Section C 审计

香港注册会计师考师审计笔记试卷C_question_Mar2002

SECTION A:Answer the following TWO compulsory questions. They are worth 50 marks (40% of the total Module mark).CASEYou have been asked by Mr. Ma, an audit partner of Wong & Company, the CPA firm you are working with, to handle a potential new audit engagement. During the briefing discussion you had with Mr. Ma, you were informed that Sell Well Company Limited is engaged in the import of foodstuffs from South East Asian and European countries, and distribution of these products to supermarket chains, discount stores as well as corner stores in Hong Kong. Sell Well Company Limited was established by Mr. Chan about 30 years ago and has been growing steadily since then.Mr. Wong, the senior partner of Wong & Company, is a close friend of Mr. Chan and has been advising the latter about his personal retirement plan. A 3-year business plan and the related profit forecast and cash flow projections for Sell Well Company Limited have been prepared, by Mr. Wong based on information provided by Mr. Chan. Having this information at hand, Mr. Wong introduced one of his audit clients, Great Profit Holdings Limited, to Mr. Chan. After some negotiations, Great Profit Holdings Limited acquired the entire equity interest of Sell Well Company Limited, at a consideration of HK$60,000,000 which was determined at a prospective price/earnings ratio of 2 times of the company’s forecasted year 2002 net profit of not lower than HK$30,000,000. It was agreed that the final consideration would be settled based on the financial statements for the year ending 31 December 2002 for Sell Well Company Limited, to be audited by Wong & Company, and the vendor would reimburse the purchaser for any shortfall between the audited net profit and the forecasted net profit for the year ending 31 December 2002, at a multiple of 2 times of the shortfall. It was also agreed that Mr. Chan would remain as the company’s managing director, at a monthly remuneration of HK$80,000, up to the completion of the company’s 2002 audit.You have had a meeting with Miss Li, the new Financial Controller of Sell Well Company Limited, to discuss the audit arrangements. Miss Li has provided with you certain financial information about the company for the last 2 years and the 4 months ended 30April 2002, which have been extracted and are contained in the attached appendix.During the discussion you found out that Miss Li was hired about a month ago by Mr. Chan to replace the previous accountant who had retired after 20 years of service. Miss Li’s most important current task is to work together with an outside software house to ensure prompt conversion of the company’s manual accounting systems into the newly acquired computerised systems, so finalising the management accounts for annual audit will be left to the accounting supervisor.Miss Li informed you that about 2 years ago on the advice of Cheung CPA Limited, Sell Well Company Limited’s previous auditors and tax representative, Sell Well Company Limited began to purchase most of its merchandise from an agent situated overseas. This was done as part of an overall tax saving arrangement. Miss Li did not seem to have any in depth knowledge about the arrangement; however, she agreed to set up a meeting between yourself and the tax representative to discuss this matter further.You also found out that the company trades with its customers on terms varying from cash on delivery, open accounts with 60 days credit and even on a consignment basis. After scanning the trade debtor listing at 30 April 2002, you noted that about 30 % of the balance related to a few supermarket chains and the remaining balance comprised small amounts with little shops all over Hong Kong. You also discovered that certain of these amounts related to goods delivered based on consignment terms; however, according to Miss Li, the amounts of these sales would be minimal and hard to quantify.As it is the company’s policy to achieve an overall gross profit margin of 35% for its products, the company for many years has adopted an inventory valuation policy for calculating the inventory cost. It does this by deducting a standard margin of 35% from all the products’ selling price. Both Mr. Chan and Miss Li have indicated that the company’s preceding auditors accepted this valuation policy and they do not see this to be a concern for the current audit.You believe that you have gained adequate understanding of the circumstances surrounding this potential new audit engagement and are ready to report to the audit partner.AppendixSELL WELL COMPANY LIMITEDEXTRACT OF FINANCIAL INFORMATIONIncome Statement4 Months Year Ended 30/4/2002 Year Ended 31/12/2001 Year Ended 31/12/2000(Unaudited) (Audited) (Audited)HK$’000 HK$’000 HK$’000 Turnover 37,561 100,873 80,345 Cost of sales (24,415) (65,568) (52,225)----------- ----------- ----------- Gross profit 13,146 35,305 28,120 Other revenue 89 312 145 Selling and distribution expenses (2,511) (6,867) (5,572) General and administrative expenses (2,264) (7,201) (6,833)----------- ----------- ----------- Profit from operations 8,460 21,549 15,860 Finance costs (49) (305) (267)----------- ----------- ----------- Profit before taxation 8,411 21,244 15,593 Taxation (700) (1,870) (1,300) ----------- ----------- ----------- Net profit 7,711 19,374 14,293 ====== ====== ====== Dividends paid -- (9,848) -- ====== ====== ======Balance Sheet 30/4/2002 31/12/2001 31/12/2000(Unaudited) (Audited) (Audited)HK$’000 HK$’000 HK$’000 Property, plant and equipment 10,736 8,837 9,802----------- ----------- ----------- Current assetsInventories 9,011 8,920 4,897 Trade and other debtors 24,780 25,934 27,109 Amount due from Mr. Chan 18,000 10,000 500 Bank balances and cash 1,356 1,950 990----------- ----------- ----------- 53,147 46,804 33,496 ----------- ----------- ----------- Current liabilities Trade and other creditors 23,980 25,619 28,077 Taxation payable 1,168 2,195 1,800Bank loan (secured by property, plant andequipment and Mr. Chan’s personal guarantee)11,987 8,790 3,910 ----------- ----------- ----------- 37,135 36,604 33,787 ----------- ----------- ----------- Net current assets (liabilities) 16,012 10,200 (291)----------- ----------- ----------- Net assets 26,748 19,037 9,511 ====== ====== ====== Share capital 10 10 10 Retained profits 26,738 19,027 9,501----------- ----------- ----------- Shareholders’ equities 26,748 19,037 9,511 ====== ====== ======Required:Write a memorandum to Mr. Ma in which you:(1) Commenting on the potential independence/conflict of interest issuessurrounding this new audit engagement of Sell Well Company Limited and the circumstances under which professional ethical standards have to be considered; and(15 marks)(2) Identifying the potential risks and possible reasons for the following and suggest how each risk could be addressed.• Inherent and control risks; and (20 marks)•Critical audit risks with respect to financial statement assertions.(15 marks)* * END OF SECTION A * *(QUESTIONS)* * *SECTION B:Answer the following FIVE compulsory questions. They are worth 50 marks (40% of the total Module mark).ESSAY/SHORT QUESTIONSYou are the audit manager of a CPA firm and are responsible for the audit of ABC Limited (“ABC”) for the year ended 30 April 2002.ABC engages in the trading of household electrical products and is a private company owned by ten families with equal shareholdings. Half of these shareholders have no representation in ABC’s board of directors. In September 2001, ABC acquired 70% of the equity interest of DEF Limited (“DEF”), an enterprise incorporated in the Mainland of China manufacturing household accessories with a year-end at 31 December.The financial statements of DEF for the year ended 31 December 2001 have been audited by your firm’s affiliate in the Mainland of China. You have conducted a peer review of this affiliate and were satisfied with its level of competence. DEF had a turnover of RMB93 million and made an operating loss of RMB3.9 million for the year ended 31 December 2001. Its net assets as at that date amounted to RMB19 million.For the year ended 30 April 2002, ABC’s turnover dropped by 20% to HK$180 million. Its pre-tax profit also dropped by 13% to HK$8 million. Its net assets as at 30 April 2002 amounted to HK$23 million. Materiality level for adjustment was set at 1% of ABC’s net equity.Prior to your finalising the audit, the following events occurred:Event 1ABC’s directors suddenly decided to exclude DEF from consolidation. In their opinion, it was considered impracticable to consolidate DEF because its operations were substantially different from those of ABC. Accordingly, you were requested by ABC’s directors to stop performing any further audit work on DEF for the purpose of consolidating DEF into ABC’s group accounts. In order to comply with the statutory requirements of the Companies Ordinance, ABC’s directors proposed that the group accounts laid before the members at a general meeting consist of separate audited financial statements dealing with ABC and DEF. All necessary information required by law about the results of DEF and the extent to which they have been dealt with in ABC’s accounts would be fully disclosed in ABC’s financial statements by way of notes.Event 2On 28 May 2002, a substantial customer of ABC went bankrupt after suffering unexpected losses from a major lawsuit. This customer accounted for roughly 12% of ABC’s total turnover and had an outstanding debit balance of approximately HK$1.1 million at 30 April 2002. The provisional liquidator of this customer indicated that the chance of the creditors in recovering their debts would be very slim. The directors of ABC, without any valid justification, agreed only to make an 80% provision for this balance in their accounts.Question 1Write a memorandum to your audit partner addressing each of the events described above. Suggest the appropriate type of audit report to be issued, giving reasons for your suggestions. Assume that ABC’s directors are adamant about the treatments outlined and that you encounter no major audit issues other than those described.Marks will be awarded as follows per addressing each event.(a) Event 1 (18 marks)(b) Event 2 (7 marks)(25 marks)Question 2The financial controller of a company is paid a significant part of her salary in the form of a bonus that is based on the audited financial statement profit amount. From the point of view of the external auditor, is audit risk heightened due to this compensation scheme? If the financial controller is also a member of the HKSA, what should be her responsibilities/considerations?(5 marks)Question 3During this past year, one of your CPA firm audit clients implemented a new computerised accounting system in the belief that it would reduce costs. The client formerly utilised a manual accounting system. Briefly discuss several concerns for the upcoming audit.(6 marks)Question 4A CPA plans on using analytical procedures in an upcoming audit. The client has provided all information that was requested by the CPA to perform the procedures. Briefly discuss the following:(a) What are the main advantages of performing analytical procedures in theplanning and review stages of the audit?(3 marks)(b) What are the potential disadvantages?(3 marks)Question 5(a) Explain the difference between auditing “through” a computer and using acomputer in the audit process.(2 marks)(b) Why are most audits now performed by auditing through the computer, and byusing computers as part of the audit process?(3 marks)(c) Briefly explain some of the techniques of auditing through the computer, andusing a computer as an auditing tool.(3 marks)* * END OF EXAMINATION PAPER * *(QUESTIONS)* * *。

审计工作底稿编制指南

信永中和会计师事务所审计工作底稿编制指南一前言1为了规范审计工作底稿的编制、复核、使用及管理,根据《中国注册会计师审计准则第1131号–审计工作底稿》制定本指南。

2本指南主要目标在于向审计人员在执行审计业务过程中编制、复核、使用和管理审计工作底稿时提供指导,如无其他恰当特殊理由,审计人员应遵照执行。

二释义1本指南中审计工作底稿是指对制定的审计计划、实施的审计程序、获取的相关的审计证据,以及得出审计结论作出的记录。

审计工作底稿可以由审计人员编制形成,也可以由被审计单位或其他第三者提供,经审计人员审核后形成。

2 本指南中审计证据是指在审计业务过程中,为了得出审计结论,形成审计意见而使用的所有信息,包括财务报表依据的会计记录中含有的信息和其他信息。

3 本指南中审计档案是指在规划审计工作、实施审计程序、报告审计意见的过程中形成的记录,并对其进行综合整理、分类归档后形成的档案资料。

三总则1 真实性。

系指审计工作底稿中各类资料来源应真实可靠、内容完整。

2 相关性。

系指审计中应根据确定的审计目标在实施完整的审计程序,索取相关审计证据后明确表达专业判断意见。

3 必要性。

系指审计工作底稿中应保存所有必要的审计证据。

4 有效性。

系指审计工作底稿中审计证据对审计结论支持充分,避免资料的重复索取和引用。

5 简洁性。

系指审计工作底稿内容应简明扼要、突出重点,力求突出对审计结论有重大影响的内容。

四一般原则1审计工作底稿基本内容1.1 审计工作底稿应同时包括以下基本内容:1)被审计单位名称:即财务报表的编制单位,若财务报表编报单位为某一集团的下属公司,则应同时写明下属公司的名称,被审计单位名称可写简称。

举例:被审计单位为联通新时空移动通信有限公司天津分公司,审计工作底稿中可写为:新时空天津分公司。

2)审计项目名称:即某一财务报表项目名称或某一审计程序及实施对象的名称,如具体审计项目是某一会计科目,则应同时写明该会计科目。

举例:如审计人员负责审计利润表中管理费用科目,审计工作底稿中审计项目名称为:管理费用。

oracle19c 审计策略

oracle19c 审计策略下载提示:该文档是本店铺精心编制而成的,希望大家下载后,能够帮助大家解决实际问题。

文档下载后可定制修改,请根据实际需要进行调整和使用,谢谢!本店铺为大家提供各种类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by this editor. I hope that after you download it, it can help you solve practical problems. The document can be customized and modified after downloading, please adjust and use it according to actual needs, thank you! In addition, this shop provides you with various types of practical materials, such as educational essays, diary appreciation, sentence excerpts, ancient poems, classic articles, topic composition, work summary, word parsing, copy excerpts, other materials and so on, want to know different data formats and writing methods, please pay attention!Oracle 19c 审计策略详解在当今数字化时代,数据安全和合规性已成为企业管理的关键焦点之一。

ACCA F8备考Tips:审计各阶段及流程详解

ACCA F8备考Tips:审计各阶段及流程详解F8(Audit and Assurance)是一门实务性很强的课程,要求大家熟悉审计工作流程,应用会计知识判断被审计单位的财务报告编制过程及结果是否有误。

自2016年9月开始实施的新考试题型包括Section A和Section B两大部分,Section A(Objective Test Cases)共有三道Case,每个Case有五道选择题,每题两分,涉及范围包括大纲的方方面面;Section B共有三道大题,第一题30分,第二题和第三题各自20分,常见的题型包括auditrisk & auditor’s response,internal controldeficiencies/strengths & TOCs,以及substantive procedures等。

大题对大家书面表达的要求比较高,所以理解审计逻辑,勤加练习并学会总结对于大部分没有实务经验的同学们而言非常必要。

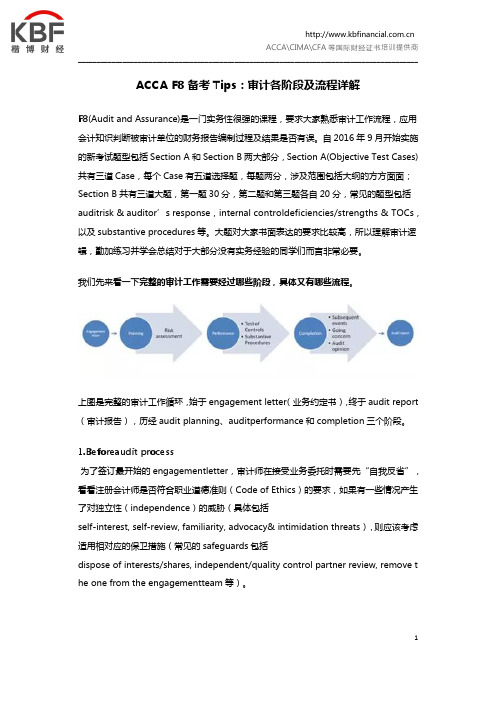

我们先来看一下完整的审计工作需要经过哪些阶段,具体又有哪些流程。

上图是完整的审计工作循环,始于engagement letter(业务约定书),终于audit report (审计报告),历经audit planning、auditperformance和completion三个阶段。

1.Beforeaudit process为了签订最开始的engagementletter,审计师在接受业务委托时需要先“自我反省”,看看注册会计师是否符合职业道德准则(Code of Ethics)的要求,如果有一些情况产生了对独立性(independence)的威胁(具体包括self-interest, self-review, familiarity, advocacy& intimidation threats),则应该考虑适用相对应的保卫措施(常见的safeguards包括dispose of interests/shares, independent/quality control partner review, remove t he one from the engagementteam等)。

中英对照审计准则1121号

中国注册会计师审计准则第1121号——对财务报表审计实施的质量控制(2010年11月1日修订)CHINESE CPA STANDARD ON AUDITING 1121 QUALITY CONTROL FOR AN AUDIT OF FINANCIAL STATEMENTS (asrevised November 1, 2010)第一章总则Chapter I General Provisions第一条为了规范注册会计师对财务报表审计实施质量控制程序的责任,以及项目质量控制复核人员的责任,制定本准则。

Article 1 This Chinese CPA Standard on Auditing (CSA) is formulated to regulate the specific responsibilities of the CPA regarding quality control procedures for an audit of financial statements, and, where applicable, the responsibilities of the engagement quality control reviewer.第二条注册会计师在使用本准则时,需要结合相关职业道德要求。

Article 2 This SCA is to be read in conjunction with relevant ethical requirements.第三条建立和保持质量控制制度(包括政策和程序),是会计师事务所的责任。

按照《质量控制准则第5101号——会计师事务所对执行财务报表审计和审阅、其他鉴证和相关服务业务实施的质量控制》的规定,会计师事务所有义务建立和保持质量控制制度,以合理保证:(一)会计师事务所及其人员遵守职业准则和适用的法律法规的规定;(二)会计师事务所和项目合伙人出具适合具体情况的审计报告。

《审计学C》第七章章内部控制及其评价与审计

⑷内部控制系统按控制方式分类 ①预防性内部控制系统 ——是指那些目的在于防止差错和舞弊行为发生而 设置的措施和程序,如开票与收款分离、开支票与 管印章分离等。 ②察觉性内部控制系统 ——是指当错弊行为发生后,能够立即自动发出信 号,并及时采取纠正或补救的方法、措施和程序, 如定期结账与对账、定期财产清查、定期轮岗等。

7.1.3内部控制的目标和要素 ⑴内部控制的目标 2008年我国《企业内部控制基本规范》提出的内部 控制目标包括: ①确保企业战略的实现; ②运营的效果和效率 ; ③财务报告的可靠性 ; ④资产的安全、完整; ⑤符合相关的法律和法规。 ⑵内部控制的要素 2008我国《企业内部控制基本规范》提出的内部控 制包括内部环境、风险评估、控制活动、信息与沟 通、内部监督五要素。

7.1.2建立内部控制的必要性 ⑴科学管理的要求 跨国经营管理幅度扩大,经营地点分散。 ⑵法律法规的要求 建立有效的内部控制是企业应履行的一项法律责任, 检查和评价内部控制是年度财务报表审计必不可少 的内容。 ⑶成本-效益原则的要求 客观上要求企业加强内部控制的因素有: ①避免违规; ②降低惩罚; ③减少欺诈; ④管理跨国公司风险;

⑵内部控制系统按工作范围分类 ①内部管理控制系统 ——是以提高经营效率、工作效率为目的,用于行 政和业务管理方面的方法、措施和程序,如人事、 技术、质量检验等内部控制。 ②内部会计控制系统 ——是以保护财产物资和确保会计资料可靠性为目 的,用于会计业务和与之相关的其他业务管理方面 的方法、措施和程序,如成本费用、记账程序、货 币资金等内部控制。

自然环境因素 ●自然灾害 ●环境状况

C.风险应对策略

风险规避 风险降低 风险分担

企业对超出风险承受度的风险,通过放弃或者停止与该风险 相关的业务活动以避免和减轻损失的策略。 企业在权衡成本效益之后,准备采取适当的控制措施降低风 险或者减轻损失,将风险控制在风险承受度之内的策略。 企业准备借助他人力量,采取业务分包、购买保险等方式和 适当的控制措施,将风险控制在风险承受度之内的策略。 企业对风险承受度之内的风险,在权衡成本效益后,不准备 采取控制措施降低风险或者减轻损失的策略。

职称头衔中英文对照

[中英文对照]职衔职称 --------------------------------------------------------------------------------

食品伙伴网 (2005-04-10) 进入论坛

立法机关 LEGISLATURE 中华人民共和国主席/副主席 President/Vice President, the People’s Republic of China 全国人大委员长/副委员长 Chairman/Vice Chairman, National People’s Congress 秘书长 Secretary-General 主任委员 Chairman 委员 Member (地方人大)主任 Chairman, Local People’s Congress 人大代表 Deputy to the People’s Congress 政府机构 GOVERNMENT ORGANIZATION 国务院总理 Premier, State Council 国务委员 State Councilor 秘书长 Secretary-General (国务院各委员会)主任 Minister in Charge of Commission for (国务院各部)部长 Minister 部长助理 Assistant Minister 司长 Director 局长 Director 省长 Governor 常务副省长 Executive Vice Governor 自治区人民政府主席 Chairman, Autonomous Regional People’s Government 地区专员 Commissioner, prefecture 香港特别行政区行政长官 Chief Executive, Hong Kong Special Administrative Region 市长/副市长 Mayor/Vice Mayor 区长 Chief Executive, District Government 县长 Chief Executive, County Government

中国政府职位翻译

中国政府职位翻译一、全国人民代表大会常务委员会standingcommitteeofthenationalpeople’scongress(npc)委员长chairman副委员长vice-chairman秘书长secretary-general副秘书长deputysecretary-general委员member全国人民代表大会…委员会…comimittee/CommissionOFTHENPC主任委员Chairman副主任委员Vice—Chairman委员Member二、中国人民政治协商会议全国委员会NationalCommitteeOfTheChinesePeople’SPoliticalCon-SultativeConference(CPPCC)主席Chairman副主席Vice—Chairman秘书长Secretary—General常务委员MemberOfTheStandingCommittee政协全国委员会…委员会mitteeOfTheNationalCommitteeOfTheCPPCC主任委员Chairman副主任委员Vice—Chairman委员Member三、中华人民共和国People’SRepublicOfChina(Prc)主席President副主席Vice-President四、中华人民共和国中央军事委员会PRCCentralMilitaryCommission(CMC)主席Chairman副主席Vice—Chairman委员Member五、最高人民法院SupremePeople’SCout院长President副院长Vice—President审判委员会委员MemberOfTheJudicialCommittee审判员Judge助理审判员AssistantJudge书记员Clerk六、最高人民检察院SupremePeople’SProcuratorate检察长Procurator—General副检察长DeputyProcurator—General检察委员会委员MemberOfTheProcuratorialCommittee检察员Procurator助理检察员AssistantProcurator书记员Clerk七、国务院StateCouncil总理Premier副总理Vice—Premier国务委员StateCouncillor秘书长Secretary—General副秘书长DeputySecretary—General中华人民共和国…部MinistryOfThePeople’SRepublicOfChina部长Minister副部长Vice-Minister部长助理AssistantMinister中华人民共和国国家…委员会StateCommissionOfThePeople’SRepublicOfChina主任Minister副主任Vice—Minister国务院…办公室OfficeOfTheStateCouncil主任Director(Minister)副主任DeputyDirector(Vice—Minister)...银行Bank行长Governor(OfTheCentralBank)President(OfOtherBanks)副行长DeputyGovernor(OfTheCentralBank)Vice—President(OfOtherBanks)中华人民共和国审计署AuditingAdministrationOfThePeopleisRepublicOfChina审计长Auditor—General副审计长DeputyAuditor—General…局Bureau局长Director—General副局长DeputyDirector—General注:如是正部级或副部级局长,可在其职务后加括号注其级别;个别局的局长、副局长,如:专利局局长、副局长可用Commissioner,DeputyCommissioner...署Administration署长Administrator副署长DeputyAdministrator国务院…室OfficeOfTheStateCouncil主任Director(Minister)副主任DeputyDirector(Vice—Minister)...总会Council会长President副会长Vice—President新华通讯社XinhuaNewsAgency社长Director副社长DeputyDirector...院Academy院长President副院长VicePresident…领导小组LeadingGroup组长Head八、各部(委、办、局)内职务名称PositionsOfDepartments,Offices,BureauxOfMinistries/Commjssions办公厅主任Director—GeneralOfTheGeneralOffice副主任DeputyDirector—General局长Director—GeneralOfABureau副局长DeputyDirector—General厅长Director—GeneralOfADepartment副厅长DeputyDirector—General司长Director—GeneralOfADepartment副司长DeputyDirector—General处长DirectorOfADivision副处长DeputyDirector科长SectionChief副科长DeputySectionChief主任科员PrincipalStaffMember副主任科员SeniorStaffMember巡视员Counsel助理巡视员AssistantCounsel调研员Consultant助理调研员AsstantConsultant科员StaffMember办事员Clerk1、立法机关Legislature中华人民共和国主席/副主席President/VicePresident,thePeople'sRepublicofChina全国人大委员长/副委员长Chairman/ViceChairman,NationalPeople'sCongress 秘书长Secretary-General主任委员Chairman委员Member地方人大主任Chairman,LocalPeople'sCongress人大代表DeputytothePeople'sCongress2、政府机构GovernmentOrganization国务院总理Premier,StateCouncil国务委员StateCouncilor秘书长Secretary-General国务院各委员会主任MinisterinChargeofCommissionfor国务院各部部长Minister部长助理AssistantMinister司长Director局长Director省长Governor常务副省长ExecutiveViceGovernor自治区人民政府主席Chairman,AutonomousRegionalPeople'sGovernment地区专员Commissioner,prefecture香港特别行政区行政长官ChiefExecutive,HongKongSpecialAdministrativeRegion 市长/副市长Mayor/ViceMayor区长ChiefExecutive,DistrictGovernment县长ChiefExecutive,CountyGovernment乡镇长ChiefExecutive,TownshipGovernment秘书长Secretary-General办公厅主任Director,GeneralOffice部委办主任Director处长/副处长DivisionChief/DeputyDivisionChief科长/股长SectionChief科员Clerk/Officer发言人Spokesman顾问Adviser参事Counselor巡视员Inspector/Monitor特派员Commissioner3、外交官衔DiplomaticRank特命全权大使AmbassadorExtraordinaryandplenipotentiary 公使Minister代办Charged'Affaires临时代办Charged'AffairesadInterim参赞Counselor政务参赞PoliticalCounselor商务参赞CommercialCounselor经济参赞EconomicCounselor新闻文化参赞PressandCulturalCounselor 公使衔参赞Minister-Counselor商务专员CommercialAttaché经济专员EconomicAttaché文化专员CulturalAttaché商务代表TradeRepresentative一等秘书FirstSecretary武官MilitaryAttaché档案秘书Secretary-Archivist专员/随员Attaché总领事ConsulGeneral领事Consul1、司法、公证、公安Judiciary,notaryandpublicsecurity人民法院院长President,People'sCourts人民法庭庭长ChiefJudge,People'sTribunals审判长ChiefJudge审判员Judge书记ClerkoftheCourt法医LegalMedicalExpert法警JudicialPoliceman人民检察院检察长Procurator-General,People'sprocuratorates 监狱长Warden律师Lawyer公证员NotaryPublic总警监CommissionerGeneral警监Commissioner警督Supervisor警司Superintendent警员Constable2、政党Politicalparty中共中央总书记GeneralSecretary,theCPCCentralCommittee政治局常委Member,StandingCommitteeofPoliticalBureau,theCPCCentralCommittee 政治局委员Member,PoliticalBureauoftheCPCCentralCommittee书记处书记Member,secretariatoftheCPCCentralCommittee中央委员Member,CentralCommittee候补委员AlternateMember党组书记secretary,PartyLeadershipGroup1、社会团体Nongovernmentalorganization会长President主席Chairman名誉顾问HonoraryAdviser理事长President理事Trustee/CouncilMember总干事Director-General总监Director工商金融Industrial,commercialandbankingcommunities 董事长Chairman执行董事ExecutiveDirector总裁President总经理GeneralManager;C.E.O(ChiefExecutiveOfficer)经理Manager财务主管Controller公关部经理PRManager营业部经理BusinessManager销售部经理SalesManager推销员Salesman采购员Purchaser售货员SalesClerk领班Captain经纪人Broker高级经济师SeniorEconomist高级会计师SeniorAccountant注册会计师CertifiedPublicAccountant出纳员Cashier审计署审计长Auditor-General,AuditingAdministration 审计师SeniorAuditor审计员AuditingClerk统计师Statistician统计员StatisticalClerk厂长factoryManagingDirector车间主任WorkshopManager工段长SectionChief作业班长Foreman仓库管理员Storekeeper教授级高级工程师ProfessorofEngineering高级工程师SeniorEngineer技师Technician建筑师Architect设计师Designer机械师Mechanic化验员ChemicalAnalyst质检员QualityInspector2、农业技术人员Professionalofagriculture高级农业师SeniorAgronomist农业师Agronomist助理农业师AssistantAgronomist农业技术员AgriculturalTechnician3、教育科研Educationandresearchdevelopment中国科学院院长President,ChineseAcademyofSciences 主席团执行主席ExecutiveChairman科学院院长President(Academies)学部主任DivisionChairman院士Academician大学校长President,University中学校长Principal,SecondarySchool小学校长Headmaster,PrimarySchool学院院长DeanofCollege校董事会董事Trustee,BoardofTrustees教务主任DeanofStudies总务长DeanofGeneralAffairs注册主管Registrar系主任DirectorofDepartment/DeanoftheFaculty 客座教授VisitingProfessor交换教授ExchangeProfessor名誉教授HonoraryProfessor班主任ClassAdviser特级教师TeacherofSpecialGrade研究所所长Director,ResearchInstitute研究员Professor副研究员AssociateProfessor助理研究员ResearchAssociate研究实习员ResearchAssistant高级实验师SeniorExperimentalist实验师Experimentalist助理实验师AssistantExperimentalist实验员LaboratoryTechnician教授Professor副教授AssociateProfessor讲师Instructor/Lecturer助教Assistant高级讲师SeniorLecturer讲师Lecturer助理讲师AssistantLecturer教员Teacher指导教师Instructor1、医疗卫生Healthandmedicalcommunity 主任医师(讲课)ProfessorofMedicine主任医师(医疗)ProfessorofTreatment儿科主任医师ProfessorofPediatrics主治医师Doctor-in-charge外科主治医师Surgeon-in-charge内科主治医师Physician-in-charge眼科主治医师Oculist-in-charge妇科主治医师Gynecologist-in-charge 牙科主治医师Dentist-in-charge医师Doctor医士AssistantDoctor主任药师ProfessorofPharmacy主管药师Pharmacist-in-charge药师Pharmacist药士AssistantPharmacist主任护师ProfessorofNursing主管护师Nurse-in-charge护师NursePractitioner护士Nurse主任技师SeniorTechnologist主管技师Technologist-in-charge技师Technologist技士Technician2、新闻出版Newsmedia总编辑Editor-in-chief高级编辑FullSeniorEditor主任编辑AssociateSeniorEditor 编辑Editor助理编辑AssistantEditor高级记者FullSeniorReporter主任记者AssociateSeniorReporter 记者Reporter助理记者AssistantReporter编审ProfessorofEditorship编辑Editor助理编辑AssistantEditor技术编辑TechnicalEditor技术设计员TechnicalDesigner校对Proofreader3、翻译Translation译审ProfessorofTranslation翻译Translator/Interpreter助理翻译AssistantTranslator/Interpreter 电台/电视台台长Radio/TVStationController 播音指导DirectorofAnnouncing主任播音员ChiefAnnouncer播音员Announcer电视主持人TVPresenter电台节目主持人DiskJockey4、工艺、美术、电影Arts,craftsandmovies 导演Director演员Actor画师Painter指挥Conductor编导Scenarist录音师SoundEngineer舞蹈编剧Choreographer 美术师Artist制片人Producer剪辑导演MontageDirector 配音演员Dabber摄影师Cameraman化装师Make-upArtist舞台监督StageManager。

财务审计报告三表一注

财务审计报告三表一注Financial Audit Report: Three Statements and One Note三段英文一段中文,风格和句子样式随机,形成一篇结合文档。

---**Section 1: Balance Sheet**The balance sheet presents the financial position of the company at a specific point in time.It consists of assets, liabilities, and shareholders" equity.Assets are divided into current assets and non-current assets, while liabilities are categorized into current liabilities and long-term liabilities.Shareholders" equity represents the residual interest in the assets of the company after deducting liabilities.**section 1: 资产负债表**资产负债表展示了公司在特定时间点的财务状况。

它包括资产、负债和股东权益。

资产分为流动资产和非流动资产,负债分为流动负债和长期负债。

股东权益代表公司在扣除负债后剩余的资产权益。

---**Section 2: Income Statement**The income statement, also known as the profit and loss statement, shows the company"s revenues, expenses, and net income or loss over a specific period.Revenues are generated from the sale of goods or services, while expenses include the costs of goods sold, operating expenses, andincome taxes.The difference between revenues and expenses is the net income or loss, which is ultimately transferred to the statement of changes in equity.**section 2: 利润表**利润表,亦称损益表,展示了公司在特定时间段内的收入、费用以及净收入或亏损。

审计师《企业财务管理》考点:筹资与投资循环审计

审计师《企业财务管理》考点:筹资与投资循环审计审计师《企业财务管理》考点:筹资与投资循环审计导语:在审计师考试中,关于筹资与投资循环审计的考试内容你知道多少?下面是店铺整理的相关的考试内容重点,需要学习的小伙伴一起来看看吧。

内容与重点1、业务循环性质。

资本循环内部控制和主要文件。

2、业务循环内部控制测评和审计目标。

资本循环内部控制测评和审计目标3、所有者权益审计。

实收资本审计内容;资本公积审计内容;盈余公积审计内容。

4、举债筹资审计(中级要求)。

短期借款、长期借款、应付债券、长期应付款、借款费用审计内容。

5、投资审计(中级要求)。

长期股权投资、交易性投资审计内容。

第一节本业务循环性质知识点一、业务循环综述筹资与投资循环业务涉及资金筹集、资金投入业务过程,其业务流程具体包括:确定资金需求量、选择筹资方式、审批授权、签订筹资协议、取得资金、还本付息或发放股利、选择并决定投资项目、签订投资协议并执行、投资项目管理、收回投资本息知识点二、业务循环中的主要文件筹资与投资业务循环涉及的主要凭证和记录:1.资本投入的有关凭证、账簿2.举债筹资及其清偿的有关凭证、账簿3.盈余公积的有关文件与记录4.投资的文件和记录知识点三、业务循环中的内部控制(掌握P321)1、职责分工(1)筹资、投资决策与执行相互独立;(2)筹资、投资业务执行与记录相互独立:(3)筹资、投资业务执行与内部监督相互独立:(4)财会部门内部对资金的收付、记录、复核相互独立;(5)盈余公积核算、复核由不同人员完成.有关明细账与总账记录分开。

2、信息传递程序控制(1)授权程序——所有的资本交易事项,都必须经过企业最高权力机构的事先审批与授权;最高管理机构制定举债政策及内部批准程序;进行投资时,有正式的授权审批程序;由股东大会或董事会做出利润分配决定;[$STARTSECTION-670584--$$]例题:(2008初)根据筹资和投资循环内部控制要求,可批准股票发行、增资等资本交易事项的是:A.公司的总经理B.公司的财务部门C.公司的审计部门D.公司的最高权力机构答案:D(2)文件和记录的`使用——设计或取得原始凭证、进行明细记录,作为内部控制的重要措施;(3)审核制度——建立审核制度,审查筹资与投资业务3、实物控制实物控制就是要限制非授权人接近实物文件和实物资产,以保证各种实物安全。

审计英语生产与存货循环的审计

审计英语生产与存货循环的审计一、考情分析从专业阶段历年考试情况来看,在往年考试中曾针对该章存货监盘的知识点考查了英语,本章属于重点章节,每年必考,考点具有明显的特征。

尤其是对“存货的监盘”这一知识点的考查,主要以简答题为主。

二、专业词汇生产与存货循环:Production and inventory cycle存货监盘:Supervision of inventory count控制测试:Test of control实质性程序:Substantive procedures检查:Inspect观察:Observe可靠性:Reliability发生:Occurrence完整性:Completeness权利和义务:Rights and obligations认定:Assertions重大错报风险:Risk of material misstatement顺查:Trace逆查:Vouch截止:Cut-off资产负债表日:Balance sheet date盘点日:Counting date调整:Adjustment替代审计程序:Alternative audit procedures存在性:Existence充分的:Sufficient适当的:Appropriate审计证据:Audit evidence无保留意见:Unqualified opinion第三方:Third party受托代存存货:Consigned inventory抵押物:Pledge债权人:Creditor三、重点、难点讲解存货监盘Supervision of inventory taking注册会计师应当实施下列审计程序,对存货的存在和状况获取充分、适当的审计证据:CPA should perform following audit procedures to obtain sufficient appropriate audit evidences related to existence and condition of inventory.(1)账——对期末存货记录实施审计程序,以确定其是否准确反映实际的存货盘点结果。

GJB9001C质量审计程序(含完整表单)

GJB9001C质量审计程序(含完整表单)1.简介本文档旨在介绍GJB9001C质量审计程序及其相关表单。

GJB9001C是中国军用航空产品的质量管理体系要求的标准之一,对于确保产品质量以及制定改进建议具有重要意义。

质量审计程序是执行GJB9001C标准的关键步骤之一,通过审核与评估组织的运作和质量管理体系,发现问题并提出解决方案。

2.GJB9001C质量审计程序步骤2.1 准备在进行质量审计前,需做好准备工作,包括确定审计目标、制定审计计划、组织审计团队和准备审计所需的材料和信息等。

2.2 审核审计包括对组织的运作和质量管理体系的审核与评估。

审计团队将根据GJB9001C标准的要求,对组织的各项指标和流程进行审查。

2.3 发现问题在审核过程中,审计团队将记录发现的问题和不符合GJB9001C标准的情况。

问题可能涉及到组织的流程、产品质量、文件管理等方面。

2.4 提出解决方案根据发现的问题,审计团队将提出相应的改进和解决方案,以符合GJB9001C标准的要求。

解决方案应包括具体的操作指导和改进措施。

2.5 审核结果审计团队将根据评估结果,提供一份审核报告,包括审计发现的问题、提出的解决方案和建议。

此报告将作为后续改进和修正质量管理体系的依据。

3.完整表单以下是GJB9001C质量审计程序相关的完整表单,包括:审计计划表审计记录表非符合项整改措施表审计结果报告表注意:以上表单的具体内容和格式可根据实际情况进行调整和定制。

4.结论GJB9001C质量审计程序是确保军用航空产品质量和提出改进措施的重要步骤。

通过执行审计步骤,组织可以发现问题、提出解决方案,并通过改进和修正质量管理体系来提升产品质量。

本文档提供了GJB9001C质量审计程序的简介以及相关的完整表单,帮助组织有效执行质量审计程序。

人格混同审计申请书

人格混同审计申请书示例1:标题:深入探讨人格混同审计申请书引言:人格混同审计申请书是一种重要的法律文件,它在审计过程中起到关键的作用。

本文旨在深入探讨人格混同审计申请书,探索其定义、重要性和编写要点,以帮助读者更好地理解和运用该申请书。

第一部分:定义人格混同审计申请书解释人格混同审计申请书的概念:人格混同是指在审计工作中,存在因个人利益、职务不当行为等原因导致个人与企业或机构人格混淆的现象。

人格混同审计申请书则是着眼于确定和防止此类行为的一份书面申请。

第二部分:人格混同审计申请书的重要性探讨人格混同审计申请书在审计工作中的重要性:首先,该申请书有助于规范审计工作,防止人格混同的出现;其次,它为审计机构提供了一种手段,以客观地评估审计人员的道德、诚信和独立性。

第三部分:编写人格混同审计申请书的要点介绍编写人格混同审计申请书的关键要点:包括明确申请书的目的和用途、详细描述人格混同的可能风险和影响、列出防范措施和建议、注明申请人的个人背景和资格、附上必要的证明材料等。

第四部分:案例分析和实际应用通过案例分析,探讨人格混同审计申请书在实际应用中的作用和效果:选取一个真实的案例,解释该案例中人格混同的情况,并探讨申请书对发现和防止此类问题的影响。

结论:通过对人格混同审计申请书的深入探讨,我们认识到它在审计工作中的重要性和作用。

正确编写和使用人格混同审计申请书,可有效预防和解决人格混同问题,维护审计的独立性和公正性。

同时,申请书也应不断完善和更新,以适应不断变化的审计环境。

示例2:人格混同审计申请书是一种重要的法律文件,旨在申请对某个公司或组织进行人格混同审计。

人格混同审计是一种统计方法,用于评估某个实体是否存在人格混同,即在不同身份之间混淆使用相同的个人或法人实体。

尊敬的审计委员会:我写信是为了申请对(公司/组织名称)进行人格混同审计。

此次申请是基于以下几点考虑:首先,在本次审计之前,根据我们的初步调查,我们发现了一些可能存在的人格混同的迹象。

C语言中的安全代码审计工具与平台

C语言中的安全代码审计工具与平台随着计算机科学的发展,软件安全越来越受到重视。

在软件开发过程中,漏洞和错误的存在可能会导致潜在的安全隐患,而这些问题往往可以通过代码审计来发现和解决。

C语言作为一种广泛应用于系统开发和嵌入式设备的编程语言,其安全代码审计工具和平台的发展也越发重要。

一、什么是安全代码审计工具?安全代码审计工具是指一类软件工具,用于检测源代码中潜在安全问题的存在。

这些工具通过对代码进行静态分析、漏洞扫描等方式,识别并报告代码中的漏洞、弱点和不安全的编码实践。

安全代码审计工具可以帮助开发人员在代码层面上发现并修复潜在的安全漏洞,提升代码的安全性和可靠性。

二、C语言中的安全代码审计工具有哪些?1. CppcheckCppcheck是一个开源的C/C++代码静态分析工具,主要用于检测代码中的潜在错误和安全问题,如缓冲区溢出、空指针解引用等。

Cppcheck提供了一个命令行界面和集成开发环境插件,方便开发人员在开发过程中进行静态代码分析。

2. Clang Static AnalyzerClang Static Analyzer是一个基于LLVM的C/C++静态代码分析工具,用于发现源代码中的各种常见错误、内存泄漏、空指针引用等问题。

Clang Static Analyzer提供了一个命令行工具和集成开发环境插件,可以快速检测和修复代码中的安全问题。

3. CodeSonarCodeSonar是一款商业化的静态分析工具,可用于发现C和C++代码中的内存泄漏、数据竞争、空指针引用等问题。

CodeSonar通过对代码进行深入分析,并生成详细的报告,帮助开发人员快速定位和解决安全问题。

4. CoverityCoverity是一种广泛应用的静态代码分析工具,用于发现各种语言中的安全漏洞。

对于C语言而言,Coverity可以检测和修复内存泄漏、缓冲区溢出、空指针解引用等问题。

Coverity支持多种集成开发环境和持续集成工具,方便开发人员在日常开发中使用。

C语言代码审计与安全评估

C语言代码审计与安全评估随着计算机技术的不断发展,软件安全问题成为了一个日益严重的挑战。

在软件开发过程中,C语言作为一种常用的编程语言,其代码审计与安全评估显得尤为重要。

本文将探讨C语言代码审计的必要性,以及如何进行安全评估。

一、C语言代码审计的重要性C语言作为一门底层语言,广泛应用于系统开发、嵌入式设备等领域。

然而,C语言的特性也为代码的安全性带来了潜在威胁。

不合理的内存操作、缓冲区溢出、代码注入等问题经常被黑客利用,导致系统被攻击。

因此,对C语言代码进行审计,尽早发现和修复潜在的安全漏洞,对保障软件系统的安全运行至关重要。

二、C语言代码审计的流程C语言代码审计主要涵盖以下几个步骤:1. 静态代码分析通过工具对C语言代码进行静态分析,识别可能存在的安全问题。

常用的静态分析工具有Coverity、Clang等,它们能够检测出内存泄漏、空指针解引用、非法内存访问等问题。

2. 动态代码分析通过代码运行时的动态分析,模拟攻击场景,发现代码的安全漏洞。

动态分析工具可以检测到安全漏洞,如缓冲区溢出、代码注入等。

常见的动态分析工具有Valgrind、GDB等。

3. 代码漏洞修复在代码审计的过程中,发现存在安全漏洞的代码需要及时修复。

修复漏洞的方式多种多样,例如增加边界检查、改进内存分配方式等。

修复后,需要进行功能测试和安全测试,确保修复的代码没有引入新的问题。

三、C语言代码安全评估的方法C语言代码的安全评估不仅包括审计代码中的潜在问题,还需对系统的整体安全性进行评估。

以下是一些常用的安全评估方法:1. 漏洞扫描漏洞扫描是一种常见且有效的安全评估方法。

通过使用扫描工具,对系统进行全面的漏洞检测,如SQL注入、跨站脚本攻击等。

扫描结果能够帮助开发人员及时了解系统的安全状况,并采取相应的措施进行修复。

2. 安全渗透测试安全渗透测试是一种模拟真实黑客攻击的评估方法。

通过合法的方式,对系统进行渗透测试,发现系统中可能存在的漏洞和安全隐患。

C语言中的安全日志记录与审计

C语言中的安全日志记录与审计在计算机安全领域中,安全日志记录和审计是至关重要的措施,有效地保护系统免受潜在威胁。

C语言作为一种广泛应用的编程语言,也具备了一些用于安全日志记录和审计的功能和特性。

本文将介绍C 语言中的安全日志记录与审计的相关内容,并探讨如何在C语言项目中应用这些技术。

1. 安全日志记录的重要性在一个复杂的计算机系统中,安全日志记录可以提供关键的信息用于检测和响应潜在的安全事件。

通过记录事件的时间、类型、源IP、目的IP等信息,可以帮助管理员追踪和分析恶意行为,并及时采取相应的措施。

安全日志记录还可以用于法律调查和取证,为确认安全事件的发生和追踪攻击者的行踪提供重要的依据。

2. C语言中的安全日志记录在C语言中,可以使用标准库中的文件操作函数来实现安全日志记录。

通过使用fopen()打开一个文件,并使用fprintf()函数将日志信息写入文件中,可以方便地实现日志的记录。

在编写日志时,应该包含足够的信息来描述事件,同时还需要注意日志的格式和结构化,以便后续的审计分析。

下面是一个简单的示例代码,用于在C语言中实现安全日志记录:```c#include <stdio.h>#include <time.h>void writeLog(const char* message) {FILE* logFile = fopen("security.log", "a");if (logFile == NULL) {printf("Failed to open log file.\n");return;}time_t now = time(NULL);struct tm* ts = localtime(&now);fprintf(logFile, "%04d-%02d-%02d %02d:%02d:%02d - %s\n", ts->tm_year+1900, ts->tm_mon+1, ts->tm_mday,ts->tm_hour, ts->tm_min, ts->tm_sec, message);fclose(logFile);}int main() {// 一些操作writeLog("User logged in successfully.");// 一些其他操作writeLog("Access denied for unauthorized user.");return 0;}```以上代码中,writeLog()函数用于将指定的信息写入security.log文件中。

cpas审计信息系统工作底稿

cpas审计信息系统工作底稿

一、调查

该审计步骤用来将控制目标下的相关活动用文档记录下来,对组织声称已实施的控制措施与程序进行识别,并且确认其存在。

与相关的管理者和员工进行会见以理解。

用文档记录与过程相关的IT资源,特别是那些被审计的IT流程所影响的IT资源。

确认理解了审核的过程、过程的关键性能指标(KPI)、实际的控制状况。

例如,可以通过对过程的抽查来进行了解。

二、评价控制

该审计步骤用来评估当前已有控制措施的有效性或达到控制目标的程度,主要是决定测试什么、是否测试及如何测试的问题。

通过对比已确定的标准及行业最佳实践、控制方法的关键成功要素(CSF)和利用审计师的职业判断,来评价待审核过程所应用的控制措施的适宜性。

三、评估符合性

该审计步骤用来确定已建立的控制措施是按组织规定的方式,持续地、一致地在起作用,并且对控制环境的适宜性做出结论。

得到所选项目和阶段的直接或间接的证据,使用直接和间接的证据来保证待审核的项目和阶段一直遵守相关控制程序的要求。

对过程输出结果的充分性进行有限的审核。

为了证明IT流程是分的,确定需要进行实质性测试的程度和其

他需要进行的工作。

四、证实风险

该审计步骤通过使用分析技术和可选的咨询资源,证实控制目标没有被实现时所带来的风险。

目标是支持其审计判断,并督促管理者采取行动。

审计师要创造性地寻找和提出通常是敏感的和机密的信息。

用文档记录下控制弱点及其引起的威胁和漏洞。

识别并记录实际的影响和潜在的影响,例如,利用因果分析的方法。

提供比较信息。

例如,通过基准比较的方法。

审计cpas实验总结

审计cpas实验总结实验目的:审计学是一门会计学专业综合性应用性较强的专业课程,对审计学的教学中辅之以实验教学,对于有效地弥补课堂教学之不足,提高学生对审计工作实务的理解和操作能力。

审计业务实验主要目的是:借助审计实验室环境的仿真性和实验资料的真实性模拟CPA审计工作实务流程,完成从业务谈判、了解被审计单位及其环境并评估审计风险、针对重大错报风险实施进一步审计程序、结束审计工作等审计的全过程,进一步提高学生分析问题和解决问题的综合能力,为毕业后尽快适应实际工作打下良好的基础。

实验要求:1、了解实验项目的,认真阅读教材和实验指导书,做好预习;2、理解实验项目的操作原理;3、掌握实验项目的业务处理。

实验内容:1、审计业务的承接。

与客户的业务委托人商谈,询问相关问题,了解客户;针对客户所在的行业和客户自身的情况进行审计风险分析,以决定是否承接业务;讨论审计收费与付款方式;告知客户的会计责任及应协助的工作;签订审计业务约定书。

2、编制审计计划。

组成审计小组;开展初步业务活动;确定审计重要性和审计风险;编制审计计划(总体审计策略和具体审计计划),进行审计前培训。

3、编制工作底稿。

分小组按不同的审计程序设计不同的工作底稿,如存货盘点表、内部控制调查表、现金盘点表、试算平衡表。

掌握审计工作底稿的要素及编制审核的要4、重大错报风险的评估。

由教师设计内部控制案例,模拟企业的供应、生产、销售各环节的业务活动。

由学生分小组讨论企业存在的重大错报风险。

5、执行进一步审计程序。

根据重大错报风险进行控制测试和实质性程序。

运用询问、观察、检查和穿行测试程序对内部控制进行测试。

掌握存货监盘、应收账款函证等实质性程序。

6、分析程序。

从网上搜索上市公司年度财务报表,由学生采用比较分析、比率分析等方法发现异常报表项目和波动情况。

7、报表循环审计。

利用会计实验课程的学生编制的凭证、账簿、报表,运用基本的审计程序进行审计。

采用分组的形式,按销售与收款循环、采购与付款循环、存货与仓储循环、投资与融资循环进行分组实验。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Reporting1.Unmodified audit report1)Title: so users know this is the report of an independent auditor.2)Addressee: to identify who the report is being written to. These are the peoplewho can place reliance on the report.3)Introductory paragraph: to confirm:a)Which entity is being auditedb)That the financial statements have been auditedc)What the financial statements actually are—normally by stating their titlessuch as Income Statement and Statement of Financial Positiond)Which accounting policies have been used to prepare the financialstatementse)The accounting period covered by the financial statements being audited.In other words the user now knows which parts of a company report have been audited.4)Management’s responsibility for financial statements: to let the readers of thefinancial statements know that it is management who:●Are responsible for the preparation of the financial statements( includingensuring compliance with the relevant reporting framework), and●Establish the internal control system to ensure that the financialstatements are free from material misstatement.5)Auditor’s responsibility: to give information about the work of the auditor inauditing the financial statements. Specifically:●ISAs were used—not just the standards the auditor thought were relevant●The auditor has complied with ethical standards—so the audit wascarried out ―professionally‖●That audit work was planned to try to ensure the financial statements arefree from material misstatement—in other words immaterial errors maystill be there.6)Auditor’s opinion: the important part of the report—this is the auditor’sprofessional opinion on whether the financial statements give a true and fair view in accordance with the relevant financial reporting framework.The opinion has to be there so users of the financial statements know whether or not those statements are basically ‖correct‖.7)Other reporting responsibilities: many jurisdictions have other reportingrequirements—the auditor must also comply with these. For example, in the United Kingdom there is the requirement to comply with the requirements of the Companies Act 2006.8)Signature of the auditor: So users know who has actually carried out the audit.The signature is either that of the auditor or the audit firm that the engagement partner works for.9)Date of the auditor’s report: The date shows when the report was signed.However, the date will be not be earlier than the date the directors sign the financial statements—it is only at this time that the directors formally take responsibility for the financial statements.10)Auditor’s address: this is the location—normally the city—where the auditorworks—so the auditor can be traced if necessary. For example to resolve a query on the financial statements.Unmodified audit reports: elements•Title –independent auditor’s report•Addressee –usually the shareholders•Introductory Paragraph –identifying the information audited•Management’s Responsibility –preparation of financial statements •Auditor’s Responsibility –explanation of duties, & what can be expected of opinion•Auditor’s Opinion –reflecting statutory obligations•Other Reporting Responsibilities –dependent on jurisdiction•Signature –of senior statutory auditor (UK) or firm•Date –as near to approval of financial statements as possible•Address –of auditor’s office.•To what extent does an unmodified audit report address the issue of the expectations gap?•Audit reports have varied in length over time –from short-form (introductory paragraph & opinion) to long-form (as currently).•The long-form report evolved as a response to concerns over the expectation gap –by communicating more information about thenature of an audit regulators hoped to reduce the expectations gap.•Success seems to have been limited – academic research indicates that the existence of the opinion & the reputation of the auditor, rather than the wording of the report, is of concern to users.•Regulators continue to consider the appropriate wording.Unmodified, but with “emphasis of matter” or “other matter”paragraph•The ―emphasis of matter‖ or ―other matter‖ paragraph will be shown after the opinion paragraph•Required for:• A matter, although appropriately presented or disclosed in the financial statements, that is of such importance that it isfundamental to users’ understanding of the financialstatements; or•Any other matter that is relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report. Describes the matter to be brought to the attention of addressee and the possible effect on financial statements, quantified where possible Modified audit reports:Three types:1.Pervasive effects on the financial statements are those that, in the auditor’s judgment:i.Are not confined to specific elements, accounts or items of thefinancial statements;ii.If so confined, represent or could represent a substantial proportion of the financial statements; orIn relation to disclosures, are fundamental to users’ understanding of the financial statements2. Inability to obtain evidenceMay arise from:a)Circumstances beyond the control of the entity;b)Circumstances relating to the nature or timing of the auditor’s work;orc)Limitations imposed by management.d)Auditor should not accept an engagement where managementimpose a limitation on the scope of the auditor’s work likely to result in a disclaimere)If a limitation is imposed after the engagement is accepted theauditor should consider resigningf)Where a limitation in scope requires modification the report shoulddescribe the limitation and indicate necessary adjustmentsg)In the UK, a limitation will require some ―by exception‖ reporting3.Financial Statements are materially misstatedMaterial misstatements may arise in relation to:a)Appropriateness of selected accounting policiesb)Application of selected accounting policiesc)Appropriateness or adequacy of disclosures in the financialstatements.。