案例4--Warren E. Buffet

英文市场营销案例Warren-Buffett

Warren BuffettWarren Buffett (born August 30,1930) is a US investor, businessman, and philanthropist. He is one of the most successful investors in history, the largest shareholder and C.E.O. of Berkshire Hathaway, and in 2008 was ranked by Forbes as the richest person in the world with an estimated net worth of approximately $62 billion.Buffett is often called the “Oracle of Omaha” or the “Sage of Omaha”and is noted for his adherence to the value investing philosophy and for his personal frugality despite his immense wealth. Despite his overall frugality, he flies in a corporate jet named the Indefensible.Buffett is also a notable philanthropist, having pledged to give away 85 percent of his fortune to the Gates Foundation. He also serves as a member of the board of trustees at Grinnell College.In 1999, Buffett was named the top money manager of the twentieth century in a survey by the Carson Group, ahead of Peter Lynch and John Templeton. In 2007, he was listed among Time’s 100 Most Influential People in the world.He worked at his grandfather’s grocery store. In 1943, Buffett filed his first income tax return, deducting his bicycle and watch as a work expense for $35 for his work as newspaper delivery boy. After his father was elected to Congress, Buffett was educated at Woodrow Wilson High School, Washington, D.C. In 1945, in his freshman year of high school, Buffett and afriend spent $25 to purchase a used pinball machine, which they placed in a barber shop. Within months, they owned three machines in different locations.Buffett first enrolled at The Wharton School, University of Pennsylvania,(1947-49) where he joined the Alpha Sigma Phi Fraternity. In 1950, he transferred to the University of Nebraska where he received a B.S. in Economics. Buffett then enrolled at Columbia Business School after learning that Benjamin Graham,(the author of The Intelligent Investor),and David Dodd, two well-known securities analysts, taught there. He then received a M.S. in Economics from Columbia University in 1951.In Buffett’s own words: I’m 15 percent Fisher and 85 percent Benjamin Graham.The basic ideas of investing are to look at stocks as business, use the market’s fluctuations to your advantage, and seek a margin of safety. That’s what Ben Graham taught us. A hundred years from now they will still be the cornerstones of investing.At only six years old, Buffett purchased 6-packs of Coca Cola from his grandfather’s grocery store for twenty five cents and resold each of the bottles for a nickel, pocketing a five cent profit. While other children his age were playing hopscotch and jacks, Warren was making money. Five years later, Buffett took his step into the world of high finance. At eleven years old, he purchased three shares of Cities Service Preferred at $38 per share forboth himself and his older sister, Doris. Shortly after buying the stock, it fell to just over $27 per share. A frightened but resilient Warren held his shares until they rebounded to $40. He promptly sold them a mistake he would soon come to regret. Cities Service shot up to $200. The experience taught him one of the basic lessons of investing: patience is a virtue.By the late’70s, his reputation had grown to the point that the rumor Warren Buffett was buying a stock was enough to shoot its price up 10%. The irony was that Warren Buffett never sold a single share of his company, meaning his entire available cash was the $50000 salary he received. During this time, he made a comment to a broker, “Everything I got is tied up in Berkshire. I’d like a few nickels outside.”。

可口可乐饮品营销策划案经典营销策划方案案例

可口可乐饮品营销策划案经典营销策划方案案例文稿归稿存档编号:[KKUY-KKIO69-OTM243-OLUI129-G00I-FDQS58-2016年04月可口可乐营销策划案目录第一章摘要 (3)第二章公司介绍 (3)宗旨 (3)公司简介 (4)产品及服务 (4)价值评估 (5)公司管理 (5)组织,协作及对外关系 (6)知识产权策略 (6)风险 (7)第三章市场分析 (7)市场介绍 (7)产品及目标市场 (7)顾客购买准则 (9)销售策略 (9)市场份额或渗透率 (9)第四章竞争性分析 (10)一、可口可乐与百事可乐的对比分析 (10)二、竞争策略与行业壁垒 (15)第五章产品与服务 (16)一、产品品种规划 (16)二、包装 (16)三、服务 (16)第六章市场与销售 (17)一、市场计划 (17)二、销售策略 (17)三、销售渠道与伙伴 (18)四、销售周期 (20)五、定价策略 (20)六、市场联络 (21)第一章摘要可口可乐公司作为一家世界闻名的饮料公司,在生产销售方面有其独特的精髓,而它与百事可乐的竞争也是人们关注的焦点。

所以我们在这份策划中,将对可口可乐的优势和不足进行客观的分析,然后加上我们独巨匠心的观点,希望能为其他公司提供有效的参考。

第二章:公司介绍一、宗旨(任务)可口可乐公司宗旨:让可口可乐成为全球最大饮料制造商,追求最大利润,积极回馈社会,形成双赢的局面,建立可乐帝国。

使命陈述:因应社会的快速转变,追求速度与新鲜感,电视广告不断推陈出新,跟着时下年轻人的脚步走,让人有挡不住的感觉,觉得喝可口可乐就是跟着潮流走。

让收集可口可乐相关的产品是一种流行的象征。

二、公司简介可口可乐公司 (Coca-Cola Company)成立于1892年,公司总部设在美国亚特兰大。

1960年进入美国最大的100家工业公司的行列;1983年居第48位。

1960-1983年,该公司的销售额、资产额和净收入的年均增长率分别为12.2%、11.5%和12.3%。

warren buffett

• Buffett's fortune dream began from the age of 5, but he did not take money as the ultimate goal. He likes looking at money increase in the number, but by no means eager for money.

• In June 2006, he announced a plan to give away his fortune to charity, with 83% of it going to the Bill & Melinda Gates Foundaemporaries-richest man in history such as oil Baron Rockefeller, steel Baron Andrew Carnegie, and software King Bill Gates later, Warren Buffett is outstanding. As other people's wealth all came from a product or an invention, but Buffett is a purely investor.

• Even as a child, Buffett displayed an interest in making and saving money.

He went door to door selling chewing gum, Coca-Cola, or

weekly magazines. For a while, he worked in his grandfather's grocery store. While still in high school he was successful in making money by delivering newspapers, selling golfballs and stamps, and detailing cars, among other means.

srdc交易办法初级教程

现在来做: 1)回头测试尽可能多的 k 线,最少 20 个 2)对于每次交易,研究其点数(minus spread) 3)多少 k 线能差出最少 5 个点数? 4)多少 k 线能差出多于 10 个点数? 5)多少 k 线之间能差出少于 5 个点数? 现在你有了答案。兴奋么?应该的! 怎么用这个方法来交易呢? 准备工作 在新的日 k 线开始的时候: 1)画支撑位 2)画阻力位 拜托请在前一天的 k 线上画。。。。。 画出趋势线并且判断趋势。这样,你就可以预期价格会向哪里运行。或者向着支撑位,或者 阻力位。

设置趋势,画 channel (筛选)

15mins chart 这部分可能对场景二比场景三更重要. 这是一个用 SRDC 方法来应用移动平均线的介绍。对 我们来说,移动平均线(MA)是最简单得阻力和支撑位。恰当的 MA 区间可以成为一个好 地趋势设置指示。这里有很多我们可以用得,为了简单,我们用 84SMA. 实际上我们用 84SMA 来画轨道. 轨道的开始和末端由蜡烛相对 84SMA 得开始位置 (00:00GMT)决定。 当初始位置> 84SMA 趋势向上 当初始位置< 84SMA 趋势向下 用这个 trendsetter 可以决定是否开始交易,你可能会错过很多好的单子,但是很快你就会掌 握,你会最终学会避免很多坏单现在的趋势画成轨道,除非一个趋势延续连续超过三天,否则化轨道的时候 一定要包含前一个趋势(trend,不知道这个词翻得对不对)

可以同时作两个方向的交易么? 当然。但是箱体最好在轨道的中部,方向偏离得越大,获利可能性就越大。 消息呢?从我的经验来看,当我在交易的时候,在通告出来 1 分钟前,我通常设置 stop loss 成 breakeven。但如果你没有在交易,记住这句话, “轨道比消息强”. 止损(SL) 价值一百万美金的问题,最好的止损点在那里? 三个方法设置你得止损点 箱体大小:箱体能覆盖到所有 whipsaw,当箱体变太大的时候,它可能会吓到我邻居的狮 子。 这个是 GBPUSD 对吧? 所以,50 点 是最安全的。 15 分钟图上的 84SMA 或者 一小时的 21SMA 就是这样。 还有很多方法来交易。但是,我认为现在的解释足够了。我希望这个能加强你对其他 SRDC 的交易。 对 SRDC 质疑或者不满的, 我建议你把意见留到别处,回家和老婆说去。不要在这个帖子 里讲,因为我们对你愚蠢的思想不感兴趣。 我提前说这些因为我 100%讨厌怀疑者。我在这里免费教大家以及分享我的经验,我不是在 受审,你才是! 所以,丢掉你的自傲,趁我还在免费降解的时候开始学习。 责任?交易是你自己的,所以你要对你自己负责,而不是我。 其余的,我等着你们用 SRDC 成功和开心的交易! 我爱你们!

Buffet案例

1.Would the PacifiCorp acquisition serve the long-term goals of Berkshire Hathaway? PacifiCorpis a major player in the quickly expanding western region, particularly Utah, one of the fastest-growing states. Utah's rising population is boosting power demand by 4% a year. That's a huge growth opportunity for MidAmerican. Plus, PacifiCorp is one of the industry's low-cost energy providers. The acquisition will bring the revenue of $10billion a year and the power generation capacity of 16,000 watts to MidAmerican, which can supply 1,280 households. Therefore, the PacifiCorp acquisition serves the long-term goals of Berkshire Hathaway.2.Was the bid price appropriate?Based on the multiples for comparable regulated utilities, we can see that the range of possible enterprise values for PacifiCorp is from $6.252 billion to $9.289 billion and the range of possible market value of equity is from $4.277 billion to $5.904 billion. In this case, Berkshire used $9.4 billion to acquire the electric utility PacifiCorp. This price is out of the range neither of possible enterprise value nor of possible market value.A very obvious question is raised here-why Berkshire was willing to purchase PacifiCorp at such high price? Buffet defined intrinsic value as the discounted value of the cash that can be takenout of a business during its remaining life. But the intrinsic value is difficult to calculate. The valuation method of comparable companies in this case measures the cost rather than the future earning because of the use of historical data. In addition, in Buffet’s point of view, Berkshire might have a good development and future after its takeover of PacifiCorp. The intrinsic value of PacifiCorpcould be more valuable than its cost. So the bid price was appropriate.3.How did Berkshire’s offer measure up against the company’s valuation implied by themultiples for comparable firms?Since PacifiCorp is a privately held company that does not pay a dividend, the dividend discount model cannot be used.An implied valuation using multiples from comparable regulated utilities is applied then.In the case, Exhibit 9 reveals some financial data for the PacifiCorp and Exhibit 10 demonstrates the implied valuation for PacifiCorp using average and median of the company. 1)Enterprise Value Multiple = Enterprise Value / Rev or EBIT or EBITDA or Net Income ofComparable CompaniesImplied value of PacifiCorp = The medium or mean of Enterprise Value Multiples* Rev or EBIT or EBITDA or Net Income of PacifiCorp2)MV Equity Multiple = MV Equity/EPS or Book Value of Comparable CompaniesImplied value of PacifiCorp = The medium or mean of MV Equity Multiples* EPS or Book Value of PacifiCorp4.What might account for the share price increase for Berkshire Hathaway at the announcement? The stock market reaction to the PacifiCorp acquisition by Berkshire Hathaway appears to portray the deal as a win-win situation, creating value for both companies.Under acquisition accounting, the $2.55 billion increase in market value of Berkshire Hathaway is the increase in goodwill of the company.The reasons are listed below.●Buffet expected that PacifiCorp would have good future earnings and could enhance theperformance of Berkshireas well. The acquisition boosted the confidence of investors.Moreover, the market was optimistic about the purchase.●The stock performance of Berkshire underperformed S&P 500 Index while the ScottishPower outperformed the index.。

新视野大学英语听说教程4答案(含Culture_talk_和Homework)

新视野大学英语4听说教程答案Unit OneWarming UpF T NGListeningUnderstanding Short Conversations1~5 A C B B D6~10 B A C C DUnderstanding a Long Conversation1~5 A B A C BUnderstanding a Passage1~5 A A D B CUndenstanding a Radio Program1 married in ST.Paul’s Cathedral2 was a guest at the wedding ceremory3 wore a hat with flowers at the wedding4 is remmembered as having been naughty5 was one of the designers of the wedding dressCulture TalkT F F TListening and Speaking1 They have high status.2 They get the attentions of the public.3 Using their fame to make money.HomeworkSupplementary ListeningTask 11~5 D A B B ATask 21~5 C A B B ATask 31、shortage2、assigned3、centered4、hospitallization5、treatment6、colleague7、decentialized8、There’re nurse-managers instead of head-nurses9、decidea among themselves who will work what to do and when10、an equal with other wise presidents of the hospitalUnit TwoWarming Up1、Her new book2、Original3、Use your own words to complete it,this question has no correct answers. ListeningUnderstanding Short Conversations1~5 D D D C B6~10 A A B C DUnderstanding a Long Conversation1~5 D A B B AUnderstanding a Passage1~5 B C D A CUndenstanding a Radio Program1 C2 A3 A4 C5 DCulture TalkF F T TListening and Speaking1(The Left Answer) It makes their point and makes you happy.2(The Right Answer) It is difficult to do.3(The Right Answer) Sometimes it’s dangerous.HomeworkSupplementary ListeningTask 11~5 D A B B ATask 21~5 B D A C ATask 31、sketch2、shadow3、paintings4、abroad5、Europe6、jewels7、exqute8、pictures of rooms with handsome dressed people in them9、not only the clothes and the lines of their faces10、but he was far greater than he would ever becomeUnit ThreeWarming Up1、god of mercy2、money,strength and health3、lucky onesListeningUnderstanding Short Conversations1~5 C D C B B6~10 B A C A BUnderstanding a Long Conversation1~5 A B D C BUnderstanding a Passage1~5 A B D B CUndenstanding a Radio Program1 An Australian scientist who won the Nobel Prize.2 The mysterious field of infectious diseases.3 By accident.4 It was probably extremely significant.5 He couldn't handle all that.Culture TalkT F T TListening and Speaking1 The poor trend to be angry easily and it will fanilly make a civil war.2 It can control the rate og crimes3 It can increase the econimicsHomeworkSupplementary ListeningTask 11~5 B C A D CTask 21~5 B A C B CTask 31、September2、retire3、retirement4、reduction5、practical6、pensions7、leisure8、The club arranges discussion groups and handicraft sessions9、a member can attend any course held there free of charge10、the financial section on Mondays and Wednesdays between six and eight p.m.Unit FourWarming Up1、Xerox’s Palo Alto Re search Center2、Verizon3、AmazonListeningUnderstanding Short Conversations1~5 B A D D A6~10 D C C A AUnderstanding a Long Conversation1~5 C B B B CUnderstanding a Passage1~5 A C B A CUndenstanding a Radio Program1 became Bill Gates' greatest contribution2 makes use of Gates' system3 was the plaything of nerds4 became a business tool5 made it a wish to dominate like Bill Gates6 was not fit to comment on upcoming innovationCulture TalkT T F FListening and Speaking1(The Left Answer) It provides a lot of information.2(The Right Answer) Some of the information is very dangerous.3(The Right Answer) Some of the information is not accurate.HomeworkSupplementary ListeningTask 11~5 B A B C ATask 21~5 A A B B ATask 31、fundamental2、dramatically3、majority4、workplace5、self-employed6、breadth7、notions8、its applications in personal computers, digital communications, and factory robots9、still unimagined technology could produce a similar wave of dramatic changes10、will have the greatest advantage and produce the most wealthUnit FiveWarming UpF NG TListeningUnderstanding Short Conversations1~5 A D D D B6~10 C D C A DUnderstanding a Long Conversation1~5 B B A C CUnderstanding a Passage1~5 D A B B AUndenstanding a Radio Program1 the perfect man checklists2 what the perfect man looks like3 much younger for yourself4 to develop your perfect man checklist5 burning the perfect man checklistCulture Talk1 Korean2 HongKong3 England4 USAListening and Speaking1 It can cause one to be dependent.2 It’s a nuisance.3 It will limit your freedom.HomeworkSupplementary ListeningTask 11~5 C D A B DTask 21~5 A C A C DTask 31、emerging2、residents3、participants4、companionship5、soldiers6、isolate7、extraordinary8、who happened to live by themselves die at twice the rate of those live with others9、It’s clear that reaching out to other can have our body strong10、Only 5 percent of U.S. consisted of the person living alone.Unit SixWarming Up1 Whether the man should return to society.2 15 years.3 Use your own words to complete it,this question has no correct answers. ListeningUnderstanding Short Conversations1~5 C B C D B6~10 C A D D BUnderstanding a Long Conversation1~5 A B C C DUnderstanding a Passage1~5 C D D A BUndenstanding a Radio Program1 Centennial Olympic Park2 North Cardwell,New Jersey3 Oklahoma City,Oklahoma4 the FBI laboratories5 ground zero6 an Atlanta abortion clinicCulture Talk1 USA2 Germany3 Singapore4 CanadaListening and Speaking1(The Left Answer) Punishing the criminals will deter others.2(The Right Answer) It is good for society.3(The Right Answer) It has no victims.HomeworkSupplementary ListeningTask 11~5 D C B A ATask 21~5 C B B A DTask 31、impeach2、scandal3、gambling4、Representatives5、accusations6、procedures7、opposition8、resigned as secretary of social welfare and urged the president to resign9、five economic advices to the President have resigned10、some committees in the House of RepresentativesUnit SevenWarming UpT F NGListeningUnderstanding Short Conversations1~5 B C A A D6~10 C B D A BUnderstanding a Long ConversationUnderstanding a Passage1~5 C C D B BUndenstanding a Radio Program1 shows God’s part in creating the universe.2 shows the existence of a man thousands of years ago.3 shows messages inscribed in DNA.4 shows a court opinion against Intelligent Design.5 shows God’s existence.Culture TalkT T F FListening and Speaking1 Groups are similar biologically except for skin color.2 Groups have different culture3 Groups provide something unique.HomeworkSupplementary ListeningTask 11~5 D D A B BTask 21~5 A C B A DTask 31、would-be2、intelligence3、genes4、athletic5、medical6、disclosed7、consideration8、the sum American egg donors expect to be paid9、plus all the costs of medical treatment and insurance10、almost half the cost of fees for the students’ four-year college course.Unit EightWarming Up1 going to quit2 work harder3 majority raceListeningUnderstanding Short Conversations1~5 C A A B C6~10 D D A C BUnderstanding a Long ConversationUnderstanding a Passage1~5 D A B B AUndenstanding a Radio Program1 Bill Gates2 Warren Buffet3 KP Singh4 Martha Stewart5 Ronald Lauder6 Louisa KrollCulture Talk1 Japan2 UK3 America4 Hong Kong Listening and Speaking1 Society should be fair.2 Women should enjoy representation.3 It makes leaders help to do something for women.HomeworkSupplementary ListeningTask 11~5 A C D B CTask 21~5 A D B B BTask 31、greeted2、freshman3、spite4、fluke5、agitated6、faculty7、particularly8、I had the highest average in the freshman class9、Then, she took out a copy of the examination paper10、I was so angry that I started punding herUnit NineWarming Up1 Whether it’s Chinese enough to appeal to Chinese people2 American culture3 Use your own words to complete it,this question has no correct answersListeningUnderstanding Short Conversations1~5 A C B D C6~10 D A A B CUnderstanding a Long Conversation1~5 D A B B AUnderstanding a Passage1~5 D B B C CUndenstanding a Radio Program1 His brother’s two daughters.2 They drove there.3 Children under three.4 They watched the parade.5 He sat down and had a rest for a few minutes.Culture TalkT T F TListening and Speaking1 Fantastic rides.2 So much to see.3 Great memories never to forget.HomeworkSupplementary ListeningTask 11~5 C B A C DTask 21~5 B A D C BTask 31、Authorities2、grant3、opera4、not traditional5、staged6、journolists7、tunnel8、Great performer is special for new introduction of the story9、who kills all suitors who can answer her three riddles10、Some Chinese audience complain that the princess has none of the grace of a true Chinese ladyUnit TenWarming UpNG T FListeningUnderstanding Short Conversations1~5 D B A C B6~10 B B C B AUnderstanding a Long Conversation1~5 D B C A BUnderstanding a Passage1~5 C B D D AUndenstanding a Radio Program1 is something not known for sure2 is trying to figure out how dreams help in solving problems3 is something everyone should do4 is important in interpreting dreams5 is something a person might be afraid ofCulture TalkT T F TListening and Speaking1 It causes stress.2 What area you may develop.3 High score can bring you confidence.HomeworkSupplementary ListeningTask 11~5 C D C A ATask 21~5 A D C B ATask 31、rarely2、consulting3、renting4、agent5、appointment6、exchange7、praises8、the people who work there actually know where things are and they'll take you right to them9、I will tell you what I really like about Publix10、There's a different grocery store near my house, but all that the employees do there is to grunt。

案例4--Warren E. Buffet

沃伦E.巴菲特1995阅读“沃伦E. 巴菲特”案例,回答下列问题,请注意你可以提出你自己感兴趣的问题,以代替下列问题。

1、在宣布收购的当天,GEICO公司和Berkshire Hathaway公司股票价格变动可能意味着什么?特别是,在Berkshire的市场资产净值中7.18亿美元的利润对GEICO的内在价值意味着什么?(注:在知道消息之前,Berkshire拥有GEICO的33.25百万的股票)2、根据Value Line公司的预测信息,GEICO的可能的内在价值在什么范围内?你对此估计范围有什么疑问?3、Berkshire Hathaway表现的怎么样?在总体上?在对Scott & Fetaer的投资上表现的怎么样?在早期购买GEICO的股票投资上?在可自由兑换的有价证券投资上?4、在沃伦E.巴菲特的观点中,内在价值是什么?为什么受到如此高的重视?它是如何估算的?内在价值的替代方案是什么?并且为什么巴菲特拒绝了它们?5、请客观地评价一下巴菲特的投资理念,并且指明你同意他的哪些观点,不同哪些观点?6、Berkshire的股东应该认可对GEICO的收购活动吗?1995年8月25日,Berkshire Hathaway 公司的CEO沃伦 E.巴菲特宣布他的公司将收购GEICO公司在外边的49.6%的股票份额。

这个23亿美元的交易将支付GEICO的股东们每股70美元,远远高于宣布前的每股市场价格55.75美元。

观测者对Berkshire Hathaway 公司将支付的26%的股票溢价感到吃惊,尤其是巴菲特不打算对GEICO做出任何的改变,而且这两家公司的合并没有明显的协同效应。

在宣布的当天,Berkshire Hathaway 公司股票的收盘价上涨了2.4%,对公司的整个市场价值而言则增加了7.18亿美元1。

在那一天,标准普尔500股价指数的收盘价上涨了0.5%。

对GEICO公司的收购活动使得人们重新认识了投资大师沃伦 E.巴菲特。

Warren Buffet

D. Don't go on brand name; just wear those things in which you feel comfortable. E. Don't waste your money on unnecessary things; just spend on them who really in need rather. F. After all it's your life then why give chance to others to rule our life."

Don't buy more than what you "really need" and encourage your children to do and think the same

JBA

4.He drives his own car everywhere and does not have a driver or security people around him.

There was a one hour interview on CNBC with Warren Buffet, the second richest man who has donated $31 billion to charity. Following are some very interesting aspects of his life

JBA

1.He bought his first share at age 11 and he now regrets that he started too late!

Things were very cheap that time Encourage your children to invest

新视野大学英语第二版第四册听说教程答案(完整版)

新视野大学英语 4 听说教程答案Unit OneWarming UpF T NGListeningUnderstanding Short Conversations1~5A C B B D6~10B A C C DUnderstanding a Long Conversation1~5A B A C BUnderstanding a Passage1~5A A D B CUndenstanding a Radio Program1married in ST.Paul ’ s Cathedral2was a guest at the wedding ceremory3wore a hat with flowers at the wedding4is remmembered as having been naughty5was one of the designers of the weddingdress Culture TalkTFFT Listening andSpeaking1They have high status.2They get the attentions of the public.3Using their fame to make money.HomeworkSupplementaryListening Task 11~5 DABBA Task 21~5 CABBA Task 31、 shortage2、 assigned3、 centered4、 hospitallization5、 treatment6、 colleague7、 decentialized8、 There ’ re nurse-managers instead of head-nurses9、 decidea among themselves who will work what to do and when 10、 an equal with other wise presidents of the hospitalUnit TwoWarming Up1、 Her new book2、 Original3、 Use your own words to complete it,this question has no correct answers. ListeningUnderstanding Short Conversations1~5 D D D C B6~10A A B C DUnderstanding a Long Conversation1~5 D A B B AUnderstanding a Passage1~5B C D A CUndenstanding a Radio Program1 C2 A3 A4 C5 DCulture TalkFFTT Listening andSpeaking1(The Left Answer)It makes their point and makes you happy.2(The Right Answer)It is difficult to do.3(The Right Answer)Sometimes it ’ s dangerous.HomeworkSupplementary ListeningTask 11~5D A B B ATask 21~5B D A C ATask 31、 sketch2、 shadow3、 paintings4、 abroad5、 Europe6、 jewels7、 exqute8、 pictures of rooms with handsome dressed people in them9、 not only the clothes and the lines of their faces10、 but he was far greater than he would ever becomeUnit ThreeWarming Up1、 god of mercy2、 money,strength and health3、 lucky onesListeningUnderstanding Short Conversations1~5 C D C B B6~10B A C A BUnderstanding a Long Conversation1~5A B D C BUnderstanding a Passage1~5A B D B CUndenstanding a Radio Program1An Australian scientist who won the Nobel Prize.2The mysterious field of infectious diseases.3By accident.4It was probably extremely significant.5He couldn't handle all that.Culture TalkT F T TListening and Speaking1The poor trend to be angry easily and it will fanilly make a civil war.2It can control the rate og crimes3It can increase the econimicsHomeworkSupplementary ListeningTask 11~5B C A D CTask 21~5B A C B CTask 31、 September2、 retire3、 retirement4、 reduction5、 practical6、 pensions7、 leisure8、 The club arranges discussion groups and handicraft sessions9、 a member can attend any course held there free of charge10、 the financial section on Mondays and Wednesdays between six and eight p.m.Unit FourWarming Up1、 Xerox ’ s Palo Alto Research Center2、 Verizon3、 AmazonListeningUnderstanding Short Conversations1~5B A D D A6~10 D C C A AUnderstanding a Long Conversation1~5 C B B B DUnderstanding a Passage1~5A C B A CUndenstanding a Radio Program1became Bill Gates' greatest contribution2makes use of Gates' system3was the plaything of nerds4became a business tool5made it a wish to dominate like Bill Gates6was not fit to comment on upcoming innovationCulture TalkTTFF Listening andSpeaking1(The Left Answer)It provides a lot of information.2(The Right Answer)Some of the information is very dangerous.3(The Right Answer)Some of the information is not accurate.HomeworkSupplementary ListeningTask 11~5B A B C ATask 21~5A A B B ATask 31、 fundamental2、 dramatically3、 majority4、 workplace5、 self-employed6、 breadth7、 notions8、 its applications in personal computers, digital communications, and factory robots9、 still unimagined technology could produce a similar wave of dramatic changes10、 will have the greatest advantage and produce the most wealthUnit FiveWarming UpF NG TListeningUnderstanding Short Conversations1~5A D D D B6~10 C D C A DUnderstanding a Long Conversation1~5B B A C CUnderstanding a Passage1~5 D A B B AUndenstanding a Radio Program1the perfect man checklists2what the perfect man looks like3much younger for yourself4to develop your perfect man checklist5burning the perfect manchecklist Culture Talk1Korean2HongKong3England4USAListening and Speaking1It can cause one to be dependent.2It ’ s a nuisance.3It will limit your freedom.HomeworkSupplementaryListening Task 11~5 CDABD Task 21~5 ACACD Task 31、 emerging2、 residents3、 participants4、 companionship5、 soldiers6、 isolate7、 extraordinary8、 who happened to live by themselves die at twice the rate of those live with others 9、 It ’ s clear that reaching out to other can have our body strong10、 Only 5 percent of U.S. consisted of the person living alone.Unit SixWarming Up1Whether the man should return to society.215 years.3Use your own words to complete it,this question has no correct answers. ListeningUnderstanding Short Conversations1~5 C B C D B6~10 C A D D BUnderstanding a Long Conversation1~5A B C C DUnderstanding a Passage1~5 C D D A BUndenstanding a Radio Program1Centennial Olympic Park2North Cardwell,New Jersey3Oklahoma City,Oklahoma4the FBI laboratories5ground zero6an Atlanta abortionclinic Culture Talk1USA2Germany3Singapore4CanadaListening and Speaking1(The Left Answer)Punishing the criminals will deter others.2(The Right Answer)It is good for society.3(The Right Answer)It has no victims.HomeworkSupplementary ListeningTask 11~5D C B A ATask 21~5C B B A DTask 31、 impeach2、 scandal3、 gambling4、 Representatives5、 accusations6、 procedures7、 opposition8、 resigned as secretary of social welfare and urged the president to resign9、 five economic advices to the President have resigned10、 some committees in the House of RepresentativesUnit SevenWarming UpT F NGListeningUnderstanding Short Conversations1~5B C A A D6~10 C B D A BUnderstanding a Long ConversationUnderstanding a Passage1~5 C C D B BUndenstanding a Radio Program1shows God s’part in creating the universe.2shows the existence of a man thousands of years ago.3shows messages inscribed in DNA.4shows a court opinion against Intelligent Design.5shows God ’ s existence.Culture TalkT T F FListening and Speaking1Groups are similar biologically except for skin color.2Groups have different culture3Groups provide something unique.HomeworkSupplementary ListeningTask 11~5 D D A B BTask 21~5A C B A DTask 31、 would-be2、 intelligence3、 genes4、 athletic5、 medical6、 disclosed7、 consideration8、 the sum American egg donors expect to be paid9、 plus all the costs of medical treatment and insurance10、 almost half the cost of fees for the students-year college’coursefour.Unit EightWarming Up1going to quit2work harder3majority raceListeningUnderstanding Short Conversations1~5CAABC6~10 DDACB Understanding aLong ConversationUnderstanding a Passage1~5 D A B B AUndenstanding a Radio Program1Bill Gates2Warren Buffet3KP Singh4Martha Stewart5Ronald Lauder6Louisa KrollCulture Talk1Japan2UK3America4Hong Kong Listening and Speaking1Society should be fair.2Women should enjoy representation.3It makes leaders help to do something for women.HomeworkSupplementaryListening Task 11~5 ACDBC Task 21~5 ADBBB Task 31、 greeted2、 freshman3、 spite4、 fluke5、 agitated6、 faculty7、 particularly8、 I had the highest average in the freshman class9、 Then, she took out a copy of the examination paper10、 I was so angry that I started punding herUnit NineWarming Up1Whether it ’ s Chinese enough to appeal to Chinese people2American culture3Use your own words to complete it,this question has no correct answersListeningUnderstanding Short Conversations1~5ACBDC6~10 DAABC Understanding aLong Conversation1~5DABBAUnderstanding a Passage1~5 D B B C CUndenstanding a Radio Program1His brother’ s two daughters.2They drove there.3Children under three.4They watched the parade.5He sat down and had a rest for a few minutes.Culture TalkTTFT Listening andSpeaking1Fantastic rides.2So much to see.3Great memories never to forget.HomeworkSupplementaryListening Task 11~5 CBACD Task 21~5 BADCB Task 31、 Authorities2、 grant3、 opera4、 not traditional5、 staged6、 journolists7、 tunnel8、 Great performer is special for new introduction of the story9、 who kills all suitors who can answer her three riddles10、Some Chinese audience complain that the princess has none of the grace of a true Chinese ladyUnit TenWarming UpNG T FListeningUnderstanding Short Conversations1~5 D B A C B6~10B B C B AUnderstanding a Long Conversation1~5D B C A BUnderstanding a Passage1~5 C B D D AUndenstanding a Radio Program1is something not known for sure2is trying to figure out how dreams help in solving problems3is something everyone should do4is important in interpreting dreams5is something a person might be afraid ofCulture TalkT T F TListening and Speaking1It causes stress.2What area you may develop.3High score can bring you confidence.HomeworkSupplementaryListening Task 11~5 CDCAA Task 21~5 ADCBA Task 31、 rarely2、 consulting3、 renting4、 agent5、 appointment6、 exchange7、 praises8、 the people who work there actually know where things are and they'll take you right to them9、 I will tell you what I really like about Publix10、 There's a different grocery store near my house, but all that the employees do there is to grunt。

Warren Buffet巴菲特

Early life

• 1956, bought Berkshire Hathaway which was a textile company on the verge of bankruptcy, but under Warren’s arrangement ,the share price rose from $7 to $ 90,000. • 1968, when the stock market looked prosperous, Warren suddenly retreated and sold most of his shares. The next year, the price of each share decreased by about 50%. • 1970~1974, when the stock market was without any vitality, Warren felt excited, because he can buy a large number of cheap stocks. With those cheap stocks, he got a large amount of money. • 1980,with the price of $ 10.96 per share, he bought 7% shares of COCA COLA, 5 years later, the price of per share was 5 times as much as those in1980.

金融圈头像七大门派!

金融圈头像七大门派!高盛首席执行官LloydBlankfein 伯克希尔·哈撒韦公司董事长WarrenBuffet江湖第一大门派,人多势众,高手云集。

虽然该派的社交媒体头像缺乏个性,但森严的气度却是金融圈新人和老大均十分推崇的。

华尔街精英如要在网上出没,以西装革履、表情认真的专业形象示人,绝不会失分,因此加入该派也成了大多数人的选择。

对应国内案例:02. 玩照派门下大V数:23/115,占20%代表人物:宏利与约翰·汉考克资产管理首席经济学家Megan Greene 勃朗特资本对冲基金经理John Hempton玩照派尽管贵为江湖第二大门派,但与工照派相比,信徒人数相差甚远。

因此该派的头像舍弃了肃穆的工作环境,以增加情趣为突破口,着力展现工作之余的个人形象。

不得不说,平易近人的社交媒体也正挖掘着华尔街人的另一面。

对应国内案例:03. 书照派门下大V 数:3/115,占2.6%代表人物:前美联储主席Ben Bernanke 安联首席经济顾问Mohamed El-Erian金融专家出书不是什么新鲜事,但爱书如命,甚至愿把社交媒体头像也留给自己著作封面的就很少了。

Bernanke头像中的回忆录《行动的勇气》,描述了美国政府与金融监管机构应对2008年大衰退的过程。

而被Mohamed El-Erian用作头像的《唯一的选择》,同样以这次危机为切入点,解释了中央银行在期间的成功与失误。

由此看来,金融危机的难忘或许是该门派人士的最大共通点。

Nick Firoozye,野村国际总经理的著作Managing Uncertainty, Mitigating Risk:Tackling the Unknown in Financial Risk Assessment and DecisionMaking对应国内案例:小编一时没有找到,欢迎大家留言提供线索!04. 家照派门下大V数:3/115,占2.6%代表人物:中国问题专家Bill Bishop 瑞索尔兹财富管理公司首席执行官Joshua Brown当你有了儿女,他们就会成为你生活的中心。

Warrent

Warrent Buffet 先⽣的投资经营思想-16条Warrent Buffet(巴菲特)在University of Florida商学院(佛罗⾥达⼤学)演讲闪烁着慈祥和智慧的光芒。

下⾯的16段原话,读起来真的是妙趣横⽣,受益匪浅。

1、当你下赌注时,可能会选择那个你最有认同感的⼈,那个最有领导才能的⼈,那个能实现他⼈利益的⼈,那个慷慨,诚实,即使是他⾃⼰的主意,也会把功劳分予他⼈的⼈。

2、不要做低回报率的⽣意。

时间是好⽣意的朋友,却是坏⽣意的敌⼈。

如果你陷在糟糕的⽣意⾥太久的话,你的结果也⼀定会糟糕,即使你的买⼊价很便宜。

如果你在⼀桩好⽣意⾥,即使你开始多付了⼀点额外的成本,如果你做的⾜够久的话,你的回报⼀定是可观的。

3、⽤对你重要的东西去冒险赢得对你并不重要的东西,简直⽆可理喻,即使你成功的概率是100⽐1,或1000⽐1。

4、抛开其他因素,如果你单纯的⾼兴做⼀项⼯作,那么那就是你应该做的⼯作。

你会学到很多东西,⼯作起来也会觉得有⽆穷的乐趣。

5、我给那些公司经理⼈的要求就是,让城墙更厚些,保护好它,拒竞争者于墙外。

你可以通过服务,产品质量,价钱,成本,专利,地理位置来达到⽬的。

6、我要找的⽣意就是简单,容易理解,经济上⾏得通,诚实,能⼲的管理层。

这样,我就能看清这个企业10年的⼤⽅向。

如果我做不到这⼀点,我是不会买的。

基本上来讲,我只会买那些,即使纽约证交所从明天起关门五年,我也很乐于拥有的股票。

如果我买个农场,即使五年内我不知道它的价格,但只要农场运转正常,我就⾼兴。

如果我买个公寓群,只要它们能租出去,带来预计的回报,我也⼀样⾼兴。

7、⼈们买股票,根据第⼆天早上股票价格的涨跌,决定他们的投资是否正确,这简直是扯淡。

正如格雷厄姆所说的,你要买的是企业的⼀部分⽣意。

这是格雷厄姆教给我的最基本最核⼼的策略。

你买的不是股票,你买的是⼀部分企业⽣意。

企业好,你的投资就好,只要你的买⼊价格不是太离谱。

EssaysOfWarrenBuffet

EssaysOfWarrenBuffetThe Essays of Warren BuffetLessons for Investors and ManagersSelected, Arranged and Introduced byLawrence A. CunninghamJohn Wiley & Sons, 264 pagesRating: 8This is as near as you will get to a book “by” Warren Buffet, and for this reason more than any other, it is the best of the Buffet book bunch. Buffett has not actually written or published any book on investment, and all the other books are based upon insights gathered from his corporate essays/letters reported in the Berkshire Hathaway (BH) annual report (see below) or from discussing investment with him and learning from his ways. What makes this book so good, is that there is very little comment or interpretation – this is pure Buffett which has been “selected and arranged” from his many essays. Therefore, it is hardly surprising that, even with his genuine modesty, Buffet says that “If I were to pick one (Buffett) book to read, this would be the one”.Cunningham is Director of the Centre of Corporate Governance and Professor of Law at the Cardoza Law School, New York City; another example of how much closer law and finance co-exist as disciplines in the US. The origin of the book (I read the revised 2002 edn) is a symposium held at Cardoza featuring this compendium of Buffett’s letters – which was attended by Buffett and his “partner” and BH Vice Chairman, Charlie Munger – another lawyer!If you have read no other work on Buffett, you can safely start with this work and get right into it, beginning with the foundations of investment through the principles laid out by Ben Graham and David Dodd, who themselves taught Buffett. Don’t be concerned that some essays are a little old hat, in that some text goes back to the late seventies (all yearly references in the footnotes). Reason: Buffet pulls apart and denounces many of the modern theories of finance/investment and illustrates why the basic principles espoused by Graham and Dodd are superior to modern financial theory. Examples: compensation through stock options (Buffett is winning the public debate on this); the dubious benefits of synergistic acquisitions; the exaggerated benefits to be derived from cashflow analysis; and the gaping holes in modern accounting –although on the latter, Buffett acknowledges that there are often no simple solutions to complex issues. Cunningham has divided the book into the primary subject areas covered by the essays, eg: corporate governance; corporate finance and investing; alternatives to common stock; M & A; accounting and valuation; accounting policy and tax matters. The reader should not be daunted by these seemingly weighty and technically laden areas, for the reason that Buffett’s writings have always been for the ordinary investor to understand. Thus, the approach is simple and replete with common sense arguments built over a lifetime ofsuccessful investing. The headings do however suggest the truth in the title, ie the book is for managers as well as for investors. A new CEO could do worse that make thishis/her first read after appointment – particularly if, as Buffett says is generally the case, they are good at their commercial discipline/endeavour, but do not really understand the allocation of capital, which is of paramount importance to shareholders.Chock-a-block with pithy wisdomBuffett has a great way with words, borne no doubt from a lifetime of study and commercial engagement/intercourse at the highest levels. Cunningham picks all this out for us in his excellent introduction with such insights as: “having first rate people on the team is more important than designing hierarchies and clarifying who reports to whom about what and at what times”(remember: Buffett runs a vary large corporate empire of controlled companies); “stay away from businesses without favourable and durable economic and competitive characteristics” (Buffett has learned this the hard way); “ a stock that has dropped very sharply compared to the market … becomes ‘riskier’ at the lower price than it was at the higher price” (another nail in the coffin of modern finance when explaining the shortfalls of beta); and in reference to the hallowed principle of diversification (see below) we are reminded that “Keynes, who was not only a brilliant economist but also an astute investor, believed that an investor should put fairly large sums into two or three business he knows something about and whose management is trustworthy. On that view, risk rises when investments and investment thinking are spread too thin”, which observation is linked to the “circle of competence” concept, which holds that investors should be aware of the scope of their competence and stay within it – the primary reason why BH did not lose money in the tech wave, for as Buffett acknowledged, he did not understand it, and with a fermenting industry like technology his attitude is much the same as with space exploration “we applaud the endeavour but prefer to skip the ride”; and finally “as happens in Wall Street all too often,what the wise do in the beginning, fools do in the end”.In revisiting these observations from the world’s greatest investor, I am reminded of the constant use of Buffett quotes by fund managers and financial planning groups as justification for their approach and products. The reality is that Buffett believes, as is pointed out in one of his letters, that most investors would do well to avoid actively managed funds (admittedly in the US context), and to simply put their money into the index – unless they can just focus on what they know, avoid undue diversification into unknown areas, and apply all the principles it has taken him a lifetime to learn from the worlds masters (eg, Graham and Dodd)!Again, Buffett is often used as justification for never trying to time the market – just hang in there and hope for the best, as no-one can call it. But even here, his writings have, it seems to me, been quoted out of context. His actual approach to market timing is far more sophisticated and pro-active. Indeed, as is pointed out in Hagstrom’s book (The Essential Buffett), Buffett closed his first investment partnership in 1969 and paid out funds, for the reason that he found the market to be highly speculative and worthwhile value increasingly scarce (p 26). Buffett refers to the super-contagious diseases of fear and greed and says that he never tries to “anticipate the arrival and departure of eitherdisease. Our goal is more modest: we simply attempt to be fearful when others are greedy and to be greedy only when others are fearful” – and his writings circa 1999 and 2000 clearly articulate a grave concern of irrational market exuberance. There are some brilliant observations about technology companies that only proves again, to me, that maturity and learning (Buffet has spades of both) are the only way to avoid such folly as we saw in this sector of the market in the late 20th century. Buffet and BH are unique, and the lessons to be drawn from their philosophy and principles cannot be ignored – any serious investor, adviser or manager (corporate or fund) must study them, even if you do not agree with everything. Buffett’s success is absolutely astounding, and anyone who reads the direct words of the maestro from this text will be better for it.One caveat: the most important lesson for DIY investors (and perhaps for fund managers!) is that of the circle of competence.A reading of this book does not bring out fully, as is covered in other Buffett books, the history and degree of study and early experience in Buffett’s life concerning investment. Buffett was quite literally born into stockbroking, he went to the best schools, had the very best teachers (ie, a happy coincidence of time, as he was there when they were), is gifted in maths and accounting, and has committed his entire life to corporate analysis and investing. Sure, you will gain insights, but this is no risk free path to replication.Finally, it should be said, for those who do not wish to spend £11.50 (I bought this in England last year), you can go to the BH website /doc/577491124.html, and you will find most of the writing there – eg, shareholders letters going back to 1977. However for a modest outlay, you get a good dissection into subject headings, and then collation under these discrete areas with footnote references, and you get the introduction and a useful index. Splash-out, save the printer, mark the text when reading it, and then revisit it one year later – the lessons will then sink in even further.MKEJan 03。

案例8-巴菲特

4、关键是正确理解巴菲特思想,避免教条化理解巴菲特投 资思想

1、巴菲特的投资业绩为何如此出众?

首先,巴菲特的起点比普通人要高。他的父亲霍华德·巴菲特 (Howard Buffet)是一名股票经纪兼四任国会议员。巴菲特的家中

市盈率反映了人们对于这支股票的的认可程度,市盈 率越高,说明人们对它的认可度越高,风险程度越大

1、没有什么比赌博心态更影响投资。 把股票当作一种正当的投资行为,而不是幻想通过 短期 的冒险投机达到一夜暴富的效果。

2、把自己当成持股公司的老板。这是巴菲特投资策略最核 心的理念。

3、永远不要做自己不懂的事情。巴菲特经常说的一句话: 如果你不了解这个产业,那么就不要买太多的股票。

4、买股票时,应假设明天股市要休市3~5年

5、如果无事可做,那就什么也不做。 他告诉投资者:最重要的是寻找符合标准的投资机会,不 能盲目妄动,要善于等待时机的出现。

6、购买价格远低于实际价值的企业,并永远拥有它们。

选择熟悉企业——只做自己擅长的领域 选择权威企业——最优秀的名牌公司 选择高成长股——最有潜力的公司股票 最好的投资时机——优秀企业出现危机时

1. 购买并长期持有优秀公司的股票 2.集中投资 3.安全边际是投资永不亏损的秘诀

15%法则

4.巴菲特投资的三不要信条

一不要迷信华尔街和听信谣言 二不要担心经济形势和股票涨跌 三不要投机、切忌冲动

5.巴菲特的投资心态

(1)情商比智商更重要,要有足够的耐心。 (2)投资不应该受感情、希望和恐惧以及时尚的摆布 (3)投资必须理性,要保持清醒的头脑 (4)像乌龟一样投资,如兔子那般获利。

presentation --warren buffet

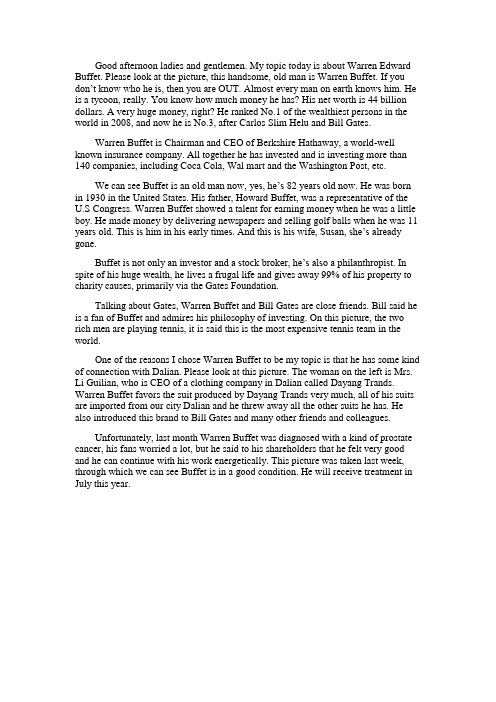

Good afternoon ladies and gentlemen. My topic today is about Warren Edward Buffet. Please look at the picture, this handsome, old man is Warren Buffet. If you don’t know who he is, then you are OUT. Almost every man on earth knows him. He is a tycoon, really. You know how much money he has? His net worth is 44 billion dollars. A very huge money, right? He ranked No.1 of the wealthiest persons in the world in 2008, and now he is No.3, after Carlos Slim Helu and Bill Gates.Warren Buffet is Chairman and CEO of Berkshire Hathaway, a world-well known insurance company. All together he has invested and is investing more than 140 companies, including Coca Cola, Wal mart and the Washington Post, etc.We can see Buffet is an old man now, yes, he’s 82 years old now. He was born in 1930 in the United States. His father, Howard Buffet, was a representative of the U.S Congress. Warren Buffet showed a talent for earning money when he was a little boy. He made money by delivering newspapers and selling golf balls when he was 11 years old. This is him in his early times. And this is his wife, Susan, she’s already gone.Buffet is not only an investor and a stock broker, he’s also a philanthropist. In spite of his huge wealth, he lives a frugal life and gives away 99% of his property to charity causes, primarily via the Gates Foundation.Talking about Gates, Warren Buffet and Bill Gates are close friends. Bill said he is a fan of Buffet and admires his philosophy of investing. On this picture, the two rich men are playing tennis, it is said this is the most expensive tennis team in the world.One of the reasons I chose Warren Buffet to be my topic is that he has some kind of connection with Dalian. Please look at this picture. The woman on the left is Mrs. Li Guilian, who is CEO of a clothing company in Dalian called Dayang Trands. Warren Buffet favors the suit produced by Dayang Trands very much, all of his suits are imported from our city Dalian and he threw away all the other suits he has. He also introduced this brand to Bill Gates and many other friends and colleagues.Unfortunately, last month Warren Buffet was diagnosed with a kind of prostate cancer, his fans worried a lot, but he said to his shareholders that he felt very good and he can continue with his work energetically. This picture was taken last week, through which we can see Buffet is in a good condition. He will receive treatment in July this year.。

Warren Buffett_2008

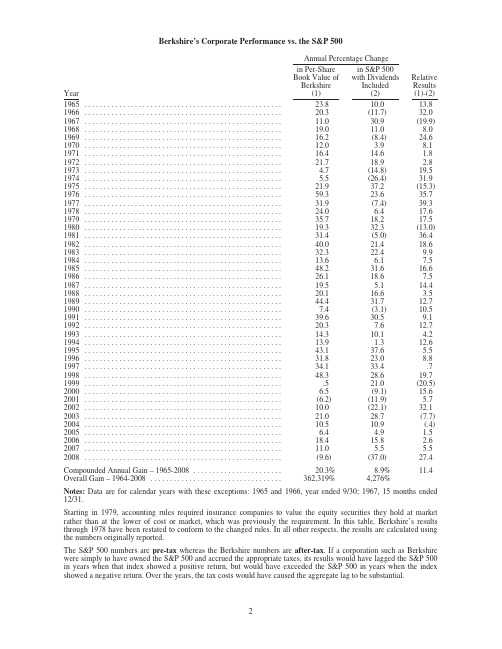

Berkshire’s Corporate Performance vs.the S&P500Annual Percentage ChangeYearin Per-ShareBook Value ofBerkshire(1)in S&P500with DividendsIncluded(2)RelativeResults(1)-(2)1965...................................................23.810.013.8 1966...................................................20.3(11.7)32.0 1967...................................................11.030.9(19.9) 1968...................................................19.011.08.0 1969...................................................16.2(8.4)24.6 1970...................................................12.0 3.98.1 1971...................................................16.414.6 1.8 1972...................................................21.718.9 2.8 1973................................................... 4.7(14.8)19.5 1974................................................... 5.5(26.4)31.9 1975...................................................21.937.2(15.3) 1976...................................................59.323.635.7 1977...................................................31.9(7.4)39.3 1978...................................................24.0 6.417.6 1979...................................................35.718.217.5 1980...................................................19.332.3(13.0) 1981...................................................31.4(5.0)36.4 1982...................................................40.021.418.6 1983...................................................32.322.49.9 1984...................................................13.6 6.17.5 1985...................................................48.231.616.6 1986...................................................26.118.67.5 1987...................................................19.5 5.114.4 1988...................................................20.116.6 3.5 1989...................................................44.431.712.7 1990...................................................7.4(3.1)10.5 1991...................................................39.630.59.1 1992...................................................20.37.612.7 1993...................................................14.310.1 4.2 1994...................................................13.9 1.312.6 1995...................................................43.137.6 5.5 1996...................................................31.823.08.8 1997...................................................34.133.4.7 1998...................................................48.328.619.7 1999....................................................521.0(20.5) 2000................................................... 6.5(9.1)15.6 2001...................................................(6.2)(11.9) 5.7 2002...................................................10.0(22.1)32.1 2003...................................................21.028.7(7.7) 2004...................................................10.510.9(.4) 2005................................................... 6.4 4.9 1.5 2006...................................................18.415.8 2.6 2007...................................................11.0 5.5 5.5 2008...................................................(9.6)(37.0)27.4 Compounded Annual Gain–1965-2008.......................20.3%8.9%11.4 Overall Gain–1964-2008..................................362,319%4,276%Notes:Data are for calendar years with these exceptions:1965and1966,year ended9/30;1967,15months ended 12/31.Starting in1979,accounting rules required insurance companies to value the equity securities they hold at market rather than at the lower of cost or market,which was previously the requirement.In this table,Berkshire’s results through1978have been restated to conform to the changed rules.In all other respects,the results are calculated using the numbers originally reported.The S&P500numbers are pre-tax whereas the Berkshire numbers are after-tax.If a corporation such as Berkshire were simply to have owned the S&P500and accrued the appropriate taxes,its results would have lagged the S&P500 in years when that index showed a positive return,but would have exceeded the S&P500in years when the index showed a negative return.Over the years,the tax costs would have caused the aggregate lag to be substantial.2BERKSHIRE HATHAWAY INC.To the Shareholders of Berkshire Hathaway Inc.:Our decrease in net worth during2008was$11.5billion,which reduced the per-share book value ofboth our Class A and Class B stock by9.6%.Over the last44years(that is,since present management took over)book value has grown from$19to$70,530,a rate of20.3%compounded annually.*The table on the preceding page,recording both the44-year performance of Berkshire’s book valueand the S&P500index,shows that2008was the worst year for each.The period was devastating as well forcorporate and municipal bonds,real estate and commodities.By yearend,investors of all stripes were bloodiedand confused,much as if they were small birds that had strayed into a badminton game.As the year progressed,a series of life-threatening problems within many of the world’s great financialinstitutions was unveiled.This led to a dysfunctional credit market that in important respects soon turnednon-functional.The watchword throughout the country became the creed I saw on restaurant walls when I wasyoung:“In God we trust;all others pay cash.”By the fourth quarter,the credit crisis,coupled with tumbling home and stock prices,had produced aparalyzing fear that engulfed the country.A freefall in business activity ensued,accelerating at a pace that I havenever before witnessed.The U.S.–and much of the world–became trapped in a vicious negative-feedbackcycle.Fear led to business contraction,and that in turn led to even greater fear.This debilitating spiral has spurred our government to take massive action.In poker terms,the Treasuryand the Fed have gone“all in.”Economic medicine that was previously meted out by the cupful has recentlybeen dispensed by the barrel.These once-unthinkable dosages will almost certainly bring on unwelcomeaftereffects.Their precise nature is anyone’s guess,though one likely consequence is an onslaught of inflation.Moreover,major industries have become dependent on Federal assistance,and they will be followed by citiesand states bearing mind-boggling requests.Weaning these entities from the public teat will be a politicalchallenge.They won’t leave willingly.Whatever the downsides may be,strong and immediate action by government was essential last year ifthe financial system was to avoid a total breakdown.Had one occurred,the consequences for every area of oureconomy would have been cataclysmic.Like it or not,the inhabitants of Wall Street,Main Street and the variousSide Streets of America were all in the same boat.Amid this bad news,however,never forget that our country has faced far worse travails in the past.Inthe20th Century alone,we dealt with two great wars(one of which we initially appeared to be losing);a dozen orso panics and recessions;virulent inflation that led to a211⁄2%prime rate in1980;and the Great Depression of the1930s,when unemployment ranged between15%and25%for many years.America has had no shortage ofchallenges.Without fail,however,we’ve overcome them.In the face of those obstacles–and many others–thereal standard of living for Americans improved nearly seven-fold during the1900s,while the Dow JonesIndustrials rose from66to11,pare the record of this period with the dozens of centuries during whichhumans secured only tiny gains,if any,in how they lived.Though the path has not been smooth,our economicsystem has worked extraordinarily well over time.It has unleashed human potential as no other system has,and itwill continue to do so.America’s best days lie ahead.*All per-share figures used in this report apply to Berkshire’s A shares.Figures for the B shares are1/30th of those shown for A.3Take a look again at the44-year table on page2.In75%of those years,the S&P stocks recorded a gain.I would guess that a roughly similar percentage of years will be positive in the next44.But neither Charlie Munger,my partner in running Berkshire,nor I can predict the winning and losing years in advance.(In our usual opinionated view,we don’t think anyone else can either.)We’re certain,for example,that the economy will be in shambles throughout2009–and,for that matter,probably well beyond–but that conclusion does not tell us whether the stock market will rise or fall.In good years and bad,Charlie and I simply focus on four goals:(1)maintaining Berkshire’s Gibraltar-like financial position,which features huge amounts ofexcess liquidity,near-term obligations that are modest,and dozens of sources of earningsand cash;(2)widening the“moats”around our operating businesses that give them durable competitiveadvantages;(3)acquiring and developing new and varied streams of earnings;(4)expanding and nurturing the cadre of outstanding operating managers who,over the years,have delivered Berkshire exceptional results.Berkshire in2008Most of the Berkshire businesses whose results are significantly affected by the economy earned below their potential last year,and that will be true in2009as well.Our retailers were hit particularly hard,as were our operations tied to residential construction.In aggregate,however,our manufacturing,service and retail businesses earned substantial sums and most of them–particularly the larger ones–continue to strengthen their competitive positions.Moreover,we are fortunate that Berkshire’s two most important businesses–our insurance and utility groups–produce earnings that are not correlated to those of the general economy.Both businesses delivered outstanding results in2008and have excellent prospects.As predicted in last year’s report,the exceptional underwriting profits that our insurance businesses realized in2007were not repeated in2008.Nevertheless,the insurance group delivered an underwriting gain for the sixth consecutive year.This means that our$58.5billion of insurance“float”–money that doesn’t belong to us but that we hold and invest for our own benefit–cost us less than zero.In fact,we were paid$2.8billion to hold our float during2008.Charlie and I find this enjoyable.Over time,most insurers experience a substantial underwriting loss,which makes their economics far different from ours.Of course,we too will experience underwriting losses in some years.But we have the best group of managers in the insurance business,and in most cases they oversee entrenched and valuable franchises. Considering these strengths,I believe that we will earn an underwriting profit over the years and that our float will therefore cost us nothing.Our insurance operation,the core business of Berkshire,is an economic powerhouse.Charlie and I are equally enthusiastic about our utility business,which had record earnings last year and is poised for future gains.Dave Sokol and Greg Abel,the managers of this operation,have achieved results unmatched elsewhere in the utility industry.I love it when they come up with new projects because in this capital-intensive business these ventures are often large.Such projects offer Berkshire the opportunity to put out substantial sums at decent returns.4Things also went well on the capital-allocation front last year.Berkshire is always a buyer of both businesses and securities,and the disarray in markets gave us a tailwind in our purchases.When investing, pessimism is your friend,euphoria the enemy.In our insurance portfolios,we made three large investments on terms that would be unavailable in normal markets.These should add about$11⁄2billion pre-tax to Berkshire’s annual earnings and offer possibilities for capital gains as well.We also closed on our Marmon acquisition(we own64%of the company now and will purchase its remaining stock over the next six years).Additionally,certain of our subsidiaries made “tuck-in”acquisitions that will strengthen their competitive positions and earnings.That’s the good news.But there’s another less pleasant reality:During2008I did some dumb things in investments.I made at least one major mistake of commission and several lesser ones that also hurt.I will tell you more about these later.Furthermore,I made some errors of omission,sucking my thumb when new facts came in that should have caused me to re-examine my thinking and promptly take action.Additionally,the market value of the bonds and stocks that we continue to hold suffered a significant decline along with the general market.This does not bother Charlie and me.Indeed,we enjoy such price declines if we have funds available to increase our positions.Long ago,Ben Graham taught me that“Price is what you pay;value is what you get.”Whether we’re talking about socks or stocks,I like buying quality merchandise when it is marked down.YardsticksBerkshire has two major areas of value.The first is our investments:stocks,bonds and cash equivalents.At yearend those totaled$122billion(not counting the investments held by our finance and utility operations,which we assign to our second bucket of value).About$58.5billion of that total is funded by our insurance float.Berkshire’s second component of value is earnings that come from sources other than investments and insurance.These earnings are delivered by our67non-insurance companies,itemized on page96.We exclude our insurance earnings from this calculation because the value of our insurance operation comes from the investable funds it generates,and we have already included this factor in our first bucket.In2008,our investments fell from$90,343per share of Berkshire(after minority interest)to$77,793,a decrease that was caused by a decline in market prices,not by net sales of stocks or bonds.Our second segment of value fell from pre-tax earnings of$4,093per Berkshire share to$3,921(again after minority interest).Both of these performances are unsatisfactory.Over time,we need to make decent gains in each area if we are to increase Berkshire’s intrinsic value at an acceptable rate.Going forward,however,our focus will be on the earnings segment,just as it has been for several decades.We like buying underpriced securities,but we like buying fairly-priced operating businesses even more.Now,let’s take a look at the four major operating sectors of Berkshire.Each of these has vastly different balance sheet and income account characteristics.Therefore,lumping them together,as is done in standard financial statements,impedes analysis.So we’ll present them as four separate businesses,which is how Charlie and I view them.5Regulated Utility BusinessBerkshire has an87.4%(diluted)interest in MidAmerican Energy Holdings,which owns a wide variety of utility operations.The largest of these are(1)Yorkshire Electricity and Northern Electric,whose 3.8million end users make it the U.K.’s third largest distributor of electricity;(2)MidAmerican Energy,which serves723,000electric customers,primarily in Iowa;(3)Pacific Power and Rocky Mountain Power,serving about1.7million electric customers in six western states;and(4)Kern River and Northern Natural pipelines, which carry about9%of the natural gas consumed in the U.S.Our partners in ownership of MidAmerican are its two terrific managers,Dave Sokol and Greg Abel, and my long-time friend,Walter Scott.It’s unimportant how many votes each party has;we make major moves only when we are unanimous in thinking them wise.Nine years of working with Dave,Greg and Walter have reinforced my original belief:Berkshire couldn’t have better partners.Somewhat incongruously,MidAmerican also owns the second largest real estate brokerage firm in the U.S.,HomeServices of America.This company operates through21locally-branded firms that have16,000 st year was a terrible year for home sales,and2009looks no better.We will continue,however,to acquire quality brokerage operations when they are available at sensible prices.Here are some key figures on MidAmerican’s operations:Earnings(in millions)20082007 U.K.utilities............................................................$339$337 Iowa utility. (425412)Western utilities (703692)Pipelines (595473)HomeServices...........................................................(45)42 Other(net).. (186130)Operating earnings before corporate interest and taxes...........................2,2032,086 Constellation Energy*.....................................................1,092–Interest,other than to Berkshire.............................................(332)(312) Interest on Berkshire junior debt.............................................(111)(108) Income tax..............................................................(1,002)(477) Net earnings.............................................................$1,850$1,189 Earnings applicable to Berkshire**..........................................$1,704$1,114 Debt owed to others.......................................................19,14519,002 Debt owed to Berkshire....................................................1,087821 *Consists of a breakup fee of$175million and a profit on our investment of$917million.**Includes interest earned by Berkshire(net of related income taxes)of$72in2008and$70in2007.MidAmerican’s record in operating its regulated electric utilities and natural gas pipelines is truly outstanding.Here’s some backup for that claim.Our two pipelines,Kern River and Northern Natural,were both acquired in2002.A firm called Mastio regularly ranks pipelines for customer satisfaction.Among the44rated,Kern River came in9th when we purchased it and Northern Natural ranked39th.There was work to do.In Mastio’s2009report,Kern River ranked1st and Northern Natural3rd.Charlie and I couldn’t be more proud of this performance.It came about because hundreds of people at each operation committed themselves to a new culture and then delivered on their commitment.Achievements at our electric utilities have been equally impressive.In1995,MidAmerican became the major provider of electricity in Iowa.By judicious planning and a zeal for efficiency,the company has kept electric prices unchanged since our purchase and has promised to hold them steady through2013.6MidAmerican has maintained this extraordinary price stability while making Iowa number one among all states in the percentage of its generation capacity that comes from wind.Since our purchase,MidAmerican’s wind-based facilities have grown from zero to almost20%of total capacity.Similarly,when we purchased PacifiCorp in2006,we moved aggressively to expand wind generation. Wind capacity was then33megawatts.It’s now794,with more coming.(Arriving at PacifiCorp,we found “wind”of a different sort:The company had98committees that met frequently.Now there are28.Meanwhile, we generate and deliver considerably more electricity,doing so with2%fewer employees.)In2008alone,MidAmerican spent$1.8billion on wind generation at our two operations,and today the company is number one in the nation among regulated utilities in ownership of wind capacity.By the way, compare that$1.8billion to the$1.1billion of pre-tax earnings of PacifiCorp(shown in the table as“Western”) and Iowa.In our utility business,we spend all we earn,and then some,in order to fulfill the needs of our service areas.Indeed,MidAmerican has not paid a dividend since Berkshire bought into the company in early2000.Its earnings have instead been reinvested to develop the utility systems our customers require and deserve.In exchange,we have been allowed to earn a fair return on the huge sums we have invested.It’s a great partnership for all concerned.************Our long-avowed goal is to be the“buyer of choice”for businesses–particularly those built and owned by families.The way to achieve this goal is to deserve it.That means we must keep our promises;avoid leveraging up acquired businesses;grant unusual autonomy to our managers;and hold the purchased companies through thick and thin(though we prefer thick and thicker).Our record matches our rhetoric.Most buyers competing against us,however,follow a different path. For them,acquisitions are“merchandise.”Before the ink dries on their purchase contracts,these operators are contemplating“exit strategies.”We have a decided advantage,therefore,when we encounter sellers who truly care about the future of their businesses.Some years back our competitors were known as“leveraged-buyout operators.”But LBO became a bad name.So in Orwellian fashion,the buyout firms decided to change their moniker.What they did not change, though,were the essential ingredients of their previous operations,including their cherished fee structures and love of leverage.Their new label became“private equity,”a name that turns the facts upside-down:A purchase of a business by these firms almost invariably results in dramatic reductions in the equity portion of the acquiree’s capital structure compared to that previously existing.A number of these acquirees,purchased only two to three years ago,are now in mortal danger because of the debt piled on them by their private-equity buyers.Much of the bank debt is selling below70¢on the dollar,and the public debt has taken a far greater beating.The private-equity firms,it should be noted,are not rushing in to inject the equity their wards now desperately need.Instead, they’re keeping their remaining funds very private.In the regulated utility field there are no large family-owned businesses.Here,Berkshire hopes to be the“buyer of choice”of regulators.It is they,rather than selling shareholders,who judge the fitness of purchasers when transactions are proposed.There is no hiding your history when you stand before these regulators.They can–and do–call their counterparts in other states where you operate and ask how you have behaved in respect to all aspects of the business,including a willingness to commit adequate equity capital.7When MidAmerican proposed its purchase of PacifiCorp in2005,regulators in the six new states we would be serving immediately checked our record in Iowa.They also carefully evaluated our financing plans and capabilities.We passed this examination,just as we expect to pass future ones.There are two reasons for our confidence.First,Dave Sokol and Greg Abel are going to run any businesses with which they are associated in a first-class manner.They don’t know of any other way to operate. Beyond that is the fact that we hope to buy more regulated utilities in the future–and we know that our business behavior in jurisdictions where we are operating today will determine how we are welcomed by new jurisdictions tomorrow.InsuranceOur insurance group has propelled Berkshire’s growth since we first entered the business in1967.This happy result has not been due to general prosperity in the industry.During the25years ending in2007,return on net worth for insurers averaged8.5%versus14.0%for the Fortune500.Clearly our insurance CEOs have not had the wind at their back.Yet these managers have excelled to a degree Charlie and I never dreamed possible in the early days.Why do I love them?Let me count the ways.At GEICO,Tony Nicely–now in his48th year at the company after joining it when he was18–continues to gobble up market share while maintaining disciplined underwriting.When Tony became CEO in 1993,GEICO had2.0%of the auto insurance market,a level at which the company had long been stuck.Now we have a7.7%share,up from7.2%in2007.The combination of new business gains and an improvement in the renewal rate on existing business has moved GEICO into the number three position among auto insurers.In1995,when Berkshire purchased control,GEICO was number seven.Now we trail only State Farm and Allstate.GEICO grows because it saves money for motorists.No one likes to buy auto insurance.But virtually everyone likes to drive.So,sensibly,drivers look for the lowest-cost insurance consistent with first-class service. Efficiency is the key to low cost,and efficiency is Tony’s specialty.Five years ago the number of policies per employee was299.In2008,the number was439,a huge increase in productivity.As we view GEICO’s current opportunities,Tony and I feel like two hungry mosquitoes in a nudist camp.Juicy targets are everywhere.First,and most important,our new business in auto insurance is now exploding.Americans are focused on saving money as never before,and they are flocking to GEICO.In January 2009,we set a monthly record–by a wide margin–for growth in policyholders.That record will last exactly28 days:As we go to press,it’s clear February’s gain will be even better.Beyond this,we are gaining ground in allied st year,our motorcycle policies increased by 23.4%,which raised our market share from about6%to more than7%.Our RV and ATV businesses are also growing rapidly,albeit from a small base.And,finally,we recently began insuring commercial autos,a big market that offers real promise.GEICO is now saving money for millions of Americans.Go to or call1-800-847-7536 and see if we can save you money as well.General Re,our large international reinsurer,also had an outstanding year in2008.Some time back, the company had serious problems(which I totally failed to detect when we purchased it in late1998).By2001, when Joe Brandon took over as CEO,assisted by his partner,Tad Montross,General Re’s culture had further deteriorated,exhibiting a loss of discipline in underwriting,reserving and expenses.After Joe and Tad took charge,these problems were decisively and successfully addressed.Today General Re has regained its luster. Last spring Joe stepped down,and Tad became CEO.Charlie and I are grateful to Joe for righting the ship and are certain that,with Tad,General Re’s future is in the best of hands.8Reinsurance is a business of long-term promises,sometimes extending for fifty years or more.This past year has retaught clients a crucial principle:A promise is no better than the person or institution making it. That’s where General Re excels:It is the only reinsurer that is backed by an AAA corporation.Ben Franklin once said,“It’s difficult for an empty sack to stand upright.”That’s no worry for General Re clients.Our third major insurance operation is Ajit Jain’s reinsurance division,headquartered in Stamford and staffed by only31employees.This may be one of the most remarkable businesses in the world,hard to characterize but easy to admire.From year to year,Ajit’s business is never the same.It features very large transactions,incredible speed of execution and a willingness to quote on policies that leave others scratching their heads.When there is a huge and unusual risk to be insured,Ajit is almost certain to be called.Ajit came to Berkshire in1986.Very quickly,I realized that we had acquired an extraordinary talent. So I did the logical thing:I wrote his parents in New Delhi and asked if they had another one like him at home. Of course,I knew the answer before writing.There isn’t anyone like Ajit.Our smaller insurers are just as outstanding in their own way as the“big three,”regularly delivering valuable float to us at a negative cost.We aggregate their results below under“Other Primary.”For space reasons,we don’t discuss these insurers individually.But be assured that Charlie and I appreciate the contribution of each.Here is the record for the four legs to our insurance stool.The underwriting profits signify that all four provided funds to Berkshire last year without cost,just as they did in2007.And in both years our underwriting profitability was considerably better than that achieved by the industry.Of course,we ourselves will periodically have a terrible year in insurance.But,overall,I expect us to average an underwriting profit.If so,we will be using free funds of large size for the indefinite future.Underwriting Profit Yearend Float(in millions)Insurance Operations2008200720082007General Re......................$342$555$21,074$23,009BH Reinsurance..................1,3241,42724,22123,692GEICO.........................9161,1138,4547,768Other Primary...................2102794,7394,229$2,792$3,374$58,488$58,698 Manufacturing,Service and Retailing OperationsOur activities in this part of Berkshire cover the waterfront.Let’s look,though,at a summary balance sheet and earnings statement for the entire group.Balance Sheet12/31/08(in millions)AssetsCash and equivalents.................$2,497 Accounts and notes receivable..........5,047 Inventory..........................7,500 Other current assets (752)Total current assets...................15,796 Goodwill and other intangibles.........16,515 Fixed assets........................16,338 Other assets........................1,248$49,897Liabilities and EquityNotes payable.......................$2,212 Other current liabilities...............8,087 Total current liabilities................10,299Deferred taxes......................2,786 Term debt and other liabilities..........6,033 Equity.............................30,779$49,897 9。

奥马哈中四条概率

奥马哈中四条概率摘要:1.引言:奥马哈的概率起源和背景2.奥马哈中四条概率的定义和解释3.每条概率的实用性和应用场景4.提高奥马哈概率判断和决策能力的方法5.结论:奥马哈中四条概率对投资和生活的启示正文:奥马哈,一个位于内布拉斯加州的小城市,因为亿万富翁沃伦·巴菲特(Warren Buffet)而闻名于世。

巴菲特是著名的投资家,他的投资哲学和策略备受推崇。

在投资领域,尤其是扑克牌游戏奥马哈,巴菲特总结出了四条概率原则,被称为“奥马哈中四条概率”(Omaha Hi-Lo)。

这些概率原则不仅在扑克牌游戏中具有指导意义,还可以应用于日常生活和投资决策中。

第一条:了解概率基本原理在奥马哈游戏中,了解每张牌的概率是非常重要的。

这要求玩家熟悉牌型、牌的大小以及每手牌获胜的概率。

同样,在现实生活中,我们需要了解各种情况发生的可能性,以便做出明智的决策。

例如,在投资领域,研究企业的基本面、行业趋势和市场环境,有助于我们判断投资项目的成功概率。

第二条:计算预期收益在奥马哈游戏中,玩家需要计算预期收益,即如果继续游戏,预期获得的收益是多少。

这需要玩家对各种可能的牌型和对手的牌进行估算。

在现实生活中,我们需要对投资项目的预期收益进行计算,以便评估项目的价值。

此外,在职业生涯规划中,计算不同选择的预期收益,有助于我们做出更明智的职业决策。

第三条:风险与收益的权衡奥马哈游戏中,风险与收益往往是成正比的。

玩家需要在追求高收益的同时,控制风险。

这要求玩家具备良好的风险收益比判断能力。

在现实生活中,投资、创业和职业发展等方面,我们都需要在风险和收益之间进行权衡。

学会识别和控制风险,以实现更高的收益。

第四条:耐心与自律奥马哈游戏的成功离不开耐心和自律。

玩家需要等待合适的时机,才能发挥出手中牌的最大价值。

在现实生活中,我们需要学会等待,抓住最佳时机,实现自身价值。

同时,自律意味着遵守规则、克制欲望,以实现长期目标。

在投资领域,耐心和自律有助于我们避免盲目跟风,坚持自己的投资策略。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

沃伦E.巴菲特1995阅读“沃伦E. 巴菲特”案例,回答下列问题,请注意你可以提出你自己感兴趣的问题,以代替下列问题。

1、在宣布收购的当天,GEICO公司和Berkshire Hathaway公司股票价格变动可能意味着什么?特别是,在Berkshire的市场资产净值中7.18亿美元的利润对GEICO的内在价值意味着什么?(注:在知道消息之前,Berkshire拥有GEICO的33.25百万的股票)2、根据Value Line公司的预测信息,GEICO的可能的内在价值在什么范围内?你对此估计范围有什么疑问?3、Berkshire Hathaway表现的怎么样?在总体上?在对Scott & Fetaer的投资上表现的怎么样?在早期购买GEICO的股票投资上?在可自由兑换的有价证券投资上?4、在沃伦E.巴菲特的观点中,内在价值是什么?为什么受到如此高的重视?它是如何估算的?内在价值的替代方案是什么?并且为什么巴菲特拒绝了它们?5、请客观地评价一下巴菲特的投资理念,并且指明你同意他的哪些观点,不同哪些观点?6、Berkshire的股东应该认可对GEICO的收购活动吗?1995年8月25日,Berkshire Hathaway 公司的CEO沃伦 E.巴菲特宣布他的公司将收购GEICO公司在外边的49.6%的股票份额。

这个23亿美元的交易将支付GEICO的股东们每股70美元,远远高于宣布前的每股市场价格55.75美元。

观测者对Berkshire Hathaway 公司将支付的26%的股票溢价感到吃惊,尤其是巴菲特不打算对GEICO做出任何的改变,而且这两家公司的合并没有明显的协同效应。

在宣布的当天,Berkshire Hathaway 公司股票的收盘价上涨了2.4%,对公司的整个市场价值而言则增加了7.18亿美元1。

在那一天,标准普尔500股价指数的收盘价上涨了0.5%。

对GEICO公司的收购活动使得人们重新认识了投资大师沃伦 E.巴菲特。

在许多方面,巴菲特是个奇迹。

巴菲特作为世界上最富有的个人投资者之一(其个人资产大约有70亿美元),同时他也受别人的尊敬甚至被人们所喜欢。

尽管他累计创造了也许是历史上最好的投资记录(从1965年到1994年其投资财富年增长复利率为28%2),Berkshire Hathaway 公司每年支付给他的作为公司CEO的薪酬仅仅为10万美元。

尽管巴菲特和公司内部其他的管理人员控制了公司47.9%的股份,然而他是以全体股东的利益在运作该公司的。

许多文章和三篇传记都以他为赞美对象3,然而他仍然是一个热情洋溢的人。

尽管被许多人称之为天才,但是他避开智力团体,而更喜欢以影响内布拉斯加人(他居住在奥马哈)和顽固投资商的行为。

相对于其他的投资“明星”,巴菲特能很快公开地承认他的投资失误。

尽管他持有哥伦比亚大学的MBA学位,并且相信他的导师Benjamin Graham教授,Benjamin Graham教授发展了以价值为基础的投资理念,该理念指导巴菲特取得成功,然而他仍然斥责商学院,由于商学院里面所开设投资和融资理论与现实的不相关性。

许多分析者试图提取巴菲特的成功秘诀。

指导巴菲特成功的关键法则到底是什么呢?这些法则能被广泛运用于20世纪90年代后期和21世纪还是它们仅仅属于巴菲特和他的时代?通过理解这些法则,分析者希望阐明Berkshire Hathaway 公司收购GEICO的谜团。

在什么假定条件下,该收购对Berkshire Hathaway 公司有利呢?在这次收购活动中巴菲特可能的动机是什么?对GEICO收购活动会被证明是成功的吗?该次投资活动和该公司其他最近的投资如Salomon Brother,USAir和Champion International相比较又会怎么样呢?Berkshire Hathaway公司的形成该公司成立于1889年,最初是一个伯克希尔棉花制造厂,最终发展成为新英格兰最大的纺织品生产商,该公司的纺织品占了该国棉纺织品生产总额的25%。

在1995年,Berkshire公司和 Hathaway公司合并,之后由于通货膨胀、技术转变和外国竞争者激烈的竞争,公司的状况开始了长期的下降。

在1965年,1在宣布收购的当天,Berkshire Hathaway 公司的股票价格增加了609.6美元,公司流通在外的股份数额为1177750股。

2巴菲特持有Berkshire Hathaway 公司股票的最初成本是每股17.578美元,在1995年8月25日每股的收盘价为每股25400美元。

3Robert G. Hagstrom, Jr., 巴菲特之路(New York: John Wiley & Sons, 1994); Andrew Kilpatrick, 巴菲特的故事巴菲特和一些合作伙伴获得了Berkshire Hathaway 公司的控制权,他们认为下降的趋势是可以逆转的。

在接下来的20年内,显而易见的是尽管大额资本投资的财务回报很一般,但它仍需要保持竞争力。

在1985年,Berkshire Hathaway 公司肢解了纺织品业务。

幸运的是,该纺织品部门在最初几年获得了足够的现金以至于公司能够购买奥马哈的两家保险公司——National Indemnity保险公司和National Fire & Marine保险公司。

其他业务的收购发生在紧随其后的20世纪70年代和20世纪80年代。

Berkshire Hathaway 公司每股的投资业绩让大多数的观察者则感到非常吃惊。

在1977年,该公司股票的年末收盘价格是89美元,在1995年8月25日,公司股票的收盘价格则高达25400美元。

相比之下,从1977年到1994年所有大公司股票的年平均总收益是14.3%4。

在同样的期间,标准普尔500股价指数从107点长到560点。

一些观察者要求巴菲特对股票进行分割以使它的个人投资者更容易获得。

巴菲特坚决拒绝了。

在1994年,Berkshire Hathaway 公司将自己描述成拥有很多从事一定数量分散业务活动的分支部门的混和公司5。

表一对各个不同分支机构的收入、营运利润、资本支出、折旧和资产做了简要的概述。

截止1994年,Berkshire Hathaway 公司投资组合业务包括以下几个部分:(1)保险公司。

在两者直接再保险的基础上,Berkshire Hathaway 公司投资组合最大的组成部分集中在财产险和事故险两个方面。

保险公司方面的投资组合包括在10个其他公开交易公司的有意思的权益收益。

该权益收益和Berkshire Hathaway 公司在这些公司没有未分配的营运收益的份额如表二所示。

由于在公认会计准则的条件下这些公司中某些公司的收益不能和Berkshire Hathaway 公司的收益加在一起,巴菲特公布了Berkshire Hathaway 公司的“look-though”6收益,如表二所示。

主要投资的未分配收益份额占了Berkshire Hathaway 公司全部“look-though”收益的4股票、债券、票据和通货膨胀(Chicago: Ibbotson Associats, 1994)5Berkshire Hathaway 公司1994年年报6“Look-though” earning是Berkshire Hathaway 公司收入报表上的经营收益加上没有在Berkshire Hathaway 公司利润表上显(表2用的是14%示的主要投资的未分配的经营收益之和,减去如果这些经营收益分配给Berkshire Hathaway 公司应交的税。

40%到50%。

表三概括了Berkshire Hathaway 公司最近几年的可转换优先股7的投资情况,可转换优先股作为许多公司的白衣骑士——这些公司中的每一个公司将成为实际或者谣言接管的目标。

(2)Buffalo News。

在纽约北部的日报公司。

(3)Fechheimer。

一个制服的生产商和批发商。

(4)Kirby。

一个家庭清洁系统及其配件的生产者和市场销售者。

(5)内布拉斯加州家具。

家庭妆饰的零售商。

(6)See’s Candies。

一个盒装巧克力和其他糖果产品的生产商和批发商。

(7)Childcraft and Word Book。

大百科全书和相关教育书籍的出版商和批发商。

(8)Campbell Hausfeld。

空中压缩机、空中交通工具和油漆系统的生产商和批发商。

(9)H.H. Brown Shoe Company; Lowell Shoe, inc.; and Dexter Shoe Company。

一个鞋类产品的生产商、进口商和批发商。

除了这些业务,Berkshire Hathaway 公司拥有一类小的业务8,该业务大约产生了4亿美元的收入。

Berkshire Hathaway 公司的收购政策对GEICO收购的宣布使得广大投资者对巴菲特的收购方法进行了重新认识。

表4给出了Berkshire Hathaway 公司1994年年报中收购策略的一般陈述。

总的来说,该收购策略显示了一个周密的纪律策略,即巴菲特从来不因为别的公司做出了Berkshire Hathaway 公司自身也可轻易做出的行动而奖励它们。

因此,分析者仔细观察这些标准以评价在什么地方他们能对巴菲特提供一些好的建议。

一个巴菲特提到的显著的例子是1986年Berkshire Hathaway 公司收购Scott & Fetzer公司。

在面对其他公司敌意收购的谣言时,该公司的管理者已经打算实行杠杆收购。

当公司的劳工部门拒绝使用公司员工持股计划来获得所需的资金时,杠杆收购便落败了。

不久,这家吸引了一些公司来主动收购它,其中包括一个来自于Ivan F Boesky的套利者。

巴菲特以3.15亿美元的报价来购买此公司(和该公司的市场价格1.726亿美元形成鲜明的对比)。

该收购之后,Scott & Fetzer公司发放给Berkshire Hathaway 公司1.25亿美元的股利,即使它当年仅仅挣到0.403亿美元。

另外,Scott & Fetzer公司在融资上非常的保守,从刚开始温和的债务到1994年的没有债务。

表5给出了Scott & Fetzer公司1986年到1994年的收益和红利情况,巴菲特指出从权益账面价值收益率来衡量,Scott & Fetzer公司将很容易地击败世界500强的企业9。

大公司股票从1986年到1994年年平均总回报为12.6%10。

巴菲特的投资理念巴菲特第一次接受正式的培训是在哥伦比亚大学,当时他的导师是Benjamin Graham教授。