中级财务会计英文版

中级财务会计英文版.课后答案(Chap03)

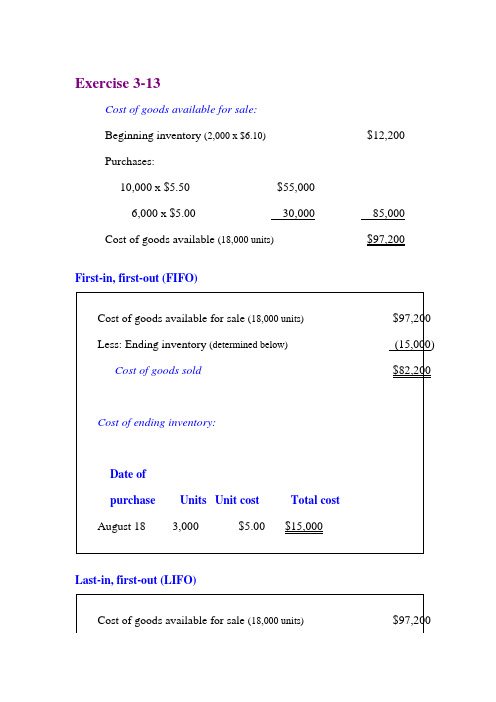

August 14

8,000 @ $ 5.50 = $44,000

2,000 @ $6.10

2,000 @ $5.50 $23,200

August 18

6,000 @ $5.00 = $30,000

2,000 @ $6.10

2,000 @ $5.50 $53,200

Cost of goods sold$82,200

Cost of ending inventory:

Date of

purchaseUnitsUnit costTotal cost

August 183,000$5.00$15,000

Last-in, first-out (LIFO)

Cost of goods available for sale(18,000 units)$97,200

12,000 units

August 14

8,000 @ $5.60 = $44,800

4,000 @ $5.60 $22,400

August 18

Available

6,000 @ $5.00 = $30,000

$52,400

= $5.24/unit

10,000 units

August 25

7,000 @ $5.24 =$36,680

Less: Ending inventory(determined below)(17,700)

Cost of goods sold$79,500

Cost of ending inventory:

Date of

purchaseUnitsUnit costTotal cost

中级财务会计英文ch13117页PPT

Inflows

Proceeds from plant assets sales

Proceeds from sales and maturities of debt and equity securities

Collections of loan principal Sale of real estate

- Incurrence of capitalized lease obligations. SFAS No. 95 provides no guidance with regard to stock

dividends or stock splits.

Chapter 13-15

Direct Method Under the direct method, a

Cash Flows from Investing Activities

Cash Flows from Financing Activities

Chapter 13-10

Cash From Operating Activities

Inflows

Receipts from customers Interest received Dividends received Refunds from suppliers Revenues received in

Outflows

Payments to purchase plant assets

Purchases of debt and equity securities

Loans to others Payments to purchase real

estate

Chapter 13-12

Cash Flows From Financing Activities

中级财务会计英文ch04

Chapter 4-8

Internal Control for Cash

Separate custody of and accounting for cash. Maintain only the minimum cash balance

needed. Provide for periodic test counts of cash

Chapter 4-7

Internal Control Policies and procedures designed to:

Protect assets. Ensure compliance with laws and company policies. Provide accurate accounting records. Evaluate performance.

• Treasury bills • Commercial paper • Money market funds

Chapter 4-5

Cash Items that are not cash

中级财务会计 英文

Intermediate Financial AccountingIntroductionFinancial accounting is a fundamental component of a company’s management and reporting process. It involves the recording, analysis, and reporting of a company’s financial transactions. A strong foundation in financial accounting is essential for any individual looking to pursue a career in finance or accounting. This document aims to provide an overview of intermediate financial accounting concepts and principles.The Accounting CycleThe accounting cycle is a series of steps that are followed in the financial accounting process to ensure accurate and reliable financial reporting. The cycle begins with the recording of transactions and ends with the preparation of financial statements. The key steps in the accounting cycle include:1.Identifying and Analyzing Transactions: This step involvesidentifying relevant financial transactions and analyzing their impact on the company’s financial position.2.Recording Journal Entries: Journal entries are recorded todocument the financial transactions. These entries are made in the generaljournal, which is a chronological record of all transactions.3.Posting to General Ledger: The information from the journal entriesis transferred to the general ledger accounts, which are used to summarizetransactions for each account.4.Preparing Trial Balance: A trial balance is prepared to ensure thatall debit and credit balances in the general ledger are equal. If there are noerrors, the total debits will equal the total credits.5.Adjusting Entries: Adjusting entries are made at the end of theaccounting period to record any transactions that have not been previouslyrecorded, such as accruals and prepayments.6.Preparing Financial Statements: Financial statements, including theincome statement, balance sheet, and cash flow statement, are prepared toreport the company’s financial performance and position.7.Closing Entries: Closing entries are made to transfer balances fromtemporary accounts (such as revenue and expense accounts) to permanentaccounts (such as retained earnings).8.Preparing Post-Closing Trial Balance: A post-closing trial balance isprepared to ensure that all temporary accounts have been closed and that the accounting records are ready for the next accounting period.Financial Statement AnalysisFinancial statement analy sis involves the examination of a company’s financial statements to assess its financial performance and position. It helps in understanding the company’s profitability, liquidity, solvency, and efficiency. The key tools and techniques used in financial statement analysis include:•Horizontal Analysis: Horizontal analysis compares financial statement items over multiple periods to identify trends and changes.•Vertical Analysis: Vertical analysis involves expressing each financial statement item as a percentage of a base amount, such as total assets or netsales, to assess the relative importance of each item.•Ratio Analysis: Ratio analysis involves calculating and interpreting financial ratios to assess the company’s liquidity, solvency, profitability, and efficiency.•Common Size Ratios: Common size ratios are used to compare the relative percentages of different items within a financial statement.•DuPont Analysis: DuPont analysis decomposes the return on equity (ROE) into its components to assess the company’s profitability, efficiency, and leverage.Revenue Recognition and Expense RecognitionThe principles of revenue recognition and expense recognition are fundamental to financial accounting. These principles determine when revenue and expenses should be recognized in the financial statements. The generally accepted accounting principles (GAAP) provide guidelines for revenue recognition and expense recognition.•Revenue Recognition: Revenue is generally recognized when it is earned and realizable. It is earned when the company has delivered goods or services to the customer, and it is realizable when the company can reasonably expect to collect the amount. There are specific criteria for recognizing revenue from different sources, such as sales of goods, provision of services, andinterest and dividends.•Expense Recognition: Expenses are recognized when they are incurred and have a cause-and-effect relationship with revenue. The matching principle requires expenses to be recognized in the same period as the revenuethey help generate. There are different methods of expense recognition, such as the accrual basis and the cash basis.Inventory Valuation MethodsInventory valuation is a crucial aspect of financial accounting, as it impacts the company’s profitability, assets, and financial ratios. There are different methods used to value inventory, including:•FIFO (First-In, First-Out): The FIFO method assumes that the first units of inventory purchased or produced are the first to be sold or used. Itresults in the cost of goods sold being based on the oldest inventory.•LIFO (Last-In, First-Out): The LIFO method assumes that the last units of inventory purchased or produced are the first to be sold or used. Itresults in the cost of goods sold being based on the most recent inventory.•Weighted Average Cost: The weighted average cost method calculates the average cost of inventory based on the average cost per unit. It is calculated by dividing the total cost of goods available for sale by the total units available for sale.Each inventory valuation method has its advantages and disadvantages, and the choice of method can have a significant impact on the company’s f inancial statements and taxes.ConclusionIntermediate financial accounting plays a vital role in providing accurate and reliable financial information for decision-making and reporting. Understanding the accounting cycle, financial statement analysis, revenue recognition and expense recognition principles, and inventory valuation methods is essential for anyone seeking to excel in the field of finance or accounting. By acquiring a solid foundation in these concepts, individuals can enhance their ability to interpret financial data and contribute to the success of their organizations.。

中级财务会计英文ch05

Inventory Categories

Merchandise inventory

Goods acquired for resale

Manufacturing inventory

Raw materials

Work-in-process

Finished goods Manufacturing supplies

Purchases Discounts A company purchases $1,000 of goods under terms of 1/10, n/30.

Net Price Method

Adjusting entry at the end of period if discount has expired and invoice is unpaid: Purchases Discounts Lost Accounts Payable

Chapter 5-19

Calculating Cost of Goods Sold (COGS)

Beginning Inventory + Purchases (net) = Cost of Goods Available for Sale - Ending Inventory = Cost of Goods Sold

Chapter 5-20

Comparison of Systems Perpetual Inventory System

Beginning inventory + Purchases (net) - Goods Sold = Ending Inventory

7.

8. 9.

Chapter 5-2

中级财务会计(英文)课件Chapter 11 Long-term Liabilities And Receivables

Recording the Issuance of Bonds

On July 1, 2004, Grimes Corporation records the semiannual interest paymsh

Interest Expense 48,000 16,000 32,000

Intermediate Accounting 11 Long-term Liabilities And Receivables

Steps a Company Must Follow When It Issues Bonds

It must receive approval from regulatory

1. Reasons for Issuance of LongTerm Liabilities

Debt financing may be the only available source of funds.

Debt financing may have a lower cost. Debt financing offers an income tax advantage.

Cash ($400,000 x .97) Discount on Bonds Payable Bonds Payable 388,000 12,000

400,000

Intermediate Accounting 11 Long-term Liabilities And Receivables

Recording the Issuance of Bonds

11 Long-term Liabilities And

Receivables

I

ntermediate Accounting

中级财务会计(英文)课件Chapter 9 Intangibles

Classification of Intangibles

Expense research and development costs as incurred

Identifiable Internally Developed

Capitalize certain costs incurred for an intangible asset with a finite life and amortize over its useful life

Intermediate Accounting 9 Intangibles

Байду номын сангаас

Classification of Intangibles

Capitalize the cost incurred to acquire an intangible assets with a finite life and amortize over its useful life.

Characteristics that Distinguish Intangibles

• There is generally a higher degree of uncertainty regarding the future benefits that may be derived. • Their value is subject to wider fluctuations because it may depend to a considerable extent on competitive conditions. • They may have value only to a particular company. • Goodwill and intangible assets with indefinite lives are not expensed.

中级财务会计英文ch11

Potentially dilutive securities: Convertible preferred stock Convertible bonds Contingent common stock issues Stock rights Stock options

Complex Capital Structure

(duபைடு நூலகம்l EPS)

Equity contracts Use treasury stock method

Convertible securities Use ifconverted method

Contingently issuable shares

Chapter 16-10

EPS Question

A company had 200,000 shares of $50 par value common stock, 10,000 of 5%, $20 par value cumulative preferred stock, and 30,000 shares of 5%, $10 par value noncumulative preferred stock outstanding during the year. Net income after taxes was $1,500,000. No dividends were declared during the year. EPS would be a. $7.50 b. $7.43 c. $7.45 d. $7.38

Chapter 16-3

Price Earnings Ratio

Market Price of Stock EPS

中级财务会计英文ch13

losses from business failures.

Chapter 13-4

Cash Flow Reporting the Trend Toward Cash Flows

Previous Funds Statements -- Statement of Changes in Financial Position (APB Opinion No. 19) Cash Basis or Working Capital Basis

advance

Outflows

Payments to suppliers Payments to employees Interest payments Income tax payments Payments on operating

leases

Chapter 13-11

Cash Flows From Investing Activities

Dividends paid to stockholders

Principal payments on loans from financial institutions

Principal payments on capital leases

Chapter 13-13

Noncash Activities

Statement of Cash Flows

Chapter

13

Intermediate Accounting 12th Edition

Kieso, Weygandt, and Warfield

Chapter 13-1

中级财务会计英文ch04

account balances. Result in the physical control of cash.

Chapter 4-9

Control of Cash Receipts

Add or deduct book errors as appropriate.

Chapter 4-20

Bank Reconciliation

Example

Prepare a July 31 bank reconciliation statement and the resulting journal entries for the Simmons Company. The July 31 bank

statement indicated a cash balance of $9,610, while the cash ledger account on that date shows a balance of $7,430.

Additional information necessary for the reconciliation is shown on the next page.

Chapter 4-18

Bank Reconciliation

Balance Per Bank Section

Start with balance per bank statement. Add deposits in transit. Deduct outstanding checks. Add or deduct bank errors as appropriate.

中级财务会计英文版95页PPT

Balance Sheet Format

Equity Classifications

Capital Stock

Other Contributed Capital

Owners’ Equity

Retained

Earnings

Chapter 3-14

Treasury Stock

Statement of Changes in Stockholders’ Equity

Chapter 3-18

Contingent Liabilities and Assets

No or No

Chapter 3-19

Loss

Probable (?)

Yes

and

Reasonably

estimated (?)

Yes

Reasonably possible

Disclosure

Report amount in financial statements

Balance Sheet Format

Liability Classifications

Accounts Payable

Short-term Notes Payable

Current Liabilities

Collections in advance of unearned revenue

Chapter 3-11

(Owner’s Equity)

Balance Sheet

Basic Accounting Identity

A = L + OE

Chapter 3-5

Balance Sheet

Basic Definitions - SFAC No. 6

中级财务会计(英文)课件Chapter 6 Cash and Receivables

Cash Management Control Over Receipts

Immediately count the receipts (by the person

opening the mail or the sales person using the cash register). Record daily all cash receipts in the accounting records. Deposit daily all receipts in the company’s bank account.

Intermediate Accounting 6 Cash and Receivables

Petty Cash A petty cash system is a cash fund created to allow a company to pay for small amounts that might be impractical or impossible to pay by check.

Intermediate Accounting 6 Cash and Receivables

Petty Cash

As money is paid from the fund, prenumbered vouchers are prepared to document the expenditures but no journal entries are made until the fund is reimbursed. At the time of reimbursement, appropriate expense accounts are debited and the cash account is credited as follows : Office Supplies Expense 120

中级财务会计-英文版复习提纲-1

Chapter 9 &10Property, Plant and Equipment一、Acuisition1.购买取得:purchase price less any trade discount, less cash discounts available(现金折扣不计入取得成本,不包括在固定资产的入账价值——享受现金折扣则扣除;若不享受则作为费用)✓Devon Company purchases a machine with a contract price of $100,000 on terms of 2/10, n/30. The company does not take the cash discount and incurs transportation costs of $2,500, as well as installation and testing costs of $3,000. Sales taxes total $5,000 on the purchase. During installation, uninsured damages of $500 are incurred. What is the cost of the machine?Contract price $100,000Discount not taken (2,000)Transportation cost 2,500Installation and testing 3,000Sales tax 5,000Cost of machine $108,500•Dr. Machine 108,500•Discounts Lost 2,000•Repair Expense 500•Cr. Cash 111,000•Note: The company does not include the $500 damage as part of the cost of the machinery because it was not a necessary cost.2.Lump-sum purchase 一揽子采购:按公允价值分配,记录cost✓ A company pays $120,000 for land and a building. The land and building are appraised at $50,000 and $75,000, respectively.3.Deferred payments 延期付款:1)首先比较资产的公允价值(the fair value of the assets)与票据的公允价值(the fair value of the liability)哪个更可靠,record可靠的那个2)如果二者均没有,则用现值记录。

中级财务会计英文ch14

statements.

Whether to recognize the effect of the change in

the current year’s net income or in the beginning retained earnings balance .

5.

6. 7. 8. 9.

Chapter 14-2

Describe the accounting for changes in estimates.

Identify changes in a reporting entity. Describe the accounting for correction of errors. Identify economic motives for changing accounting methods. Analyze the effect of errors.

Chapter 14-8

Reporting Approach Required

Retroactive Approach Retroactive Approach Prospective Approach Retroactive Approach* Retroactive Approach

Accounting Principle Changes

Changes in Accounting Principle

Three approaches for reporting changes:

1) Currently (cumulative effect). 2) Retrospectively.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Balance Sheet

Basic Definitions - SFAC No. 6

Liabilities Probable future sacrifices of economic

benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities as a result of past

Learning Objectives

1. Understand the purposes of the balance sheet. 2. Define the elements of a balance sheet. 3. Explain how to measure the elements of a balance

transactions or events.

Balance Sheet

Basic Definitions - SFAC No. 6

Owners’ Equity The residual interest in the assets of

an entity that remains after its liabilities are deducted.

finanotchiaelrsittaetmems.ents.

Current assets Current liabilities

= Working Capital Ratio

Balance Sheet Format

Liability Classifications

Capital Leases

Long-term Notes Payable

Noncurrent Liabilities

sheet. 4. Classify the assets of a balance sheet. 5. Classify the liabilities of a balance sheet. 6. Report the stockholders’ equity of a balance sheet. 7. Understand the concepts of income. 8. Explain the conceptual guidelines for reporting

Current Liabilities

Collections in advance of unearned revenue

Accrued Expenses

Working Capital

Less: Equals:

Current assets Current liabilities Working Capital

income.

Learning Objectives

9. Define the elements of an income statement. 10. Describe the major components of an income

statement. 11. Compute income from continuing operations. 12. Compute results from discontinued operations. 13. Identify extraordinary items. 14. Prepare a statement of retained earnings. 15. Report comprehensive income.

Intangibles

Noncurrent Assets

Property, Plant, & Equipment

Deferred Charges

Balance Sheet Format

Liability Classifications

Accounts Payable

Short-term Notes Payable

A = L + OE

Balance Sheet

Basic Definitions - SFAC No. 6

Assets Probable future economic benefits

obtained or controlled by a particular entity as a result of past

Balance Sheet

Resources (Assets)

Claims against resources (Liabilities)

Remaining claims accruing to owners

(Owner’s Equity)

Balance Sheet

Basic Accounting Identity

Bonds Payable

Pension Liabilities

Balance Sheet Format

Equity Classifications

Capital Stock

Other Contributed Capital

Owners’ Equity

Retained Earnings

Treasury Stock

Statement of Changes in Stockholders’ Equity

TAhiscosrtaptoermateinotnsmhouusltddsishcolwoseintvheestcmhaenngtsesbyinaintsd distrsitboucktihoonlsdteorso’wenqeuritsydaucrcinougntthewpheernioisds,uainmgong

Balance Sheet Format

Asset Classifications

Cash

Inventories

Current Assets

Receivables

Prepayments

Balance Sheet Format

Asset Classifications

Investments and funds