会计学:企业决策的基础,16e-威廉姆斯Chap016

会计学企业决策的基础

会计学企业决策的基础在现代企业中,会计学扮演着至关重要的角色。

它不仅是按照一定标准记录企业交易的基础,还能为企业提供大量的财务信息,帮助企业管理者做出正确的企业决策。

本文将介绍会计学在企业决策中的重要性以及相关底层原则和概念。

会计学在企业决策中的重要性企业决策是企业发展过程中必不可少的一部分。

它可以帮助企业管理者做出正确的选择和决策,以实现企业利润最大化和可持续发展。

而会计学正是帮助企业管理者做出正确判断和决策的重要工具之一。

下面我们将详细介绍会计学在企业决策中的作用。

提供财务信息会计学的首要任务是提供精确、客观的财务信息,让企业管理者能够了解企业的经营状况和财务状况。

通过会计学记录企业的交易信息,可以及时得到企业的资产、负债、收入和支出等财务状况。

企业管理者可以通过这些信息来判断企业是否正常运营,是否需要调整经营决策。

分析经营状况会计学不仅可以提供财务信息,还可以通过财务分析来帮助企业管理者了解企业的长期和短期财务状况。

企业管理者可以通过利润表、资产负债表和现金流量表等报表来分析企业状况,从而评估企业财务稳定性、赢利能力和成长性等因素。

预测未来趋势会计学的应用还可以帮助企业管理者预测未来趋势。

通过对过去和当前的财务状况进行分析,企业管理者可以预测未来企业的发展趋势。

这对于企业的长期规划和策略制定非常重要。

会计学的基本原则和概念要正确理解会计学在企业决策中的作用,有必要了解会计学的一些基本原则和概念。

会计主体和会计客体会计主体是指进行会计记录和报告的组织和个人,如企业、个体工商户等。

会计客体是指需要记录的经济活动,如企业的交易、收入和支出等。

会计等式会计等式是会计学中的基本概念之一。

它是指资产=负债+所有者权益。

通过这个等式,企业管理者可以了解企业的资产来源和运用情况,包括企业的负债情况和所有者权益。

会计要素会计要素是指企业在经济活动中发生的一系列基本事项。

包括资产、负债、所有者权益、收入和费用等。

会计学:企业决策的基础,16e-威廉姆斯Chap025

Reward Reward performance. performance

25-3

Return on Investment (ROI)

Return on investment is the ratio of operating income to the average investment used to generate the income.

McGraw-Hill/Irwin Copyright ©2012 The McGraw-Hill Companies, Inc. 25-1

Motivation and Aligning Goals and Objectives

Goal Congruence

Alignment of employee goals and objectives with organizational goals and objectives.

Return on Investment (ROI)

Holly Company reports the following:

Profit Sales Average Investment $ 30,000 $ 500,000 $ 200,000

Let’s calculate ROI.

25-6

Return on Investment (ROI)

ROI =

Operating Income Average Total Assets

Using ROI to evaluate business performance is often referred to as the DuPont system.

25-4

Components of ROI

会计学-企业决策的基础 问题详解

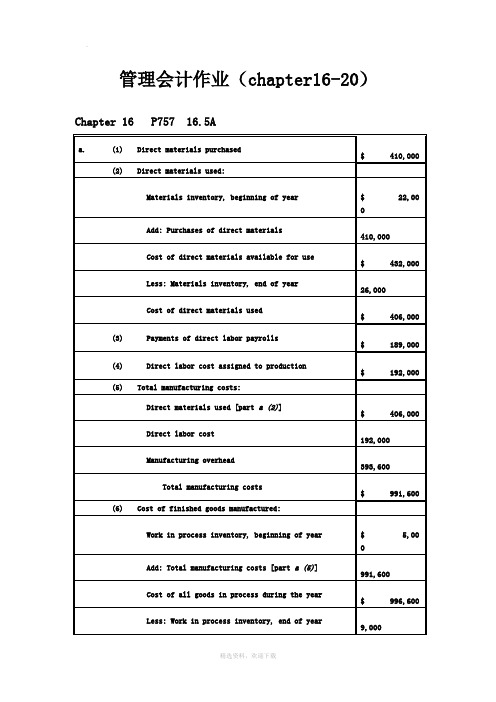

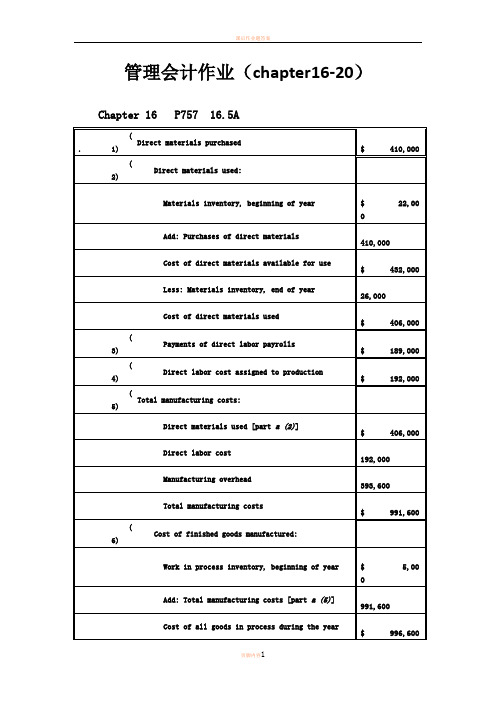

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct labor hours:ManufacturingOverhead = $337,500 = $22.50 per direct laborhourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the Basic Chunksproduct line. Thus, the company’s current practice of using direct labor hours toallocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line isoverpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costing systeminclude: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrificesignificant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex.18.1a. job costing (each project of a construction company is unique)b . both job and process costing (institutional clients may represent unique jobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d . process costing (the dog houses are uniformly manufactured in high volumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Aa4,000 EU $61.50 = $246,000 b4,000 EU $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target OperatingIncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37。

会计学企业决策的基础财务会计分册原书第十六版教学设计

会计学企业决策的基础财务会计分册原书第十六版教学设计一、教学目的本课程旨在让学生了解财务会计的基本理论和方法,并能够应用这些知识进行企业的财务分析和决策。

通过本课程的学习和实践,学生将能够:1.理解财务会计的基本概念和原则;2.掌握编制财务报表的基本方法和技巧;3.理解财务报表的分析和解读方法;4.学会运用财务分析工具进行财务分析和决策。

二、教学内容1. 财务会计基本概念和原则1.1 财务会计的定义和特点 1.2 会计原则和会计假设 1.3 财务报表的基本要素2. 编制财务报表的基本方法和技巧2.1 会计方程和会计式 2.2 记账和账户 2.3 会计凭证和会计账簿 2.4 财务报表的编制和审核3. 财务报表的分析和解读方法3.1 财务报表的分析方法 3.2 偿债能力分析 3.3 资产管理能力分析 3.4 盈利能力分析4. 运用财务分析工具进行财务分析和决策4.1 比率分析 4.2 费用-收益分析 4.3 财务预测和预算分析 4.4 投资决策分析三、教学方法本课程主要采用授课、案例讲解、课堂讨论和实践操作等教学方法。

1.授课:讲解财务会计的基本概念和原则、编制财务报表的基本方法和技巧、财务报表的分析和解读方法等核心知识点。

2.案例讲解:通过具体的案例,让学生实际操作财务报表的编制和分析,深入理解财务会计的实践应用。

3.课堂讨论:围绕企业财务报表的编制和分析,展开课堂讨论,鼓励学生自主思考和探讨。

4.实践操作:通过财务报表的编制和分析实践,让学生获取真实的企业财务信息,培养其分析和决策能力。

四、教学评价本课程的教学评价主要分为两个方面:1.学生评价:通过课堂出勤、作业、期中、期末考试等指标,对学生的学习效果进行评价。

2.教师评价:针对学生的学习情况,及时调整教学方式和方法,提高教学效果。

五、参考教材《会计学:企业决策的基础财务会计分册》原书第十六版,作者:Weygandt、Kimmel、Kieso。

会计学:企业决策的基础,16e-威廉姆斯Chap024

Use product design specifications.

24-7

Direct Labor Standards

Rate Standards Time Standards

Use wage surveys and labor contracts.

Use time and motion studies for each labor operation.

24-4

Actual and Standard Quantities and Costs

24-5

Establishing and Revising Standard Costs

Should we use normal standards or ideal standards?

Normal standards should be set at levels that are currently attainable with reasonable and efficient effort.

Standard Cost Systems

Chapter 24

PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA

24-10

A General Model for Variance Analysis

Actual Quantity × Actual Price Actual Quantity × Standard Price Standard Quantity × Standard Price

会计学企业决策的基础威廉姆斯读后感

会计学企业决策的基础威廉姆斯读后感《会计学企业决策的基础》是威廉姆斯的一本重要著作,它探讨了会计学在企业决策中的基础作用。

读完这本书,我对会计学的重要性和应用范围有了更深入的理解。

威廉姆斯在书中强调了会计信息在企业决策中的关键作用。

他指出,会计信息为企业提供了重要的数据和分析工具,帮助管理者做出明智的决策。

会计信息不仅提供了企业财务状况的全面了解,还能够分析企业的盈利能力、偿债能力以及运营效率等方面的指标。

这些信息对于企业决策者来说至关重要,它们能够帮助管理者评估企业的经营状况,制定合理的战略和目标。

威廉姆斯还介绍了会计信息的质量和可靠性对企业决策的影响。

他指出,会计信息的准确性和及时性对于决策者来说至关重要。

只有准确的会计信息才能为管理者提供可靠的依据,帮助他们做出明智的决策。

威廉姆斯还强调了会计信息的透明度和可比性的重要性。

只有当企业的会计信息具有透明度和可比性时,才能够为决策者提供有益的参考。

在阅读完《会计学企业决策的基础》后,我深刻体会到了会计学在企业决策中的重要性。

会计信息作为企业决策的基础,可以帮助管理者全面了解企业的财务状况,评估企业的盈利能力和运营效率,并为制定合理的战略和目标提供支持。

我也认识到会计信息的质量和可靠性对于决策的重要性,只有准确、透明和可比的会计信息才能够为决策者提供可靠的依据。

《会计学企业决策的基础》是一本值得深入阅读的书籍。

它为读者提供了更全面的会计学知识,帮助我们认识到会计信息在企业决策中的重要性,并为我们未来在企业决策中提供了宝贵的参考和指导。

会计学企业决策的基础财务会计分册第17版

会计学企业决策的基础财务会计分册第17版下载提示:该文档是本店铺精心编制而成的,希望大家下载后,能够帮助大家解决实际问题。

文档下载后可定制修改,请根据实际需要进行调整和使用,谢谢!本店铺为大家提供各种类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by this editor. I hope that after you download it, it can help you solve practical problems. The document can be customized and modified after downloading, please adjust and use it according to actual needs, thank you! In addition, this shop provides you with various types of practical materials, such as educational essays, diary appreciation, sentence excerpts, ancient poems, classic articles, topic composition, work summary, word parsing, copy excerpts, other materials and so on, want to know different data formats and writing methods, please pay attention!企业决策在当前竞争激烈的市场环境中显得尤为重要。

会计学企业决策的基础 课后习题 答案 chapter

Total paid-in capital=15,000,000+20,000,000+44,000,000=79,000,000 e.Book value per share of common stock=(total stockholders' equity-preferred stock)/shares stock=(143,450.000-15,000,000)/4,000,000≈32.11

会计学:企业决策的基础,16e-威廉姆斯Chap007

How Much Cash Should a Business Have?

7-2

The Valuation of Financial Assets

Basis for Valuation in Type of Financial Assets the Balance Sheet Cash (and cash equivalents) Face amount Short-term investments Current market value (marketable securities) Receivables Net realizable value

verified before payment.

• Promptly reconcile bank statements.

7-7

Cash Over and Short

On May 5, XBAR, Inc.’s cash drawer was counted and found to be $15 short.

Prevent theft and fraud.

Assure the availability of adequate amounts of cash. Prevent unnecessarily large amounts of idle cash.

7-6

Internal Control Over Cash

7-9

Reconciling the Bank Statement

Balance per Bank Balance per Depositor

会计学-企业决策的基础 答案

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct laborhours:ManufacturingOverhead = $337,500 = $22.50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the BasicChunks product line. Thus, the company’s current practice of using direct labor hours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costingsystem include: (1) a better identification of its operating inefficiencies, (2)a better understanding of its overhead cost structure, (3) a better understandingof the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex.18.1 a.job costing (each project of a construction company is unique)b.both job and process costing (institutional clients mayrepresent unique jobs)c.job costing (each set of equipment is uniquely designed and manufactured)d.process costing (the dog houses are uniformly manufactured in high volumes)e.process costing (the vitamins and supplements are uniformly manufactured in high volumes)Chapter 18 P841 18.3A4,000 EU @ $61.50 = $246,000b4,000 EU @ $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, managementwould look at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000 $10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target OperatingIncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37Welcome !!! 欢迎您的下载,资料仅供参考!。

会计学_企业决策的基础

Date 2007 June 1 15

McGraw-Hill/Irwin

Who owes us money?

© The McGraw-Hill Companies, Inc., 2008

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2008

Learning Objective

To account for purchases and sales of merchandise in a perpetual inventory system.

Retailers sell merchandise direcaw-Hill Companies, Inc., 2008

Learning Objective

To understand the components of a merchandising company’s income statement.

Cost of goods sold represents the expense of goods that are sold to customers.

McGraw-Hill/Irwin

Gross profit is a useful means of measuring the profitability of sales transactions. © The McGraw-Hill Companies, Inc., 2008

LO3

McGraw-Hill/Irwin

会计学 企业决策的基础 16版 1-5章 课后习题答案

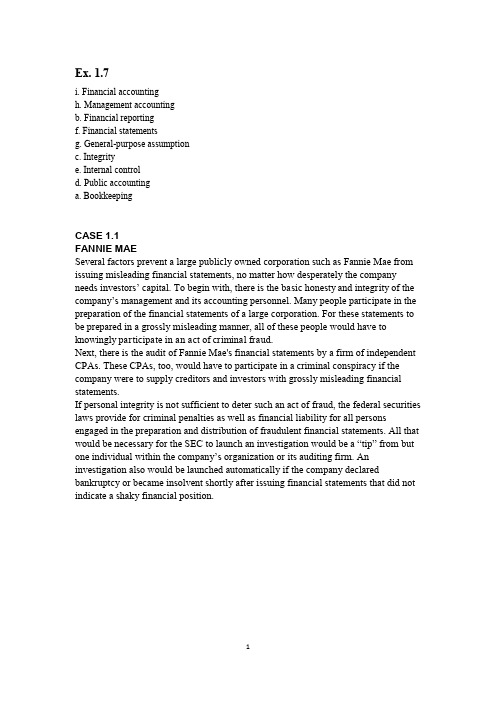

Ex. 1.7i. Financial accountingh. Management accountingb. Financial reportingf. Financial statementsg. General-purpose assumptionc. Integritye. Internal controld. Public accountinga. BookkeepingCASE 1.1FANNIE MAESeveral factors prevent a large publicly owned corporation such as Fannie Mae from issuing misleading financial statements, no matter how desperately the company needs investors’ capital. To begin with, there is the basic honesty and integrity of the company’s management and its accounting personnel. Many people participate in the preparation of the financial statements of a large corporation. For these statements to be prepared in a grossly misleading manner, all of these people would have to knowingly participate in an act of criminal fraud.Next, there is the audit of Fannie Mae's financial statements by a firm of independent CPAs. These CPAs, too, would have to participate in a criminal conspiracy if the company were to supply creditors and investors with grossly misleading financial statements.If personal integrity is not sufficient to deter such an act of fraud, the federal securities laws provide for criminal penalties as well as financial liability for all persons engaged in the preparation and distribution of fraudulent financial statements. All that would be necessary for the SEC to launch an investigation would be a “tip” from but one individual within the company’s organization or its auditing firm. An investigation also would be launched automatically if the company declared bankruptcy or became insolvent shortly after issuing financial statements that did not indicate a shaky financial position.Problem 2.1 AProblem 3.8AExercise 4.2Exercise 4.14Problem 4.5AProblem 5.2AProblem 5.5A。

会计学 企业决策的基础 财务会计分册16版6-9章答案

Chapter 6Merchandising Activitie s Ex. 6.41PROBLEM 6.1AClaypool earned a gross profit rate of 32%, which is significantly higher than the industry average. Claypool’s sales were above the industry average, and it earned $77,968 more gross profit than the “average” store of its size. This higher gross profit was earned even though its cost of goods sold was $18,000 to $20,000 higher than the industry average because of the additional transportation charges.To have a higher-than-average cost of goods sold and still earn a much larger-than-average amount of gross profit, Claypool must be able to charge substantially higher sales prices than most hardware stores. Presumably, the company could not charge such prices in a highly competitive environment. Thus, the remote location appears to insulate it from competition and allow it to operate more profitably than hardware stores with nearby competitors.PROBLEM 6.5Ac. Yes. Sole Mates should take advantage of 1/10, n/30 purchase discounts, even if itmust borrow money for a short period of time at an annual rate of 11%. Bytaking advantage of the discount, the company saves 1% by making payment 20 days early. At an interest rate of 11% per year, the bank charges only 0.6%interest over a 20-day period (11% X 20/365 = 0.6%). Thus, the cost of passing up the discount is greater than the cost of short-term borrowing.Chapter 7 Financial assetsChapter 8 Inventories and the cost of goods soldSupplementary ProblemChapter 91617。

会计学-企业决策的基础 答案

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa.Department One overhead application ratebased on machine-hours:Manufacturing Overhead$420,000=$35 per machine-hourMachine-Hours 12,00 0Department Two overhead application rate based on direct labor hours:Manufacturing Overhead$337,500=$22.50 per direct laborhourDirect Labor Hours 15,00 0Chapter 17 P805 17.8Ad .The Custom Cuts product line is very labor intensive in comparison to theBasic Chunks product line. Thus, the company’s current practice of using direct labor hours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e .The benefits the company would achieve by implementing an activity-basedcosting system include: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex. 18.1a.job costing (each project of a construction company is unique)b.both job and process costing (institutional clients may represent unique jobs)c.job costing (each set of equipment is uniquely designed and manufactured)d.process costing (the dog houses are uniformly manufactured in high volumes)e.process costing (the vitamins and supplements are uniformly manufactured in high volumes)Chapter 18 P841 18.3AInputs:•Beginning WIP•StartedOutputs:•Units completed•Ending WIP•Beginning WIP•Units started•Units completed•Ending WIP•Cost of beginning WIP•Cost added during the period•Cost of goods transferredtransferred•Add ending WIP$246,000b4,000 EU @ $13.50 =$54,000Chapter 18 P845 18.2Ba .(1)$49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2)$109 [($480,000 + $108,000 + $66,000) ÷6,000 units] (3)$158 ($49 + $109)(4)$32 ($192,000 ÷ 6,000 units)(5)$18 ($108,000 ÷ 6,000 units)b .In evaluating the overall efficiency of the Engine Department, managementwould look at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad .No. With a unit sales price of $94, the break-even sales volume in unitsis 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units)$540,000$1054,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales VolumeFixed Costs + TargetOperating IncomeUnit Contribution Margin$390,000 + $350,000= $20,000 units $37。

会计学企业决策的基础财务会计分册第十六版课程设计

会计学企业决策的基础财务会计分册第十六版课程设计课程简介本课程主要介绍财务会计的基础知识和技能,并探讨其在企业决策中的作用。

通过学习本课程,学生将了解如何解读和分析企业财务报告,掌握利润表、资产负债表和现金流量表的基本概念和构成要素,了解会计核算的基本原理和方法,并学习如何使用财务数据制定决策。

课程目标通过本课程的学习,学生将建立起对财务会计的理解,掌握财务报告的解读和分析技能,了解会计核算的基本原理和方法,以及如何使用财务数据进行决策制定。

具体目标如下:1.了解财务会计的基本概念和构成要素;2.掌握利润表、资产负债表和现金流量表的基本内容和解读方法;3.了解会计核算的基本原理和方法;4.学习如何使用财务数据进行决策制定。

课程大纲第一章企业财务会计概述本章主要介绍财务会计的基本概念和构成要素,同时也介绍了财务会计的作用和目标。

第二章财务报表本章主要介绍企业财务报表的基本构成,包括利润表、资产负债表和现金流量表,并探讨了财务报表的解读方法。

第三章会计核算本章主要介绍会计核算的基本原理和方法,包括资产、负债和所有者权益的概念和计算方法,并介绍了资产和负债的分类和计量方法。

第四章财务分析本章主要探讨了如何使用财务数据进行企业决策制定,包括各种财务比率的计算方法和解读技巧,以及财务预测和预算的方法和技巧。

课程教学方法本课程采用讲授和案例分析相结合的教学方法,通过讲解理论知识和实际案例应用,让学生了解财务会计的基础知识和技能,并掌握其在企业决策中的作用。

评分方法本课程的考核包括平时成绩和期末考试成绩。

平时成绩主要包括出勤率、课堂表现和作业成绩,占总成绩的30%,期末考试成绩占总成绩的70%。

期末考试包括主观题和客观题,主观题采用开放式问答和案例分析的形式,客观题包括选择题和填空题。

参考书目1.林达、顾炜,《会计学原理》,中国人民大学出版社,2015年版。

2.王红、李琦,《财务管理与决策》,经济管理出版社,2016年版。

会计学企业决策的基础《会计学企业决策的基础》

PPT文档演模板

会计学企业决策的基础《会计学企业 决策的基础》

国家设计的会计监督:

▪ 会计监督的三个层次: ▪ 企业内部、社会监督、国家

监督 ▪ 国家监督的六个方面: ▪ 财政、审计、税务、银行、

证券监管、保险监管。

PPT文档演模板

会计学企业决策的基础《会计学企业 决策的基础》

PPT文档演模板

会计学企业决策的基础《会计学企业 决策的基础》

会计要素:

§ 一、资产 § 资产(Assets)是指过去的交易、事项形成并由

企业拥有或者控制的资源,该资源预期会给 企业带来经济利益。 § 企业的资产按流动性分为流动资产、长期投 资、固定资产、无形资产和其他资产。

PPT文档演模板

会计学企业决策的础《会计学企业 决策的基础》

会计方法

§ 每门学科都有其特有的研究对象和方法。

§ 会计所特有的方法可概括为:

§ 1.严格的法律要求——会计记录绝大部分会 涉及与业主、客户、职工等方面的权利义务, 例如分红、收账、发工资等。一旦有民事纠 纷,甚至刑事犯罪案件,很多要向会计记录 取证。因此任何一笔会计记录都必须严格符 合解决法律问题的要求。

企业生产经营过程

•投资 者

•补偿生产消耗(C+V)

•货

•材

币

料

•在产品

•

•支付工资和费用旧 折

•固定资产

•W=C+V+M

•国家

•产成品 •货币’ •分配 •两金

•投资者

•沉淀

•企业

PPT文档演模板

会计学企业决策的基础《会计学企业 决策的基础》

财务会计信息系统:

•信息系统

会计学企业决策的基础原书第十五版教学设计教学设计

会计学企业决策的基础原书第十五版教学设计一、课程背景“会计学企业决策”是会计学专业的一门核心课程,旨在使学生掌握企业会计信息的使用和企业决策的基本理论、方法和技巧,培养学生的会计信息处理和分析的能力,以及面对企业决策问题时的分析和决策思维能力。

本课程以教材《会计学企业决策的基础》(第十五版)为主要参考书,重点介绍会计信息在企业决策中的应用,包括成本分析、预算编制、经营绩效评价、投资决策、融资决策等方面。

二、教学目标本课程旨在:•传授企业决策基本理论、方法和技巧,提高学生的管理决策水平和思维能力;•培养学生分析会计信息和企业经营状况的能力,如进行成本分析、利润分析和经营绩效评价等;•通过案例分析和课堂讨论,加强学生的解决问题的能力和实践操作经验。

三、教学内容1.企业决策的基本理论和方法•企业决策的概念和分类;•决策环境下企业会计信息的作用和分析方法;•决策的自然和社会科学基础。

2.成本分析和预算编制•成本概念和分类;•成本估算及控制技术;•预算编制的概念和目的。

3.经营绩效评价和绩效考核•经营绩效的概念和分类;•经营绩效评价的方法和指标体系;•经营绩效绩效考核的方法和实现。

4.投资决策和融资决策•投资决策的概念和分类;•投资决策的主要方法和技巧;•融资决策的概念和原则;•融资工具的选择和实现。

四、教学方法本课程采用多种教学方法,如讲授、案例分析、课堂讨论、小组讨论、实践操作等。

通过上述多种教学方法的应用,使学生在实践中不断积累经验和知识,加深理解和体会。

五、教学评估本课程主要采用成绩考核、课堂表现、作业提交和实验操作等方式进行教学评估。

具体评估内容和比重如下:•平时成绩占总评成绩的20%;•作业提交占总评成绩的20%;•期末考试占总评成绩的60%。

六、教学进度教学内容教学进度企业决策的基本理论和方法1周成本分析和预算编制2周经营绩效评价和绩效考核2周投资决策和融资决策2周综合实践操作1周七、参考教材•《会计学企业决策的基础》(第十五版),作者:帕特里克·马丁、约翰·霍尔曼,译者:张晓栋等,出版社:中国财政经济出版社。

会计学:企业决策的基础,16e-威廉姆斯Chap022

This information is used to:

Plan and allocate resources. Control operations. Evaluate the performance of center managers.

22-3

Cost Centers, Profit Centers, and Investments Centers

Cost Center A business section that has control over the incurrence of costs, but no control over revenues or investment funds.

22-4

Cost Centers, Profit Centers, and Investments Centers

Mfg. costs Commissions Salaries Other

22-5

Cost Centers, Profit Centers, and Investments Centers

Investment Center A profit center where management also makes capital investment decisions.

22-9

Successful implementation of responsibility accounting may use organization charts with clear lines of authority and clearly defined levels of responsibility.

22-6

Cost Centers, Profit Centers, and Investments Centers

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Direct Materials

Raw materials & component parts that become an integral part of finished products. Can be traced directly and conveniently to products.

Support Decision Making

Evaluate Decision Making

16-3

Demand for Accounting Information

Financial Accounting Management Accounting Provide information about the Provide information for Purpose financial position and planning, evaluating, and performance of the company. rewarding performance. Balance sheet, income Types of statement, and statement of Various, non-standard reports. Reports cash flows. Standards GAAP None Reporting Usually, the company taken A component of the Entity as a whole. company's value chain. Time Usually a year, quarter, or a Any period. Periods month. Investors, creditors, and other Management, customers, and Users external parties. others in the value chain.

16-2

Management Accounting System Framework

Top Management

Budget Plans: Future

Actual Results: Current

Performance Evaluation: Past

Decision Making

16-4

Accounting for Manufacturing Operations

The cost to produce a unit of product includes: Direct material Direct labor Manufacturing overhead

16-5

Management Accounting

A Business Partner

Chapter 16

PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA

Finished Goods

Direct labor × hours

Wage rate

Those employees who work directly on the goods being manufactured.

The cost of employees who do not work directly on the goods is considered indirect labor and is part of manufacturing overhead.

Does not include selling or general and administrative expenses.

16-8

Flow of Physical Goods in Production

Direct Materials Purchased Direct Materials Used

If materials cannot be traced directly to products, the materials are considered indirect and are part of manufacturing overhead.

16-6

Direct Labor

Includes the payroll cost of direct workers.

Accounting systems help to identify who has authority over assets. Accounting information supports planning and decision-making. Accounting reports provide a means of monitoring, evaluating, and rewarding performance.

16-7

Manufacturing Overhead

All manufacturing costs other than direct materials and direct labor. Includes:

Indirect materials. Indirect labor. Machinery and equipment costs. Cost of regulatory compliance.

McGraw-Hill/Irwin Copyright ©2012 The McGraw-Hill Companies, Inc.

Management Accounting: Basic Framework

Management accounting and assigning decision-making authority.