财会专业英语全套课件

合集下载

英文版财务会计PPT 1(1)

– Cash – Accounts receivable – Merchandise inventory – Furniture – Land

英文版财务会计PPT 1(1)

Claims to the Assets

• Liabilities – economic obligations payable to an individual or organization outside the business

Owner’s Equity

OWNER’S EQUITY

INCREASES

OWNER’S EQUITY DECREASES

Owner Investments

Owner Withdrawals

Owner’s Equity

Revenues

Expenses

英文版财务会计PPT 1(1)

Revenues

• Amounts earned by delivering goods or services to customers

英文版财务会计PPT 1(1)

Decision Makers

• Individuals • Businesses • Investors • Creditors • Taxing Authorities

英文版财务会计PPT 1(1)

Financial vs. Managerial Accounting

Entity Concept

• Accounting Entity – organization that stands apart as a separate economic unit

英文版财务会计PPT 1(1)

Reliability (Objectivity) Principle

英文版财务会计PPT 1(1)

Claims to the Assets

• Liabilities – economic obligations payable to an individual or organization outside the business

Owner’s Equity

OWNER’S EQUITY

INCREASES

OWNER’S EQUITY DECREASES

Owner Investments

Owner Withdrawals

Owner’s Equity

Revenues

Expenses

英文版财务会计PPT 1(1)

Revenues

• Amounts earned by delivering goods or services to customers

英文版财务会计PPT 1(1)

Decision Makers

• Individuals • Businesses • Investors • Creditors • Taxing Authorities

英文版财务会计PPT 1(1)

Financial vs. Managerial Accounting

Entity Concept

• Accounting Entity – organization that stands apart as a separate economic unit

英文版财务会计PPT 1(1)

Reliability (Objectivity) Principle

会计英语ppt课件26页PPT

How does it go about the research process Critical appraisal - pluses/minuses, what do I learn from it for my

research?

2 Designing the analysis

– General issues - myself – Specific examples from subject areas Cahan/Berkman/Rouse

STRUCTURE

• From developing the idea to presenting the completed piece of research

1. Developing the idea

Formulating testable hypotheses – traditional approach Theoretical modelling

THE SCIENTIFIC RESEARCH PRO4CESS

Research Topic

Research Problem

Hyesign

Variable Measurement

Analyses

Interpret Results

Conclusions

• Good research is systematic, logical, objective and critical – enthusiasm is good, passion dangerous

A WARNING

• Accounting and finance deal with human behaviour – it is not hard science

research?

2 Designing the analysis

– General issues - myself – Specific examples from subject areas Cahan/Berkman/Rouse

STRUCTURE

• From developing the idea to presenting the completed piece of research

1. Developing the idea

Formulating testable hypotheses – traditional approach Theoretical modelling

THE SCIENTIFIC RESEARCH PRO4CESS

Research Topic

Research Problem

Hyesign

Variable Measurement

Analyses

Interpret Results

Conclusions

• Good research is systematic, logical, objective and critical – enthusiasm is good, passion dangerous

A WARNING

• Accounting and finance deal with human behaviour – it is not hard science

财务专业英语ppt课件

E1-2 Divide into groups as instructed by your professor and discuss the following:

a. How does the description of accounting as the "language of business" relate to accounting as being useful for investors and creditors?

a. Information used to determine which products to produce. b. Information about economic resources, claims to those resources,

and changes in both resources and claims. c. Information that is useful in assessing the amount, timing, and

•Definition of Accounting: business language information system basis for decisions

•Types of Accounting Information: (1)Financial Accounting: •Internal users

篮球比赛是根据运动队在规定的比赛 时间里 得分多 少来决 定胜负 的,因 此,篮 球比赛 的计时 计分系 统是一 种得分 类型的 系统

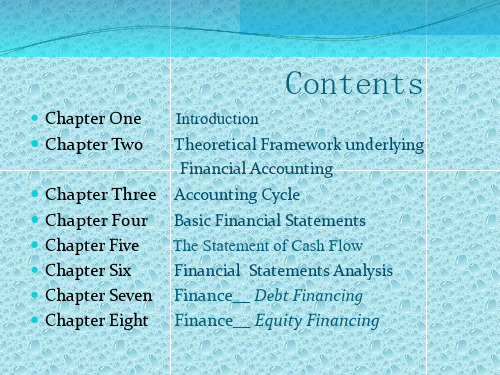

Contents

Chapter One

Chapter Two

Chapter Three Chapter Four

a. How does the description of accounting as the "language of business" relate to accounting as being useful for investors and creditors?

a. Information used to determine which products to produce. b. Information about economic resources, claims to those resources,

and changes in both resources and claims. c. Information that is useful in assessing the amount, timing, and

•Definition of Accounting: business language information system basis for decisions

•Types of Accounting Information: (1)Financial Accounting: •Internal users

篮球比赛是根据运动队在规定的比赛 时间里 得分多 少来决 定胜负 的,因 此,篮 球比赛 的计时 计分系 统是一 种得分 类型的 系统

Contents

Chapter One

Chapter Two

Chapter Three Chapter Four

《财务会计英语讲座》课件

Debit - An entry made on the left side of an account to record increases in assets or decreases in liabilities

Credit - An entry made on the right side of an account to record decreases in assets or increases in liabilities

Liability - Obligations of the entity arising from past events, the settlement of which is expected to result in an output from the entity of resources embodying economic benefits

Financial analysis is essential for decision making, as it allows management to identify opportunities for improvement, assessment risk, and make informed decisions about investment, financing, and other financial decisions

It is essential to maintain proper accounting records to ensure compliance with legal and regulatory requirements

Daily accounting processing requires attention to detail and a high level of accuracy to ensure the integrity and reliability of financial information

会计学英文版ppt课件

managers and other users of its financial statements.The

accounts within the chart of accounts are numbered for use

as references.

Balance Sheet Accounts

accounts.

Prepare an unadjusted trial

balance and explain how it can be used to discover errors.

Using Accounts to Record Transactions

As a result,accounting systems are designed to show the increases and decreases in each accounting equation element as a separate record.This record is

accounts.

Describe and illustrate

journalizing transaction using the double-entry

accounting system.

Describe and illustrate the journalizing and

posting of transactions to

Examples ——wages expense, rent expense, utilities expense, supplies expense, and miscellaneous expense.

A chart of accounts should meet the needs of a company’s

accounts within the chart of accounts are numbered for use

as references.

Balance Sheet Accounts

accounts.

Prepare an unadjusted trial

balance and explain how it can be used to discover errors.

Using Accounts to Record Transactions

As a result,accounting systems are designed to show the increases and decreases in each accounting equation element as a separate record.This record is

accounts.

Describe and illustrate

journalizing transaction using the double-entry

accounting system.

Describe and illustrate the journalizing and

posting of transactions to

Examples ——wages expense, rent expense, utilities expense, supplies expense, and miscellaneous expense.

A chart of accounts should meet the needs of a company’s

财务会计英文版 09 PPT

$540,000

Accounting, 5/E GUOWEI HUST 9 - 6

7

华中科技大学管理学院

Gross Profit

Sales revenues – Cost of goods sold = Gross margin (before operating expenses)

Gross margin – Operating expenses = Net income

Specific identification $1,965.00

FIFO

$1,900.00

LIFO

$2,125.00

Weighted-average

$1,977.50

Accounting, 5/E GUOWEI HUST 9 - 24

25

华中科技大学管理学院

Comparison of Methods

Accounting, 5/E

20 Units @ $20 (Jan) GUOWEI HUST 9 - 20

21

华中科技大学管理学院

Last-In, First-Out

Cost of Goods Sold Oct $ 775 May 1,350 Total $2,125

25 Units @ $31 (Oct)

18

华中科技大学管理学院

Weighted Average

$2,825 total cost/100 units = $28.25/unit Cost of goods sold = 70 × $28.25 = $1977.50

Ending inventory = 30 × $28.25 = $847.50 Accounting, 5/E GUOWEI HUST 9 - 18

Accounting, 5/E GUOWEI HUST 9 - 6

7

华中科技大学管理学院

Gross Profit

Sales revenues – Cost of goods sold = Gross margin (before operating expenses)

Gross margin – Operating expenses = Net income

Specific identification $1,965.00

FIFO

$1,900.00

LIFO

$2,125.00

Weighted-average

$1,977.50

Accounting, 5/E GUOWEI HUST 9 - 24

25

华中科技大学管理学院

Comparison of Methods

Accounting, 5/E

20 Units @ $20 (Jan) GUOWEI HUST 9 - 20

21

华中科技大学管理学院

Last-In, First-Out

Cost of Goods Sold Oct $ 775 May 1,350 Total $2,125

25 Units @ $31 (Oct)

18

华中科技大学管理学院

Weighted Average

$2,825 total cost/100 units = $28.25/unit Cost of goods sold = 70 × $28.25 = $1977.50

Ending inventory = 30 × $28.25 = $847.50 Accounting, 5/E GUOWEI HUST 9 - 18

第3章 Financial Statements《会计英语》PPT课件

Land

Total Assets

133 500

68 000

$350 000

Unit 1 Balance Sheet

Exhibit 3-1-1A balance sheet in report form

ABC Co. LTD

Balance Sheet

December 31, 20

Liabilities & Owners’Equity

$225 000

45 000

270 000

350 000

Unit 1 Balance Sheet

Exhibit 3-1-2 A balance sheet in account form

ABC Co. LTD

Balance Sheet

December 31, 20_ _

Assets

Cash

Accounts Receivable

ABC Co. LTD

Balance Sheet

December 31, 20

Assets

Cash

Accounts Receivable

Supplies

$20 500

65 000

1 500

Cleaning Equipment

39 000

Delivery Equipment

22 500

Buildings

business arrived at this financial position.

Unit 1 Balance Sheet

➢FORMAT OF BALANCE SHEET. The balance sheet may be arranged in

either account form or report form.

Total Assets

133 500

68 000

$350 000

Unit 1 Balance Sheet

Exhibit 3-1-1A balance sheet in report form

ABC Co. LTD

Balance Sheet

December 31, 20

Liabilities & Owners’Equity

$225 000

45 000

270 000

350 000

Unit 1 Balance Sheet

Exhibit 3-1-2 A balance sheet in account form

ABC Co. LTD

Balance Sheet

December 31, 20_ _

Assets

Cash

Accounts Receivable

ABC Co. LTD

Balance Sheet

December 31, 20

Assets

Cash

Accounts Receivable

Supplies

$20 500

65 000

1 500

Cleaning Equipment

39 000

Delivery Equipment

22 500

Buildings

business arrived at this financial position.

Unit 1 Balance Sheet

➢FORMAT OF BALANCE SHEET. The balance sheet may be arranged in

either account form or report form.

财会英语课件

2

Warm-up

1) Are you interested in accounting? 2) How do you know about accounting? 3) Do you think English for Accounting is important? Why? 4) Do you think English for Accounting is difficult? 5) How do you improve your English study?

In-class Activities (rs of Accounting Information 1) The two groups who use accounting information are -- those who have direct financial interest -- those who have indirect financial interest 2) The users with direct financial interest are -- present and potential investors -- present and potential creditors -- management 11

Chapter 1

General View of Accounting

Main Points: 1. Definition of Accounting 2. The Users of Accounting Information 3. Accounting Profession

1

Objectives

In-class Activities (2-1)

会计英语ppt课件

2. We show that behaviour is clearly asymmetric over the economic cycle with much stronger reactions in growth than in downturns

3. We show a second asymmetry in that markets do not respond in the same way to positive as they do to negative shocks

Cui Zhe School of Business Nantong University

OBJECTIVE

• To ensure you have the skills necessary to produce an excellent dissertation

STRUCTURE

• From developing the idea to presenting the completed piece of research

• Over-riding theme BE METHODICAL

• When you get to the literature review take careful notes – set up some sort of filing system

– It is your choice whether it is electronic, physical or a combination but Endnote is useful for references

GETTING STARTED

• Don’t rush • Choose something you are interested in • Something which is useful to the rest of your

3. We show a second asymmetry in that markets do not respond in the same way to positive as they do to negative shocks

Cui Zhe School of Business Nantong University

OBJECTIVE

• To ensure you have the skills necessary to produce an excellent dissertation

STRUCTURE

• From developing the idea to presenting the completed piece of research

• Over-riding theme BE METHODICAL

• When you get to the literature review take careful notes – set up some sort of filing system

– It is your choice whether it is electronic, physical or a combination but Endnote is useful for references

GETTING STARTED

• Don’t rush • Choose something you are interested in • Something which is useful to the rest of your

财会专业英语课件

Special Terms

• • • • • • • • • • • • • • • (31) revenue recognition principle 收入确认原则 (32) revenue (n.)收入 (33) goods (n.) 货物 (34) fair value 公允价值 (35) Materiality principle 重要性原则 (36) matching principle 配比原则 (37) expense (n.) 费用 (38) conservatism principle 谨慎性原则 (39) income (n.) 收入,收益 (40) full disclosure principle 充分披露原则 (41) financial position 财务状态 (42) ethics (n.) 道德规范 (43) confidentiality (n.) 守密 (44) competence (n.) 能力,胜任 (45) integrity (n.) 廉正,正直

Special Terms

• • • • • • • • • • • • • • • (1) accounting (n.) 会计,会计学 (2) accountant (n.) 会计师,会计人员 (3) bookkeeping (n.) 簿记 (4) bookkeeper (n.) 簿记员 (5) financial (a.) 财政的,财务的,金融的,会计的 (6) accounting equation 会计方程式,会计恒等式 (7) internal control 内部控制 (8) audit (n.)审计;查账 (9) public accounting 公共会计 (10) private accounting 私用会计,专用会计,个体会计 (11) governmental accounting 政府会计 (12) accounting entity 会计主体 (13) single proprietorship (n.)独资企业,所有权,业主权 (14) partnership (n.)合伙企业 (15) corporation (n.)公司

《会计专业英语辅导》PPT课件

❖ 2.Most companies have fewer assets accounts than liability account.大多数公 司资产账目比负债账目少。 错

二、判断题〔10分〕

❖ 3.If the number of debit entries in an account is greater than the number of credit entries, the account will have a debit balance.如果借方帐目的数量比贷方工 程的数量大,该帐户将有借方余额。 错

三、简答题〔10分〕

❖ (3) The first-in, first-out method which is often referred to as FIFO, is based upon the assumption thais the first merchandise sold. Each sale is made out of the older goods in stock; the ending inventory therefore consists of the most recently acquired goods.

一、选择题〔40分〕

❖ 3.During a period of rising prices, the inventory method that yields the highest net income and the lowest inventory value, respectively, will be ____D_________.

❖ A. Tangible 有形的 ❖ B. Long-lived ❖ C. Unchanged outlook ❖ D. For resale

二、判断题〔10分〕

❖ 3.If the number of debit entries in an account is greater than the number of credit entries, the account will have a debit balance.如果借方帐目的数量比贷方工 程的数量大,该帐户将有借方余额。 错

三、简答题〔10分〕

❖ (3) The first-in, first-out method which is often referred to as FIFO, is based upon the assumption thais the first merchandise sold. Each sale is made out of the older goods in stock; the ending inventory therefore consists of the most recently acquired goods.

一、选择题〔40分〕

❖ 3.During a period of rising prices, the inventory method that yields the highest net income and the lowest inventory value, respectively, will be ____D_________.

❖ A. Tangible 有形的 ❖ B. Long-lived ❖ C. Unchanged outlook ❖ D. For resale

Module 2 财务会计入门英文版 PPT 21

LO 3: Journalising

Journalizing – Simple journal entries.

On September 1, stockholders invested $15,000 cash in exchange for ordinary shares, and Softbyte purchased computer equipment for $7,000 cash.

Record of increases and decreases in a specific asset, liability, equity, income, or expense item.

Account Name

Debit / Dr.

Credit / Cr.

Debit = “Left” Credit = “Right”

LO 4: The Ledger

Chart of Accounts

Illustration 2-18

LO 4: The Ledger

Standard Form of Account

➢ T-account form used in accounting textbooks. ➢ Ledger form used in practice.

1 600

Service Revenue

1 600

31 Cash

900

Accounts Receivable

900

Required

(a) Post the transactions to T accounts.

(b) Prepare a trial balance as at 31 August 2011.

会计学专业英语课件共350页

Users of Accounting Information

External users Internal users

Internal users of accounting information

• Question:

– How to define internal users of accounting information?

• Recording transactions and preparing financial statements

• Design of accounting system • Cost accounting • Internal control and auditing

Accounting for Governments and Nonproit Organizations

– practicing members – non-practicing members

• Auditing 审计,审计学

– Audit

– Internal/external auditing

– Auditor

The primary services offered by CPA

• Auditing • Income tax services • Management advisory (consultancy or

• Enron

• ACCA (Association of Chartered Certificated Accountants) accaglobal

• AICPA (American Institute of CPA) • CICPA (Chinese Institute of CPA)

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Speity principle 客观性原则 • (17) financial statement 财务报表 • (18) accounting transaction 会计事项 • (19) purchase orders 购货订单、订货单 • (20) invoices (n.)发票 • (21) receipts (n.)收条,收据 • (22) checks (n.) 支票 • (23) cost (n.) 成本 • (24) cost principle 成本原则 • (25) historical cost 历史成本 • (26) asset (n.)资产 • (27) going concern 持续经营 • (28) accounting period 会计期间 • (29) merchandise (n.)商品,货物 • (30) liquidation (n.)偿还,清算

• An individual who earns living by recording the financial activities of business is known as a bookkeeper, while the process of classifying and summarizing business transactions and interpreting their effects is accomplished by the accountant.

1.2 The field of professional accounting

There are three fields of professional accounting: • Public accounting is an area of accounting where accountants

Special Terms

• (31) revenue recognition principle 收入确认原则 • (32) revenue (n.)收入 • (33) goods (n.) 货物 • (34) fair value 公允价值 • (35) Materiality principle 重要性原则 • (36) matching principle 配比原则 • (37) expense (n.) 费用 • (38) conservatism principle 谨慎性原则 • (39) income (n.) 收入,收益 • (40) full disclosure principle 充分披露原则 • (41) financial position 财务状态 • (42) ethics (n.) 道德规范 • (43) confidentiality (n.) 守密 • (44) competence (n.) 能力,胜任 • (45) integrity (n.) 廉正,正直

Special Terms

• (1) accounting (n.) 会计,会计学 • (2) accountant (n.) 会计师,会计人员 • (3) bookkeeping (n.) 簿记 • (4) bookkeeper (n.) 簿记员 • (5) financial (a.) 财政的,财务的,金融的,会计的 • (6) accounting equation 会计方程式,会计恒等式 • (7) internal control 内部控制 • (8) audit (n.)审计;查账 • (9) public accounting 公共会计 • (10) private accounting 私用会计,专用会计,个体会计 • (11) governmental accounting 政府会计 • (12) accounting entity 会计主体 • (13) single proprietorship (n.)独资企业,所有权,业主权 • (14) partnership (n.)合伙企业 • (15) corporation (n.)公司

accounting • 3. Understand divisions of accounting work • 4. Understand the forms of organization • 5. Explain accounting concepts and principles • 6. Understand Ethics in accounting

Accounting English

张国华 王晓巍 主编 科学出版社出版

UNIT 1 BOOKKEEPING CYCLE

Chapter 1 Introduction to Accounting

Learning objectives: • After completing this chapter, you should be able to: • 1. Define accounting • 2. State the difference between bookkeeping and

1.1 Bookkeeping and Accounting

• Accounting is an information system that identifies, measures, records and communicated relevant, reliable, consistent and comparable information about an organization’s economic activities. Its objective is to help people make better decisions.

perform their services for the general public rather than for a single organization. The basic services provided by a public accountant are auditing, preparing tax reports, assisting in various tax problems, and making recommendations for business decisions. • Private accounting is an area of accounting where accountants perform their services for a single organization. The private accountant maintains the accounting records and provides management with financial data needed for business decisions. • Government and nonprofit accounting is an area of accounting where accountants perform their service for local, state, and federal