香港国际财务报告准则(中英文对照版)

ifrs会计准则香港-概述说明以及解释

ifrs会计准则香港-概述说明以及解释1.引言概述部分的内容可以如下编写:1.1 概述近年来,国际金融市场的融合和全球化的趋势日益明显,各国之间的商业活动也日益频繁。

为了使不同国家的企业财务报表具有可比性和透明度,国际会计准则委员会(IASB)和国际财务报告准则(IFRS)于2001年推出了国际财务报告准则(IFRS)。

香港作为全球金融中心之一,对国际金融市场的发展具有重要的影响力。

为了与国际接轨并提升香港企业在全球市场的竞争力,香港于2005年起开始实施IFRS会计准则。

IFRS会计准则旨在统一和规范企业的财务报告,从而提供真实、准确和可比的信息,帮助投资者和其他利益相关方做出明智的决策。

这一准则与之前的香港财务报告准则(HKFRS)相比,更加注重市场的国际标准化和一致性。

香港在实施IFRS会计准则的过程中,积极推动着相关法规和制度的完善,包括在香港证券监管机构规定上对上市公司的要求等。

随着香港与国际金融市场的联系日益紧密,IFRS会计准则在香港的应用也在逐渐扩大。

本文将详细讨论IFRS会计准则在香港的应用情况,包括其对香港企业财务报告的影响、香港市场的接受程度以及遇到的挑战和改进方向等。

通过深入研究IFRS会计准则在香港的实施和应用情况,我们可以更好地了解其在全球金融市场中的地位和作用,为香港企业的发展提供有益的参考。

文章结构部分的内容可以包括以下内容:文章结构部分的主要目的是为读者提供对整篇文章的整体了解,以便他们能够更好地理解文章的主题和内容。

以下是文章结构部分的一些可能内容:1.2 文章结构本文将按照以下几个方面进行探讨:1.2.1 第一部分:IFRS会计准则的概述在第一部分中,将对IFRS会计准则进行简要概述。

将介绍IFRS的起源和发展背景,以及IFRS在全球范围内的适用情况。

同时,还将讨论IFRS 会计准则的主要特点和目标,以帮助读者对该准则有一个初步的了解。

1.2.2 第二部分:IFRS会计准则在香港的应用第二部分将详细介绍IFRS会计准则在香港的应用情况。

香港会计报表(中英文对照)

Write-back of trade payables

应付贸易账款拨回

未se in inventories of properties Increase in other inventories Increase in trade and other receivables Increase in investments held for trading Increase in trade and other payables Increase in sales deposits received Cash generated from operation

現金及等同現金項目之變動

現金及等同現金項目之變動 現金及等同現金項目承上年度 結轉現金及等同現金項目

Analysis of the balance of cash and cash equivalents Bank balances and cash

現金及等同現金項目的分析 銀行結存及現金

应付所得税

小計 资本及储备 资本 年初未分配利润 本年度纯利 股息 利润分配-提取储备基金 法定储备

Capital reserves Property revaluation reserve Sub-total Minority interests Non-Current Liabilities Bank borrowings, due after one year Other borrowings, due after one year Long term payables Deferred taxation Sub-total

已收股息 已付所得稅 已付土地增值稅 所得稅退回 經營業務之現金流量淨額 投资业务 利息收入 购置物业,厂房及设备 出售物业,厂房及设备之收入 附属公司收购 增持予附属公司之权益 出售一间附属公司之净现金收入 出售一间共同控制公司之实收现金 收到一间共同控制公司的股息 来自关联公司的(预付款)还款 向共同控制公司支付的预付款 向共同控制公司出资 源自投资之现金净值 融資業務 小股东投入资本 应付关联公司款额之减少 应付股东款项之增加 应付共同控制公司款项之增加(减 少) 新筹集银行贷款 偿还银行贷款 偿还其它借款 已付股息 已付利息 融資業務小计

国际会计准则(1~41)中英文目录对照

国际会计准则(1~41)中英文目录对照国际会计准则(1~41)中英文目录对照1.IAS1:Presentation of Financial Statements《IAS1——财务报表的列报》2.IAS2:Inventories《IAS2——存货》3.IAS3:Consolidated Financial Statements《IAS3——合并财务报表》(已被IAS27和IAS28取代)4.IAS4:Depreciation Accounting《IAS4——折旧会计》(已被IAS16、IAS22和IAS38取代)5.IAS5:Information to Be Disclosed in Financial Statements《IAS5——财务报表中披露的信息》(已被IAS1取代)6.IAS6:Accounting Responses to Changing Prices《IAS6——物价变动会计》(已被IAS15取代)7.IAS7:Cash Flow Statements《IAS7——现金流量表》8.IAS8:Accounting Policies, Changes in Accounting Estimates and Errors 《IAS8——当期净损益、重大差错和会计政策变更》9.IAS9:Accounting for Research and Development Activities《IAS9——研发活动会计》(已被IAS38取代)10.IAS10:Events after the Balance Sheet Date《IAS10——资产负债表日后事项》11.IAS11:Construction Contracts《IAS11——建造合同》12.IAS12:Income Taxes《IAS12——所得税》13.IAS13:Presentation of Current Assets and Current Liabilities 《IAS13——流动资产和流动负债的列报》(已被IAS1取代)14.IAS14:Segment Reporting《IAS14——分部报告》15.IAS15:Information Reflecting the Effects of Changing Prices《IAS15——反映物价变动影响的信息》(2003年已被撤销)16.IAS16:Property, Plant and Equipment《IAS16——不动产、厂场和设备》17.IAS17:Leases《IAS17——租赁》18.IAS18:Revenue《IAS18——收入》19.IAS19:Employee Benefits《IAS19——雇员福利》20.IAS20:Accounting for Government Grants and Disclosure of Government Assistance《IAS20——政府补助会计和政府援助的披露》21.IAS21:The Effects of Changes in Foreign Exchange Rates《IAS21——汇率变动的影响》22.IAS22:Business Combinations《IAS22——企业合并》(已被IFRS3取代)23.IAS23:Borrowing Costs《IAS23——借款费用》24.IAS24:Related Party Disclosures《IAS24——关联方披露》25.IAS25:Accounting for Investments《IAS25——投资会计》(已被IAS39 和IAS40取代)26.IAS26:Accounting and Reporting by Retirement Benefit Plans《IAS26——退休福利计划的会计和报告》27.IAS27:Consolidated and Separate Financial Statements《IAS27——合并财务报表及对子公司投资会计》28.IAS28:Investments in Associates《IAS28——对联合企业投资会计》29.IAS29:Financial Reporting in Hyperinflationary Economies《IAS29——恶性通货膨胀经济中的财务报告》30.IAS30:Disclosures in the Financial Statements of Banks and Similar Financial Institutions《IAS30——银行和类似金融机构财务报表中的披露》31.IAS31:Interests in Joint Ventures《IAS31——合营中权益的财务报告》32.IAS32:Financial Instruments: Disclosure and Presentation《IAS32——金融工具:披露和列报》33.IAS33:Earnings per Share《IAS33——每股收益》34.IAS34:Interim Financial Reporting《IAS34——中期财务报告》35.IAS35:Discontinuing Operations《IAS35——终止经营》(已被IFRS5取代)36.IAS36:Impairment of Assets《IAS36——资产减值》37.IAS37:Provisions, Contingent Liabilities and Contingent Assets 《IAS37——准备、或有负债和或有资产》38.IAS38:Intangible Assets《IAS38——无形资产》39.IAS39:Financial Instruments: Recognition and Measurement《IAS39——金融工具:确认和计量》40.IAS40:Investment Property《IAS40——投资性房地产》41.IAS41:Agriculture《IAS41——农业》国际会计准则中文版文件格式:Pdf可复制性:可复制TAG标签:会计学点击次数:更新时间:2010-03-30 15:23介绍国际会计准则中文版,国际会计准则在2008年做了更新,中文版不知道是否同步更新,这个对于会计从业人员的帮助很大,在网上找了很久中文版都是2003的老版本,不知道楼主上传的版本对我是否有用。

香港会计准则-准则对比

IFRS 2

No

IFRS 3 Revised No

Insurance Contracts

IFRS 4

No

No

No

HKFRS 5

Non-current Assets Held for Sale and IFRS 5 Discontinued Operations Exploration for and Evaluation of Mineral Resources Financial Instruments: Disclosures Operating Segments Financial Instruments IFRS 6

HKAS No. Title IAS No.

Differences in Transitional Provisions

No

Differences in Other Textual Differences Effective Dates

No Minor textual differences – explanation of legal requirements which do not give rise to differences. No

6

Comparison between HK Financial Reporting Standards and International Financial Reporting Standards as at 31 December 2011

HKAS No. Title IAS No.

Differences in Transitional Provisions

HKAS No. Title IAS No.

Differences in Transitional Provisions

hkas会计准则

HKAS会计准则简介HKAS会计准则是指香港会计师公会(Hong Kong Institute of Certified Public Accountants)发布的会计准则,也被称为香港国际财务报告准则(Hong Kong International Financial Reporting Standards,简称HKIFRS)。

这些准则是香港上市公司和其他组织编制财务报表时必须遵循的规范。

背景香港作为一个国际金融中心,吸引了众多国际投资者和跨国公司。

为了提高香港财务报告的透明度和可比性,香港会计师公会决定采纳国际财务报告准则,即HKAS会计准则。

HKAS会计准则的特点1.国际接轨:HKAS会计准则与国际财务报告准则(IFRS)高度一致,香港的财务报表可以与全球范围内其他国家和地区的报表进行比较和分析。

2.专业权威:HKAS会计准则由香港会计师公会制定,公会是香港会计行业的权威机构,准则制定过程经过广泛的专业讨论和研究。

3.灵活性:HKAS会计准则允许企业根据自身的具体情况进行会计政策的选择,以反映其业务模式和财务状况。

4.信息披露:HKAS会计准则强调信息披露的重要性,要求企业在财务报表中提供充分、准确、及时的信息,以帮助用户做出明智的经济决策。

HKAS会计准则的应用范围HKAS会计准则适用于以下组织:1.香港上市公司:所有在香港联合交易所上市的公司必须遵循HKAS会计准则编制财务报表。

2.金融机构:银行、保险公司和其他金融机构也需要遵循HKAS会计准则,以确保其财务报表的准确性和可比性。

3.非营利组织:慈善机构、社团和其他非营利组织也被要求按照HKAS会计准则编制财务报表。

HKAS会计准则的主要内容HKAS会计准则包括以下重要内容:1.财务报表:规定了财务报表的要求和格式,包括资产负债表、利润表、现金流量表和所有者权益变动表等。

2.会计政策:对企业在编制财务报表时应采用的会计政策进行了规定,以确保财务报表的一致性和准确性。

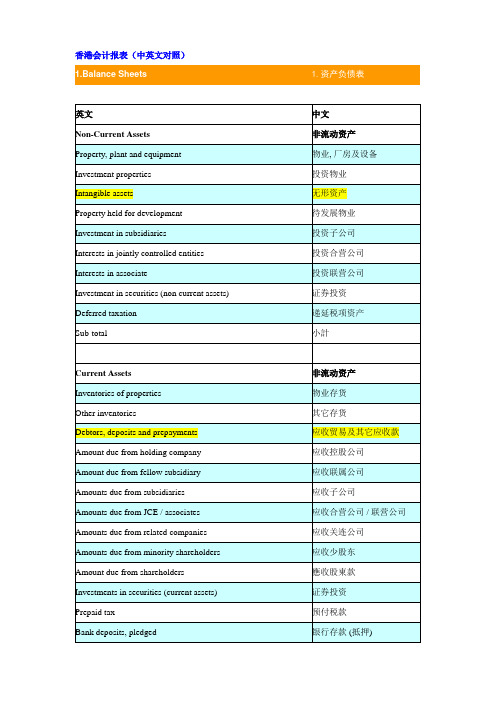

香港会计报表--中英文对比

香港会计报表2011-04-04 14:41:02| 分类:会计知识| 标签:|字号大中小订阅香港会计报表1.Balance Sheets 1.资产负债表英文中文Non-Current Assets 非流动资产Property, plant and equipment 物业, 厂房及设备Investment properties 投资物业Intangible assets 无形资产Property held for development 待发展物业Investment in subsidiaries 投资子公司Interests in jointly controlled entities 投资合营公司Interests in associate 投资联营公司Investment in securities (non current assets) 证券投资Deferred taxation 递延税项资产Sub-total 小計Current Assets 非流动资产Inventories of properties 物业存货Other inventories 其它存货Debtors, deposits and prepayments 应收贸易及其它应收款Amount due from holding company 应收控股公司Amount due from fellow subsidiary 应收联属公司Amounts due from subsidiaries 应收子公司Amounts due from JCE / associates 应收合营公司/ 联营公司Amounts due from related companies 应收关连公司Amounts due from minority shareholders 应收少股东Amount due from shareholders 應收股東款Investments in securities (current assets) 证券投资Prepaid tax 预付税款Bank deposits, pledged 银行存款(抵押) Bank balances, deposits and cash 银行结余及现金Sub-total 流动资产小計Current Liabilities 流动负债Trade and other payables 应付贸易及其它应收款Sales deposits received 销售定金Amounts due to subsidiaries 应付子公司Amounts due to immediate holding 应付控股公司Amounts due to fellow subsidiaries 应付联属公司Amount due to JCE/associates 应付合营公司/ 联营公司Amounts due to related companies 应付关连公司Amount due to shareholders 应付股东款Amount due to minority shareholders 应付少股东Bank borrowings, due within one year 银行借款(一年内) Other borrowings, due within one year 其它借款(一年内) Income tax payable 应付所得税Sub-total 小計Capital and Reserves 资本及储备Paid-up capital 资本Retained earnings b/f 年初未分配利润This year's profit 本年度纯利Dividend 股息Reserve appropriation 利润分配-提取储备基金Statutory reserve 法定储备Capital reserves 资本公积-股权投资准备Property revaluation reserve 投资物业重估储备Sub-total 所有者权益小計Minority interests 少股东权益Non-Current Liabilities 非流动负债Bank borrowings, due after one year 银行借款(一年以上) Other borrowings, due after one year 其它借款(一年以上) Long term payables 长期应付款Deferred taxation 递延税款Sub-total 小計2.INCOME STATEMENT 2.损益表英文中文Turnover 营业收入Business Tax 主营业务税金及附加Cost of sales 营业成本经营毛利Gross MarginOther operating income 其它业务收入Interest Income 利息收入Gain from investment in securites 投资收益Change in fair value of investment properties 投资物业公平价值之溢利Other operating expenses 其它业务支出Selling expenses 营业费用Administrative expenses 管理费用Provision on investment in securities 持有作买卖之投资公平价值之溢利Finance costs 财务费用Share of results of jointly controlled entities 应占合营公司业绩Taxation 税项Minority interests 少股东损益This year's (profit) loss 本年度利纯3.CASH-FLOWSTATEMENT 3.现金流量表英文中文Operating activities: 经营活动Profit before tax 稅前經營溢利Adjustment:- 調整:- Share of result of jointly controlled entities 应占共同控制公司业绩Depreciation 折舊Allowance for doubtful debts (补贴拨回),呆坏帐补贴Change in fair value of investment properties 投资物业公平价值之溢利Change in fair value of investments held for trading 持有作买卖之投资之公平价值溢利interest received 利息收入Finance costs 财务费用Impairment loss on goodwill of JCE 共同控制公司之商誉减值损失Impairment loss on goodwill arising on acquisition of 增持予附属公司之权益导致商誉减值损失additional interest in subsidiaries 出售物业、厂房及设备之亏损(收益)Loss on disposal of PPE 持有作买卖之投资之亏损(收益)Gain on disposal of jointly controlled entities 出售一间共同控制公司之收益Write-back of trade payables 应付贸易账款拨回未計流動資金變動前之經營業務及現金流量Increase in inventories of properties 物业存货之减少(增加)Increase in other inventories 其它存货之减少(增加)Increase in trade and other receivables 应收贸易及其它款项之增加Increase in investments held for trading 持有作买卖之投资的减少(增加)Increase in trade and other payables 应付贸易及其它账款之增加(减少)Increase in sales deposits received 销售定金之增加(减少)Cash generated from operation 經營業務產生之現金Dividend received 已收股息Tax paid- income tax 已付所得稅Tax paid- land value added tax 已付土地增值稅Refund of tax 所得稅退回Net cash inflow generated from operation 經營業務之現金流量淨額投资业务Interest received 利息收入Purchase of property, plant and equipment 购置物业,厂房及设备Proceeds from disposal of property, plant and equipment 出售物业,厂房及设备之收入附属公司收购[size=+0] Acquisition of additional interest in sub 增持予附属公司之权益Net cash from disposal of a subsidiary 出售一间附属公司之净现金收入[size=+0]Cash received on disposal of a JCE 出售一间共同控制公司之实收现金Dividend received from a JCE 收到一间共同控制公司的股息Repayment from related companies 来自关联公司的(预付款)还款Advances to JCE 向共同控制公司支付的预付款Capital contributions to JCE 向共同控制公司出资Net cash from investing activities 源自投资之现金净值Financing activities 融資業務Capital contribution from minority shareholders 小股东投入资本Decrease in amounts due to related companies 应付关联公司款额之减少Increase in amounts due to shareholders 应付股东款项之增加Increase in amounts due to JCE 应付共同控制公司款项之增加(减少)New bank loans raised 新筹集银行贷款Repayment of bank loans 偿还银行贷款Repayment of other borrowings 偿还其它借款Interest paid 已付股息Dividend paid 已付利息Net cash from financing activities 融資業務小计Net increase/ (decrease) in cash & cash equivalent 現金及等同現金項目之變動Net increase/ (decrease) in cash & cash equivalents 現金及等同現金項目之變動Cash & cash equivalent at 1 January 現金及等同現金項目承上年度Cash & cash equivalent at 30 November 結轉現金及等同現金項目Analysis of the balance of cash and cash equivalents 現金及等同現金項目的分析Bank balances and cash 銀行結存及現金/sycc1/kjcs/200804/58.html会计科目中英对照表1001 现金Cash on hand1002 银行存款Cash in bank1009 其他货币资金Other monetary fund100901 外埠存款Deposit in other cities100902 银行本票Cashier's cheque100903 银行汇票Bank draft100904 信用卡Credit card100905 信用保证金Deposit to creditor100906 存出投资款Cash in investing account1101 短期投资Short-term investments110101 股票Short-term stock investments 110102 债券Short-term bond investments 110203 基金Short-term fund investments 110110 其他Other short-term investments1102 短期投资跌价准备Provision for loss on decline in value of short-term investments1111 应收票据Notes receivable1121 应收股利Dividends receivable1131 应收账款Accounts receivable1133 其他应收款Other receivable1141 坏账准备Provision for bad debts1151 预付账款Advance to suppliers1161 应收补贴款Subsidy receivable1201 物资采购Materials purchased1211 原材料Raw materials1221 包装物Containers1231 低值易耗品Low cost and short lived articles1232 材料成本差异Cost variances of material1241 自制半成品Semi-finished products1243 库存商品Merchandise inventory1244 商品进销差价Margin between selling and purchasing price on merchandise 1251 委托加工物资Material on consignment for further processing1261 委托代销商品Goods on consignment- out1271 受托代销商品Goods on consignment-in1281 存货跌价准备Provision for impairment of inventories1291 分期收款发出商品Goods on installment sales1301 待摊费用Prepaid expense1401 长期股权投资Long-term equity investments 140101 股票投资Long-term stock investments 140102 其他股权投资Other long-term equity investments 1402 长期债权投资Long-term debt investments 140201 债券投资Long-term bond investments 140202 其他债权投资Other long-term debt investments1421 长期投资减值准备Provision for impairment of long-term investments1431 委托贷款Entrusted loan143101 本金Principal of entrusted loan 143102 利息Interest of entrusted loan 143103 减值准备Provision for impairment of entrusted loan 1501 固定资产Fixed assets-cost1502 累计折旧Accumulated depreciation1505 固定资产减值准备Provision for impairment of fixed assets1601 工程物资Construction material 160101 专用材料Specific purpose materials 160102 专用设备Specific purpose equipments 160103 预付大型设备款Prepayments for major equipments160104 为生产准备的工具及器具Tools and instruments prepared for production1603 在建工程Construction in process1605 在建工程减值准备Provision for impairment of construction in process1701 固定资产清理Disposal of fixed assets1801 无形资产Intangible assets1815 未确认融资费用Unrecognized financing charges 1901 长期待摊费用Long-term deferred expenses 1911 待处理财产损溢Profit & loss of assets pending disposal191101 待处理流动资产损溢Profit & loss of current-assets pending disposal191102 待处理固定资产损溢Profit & loss of fixed assets pending disposal2101 短期借款Short-term loans2111 应付票据Notes payable2121 应付账款Accounts payable 2131 预收账款Advance from customers 2141 代销商品款Accounts of consigned goods 2151 应付工资Wages payable2153 应付福利费Welfare payable 2161 应付股利Dividends payable 2171 应交税金Taxes payable 217101 应交增值税Value added tax payable 21710101 进项税额Input VAT 21710102 已交税金Payment of VAT 21710103 转出未交增值税Outgoing of unpaid VAT 21710104 减免税款VAT relief 21710105 销项税额Output VAT 21710106 出口退税Refund of VAT for export 21710107 进项税额转出Outgoing of input VAT21710108 出口抵减内销产品应纳税额Merchandise VAT from expert to domestic sale21710109 转出多交增值税Outgoing of over-paid VAT 217102 未交增值税Unpaid VAT217103 应交营业税Business tax payable 217104 应交消费税Consumer tax payable 217105 应交资源税Tax on natural resources payable 217106 应交所得税Income tax payable 217107 应交土地增值税Land appreciation tax payable217108 应交城市维护建设税Urban maintenance and construction tax payable217109 应交房产税Real estate tax payable 217110 应交土地使用税Land use tax payable 217111 应交车船使用税Vehicle and vessel usage tax payable 217112 应交个人所得税Personal income tax payable 2176 其他应交款Other fund payable2181 其他应付款Other payables2191 预提费用Accrued expenses2201 待转资产价值Pending transfer value of assets 2211 预计负债Estimable liabilities2301 长期借款Long-term loans2311 应付债券Bonds payable231101 债券面值Par value of bond231102 债券溢价Bond premium231103 债券折价Bond discount231104 应计利息Accrued bond interest2321 长期应付款Long-term payable2331 专项应付款Specific account payable2341 递延税款Deferred tax3101 实收资本(或股本)Paid-in capital(or share capital)3103 已归还投资Retired capital 3111 资本公积Capital reserve311101 资本(或股本)溢价Capital (or share capital) premium311102 接受捐赠非现金资产准备Restricted capital reserve of non-cash assets donation received311103 接受现金捐赠Reserve of cash donation received 311104 股权投资准备Restricted capital reserve of equity investments 311105 拨款转入Government grants received311106 外币资本折算差额Foreign currency capital conversion difference311107 其他资本公积Other capital reserve 3121 盈余公积Surplus reserve 312101 法定盈余公积Statutory surplus reserve 312102 任意盈余公积Discretionary earning surplus 312103 法定公益金Statutory public welfare fund 312104 储备基金Reserve fund 312105 企业发展基金Enterprise development fund 312106 利润归还投资Profit return for investment 3131 本年利润Profit & loss summary 3141 利润分配Distribution profit 314101 其他转入Other adjustments314102 提取法定盈余公积金Extract for statutory surplus reserve314103 提取法定公益金Extract for statutory public welfare fund 314104 提取储备基金Extract for reserve fund314105 提取企业发展基金Extract for enterprise development fund314106 提取职工奖励及福利基金Extract for staff bonus and welfare fund314107 利润归还投资Profit return of capital invested 314108 应付优先股股利Preference share dividend payable314109 提取任意盈余公积Extract for discretionary earning surplus314110 应付普通股股利Ordinary share dividend payable314111转作资本(或股本)的普通股股利Ordinary share dividend transfer to capital (or share)314115 未分配利润Undistributed profit 4101 生产成本Cost of production410101 基本生产成本Basic production cost 410102 辅助生产成本Auxiliary production cost 4105 制造费用Manufacturing overheads 4107 劳务成本Labor cost5101 主营业务收入Sales revenue5102 其他业务收入Revenues from other operations 5201 投资收益Investment income5203 补贴收入Subsidy income5301 营业外收入Non-operating profit 5401 主营业务成本Cost of sales5402 主营业务税金及附加Sales tax5405 其他业务支出Cost of other operations5501 营业费用Operating expenses5502 管理费用General and administrative expenses 5503 财务费用Financial expenses5601 营业外支出Non-operating expenses5701 所得税Income tax5801 以前年度损益调整Prior period profit & loss adjustment。

香港会计准则与国际会计准则对照表

Comparison of Hong Kong Accounting Standards with International Accounting Standards (IASs)/ International Financial Reporting Standards (IFRSs)for the June 2006 examinationsHKG document TitleINTdocumentTitleExaminablePaper(s)Preface to Hong Kong Financial Reporting Standards 1.1, 2.5, 2.6, 3.13.6Framework for the Preparation and Presentation of Financial Statements Framework for the Preparation and Presentation of Financial Statements 1.1 (Note 5), 2.5,2.6,3.1, 3.6HKAS 1 Presentation of Financial Statements IAS 1Presentation of Financial Statements 1.1, 2.5, 2.6, 3.1, 3.6HKAS 1 Amendment Capital Disclosures 1.1, 2.5, 2.6, 3.1,3.6HKAS 2 Inventories IAS 2 Inventories 1.1, 2.5, 2.6, 3.1,3.6HKAS 7 Cash Flow Statements IAS 7 Cash Flow Statements 1.1 (Note 1), 2.5(Note 1), 2.6, 3.1,3.6HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors 1.1, 2.5, 2.6, 3.1,3.6HKAS 10 Events After the Balance Sheet Date IAS 10Events After the Balance Sheet Date 1.1, 2.5, 2.6, 3.1, 3.6HKAS 11 Construction Contracts IAS 11 Construction Contracts 2.5, 2.6, 3.1, 3.6 HKAS 12 Income Taxes IAS 12 Income Taxes 2.5, 2.6, 3.1, 3.6 HKAS 14 Segment Reporting IAS 14 Segment Reporting 2.5, 2.6, 3.1, 3.6HKAS 16 Property, Plant and EquipmentIAS 16 Property, Plant and Equipment 1.1, 2.5, 2.6, 3.1, 3.6HKAS 17 Leases IAS 17 Leases 2.5, 2.6, 3.1, 3.6HKAS 18 RevenueIAS 18 Revenue 1.1, 2.5, 2.6, 3.1,3.6HKAS 19 Employee Benefits IAS 19 Employee Benefits 3.6HKAS19 Amendment Employee Benefits – Actuarial Gains and Losses, Group Plans andDisclosures3.6HKAS 20 Accounting for Government Grants and Disclosure of Government Assistance IAS 20Accounting for Government Grants and Disclosure of GovernmentAssistance2.5, 2.6,3.1, 3.6HKAS 21 The Effects of Changes in Foreign Exchange Rates IAS 21 The Effects of Changes in Foreign Exchange Rates 3.6HKAS 23 Borrowing Costs IAS 23 Borrowing Costs 2.5, 2.6, 3.1, 3.6 HKAS 24 Related Party Disclosures IAS 24 Related Party Disclosures 2.5, 2.6, 3.1, 3.6 HKAS 27 Consolidated and Separate Financial Statements IAS 27 Consolidated and Separate Financial Statements 2.5, 2.6, 3.1, 3.6HKAS 28 Investments in AssociatesIAS 28 Investments in Associates2.5, 2.6,3.1, 3.6HKAS 29 Financial Reporting in Hyperinflationary Economies IAS 29 Financial Reporting in Hyperinflationary Economies 3.6HKAS 31 Investments in Joint Ventures IAS 31 Interests in Joint Ventures 2.5, 2.6, 3.1, 3.6 HKAS 32 Financial Instruments: Disclosure and Presentation IAS 32 Financial Instruments: Disclosure and Presentation 2.5, 2.6, 3.1, 3.6 HKAS 33 Earnings per Share IAS 33 Earnings per Share 2.5, 2.6, 3.1, 3.6HKAS 34 Interim Financial Reporting IAS 34 Interim Financial Reporting 3.6HKAS 36 Impairment of Assets IAS 36 Impairment of Assets 2.5, 2.6, 3.1, 3.6HKAS 37 Provisions, Contingent Liabilities and Contingent Assets IAS 37 Provisions, Contingent Liabilities and Contingent Assets 1.1 (Note 2), 2.5,2.6,3.1, 3.6HKAS 38 Intangible Assets IAS 38 Intangible Assets 1.1 (Note 3), 2.5,2.6,3.1, 3.6HKAS 39 Financial Instruments: Recognition and Measurement IAS 39 Financial Instruments: Recognition and Measurement 2.5, 2.6, 3.1, 3.6HKAS 39 Amendment Transition and Initial Recognition of Financial Assets and FinancialLiabilities2.5, 2.6,3.1 ,3.6HKAS 39AmendmentCash Flow Hedge Accounting of Forecast Intragroup Transactions 2.5, 2.6, 3.1 ,3.6 HKAS 39AmendmentThe Fair Value Option 2.5, 2.6, 3.1 ,3.6HKAS 39 & HKFRS 4 Amendment Financial Instruments: Recognition and Measurement and InsuranceContracts – Financial Guarantee Contracts2.5, 2.6,3.1 ,3.6(HKFRS 4 Amend3.6 only)HKAS 40 Investment Property IAS 40 Investment Property 2.5, 2.6, 3.1, 3.6HKAS 41 Agriculture IAS 41 Agriculture 3.6 HKFRS 1 First-time adoption of Hong Kong Financial Reporting Standards IFRS 1 First –time adoption of International Financial Reporting Standards 2.5, 2.6, 3.1, 3.6HKFRS 1 & 6 Amendment First-time Adoption of Hong Kong Financial Reporting Standards andExploration for and Evaluation of Mineral Resources2.5, 2.6,3.1, 3.6(HKFRS 6 Amend3.6 only)HKFRS 2 Share-based Payment IFRS 2 Share-based Payment 3.6HKFRS 3 Business Combinations IFRS 3 Business Combinations 1.1 (Note 6), 2.5,2.6,3.1, 3.6 HKFRS 4 Insurance Contracts IFRS 4 Insurance Contracts 3.6HKFRS 5 Non-current Assets Held for Sale and Discontinued Operations IFRS 5 Non-current Assets Held for Sale and Discontinued Operations 1.1 (Note 4), 2.5,2.6,3.1, 3.6 HKFRS 7 Financial Instruments: Disclosures IFRS 7 Financial Instruments: Disclosures 2.5, 2.6, 3.1, 3.6 HKFRS 6 Exploration for and Evaluation of Mineral Resources IFRS 6 Exploration for and Evaluation of Mineral Resources 3.6HK-INT 3 Revenue – Pre Completion Contracts for the Sale of DevelopmentProperties2.5, 2.6,3.1, 3.6 HK-INT 4 Leases – Determination of The Length of Lease Term in respect of HongKong Land Leases2.5, 2.6,3.1, 3.6 HKAS-INT 10 Government Assistance – No Specific Relation to Operating Activites SIC 10 Government assistance – No specific relation to operating activities 2.5, 2.6, 3.1, 3.6 HKAS-Int 12 Consolidation – Special Purpose Entities SIC 12 Consolidation – Special Purpose Entities 3.6HKAS-Int 12 Amendment Scope of HKAS-Int 12 Consolidation – Special Purpose Entities3.6HKAS-Int 13 Jointly Controlled Entities – Non-Monetary Contributions by Venturers SIC 13 Jointly Controlled Entities – Non-Monetary Contributions by Venturers 3.6 HKAS-Int 15 Operating Leases – Incentives SIC 15 Operating Leases – Incentives 3.6 HKAS-Int 21 Income Taxes – Recovery of Revalued Non-Depreciable Assets SIC 21 Income Taxes – Recovery of Revalued Non-Depreciable Assets 3.6HKAS-Int 25 Income Taxes – Changes in the Tax Status of an Enterprise or Its Shareholders SIC 25 Income Taxes – Changes in the Tax Status of an Enterprise or ItsShareholders3.6HKAS-Int 27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease SIC 27 Evaluating the Substance of Transactions In the Legal Form of a Lease3.6HKAS-Int 29 Disclosure – Service Concession Arrangements SIC 29 Disclosure – Service Concession Arrangements 3.6HKAS-Int 31 Revenue – Barter Transactions Involving Advertising Services SIC 31 Revenue – Barter Transactions Involving Advertising Services 3.6HKAS-Int 32 Intangible Assets – Web Site Costs SIC 32 Intangible Assets – Web Site Costs 3.6HKFRS-Int 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities 3.6HKFRS-Int 4 Determining Whether an Arrangement contains a Lease IFRIC 4 Determining Whether an Arrangement contains a Lease 2.5, 2.6, 3.1, 3.6HKFRS-Int 5 Rights to Interests arising from Decommissioning, Restoration and Environmental Rehabilitation Funds IFRIC 5 Rights to Interests arising from Decommissioning, Restoration andEnvironmental Funds3.6 IFRIC 7 Applying the Restatement Approach under IAS 29, Financial Reporting in Hyperinflationary Economies3.6 DP Preliminary Views on Accounting Standards for Small and Medium-sized Entities3.6 ED Proposed Amendment to IFRS 3, Business Combinations 3.6 ED Proposed Amendment to IAS 27, Consolidated and Separate FinancialStatements3.6 ED Proposed Amendment to IAS 37, Provisions, Contingent Liabilities andContingent Assets3.6 DP Measurement Bases for Financial Reporting – Measurement on InitialRecognition3.6 DP Management Commentary 3.6Notes1. Cash flow statements are examinable for 1.1 and2.5 but excluding group cash flow statements and cash flow statements including foreign currency.2. Examinable for 1.1 only to the extent of candidates providing definitions and simple calculations.3. Examinable for 1.1 only to cover basic knowledge of Research and Development and Goodwill.4. Examinable for 1.1 only to cover disclosures in relation to Discontinuing Operations.5. The Framework for the preparation of financial statements is examinable for 1.1 at an introductory level only.6. Examinable for 1.1 only to cover basic consolidation.。

英文版国际财务报告准则

《国际财务报告准则第3号:企业合并》(最新英文版)推荐《国际财务报告准则第3号:企业合并》(最新英文版)IFRS 3Intern ati onal Finan cial Report ing Stan dard 3 : Busin ess Comb in ati onsThis versi on in cludes ame ndme nts result ing from IFRSs issued up to 31 December 2006.IAS 22 Busin ess Comb in ati ons was issued by the Intern ati onal Acco unti ng Sta ndards Committee in October 1998. It was a revisi on of IAS 22 B usin ess Comb in atio ns (issued in December 1993), which replaced IAS 22 Acco un ti ng for Busin ess Comb in atio ns (issued in November 1983).In April 2001 the In ternatio nal Acc ounting Sta ndards Board (IASB) res olved that all Stan dards and In terpretati ons issued un der previous Co n stituti ons con ti nued to be applicable uni ess and un til they were ame n ded or withdraw n.In March 2004 the IASB issued IFRS 3 Bus in ess Combi natio ns. It replac ed IAS 22 and three In terpretati ons:IFRS 3Intern ati onal Finan cial Report ing Stan dard 3 Busin ess Comb in ati ons (IFRS 3) is set out in paragraphs 1 - 87 and Appendices A - C. All the pa ragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in Appendix A are in italics the first tim e they appear in the Standard. Definitions of other terms are given i n the Glossary for International Financial Reporting Standards. IFRS 3 should be read in the con text of its objective and the Basis for Co n clusi ons, the Preface to Intern ati onal Finan cial Report ing Stan dards and the Framework for the Preparati on and Prese ntati on of Finan cial Stateme nts. IAS 8 Acco unting Policies, Chan ges in Acco un ti ng Estimate s and Errors provides a basis for select ing and appl ying acco un ti ng p olicies in the abse nee of explicit guida nee.IFRS 3IntroductionIN1International Financial Reporting Standard 3 Business Combinations (I FRS 3) replaces IAS 22 Business Combinations. The IFRS also replaces the following Interpretations: .SIC-9 Business Combinations —Classification either as Acquisitions or Unitings of InterestsSIC-22 Business Combinations —Subsequent Adjustment of Fair Values an d Goodwill Initially ReportedSIC-28 Business Combinations —“ Date of Exchange ” and Fair Value of Equity Instruments.Reasons for issuing the IFRSIN2 IAS 22 permitted business combinations to be accounted for using one of two methods: the pooling of interests method or the purchase m ethod. AlthoughIAS 22 restricted the use of the pooling of interests method to busin ess combinations classified as unitings of interests, analysts and ot her users of financial statements indicated that permitting two metho ds of accounting for substantially similar transactions impaired the comparability of financial statements. Others argued that requiring m ore than one method of accounting for such transactions created incen tives for structuring those transactions to achieve a desired account ing result, particularly given that the two methods produce quite dif ferent results.IN3 These factors, combined with the prohibition of the pooling of in terests method in Australia, Canada and the United States, prompted t he International Accounting Standards Board to examine whether, given that few combinations were understood to be accounted for in accorda nce with IAS 22 using the pooling of interests method, it would be advantageous for international stand ards to converge with those in Australia and North America by also pr ohibiting the method.IN4 Accounting for business combinations varied across jurisdictions in other respects as well. These included the accounting for goodwill and intangible assets acquired in a business combination, the treatment of any excess of the acquirer ' s interest in the fair values of identifiable net assets acquired over the cost of the business combination, and the recognition of liabilities for terminat ing or reducing the activities of an acquiree.IN5 Furthermore, IAS 22 contained an option in respect of how the pur chase method could be applied: the identifiable assets acquired and l iabilities assumed could be measured initially using either a benchma rk treatment or an allowed alternative treatment. The benchmark treat ment resulted in the identifiable assets acquired and liabilities ass umed being measured initially at a combination of fair values (to the extent of the acquirer 's ownership interest) and pre -acquisition carrying amounts (to the extent of any minority interest). The allowed alternative treatment resulted in the identifiable assets acquired an d liabilities assumedIFRS 3being measured initially at their fair values as at the date of acqui sition. The Board believes that permitting similar transactions to be accounted for in dissimilar ways impairs the usefulness of the infor mation provided to users of financial statements, because both compar ability and reliability are diminished.IN6Therefore, this IFRS has been issued to improve the quality of, and s eek international convergence on, the accounting for business combina tions, including: (a) the method of accounting for business combinations; (b) the initial measurement of the identifiable assets acquired and liab ilities and contingent liabilities assumed in a business combination;(c) the recognition of liabilities for terminating or reducing the a ctivities of an acquiree; (d) the treatment of any excess of the acqu irer ' s interest in the fair values of identifiable net assets acquir ed in a business combination over the cost of the combination; and (e) the accounting for goodwill and intangible assets acquired in a busi ness combination. Main features of the IFRSIN7 This IFRS:(a) requires all business combinations within its scope to be account ed for by applying the purchase method.(b) requires an acquirer to be identified for every business combination within its scope. The acquirer is the combining entity that obtains control of theother combining entities or businesses.(c) requires an acquirer to measure the cost of a business combinatio n as the aggregate of: the fair values, at the date of exchange, of a ssets given, liabilities incurred or assumed, and equity instruments issued by the acquirer, in exchange for control of the acquiree; plus any costs di rectly attributable to the combination.(d) requires an acquirer to recognise separately, at the acquisition date, the acquiree 's identifiable assets, liabilities and contingent liabilities that satisfy the following recognition criteria at that d ate, regardless of whether they had been previously recognised in the acquiree 's financial statements:(i) in the case of an asset other than an intangible asset, it is pro bable that any associated future economic benefits will flow to the a cquirer, and its fair value can be measured reliably;(ii) in the case of a liability other than a contingent liability, itis probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and its fair value can be measured reliably; and(iii) in the case of an intangible asset or a contingent liability,its fair value can be measured reliably.(e) requires the identifiable assets, liabilities and contingent liab ilities that satisfy the above recognition criteria to be measured in itially by the acquirer at their fair values at the acquisition date, irrespective of the extent of any minority interest.(f) requires goodwill acquired in a business combination to be recogn ised by the acquirer as an asset from the acquisition date, initially measured as the excess of the cost of the business combination over the acquirer 's interest in the net fair value of the acquiree 's ide ntifiable assets, liabilities and contingent liabilities recognised i n accordance with (d) above.(g) prohibits the amortisation of goodwill acquired in a business com bination and instead requires the goodwill to be tested for impairmen t annually, ormore frequently if events or changes in circumstances indicate that t he asset might be impaired, in accordance with IAS 36 Impairment of A ssets.(h) requires the acquirer to reassess the identification and measurem ent of the acquiree 's identifiable assets, liabilities and contingent liabilities and themeasurement of the cost of the busines s combination if the acquirer 's interest in the net fair value of the items recognised in accordance with (d) above exceeds the cost of the combination. Any excess remai ning after that reassessment must be recognised by the acquirer immed iately in profit or loss.(i) requires disclosure of information that enables users of an entit y's financial statements to evaluate the nature and financial effect of:(i) business combinations that were effected during the period; (ii) business combinations that were effected after the balance sheet date but before the financial statements are authorised for issue; and (i ii) some business combinations that were effected in previous periods.(j) requires disclosure of information that enables users of an entit y's financia l statements to evaluate changes in the carrying amount of goodwill during the period. Changes from previous requirementsIN8 The main changes from IAS 22 are described below. Method of accou ntingIN9 This IFRS requires all business combinations within its scope to be accounted for using the purchase method. IAS 22 permitted business combinations to be accounted for using one of two methods: the pooling of interests meth od for combinations classified as unitings of interests and the purch ase method for combinations classified as acquisitions.Recognising the identifiable assets acquired and liabilities and cont ingent liabilities assumedIN10This IFRS changes the requirements in IAS 22 for separately recognisi ng as part of allocating the cost of a business combination:(a) liabilities for terminating or reducing the activities of the acq uiree; and (b) contingent liabilities of the acquiree.This IFRS also clarifies the criteria for separately recognising inta ngible assets of the acquiree as part of allocating the cost of a com bination.IN11This IFRS requires an acquirer to recognise liabilities for terminati ng or reducing the activities of the acquiree as part of allocating t he cost of the combination onlywhen the acquiree has, at the acquisition date, an existing liability for restructuring recognised in accordance with IAS 37 Provisions, C ontingent Liabilities and Contingent Assets. IAS 22 required an acqui rer to recognise as part of allocating the cost of a business combina tion a provision for terminating or reducing the activities of the acquiree that was not a liability of the acquiree a t the acquisition date, provided the acquirer satisfied specified cri teria.IN12This IFRS requires an acquirer to recognise separately the acquiree 's contingent liabilities (as defined in IAS 37) at the acquisition dat e as part of allocating the cost of a business combination, provided their fair values can be mea sured reliably. Such contingent liabilities were, in accordance with IAS 22, subsumed within the amount recognised as goodwill or negative goodwill.IN13 IAS 22 required an intangible asset to be recognised if, and only if, it was probable that the future economic benefits attributable to th e asset would flow to the entity, and its cost could be measured reliably. The probability reco gnition criterion is not included in this IFRS because it is always c onsidered to be satisfied for intangible assets acquired in business combinations. Additionally, this IFRS includes guidance clarifying that the fair value of an int angible asset acquired in a business combination can normally be measured with sufficient relia bility to qualify for recognition separately from goodwill. If an int angible asset acquired in a business combination has a finite useful life, there is a rebutt able presumption that its fair value can be measured reliably.Measuring the identifiable assets acquired and liabilities and contin gent liabilities assumedIN14IAS 22 included a benchmark and an allowed alternative treatment for the initial measurement of the identifiable net assets acquired in a business combination, and therefore for the initial measurement of any minority interests. This IFRS requires the acquiree 's identifiable assets, liabilities and contingent liabilities recognised as part of allocating the cost of the combination to be measured initially by the acquirer at their fair values at the acquisit ion date. Therefore, any minority interest in the acquiree is stated at the minority 's proportion of the net fair values of those items. This is consistent with I AS 22's allowed alternative treatment.Subsequent accounting for goodwillIN15This IFRS requires goodwill acquired in a business combination to be measured after initial recognition at cost less any accumulated impai rment losses.Therefore, the goodwill is not amortised and instead must be tested f or impairment annually, or more frequently if events or changes in ci rcumstances indicate that it might be impaired. IAS 22 required acquired goodwill to be systematically amortised over its useful life, and included a rebuttable presumption that its useful life could not exceed twenty years from i nitial recognition.Excess of acquirer 's interest in the net fair value of acquiree 's i dentifiable assets, liabilities and contingent liabilities over costIN16This IFRS requires the acquirer to reassess the identification and me asurement of the acquiree 's identifiable assets, liabilities and con tingent liabilities and the measurement of the cost of the combination if, at the acquisition dat e, the acquirer 's interest in the net fair value of those items exce eds the cost of the mbination. Any excess remaining after that reasse ssment must be recognised by the acquirer immediately in profit or lo ss. In accordance with I AS 22, any excess of the acquirer 's interestin the net fair value of the identifiable assets and liabilities acqu ired over the cost of the acquisition was accounted for as negative goodwill as follows:(a) to the extent that it related to expectations of future losses an d expenses identified in the acquirer ' s acquisition plan, it was required to be carried forward and recognised as income in the same period in which the futu re losses and expenses were recognised.(b) to the extent that it did not relate to expectations of future lo sses and expenses identified in the acquirer 's acquisition plan, it was required to be recognised as income as follows:(i) for the amount of negative goodwill not exceeding the aggregate f air value of acquired identifiable non-monetary assets, on a systemat icbasis over the remaining weighted average useful life of the identifi able depreciable assets.(ii) for any remaining excess, immediately.International Financial Reporting Standard 3Business CombinationsObjectiveThe objective of this IFRS is to specify the financial reporting by a n entity when it undertakes a business combination. In particular, it specifies that all business combinations should be accounted for by applying the purchase method. Therefore, the a cquirer recognises the acquiree ' s identifiable assets, liabilities and contingent liabilities at their fair values at th e acquisition date, and also recognises goodwill, which is subsequent ly tested for impairment rather than amortised.Scope2 Except as described in paragraph 3, entities shall apply this IFRS when accounting for business combinations.3 This IFRS does not apply to:(a) business combinations in which separate entities or businesses ar e brought together to form a joint venture.(b) business combinations involving entities or businesses under comm on control.(c) business combinations involving two or more mutual entities.(d) business combinations in which separate entities or businesses ar e brought together to form a reporting entity by contract alone witho ut the obtaining ofan ownership interest (for example, combinations in which separate en tities are brought together by contract alone to form a dual listed corporation). Identifying a business combination4 A business combination is the bringing together of separate entitie s or businesses into one reporting entity. The result of nearly all business combinations is thatone entity, the acquirer, obtains control of one or more other busine sses, the acquiree. If an entity obtains control of one or more other entities that are not businesses, the bringing together of those entities is not a business combination. When an entity acquires a group of assets or net assets that does not constitute a business, it shall allocate the cost of the group between the individ ual identifiable assets and liabilities in the group based on their r elative fair values at the acquisition date.5A business combination may be structured in a variety of ways for leg al, taxation or other reasons. It may involve the purchase by an enti ty of the equity of anotherentity, the purchase of all the net assets of another entity, the ass umption of the liabilities of another entity, or the purchase of some of the net assets of another entity that together form one or more businesses. It may be effected by the issue of equity instruments, the transfer of cash, cash equiva lents or other assets, or a combination thereof. The transaction may be between the shareholders of the combining entities or between one entity and the shareholders of another entity.It may involve the establishment of a new entity to control the combi ning entities or net assets transferred, or the restructuring of one or more of the combining entities.6A business combination may result in a parent-subsidiary relationship in which the acquirer is the parent and the acquiree a subsidiary of the acquirer. In such circumstances, the acquirer applies this IFRS in its consolidated fin ancial statements. It includes its interest in the acquiree in any se parate financial statements it issues as an investment in a subsidiar y (see IAS 27 Consolidated and Separate Financial Statements).7A business combination may involve the purchase of the net assets, in cluding any goodwill, of another entity rather than the purchase of t he equity of the other entity. Such a combination does not result in a parent-subsidiary rel ationship.8Included within the definition of a business combination, and therefo re the scope of this IFRS, are business combinations in which one ent ity obtains control of another entity but for which the date of obtaining control (ie the ac quisition date) does not coincide with the date or dates of acquiring an ownership interest (ie the date or dates of exchange). This situation may arise, for example, wh en an investee enters into share buy-back arrangements with some of i ts investors and, as a result, control of the investee changes.9This IFRS does not specify the accounting by venturers for interests in joint ventures (see IAS 31 Interests in Joint Ventures).Business combinations involving entities under common control10A business combination involving entities or businesses under common control is a business combination in which all of the combining entit ies or businesses are ultimately controlled by the same party or parties both before and af ter the business combination, and that control is not transitory.11A group of individuals shall be regarded as controlling an entity whe n, as a result of contractual arrangements, they collectively have th e power to govern its financialand operating policies so as to obtain benefits from its ac tivities. Therefore, a business combination is outside the scope of t his IFRS when the same group of individuals has, as a result of contractual arrangements, ul timate collective power to govern the financial and operating policie s of each of the combining entities so as to obtain benefits from their activities, an d that ultimate collective power is not transitory.12An entity can be controlled by an individual, or by a group of indivi duals acting together under a contractual arrangement, and that indiv idual or group of individuals may not be subject to the financial reporting requirement s of IFRSs. Therefore, it is not necessary for combining entities to be included as part of thesame consolidated financial statements for a business combination to be regarded as one involving entities under common control.312 . IASCFIFRS 3The extent of minority interests in each of the combining entities be fore and after the business combination is not relevant to determinin g whether the combination involves entities under common control. Similarly, the fa ct that one of the combining entities is a subsidiary that has been e xcluded from the consolidated financial statements of the group in accordance with IAS 27 is not relevant to determining whether a combination involves ent ities under common control.Method of accounting14All business combinations shall be accounted for by applying the purc hase method.15The purchase method views a business combination from the perspective of the combining entity that is identified as the acquirer. The acqu irer purchases net assets and recognises the assets acquired and liabilities and conting ent liabilities assumed, including those not previously recognised by the acquiree.The measurement of the acquirer 's assets and liabilities is not affe cted by the transaction, nor are any additional assets or liabilities of the acquirer recognised as a result of the transaction, because they are not the subjects of the transaction.Application of the purchase method16 Applying the purchase method involves the following steps:(a) identifying an acquirer;(b) measuring the cost of the business combination; and(c) allocating, at the acquisition date, the cost of the business com bination to the assets acquired and liabilities and contingent liabil ities assumed.Identifying the acquirer17 An acquirer shall be identified for all business combinations. The ac quirer is the combining entity that obtains control of the other comb ining entities or businesses.18 Because the purchase method views a business combination from the acq uirer 's perspective, it assumes that one of the parties to the trans action can be identified as the acquirer.19 Control is the power to govern the financial and operating policies o f an entity or business so as to obtain benefits from its activities.A combining entity shall be presumed to have obtained control of another combining entity when it acquires more than one- half of that other entity ' s voting rights, u nless it can be demonstrated that such ownership does not constitute control. Even if one of the combining entities does not acquire more than one-half of the voting rights of another combining entity, it might have obtained control of that othe r entity if, as a result of the combination, it obtains:(a) power over more than one-half of the voting rights of the other e ntity by virtue of an agreement with other investors; or(b) power to govern the financial and operating policies of the other entity under a statute or an agreement; or(c) power to appoint or remove the majority of the members of the boa rd of directors or equivalent governing body of the other entity; or(d) power to cast the majority of votes at meetings of the board of d irectors or equivalent governing body of the other entity.20Although sometimes it may be difficult to identify an acquirer, there are usually indications that one exists. For example:(a) if the fair value of one of the combining entities is significant ly greater than that of the other combining entity, the entity with t he greater fair value is likely to be the acquirer;(b) if the business combination is effected through an exchange of vo ting ordinary equity instruments for cash or other assets, the entity giving upcash or other assets is likely to be the acquirer; and(c) if the business combination results in the management of one of t he combining entities being able to dominate the selection of the management team of the resulting combined entity, the entity whose ma nagement is able so to dominate is likely to be the acquirer.21In a business combination effected through an exchange of equity inte rests, the entity that issues the equity interests is normally the acquirer. How ever, all pertinent facts and circumstances shall be considered to determine wh ich of the combining entities has the power to govern the financial and operatin g policiesof the other entity (or entities) so as to obtain benefits from its(or their) activities.In some business combinations, commonly referred to as reverse acquis itions, the acquirer is the entity whose equity interests have been acquired and the issuing entity is the acquiree. This might be the case when, for example, a p rivate entity arranges to have itself ‘acquired ' by a smaller public entity as ameans ofobtaining a stock exchange listing. Although legally the issuing publ ic entity is regarded as the parent and the private entity is regarded as the subs idiary, the legal subsidiary is the acquirer if it has the power to govern the fi nancial and operating policies of the legal parent so as to obtain benefits from its activities. Commonly the acquirer is the larger entity; however, the facts and ci rcumstances surrounding a combination sometimes indicate that a smaller entity ac quires a larger entity. Guidance on the accounting for reverse acquisitions is provided in paragraphs B1 - B15 of Appendix B.22When a new entity is formed to issue equity instruments to effect a b usiness combination, one of the combining entities that existed before the co mbination shall be identified as the acquirer on the basis of the evidence avai lable.23Similarly, when a business combination involves more than two combini ng entities, one of the combining entities that existed before the combi nation shallbe identified as the acquirer on the basis of the evidence available. Determining the acquirer in such cases shall include a consideration of, amongst other things, which of the combining entities initiated the combination and whether the assetsor revenues of one of the combining entities significantly exceed tho se ofthe others.314 . IASCFIFRS 3Cost of a business combination24The acquirer shall measure the cost of a business combination as the aggregate of:(a)the fair values, at the date of exchange, of assets given, liabilitie s incurredor assumed, and equity instruments issued by the acquirer, in exchang e for control of the acquiree; plus(b) any costs directly attributable to the business combination.25The acquisition date is the date on which the acquirer effectively ob tains controlof the acquiree. When this is achieved through a single exchange tran saction, the date of exchange coincides with the acquisition date. However, a busi ness combination may involve more than one exchange transaction, for examp lewhen it is achieved in stages by successive share purchases. When thi s occurs:(a)the cost of the combination is the aggregate cost of the individual transactions; and (b)the date of exchange is the date of each exchange transaction (ie the datethat each individual investment is recognised in the financial statem entsof the acquirer), whereas the acquisition date is the date on which t he acquirer obtains control of the acquiree.26Assets given and liabilities incurred or assumed by the acquirer in e xchange for control of the acquiree are required by paragraph 24 to be measured a t their fair values at the date of exchange. Therefore, when settlement of all or any part ofthe cost of a business combination is deferred, the fair value of tha t deferred component shall be determined by discounting the amounts payable to t heir present value at the date of exchange, taking into account any premiu m or discount likely to be incurred in settlement.27The published price at the date of exchange of a quoted equity instru ment provides the best evidence of the instrument 's fair value and shall be used, exceptin rare circumstances. Other evidence and valuation methods shall be considered only in the rare circumstances when the acquirer can demonstrate that the published price at the date of exchange is an unreliable indicator of fair value,and that the other evidence and valuation methods provide a more reli able measure of the equity instrument ' s fair value. The published price at the date ofexchange is an unreliable indicator only when it has been affected by the thinness of the market. If the published price at the date of exchange is an u nreliable indicator or if a published price does not exist for equity instrumen ts issued bythe acquirer, the fair value of those instruments could, for example, be estimatedby reference to their proportional interest in the fair value of the acquirer or by reference to the proportional interest in the fair value of the acqui ree obtained, whichever is the more clearly evident. The fair value at the date of exchange of monetary assets given to equity holders of the acquiree as an alterna tive to equity。

香港财务报告准则体系

香港财务报告准则体系中文版中国会计准则委员会与香港会计师公会关于内地企业会计准则与香港财务报告准则等效的联合声明附件一的附录2香港财务报告准则体系________________________________________________________________ _________ 编制和呈报财务报表的框架香港财务报告准则香港财务报告准则第1号——首次采用香港财务报告准则香港财务报告准则第2号——以股份为基础的支付香港财务报告准则第3号——企业合并香港财务报告准则第4号——保险合同香港财务报告准则第5号——持有待售的非流动资产和终止经营香港财务报告准则第6号——矿产资源的勘查与评估香港财务报告准则第7号——金融工具披露香港会计准则香港会计准则第1号——财务报表列报香港会计准则第2号——存货香港会计准则第7号——现金流量表香港会计准则第8号——会计政策、会计估计变更和差错香港会计准则第10号——资产负债表日后事项香港会计准则第11号——建造合同香港会计准则第12号——所得税香港会计准则第14号——分部报告香港会计准则第16号——不动产、厂场和设备香港会计准则第17号——租赁香港会计准则第18号——收入香港会计准则第19号——雇员福利香港会计准则第20号——政府补助的会计和政府援助的披露香港会计准则第21号——汇率变动的影响香港会计准则第23号——借款费用香港会计准则第24号——关联方披露香港会计准则第26号——退休褔利计划的会计和报告香港会计准则第27号——合并财务报表和单独财务报表香港会计准则第28号——联营中的投资香港会计准则第29号——恶性通货膨胀经济中的财务报告香港会计准则第31号——合营中的权益香港会计准则第32号——金融工具列报香港会计准则第33号——每股收益香港会计准则第34号——中期财务报告香港会计准则第36号——资产减值香港会计准则第37号——准备、或有负债和或有资产香港会计准则第38号——无形资产香港会计准则第39号——金融工具确认和计量香港会计准则第40号——投资性房地产香港会计准则第41号——农业香港(国际财务报告解释委员会)解释公告香港(国际财务报告解释委员会)解释公告第1号——已存在的拆卸、复原及其他类似的负债项目的改变香港(国际财务报告解释委员会)解释公告第2号——会员于合作实体的股权及相类似工具香港(国际财务报告解释委员会)解释公告第4号——确定一项协议是否包含租赁香港(国际财务报告解释委员会)解释公告第5号——对来自拆卸、复原及环境复原基金权益的权利香港(国际财务报告解释委员会)解释公告第6号——参与特定市场而产生的负债:废旧电子电气设备香港(国际财务报告解释委员会)解释公告第7号——《香港会计准则第29号——恶性通货膨胀经济中的财务报告》所规定的重述方法的应用香港(国际财务报告解释委员会)解释公告第8号——《香港财务报告准则第2号》的范围香港(国际财务报告解释委员会)解释公告第9号——嵌入衍生工具的重新评估香港(国际财务报告解释委员会)解释公告第10号——中期财务报告和减值香港(常设解释委员会)解释公告香港(常设解释委员会)解释公告第10号——政府援助:与经营活动没有特定联系的政府援助香港(常设解释委员会)解释公告第12号——合并:特殊目的实体香港(常设解释委员会)解释公告第13号——共同控制实体:合营者的非货币性投入? 香港(常设解释委员会)解释公告第15号——经营租赁:激励措施香港(常设解释委员会)解释公告第21号——所得税:已重估非折旧资产的收回香港(常设解释委员会)解释公告第25号——所得税:企业或其股东纳税状况的改变? 香港(常设解释委员会)解释公告第27号——评价以法律形式体现的租赁交易的实质? 香港(常设解释委员会)解释公告第29号——披露:特许权服务协议香港(常设解释委员会)解释公告第31号——收入:涉及广告服务的易货交易香港(常设解释委员会)解释公告第32号——无形资产:网站成本香港解释公告香港解释公告第1号——基础设施的适当会计政策香港解释公告第3号——收入:开发中房地产的预售合约香港解释公告第4号——关于香港土地租赁中租赁期限长度的确定二零零七年十二月六日。

International Financial Reporting Standards 国际财务报告准则

International Financial Reporting Standards 国际财务报告准则International Accounting Standards 国际会计准则国际会计准则理事会(IASB)所颁布的准则称为国际财务报告准则(可以理解它是一本书),其中包括国际会计准则(只是书里的一部分,包括41个小准则)和解释公告。

国际财务报告准则以前也叫国际会计准则来着IFRS共有四部分:A.编报财务报表的框架(1个)(相当与中国的基本准则)B.国际财务报告准则(5个)1.国际财务报告准则第1号——首次采用国际财务报告准则2.国际财务报告准则第2号——以股份为基础的支付3.国际财务报告准则第3号——企业合并4.国际财务报告准则第4号——保险合同5.国际财务报告准则第5号——持有待售的非流动资产和终止经营C.国际会计准则(发布了41个,有效的32个)1.国际会计准则第1号——财务表报的列报2.国际会计准则第2号——存货3.国际会计准则第7号——现金流量表4.国际会计准则第8号——会计政策、会计估计变更和差错5.国际会计准则第10号——资产负债表日后事项6.国际会计准则第11号——建造合同7.国际会计准则第12号所——所得税8.国际会计准则第14号——分部报告9.国际会计准则第15号——国际会计准则理事会决议:理事会撤销《国际会计准则第15号》10.国际会计准则第16号——不动产、厂场和设备11.国际会计准则第17号——租赁12.国际会计准则第18号——收入13.国际会计准则第19号——雇员福利14.国际会计准则第20号——政府补助的会计和政府援助的披露15.国际会计准则第21号——汇率变动的影响16.国际会计准则第23号——借款费用17.国际会计准则第24号——关联方披露18.国际会计准则第26号——退休福利计划的会计和报告19.国际会计准则第27号——合并财务报表和单独财务报表20.国际会计准则第28号——联营中的投资21.国际会计准则第29号——恶性通货膨胀经济中的财务报告22.国际会计准则30号——银行和类似金融机构财务报表中的披露23.国际会计准则第31号——合营中的权益24.国际会计准则第32号——金融工具:披露和列报25.国际会计准则第33号——每股收益26.国际会计准则第34号——中期财务报告27.国际会计准则第36号——资产减值28.国际会计准则第37号——准备、或有负债和或有资产29.国际会计准则第38号——无形资产30.国际会计准则第39号——金融工具:确认和计量31.国际会计准则第40号——投资性房地产32.国际会计准则第41号——农业D.解释公告(11个)国际财务报告解释委员会前言1.解释公告第7号——引入欧元2.解释公告第10号——政府援助:与经营活动没有特定联系的政府援助3.解释公告第12号——合并:特殊目的主体4.解释公告第13号——共同控制主体:合营者的非货币性投入5.解释公告第15号——经营租赁:激励措施6.解释公告第21号——所得税:已重估非折旧资产的收回7.解释公告第25号——所得税:主体或其股东纳税状况的改变8.解释公告第27号——评价涉及租赁法律形式的交易的实质9.解释公告第29号——披露:服务特许权协议10.解释公告第31号——收入:涉及广告服务的易货交易11.解释公告第32号——无形资产:网站成本就是这样的一本书,以前叫IAS,现在改名了,叫IFRS,可能是IASB的工作人员觉得叫IFRS更有权威性,毕竟会计人员的职能最终就是表现在财务报告上。

香港会计科目、财务报表(中英对照)

⾹港会计科⽬、财务报表(中英对照)⾹港会计科⽬(中英⽂对照)编码科⽬名称(简体)科⽬名称(繁体)科⽬名称(英⽂)1资产資產Assets110现⾦現⾦Cash1101库存现⾦庫存現⾦Cash on hand11011库存现⾦-港币庫存現⾦-港幣Cash on hand-HKD11012库存现⾦-美元庫存現⾦-美元Cash on hand-USD1102银⾏存款銀⾏存款Cash in banks11021汇丰银⾏存款匯豐銀⾏存款HSBC110211汇丰银⾏存款-港币匯豐銀⾏存款-港幣HSBC-HKD110212汇丰银⾏存款-美元匯豐銀⾏存款-美元HSBC-USD11022中国银⾏存款中國銀⾏存款BOC110221中国银⾏存款-港币中國銀⾏存款-港幣BOC-HKD110222中国银⾏存款-美元中國銀⾏存款-美元BOC-USD1103定期存款定期存款Time deposits11031汇丰银⾏定期存款-港币匯豐銀⾏定期存款-港幣Time deposits of HSBC-HKD11032汇丰银⾏定期存款-美元匯豐銀⾏定期存款-美元Time deposits of HSBC-USD1104零⽤⾦零⽤⾦Petty cash11041零⽤⾦-港币零⽤⾦-港幣Petty cash-HKD11042零⽤⾦-美元零⽤⾦-美元Petty cash-USD113短期投资短期投資Short-term investments1131有价证券有價證券Marketable securities1132备抵有价证券跌价损失備抵有價證券跌價損失Allowance for market decline marketable securities 1141应收票据應收票據Notes receivable11411应收票据-港币應收票據-港幣Notes receivable-HKD11412应收票据-美元應收票據-美元Notes receivable-USD1142贴现应收票据貼現應收票據Notes receivable discounted1143备抵坏帐-应收票据備抵壞帳-應收票據Allowance for bad debts-notes receivable1144应收帐款應收帳款Accounts receivable11441应收帐款-港币應收帳款-港幣Accounts receivable-HKD11442应收帐款-美元應收帳款-美元Accounts receivable-USD1145备低坏帐-应收帐款備低壞帳-應收帳款Allowance for bad debts-accounts receivable 1148应收退税款應收退稅款Tax refunds receivable1149留抵税额留抵稅額Tax retained1150应收收益應收收益Accrued income1159其他应收款其他應收款Other receivables11591其他应收款-港币其他應收款-港幣Other receivables-HKD11592其他应收款-美元其他應收款-美元Other receivables-USD1160备抵坏帐-其他应收款備抵壞帳-其他應收款Allowance for bad debts-other receivable1201商品存货商品存貨Merchandise inventory12011商品存货(永续盘存)商品存貨(永續盤存)Merchandise inventory12012商品存货(定期盘存)商品存貨(定期盤存)Merchandise inventory(Stock Closing)1202制成品製成品Finished goods1203在制品在製品Goods in process1204原料原料Raw materials1205物料物料Supplies1206在途材料在途材料Material & supplies in transit1207回收料回收料Reproduced materials1208借出原料借出原料Lend materials1209瑕疵品瑕疵品Defective work1215备抵存货跌价损失備抵存貨跌價損失Allowance for market decline-inventory124预付款项預付款項Prepayments1241预付货款預付貨款Advance payments to suppliers1242⽤品盘存⽤品盤存Office supplies on hand1243预付费⽤預付費⽤Prepaid expenses1244预付税款預付稅款Prepaid taxes1245其他预付款其他預付款Other prepayments1250应收关系企业款應收關係企業款Accounts receivable-relationship126其他流动资产其他流動資產Other current assets1261进项税额進項稅額Input tax1262其他流动资产其他流動資產Other current assets13长期投资⾧期投資Long-term investments1301长期投资⾧期投資Investments in stocks1302备抵长期投资损失備抵⾧期投資損失Allowance for loss on long-term investments14固定资产固定資產Fixed assets or Plant assets140⼟地⼟地Land1401⼟地⼟地Land1402累计折旧-⼟地累計折舊-⼟地Accumulated depreciation-Land141房屋及建筑房屋及建築Buildings and structures1411房屋及建筑房屋及建築Buildings and structures1412累计折旧-房屋及建筑累計折舊-房屋及建築Accumulated depreciation-Buildings and structures 142机器设备機器設備Machinery & equipment1421机器设备機器設備Machinery & equipment1422累计折旧-机器设备累計折舊-機器設備Accumulated depreciation-Machinery & equipment 143⽔电设备⽔電設備Power equipment1431⽔电设备⽔電設備Power equipment1432累计折旧-⽔电设备累計折舊-⽔電設備Accumulated depreciation-Power equipment144交通设备交通設備Transportation facilities1441交通设备交通設備Transportation facilities1442累计折旧-交通设备累計折舊-交通設備Accumulated depreciations-Transportation facilitie 145⽣财器具⽣財器具Furniture and fixtures1451⽣财器具⽣財器具Furniture and fixtures1452累计折旧-⽣财器具累計折舊-⽣財器具Accumulated depreciation-furniture and fixtures146⼯具设备⼯具設備Tools & equipment1461⼯具设备⼯具設備Tools & equipment1462累计折旧-⼯具设备累計折舊-⼯具設備Accumulated depreciation-Tools & equipment148杂项设备雜項設備Miscellaneous equipment1481杂项设备雜項設備Miscellaneous equipment1482累计折旧-杂项设备累計折舊-雜項設備Accumulated depreciation-Miscellaneous equipment 149未完⼯程及预付⼯程及设备款未完⼯程及預付⼯程及設備款Construction work in progress and advance payments 1491未完⼯程未完⼯程Construction work in progress1492预付⼯程及设备款預付⼯程及設備款Advance payments on construction and equipment 15其他资产其他資產Other assets151递延费⽤遞延費⽤Deferred charges1511开办费開辦費Organization costs1512递延权利⾦遞延權利⾦Deferred royalties1521存出保证⾦存出保證⾦Guarantee deposits paid1531催收款项催收款項Accounts receivable overdue1532备抵坏帐-催收款项備抵壞帳-催收款項Allowance for bad debts1541闲置资产閒置資產Idle assets1542累计折旧-闲置资产累計折舊-閒置資產Accumulated depreciation-idle assets1601应收保证票据應收保證票據Guarantee notes1602存出保证票据存出保證票據Certified notes2负债負債Liabilities210短期借款短期借款Short-term loans2101银⾏透⽀銀⾏透⽀Bank overdrafts2102银⾏借款銀⾏借款Bank loans2103购料贷款購料貸款Purchases loans2109其他短期借款其他短期借款Other short-term loans2110应付商业本票應付商業本票Commercial papers payable2111应付商业本票折价應付商業本票折價Discount on commercial papers payable2141应付票据應付票據Notes payable2142其他应付票据其他應付票據Other notes payable2143应付帐款應付帳款Accounts payable21431应付帐款-港币應付帳款-港幣Accounts payable-HKD21432应付帐款-美元應付帳款-美元Accounts payable-USD2146应付费⽤應付費⽤Accrued expenses2147应付股利應付股利Dividends payable2148应付税捐應付稅捐Other taxes payable2151销项税额銷項稅額Other notes payable2159其他应付款其他應付款Other payables2160应付所得税應付所得稅Income taxes payable225预收款项預收款項Accounts collected in advance2251预收货款預收貨款Advances from customers2254其他预收款其他預收款Other accounts collected in advance 2255代收款代收款Collection for others2270其他流动负债其他流動負債Other current liabilities24长期负债⾧期負債Long-term liabilities240长期债务⾧期債務Long-term loans payable2401长期借款⾧期借款Long-term loans payable2402长期应付款⾧期應付款Long-term payables2405其他长期负债其他⾧期負債Other long-term liabilities25其他负责其他負責Other liabilities2501存⼊保证⾦存⼊保證⾦Guarantee deposits received26信托代理及保证负债信託代理及保證負債Trust collection and guarantee liabilities 2601存⼊保证票据存⼊保證票據Guarantee notes received2602应付保证票据應付保證票據Commitments on guarantee notes3股东权益股東權益Stockholders' equity31投⼊资本投⼊資本Paid-in capital3101股本股本Capital stock3109预收股本預收股本Capital received in advance3201增资准备增資準備Additional capital surplus3301资本公积資本公積Capital surplus34保留盈馀保留盈餘Retained earnings340已指拨保留盈馀已指撥保留盈餘Appropriated retained earnings3401法定公积法定公積Legal surplus341未指拨保留盈馀未指撥保留盈餘Unappropriated retained earnings 3411保留盈馀(累积亏损)保留盈餘(累積虧損)Retained earnings or Accumulated loss 3412本期损益本期損益Profit or loss-current periods4营业收⼊營業收⼊Operating revenues41营业收⼊營業收⼊Operating revenues410销货收⼊銷貨收⼊Sales revenues4101销货收⼊銷貨收⼊Sales4102销货退回銷貨退回Sales returns4104销货折让銷貨折讓Sales allowances420劳务收⼊勞務收⼊Service revenues4201加⼯收⼊加⼯收⼊Revenue form reprocessing4209其他营业收⼊其他營業收⼊Other operating revenues5营业成本營業成本Operating costs510销货成本銷貨成本Cost of goods sold5101销货成本銷貨成本Cost of goods sold5401直接⼈⼯直接⼈⼯Direct labor5500制造费⽤製造費⽤Manufacturing overhead56劳务成本勞務成本Service costs560劳务成本勞務成本Service costs5601劳务成本勞務成本Service costs5901其他营业成本其他營業成本Other operating costs6营业费⽤營業費⽤Operating expenses61营业费⽤營業費⽤Operating expenses6101⽔费⽔費Water6102电费電費ELECTRICITY6103电话费電話費TELEPHONE6104⽂具及印刷⽂具及印刷STATIONERY6105租⾦租⾦RENT6106娱乐交际费娛樂交際費ENTERTAINMENT & GIFT6107维修保养费維修保養費GENERAL REPAIR & MAINTENANCE 6108交通费交通費TRAVELLING6109保险费保險費INSURANCE6110⼴告费廣告費ADVERTISING6111管理费管理費MANAGEMENT FEES6112邮费郵費POSTAGE6113出⼝运费出⼝運費CARRIAGE OUTWARDS6118⼊⼝运费⼊⼝運費CARRIAGE INWARDS6119核数费核數費AUDIT FEES6120佣⾦⽀出佣⾦⽀出COMMISSION6121专业法律费專業法律費PROFESSIONAL & LEGAL CHARGES6122杂费雜費SUNDRY62折旧费折舊費Depreciation Expenses6201⼟地折旧费⼟地折舊費Land Depreciation Expenses6202房屋及建筑折旧费房屋及建築折舊費Buildings and structures Depreciation Expenses 6203机器设备折旧费機器設備折舊費Machinery & equipment Depreciation Expenses 6204⽔电设备折旧费⽔電設備折舊費Power equipment Depreciation Expenses6205交通设备折旧费交通設備折舊費Transportation facilities Depreciation Expenses 6206⽣财器具折旧费⽣財器具折舊費Furniture and fixtures Depreciation Expenses 6207⼯具设备折旧费⼯具設備折舊費Tools & equipment Depreciation Expenses 6208杂项设备折旧费雜項設備折舊費Miscellaneous equipment Depreciation Expenses 7营业外收⼊及⽀出營業外收⼊及⽀出Non-operating income and expenses71营业外收⼊營業外收⼊Non-operating income710营业外收⼊營業外收⼊Non-operating income7101利息收⼊利息收⼊Interest income7102财产交易增益財產交易增益Gain on disposal of assets7103租赁收⼊租賃收⼊Rent income7104佣⾦收⼊佣⾦收⼊Commission income7105商品盘盈商品盤盈Gains on physical inventory7106兑换收⼊兌換收⼊Exchange gains7107退税收⼊退稅收⼊Tax refunds income7108投资收⼊投資收⼊Gain on investments7109其他收⼊其他收⼊Other non-operating income72营业外⽀出營業外⽀出Non-operating expenses720营业外⽀出營業外⽀出Non-operating expenses7201利息⽀出利息⽀出Interest expenses7202财产交易损失財產交易損失Loss on disposal of assets7203灾害损失災害損失Loss on calamity7204存货跌价损失存貨跌價損失Loss on market decline of inventory7205盘存损失盤存損失Loss on physical inventory7206兑换损失兌換損失Exchange losses7208投资损失投資損失Loss on investments7209其他营业外⽀出及损失其他營業外⽀出及損失Other non-operating expenses & losses8⾮常损益及会计原则变更累积影响数⾮常損益及會計原則變更累積影響數Extraordinary items and cumulative effect81⾮常损益⾮常損益Extraordinary items8101⾮常损益⾮常損益Extraordinary items8202会计原则变更累积影响数會計原則變更累積影響數Cumulative effect of changes in accounting princip 9所得税所得稅Income taxes91所得税所得稅Income taxes910所得税所得稅Income taxes9101预计所得税預計所得稅Income taxes⾹港会计报表(中英⽂对照)1.Balance Sheets 1.资产负债表英⽂中⽂Non-Current Assets⾮流动资产Property, plant and equipment物业, ⼚房及设备Investment properties投资物业Intangible assets⽆形资产Property held for development待发展物业Investment in subsidiaries投资⼦公司Interests in jointly controlled entities投资合营公司Interests in associate投资联营公司Investment in securities (non current assets)证券投资Deferred taxation递延税项资产Sub-total⼩計Current Assets⾮流动资产Inventories of properties物业存货Other inventories其它存货Debtors, deposits and prepayments应收贸易及其它应收款Amount due from holding company应收控股公司Amount due from fellow subsidiary应收联属公司Amounts due from subsidiaries应收⼦公司Amounts due from JCE / associates应收合营公司 / 联营公司Amounts due from related companies应收关连公司Amounts due from minority shareholders应收少股东Amount due from shareholders應收股東款Investments in securities (current assets)证券投资Prepaid tax预付税款Bank deposits, pledged银⾏存款 (抵押)Bank balances, deposits and cash银⾏结余及现⾦Sub-total流动资产⼩計Current Liabilities流动负债Trade and other payables应付贸易及其它应收款Sales deposits received销售定⾦Amounts due to subsidiaries应付⼦公司Amounts due to immediate holding应付控股公司Amounts due to fellow subsidiaries应付联属公司Amount due to JCE/associates应付合营公司 / 联营公司Amounts due to related companies应付关连公司Amount due to shareholders应付股东款Amount due to minority shareholders应付少股东Bank borrowings, due within one year银⾏借款 (⼀年内) Other borrowings, due within one year其它借款 (⼀年内) Income tax payable应付所得税Sub-total⼩計Capital and Reserves资本及储备Paid-up capital资本Retained earnings b/f年初未分配利润This year's profit本年度纯利Dividend股息Reserve appropriation利润分配-提取储备基⾦Statutory reserve法定储备Capital reserves资本公积-股权投资准备Property revaluation reserve投资物业重估储备Sub-total所有者权益⼩計Minority interests少股东权益Non-Current Liabilities⾮流动负债Bank borrowings, due after one year银⾏借款 (⼀年以上)Other borrowings, due after one year其它借款 (⼀年以上)Long term payables长期应付款Deferred taxation递延税款Sub-total⼩計2.INCOME STATEMENT 2.英⽂中⽂Turnover营业收⼊Business Tax主营业务税⾦及附加Cost of sales营业成本Gross Margin 经营⽑利Other operating income其它业务收⼊Interest Income利息收⼊Gain from investment in securites投资收益Change in fair value of investment properties投资物业公平价值之溢利Other operating expenses其它业务⽀出Selling expenses营业费⽤Administrative expenses管理费⽤Provision on investment in securities持有作买卖之投资公平价值之溢利Finance costs财务费⽤Share of results of jointly controlled entities应占合营公司业绩Taxation税项Minority interests少股东损益This year's (profit) loss本年度利纯3.CASH-FLOWSTATEMENT 3.现⾦流量表英⽂中⽂Operating activities:经营活动Profit before tax稅前經營溢利Adjustment:-調整:-Share of result of jointly controlled entities应占共同控制公司业绩Depreciation折舊Allowance for doubtful debts(补贴拨回),呆坏帐补贴Change in fair value of investment properties投资物业公平价值之溢利Change in fair value of investments held for trading持有作买卖之投资之公平价值溢利interest received利息收⼊Finance costs财务费⽤Impairment loss on goodwill of JCE共同控制公司之商誉减值损失Impairment loss on goodwill arising on acquisition of增持予附属公司之权益导致商誉减值损失additional interest in subsidiaries出售物业、⼚房及设备之亏损(收益)Loss on disposal of PPE持有作买卖之投资之亏损(收益)Gain on disposal of jointly controlled entities出售⼀间共同控制公司之收益Write-back of trade payables应付贸易账款拨回 未計流動資⾦變動前之經營業務及現⾦流量Increase in inventories of properties物业存货之减少(增加)Increase in other inventories其它存货之减少(增加)Increase in trade and other receivables应收贸易及其它款项之增加Increase in investments held for trading持有作买卖之投资的减少(增加)Increase in trade and other payables应付贸易及其它账款之增加(减少)Increase in sales deposits received销售定⾦之增加(减少)Cash generated from operation經營業務產⽣之現⾦Dividend received已收股息Tax paid- income tax已付所得稅Tax paid- land value added tax已付⼟地增值稅Refund of tax所得稅退回Net cash inflow generated from operation經營業務之現⾦流量淨額 投资业务Interest received利息收⼊Purchase of property, plant and equipment购置物业,⼚房及设备Proceeds from disposal of property, plant and equipment出售物业,⼚房及设备之收⼊ 附属公司收购Acquisition of additional interest in sub增持予附属公司之权益Net cash from disposal of a subsidiary出售⼀间附属公司之净现⾦收⼊Cash received on disposal of a JCE出售⼀间共同控制公司之实收现⾦Dividend received from a JCE收到⼀间共同控制公司的股息Repayment from related companies来⾃关联公司的(预付款)还款Advances to JCE向共同控制公司⽀付的预付款Capital contributions to JCE向共同控制公司出资Net cash from investing activities源⾃投资之现⾦净值Financing activities融資業務Capital contribution from minority shareholders⼩股东投⼊资本Decrease in amounts due to related companies应付关联公司款额之减少Increase in amounts due to shareholders应付股东款项之增加Increase in amounts due to JCE应付共同控制公司款项之增加(减少)New bank loans raised新筹集银⾏贷款Repayment of bank loans偿还银⾏贷款Repayment of other borrowings偿还其它借款Interest paid已付股息Dividend paid已付利息Net cash from financing activities融資業務⼩计Net increase/ (decrease) in cash & cash equivalent現⾦及等同現⾦項⽬之變動Net increase/ (decrease) in cash & cash equivalents現⾦及等同現⾦項⽬之變動Cash & cash equivalent at 1 January現⾦及等同現⾦項⽬承上年度Cash & cash equivalent at 30 November結轉現⾦及等同現⾦項⽬Analysis of the balance of cash and cash equivalents 現⾦及等同現⾦項⽬的分析Bank balances and cash銀⾏結存及現⾦。

国际会计准则中英对照(去 Logo)

IFRS and IAS Summaries(2011)《国际财务报告准则》及《国际会计准则》摘要(2011)This extract has been prepared by IFRS Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.本摘要由国际财务报告准则基金会职员编制,未经国际会计准则理事会正式批准。

涉及相关要求必须遵照《国际财务报告准则》。

中英文对照 English with Chinese TranslationIFRS and IAS Summaries(2011)《国际财务报告准则》及《国际会计准则》摘要(2011)This extract has been prepared by IFRS Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.本摘要由国际财务报告准则基金会职员编制,未经国际会计准则理事会正式批准。

涉及相关要求必须遵照《国际财务报告准则》。

The Conceptual Framework for Financial Reporting 2011 as issued at 1 January 2011财务报告的概念框架2011截至2011年1月1日发布This extract has been prepared by IFRS Foundation staff and has not been approved by the IASB. For the requirements reference must be made to the Conceptual Framework for Financial Reporting 2010.本摘要由国际财务报告准则基金会职员编制,未经国际会计准则理事会正式批准。

香港会计报表中英文对照精修订

Gainfrominvestmentinsecurites

投资收益

Changeinfairvalueofinvestmentproperties

投资物业公平价值之溢利

Otheroperatingexpenses

其它业务支出

Selling?expenses

营业费用

Administrative?expenses

Sub-total

流动资产小计

Current?Liabilities

流动负债

Tradeandotherpayables

应付贸易及其它应收款

Salesdepositsreceived

销售定金

Amountsduetosubsidiaries

应付子公司

Amountsduetoimmediateholding

应收控股公司

Amountduefromfellowsubsidiary

应收联属公司

Amountsduefromsubsidiaries

应收子公司

AmountsduefromJCE/associates

应收合营公司/联营公司

Amountsduefromrelatedcompanies

应收关连公司

Amountsduefromminorityshareholders

新筹集银行贷款

Repaymentofbankloans

偿还银行贷款

Repaymentofotherborrowings

偿还其它借款

Interest?paid

已付股息

Dividend?paid

已付利息

Netcashfromfinancingactivities

融资业务小计

香港会计报表(中英文对照)

Amounts due to related companies

应付关连公司

Amount due to shareholders

应付股东款

Amount due to minority shareholders

应付少股东

Bank borrowings, due within one year

Proceeds from disposal of property, plant and equipment

出售物业,厂房及设备之收入

附属公司收购

Acquisition of additionalinterest in sub

增持予附属公司之权益

Net cash from disposal of a subsidiary

营业费用

Administrative expenses

管理费用

Provision on investment in securities

持有作买卖之投资公平价值之溢利

Finance costs

财务费用

Share of results of jointly controlled entities

应占合营公司业绩

融資業務小计

Net increase/ (decrease) in cash & cash equivalent

現金及等同現金項目之變動

Net increase/ (decrease) in cash & cash equivalents

現金及等同現金項目之變動

Cash & cash equivalent at 1 January

Increase in trade and other receivables

香港会计准则和国际会计准则

香港会计准则和国际会计准则

香港会计准则(Hong Kong Financial Reporting Standards,HKFRS)是根据香港会计师公会发行的会计及审计条例(Cap 50)等相关法规所制定的会计准则,适用于香港境内的上市公司、金融机构和大部分其他企业。

国际会计准则(International Financial Reporting Standards,IFRS)是由国际会计准则理事会(International Accounting Standards Board,IASB)制定的国际会计准则。

IFRS旨在提供统一且可比较的财务报告,适用于全球范围内的企业。

尽管香港有自己的会计准则(HKFRS),但在2005年之后,香港决定采用IFRS作为其主要的会计准则,并将HKFRS作为IFRS的本地版本,适用于香港的企业。

因此,香港的会计准则与国际会计准则高度一致,但在一些特定情况下可能存在一些差异或附加规定,以适应香港的法规和市场要求。

hkfrs5