西方财务会计课后习题答案

西方财务会计课后题5-8答案

西方财务会计课后题5-8答案CHAPTER 51. THE KNOWLEDGE THAT JOB ROTATION IS PRACTICED AND THAT ONE EMPLOYEE MAY PERFORM ANOTHER’S JOB AT A LATER DATE TENDS TO DISCOURAGE DEVIATIONS FROM PRESCRIBED PROCEDURES. ALSO,ROTATION HELPS TO DISCLOSE ANYIRREGULARITIES THAT MAY OCCUR.2. Authorizing complete control over a sequence of related operations by one individual presents opportunities for inefficiency, errors, and fraud. The control over a sequence of operations should be divided so that the work of each employee is automatically checked by another employee in the normal course of work. A system functioning in this manner helps prevent errors and inefficiency. Fraud is unlikely without collusion between two or more employees.3. To reduce the possibility of errors and embezzlement, the functions of operations and accounting should be separated. Thus, one employee should not be responsible for handling cash receipts (operations) and maintaining the accounts receivable records (accounting).4. No. Combining the responsibility for related operations, such as combining the functions of purchasing, receiving, and storing of supplies, increases the possibility of errors and fraud.5. The control procedure requiring thatresponsibility for a sequence of related operations be divided among different persons is violated in this situation. This weakness in the internal control may permit irregularities. For example, the ticket seller, while acting as ticket taker, could admit friends without a ticket.6. The responsibility for maintaining the accountingrecords should be separated from the responsibility for operations so that the accounting records can serve as an independent check on operations.7. The individual accounts receivable ledgeraccounts provide business managers information on the status of individual customer accounts, which is necessary for managing collections.Managers need to know which customers owe money, how much they owe, and how long the amount owed has been outstanding.8. The major advantages of the use of specialjournals are substantial savings in record-keeping expenses and a reduction of record-keeping errors.9. a. 250;b. None10. a. 250; b. 111. a. Sometime following the end of the currentmonth, one of two things may happen: (1) an overdue notice will be received from Hoffman Co., and/or (2) a letter will be received from Hoffer Co., informing the buyer of theoverpayment. (It is also possible that the error will be discovered at the time of making payment if the original invoice is inspected at the time the check is being written.)b. T he schedule of accounts payable would notagree with the balance of the accounts payable account. The error might also be discovered at the time the invoice is paid.c. The creditor will call the attention of the debtorto the unpaid balance of $1,000.d. T he error will become evident during theverification process at the end of the month. The total debits in the purchases journal will be less than the total credits by $2,000.12. a. No, the error will not cause the trial balancetotals to be unequal.b. N o, the sum of the balances in the creditorsledger will not agree with the balance of the accounts payable account in the general ledger.13. a. Cash payments journal; b. Purchasesjournal; c. Cash payments journald. P urchases journal;e. Cash payments journal14. An electronic form is a software window thatprovides the inputs for a particular transaction.For example, a check form provides the inputs (payee, amount, date) for a cash payment transaction. An electronic invoice provides theinputs (customer, amount sold, item sold) for recording revenues earned on account.15. The use of controlling accounts to verify theaccuracy of subsidiary accounts is used in a manual system. In a computerized system, it is assumed that the computer will accurately sum the individual transactions in the subsidiary accounts in determining the aggregate balance.Thus, there is no need for controlling accounts for controlling the accuracy of the individual postings.16. For automated systems that use electronic formsthe special journals are not used to record original transactions. Rather, elec-tronic forms capture the original transaction detail from an invoice, for example, and automatically post the transaction details to the appropriate ledger accounts.17. E-commerce can be used by a business toconduct transactions directly with customers.Thus, an order can be received directly from the customer’s Internet input and cash can be received from the credit card. Many times, the cash is received prior to actually shipping the product, resulting in a faster revenue/collection cycle. Reducing paperwork throughout the cycle also improves the efficiency of the process. For example, all of the accounting transactions can be fed automatically from the initial Web-based inputs.EX. 5–1As an internal auditor, you would probably disagree with the change in policy. First Charter has some normal business risk associated with default on bank loans. One way to help minimize this is to carefully evaluate loan applications. Large loans present greater risk in the event of default than do smaller loans. Thus, it is reasonable to have more than one person involved in making the decision to grant a large loan. In addition, loans should be granted on their merits, not on the basis of favoritism or mere association with the bank president. Allowing the bank president to have sole authority to grant large loans can lead to the president granting loans to friends and business associates, without the required due diligence. This can result in a bank becoming exposed to very poor credit risks. Indeed, this scenario is one of the causes of savings and loan and bank failures of the past.Ex. 5–2This is an example of a fraud with significant collusion. Frauds that are perpetrated with multiple parties in different positions of control make detecting fraud more difficult. In this case, the fraud began with an employee responsible for authorizing claim payments. This is a sensitive position because his decisions would initiate payments. However, claims would need to be authorized and verified before payment would be made. Knowing this, the employee made sure each claim had a phony “victim.” Thus, there was a verifiable story behindeach claim. Only by tracking physical evidence of the accident could it be discovered that the claim was fictitious. However, the very nature of the process was to resolve small claims quickly without excessive control. Lastly, corrupt lawyers were brought into the fraud to act as attorneys for the claimants. This gave the claims even more credibility. In actuality, the lawyers had done legitimate business with the trucking company, so all appeared normal. This fraud was discovered when the fraudulent employee’s bank noticed irregularities in his bank account and notified authorities. As the saying goes, “Follow the money!” As a side note, the corrupt claims administrator fell into this behavior due to gambling problems.Ex. 5–3Event Sound should not have relied on the unusual nature of the vendors and delivery frequency to uncover this fraud. The purchase and payment cycle is one of the most critical business cycles to control, because the potential for abuse is so great. Purchases should be initiated by a requisition document. This document should be countersigned by a superior so that two people agree as to what is being purchased. The requisition should initiate a purchase order to a vendor for goods or services. The vendor responds to the purchase order by delivering the goods. The goods should be formally received using a receiving document. An accounts payable clerk matches the requisition, purchase order, and invoice before anypayment is made. Such “triple matching” prevents unauthorized requests and payments. In this case, the requests were unauthorized, suggesting that the employee had sole authority to make a request. Second, this employee had access to the invoices. This access allowed the employee to change critical characteristics of the invoice to hide the true nature of the goods being received. The invoice should have been delivered directly to the accounts payable clerk to avoid corrupting the document. There apparently was no receiving document (common for smaller companies); thus, only the invoice provided proof of what was received and to be paid. If there had been a receiving report, the invoice could not have been doctored and gone undetected, because it would not have matched the receiving report.Note to Instructors: This exercise is based on an actual fraud.Ex. 5–4a. The most difficult frauds to detect are those thatinvolve the senior management of a company that is in a conspiracy to commit the fraud. The senior managers have the power to access many parts of the accounting system, while the normal separation of duties is subverted by involving many people in the fraud. In addition, the authorization control is subverted because most of the authorization power resides in the senior management.b. Overall, this type of fraud can be stopped if thereis strong oversight of senior management, such as an audit committee of the board of directors. Individual “whistle blowers” in the company can make their concerns known to the independent or internal auditors who, in turn, can inform the audit committee. The audit committee should be independent of management and have the power to monitor the actions of management.Ex. 5–51. General ledger accounts: (e);2.Subsidiary ledgeraccounts: (a), (b), (c), (d)Ex. 5–6a. Cash receipts journal;b.Cash receipts journal;c. General journal (not a revenue transaction)d. General journal;e. Cash receipts journal;f. Cash receipts journalg. Cash receipts journal;h.Revenue journal;i.C ash receipts journal;j. General journalEx. 5–7a. Cash payments journal;b.Purchases journal;c.Cash payments journal;d.General journale. General journal;f.Cash payments journal;g.Purchases journal;h.Cash payments journali. General journal;j.General journal;k.PurchasesjournalEx. 5–8Nov.3 Provided service on account; posted from revenue journal.9 Granted allowance or corrected error relatedto sale of November 3; posted from general journal.13 Received cash for balance due; posted fromcash receipts journal.Ex. 5–9REVENUE JOURNAL PAGE 8 Invoice Post. AccountsRec. Dr.Date No. Account Debited Ref. FeesEarned Cr.20061 Mar.2 512 Conrad Co. ......... ✓790 12 8 513 Orlando Co. ........ ✓310 23 12 514 Drake Inc. ........... ✓580 34 22 515 Electronic Central, Inc. ✓25031 Total ...................... 1,930 5CASH RECEIPTS JOURNAL PAGE 12Fees Accts.Post.Earned Rec. CashDate Account Credited Ref. Cr. Cr.Dr.20061 Mar.4 CMI, Inc. ...... ✓ ........ 240 240 12 19 Drake Inc. .... ✓ ........ 530 530 23 27 Fees Earned ... 70 ........ 70 34 29 Conrad Co. ... ✓ ........ 790 790 45 31 Fees Earned ... 40 ........ 40 56 31 Total ............... 110 1,560 1,670 6 Ex. 5–101. General ledger account: (c), (e), (h), (j), (k), (l)2. Subsidiary ledger account: (a), (b), (d), (f), (g), (i);3. No posting required: (m)Ex. 5–111. General ledger account: (b), (c), (d), (f), (g), (i),(k), (l)2. Subsidiary ledger account: (a), (e), (h);3. Noposting required: (j)Ex. 5–12Feb.6 Purchased services, supplies, equipment, or other commodities on account; posted from purchases journal.10 Received allowance or corrected error related to purchase of February 6; posted from general journal.16 Paid balance owed; posted from cash payments journal.Ex. 5–14Revenue journal: (d), (i);Cash receipts journal: (a),(e)Purchases journal: (g), (h);Cash payments journal:(b), (f);General journal: (c), (j)Ex. 5–151. The Cash column is for debits (not credits).2. The Other Accounts column is for credits (notdebits).3. A better order of columns would be to place theOther Accounts Cr. column to the left of the Fees Earned Cr. column.A recommended and corrected cash receiptsjournal is as follows:CASH RECEIPTS JOURNALPAGE 12DA TE ACCOUNTCREDITEDPOST.REF.OTHERACCOUNTSCR.FEESEARNEDCR.ACCOUNTSREC.CR.CASHDR.Ex. 5–13PURCHASES JOURNAL PAGE 36OTHER ACCOUNTS DR.D A TE ACCOUNTCREDITEDPOSTREF.ACCOUNTSPAYABLECR.CLEANINGSUPPLIESDR.ACCOUNT POSTREF.AMOUNT20 071 M ay 3 IndustrialProducts, Inc.✓85 85 12 12 Carver PaperProducts, Inc.✓205 205 23 17 Liquid KleanSupplies✓170 170 374 20 FountainLaundry Service✓70 Laundry ServiceExp.53 70 45 31Total 530 460 70 5CASH PAYMENTS JOURNAL PAGE 41OtherAccountsCheck Post.AccountsPayableCashDate No.Account Debited Ref. Dr. Dr. Cr.20071 May1 57 Liquid Klean Supplies ..... ✓145 145 12 8 58 Equipment ......... 18 450 ........ 450 24 15 59 Fountain Laundry Service .... ✓115 115 45 25 60 Industrial Products, Inc. ....... ✓85 85 56 31 61 Salary Expense .. 51 2,900 ........ 2,900 67 31 Total ................... 3,350 345 3,695 77Ex. 5–16a.REVENUE JOURNAL PAGE 1D A TE INVOICENO.ACCOUNTDEBITEDPOST.REF.ACCTS.REC.DR.FEESEARNEDCR.SALESTAXPAYABLECR.1 June16 1 A. Sommerfeld ✓315 300 15 12 19 2 K. Lee ✓126 120 6 23 21 3 J. Koss ✓84 80 4 34 22 4 D. Jeffries ✓126 120 6 45 26 5 J. Koss ✓273 260 13 56 28 6 K. Lee ✓63 60 3 67 30 987 940 47 78 (12) (41) (22) 8JOURNAL PAGE 1Post.Date Description Ref.DebitJune24 Office Supplies ............... 14 168Fees Earned ................... 41 160Sales Tax Payable .......... 22 8 ACCOUNTS RECEIVABLE SUBSIDIARYLEDGERD. JeffriesPost.Date Item Ref. Dr. Cr. Balance2006June22 ............................. R1 126 .. 126J. Koss2006June21 ............................. R1 84 . (84)26 ............................. R1 273 .. 357K. Lee2006June19 ............................. R1 126 .. 12628 ............................. R1 63 .. 189A. SommerfeldJune16 ............................. R1 315 .. 315b.GENERAL LEDGERAccounts Receivable 12Post. Balance Date Item Ref. Dr. Cr. Dr. Cr. 2006June30 ........................... R1 987 987Office Supplies 14 2006June24 ........................... J1 168 168Sales Tax Payable 22 2006June24 ........................... J1 .... 8 .. (8)30 ........................... R1 .. 47 (55)Fees Earned 41 2006June24 ........................... J1 160 .16030 ........................... R1 9401,100c. 1. $987 ($126 + $357 + $189 + $315)2. $987CHAPTER 61. Merchandising businesses acquire merchandise for resale to customers. It is the selling of merchandise, instead of a service, that makes the activities of a merchandising business different from the activities of a service business.2. Yes. Gross profit is the excess of (net) sales over cost of merchandise sold. A net loss arises when operating expenses exceed gross profit. Therefore, a business can earn a gross profit but incur operating expenses in excess of this gross profit and end up with a net loss.3. a. Increase c. Decrease;b. Increase d.Decrease4. Under the periodic method, the inventory records do not show the amount available for sale or the amount sold during the period. In contrast, under the perpetual method of accounting for merchandise inventory, eachpurchase and sale of merchandise is recorded in the inventory and the cost of merchandise sold accounts. As a result, the amount of merchandise available for sale and the amount sold are continuously (perpetually) disclosed in the inventory records.5. The multiple-step form of income statement contains conventional groupings for revenues and expenses, with intermediate balances, before concluding with the net income balance. In the single-step form, the total of all expenses is deducted from the total of all revenues, without intermediate balances.6. The major advantages of the single-step form of income statement are its simplicity and its emphasis on total revenues and total expenses as the determinants of net income. The major objection to the form is that such relationships as gross profit to sales and income from operations to sales arenot as readily determinable as when the multiple-step form is used.7. Revenues from sources other than theprincipal activity of the business are classified as other income.8. Sales to customers who use bank credit cardsare generally treated as cash sales. The credit card invoices representing these sales are deposited by the seller directly into the bank, along with the currency and checks received from customers. Sales made by the use of nonbank credit cards generally must be reported periodically to the card company before cash is received. Therefore, such sales create a receivable with the card company. In both cases, any service or collection fees charged by the bank or card company are debited to expense accounts.9. The date of sale as shown by the date of theinvoice or bill.10. a. 2% discount allowed if paid within tendays of date of invoice; entire amount of invoice due within 60 days of date of invoice.b. P ayment due within 30 days of date ofinvoice.c. Payment due by the end of the month inwhich the sale was made.11. a. A credit memorandum issued by theseller of merchandise indicates the amount for which the buyer's account is to be credited (credit to Accounts Receivable) and the reason for the sales return or allowance.b. A debit memorandum issued by the buyerof merchandise indicates the amount for which the seller's account is to be debited (debit to Accounts Payable) and the reason for the purchases return or allowance.12. a. The buyer;b. The seller13. Examples of such accounts include thefollowing: Sales, Sales Discounts, Sales Returns and Allowances, Cost of Merchandise Sold, Merchandise Inventory.14. Cost of Merchandise Sold would be debited;Merchandise Inventory would be credited. EXERCISESEx. 6–1a. $490,000 ($250,000 + $975,000 – $735,000);b.40% ($490,000 ÷ $1,225,000)c. No. If operating expenses are less than grossprofit, there will be a net income. On the other hand, if operating expenses exceed gross profit, there will be a net loss.Ex. 6–2 $15,710 million ($20,946 million –$5,236 million)Ex. 6–3a. Purchases discounts, purchases returns andallowancesb. Transportation in;c.Merchandise availablefor sale;d. Merchandise inventory (ending)Ex. 6–41. The schedule should begin with the January1, not the December 31, merchandise inventory.2. Purchases returns and allowances andpurchases discounts should be deducted from(not added to) purchases.3. The result of subtracting purchases returnsand allowances and purchases discounts from purchases should be labeled “net purchases.”4. Transportation in should be added to netpurchases to yield cost of merchandisepurchased.5. The merchandise inventory at December 31should be deducted from merchandiseavailable for sale to yield cost of merchandisesold.A correct cost of merchandise sold section isas follows:Cost of merchandise sold:Merchandise inventory, January 1, 2006 $ Purchases ............................ $600,000Less:Purchases returns and allowances$14,000Purchases discounts .... 6,000 20,000Net purchases ..................... $580,000Add transportation in ........ 7,500Cost of merchandise purchased 587 Merchandise available for sale $71 Less merchandise inventory,December 31, 2006 ......... 120,000 Cost of merchandise sold ... $599,500Ex. 6–5Net sales: $3,010,000 ($3,570,000 –$320,000 –$240,000)Gross profit: $868,000 ($3,010,000 – $2,142,000)Ex. 6–6THE MERIDEN COMPANYIncome StatementFor the Year Ended June 30, 2006Revenues:Net sales ..........................................$5,400,000Rent revenue ..................................30,000Total revenues .............................$5,430,000Expenses:Cost of merchandise sold ..............$3,240,000Selling expenses .............................. 480,000 Administrative expenses ................ 300,000 Interest expense ............................. 47,500Total expenses ..............................4,067,500Net income ...........................................$1,362,500Ex. 6–71. Sales returns and allowances and salesdiscounts should be deducted from (not added to) sales.2. Sales returns and allowances and salesdiscounts should be deducted from sales to yield "net sales" (not gross sales).3. Deducting the cost of merchandise sold fromnet sales yields gross profit.4. Deducting the total operating expenses fromgross profit would yield income from operations (or operating income).5. Interest revenue should be reported underthe caption “Other income” and should beadded to Income from operations to arrive atNet income.6. The final amount on the income statementshould be labeled Net income, not Grossprofit.A correct income statement would be asfollows:THE PLAUTUS COMPANYIncome StatementFor the Year Ended October 31, 2006Revenue from sales:Sales .................................... $4,200,000Less:Sales returns and allowances $81,200Sales discounts ............ 20,300 101,500Net sales ........................... $4,098,500 Cost of merchandise sold ...... 2,093,000 Gross profit ............................ $2,005,500 Operating expenses:Selling expenses .................. $203,000 Transportation out ............. 7,500Administrative expenses .... 122,000Total operating expenses 332,500 Income from operations ........ $1,673,000 Other income:Interest revenue ................. 66,500 Net income .............................. $1,739,500 Ex. 6–8a. $25,000;e.$40,000;b.$210,000;f.$520,000;c. $477,000;g. $757,500;d.$192,000;h. $690,000Ex. 6–9a. Cash ......................................... 6,900Sales .............................................. 6,900Cost of Merchandise Sold ...... 4,830Merchandise Inventory ............... 4,830b. Accounts Receivable .............. 7,500Sales .............................................. 7,500Cost of Merchandise Sold ...... 5,625Merchandise Inventory ............... 5,625c. Cash ....................................... 10,200Sales .............................................. 10,200Cost of Merchandise Sold ...... 6,630Merchandise Inventory ............... 6,630d. Accounts Receivable—American Express7,200Sales .............................................. 7,200Cost of Merchandise Sold ...... 5,040Merchandise Inventory ............... 5,040e. Credit Card Expense (675)Cash (675)f. Cash ......................................... 6,875Credit Card Expense (325)Accounts Receivable—American Express 7,2 Ex. 6–10It was acceptable to debit Sales for the $235,750. However, using Sales Returns and Allowancesassists management in monitoring the amount ofreturns so that quick action can be taken ifreturns become excessive.Accounts Receivable should also have beencredited for $235,750. In addition, Cost of Merchandise Sold should only have beencredited for the cost of the merchandise sold, notthe selling price. Merchandise Inventory should also have been debited for the cost of the merchandise returned. The entries to correctly record the returns would have been as follows: Sales (or Sales Returns and Allowances) 235,750Accounts Receivable .................... 235,750Merchandise Inventory ..... 141,450Cost of Merchandise Sold ........... 141,450 Ex. 6–11a. $7,350 [$7,500 – $150 ($7,500 × 2%)]b. Sales Returns and Allowances7,500Sales Discounts (150)Cash .............................................. 7,350Merchandise Inventory ......... 4,500Cost of Merchandise Sold ........... 4,500 Ex. 6–12(1) S old merchandise on account, $12,000.(2) R ecorded the cost of the merchandise soldand reduced the merchandise inventory account, $7,800.(3) A ccepted a return of merchandise andgranted an allowance, $2,500.(4) U pdated the merchandise inventory accountfor the cost of the merchandise returned,$1,625.(5) R eceived the balance due within the discountperiod, $9,405. [Sale of $12,000, less return of$2,500, less discount of $95 (1% × $9,500).]Ex. 6–13a. $18,000;b. $18,375;c.$540 (3% ×$18,000);d. $17,835Ex. 6–14a. $7,546 [Purchase of $8,500, less return of$800, less discount of $154 ($7,700 × 2%)]b. Merchandise InventoryEx. 6–15Offer A is lower than offer B. Details are as follows:A BList price ......................................... $40,000$40,300 Less discount .................................. 800 403$39,200$39,897 Transportation (625)$39,825$39,897 Ex. 6–16(1) P urchased merchandise on account at a netcost of $8,000.(2) P aid transportation costs, $175.(3) A n allowance or return of merchandise wasgranted by the creditor, $1,000.(4) P aid the balance due within the discountperiod: debited Accounts Payable, $7,000,and credited Merchandise Inventory for theamount of the discount, $140, and Cash,$6,860.Ex. 6–17a. Merchandise Inventory ......... 7,500Accounts Payable ......................... 7,500b. Accounts Payable ................... 1,200Merchandise Inventory ............... 1,200c. Accounts Payable ................... 6,300Cash .............................................. 6,174Merchandise Inventory (126)Ex. 6–18a. Merchandise Inventory ....... 12,000Accounts Payable—Loew Co. ..... 12,000 b. Accounts Payable—Loew Co. ........ 12,000Cash .............................................. 11,760Merchandise Inventory (240)c. Accounts Payable*—Loew Co.2,940Merchandise Inventory ............... 2,940 d. Merchandise Inventory ......... 2,000Accounts Payable—Loew Co. ..... 2,000 e. Cash .. (940)Accounts Payable—Loew Co. (940)*Note: The debit of $2,940 to Accounts Payable in entry (c) is the amount of cash refund due from Loew Co. It is computed as the amount that was paid for the returned merchandise, $3,000, less the purchase discount of $60 ($3,000 × 2%). The credit to Accounts Payable of $2,000 in entry (d) reduces the debit balance in the account to $940, which is the amount of the cash refund in entry (e). The alternative entries below yield the same final results.c. Accounts Receivable—Loew Co. ... 2,940Merchandise Inventory ............... 2,940 d. Merchandise Inventory .................. 2,000Accounts Payable—Loew Co. ..... 2,000 e. Cash .. (940)Accounts Payable—Loew Co. ........ 2,000Accounts Receivable—Loew Co. 2,940 Ex. 6–19a. $10,500;b.$4,160 [($4,500 –$500) ⨯0.99] +$200;c. $4,900;d. $3,960;e. $834 [($1,500 – $700) ⨯ 0.98] + $50Ex. 6–20a. At the time of sale c. $4,280;b.$4,000;d. Sales Tax PayableEx. 6–21a. Accounts Receivable ....................... 9,720Sales .............................................. 9,000Sales Tax Payable (720)Cost of Merchandise Sold ............... 6,300Merchandise Inventory ............... 6,300 b. Sales Tax Payable ............................ 9,175。

西方财务会计课后习题答案

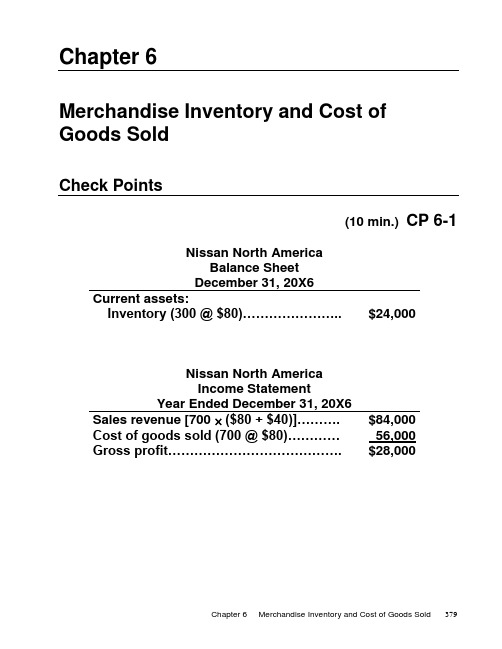

西方财务会计课后习题答案Merchandise Inventory and Cost of Goods SoldCheck Points(10 min.) CP 6-1Nissan North AmericaBalance SheetDecember 31, 20X6Current assets:Inventory (300 @ $80)…………………..$24,000Nissan North AmericaIncome StatementYear Ended December 31, 20X6Sales revenue [700 ($80 + $40)]……….$84,000Cost of goods sold (700 @ $80)………… 56,000Gross profit………………………………….$28,000(10-15 min.) CP 6-2 1. (Journal entries)Inventory…………………………………..100,000Accounts Payable…………………….100,000 Cash ($140,000 ⨯.20)……………………28,000Amounts Receivable ($140,000 ⨯ .80).. 112,000Sales Revenue………………………...140,000 Cost of Goods Sold……………………..60,000Inventory ($100,000 ⨯.60)…………..60,000 2. (Financial statements)BALANCE SHEETCurrent assets:Inventory ($100,000 –$60,000)……………….$40,000 INCOME STATEMENTSales revenue………………………………………$140,000Cost of goods sold……………………………….. 60,000Gross profit…………………………………………$ 80,000(10 min.) CP 6-3Billions Inventory………………………… 6.4Cash…………………………... 6.4 Accounts Receivable………….28.5Sales Revenue……………….28.5Cost of Goods Sold…………… 6.2Inventory……………………... 6.2 Cash………………………………26.3Accounts Receivab le……….26.3(10 min.) CP 6-41. I nventory costs are increasing from $10 to $14 to $18 per unit.2. FIFO results in the highest cost of ending inventory($360)because under FIFO the ending inventory is costed at the last costs incurred during the period. When costs are increasing, the last costs are the highest costs.FIFO results in the lowest cost of goods sold. This occurs because the oldest costs are assigned to cost of goods sold.When costs are increasing, the oldest costs are the lowest.FIFO results in the highest gross profit because cost of goods sold, the expense, is the lowest. (Sales revenue is unaffected by the inventory costing method.)3. LIFO results in the lowest cost of ending inventory($240)because under LIFO, the ending inventory is costed at the oldest costs. When costs are increasing, the oldest costs are the lowest costs.LIFO results in the highest cost of goods sold. This occurs because the last costs of the period are assigned to cost of goods sold. When costs are increasing, the last costs are the highest.LIFO results in the lowest gross profit because cost of goods sold, the expense, is the highest. (Sales revenue is unaffected by the inventory costing method.)(10 min.) CP 6-5a b cAverageCost FIFO LIFO Cost of goods sold:Average (50 @ $15*) $750FIFO (10 @ $10) + (25 @ $14) + (15 @ $18) $720LIFO (25 @ $18) + (25 @ $14) $800 Ending inventory:Average (10 @ $15*) $150FIFO (10 @ $18) $180LIFO (10 @ $10) $100 _____*Average cost= ($100 + $350 + $450)= $15per unit (10 + 25 + 25)(10-15 min.) CP 6-6Kinko’sIncome StatementYear Ended December 31, 20XXAverage FIFO LIFO Sales revenue (600 ⨯ $20) $12,000 $12,000 $12,000 Cost of goods sold (600 ⨯ $9.90*)5,940(100 ⨯ $9) + (500 ⨯ $10) 5,900(600 ⨯ $10) 6,000 Gross profit 6,060 6,100 6,000 Operating expenses 4,000 4,000 4,000 Net income $ 2,060 $ 2,100 $ 2,000 _____*Beginning inventory (100 @ $9.20)…………..$ 920 Purchases (700 @ $10)………………………… 7,000Goods available…………………….……………$7,920 Average cost per unit $7,920 / 800 units…$ 9.90(10 min.) CP 6-7Kinko’sIncome StatementYear Ended December 31, 20XXAverage FIFO LIFO Sales revenue (600 ⨯ $20) $12,000 $12,000 $12,000 Cost of goods sold (600 ⨯ $9.90*)5,940(100 ⨯ $9) + (500 ⨯ $10) 5,900(600 ⨯ $10) ______ ______ 6,000 Gross profit 6,060 6,100 6,000 Operating expenses 4,000 4,000 4,000 Income before income tax $ 2,060Income tax expense (40%) $ 824*From CP 6-6(5 min.) CP 6-8 Lands’ End managers can delay purchases of inventory until the next year. Under LIFO, high inventory costs that would have been paid for inventory do not become expense as cost of goods sold in the current year. As a result, the current year’s income statement reports a higher net income than Lands’ End would have reported if the company had replaced inventory before year end.(5-10 min.) CP 6-9Millions BALANCE SHEETCurrent assets:Inventories, at market (which is lower than cost).. $ 330 INCOME STATEMENTCost of goods sold [$1,001 + ($333 –$330)]…………$1,004(10 min.) CP 6-101. FIFO2. LIFO Gross profitpercentage:Gross profit= $460*= 46%$340**= 34%Net sales revenue $1,000 $1,000 _____* $1,000 – $540 = $460** $1,000 – $660 = $340Inventory turnover:Cost of goods sold= $540 $660Average inventory ($100 + $360) / 2 ($100 + $240) / 2= 2.3 times = 3.9 times3. Gross profit percentage — FIFO looks better.4. Inventory turnover — LIFO looks better.(10-15 min.) CP 6-11 1. Beginning inventory……………………………... $ 300,000+ Purchases……………………………………….… 1,600,000 = Goods available…………………………………... 1,900,000 –Cost of goods sold………………………………. (1,800,000) = Ending inventory……………………………….…2. Beginning inventory……………………………..+ Purchases……………………………………….…= Goods available…………………………………...–Cost of goods sold:Sales revenue……………………….$3,000,000Less estimated gross profit (40%) (1,200,000)Estimated cost of goods sold……………….= Estimated cost of ending inventory…………... $ 100,000(5-10 min.) CP 6-12CorrectAmount(Millions)a. Inventory ($333 + $3)…………………………………$ 336b. Net sales (unchanged)……………………………….$1,755c. Cost of goods sold ($1,001 –$3)…………………...$ 998d. Gross profit ($754 + $3)……………………….……..$ 757(10 min.) CP 6-13 1. Last year’s reporte d gross profit was understated.Correct gross profit last year was $5.6 million ($4.0 + $1.6). 2. This year’s gross profit is overstated.Correct gross profit for this year is $3.2 million ($4.8 – $1.6).3. Lang’s perspective is better because correcti ng the errorchanges the trend of correct gross profit from up (good) to down (bad), as follows:MillionsLast Year This Year Trend Reported gross profit……..$4.0 $4.8 Up (Good) Correct gross profit……….$5.6 $3.2 Down (Bad)(5-10 min.) CP 6-14 1. Ethical. There is nothing wrong with buying inventorywhenever a company wishes.2. Ethical. Same idea as 1.3. Unethical. The company falsified its reported amounts ofinventory and net income.4. Unethical. The company falsified its reported inventorypurchases, cost of goods sold, and net income in order to cheat the government (and the people) out of income tax.5. Unethical. The company falsified its reported amount ofinventory in order to cheat the government (and the people) out of taxes.Exercises(15-20 min.) E 6-1 Req. 1 (journal entried)Perpetual System1. Purchases: ThousandsInventory…………………….……….… 2,200Accounts Payable………………….2,2002. Sales:Cash ($3,500 ⨯.20) (700)Accounts Receivable ($3,500 ⨯ .80). 2,800Sales Revenue…………….……….3,500 Cost of Goods Sold………………….. 2,100Inventory………………….………....2,100Req. 2 (financial statement amounts)BALANCE SHEET Thousands Current assets:Inventory ($370 + $2,200 – $2,100)... $ 470 INCOME STATEMENTSales revenue…………………………….$3,500Cost of goods sold……………………… 2,100Gross profit……………………………….$1,400(15-25 min.) E 6-2JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT1 Inventory ($640 + $1,870 + $900)……….3,410Accounts Payable………………………3,4102 Accounts Receivable (17 @ $500)……...8,500Sales Revenue…………………………..8,500 Cost of Goods Sold……………………….2,800*Inventory…………………………………2,8003 Sales revenue………………………………$8,500Cost of goods sold……………………….. 2,800Gross profit…………………………………$5,700Ending inventory ($800 + $3,410 –$2,800)……...$1,410 _____*(9 @ $160) + (8 @ $170) = $2,800(10-15 min.) E 6-3 1.Cost of Goods Sold Ending Inventory(a) Specificunit cost (6 @ $160) + (11 @ $170) = $2,830 (3 @ $160) + (5 @ $180) = $1,380 (b) Averagecost 17 ⨯ $168.40* = $2,863 8 ⨯ $168.40* = $1,347 _____*Average cost per unit = ($800 + $640 + $1,870 + $900)= $168.40(5 + 4 + 11 + 5)(c) FIFO (9 @ $160) + (8 @ $170) = $2,800 (5 @ $180) + (3 @ $170) $1,410(d) LIFO (5 @ $180) + (11 @ $170) + (1 @ $160) $2,930 (8 @ $160) $1,2802. LIFO produces the highest cost of goods sold.FIFO produces the lowest cost of goods sold.The increase in inventory cost from $160 to $170 to $180 per unit causes the difference in cost of goods sold.(15-20 min.) E 6-4 Cost of goods sold:LIFO ($2,930) –FIFO ($2,800)…………………………$130 In come tax rate……………………………………….. .35 LIFO advantage in tax savings…………………………..$ 46(15 min.) E 6-51. a. FIFOCost of goods sold:(5 @ $90) + (5 @ $95)……………...$925Ending inventory:7 @ $95………………………………$665b. LIFOCost of goods sold:10 @ $95……………………………..$950Ending inventory:(5 @ $90) + (2 @ $95)……………...$6402.VPA, Inc.Income StatementMonth Ended May 31, 20XXSales revenue (3 @ $150) + (7 @ $155)................$1,535 Cost of goods sold. (925)Gross profit (610)Operating expenses (310)Income before income tax (300)Income tax expense (40%) (120)Net income………………………………………………$ 180(15 min.) E 6-6Millions1. Gross profit: FIFO LIFOSales revenue……………………………………$4.9 $4.9 Cost of goods soldFIFO: 600,000 ⨯$7…………………………… 4.2LIFO: (400,000 ⨯ $5) + (100,000 ⨯ $6)+ (100,000 ⨯$7)……………………… 3.3 Gross profit………………………………………$ .7 $1.6 2. Gross profit under FIFO and LIFO differ because inventorycosts decreased during the period.If you base your prediction on the decrease in inventory unit cost, then, yes, you would predict that LIFO gross profit would be higher.But if you assume that FIFO produces higher gross profit, then, no, the actual result does not follow your prediction.(15-20 min.) E 6-7 DATE: _____________TO: Rick TaborFROM: Student NameSUBJECT: Proposal for Saving Income TaxWe can save income tax by buying above-normal quantities of inventory before the end of the year. Inventory costs are rising, and the company uses the LIFO inventory method. Under LIFO, the higher cost of year-end purchases of inventory goes straight into cost of goods sold. This increases cost of goods sold and decreases net income and income taxes. Because our inventory levels are lower than normal, we need the inventory anyway. In effect, we can use our cash to buy inventory or to pay income taxes. I think it would be wiser to buy inventory.(10-15 min.) E 6-8 Specificunit cost 1. Used to account for automobiles, jewelry, and art objects.Average 2. Provides a middle-ground measure of ending inventory and cost of goods sold.FIFO 3. Maximizes reported income.LIFO 4. Matches the most current cost of goods sold against sales revenue.LIFO 5. Results in an old measure of the cost of ending inventory.LIFO 6. Generally associated with saving income taxes. FIFO 7. Results in a cost of ending inventory that is close to the current cost of replacing the inventory.LIFO 8. Enables a company to buy high-cost inventory at year end and thereby to decrease reportedincome.LIFO 9. Enables a company to keep reported income from dropping lower by liquidating older layers ofinventory.LCM 10. Writes inventory down when replacement cost drops below historical cost.(5-10 min.) E 6-9Jeffrey CorporationIncome Statement (partial)Year Ended December 31, 20X4Sales revenue ………………………………………………$225,000 Cost of goods sold [$110,000 + ($18,000 – $17,000)].. 111,000 Gross profit…………………………………………………$114,000 Note: Cost was used for beginning inventory because cost was lower than market. Market (replacement cost) wasused for ending inventory because market was lowerthan cost.(20-25 min.) E 6-10(15-20 min.) E 6-11 (Amounts in millions)a. $ 1,055 (Let a = beginning inventory;a + $7,344 – $1,294 = $7,105a = $1,055)b. $ 12,459 ($19,564 – $7,105)d. $150,255 ($191,329 – $41,074)c. $151,904 (Let c = Purchases;$19,793 + c– $21,442 = $150,255c = $151,904)e. $ 12,650 ($33,726 – $21,076)f. $ 4,367 ($972 + $3,395)g. $ 546 ($513 + $1,005 – $972)The Coca-Cola CompanyIncome StatementYear Ended December 31, 20XX(Millions) Net sales $19,564Cost of goods soldBeginning inventory $1,055Net purchases 7,344Goods available 8,399Ending inventory (1,294)Cost of goods sold 7,105 Gross profit 12,459Operating and other expenses 7,886Income before tax 4,573Income tax expense ($4,573 .333) 1,523Net income $ 3,050(20-30 min.) E 6-12Company Gross ProfitPercentage Inventory TurnoverCoca-Cola $12,459= 63.7%$7,105= 6.0 times $19,564 ($1,055 + $1,294) / 2Wal-Mart$41,074= 21.5%$150,255= 7.3 times $191,329 ($19,793 + $21,442) / 2Intel $21,076= 62.5%$12,650= 6.8 times $33,726 ($1,478 + $2,241) / 2Estée Lauder $3,395= 77.7%$972= 1.8 times $4,367 ($513 + $546) / 2These ratio values explain the merchandising philosophies of these companies. Wal-Mart has the lowest gross profit percentage (21.5%) and the fastest rate of inventory turnover (7.3 times per year). This makes sense for a volume discounter.Estée Lauder has the highest gross profit percentage (77.7%) and the slowest inventory turnover (1.8 times per year). High markups and low turnover go hand-in-hand.Coca-Cola’s and Intel’s ratios fall between these extremes. These ratio data suggest that Intel is the most profitable company of this group.(10 min.) E 6-13Billions Sales……………………………………………...$45.7 Cost of goods soldBeginning inventory………………………..$ 5.5Purchases……………………………………. 33.2Goods available……………………………..38.7Ending inventory…………………………… (6.6)Cost of goods sold…………………………. 32.1 Gross profit……………………………………..$13.6Gross profit percentage = $13.6= 29.8% $45.7Inventory turnover =$32.1= 5.3 times ($5.5 + $6.6) / 2(10-15 min.) E 6-14 Year ended January 31, 20X4: Millions Budgeted cost of goods sold ($6,500 1.08)………... $7,020 Budgeted ending inventory…………………………….. 2,200 Budgeted goods available………….…………………… 9,220 Actual beginning inventory…………………………….. (1,900) Budgeted pu rchases…………………………………….. $7,320(10-15 min.) E 6-15 Beginning inventory………………………$ 48,000 Net purchases……………………………… 136,000 Goods available……….…………………...184,000 Cost of goods sold:Net sales revenue……………………… $200,000Less estimate d gross profit of 40%… (80,000)Estimated cost of goods sold………... 120,000 Estimated cost of inventory destroyed.. $ 64,000Another reason managers use the gross profit method to estimate ending inventory is to test the reasonableness of ending inventory from (a) the perpetual inventory records or (b) a physical count.(10-15 min.) E 6-16Allergan, Inc.Income StatementYear Ended September 30,20X5 20X4Sales revenue $149,000 $122,000 Cost of goods sold:Beginning inventory $27,000 $12,000Net purchases 72,000 66,000 Goods available 99,000 78,000 Ending inventory (16,000) (27,000)*Cost of goods sold 83,000 51,000 Gross profit 66,000 71,000 Operating expenses 30,000 20,000 Net income $ 36,000 $ 51,000 *$18,000 + $9,000 = $27,000Allergan actually performed poorly in 20X5, compared to 20X4, with net income down from $51,000 to $36,000. The understatement of inventory at the end of 20X4 caused 20X4 net income to be understated. Then this same error caused 20X5 net income to be overstated, giving the false impression that profits were higher in 20X5. In reality, net income was down in 20X5.(10 min.) E 6-17Millions INCOME STATEMENTSales revenue…………………………………………..$18,144 Cost of goods sold ($5,456 –$100)………………... 5,356 Gross profit……………………………………………..$12,788(5-10 min.) E 6-18a. Use average cost.b. Use FIFO.c. Use FIFO.d. Use any method. They all produce the same resultsbecause costs are stable.e. Buy inventory late in the year.f. Company is using LIFO.(20-30 min.) E 6-19 Req. 1Actual cost of goods sold =1. From purchase in December (30 @ $1,300)……..$ 39,0002. From purchase in June (50 @ $1,200)…………….60,0003. From purchase in February (20 @ $1,100)……….22,0004. From beginning inventory (30 @ $1,000)………... 30,000Actual cost of goods sold………………………..$151,000Req. 2Cost of goods sold with the additional year-end purchase (this would have avoided a LIFO liquidation) =1. From purchase in December (60* @ $1,300)…….$ 78,0002. From purchase in June (50 @ $1,200)…………….60,0003. From purchase in February (20 @ $1,100)………. 22,000Cost of goods sold (with no LIFO liquidation). $160,000 _____*Must purchase a total of 60 units in December to keep ending inventory at 40 units, which was the level of beginninginventory.(continued) E 6-19 Req. 3The LIFO liquidation•Boosted gross profit by $9,000 ($160,000 – $151,000).•Cost the company $3,600 ($9,000 ⨯ .40) in income tax.•Boosted net income by $5,400 ($9,000 – $3,600).•Was bad for the company because the additional income tax drained off valuable cash. Paying the added tax was not worth the boost in net income because the company would have to replenish its inventory anyway, so it’s better to go ahead and buy the goods before year end. That action would save the cash that was wasted on taxes.(20-30 min.) E 6-20 Sales, gross profit, net income, the gross profit percentage, and inventory turnover showed the following trends:Dollars in millions 20X7 20X6 20X5 Sales $37.0 $35.9 $33.7 Cost of sales 29.7 28.1 26.3 Gross profit 7.3 7.8 7.4Net income (net loss) (0.2) 0.4 0.5Gross profit= $7.3= .197$7.8= .217$7.4= .220percentage $37.0 $35.9 $33.7Inventory= $29.7= 4.4$28.1= 4.1$26.3= 4.1turnover ($7.1 + $6.4) / 2 ($6.5 + $7.1) / 2 ($6.4 + $6.5) / 2The gross profit percentage dropped significantly while the rate of inventory turnover improved. This suggests that Zmart was having to discount its merchandise more and more just to sell the goods. The end result was a net loss in 20X7.Selling, general and administrative expenses increased significantly, which suggests that Zmart was having to advertise heavily in order to sell its inventory.Practice Quiz1. d ($7,200 – $5,500 = $1,700)2. b ($2,000 + $6,000 – $5,500 = $2,500)3. a4. c [(3,400 @ $10.75) + (100 @ $10.30) = $37,580]5. d (3,400 @ $10.75 = $36,550)6. a7. d ($144,000 + $216,000 = $360,000)8. c9. c10. c [$620,000 – ($70,000 + $400,000 – $40,000) =$190,000]11. b ($10,000 + X – $15,000 = $90,000; X = $95,000)12. c13. d [($500,000 – $200,000) ($25,000 + $35,000) / 2] =10 times14. a Net sales = $480,000 ($490,000 – $10,000)COGS = $50,000 + ($230,000 + $20,000 – $6,000–$4,000) – $40,000 = $250,000GP% = ($480,000 – $250,000) / $480,000 = 47.9%15. b $53,500 + $75,500 – $93,000 (1 – .30) = $63,90016. b17. aProblemsGroup A(20-30 min.) P 6-1A Req. 1Inventory……………………………………..9,580,000 Accounts Payable……………………….9,580,000Accounts Payable………………………….9,110,000 Cash……………………………………….9,110,000Cash…………………………………………..4,700,000Accounts Receivable………………………8,700,000 Sales Revenue…………………………… 13,400,000 Cost of Goods Sold………………………...9,880,000Inventory…………………………………..9,880,000 [$6,300,000 + $1,360,000 + $1,920,000 + (10,000 units ⨯ $30*)]_____*$1,500,000 / 50,000 units = $30 per unit.Operating Expenses………………………..2,130,000 Cash ($2,130,000 ⨯2/3)………………….1,420,000 Accrued Liabilities ($2,130,000 ⨯ 1/3)... 710,000 Income Tax Expense……………………….556,000 Income Tax Payable……………………..556,000 [($13,400,000 – $9,880,000 – $2,130,000) ⨯ .40 = $556,000](continued) P 6-1A Req. 2Req. 3Lord & Taylor - AtlantaIncome StatementYear Ended January 31, 20X0Sales revenue ……………………………$13,400,000Cost of goods sold…………………….. 9,880,000Gross profit………………………………3,520,000Operating expenses…………………… 2,130,000Income before t ax………………………1,390,000Income tax expense (40%)……………. 556,000Net income……………………………….$ 834,000(20-30 min.) P 6-2A Req. 1The store uses FIFO.This is apparent from the flow of costs out of inventory. For example, the March 8 sale shows a unit cost of $19, which came from the beginning inventory. This is how FIFO, and only FIFO, works.Req. 2Cost of goods sold:27 ⨯$19 = $ 51323 ⨯ 19 = 4371 ⨯ 20 = 2025 ⨯ 20 = 500$1,470Sales 27 + 23 = 50 units ⨯ $36 = $1,8001 + 25 = 26 units ⨯ $37 = 962 $2,762 Cost of goods sold……………………………………. (1,470) Gross profit……………………………………………...$1,292 Req. 3Cost of March 31 inventory (24 ⨯ $21) + (10 ⨯ $20). $ 704(20-30 min.) P 6-3A Req. 1Cost of Goods Sold Ending Inventory Average cost 696 ⨯ $82.6626* $57,533 214 ⨯ $82.6626* $17,690 ____*Average cost= ($10,640 + $17,577 + $7,790 + $17,640 + $21,576)= $82.6626per unit (140 + 217 + 95 + 210 + 248)FIFO (140 @ $76) + (217 @ $81)+ ( 95 @ $82) + (210 @ $84)+ ( 34 @ $87) = $56,605 214 @ $87 = $18,618 LIFO (248 @ $87) + (210 @ $84)+ ( 95 @ $82) +(143 @ $81) = $58,589 140 @ $76 +(74 @ $81) = $16,634(continued) P 6-3A Req. 2LIFO’s cost of goods sold is highest for Hot Wheels because (a) the company’s prices are rising and (b) LIFO assigns to cost of goods sold the cost of the latest inventory purchases. When costs are rising, these latest inventory costs are the highest, and that makes cost of goods sold the highest under LIFO.Req. 3Hot Wheels Motorcycles, Inc.Income StatementMonth Ended December 31, 20XXSales revenue (696 @ $130)……………………..$90,480Cost of goods sold……………………………….. 58,589Gross profit…………………………………………31,891Operating expenses……………………………… 22,000Income before income taxes…………………….9,891Income tax expense (40%)………………………. 3,956Net income………………………………………….$ 5,935(30-40 min.) P 6-4A Req. 1 (partial income statementsBlockbuster Digital ImagesIncome StatementYear Ended December 31, 20XXAVERAGE FIFO LIFOSales revenue $11,200 $11,200 $11,200Cost of goods sold 8,392 8,255 8,520 Gross profit $ 2,808 $ 2,945 $ 2,680 Computations of cost of goods sold:Average cost= ($1,215 + $2,520 + $2,010 + $1,400 + $2,590)= $3.3569per unit (400 + 800 + 600 + 400 + 700)COGS at average cost = 2,500 $3.3569 = $8,392 FIFO COGS = (300 @ $3.00) + (900 @ $3.15) + (600 @ $3.35) + (400 @ $3.50)+ (300 @ $3.70)= $8,255 LIFO COGS = (700 @ $3.70) + (400 @ $3.50) + (600 @ $3.35) + (800 @ $3.15) = $8,520(continued) P 6-4A Req. 2Use the FIFO method to report the highest net income because cost of goods sold is lowest (gross profit is highest) under FIFO when inventory costs are rising.(15-20 min.) P 6-5A LM Electronics should apply the lower-of-cost-or-market rule to account for inventories. The current replacement cost of ending inventory is less than LM’s actual cost, so LM must write the inventory down to current replacement cost, with the following journal entry:Cost of Goods Sold…………1,500,000Inventory…………………..1,500,000 To write inventory down to market value.LM should report the following amounts in its financial statements:BALANCE SHEETInventory ($8,900,000 –$1,500,000)……………..$ 7,400,000 INCOME STATEMENTCost of goods sold ($27,400,000 + $1,500,000). $28,900,000 Accounting conservatism is the reason to account for inventory at the lower of cost or market value. Conservatism directs accountants to write inventory down if cost appears unrealistically high. In this case conservatism comes into play because the current replacement cost (ma rket value) of LM’s ending inventory is less than cost. Under the lower-of-cost-or-market rule, this requires a write-down of the inventory value to current replacement cost.Student responses may vary.(20-30 min.) P 6-6A Req. 1Hershey TargetMillionsGross profit percentage:Sales……………………$4,221 $36,362 Cost of sales………….. 2,471 25,295 Gross profit……………$1,750 $11,067Gross profit $1,750= 41.5% $11,067= 30.4%percentage: $4,221 $36,362 Inventory turnover:Cost of goods sold= $2,471 $25,295Average inventory ($605 + $602) / 2 ($4,248 + $3,798) / 2= 4.1 times = 6.3 timesReq. 2These statistics do not indicate which company should be more profitable. Hershey has a higher gross profit percentage, but Target turns its inventory over more rapidly. On one measure Hershey looks better; on the other measure Target is better. Another factor that makes it difficult to tell which company should be more profitable is that the gross profit percentage and inventory turnover do not take into account operating expenses.(25-30 min.) P 6-7A Req. 1 (estimate of ending inventory by the gross profit method)Beginning inventory………………………$1,292,000 Purchases…………………………………..$6,585,000 Less: Purchase dis counts…………..(149,000)Purchase returns……………… (8,000) Net purchases…………………………... 6,428,000 Goods available……………………………7,720,000 Cost of goods sold:Sales revenue…………………………… $8,657,000Less: Sales returns…………………. (17,000) Net sales………………………………….8,640,000Less: Estimated gross profit of 40%.. (3,456,000)Estimated cost of goods sold………... 5,184,000 Estimated cost of ending inventory……$2,536,000(continued) P 6-7A Req. 2 (income statement through gross profit)Kinko’sIncome Statement (partial)Month of March, 20XXSales revenue…………………………..$8,657,000 Less: Sales returns………………… (17,000)Net sales revenue…………………...8,640,000 Cost of goods sold……………………. 5,184,000*Gross profit……………………………..$3,456,000_____*Cost of goods sold:Beginning inventory………………………...$1,292,000Purchases……………………...$6,585,000Less: Purchases discounts. (149,000)Purchase returns……. (8,000)Net purc hases……………………………….. 6,428,000Goods available……………………………...7,720,000Less: Ending inventory……………………. (2,536,000)Cost of goods sold………………………….$5,184,000(20-30 min.) P 6-8A Req. 1Cost of sales, budgeted ($720,000 ⨯ 1.05).. $756,000+ Ending inventory, budgeted………………... 80,000= Cost of goods available……………………...836,000–Beginning inventory…………………………. (70,000)= Purchases, budgeted ………………………..$766,000Req. 2Stop-n-Go StoreBudgeted Income StatementYear Ended December 31, 20X4Sales ($960,000 ⨯1.05)……………………..$1,008,000Cost of sales ($720,000 ⨯1.05)…………… 756,000Gross profit…………………………………...252,000Operating expenses………………………… 102,000Net income……………………………………$ 150,000(15-20 min.) P 6-9A Req. 1 (corrected income statements)Monaco Gemstones, Inc.Income Statement (adapted; amounts in thousands)Years Ended 2007, 2006, and 20052007 2006 2005Net sales revenue……………...$1,412 $1,231 $1,138 Cost of goods sold:Beginnin g inventory………..$ 249 $ 309 $ 234Purchases…………………… 859 729 663Goods available……………..1,108 1,038 897Ending inventory…………… (311) (249) (309)Cost of goods sold………… 797 789 588 Gross profit……………………..615 442 550 Operating expenses…………... 500 437 420 Net income………………………$ 115 $ 5 $ 130(continued) P 6-9A Req. 2 (net income and owner equity effects of inventory errors)Prior to correction: 2007 2006 2005Net income for the year was Under by $20 million Over by $70 million Under by $50 millionReq. 3The corrections did not change total net income over the three-year period. The corrections made the company’s trend of net income look worse —with net income dropping sharply in 2006 and with 2007’s net income lower than net income in 2005.ProblemsGroup B(20-30 min.) P 6-1B Req. 1Inventory…………………………………….11,500,000 Accounts Payable………………………11,500,000Accounts Payable………………………….11,390,000 Cash……………………………………….11,390,000Cash………………………………………….5,300,000Accounts Receivable……………………...11,100,000 Sales Revenue…………………………..16,400,000 Cost of Goods Sold.…………………….…12,100,000Inventory………………………………….12,100,000 [$6,300,000 + $3,250,000 + $1,950,000 + (10,000 units ⨯ $60*)]_____*$1,200,000 ) 20,000 units = $60 per unitOperating Expenses……………………….4,000,000 Cash ($4,000,000 ⨯.80)………………...3,200,000 Accrued Liabilities ($4,000,000 ⨯ .20). 800,000 Income Tax Expense………………………120,000 Income Tax Payable……………………120,000 [($16,400,000 – $12,100,000 – $4,000,000) ⨯ .40 = $120,000]。

西方会计学课后题答案第二章

西方会计学课后题答案第二章1、以下有关“资产=负债+所有者权益”等式的表述不正确的是()。

[单选题] *是编制资产负债表的理论基础表明了企业一定时期的财务状况(正确答案)反映了资产、负债、所有者权益三要素之间的内在联系和数量关系该等式也称为静态会计等式2.下列各项中,导致企业当期营业利润减少的是()。

[单选题] *租出非专利技术的摊销额(正确答案)对外公益性捐赠的商品成本支付的税收滞纳金自然灾害导致生产线报废净损失3.下列各项中,关于企业应付票据会计处理的表述正确的是()。

[单选题] *应将到期无力支付的商业承兑汇票的账面余额转作短期借款申请银行承兑汇票支付的手续费应计入当期管理费用应将到期无力支付的银行承兑汇票的账面余额转作应付账款应以商业汇票的票面金额作为应付票据的入账金额(正确答案)4.下列各项中,企业销售商品收到银行承兑汇表应借记的会计科目是() [单选题] *其他应收款应收票据(正确答案)其他货币资金银行存款5.企业以银行存款偿还到期的短期借款,关于这笔经济业务,下列说法正确的是()。

[单选题] *导致资产、负债同时减少(正确答案)导致资产、负债同时增加导致负债内部增减变动,总额不变导致所有者权益减少,负债减少6.某企业赊销设备一台,成本50万元,合同约定三个月内付款,应填制() [单选题] *付款凭证转账凭证(正确答案)收款凭证累计凭证7.下列各项中,不影响留存收益总额的是()。

[单选题] *以盈余公积发放现金股利以盈余公积转增资本以盈余公积弥补亏损(正确答案)以实现的净利润分配现金股利某企业2020年当期所得税费用为650万元,递延所得税负债的年初数为45万元,年末数为58万元;递延所得税资产的年初数为36万元,年末数为32万元。

不考虑其他因素,该企业2020年应确认的所得税费用为()万元。

[单选题] *650633667(正确答案)6639.2019年10月1日,甲股份有限公司委托证券公司发行股票5 000万股,每股面值1元,每股发行价格6元,向证券公司支付佣金900万元,从发行收入中扣除。

西方财务会计第六章答案

西方财务会计第六章答案chapter 6 Accounting for merchandising businessesClass Discussion Questions1. Mercha ndising businesses acquire merchandise for resale to customers. It is the selling ofmerchandise, instead of a service, that makes the activities of a merchandising business dif-ferent from the activities of a service business.2. Yes. Gross profit is the excess of (net) sales over cost of merchandise sold. A net loss ariseswhen operating expenses exceed gross profit. Therefore, a business can earn a gross profit but incur operating expenses in excess of this gross profit and end up with a net loss.3. a. Incr ease c. Decreaseb. Increase d. Decrease4. U nder the periodic method, the inventory records do not show the amount available for saleor the amount sold during the period. In contrast, under the perpetual method of accounting for merchandise inventory, each purchase and sale of merchandise is recorded in the invento-ry and the cost of merchandise sold accounts. As a result, the amount of merchandise availa-ble for sale and the amount sold are continuously (perpetually) disclosed in the inventory records.5. The multiple-step form of income statement contains conventional groupings for revenuesand expenses, with intermediate balances, before concluding with the net income balance. In the single-step form, the total of all expenses is deducted from the total of all revenues, with-out intermediate balances.6. The major advantages of the single-step form of income statement are its simplicity and itsemphasis on total revenues and total expenses as the determinants of net income. The major objection to the form is that such relationships as gross profit to sales and income from opera-tions to sales are not as readily determinable as when the multiple-step form is used.7. a. 2% discount allowed if paid within ten days of date of invoice; entire amount of invoicedue within 60 days of date of invoice.b. Payment due within 30 days of date of invoice.c. Payment due by the end of the month in which the sale was made.8. a. A credit memorandum issued by the seller of merchandise indicates the amount for whichthe buyer's account is to be credited (credit to Accounts Receivable) and the reason for the sales return or allowance.b. A debit memorandum issued by the buyer of merchandise indicates the amount for whichthe seller's account is to be debited (debit to Accounts Payable) and the reason for the purchases return or allowance.9. a. The buyerb. The seller10. E xamples of such accounts include the following: Sales, Sales Discounts, Sales Returns andAllowances, Cost of Merchandise Sold, Merchandise Inventory.Ex. 6–1a. $490,000 ($250,000 + $975,000 – $735,000)b.40% ($490,000 ÷ $1,225,000)c. No. If operating expenses are less than gross profit, there will be a net income. On the otherhand, if operating expenses exceed gross profit, there will be a net loss.Ex. 6–2 : $15,710 million ( $20,946 million – $5,236 million ) Ex. 6–3a. Purchases discounts, purchases returns and allowancesb. Transportation in;c. Merchandise available for saled. Merchandise inventory (ending)Ex. 6–41. The schedule should begin with the January 1, not the December 31, merchandise inventory.2. Purchases returns and allowances and purchases discounts should be deducted from (notadded to) purchases.3. The result of subtracting purchases returns and allowances and purchases discounts frompur chases should be labeled ―net purchases.‖4. Transportation in should be added to net purchases to yield cost of merchandise purchased.5. The merchandise inventory at December 31 should be deducted from merchandise availablefor sale to yield cost of merchandise sold.A correct cost of merchandise sold section is as follows:Cost of merchandise sold:Merchandise inventory, January 1, 2006 ........ $132,000 Purchases ........................................................... $600,000Less: Purchases returns and allowances$14,000Purchases discounts .............................. 6,000 20,000 Netpurchases ..................................................... $580,000Add transportation in ....................................... 7,500Cost of merchandise purchased ................. 587,500 Merchandise available for sale ......................... $719,500 Less merchandise inventory,December 31, 2006....................................... 120,000 Cost of merchandise sold .................................. $599,500 Ex. 6–5 Net sales: $3,010,000 ( $3,570,000 – $320,000 – $240,000 ) Gross profit: $868,000 ( $3,010,000 – $2,142,000 )Ex. 6–6THE MERIDEN COMPANYIncome StatementFor the Year Ended June 30, 2006Revenues:Net sales ................................................................................. $5,400,000Rent revenue ......................................................................... 30,000Total revenues................................................................... $5,430,000 Expenses:Cost of merchandise sold ..................................................... $3,240,000Selling expenses .................................................................... 480,000 Administrative expenses ...................................................... 300,000 Interest expense .................................................................... 47,500 Total expenses ................................................................... 4,067,500 Net income ..................................................................................... $1,362,500Ex. 6–71. Sales returns and allowances and sales discounts should be deducted from (not added to)sales.2. Sales returns and allowances and sales discounts should be deducted from sales to yield "netsales" (not gross sales).3. Deducting the cost of merchandise sold from net sales yields gross profit.4. Deducting the total operating expenses from gross profit would yield income from operations(or operating income).5. Interest revenue should be reported under the caption ―Other income‖ and should be addedto Income from operations to arrive at Net income.6. The final amount on the income statement should be labeled Net income, not Gross profit.A correct income statement would be as follows:THE PLAUTUS COMPANYIncome StatementFor the Year Ended October 31, 2006Revenue from sales:Sales .................................................................... $4,200,000Less: Sales returns and allowances ............... $81,200Sales discounts ....................................... 20,300 101,500Net sales ........................................................ $4,098,500 Cost of merchandise sold ........................................ 2,093,000 Gross profit .............................................................. $2,005,500 Operating expenses:Selling expenses ................................................. $ 203,000Transportation out ............................................ 7,500Administrative expenses ................................... 122,000Total operating expenses ............................ 332,500 Incomefrom operations .......................................... $1,673,000 Other income: Interest revenue ................................................. 66,500Net income ................................................................ $1,739,500 Ex. 6–8a. $25,000 c. $477,000 e. $40,000 g. $757,500b. $210,000 d. $192,000 f. $520,000 h. $690,000Ex. 6–9a. Cash ......................................................................................... 6,900Sales ................................................................................... 6,900 Cost of Merchandise Sold ...................................................... 4,830 Merchandise Inventory .................................................... 4,830b. Accounts Receivable ............................................................... 7,500Sales ................................................................................... 7,500 Cost of Merchandise Sold ...................................................... 5,625 Merchandise Inventory .................................................... 5,625c. Cash ......................................................................................... 10,200Sales ................................................................................... 10,200 Cost of Merchandise Sold ...................................................... 6,630 Merchandise Inventory .................................................... 6,630d. Accounts Receivable—American Express ........................... 7,200Sales ................................................................................... 7,200 Cost of Merchandise Sold ...................................................... 5,040 Merchandise Inventory .................................................... 5,040e. Credit Card Expense (675)Cash (675)f. Cash ......................................................................................... 6,875Credit Card Expense (325)Accounts Receivable—American Express ..................... 7,200Ex. 6–10It was acceptable to debit Sales for the $235,750. However, using Sales Returns and Allow-ances assists management in monitoring the amount of returns so that quick action can be taken if returns become excessive.Accounts Receivable should also have been credited for $235,750. In addition, Cost of Mer-chandise Sold should only have been credited for the cost of the merchandise sold, not the selling price. Merchandise Inventory should also have been debited for the cost of the merchandise re-turned. The entries to correctly record the returns would have been as follows: Sales (or Sales Returns and Allowances) ............................. 235,750 Accounts Receivable ......................................................... 235,750 Merchandise Inventory .......................................................... 141,450 Cost of Merchandise Sold ................................................ 141,450 Ex. 6–11a. $7,350 [$7,500 –$150 ($7,500 × 2%)]b. Sales Returns and Allowances .............................................. 7,500Sales Discounts (150)Cash ................................................................................... 7,350Merchandise Inventory .......................................................... 4,500 Cost of Merchandise Sold ................................................ 4,500Ex. 6–12(1) Sold merchandise on account, $12,000.(2) Recorded the cost of the merchandise sold and reduced the merchandise inventory account,$7,800.(3) Accepted a return of merchandise and granted an allowance, $2,500.(4) Updated the merchandise inventory account for the cost of the merchandise returned,$1,625.(5) Received the balance due within the discount period, $9,405. [Sale of $12,000, less return of$2,500, l ess discount of $95 (1% × $9,500).]Ex. 6–13a. $18,000b. $18,375c. $540 (3% × $18,000)d. $17,835Ex. 6–14a. $7,546 [Purchase of $8,500, less return of $800, less discount of $154 ($7,700 × 2%)]b. Merchandise InventoryEx. 6–15Offer A is lower than offer B. Details are as follows:A BList price ............................................................................... $40,000 $40,300Less discount ......................................................................... 800 403 $39,200 $39,897 Transportation (625)$39,825 $39,897Ex. 6–16(1) Purchased merchandise on account at a net cost of $8,000.(2) Paid transportation costs, $175.(3) An allowance or return of merchandise was granted by the creditor, $1,000.(4) Paid the balance due within the discount period: debited Accounts Payable, $7,000, and cre-dited Merchandise Inventory for the amount of the discount, $140, and Cash, $6,860.Ex. 6–17a. Merchandise Inventory .......................................................... 7,500Accounts Payable ............................................................. 7,500b. Accounts Payable ................................................................... 1,200Merchandise Inventory .................................................... 1,200c. Accounts Payable ................................................................... 6,300Cash ................................................................................... 6,174Merchandise Inventory (126)a. Merchandise Inventory .......................................................... 12,000Accounts Payable—Loew Co. ......................................... 12,000b. Accounts Payable—Loew Co. ............................................... 12,000Cash ................................................................................... 11,760Merchandise Inventory (240)c. Accounts Payable*—Loew Co. ............................................. 2,940Merchandise Inventory .................................................... 2,940d. Merchandise Inventory .......................................................... 2,000Accounts Payable—Loew Co. ......................................... 2,000e. Cash (940)Accounts Payable—Loew Co. (940)*Note: The debit of $2,940 to Accounts Payable in entry (c) is the amount of cash refund due from Loew Co. It is computed as the amount that was paid for the returned merchandise, $3,000, less the purchase discount of $60 ($3,000 × 2%). The credit toAccounts Payable of $2,000 in en-try (d) reduces the debit balance in the account to $940, which is the amount of the cash refund in entry (e). The alternative entries below yield the same final results.c. Accounts Receivable—Loew Co. .......................................... 2,940Merchandise Inventory .................................................... 2,940d. Merchandise Inventory .......................................................... 2,000Accounts Payable—Loew Co. ......................................... 2,000e. Cash (940)Accounts Payable—Loew Co. ............................................... 2,000 Accounts Receivable—Loew Co. .................................... 2,940Ex. 6–19a. $10,500b. $4,160 [($4,500 – $500) ? 0.99] + $200c. $4,900d. $3,960e. $834 [($1,500 – $700) ? 0.98] + $50Ex. 6–20a. At the time of sale c. $4,280b. $4,000 d. Sales Tax PayableEx. 6–21a. Accounts Receivable ............................................................... 9,720Sales ................................................................................... 9,000Sales Tax Payable (720)Cost of Merchandise Sold ...................................................... 6,300 Merchandise Inventory .................................................... 6,300b. Sales Tax Payable ................................................................... 9,175Cash ................................................................................... 9,175a. Accounts Receivable—Beta Co. ........................................... 11,500Sales ................................................................................... 11,500 Cost of Merchandise Sold ...................................................... 6,900 Merchandise Inventory .................................................... 6,900b. Sales Returns and Allowances (900)Accounts Receivable—Beta Co. (900)Merchandise Inventory (540)Cost of Merchandise Sold (540)c. Cash ......................................................................................... 10,388Sales Discounts (212)Accounts Receivable—Beta Co. ...................................... 10,600 Ex. 6–23a. Merchandise Inventory .......................................................... 11,500Accounts Payable—Superior Co. ................................... 11,500b. Accounts Payable—Superior Co. (900)Merchandise Inventory (900)c. Accounts Payable—Superior Co. ......................................... 10,600Cash ................................................................................... 10,388Merchandise Inventory (212)Ex. 6–24a. debit c. credit e. debitb. debit d. debit f. debitEx. 6–25(b) Cost of Merchandise Sold (d) Sales (e)Sales Discounts(f) Sales Returns and Allowances (g) Salaries Expense (j) Supplies ExpenseEx. 6–26a. 2003: 2.07 [$58,247,000,000 ÷ ($30,011,000,000 + $26,394,000,000)/2]2002: 2.24 [$53,553,000,000 ÷ ($26,394,000,000 + $21,385,000,000)/2]b.These analyses indicate a decrease in the effectiveness in the use of the assets to generateprofits. This decrease is probably due to the slowdown in the U.S. economy during 2002–2003. However, a comparison with similar companies or industry averages would be helpful in making a more definitive statement on the effectiveness of the use of the assets.Ex. 6–27a. 4.13 [$12,334,353,000 ÷ ($2,937,578,000 + $3,041,670,000)/2]b. Although Winn-Dixie and Zales are both retail stores, Zales sells jewelry at a much slowervelocity than Winn-Dixie sells groceries. Thus, Winn-Dixie is able to generate $4.13 of sales for every dollar of assets. Zales, however, is only able to generate $1.53 in sales per dollar of assets. This makes sense when one considers the sales rate for jewelry and the relative cost of holding jewelry inventory, relative to groceries. Fortunately, Zales is able to counter its slow sales velocity, relative to groceries, with higher gross profits, relative to groceries. Appendix 1—Ex. 6–28a. and c.SALES JOURNALCost of MerchandiseSold Dr.Invoice Post.Accts. Rec. Dr. MerchandiseDate No. Account Debited Ref.Sales Cr. Inventory Cr.2006Aug. 3 80 Adrienne Richt ................... ?12,000 4,0008 81 K. Smith .............................. ?10,000 5,50019 82 L. Lao .................................. ?9,000 4,00026 83 Cheryl Pugh ........................ ?14,000 6,50045,000 20,000b. andc.PURCHASES JOURNALAccounts Merchandise OtherPost Payable Inventory Accounts Post.Date Account Credited Ref.Cr. Dr. Dr. Ref. Amount2006Aug. 10 Draco Rug Importers ................. ?8,000 8,00012 Draco Rug Importers ................. ?3,500 3,50021 Draco Rug Importers ................. ?19,500 19,50031,000 31,000d.Merchandise inventory, August 1 ............................................... $ 19,000Plus: August purchases ................................................................ 31,000Less: Cost of merchandise sold ................................................... (20,000)Merchandise inventory, August 31 ............................................. $ 30,000ORQuantity Rug Style Cost2 10 by 6 Chinese* $ 7,5001 8 by 10 Persian 5,5001 8 by 10 Indian 4,0002 10 by 12 Persian 13,000 $ 30,000*($4,000 + $3,500)。

西方财务会计课后题9-12答案