Return Report of Mini Case in Coroperate Finance

Firstdescription...

Case reportFirst description of Anaerococcus octavius as cause of bacteremiaFernando Cobo*,Jos e María Navarro-MaríDepartment of Microbiology and Instituto Biosanitario,University Hospital Virgen de Las Nieves,Department of Medicine,University of Granada,Granada, Spaina r t i c l e i n f oArticle history:Received13September2019 Received in revised form20November2019Accepted21November2019 Available online22November2019Handling Editor:Boyanova LyudmilaKeywords:A.octaviusbacteremiaCancerAnaerobeAntimicrobials a b s t r a c tAnaerococcus spp.are Gram-positive anaerobic cocci involved in human skin and soft-tissue infections, among other diseases.We report thefirst known case of bacteremia due to A.octavius,detected in an elderly patient.A71-year-old woman with a history of breast cancer presented with fever and cognitive impairment for more than three days.A.octavius was isolated in blood cultures,and only resistance to clindamycin was reported.Her general condition improved after treatment with metronidazole and she was discharged.©2019Elsevier Ltd.All rights reserved.1.IntroductionAnaerococcus octavius(formerly Peptostreptococcus octavius)are obligate anaerobic non-spore-forming cocci that have not previ-ously been associated with human infections.This microorganism wasfirst described by Murdoch et al.,in1997[1]and reassigned to the Anaerococcus genus by Ezaki et al.,in2001[2].It has frequently been isolated in skin,vagina,and nasal cavity[2],but no human infections in pure culture have been reported in the literature.We recently diagnosed thefirst case of bacteremia caused by A.octavius,detected in an elderly patient.This pathogen was encountered as a pure culture in this infection.2.Case reportAn immunocompetent71-year-old woman was admitted to the Neurology Department due to fever and cognitive impairment for more than three days.Family history included liver cancer of her father and lung cancer of her mother.The patient was referred from the Emergency Department due to a worsening of her general condition.In the neurological examination,only a motor dysfunc-tion was documented.She had been diagnosed with breast cancer three years earlier,treated with tumorectomy and local radio-therapy,and had a history of mitral and aortic insufficiency.She had never received chemotherapy,and there was no evidence of tumor recurrence at her admission.Physical examination revealed the presence of fever(38.5 C),pulse of95bpm,and mitral and aortic heart murmurs,and blood analysis showed elevated C-reactive protein(13mg/L).Remaining parameters,including liver and renal function,were normal.Chest X-ray showed no remarkablefindings, and brain CT scan did not reveal intracranial expansive processes or acute hemorrhagic lesions.After taking two sets of blood cultures, treatment was started with intravenous(i.v.)cefotaxime(1g/8h/3 days);on day2of incubation,both anaerobic bottles were found to be positive(BD BACTEC FX40,Becton Dickinson).The sample was subcultured in aerobic or anaerobic blood agar(BD Columbia Agar with5%Sheep Blood,Becton Dickinson,Franklin Lakes,NY).All media were incubated at37 C.The anaerobic system used was the AnaeroGen Compact(Oxoid Ltd,Wide Road,Basingstoke,England).Gram staining of the blood cultures exhibited abundant Gram-positive cocci;on the second day of incubation,abundant col-onies of these microorganisms were observed in pure culture,in anaerobic blood agar alone.MALDI-TOF MS version8(7854msp) (Bruker Biotyper,Billerica,MA)was employed to identify the strain as Clostridium beijerinckii(score1.18)and it was sent to the National*Corresponding author.Department of Microbiology and Instituto Biosanitario, Hospital Virgen de las Nieves Avda Fuerzas Armadas,218014Granada,Spain.E-mail addresses:**************************************,microhaya@gmail. com(F.Cobo).Contents lists available at ScienceDirectAnaerobejo urn al homepage:/locate/an aerobehttps:///10.1016/j.anaerobe.2019.1021301075-9964/©2019Elsevier Ltd.All rights reserved.Anaerobe61(2020)102130Centre for Microbiology(Majadahonda,Madrid,Spain)forfinalidentification.The isolate was identified by means of16S rDNAsequence analysis using a previously reported method[3].A frag-ment of1101bp was obtained,giving99.2%similarity withA.octavius(Gene Bank sequence:NR_026360).Antimicrobial sus-ceptibility testing was performed by using the E-test.According the2019EUCAST criteria[4],the strain was susceptible to all antimi-crobials tested except clindamycin.The following MIC values wereobtained for this strain:penicillin(<0.016m g/mL),amoxicillin-clavulanate(<0.016m g/mL),piperacillin-tazobactam(0.032m g/ mL),clindamycin(>256m g/mL),meropenem(<0.002m g/mL), imipenem(<0.002m g/mL),vancomycin(0.25m g/mL),and metro-nidazole(0.38m g/mL).Antimicrobial treatment was changed to i.v.metronidazole(1.5g/day/5days)and the condition of the patient improved,allowingher discharge from the hospital.At5months of follow-up,thegeneral condition of the patient remains good.3.DiscussionWe report thefirst case of bacteremia due to A.octavius,detected in a71-year-old woman with a breast cancer.Only resis-tance to clindamycin was documented,and treatment withmetronidazole was established,observing an improvement in hergeneral condition.Anaerococcus genus encompasses13species,with A.prevotiibeing the most frequent.Members of the genus are typically iso-lated from the human vagina and purulent secretions[2].A.prevotiiis often recovered from vaginal discharges and from different typesof abscess[5],ctolyticus and A.vaginalis have been isolatedfrom diabetic foot and pressure ulcers[6],and strains of A.octaviushave been recovered from nasalflora,skin,and vagina[7,8].A.vaginalis and A.prevotii have been identified in blood cultures bymass spectrometry and16S rRNA gene sequencing[9];however,toour best knowledge,no bloodstream infections due to A.octaviushave previously been reported.In the present case,the source ofinfection was unknown,although the most likely route would becolonization of the upper respiratory tract.The definitive diagnosis of anaerobes is based on phenotypictests and/or molecular methods.The availability of proteomictechniques such as MALDI-TOF MS in routine clinical laboratoryanalysis facilitates thefinal identification of these bacteria and therecognition of new species of anaerobes.However,as in the presentreport,molecular techniques are needed for thefinal identification,especially when the MALDI-TOF MS score is low[10].In the presentcase,the microorganism was included in the version of the data-base used but with only two inputs,which may explain the lowscore.Anaerococcus species are considered susceptible to penicillinsoverall,but resistance to tetracycline,erythromycin,and clinda-mycin has been reported by some authors[11].Resistance ofA.prevotii to clindamycin,levofloxacin and ceftazidime has beendescribed[12,13],and A.murdochii has shown resistance to kana-mycin and clindamycin and intermediate resistance to penicillin[14].However,another study found that four isolates of Anaero-coccus species were susceptible to clindamycin,among other anti-microbials[15].In the present case,resistance to clindamycin(MIC >256m g/mL)was observed,as in some recent studies,therefore,the antibiotic is not appropriate as empirical treatment.In conclusion,this study shows that Anaerococcus species cancause infections in pure culture,and presents thefirst known report of A.octavius as a cause of bloodstream infection.These findings and recent studies on the antimicrobial resistance of Anaerococcus spp.strongly support the need for caution in the antimicrobial treatment of these infections,especially in the se-lection of empirical therapy,and for the routine susceptibility testing of Gram-positive anaerobes.FundingNone.Declaration of competing interestThe authors declare no conflict of interest. AcknowledgementsThe authors thank Dr.Juan Antonio S a ez from the National Centre for Microbiology(Majadahonda,Madrid,Spain)for the definitive identification of the strain.References[1] D.A.Murdoch,M.D.Collins,A.Willems,J.M.Hardie,K.A.Young,J.T.Magee,Description of three new species of the genus Peptostreptococcus from human clinical specimens:Peptostreptococcus harei sp.nov.,Peptostreptococcus ivorii sp.nov.,and Peptostreptococcus octavius sp.nov,Int.J.Syst.Bacteriol.47 (1997)781e787.[2]T.Ezaki,Y.Kawamura,N.Li,Z.Y.Li,L.Zhao,S.Shu,Proposal of the generaAnaerococcus gen.nov.,Peptoniphilus gen.nov.,and Gallicola gen.nov for members of the genus Peptostreptococcus,Int.J.Syst.Evol.Microbiol.51 (2001)1521e1528.[3]M.Drancourt,C.Bollet,A.Carlioz,R.Martelin,J.P.Gayral,D.Raoult,16S ri-bosomal DNA sequence analysis of a large collection of environmental and clinical unidentifiable bacteria isolates,J.Clin.Microbiol.38(2000) 3623e3630.[4]European Committee on antimicrobial susceptibility testing,BreakpointTables for Interpretation of MICs and Zone Diameters,2019,Version9.0..[5]butti,R.Pukall,K.Steenblock,Complete genome sequence of Anaero-coccus prevotii type strain(PC1),Stand.Genom.1(2009)159e165.[6]S.E.Dowd,R.D.Wolcott,Y.Sun,T.McKeehan,E.Smith,D.Rhoads,Poly-microbial nature of chronic diabetic foot ulcer biofilm infections determined using bacterial tag encoded FLX amplicon pyrosequencing(bTEFAP),PLoS One 3(2008)e3326.[7] D.A.Murdoch,I.J.Mitchelmore,S.Tabaqchali,The clinical importance of gram-positive anaerobic cocci isolated at St Bartholomew’s Hospital.London,J.Med.Microbiol.41(1994)(1987)36e44.[8] C.G.A.Thomas,R.Hare,The classification of anaerobic cocci and their isolationin normal human beings and pathological processes,J.Clin.Pathol.7(1954) 300e304.[9] Scola,P.E.Fournier,D.Raoult,Burden of emerging anaerobes in theMALDI-TOF and16S rRNA gene sequencing era,Anaerobe17(2011)106e112.[10] E.Nagy,S.Becker,M.Kostrzewa,N.Barta,E.Urb a n,The value of MALDI-TOFMS for the identification of clinically relevant anaerobic bacteria in routine laboratories,J.Med.Microbiol.61(2012)1393e1400.[11]J.S.Brazier,V.Hall,T.E.Morris,M.Gal,B.I.Duerden,Antibiotic susceptibilitiesof Gram-positive anaerobic cocci:results of a sentinel study in England and Wales,J.Antimicrob.Chemother.52(2003)224e228.[12] E.J.Goldstein, D.M.Citron, C.V.Merriam,Y.A.Warren,K.L.Tyrrell,H.T.Fernandez,In vitro activity of ceftobiprole against aerobic and anaerobicstrains isolated from diabetic foot infections,Antimicrob.Agents Chemother.50(2006)3959e3962.[13] E.J.Goldstein, D.M.Citron,Y.A.Warren,K.L.Tyrrell, C.V.Merriam,H.T.Fernandez,In vitro activities of dalbavancin and12other agents against329aerobic and anaerobic gram-positive isolates recovered from diabetic foot infections,Antimicrob.Agents Chemother.50(2006)2875e2879.[14]Y.Song,C.Liu,S.M.Finegold,Peptoniphilus gorbachii sp.nov.,Peptoniphilusolsenii sp.nov.,and Anaerococcus murdochii sp.nov.isolated from clinical specimens of human origin,J.Clin.Microbiol.45(2007)1746e1752.[15] D.A.Murdoch,I.J.Mitchelmore,The laboratory identification of gram-positiveanaerobic cocci,J.Med.Microbiol.34(1991)295e308.F.Cobo,J.M.Navarro-Marí/Anaerobe61(2020)102130 2。

Chapter 21 Chekhov 契诃夫

Chapter 21 Chekhov 契诃夫Anton Chekhov (1860-1904)·Russian writer, who brought both the short story and the drama to new prominence卓越in Russia and eventually in the Western world.·One of 3 greatest short story writers·"Medicine is my lawful wife", he once said, "and literature is my mistress情妇."His life & works:Born in the small seaport of Taganrog, Ukraine乌克兰on January 17th in the year 1860.He was the grandson of a serf农奴who had bought his freedom.Father, owner of a grocer杂货店.He lived an unhappy life in his childhood●Chekhov spent his early years under the shadow of his father's religious fanaticism 狂热while working long hours in his store.●Chekhov…s mother was an excellent storyteller讲故事的人who entertained the childrenwith tales of her travels all over Russia before she had married.●"Our talents we got from our father, but our soul from our mother."His education:●Chekhov attended a school for Greek boys in his hometown.●Later, his father went bankrupt. In order to avoid the debtor's prison, the family fled toMoscow, Chekhov's mother physically and emotionally broken.The family moved to Moscow.Chekhov, only 16 at the time, decided to remain in his hometown and supported himself by tutoring as he continued his schooling for 3 more years.He tried various kinds of jobs●Tutor.家庭教师●He began to write humorous short stories.In 1879 he entered the University of Moscow to study medicine.●It was from this time that Chekhov began to publish comic short stories and used themoney to support himself and his family.●His early stories ironically satirized讽刺the servile奴隶的character of the people●The Death of a Government Clerk《一个文官的死》(1883)Ivan, sneeze喷嚏; spatter溅on the bald秃头head of a general,the high political pressure政治压力of Tzarist Russia.● A Chameleon《变色龙》(1884)Otchumyelov, A police officer‟s double sides: flattery奉承and terribleHe developed his ability to say a great deal in a few words.At the same time, he began to explore serious themes that figure in his later work, such as human isolation隔离and the difficulty of communication.In 1884 Chekhov became a doctor. Around this year, he found himself coughing blood (tuberculosis).肺结核Meanwhile, he continued to write.Chekhov was awarded the Pushkin Prize in 1888. "for the best literary production distinguished by high artistic worth"His travel in 1890●Chekhov made an arduous努力的9650-km journey across Siberia by train, river steamer,and horse-drawn carriage to conduct a sociological and medical survey in a Russian penal colony流放地on Sakhalin Island库页岛, off the eastern coast of Russia.A Journey To Sakhalin库页岛is an amazing document.●“Hell Island!”●This book had some influence in moderating the harsh严厉的prison rule on the island. Around the year 1890, Chekhov moved toward publishing longer, more serious and more technically accomplished stories.●Ward No. 6(1892)《第六病室》mental patientsDoctor Andrey Y efimitch 拉京The door keeper Nikita 尼基达The story deals with the persecution to the common peopleand the consequences of indifference to human suffering.● A Man in a Case (1898)《套中人》Byelikov “I hope it won't lead to anything!”The story satirized讽刺the old tradition and autocratic专制的government.He also wrote plays戏剧:In his dramatic works Chekhov sought to convey the texture本质of everyday life, moving away from traditional ideas of plot情节and conventions惯例of dramatic speech.The major theme in Anton Chekhov's plays:●the psychologically bitterness苦难、怨恨of the Russian intellectuals知识分子●The Seagull《海鸥》(1896)Three a rtists‟ unfortunate fate.●Uncle V anya《万尼亚舅舅》(1899)The embodiment体现of the Russian intellectuals’unfortunate fate●Three Sisters《三姐妹》(1901)Three kind-hearted intellectual sisters and their helplesswaitingThe three sisters never realized their dream to go to Moscow (a major symbolic element).The Cherry Orchard《樱桃园》(1904)is his last drama works●The play concerns an aristocratic Russian woman and her family as they return to thefamily's estate (which includes a large and well-known cherry orchard) just before it is auctioned拍卖to pay the debt.the passing away of the old, aristocratic RussiaLopakhin,the former serf, who becoming an upstart暴发户, rich and powerful but rude and violent.Lopakhin had all the trees cut down, …This symbolizes the society changed by capitalism资本主义with its violence.Lopakhin, a neighbor of Madame Ranevsky, the former serf●The story presents themes of cultural futility无用、徒劳—both the futility ofthe aristocracy贵族 to maintain its status and the futility of the bourgeoisie资产阶级to find meaning in its newfound materialism唯物主义.Chekhov and Olga, 1901, on honeymoon 结婚His style (1):●Taking a cool冷静的, objective stance立场toward his characters, Chekhov conveystheir inner lives内心生活and feelings indirectly, by suggestion rather than statement陈述.His style (2):His plots are usually simple, and the endings of both his stories and his plays tend toward openness开放rather than finality定局.His style (3) - his realism:Chekhov‟s works create the effect of profound experience taking place beneath the surface in theordinary lives of unexceptional people.A warm-hearted writer●“We shall find the peace. We shall hear the angels. We shall see the sky sparkled闪耀with diamonds.”contents● 1. Russian background in late 19th century● 2. His early short stories● 3. his works after 1890s.● 4. His representative: Ward No. 6《第六病室》The Man in a Case《套中人》1. BackgroundA. society polarized偏振的.●Reform of Muzhik. (Emancipation reform ) The peasants who had lost their land andrushed into cities became industrial workers.●Contradiction between working class and bourgeoisie.B. The Russian PopulistsThe Russian Populists : to resist the prevail流行of capitalism with the traditional Russian patriarchal clan system 宗法制so as to establish the Russian socialism.In 1880s The social contradiction turned severe and the Russian government of Tzarist俄国帝制的autocracy 专制strengthened political pressure on the people.C. high political pressure●The Russian Populists assassinated暗杀Tzar Alexander II in 1881. This terrorist恐怖主义者action caused the overwhelming压倒性的revenge报复of Russian government over the Russian people.●In turn, Russian people became more and more intolerant of the government.2. his early storiesHis early stories ironically satirized the servile character of the people.●The Death of a Government Clerk《一个文官的死》● A Chameleon《变色龙》ONE fine evening, a no less fine government clerk called Ivan Dmitritch T chervyakov was sitting in the second row of the stalls, gazing through an opera glass at the Cloches de Corneville. "I have spattered him," thought T chervyakov, "he is not the head of my department, but still it is awkward. I must apologize."In mid-1880s his stories reveals a sympathy toward the miserable people.●Sorrow《哀伤》THE turner, Grigory Petrov, who had been known for years past as a splendid craftsman工匠, and at the same time as the most senseless愚蠢的peasant in the Galtchinskoy district区域, was taking his old woman to the hospital.His old woman died●At last, to make an end of uncertainty, without looking round he felt his old woman's coldhand. The lifted hand fell like a log.●"She is dead, then! What a business!"●And the turner cried. He was not so much sorry as annoyedHe nearly went insane疯狂的●V anka《万卡》V ANKA ZHUKOV, a boy of nine, who had been for three months apprenticed to Alyahin the shoemaker, was sitting up on Christmas Eve. Waiting till his master and mistress and their workmen had gone to the midnight service, he took out of his master's cupboard a bottle of ink and a pen with a rusty nib, and, spreading out a crumpled sheet of paper in front of him, began writing.His grandpa:●He was a thin but extraordinarily nimble and lively little old man of sixty-five, with aneverlastingly laughing face and drunken eyes. By day he slept in the servants' kitchen, or made jokes with the cooks; at night, wrapped in an ample sheepskin, he walked round the grounds and tapped with his little mallet木槌.3. His works after 1889After 1889 Chekhov turned into serious criticism on dark reality in his short stories.Ward No. 6《第六病室》The Man in a Case《套中人》(1888)4. His representativeWard No. 6《第六病室》:It deals with the consequences of indifference漠不关心to human suffering.·Andrey Y efimitch拉京,Doctor of Ward No. 6, a humanist, who believes in non-violence●In response to the last question Andrey Y efimitch turned rather red and said: "Y es, he ismentally deranged, but he is an interesting young man."●They asked him no other questions.Nikita tortures折磨Andrey Y efimitch:Nikita opened the door quickly, and roughly with both his hands and his knee shoved Andrey Y efimitch back, then swung his arm and punched him in the face with his fist.Andrey Y efimitch dies死:Next day Andrey Y efimitch was buried. Mihail Averyanitch and Daryushka were the only people at the funeral葬礼.·Nikita尼基达,The porter守门人, Nikita, an old soldier wearing rusty生锈的good-conduct stripes, is always lying on the litter with a pipe烟斗between his teeth. He has a grim冷酷的, surly板面孔的, battered磨损的-looking face, overhanging eyebrows which give him the expression of a sheep-dog of the steppes, and a red nose;he is short and looks thin and scraggy瘦弱的, but he is of imposing deportment行为举止and his fists are vigorous. He belongs to the class of simple-hearted, practical实际的, and dull-witted people, prompt in carrying out orders, who like discipline better than anything in the world, and so are convinced that it is their duty to beat people.His cruelty:He showers blows on the face, on the chest, on the back, on whatever comes first, and is convinced that there would be no order in the place if he did not.·Ivan Dmitritch Gromov格罗莫夫,a man of thirty-three, who is a gentleman by birth, and has been a court usher接待员and provincial secretary, suffers from the mania狂热of persecution.迫害an official called Gromov,Some twelve or fifteen years ago an official called Gromov, a highly respectable and prosperous person, was living in his own house in the principal street of the town. he was well educated and well read; according to the townspeople's notions, he knew everything, and was in their eyes something like a walking encyclopedia活百科全书He became persecution mania受迫害妄想症●In the morning Ivan Dmitritch got up from his bed in a state of horror惊骇, with coldperspiration汗水on his forehead, completely convinced that he might be arrested any minute.Ward No. 6 is a symbol of the Tzarist Russia●And its only function is to persecute迫害the common people in Russia.●Nikita symbolizes tools of the government.The Man in a Case《套中人》(1888):Byelikov tried to hide his thoughts●And Byelikov tried to hide his thoughts also in a case. The only things that were clear tohis mind were government circulars通告and newspaper articles in which something was forbidden.●Byelikov always says,"It is all right, of course; it is all very nice, but I hope it won't leadto anything!“●"Byelikov had a little bedroom like a box; his bed had curtains. When he went to bed hecovered his head over; it was hot and stuffy; the wind battered on the closed doors; there was a droning noise in the stove and a sound of sighs from the kitchen -- ominous sighs. . . . And he felt frightened under the bed-clothes.●He was afraid that something might happen, that Afanasy might murder him, that thievesmight break in, and so he had troubled dreams all night, and in the morning, when we went together to the high-school, he was depressed and pale, and it was evident that the high-school full of people excited dread and aversion恐惧和厌恶in his whole being, and that to walk beside me was irksome to a man of his solitary temperament.●"Y ou see and hear that they lie," said Ivan Ivanovitch, turning over on the other side,"and they call you a fool for putting up with their lying. Y ou endure insult and humiliation, and dare not openly say that you are on the side of the honest and the free, and you lie and smile yourself; and all that for the sake of a crust of bread, for the sake of a warm corner, for the sake of a wretched little worthless rank in the service. No, one can't go on living like this."不能这样生活Anthropus!恋爱的人。

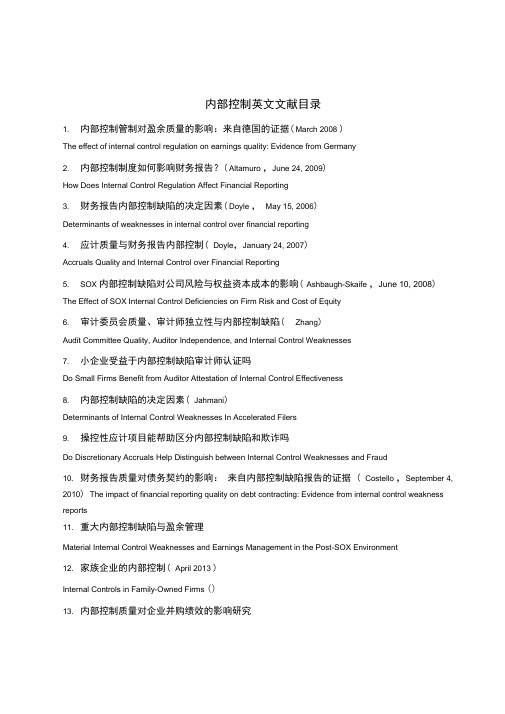

(完整版)内部控制英文文献目录

内部控制英文文献目录1. 内部控制管制对盈余质量的影响:来自德国的证据( March 2008 )The effect of internal control regulation on earnings quality: Evidence from Germany2. 内部控制制度如何影响财务报告?( Altamuro ,June 24, 2009)How Does Internal Control Regulation Affect Financial Reporting3. 财务报告内部控制缺陷的决定因素( Doyle ,May 15, 2006)Determinants of weaknesses in internal control over financial reporting4. 应计质量与财务报告内部控制( Doyle,January 24, 2007)Accruals Quality and Internal Control over Financial Reporting5. SOX 内部控制缺陷对公司风险与权益资本成本的影响( Ashbaugh-Skaife ,June 10, 2008) The Effect of SOX Internal Control Deficiencies on Firm Risk and Cost of Equity6. 审计委员会质量、审计师独立性与内部控制缺陷( Zhang)Audit Committee Quality, Auditor Independence, and Internal Control Weaknesses7. 小企业受益于内部控制缺陷审计师认证吗Do Small Firms Benefit from Auditor Attestation of Internal Control Effectiveness8. 内部控制缺陷的决定因素( Jahmani)Determinants of Internal Control Weaknesses In Accelerated Filers9. 操控性应计项目能帮助区分内部控制缺陷和欺诈吗Do Discretionary Accruals Help Distinguish between Internal Control Weaknesses and Fraud10. 财务报告质量对债务契约的影响:来自内部控制缺陷报告的证据 ( Costello ,September 4, 2010) The impact of financial reporting quality on debt contracting: Evidence from internal control weakness reports11. 重大内部控制缺陷与盈余管理Material Internal Control Weaknesses and Earnings Management in the Post-SOX Environment12. 家族企业的内部控制( April 2013 )Internal Controls in Family-Owned Firms ()13. 内部控制质量对企业并购绩效的影响研究Study on the Impact of the Quality of Internal Control on the Performance of M&A14. 内部控制质量与信用违约互换利差( January 2014)Internal Control Quality and Credit Default Swap Spreads15. 家族企业内部控制:特征和后果Internal Control in Family Firms: Characteristics and Consequences16. 内部控制报告与会计信息质量:洞察”遵守或解释的“内部控制制度Internal control reporting and accounting quality :Insight "comply-or-explain" internal control regime17. 内部控制报告与会计稳健性Internal Control Reporting and Accounting Conservatism18. 会计信息质量影响产品市场契约吗?来自政府合同授予的证据( March 2014 )Does Accounting Quality Influence Product Market Contracting? Evidence from Government Contract Awards19. 公司特征与财务报告质量:尼日利亚制造业上市公司的证据20. 内部控制情况与专家审计师选择The Association between Internal Control Situations and Specialist Auditor Choices21. 审计费用反应了控制风险的风险溢价吗( 2013-07 )Do Audit Fees Reflect Risk Premiums for Control Risk?22. 内部控制质量与审计定价Internal Control Quality and Audit Pricing under the Sarbanes-Oxley Act23. 内部控制缺陷与权益资本成本:来自萨班斯法案404 节披露的证据Internal Control Weakness and Cost of Equity: Evidence from SOX Section 404 Disclosures24. 内部控制缺陷与信息不确定性Internal Control Weaknesses and Information Uncertainty25. 重大内部控制缺陷与股票价格崩溃危险:来自404 条款披露的证据( May 2013 )Material Weaknessin Internal Control and Stock Price Crash Risk: Evidence from SOX Section 404 Disclosure 26. SOX 内部控制缺陷对公司风险与权益资本成本的影响The Effect of SOX Internal Control Deficiencies on Firm Risk and Cost of Equity27. 信用评级、债务成本与内部控制信息披露:SOX302 和SOX404 法的比较28. 萨班斯-奥克斯利法案对会计信息债务契约价值的影响The Effect of Sarbanes-Oxley on the Debt Contracting Value of Accounting Information29. 财务报告内部控制的不利意见与审计师解聘/辞职Adverse Internal Control over Financial Reporting Opinions and Auditor Dismissals/Resignations30. 新管理人员任命与随后的SOX 法案404 的意见Appointment of New Executives and Subsequent SOX 404 Opinion31. 萨班斯奥克斯利:有关萨班斯法案404 影响的证据Sarbanes-Oxley: The Evidence Regarding the Impact of Sox 40432. 内部控制有效性自愿披露的经济决定因素及后果:从首次公开发行的证据( March 2013 ) Economic Determinants and Consequences of Voluntary Disclosure of Internal Control Effectiveness: Evidence from Initial Public Offerings33. 非营利组织中内部控制问题的原因和后果The Causes and Consequences of Internal Control Problems in Nonprofit Organizations34. SOX 内部控制披露在公司控制权市场中的价值The Value of SOX Internal Control Disclosures in the Market for Corporate Control35. 内部控制缺陷与销售、一般的及行政费用的非对称性行为Internal Control Weakness and the Asymmetrical Behavior of Selling, General, and Administrative Costs36. 内部控制缺陷及补救措施披露对投资者感知的盈余质量的影响The Impact of Disclosures of Internal Control Weaknesses and Remediation on Investor-Perceived Earnings Quality37. 内部控制缺陷与美国上市的中国公司与美国公司的审计师SOX Internal Control Deficiencies and Auditors of U.S.-Listed Chinese versus U.S. Firms38. 内部控制信息披露与代理成本—来自瑞士的非金融类上市公司的证据( January 2013) Internal Control Disclosure and Agency Costs Evidence from Swiss listed non-financial Companies39. 萨班斯奥克斯利法案与公司投资:来自自然实验的新证据The Sarbanes-Oxley Act and Corporate Investment: New Evidence from a Natural Experiment40. 国内投资者保护、所有权结构与交叉上市公司遵守SOX 要求披露内部控制缺陷Home Country Investor Protection, Ownership Structure and Cross-Listed Firms 'Compliance with SOX-Mandated Internal Control Deficiency Disclosure41. 审计师对披露重大缺陷相关风险的看法Auditors ' Percenpsti o f the Risks Associated with Disclosing Material Weaknesses42. 交叉上市公司提供与美国公司相同质量的披露?来自萨班斯-奥克斯利法案302 条款下的内部控制缺陷信息披露的证据Do cross-listed firms provide the same quality disclosure as U.S. firms? Evidence from the internal control deficiency disclosure under Section 302 of the Sarbanes-Oxley Act43. 内部控制缺陷与并购绩效Internal Control Weaknesses and Acquisition Performance44. 萨班斯-奥克斯利法案302 条款下的内部控制缺陷对审计费用的影响The Effect of Internal Control Weakness under Section 404 of the Sarbanes-Oxley Act on Audit Fees45. 审计师对财务报告内部控制的评价对审计费用、债务成本及净遵从收益The Effect of Auditors ' Assessment of Internal Control of over Financial Reporting on Audit Fees, Cost of Debt and Net Compliance Benefit46. 上市公司披露的信息含量与萨班斯-奥克斯利法案Information Content of Public Firm Disclosures and the Sarbanes-Oxley Act47. 财务错报与股票市场的契约:从增发的证据Financial Misstatements and Contracting in the Equity Market: Evidence from Seasoned Equity Offerings48. 公司治理质量与SOX 302 条款下内部控制报告Corporate Governance Quality and Internal Control Reporting Under Sox Section 30249. 审计委员会质量、审计师独立性与内部控制缺陷Audit Committee Quality, Auditor Independence, and Internal Control Weaknesses50. SOX404 条款的影响:成本,盈余质量与股票价格The Effect of SOX Section 404: Costs, Earnings Quality, and Stock Prices51. 内部控制缺陷与银行贷款契约:来自SOX404 条款披露的证据Internal Control Weakness and Bank Loan Contracting: Evidence from SOX Section 404 Disclosures52. 审计师对财务报告内部控制的决策:分析、综合和研究方向Auditors I'nternal Control Over Financial Reporting Decisions: Analysis, Synthesis, and Research Directions 53. 应计质量与财务报告内部控制( Doyle ,The Accounting Review, forthcoming )Accruals Quality and Internal Control over Financial Reporting54. 业绩基础CEO 和CFO 薪酬对内部控制质量的影响The impact of performance-based CEO and CFO compensation on internal control quality55. 内部控制重大缺陷与CFO 薪酬Internal Control Material Weaknesses and CFO Compensation56. 财务报告内部控制缺陷的决定因素Determinants of weaknesses in internal control over financial reporting57. 内部控制与管理指南Internal Control and Management Guidance58. 2002 萨班斯-奥克斯利法案302 条款下内部控制缺陷的市场反应以及这些缺陷的特征Market Reactions to the Disclosure of Internal Control Weaknesses and to the Characteristics of thoseWeaknesses under Section 302 of the Sarbanes Oxley Act of 200259. 自愿报告内部风险管理和控制系统的经济激励Economic Incentives for Voluntary Reporting on Internal Risk Management and Control Systems60. 后萨班斯法案时代审计意见的信息含量The information content of audit opinions in the post-sox era61. 上市公司披露的信息含量与萨班斯-奥克斯利法案( April, 2010 )Information Content of Public Firm Disclosures and the Sarbanes-Oxley Act62. 信息摩擦如何影响公司资产流动性的选择?萨班斯法案404 条款的影响How do Informational Frictions Affect the Firm s Choice of A'sset Liquidity? The Effect of SOX Section 404 63. 已审计的信息披露给资本市场参与者带来利益是什么( December 19, 2013)What are the benefits of audited disclosures to equity market participants64. 诉讼风险与审计定价:公众股权的作用( January 7, 2013)Litigation Risk and Audit Pricing: The Role of Public Equity65. 萨班斯-奥克斯利法案对IPO 和高收益债券发行人的影响The Impact of Sarbanes-Oxley on IPOs and High Yield Debt Issuers66. 来自金融危机的公司治理的经验教训The Corporate Governance Lessons from the Financial Crisis67. 谁对企业欺诈吹口哨Who Blows the Whistle on Corporate Fraud68. 内部控制缺陷与现金持有价值Internal Control Weakness and Value of Cash Holdings69. 民族文化和制度环境对内部控制信息披露的影响The impact of national culture and institutional Environment on internal control disclosures70. 财务报告质量与权益资本成本之间联系的讨论:一些个人的意见( June 6, 2013)Some Personal Observations on the Debate on the Link between Financial Reporting Quality and the Cost of Equity Capital71. 使用盈利预测同时估计企业层面的权益资本成本和长期增长Using Earnings Forecasts to Simultaneously Estimate Firm-Specific Cost of Equity and Long-Term Growth72. 高管薪酬差距与权益资本成本Executive Pay Disparity and the Cost of Equity Capital73. 财务报告质量与公司债券市场(博士论文,Mingzhi Liu, 2011 )Financial Reporting Quality and Corporate Bond MarketsReferencesAboody, D., J. Hughes, and J. Liu. (2005) Earnings quality, insider trading, and cost of capital. Journalof Acco un ti ng Research 43: 651 -673.Akins, B., J. Ng and R. Verdi (2012) Investor competition over information and the pricing of information asymmetry. The Accounting Review 87(1): 35-58.Ali, A., A. Klein and J. Rosenfeld. (1992) Analysts ' use of information abouttrpaenrsmitaonryent andearnings components in forecasting annual EPS. The Accounting Review 67: 183-198.Amihud, Y., and H. Mendelson. (1986) Asset pricing and the bid-ask spread. Journal of Financial Econo mics 17: 223 —49.Artiach, T. and P. Clarkson. (2011) Disclosure, conservatism and the cost of equity capital: A review of the foundation literature. Accounting and Finance 51(1): 2-49.Ashbaugh-Skaiffe, H., D. Collins, W. Kinney, Jr., and R. LaFond (2009) The effect of SOX internal control deficiencies on firm risk and cost of equity. Journal of Accounting Research 47(1): 1-43.Armstrong, C., J. Core, D. Taylor and R. Verrecchia (2011) When does information asymmetry affect the cost of capital? Journal of Accounting Research 49(1): 1-40.Balakrishnan, K., R. Vashishtha and R. Verrecchia (2012) Aggregate competition, information asymmetry and cost of capital: Evidence from equity market liberalization. Working paper, University of Pennsylvania.Barron, O., O. Kim, S. Lim and D. Stevens (1998) Using analysts forecasts to measure properties on analysts ' information environmeTnth.e Accounting Review 73: 421-433.Barry, C., and S. Brown. (1985) Differential information and security market equilibrium. Journal of Financial and Quantitative Analysis 20: 407 T22.Barth, M., W. Beaver, and W. Landsman (2001) The relevance of value-relevance literature for financial accounting standard setting: Another view, Journal of A”ccounting and Economics (Sept): 77-104.Barth, M., Y. Konchitchki and W. Landsman (2013) Cost of capital and earnings transparency. Journal of Accounting and Economics , forthcoming.Beyer A., D. Cohen, T. Lys and B. Walther (2010) The financial reporting environment: Review of the recent literature. Journal of Accounting and Economics 50: 296-343.Bhattacharya, N., F. Ecker, P. Olsson, and K. Schipper (2012) Direct and mediated association among earnings quality, information asymmetry, and the cost of capital, The Accounting Review 87(2): 449-482. Botosan, C. (1997) Disclosure level and the cost of equity capital. The Accounting Review 72: 323 -350. Botosan, C., and M. Plumlee. (2002) A re-examination of disclosure level and the expected cost of equity capital. Journal of Accounting Research 40: 21 ZO.Botosan, C., M. Plumlee and Y. Xie (2004) The role of information precision in determining the cost of equity capital. Review of Accounting Studies 9 (2-3): 233-259.Botosan, C., and M. Plumlee. (2005) Assessing alternative proxies for the expected risk premium. The Accounting Review 80: 21-53.Botosan, C., M. Plumlee and H. Wen. (2011) The relation between expected returns, realized returns, and firm risk characteristics. Contemporary Accounting Research 28(4): 1085-1122.Brown, P. and T. Walter (2012) The CAPM: Theoretical validity, empirical intractability and practical applications. Abacus 1-7.Callahan, C., R. Smith and A. Spencer (2012) An examination of the cost of capital implications of FIN 46. The Accounting Review 87(4): 1105-1134.Chava, S., and A. Purnanandam (2010) Is default risk negatively related to stock returns? Review of Financial Studies 23: 2523-2559.Chen, S., B. Miao and T. Shevlin (2013) A new measure of disclosure quality: The level of disaggregation of accounting data in annual reports. Working paper, The University of Texas at Austin. Christensen, P., L. de la Rosa and G. Feltham (2010) Information and the cost of capital: An ex ante perspective. The Accounting Review 85(3): 817-848.Clarkson, P., J. Guedes and R. Thompson (1996) On the diversifiability, observability, and measurement of estimation risk. Journal of Financial and Quantitative Analysis 31: 69084.Claus, J., and J. Thomas (2001) Equity premia as low as three percent? Evidence from analysts earnings forecasts for domestic and international stock markets. The Journal of Finance 56(5): 1629-1666.Clinch G., and B. Lombardi (2011) Information and the cost of capital: the Easley- O' Hara(2004) modelwith endogeneous information acquisition. Australian Journal of Management 36(5): 5-14.Coles, J., U. Loewenstein, and J. Suay. (1995) On equilibrium pricing under parameter uncertainty. The Journal of Financial and Quantitative Analysis 30: 347 -374.Core, J., (2001) A review of the empirical disclosure literature: Discussion. Journal of Accounting and Economics 31: 441-456.Core, J., W. Guay and R. Verdi, (2008) Is accruals quality a priced risk factor? Journal of Accountingand Economics 46: 2-22.Daniel, K. and S. Titman, 1997, Evidence on the characteristics of cross-sectional variation in common stock returns. Journal of Finance 52, 1-33.Daske, H., L Hail, C. Leuz and R. Verdi (2008) Mandatory IFRS reporting around the world: Early evidence on the economic consequences. Journal of Accounting Research 46: 1085-1142.Daske, H., L Hail, C. Leuz and R. Verdi, (2013) Adopting a label: Heterogeneity in the economic consequences around IAS/IFRS adoptions. Journal of Accounting Research 51(3):495-548.Dechow, P. and I. Dichev. (2002) The quality of accruals and earnings: the role of accrual estimation errors. The Accounting Review 77 (Supplement): 35-59.Dechow, P., W. Ge and C. Schrand (2010) Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of Accounting and Economics 50: 344-401.Dhaliwal, D., L. Krull and W. Moser (2005) Dividend taxes and implied cost of equity capital. Journal of Accounting Research 43(5): 675-708.Dhaliwal, D., L. Krull and O. Li (2007) Did the 2003 Tax Act reduce the cost of equity capital? Journal of Accounting and Economics 43(1): 121-150.Diamond, D., and R. Verrecchia. (1991) Disclosure, liquidity, and cost of capital. Journal of Finance 46: 1325 -59. Dye, R., (2001) An evaluation of “ essayson disclosure a”nd the disclosure literature in accounting. Journal of Accounting and Economics 32: 181-235.Easley, D., S. Hvidkjaer and M. O'Hara.(2002) Is information risk a determinant of asset returns. Journal of Finance 57: 2185-2221.Easley, D., and M. O' Hara. (2004) Information and the cost of capital. Journal of Fi nance 59: 1553-1583. Easton, P. (2004) PE ratios, PEG ratios, and estimating the implied expected rate of return on equity capital. The Accounting Review 79(1): 73-96.Easton, P., and S. Monahan. (2005) An evaluation of accounting based measures of expected returns. The Accounting Review 80: 501 -538.Easton, P., and S. Monahan. (2010) Evaluating accounting-based measures of expected returns: Easton and Monahan and Botosan and Plumlee redux. Working paper, University of Notre Dame.Ecker, F., J. Francis, I. Kim, P. Olsson, and K. Schipper (2006). A returns-based representation of earnings quality. The Accounting Review 81: 749 -780.Fama, E., and J. MacBeth. 1973. Risk, return, and equilibrium: Empirical tests. Journal of Political Economy 81: 607-636.Fama, E., and K. French. (1992) The cross-section of expected stock returns. Journal of Finance 47(2): 427-465. Fama, E., and K. French. (1993) Common risk factors in the returns on bonds and stocks. Journal of Financial Economics 33: 3-56.Francis, J., LaFond, R., Olsson, P., and K. Schipper. (2004) Costs of equity and earnings attributes. The Accounting Review 79: 967-1010.Francis, J., LaFond, R., Olsson, P., and K. Schipper. (2005) The market pricing of accruals quality. Journal of Accounting & Economics 39: 295-327.Francis, J., Nanda, D., and P. Olsson. (2008) Voluntary disclosure, information quality, and costs of capital. Journal of Accounting Research 46 (1): 53-99.Gebhardt,W., C. Lee and B. Swaminathan (2001) Towards an ex ante cost of capital. Journal of Accounting Research 39(1): 135-176.Goh, B-W., J. Lee, C-Y. Lim and T. Shevlin (2013) The effect of corporate tax avoidance on the cost of equity. Working paper, Singapore Management University.Gow, I., G. Ormazabal and D. Taylor (2010) Correcting for cross-sectional and time-series dependence in accounting research The Accounting Review 85(2): 483-512.Gray, P., P. Koh and Y. Tong (2009) Accruals quality, information risk and cost of capital: Evidence from Australia. Journal of Business Finance and Accounting 36(1-2): 51-72.Guay, W., S.P. Kothari and S. Shu (2011) Properties of implied cost of capital using analysts forecasts. Australian Journal of Management 36(2): 125-149.Hail, L. (2002) The impact of voluntary corporate disclosure on the ex-ante cost of capital for Swiss firms European Accounting Review 11: 741-773.Hail, L., and C. Leuz. (2006) International differences in the cost of equity capital: Do legal institutions and securities regulation matter? Journal of Accounting Research 44(3): 485-531.Healy, P., and K. Palepu (2001) Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics 31: 405-440. Hirshleifer, D., K. Hou, and S.H. Teoh (2012) The accrual anomaly: Risk or mispricing? ManagementScienee (58-2); 320 -335.Holthausen, R., and R. Watts (2001) The relevance of value-relevance literature for financial accounting standard setting. Journal of Accounting and Economics (Sept): 3-75.Hribar, P. and T, Jenkins. (2004) The effect of accounting restatements on earnings revisions and the estimated cost of capital. Review of Accounting Studies 9(2-3): 337-356.Hughes, J. S., J. Liu, and J. Liu. (2007) Information asymmetry, diversification, and cost of capital. The Accounting Review 82: 705-729.Hughes, J. S., J. Liu, and J. Liu. (2009) On the association between expected returns and implied cost of capital R”eview of Accounting Studies 14: 246-259.Hutchens, M. and S. Rego (2013) Tax risk and the cost of equity capital. Working paper, Indiana University. Hwang, L-S., W-J. Lee, S-Y. Lim and K-H. Park, (2013) Does information risk affect the implied cost of equity capital? An analysis of PIN and adjusted PIN. Journal of Accounting and Economics 55(2-3): 148-167.Kim, D., and Y. Qi (2010) Accruals quality, stock returns, and macroeconomic conditions. The Accounting Review 85(3): 937-978.Klein, R., and V. Bawa. (1977) The effect of estimation risk on optimal portfolio choice. Journal of Financial Economics 3: 215-231.Kothari, S.P., X. Li and J. Short. (2009) The effect of disclosures by management, analysts, and financial press oncost of capital, return volatility, and analyst forecasts: A study using content analysis. The Accounting Review82(5): 1255-1297.Kravet, T. and T. Shevlin. (2010) Accounting restatements and information risk. Review of Accounting Studies 15: 264-294.Kyle, A. (1985) Continuous auctions and insider trade. Econometrica 53(6): 1315-1335.Lambert, R., C. Leuz, and R. Verrecchia. (2007) Accounting information, disclosure, and the cost of capital. Journal of Accounting Research 45(2): 385-420.Lambert, R., C. Leuz, and R. Verrecchia. (2012) Information asymmetry, information precision, and the cost of capital. Review of Finance 16: 1-29.Lambert, R., (2009) Discussion of “onthe association between expected returns and implied cost of capital R”eview of Accounting Studies 14: 260-268.Leuz, C., and R. Verrecchia (2004) Firms ' capital allocatio n choices, in formati on qhuaCys tandcapital. Work ing paper, Uni versity of Penn sylva nia.Li, V., T. Shevli n and D. Shores (2013) Revisit ing the AQ measure of accrual quality. Work ing paper, Uni versityof Wash ington.Lys, T., and S. Sohn. (1990) The associati on betwee n revisi ons of finan cial an alyst forecastsearning and security price cha nges. Jour nal of Acco un ti ng and Econo mics 13: 341-363.Mashruwala, C. and S. Mashruwala (2011) The pric ing of accrual quality: January versus the rest of the year. TheAccou nting Review 86(4): 1349-1381.McInnis, J. (2010) Earnings smoothness, average returns and implied cost of equity capital. The Accou ntingReview 85(1): 315-341.Mohanram, P., and D. Gode (2013) Removing predictable analyst forecast errors to improve implied cost of equity estimates. Review of Acco un ti ng Studies 18: 443-478.Ogneva, M., K.R. Subramanyam, and K. Raghunandan (2007) Internal control weakness and cost of equity: Evidenee from SOX Section 404 disclosures. The Accou nti ng Review 82(5) :1255-1297.Ogneva, M., (2012) Accrual quality, realized returns, and expected returns: The importanee of con trolli ng forcash flow shocks, The Accou nting Review 87(4): 1415-1444.Peterse n, M., (2009) Estimati ng sta ndard errors in finance data pan els: Compari ng approaches. Reviewof Financial Studies 22(1): 435-480.Petkova, R. (2006) Do the Fama-Fre nch factors proxy for inno vati on in predictive variables? Journal of Finance61: 581-612.Reidl, E., and G. Serafeim (2011) In formati on risk and fair values: An exam in ati on of equity betas. Journal ofAccounting Research 49(4): 1083-1122.Strobl, G., (2013) Earnings manipulation and the cost of capital. Journal of Accounting Research, forthco ming. Verrecchia, R. (2001) Essays on disclosure. Journal of Accounting and Economics 32: 97-180.Vuolteenaho, T. (2002) What drives firm-level stock returns? The Journal of Finance 57: 233 -264.How Do Various Forms of Auditor Rotation Affect Audit Quality? Evidence from China内部控制质量、企业风险与权益资本成本一一理论分析与实证检验1. Accruals Quality and In ternal Con trol over Finan cial Report in g.Acco un ti ng Review, Oct2007, V ol.82 Issue52. Audit Committee Quality and Internal Control An Empirical Analysis.FullAccounting Review, Apr2005, Vol.80 Issue 23. Bala ncing the Dual Resp on sibilities of Busin ess Un it Con trollers Field and Survey Evide nee. Accounting Review, Jul2009, Vol. 84 Issue44. Corporate Governance and Internal Control over Financial Reporting A Comparison ofRegulatory Regimes Accou nting Review, May2009, Vol. 84 Issue 35. Ear nings Man ageme nt of Firms Report ing Material In ternal Con trol Weak nesses un der Sect ion 404of the Sarbanes-Oxley Act. Auditing, Nov2008, Vol. 27 Issue 26. Economic Incentives for V oluntary Reporting on Internal Risk Management and Control Systems.Auditing, May2008, V ol. 27 Issue 67. Firm Characteristics and Volu ntary Man ageme nt Reports on In ternal Con trol. Audit ing, Nov2006,Vol. 25 Issue28. Former Audit Partners on the Audit Committee and Internal Control Deficiencies. Accounting Review,Mar2009, Vol. 849.Internal Control Quality and Audit Pricing under the Sarbanes-Oxley Act . Auditing, May2008, Vol.2710.Internal Control Weakness and Cost of Equity Evidenee from SOX Section 404 Disclosures Accou nti ngReview, Oct2007, Vol. 8211.I nternal Control Weak nesses and In formatio n Un certai nty. Accou nting Review, May2008, Vol. 8312.lnternal Controls and the Detection of Management Fraud. Journal of Accounting Research, Sprin g99,Vol. 3713.Reduci ng Man ageme nt's In flue nee on Auditors Judgme nts An Experime ntal In vestigati on of SOX404 Assessme nts Acco un ti ng Review, Nov2008, V)l. 8314.SOX Section 404 Material WeaknessDisclosures and Audit Fees.Full Auditing, May2006, Vol. 2515.The Effect of SOX Internal Control Deficiencies and Their Remediation on Accrual Quality. AccountingReview, Jan2008, Vol. 8316.The Impact of SOX Section 404 Internal Control Quality Assessment on Audit Delay in the SOX Era.Auditing, Nov2006, Vol. 25Ashbaugh-Skaife, H., Collins, D. W., & Kinney Jr., W. R. (2007). The discovery and reporting of internal con trol deficie ncies prior to SOX-ma ndated audits. Jour nal of Acco unting and Economics, 44(1 —2), 166 -92.Ashbaugh-Skaife, H., Collins, D. W., Kinney Jr, W. R., & Lafond, R. (2009). The Effect of SOX Internal Control Deficiencies on Firm Risk and Cost of Equity. Journal of Accounting Research, 47(1),1 -43.Bahramian, A. (2011), Evaluation of the effectiveness of internal controls in an Investment Company, Master Thesis in Imam Hossein University, Iran.Daraby, M, (2006), analyzing the effect of strengthening internal controls, audit reports of companies listed on the Stock Audit, Master Thesis in Azan Islamic university.Doyle, J., Ge, W., & McVay, S. (2007). Determinants of weaknesses in internal control over financial reporting. Journal of Accounting and Economics, 44(1 -2), 193 -223.Feng, M., Li, C., & McVay, S. (2009). Internal control and management guidance. Journal of Accounting and Economics, 48(2 -3), 190 -209.Maham K., Poriya Nasab, A. (2000), Internal control) Integrated Framework( , Report of the Committee of the Commission Tardy, azman Hesabresy, Pages 118, 135.Ogneva, M., Subramanyam, K. R., & Raghunandan, K. (2007). Internal control weakness and cost of equity: evidence from SOX Section 404 disclosures. The Accounting Review, 82(5), 1255-1297.Rezaie Jahangoshaee, H, (1996). A analytical study of the degree of reliance of independent auditors on firms internal controls, Master Thesis, shahid Beheshti University, Iran.。

新核心综合学术英语教程 4 Unit 3 参考答案

Focusing on ReadingTask 11.G2. E3. C4. F5. A6. D7.J8. B9.L10.H 11. N 12. M 13. Q 14.K 15. I 16.R 17.O 18.PTask 21)The reasons are as follows”Firstly, students sometimes view academic dishonesty as a normal incidence and something ordinary. There are many reasons that they use to justify their cheating.Secondly, new techniques of cheating have been developed, including the use of high-tech tools, although the old ones are still dominant on campus, which makes it even more difficult for the faculty to identify.Thirdly, it is a common view to equate grades with the value of the student. Furthermore, grades are used to predict one’s future success. So some students tend to practice academic dishonesty with the aim of getting higher grades.Fourthly, little is known about the degree of academic dishonesty and no methods are devised to combat the problem. Besides, there are no strategies for deterring academic dishonesty for the faculty.Fifthly, honor codes are essential to reducing the level of cheating in colleges and should be established. However, their importance has been neglected.Last but not least, academic dishonesty is no longer a task of classroom management that can well be remedied by a single faulty with teaching responsibility. Administrators and professional organizations are expected to work together to maintain a healthy learning environment with a high level of trust between the faculty and the administration.2)Old techniques include bringing notes to class and having information written on water bottles,pens and gum wrappers. New techniques of cheating include using cell phones to get the information, communicate with others outside the exam room to obtain answers and searching answers on the web during an exam.Other forms include copying test responses from a classmate, taking exams for other people, failure to cite other people’s work, and purchasing research papers and presenting them as his/her work. Also actions such as breaking into the office or teachers files to access the test or answer key, sabotaging peers ongoing work or gaining illegal access to school computers to change official grades are all forms of academic dishonesty. (B)3)There are many reasons that students use to justify cheating: lack of time, poverty, uncaringinstructors, laziness, peer pressure, poor rile models, fear of failure and technology that has allowed cheating to be done easily. (C)Besides, research shows that a common view equates grades with the value of the student.Secondly, grades are used to predict one’s future success. This may cause the students to practice academic dishonesty.4)Studies show that honor codes were essential to reducing the level of cheating in colleges.Honor codes would be more successful when they were combined with a climate that emphasized the importance of academic integrity and an honor system that allowed for strong student involvement in the enforcement of academic integrity initiatives. Therefore, the administration should strive in the creation of the campus environment, seek the full support of all the college constituents, and ensure the implementation of the honor codes at theinstitution. (N)5)Academic fraternity means “all the people who work in academia.”It can stress integrity as a core institutional value that will shape the students’academic success.Task 31. a2. j3. W4. m5. k6. o7. v8. x9.n 10.b 11. u 12.y 13.d14. i 15. f 16. z 17. t 18.p 19. S 20. q 21. e 22. g 23. c 24. h 25. l 26. rTask 51)Another kind of academic dishonesty happens sometimes among researchers when they yieldto the temptation of making a series of great discoveries. So they invent false information to deceive others, and then publish them.2)Bouville(2010) held that the major reason for the students to avoid academic dishonesty wasto obey the rules and escape punishment. Cheaters may get high grades which they do not deserve, and this unfair advantage will tempt them to continue with this fraudulent behaviour.3)Third, in each department there should be experienced faculty members, acting as academicintegrity chairmen, who are responsible for contacting and offering help to their fellow colleagues. Lastly, for faculty members who have tackled the cases of academic dishonesty well, public thanks and admiration should be given to them for what they have done.Task 6Main idea: Students developed new techniques of cheating, while the old ones are still dominant on campus.Task 7In the area of education, academic dishonesty is a chronic problem. Students have developed new techniques of cheating, while the old ones are still dominant on campus. Cheaters follow dishonest practices because of many reasons. Prevention of academic dishonesty demands joint efforts from students, teachers and administrators, of which the students’ contribution is vital for they are the ones to be subjected to the penalties. For the teachers, they can adopt four strategies to maintain academic integrity and meanwhile make efforts to motivate the students. For the administrators, they should strive in the creation of a healthy academic climate and ensure the implementation of the honor codes.Task 8(omitted)Task 9(omitted)Task 10Academic DishonestyAcademic dishonesty occurs when a student uses or attempts to use unauthorized information in the taking of an exam; or submits as his or her own work themes, reports, drawings, laboratory notes, or other products prepared by another person; or knowingly assists another student in such acts or plagiarism. Such behavior is abhorrent to the university, and students found responsible for academic dishonesty face expulsion, suspension, conduct probation, or reprimand. Instances of academic dishonesty ultimately affect all students and the entire university community by degrading the value of diplomas when some are obtained dishonestly, and by lowering the grades of students working honestly.Examples of specific acts of academic dishonesty include but are not limited to:a) Obtaining unauthorized information. Information is obtained dishonestly, for example, bycopying graded homework assignments from another student, by working with another student on a take-home test or homework when not specifically permitted to do so by the instructor, or by looking at your notes or other written work during an examination when not specifically permitted to do so.b) Tendering of information. Students may not give or sell their work to another person who plans to submit it as his or her own. This includes giving their work to another student to be copied, giving someone answers to exam questions during the exam, taking an exam and discussing its contents with students who will be taking the same exam, or giving or selling a term paper to another student.c) Misrepresentation. Students misrepresent their work by handing in the work of someone else. The following are examples: purchasing a paper from a term paper service; reproducing another person’s paper (even with modifications) and submitting it as their own; having another studentdo their computer program or having someone else take their exam.d) Bribery. Offering money or any item or service to a faculty member or any other person to gain academic advantage for yourself or another is dishonest.e) Plagiarism. Unacknowledged use of the information, ideas, or phrasing of other writers is an offense comparable with theft and fraud, and it is so recognized by the copyright and patent laws. Literary offenses of this kind are known as plagiarism.One is responsible for plagiarism when: the exact words of another writer are used without using quotation marks and indicating the source of the words; the words of another are summarized or paraphrased without giving the credit that is due; the ideas from another writer are borrowed without properly documenting their source.Acknowledging the sources of borrowed material is a simple, straightforward procedure that will strengthen the paper and assure the integrity of the wri ter. The Student’s Guide to English 104 —105, provides guidelines to aid students in documenting material borrowed from other sources, as does almost every handbook on writing style.Academic dishonesty is considered to be a violation of the behavior expected of a student in an academic setting as well as a student conduct violation. A student found responsible for academic dishonesty or academic misconduct is therefore subject to the appropriate academic penalty; to be determined by the instructor of the course, as well as sanctions under the university Student Disciplinary Regulations.If an instructor believes that a student has behaved dishonestly in a course, the following steps are to be followed:1. The instructor should confront the student with the charge of dishonesty and arrange a meetingwith the student to discuss the charge and to hear the student’s explanation.2. If the student admits responsibility for academic misconduct, the instructor shall inform the student (a) of the grade on the work in which the dishonesty occurred, and (b) how this incident will affect subsequent evaluation and the final grade. Because academic dishonesty is also a student conduct violation under Section 4.2.1 of the Student Disciplinary Regulations, the instructor must report the incident in writing to the Dean of Students.After investigating the incident and discussing it with the instructor, the Dean of Students, or his/her designee, will meet with the student and depending on the severity of the offense as well as on the student’s past conduct record, may handle the matter through an administrative hearing or schedule a hearing before the All University Judiciary (AUJ).This hearing, conducted according to the procedures outlined in the Student Disciplinary Regulations, is to determine the disciplinary action to be taken. In any case, the student’s academic adviser will be informed of the incident but may not insert any record of it in the student’s academic file.3. If the student claims to be not responsible for the alleged violation of academic misconduct, the instructor may not assign the student a grade for the work in question until the question of responsibility is resolved, unless circumstances require that an interim grade be assigned. The instructor shall consult with his or her department chair and report the incident in writing to the Dean of Students.The Dean of Students will refer the case to the Office of Judicial Affairs for investigation. After reviewing the report and completing an investigation, the Office of Judicial Affairs will file aformal complaint against the student if it is determined that there is cause to believe academic misconduct occurred. The case may be adjudicated through an administrative hearing or referred to a hearing before the All University Judiciary (AUJ) depending on the nature and severity of the violation as set forth in the Student Disciplinary Regulations.If the case is referred to the AUJ both the student and instructor will be invited to attend an AUJ hearing and present pertinent information. If the Administrative Hearing Off icer (in a minor case) or the AUJ (in a major case) finds the student responsible for the charge of academic misconduct, the instructor will inform the student (a) of the grade on the work in which the dishonesty occurred, and (b) how this incident will affect subsequent evaluation and the final grade. The Administrative Hearing Officer or AUJ will determine the appropriate disciplinary action with respect to the nature of the violation.If the Administrative Hearing Officer or AUJ finds the student “not responsible” for academic misconduct, the instructor will grade the student accordingly on the work in question and the student’s grade in the course will not be adversely affected. If th e student is found responsible the student’s adviser will be informed of the decision but shall not insert any record of the action in the student’s academic file.4. If a student either admits dishonest behavior or is found responsible for academic misconduct by the AUJ, the Off ice of Judicial Affairs (OJA) or AUJ may impose any of the following sanctions:a) Disciplinary Reprimand: An official written notice to the student that his/her conduct is in violation of university rules and regulations.b) Conduct Probation: A more severe sanction than a disciplinary reprimand, to include a period of review and observation during which the student must demonstrate the ability to comply with university rules, regulations, and other requirements stipulated for the probation period.c) Suspension/Deferred Suspension: The suspension is deferred subject to a definite or indefinite period of observation and review. If a student is found responsible for a further violation of the university Student Disciplinary Regulations or an order of a judiciary body, suspension will take place immediately.Def i niteThe student is dropped from the university for a specific length of time. This suspension cannot be for less than one semester or more than two years.Indef i nite:The Student is dropped from the university indefinitely. Reinstatement may be contingent upon meeting the written requirements of the AUJ specified at the time the sanction was imposed. Normally, a student who is suspended indefinitely may not be reinstated for a minimum of two years.d) Expulsion: The student is permanently deprived of the opportunity to continue at the university in any status.5. A student accused of academic misconduct has the option to stay in the class or to drop the class if the drop is made within the approved time periods and according to the regulations established by the university. If the student chooses to drop the class, the student will be required to sign a statement of understanding that if the student is later found responsible for academic misconduct, then the student will receive an F for the course.6. Procedures for appeal of either the All University Judi ciary’s conduct decision or theinstructor’s grade are outlined in the Student Information Handbook.7. In instances in which the student admits responsibility or is judged to be responsible by OJA or the AUJ, a staff member of the Dean of Students Off ice will counsel the student in an effort to deter any further such incidents.8. Student records concerning academic dishonesty are maintained in the Dean of Students Office for a period of seven years, after which the file records are purged. These student records are confidential; nothing from them appears on a student’s academic transcript.9. In the event that an instructor is uncertain how to handle an incident of suspected academic dishonesty, the Dean of Students is available at any time to provide advice and assistance to the instructor in deciding a proper course of action to be taken.10. Students enrolled in the College of Veterinary Medicine are bound by an honor code. A chargeof academic dishonesty may be made by a student or instructor to the Interclass Honor Board chairperson according to the procedures outlined in the Honor Code, or the instructor may follow procedures outlined above. The Interclass Honor Board functions as the judiciary of the College of Veterinary Medicine for the allegations presented to it.Other violations related to academic misconduct may include subsection 4.1.11 Misuse of Computers and subsection 4.2.20 Unauthorized Sale of Others’Intellectual Works.These subsections are located in the Iowa State University Student Disciplinary Regulations under section 4 of the Conduct Code.</~catalog/2005-07/geninfo/dishonesty.html>Short reportAcademic dishonesty occurs when a student uses or attempts to use unauthorized information in the taking of an exam; or submits as his or her own work themes, reports, drawings, laboratory notes, or other products prepared by another person; or knowingly assists another student in such acts or plagiarism. Such behavior is abhorrent to the university, and students found responsible for academic dishonesty face expulsion, suspension, conduct probation, or reprimand. Instances of academic dishonesty ultimately affect all students and the entire university community by degrading the value of diplomas when some are obtained dishonestly, and by lowering the grades of students working honestly.Examples of specific acts of academic dishonesty include obtaining unauthorized information, tendering of information, misrepresentation, bribery, plagiarism, etc. Academic dishonesty is considered to be a violation of the behavior expected of a student in an academic setting as well as a student conduct violation.In Iowa State University, a student found responsible for academic dishonesty or academic misconduct is therefore subject to appropriate academic penalty or to be determined by the instructor of the course, as well as sanctions under the university Student Disciplinary Regulations. If an instructor believes that a student has behaved dishonestly in a course, ten steps are to be followed to handle the problem. The case of Iowa State UniversityResearch Paper WritingTask 1Background part:The introductionObjective:To give an overview of various forms of academic dishonesty, student responses to academic dishonesty when it occurs and the measures taken by the faculty and institutional administrator to prevent its occurrence in their institutions.Synthesis of different views on a particular field: For example, in the section “Forms of Academic Dishonesty,” in Para. B, there are opinions of both Jonson and Martin (2005) and Petress (2003), which are organized by transitional words, such as “Petress noted of other forms of academic dishonesty ...”Similarities or differences of outside sources:For example, in the section “Faculty and Academic Dishonesty”, when it comes to what the faculty should do to reduce academic dishonesty, there are various opinions from Para J to L. Perress (2003) holds that they should set role models for the students and implement the measures that will help prevent academic dishonesty. Whitley and Keith-Spiegel believe that they should be encouraged to form a statement concerning academic integrity in their syllabi and to discuss integrity concerns in their classrooms. Kibler notes four strategies to help the faculty to implement academic integrity. Cole and Kiss suggest that more efforts should be made to motivate the students by the teachers.Task 2a. The forms of cheating.Text 3 deals with students’ new and old techniques of cheating, together with researchers’ practices of academic dishonesty.Reading 1 focuses on academic dishonesty in online courses.Reading 1 gives more updated and reliable information.b. The reasons that students offer for their cheating.In Text 3 the reasons the students use to justify their cheating include: lack of time, poverty, uncaring instructors, laziness, peer pressure, poor role models, fear of failure and technology that has allowed cheating to be done easily. (Para. C)In Reading 1, the reasons are multifold because opinions vary. Some of the reasons are based on a student’s individual characteristics (Gerdeman 2001), some are relevant to peer inf luence or peers’acceptability of cheating (Stephens, 2007), while others have something to do with the existence of an honor code (McCabe, 2002). Meanwhile, there are other common reasons by Chiesl and Bunn, of which seeing other students cheat and the perception of the percentage of students who cheat are the most significant. (Para. I,J,K)Reading 1 gives more updated and reliable information.c. The definition of academic dishonesty.In Text 3, there is no specific definition of academic dishonesty.In Reading 1, the author believes that definitions of academic dishonesty across studies tend to be about the same. Using the scale of Don McCabe (2002), the author defines academic dishonesty from eight aspects. Other studies differentiate planned and panic cheating, e.g., Bunn, Caudill and Gropper (1992). In a comparative study of online versus on-ground academic dishonesty, Stuber- McEwen, Wisely, and Hoggat (2009) believe that there are seven forms. Stephens, Young, and Calabrese (2007) examined various forms of conventional and digital cheating. With regard toe-learning, Underwood (2003) and Rogers (2000) def ine the term respectively, while Howell et al (2009) reviews various forms of technological cheating. (Para.B, C, D, E, F, G)Reading 1Task 31) Serious and formal2) Angry and bitter3) Angry and ironical4) Angry and ironical5) Ironical6) Ironical7) Angry and ironical8) Angry9) Ironical10) Tranquil and formal11) Tranquil12) Tranquil and formal13) Formal and serious14) Formal and serious15) Expressing the speaker’s surprise and attitude against this16) Tranquil17) Expressing surprise, Ironical18) Appealing to the readers’ emotions by the use of questions, Ironical19) Appealing to the readers’ emotions by the use of questions, Angry and ironical20) “You” is used in the sentence to indicate people in general to appeal to their emotions, whichshortens the distance between the speaker and the readers21) Appealing to the readers’ emotions by the use of questions22) Appealing to the readers’ emotions by the use of facts and questions. Expressing the speaker’sdisagreementTask 41) Which one is a stand-alone literature review and which one is a literature review as a partof the paper?Text 3 and Reading 1: stand-alone literature reviewReading 2: literature review as a part of the paper2) What similarities and differences characterize the three papers in terms of writing style?Similarities: All of them follow almost the same pattern, i.e., introduction, body, and conclusion.Differences: Text 3 and reading 1 synthesize other people’s research and f indings to draw the conclusion, while Reading 2 uses the author’s own research and f indings. Therefore, in Reading 2 there is the part of “Methods”, which explains in detail the participants, materials, and design and procedure. The first-person narration is used to describe the process, which makes it less formal than the other two papers.3) What are the objectives of the three papers respectively?Text 3: To give an overview of various forms of academic dishonesty, student responses to academic dishonesty when it occurs and the measures taken by the faculty and institutional administrator to prevent its occurrence in their institutions.Reading 1: Examine perceptions of academic dishonesty in online and face-to-face courses, and discuss methods to reduce academic dishonesty in online courses.Reading 2: To investigate participants’ attitudes toward cheating and the effects of academic motivation, self-eff icacy, and academic integrity on cheating behaviors.4) How many aspects or sections do the two stand-alone literature review contain respectively?What are they?ThreeIntroduction, body, and conclusion5) Is the order of those aspects in each literature review logic al? And what’s the relationship?Yes.The literature review consists of three aspects: an introduction, a body, and a conclusion. The introduction part may tell the reason one is writing a review; the signif icance of the topic; the scope of the review; the organizational pattern of the review. The body will have a clear classif ication and synthesis of one’s reviewed readings in terms of chronological order or importance order. The conclusion should have a summary of the main agreements and disagreements in the literature and then any gaps or areas for further research. At last one’s overall perspective on the topic should be dealt with.6) How do the two authors illustrate their arguments in each section? Do they use their own research and f i ndings or synthesize other people’s research and f i ndings?By synthesizing other people’s research and f indings.No.Reading 2Task 51) indicate, is, identified, tend, will be2) predicted, was, have suggested, are, showed, appeared, were, wereTask 6A chimera is an individual composed of cells with different embryonic origins. The successful isolation of f ive human embryonic stem cell (HESC) lines in 1998 increased scientists’ ability to create human/non-human chimeras and prompted extensive bioethics discussion, resulting in what has been dubbed “the other stem cell debate” (Shreeve 2005). The debate about chimeras has focused on five main arguments. The Unnaturalness Argument explores the ethics of violatingnatural species boundaries. The Moral Confusion Argument alleges that the existence of entities that cannot be definitively classified as either human or non-human will cause moral confusion that will undermine valuable social and cultural practices. The Borderline-Personhood Argument focuses on great apes and concludes that their borderline-personhood confers a high enough degree of moral status to make most, if not all, chimeric research on them impermissible. The Human Dignity Argument claims that it is an affront to human dignity to give an individual “trapped” in the body of a non-human animal the capacities associated with human dignity. Finally, the Moral Status Framework maintains that research in which a non-human animal’s moral status is enhanced to that of a normal adult human is impermissible unless reasonable assurances are in place that its new moral status will be respected, which is unlikely given the motivations for chimeric research and the oversight likely to be provided.These arguments provide different rationales for restricting chimeric research and have different implications for the range of chimeric research that will be deemed unethical.</entries/chimeras/#Int>Task 71) Which sentences provide the background of the paper?Academic dishonesty is a problem that has been plaguing colleges and universities for generations. An investigation of any institution today will certainly reveal some forms of academic dishonesty.2) Which sentences form the literature review?Researchers of academic dishonesty vary in their reports of how many students cheat in college.3) What is the main limitation of the previous studies that the author mentioned?However, most research on academic dishonesty has relied primarily on self-reports of cheating behaviors.4) What’s the objective of the paper?The purpose of the study is to investigate participants’ attitudes toward cheating and the effects of academic motivation, self-efficacy, and academic integrity on cheating behaviors.5) What are the methods that the author will use?The present study includes an empirical portion in which participants are put in a situation in which cheating may be to their advantage.6) What is the author’s hypothesis?The hypothesis is that participants would be most likely to cheat when they are offered a monetary reward for success.Task 8Introduction 11) an introduction of the topic and its background2) a review about the previous studies3) the limitation of the previous studies4) a gap for the signif icance of the study5) the hypothesis of the author6) the objective of the paper7) the methodologyIntroduction 21) an introduction of the topic and its background2) a review about the previous studies and the limitation of the previous studies3) the limitation of the previous studiesTask 91) A2) B3) E4) C5) D6) FTask 10This paper details the strategies used for curbing academic dishonesty in online courses.Task 11Biologists have long known of patterns of inheritance, and eventually of inheritance mechanisms, that go beyond genetic inheritance (Jablonka & Lamb 2005; Sapp 1987). Two fundamental types of arguments led to this conclusion: arguments based on observations regarding patterns of inheritance, and arguments concerned with the localization of hereditary factors inside cells. Arguments of the first kind were based on hereditary relations and inheritance patterns that fail to conform to the rules ofMendelian inheritance (e.g., maternal inheritance). If Mendelian inheritance patterns are the result of the way the chromosomes in the eukaryotic cell nucleus behave, non-Mendelian heredity must depend on separate inheritance processes, mechanisms, or systems (Beale 1966; Sager 1966). Second, there were observations of hereditary phenomena that seemed to depend on factors residing in the cytoplasm of cells, rather than their nucleus, where the genetic material is localized. The interpretation of these observations was highly contested (Darlington 1944; Sapp 1987). Today, we know that some of these observations are related to the (maternal) inheritance of organelles residing in the cytoplasm, such as the mitochondria and chloroplasts, organelles which carry their own DNA. This however does not encompass all the mechanisms which underlie cytoplasmatic inheritance. Paradigmatic work on cytoplasmatic inheritance done by Sonneborn, Beale, Nanney, and their colleagues in the 1950s and 1960s, was concerned with patterns of inheritance in unicellular organisms, and in particular the protist genus Paramecium. It was suggested that the self-sustaining regulatory loops that maintain gene activity or inactivity in a cell would persist through cell division, provided the non-DNA components of the system (many of which reside in the cytoplasm in eukaryotic microogranisms) were shared among daughter cells. In this way, alternative regulatory phenotypic states would be inherited. Among the properties whose inheritance was studied were mating-type variations, serotype variations, and the structural or “surface inheritance” of ciliary structures. Remarkably, microsurgical changes to the ciliary structures on the surface of Paramecium cells are inherited by offspring. The stability of induced characters once the stimulus was removed (called “cellular memory”) and the number of generations characters were maintained varied widely.However, the results indicated that long-term stability and heritability need not be the result of changes to the DNA sequence (Nanney 1958).During the 1950s to 1970s a growing set of observations indicated that determined and differentiated states of cells are transmitted in cell lineages. These observations concerned studies of Drosophila imaginal discs by Ernst Hadorn; Briggs and King’s cloning experiments with amphibians; Mary Lyon’s work on X-chromosome inactivation; and work establishing the in vitro clonal stability of cultured cell lines. Eventually, the term epigenetic inheritance came to refer to hereditary variation that does not involve changes to the DNA sequence.The brief account of some of the early work on unicellular organisms given above illustrates some。

Over-and-under pericardial cov