GAAP_Matching Principle 一般公认会计原则

什么是公认会计原则(GAAP)

什么是公认会计原则(GAAP)当今社会,财务会计已经发展成一门务实的科学,它的发展依赖于一系列保证财务数据创建和使用的规范和标准,其中被称为公认会计原则(GAAP)的原则是其中最重要的部分。

公认会计原则的定义是指衡量和披露会计信息的概念性框架,其核心目标是实现信息透明,将当前和历史真实的经济状况披露出来,以及保证财务报告的一致性和可比性。

1. GAAP 都包括什么内容?GAAP 是一组框架,用于衡量和披露会计信息,它的内容涉及会计的两个主要方面:会计原则,准则,指导方针和方法。

其中,会计原则是最基本的,需要会计人员遵守和记录财务信息;会计准则是更高级的,系统性地整合会计原则;其他指导方针和方法,部分是更具体的参考,已经实施了会计原则和准则的具体披露。

2. GAAP 的历史渊源GAAP 可以追溯到 1933 年美国实行的《证券法》,该法在 U.S. 法律体系中规定,私营企业发行股票时,需要将其财务状况正确地披露出来,为了实现该要求,于是“美国联邦证券和交易委员会”(SEC)制定了相关的指导准则,从而催生了 GAAP 的概念。

3. GAAP 的发展趋势GAAP 的发展问世以来,一直在发展壮大,追求新高度,当前 GAAP 早已跳脱公司和法律框架,拓展到国际,它呼唤着国家与国家之间的信息共享,市场的全球化,行业的垄断,以及各公司的国际化,因此它的发展趋势也是不断地进行改变和完善。

4. GAAP 的实施和适用随着全球化的进程,越来越多的国家接受 GAAP,最终实现了 GAAP 统一适用,而 GAAP 的实施则需要政府、监管机构和财务会计技术人员紧密合作,形成系统框架,使得 GAAP 得以全面、有效地运用。

名词解释 gaap

gaap的名词解释

-----------------------------------------------------------------------------------------------GAAP是“Generally Accepted Accounting Principles”的缩写,翻译为“普遍公认的会计原则”。

它是指被广泛接受并用于财务报告与会计实践的一系列规则、标准和原则。

GAAP旨在确保财务报告的准确性、可比性和透明度,以便投资者、债权人和其他利益相关方能够理解和评估一个企业的财务状况。

以下是GAAP的一些关键特点和常见的原则:

1、重要性:GAAP强调将重要信息披露给用户,以影响他们对企业的经济决策。

2、一致性:GAAP要求企业在会计处理上保持一致性,以便不同时间段和实体之间进行比较。

3、实体概念:GAAP视企业为独立的法律实体,独立于其所有者和管理层。

4、费用效益:GAAP鼓励企业根据成本效益原则来确定会计政策

和过程。

5、包容性:GAAP希望涵盖各种类型的企业和交易,并提供灵活性以适应不同的行业和情况。

6、历史成本原则:GAAP要求企业以历史成本记录资产和负债,并在特定情况下进行调整。

7、全面收入原则:GAAP要求企业将其所有的经营活动、投资活动和筹资活动的收入都包括在内,以反映企业的全面财务状况。

需要注意的是,GAAP在不同国家和地区可能会有一些差异。

例如,美国的GAAP与国际上通用的国际财务报告准则(IFRS)存在一些差异。

因此,在特定的环境中,可能需要遵循适用的本地或行业特定的会计原则。

审计与财务会计的一个重要术语

审计与财务会计的一个重要术语“公认会计原则”在美国的发展葛家澍(厦门大学会计系 361005)作为财务会计的一个术语,或作为财务报告的一种规范,“公认会计原财”(principles GAAP)在会计界已众所周知。

但是,从2002年美国总统批准了((Sarbances and oxley Act》(2002年公开公司会计改革与投资者保护法案,以下简称SOA)之后,这一术语的性质和地位就有所改变。

一、民间提出,民间认可公认会计原则是1933年美国重新恢复在1929年爆发经济大危机时全面崩溃的证券市场(资本市场)的产物。

1929—1933年的美国经济大危机标志着自由化的市场经济严重失灵,这就需要政府进行干预并采取一种制度安排,最突出的政府干预是在罗斯福总统的领导和推动下,1933年颁布《证券法》和1934年颁布《证券交易法》并在1934年成立《证券交易委员会》(SEC)来执行这两个证券法规,对证市场实行严厉的监管。

然而,两个证券法规虽然要求制定会计准则,并没有涉及“GAAP”这个术语。

大约在1933年前后,美国会计协会(AIA①)和纽约证券交易所(NYSE)这两个机构都是民间组织,联合研究如何改进企业(主要是上市公司)的财务报表,经过讨论由AICPA发行了题为“公司帐目的的审查”(Audits of Corporate Accounts)的小册子。

其中:第一,首先用“原则(principles)代替“实务”(practies),修正了审计报告中的用语。

第二,其次建议在审计报告中表态时,使用“认可的会计原则”(Accepted Principles of Accounting)这样的字眼。

第三,为了表明什么是当时认可的会计原则,小册子列举了5条规则(这5条规则是1933年7月1日由纽约证券交易所的主席宣布的):1.未实现的利润(unrealized profit)不应直接或间接贷记收益帐户(Income account);在正常过程中已经生效的销售,才认为其中的利润已经发现;2.除非企业改组(neorganzition),宣布调整(如合并,变换了股东权益),或准改组(Quasi-neorgan-zition是在帐外消除亏损的一种特殊程序),否则,资本盈余(Capital surplies)不能用来调剂任何一年的收益;3.附属公司在合并以前赚得的盈余不能作为控股公司和附属公司的合并赚得的一部分;4.库藏股(Treaoury stock)的股利不能贷记收益帐户;5.由本企业高级职员、雇员和联系公司(Affili-tated companies)开出的应收票据和他们的欠款(应收帐款)在资产负债表中应单独表示。

GAAP_Historical Cost Principle 一般公认会计原则

GAAP – Historical cost / Cost principleThis discussion focus on the objectives, description and application of this principle. Examples will be given to strengthen the understanding and capability to apply this principle at real situation.Objective: To guide managers that the assets are recorded at their original cost and that the accounting record of the asset continues to be based on cost rather than on current market value.Description:The term “cost” refers to the amount spent when an item was originally obtained, whether that purchase happened last year or thirty years ago. For this reason, the amounts shown on financial statements are referred to as “historical cost” amounts.Application:Under this accounting principle, asset amount are not adjusted upward for inflation. In fact, as a general rule, asset amount does not reflect the amount of money a company would receive if it was to sell the asset at today’s market value.Advantages∙Historical cost accounts are straightforward to produce.∙Do not record gains until they are realized.∙Historical cost accounts are still used in most accounting systems Disadvantages∙Give no indication of current values of the assets of a business.∙Do not record the opportunity costs of the use of older assets, particularly property, which may be recorded at a value based on costs incurred many years ago.∙Do not measure the loss of value of monetary assets as a result of inflation.Example 1:Top Company purchased land in Year 1 for $300,000 in cash and continues to hold that land, the company's balance sheet in the year Yr 2 will report the land at $300,000 (even the market value of the land at Yr 2 is $500,000).Entry:Purchase of land in Yr 1Dr Land $300,000Cr Cash $300,000Balance sheet in Yr 1:Even the market value of the land is $500,000 in Yr 2, we should still report it as $300,000, the value paid when the land is purchased.Example 2:Fat Company purchased a piece of land for $400,000; some reasonable and necessary costs were included in the calculation of the Acquisition cost of Land. Such as fees paid to the county in $1,500, removal of an unwanted building was $100,000, and leveling was $20,000. What is the balance of Land account?Land $400,000Fees paid to the county 1,500Removal building 100,000Leveling +20,000Acquisition cost $521,500The balance of Land account is $521,500.Why?It’s because they are the costs of bringing the land to its intended use. Assume that Fat Company holds the land for one year, and then offers it for sale at price $1,000,000. The cost principle requires that the accounting value of the land remain at $521,500.Final comment:After discussing the historical cost above; here comes another value in accounting. “Mark-to-market” or “fair value accounting” refers to accounting for the value of an asset or liability based on the current market price of the asset or liability, or for similar assets and liabilities, or based on another objectively assessed "fair" value.Mark-to-market accounting can make values on the balance sheet change frequently, as market conditions change. In contrast, book value, based on the original cost/price of an asset or liability, is more stable. Mark-to-market accounting can become inaccurate if market prices deviate from the "fundamental" values of assets and liabilities because buyers and sellers are unable to collectively and accurately value the future value of income from assets and expenses from liabilities, possibly due to incorrect information or over-optimistic and over-pessimistic expectations.Despite of having several limitations in historical cost accounting, most of the people still believe that historical cost financial statements are more reliable than market value statements. As historical cost accounting is based on actual transactions, the recorded amounts are reliable and verifiable and free from management bias. In addition, under historical cost accounting, there is no scope for manipulation, because the data is supported by sufficient evidences such as: invoices, receipts etc.。

一般公认会计原则

谢谢观看

权责原则

在大多数情况下,公认会计原则规定,使用权责发生制会计,而非现金基础的会计。权责发生制原则会计, 坚持下面所讨论的收入确认,核对,及成本的原则,抓住了财务方面在会计期间发生时每一个经济活动,无论现 金何时易手。根据现金的基础会计,当该公司收到的现金或同等价值时才被计作收入,公司只有支付出现金或等 值项才计作开支。

一般公认会计原则

GAAP

目录

01 理论背景

02 基本假设

基本信息

Generally Accepted Accounting Principle是一般公认会计原则,1937年美国会计程序委员会(CAP)发 表第一号会计研究公告,开创了由政府机关或行业组织颁布“一般通用会计”的先河。

理论背景

理论背景

一般公认会计原则是指适用于各个不同行业的企业的,包括从会计的基本概念、基本假设等基本原理到具体 会计计量和编制财务报表的程序及方法的规定。通常一个国家的会计体系就是指一般通用会计。

一般可以分为国际性和区域性的,如美国的叫US GAAP中国的就是2006年新颁布的会计准则,一般由专门的 会计准则委员会制定。

充分公开原则要求财务报表包括披露该等资料。用脚注补充财务报表来转达这一信息,并说明该公司用于记 录和报告的商业交易的政策。

时间段

大多数企业存在很长一段时间,所以必须用人为的时间段来报告商业活动的结果。根据报告的类型,使用的 时间段可能会是一天,一个月,一年,或其他任意确定时期。

用人为的时间段导致某些交易应予如何记录的问题。举例来说,会计师应如何报告能使用五年的设备费用? 将整个费用报告在购买的那一年,可能使该公司在今年无利润和随后几年不合理的利润,一旦已经确立时间段, 会计师使用公认会计原则,以记录和报告会计期间的交易。

一般公认会计原则(GAAP)

一般公認會計原則(GAAP)壹、財務會計之環境一、會計的意義及基本特質會計的定義:*美國會計學會(AAA):會計是對經濟資訊的認定、衡量、與溝通的程序,以協助資訊使用者做審慎的判斷與決策。

」*美國會計師協會(AICPA):會計係一種服務性之活動,其功能在提供有關經濟個體之數量化資訊…尤其是財務資訊…予使用者,以便使用者藉此資訊在各種行動方案中,做一明智的抉擇。

」*會計可藉由三項基本特性而定義:(1)確認、衡量與溝通,(2)關於經濟個體的財務資訊,(3)給相關使用者以協助其釐定決策。

二、財務報表(financial statement)及財務報導(financial reporting)1.會計的兩大支派----財務會計與管理會計*財務會計之意義:研究如何提供有用資訊以幫助企業外部使用人做決策者,稱為財務會計。

*管理會計之意義:研究如何提供有用資訊以幫助企業內部管理當局做決策者,稱為管理會計。

2.財務報表(含附註揭露)為財務會計之最終產品,用以顯示一企業之財務資訊(會計資訊)。

財務報表包括資產負債表、損益表、現金流量表、業主權益變動表及財務報表附註,附註為財務報表不可分割(integral part)的一部份。

3.財務報表加上補充附表(supplementary schedules)及其他報導方式(如管理當局的討論及分析、財務預測、致股東函、公開說明書)合稱財務報導。

4.財務報表及財務報導之關係財務報導財務報表主要報表+附註+管理當局的討論及分析+財務預測+致股東函+公開說明書三、會計與資本分配1.資本市場分為初級市場與次級市場。

初級市場又稱發行市場,係指公司原始向社會大眾投資人發行股票、債券或其他權益憑證,亦即原始發行證券的市場。

次級市場又稱交易市場,為以發行證券之交易市場,如證券交易所及證券櫃檯買賣中心等,方便已發行證券之流通轉讓。

初級市場(發行市場) 股票資本市場投資人次級市場(交易市場) 公司債公司向外吸收資金貸款金融市場發行票券債權人賒帳2.資本分配過程四、財務會計所面臨之問題及挑戰1.挑戰(1)非財務指標(2)預期資訊(3)軟體資產(4)時效性2.為克服上述之挑戰,美國會計師協會特殊問題委員會建議未來財務報表應包括下列資訊:(1)財務資料與非財務資料*財務報表與其相關策路。

GAAP_RevenueRecognitionPrinciple一般公认会计原则

GAAP_RevenueRecognitionPrinciple一般公认会计原则GAAP – Revenue Recognition PrincipleThis discussion focuses on the objectives, description and application of this principle. Examples will be given to strengthen the understanding and capability to apply this principle at real situation.Objective:To set forth the criteria for recognizing and recording revenue in the accounting period.Description:According to the revenue recognition principle, revenue must be reported when it is realized and earned, not necessarily when the actual cash is received. In addition, the following four criteria or conditions must also be met for revenue to be recognized:1. Delivery has occurred or services have been rendered2. Persuasive evidence of an arrangement for customer payment exists3. Price is fixed or determinable4. Collection is reasonably assuredApplication:Revenue is an item that investors and analysts always pay attention to. In order to avoid misrepresentation (overstatement and understatement) of revenue, GAAP has provided additional guidance for revenue reporting for different situations.For the traditional retail business, goods are delivered to the customers at the same time cash is received, and revenue will be recognized at the time of sales. However in other case that cash could be collected before or after goods or services are delivered,the timing of cash receipts from customers does not dictate when businesses report revenues.Instead, revenue will usually be recognized when the title, risks, and rewards of ownership have transferred to the customers. Depending on the situations, revenue may be recognized at different point of time.Example #1 (cash received at the same period goods/services delivered):The newspaper stand sells Macao Daily News to a customer who pays $4 cash and takes away the newspaper immediately.Entries:Dr. Cash…………… $4Cr. Revenue…………..$4Since cash is received at the same time the newspaper is delivered and all the four criteria are met, revenue will be recognized right away:Example #2 (cash received before goods/services delivered): On Jan 1, the Fortune Magazine has received a subscription form and $120 from an IFT student for subscribing 12 issues of Fortune Magazine ($10/issue). The student will receive 1 issue of the magazine on the last day of each month for 12 consecutive months. Entries:Jan 1 (cash received):Dr. Cash………………$120Cr. Unearned revenue …..... $120Jan 31 (and last day of every month):Dr. Un earned revenue… $10Cr. Revenue ………………..$10When the company received the $120 annual subscription fee for the magazine, criteria #1 has not been met and revenuecould not be recognized at that point of time. The cash received represented obligations to provide future magazine issues to the students which will be booked to the “Unearned Revenue” account temporarily.By definition, “Unearned Revenue” is the collection of cash from customers or clients before goods or services are delivered. Since the goods or services have not been delivered yet, the revenue cannot be considered as “earned”, these cash receipts are considered future obligations to the customers and will be booked to “Unearned Revenue” as a liability account. Only when the goods or services are partial ly or fully delivered, the n the related amount will be unwound from the “Unearned Revenue” account and finally be recognized as “Revenue” earned.In the above example, by the end of each month when the company deliveries the magazine to the student, it earns and records the revenue and reduces the liability account or “Unearned Revenue” account balance.Example #3 (cash received after goods/services delivered): An old customer filled in the cleaning form and dropped off his jacket for cleaning at Dave’s Dry Cleaning on June 30, listed price for cleaning such jacket is $30. Dave cleans the jacket on July 1, but customers do not claim and pay for the jacket until August 1. Entries:June 30 (Customer requests service):No Journal EntryJuly 1 (Service performed):Dr. Accounts Receivable …$30Cr. Revenue……………………..$30August 1 (Cash Received):Dr. Cash………………… $30Cr. Accounts Receivable ….…$30Under the revenue recognition principle, Dave’s earns revenue on July 1, rather than August 1 when cash is received, since it performed the service and met all the four criteria for revenue recognition. On July 1, Dave’s would report a receivable on its balance sheet and revenue in its income statement for the service performed.Final Comment:The following chart summarized the revenue recognition timing for different scenarios as illustrated in the above examples.SCENARIOS 1:Cash received same period goods/services are delivered --> Eg. Sale of product for cash --> Revenue Recognition at date of sale (date of delivery)SCENARIOS 2:Cash received before goods/services are delivered --> Eg. Revenue from subscriptions --> Revenue Recognition as time passes or upon consumptionsSCENARIOS 3:Cash received after goods/services are delivered --> Eg. Sale of service on credit --> Revenue Recognition when services performed and billable。

GAAP通用会计准则

GAAP通用会计准则一、简介GAAP通用会计准则(Generally Accepted Accounting Principles)是指一套广泛被公认的标准和规范,主要适用于美国境内的企业进行财务报表编制和报告。

该准则的目的是保证财务报表的准确性和可比性,以便投资者、债权人、管理层和其他利益相关者能够对企业的财务状况和经营状况有清晰的了解。

本文将对GAAP通用会计准则的相关内容进行探讨。

二、财务报表GAAP通用会计准则要求企业按照一定的报表格式编制财务报表,通常包括资产负债表、损益表、现金流量表和股东权益变动表等。

这些报表需要按照特定的规定和原则进行填报,以确保财务信息的准确性和可比性。

1. 资产负债表资产负债表是企业某一特定日期的资产、负债和股东权益的快照。

根据GAAP通用会计准则,资产负债表需要按照一定的分类和顺序呈现,包括流动资产、非流动资产、流动负债、非流动负债和股东权益等项目。

2. 损益表损益表反映了企业在特定会计期间内的收入、成本、费用和利润等信息。

GAAP通用会计准则规定了损益表的格式和内容,包括营业收入、营业成本、营业费用、税前利润等项目。

3. 现金流量表现金流量表反映了企业在特定会计期间内的现金收入和现金支出情况。

GAAP通用会计准则要求现金流量表按照经营活动、投资活动和筹资活动进行分类,并提供净现金流量的信息,以便分析企业的现金流量状况。

4. 股东权益变动表股东权益变动表展示了企业在特定会计期间内股东权益的变动情况。

GAAP通用会计准则要求股东权益变动表包括股东投入、利润分配和其他综合收益等项目。

三、会计原则和假设GAAP通用会计准则依赖于一系列会计原则和假设,以保证财务报表的准确性和可比性。

以下是一些常见的会计原则和假设:1. 实体概念会计原则中的实体概念指明企业应该作为一个独立的实体对待,与业主和其他实体区分开来。

这意味着企业应该将其财务状况和经营情况与个人或其他实体的财务状况和经营情况进行分开。

美国GAAP和IFRS的主要区别

美国GAAP和IFRS的主要区别美国GAAP和IFRS的主要区别Generally Accepted Accounting Principles是一般公认会计原则,1937年美国会计程序委员会(CAP)发表第一号会计研究公告,开创了由政府机关或行业组织颁布"一般通用会计"的先河。

下面店铺准备了关于美国GAAP和IFRS的主要区别,提供给大家参考!1、在减值损失的计量上,IFRS规定基于可收回金额(资产的使用价值和公允价值减销售成本的较高者)。

US GAAP规定基于公允价值。

2、在资产剩余价值的计量上,IFRS规定在假定资产已经使用完毕﹐且符合其使用年限结束时的预期状况的情况下﹐以资产目前的净销售价格计量。

US GAAP规定通常是资产未来处置时预期收入的折现值。

3、在商誉减值测试的层次上,IFRS规定现金产出单元或一组现金产出单元。

其代表了出于企业内部管理目的而对商誉做出监察的最低组织层次﹐其不能大于一个业务或地区分部。

US GAAP规定报告单位——业务分部或组织内的更低一个层次。

在商誉减值的计算上,IFRS规定一步法比较现金产出单元的可收回金额(公允价值减销售成本和使用价值的较高者)和其账面价值。

US GAAP规定两步法:比较报告单位的公允价值和其包括商誉在内的账面价值;如果公允价值大于账面价值﹐没有减值(不需要进行第二步);比较商誉的内含公允价值和其账面价值。

在不可确定年限的无形资产的减值上,IFRS规定商誉和其他不可确定使用年限的无形资产包括在现金产出单元中﹐对现金产出单元进行减值测试。

US GAAP规定商誉包括在现金产出单元中﹐其他不可确定使用年限的无形资产则作单独测试。

4、在减值损失的转回上,IFRS规定如果满足一定的标准﹐减值损失应转回﹐但商誉的减值损失不可转回。

US GAAP规定减值损失不可转回。

5、在准备的计量上,IFRS规定清算债务的最佳估计﹐通常采用预期价值法﹐并要求采用折现的方法。

GAAP_Prudence 一般公认会计原则

GAAP - PrudenceThis discussion focuses on the objectives, description and application of this principle. Examples will be given to strengthen the understanding and capability to apply this principle at real situation.Objective:To lead managers to anticipate or disclose losses and liabilities, but it does not allow a similar action for gains and assets.“Anticipate no profits, but anticipate all losses”Description:This accounting principle states that if doubt exists between two acceptable alternatives, the manager should choose the alternative that will result in a lesser asset amount and/or a lesser profit. However, it does not mean understating assets or income. Application:If a situation arises where there are two acceptable alternatives for reporting an item, prudence directs the management to choose the alternative that will result in less net income and/or less asset amount.Example:Under lower-of-cost-or-market (LCM) method, inventory is reported at the lower of its cost or market value, which results in higher cost of goods sold and lower net income. Thus net income and assets are reported at their lowest reasonable amount.Cost of goods sold = Beginning inventory + purchase – Ending inventoryNet income = Sales – Cost of goods sold – other expenses (operating and non-operating) By using LCM, the inventory is reported at either the cost or market value, whichever is lower, assuming the other factors remain unchanged.Cost of goods sold = Beginning inventory + purchase – Ending inventoryFinally, the higher Cost of goods sold leads a lower amount of net income, also assuming the other factors remain unchanged.Net income = Sales – Cost of goods sold – other expenses (operating and non-operating)Another example on prudent accounting practice is the practice of accelerated depreciation method. This method results in earlier recording of expense or later recording of revenue. It effects in the postponing on the report of net income and therefore is conservative.Example 2:At the beginning of the year, Southwest purchased equipment for $62,500 cash. The equipment has an estimated useful life of 3 years and an estimated residual value of $2,500. Southwest uses Double-declining method (accelerated depreciation) to calculate the depreciation expense.Entries:Recording Depreciation expense for the first yearDr Depreciation Expense $41,667 (Note 1)Cr Accumulated Depreciation $41,667Note 1:Annual Depreciation expense = Net book value x (2/useful life in years)$41,667 = $62,500 x (2/3 years)Recording Depreciation expense for the second yearDr Depreciation Expense $13,889 (Note 2)Cr Accumulated Depreciation $13,889Note 2:Annual Depreciation expense = Net book value x (2/useful life in years)$13,889 = $(62,500 – 41,667) x (2/3 years)Final comment:Managers are always optimists. Without any constraints, this optimism could find its way into the company’s reported assets and profits. Managers may try to present too favorable a view of the company, and to show a better performance of them than it actually was. However, by so doing, this may result in an overstating of the assets and net income, and mislead the outsiders.。

美国会计准则GAAP与国际会计准则IFRS

资料范本本资料为word版本,可以直接编辑和打印,感谢您的下载美国会计准则GAAP与国际会计准则IFRS地点:__________________时间:__________________说明:本资料适用于约定双方经过谈判,协商而共同承认,共同遵守的责任与义务,仅供参考,文档可直接下载或修改,不需要的部分可直接删除,使用时请详细阅读内容这个问题相当复杂。

呵呵,牵涉到法律基础,即大陆法系和英美法系(海洋法系)。

由于人文法律传统等一息列因素造成严重的差异。

著名案例就是1993年戴姆勒奔驰在纽约上市,按德国会计审核盈利6亿多马克的账本到美国变成了18亿负债,造成欧洲大陆很多公司不愿意到美国上市,影响很坏,美国国会震动。

究其原因就是会计规则的不同。

需要系统的学习才能了解大概。

我有以前学习的存文附上,请参阅。

前言随着资本市场的全球化,建立世界性统一的财会制度已迫在眉睫。

例如,一家外国公司若想在美国上市,必须按照美国一般公认会计原则GAAP(GenerallyAcceptedAccountingStandard,以下简称GAPP)编制年度财务报表,美国证券交易委员会SEC(SecuritiesandExchangeCommission,以下简称SEC)拒绝接受按照别国会计准则编制的财务报表。

除GAAP外,国际会计准则IAS(InternationalAccountingStandard,以下简称IAS),现被称为国际财务报告准则IFRS(InternationalFinancialReportingStandard,以下简称IFRS)也享有越来越重要的国际地位。

2000年7月,德国财务监督执行组织DRSC(DeutscheRechnungslegungStandardCommittee明文规定,上市集团公司可以按照国际上通用的会计准则GAAP或IFRS合并编制财务报表,但必须将其翻译为德语,并选用本位币———欧元作为计价单位。

GAAP通用会计准则

持续经营的原则

除非另有说明,财务报表在准备时假设该公司将继续无限期经营。因此,资产不必以清仓价出售,债务也不需要提前付清。这个原则导致资产和短期被分类为短期(目前)和长远。 长期资产 ,预计将要占有一年以上。长期负债一年内不会到期。

GAAP

求助编辑百科名片

Generally Accepted Accounting Principles是一般公认会计原则,1937年美国会计程序委员会(CAP)发表第一号会计研究公告,开创了由政府机关或行业组织颁布“一般通用会计”的先河。

目录

概述

基本假设经济实体的假设

货币单位假设

编辑本段基本假设

会计师现行使用的一套原则取决于一些基本的假设。在接下来介绍基本假设和原则,被认为是公认会计原则而且适用于大多数的财务报表。除这些概念之外,还有其他更多的技术标准,会计师在准备财务报表时必须遵循。

经济实体的假设

每个经济实体必须保持分开的财务记录。经济实体,包括企业,政府,学区,教堂,和其他社会组织。虽然来自许多不同的实体的会计信息可以因财务报告的需要合并,每一个经济活动,必须与特定的实体关联并被记录。此外,商业记录绝对不能包括业主个人的资产或负债。

充分公开的原则

时间段的假设

权责发生制原则会计

收入确认原则

匹配的原则

成本的原则

持续经营的原则

相关性,可靠性和一致性

谨慎性原则

重要性的原则

概述

基本假设 经济实体的假设

货币单位假设

充分公开的原则

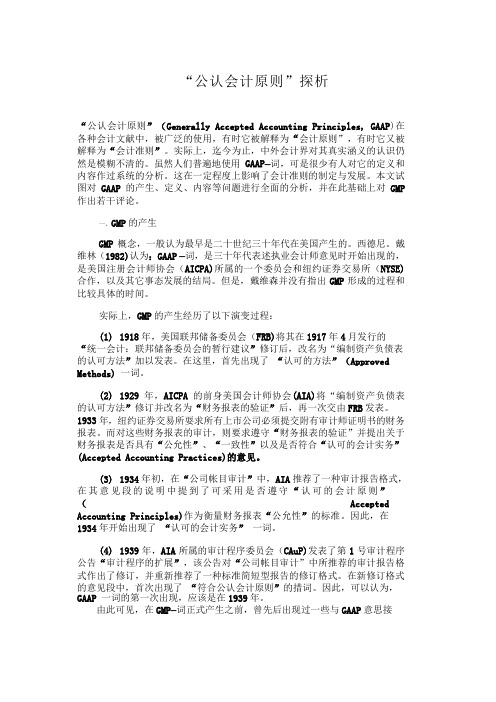

美国 GAAP 与国际财务报告准则的差异及影响

美国 GAAP 与国际财务报告准则的差异及影响美国 GAAP(Generally Accepted Accounting Principles,一般公认会计原则)和国际财务报告准则(International Financial Reporting Standards,IFRS)在全球的会计领域都有着重要的地位,但它们之间存在着不少差异,这些差异给企业和财务工作者带来了各种影响。

咱们先来说说这两者在资产计价方面的差别。

美国 GAAP 对于资产减值的转回限制比较严格,可 IFRS 相对来说就宽松一些。

比如说,一家企业拥有一批存货,按照美国 GAAP,如果这批存货减值了,后来市场情况又变好了,想把减值转回,那可不容易。

但要是按照 IFRS 的规定,就有更大的可能性把减值转回。

再看收入确认这块儿。

美国 GAAP 强调的是风险和报酬的转移,而IFRS 更注重控制权的转移。

我之前遇到过这么个事儿,有一家制造玩具的公司,和一个零售商签订了合同。

按照合同,玩具公司要把一批玩具发给零售商。

在美国 GAAP 下,得等到零售商把这批玩具卖得差不多了,玩具公司才能确认收入。

可要是按照 IFRS,只要零售商拿到这批玩具,控制权转移了,玩具公司就能确认收入。

这就导致同一项业务,在不同的准则下,确认收入的时间可能完全不一样。

还有在租赁业务的处理上,差异也不小。

美国 GAAP 把租赁分为经营租赁和融资租赁,而 IFRS 现在基本上都要求按照“使用权模型”来处理租赁业务。

记得有一次参加一个财务研讨会,会上就有专家专门拿这两种准则下租赁业务的处理来举例。

比如说租一个办公室,如果按照美国 GAAP 被认定为经营租赁,那么相关的资产和负债可能就不会在承租方的报表中体现。

但要是按照 IFRS 的要求,可能就得在报表中反映出来。

这些差异带来的影响那可多了去了。

对于跨国企业来说,那真是个头疼的事儿。

不同国家和地区可能要求使用不同的准则,这就意味着企业得准备两套甚至更多套的财务报表,成本增加不说,还容易出错。

“公认会计原则”探析原则”

“公认会计原则”探析“公认会计原则”(Generally Accepted Accounting Principles, GAAP)在各种会计文献中,被广泛的使用,有时它被解释为“会计原则”,有时它又被解释为“会计准则”。

实际上,迄今为止,中外会计界对其真实涵义的认识仍然是模糊不清的。

虽然人们普遍地使用GAAP—词,可是很少有人对它的定义和内容作过系统的分析。

这在一定程度上影响了会计准则的制定与发展。

本文试图对GAAP的产生、定义、内容等问题进行全面的分析,并在此基础上对GMP 作出若干评论。

一、GMP的产生GMP概念,一般认为最早是二十世纪三十年代在美国产生的。

西德尼。

戴维林(1982)认为:GAAP —词,是三十年代表述执业会计师意见时开始出现的,是美国注册会计师协会(AICPA)所属的一个委员会和纽约证券交易所(NYSE) 合作,以及其它事态发展的结局。

但是,戴维森并没有指出GMP形成的过程和比较具体的时间。

实际上,GMP的产生经历了以下演变过程:(1) 1918年,美国联邦储备委员会(FRB)将其在1917年4月发行的“统一会计:联邦储备委员会的暂行建议”修订后,改名为“编制资产负债表的认可方法”加以发表。

在这里,首先出现了“认可的方法”(Approved Methods) 一词。

(2) 1929年,AICPA的前身美国会计师协会(AIA)将“编制资产负债表的认可方法”修订并改名为“财务报表的验证”后,再一次交由FRB发表。

1933年,纽约证券交易所耍求所有上市公司必须提交附有审计师证明书的财务报表。

而对这些财务报表的审计,则要求遵守“财务报表的验证”并提出关于财务报表是否具有“公允性”、“一致性”以及是否符合“认可的会计实务”(Accepted Accounting Practices)的意见。

(3) 1934年初,在“公司帐目审计”中,AIA推荐了一种审计报告格式,在其意见段的说明中提到了可采用是否遵守“认可的会计原则”(Accepted Accounting Principles)作为衡量财务报表“公允性”的标准。

会计 附录《词汇表》

附录词汇表会计(Accounting):周期性地记录和报告企业的财务交易并分析企业的财务报表。

应付账款(Accounts payable,又称应付商业账款,trade payables):企业由于按赊销方式购买商品或劳务而欠付供应商的款项。

应收账款(Accounts receivable):企业以赊销的方式向客户销售商品或提供劳务所形成的客户欠付的款项。

应计负债(Accrued liabilities,又称应计费用,accrued expenses):企业欠付供应商或雇员的与当期有关但未支付的费用。

累计折旧(Accumulated depreciation):在资本资产的寿命期内至今为止已经对其计提折旧的总金额。

累计折旧在资产负债表上是作为一个备抵项目来列示的(见下面的定义),用来抵减相应资产的原始成本。

资本资产的原始成本与累计折旧之差称为账面净值。

权责发生制会计(Accrual accounting):将收入和费用记录在其发生的期间、而不一定是实际发生现金交易期间的一种会计处理方法。

权责发生制会计是以配比原则为基础的。

坏账准备(Allowance for doubtful accounts,AFDA)资产负债表上描述管理人员对任意特定时点上可能无法收回的应收账款总额所做的恰当的估计的一个项目。

坏账准备是应收账款账户的备抵账户。

资产(Asset):所有者目前以及未来期间所拥有的可以用货币计量其价值的经济资源。

审计师(Auditor):企业外部执行特定的程序、对企业账务数据的准确性和完整性发表意见以使账务报表使用者放心的会计师。

审计报告(Audit report):由审计师编制的慨括性的说明所执行的审计程序、审计范围,以及就账务数据的准确性和完整性发表意见的一页书面文件。

坏账(Bad debts):预计在当期收回有很大疑问的赊销金额。

资产负债表(Balance sheet):企业的三种主要财务报表之一。

美国 GAAP 下的存货会计处理及案例分析

美国 GAAP 下的存货会计处理及案例分析在美国,GAAP(一般公认会计原则)对于存货的会计处理可是有一套严格又讲究的规则。

这玩意儿可不像咱们平常买菜算账那么简单,里面的门道多着呢!咱们先来说说啥是存货。

存货呀,就是企业准备拿来卖或者在生产过程中要用的那些东西,像原材料、在产品、半成品、产成品等等。

比如说一家服装厂,那布料就是原材料,正在加工的衣服就是在产品,差不多快做好的衣服就是半成品,已经做好放在仓库等着卖出去的衣服那就是产成品,这些统统都算存货。

那美国 GAAP 下怎么处理存货呢?首先得确定存货的成本。

这成本可不单单是买这些东西花的钱,还包括运输费、装卸费、保险费等等,反正就是为了让这些存货到企业手里能准备好用,花的各种合理必要的费用都得算进去。

然后就是存货的计价方法。

美国 GAAP 允许用好几种方法,像先进先出法(FIFO)、后进先出法(LIFO)、加权平均法等等。

先进先出法就好比排队买冰淇淋,先排到的先买先出去;后进先出法呢,则是反过来,后进来的先出去;加权平均法就是把所有的成本加起来除以数量,算出一个平均成本。

比如说有个小杂货店,年初进了一批巧克力,进价 1 块钱一块。

到了年中,又进了一批,进价 15 块钱一块。

如果用先进先出法,卖的时候先卖年初进的那批,成本就按 1 块钱算;要是用后进先出法,就先卖年中进的,成本按 15 块算。

再来讲讲存货的减值。

如果存货的市场价值低于成本了,那就要计提减值准备。

这就好比你买了个手机,本来花了 5000 块,结果过了段时间,新手机出来了,你这个二手的只能卖 3000 块,那你就得承认损失 2000 块。

给您说个我亲身经历的事儿。

我有个朋友开了家小超市,有一年快过年的时候,他进了一大批年货,想着过年能大卖一笔。

结果那年过年大家流行出去旅游,买年货的人少了很多。

到了年后,那些年货还堆在仓库里。

他按照美国 GAAP 一算,发现这些存货的价值下降了不少,得计提减值准备,愁得他头发都快白了。

方式保守‘一般公认会计原则GAAP’

圖1-1 直接金融與間接金融的程序

間接金融

直接金融

企業內部之組織形態

A

CEO B C

王品組織圖

企業簡要組織圖

14

企業內部之組織形態 鴻海組織圖

董事會 稽核經理 執行長 總裁 生產部門 會計部

財 務 會 計 成 本 會 計 稅 務 會 計 資 料 處 理 信 用 管 理 營 運 資 金

CEO A B C

18

企業目標

2. 目標之特性

良好的企業目標應具備下列基本特性: 目標與期限明確:模糊的目標會因不同 的人而有不一樣的決策。 具有確切與及時的衡量標準:讓管理者 可立即檢驗執行的成效。

不增加他人之成本:增加社會的有形及無 形成本,未來反而對公司不利。

19

企業目標

3. 股價極大化之問題

總體環境

作法

表1-1 簡化的資產負債表格式

表1-1 簡化 來 源

9

認識財務管理(3/5)

投資學:風險、報酬的折衷藝術 投資 以現時投入以期能在未來換取較原先投入更多的回報 風險 確知或可估計某些特定狀況下,最終結果的不穩定性 投資的應用 各種實質面和金融面的投資行為及程序 「投資程序」,亦即投資決策的形成過程,則包括投資 政策的規劃、證券分析及投資組合管理三類課題

估計成本的缺失:「一般公認會計原則 (GAAP)」重視歷史成本,會使損益產生明顯 的差異。 窗飾:經理人會採取一些人為方式來美化財 務報表,造成報表上的利潤失真。

104年日本東芝企業淨利被報灌水12億美元

17

企業目標

財務管理的目標 ~股東財富極大化

~極大化每股普通股的目前價值 ;意即追求股東權益市值之極大化

GAAP通用会计准则(GAAP general accounting standards)

GAAP通用会计准则(GAAP general accounting standards)GAAPAsk for the editor's encyclopedia cardGenerally Accepted Accounting all is the Generally Accepted Accounting Principles, the United States in 1937 Accounting program committee (CAP) published the first study announcement, created by the government organ or trade organization issued "general general Accounting".directoryAn overview of theBasic assumptions of economic entitiesMonetary unit hypothesisThe principle of full disclosureAssumption of time periodAccrual basis accountingPrinciple of revenue recognitionPrinciple of matchingPrinciple of costThe principle of continuous operation Relevance, reliability, and consistency Principle of prudencePrinciple of importanceAn overview of theBasic assumptions of economic entities Monetary unit hypothesisThe principle of full disclosure Hypothesis of time periodAccrual basis accountingPrinciple of revenue recognition Principle of matchingPrinciple of costThe principle of continuous operation Relevance, reliability, and consistency Principle of prudencePrinciple of importanceExpand the overview of this paragraphGenerally refers to the general accounting principles applicable to various companies in different industries, ranging from basic concept, basic hypothesis of the basic principle of accounting to prepare financial statements on the specific accounting measurement and the provisions of the procedures and methods. Generally, a country's accounting system refers to general general accounting. Generally, it can be divided into international and regional, such as the US GAAP China, which is the new accounting standard issued in 2006, which is usually formulated by the special accounting standards committee. Accountants use generally accepted accounting principles (GAAP) to guide them to record and report financial information. Gaap consists of a broad set of principles established by the accounting and securities and exchange commission (SEC). Two laws, the securities act of 1933 and the securities exchange act of 1934, gave the securities and exchange commission the power to establish reports and open rules. However, the securities and exchange commission usually only supervises work, and the financial accounting standards board and the government accounting standards board (GASB) establish these rules. The government accounting standards board sets accounting standards for state and local governments.Edit the basic assumptions of this paragraphThe current set of principles used by accountants depends on some basic assumptions. The following is the introduction of basic assumptions and principles, considered to be generally accepted accounting principles and applicable to most financial statements. In addition to these concepts, there are more technical standards that accountants must follow when preparing financial statements.The assumptions of the economic entityEach economic entity must maintain separate financial records. Economic entities, including businesses, governments, school districts, churches, and other social organizations. Although accounting information from many different entities can be consolidated for financial reporting requirements, each economic activity must be associated with a specific entity and recorded. In addition, business records must not include owners' personal assets or liabilities.Monetary unit hypothesisAn accounting record of an economic entity only includes transactions that can be quantified. Some economic activities that affect the company, such as hiring a new chief executive or introducing new products, are not easily quantified as monetary units and therefore will not appear in the company's accounting records. In addition,Accounting records must be recorded in a stable currency. American companies, usually, use the dollar for this purpose.The principle of full disclosureFinancial statements usually provide information about the company's past performance. However, ongoing litigation, incomplete transactions, or other circumstances may have an imminent and significant impact on the company's financial position. The full disclosure principle requires financial statements including disclosure of such information. Use a footnote to make a financial statement to convey this information and explain the company's policy on the business transactions used to record and report.Hypothesis of time periodMost businesses have been around for a long time, so they have to report the results of their business activities for a period of time. Depending on the type of report, the period of use may be one day, one month, one year, or any other period of determination. The question of how to record certain transactions as a result of the time period. For example, how should an accountant report a cost of equipment for five years? The entire expense report in the purchase of that year, may make the company no profit this year and subsequent years reasonable profit, not once established period, accountants use generally accepted accounting principles, to record and report accounting period.Accrual basis accountingIn most cases, the accepted accounting principles dictate that accrual accounting, rather than cash basis accounting, is used.Accrual basis accounting principle, adhere to the following discussion of revenue recognition, check, and the cost principle, grasp the financial aspect in accounting period occurs every economic activity, regardless of when cash changes hands. Based on the cash basis accounting, when the company receives cash or equivalent value, the company only pays cash or equivalent.Principle of revenue recognitionWhen the product delivery or service is made, it is recognized as revenue and does not consider the specific time of the cash flow. Suppose the store ordered 500 computer discs from wholesalers in March, received in April and paid in May. Wholesalers confirm sales at the time of the delivery in April, not when the deal is finalized in March or when cash is received in May. Similarly, if a lawyer receives a $100 offer from a client, the department of justice does not recognize the income of the money until he or she is actually performing the $100 service for the client.Principle of matchingThe cost of doing business is recorded at the same time that income is generated. For example, the cost includes the cost of the sale of the goods, the salaries and the commissions earned, the insurance premium, the used supply, and the estimated potential for the sale of the goods. Consider wholesalers shipped 500 CDS to stores in April. When revenue is confirmed, these discs change from asset (storage) to expenses (cost of goods sold) so that profits can be determined.Principle of costThe cost of the asset entry is the value of the acquisition. In the United States, even if assets, such as land or buildings, become more valuable over time, they won't be revalued in financial reports.The principle of continuous operationUnless otherwise stated, the financial statements are prepared to assume that the company will continue to operate indefinitely. So, assets don't have to be sold at a clearance price,Debt is not paid in advance. This principle leads to asset and short term classification as short term (current) and long term. Long-term assets are expected to take over a year. Long-term liabilities don't expire in a year.Relevance, reliability, and consistencyTo function, financial information must be relevant, reliable, and written in a consistent manner. Relevant information helps policy makers understand the company's past performance, current situation, and future prospects, so that decision makers can make timely decisions. Individual information to meet the needs of users, of course, may be different, make the information needs of different format, internal users often than external users need more detailed information, external users only need to know the value of the company or its abilityto repay the loan. Reliable information is verifiable and objective. The preparation of consistent information is the same method used in every accounting period to make meaningful comparisons between different periods of the same company and the financial statements of different companies.Principle of prudenceAccountants must use their judgment to record trades when estimating. The number of years in which the equipment continues to be produced and the amount of accounts receivable cannot be cashed out as an example of the need for evaluation. In the financial data report, accountants follow the principle of prudence, which requires the choice of a more unfavorable one in the two estimates that are equally likely to occur. For example, suppose that a manufacturing firm's warranty department for product X in the past two years has recorded the return rate of 3%, but the engineering department of the company insist on the return rate is only a statistical anomaly, and less than 1% in the coming year product X will require service. Unless the engineering department provides compelling evidence to support its assessment, the company's accountants must adhere to the principle of prudence and plan a return rate of 3%. Loss and expense, such as warranty maintenance - when possible and reasonable estimates are recorded. When the implementation proceeds will be recorded.Principle of importanceAccountants abide by the principle of importance, and any accounting principles can be ignored if the state requires,without affecting the user's financial information. Of course, it's not important to track back needles or a few pages of paper for any company's accounting department, causing undue burdens. While there is no clear measure of importance, accountants must sound judgment on such matters. Thousands of dollars are not necessarily important for big companies like general motors, but the same amount is important for a small family business.。

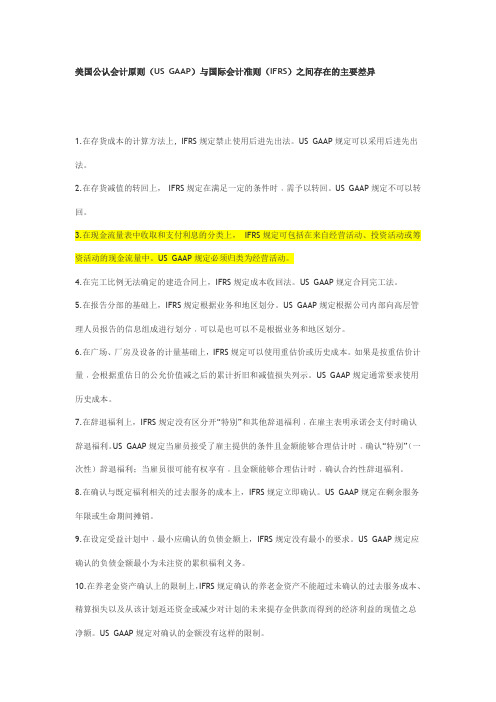

美国公认会计原则GAAP和国际会计准则IFRS差异

美国公认会计原则(US GAAP)与国际会计准则(IFRS)之间存在的主要差异1.在存货成本的计算方法上, IFRS规定禁止使用后进先出法。

US GAAP规定可以采用后进先出法。

2.在存货减值的转回上,IFRS规定在满足一定的条件时﹐需予以转回。

US GAAP规定不可以转回。

3.在现金流量表中收取和支付利息的分类上,IFRS规定可包括在来自经营活动、投资活动或筹资活动的现金流量中。

US GAAP规定必须归类为经营活动。

4.在完工比例无法确定的建造合同上,IFRS规定成本收回法。

US GAAP规定合同完工法。

5.在报告分部的基础上,IFRS规定根据业务和地区划分。

US GAAP规定根据公司内部向高层管理人员报告的信息组成进行划分﹐可以是也可以不是根据业务和地区划分。

6.在广场、厂房及设备的计量基础上,IFRS规定可以使用重估价或历史成本。

如果是按重估价计量﹐会根据重估日的公允价值减之后的累计折旧和减值损失列示。

US GAAP规定通常要求使用历史成本。

7.在辞退福利上,IFRS规定没有区分开“特别”和其他辞退福利﹐在雇主表明承诺会支付时确认辞退福利。

US GAAP规定当雇员接受了雇主提供的条件且金额能够合理估计时﹐确认“特别”(一次性)辞退福利;当雇员很可能有权享有﹐且金额能够合理估计时﹐确认合约性辞退福利。

8.在确认与既定福利相关的过去服务的成本上,IFRS规定立即确认。

US GAAP规定在剩余服务年限或生命期间摊销。

9.在设定受益计划中﹐最小应确认的负债金额上,IFRS规定没有最小的要求。

US GAAP规定应确认的负债金额最小为未注资的累积福利义务。

10.在养老金资产确认上的限制上,IFRS规定确认的养老金资产不能超过未确认的过去服务成本、精算损失以及从该计划返还资金或减少对计划的未来提存金供款而得到的经济利益的现值之总净额。

US GAAP规定对确认的金额没有这样的限制。

11.在确认缩减利得的时间上,IFRS规定当有关企业有明确表示将福利计划缩减﹐且已经对外宣布时﹐确认缩减利得和损失。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

GAAP – Matching Principle

This discussion focuses on the objective, description and application rules of this principle. Examples have been given to strengthen your understanding.

Objective: Guides you how to record "expenditure" (expenses).

Description: The amount of “expenses” incurred to generate an amount of “revenue” should be matched to that amount of “revenue” at the period when the “revenue” is earned. This is in regardless when money is received or paid.

Application Rules:

If payment of $ will bring "future" benefits --> record as "Asset"

If payment of $ will bring "current" benefits --> record as "Expense"

If payment of $ will bring "NO" benefits --> record as "Loss"

Example:

Your company paid $100,000 cash for the purchase of a car on 1 September. Your financial year ends by 31 October of the year.

Scenario 1: The car is for the delivery of goods to customers.

Entries:

Dr Car 100k

Cr Cash 100k

Note: “Car” is classified as “non-current asset”

Explanation:

a) The car in this case fulfills the criteria of a non-current asset, since

- you have ownership / control

- you have no intention to resale for revenue

- it can be measured in monetary value ($100k)

- it has economic benefits (for delivery of goods)

- you will probably keep it for more than 12 months (owing to its nature)

b) Though the car is purchased on 1 September, however, there is no hint showing that you have the intention to "throw" it away in just a few days or weeks.

c) According to point b), this car can bring upon "future" benefits, since your company will probably use it for quite a period of time. (e.g. Oct, Nov, Dec etc)

d) Consequently, the payment of this $100,000 will bring upon "future" benefits, so we record it as an "asset". In this case, as non-current asset (NCA).

e) "Non-current asset" is a permanent ledger, with which the balance will be carried down to the next financial period and the ledger will NOT be closed. It is to be recorded in the Balance Sheet.

Scenario 2: (Same example applies but) The car is used as a gift for the lucky draw of a marketing activity for your company.

Entries:

Dr Marketing Expenses 100k

Cr Cash 100k

Note: “Marketing expenses” is classified as “expense”

Explanation:

a) The car still fulfills all the criteria of a non-current asset as mentioned in Scenario 1.

b) However, under this scenario, the car is purchased only as a "gift" of the lucky draw - which is a marketing activity of your company. The car "will not" and "cannot" be kept after the lucky draw, because it will be given as a gift to the winner (which surely will NOT be your company!).

c) According to point b), this car can bring upon "current" benefits ONLY, since your company cannot "use" it for a period of time. (it can be used in the same manner as a "gift" only, e.g. a coupon!)

d) Consequently, the payment of this $100,000 will bring upon "current" benefits, so we record it as "expense". In this case, as marketing expenses.

e) "Expense" is a temporary ledger, which is to be closed by the end of the financial year and recorded in Income Statement.

Final Comment:

See the differences? Though the same amount of $ is paid (in this e.g. $100k) and the same item is purchased (in this e.g. the car), however because the duration of benefits that will bring upon by this item (or amount of $) differs (scenario 1 --> long term; scenario 2 --> current), then this same amount of $ will be recorded differently (scenario 1 --> as NCA; scenario 2 --> as expenses).

This is exactly what the "matching principle" of the GAAP tells us. It guides us how to record an "amount of expenditure", based on how long the company can benefit from the relative amount of payment.

Though this is NOT all!

The matching principle also tells us "when" we should record an amount of expenses -- it is when revenue is generated due to this amount of expenses, therefore, comes the "adjustment". In short, matching principle guides us how and when to record expenditure.。