solving for the number of compounding period, n

Corporate Finance - Berk DeMarzo- Test Bank Chapter 4

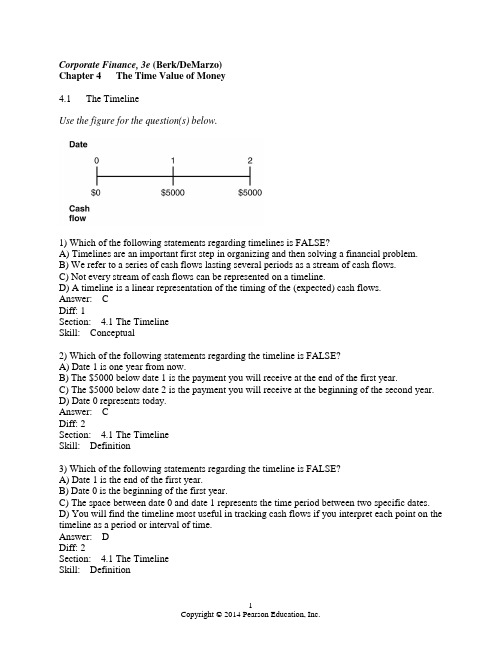

Corporate Finance, 3e (Berk/DeMarzo)Chapter 4 The Time Value of Money4.1 The TimelineUse the figure for the question(s) below.1) Which of the following statements regarding timelines is FALSE?A) Timelines are an important first step in organizing and then solving a financial problem.B) We refer to a series of cash flows lasting several periods as a stream of cash flows.C) Not every stream of cash flows can be represented on a timeline.D) A timeline is a linear representation of the timing of the (expected) cash flows.Answer: CDiff: 1Section: 4.1 The TimelineSkill: Conceptual2) Which of the following statements regarding the timeline is FALSE?A) Date 1 is one year from now.B) The $5000 below date 1 is the payment you will receive at the end of the first year.C) The $5000 below date 2 is the payment you will receive at the beginning of the second year.D) Date 0 represents today.Answer: CDiff: 2Section: 4.1 The TimelineSkill: Definition3) Which of the following statements regarding the timeline is FALSE?A) Date 1 is the end of the first year.B) Date 0 is the beginning of the first year.C) The space between date 0 and date 1 represents the time period between two specific dates.D) You will find the timeline most useful in tracking cash flows if you interpret each point on the timeline as a period or interval of time.Answer: DDiff: 2Section: 4.1 The TimelineSkill: DefinitionUse the information for the question(s) below.Joe just inherited the family business, and having no desire to run the family business, he has decided to sell it to an entrepreneur. In exchange for the family business, Joe has been offered an immediate payment of $100,000. Joe will also receive payments of $50,000 in one year, $50,000 in two years, and $75,000 in three years. The current market rate of interest for Joe is 6%.4) Draw a timeline detailing Joe's cash flows from the sale of the family business.Answer:Diff: 2Section: 4.1 The TimelineSkill: Conceptual5) You have been offered the following investment opportunity, if you pay $2500 today, you will receive $1000 at the end of each of the next three years. Draw a timeline detailing this investment opportunity.Answer:Diff: 1Section: 4.1 The TimelineSkill: ConceptualUse the table for the question(s) below.Year A B0 -$150 -$2251 40 1752 80 1253 100 -506) Draw a timeline detailing the cash flows from investment "A." Answer:Diff: 1Section: 4.1 The TimelineSkill: Conceptual7) Draw a timeline detailing the cash flows from investment "B." Answer:Diff: 1Section: 4.1 The TimelineSkill: ConceptualUse the information for the question(s) below.Suppose that a young couple has just had their first baby and they wish to ensure that enough money will be available to pay for their child's college education. Currently, college tuition, books, fees, and other costs, average $12,500 per year. On average, tuition and other costs have historically increased at a rate of 4% per year.8) Assume that college costs continue to increase an average of 4% per year and that all her college savings are invested in an account paying 7% interest. Draw a timeline that details the amount of money she will need to have in the future four each of her four years of her undergraduate education.Answer:18 19 20 2125,322.71 $25,322.71(1.)1$25,322.71(1.04)2$25,322.71(1.04)3Note that the tuition for the first year is calculated as: $12,500(1.04)18 = $25,322.71Diff: 2Section: 4.1 The TimelineSkill: Conceptual9) Suppose that a young couple has just had their first baby and they wish to insure that enough money will be available to pay for their child's college education. They decide to make deposits into an educational savings account on each of their daughter's birthdays, starting with her first birthday. Assume that the educational savings account will return a constant 7%. The parents deposit $2000 on their daughter's first birthday and plan to increase the size of their deposits by 5% each year. Draw a timeline that details the amount that would be available for the daughter's college expenses on her 18th birthday.Answer:Diff: 2Section: 4.1 The TimelineSkill: Analytical4.2 The Three Rules of Time Travel1) Which of the following statements is FALSE?A) The process of moving a value or cash flow forward in time is known as compounding.B) The effect of earning interest on interest is known as compound interest.C) It is only possible to compare or combine values at the same point in time.D) A dollar in the future is worth more than a dollar today.Answer: DExplanation: D) A dollar in the future is worth less than a dollar today.Diff: 1Section: 4.2 The Three Rules of Time TravelSkill: Conceptual2) Which of the following statements is FALSE?A) Finding the present value and compounding are the same.B) A dollar today and a dollar in one year are not equivalent.C) If you want to compare or combine cash flows that occur at different points in time, you first need to convert the cash flows into the same units or move them to the same point in time.D) The equivalent value of two cash flows at two different points in time is sometimes referred to as the time value of money.Answer: AExplanation: A) Finding the present value and discounting are the same.Diff: 1Section: 4.2 The Three Rules of Time TravelSkill: Conceptual3) At an annual interest rate of 7%, the future value of $5,000 in five years is closest to:A) $3,565B) $6,750C) $7,015D) $7,035Answer: CExplanation: C) FV = PV(1 + i)N = 5000(1.07)5 = 7,012.76Diff: 1Section: 4.2 The Three Rules of Time TravelSkill: Analytical4) At an annual interest rate of 7%, the present value of $5,000 received in five years is closest to:A) $3,565B) $6,750C) $7,015D) $7,035Answer: AExplanation: A) PV = FV/(1 + i)N = 5000(/1.07)5 = 3,564.93Diff: 1Section: 4.2 The Three Rules of Time TravelSkill: AnalyticalUse the following information to answer the question(s) below.Consider the following four alternatives:1. $132 received in two years.2. $160 received in five years.3. $200 received in eight years.4. $220 received in ten years.5) The ranking of the four alternatives from most valuable to least valuable if the interest rate is 7% per year would be:A) 1, 2, 3, 4B) 4, 3, 2, 1C) 3, 4, 2, 1D) 3, 1, 2, 4Answer: DSection: 4.2 The Three Rules of Time TravelSkill: Analytical6) The ranking of the four alternatives from most valuable to least valuable if the interest rate is 6% per year would be:A) 1, 2, 3, 4B) 1, 3, 2, 4C) 4, 3, 1, 2D) 3, 4, 2, 1Answer: DSection: 4.2 The Three Rules of Time TravelSkill: AnalyticalUse the following information to answer the question(s) below.Your great aunt Matilda put some money in an account for you on the day you were born. This account pays 8% interest per year. On your 21st birthday the account balance was $5,033.83.7) The amount of money that your great aunt Matilda originally put in the account is closest to:A) $600B) $800C) $1,000D) $1,200Answer: CExplanation: C) PV = FV/(1 + i)N = 5033.83(/1.08)21 = 1,000Diff: 1Section: 4.2 The Three Rules of Time TravelSkill: Analytical8) The amount of money that would be in the account if you left the money there until your 65th birthday is closest to:A) $29,556B) $148,780C) $168,824D) $748,932Answer: BExplanation: B) FV = PV(1 + i)N = 5033.83(1.08)(65 - 21) = $148,779.85Diff: 2Section: 4.2 The Three Rules of Time TravelSkill: Analytical9) Which of the following statements is FALSE?A) The process of moving a value or cash flow backward in time is known as discounting.B) FV =C) The process of moving a value or cash flow forward in time is known as compounding.D) The value of a cash flow that is moved forward in time is known as its future value. Answer: BExplanation: B) FV = C(1 + r)nDiff: 1Section: 4.2 The Three Rules of Time TravelSkill: Conceptual10) Consider the following time line:If the current market rate of interest is 8%, then the present value of this timeline is closest to:A) $1000B) $857C) $860D) $926Answer: BExplanation: B) PV = FV/(1 + r)n = 1000/(1.08)2 = 857.34 or approximately $857Diff: 1Section: 4.2 The Three Rules of Time TravelSkill: AnalyticalIf the current market rate of interest is 10%, then the future value of this timeline is closest to:A) $666B) $500C) $605D) $650Answer: AExplanation: A) FV = PV(1 + r)n = 500(1.10)3 = 665.50 which is approximately $666 Diff: 1Section: 4.2 The Three Rules of Time TravelSkill: Analytical12) Consider the following timeline:If the current market rate of interest is 7%, then the future value of this timeline as of year 3 is closest to:A) $1720B) $1500C) $1404D) $1717Answer: AExplanation: A) FV = PV(1 + r)nFV = 500(1.07)3 + 500(1.07)2 + 500(1.07)1 = $1719.97 or approximately $1720Diff: 3Section: 4.2 The Three Rules of Time TravelSkill: AnalyticalIf the current market rate of interest is 9%, then the present value of this timeline as of year 0 is closest to:A) $492B) $637C) $600D) $400Answer: AExplanation: A) PV = FV(1 + r)n100/(1.09)1 = 91.74200/(1.09)2 = 168.34300/(1.09)3 = 231.66Sum = 491.74 which is approximately $492Diff: 3Section: 4.2 The Three Rules of Time TravelSkill: Analytical14) Consider the following timeline:If the current market rate of interest is 8%, then the value as of year 1 is closest to:A) $0B) $1003C) $540D) $77Answer: DExplanation: D) Two part problem:FV = PV(1 + r)n = 500(1.08)1 = $540PV = FV/(1 + r)n = -500/(1.08)1 = -$463So the answer is $540 + -$463 = $77Diff: 2Section: 4.2 The Three Rules of Time TravelSkill: Analytical4.3 Valuing a Stream of Cash Flows1) Consider the following timeline detailing a stream of cash flows:If the current market rate of interest is 8%, then the present value of this stream of cash flows is closest to:A) $22,871B) $21,211C) $24,074D) $26,000Answer: BExplanation: B) PV = 5000/(1.07)1 + 6000/(1.07)2 + 7000/(1.07)3 + 8000/(1.07)4 =$21,210.72Diff: 2Section: 4.3 Valuing a Stream of Cash FlowsSkill: Analytical2) Which of the following statements is FALSE?A) FV =B) PV =C) FV = C n × (1 + r)nD) Most investment opportunities have multiple cash flows that occur at different points in time. Answer: ADiff: 1Section: 4.3 Valuing a Stream of Cash FlowsSkill: Conceptual3) Consider the following timeline detailing a stream of cash flows:If the current market rate of interest is 8%, then the future value of this stream of cash flows is closest to:A) $11,699B) $10,832C) $12,635D) $10,339Answer: AExplanation: A) FV = 1000(1.08)4 + 2000(1.08)3 + 3000(1.08)2 + 4000(1.08)1 = $11,699 Diff: 2Section: 4.3 Valuing a Stream of Cash FlowsSkill: Analytical4) Consider the following timeline detailing a stream of cash flows:If the current market rate of interest is 10%, then the present value of this stream of cash flows is closest to:A) $674B) $600C) $460D) $287Answer: CExplanation: C) PV = 100/(1.10)1 + 100/(1.10)2 + 200/(1.10)3 + 200/(1.10)4 = $460Diff: 2Section: 4.3 Valuing a Stream of Cash FlowsSkill: Analytical5) Consider the following timeline detailing a stream of cashflows:If the current market rate of interest is 6%, then the future value of this stream of cash flows is closest to:A) $1,723B) $1,500C) $1,626D) $1,288Answer: AExplanation: A) FV = 100(1.06)5 + 200(1.06)4 + 300(1.06)3 + 400(1.06)2 + 500(1.06)1 = $1723Diff: 2Section: 4.3 Valuing a Stream of Cash FlowsSkill: AnalyticalUse the following timeline to answer the question(s) below.0 1 2 3$600 $1,200 $1,8006) At an annual interest rate of 7%, the future value of this timeline in year 3 is closest to:A) $3,295B) $3,600C) $3,770D) $4,035Answer: CExplanation: C) FV = PV(1 + i)N = $600(1.07)2 + 1,200(1.07)1 + 1,800 = 3,770.94Diff: 2Section: 4.3 Valuing a Stream of Cash FlowsSkill: Analytical7) At an annual interest rate of 7%, the present value of this timeline in year 0 is closest to:A) $3,080B) $3,600C) $3,770D) $4,035Answer: AExplanation: A) PV = FV/(1 + i)N = $600/(1.07)1 + 1,200/(1.07)2 + 1,800/(1.07)3 = 3,078.21 Diff: 2Section: 4.3 Valuing a Stream of Cash FlowsSkill: Analytical8) At an annual interest rate of 7%, the future value of this timeline in year 2 is closest to:A) $3,080B) $3,525C) $3,770D) $4,035Answer: BExplanation: B) FV year 2 = $600(1.07)1 + 1,200 + 1,800/(1.07)1 = 3,524.24Diff: 3Section: 4.3 Valuing a Stream of Cash FlowsSkill: Analytical9) Taggart Transcontinental currently has a bank loan outstanding that requires it to make three annual payments at the end of the next three years of $1,000,000 each. The bank has offered to allow Taggart Transcontinental to skip making the next two payments in lieu of making one large payment at the end of the loan's term in three years. If the interest rate on the loan is 6%, then the final payment that the bank will require to make Taggart Transcontinental indifferent between the two forms of payments is closest to:A) $2,673,000B) $3,000,000C) $3,184,000D) $3,375,000Answer: CExplanation: C) FV = PV(1 + i)N = $1,000,000(1.06)2 + 1,000,000(1.06)1 + 1,000,000 = 3,183,600Diff: 2Section: 4.3 Valuing a Stream of Cash FlowsSkill: AnalyticalUse the information for the question(s) below.Joe just inherited the family business, and having no desire to run the family business, he has decided to sell it to an entrepreneur. In exchange for the family business, Joe has been offered an immediate payment of $100,000. Joe will also receive payments of $50,000 in one year, $50,000 in two years, and $75,000 in three years. The current market rate of interest for Joe is 6%.10) In terms of present value, how much will Joe receive for selling the family business? Answer: PV = $100,000 + $50,000/(1.06)1 + $50,000/(1.06)2 + $75,000/(1.06)3 = $254,641 Diff: 2Section: 4.3 Valuing a Stream of Cash FlowsSkill: Analytical4.4 Calculating the Net Present ValueUse the following information to answer the question(s) below.Nielson Motors is considering an opportunity that requires an investment of $1,000,000 today and will provide $250,000 one year from now, $450,000 two years from now, and $650,000 three years from now.1) If the appropriate interest rate is 10%, then the NPV of this opportunity is closest to:A) ($88,000)B) $88,000C) $300,000D) $1,300,000Answer: BExplanation: B) NPV = -1,000,000 + 250,000/(1.10)1 + 450,000/(1.10)2 + 650,000/(1.10)3 = 87,528.17Diff: 2Section: 4.4 Calculating the Net Present ValueSkill: Analytical2) If the appropriate interest rate is 10%, then Nielson Motors should:A) invest in this opportunity since the NPV is positive.B) not invest in this opportunity since the NPV is positive.C) invest in this opportunity since the NPV is negative.D) not invest in this opportunity since the NPV is negative.Answer: AExplanation: A) NPV = -1,000,000 + 250,000/(1.10)1 + 450,000/(1.10)2 + 650,000/(1.10)3 = 87,528.17Invest since positive NPVDiff: 2Section: 4.4 Calculating the Net Present ValueSkill: Analytical3) If the appropriate interest rate is 15%, then Nielson Motors should:A) invest in this opportunity since the NPV is positive.B) not invest in this opportunity since the NPV is positive.C) invest in this opportunity since the NPV is negative.D) not invest in this opportunity since the NPV is negative.Answer: DExplanation: D) NPV = -1,000,000 + 250,000/(1.15)1 + 450,000/(1.15)2 + 650,000/(1.15)3 = -14,958.49Do Not Invest since negative NPVDiff: 2Section: 4.4 Calculating the Net Present ValueSkill: Analytical4) Kampgrounds Inc. is considering purchasing a parcel of wilderness land near a popular historic site. Although this land will cost Kampgrounds $400,000 today, by renting out wilderness campsites on this land, Kampgrounds expects to make $35,000 at the end of every year indefinitely. If the appropriate discount rate is 8%, then the NPV of this new wilderness campsite is closest to:A) -$50,000B) -$37,500C) $37,500D) $50,000Answer: CExplanation: C) NPV = -400,000 + $35,000/.08 = 37,500Diff: 1Section: 4.4 Calculating the Net Present ValueSkill: Analytical5) Wyatt oil is considering drilling a new self sustaining oil well at a cost of $1,000,000. This well will produce $100,000 worth of oil during the first year, but as oil is removed from the well the amount of oil produced will decline by 2%, per year forever. If the Wyatt oil's appropriate interest rate is 8%, then the NPV of this oil well is closest to:A) -$250,000B) $0C) $250,000D) $1,000,000Answer: BExplanation: B) NPV = -1,000,000 + $100,000/(.08 - (-.02)) = $0Diff: 2Section: 4.4 Calculating the Net Present ValueSkill: Analytical4.5 Perpetuities and Annuities1) Which of the following statements regarding perpetuities is FALSE?A) To find the value of a perpetuity one cash flow at a time would take forever.B) A perpetuity is a stream of equal cash flows that occurs at regular intervals and lasts forever.C) PV of a perpetuity =D) One example of a perpetuity is the British government bond called a consol.Answer: CExplanation: C) PV of a perpetuity =Diff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: Conceptual2) Which of the following statements regarding annuities is FALSE?A) PV of an annuity = C ×B) The difference between an annuity and a perpetuity is that a perpetuity ends after some fixed number of payments.C) An annuity is a stream of N equal cash flows paid at regular intervals.D) Most car loans, mortgages, and some bonds are annuities.Answer: BExplanation: B) A perpetuity never ends.Diff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: Conceptual3) Which of the following statements regarding growing perpetuities is FALSE?A) We assume that r < g for a growing perpetuity.B) PV of a growing perpetuity =C) To find the value of a growing perpetuity one cash flow at a time would take forever.D) A growing perpetuity is a cash flow stream that occurs at regular intervals and grows at a constant rate forever.Answer: ADiff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical4) Which of the following statements regarding growing annuities is FALSE?A) A growing annuity is a stream of N growing cash flows, paid at regular intervals.B) We assume that g < r when using the growing annuity formula.C) PV of a growing annuity = C ×D) A growing annuity is like a growing perpetuity that never comes to an end.Answer: DExplanation: D) An annuity does end.Diff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: Conceptual5) Which of the following statements is FALSE?A) The difference between an annuity and a perpetuity is that an annuity ends after some fixed number of payments.B) Most car loans, mortgages, and some bonds are annuities.C) A growing perpetuity is a cash flow stream that occurs at regular intervals and grows at a constant rate forever.D) An annuity is a stream of N equal cash flows paid at irregular intervals.Answer: DExplanation: D) annuities are paid at regular intervals.Diff: 2Section: 4.5 Perpetuities and AnnuitiesSkill: Conceptual6) Which of the following formulas is INCORRECT?A) PV of a growing annuity = C ×B) PV of an annuity = C ×C) PV of a growing perpetuity =D) PV of a perpetuity =Answer: AExplanation: A) PV of a growing annuity = C ×Diff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: ConceptualUse the information for the question(s) below.Suppose that a young couple has just had their first baby and they wish to ensure that enough money will be available to pay for their child's college education. Currently, college tuition, books, fees, and other costs, average $12,500 per year. On average, tuition and other costs have historically increased at a rate of 4% per year.7) Assuming that costs continue to increase an average of 4% per year, tuition and other costs for one year for this student in 18 years when she enters college will be closest to:A) $12,500B) $21,500C) $320,568D) $25,323Answer: DExplanation: D) FV = PV (1 + i )N = $12,500(1.04)18 = $25,322.71Diff: 2Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical8) Assuming that college costs continue to increase an average of 4% per year and that all her college savings are invested in an account paying 7% interest, then the amount of money she will need to have available at age 18 to pay for all four years of her undergraduate education is closest to:A) $97,110B) $107,532C) $101,291D) $50,000Answer: AExplanation: A) This is a two step problem.Step #1 determine the cost of the first year of college.FV = PV (1 + i )N = $12,500(1.04)18 = $25,322.71Step #2 figure out the value for four years of college.PV of a growing annuity due = C ×(1 + r ) = $25,322.71 × ⎪⎪⎪⎪⎭⎫ ⎝⎛-⎪⎭⎫ ⎝⎛++07.104.141(1 + .07) = $97,110.01 Diff: 3Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical9) The British government has a consol bond outstanding that pays ₤100 in interest each year. Assuming that the current interest rate in Great Britain is 5% and that you will receive your first interest payment one year from now, then the value of the consol bond is closest to:A) ₤1000B) ₤1100C) ₤2100D) ₤2000Answer: DExplanation: D) PVP = C/r = 100/.05 = 2000Diff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical10) The British government has a consol bond outstanding that pays ₤100 in interest each year. Assuming that the current interest rate in Great Britain is 5% and that you will receive your first interest payment immediately upon purchasing the consol bond, then the value of the consol bond is closest to:A) ₤2000B) ₤2100C) ₤1000D) ₤1100Answer: BExplanation: B) PVP = C/r= 100/.05 = 2000 + 100 immediate interest payment = ₤2100 Diff: 2Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical11) If the current rate of interest is 8%, then the present value of an investment that pays $1000 per year and lasts 20 years is closest to:A) $18,519B) $45,761C) $9,818D) $20,000Answer: CExplanation: C) PV = C/r (1 - (1 + r)-N) = 1000/.08 (1 - (1 + 0.08)-20)PV = $9,818Diff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical12) If the current rate of interest is 8%, then the future value 20 years from now of an investment that pays $1000 per year and lasts 20 years is closest to:A) $45,762B) $36,725C) $9,818D) $93,219Answer: AExplanation: A) FV = C/r((1+r)N -1) = 1000/0.08((1+0.08)20 - 1)FV = $45,762Diff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical13) Suppose that a young couple has just had their first baby and they wish to insure that enough money will be available to pay for their child's college education. They decide to makedeposits into an educational savings account on each of their daughter's birthdays, starting with her first birthday. Assume that the educational savings account will return a constant 7%. The parents deposit $2000 on their daughter's first birthday and plan to increase the size of their deposits by 5% each year. Assuming that the parents have already made the deposit for their daughter's 18th birthday, then the amount available for the daughter's college expenses on her 18th birthday is closest to:A) $42,825B) $97,331C) $67,998D) $103,063Answer: BExplanation: B) FV of a growing annuity$2,000 × ⎪⎪⎪⎪⎭⎫ ⎝⎛-⎪⎭⎫ ⎝⎛++07.105.1181(1.07)18 = $97,331 Diff: 2Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical14) Since your first birthday, your grandparents have been depositing $1000 into a savings account on every one of your birthdays. The account pays 4% interest annually. Immediately after your grandparents make the deposit on your 18th birthday, the amount of money in your savings account will be closest to:A) $25,645B) $36,465C) $12,659D) $18,000Answer: AExplanation: A) FV = C/r((1+r)N -1) = 1000/0.04((1+0.04)18 - 1)FV = $25,645Diff: 2Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical15) Consider a growing perpetuity that will pay $100 in one year. Each year after that, you will receive a payment on the anniversary of the last payment that is 6% larger than the last payment. This pattern of payments will continue forever. If the interest rate is 11%, then the value of this perpetuity is closest to:A) $1,667B) $588C) $2,000D) $909Answer: CExplanation: C) PV growing Perpetuity = C/r - g = 100/(.11 - .06) = $2000Diff: 1Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical16) You are thinking about investing in a mine that will produce $10,000 worth of ore in the first year. As the ore closest to the surface is removed it will become more difficult to extract the ore. Therefore, the value of the ore that you mine will decline at a rate of 8% per year forever. If the appropriate interest rate is 6%, then the value of this mining operation is closest to:A) $71,429B) $500,000C) $166,667D) This problem cannot be solved.Answer: AExplanation: A) PVP = C/r - g = 10,000/(.06 - -.08) = 10,000/.14 = $71,429Diff: 3Section: 4.5 Perpetuities and AnnuitiesSkill: AnalyticalUse the information for the question(s) below.Assume that you are 30 years old today, and that you are planning on retirement at age 65. Your current salary is $45,000 and you expect your salary to increase at a rate of 5% per year as long as you work. To save for your retirement, you plan on making annual contributions to a retirement account. Your first contribution will be made on your 31st birthday and will be 8% of this year's salary. Likewise, you expect to deposit 8% of your salary each year until you reach age 65. Assume that the rate of interest is 7%.17) The present value (at age 30) of your retirement savings is closest to:A) $87,000B) $108,000C) $46,600D) $75,230Answer: AExplanation: A) First deposit = .08 × $45,000 = $3,600$3,600 × ⎪⎪⎪⎪⎭⎫ ⎝⎛-⎪⎭⎫ ⎝⎛++07.105.1351 = $87,003Diff: 2Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical18) The future value at retirement (age 65) of your savings is closest to:A) $497,530B) $928,895C) $1,263,236D) $108,000Answer: BExplanation: B) First deposit = .08 × $45,000 = $3,600$3,600 × ⎪⎪⎪⎪⎭⎫ ⎝⎛-⎪⎭⎫ ⎝⎛++07.105.1351(1.07)35 = $928,895 or PVA (growing) = $3,600 × ⎪⎪⎪⎪⎭⎫ ⎝⎛-⎪⎭⎫ ⎝⎛++07.105.1351= $87,003FV = PV (1 + i )N = $87,003(1.07)35 = $928,895Diff: 2Section: 4.5 Perpetuities and AnnuitiesSkill: Analytical。

CFA考试投资分析的数量方法投资工具

第一章:货币的时间价值Chapter ⒈ The Time Value of Money§⒈解释利息率是对投资者的不同风险予以回报的实际无风险利率和风险溢价的总和利息率和折现率(Interest Rates and Discount Rates)货币时间价值概念的基础:收益率(rates of return)、利息率(interest rate)、要求的收益率(required rates of return)、折现率(discount rates)、机会成本(opportunity costs)、通货膨胀(inflation)和风险(risk)。

货币的时间价值,反映了时间、现金流量和利息率三者之间的关系。

投资者偏好现在消费。

利息率是投资者推迟现在消费的回报。

在确定世界,利息率被认为是无风险(risk-free)利率。

一般是国家的短期债券,如美国的国库券(Treasury-bills, T-bills)。

在不确定的世界,有两个因素影响利息率:①通货膨胀。

贷款者承担通货溢价(inflation premium)和推迟消费的机会成本。

因此,货币的名义成本(nominal cost of money),由实际利率(real rate)和通货溢价组成。

②风险。

贷款者还承担了不履行风险(default risk)。

因此,利息率包括:名义的无风险利率和不履行风险溢价。

利息率的意义:①收益要求率。

即促使投资者放弃现在消费所要求的收益。

②折现率(利息率和折现率可以交互使用)。

③机会成本。

即投资者按某一选择行为而放弃其他选择所失去的价值。

影响利息率最重要的因素是:资金的供求关系。

§⒉计算整笔现金的终值(FV)和现值(PV)单一现金流量的终值(The Future Value of a Single Cash Flow)整笔现金流(或lump-sum investment)的终值计算公式(N的初值为0):基本概念:①简单利息(simple interest),即利息率乘原始本金。

财务管理专业英语-The Time Value of Money

5 years: PV = 500 / (1.1)5 = 310.46 10 years: PV = 500 / (1.1)10 = 192.77

4

Effects of Compounding

Simple interest Compound interest Consider the previous example

FV with simple interest = 1000 + 50 + 50 = 1100 FV with compound interest = 1102.50 The extra 2.50 comes from the interest of .05(50)

12

PV – One Period Example

Suppose you need $10,000 in one year for the down payment on a new car. If you can earn 7% annually, how much do you need to invest today?

8

Future Values – Example 3

Suppose you had a relative deposit $10 at 5.5% interest 200 years ago. How much would the investment be worth today?

FV = 10(1.055)200 = 447,189.84

16

topic1

Topic 1: Relationship Between Risk and ReturnBUS 442 Investment Theory and Portfolio ManagementOne of the most important concepts in investment theory is the relationship between risk and return. It is this relationship that drives the theoretical foundation of many investment models (such as the Capital Asset Pricing Model). Before we begin our discussion on the development of theoretical models that attempt to “capture” the relationship between risk and return, we need to first understand how these two variables (or measurements) are determined.1. (Rate of) ReturnIn your own words, explain what rate of return represents and why it is so important to an investor?One of the measurements of return is the holding period return (HPR), which represents the return an investor received for holding an investment for a certain amount of time. The formula for determining the HPR is as follows:pricePurchase income Current gain/loss Capital price Purchase income Current price) Purchase price (Sale +=+-=HPRFrom the above formula, it is clear that the HPR is dependent on two components:(a) Capital gain/loss(b) Current incomeRefer to In-class Example 1It is important to understand that the HPR is an ex-post return, i.e. a return that has already taken place. It is sometimes known as the historical return. Another thing that you should be aware of is that the HPR is a measurement for return over a single period (i.e. 4 months, 5 years, etc.)What happen if you needed to determine the investment returns over multiple periods? In other words, what if you are interested in the average returns of an investment over a number of quarters or years? There are three different measures for average returns: (a) arithmetic average, (b) geometric average, and (c) dollar-weighted average return. It is important for you to understand the advantages and disadvantages for each of the three return measurements.(a)Arithmetic average(i)Advantage(ii)Disadvantage(b)Geometric average(i)Advantage(ii)Disadvantage(c)Dollar-weighted average return(i)Advantage(ii)DisadvantageRefer to In-class Example 2In order to compare the performances among different investments, it is important to make sure that you are doing so on equal terms. In other words, you need to “compare apples with apples”. One way to do this is to annualize all your returns before making the comparisons. There are two common annualized returns: (a) annual percentage rates (APR) and (b) effective annual rate (EAR).(a) Annual percentage rate (APR)Explain how the APR of an investment is determined. What does this measurement ignored?(b) Effective annual rate (EAR)Explain the difference between APR and EAR.The relationship between the EAR and the APR of an investment can be expressed with the formula as follows:nn APR EAR ⎪⎭⎫ ⎝⎛+=+11where n = number of compounding period per year.Keep in mind that the formula has to be “modified” when you are dealing with continuous compounding. In this case, the relationship between EAR and APR is determined by the formula as follows:1-=APR e EARRefer to In-class Example 32. Uncertainty and its Impact on ReturnWhen it comes to investments, there are always some levels of uncertainty associated with future holding period returns. Such uncertainty is commonly known as the risk of the investment.What cause s the uncertainty (or volatility) of an investment’s returns? The answer depends on the nature of the investment, the performance of the economy, and other factors. In other words, when you “dissect” the uncertainty of an investment’s return, you will real ize that it is made up of different components. The following are some of the components:(a) Business risk : This is the uncertainty regarding the earnings (or profitability) of a firm as a result ofchanges in demand, input prices, and technological obsolescence.(b) Default risk : This is the uncertainty regarding an issuing firm’s ability to pay interest, principal, etc. on itsdebt instruments.(c) Inflation risk : This is the uncertainty over future rates of inflation. If the return from an investment is barelykee ping up with the rate of inflation, an investor’s purchasing power will be eroded as time goes on. In other words, the investor will receive a lesser amount of purchasing power than what was originally invested because the cost of buying everything has gone up. Inflation risk is also known as purchasing power risk .(d) Market risk : This represents the changes in an investment’s price (or market value) as a result of an eventthat affects the entire market. An example is the impact of a market correction or a market crash on an investment’s return.(e) Interest rate risk : This represents the fluctuation in the value of an investment when market interest ratechanges. This has a big impact on interest-paying investments because as market interest rate rises (falls), a n investor’s money is tied up in a bond that pay less (more) than the going rate, and hence the value of the investor’s bond decreases (increases).(f) Liquidity risk : This is the risk of not being able to sell an investment immediately with a reasonable price. (g) Political risk : This is caused by changes in the political environment that affect an investment’s marketvalue. Political risk can be classified as either domestic or foreign political risk. An example of domestic political risk is a change in the tax laws, and an example of foreign political risk is a change in a foreign government’s policy regarding capital outflow.(h) Callability risk : This is the risk that an investment is recalled (or retired) prior to the original stated date.This type of risk is most applicable to long-term bonds and preferred stocks. This usually happens when the issuing firms find the market conditions favorable in “refinancing” such investments.(i) Exchange rate risk : This is the uncertainty regarding the changes in exchange rates that might affect thevalue of an investment. Exchange rate uncertainty has an impact on both domestic and foreign investments. Why is this the case?It is important to understand that the components of risk present and the “size” of each component differ f rom one investment to another investment. For example, certain investments have no liquidity risk while other investments have extremely high level of liquidity risk.Now that you knew more about the concept of risk, how do we measure it? We can determine the risk of an investment using the scenario analysis approach. This approach is based on an investment’s expected return rather than its historical return.In your own words, explain what the expected return represents (or measures).The expected return of an investment can be determined using the following formula:)(...)()(][)(2211n n i i p r p r p r p r r E ⨯++⨯+⨯=⨯=∑where i p = probability of a given scenario and n = the number of scenarios.The above formula should look familiar to you since you would have encountered it in statistics and introductory finance courses. Now that you are once again comfortable with the formula to calculate the expected return, lets take a look at a slightly more complex formula for calculating the standard deviation, which is a common measurement for risk.[][]22)()(r E p r i i -⨯=∑σIt is easier to understand the concept of standard deviation when we look at the distribution curve of the returns of an asset. The following graph depicts the distribution curves of the returns of two assets, A and B, which have the same expected return.Frequency Return Mean Asset AAsset BWe know the standard deviation measures how far the returns deviate from the asset’s average return. In the preceding graph, we know that the standard deviation of Asset B is greater than that of Asset A because we can visually verify that the returns of Asset B deviate more from its mean return. Another way to compare the volatility (or standard deviation) of two assets is to look at the shapes of the distribution curves. The flatter (or more spread out) the curve, the more volatile the returns; and the narrower the curve, the less volatile the returns.Refer to In-class Example 4It is important to understand that the formula above is an ex-ante formula. In other words, it tries to “predict” the volatility of a particular investment’s returns in the future. However, it is also crucial to analyze how the investment had behaved in the past. In order to accomplish this, we will need to analyze the volatility of the investment’s historical return.The concepts behind standard deviations based on expected returns and historical returns are very similar. They both look at the average deviation of the returns from the investment’s average return. The only differ ence is that one uses the expected return for the average return while the other uses average historical return for the average return (which is denoted by x ). The following is the formula for calculating the standard deviation based on historical returns:[]122--=∑n x n x sIt is important to note that most investors use a small sample of an investment’s historical returns to determine its volatility. As a result, we will be determining the standard deviation of an investment’s return based on a sample rather than the population. In other words, we are solving for the sample standard deviation, and this is usually denoted by s rather than σ (as indicated by the formula above).Refer to In-class Example 5。

cbok完整版

CANDIDATE BODY OF KNOWLEDGE TMThe CFA curriculum is grounded in the practice of the investment profession. CFA Institute periodically conducts a job analysis involving CFA charterholders around the world to determine those elements of the body of investment knowledge and skills that are important to charterholders in their practice. The most recent job analysis was completed in 2001. The survey results define the Candidate Body of Knowledge (CBOK TM) and to determine how much emphasis each of the major topic areas receives on the CFA examinations.The CBOK is organized into four major topic areas: ethical and professional standards, tools and inputs for investment valuation and management, asset valuation, and portfolio management and performance presentation.Two features of the CBOK are especially relevant to the CFA examinations. First, the curriculum for each level of the CFA Program is organized primarily around a functional area: The Level I study program emphasizes tools and inputs and includes an introduction toasset valuation and portfolio management techniques.The Level II study program emphasizes asset valuation and includes applications of the tools and inputs (including economics, financial statement analysis, and quantitativemethods) in asset valuation.The Level III study program emphasizes portfolio management and includes strategiesfor applying the tools, inputs, and asset valuation models in managing equity, fixedincome, and derivative investments for individuals and institutions.Second, because they are an integral part of the other three functional areas of investment management, ethical and professional standards are covered at all three levels of the curriculum.CFA® CANDIDATE BODY OF KNOWLEDGERevised 2001I.ETHICAL AND PROFESSIONAL STANDARDSA.Professional Standards of Practice1.The Code of Ethics2.Standards of Professional Conducta.Standard I: Fundamental responsibilitiesb.Standard II: Relationships with and responsibilities to the profession(1)Use of professional designation(2)Professional misconduct(3)Prohibition against plagiarismc.Standard III: Relationships with and responsibilities to the employer(1)Obligation to inform employer of code and standards(2)Duty to employer(3)Disclosure of conflicts to employer(4)Disclosure of additional compensation arrangements(5)Responsibilities of supervisorsd.Standard IV: Relationships with and responsibilities to clients and prospects(1)Reasonable basis and representations(2)Research reports(3)Independence and objectivity(4)Fiduciary duties(5)Portfolio investment recommendations and actions(6)Fair dealing(7)Priority of transactions(8)Preservation of confidentiality(9)Prohibition against misrepresentation(10) Disclosure of conflicts to clients and prospects(11) Disclosure of referral feese.Standard V: Relationships with and responsibilities to the investing public(1)Prohibition against use of material nonpublic information(2)Performance presentation3.Disciplinary sanctions for violationsB.Topical Issues1.Corporate governance2.Soft dollar standards3.Fiduciary duty4.Insider tradinga.Mosaic Theoryb.Selective disclosure vs. full disclosure5.Personal investingII.QUANTITATIVE METHODSA.Time Value of Money1.Future value of a single cash flowa.Calculating the future value of a single cash flowb.Frequency of compoundingc.Continuous compoundingd.Annual and effective interest rates2.Future value of a series of cash flowsa.Equal cash flows(1)Ordinary annuity(2)Annuity dueb.Unequal cash flows3.Present value of a single cash flowa.Calculating the present value of a single cash flowb.Frequency of compounding4.Present value of a series of cash flowsa.Calculating the present value of a series of equal cash flows(1)Ordinary annuity(2)Annuity dueb.Present value of a series of unequal cash flowsc.Present value of an infinite series of equal cash flows (perpetuity)5.Equivalence of present and future value6.Other applications of the time value of moneya.Solving for interest rates and growth ratesb.Solving for the number of periodsc.Solving for the size of annuity payments7.Discounted cash flow analysis present value ruleb.Internal rate of return rulec.Problems with the internal rate of return rule8.Simple interest and money-market conventionsa.Bank-discount yieldb.Periodic yieldc.Bond-equivalent yieldd.Effective annual yielde.CD-equivalent yield9.Investment measures of returna.Dollar-weighted rate of returnb.Time-weighted rate of returnB.Basic Statistical Concepts1.Nature of statisticsa.Populations and samplesb.Types of statistical data(1)Nominal data(2)Ordinal data(3)Interval data(4)Ratio data2.Frequency distributions3.Measures of central tendencya.Population meanb.Sample meanc.Mediand.Modee.Quartiles, quintiles, deciles, and percentilesf.Weighted meang.Geometric mean(1)Geometric mean return(2)Relationship to arithmetic mean return4.Measures of dispersiona.Measures of absolute dispersion(1)Range(2)Mean absolute deviation(3)Variance and standard deviation(a)Population variance and standard deviation(b)Sample variance and standard deviationb.Relative dispersion5.Measures of skewness6.Measures of kurtosisC.Probability Concepts and Random Variables1.Probability conceptsa.Definitions, including outcome, event, sample space, and mutually exclusiveb.Objective probability(1)Classical probability(2)Empirical concept(3)Subjective probability2.Methods of countinga.Multiplication rule of countingb.Factorial rulec.Permutation rulebination rule3.Random variables and probabilitya.Random variableb.Univariate probability distributionc.Discrete versus continuous random variablesd.Probability density functione.Cumulative density function4.Probability theorems/axiomsa.The complement ruleb.The special rule of additionc.General rule of additiond.Rule of multiplication(1)Independent events(2)Dependent events(3)Decision trees(4)Bayes’ Theorem5.Expected value, variance, and covariance/correlationa.Expected value(1)Random variable(2)Constant times a random variable(3)Sum of random variables(4)Weighted sumb.Multivariate probability distributionc.Variance(1)Random variable(2)Constant times a random variable(3)Random variable plus a constantd.Covariance(1)Between two random variables(2)Constant times a random variablee.Correlation coefficient between two random variablesf.Covariance among more than two random variables6.Standardized random variablesmon Probability Distributions1.Discrete random variablesa.Discrete uniform distributionb.Binomial distributionc.Expected value and variance of a binomial random variable2.Continuous probability distributionsa.Uniform distributionb.Normal distributionc.Standard normal distributiond.Cumulative density for the standard normal distributione.Finding standard normal distribution areasf.Confidence intervalsg.Mean-variance portfolio selectionh.Monte Carlo simulation3.Lognormal distributiona.Lognormal stock pricesb.Price relativesE.Sampling and Estimation1.Random samplesa.Sampling in investment analysisb.Time series and cross-sectional datac.Data-snooping biasd.Sample selection bias(1)Survivorship bias(2)Delisting bias2.Distribution of the sample mean3.Point and interval estimates of the population meana.Point estimatorsb.Confidence intervals when sampling from a normal distribution with knownvariancec.Confidence intervals when sampling from a normal distribution with unknownvarianceing t distribution tablese.Confidence intervals when sampling from a non-normal populationF.Statistical Inference and Hypothesis Testing1.Establishing hypothesesa.Null hypothesisb.Alternative hypothesis2.Testing hypothesesa.Test criterionb.Two-tail testsc.One-tail testsd.Type I error (rejecting a true null hypothesis)e.Type II error (failing to reject a false null hypothesis)3.Types of hypothesis testinga.Testing the mean of a single sample when the population standard deviation is notknownb.Testing the difference between the population means of two samples(1)Population variances are known(2)Population variances are not known but assumed equal(3)Dependent samples: paired datac.Testing the proportion of a single sample: significance tests with small samplesd.Significance tests and confidence intervals for a single variance(1)Confidence interval for the sample variance(2)Hypothesis test about a single population variance(3)Testing the equality of two variances: the F-distribution4.Analysis of variance (ANOVA)a.Single-Factor analysis of varianceb.F-test for equality of factor-level meansputing sums of squaresd.Degrees of freedomG.Correlation Analysis and Linear Regression1.Correlation analysisa.Scatter plots and correlation analysisputing the correlation coefficientc.Testing the significance of the correlation coefficient2.Linear regressiona.Linear regression with one independent variableb.Assumptions of the linear regression modelc.Standard error of estimated.Coefficient of determinatione.Confidence intervals and testing hypotheses(1)Significance level(2)Standard error of the estimated coefficient(3)Critical value for rejecting the null hypothesisf.Prediction intervalsg.Limitations to regression analysisH.Multivariate Regression1.Multiple linear regressiona.Assumptions of the multiple linear regression modelb.Standard error of estimate in multiple linear regressionc.Predicting the dependent variable in a multiple regression modeld.Testing whether all the regression coefficients are equal to zeroing dummy variables in regressions3.Heteroskedasticitya.Types of heteroskedasticityb.Tests that evaluate heteroskedasticityc.Correcting for heteroskedasticity4.Serial correlation and Durbin-Watson testa.Consequences of serial correlationb.Durbin-Watson statistic to test for serial correlationc.Correcting for serial correlationd.Generalized least squares5.Multicollinearity6.Models with qualitative dependent variablesI.Time Series Analysis1.Trends2.Limitations to trends3.Fundamental issues in time series4.Autoregressive time series modelsa.Mean reversionb.Multiperiod forecastsc.Instability of regression coefficients5.Random walks and unit roots6.Moving-average time series modelsa.Smoothing past values with a moving averageb.Moving average models for forecasting7.Seasonality in time-series modelsJ.Portfolio Concepts1.Optimal portfolios with three assets2.Minimum Variance Frontier for many assets3.Instability in the Minimum Variance Frontier4.Diversification and portfolio size5.Risk free assets and the trade-off between risk and return6.The Capital Allocation Line7.The Capital Asset Pricing Model (CAPM)8.Estimates based on historical means, variances and covariances9.The Market Model10.Adjusted-beta Market Models11.The structure of factor models12.Arbitrage Pricing Theory (APT) and the factor model13.Multifactor models in current practiceIII.E CONOMICSA.Market Forces of Supply and Demand1.Determinants of individual demand2.Determinants of individual supply3.Equilibrium price4.Analyzing changes in equilibrium5.How prices allocate resourcesB.Elasticity1.Determinants of price elasticity of demand2.Determinants of price elasticity of supply3.Microeconomic government policies4.Analysis of price ceilings5.Analysis of price floors6.Tax incidence7.Market efficiencyC.The Firm and Industry Organizationanization of the business firma.Basic types of business firmsb.The principal-agent problem2.Costs of productiona.Opportunity cost, explicit cost, and implicit costb.Accounting cost versus opportunity costc.The production functiond.Fixed and variable costse.Average and marginal costf.Cost curves and their shapesg.Diminishing returns and cost curvesh.Output and costs in the long run3.Firms in competitive marketsa.Definition of competitionb.Revenue of a competitive firmc.Profit maximization for the competitive firmd.Accounting profit and economic profite.The competitive firm’s supply curvef.The supply curve in a competitive market4.Monopolya.Barriers to entry (e.g., economics of scale, government licensing, patents, controlof essential resources)b.How monopolies make production and pricing decisionsc.Public policy and monopolies5.Oligopolya.Duopolyb.Equilibrium for an oligopolyc.Game theory and the economics of cooperationd.Public policy when entry barriers are high6.Monopolistic competitiona.Price and output in competitive markets with differentiated productsb.Allocative efficiency in monopolistic competitionD.Supply and Demand for Productive Resources1.Demand for resourcesa.Marginal productivity and the firm’s hiring decisionb.Supply, demand, and resource prices2.Capital marketsa.Interest ratesb.Determination of interest ratesc.Money rate versus real rate of interestd.Interest rates and riskE.Measuring National Income1.Gross Domestic Product (GDP)ponents of GDP3.Real versus nominal GDPa.GDP deflatoring the GDP deflator to derive real GDPc.The consumer price index4.Problems with GDP as a measure of national productF.Economic Fluctuations and Unemployment1.Descriptive terms in business cycle analysis2.Index of leading economic indicators3.Types of unemployment4.Problems of measuring unemploymentG.The Monetary System1.Role of a central bank2.Tools of monetary controla.Open-market operationsb.Reserve requirementsc.Discount rateH.Inflation: Causes and Consequences1.Causes of inflation2.Quantity theory of money3.Equation of exchange4.Deflation/stagflationI.International Trade1.Gains from specialization and trade2.Economics of trade restrictionsa.Economics of tariffsb.Economics of quotasc.Other nontariff barriers to traded.Exchange-rate controls as a trade restrictionJ.International Finance1.Foreign exchange marketanization of the foreign exchange marketb.The spot marketc.The forward marketd.Interest rate parity theory2.Determination of exchange ratesa.Nominal exchange ratesb.Real exchange ratesc.Purchasing-power parity3.Balance of paymentsa.Current-account transactionsb.Capital-account transactionsc.Official reserve accountK.The Macroeconomics of an Open Economy1.Supply and demand for loanable funds and for foreign-currency exchangea.The market for loanable fundsb.The market for foreign-currency exchange2.Equilibrium in the open economy foreign investment flowsernment budget deficitsc.Trade policyd.Political instability and capital flightL.Aggregate Demand and Aggregate Supply1.The aggregate demand curvea.Reasons for downward sloping aggregate demand curve (e.g., wealth effect,interest rate effect, exchange rate effect)b.Shifts in the aggregate demand curve2.The aggregate supply curvea.Short-run aggregate supply curveb.Long-run aggregate supply curvec.Shifts in the short-run aggregate supply curve3.The influence of monetary policy on aggregate demanda.Money supply and money demandb.Transmission of monetary policyc.Unanticipated expansionary monetary policyd.Unanticipated restrictive monetary policye.Timing of monetary policyf.Anticipated monetary policy4.The influence of fiscal policy on aggregate demanda.Fiscal policy and the crowding-out effectb.Problems of proper timing of fiscal policyc.Fiscal policy as a stabilization toold.Supply-side effects of fiscal policy5.Expectations and economic policya.Adaptive expectations hypothesisb.Rational expectations hypothesisc.The differences between adaptive and rational expectationsd.The implications of adaptive and rational expectationse.Activist versus nonactivist stabilization policyM.Sources of Economic Growth1.Physical capital2.Human capital3.Technological progress4.Institutional environment (e.g., property rights, political stability, competitivemarkets, stable money and price, an open economy, moderate marginal tax rates) ernment Regulation1.Regulation of business2.Costs of regulationO.Natural Resource MarketsP.Relationship of Economic Activity to the Investment ProcessIV.FINANCIAL STATEMENT ANALYSISA.Financial Reporting System1.General concepts and rules2.U.S. Generally Accepted Accounting Principles (GAAP)3.International Accounting Standards (IAS)B.Principal Financial Statements1.Balance sheeta.Format and classification (e.g., assets, liabilities, stockholders’ equity)b.Measurement of assets and liabilitieses of the balance sheet2.Income statementa.Format and classificationb.The accrual concept of incomec.Revenue and expense recognition(1)General principles(2)Percentage-of-completion method(3)Completed contract method(4)Installment method(5)Cost recovery methodd.Nonrecurring items (e.g., extraordinary items, unusual items, restructuringcharges, discontinued operations, changes in accounting standards, disclosure ofnonrecurring items, analysis of nonrecurring items)e.Earnings qualityf.Earnings per share3.Statement of cash flowsa.Direct and indirect method cash flow statementsb.Preparing a direct method statement of cash flows (e.g., cash flow fromoperations, investing cash flow, financing cash flow)c.Indirect methodd.Reported versus observed changes in assets and liabilities (e.g., acquisitions anddivestitures, translation of foreign subsidiaries)e.Analysis of cash flow information4.Statement of stockholders’ equitya.Format, classification, and usesb.Other comprehensive income5.Other sources of financial informationa.Letter to shareholdersb.Footnotesc.Management discussion and analysisd.Segment/disaggregated informatione.Operating and performance dataf.Forward looking information/plansg.Role of the auditorh.Annual report to regulators (e.g., Form 10K in U.S.)i.Proxy statementj.Change in material status report (e.g., Form 8K in U.S.)k.Quarterly reportsl.News releasesC.Earnings Quality and Nonrecurring Items1.Earnings qualitya.Stock optionsb.Revenue recognitionc.Assumptionsd.Reserves2.Nonrecurring itemsa.Extraordinary itemsb.Restructuring chargesc.Unusual itemsD.Analysis of Inventories1.Relationship between inventory and cost of goods solda.Stable pricesb.Rising prices2.Inventory methodsa.Specific identificationb.First-in, first-out (FIFO)c.Average costst-in, first-out (LIFO)e.Adjustment from LIFO to FIFO(1)Adjustment of inventory balances(2)Adjustment of cost of goods soldf.Adjustment of income to current cost incomeg.Effect of LIFO/FIFO choice on financial ratios (e.g., profitability, liquidity,activity, solvency)h.Analysis implications of changes to and from LIFOparison of companies using different inventory valuation methodsj.International comparisons of inventory accounting methodsE.Analysis of Long-Lived Assets1.Capitalization versus expensinga.Financial statement effects of capitalization (e.g., income variability, profitability,cash flow from operations, leverage ratios)b.Capitalization of interest costsc.Intangible assets (e.g., research and development, patents and copyrights,franchises and licenses, brands and trademarks, goodwill)d.Asset revaluatione.International differencesf.Adjustments for capitalization and expensingg.Need for analytic adjustments2.Depreciation methodsa.Alternatives (e.g., annuity or sinking fund depreciation, straight line depreciation,accelerated depreciation)b.Depletionc.Amortizationd.Depreciation method disclosurese.Impact of depreciation methods on financial statementsf.Accelerated depreciation and taxesg.Impact of inflation on depreciationh.Changes in depreciation method3.Analysis of fixed asset disclosures4.Impairment of long-lived assets5.Retirement of long-term assets6.Liabilities for closure and environmental costsF.Analysis of Income Taxes1.Issues in tax and financial reporting2.Deferred tax assets and liabilitiesa.Accounting for deferred taxesb.Analysis of deferred tax assetsc.Non-U.S. financial reporting (e.g., IASC standards)G.Analysis of Financing Liabilities1.Analysis of balance sheet debta.Analysis of current liabilitiesb.Analysis of long-term debtc.Analysis of debt with equity features (e.g., convertible bonds, warrants,commodity bonds, perpetual debt, preferred stock)d.Analysis of changes in interest rates (e.g., estimating the market value of a firm’sdebt)e.Retirement of debt prior to maturity2.Bond covenants3.International accounting and reporting practices for balance sheet debtH.Analysis of Leases1.Incentives for leasing2.Lease classification issues from lessee perspective (e.g., capital lease, operating lease)3.Financial reporting by lessees4.Financial reporting by lessors5.Financial reporting for sales with leasebacksI.Analysis of Off-Balance-Sheet Assets and Liabilities1.Disclosure of off-balance-sheet assets2.Disclosure of off-balance-sheet liabilities3.Take-or-pay and throughput arrangements4.Sale of receivables5.Finance subsidiaries6.Joint ventures and investment in affiliatesJ.Analysis of Pensions, Stock Compensation, and Other Employee Benefits1.Disclosuresponents of pension costb.Plan statusc.Reconciliationd.Assumptions used to calculate pension cost and obligations2.Analysis of pension costs and liabilitya.Importance of assumptions(1)Factors affecting benefit obligations (e.g., service cost, interest cost, actuarialgains and losses, prior service cost from plan amendments, benefits paid)(2)Factors affecting plan assets (e.g., employer contribution, return on assets,benefits paid)(3)Factors affecting pension expense (e.g., service cost and interest cost,expected return on assets, amortization of gains or losses, amortization ofprior service cost, amortization of transition asset or liability)b.Analysis of plan status, costs, and cash flowsc.Impact of pension reporting on corporate earnings3.Employee stock compensation plansa.Disclosuresb.Analysis of costs and liabilityK.Analysis of Inter-Corporate Investments1.Accounting for marketable securitiesa.Cost methodb.Market methodc.Lower of cost or market methodd.U.S. and international accounting requirements2.Analysis of marketable securitiesa.Separation of operating from investment resultsb.Effects of classification of marketable securitiesc.Analysis of investment performance3.Equity method of accountinga.Conditions for useb.Equity accounting and analysis4.Consolidations policy and proceduresparison of consolidation with the equity methodb.Analysis of minority interestc.Non-U.S. consolidation practicesd.Analysis of segment dataL.Analysis of Business Combinations1.Accounting for acquisitions2.Effects of accounting methods3.International differences in accounting for business combinations4.Analysis of goodwill5.Choosing the acquisition method6.Spin-offs and tracking stocksM.Analysis of Multinational Operations1.Effects of exchange rate changes on a firm’s actual and reported performancea.Flow effectb.Holding gain/loss effect2.Basic accounting issuesa.Choice of exchange rates (e.g., historical rate or current rate)b.Assets or liabilities to be adjusted for exchange rate changesc.Treatment of translation gains and losses3.Prescribed foreign currency translation4.Choice of the functional currency for a foreign subsidiaryparison of translation and remeasurementa.Income statement effectsb.Balance sheet effectsc.Impact on financial ratiosd.Impact on reported cash flows6.Analysis of foreign currency disclosuresa.Exchange rate changes: exposure and effectsN.Ratio and Financial Analysismon-size statements2.Activity analysis and turnover ratiosa.Short-term and long-term activity ratiosb.Turnover ratios (inventory, receivables, payables, working capital, fixed asset andtotal asset)3.Liquidity analysisa.Length of cash cycleb.Working capital ratios4.Long-term debt analysisa.Debt covenantsb.Debt ratiosc.Interest coverage ratios5.Profitability analysisa.Return on sales (gross margin, operating margin, pretax margin, profit margin)b.Return on investment (e.g., return on assets, return on total capital, return onequity)6.Operating and financial leverage7.Earnings per share (EPS)a.Basic EPSb.Diluted EPSc.Weighted-average number of common shares outstandingd.Convertible securitiese.Options and warrantsf.Contingent shares8.Other ratios and value metricsa.Earnings before interest, taxes, depreciation and amortization (EBITDA)b.Price-to-earnings (P/E)c.Price-to-book value (P/B)9.Integrated ratio analysis10.Valuation implications of financial statement analysisa.Inter-corporate investmentsb.Business combinationsc.Multinational operationsd.Ratio and financial analysisV.CORPORATE FINANCEA.Fundamental Issues1.Forms of business organizationa.Sole proprietorshipb.Partnershipc.Corporation2.Corporate governance issuesa.Agency relationships (i.e., stockholders, management, other stakeholders)b.Managerial incentives to act in stockholders’ interestsB.Capital Investment Decisions1.Investment decision criteria present value (NPV) approachb.Payback period rulec.Discounted payback ruled.Average accounting returne.Internal rate of return (IRR) approachf.Profitability index2.Cash flow projectionsa.Incrementalmon pitfalls (e.g., sunk costs, opportunity costs, side effects, net workingcapital, financing costs)c.Project cash flows and alternative definitions of operating cash flowses of discounted cash flow analysis3.Project analysis and evaluationa.Scenario analysisb.Sensitivity analysisc.Simulation analysis4.Capital rationingC.Business and Financial Risk1.Breakeven analysisa.Fixed versus variable costsb.Accounting break-even2.Operating leveragea.Implications (e.g., forecasting risk)b.Measurement (i.e., degree of operating leverage)3.Financial leveragea.Implications (e.g., forecasting risk)b.Measurement (e.g., degree of financial leverage)4.Total combined leverageD.Long Term Financial Policy1.Cost of capitala.Required return and cost of capitalb.Cost of equity (e.g., dividend growth model approach and security market lineapproach)c.Cost of debt and preferred stock。

罗斯《公司理财》第9版精要版英文原书课后部分章节答案