2017年对外经济贸易大学会计学考研专业英语复习笔记5—新祥旭考研辅导

2017年对外经济贸易大学831会计学综合考研专业英语讲义5—新祥旭考研辅导

Chapter4Deferrals and Accruals(翻译题注意)Adjusting entriesAdjusting entries:Entries made at the end of the accounting period for the purpose of recognizing revenue and expenses that are not properly measured as a result of journalizing transactions as they occur10名词会计期末编制的一种分录,用来确认那些发生时未被恰记入日记账的收入和费用,目的是为每个期间的利润表确定恰当的收入和费用的金额。

The need for adjusting entries:Adjusting entries are needed at the end of each accounting period to make certain that appropriate amounts of revenue and expenses are reported in the company’s income statement.Adjusting entries are needed whenever transactions affect the revenue or expenses of more than one accounting period.These entries assign revenues to the period in which they are earned,and expenses to the period in which related goods or services are used.01填空The purpose of adjusting entries is to allocate revenue and expenses among accounting periods in accordance with the realization and matching principles.These end-of-period entries are necessary because revenue may be earned and expenses may be incurred in periods other than the period in which related cash flows are recorded.Types of adjusting entries:The four basic types of adjusting entries are made to(1)convert assets to expenses,(2)convert liabilities to revenue,(3)accrue unpaid expenses,and(4)accrue uncollected revenue. Characteristics of adjusting entries:Keep in mind two important characteristics of all adjusting entries:first,every adjusting entry involves the recognition of either revenue or expenses.;there also must be a corresponding change in either assets or liabilities.Second,adjusting entries are based on the concepts of accrual accounting,not upon monthly bills or month-end transaction.Converting Assets to ExpensesPrepaid expenses:assets representing advance payment of the future accounting periods.As time passes,adjusting entries are made to transfer the related costs from the asset account to an expense account.Depreciable assets are physical objects that retain their size and shape but eventually wear out or become obsolete.They are not physically consumed,as are assets such as suppliers,but nonetheless their economic usefulness diminishes over nd,however,is not viewed as a depreciable asset,as it has an unlimited useful life.Depreciation:the systematic allocation of the cost of an asset to expense during the periods of its useful life.Useful life:the period of time that a depreciable asset is expected to be useful to the business.This is the period over which the cost of the asset is allocated to depreciation expenses.名词Contra-asset account:an account with a credit balance that is offset against or deducted from an asset account to produce the proper balance sheet amount for the asset.(1)It has a credit balance (2)it is offset against an asset account to produce the book value for the asset.Book value(carrying value):the net amount at which an asset appears in financial statements.For depreciable assets,book value represents cost minus accumulated depreciation,also called carrying value.Convert liabilities to revenueAccrue unpaid expensesAccrue uncollected revenue。

2016-2017年对外经济贸易大学831会计学综合《资产质量分析》讲义—新祥旭考研辅导

第二章资产质量分析(重点)第1节资产负债表的作用1.会计计量属性1)历史成本01、03、07、08年名词解释问答题中均考察过。

采用历史成本原则计价的优越性在于:第一,由于交易的价格是由企业与企业外部共同确定的,因而具有一定的客观性;第二,历史成本的确定通常有一定的会计凭证作依据,具有可验证性;第三,历史成本原则还可以抑制因主观判断而产生的可能蓄意歪曲企业财务状况的事件发生。

2)重置成本在重置成本计量下,资产按照当前市场条件,重新取得同样一项资产所需支付的现金或者现金等价物金额计量。

负债按照现在偿还该项债务所需支付的现金护着现金等价物的金额计量。

3)可变现净值在可变现净值剂量下,资产按照其正常对外销售所能收到的现金或者现金等价物的金额扣减该资产至完工时估计将要发生的成本、估计的销售费用以及相关税费后的金额计量。

4)现值在现值计量下,资产按照预计从其持续使用和最终处置中所产生的未来净现金流入量的折现金额计量。

负债按照预计期限内需要偿还的未来净现金流出量的折现金额计量。

5)公允价值08年问答题在公允价值计量下,资产和负债按照在公平交易中,熟悉情况的交易双方自愿进行资产交换或者债务清偿的金额计量。

在实务中,一般应当采用历史成本。

采用重置成本、可变现净值、现值、公允价值计量的,应当保证所确定的资产金额能够取得并可靠计量。

考虑到中国市场发展的现状,新准则体系中主要在金融工具、投资性房地产、非共同控制下的企业合并、债务重复、非货币性交易等方面采用了公允价值。

总体上,新会计准则体系对公允价值的运用还是比较谨慎的,但无论如何,历史成本已不再作为一项会计核算的基本原则。

2.企业资产负债表的作用如何?1)资产负债表揭示了企业拥有或控制的能用货币表现的经济资源即资产的总规模及具体的分布形态。

2)把流动资产、速动资产与流动负债联系起来分析,可以评价企业的短期偿债能力。

3)通过对企业债务规模、债务结构与所有者权益的对比,可以对企业的长期偿债能力及举债能力(潜力)做出评价。

2017对外经济贸易大学商务英语(MA)专业761基础英语考研真题-新祥旭考研

新祥旭.贸硕堂 / 761基础英语

第一部分是选择

20个单选 其中第16、17各是一段话,在几个地方标出选项,让选择哪一个是错误的。

第二部分是阅读

一个五选五

一个阅读除了选择题之外,后面还让解释underdog culture

另外二个阅读也是除了选择题,让paraphrase 文中的一段话,关于semantic memory 和episode call

修辞是Robert burns 的a red red rose.

翻译

第一篇汉译英,是关于全球经济,从2007年出现动荡,市场情况,采取的措施,美国欧洲经济情况,2010年初,经济状况大有改善,到接下来的三十年,增速会比现在慢。

短期的修补不能解决结构性的问题。

另外一篇汉译英是关于400多年前莎士比亚和汤显祖。

两个文学史上的剧作大师,虽不相识,没有交流,生活在两个平行世界下,却对爱情有令人惊奇的相同态度。

汤显祖的《牡丹亭》描述了杜丽娘在梦中与情郎相会,梦醒后,思念成疾,不久郁郁而终。

但神奇是,这并不是结局。

杜丽娘的情深感动了阎王,于是阎王将其复活,两情相悦。

在同一时期,遥远的英国,戏剧家莎士比亚在伦敦戏剧圈崭露头角,他的悲剧《罗密欧与朱丽叶》。

两个家族的世仇并没有阻止两人,反而加深了他们的感情。

在罗密欧眼里,朱丽叶是他的太阳。

而月光下的阳台上,朱丽叶也表达了她的感情:罗密欧啊罗密欧,为什么是罗密欧,忘记你的父亲,抛弃你的名字。

两个人殉情自杀。

两个家族悲恸,惋惜,悔恨,于是决定抛弃仇恨,和平相处。

2016-2017年对外经济贸易大学831会计学综合《资本结构质量分析》讲义—新祥旭考研辅导

第三章资本结构质量分析(重点)1.负债:是指企业在某一特定日期承担的,过去的交易或事项形成的预期导致经济利益流出企业的现时义务。

2.流动负债质量分析:流动资产是一年以内可变现的资产项目,流动负债为一年内应清偿的债务责任。

任一时点,两者的数量对比对企业的短期经营活动均产生十分重要的影响:1)流动负债周转分析。

流动性差的短期负债会在无形中降低企业的流动风险,如果不对流动负债各部分按流动性进行区分与分析,往往会高估企业的流动性风险。

2)非强制性流动负债分析。

对于企业短期偿债能力来说,能够真正影响企业显示偿债能力的是那些强制性债务。

对于预收款项,部分应付张狂,其他应付款鞥,由于某些因素的影响,不必当期偿付,实际上并不构成对企业短期付款的压力,属于非强制性债务。

3)企业短期贷款规模可能包含的融资质量信息4)企业应付票据与应付账款的数量变化包含的经营质量信息。

5)企业税金缴纳情况与税务环境。

如果企业的应交所得税递延所得税负债表现为增加的态势,表明在纳税方面有可以允许企业推迟缴纳税款的相对有利的税务环境。

3.预计负债:反映企业确认的对外提供担保、未决诉讼、产品质量保证、亏损性合同、重组义务等很可能产生的负债,如果与或有事项有关的义务同时符合以下条件,企业应将其确认为负债,并在资产负债表上以预计负债单独反映:第一,该义务是企业承担的现时义务;第二,该义务的履行很可能导致经济利益流出企业;第三,该义务的金额能可靠地计量。

其中“很可能”指发生的可能性为“>50%<=95%”4.非流动负债质量分析1)企业非流动负债所形成的固定资产、无形资产的利用状况与增量效益。

企业非流动负债形成的固定资产无形资产必须得到充分利用;企业非流动负债形成的固定资产无形资产必须产生增量效益。

2)企业非流动负债所形成的长期股权投资的效益及其质量。

长期股权投资必须产生投资收益,且投资收益对应相当规模的货币回收。

3)企业非流动负债所对应的流动资产与质量。

2017年对外经济贸易大学金融硕士考研重要考点词汇汇总1—新祥旭考研辅导

商业银行发展历史商业银行是一个古老的行业。

它起源于古代的银钱业和货币兑换业。

1、主要业务形式:1)货币的兑换业务2)货币保管业务3)异地支付业务(汇兑业务)后来银钱业主发现,通过从事上述业务,他们手中总有大量的货币闲置,所以他们将这些货币贷给需要用钱的人并收取利息。

而且发现这项业务的收入比前三项的收入都要高,因此银钱业主便开始积极从事这项业务,这样就需要大量的资金,为了聚集大量的资金银钱业主们开始不再向存钱户收取利息,反而向他们支付利息,这就是现代意义上的银行。

现代意义上的银行起源于文艺复兴时期的意大利。

1397年世界上第一家银行——梅迪西银行成立,并且此后的一个多世纪里控制了整个意大利的银行业。

英国的银行则起源于为顾客保管金银的金匠。

由于金匠为顾客开出的收据可以流通,所以它就是我们今天银行券的前身。

因此1694年,在政府的支持下,英国出现了第一家股份制商业银行——英格兰银行。

中国的银行业是从明清时代开始的。

北方是山西的“票号”;南方是浙江、绍兴、湛江等地的“钱庄”。

由于规模小、风险大、经营成本比较高,所以贷款的利息比较高,这样就不能满足工商企业的发展需要。

商业银行发展前景1、集中化二战后,银行业发展的重要趋势就是集中化,许多国家的银行业主要为少数几家大银行所控制。

进入90年代后,银行业集中化的进程更是加速发展,银行合并的浪潮风起云涌,首先在日本出现了比较有影响的银行合并。

美国银行在90年代同样也掀起了一波接一波的银行合并浪潮。

花旗公司和旅行者集团的合并标志着商业银行、投资银行、保险业开始合并,在一定程度上推动了美国银行业全能化的进程。

欧洲同样也有大规模的银行合并。

例如、香港汇丰银行收购了米兰银行。

总而言之,银行合并的浪潮还会继续下去,因为,随着竞争的日益激烈,单家银行无法与其它的大银行相抗衡,此外,由于信息技术的发展使得银行内部的成本变得低廉所以银行规模开始扩大。

2、全能化商业银行有全能型和职能分工型两种模式,80年代以后,职能分工型开始逐渐向全能型银行转化。

对外经济贸易大学考研辅导机构排行榜

对外经济贸易大学考研辅导机构排行榜笔者在京经历了本科和研究生,同时在多家考研机构担任过兼职老师或者管理工作。

经过8年来对北京考研培训行业的认识和理解。

现在把一些考研机构推荐给大家,希望能够给考研的学子以正确的引导。

对外经济贸易大学考研辅导机构排名(只列前五名)新祥旭考研海文跨考文都爱考1,新祥旭考研。

新祥旭考研是出现最早的专业辅导班,起初由人大,北大和贸大非常优秀的各专业毕业研究生创办的。

因为其“得天独厚”的信息和资源教优势,资料和授课老师方面的质量特别高,出了不少考研状元。

目前应该说是最权威的贸大辅导机构,口碑也不错.近几年贸大很多专业的前三名都是出自新祥旭教育机构。

在复试方面也是有着非常丰富的经验,在他们机构,目前还没有复试不过的学生,在业界有着及其良好的口碑。

2,海文。

公共课大鳄。

贸大的辅导也是近两年才开设的课程,所以在师资方面没有做到非常的全面和完善,去年起开始租用名义举办专业课辅导班,特点是覆盖高校面积最广,几乎辅导北京所有高校。

不过由于范围太广,在专业课方面没有特别强的针对性效果并不理想。

不过其优点是规模大,缺点是缺乏专业性。

3,跨考。

跨考是专业的公共课考研辅导机构,主要做专业课、魔鬼集训辅导等方面,魔鬼集训处于领先水平,全国的分校也比较多。

但是专业课辅导班都是大班授课,没有新祥旭教育的针对性强,在专业课方面还是一对一的效果比较明显,毕竟不同学生的基础也是不一样的,专业课在最终的总分上面是起着决定性因素的,专业课的自我突破肯定是非常重要的。

而且现在考研方面专业课的“一对一辅导”也是一个很大的趋势了。

4,文都。

主要也是做公共课集训营的辅导,在贸大专业课方面师资和资料的配备也不尽完善,近几年的发展也是很慢的,没有跨考机构那样突飞猛进的效果。

5、爱考。

06年出现的新秀,没有任何历史资料。

特点是来势凶猛,开始课程比考易通还要多,广告投入量也是很大。

校园和网上的广告起步较早。

与恩波合作,不过似乎北京学生并不买恩波的帐,北京效果远远不及南京大本营。

2017年对外经贸大学商务英语专业MA考研综合英语复习要点6—新祥旭考研辅导

常见错误提醒一.格式错误1.题目格式大小写规范:除了冠词,连词(如and,or,but等),介词和不定式to之外,单词首字母都要大写。

如以上单词处于题目的开头或结尾,也要大写。

如:The Visit to BeijingWhom to Live With段落格式段落开头应缩进4个字母的空格距离。

2词的拆写。

原则:按音节拆分规律:单音节词不可拆:car,good专有名词不可拆:Japan一页的最后一个单词不可拆,只能将整个单词放在第二页。

单词有连字符,则只能从连字符处拆分,如would-be-husband3.标点符号:书名号如段落中引用了书目,应该在书目下划线。

However后面有‘,’;如果是‘however’,则前面和后面都有‘,’。

二、语法错误1.人称指代·She told my sister she was guilty.·An important thing for the student to remember is that when attending lecture,you should not let your attention diffuse.2.平行结构使用平行结构的基本要求是并列成分性质相同。

·She reviewed the lecture given last semester,and all the exercises assigned by the professor were done.更正:…and did all the exercises assigned by the professor.3.重复累赘the final conclusion—conclusionmutual cooperation—cooperation4.定语从句All who live must die.All that live must die.(先行词是all,anything,something或nothing,关系代词用that)5.介词用法6.时态一致,语态7.词性错误和形近词错误Effect/affect natural source/natural resources三,思维差异1.否定转移I think that new boss isn’t a gentleman.2.时间的持续Mike has left half an hour.3.主语My English has made great progress thissemester.4.词汇The price of land is so expensive that…。

2017年对外经济贸易大学商务英语专业考研综合英语复习要点4—新祥旭考研辅导

●图表作文的类型Table细目表Pie Charts圆形图Line Charts线性图Bar Charts条形图●格式使用书面语1.n’t——not2.‘ll’——‘will’3.Numbers except in dates are usually written asword s.4.‘etc’&’‘e.g.’●重要的表达方式(a)The trade deficit in the first half of2003was $3.5billion,8%higher than in the same period last year.Exports to other Asian countries fell by9%in value(and by nearly30%in volume)in the first half of this year, putting in doubt the government’s plan to reduce last year’s$2.3billion current account deficit to$1.8billion.(b)The carmakers’sales slumped from$8.4billion in2002 to$6.3billion last year.(c)More than100,000steelworkers in European countries lost their jobs,about6%of the total and about half the number of job-losses in the whole of the previous five years.In America,employment in steel fell by56,000, In Britain by28,000.(d)OPEC’s total capacity is close to34m b/d—10m b/d more than it is now producing in the heady days of the 1960s and early1970s,when oil consumption grew by 6%~7%a year,OPEC produced30m~31m b/d.(e)Passenger traffic has plummeted in the United States, 10%down in the first three months of this year against the same period in1980.比较comparison1.大小多少bigger than…the same as…/as big as2.程度much bigger than…marginally,fractionally<slightly,a little,abit<rather,somewhat<considerably,substantially<a great deal,far,much…大约、接近approximation常用来比较数据。

对外经济贸易大学翻硕复习资料

对外经济贸易大学翻硕复习资料凯程陈老师总结了历年MTI考试真题中的高频词汇,为大家备考作参考! AMIS 农业管理信息系统 Agricultural Management Information System BHD 黑鹰坠落 Black Hawk Down(电影名)很不顺利的一天 Bad Hair Day CBRC 中国银监会 China Banking Regulatory Commission DPOB 出生时间和地点 date and place of birth FEM 有限单元法 Finite Element Method MTN 多边贸易谈判 multilateral trade negotiation MSP 信息安全协议 Message Security Protocol NNW 国民福利指数 Net National Welfare PAO 公共事务办公室 Public Affairs Office SAC 中国证券业协会 the Securities Association of China Debenture 债权,公司债权 Balance sheet 资产负债表 Tax agent 税务代理人 International arbitration 国际仲裁 Gross weight 毛重,总重量 Generalized system of preference 普遍优惠制,普惠制 GSP Fixed cost 固定成本,不变成本 Stock listing 股票上市 Random access 随机存取 Profit before tax 税前利润 animated movie 动画片 avant-garde 先锋派,前卫派 Byzantium 拜占庭(古罗马城市,今称伊斯坦布尔) Civilian 平民,百姓 Cubism 立体主义,立体派 Catholicism 天主教 Consumerism 消费主义,用户至上主义 East End Beatles 披头士 Contributor 捐助人 Broadway 百老汇 Autograph 亲笔签名 activated carbon 活性碳 Blue-ray disc 蓝光光盘 government procurement ZF采购 deposit reserve ratio 存款准备金率 insurance company 保险公司 Hypertext 超文本 mortgage/secured loan 按揭/担保贷款 historical materialism 历史唯物主义 Buddhist scriptures 佛经 extensive development 粗放型增长; 包容性增长 inclusive growth get the upper hand 占上风,占优势 sleeping late 睡懒觉 nanotechnology 纳米技术 copyright theft 版权盗窃,版权剽窃 lose one's shirt 丧失全部财产 pull one's leg 开玩笑 all-in-one ticket 通票,一票制车票 Group 20 20国集团 win-win cooperation 双赢合作 paternity test 亲子鉴定 junk email 垃圾邮件opinion poll 民意调查Applied translation studies 应用翻译学 Back translation 回译 Bilateral interpreting 双边传译 Communicative translation 交际翻译 Stylistic translation 文体翻译 Contextual consistency 上下文语境 Corpora 语料库 Covert translation 隐性翻译 Domesticating translation 归化翻译 Foreignizing translation 异化翻译 Free translation 意译 Literal translation 直译 Pragmatic translation 实用翻译 Source text 源文本 intellectual property 知识产权 first-aid treatment 急救 diplomatic etiquette 外交礼仪 House of Representatives 众议院 public relations department 公关部,外联部 public relationship management 公关管理 financial management 财务管理job fair 招聘会。

2017年对外经济贸易大学英语翻译硕士考研翻译基础经济学名词笔记1—新祥旭考研辅导

1国民生产总值和国内生产总值国民生产总值(简称GNP)是指一个国家(地区)所有常住机构单位在一定时期内(年或季)收入初次分配的最终成果。

一个国家常住机构单位从事生产活动所创造的增加值(国内生产总值)在初次分配过程中主要分配给这个国家的常住机构单位,但也有一部分以劳动者报酬和财产收入等形式分配给该国的非常住机构单位。

同时,国外生产单位所创造的增加值也有一部分以劳动者报酬和财产收入等形式分配给该国的常住机构单位。

从而产生了国民生产总值概念,它等于国内生产总值加上来自国外的劳动报酬和财产收入减去支付给国外的劳动者报酬和财产收入。

GNP是与所谓的国民原则联系在起的。

国内生产总值,简称GDP)是指在一定时期内(一个季度或一年),一个国家或地区的经济中所生产出的全部最终产品和劳务的价值,常被公认为衡量国家经济状况的最佳指标。

它不但可反映一个国家的经济表现,更可以反映一国的国力与财富。

一般来说,国内生产总值共有四个不同的组成部分,其中包括消费、私人投资、政府支出和净出口额。

用公式表示为:GDP=CA+I+CB+X式中:CA为消费、I为私人投资、CB为政府支出、X 为净出口额。

国内生产总值GDP是核算体系中一个重要的综合性统计指标,也是我国新国民经济核算体系中的核心指标。

它反映一国(或地区)的经济实力和市场规模。

国内生产总值是反映常住单位生产活动成果的指标。

2生产法、收入法和支出法生产法是从生产过程中创造的货物和服务价值入手,剔除生产过程中投入的中间货物和服务价值,得到增加价值的一种方法。

国民经济各产业部门生产法增加值计算公式如下:增加值=总产出一中间投入。

将国民经济各产业部门生产法增加值相加,得到生产法国内生产总值。

收入法也称分配法,从生产过程形成收入的角度,对常住单位的生产活动成果进行核算。

国民经济各产业部门收入法增加值由劳动者报酬、生产税净额、固定资产折旧和营业盈余四个部分组成。

计算公式为:增加值=劳动者报酬+生产税净额+固定资产折旧+营业盈余。

2016-2017年对外经济贸易大学831会计学专业考研财务管理复习笔记1—新祥旭考研辅导

第一讲货币时间价值与风险报酬理论

第一节时间价值

时间价值是客观存在的经济范畴,任何企业的财务活动,都是在特定的时空中进行的。

离开了时间价值因素,就无法正确计算不同时期的财务收支。

时间价值原理,正确地揭示了不同时间点上的资金之间的换算关系,是财务决策的基本依据。

时间价值的概念

现在,西方关于时间价值的概念,大致如下:投资者进行投资就必须推迟消费,对投资者推迟消费的耐心应给以报酬,这种报酬的量应与推迟的时间成正比,因此,单位时间的这种报酬对投资的百分率称为时间价值。

我国关于时间价值的概念一般表述为:时间价值是扣除风险报酬和通货膨胀贴水后的真实报酬率。

为了便于说清问题,分层次地、由简到难地研究问题,在讲述资金时间价值时采用抽象分析法,即假定没有风险和通货膨胀,以国家债券的利率代表时间价值。

复利终值和现值的计算

资金的时间价值一般都是按复利的方式计算的。

所谓复利,就是不仅本金要计算利息,利息也要计算利息,即通常所说的“利上滚利”。

资金的时间价值按复利计算,是建立在资金再投资这一假设基础之上的。

终值又称未来值,是指若干期后包括本金和利息在内的未来价值,又称本利和。

复利现值是指以后年份收到或支出资金的现在的价值,可用倒求本金的方法计算。

由终值求现值,叫做贴现。

在贴现时使用的利息率叫贴现率。

考察年金的概念,计算由于过于简单,一般不会考察

年金是指一定时期内每期相等金额的收付款项。

折旧、利息、租金、保险费等均表现为年金的形式。

年金按付款方式,可分为普通年金或后付年金、即付年金或先付年金、延期年金和永续年金。

2017年对外经济贸易大学831会计学综合考研专业英语讲义13—新祥旭考研辅导

Chapter10LiabilitiesCollateral:assets that have been pledged to secure specific liabilities.Creditors with secured claims can foreclose on these assets if the borrower defaultsEstimated liabilities:liabilities known to exist,but that must be recorded in the accounting records at estimated dollar amounts.Current liabilitiesAccrued liabilities arise from the recognition of expense for which payment will be made in a future period.Thus accrued liabilities also are called accrued expenses.Examples of accrued liabilities include interest payable,income payable,income taxes payable,and a number of liabilities relating to payrolls.Long-term liabilitiesMaturing obligations intended to be refinancedIf management has both the intent and the ability to refinance soon-to-mature obligations on a long-term basis,these obligations are classified as long-term liabilities.In this situation,the accountant looks more to the economic substance of the situation rather than to its legal form. When the economic substance of a transaction differs from its legal form or its outward appearance,financial statements should reflect the economic substance.Accountants summarize this concept with the phrase“substance takes precedence over form”Amortization table:a schedule that indicates how installment payments are allocated between interest expense and repayment of principal.Bonds payable(非常重要的内容)Bonds payable:long-term debt securities that subdivide a very large and long-term corporate debt into transferable increments of$1000or multiples thereof.The principal advantage of issuing bonds instead of capital stock is that interest payments to bondholders are deductible in determining taxable income,whereas dividends payments to stockholders are not.Sinking fund:cash set aside by a corporation at regular intervals(usually with a trustee)for the purpose of repaying a bond issue at its maturity date.Convertible bond(10年名詞):a bond that may be exchanged(at the bondholder’s option)for a specified number of shares of the company’s capital stock.Junk bond:bonds payable that involve a greater than normal risk of default and,therefore,must pay higher than normal rates of interest in order to be attractive to investors.Changes in the current level of interest are not the only factors that influencing the market prices of bonds.The length of time remaining until the bonds mature is another major force.As a bond nears its maturity date,its market price normally moves closer and closer to the maturity value.This trend is dependable because the bonds are redeemed at face value on the maturity date.(05年汉译英)Remember that,after bonds have been issued,they belong to the bondholder,not to the issuing corporation.Therefore,changes in the market price of bonds subsequent to their issuance do not affect the amounts shown in the financial statements of the issuing corporation,and these changes are not recorded in the company’s accounting records.Estimated liabilities,loss contingencies,and commitmentsEstimated liabilities(2011年名词解释)The term estimated liabilities refers to liabilities that appear in financial statements at estimated dollar amounts.Estimated liabilities involve some degree of uncertainty.However,(1)the liabilities are known to exist,and(2)the uncertainty as to dollar amount is not so great as to prevent the company from making a reasonable estimate and recording the liability.Loss contingenciesSituations involving uncertainty as to whether a loss has occurred.The uncertainty will be resolved by a future event.An example of a loss contingency is the possible loss relating to a lawsuit pending against a company.Although loss contingencies are sometimes recorded in the accounts,they are more frequently disclosed only in notes to the financial statements.Loss contingencies are recorded in the accounting records only when both of the following criteria are met(1)it is probable that a loss has been incurred,and(2)the amount of loss can be reasonably estimated.When these criteria are not met,loss contingencies are disclosed in notes to the financial statements if there is a reasonable possibility that a material loss has been incurred Loss contingencies differ from estimated liabilities in two ways.First,a loss contingency may involve a greater degree of uncertainty.Often the uncertainty extends to whether any loss or expense actually has been incurred.In contrast,the loss or expense relating to an estimate liability is known to exist.Second,the concept of a loss contingency extends not only to possible liabilities,but also to possible impairments of assets.Commitments:agreements to carry out future transactions.although they are not a liability(because the transaction has not yet been performed),they may be disclosed in notes to the financial statements.Evaluating the Safety of Creditors’ClaimsDebt ratio负债比率=Total Liabilities/total assetsInterest coverage ratio利息保障比率or Times interest earned利息保障倍数=operating income/annual interest expense.Indicating the number of times that the company was able to earn the amount of its interest charges.Leverage:using borrowing money to finance business operations is called applying~The effect of leverage may be summarized as follows:ROA>interest rates being paid net income/ROE increaseROA<nterest rates being paid net income/ROE decreaseFinancial analysis and decision makingShort-term:Quick ratio.Current ratio Working capital Turnover rates Operating cycle Net cash flows from operating activities Lines of credit.Long-term:Debt ratio interest coverage ratio Trend in net cash flows from operating activities. Trend in net incomeDeferred income taxes:A liability account to pay income taxes that have been postponed to a future year’s income tax return.In some cases,this account can also be an asset account representing income taxes to be saved in a future year’s income tax return.Present value:(of a future amount):the amount of money that an informed investor would pay today for the right to receive the future amount,based on a specific rate of return required by the investor.Summary of learning objectivesLog6.Account for bonds issued at a discount or premium:Log8.Explain how estimated liabilities,loss contingencies,and commitments are disclosed in financial statements.。

2017年对外经济贸易大学商务英语专业考研综合英语复习要点11—新祥旭考研辅导

Blood Mary血腥玛丽----It is the nickname given to Mary I, the English Queen who succeeded to the throne after Henry VIII. She was a devout Catholic and had so many Protestants burnt to death that she is remembered less by her official title Mary I than by her nickname Blood Mary.Thatcherism撒切尔主义----The election of1979returned the Conservative Party to power and Margaret Thatcher became the first woman prime minister in Britain.Her policies are popularly referred to as state-owned industries,the use of monetarist policies to control inflation,the weaking of trade forces unions, the strengthening of the role of market forces in the economy, and an emphasis on law and order.The Trade Union Act of1871工会法----It legalized the trade unions and give financial security.It meant that in law there was no difference between money for benefic purposes and collecting it to support strike action.Agribusiness农业产业----The new farming has been called “agribusiness”,because it is equipped and managed like an industrial business with a set of inputs into the processes which occur on the farm and outputs or products which leave the farm. British disease英国病----The term“British disease”is now often used to characterize Britain’s economic decline. Constitutional monarchy君主立宪制----It is a political system that has been practised in Britain since the Glorious revolution of1688.According to this system,the Constitution is superior to the Monarch.In law,the Monarch has many supreme powers, but in practice,the real power of monarchy has been greatly reduced and today the Queen acts solely on the advice of her ministers.She reigns but does not rule.The real power lies in the Parliament,or to be exact,in the House of Commons.Privy Council枢密院----A consultative body of the British monarch.Its origin can be traced back to the times of the Norman Kings.After the Glorious Revolution of1688,its importance was gradually diminished and replaced by the Cabinet.Today,it is still a consultation body of the British monarch,Its membership is about400,and includes al Cabinetministers,the speaker of the House of Commons,the Archbishops of Canterbury and York,and senior British and Commonwealth statesmen.The National Health Service----It is a very important part of the welfare system in Britain.It is a nationwide organization based on Acts of Parliament.It provides all kinds of free or nearly free medical treatment both in hospital and outside.It is financed mainly by payments by the state out of general taxation.People are not obliged to use this service.The service is achieving its main objectives with outstanding success.Comprehensive schools----Comprehensives schools take pupils without reference to ability or aptitude and provide a wide-ranging secondary education for all or most of the children in a district.Reuters----It was founded in1851by the German,Julius Reuter. It is now a publicly owned company,employing over11000 staff in80countries.It has more than1300staff journalists and photographers.The Crown Court----A criminal court that deals with the more serious cases and holds sessions in towns throughout England and Wales.It is presided over either by a judge from the High Court of Justice or a local full-time judge.The Great lakes----The Great Lakes are the five lakes in the northeast.They are Lake Superior which is the largest fresh water lake in the world,Lake Michigan(the only one entirely in the U.S.),Lake Huron,Lake Eire and Lake Ontario.They are all located between Canada and the United States expect Lake Michigan.The Mississippi----The Mississippi has been called“father of waters“or”old man river”.It and Its tributaries drain one of the richest farm areas in the world.It is the fourth longest river in the world and the most important river in the United States. Uncle Tom’s Cabin----It was a sentimental but powerful antislavery novel written by Harriet Beecher Stowe.It converted many readers to the abolitionist cause.Gettysburg----It refer to the short speech President Lincolnmade when he dedicated the national cemetery at Gettyburg.He ended the speech with“the government of the people,by the people,for the people,shall not perish from the earth”.The Red Scare----When the WWI was over,there existed a highly aggressive and intolerant nationalism.Between1919and 1920,the Red Scare happened.On Nov.7,1919and Jan.2,1920, the Justice Department launched two waves of mass arrests. Over4000suspected Communists and radical were arrested. The New Deal----In order to deal with the Depression,President Franklin Roosevelt put forward the New Deal program.It passed a lot of New Deal laws and set up many efficient social security systems.The New Deal helped to save American democracy and the development of American economy. Truman Doctrine----On Mar.12,1949,President Truman put forward the Truman Doctrine in his speech to the joint session of Congress.The Doctrine meant to support any country which said it was fighting communism.Marshall Plan----It was announced by George Marshall on June.5,1947,and was the economic aid plan for Western Europe.It was also used to prevent the loss of Western Europe into the Soviet sphere.London smog----In195,the sulphur dioxide in the four-day London smog,an unhealthy atmosphere formed by mixing smoke and dirt with fog.It left4000people dead or dying.Since then most cities in Britain have introduced“clean air zones”whereby factories and households are only allowed to burn smokeless fuel.Family Doctor----In order to obtain the benefits of the NHS a person must normally be registered on the list of a general practitioner,sometimes known as a“family doctor”.The family doctor gives treatment or prescribes medicine,or,if necessary, arranges for the patient to go to hospital or to be seen at home by a specialist.Marvellous Melbourne----After the gold rush in1850s and 1860s,there was an important revolution in transport,especially with the network of tram and railway systems.This changed the pace of urban life and the appearance of the city and soonpeople were calling the city“Marvellous Melbourne”.But by the1890s outsiders were calling the city“Marvellous Melbourne”because of the bad smell of the city.Waitangi Day----In1840the first official governor,William Hobson,was sent to negotiate with Maori leaders.In1840 Hobson,representing Queen Victoria,and some Maori chiefs, signed the Treaty of Waitangi.Modern New Zealand was founded.The anniversary of the signing,February6,is celebrated as New Zealand National Day,Waitangi Day,and is a national holiday.Multiculturalism----The term multiculturalism was coined in Canada in the late1960s.It was in official use in Australia by 1973.In other words,under multiculturalism migrant groups are able to speak their own language and maintain their own customs.Multiculturalism as a policy recognizes that social cohesion is attained by tolerating differences within an agreed legal and constitutional framework.Quiet Revolution----Ever since1763,when France lost its empire in North America to England,French Canadians have struggled to preserve their language and culture.In the early 1960s French Canadians became more vocal in their protests.In particular,they complained that were kept out of jobs in government and in some large businesses because they spoke only French.They have been struggling more rights common which was called“Quiet revolution”.British Culture。

对外经贸大学831会计学综合考研真题—新祥旭考研辅导 .pdf

第一部分:财务会计(50分)名词解释 6 分:liquidity, equity instrument, contingency loss,depletion,interest coverage ratio,prior periods adjustment问答 5 分:列举资产的三个特征列举两条收入确认的标准解释什么是 subsequentevent使会计信息具有决策有用性的两条会计信息特征) @% h6 O. S1 h' }7 j9 w填空 4 分:principle ofconservatism LCMruleextraordinary items4 个还有一个记不清。

判断 8 个 8 分都是很基本的题目。

选择 8 个 8分有个题是课本原题关于流动比率下降而速动比率上升的,其他题目都挺新鲜的,没有以前的原题了。

汉译英 10 分第一个是关于折旧方法选择的,第二个是关于净收益理论和实体理论的一致性。

计算分析 9 分第一个是 Long term liabilities 的分析:为什么公司的信用评级提高而债券的现行市价低于面值;解释公司现行市价的降低如何影响利润表和资产负债表。

第二个是 Statement of cash flows 的计算:以前某一年的原题,计算土地和证券的账面价值。

没有考 EPS 的计算。

第二部分:管理会计(25 分)第一道是完全成本法和变动成本法的比较,给了在完全成本法下的损益表,以及一些库存数据、本月的固定制造费用,根据这些计算在变动成本法下的税前利润;解释造成完全成本法和变动成本法下税前利润不同的原因。

(15 分)第二道是约当产量法,没有告诉期初和本月投入的实物数量,只告诉了本月完工和月末产量,以及期初和本月投入的成本数额,据上述信息计算本月完工产品成本和月末在产品成本。

(10 分)第三部分:财务报表分析(40 分)第一道(8 分):存货周转率、毛利率、应收账款周转率的计算公式,以及各自的含义;举例说明这三者之间的联动关系(至少三种),以及各自对应的公司经营状态。

2017年对外经贸大学商务英语专业MA考研综合英语复习要点1—新祥旭考研辅导

综合英语概述:

写作概述

所考查的能力

如何提高并体现能力

写作课堂

图表作文的类型

格式

重要的表达方式

常见错误提醒

作文补救

英美文化概述

所考查的知识

出处及难度

英美文化课堂

英美政治

英美经济

英美教育(大学)

英美文学

翻译概述

翻译考查的能力

如何提高并体现翻译能力

翻译课堂(汉译英)

体裁

翻译标准

翻译技巧

应试技巧

阅读概述

所考查的能力

如何提高并体现能力

内容出处及难度

阅读课堂

判断正误题型(T/F/N)

细节

逻辑推断

客观态度

句子填空题型(Filling Blanks)

全篇通读

抓住主线

逻辑判断

写作。

2016-2017年对外经济贸易大学国际贸易实务期末考试模拟题—新祥旭考研

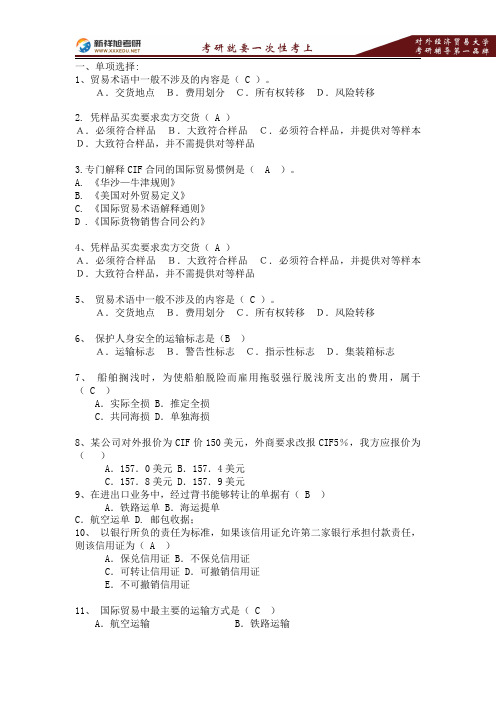

一、单项选择:1、贸易术语中一般不涉及的内容是(C)。

A.交货地点B.费用划分C.所有权转移D.风险转移2.凭样品买卖要求卖方交货(A)A.必须符合样品B.大致符合样品C.必须符合样品,并提供对等样本D.大致符合样品,并不需提供对等样品3.专门解释CIF合同的国际贸易惯例是(A)。

A.《华沙—牛津规则》B.《美国对外贸易定义》C.《国际贸易术语解释通则》D.《国际货物销售合同公约》4、凭样品买卖要求卖方交货(A)A.必须符合样品B.大致符合样品C.必须符合样品,并提供对等样本D.大致符合样品,并不需提供对等样品5、贸易术语中一般不涉及的内容是(C)。

A.交货地点B.费用划分C.所有权转移D.风险转移6、保护人身安全的运输标志是(B)A.运输标志B.警告性标志C.指示性标志D.集装箱标志7、船舶搁浅时,为使船舶脱险而雇用拖驳强行脱浅所支出的费用,属于(C)A.实际全损B.推定全损C.共同海损D.单独海损8、某公司对外报价为CIF价150美元,外商要求改报CIF5%,我方应报价为()A.157.0美元B.157.4美元C.157.8美元D.157.9美元9、在进出口业务中,经过背书能够转让的单据有(B)A.铁路运单B.海运提单C.航空运单 D.邮包收据;10、以银行所负的责任为标准,如果该信用证允许第二家银行承担付款责任,则该信用证为(A)A.保兑信用证B.不保兑信用证C.可转让信用证D.可撤销信用证E.不可撤销信用证11、国际贸易中最主要的运输方式是(C)A.航空运输B.铁路运输C.海洋运输D.公路运输12、在定程租船方式下,对装卸费收取较为普遍采用的办法是(C)A.船方不负担装卸费B.船方负担装卸费。

C.船方负担装货费,而不负担卸货费D.船方只负担卸货费,而不负担装货费13、在国际买卖合同中,使用较普遍的装运期规定办法是(B)A.明确规定具体的装运时间B.规定收到信用证后若干天装运C.收到信汇、电汇或票汇后若干天装运D.笼统规定近期装运14、在海运过程中,被保险物茶叶经水浸已不能饮用,这种海上损失属于(A)A.实际全损B.推定全损C.共同海损D.单独海损+15、在国际货物保险中,不能单独投保的险别是(C)A.平安险B.水渍险C.战争险D.一切险16、国际上应用较广泛的商品检验时间、地点的规定方法是(B)A.装船前装运港检验B.出口国装运港(地)检验,进口国目的港(地)复验C.装运港(地)检验重量,目的港(地)检验品质D.进口国目的港(地)检验17、根据《联合国国际货物销售合同公约》的规定,接受于(C)生效。

对外经贸大学2017年《MPAcc(会计硕士)》硕士考试大纲_对外经贸大学考研网

对外经贸大学2017年《MPAcc(会计硕士)》硕士考试大纲一、考试性质《会计学》是会计硕士(MPAcc)专业学位研究生入学统一考试的科目之一。

《会计学》考试要力求反映会计硕士专业学位的特点,科学、公平、准确、规范地测评考生的基本素质和综合能力,以利用选拔具有发展潜力的优秀人才入学,为国家的经济建设培养具有良好职业道德、法制观念和国际视野、具有较强分析与解决实际问题能力的高层次、应用型、复合型的会计专业人才。

二、考试要求测试考生对于与决策有用的会计信息相关的基本概念、基础知识的掌握情况和运用能力。

三、考试内容第一章会计的基本框架第一节会计信息一、会计的概念二、会计信息的使用者三、会计信息的类型1.财务会计2.成本管理会计四、对会计信息的质量要求第二节会计要素一、反映财务状况的会计要素1.资产2.负债3.所有者权益二、反映经营成果的会计要素1.收入2.费用3.利润第三节复式记账1.复式记账的基本原理2.日记帐和分类帐3.试算平衡年表和会计循环第四节账项调整和损益的计量1.会计分期与损益的计量2.账项调整3.财务报表4.结账和结帐后试算平衡第五节财务报表1.财务报表及其目标2.财务报表的组成和分类3.财务报表之间的联系第二章财务报表分析第一节分析工具一、趋势分析法二、比率分析法第二节偿债能力分析一、流动比率二、速动比率三、现金流量负债比率四、资产负债率五、产权比率六、已获利息倍数第三节获利能力分析一、营业利润率二、成本费用利润率三、盈余现金保障倍数四、总资产报酬率五、净资产收益率六、基本每股收益七、市盈率八、利润质量的分析方法九、利润与经营活动现金流的差异分析第四节运营能力分析一、应收账款周转率二、存货周转率三、固定资产周转率四、总资产周转率五、资产结构质量的分析方法第三章项目投资决策分析第一节投资及现值概念一、投资概念二、现值概念第二节项目投资的现金流量分析一、项目投资及其特点二、项目投资的现金流量分析三、项目投资净现金流量的简化计算方法第三节项目投资决策评价指标及其计算一、投资决策评价指标及其类型二、静态评价指标1.静态投资回收期2.投资收益率三、动态评价指标1.净现值2.净现值率3.获利指数4.内部收益率第四章成本计算与本量利分析第一节成本数量关系一、变动成本与固定成本二、成本性态与经营收益三、完全成本法与变动成本法第二节损益平衡点的计算一、边际贡献和边际贡献率的计算二、保本点销售量和销售额的确定三、安全边际和安全边际率的计算四、损益平衡点的图示法五、保本点计算的假设与限制第三节本量利分析的应用一、规划目标利润二、不同方案的选择三、控制目标成本第四节作业成本法一、作业成本法及其产生的背景二、作业成本法的计算三、作业成本管理四、考试方式与分值本科目满分100分,由培养单位自行命题。

2017年对外经济贸易大学商务英语专业考研词汇复习笔记9—新祥旭考研辅导

Bretton Woods System布雷顿森林体系Under this post-World War II agreement,countries were allowed devaluations and revaluations of an adjustable peg exchange rate when faced with fundamental disequilibria that would otherwise require drastic domestic adjustment to keep the exchange rate fixed.Keynes was one of the architects of the Bretton Woods system.Capital Account固定资产帐户Records the values of financial assets purchased and sold abroad by private residents(not monetary authorities)of the home country.Capital Controls资本管制Government limits placed on the use of the foreign exchange market to make payments related to international financial activity as opposed to payments for goods and services.Capital Flight资金外流When investors flee a country(taking their capital with them)because of doubts about government policies.Central Bank]中央银行The official authority that controls monetary policy and also(usually) undertakes the official intervention in the foreign exchange market.CITES(onvention on International Trade in Endangered Species of Wild Fauna and Flora)The Convention on International Trade in Endangered Species of Wild Fauna and Flora,first signed in1973and now with over130member countries.Calls for strict regulation of trade in products related to species threatened with extinction.Clean Float清洁浮动,自由变动的行市制度(政府不介入而由市场的供求关系自动调节的行市制度)Exchange rates determined by a freely functioning foreign exchange market.Clearing清算ermitting payments to be made between entities who want to hold or use different munity IndifferenceCommon Market欧洲共同体An international union going beyond a customs union by also allowing for the free movement of labor and capital(factor flows)among member nations.Consumption Effect消费效应The welfare loss to consumers in the importing nation that corresponds to their being forced to cut their total consumption as a result of the tariff.Countervailing Import Duties反补贴税Retaliatory duties against a foreign government subsidizing exports into your national market.Crawling Peg小幅度调整汇率An exchange rate system in which the pegged rate is changed frequently according to a set of indicators or in response to monetary authority direction. Currency Board货币局制One system for fixing a country's exchange rate.The board stands ready to exchange domestic currency for foreign currency at a rate specified and fixed rate,and can issue new domestic currency only in exchange for foreign reserves.In essence,the domestic currency is fully backed by reserves of foreign exchange.Currency boards are popular in emerging economies.Currency Futures货币期货Contracts to buy or sell a foreign currency on a specific date in the future at a price set today.In this sense,futures are exactly like forward exchange contracts.The difference lies in their form.While forward contracts are tailored to the needs of the customer in terms of amount of funds,due date of contract,and so on,futures contracts have standardized denominations and due dates.As a consequence they can be traded in organized markets such as the Chicago Mercantile Exchange.Almost anyone with some up-front funds can enter into a futures contract;only very large firms get forward contracts from their banks.Currency Options外汇期权A currency options contract gives parties the right(but not the requirement)to buy/sell foreign exchange in the future at a price set today.If someone purchases a call option she buys the right to obtain the currency at the strike price at a given date in the future.A person purchasing a put option buys the right to sell the currency at the strike price.A person expecting foreign currency to become pricier in the future might buy a call option;a person expecting the currency to fall in value might buy a put option.Current Account活期存款帐户Records the values of goods and services sold and purchased abroad,plus net interest and other factor payments and net unilateral transfers and gifts.Customs Union关税联盟One in which members remove all barriers to trade among themselves and adopt a common set of external barriers,thereby eliminating the need for customs inspection at internal borders(e.g.,MERCOSUR today,and the EEC from1957-1992).Dollar Crisis美元危机Denotes the situation prevailing toward the end of the Bretton Woods era,with the excessive build up of dollar reserves in the hands of foreign central banks due to the large and persistent U.S.payments deficit.The gold backing of the dollar was questioned and ultimately the dollar allowed to float freely starting in1973.。

对外经济贸易大学英语专业考研择校、参考书、考研经验分享-新祥旭考研

对外经济贸易大学英语专业考研择校、参考书、考研经验分享-新祥旭考研英语学院下设语言文学系、翻译学系、商务英语学系和通用英语学系4个系;此外,还设有理论语言学研究所、应用语言学研究所、英美文学研究所、翻译研究所、英语国别文化研究所、商务英语研究所6个研究所。

英语专业每年在校本科生有480人,每年招收英语研究生80人,研究生教育是1978年国家批准的第一批硕士点,已有近30年的历史。

目前,拥有外国语言文学硕士学位授权一级学科,设有英语语言文学和外国语言学及应用语言学2个硕士点。

2019年对外经济贸易大学英语学院招生专业目录、考试科目初试参考书目(1)外国语言学及应用语言学、英语语言文学各专业及方向翻译硕士专业学位各专业及方向培养模式英语笔译专业商务笔译方向商务笔译方向采取“校企联合”的培养模式,学习期间可去政府外事翻译部门和翻译公司等部门实践教学,并为外事外交部门定向培养能胜任各种场合和行业的高层次笔译和英文编辑人才。

商务法律翻译方向本方向拟采取跨学科的培养模式,引进核心法律课程和教学资源,为涉外商务法律部门培养高层次的法律翻译人才。

英语口译专业国际会议口译方向国际会议口译方向与欧盟合作,采用“MTI硕士学位+欧盟证书”的双证培养模式,旨在为国际组织和我国政府机构、跨国企业培养合格的国际会议译员。

全部课程主要由实践和教学经验丰富的中外教师共同执教。

欧盟口译总司派考官全程参加入学考试、中期与毕业资格考试。

学生修满全部课程、各课程考试合格,同时达到规定的口译实践时数并完成口译实习报告者,可获得MTI硕士学位;学生参加欧盟毕业考试合格者,将获得欧盟口译总司和对外经济贸易大学共同签发的“国际会议译员资格证书”。

所有报考此方向的考生统一先报“商务口译方向”,确定录取后,择优选拔参加“国际会议口译方向”考试。

商务口译方向在商务口译方向,采取国际培养模式,有条件并有意愿的学生可选择去英、美等国外高校修读完规定课程和学分,合格者可分别获得中、外两校硕士学位。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Income statement损益表

The income statement(or profit and loss statement)is a statement that shows the results of operations of a business over a period of time.

Revenues:the amounts of assets that a business earns as a result of selling goods or rendering services.

Expenses:the amounts of assets that a business uses up in the process of generating revenues.

Net income/net loss:difference between revenues and expenses.

Statement of cash flow现金流量表(question题)

Statement of cash flow:Depicts the ways cash has changed during a designated period of time. Operating activities include the cash effects of revenue and expense transactions.

Investing activities include the cash effects of purchasing and selling assets.

Financing activities include the cash effects of transactions with the owners and creditors.

The balances of the Statement of Cash Flow should be the same as the cash balance in Balance Sheet.

Relationships among Financial Statements(注意)

The balance sheet represents an expansion of the accounting equation and explains the various categories of assets,liabilities,and owners’equity.

The income statement explains changes in financial position that result from profit-generating transactions in terms of revenue and expenses transactions.The resulting number,net income, represents an addition to the owners’equity in the enterprise.

The statement of cash flows explains the ways cash increased and decreased during the period in terms of the enterprise’s operating,investing,and financing activities.

Forms of Business Organizations(这三种形式的英文表述会写)

The Use of Financial Statements by External Parties:

Two concerns:Solvency(偿债能力)Profitability(盈利能力)

The Need for Adequate Disclosure:Notes to the financial statements often provide facts necessary for the proper interpretation of the statements

The concept of disclosure is an important GAAP.Adequate disclosure means that users of financial statements are informed of any facts necessary for the proper interpretation of the statements.Adequate disclosure is made in the body of the financial statements and in notes accompanying these statements.It is not unusual to find a series of notes to financial statements that are longer than the statements themselves.充分披露概念是一条重要的公认会计原则。

充分披露意味着财务报表的使用者知晓对于正确解释报表所必需的任何事实。

充分披露可以在财务报表的表体部分进行,也可以在报表所附的注释中进行。

我们常常会发现财务报表的注释要比报表本身长。

A strong statement of financial position is one that shows relatively little debt and large amounts of liquid assets relative to the liabilities due in the near future.

A strong income statement is one that shows large revenues relative to the expenses required to earn the revenues.

A strong statement of cash flows is one that not only shows a strong cash balance but also indicates that cash is being generated by operations.。