微软公司平衡计分卡架构

平衡计分卡的基本框架和应用步骤

平衡计分卡(Balanced Scorecard)是一种综合性的管理工具,能够帮助组织制定和执行战略,监督和指导组织运营活动,改善绩效评价体系。

下面将介绍平衡计分卡的基本框架和应用步骤。

一、平衡计分卡的基本框架1.财务视角财务视角是平衡计分卡的一个重要组成部分。

在这个视角中,组织关注的是通过提高利润、降低成本等方式实现财务目标,并且要求持续地提高其财务绩效。

2.客户视角客户视角是平衡计分卡的第二个关键要素。

在这个视角中,组织需要明确客户的需求和期望,以提高客户满意度并增加客户忠诚度。

3.学习与成长视角学习与成长视角是平衡计分卡的第三个关键要素。

在这个视角中,组织关注的是持续改进和学习,包括员工的培训与发展、技术创新等。

4.内部流程视角内部流程视角是平衡计分卡的第四个关键要素。

在这个视角中,组织需要关注关键业务流程的改进,提高效率和减少成本。

二、平衡计分卡的应用步骤1.明确战略目标组织需要明确自己的战略目标,并将其转化为具体的绩效指标。

这些绩效指标需要涵盖财务、客户、学习与成长、内部流程等方面。

2.制定策略地图接下来,组织需要制定策略地图,将战略目标与具体的行动计划进行对应。

通过策略地图,组织可以清晰地把握自己的战略逻辑,并且明确不同绩效指标之间的因果关系。

3.制定绩效指标在制定绩效指标的过程中,需要注意指标的选择要具备SMART原则,即具体、可衡量、可达成、相关性和时限性。

要求绩效指标之间应该相互协调,相互促进。

4.制定行动计划在制定行动计划的过程中,需要将策略地图和绩效指标转化为具体的行动措施,包括资源的分配、责任的明确等。

5.实施和监控组织需要执行行动计划,并对绩效指标进行监控和评估。

通过不断地监控和反馈,组织可以及时调整自己的战略,确保其能够持续地提高绩效。

以上就是关于平衡计分卡的基本框架和应用步骤的介绍。

平衡计分卡是一种强大的管理工具,能够帮助组织实现战略目标,并保持持续的竞争优势。

希望以上内容能够为您带来一些帮助。

平衡计分卡概述(PPT 94张)

内部流程 角度

供应 生产 销售 服务 风险管理

内部

优化客户服务 • 顺畅的跨事业部服务 • 高效的客户服务 业务增长 • 低制度化机会带来的额收益 • 商业机会优化 • 创新性服务开发 • 引入联盟和合资项目 • 跨事业部研发协调 • 确保市场驱动能力 • 行业领先的雇员满意度 • 世界级的有效领导力

战略地图 自上而下的分解过程:

企 业 总 战 略

财务层面的战略目标 顾客层面的策略选择 内部流程的策略目标

学习与成长的战略目标

战略地图 自下而上的支持和反馈:

企业总战略

财务层面的战略目标

顾客层面的策略选择

内部流程的策略目标

学习与成长的战略目标

如何设计编制战略地图

• • • • • 明确最高目标 先在四个纬度里面找目标指标还是先构造因果关系链条 集体研讨,根据长期战略、中期战略、短期战略构造因果关系链条 确定重要的因果关系 描述战略主题

2. 调整客户价值主张 – 阐明目标细分市场 – 阐明客户价值主张 – 选择指标 – 使客户目标和财务增 长目标协调 3. 确定价值提升/持续 性结果规划时间表 – 制定缩小价值差距的 时间表 – 把价值差距分配给不 同的战略主题

4. 确定战略主题/关键成功 5. 提升战略资产准备度 /确定协调无形资产 要素和流程 – 确定对战略实现有重 要影响的少数关键流 程(战略主题) – 设定指标和目标值 – 确定支持战略流程所 要求的人力、信息和 组织资本 – 评估支持战略的资产 准备度 – 确定指标和目标值

内容

1 2 3 4

平衡计分卡关键概念

开发战略地图 构建业绩评价体系

BSC/KPI/MBO比较

平衡计分卡的历史发展 • 创始人:卡普兰与诺顿博士

平衡计分卡

平衡计分卡

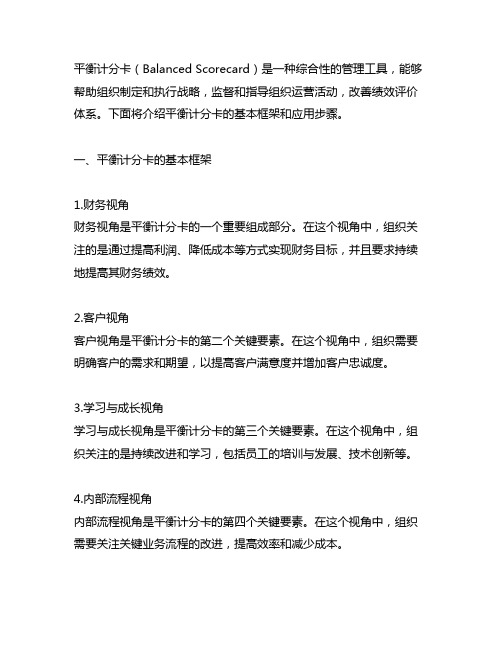

一、平衡计分卡的基本框架

平衡计分卡(The Balanced Score Card,简称BSC)从财务、客户、内部流程、学习与成长四个角度分解、落实战略,将战略转变为具体的目标和行动。

基本框架如下:

二、平衡计分卡四个平衡

运用平衡计分卡对战略目标进行分解,应做到四个平衡:长期指标与短期指标的平衡、内部指标与外部指标的平衡、财务指标与非财务指标的平衡、驱动指标与结果指标的平衡。

三、平衡计分卡总体结构

▪ 战略图:一种用直观的方法呈现组织战略的工具 ▪ 战略目标:对战略的具体组成部分的陈述 ▪ 衡量指标:是跟踪和监控战略目标完成情况的方法 ▪ 目标值:是某一个指标的期望值水平

▪ 行动方案:为了完成某项战略目标,或提高某个指标 的目标值所制定的关键行动计划

愿景。

简述平衡计分卡的框架

简述平衡计分卡的框架平衡计分卡是一种广泛应用于企业管理的战略工具,它将企业的战略目标转化为具体的关键绩效指标,以此衡量企业的绩效和创建跨部门协作的环境。

这个框架由四个关键的视角和四个关键维度组成。

第一个视角是财务视角。

在这个视角下,平衡计分卡主要关注企业如何提高财务绩效。

在衡量财务绩效时,需要定义一些关键的指标,如营收、毛利率、净利润率、现金流等。

这些指标能够直接显示企业财务状况的健康度。

第二个视角是客户视角。

在这个视角下,平衡计分卡关注的是企业如何满足客户的需求。

对于客户来说,企业提供的产品或服务的质量、周期和价格等显然是非常关键的因素。

因此,企业需要定义一些关键的指标,如市场份额、客户满意度、客户投诉率和产品质量等。

第三个视角是内部流程视角。

在这个视角下,平衡计分卡关注的是企业的流程效率和质量。

在企业中,各种不同的流程都需要被考虑,如生产、物流和销售等。

此外,企业需要定义一些关键的指标,如研发周期、产品交货率、生产效率和成本效益等。

第四个视角是学习与成长视角。

在这个视角下,平衡计分卡关注的是企业如何提高人员的技能和知识水平,以及如何增强企业的创新性。

这个视角也可以称之为学习视角。

企业需要定义一些关键的指标,如员工满意度、培训率、知识管理和创新激励等。

总之,平衡计分卡是一个全面而有指导意义的战略工具,它能够帮助企业进行战略管理、绩效管理和跨部门协作。

如果企业能够合理定义关键指标,并据此制定相应的战略和行动计划,那么平衡计分卡将成为企业成功的关键因素之一。

微软平衡计分卡架构详细介绍

制定关键绩效指标

添加标题

添加标题

添加标题

添加标题

分解目标:将战略目标分解为可操作的具体目标

明确战略目标:根据企业战略,确定关键绩效指标

确定权重:根据重要程度,为每个具体目标设定合理的权重

制定行动计划:为实现每个关键绩效指标,制定具体的行动计划

促进跨部门协作:平衡计分卡将不同部门和团队的目标整合在一起,促进跨部门协作

改进决策制定:平衡计分卡提供全面的绩效数据,帮助决策者做出更明智的决策

增强员工激励:通过平衡计分卡将员工绩效与奖励相结合,激发员工积极性和创造力

经验教训总结

经验教训总结

解决方案和实施效果

实施过程遇到的问题和挑战

案例背景介绍

感谢观看

优化绩效指标体系以提高员工积极性和工作效率

鼓励员工提出改进意见,共同完善绩效指标体系

微软平衡计分卡架构优势与局限性

06

优势:促进战略目标与绩效指标的紧密结合;有助于提高组织整体绩效;有利于组织长期发展。

微软平衡计分卡架构能够将组织的战略目标与绩效指标紧密结合,确保员工的行为与组织目标保持一致。 通过明确、量化的绩效指标,组织能够更好地了解业务状况,及时调整战略方向,确保目标的实现。 微软平衡计分卡架构还提供了强大的数据分析功能,帮助组织深入了解业务数据,为决策提供有力支持。 有助于提高组织整体绩效有助于提高组织整体绩效微软平衡计分卡架构能够全面评估组织的绩效,不仅关注财务指标,还考虑客户满意度、内部流程、学习与成长等多个方面。 通过平衡计分卡,组织能够发现潜在的问题和机会,及时采取措施加以改进,从而提高整体绩效。 微软平衡计分卡架构还鼓励员工参与决策和制定目标,激发员工的积极性和创造力,提高工作效率。 有利于组织长期发展有利于组织长期发展微软平衡计分卡架构着眼于组织的长期发展,通过制定具有挑战性的目标,激发员工的潜力,为组织的长远发展奠定基础。 平衡计分卡还强调员工的学习与成长,鼓励员工不断提升自身能力,为组织的持续发展提供源源不断的动力。 通过定期评估和调整平衡计分卡的目标和指标,组织能够适应不断变化的市场环境,确保长期发展的稳健性。

微软公司平衡计分卡架构概述0

ห้องสมุดไป่ตู้

Six Sigma) 系統擴充之容易度

Microsoft® BSC framework

微軟平衡計分卡架構

個人化的 入口網站

知識管理 e-Learing 微軟

最佳實例

平衡計分卡

可執行與 可運作 的工具

架構

策略與矩陣 管理

商業智慧

個人化的入口網站

Scoreboard 平衡計分卡摘要

可執行與可運作的工具

微软公司平衡计分卡架构概 述0

Click to edit Master title style

Click to edit Master subtitle style

BSC架構所應須具備的條件

提供發展 BSC 的指導原則 & strategy-focused metrics

彈性的展現方式(策略與矩陣管理) 多樣化的資料存取方式 (Multiple Data Source) 整合分析的能力, 例如 OLAP Reports 可執行與可運作的工具 (Actionable tools) 整合教育訓練與溝通 KM: 知識管理, BSC相關文件的管理 與其他系統的整合(例如 ERP, BI, ISO 9000,

DemoMicrosoft BSC Toolkit

Underlying Concepts

一系列技術,工具與最佳實例的組成 讓企業使用熟悉的工具來加速BSC的建置 BSC 不是 software package, 而是可延伸

的發展平台 整合現有系統與 BI 系統 彈性, 開放, 具發展空間的架構 時效性, 低成本, 可延展, 易管理

微软平衡计分卡架构(ppt)1

下页更精彩

我们的加盟优势:

如需要了解,请咨询QQ:1097251560, 淘宝标准加盟样榜店: /

1、不受地域限制,无须存货,无资金压力及风险。 无能您是在中国的任何一个城市,都可以在网络上代理销售我们的产品, 你无须自己存货,我们可以从我们的产品仓库帮你发货,您只需把你的顾 客地址告诉我们就可以了。 2、无需专业技术,只要你每天有上网的时间都可以做。 您只要有一个淘宝帐号,我们可以帮你装修网店及提供推广的技术指导, 你只要每天挂上QQ及旺旺接受客户咨询及订单就可以了,当你收到客户的 货款后,直接安排我们给客户发货就行了。 3、收入丰厚 加盟我们的客户新手一般第一个月的收入都有1000左右, 爱学习,了解网店经营的一般的三个月内能达到有上万元的月收入。

Measures

Targets

Initiatives

學習與成長

驅動未來績效

Source: The Balanced Scorecard Collaborative

各事業體 Strategy & BSC的連結

Group Balanced Scorecard

SBU1 SBU2 SBU3

SBU Scorecards

Measures Targets Initiatives

財務

“To satisfy our Objectives shareholders and customers, what business processes must we excel at?”

股東與顧客的外界衡量

“To achieve Objectives our vision, how should we appear to our customers?”

主要績效指標(Key Performance Indicator, KPI):策略目標進 程或關鍵流程的衡量基礎,且必須是可數量化的

微软平衡计分卡架构4

quickstartsps.asp

For information about the Balanced Scorecard:

The Balanced Scorecard Collaborative: http:// The Balanced Scorecard Institute http://

Case Study

Microsoft Scorecard Portal

HTML Foundation Knowledge Base

Collaborative Interface

Key Metrics

Discussions

Drill Down Detail

Strategic Initiative

Realizing Your Business Potential

Processes

Technology Strategy

•

1、有时候读书是一种巧妙地避开思考 的方法 。20.9. 2120.9. 21Monday, September 21, 2020

•

2、阅读一切好书如同和过去最杰出的 人谈话 。07:2 4:0307: 24:0307 :249/2 1/2020 7:24:03 AM

•

9、一个人即使已登上顶峰,也仍要自 强不息 。上午 7时24 分3秒上 午7时2 4分07: 24:0320 .9.21

• 10、你要做多大的事情,就该承受多大的压力。9/21/2

020 7:24:03 AM07:24:032020/9/21

• 11、自己要先看得起自己,别人才会看得起你。9/21/2

ate Investment Trust (REIT) 員工人數: 1600 每年收入: $1.3 billion

微软平衡计分卡架构汇总(7个doc)8

1990年研究計劃 – 未來組織績效衡量方法,12家企業共同參與 由哈佛教授 Robert Kaplan與Nolan Norton Institute執行長David Norton所共同研究發展

1992年:發表 BSC 1993年:發表 BSC的實踐 1996年:發表 BSC在策略管理體系的應用 2000年:發表 企業的策略性的應用

BSC Management Process

建構績效管理制度與平衡計分卡

發展平衡計分卡之步驟

釐清策略

經營環境 願景與使命 營運方針目標

業務策略 經營模式

設計平衡計分卡

財務構面策略目標 客戶構面策略目標 流程構面策略目標 學習構面策略目標

各構面KPI 策略地圖 & 因果關係圖

K00

“Using the Balanced Scorecard as a Strategic Management System”, Jan-Feb 1996

“Having Trouble With Your Strategy? Then Map It”, Sept-Oct 2000

Recognized by the Harvard Business

Measuring Success

Bringing the Balanced Scorecard to Life

微軟技術顧問服務部 Laura Huang 黃淑翠

“If you can’t measure it,

you can’t manage it.”

若您無法衡量企業經營績效 您便無法有效管理企業

建構平衡計分卡與績效管理制度

定期討論與回饋

KPIs 資料收集 與衡量

BSC KPI, 策略, 目標設定

平衡计分卡框架

平衡计分卡框架平衡计分卡框架(Balanced Scorecard)是一种管理工具,旨在帮助企业在战略层面进行管理和衡量绩效。

它的设计理念是从四个角度来考虑企业的绩效指标,分别是财务、客户、内部业务流程和学习成长四个方面,以建立一个全面的绩效指标系统。

该框架的设计初衷是帮助企业在制定战略目标后能够实施,并且在实施过程中积极的调整和改进战略。

平衡计分卡可以帮助企业管理层清楚地认识到企业的整体战略目标解构,更好地与员工合作、实现战略目标,从而带来更好的结果。

平衡计分卡在其设计上非常适用于中大型企业,特别是那些有多个部门或位置的企业。

此框架的应用可以有效的将部门和位置之间的关系集成起来,以便更好地合作实现共同的战略目标。

此外,平衡计分卡也可以帮助企业在各部门之间建立更为协调的关系,加速企业在内部和外部的沟通和信息共享。

按照平衡计分卡框架的设计思路,财务、客户、内部业务流程和学习成长四个方面应该是相互依存的。

财务是一个企业的生命线所在,任何企业都必须在财务上取得成功。

但是单纯的追求财务方面的成功并不能保证企业能够持续成功下去,客户和内部的流程也是至关重要的因素。

企业的客户是企业发展的推动力,内部的流程是企业发展的保障。

在此体系中,学习成长是一个非常重要的环节,它指的是企业与员工的学习和发展。

企业必须不断发展和更新自己的技能和知识,在拥有这些技能和知识的情况下,企业才有可能在剩余的三个方面取得成功。

需要注意的是,平衡计分卡并不是一种简单的框架,它需要很好的理解和实施。

平衡计分卡的实施需要一个全面的计划和项目管理,这些计划需要充分考虑到每个部门和位置的不同情况。

在实行平衡计分卡时,每个员工应该能够理解自己的工作与整个企业的战略目标有什么联系。

所有员工都必须理解他们各自的局限性,并在企业与员工的学习和发展方面得到充分的支持。

平衡计分卡框架可以在不同层级上使用。

在组织层级上,可以通过平衡计分卡框架的实施来实现整个企业的战略目标。

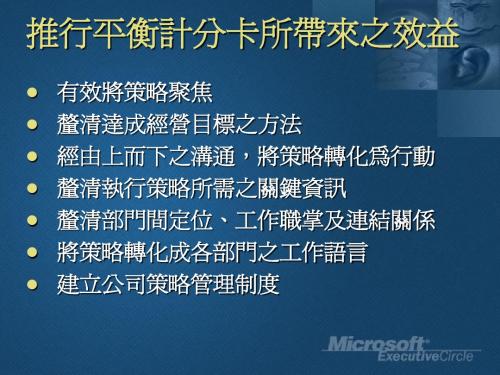

BSC - 实施 - 微软 - 推行平衡计分卡所带来之效益

執行的障礙與困難點

有效執行策略的四項障礙

The Vision Barrier

Only 5% of the work force understands the strategy

The People Barrier

Only 25% of managers have incentives linked to strategy

60% of organizations Don’t link budgets to strategy Source: Fortune

成功關鍵因素

企業領導者的帶動 動員企業作改變

- Mobilization - Strategic Management

將策略轉換成 作業條例

- Strategy maps - Balanced Scorecard - Integrate operational tools

下页更精彩

我们的加盟优势:

如需要了解,请咨询QQ:1097251560, 淘宝标准加盟样榜店: /

4、高回报 我们是正规做出口厂品的厂家,我们的货出品有的几十元到海 外,在网上零售都是几百元的,回报非常丰厚。下面我们的产 品及产品报价单。 5、免加盟费,零风险。 加盟我们的网店代理分销商,只需交600元加盟保证金,当代 销20块产品后,公司将退还其600元的加盟保证金。 只要您有成功梦想,有成功的激情,我们相信,你一定能成功, 同时也请你相信,我们将是你成功路上的一名最好的伙伴。 如需要了解,请咨询QQ:1097251560, 淘宝标准加盟样榜店:/

下页更精彩

我们的产品批发价:

如需要了解,请咨询QQ:1097251560, 淘宝标准加盟样榜店: /

我们的成功案例:

平衡计分卡平衡计分卡框架

平衡计分卡平衡计分卡框架for enterprise performance management. It presents basic information on the Balanced Scorecard performance management methodology, and identifies key business issues that must be addressed in developing and deploying a balanced scorecard. The paper then presents the Microsoft Balanced Scorecard Framework (BSCF)—a comprehensive set of techniques, tools, and best practices to speed scorecard implementation using toolsets with which organizations are familiar.An extensive body of research and literature describing the Balanced Scorecard exists. That body of knowledge is constantly being expanded by The Balanced Scorecard Collaborative, Balanced Scorecard Institute, various consulting organizations, software companies, and client organizations. This paper cannot comprehensively cover such a complex topic or reflect accurately many of the nuances of scorecard development and implementation. Instead, it presents a basic conceptual overview of the Balanced Scorecard. Interested readers are encouraged to use the bibliography presented at the end of this paper as a guide to more detailed information.ContentsExecutive Summary (1)Introduction (2)About the Balanced Scorecard (3)Background and History (3)Empowering the Knowledge Worker (4)Elements of the Balanced Scorecard (4)Critical Success Factors for BSC Development (8)Common Pitfalls (9)Automating the Balanced Scorecard (10)The Microsoft Balanced Scorecard Framework (12)Facets of the Framework (12)Conclusion (22)Selected Bibliography (23)Useful Web Sites (23)Executive SummaryTraditional performance measures are insufficient to gauge performance and guide organizations in today’s rapidly changing, complex economic landscape. Organizations need to link performance measurement to strategy, and must measure performance in ways that both promote positive future results and reflect past performance.The Balanced Scorecard has developed over the last eleven years as a powerful way to implement strategy and continuously monitor strategic performance. Creating a strategy focused organization (the phrase coined by the founders of the Balanced Scorecard methodology) is a significant, challenging culture change for many organizations. Success in achieving this change requires:∙Consistent executive support and involvement.∙Education, communication, and visibility of the strategy and measurements of its effectivenessthroughout the organization.∙Constant feedback loops so that strategy is an every-day consideration.∙Tools to enable non-technical users tounderstand the key drivers of the measures.∙Translation of the strategy to operational terms so that alignment to strategy andimplementation of it occur at all levels of anorganization.Organizations that have successfully implemented the Balanced Scorecard have achieved remarkable transformations in their financial performance, in many cases vaulting to the top ranks in their industry groups.Many aspects of Balanced Scorecard development and deployment depend on effective use of technology to be successful. Numerous software packages have been developed to help automate the Balanced Scorecard, but it is very difficult to deliver the needed capabilities in a single software package. Therefore, the Microsoft Balanced Scorecard Framework has been developed to allow organizations to:∙Develop and deploy a scorecard economically using an existing infrastructure.∙Manage and display the data and knowledge pertinent to Balanced Scorecards.∙Facilitate analysis of measures so that prompt corrective action can take place.The framework provides a comprehensive, flexible, cost-effective way to deploy the Balanced Scorecardand deliver superior returns on people, processes, customers, and technologies.IntroductionHow do we communicate strategy through a complex, multi-faceted, decentralized global organization? How do we align our organization and minimize superfluous activities so that we’re all working efficiently to the same ends? How do we measure the effectiveness of our strategy and its implementation? How do we promote a culture of agility to respond to the rapidly changing business climate we face?As business leaders wrestle with these questions each day, they confront the reality that, “If you can’t measure it, you can’t manage it.” In other words, effective performance management requires accurate performance measurement.Leaders also understand that performance measurement itself is not enough. The value of measurement is that it identifies where action should be taken. So, effective performance measurement systems must be able to:∙Accurately reflect a business situation.∙Guide employees to take the right actions in situations where action is required.∙Gauge the effectiveness of those actions.A performance measurement system, then, is a closed loop system that embodies situational analysis of information, corrective actions, and result evaluation.The Balanced Scorecard is a proven performance measurement system. It is a comprehensive strategic performance management system and methodology. It is a framework for defining, refining and communicating strategy, for translating strategy to operational terms, and for measuring the effectiveness of strategy implementation.This paper briefly describes the history, evolution, and key elements of the Balanced Scorecard. It then identifies the critical success factors for a Balanced Scorecard implementation. Finally, it presents the Microsoft Balanced Scorecard Framework (BSCF) as a way to leverage a corporation’s existing investments and capabilities to develop and deploy a scorecard in a timely, cost-effective, scalable, manageable, and reliable way.About the Balanced ScorecardBackground and HistoryThe Balanced Scorecard came into being in the late 1980s and early 1990s as a method to help companies manage their increasingly complex and multi-faceted business environments.Corporations then were faced with a number of challenges. Market share in many industries was vanishing at an alarming rate due to globalization, liberalization of trade, technology innovation, and domestic quality issues. The economy was in transition from product-driven to service-driven. The composition of the workforce was changing, and companies’ workforce needs were changing.In spite of all these changes, most businesses still relied on traditional measures of performance based on a centuries-old accounting model, which failed to accurately reflect the true health (and future prospects) of an organization. The need for better information to respond to rapidly changing market conditions was obvious.In response to these stresses, and the shortcomings of traditional financial performance measures, Professor Robert Kaplan and David Norton began to shape the concept of the Balanced Scorecard during aresearch project with 12 companies in the late1980s. They understood the limitations of relying too much on purely financial measures. They realized that many of the ways to improve short-term financial performance—such as reducing headcount, and cutting expenses for training, R&D, marketing, and customer service—might be detrimental to the future financial health of the company. Conversely, companies might appear to be doing poorly from a financial perspective because they were investing in the core capabilities that could drive superior future performance. Furthermore, they perceived the limitation of reliance on lagging indicators that convey past performance results, but do not generally provide a reliable indication of future performance.Kaplan and Norton also perceived that employees throughout a company often did not understand how their role related to strategy and financial measures, leading employees to feel powerless to impact the things that were being measured.So, Kaplan and Norton introduced the Balanced Scorecard as a way for companies to measure and report performance in a way that balanced:∙Multiple perspectives.∙Both leading and lagging indicators.Inward-facing measures, like productivity, and also outward-facing measures, like customerloyalty.The results of their initial research work with 12 companies were published in 1992 in the Harvard Business Review. Fueled by the positive response to their initial article and successful consulting work, Kaplan and Norton continued to develop the concept of the Balanced Scorecard, and published the book, The Balanced Scorecard in 1996. By that time, the focus of the Balanced Scorecard had evolved from an emphasis on measures and reporting, to a methodology for promoting strategic management of the organization.As more and more organizations began to embrace and experiment with the Balanced Scorecard concept, a growing number of tools and techniques emerged, building on many of the initial concepts. In 2000, Norton and Kaplan released their second book, The Strategy Focused Organization, which describes that evolution to a broader concept of enterprise strategic management.The Balanced Scorecard is a dynamic methodology, and the understanding of its potential deepens as Kaplan and Norton proceed with innovative work, such as developing scorecards for support functions like Human Resources and Information Technology (IT).Empowering the Knowledge WorkerToday, companies face the same pressures as 10 years ago, but in a radically different economic landscape. A new pressure, then barely on the horizon, has revolutionized the way many businesses must operate—the Internet. The Internet’s impact is ubiquitous. Among other impacts, it has lowered entry barriers to many markets; empowered the customer with information and choice; brought new distribution channels; and spawned entire industry sectors around activities such as customer relationship management, supply chain integration, security, and the marketing of information.The economy has transitioned to what some call the Age of Information—an economy in which Gross Domestic Product is increasingly dominated by services. In this service economy, the knowledge worker has replaced the production assembly line worker as a key factor of production. Knowledge workers use and process data or information, and in collaboration with other workers, create knowledge and take action, thereby increasing value.This value creation process is predominantly intangible in nature. In 1998, over 75% of the market value of the S&P 500 was captured in intangible assets. Intangible assets, like any other asset, are factors of production that should be usedto generate value. These intangible factors of production are used in ways that may be many times removed from revenue generation or cost reduction; they are frequently indirect contributors to production of a product or service. For example, IT investments involve extensive use of knowledge workers and capital, and are a powerful service facilitator with significant impacts on costs and internal and external customer relationships, but rarely are there direct correlations between IT projects and increased revenue or reduced cost.So, organizational financial performance is increasingly contingent on generating returns on intangible factors of production. Therefore, organizations must apply the knowledge worker’s expertise in ways that serve a defined corporate strategy to achieve a return on that worker. It follows that organizations must both empower the knowledge worker and measure their performance in relation to strategy.However, organizations are finding it extremely difficult to implement strategy and measure effectiveness of that strategy. According to Fortune Magazine, only 10% of the strategies that are effectively created get effectively implemented. A related finding by Norton and Kaplan is that without the Balanced Scorecard, 85% of executive teams spendless than 1 hour per month discussing strategy. So even when companies invest a lot of time in refining their values, mission statements, and strategic initiatives, those ideas rarely trickle down totruly transform an organization, and the average employee does not have a clear understanding how his or her actions influence ultimate performance measures such as stock price or earnings per share.The Balanced Scorecard is a proven way to align an organization with strategy, harness knowledge workers’ efforts to strategic ends, and ultimately deliver improved financial returns on employees, technology investments, business processes, and customer relationships.Elements of the Balanced ScorecardThe Balanced Scorecard is an approach to describing and communicating strategies. It is also a way of selecting performance measures that will drive a unique organizational strategy. Dr. Norton describes the Balanced Scorecard as follows:“A balanced scorecard is a system oflinked objectives, measures, targets andinitiatives which collectively describethe strategy of an organization and howthe strategy can be achieved. It cantake something as complicated andquestion become the objectives associated with that perspective, and performance is then judged by the progress to achieving these objectives. There is an explicit causal relationship between the perspectives: good performance in the Learning and Growth objectives generally drives improvements in the Internal Business Process objectives, which should improve the organization in the eyes of the customer, which ultimately leads to improved financial results.Though there are four basic perspectives proposed, it is important to understand that these perspectives reflect a unique organizational strategy. So the perspectives and key questions should be amended and supplemented as necessary to capture that strategy. For example, a non-profit or government organization would not have the same perspectives as a for-profit corporation.Objectives and MeasuresObjectives are desired outcomes. The progress toward attaining an objective is gauged by one or more measures. As with perspectives, there are causal relationships between objectives. In fact, the causal relationship is defined by dependencies among objectives. So, it is critical to set measurable, strategically relevant, consistent, time-delineated objectives.Measures are the indicators of how a business is performing relative to its strategic objectives. Measures, or metrics, are quantifiable performance statements. As such, they must be:∙Relevant to the objective and strategy.∙Placed in context of a target to be reached in an identified time frame.∙Capable of being trended.∙Owned by a designated person or group who has the ability to impact those measures.An organization is likely to have a variety of types of measures. Some will be calculated from underlying data. Others will be aggregated index measures that assign different weights to multiple contributing measures. Some are frequently measured and others may only be measured on a quarterly or annual basis.It is important to balance lagging indicators—which includes most financial measures—with leading indicators—areas where good performance will leadto improved results in the future.It is also important to balance internal measures, such as cost reduction, injury incident rates, and training programs, with external measures like market share, supplier performance, and customer satisfaction.InitiativesAn initiative is a change process or activity designed to achieve one or more objectives. The initiative is what will move a measure toward its target value. Initiatives may be large or small in scope. They generally are owned by a person or group, and are managed like projects.Strategy Maps, Strategic Themes, and MatricesSince even a relatively simple scorecard can contain an overwhelming amount of information, several tools have been developed to help communicate large, complex quantities of information in simple, easily understood ways.Strategy MapsMapping a strategy is an important way to evaluate and make visually explicit an organization’s perspectives, objectives, and measures, and the causal linkages between them. Organizing objectives in each defined perspective, and mapping the strategic relationships among them, serves as a way to evaluate objectives to make sure they are consistent and comprehensive in delivering the strategy.The strategy map is a visual way to communicate to different parts of the organization how they fit into the overall strategy. It facilitates cascadinga balanced scorecard through an organization, because it can be created at different levels of an organization, and each level’s map can be viewed for alignment with the overall strategy map.Figure 1: Example Strategy MapStrategic ThemesThe strategy map in Figure 1 shows a strategic theme. The strategic theme is a grouping of similar objectives and their measures across perspectives. It helps make a complex strategy more understandable by organizing and categorizing objectives and measures. It also reduces the amount of information and number of causal linkages that need to be drawn on a strategy map. A complex organization might have several strategic themes, with objectives and measures designed to gauge the effectiveness of the organization in pursuing those themes.Strategy MatrixThe strategy matrix is another useful visualization and summarization tool. It displays objectives, measures, targets, and initiatives in one table. The strategy matrix can point to areas where scorecard elements might be out of balance. For example, there may be a cluster of initiatives around one1.Mobilize change through executive leadership.Building a strategy focused organizationusually involves significant culture change.Organizational change is an evolutionaryprocess. Consistent executive leadership,involvement, active sponsorship, and supportare critical to maintaining momentum throughthe challenges that organizations inevitablyencounter.The executive team must be in agreement onstrategies and must drive the scorecard process for it to be successful. Often executives are too busy to be intimately involved in theprocess, so a cross-functional team is formed.This can be successful if:∙The executive team has first participated in facilitated sessions at which thefundamental mission, vision, and strategicthemes are established.∙The team has the ear of the leadership and can readily escalate issues to executivesfor resolution.∙Executives continue to communicate their support for, and involvement in, theBalanced Scorecard initiative.2.Make strategy a continual process. A strategicfocus is not maintained if strategy formulation becomes a one-time activity. Feedback loops are needed to constantly focus attention on andreevaluate the strategy and the measures. Tosupport strategy evaluation, tools forreporting and analysis should be deployed toenable analysis of the factors influencing the measures. The budget process also is oftenlinked to strategy, and in some cases theBalanced Scorecard replaces traditional budget formulation as a way to allocate funds.3.Make strategy everyone’s job. This is donethrough strategic education and awareness and by cascading the scorecard down through theorganization, so that business units,departments—or even individuals—create their own scorecards. The linkages to strategy areexplicitly defined at all levels. This helpsdepartments and individuals understand and find new ways to support the strategy of theorganization. It also helps ensure thatemployees at all levels are being measured and compensated in ways that support that strategy.4.Align the organization to the strategy. Thisinvolves evaluating current organizationalstructures, lines of reporting, and policiesand procedures to ensure that they areconsistent with the strategy. It can includere-alignment of business units or re-definingthe roles of different support units to makesure that each part of the organization islined up to best support the strategy.5.Translate the strategy into operational terms.Tools like the strategy maps, cascadedscorecards, and strategy grids are used tointegrate strategy with the operational tasksthat employees perform daily. This ensures that tasks are done in ways that support thestrategies.Common PitfallsWhen Kaplan and Norton’s second book, The Strategy Focused Organization was published, the Harvard Business Review hailed the Balanced Scorecard as one of the most significant contributions to management practice in the last 75 years. However, despite its well-publicized successes, the majority of organizations that adopt a scorecard fail to reap the rewards they expect. In researching these disappointments, some common themes stand out:1.Measures that do not focus on strategy. Acommon problem is that an organization willadopt some new non-financial measures, but failto align the measures adequately with strategy.According to Dr. Norton,“The biggest mistake thatorganizations make is thinking thatthe scorecard is just aboutmeasures. Quite often they willdevelop a list of financial and non-financial measures and believe theyhave a scorecard. This, I believe,is dangerous.”For example, in one case a bank’s ITdepartment had identified measures andbenchmarks for being a world class ITdepartment. According to those measures, they had done very well. However, the measures used by the IT department were not tied in with the overall business strategy and thereforediscouraged the IT department from meeting the strategic business needs.2.Failure to communicate and educate. A scorecardis only effective if it is clearly understood throughout an organization. Frequently,scorecards will be developed at the executive level, but not communicated or cascaded downthrough an organization. Without effectivecommunication throughout the organization, abalanced scorecard will not spur lasting change and performance improvement.3.Measures tied to compensation too soon. It isgenerally a good idea to tie compensation tothe Balanced Scorecard. However, severalfactors suggest it can be a mistake to do that too early in the lifecycle of the scorecard.∙Rarely is an initial scorecard leftunrevised. So, if an organization tiescompensation to measures that are not infact driving desired behavior, a powerfulmotivator has been instituted that willdrive an unwise action.∙Data may be incomplete or inaccurate, so measures may not be correct. If employees’paychecks are adversely impacted, seriousmorale problems and invalidation of thescorecard inevitably result.∙It may take time to determine realistic targets, and penalizing people for failingto achieve an unreachable target willsurely have a negative impact on morale andeventually profits.4.No accountability. Accountability and highvisibility are needed to help drive change.This means that each measure, objective, datasource, and initiative must have an owner.Without this level of detailed implementation,a perfectly constructed scorecard will notachieve success, because nobody will be heldaccountable for performance.5.Employees not empowered. While accountabilitymay provide strong motivation for improvingperformance, employees must also have theauthority, responsibility and tools necessary to impact relevant measures. Otherwise theywill resist involvement and ownership.Resources must be made available, andinitiatives funded, to achieve success.Employees are likely to need new informationtools to help them understand the drivers ofmeasures for which they are responsible so they can take action. These tools can includesystems for analysis and early warningindicators, exception reports andcollaboration.6.Too many initiatives. Large, decentralizedorganizations usually find that crossover and duplication among initiatives can beidentified. Cross-matching scorecard objectives with current and planned initiatives can be an important way to focus and align a company.This method will identify cases whereobjectives are supported inappropriately.Rather than relying on budgeting for strategicfunding, this process eliminates waste, speedsscorecard implementation, and helps anorganization prioritize their initiatives tobetter support their strategy.Automating the Balanced ScorecardA successful BSC program relies extensively on data, education, and communication to promote, monitor, and reinforce behavior modifications—all processes that can be facilitated easily by information technology.Automation is EssentialAutomation is essential in order to manage the vast amount of information related to a company’s mission and vision, strategic goals, objectives, perspectives, measures, causal relationships, and initiatives. The alternative is a manual process, which significantly increases the effort and cost of scorecard development and sets back progress in the early stages of the BSC development, when momentum is critical.Automation can foster quicker culture change, both during development and in the ongoing use of the BSC. If the software used is intuitive and can be deployed through an organization readily, it canbring visibility to the BSC process, ease a cultural transition, and enable participation by a wider audience.Approaches to AutomationA number of software development companies have sought to develop an automated solution and capitalize on the success of the Balanced Scorecard. Various approaches to BSC automation exist, depending on the orientation of the software company:Proprietary business intelligence (BI) products. One class of scorecard automation software has formed around proprietary BI software products. BI software is designed to support an organization’s reporting and analysis needs. Naturally, a BI software vendor will see the BSC as an extension of BI, and so will develop it as an add-on to their product line. While these packages can meet some of the analytical needs that support a balanced scorecard, they tend to have several limitations:∙They can lead an organization to focus on measures derived from available data ratherthan strategic objectives.∙They do not generally provide neededcapabilities with regard to strategycommunication and managing non-numericinformation like reasons for selecting aspecific measure.They often have per-seat license costs that may be appropriate for a smaller number of advanced analytical users but can be cost-prohibitivefor the widespread deployment that is needed to drive effective strategy execution.ERP-centric applications. Another class of BSC software is designed by Enterprise Resource Planning (ERP) software companies to interface with their transactional systems and to try to combat the common perception that their reporting capabilities are unduly limited. These ERP-centric applications tend to emphasize use of the ERP system’s data and may not be as well suited for integrating external data. Due to a heavy database orientation, they generally do not provide ways to manage the unstructured content that is key to educating and communicating with a large employee population. They also usually have per-user costs that can discourage broad use.BSC-specific applications. The BSC-specific applications generally offer a good presentation layer, but may be limited in their ability to integrate multiple data sources and to enable automation of data collection and transformation.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Recognized by the Harvard Business

Review as one of the “most important management practices of the past 75 years.“

什麼是平衡計分卡BSC?

發展BSC是一連串由企業願景(Vision)展開至四個構面之主 要績效衡量指標之過程

Project duration: site acquisition to

opening day

% of stores opened on schedule

活動 主要績效指標(Key Performance Indicator, KPI):策略目

標進程或關鍵流程的衡量基礎,且必須是可數量化的

BSC 的四個構面

衡量過去努力成果

“To succeed financially, Objectives how should we appear to our shareholders?”

“To achieve our vision, Objectives Measures Targets Initiatives

學習與成長 how will we

sustain our ability to change and improve?”

驅動未來績效

Source: The Balanced Scorecard Collaborative

Avg purchase amount

Customer Perspective

Cause & Effect

Fact-based site selection

Lag between market selection and site acquisition

Development Project Management

“If you can’t measure it, you can’t manage it.” 若您無法衡量企業經營績效 您便無法有效管理企業

Robert Kaplan and David Norton

Authors of “The Balanced Scorecard”

平衡計分卡的背景與發展歷程

Avg. # of days to

break even

Increase Sales Efficiency

Revenue per FTE

Great New Locations

Avg daily customers at new stores in first 6 months

# repeat customers

執行長David Norton所共同研究發展

1992年:發表 BSC

1993年:發表 BSC的實踐

1996年:發表 BSC在策略管理體系的應用

平衡計分卡的發展史

衡量的方法

整合與溝通

企業策略管理

1992

Articles in Harvard Business Review:

“The Balanced Scorecard – Measures that Drive Performance”, Jan-Feb 1992

微軟平衡計分卡架構

Measuring Success Bringing the Balanced

Scorecard to Life

微軟技術顧問服務部

Agenda

平衡計分卡 Balanced Scorecard (BSC) 建構績效管理制度與平衡計分卡 執行的障礙與困難點 微軟平衡計分卡架構 Demo-Microsoft BSC Toolkit Case Study Q&A

四個構面(Perspectives) 財務、顧客、內部流程、學習成長 策略主題(Strategic Theme):長期而言,應完成的事項,

貫穿四個構面 策略目標(Strategic Objectives):為達成組織之策略主題

所定的短期目標 關鍵流程(Critical Process):支持達成策略目標的的作業

Measures Targets

財務

Initiatives

股東與顧客的外界衡量

有關重大企業流程, 創新能力, 學習及成長的內部衡量

“To achieve our vision, Objectives Measures Targets

how should we appear to our

顧客

customers?”

1996

“Putting the Balanced Scorecard to Work”, Sept-Oct 1993

Hale Waihona Puke 2000“Using the Balanced Scorecard as a Strategic Management System”, Jan-Feb 1996

“Having Trouble With Your Strategy? Then Map It”, Sept-Oct 2000

第一代績效衡量: 僅聚焦於財務面

第二代績效衡量: 加入無形資產的衡量, 如產品研發設計, 客 戶關係, 員工教育訓練, 行銷資訊, 企業知識管理等

1998 年 超過 75% 的S&P 500 市場價值是來自無形資產

發展史

1990年研究計劃 – 未來組織績效衡量方法,12家企業共同參 與

由哈佛教授 Robert Kaplan與Nolan Norton Institute

策略地圖 & 因果關係

Theme: Smart, Profitable Expansion

Financial Perspective

50% Revenue from New Stores by Year 3

% revenue from stores opened in last 3 years

Revenue from new stores

Initiatives

Vision and Strategy

“To satisfy our shareholders Objectives Measures Targets Initiatives

內部流程 and customers,

what business processes must we excel at?”