basket consists of two-thirds sake and one-third TV sets. The price ofsake in yen is rising at a rate of 10% per year. The price of TV sets is constant. The Japanese consumer price index inflation is therefore equal to+=21(10%)(0%) 6.67%33b. Relative PPP states thatFC 10DC1.1I S S I +=+ Because the exchange rate is given to be constant, we have S 0 = S 1, which implies S 1/S 0 = 1. As a result, in our example, PPP would hold if 1 + I FC = 1 + I DC (i.e., I FC = I DC ). Because the Japanese inflation rate is 6.67% and the American inflation rate is 0%, we do not have I FC = I DC , and PPP does not hold.10. a. i. The law of one price is that, assuming competitive markets and no transportation costs ortariffs, the same goods should have the same real prices in all countries after convertingprices to a common currency.ii. Absolute PPP, focusing on baskets of goods and services, states that the same basket ofgoods should have the same price in all countries after conversion to a common currency.Under absolute PPP, the equilibrium exchange rate between two currencies would be the ratethat equalizes the prices of a basket of goods between the two countries. This rate wouldcorrespond to the ratio of average price levels in the countries. Absolute PPP assumes noimpediments to trade and identical price indexes that do not create measurement problems.iii. Relative PPP holds that exchange rate movements reflect differences in price changes(inflation rates) between countries. A country with a relatively high inflation rate willexperience a proportionate depreciation of its currency’s value vis-à-vis that of a countrywith a lower rate of inflation. Movements in currencies provide a means for maintainingequivalent purchasing power levels among currencies in the presence of differing inflationrates.Relative PPP assumes that prices adjust quickly and price indexes properly measure inflationrates. Because relative PPP focuses on changes and not absolute levels, relative PPP is morelikely to be satisfied than the law of one price or absolute PPP.b. i. Relative PPP is not consistently useful in the short run because of the following:(1) Relationships between month-to-month movements in market exchange rates and PPPare not consistently strong, according to empirical research. Deviations between the ratescan persist for extended periods. (2) Exchange rates fluctuate minute by minute becausethey are set in the financial markets. Price levels, in contrast, are sticky and adjust slowly.(3) Many other factors can influence exchange rate movements rather than just inflation.ii. Research suggests that over the long term, a tendency exists for market and PPP rates tomove together, with market rates eventually moving toward levels implied by PPP.10 Solnik/McLeavey • Global Investments, Sixth Edition11. a. If the treasurer is worried that the franc might appreciate in the next three months, she couldhedge her foreign exchange exposure by trading this risk against the premium included in theforward exchange rate. She could buy 10 million Swiss francs on the three-month forward market at the rate of SFr 1.5320 per €. The transaction will be contracted as of the current date, butdelivery and settlement will only take place three months later.b. Three months later, the company received the 10 million Swiss francs at the forward rate ofSFr 1.5320 per € agreed on earlier. Thus, the company needed (SFr 10,000,000)/(SFr 1.5320per €), or €6,527,415. If the company had not entered into a forward contract, the companywould have received the 10 million Swiss francs at the spot rate of SFr 1.5101 per €. Thus, thecompany would have needed (SFr 10,000,000) / (SFr 1.5101 per €), or €6,622,078. Therefore,the company benefited by the treasurer’s action, because €6,622,078 – €6,527,415 = €94,663were saved.12. The nominal interest rate is approximately the sum of the real interest rate and the expected inflationrate over the term of the interest rate. Even if the international Fisher relation holds, and the realinterest rates are equal among countries, the expected inflation can be very different from one country to another. Therefore, there is no reason why nominal interest rates should be equal among countries.13. Because the Australian dollar is expected to depreciate relative to the dollar, we know from thecombination of international Fisher relation and relative PPP that the nominal interest rate inAustralia is greater than the nominal interest rate in the United States. Further, the nominal interest rate in the United States is greater than that in Switzerland. Thus, the nominal interest rate inAustralia has to be greater than the nominal interest rate in Switzerland. Therefore, we can say from the combination of international Fisher relation and relative PPP that the Australian dollar is expected to depreciate relative to the Swiss franc.14. According to the approximate version of the international Fisher relation, r Sweden − r US = I Sweden − I US . So, 8 − 7 = 6 − I US , which means that I US = 5%.According to the approximate version of relative PPP,−=−10Sweden US 0S S I I S where, S 1 and S 0 are in $:SKr terms. I Sweden − I U S = 6 − 5 = 1%, or 0.01. So, (6 − S 0)/S 0 = 0.01. Solving for S 0, we get S 0 = SKr 5.94 per $.According to the approximate version of IRP,−=−0Sweden US 0F S r r S where, F and S 0 are in $:SKr terms. r Sweden − r US = 8 − 7 = 1%, or 0.01. So, (F − 5.94)/5.94 = 0.01. Solving for F , we get F = SKr 6 per $.Because we are given the expected exchange rate, we could also have arrived at this answer by usingthe foreign exchange expectations relation.Chapter 2 Foreign Exchange Parity Relations 1115. According to the international Fisher relation,++=++Switzerland Switzerland UK UK1111r I r I So,++=++Switzerland 110.0410.1210.10r therefore, r Switzerland = 0.0589, or 5.89%.According to relative PPP,+=+Switzerland 10UK11I S S I where, S 1 and S 0 are in £:SFr terms.So,110.04.310.10S +=+ Solving for S 1 we get S 1 = SFr 2.8364 per £.According to IRP,+=+Switzerland 0UK11r F S r where, F and S 0 are in £:SFr terms.So,10.0589.310.12F +=+ Solving for F , we get F = SFr 2.8363 per £. This is the same as the expected exchange rate in oneyear, with the slight difference due to rounding.16. During the 1991–1996 period, the cumulative inflation rates were about 25 percent in Malaysia,61 percent in the Philippines, and 18 percent in the United States. Over this period, based on relative PPP, one would have expected the Malaysian ringgit to depreciate by about 7 percent relative to the United States dollar (the inflation differential). In reality, the Malaysian ringgit appreciated by about 8 percent. Similarly, in view of the very high inflation differential between the Philippines and the United States, one would have expected the Philippine peso to depreciate considerably relative to the dollar. But it did not. Thus, according to PPP, both currencies had become strongly overvalued.12 Solnik/McLeavey • Global Investments, Sixth Edition17. a. According to PPP, the current exchange rate should bePif Pif 1010$$10//PI PI S S PI PI == where subscript 1 refers to the value now, subscript 0 refers to the value 20 years ago, PI refers toprice index, and S is the $:pif exchange rate. Thus, the current exchange rate based on PPP should be1200/1002pif 1 per $.400/100S ⎛⎞==⎜⎟⎝⎠b. As per PPP, the pif is overvalued at the prevailing exchange rate of pif 0.9 per $.18. Exports equal 10 million pifs and imports equal $7 million (6.3 million pifs). Accordingly, the tradebalance is 10 − 6.3 = 3.7 million pifs.• Balance of services includes the $0.5 million spent by tourists (0.45 million pifs).• Net income includes $0.1 million or 0.09 million pifs received by Paf investors as dividends,minus 1 million pifs paid out by Paf as interest on Paf bonds (− 0.91 million pifs).• Unrequited transfers include $0.3 million (0.27 million pifs) received by Paf as foreign aid.• Portfolio investment includes the $3 million or 2.7 million pifs spent by Paf investors to buyforeign firms. So, portfolio investment = −2.7 million pifs.Based on the preceding,• Current account = 3.24 (= 3.70 + 0.45 − 0.91)• Capital account = 0.27• Financial account = −2.7The sum of current account, capital account, and financial account is 0.81. By definition of balance ofpayments, the sum of the current account, the capital account, the financial account, and the change in official reserves must be equal to zero. Therefore, official reserve account = −0.81.The following summarizes the effect of the transactions on the balance of payments.Current account 3.24Trade balance 3.70Balance of services 0.45Net income – 0.91Capital account 0.27Unrequited transfers 0.27Financial account – 2.70Portfolio investment – 2.70Official reserve account – 0.8119. a. A traditional flow market approach would suggest that the home currency should depreciatebecause of increased inflation. An increase in domestic consumption could also lead to increased imports and a deficit in the balance of trade. This deficit should lead to a weakening of the homecurrency in the short run.b. The asset market approach claims that this scenario is good for the home currency. Foreigncapital investment is attracted by the high returns caused by economic growth and high interestrates. This capital inflow leads to an appreciation of the home currency.Chapter 2 Foreign Exchange Parity Relations 13 20. a. i. The immediate effect of reducing the budget deficit is to reduce the demand for loanablefunds because the government needs to borrow less to bridge the gap between spending andtaxes.ii. The reduced public-sector demand for loanable funds has the direct effect of lowering nominal interest rates, because lower demand leads to lower cost of borrowing, iii. The direct effect of the budget deficit reduction is a depreciation of the domestic currency and the exchange rate. As investors sell lower yielding Country M securities to buy thesecurities of other countries, Country M’s currency will come under pressure andCountry M’s currency will depreciate.b. i. In the case of a credible, sustainable, and large reduction in the budget deficit, reducedinflationary expectations are likely because the central bank is less likely to monetize thedebt by increasing the money supply. Purchasing power parity and international Fisherrelationships suggest that a currency should strengthen against other currencies whenexpected inflation declines.ii. A reduction in government spending would tend to shift resources into private-sector investments, in which productivity is higher. The effect would be to increase the expectedreturn on domestic securities.。

国际投资第六版作业课后练习答案(30题例题6.3)

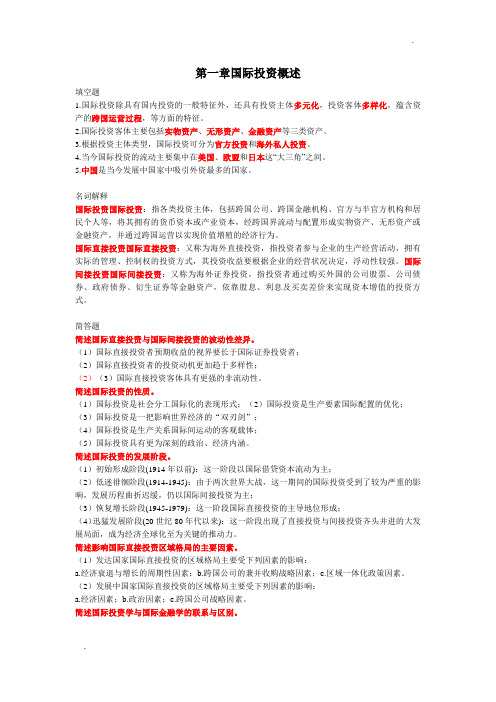

第一章 15/16/20第二章 4/6/9/15/16/19/20第三章 3/5/9/16/18第四章 8/13/15/16/17第五章 2/7/10/15/17第六章 6/8/10/12/13第五章2、一家在巴黎交易所上市的法国公司法国液化空气集团(Air Liquide) 的中央限价委托单集合如下所示:宾出権令买入指令限价眼份SOO1511455002 000150W 2 0001 (JDO149142 1 00050014?141 2 000500146140I 000A.文森特•雅克(Vincent Jacquet )先生希望买入1500股,浴室他输入了一个买入指令。

那么他会以什么价格买到这些股票?B.假定雅克先生原本想卖出投资组合中的 1000股该公司股票,那么他会以什么价格卖出这些股票?解:a、 Vice nt将会以146的价钱买入 500股,147的价格买入 500股,149买入500股。

b、以145的价钱卖出500,143卖出500股票。

7、美国股市的市值超过美国的GDP大多数欧洲国家则相反,一下哪项不是其原因:A.在欧洲,国有公司所占比重更大;B.欧洲银行不能持有其客户公司的股票;C.许多欧洲公司非常依赖银行融资;D.私有公司在欧洲是一种传统.选择b。

因为美国银行可以持有公司股票,所以美国股市的市值超过美国GDP10、大众汽车(Volkswagen)的股票在法兰克福股票交易所交易.一个美国投资者以每股56.91欧元的价格买入 1000股,此时汇率为0.9790~0.9795欧元/美元.三个月之后,这个投资者得到每股0.50欧元的股利,他决定以当期每股 61.10欧元的价格卖出股票•此时汇率是 0.9810~0.9815欧元/美元.德国的预扣股利所得税率是15%,而且美国和德国签署了一个关于避免双重征税的税收协定•A.投资者收到的税后股利是多少(以美元计价)?B投资者在大众汽车的整个交易中的资本利得是多少?C在美国税收制度下,投资者应该公布多少股利收入•获得多少税收抵免?解:a、税后股利=0.5 X 1000 X( 1-15%) =425?425 X 0.9810=$416.93b、 56.91 X 1000 X 0.9795=$55743.3561.10 X 1000 X 0.9810=$59939.1资本利得=59939.1-55743.35=4395.75C因为有税收协定所以税收抵扣 =? 0.5 X 1000 X 0.9810=$490.5015、一个美国机构投资者想购买美国聚乙烯工业公司(British Polythene Industries )的10000股股票。

国际投资学(课后题)

第一章国际投资概述填空题1.国际投资除具有国内投资的一般特征外,还具有投资主体多元化,投资客体多样化,蕴含资产的跨国运营过程,等方面的特征。

2.国际投资客体主要包括实物资产、无形资产、金融资产等三类资产。

3.根据投资主体类型,国际投资可分为官方投资和海外私人投资。

4.当今国际投资的流动主要集中在美国、欧盟和日本这“大三角”之间。

5.中国是当今发展中国家中吸引外资最多的国家。

名词解释国际投资国际投资:指各类投资主体,包括跨国公司、跨国金融机构、官方与半官方机构和居民个人等,将其拥有的货币资本或产业资本,经跨国界流动与配置形成实物资产、无形资产或金融资产,并通过跨国运营以实现价值增殖的经济行为。

国际直接投资国际直接投资:又称为海外直接投资,指投资者参与企业的生产经营活动,拥有实际的管理、控制权的投资方式,其投资收益要根据企业的经营状况决定,浮动性较强。

国际间接投资国际间接投资:又称为海外证券投资,指投资者通过购买外国的公司股票、公司债券、政府债券、衍生证券等金融资产,依靠股息、利息及买卖差价来实现资本增值的投资方式。

简答题简述国际直接投资与国际间接投资的波动性差异。

(1)国际直接投资者预期收益的视界要长于国际证券投资者;(2)国际直接投资者的投资动机更加趋于多样性;(2)(3)国际直接投资客体具有更强的非流动性。

简述国际投资的性质。

(1)国际投资是社会分工国际化的表现形式;(2)国际投资是生产要素国际配置的优化;(3)国际投资是一把影响世界经济的“双刃剑”;(4)国际投资是生产关系国际间运动的客观载体;(5)国际投资具有更为深刻的政治、经济内涵。

简述国际投资的发展阶段。

(1)初始形成阶段(1914年以前):这一阶段以国际借贷资本流动为主;(2)低迷徘徊阶段(1914-1945):由于两次世界大战,这一期间的国际投资受到了较为严重的影响,发展历程曲折迟缓,仍以国际间接投资为主;(3)恢复增长阶段(1945-1979):这一阶段国际直接投资的主导地位形成;(4)迅猛发展阶段(20世纪80年代以来):这一阶段出现了直接投资与间接投资齐头并进的大发展局面,成为经济全球化至为关键的推动力。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

第一章1.名词解释:国际投资:是指以资本增值和生产力提高为目标的国际资本流动,是投资者将其资本投入国外进行的一阴历为目的的经济活动。

国际公共(官方)投资: 是指一国政府或国际经济组织为了社会公共利益而进行的投资,一般带有国际援助的性质。

国际私人投资:是指私人或私人企业以营利为目的而进行的投资。

短期投资:按国际收支统计分类,一年以内的债权被称为短期投资。

长期投资:一年以上的债权、股票以及实物资产被称为长期投资。

产业安全:可以分为宏观和中观两个层次。

宏观层次的产业安全,是指一国制度安排能够导致较合理的市场结构及市场行为,经济保持活力,在开放竞争中本国重要产业具有竞争力,多数产业能够沈村冰持续发展。

中观层次上的产业安全,是指本国国民所控制的企业达到生存规模,具有持续发展的能力及较大的产业影响力,在开放竞争中具有一定优势。

资本形成规模:是指一个经济落后的国家或地区如何筹集足够的、实现经济起飞和现代化的初始资本。

2、简述20世纪70年代以来国际投资的发展出现了哪些新特点(一)投资规模,国际投资这这一阶段蓬勃发展,成为世纪经济舞台最为活跃的角色。

国际直接投资成为了国际经济联系中更主要的载体。

(二)投资格局,1.“大三角”国家对外投资集聚化 2.发达国家之间的相互投资不断增加 3.发展中国家在吸引外资的同时,也走上了对外投资的舞台(三)投资方式,国际投资的发展出现了直接投资与间接投资齐头并进的发展局面。

(四)投资行业,第二次世界大战后,国际直接投资的行业重点进一步转向第二产业。

3.如何看待麦克杜格尔模型的基本理念麦克杜格尔模型是麦克杜格尔在1960年提出来,后经肯普发展,用于分析国际资本流动的一般理论模型,其分析的是国际资本流动对资本输出国、资本输入国及整个世界生产和国民收入分配的影响。

麦克杜格尔和肯普认为,国际间不存在限制资本流动的因素,资本可以自由地从资本要素丰富的国家流向资本要素短缺的国家。

资本流动的原因在于前者的资本价格低于后者。

资本国际流动的结果将通过资本存量的调整使各国资本价格趋于均等,从而提高世界资源的利用率,增加世界各国的总产量和各国的福利。

虽然麦克杜格尔模型的假设较之现实生活要简单得多,且与显示生活有很大的反差,但是这个模型的理念确实是值得称道的,既国际投资能够同时增加资本输出输入国的收益,从而增加全世界的经济收益。

第二章三优势范式决定跨国公司行为和对外直接投资的最基本因素有三,即所有权优势、内部化优势和区位优势。

所有权特定优势(Ownership)指一国企业拥有能够得到别国企业没有或难以得到的资本、规模、技术、管理和营销技能等方面的优势。

邓宁认为的所有权特定优势有以下几个方面:①资产性所有权优势。

对有价值资产的拥有大公司常常以较低的利率获得贷款,并且具有广泛的资金来源渠道。

②交易性所有权优势。

企业所拥有的无形资产,包括生产诀窍、营销技能、信息、专利、管理、品牌、商誉等。

大公司拥有丰富的组织管理经验和大批各种专业的人才,形成管理方面的优势。

③规模经济优势。

规模经济带来的研发、创新优势以及低成本优势。

企业规模越大,就越容易向海外扩张,成为国际企业。

寡头企业多利用直接投资来扩大化规模经济的优势。

内部化优势(Internalization)内部化优势是指拥有所有权优势的企业为避免市场不完善而把企业的所有权优势保持在企业内部所获得的优势。

由于外部市场的不完美及市场失灵,企业必须具有把所有权优势内部化的能力。

只有通过内部化在一个共同所有的企业内部实行供给和需求的交换关系,用企业自己的程序来配置资源,才能使企业的垄断优势发挥最大的效用。

所有权优势指出了对外直接投资的能力,而内部化优势决定了企业对外直接投资的目的与形式。

但是,一个企业具备了所有权优势并将之内部化,还不能准确地解释直接投资活动,因为出口也能发挥这两种优势。

因此,所有权优势和内部化优势仍只是对外直接投资的必要条件,而非充分条件。

区位特定优势(Location)指一个国家或地区比另一国家或地区能为外国厂商在本国或本地区投资设厂提供更有利的条件的优势,也即某一个国家或地区的投资环境。

区位特定优势决定企业对外直接投资的国际生产布局的地点选择。

具体的区位因素包括:①劳动成本和自然资源。

对外直接投资在选择区位时,优先考虑劳动力成本较低的地区,尤其是标准化以后的产品。

优越的地理位置、丰富的自然资源、合适的气候条件②市场潜力。

多数情况下,国际企业只有当其产品能够进入或部分进入东道国市场的条件下,才会作出直接投资的决定。

③关税与非关税壁垒。

贸易壁垒会影响国际企业在直接投资和出口之间进行选择。

④政府政策。

政府的政策情况和投资环境状况直接影响投资的国家风险,包括有关的金融贸易政策、法律完善程度、基础设施、公用事业、运输通讯等情况。

2.试述垄断企业优势理论和内部化理论的异同垄断优势理论从市场不完全性和企业的特定优势角度出发,论述了发达国家企业对外直接投资的动机和决定因素。

而市场内部化理论着重从自然性市场不完全出发。

并结合国际分工和企业国际生产组织形式分析企业对外直接投资行为。

(书)企业拥有这些特有财产本身的特殊优势,这种财产的内部化过程赋予了企业以特有的优势。

内部化理论通过对中间产品市场缺陷的论述,将海默的理论进一步延伸,将交易成本纳入不完全市场的研究中。

只要内部化的收益大于内部市场交易成本和为实现内部化而付出的成本,企业便拥有内部化优势,从而可以实现跨国经营。

内部化理论从成本和收益的角度解释国际直接投资的动因。

(ppt.)3.试述发展中国家对外直接投资的适用性理论发展中国家国际直接投资的适用性理论1.小规模技术理论:美国经济学家威尔斯80年代提出的小规模技术理论弥补了传统直接投资理论把竞争优势绝对化的不足。

认为发展中国家跨国企业的竞争优势来自低生产成本,这种低生产成本是与其母国的市场特征紧密相关的。

威尔斯主要从三个方面分析了发展中国家跨国企业的比较优势:(1)拥有为小市场需要提供服务的小规模生产技术。

(2)发展中国家在民族产品的海外生产上颇具优势。

(3)低价产品营销战略。

2.技术地方化理论:英国经济学家拉奥在对印度跨国公司的竞争优势和投资动机进行深入研究后提出的。

主要观点:发展中国家企业对进口的技术和产品加以改造和创新,更好满足当地市场,便会形成独特的竞争优势。

证明落后国家企业以比较优势参与国际生产和经营活动的可能性。

3.国家利益优先取得论:从国家利益的角度看,大多数发展中国家,尤其是社会主义国家的企业,其对外直接投资有其本身的特殊性。

这些国家的企业按优势论的标准来衡量是根本不符合跨国经营的条件。

但是由于国家战略利益的原因,企业不得不进行对外直接投资,寻求和发展自身的优势。

在这种情况下,国家将支持和鼓励企业进行跨国经营活动。

第三章一、名词解释1.国际投资环境指影响国际投资的各种因素相互依赖、相互完善、相互制约所形成的矛盾统一体,国际直接投资环境的优劣直接决定了一国对外资吸引力的大小。

2硬环境指能够影响投资环境的外部物质条件,如能源供应、交通和通信、自然资源以及社会生活服务设施等。

3软环境指能够影响国际直接投资的各种非物质形态的因素,如外资政策、法规、经济管理水平、职工技术熟练程度以及社会文化传统等等。

4.冷热比较分析法指出要从政治稳定性、市场机会、经济发展与成就、文化一元化、法令障碍、实质障碍、地理与文化差异等7个方面对各国投资环境进行综合比较分析。

其中,政治稳定性、市场机会、经济发展与成就、文化一元化同属“热”因素,而法令障碍、实质障碍、地理与文化差异同属“冷”因素。

“热”因素越大,“冷”因素越小,一国投资环境越好,外国投资者在该国的投资参与成分就越大。

3.简述国际直接投资环境的重要性及其决定因素P73重要性:它是开展国际投资活动所具备的一切条件的有机整体。

国际直接投资环境的优劣直接决定了一国对外资吸引力的大小。

决定因素:自然因素:它是跨国投资企业生存和发展的必要条件,某些情况下对一定的投资项目起着决定性作用;经济环境:是最直接、最基本的因素,也是首要考虑的因素。

政治因素:是指东道国的政治状况、政策和法规;法律环境:是直接关系到安全性的问题的重要方面社会因素:指对投资有重要影响的社会方面的关系。

3.试总结各种国际投资环境评估方法的基本思路和共性 P81基本思路和共性是将总投资环境分解为若干具体指标,然后再综合评判。

4. 案例分析分别运用等级尺度法和要素评价分类法对英国的投资环境进行计分和评价P84等级尺度法:1.货币稳定性(4-20分)2.近五年通货膨胀率(2-14分)3.资本外调(0-12分)4.外商股权(0-12分)5.外国企业与本地企业之间的差别待遇和控制(0-12分)6.政治稳定性(0-12分)7.当地资本供应能力(0-10分)8.给予关税保护的态度(2-8分)要素评价法:I=AE/CF(B+D+G+H)+x 投资环境激励系数(A)城市规划完善度因子(B)利税因子(C)劳动生产率因子(D)地区基础因子(E)效率因子(F)市场因子(G)管理权因子(H)5. 试结合本章专栏3-1和专栏3-3,分析我国改善投资环境的重点和具体措施。

改善投资环境的重点是改善软环境和社会因素中的价值观念、教育水平、社会心理与习惯。

具体措施是降低贸易壁垒、提高私有财产保护程度、降低企业运行障碍、提高政府清廉程度、提高经济自由程度和提高法律完善程度。

4.国际投资环境具有1)综合性:国际投资的特点和现代经济社会的复杂性,决定了国际投资环境整体是由多种因素综合构成的。

2)系统性:构成国际投资环境的各个因素既有各自独立的性质和功能,又是相互连接、相互作用的,它们共同构成国际投资环境系统。

这个系统的功能强弱不仅取决于各个因素的状况,而且还取决于各种因素相互间的协调程度。

3)层次性:影响国际投资活动的各种外部因素是存在于不同的空间层次上的,有国际因素、国家因素、国内地区因素和厂址因素。

国家环境包括政治、法律、经济、社会喝自然五大因素,但厂址环境一般不包括政治、法律因素,而在国家环境中政治、法律、经济因素是最重要的;在厂址环境中,自然和广义的基础设施等尤为重要。

对于投资者来说这一性质要求投资环境时,必须对四个层次的投资环境都进行分析的基础上,对整个投资环境进行综合评价。

4)相对性:同样的投资环境会对不同的投资活动,显示出不同的功能作用。

产生这一性质的原因在于,国际投资本来就是相对于投资活动而言的,不同的投资活动所要求的投资环境和受同一环境因素的影响是不同的。

这启示人们在评价和改善投资环境时,不仅可以从共性出发,进行总体上的评价和改善,而且应从特殊性出发,针对具体投资活动评价和改善。

第四章.1名词解释:(International Direct Investment)是指一国的自然人、法人或单独或共同出资,在其他国家的境内创立新企业,或增加扩展原有企业,或收购现有企业,并且拥有有效管理控制权的投资行。