解读浑水关于分众传媒的报告

分众传媒-从上市到退市

“我觉得就那么点等电梯的时间还要我强迫接受广告,很受不了。”

分众五战 “浑水”

2011.11.22

浑水第一份质疑分众 传媒的报告,认为分 众传媒数码液晶屏数 量夸大50%。分众传 媒股价应声下跌 39.49%,最低时跌 幅曾达60%。

2011.11.29

浑水第二次质疑分众 传媒,质疑分众传 媒在好耶投资中存 在内幕交易

分众传媒

2007年曾经市值超过40亿美元 纳斯达克中国上市公司龙头股

各自为主

手机媒体

分众收购不同公司之前、各种新媒体广告 代理公司各自在自己的领域占有优势

楼宇、公寓广告

互联网

影院、超市

收购整合

手机媒体 楼宇、公寓广告

互联网 影院、超市

资本市场和投资者的压力

江南春: 资本市场不由得你,没有增长动力就无法达到投 资者的预期,不是说我们有没有竞争力的问题,是你今天 表现很好,对后面都是累赘,因为大家对你的预期很高。 所以,在后面的增长速度就不能很低。我们的压力必然很 大,不是说我们就高枕无忧了

$500,000

2003.5

2004.4

2004.11

《福布斯》

江南春以最快的速度占领当地的主要 高档写字楼,剩下的市场空间留给了

随后出现的模仿者

快速占领市场

分众凭借强大的资本力量,在全国各地迅速 高效地占有了这项稀缺性资源。2005.3,以 楼宇覆盖量计算,分众占据70%,而以液晶 电视数量比较,分众占据77%

随后分众无线旗下SP公司被取消了SP资格。2008年第一季度亏损达

5380万美元

3

资金链断裂传闻:

快速收购=> 推高股价=>继续收购

分众收购的对象包括直接竞争对手,包括未形成竞争合作伙伴,收购

分众传媒2019年决策水平分析报告

2019年分众传媒成本费用总额为974,510.29万元,其中:营业成本为 664,960.41万元,占成本总额的68.24%;销售费用为225,625.59万元, 占成本总额的23.15%;管理费用为57,607.22万元,占成本总额的5.91%; 财务费用为-1,968.99万元,占成本总额的-0.2%;营业税金及附加为 28,286.06万元,占成本总额的2.9%。2019年销售费用为225,625.59万元, 与2018年的233,100.43万元相比有所下降,下降3.21%。2019年在销售 费用下降的同时营业收入却出现了更大幅度的下降,并引起营业利润的下 降,企业市场销售形势迅速恶化,应当采取措施,调整销售战略或销售力 量。2019年管理费用为57,607.22万元,与2018年的41,219.72万元相比 有较大增长,增长39.76%。2019年管理费用占营业收入的比例为4.75%, 与2018年的2.83%相比有所提高,提高1.91个百分点。这在营业收入大幅 度下降情况下常常出现,但要采取措施遏止盈利水平的大幅度下降趋势。

0 33,365.83

0

38,804.6 108.39 18,620.8

0 18,620.8

0

26,923.03

40.15 19,209.5

22.56 15,674.17

0

1,455,283.1

1,424,040.2

2.19

47.03 968,563.81

0

2

7

内部资料,妥善保管

第2页 共6页

分众传媒2019年决策水平报告

分众传媒2019年决策水平报告

分众传媒2019年决策水平报告

一、实现利润分析

2019年实现利润为234,816.5万元,与2018年的694,193.23万元相比 有较大幅度下降,下降66.17%。实现利润主要来自于内部经营业务,企业 盈利基础比较可靠。2019年营业利润为236,601.57万元,与2018年的 695,328.78万元相比有较大幅度下降,下降65.97%。在营业收入大幅度下 降的同时经营利润也大幅度下降,企业经营业务开展得很不理想。

分众传媒分析报告

分众传媒分析报告1. 背景介绍分众传媒是一家中国领先的户外传媒公司,成立于2003年。

公司主要从事户外广告牌、公交车广告、电梯广告等传媒形式的销售和推广。

该公司在中国市场占据了重要地位,并且在海外也有一定的业务拓展。

本文将对分众传媒进行详细的分析,以深入了解该公司的业务模式、竞争优势和未来发展前景。

2. 业务模式分析分众传媒通过与房地产开发商、交通运输公司以及其他广告客户的合作,将广告牌、公交车广告等媒体资源出租或销售给客户。

该公司的主要收入来源是广告销售和租赁。

分众传媒通过自有媒体资源和与其他媒体资源提供商的合作,形成了庞大的户外媒体网络,为广告客户提供了广告展示的渠道。

3. 竞争优势分析分众传媒在中国的广告市场拥有一定的竞争优势。

其主要竞争优势包括: - 广告资源优势:分众传媒在全国范围内拥有大量的广告资源,包括广告牌、公交车广告等。

这些广告资源的分布广泛,能够覆盖到不同地区的潜在消费者。

- 客户合作关系:分众传媒与众多房地产开发商、交通运输公司以及其他广告客户建立了长期稳定的合作关系。

这些合作关系在一定程度上保证了公司的收入稳定性。

- 团队专业素质:分众传媒拥有一支经验丰富、专业素质高的团队。

他们具有市场调研、广告策划和销售等方面的专业知识和技能,能够为客户提供全方位的广告解决方案。

4. 市场前景展望分众传媒作为中国领先的户外传媒公司,未来的市场前景十分广阔。

以下是未来发展的几个趋势和机遇: - 数字化转型:随着科技的发展,传统户外广告正在逐渐数字化。

分众传媒可以通过数字化转型,为客户提供更加精准的广告投放和数据分析服务。

- 地理扩张:分众传媒在海外市场也有一定的业务拓展。

未来,公司可以继续在国内外市场扩大业务规模,进一步提高市场份额。

- 创新广告形式:随着人们对广告的接受度下降,创新广告形式将成为未来的发展趋势。

分众传媒可以通过开发新的广告形式,吸引更多广告客户并获得竞争优势。

5. 风险与挑战在市场发展过程中,分众传媒也面临一些风险和挑战: - 竞争加剧:随着市场的发展,竞争对手不断增多,市场竞争压力也越来越大。

分众传媒2019年财务分析结论报告

分众传媒2019年财务分析综合报告分众传媒2019年财务分析综合报告一、实现利润分析2019年实现利润为234,816.5万元,与2018年的694,193.23万元相比有较大幅度下降,下降66.17%。

实现利润主要来自于内部经营业务,企业盈利基础比较可靠。

在营业收入大幅度下降的同时经营利润也大幅度下降,企业经营业务开展得很不理想。

二、成本费用分析2019年营业成本为664,960.41万元,与2018年的491,649.2万元相比有较大增长,增长35.25%。

2019年销售费用为225,625.59万元,与2018年的233,100.43万元相比有所下降,下降3.21%。

2019年在销售费用下降的同时营业收入却出现了更大幅度的下降,并引起营业利润的下降,企业市场销售形势迅速恶化,应当采取措施,调整销售战略或销售力量。

2019年管理费用为57,607.22万元,与2018年的41,219.72万元相比有较大增长,增长39.76%。

2019年管理费用占营业收入的比例为4.75%,与2018年的2.83%相比有所提高,提高1.91个百分点。

这在营业收入大幅度下降情况下常常出现,但要采取措施遏止盈利水平的大幅度下降趋势。

本期财务费用为-1,968.99万元。

三、资产结构分析2019年企业不合理资金占用项目较少,资产的盈力能力较强,资产结构合理。

从流动资产与收入变化情况来看,流动资产下降慢于营业收入下降,资产的盈利能力下降,与2018年相比,资产结构趋于恶化。

四、偿债能力分析从支付能力来看,分众传媒2019年是有现金支付能力的。

企业财务费用小于0或缺乏利息支出数据,无法进行负债经营风险判断。

五、盈利能力分析分众传媒2019年的营业利润率为19.50%,总资产报酬率为12.35%,内部资料,妥善保管第1 页共3 页。

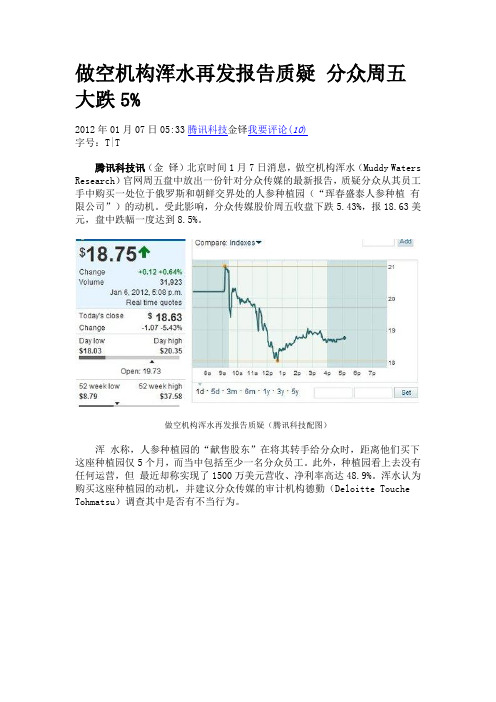

做空机构浑水再发报告质疑

做空机构浑水再发报告质疑分众周五大跌5%2012年01月07日05:33腾讯科技金铎我要评论(10)字号:T|T腾讯科技讯(金铎)北京时间1月7日消息,做空机构浑水(Muddy Waters Research)官网周五盘中放出一份针对分众传媒的最新报告,质疑分众从其员工手中购买一处位于俄罗斯和朝鲜交界处的人参种植园(“珲春盛泰人参种植有限公司”)的动机。

受此影响,分众传媒股价周五收盘下跌5.43%,报18.63美元,盘中跌幅一度达到8.5%。

做空机构浑水再发报告质疑(腾讯科技配图)浑水称,人参种植园的“献售股东”在将其转手给分众时,距离他们买下这座种植园仅5个月,而当中包括至少一名分众员工。

此外,种植园看上去没有任何运营,但最近却称实现了1500万美元营收、净利率高达48.9%。

浑水认为购买这座种植园的动机,并建议分众传媒的审计机构德勤(Deloitte Touche Tohmatsu)调查其中是否有不当行为。

盛泰人参种植有限公司注册办公室所在地(腾讯科技配图)分众传媒副总裁嵇海荣今日凌晨在微博上对此回应称:“浑水公司提出的猜疑,完全不符事实。

实际上是分众收购吉林一家加盟商叫吉林分众,吉林分众的股东在三年对价期间,去购买了一个在老少边穷地区享受很好税收优惠政策的种植公司并将业务改为LCD广告销售,之后这个公司作为吉林分众LCD业务的销售公司也成为分众的子公司”。

嵇海荣表示:“由这个公司来销售LCD广告可享受当地二年的特殊所得税优惠。

分众对吉林的整个业务收购三年总对价也就二三百万美元,三年结束后老股东之一的王峰(微博)还按此对价回购了百分之十五并继续在吉林分众担任股东及总经理。

分众下周会公告并充分地解答疑问。

”嵇海荣还表示,值得质疑的倒是浑水公司每次发报告之前一段时间总会有几家基金先知先觉地做空或购买大把看空期权,建议相关部门加以调查。

以下为报告全文:分众传媒收购位于俄罗斯和朝鲜边界的一家人参种植园表明,分众传媒的收购存在问题。

浑水对分众传媒的调研报告

Note: You should assume we have a short position in FMCN as of this report – prior to reading this reportsee important disclaimer on the last page (page 9).FMCN: Reiterating Strong SellMuddy Waters, LLCFebruary 9, 2012 Muddy Waters was Right about FMCN’s LCD Network Overstatement;Independent Verification Counted Cardboard Posters Instead of LCDsWeak Attempt at Jedi Mind Trick ExposedIn our November 21, 2011 report on FMCN, we accused management of fraudulently overstating the size of its LCD Network. FMCN had previously defined the LCD Network as a “network of flat-panel television displays.” FMCN first vehemently denied our charges that it overstated the LCD Network size, and then independently “verified” that its previously reported number of 185,174 LCD Network displays was correct. However, over 30,500 of those “verified” displays are not LCD televisions at all – rather, they are mere cardboard posters. Not only does this mean that FMCN management was brazenly lying to investors in the wake of our report, but the lies sharply call into question the veracity of FMCN’s reported financials. We estimate that each LCD television generates monthly revenue seven times that of a cardboard poster. Separately, on November 29, 2011 we pointed out that FMCN had previously grossly lied about the size of its movie theater advertising network. FMCN’s recent attempt to explain away that lie is almost as ridiculous as its conflation of cardboard with LCDs. The implication for investors is that if the inputs to the financials (network sizes) are lies, then why wouldn’t the outputs (revenue and profit) also be lies? As the old saying goes, “garbage in, garbage out.”Muddy Waters was Right All AlongIndependent “verification” proves Muddy Waters was correct when we concluded FMCN lied about the size of its LCD Commercial Display Network. In order for FMCN to meet its disclosed numbers, it had to include approximately 30,500 cardboard posters in its LCD display network count. In other words, per FMCN’s own verified data, over 15% of FMCN’s LCD network consists not of LCDs – but of cardboard.FMCN’s prior disclosures on its network make no allowance for cardboard displays. FMCN wrote the following in its 2007, 2008, 2009, and 2010 20-Fs:“Our L CD d isplay n etwork, w hich r efers t o o ur n etwork o f f lat-‐paneltelevision d isplays p laced…”11 2010 20-F pp. 38-9, 2009 20-F p. 36, 2008 20-F p. 35, 2007 20-F p.33.FMCN has made it unambiguous that “LCD” means Liquid Crystal – not Light Cardboard – Display. At least that was the case before Muddy Waters exposed FMCN’s fraud.(Based on strong evidence Muddy Waters still believes FMCN separately double counted another 32,500 Digital 2.0 displays from the poster frame segment as “LCD 2.0 Digital Picture Screens” under the LCD Network segment in order to get to its “verified” number.)We reiterate. In order to rebut Muddy Waters’s conclusion that FMCN overstated the size of its LCD Commercial Display Network, FMCN had to include 30,500 of the cardboard objects shown in the below picture (from FMCN’s website):Therefore, even putting aside the issue of whether FMCN double-counted some (actual) LCDs, FMCN overstated the size of its LCD Commercial Display Network. Muddy Waters was correct from the beginning.FMCN attempted to pull a Jedi mind trick by referring to the roughly 30,500 cardboard posters as “LCD 1.0 picture frame devices.” It strikes us that only a management with a significant degree of contempt for its shareholders would attempt to pass off a piece of cardboard as an LCD television. However, this is the same management that: •told investors its movie theater network was 17.6x the number of movie theatersin existence in China. (We discuss management’s almost-as-ridiculousjustification for this lie infra.)•traded in and out of Allyes, causing substantial losses to shareholders while generating tens of millions in profit for insiders and their friends (explaining that such insider gains were necessary to incentivize management, including soon-to-join members).• claimed to have acquired six SMS advertising companies that it in fact did not.2•Took Olympus style acquisition write downs of $1.1 billion on $1.6 billion in acquisitions.FMCN’s management either believes that investors are stupid, or that its Jedi powers are overwhelming.Muddy Waters was 100% correct that FMCN deliberately overstated the size of its LCD network. In FMCN’s responses to our reports, FMCN management has purposely deceived shareholders and analysts by including cardboard posters in the LCD count. We intend to bring this outrage to the attention of the SEC, but in the meantime we suggest FMCN now describe this network in its filings and communications as the “LCD and Cardboard Display Network.”Hidden in Plain Sight – How FMCN Used Cardboard Posters to Make its LCD NumberRemember when we asked whether independent verification in China is better than toilet paper?3 FMCN has provided its own resounding response of “NO!”On January 6th, 2012 FMCN announced that Ipsos Marketing Company completed a full count of FMCN’s LCD display network, and that FMCN currently has 185,174 displays in the network.4The problem is that 30,542 of these LCD displays aren’t LCDs at all – they’re just simple cardboard posters. FMCN ludicrously labeled these posters “LCD 1.0 picture frame devices” in five of its responses to our first report.5 In addition to cardboard having no meaningful characteristics in common with an LCD,6 a cardboard poster can hardly be called a “device.”2 FMCN claimed to have acquired parties to VIE agreements with these handset advertisers, but for numerous reasons outlined in our November 21st report, this explanation does not hold water.3 MW December 9, 2011 report reiterating Strong Sell on FMCN.4 /phoenix.zhtml?c=190067&p=irol-newsArticle&ID=1645519&highlight=5 2011: November 22 & 29, December 14 & 22; January 6, 2012.6 It’s arguably noteworthy that both contain carbon atoms.“When I use a word’” Humpty Dumpty said, in rather ascornful tone, “it means just what I choose it to mean –neither more nor less.”7On January 6, 2012, FMCN filed the 2nd amendment to its 2010 20-F. In the amendment, FMCN discusses the inclusion of the “LCD 1.0 picture frame devices” in its LCD network size count. FMCN then tells us in the amended 20-F that these are really just cardboard posters. There are numerous references to this surprising fact throughout the filing, but the most telling is:Advertisements on our poster frame network and LCD 1.0 picture frame deviceson our LCD display network consist of full-color glossy advertising postersdesigned and provided by our advertising clients.8Note that in the above disclosure, FMCN is stating that the “LCD display network” contains cardboard posters. In other words, FMCN has valmorphanized9 cardboard into LCD. Who does that???!!!FMCN’s excuse for why it gets to call cardboard by the name “LCD” is similarly laughable. FMCN claims it used the cardboard posters instead of LCDs in these 30,500 locations because adequate power to run LCD televisions was unavailable.10 (Interestingly this problem only occurs in the well-developed Tier 2 cities of Tianjin,7 Humpty Dumpty quote and illustration from Carroll, Lewis Through the Looking Glass (1872).8 2nd Amended 2010 20-F, filed January 20, 2012, p. 46.9 /define.php?term=valmorification10 2nd Amended 2010 20-F, filed January 20, 2012, p. 42, and see FMCN November 29, 2011 press releaseKunming, and Shijiazhuang,11 which have a combined population of 29.4 million12) Because these posters were installed by the LCD division, which really, really wanted to put TVs in there but (goshdarnit!) wasn’t able to, FMCN think it’s justifiable to label the posters “LCD 1.0” “devices” and include them in the LCD network count.FMCN missed its opportunity to make clear that it had cardboard posters in its LCD count prior to:•calling Muddy Waters’s conclusion that FMCN overstates its LCD Network size “unfounded”,13•spending shareholder money on two “verifications” of its LCD network size when management knew that at least 30,500 of the “LCDs” were really cardboard, and thus contradicted FMCN’s own well-established definition of “LCD”, and •threatening to sue Muddy Waters.14Putting the above behavior aside, FMCN’s purported reason for installing cardboard posters instead of LCD TVs (lack of adequate power) is obviously yet another lie.A 17-inch LCD consumes peak power of approximately 20 watts.15 A typical elevator will draw upward of 50,000 watts during operation.16 (20 watts is 0.04% of 50,000 watts.) Moreover, even a tiny elevator (5’ x 5’) would require a 40-watt light bulb to light its interior.17How on God’s great earth could FMCN not find adequate power for an LCD television in either the elevator or elevator lobby? Are these posters in mine shafts?It is unreasonable to believe that FMCN’s LCD division, with its expertise honed from installing and maintaining over 100,000 real LCDs, could not find power sources for 30,500 LCDs in three Tier 2 cities. The real reason FMCN counted 30,500 cardboard posters in the LCD network is that Muddy Waters caught the company with its pants down, and management is now trying to lie its way out of trouble.So yes, when an independent report (supposedly) verifying the size of a flat-panel television network includes over 30,500 cardboard posters in its count, the report’s contents are as valueless as non-commercial excrement. Excrement, along with a study concluding FMCN didn’t overstate its network size, is better contained in soft colorless toilet paper.11 /phoenix.zhtml?c=190067&p=irol-newsArticle&ID=1634311&highlight=12 13 /phoenix.zhtml?c=190067&p=irol-newsArticle&ID=1632858&highlight=14 See FMCN’s January 6th and 9th press releases explaining that its acquisition of a ginseng farm was nothing more than a (dodgy) tax shelter.15 /en_US/product-and-parts/detail.page?&LegacyDocID=MIGR-7193016 /downloads/10KTechGuide.pdf17 Assuming a lighting requirement of 15 lumens / sq. ft. (375 lumens), one would need a General Electric A15 incandescent 40-watt light bulb, which produces 415 lumens.We believe that the post-MW report conflation of cardboard with LCD amounts to securities fraud and a violation of GAAP segment reporting principles (carried over from SFAS 131) – we see no Humpty Dumpty defense available under 10(b)-5. In any event, those points are for Deloitte, the SEC, and courts hearing investor class actions to ultimately decide.Movie Theater Count – A Coverup Almost as RidiculousOn November 29, 2011, we showed that FMCN in 2007 and 2008 20-F filings claimed to have 27,164 movie theaters in its network when the potential size of the market (per government statistics) was only 1,545 theaters. In other words, FMCN claimed to have market share of 1,758.2%.Here is how FMCN worded (emphasis added) its obviously false movie theater count disclosure in 2008:The cost of revenue for our movie theater and traditional outdoor billboardnetwork increased 101% from $28.5 million in 2007 to $57.3 million in 2008. The increase is primarily attributable to:…3) increased leasing costs associated withtime we rent on movie theater screens as a result of an increase in the number oftheaters we lease in our network from 10,930 in 2007 to 27,164 in 2008. Following our exposure of this lie, here is management’s tortured attempt to explain it away:Prior to 2009, we calculated the size of its movie theater network by calculatingthe number of screens on which each of its advertisers had purchased advertising and then summing the screen count for each advertiser to produce an aggregatenumber of screens. 18Per this revisionist definition, management wants investors to believe that FMCN previously defined “theater” as Σ(customers x screens purchased).19 Oh but there would be so many questions unanswered if this were true! For instance, would there be a new “theater” each time a customer re-purchased time on the same screen; or, is each “theater” all customer-buys on that screen, and if so, over what period?Management offered this explanation because they twice assumed investors are stupid – first when FMCN claimed to have 27,164 theaters, and then when management thought it could redefine the plain English meaning of “theater.” Chairman Jiang, investors aren’t that stupid – if you occasionally took some buy-side investors’ questions on the earnings worship calls, you’d probably know that.2018 2nd Amended 2010 20-F, filed January 20, 2012, p. 43.19 We’re not 100% sure we understand how FMCN purports to have calculated “theaters” – trying to figure the equation out is a bit like trying to determine the GPS coordinates for Narnia.20 As we pointed out on p. 18 of our November 21, 2011 report, FMCN has not taken any buy-side questions since its Q1 2007 call.What These Lies Mean for Investors’ MoneySince our initial report, we’ve heard some investors and analysts downplay the significance of these lies,21 and instead dissemble by focusing on the great numbers FMCN is reporting. However, because the lies about the number of LCD televisions and movie theaters in the network were used to support growth in reported revenues and profits, one has to wonder whether reported numbers are real. This is particularly true because we estimate that the average LCD television generates monthly revenue seven times that of a cardboard poster. Why would FMCN lie about the inputs to the numbers without also lying about the outputs?Our concern about whether FMCN’s core business numbers are accurate is most acute because FMCN’s LCD and cardboard display network business is opaque in the two areas that matter most – advertisement ASPs and location lease costs.FMCN’s LCD and cardboard display network business model is highly opaque on the revenue side. FMCN’s rate card is irrelevant to the revenues that FMCN generates because most customers receive a substantial discount from the rate card. The problem is that it is impossible to independently determine the discount levels.In the course of our research, we determined that the minimum discount offered to customers for Tier 1 advertisements is approximately 65% off the rate card. We believe that there are customers that receive Tier 1 ad discounts of more than 90% off the rate card. Further, we found that the discounts on Tier 2 ads are greater than those of Tier 1. We also found that most Tier 3 and 4 ads are usually free.There is no way to independently determine the weighted average discount by tier. It is therefore impossible to independently determine FMCN’s ASP. You have to take management at its word. We don’t.The screen location lease costs vary widely, and it is impossible to independently verify FMCN’s reporting of these numbers. In our research of location costs in Shanghai Class A office buildings, we found that FMCN pays anywhere from approximately $50 (RMB 300) per screen per month to $1,500 (RMB 10,000) per screen per month. Presumably the screens in residential buildings cost less, but we found it difficult to develop a reliable blended estimate. Because screen location lease costs can vary by orders of magnitude between similar locations, they cannot be independently verified. Thus, you have to take management at its word. Again, we don’t.21 We heard one second hand account of a conversation between an investor and an analyst with a major bank. We were told that during the conversation, the analyst claimed to have previously noted that the theater count was implausible, yet the analyst never became concerned about FMCN as a result.This management has demonstrated time and again that it should not be taken at its word. Further, the over the top nature of these lies paints the picture of a management who views its investors and analysts as gullible and worthy of contempt. We believe that the opacity of FMCN’s business model offers far too great of an opportunity for this management, with its demonstrated track record of lying and self-dealing, to play games with the numbers.AcknowledgementWhile we were satisfied that FMCN was double-counting the LCD 2.0 Digital Picture Screens to make its reported LCD network screen count, we had not caught FMCN’s admission that it needed to count over 30,500 cardboard posters in order to make its number. (The key information was largely buried in the recently filed 2nd amendment to FMCN’s 2010 20-F.)The credit for this observation belongs to published author and Seeking Alpha contributor Matt Berry. (Interestingly, Mr. Berry’s book is a guide to righteous behavior. We have expressed a copy of Mr. Berry’s book to Chairman Jiang.)22In an article published on February 6th, Mr. Berry called FMCN out on the LCD screens and the ridiculous explanation the company offered for its movie theater lie. We were impressed by both Mr. Berry’s analysis and use of sarcasm – particularly in equating FMCN’s conflation of cardboard and LCDs to conflating Ferraris and bicycles. Mr. Berry, our hat is off to you.WARNING: A printout of this Report is not a CRT Display22 Mr. Berry authored The Mechanics of Virtue: A Cynic’s Guide to Righteous Behavior, CreateSpace (Dec. 2009).DisclaimerUse of Muddy Waters LLC’s research is at your own risk. You should do your own research and due diligence before making any investment decision with respect to securities covered herein. You should assume that as of the publication date of any report or letter, Muddy Waters, LLC (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a short position in the stock (and/or options of the stock) covered herein, and therefore stands to realize significant gains in the event that the price of stock declines. Following publication of any report or letter, we intend to continue transacting in the securities covered therein, and we may be long, short, or neutral at any time hereafter regardless of our recommendation. This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Muddy Waters, LLC is not registered as an investment advisor. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Muddy Waters, LLC makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Muddy Waters, LLC does not undertake to update or supplement this report or any of the information contained herein. Before viewing the contents of this report, you agree that any dispute arising from your use of this report or viewing the material herein shall be governed by the laws of the State of California, without regard to any conflict of law provisions. You knowingly and independently agree to submit to the personal and exclusive jurisdiction of the superior courts located within the State of California and waive your right to any other jurisdiction or applicable law, given that Muddy Waters, LLC has offices in California. The failure of Muddy Waters, LLC to exercise or enforce any right or provision of this disclaimer shall not constitute a waiver of this right or provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to use of this report or the material herein must be filed within one (1) year after such claim or cause of action arose or be forever barred.。

分众传媒主业经营现状及对浑水作空报告的再分析

分众传媒主业经营现状及对浑水作空报告的再分析本文主要对分众传媒近几年尤其是回归A股后的经营情况、主营业务、业务模式进行深度分析,在次基础上,对2011年浑水作空公司的几方面原因进行再回顾,找到公司的投资价值及风险因素。

一、公司经营现状1.1 营收情况2015年公司实现营业收入86.27亿元,净利润33.89亿元,分别增长15.07%和40.35%,实现扣非后净利润30.69亿元,同比增长44.5%,超过2015年承诺业绩29.59亿元,经营性净现金流26.3亿元,ROE高达73.7%。

2016年上半年公司实现营业收入49.27亿元,同比增长22.40%;归母净利润19.01亿元,同比增长23.58%。

对于2015年年报,公司净利润增速高于收入增速,公司解释如下:从公司运营看,稳定及有经验的管理团队通过媒体资源的持续优化、媒体运营成本的有效控制和媒体运营效率的提升,实现在相对增长有限的成本下的媒体覆盖率和刊挂率稳步提升。

与此同时,由于公司旗下各媒体在市场份额上的处于主导地位,在主营业务成本最重要的构成部分媒体租赁成本上拥有很强的议价能力,因此运营成本上升幅度较为有限,低于营收增长速度,因此2015年净利润增长率40.35%高于主营业务收入的增长率15.07%。

简单理解就是公司各项成本控制较好,而刊挂率及媒体覆盖率提升,导致毛利率提升,净利润增速高于收入增速。

数据来源:公司公告按照2014 年我国全媒体渠道广告收入计算,分众传媒广告收入位列第6 位,仅次于BAT 和两大电视媒体平台(CCTV&湖南卫视)。

但从增速看,以BAT为代表的互联网广告增速较快,而以CCTV、湖南卫视为代表的电视广告增速较慢。

表1 各广告媒体营收TOP15(按2014 年排列;亿元)数据来源:各公司财报、中国广告协会、艾瑞、CTR1.2 营收结构公司主要产品为楼宇媒体(包含楼宇视频媒体和框架媒体)、影院银幕广告媒体、卖场终端视频媒体等。

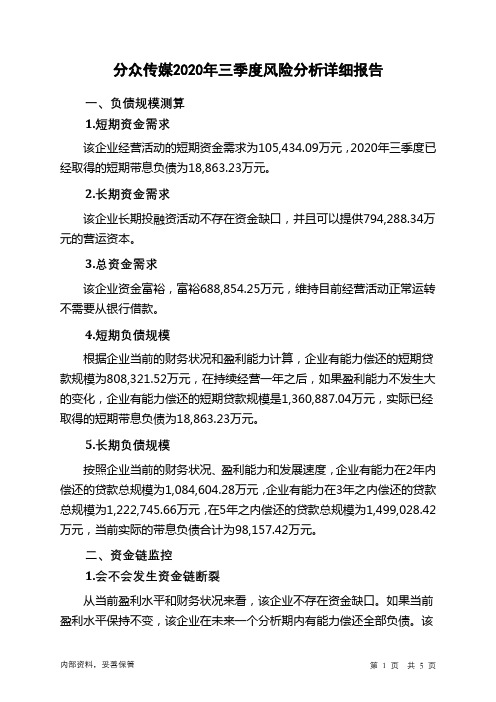

分众传媒2020年三季度财务风险分析详细报告

分众传媒2020年三季度风险分析详细报告

一、负债规模测算

1.短期资金需求

该企业经营活动的短期资金需求为105,434.09万元,2020年三季度已经取得的短期带息负债为18,863.23万元。

2.长期资金需求

该企业长期投融资活动不存在资金缺口,并且可以提供794,288.34万元的营运资本。

3.总资金需求

该企业资金富裕,富裕688,854.25万元,维持目前经营活动正常运转不需要从银行借款。

4.短期负债规模

根据企业当前的财务状况和盈利能力计算,企业有能力偿还的短期贷款规模为808,321.52万元,在持续经营一年之后,如果盈利能力不发生大的变化,企业有能力偿还的短期贷款规模是1,360,887.04万元,实际已经取得的短期带息负债为18,863.23万元。

5.长期负债规模

按照企业当前的财务状况、盈利能力和发展速度,企业有能力在2年内偿还的贷款总规模为1,084,604.28万元,企业有能力在3年之内偿还的贷款总规模为1,222,745.66万元,在5年之内偿还的贷款总规模为1,499,028.42万元,当前实际的带息负债合计为98,157.42万元。

二、资金链监控

1.会不会发生资金链断裂

从当前盈利水平和财务状况来看,该企业不存在资金缺口。

如果当前盈利水平保持不变,该企业在未来一个分析期内有能力偿还全部负债。

该

内部资料,妥善保管第1 页共5 页。

浑水报告自媒体主讲人简介

浑水报告自媒体主讲人简介

【实用版】

目录

1.浑水报告的背景与意义

2.自媒体主讲人的简介

3.对浑水报告的评价与看法

正文

浑水报告是一份备受关注的报告,它揭示了一些公司财务造假的真相,对市场产生了深远的影响。

这份报告出自一位自媒体主讲人之手,他的身份和背景引发了人们的关注。

这位自媒体主讲人,他的名字并未在文本中提及,但他的经历和专业知识却让人印象深刻。

他有丰富的金融行业经验,对公司财务分析有着深入的理解和独到的见解。

他以自媒体的形式,向公众普及财务知识,帮助投资者识别风险,保护自己的权益。

浑水报告的出台,展示了这位自媒体主讲人的专业素养和责任感。

他的行为,对于维护市场的公正和公平,保护投资者的权益,起到了积极的作用。

他的行为,也得到了广大投资者的认可和支持。

然而,这位自媒体主讲人的行为,也引发了一些争议。

有人认为,他的行为侵犯了公司的隐私权,给公司带来了不必要的困扰。

但是,更多的人认为,他的行为是正义的,是在维护市场的公正和公平。

总的来说,这位自媒体主讲人的行为,是值得我们赞扬和学习的。

他的专业素养和责任感,为我们树立了一个好的榜样。

第1页共1页。

浑水搅局分众

兀 。

是夜 注定无 眠 。当天上 午 9 , 点 江

兵 来 将 挡

一

南春 紧急召集公司高管 商议应对之

根 财务和律 如既 往 , 水率 先 挑起 战 火 , 浑 打 策 。 据高 管们准 备的 材料 , 师 立 即着手 撰 写 回应声 明 ;分众 的首 了分众 一个措 手不 及 。

费用不菲。 数匿名调查机构都会与做空基金合作,因此一般在公开发布质疑报 股东损失对企业来说 ,

告 前一 至两个 星 期 , 已经有合 作 的做 空基 金入 场 持有 看空 期权 了 , 就 猎 杀成 功后双 方 利益共 享 。

这还只 是冰 山一 角。

一

在 巨额 利益 的推动 下 ,。统计显 示 , 仅在 21 年就 有超 过 2 起 , 01 0 占美 国 证券 类集 体诉讼 案件 的 四分 之一 左右 。

从 上午 1 点 半直 至 下 午 , 0 嵇海 荣

出 ,分 众在 美 股价 应 声暴 跌 ,开盘 价 的座 机 和手机 几乎 被媒 体打爆 。 当天下 午 5点 , 在 媒 体截 稿 前 , 赶 2. 美元 ,盘中一度下探至 8 9 5o 5 . 美 7

元 , 幅近 6 %! 跌 6

21 年 1 2 01 1月 1日,浑水在美抛 席财务官和投资者关系部负责人与投

出一 份 长达 8 页 的研 究报 告 , 指分 资人沟通 ;嵇海荣则带领公关部联络 0 直

众传 媒虚 报数 据 、 高溢 价 收购 、 交 媒 体 。 内幕

易三 宗罪 , “ 并 强烈 建议 卖出 ” 。消息一

分众正式发布 一份简短的中文声明 ,

第一现场

SP OT

江南春“浑水之战”:分众反猎杀浑水做空失利

江南春“浑水之战”:分众反猎杀浑水做空失利 2011年11月27日 09:13 中国经营报微博江南春(微博)怒了!北京时间2011年11月22日凌晨,纳斯达克股票市场,分众传媒(Nasdaq:FMCN)以每股23.1美元开盘后就一路狂跌,最低报每股8.79美元,降幅一度高达66%,13.6亿美元市值一日蒸发。

股价暴跌原因是国际做空机构浑水公司(Muddy Waters)发布了一份有关分众传媒的研究报告,将分众传媒描述为“中国的奥林巴斯(微博)”(11月8日,奥林巴斯被爆出财务造假丑闻),股票定为“强烈卖出”级别。

“这种到处造谣,联手做空基金恶意图利的人为什么没人告他们呢?这些人应该得到法律的惩处!!!”此后江南春第一时间发微博,一连用了三个惊叹号,愤怒之情溢于言表。

截至《中国经营报》记者发稿日,分众股票表现已经部分回暖。

一份报告导致分众传媒股价暴跌,此事系人为作局,还是江南春体系危局被暴露?“浑水”再摸鱼作为此事的主角之一——浑水公司(Muddy Waters)想必大家并不陌生,它曾是做空中国概念股的主要幕后策划者。

2011年年中,正是在这家公司的运作下,导致东方纸业(ONP)、绿诺科技(RINO)、多元环球水务(DGW) 和中国高速传媒(CCME)等四家在美国上市的中国公司股价大跌,最终导致被交易所停牌或摘牌。

这一次,浑水再次做空,摸到的鱼是中国第一只在纳斯达克上市的中国传媒概念股——分众传媒。

在一份长达79页的报告中,最令人印象深刻的字眼就是:分众传媒财务问题堪比奥林巴斯。

报告指出:像奥林巴斯一样,分众传媒在收购中,故意显著地支付过高的收购价,自2005年以来在价值16亿美元的收购中,通过这种行为减记11亿美元,这相当于分众传媒目前市值的1/3。

“我们的研究显示,分众传媒对一些从来没有实际购买的公司,声称收购、减记和处置它。

投资者应关注这些交易中现金的实际流向,及其报告结果的可靠性。

”浑水公司的报告原文如是表达。

做空机构浑水质疑分众传媒报告全文摘译

做空机构浑水质疑分众传媒报告全文摘译imeigu2020-11-22 20:50:37来源:(i美股讯)北京时刻11月22日消息,做空机构浑水(Muddy Waters Research)周一发布对分众传媒首份报告,给予其“强烈卖出”评级。

受该报告阻碍,分众传媒股价暴跌39.49%收报15.43美元,创下52周新低。

浑水公司团队今年夏天对分众公司进行详尽调查,调查内容包括分众所有公司的中国工商局文件、SEC报告和会议和所有公布新闻稿。

另外,该团队进行了实地的田野调查,和多位产业专家进行访谈。

i美股摘译浑水质疑报告全文,要紧分为三个部份:第一部份:分众LCD显示屏的数量和成效均被高估1,观点:分众将其拥有的LCD显示屏高估了约50%-分众表示截止今年三季度末,其拥有178382个LCD显示屏;-浑水公司调查显示:分众只有12万个屏幕,包括大约1.5万个是通过经销协议取得。

那个数量与分众2007年年报发布的112298个屏幕接近。

2, 观点:分众对其在一线城市的显示屏数量高估了约67%-分众表示其在一线城市显示屏超过5万个,且其LCD网络营收的60%来自于一线城市。

-浑水公司调查显示:事实上少于3万个。

分众表示其拥有所有的一线城市屏幕网络,但事实上分众在北京的10%的显示屏是由经销商运营。

一线城市的广告有效率较二线城市高出约141.9%;分众大约5万个显示屏(超过屏幕总量的40%)在三四线城市,调查表示很少有广告商情愿在这些三四线城市投放广告,且营收潜力超级小;这些屏幕的投资总额大约2000万美元,屏幕网络的运营费用(尤其是升级到每周人工改换存储卡)不低。

3,观点:分众的大多数屏幕均不在营收能力更大的商业办公楼宇-分众表示大多数LCD地处于交通繁华的商业办公楼宇;-浑水公司调查显示:分众仅有约总屏幕数的30%处于商业楼宇。

在一线城市,仅有45%的屏幕在商业办公楼宇;二线城市,仅有30%屏幕在商业办公楼宇;其他均在住宅楼宇。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

解读浑水关于分众传媒的报告

先说明清楚,大家没必要过分去迷信国外机构,因为我们认为浑水(Muddy Waters)这份报告有很多不

足的地方。

不过,对于投资者来说,它这份报告里面提了很多个硬伤,足以让投资者警醒。

浑水22号出来这份报告,我们发现国内真正去认真把这份报告读完的人居然没几个,至少在网上我们是没有看

到真正读完这份报告的人,可见风气之浮躁。

想赚钱的人,还是下些功夫吧,回报和你的付出是成正

比的。

这份报告指出来分众传媒两个问题:虚增屏幕数量(算是经营数据造假)和公司高管掏空上市公司。

里面涉及了当今互联网几个大佬(江南春、沈南鹏等)——这一点怕是国内的媒体都没注意的吧?我

们担心的是,如果这个事情持续发酵,届时美国证监会和司法机构介入的话,那牵扯的事情就大了。

就目前的情况而言,我们估计分众传媒不会把事情闹到法庭上,至于美国那边的投资者会不会这么干,就不知道了,这些大佬们肯定不想看到事情整到法律层面上去。

其实,如果企业是真正有料的,绝对

不用担心做空者的袭击,像展讯通信那样被浑水出报告做空,当天打到8块多美元,之后不但收涨回

跌幅,还涨到29块创出历史新高,浑水反而成了多头的助手。

另外,我们博客纯属个人的看法,没有牵扯到任何个人利益进来,没有买卖分众传媒的股票。

还有,

我们的博文被一些媒体抄袭已经不是一天两天的事了,希望有点良心尊重一些我们码字的汗水,至少“引用”的时候也提前告知一声吧。

事情简介

2011年11月22日浑水出具一份长达80页的报告,质疑分众传媒(NASDAQ: FMCN)经营数据造假

以及高层掏空上市公司,并给出“强烈推荐卖出”的评级,导致分众传媒股票暴跌40%,最低价曾到

8.79美元。

随后,分众传媒当夜提出驳斥,否认所有指控。

而后,美国一家大投行也出面力挺分众传媒,指其目标价46美元不变。

过后,浑水的网站被黑,但是它依然写着“分众传媒依然给强烈卖出的

意见”。

简单解读

浑水主要是指责分众传媒经营数据造假和高管掏空上市公司两大罪状。

1.经营数据造假

浑水指出三点:

•分众传媒2011年9月30日宣称自己的终端网络共有178,382块LCD屏,经浑水12位员工约半年时间的查证,分众传媒只拥有不超过120,000块LCD屏,只有他公布数据的67%;

•分众传媒宣称在一线城市有50,000块终端显示屏,实际不足30,000块,超过40%的显示屏分布在三四线城市,其广告宣传效果显然比一线城市差很远。

•分众传媒宣称绝大多数的LCD屏布局在“人流量密集的商业办公楼”,但事实上只有30%的显示屏是在商业办公楼,其中一线城市的显示屏有45%分布在商业办公楼,二线城市有30%分

布在商业办公楼。

整体来看有70%的终端显示屏分布在居民住宅楼,广告效果显然要逊于在

商业办公楼。

我们认为,由于浑水并没有给出他们所得这些数据的直接证据,这里的指责很难去推断。

分众传媒随

后的回应是说它的广告牌不仅包括LCD屏,还包括一些户外海报等。

但是这件事如果被分众传媒各客户认可,那他们有足够的理由去怀疑分众传媒的广告媒介网络分布,那以后分众传媒的议价能力会被

大大削弱,对分众传媒的经营会造成严重的负面影响。

2.高管掏空上市公司

浑水指出:分众传媒自2005年在纳斯达克上市之后先后收购大量的公司,但所有的收购都是分众传媒高层导演的掏空上市公司的把戏。

根据报告,我们总结了以下几种操作手段:

•高溢价收购内部人士的公司,并确认大量的“商誉”,所谓商誉就是收购金额超过净资产的部分。

然后基本在收购后一年内即对商誉计提大量的减值,有时甚至将收购的资产减记为“零”。

最

后分众传媒会处置掉这些“减值的资产”,会低价卖回给出让方/内部人士,或者将“减记到零”

的资产白送给出让方/内部人士。

至少有21家被收购的公司最终减记至“零”,然后白送给出

让方/内部人士。

•有6宗“莫须有”的收购,根本没有真正发生过的,也通过上述方法使内部人士“空手套白狼”。

•在收购目标公司时,承诺为目标公司清偿巨额的负债。

很容易想到,那个巨额负债的债主必然是分众传媒的某位高层人员。

相比我们了解过的A股某些公司的做法,分众传媒的手段其实很简单(在美国的资本市场上还用简单

手法,那真是找打了),说白了就是“高买低卖”,亏了公司,肥了个人。

通过这种方法,内部人士至

少套现了17亿美元,合计约108亿人民币。

这些减记在收购后很短的时间内就做出减记——比如好耶

就在收购后半年减记了,是非常不合常理的做法,很可能就是为了规避审计。

涉及的内部人士分别有Jason Jiang(江南春); Neil Shen(沈南鹏); Xiong Xiang Dong(熊向东)等。

如表1所示,我们摘抄了分众传媒金额较大的几个收购案例,感兴趣的朋友可以自己去翻阅浑水的报告,里面记载了大量的细节,甚至在最后的附件中浑水都还贴出了收购合同的扫描件。

说实话,虽然分众传媒出来否认了,但是否认的理由是很不给力的。

浑水在里面列举了大量的事实以说明分众传媒的失败收购是有意的,而分众传媒只是简单把这些失败的收购归类到市场因素等客观层面。

表1 分众传媒金额较大的收购案例

资料来源:Muddy Water

分众传媒在运作这些项目的时候涉及大量的人员,关系极为复杂,我们不再做过的介绍,仅摘抄了浑水报告中的一张人物关系图,感兴趣的朋友可以深究一下。

值得注意的是:里面还涉及到多家在美国的上市公司(主要是沈南鹏那边的),包括如家、携程、博纳、新浪等。

分众传媒是迄今为止被这些做空力量狙击的最大的中国公司了,要说浑水和其背后的一些机构只看上分众传媒,那是不可能的,我们相信这些企业也一样会被他们盯上。

图1 分众传媒人物关系图

资料来源:Muddy Water。