关于增值税的国外文献

企业增值税纳税筹划外文文献翻译最新

外文文献翻译:原文+译文原文The research of corporate V AT planningPhillips J DAbstractEnterprise tax planning is very necessity. But most tax planning of enterprise is so difficult, the manager normally feel do not know how to start it. This is mainly because when doing tax planning personnel breadth and depth of thinking is limited. In fact, in view of the enterprise a certain business, as long as the tax personnel to all business related tax law research understand the relevant rules and regulations are in place, so companies when doing tax planning should be no problem. For example and to increase "camp" the tax planning, the categories of taxes that must be considered including the business tax and value-added tax, the relevant expenses such as urban maintenance and construction tax and educational expenses to add. Of course, the enterprise can not only consider when do tax planning; a business enterprise's business is very broad, so when doing tax planning to overall consideration. Keywords: value-added tax; the individual income tax; Tax rate; Tax planning1 IntroductionEnterprises between the increasingly fierce markets competitions, enterprises want to gain share in the market, a place, you must adapt to the evolution of natural law, has the stronger than other enterprise competitive power, and this kind of competition power depend mainly on market segment and reduce the cost. Undoubtedly tax is an important part in enterprise cost, the main body of enterprise tax include value added tax, income tax, business tax, consumption tax, etc., and occupy the largest proportion of is value added tax, accounting earnings and the realization of the goal of the enterprise plays an important significance. Because different countries have different social and economic development to its policy orientation, so differences exist in different countries and different industries, the tax policy and accounting system for the choice of accounting methods more flexible, which provides a choice of V AT tax conditions and space? The V AT tax planning forenterprise attention, recognition and more and more attention. Tax planning in gradually improve, already have a systematic and market characteristics. And the development of society, market economy unceasing prosperity, has prompted the company constantly innovate oneself production mode, operation concept, management style, etc.For the survival and development to adapt to market competition, enterprises will use every possible method to increase the interest, as far as possible to reduce the amount of unnecessary consumption, so how to reduce the tax burden is the problem that managers must consider carefully. Modern enterprises in pursuit of the enterprise value maximization as the goal development relative to evade taxes and tax risk of higher taxes, so business leaders can choose to reduce the tax, tax planning the implementation of reasonable overall planning can make the company a huge income.2 V AT descriptionsValue-added tax is the enterprise product in the process of production, circulation, and the value added part of the labor service or value added, the additional levy taxes. No matter which country, regardless of its power, as long as it is a value-added tax, to enact specific regulations on value-added tax. Generally divided into three kinds, one is the production, the second is income-producing, and three is a consumer.2.1 Production-type V ATProduction-oriented V AT has relationship with the company's production, it is well known that a mature enterprise need fixed plant, equipment, products used in the production of raw materials, transportation, fuel, fixed assets, product sales and production of profit, the sales revenue minus the production and operation of the balance of the raw materials, fuel and power as prescribed by the state of appreciation, this also is the basis of the production V AT, in principle, value added tax is not to be bought and depreciation of fixed assets, value added tax is a period of time limit, the tax basis by the tax unit labor balance, and used in the production of loss and the balance of sales revenue, which belongs to the category of value-added tax, fixed assets depreciation is used in the process of transfer value, is also a part of value-added tax levy, which is called double taxation. Based on this, with a largeenterprise as an example, the higher its value of fixed assets, to the payment of taxes, the more because of the wear and depreciation is not deducted, in the process of production is also repeat pay; This part of income is almost equivalent to the gross national product, so called the production-oriented V AT, it includes the rent, wages, profits, interest and depreciation of fixed assets, etc.2.2 Consumption-type V ATIn a word, it is not including the current depreciation of fixed assets and net income tax, including the taxpayers' wages, profits, interest, and rent, etc., in terms of a country, relative to the production-oriented V AT is gross national product, net national product. It is deducted for the production of all the value of fixed assets and depreciation forehead, purchased raw materials and labor value of net income, after is the income of the enterprise production and sales, including spending part, such as wages, so called income-producing V AT.2.2 Income-type V ATDue to the use of standard, advanced, has a legal basis, is engaged in the tax accounting practical operation is simple, popular among countries in the world. A category is a one-off deducted for production and operation of the fixed assets value and the value of the purchase raw materials in the tax, that is to say, the taxpayer’s tax products for production and operation, and are not all the outsourcing material to this category. Fixed assets has been imposed production V AT, of course, but the operator is used as a purchase of fixed assets, its tax gold when the purchase has been deducted, relatively, this part of the goods as fixed assets, there would be no tax, as the nature of the V AT collection does not include other production of raw materials, only including the management of all sales of consumer goods. Consumer is a use of special V AT invoices for V AT tax withholding of taxes, occupies a certain advantage, due to its treatment scope strictly enforced, standard, has certain advancement, and are applicable in many countries.3 The characteristics of added-value tax3.1 Wide taxEnterprise engaged in the work of production and sales for the main V ATcollection objects, individuals engaged in business also in the collection and processing, such as small restaurants, small articles of daily use operators, etc., are widely applicable to all kinds of ownership enterprises and individuals, embodies the fairness of the tax system.3.2 Indirect taxV AT calculation is not directly to value multiplied by the applicable tax rate to calculate the tax payable, but by buried output tax and tax balance to determine the tax payable. Although V AT is the value-added tax on appreciation forehead that increases the value or goods, but in the actual execution process, due to the added value of goods or services or goods value is a difficult to calculate the data, so the V AT only by way of indirect tax. Indirect tax measures increased the difficulty of the value-added tax calculation and collection management.3.3 Additional taxGoods have to be sold by pricing, V AT tax refers to the outside valence is not including commodity tax on the original price. When selling goods, should will receive all the money was divided into excluding V AT price sales and value added tax, and on the special V AT invoices to the tomb-sweeping day, respectively, in this way, the V AT on revenues, costs and profits will not occur, also need not collect V AT included in the income statement. Although it is important to note that the V AT is outside valence tax, but the sales direction while receiving payment from buyers tend to be merged charge, through a certain calculation formula of a sales tax were decomposed into will not sales tax and value-added tax, and fill in the V AT special invoice respectively, rather than in the place where has to determine the price of the total sales of value-added tax calculated separately again.3.4 Special invoiceV AT is absolute and levy, in order to avoid only partially and the phenomenon of double taxation, must carry on the effective control of each link, implement V AT is unified, special invoices, and according to the stated on the invoice amount to impose a tax deduction method, this is the main method for effective control. Countries introduced related management way, strengthen the management of the specialinvoice, the rules on the scope of the use of special V AT invoices, the invoice issued the purpose to make clear a regulation, also completed, enterprises have an obligation to give the buyer special invoices for value-added tax, and to do specialized tickets, taxable services shall be paid not, except duty-free goods also. All invoices shall be protected by law. Special invoices for specific use measures enterprises in strict accordance with the provisions of the calculation, on the basis of the in and out of balance of the current period by the enterprise, both reasonable and legitimate, is the duty of the taxpayer. Thus, to strengthen the taxpayer over the use of special V AT invoices highlighted the value-added tax levy management effect.4 The V AT tax planningV AT tax planning is the content of the enterprise according to their own economic activities, on the premise of not illegal, V AT tax matters to the enterprise to seek planning V AT tax minimization of planning and arrangement. It has the following features:4.1The result of V AT tax planningCity building duty and educational expenses to add belongs to attach tax, as the value-added tax falls. But at the same time, if the two tax drops, can lead to enterprise's total profits, so the enterprise income tax will rise. So, the result of the tax planning may be related to some deviation from the ultimate goal of enterprises to reduce tax burden.4.2 V AT special invoices for value-added tax planningInvoice buckle tax law is a common way to calculate the V AT payable taxes, so special invoices for value-added tax management is the key content of value added tax management. Enterprise product sales directly affected by the special invoices for value-added tax, can open will promote the further development of the enterprise; on the other hand, will affect the size of the enterprise. So, V AT tax planning is the need of the development of the enterprise, therefore in the process of V AT tax planning, to consider the problem of special V AT invoices to the enterprise development prospects.4.3 The planning of the tax burden onKnown to value added tax is a turnover tax, also proves that it is the identity ofthe indirect tax, from the nature of the object defined, flow from it this is the flow of goods, the circulation tax included in commodity prices, determines the turnover does not open automatically. And tax excluded in price, taxes are independent in accounting book, looks like has nothing to do with the price, but it is also part of the purchase price, income tax is directly understand hang, V AT tax on hidden is indirectly. Because of V AT qualitative, its scope covers almost all walks of life, can say all the goods in the column, but for taxpayers, because taxes will rise in price is not reasonable publicly, will be opposed by the consumers. So, the taxpayer can only secretly push up commodity prices, will tax include in the price, do not attract the attention of consumers, easy will be passed on to the purchaser, tax and consumers don't know, so don't oppose.文献出处:Phillips J D. The research of corporate V AT planning [J]. The Accounting Review, 2016, 1(3): 40-52.译文企业增值税纳税筹划研究Phillips J D摘要企业进行纳税筹划是非常有必要性的。

关于土地增值税近五年的参考文献最新

关于土地增值税近五年的参考文献最新一、纳税筹划的概述与现状1.1纳税筹划的概念西方国家被视为“智慧者的文明行为”的纳税筹划,在我国过去较长时期被人们视为神秘地带和禁区。

直到1994年,我国第一部由中国国际税收研究会副会长、福州市税务学会会长唐腾祥与唐向撰写,题为《税收筹划》的专著由中国财经出版社出版,才揭开了纳税筹划的神秘面纱。

随着我国经济对外开放程度的提高以及纳税人理财意识的提高,越来越多的纳税人已经开始精心研究税收法规和企业财务管理知识,以合法的方式达到减轻税负、提高经济效益的目的,纳税筹划也因此成为人们关注的热门话题。

印度税务专家NJY.雅萨斯威在《个人投资和纳税筹划》一书中说,纳税筹划是“纳税人通过财务活动的安排,以充分利用税收法规所提供的包括减免在内的一切优惠,从而获得最大的税收利益”。

天津财经大学盖地教授在《税务筹划》一书中认为,税务筹划有狭义和广义之分。

归结到一起可总结为“税务筹划是纳税人依据所涉及的税境,在遵守税法、尊重税法的前提下,以规避涉税风险,控制或减轻税负,有利于实现企业财务目标的谋划、对策和安排”。

张中秀在其主编的《公司避税节税转嫁筹划》一书中从“税收筹划”所包含的方法上给出定义。

他指出:“税收筹划是指纳税人通过非违法的避税方法和合理的节税方法以及税负转嫁方法达到尽可能减小纳税的行为”。

可以用公式表示为:纳税筹划=避税筹划+节税筹划+转嫁筹划。

江西财经大学王兆高教授在《税收筹划》一书中写道:“税收筹划是纳税人在不违反现行税法的前提下,再对税法进行精细比较后,对纳税支出最小化和资本收益最大化综合方案的纳税优化选择,它是设计法律、财务、经营、组织、交易等方面的综合经济行为”。

刘玉章在《房地产企业财税操作技巧》一书中说,纳税筹划是“纳税人依据税法规定(含税收法律、法规以及国家有关税收规定),通过对筹资、投资和经营活动实现进度的合理安排达到规避纳税风险、税负相对最小化和经济利益最大化目的的管理活动”。

浅议增值税的改革历程与发展方向

Value Engineering1增值税的改革历程增值税的发展历程可以分为四个阶段:增值税的引入阶段、生产型增值税阶段、消费型增值税阶段和营业税改增值税阶段。

1.1增值税的引入阶段经过调查研究,我国于1980年在柳州市、长沙市、襄樊等城市的的机械设备和农业机2个制造行业试点开征增值税。

经过五年试点的不断扩张,于1984年确定在全国范围内对机器机械、汽车、钢材等12类货物征收增值税。

但此时的增值税征收率级别很多,征税范围不包含所有的商品和全部阶段,只有增值税的记税方式,并无增值税的实质。

1.2生产型增值税阶段生产型增值税,指计算增值税时不允许扣除固定资产价值中所含有的增值税税款。

1994年全面改革流转税,增值税制度全面引入货物和加工修理修配劳务领域,包括生产加工、维修机电维修劳务和进口货品;取消产品税,统一实行生产型增值税;内外资企业实行简单统一的税率,包括基本税率17%和低税率13%,小规模纳税人适用6%和4%的征收率;实行发票注明税额抵扣制度,用于生产经营的外购原材料、外购燃料、外购动力等物质资料的进项税可以从销项税中扣除。

1.3消费型增值税阶段消费型增值税,指在计算增值税时允许一次性扣除固定资产价值中所含有的增值税税款。

2003年,我国开始对增值税进行改革,在原有的增值税进项税可抵扣项目中,增加了外购除不动产之外的其他固定资产进项税额可抵扣的规定。

但是由于外购不动产和接受外部劳务的进项税额仍然不可抵扣,此时的增值税并不是完全意义上的消费型增值税,只能算是“准消费型增值税”。

2004年,我国正式开始推行由生产型增值税向消费型增值税的转型发展试点。

首先在东北三省的黑龙江省、山东省和大连推行扩张增值税抵税范畴的试点,并于2009———————————————————————基金项目:2018年度广东省普通高校青年创新人才类项目(人文社科):营改增后粤港澳大湾区创新创业税制保障研究(2018WQNCX264)。

增值税的国际比较与借鉴

增值税的国际比较与借鉴在当今全球化的背景下,各国之间的税制也越来越互相影响与借鉴。

其中,增值税作为一种普遍存在的税种,在各国之间也发生了一些相似和差异的变化。

本文将就增值税的国际比较与借鉴展开探讨。

一、增值税的定义与机制增值税是一种按货物或服务的增值额来征税的税种。

它存在于很多国家,包括中国、德国、法国等。

增值税的征收机制可以简单概括为“货物和服务产生的增值,纳税人按一定比例缴纳税款”。

增值税的机制确保了税负的分摊,有效地减少了按传统办法征收的直接税或间接税的种种不便。

二、国际增值税的比较1. 税率比较不同国家之间的增值税税率存在相当大的差异。

以欧洲国家为例,法国和德国的增值税税率较高,分别为20%和19%;而意大利和西班牙的增值税税率相对较低,分别为10%和12%。

此外,某些国家还对特定商品或服务设置不同的税率,如德国对食品征收7%的税率。

2. 税务政策比较不同国家对增值税的税务政策也有所不同。

例如,英国实行了增值税零税率制度,即对某些特定商品或服务征收0%的税率,如食品和儿童读物;而中国的增值税制度中则包含了多种税率和不同的税率减免政策。

3. 退税政策比较某些国家还在增值税制度中设立了退税政策,以吸引外国投资和旅游消费。

例如,法国和意大利允许非欧盟旅客在离境时退还部分增值税;而中国也在一些地区设立了退税机制,鼓励出境消费。

三、国际增值税的借鉴国家之间在增值税制度上的差异,提供了借鉴与学习的机会。

各国可以从其他国家的经验中吸取有益的经验,优化和改进自己的增值税制度。

1. 税收政策借鉴国家可以通过比较不同国家的增值税税率和税收政策,优化自己的税收体系。

可以借鉴其他国家的税率设定,合理分配税负,保证税收的公平性和效率性。

2. 退税政策借鉴考虑到全球旅游业的快速发展,国家可以借鉴一些旅游业发达的国家的退税制度,吸引外国游客在本国消费。

通过退还部分增值税,可以鼓励更多的外国游客在本国进行消费,促进旅游业的发展,增加国家的财政收入。

国外增值税理论研究及案例分析

国外增值税理论研究及案例分析摘要:增值税是目前全球流行的重要税种,随着经济全球化的历程,各国增值税体系也在动态调整和改进。

学者对增值税存在一些争议。

本文对国外增值税进行了理论研究,同时分析了各国增值税的发展情况,为我国在增值税领域提供一些参考模型,为我国税务改革提供经验借鉴。

关键词:增值税;理论研究;案例分析前言1918 年德国实业家Dr. Wilhelm von Siemens 提出一种代替营业税的税制设想,也即最初的增值税的概念1954 年4 月,法国税务机关成功的实现营业税到增值税的改革,最初是针对大企业,后续扩展至工业、农业、商业、服务业等行业。

截至2013 年,已有160 多个国家和地区实行增值税。

增值税也有其固有的弊端,本文对增值税进行了系统的理论研究,并分析了各国增值税实施的细节和差异,意图为我国的税制改革提供借鉴和参考。

一增值税理论研究1.与营业税比较增值税(Value Added Tax) 是基于商品或服务的增值而征税的一种间接税,也是消费税(Consumption Tax)的一种表现形式,在很多国家(例如澳大利亚、加拿大等)被称为商品及服务税(Goods and Services Tax)。

毫无疑问,增值税的目的就是产生税收收入。

它和销售税的共同点在于,最终只有消费者付出了费用;不同之处在于,销售税在产品最终销售给消费者的环节上才征税,只收集汇总一次,而增值税在每个供应链采购产品业务的时候都会发生,每一个商业环节的增值部分都需要征税。

增值税与营业税相比,主要缺点在于,在供应链中每个环节都进行征税,因此需要额外的会计手段,这使得增值税的征收变得复杂。

目前新西兰对一些产业进行了税收豁免,例如物业出租、捐款、贵金属和金融服务等,简化了增值税征收的体系。

2.增值税征收根据征收的方法进行区分,增值税有两种计税方法:发票法(Invoice-Based)和账簿法(Accounts-Based)。

中国增值税与国外在增值税的对比,以及对中国的建议。

税收基础知识结课论文题目:中外增值税制度比较分析系部(院):工商系专业:10工商学号:***********名:**摘要:增值税做为本世纪流转税体系中的一个新的税种,由于其具有有效消除重叠征税、保持税收中性、收入稳定等特点,愈来愈为世界各国所推崇。

增值税从产生至今,目前已有100多个国家将其作为本国的主要税种。

2010年12月,增值税改革进入立法程序。

这意味着历经26年的生产型增值税即将退出历史舞台,主宰税收重心的,将是更为完善,对经济的贡献必将发挥更大作用的消费型增值税。

转型之后,我国新的消费型增值税具有重大积极意义,但其本身蕴含的巨大优越性将充分释放。

本文介绍了法国、英国、德国、韩国等国家关于增值税制度中的相关规定,从比较借鉴的角度,分析优缺点,提出了完善我国增值税制度的建议。

关键词:增值税;改革;消费性增值税;比较;完善;目录:一、增值税在中国1.我国经济现状2. 我国消费型增值税改革的意义二、增值税在国外1.增值税在法国1.1 法国增值税制度的形成1.2 增值税中应税交易的规定1.3 税基规定和税率设计1.4 增值税进项扣除和扣除调整1.5 特税增值税纳税人的规定1.6 出口退税2.增值税在德国2.1 主要特征2.2 征税对象2.3 免税范围2.4 税基2.5 税率2.6 预付税抵扣2.7 征税程序三、完善我国增值税制度的建议1.进一步扩大扣税范围2.扩大增值税的征税范围3.进一步缩小增值税减免税优惠范围4.加强增值税的管理一、增值税在中国1.我国经济现状当前,全球的经济处于金融危机过后的“后危机时代”,经济复速度放缓。

我国的经济也不例外。

国内宏观经济进入调整周期、经济转型压力凸现、国际金融市场剧烈动荡,国内外各种因素的叠加使得国内的出口和投资都面临着严峻挑战,国民经济增长速度的放缓使得经济下滑的危险加大,微观经济体经营状况令人担忧。

同时,我国“十二五”规划出台。

在这种情况下,政府继续出台了一系列政策,目标是稳定经济增长。

国内外增值税比较研究典型国家或地区增值税

参考内容

内容摘要

在全球化的背景下,增值税(VAT)已成为各国财政收入的重要来源之一。然 而,尽管增值税在许多国家得到广泛实施,但其在不同国家的具体实施方式仍存 在差异。本次演示将对国外增值税与国内增值税进行比较,以探讨它们之间的异 同。

一、定义和征税范围

1、国外增值税

1、国外增值税

在国外,增值税通常被定义为一种消费税,对商品和服务的最终消费者征收。 在欧盟范围内,增值税是对商品和服务的生产、流通、消费等各个环节征收的间 接税。其征税范围广泛,包括商品、劳务、进口等。

2、国内增值税

2、国内增值税

国内增值税制度的实施也对经济发展产生了一定的影响。首先,增值税的征 收保证了财政收入的稳定增长。其次,增值税的征税范围广泛,有利于促进商品 流通和经济发展。此外,国内增值税的税收优惠政策有利于促进特定产业的发展。 同时,国内增值税的抵扣制度有利于降低企业税负,促进企业技术进步和转型升 级。

三、国内外增值税的比较研究

1、税率结构:各国增值税的税率结构不尽相同。一些国家的税率相对较高, 如法国、意大利等;而另一些国家的税率则相对较低,如英国、加拿大等。此外, 有些国家的税率结构较为简单,而有些国家则根据商品和服务的不同类型设置了 不同的税率。

三、国内外增值税的比较研究

2、征管方式:各国在增值税的征管方式上也存在差异。一些国家的税务机关 负责征收和管理增值税,而另一些国家则将这部分职责外包给第三方机构。此外, 一些国家采用了电子发票和数字化征管手内增值税

国内增值税的税率根据行业和地区不同而有所差异。一般来说,税率分为一 般税率和低税率两种形式。此外,国内增值税也有一些税收优惠政策,如对农产 品、节能环保等产业的税收优惠。

三、征管和抵扣制度

浅析增值税的起源与发展

浅析增值税的起源与发展增值税是一种按照货物或劳务增值额计征的一种税收制度。

它最早起源于欧洲,自20世纪50年代以来得到广泛的应用和发展。

增值税的起源与发展,是一个与国家经济形势、社会状况、税收体制有着密切联系的过程。

本文将从增值税的起源、发展历程、对经济发展的影响等方面进行浅析。

一、增值税的起源增值税的起源可以追溯到19世纪末的法国。

1872年,法国实行了货物交易税,这是增值税的鼻祖。

这种税制存在很多弊病,无论是逃税现象还是遇到经济危机时税收收入锐减的情况。

为了解决这些问题,法国于1954年开始实行一种新的税收制度——货物和服务税。

这种税制标志着现代增值税的诞生。

并于1967年在法国全面实施了增值税。

此后,增值税迅速在欧洲得到了推广和发展。

德国、意大利、英国等国家也相继引入了这种新型税制。

在不久后,增值税的应用就遍及了欧洲大部分国家。

其后,增值税成为一种全球性的税收政策。

二、增值税的发展历程1. 制度的完善从20世纪50年代到20世纪70年代,欧洲各国先后开始实行增值税,这一时期主要是在探索阶段。

在20世纪80年代以后,随着全球经济的全面开放和国际经济一体化进程的加速,国际间的资源流动性大大增强,增值税的制度逐渐完善。

制度完善主要体现在税率的不断调整、纳税人多元化和征收方式的创新等方面。

2. 税率的调整3. 税收政策的创新随着经济全球化的深入和技术的不断进步,很多国家开始在增值税政策上进行创新。

他们在增值税的征收方式上引入了新的科技,例如电子票据、电子支付等。

进一步优化了税收征管的效率,提高了税收的合规性。

这些创新的举措也显示了各国政府对于增值税制度的重视和发展。

1. 减负促发展2. 促进资源的合理配置增值税的征收方式是在商品销售环节逐级征收,这意味着只有在商品最终销售时,才真正向消费者收取增值税。

这种征收方式可以促进资源的合理配置,提高资源利用效率。

并且可以避免了生产者和消费者之间直接税负担过重的问题,有利于优化资源配置。

浅析增值税的起源与发展

浅析增值税的起源与发展增值税是一种对商品和服务按一定金额的增值额征收税费的一种税收制度。

它起源于20世纪中叶的欧洲,随后在世界范围内得到了广泛的应用和发展。

本文将从增值税的起源、增值税的基本原理、增值税的发展等方面进行浅析,以便更好地理解增值税及其在全球税收体系中的地位与作用。

一、增值税的起源增值税的起源可以追溯到法国。

1954年,法国政府推出了世界上第一项增值税制度,以应对当时国家财政困难的局面。

增值税以其简单、透明、高效的特点,很快在法国获得了成功,其他欧洲国家也纷纷效仿。

随着时间的推移,增值税逐渐成为一种全球性的税收模式。

二、增值税的基本原理增值税主要通过在商品或服务的每个环节中征收税费的方式来实现。

具体来说,企业在销售产品时,需要向国家税务机关缴纳销售额一定比例的税款。

而企业在购买原材料或其他产品时,也可以从税务机关领取相应比例的税款退还。

这种退税制度有效保障了企业的生产经营活动,同时也能够确保国家税收的公平和稳定。

三、增值税的发展随着全球经济的不断发展,增值税制度也不断完善和发展。

在增值税的起源国法国,增值税税率由原来的10%提高到目前的20%。

其他国家也纷纷调整增值税税率,并对于特定行业或商品实行差异化税率政策,以达到税收调控的目的。

此外,一些国家还通过增值税制度的改革,加强了税务管理、打击了偷税漏税等不法行为,提高了税收征管的效率和质量。

四、增值税的优势与问题增值税作为一种现代化的税收制度,具有以下几个优势:首先,增值税能够减少税负不对称的情况,确保税收的公平性。

其次,增值税以环节征税的方式,有效避免了税收的重复征收。

再次,增值税制度简化了税务手续和申报程序,提高了企业的经营效率。

然而,增值税制度也存在一些问题,如税率过高可能会对部分企业的经营造成压力,对中小微企业的发展不利。

总之,增值税作为一种重要的税收制度,在全球范围内得到了广泛的应用和发展。

它简化了税收的征管程序,提高了税收的公平性和效率,为国家财政提供了可靠的经济支持。

增值税研究国外文献综述

[5 N u a , 6 ] 6 , em r 1 3 。而且 , k 9 实践证明增值税就是一 种在适 当 的时 候 出现 的 恰 当 的税 种 。更 高 的 收 入 需 求 、 大 的政府支 出计 划 和计 算 机 会 计 有 助 于增 值 税 扩 的推广 [0 D Gaf16 ] 3 , e ra,98 ④。在 民 主 国家 , 值 税 是 增 种好 的 和平 税 , 而不是 好 的战争税 。 16 95年 , 只有法 国推行 了增值税 [7 N n,96 ⑥, 6 , o" 6 3 1 芬兰和美 国的密歇根州 采用的是改 良的形式 。如今 , 增 值税 已经成为世界上最 受欢迎 的税种 之一 。

k ̄的一 篇经典 论 文 中 为增 值 税 构筑 了全 面 的哲 学伦 i 理基 础 , 照税 收公平 的受 益原则 , 值税 就是 “ 按 增 服务 成本 ” 变量 。 增 值税 的蓬 勃发展 归功 于增值 税拥 有 一个全 新 的 名称 , 这使 得欧盟 在 为其 成 员 国 寻求 一 个 具 有 相对 一

口,湖南 长沙 4 0 1 ) 11 6

[ 摘

要 ] 关于增值 税的基 本理论 问题 , 累退性 、 如 增值税对 国际 贸易、 济增 长、 经 价格等方面的影响 , 需要 全

方位 的 多 角度 审视 ; 增值 税 制度 改 革 与 完善 的 过程 中 , 共 部 门 、 业 、 融 、 房 服 务 等部 门的 增 值 税 制 度 设 计 在 公 农 金 住

增值 税起 源于 德 国和 美 国 , 一次 世 界 大 战后 不 第

的研 究 。增值 税在 生 产 和 销售 的 各个 阶段征 收 , 与所

久 , 值 税 的 基 本 原 理 在 这 两 个 国 家 就 已 经 开 始 萌 增 芽①。2 O世纪 5 O年代 , 欧和美 国掀起 了研究 增 值税 西

增值税发明

增值税发明

增值税的概念最早是由美国耶鲁大学教授亚当斯在1917年提出的。

然而,关于增值税的发明,通常认为是在1954年,由时任法国税务总局局长助理的莫里斯·洛雷(Maurice Lauré)所推动并实施的,他因此被誉为“增值税之父”。

增值税是一种对商品和服务的新增价值或附加值进行征收的税。

在实际的商品生产和流通过程中,对商品新增价值或附加值的准确计算是非常困难的,因此,增值税的征收通常是通过税款抵扣的办法来实施的。

这种方法可以避免在商品的生产和流通过程中的重复征税问题,因此被许多国家广泛采用。

自法国在1954年实施增值税以来,该税种因其独特的优越性而逐渐被全球大多数国家所接受。

至今,全世界已有大约170多个国家实行了增值税制度。

然而,值得注意的是,尽管美国学者最早提出了增值税的概念,但美国并没有实施增值税制度,而是坚持并完善了以所得税为主要税种的税收制度。

这可能是由于美国的金融结算体系相对完善,所得税管理具有更大的优越性,或者更彻底地体现了增值的理念。

总的来说,增值税的发明和实施对于全球税收制度的发展产生了深远的影响。

浅析增值税的起源与发展

浅析增值税的起源与发展增值税是一种按照商品、服务增值额定额分期征收的一种税收制度,是一种国际通行的税制。

增值税的起源可以追溯到20世纪30年代,当时法国政府首次引入了增值税,成为第一个采用增值税的国家。

随后,增值税在欧洲迅速传播开来,成为世界各国广泛采用的税收制度。

本文将从增值税的起源和发展,以及其在全球范围内的运用情况进行浅析。

增值税的起源可以追溯到20世纪30年代的法国。

当时,法国经济面临严重的财政危机,政府急需找到一种新的税收制度来填补财政赤字。

于是,法国政府在1930年代初期开始研究和试行增值税。

在第二次世界大战之后,法国政府将增值税正式列入税收制度,并在1954年正式实施增值税。

由于法国的增值税制度取得了成功,很快得到了其他欧洲国家的关注和模仿。

随后,欧洲其他国家相继引入了增值税,逐渐成为世界各国广泛采用的税收制度。

增值税的发展经历了几个阶段。

在起步阶段,增值税主要是被欧洲国家所采用,并在1968年正式在欧洲经济共同体推行。

随着全球化进程的不断深入,增值税的使用范围不断扩大,逐渐成为一种国际通行的税收制度。

目前,绝大多数国家都采用了增值税,世界上只有少数国家没有采用这种税收制度。

随着社会经济的不断发展和税收制度的不断完善,增值税的税率和征收方式也在不断调整和优化,以适应不同国家的税收政策和经济情况。

增值税在全球范围内的应用情况也是多种多样的。

根据国际货币基金组织的数据显示, 截至目前为止,全球已有160多个国家和地区采用了增值税制度。

而增值税在不同国家的征收率也是各不相同,例如欧洲国家的增值税一般在20%左右,而一些发展中国家的增值税税率则相对较低。

增值税的征收方式也各有不同,在一些国家,增值税是在商品和服务的每一个环节都进行征收,而在一些国家则采取了简化的征收方式。

增值税在全球范围内的应用是非常灵活多样的,各国根据自身的税收政策和经济情况来制定相应的增值税政策。

在总体上来说,增值税是一种现代化的税收制度,它与传统的销售税相比,可以更加准确地实现税负分担的社会公平原则,有利于调动社会经济主体的积极性。

增值税国内外现状

增值税国内外现状增值税是一种按照商品和服务的增值额来计征税款的税种,被广泛应用于各个国家的税收制度中。

本文将对增值税在国内外的现状进行分析,并对其对国家经济的影响进行探讨。

一、国内增值税的现状我国增值税于1994年开始实行,经过多年的发展,已成为我国最主要的税种之一。

目前,我国增值税主要实行的税率分为三档,即17%、11%和6%,涵盖了绝大部分商品和服务。

这个税率体系旨在促进经济发展、调节消费结构和优化资源配置。

增值税的征收实行了增值税普通税率、减按计税和小规模纳税人等制度,使纳税人便于申报纳税,并为进一步减轻纳税人负担提供了便利。

此外,我国还采取了一系列增值税优惠政策,如高技术企业减按计税,对农产品生产企业减按一定比例计税等,以促进相关产业的发展。

二、国外增值税的现状在国外,增值税也普遍存在于各个国家的税收体系中。

不同国家对于增值税的具体税率和征收方式存在一定的差异。

如欧盟国家的增值税税率一般较高,达到20%以上,而美国则采用了营业税和销售税来代替增值税。

增值税在国外的运用也可以体现出不同国家的税收政策和经济发展模式。

部分国家将增值税的税率分为多个档次,根据不同商品和服务的属性进行分类征收。

此外,一些国家也采取类似我国的减按计税和小规模纳税人制度,以提高纳税人的便利性。

三、增值税的影响增值税作为一种间接税,在国家的经济运行中发挥着重要的作用。

以下是增值税对国家经济的主要影响:1. 提供国家财政收入。

增值税是国家重要的税收来源之一,通过增值税的征收,国家可以获取一定的财政收入,用于公共事业建设和社会福利保障。

2. 调节消费结构。

由于增值税按照商品和服务的增值额计算,对高端商品征收的税额会较高,从而提高了这类商品的售价,促使消费者减少对其的需求,从而达到了调节消费结构的目的。

3. 优化资源配置。

通过增值税的征收,可以提高商品和服务的成本,降低低效资源的利用率,从而使资源得到更为合理的配置,促进经济的可持续发展。

营业税改征增值税中英文对照外文翻译文献

营业税改征增值税中英文对照外文翻译文献(文档含英文原文和中文翻译)营业税改征增值税试点方案的进一步扩围2012年7月25日国务院总理温家宝主持召开国务院常务会议正式决定,自2012年8月1日起至年底,将自2012年1月1日起已在上海进行的交通运输业和部分现代服务业营业税改征增值税试点方案("试点方案")范围,分批扩大至其他10个省市:北京、天津、江苏、浙江、安徽、福建、湖北、广东、厦门和深圳("10个新试点地区")。

不仅如此,会议还决定,明年继续扩大试点地区,并选择部分行业作全国试点。

在本期《中国税务/商务新知》中,我们将分析试点方案进一步扩围至10个新试点地区后带来的潜在影响,并分享我们的观察。

普华永道观察根据公开统计信息,2012年上半年10个新试点地区的生产地区的生产总值超过50%。

地理上,这10个新试点地区各广布在中国北部、中部、东部和南部地区。

因此,试点方案的进一步扩围无疑会对中国下半年的宏观经济发展产生很大影响。

总体而言,10个新试点地区的试点方案应与上海的试点方案一直。

自2012年1月1日上海开展试点方案以来,财政部和国家税务总局出台了一系列关于试点方案的政策和实施细则。

理论上来说,除非将来有专门针对10个新地区的不同政策出台,这些已出台的政策文件应该适用于所有试点地区。

在10个新试点地区开展试点方案可能要面临更为复杂的问题。

与上海国税合一的情形不同,这些地区的国税局和地税局各自管理,分别负责增值税和营业税的征管。

这样可能出现各方对试点服务范围有不同的理解,尤其是对那些未在现有规定中有清楚定义的试点服务。

这可能对这些新试点地区的纳税人带来更大的挑战,特别是在营业税改增值税的过渡时期。

同时,我们也期待上海试点中遇到的实际问题能够进一步予以明确。

例如,进一步明确某些在现行办法和法规中没有明确定义的试点服务的范围,特别是认定某项咨询服务是否属于试点服务的范围,从而向境外方提供上述咨询服务时能够享受免增值税的处理;如何具体实施对符合条件的试点企业出口实行免抵退税方法等问题以及如何将这10个新试点地区的基础实际操作与上海保持一致。

税收筹划国内外文献综述

税收筹划国内外文献综述税收筹划是对税收政策进行科学合理应用和操作的一种有效手段。

随着全球经济的不断发展,税收筹划的重要性日益凸显。

本文将综述国内外相关文献,旨在为税务从业人员提供指导,进一步完善税收筹划措施。

国内文献综述从国内文献来看,税收筹划已经成为一种必备的企业经营管理手段。

肖立平等人在《税收筹划与风险管理》中指出,税收筹划是企业实现规模化、多元化、国际化的重要手段,能够有效降低企业税负,提高企业盈利能力,同时也有助于降低企业面临的各种风险。

昆明理工大学的王红红、何瑛等在《企业税收筹划情况研究》中发现,绝大部分企业把税收筹划的重点放在了收入的筹划上,而忽略了支出的筹划,这种策略不仅会导致企业成本变高,还有可能存在税收风险。

因此,企业在进行税收筹划时需要全面考虑,注重平衡收入与支出,实现最大程度的税收优惠。

此外,国内学者还对税收筹划存在的几个关键问题进行了研究。

例如,如何处理跨国企业的税收筹划问题?中国向别国转移价格的计算方法怎么制定?如何应对税务机构的税收调查?对此,包括河南财经政法大学的尤艳、杨雪在内的学者都进行了深入探讨,并提出了对应的策略建议。

国外文献综述与国内相比,国外学者在税收筹划方面的研究更具广度和深度。

例如,美国著名财经学家Avery E. Neumark在《税收筹划手册》中系统介绍了各种税收筹划的方法和技巧,并详细解释了每种方法的优缺点和使用范围。

同时,他也提醒企业在进行税收筹划时需要尽可能降低各种风险,避免违反税法规定。

欧洲也是一个税收筹划的重要研究领域。

瑞典乌普萨拉大学的Daniel C. Johansson等人在《全球税收筹划》中,深入分析了全球跨国企业的税收筹划情况,并提出了构建新的全球税收体系的可能性。

他们认为,全球税收体系需要更加公平、合理地分配全球企业的税收负担,同时也需要各国政府之间加强合作与沟通。

总结本文综述了国内外相关税收筹划研究文献,可以看出,税收筹划已经成为全球企业管理中不可或缺的一部分。

《税收服务问题研究国内外文献综述》3000字

税收服务问题研究国内外文献综述目录税收服务问题研究国内外文献综述 (1)1 国外研究现状 (1)2 国内研究现状 (2)3 文献总评 (3)参考文献 (3)1 国外研究现状税收服务的基本理论是,国外对税收制度的理论研究要比中国快得多。

17世纪中叶,英国古典统计学家威廉·佩蒂(税制)在其《税收》一书中提出,税收应遵循税收公平、税收类型决策、税收便利决策和税收成本最小化四项原则。

后两项原则需要降低行政成本,以提高税收质量和效率。

1986年,英国政府宣布了《纳税人权利宪章》。

20世纪80年代,新公共管理理论成为政府改革的一种思潮。

其核心思想是将市场机制引入公共管理,强调政府、社会和市场的关系,弱化政府职能,鼓励公共管理社会化。

美国登哈特夫妇(2010)也对新公共管理理论有了进一步的理解。

政府不能站在公民的对立面。

想要管理公民,作为服务提供者,他们需要及时了解公民的需求。

在优化纳税服务方面,美国Devriesetal(2013)对政府工作绩效评价方面研究了税务机关和纳税人的关系,他认为做好纳税服务工作,必须要加强纳税服务体系的建设,税务部门要想得到纳税的认可,必须加强服务,满足纳税人实际需求。

Nabila Nisha(2016)在研究过程中强调,电子政务快速发展的同时,发达国家已经建立起独立的电子税务局,对部分较为落后的地区来说,体系还不够完善,尤其是孟加拉国之类的发展中国家。

在她看来,电子化申报的便利方式更能够满足纳税人的基本要求。

越来越多纳税人希望能够通过互联网的便捷渠道来解决税务申报过程中出现的各种问题。

通过研究相关的因素,该学者发现网络安全需求和创新绩效等各个部分都能够影响到税务具体建设情况,也是影响纳税人满意度的重要因素。

他的研究还指出,电子政务服务的具体落实必须要建立在前期分析的基础之上,只有这样才能够提供更好的规划和实施意见。

Hall,Joshua C(2018)提到美国有着丰富的地方政府税收历史和良好的规定。

14339952_国外增值税与国内增值税的比较

L i a o n i n gE c o n o my国外增值税与国内增值税的比较〔内容提要〕本文通过对部分欧洲国家、亚洲国家增值税的简要介绍,比较分析我国的增值税制度,从中借鉴经验,以期完善我国的增值税制度。

〔关键词〕增值税流转税税率!姜昕刘彦廷增值税是指以商品生产、流通和提供劳务的各个环节的增值额作为课税对象的一种流转税。

自"#$%年提出这个概念以来,现已有"&&多个国家和地区陆续开始征收这项税款。

“道道征税,税不重征”是增值税最显著的特征,这体现了税收公平的特质,因而能够提升纳税人的纳税积极性,促进社会经济的发展。

一、欧洲国家的增值税制度"'法国的增值税制度。

增值税最早于"#$%年产生于法国。

起初,法国征收增值税的范围只包括工业生产与商品批发这两个部分,到(&世纪)&年代中期,法国将农业、商品零售业纳入到收取增值税的范畴,在("世纪的今天,法国境内的有偿活动都要缴纳增值税。

法国对于增值税采取多档税率的纳税方案:标准税率"#')*,低税率$'$*和('"*以及零税率。

低税率$'$*主要针对日常生活中所需要的食物、饮品、客运、书籍等;低税率('"*主要针对报刊、药物、音乐演出等。

法国对外出口的货物或进口后用于出口的货物以及对外的劳务输出不需要缴纳税款。

这类商品所需进行的各个环节都免除增值税,同时本环节不需要缴纳增值税。

可免除税款的项目有:部分农产品、某些特定商品的交易、有价证券的交易、报纸杂志类、保险类的交易等。

('英国的增值税制度。

(&世纪+&年代初,英国就制定了增值税征收的制度法案,随后开始征收增值税。

"#,-年英国制定了《增值税法》,确保了增值税的合法征收。

增值税纳税人是涉及货品交易和劳务交易的企业负责人。

国外关于软件产品增值税政策

国外关于软件产品增值税政策1. 介绍软件产品增值税政策是指国外针对软件产品销售和服务提供的增值税相关规定。

随着信息技术的发展,软件产业在全球范围内得到了迅猛发展,各国纷纷制定相关政策来规范和管理软件产品的销售和服务。

本文将重点介绍一些主要国家(美国、欧洲、日本)在软件产品增值税方面的政策,并对其进行比较分析。

2. 美国的软件产品增值税政策美国目前没有统一的联邦级别的增值税制度,但各州可以自行决定是否征收销售和使用税。

对于软件产品,根据美国国内收入法典第26章第61节中所定义的“智力财产权”(Intellectual Property),以及“数字商品”(Digital Goods)和“数字服务”(Digital Services)等概念,可以确定其应纳税种类和税率。

具体来说,如果软件产品被视为实体商品,则根据当地州的销售和使用税法规征收相应税款。

例如,在纽约州购买实体媒体上的软件盒子时,可能需要支付8.875%的销售税。

而如果软件产品被视为数字商品或数字服务,则根据各州的数字商品和服务税法规征收相应税款。

例如,在佛罗里达州购买在线订阅的软件服务时,可能需要支付6%的数字服务税。

需要注意的是,美国各州对软件产品增值税政策的具体规定可能有所不同,因此在销售和购买软件产品时,需要了解当地州的相关法规。

3. 欧洲的软件产品增值税政策欧洲国家在软件产品增值税方面采取了统一的政策,即根据欧盟增值税指令(VAT Directive)来征收增值税。

根据该指令,欧洲国家将软件产品分为两类:有形媒体上提供的软件和通过下载或流媒体方式提供的软件。

对于有形媒体上提供的软件,例如光盘或DVD上的安装程序,征收标准增值税率。

不同欧洲国家的标准增值税率略有差异,例如德国为19%,英国为20%。

对于通过下载或流媒体方式提供的软件,根据购买者所在地区(消费者所属国)来确定适用的增值税率。

这种方式被称为“电子增值税(eVAT)”或“远程销售增值税(RST)”。

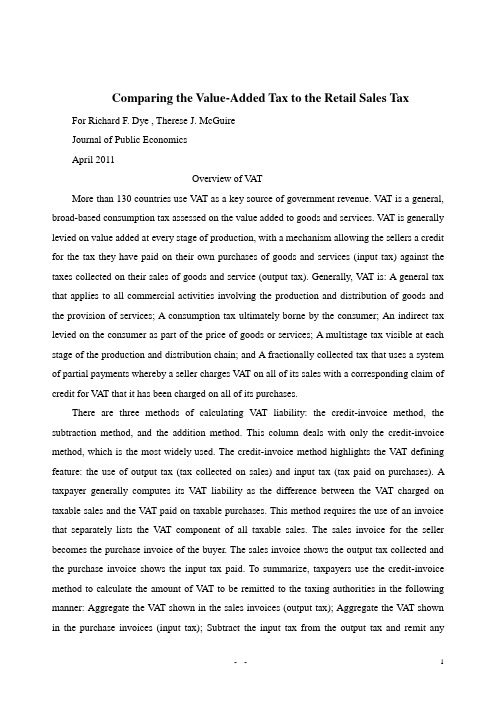

营业税改增值税英文文献

Comparing the Value-Added Tax to the Retail Sales Tax For Richard F. Dye , Therese J. McGuireJournal of Public EconomicsApril 2011Overview of V ATMore than 130 countries use V AT as a key source of government revenue. V AT is a general, broad-based consumption tax assessed on the value added to goods and services. V AT is generally levied on value added at every stage of production, with a mechanism allowing the sellers a credit for the tax they have paid on their own purchases of goods and services (input tax) against the taxes collected on their sales of goods and service (output tax). Generally, V AT is: A general tax that applies to all commercial activities involving the production and distribution of goods and the provision of services; A consumption tax ultimately borne by the consumer; An indirect tax levied on the consumer as part of the price of goods or services; A multistage tax visible at each stage of the production and distribution chain; and A fractionally collected tax that uses a system of partial payments whereby a seller charges V AT on all of its sales with a corresponding claim of credit for V AT that it has been charged on all of its purchases.There are three methods of calculating V AT liability: the credit-invoice method, the subtraction method, and the addition method. This column deals with only the credit-invoice method, which is the most widely used. The credit-invoice method highlights the V AT defining feature: the use of output tax (tax collected on sales) and input tax (tax paid on purchases). A taxpayer generally computes its V AT liability as the difference between the V AT charged on taxable sales and the V AT paid on taxable purchases. This method requires the use of an invoice that separately lists the V AT component of all taxable sales. The sales invoice for the seller becomes the purchase invoice of the buyer. The sales invoice shows the output tax collected and the purchase invoice shows the input tax paid. To summarize, taxpayers use the credit-invoice method to calculate the amount of V AT to be remitted to the taxing authorities in the following manner: Aggregate the V AT shown in the sales invoices (output tax); Aggregate the V AT shown in the purchase invoices (input tax); Subtract the input tax from the output tax and remit anybalance to the government; and In the event the input tax is greater than the output tax. The United States is the only member of the Organization of Economic Cooperation and Development that does not levy a V AT on a national level; however, V AT has become widely recognized as an important option in federal tax reform debates.Indirect taxes such as value added taxes (VAT) generate a substantial part of tax revenue in many countries. In fact, VAT systems generate a quarter of the world’s tax revenue. Nearly 130 countries now have a VAT system (with over 70 countries having adopted the system during the last 10 years) (Keen and Mintz 2004). More focus on internationally mobile tax bases has drawn attention to directing more of the tax burden to indirect taxes such as consumption taxes or VAT systems, and less to income taxes, especially capital income (Gordon and Nielsen 1997). During the harmonization of EU taxes, indirect taxes, and VAT systems received much attention (Fehr et al. 1995). A general VAT law covering all private goods and services characterizes the current EU system, but there are still many exemptions from this general instruction.Such a VAT system also exists in Norway as a consequence of the Norwegian VAT reform in 2001. The reform introduced a general VAT law on services, but many exemptions are still specified.There are several arguments in favor of a general and uniform VAT system, compared with imperfect, nonuniform (and nongeneral) systems.Such a system may improve economicefficiency and reduce administration costs, rent-seeking and fraud activities by industries that lobby for lower rates and zero ratings (Keen and Smith 2006). A general and uniform VAT system equals a uniform consumer tax on all goods and services.Such a system also implies that the producers’ net VAT rate on material inputs equals zero, irrespective of the rate structure. This is optimal according to the production efficiency theorem (Diamond and Mirrlees 1971a,1971b).A VAT system with exemptions violates the production efficiency theorem because taxation of intermediates will differ between industries. On the other hand, industries that are covered by the VAT system but have lower rates or zero ratings on their sales are favored because they can withdraw expenditures to VAT on intermediates at full rates and only levy reduced or zero rates on their sales.A general and uniform VAT system may also have positive effects on the distribution of welfare among households. If the initial situation is characterized by a VAT on most goods but only on a few services, the introduction of a uniform rate on all goods and services may improve the distribution of welfare because servic es’ share of consumption increases with income.Keen (2007) points to the lack of interest in value added taxation from the theoretical second-best literature in spite of the VAT’s popularity in practical tax policy. As mentionedabove, VAT systems are in general not uniform. Theoretical analyses demand relatively simple models and simple tax structures to be analytically tractable.In practical policies, the structures of the economy and the tax systems are quite complex, and there is a need for detailed numerical models in order to analyze the effects of different VAT systems. This paper contributes to the literature by analyzing the welfare effects of an imperfect extension of a nonuniform VAT system, and comparing different imperfect, nonuniform VAT systems with a uniform and generalVAT system within an empirically based dynamic computable general equilibrium (CGE) model for a small open economy. This model mirrors a real economy, Norway, and differs in many respects from the more simple theoretical model s that fulfill the assumptions of normative tax theory and recommend uniform commodity taxes, combined with no input taxation.In our analyses, we ask the following questions. Can the introduction of a nonuniform VAT system including only some services make the economy worse off than having a VAT system only covering goods and in that case, why? Such reforms characterize both the Norwegian VAT reform of 2001 and the EU VAT reform from the late 1990-ties. Will an additional extension to a uniform and general VAT system be welfare superior to the nonuniform (and nongeneral) VAT systems and what are important preconditions? As will be explained below, one cannot on purely theoretical grounds establish the welfare rankings of such VAT systems when there are preexisting distortions as tax wedges and market power in the economy. The baseline VAT system is a nonuniform VAT system mainly covering goods. This baseline VAT system is then compared with (1) the extended nonuniform Norwegian VAT reform of 2001, and (2) a general VAT system characterized by a uniform VAT rate on all goods and services, including public goods and services. The Norwegian VAT reform of 2001 was a step in the direction of a general VAT system by including many services, but there are still many exemptions, zero ratings and lower rates. In particular, the VAT rate on food and nonalcoholic beverages is half the general VAT rate. The policy reforms are made public revenue neutral, and changes in lump sum transfers as well as in the system specific VA T rate are studied. With a revenue-neutral change in the system-specific VAT rate, the VAT systems can be ranked with respect to welfareeffects.Ballard et al. (1987) and Gottfried and Wiegard (1991) analyze the welfare effects of different VAT systems including tax exemptions and zero ratings in static CGE models. The separability and homogeneity assumptions in their consumer demand models favor a uniform VAT system, which is supported in their policy simulations. In contrast, our model is an intertemporal CGE model for a small open economy without strict homogeneity assumptions in consumer demand. Our model is well designed for analyzing VAT reforms because itdistinguishes between many industries, input factors and consumer goods and services. The modeling and parameters in the consumer demand system and the production technology are all the results of comprehensive micro- and macroeconometric analyses of Norwegian data. The model has a detailed description of the Norwegian system of direct and indirect taxes.Specifically, net V AT rates on the input factors and gross V AT rates on the consumer goods and services are included in the model. We disregard the effects on costs of administration,rent-seeking and distribution of welfare among households. The model emphasizes the small open economy characteristics by using given world market prices and interest rates. Imperfect competition is present in the domestic markets. A uniform and general V AT system is not a priori the most efficient in our model.When comparing the two different nonuniform V AT systems, our analysis shows that an imperfect extension of the V AT system to cover more services is welfare inferior to the baseline nonuniform V AT system only covering goods. Obtaining efficiency in production is empirically important for the welfare effects of the different V AT systems. An imperfect extension of the V AT system reduces efficiency in production because intermediates will be taxed differently for different industries. Consumer efficiency is also reduced due to lower V AT on inelastic goods and higher V AT on elastic services. Introducing a general and uniform V AT system is not obviously welfare superior in a distorted economy, but we find that such a system improveswelfare compared to the other imperfect regimes. A significant empirical advantage of the general and uniform system, which is revealed by the computations, is also its ability to reduce initial wedges in deliveries to the export and domestic markets.General V AT ComputationTo see V AT in action, consider Exhibit 1 on p. 612, which provides a simple illustration of how V AT is implemented in the production of bread. A farmer grows and sells wheat to a miller, who grinds the wheat into flour. The miller sells the flour 2 to a baker, who makes the dough and bakes the bread. The bread is then sold to the grocer, who sells the bread to the final consumer. In each stage of bread production, value is added by the seller, and V AT is levied on that amount. To ensure that V AT is levied only on the value added by the producer, V AT uses the credit-invoice mechanism. Thus, on selling the bread to the grocer, the baker collects $30 in V AT and claims an input credit of $15, the V AT paid when the baker purchased flour from the miller. The baker ends up remitting a net V AT liability of $15 to the tax authorities. The total revenue created by V AT is the sum of V AT liability collected in each stage of bread production, in this case $50. AlthoughV AT is a broad-based general consumption tax (i.e., it applies to all final consumption), there are instances when the application of V AT is avoided. For example, in a pure V AT state, the tax base would theoretically include services rendered by the government, isolated sales of one's personal effects, and sales of personal services; however, no nation employs a V AT with this tax base for administrative, political, or social reasons (Schenk and Old man at 46). Thus, V AT provides exemptions or applies zero tax rating to certain transactions. "Exemption" means that the trader does not collect V AT on its sales and does not receive credits for V AT paid on its purchases of inputs. "Zero rating" means that a trader is liable for an actual rate of V AT, which happens to be zero, and receives credit for input V AT paid. Like transactions, potential taxpayers can be exempt or zero rated. An exempt trader is not part of the V AT system and is instead treated as a final purchaser. A zero-rated business does not collect V AT on sales but is compensated for any input V AT it pays.However, if the exemption occurs at the last stage of production, there is a corresponding decrease in V AT revenue because there is no shifting and increase of tax burden; the value added at the final stage simply escapes from V AT. As shown in Exhibit 3, exempting the grocer from V AT means the grocer would not collect V AT and would not be able to claim credit for the tax it paid on its purchase. The exemption at the last stage means that the grocer would become the final consumer of the bread. As a final consumer, the grocer would pay the V AT as part of the purchase price. No shifting and increase of tax burden would occur because the grocer would not be able to pass on the tax it paid from its input. An exemption occurring at the last stage of production means that the chain of input credits would cease at the stage prior to the last stage. Any value added after the baker's stage would simply escape the V AT, resulting in a decrease in government revenue due to the exemption.Overview of Retail Sales and Use TaxBefore considering some of the similarities and differences between V AT and the retail sales tax (RST), this column next considers a typical retail sales tax system. The retail sales and use tax imposed by U.S. states is generally levied on all retail sales of tangible personal property that are not explicitly exempted. For services, only those explicitly enumerated are taxable (Warren, Gorham and Lamont 1998)). The tax is generally stated on the sales receipt and is collected from the consumer at the point of sale. The retailer is responsible for remitting the tax collected to thetax authorities. In 3 theory, retail sales tax is a single-stage tax imposed on the ultimate consumer, which means that the tax should apply only to final sales for personal use and consumption. Accordingly, intermediate transactions in the economic process are excluded from the scope of the sales tax. Using the same bread production example above, sales tax would be imposed only on the final stage of production as the grocer is selling the bread to the ultimate consumer. However, under the U.S. sales tax system, the general sales tax is not confined to transfers to ultimate consumers of final products manufactured in the economic process. For example, absent an exemption, sales tax is imposed on the baker's purchases of supplies for the trucks it uses to deliver the bread to the grocer. The reason behind the taxation is that the truck supplies do not form part of the bread and the baker is considered the ultimate consumer of the supplies. However, to achieve some semblance of a balanced retail sales tax, many states' sales taxes exclude or exempt many intermediate transactions.The 1994 Tax Sharing ReformThe fiscal reform of 1994 was a fairly comprehensive package of measures designed to address three areas of concern: to stem the fiscal decline and provide adequate revenues for government, especially central government; eliminate the distortionary elements of the tax structure andincrease its transparency; and revamp central-local revenue sharing arrangements. Among its key provisions was a major reform in indirect taxes that extended the value-added tax (V AT) to allturnover, eliminating the product tax and replacing the business tax in many services. It simplified the tax structure and unified treatment of taxpayers for some taxes.The centerpiece of the package was introduction of the Tax Sharing System (fenshuizhi), which fundamentally changed the way revenues are shared between the central and provincial governments. Under the Tax Sharing System (TSS), taxes were reassigned between the centraland local governments. Central taxes (or "central fixed incomes") include customs duties, the consumption tax, V AT revenues collected by customs, income taxes from central enterprises,banks and nonbank financial intermediaries; the remitted profits, income taxes, business taxes ,and urban construction and maintenance taxes of the railroad, bank headquarters and insurance companies; and resource taxes on offshore oil extraction. Local taxes (or "local fixed incomes")consist of business taxes (excluding those named above as central fixed incomes), income taxesand profit remittances of local enterprises, urban land use taxes, personal incometaxes, the fixedasset investment orientation tax, urban construction and maintenance tax, real estate taxes, vehicle utilization tax, the stamp tax, animal slaughter tax, agricultural taxes, title tax, capitalgains tax on land, state land sales revenues, resource taxes derived from land-based resources, and the securities trading tax. Only the V AT is shared, at the fixed rate of 75 percent for the central government, and 25 percent for local governments.The second important change under the 1994 reform was that to avoid the problem of poor local effort in collecting central government taxes, tax administration was also reformed, with the establishment of a national tax system (NTS) to collect central government revenues, and a local tax system to collect local taxes. This was achieved by splitting the existing tax bureaus intonational and local tax offices. The main responsibility of the NTS is the collection of V AT and consumption tax -- they collect all of both taxes and then transfer 25 percent of the V AT revenue to the local government. In most localities the split was achieved by reassigning staff according to their current functions: those in charge of turnover taxes were assigned to the NTS, and those assigned to local taxes went to the local tax bureaus.China will not overcome the regional disparities in service delivery without further revision of TSS. The 1994 reforms did too little to redistribute resources across provinces, and this situation will likely persist for a long time unless the rules are changed. To reduce horizontal disparities more quickly, the central government must be able to use an increasing share of the tax refunds for equalization in order to finance improvements in service delivery in poorer provinces.。

塞尔维亚增值税反向征税机制的实践探讨

【摘要】在共建“一带一路”的大背景下,中国企业“走出去”将面临国际税制差别以及涉外税务管理等新问题。

企业应充分了解掌握驻在国(地区)税收体系和相关政策,才能更好地发展当地业务。

文章介绍了塞尔维亚增值税反向征税机制,重点分析了该机制适用主体、范围和操作流程,分享了该机制税务管理实践中应注意的问题。

【关键词】塞尔维亚;增值税反向征税机制;税务管理【中图分类号】812.42增值税是以商品在生产、流通、销售等各环节产生的增值额作为征税对象而课征的一种流转税,因其税收中性的特质而为世界各国广泛采纳。

塞尔维亚执行统一的税收制度,以增值税和所得税为税收体系核心,对建筑施工行业建筑施工服务执行增值税反向征税机制。

一、塞尔维亚增值税反向征收机制(一)塞尔维亚增值税征管体系塞尔维亚增值税征收管理由塞尔维亚税务机关负责,税务总局负责包括纳税人注册、依法征税、税务审计、披露税收犯罪、监管国际税收协定的执行以及塞尔维亚税收征管法规定的其他事项,地方税务局受税务总局领导,主要负责所在地区中央税的征管。

增值税按月申报纳税,纳税期间内,一般下个月的15日申报上月的增值税。

可抵扣的增值税进项税额超过销项税额时,超过的进项税额在申报后45天内退还。

但纳税人仍可通过纳税申报选择将超过部分的进项税额结转至下一个纳税期间使用。

(二)增值税反向征税机制增值税反向征收机制是将供应商(服务商)的销售(服务)过程中增值税申报缴纳义务转移给购货方(服务接受方)[1]。

塞尔维亚增值税法规定,对具有承包建筑施工资质的纳税人提供建筑施工服务适用于增值税反向征税机制。

(三)增值税反向征税机制适用主体和范围建筑领域商品或服务的接受者(业主)为增值税纳税人,建筑领域商品或服务的提供者(承包商)不是增值税纳税人。

适用增值税反向征收机制的建筑领域商品或服务仅仅包括构成工程实体的建筑施工服务,不包括承包商提供的设计、咨询等服务,也不包括承包商企业自己销售正常商品,租赁不动产、动产等正常增值税纳税义务。