ACCAF6 (Chapter 1-16)-3

acca f6知识点

acca f6知识点

ACCA F6考试是ACCA专业资格考试的其中之一,也是ACCA税务

管理领域的核心考试。

在ACCA F6考试中,考生需要掌握一定的税务管理理论和实践知识,掌握税法和税收政策的基本要求,并且需要熟

练掌握税务官员的工作方式和职责。

ACCA F6的考试范围非常广泛,主要包括以下几个方面:

1.国内和国际税收制度

ACCA F6考试主要包括国内和国际税收制度的知识点,包括个人所得税、公司所得税、增值税、营业税、关税、进口环节增值税、服务税、等等。

考生需要熟悉各种税收政策的法规和适用条件,以及税务官员

的职责和运作方式。

2.财务会计和税务会计

另外,ACCA F6考试还包括财务会计和税务会计方面的知识点,包括企业财务报表编制、税务报表编制、税务审计、税务咨询和税务筹划

等方面。

考生需要掌握税收政策与财务报表之间的关系,以及税务会

计的各项细节。

3.税务规划与管理

ACCA F6考试还包括税务规划与管理方面的知识点,考生需要掌握税务规划的基本概念、方法和技巧,以及税务风险管理和税务筹划的常

用思路和方法。

ACCA F6考试的通过要求比较高,考试难度也较大,因此考生在备考过程中需要充分掌握各项知识点,并且需要有一定的实践经验和技巧。

考生可以通过ACCA官方的教育指南、考试大纲和模拟试题等方式来

加强自己的备考,提高通过考试的概率。

总之,ACCA F6考试是ACCA专业资格考试中非常重要的一门考试,考生需要认真备考,充分掌握各项考试知识点,并且注重理论与实践

相结合,才能取得较好的考试成绩。

acca-f6-讲义

课税范围(scope of…)

税基大小的选择

Income arising in the UK Vs. worldwide income

纳税年度(eg,

tax year/ accounting period/ etc)

三大基本要素:征(课)税对象

税目(classification of income)

其他要素: 税收优惠 (exemptions & reliefs)

To minimise tax liabilities

优惠税率

eg,

small profits rate, zero-rated supply, etc

To defer tax liabilities(延期纳税)

eg,

business reliefs

其他要素: 纳税期限/违章处理

纳税期限

申报期限 (due date for filing a tax return)

缴库期限 (due dates for payment of tax)

违章处理 (penalties for non-compliance)

Her

Sources of revenue law

Statue

& case law Refer to textbook

3. Tax avoidance and tax evasion

Tax avoidance (legal)

Any

legal method of reducing your tax burden *Anti avoidance measures

ACCA F6知识要点汇总

F6知识点:第一章UK TAX SYSTEMTaxation function: encourage economic, social and environmental behaviour Structure: 税务由HMRC管理Human revenue and customs 英国税务及海关总署Source of law 立法Finance Act每年更新税率Tax year: April 6th to April 5thTax evasion is illegal 逃税非法 & Tax avoidance is legal 合理避税合法第二章Computation of taxable income and income tax liability1.Resident判定UK resident individuals UK & oversea income都交税Non‐UK resident individuals 仅UK income交税5 UK Ties:▲考试提供表格:Days inUK Previously resident Not previously resident < 16 Automatically not resident Automatically not resident 16 to 45 Resident if 4 UK ties(or more) Automatically not resident 46 to 90 Resident if 3 UK ties(or more) Resident if 3 UK ties(or more) 91 to 120 Resident if 2 UK ties(or more) Resident if 2 UK ties(or more) 121 to 182 Resident if 1 UK ties(or more) Resident if 1 UK ties(or more) 183 Automatically resident Automatically resident1. Types of incomeNon ‐saving income Trade incomeEmployment incomeProperty incomeSavings income Taxed income (20% tax 已扣)Bank interestBuilding society interest Interest received gross (未扣税)Government stocks (gilts 债券) interestNational saving & invest bank interest Dividend income 10% tax 已扣This tax credit is not refundable. Exempt income 免税收入,回答题目时必须注明时免税收入,不写没分Interest from Saving Certificates issued by National Savings and InvestmentBank(UK 国民储蓄和投资银行:储蓄账户免税,投资账户收税)国民储蓄券 Statutory redundancy money 裁员补偿Betting and gaming winnings 博彩奖金(收其他税,不收个税) Scholarships 奖学金Interest on damages for personal injuries 个人受伤赔偿,包括工资补贴等 in UK < 16Din UK < 46D, not resident in past 3 tax yearsFull time oversea work & in UK < 90Din UK >183D only home in UK Full time work in UK UK House in useSubstantive work in UK > 90D in either two past tax years more time in UK than oversea FamilyLocal authority grant 地方补助Income from investments made through new individual savings accounts (NISAs) NISA有3种, 每个Tax year overall subscription limit is 15,000。

ACCA考试经验:ACCA考官关于F6的报告介绍

ACCA考试经验:ACCA考官关于F6的报告介绍关于F6的ACCA考试已经成为过去,接下来2018年的考试马上就要到来了。

为了能够在考试的时候处理的游刃有余,acca考试经验还是需要大家了解一下的。

具体情况如下所示;考官的留言试卷有两个部分,所有的问题都是强制性的。

A部分包括15个选择题(每个2分),涵盖了广泛的课程大纲主题。

B部分有四个问题,每个值10个标记,两个长的问题每个值15个标记。

B部分提问更深入地考察考生对税务知识的理解和运用。

除了每个问题的具体问题之外,还有一些一般性的考试要点,未来的考生应该知道:考生有责任仔细检查他们已经注册的论文。

例如,一些候选人已经研究了英国的变体,但是错误地登记了中国变体,直到他们开始考试才意识到。

花些时间仔细阅读说明。

这样可以帮助考生避免花费时间写出不会打分的记分,并防止他们忽略问题中提到的重要问题。

例如,当被要求计算企业所得税(EIT)的收入或成本时,一些候选人并没有注意“收入”或“成本”这个词,而只是简单地计算了无关的EIT。

以下段落对每个部分进行汇报,并重点介绍一些关键的学习要点。

具体评论A节很高兴看到几乎所有的候选人都试图提出所有的问题。

为下一次F6考试做准备的人员建议通过这里讨论的试点文件和样本问题,仔细查看每个正确答案是如何得出的。

A部分的问题旨在提供广泛的教学大纲,未来的候选人应该旨在修改F6教学大纲的所有领域,而不是试图质疑现场。

对以下两个问题进行审查,目的是让未来的考生了解问题的类型,处理考试问题的指导以及就所选择的具体问题所涉及的主题进行技术汇报。

针对讨论的示例问题例1Pro Ltd使用相同类型的材料制造两种类型的产品(产品K和产品L)。

2015年两种产品的增值税(VAT)和增值税专用销售价格如下:增值税销售价格(增值税专用)产品免征增值税90万元产品L出口退税率16%RMB600,000Pro有限公司2015年的进项税额为人民币50,000元。

ACCA考试复习回顾《税务F6》辅导3

ACCA考试复习回顾《税务F6》辅导3本文由高顿ACCA整理发布,转载请注明出处CHARGEABLE GAINSRELATED LINKSPDF versionThis article looks at chargeable gains in either a personal or corporate context. This article is relevant to candidates sitting Paper F6 (UK)in 2013This two-part article is relevant to candidates sitting Paper F6 (UK)in either the June or December 2013 sittings, and is based on tax legislation as it applies to the tax year (Finance Act 2012)。

Question 3 of Paper F6 (UK)focuses on chargeable gains in either a personal or a corporate context, and will be for 15 marks. A small element of chargeable gains may also be included in any of the other questions.PERSONAL CHARGEABLE GAINSScope of capital gains tax (CGT)CGT is charged when there is a chargeable disposal of a chargeable asset by a chargeable person.A chargeable disposal includes part disposals and the gift of assets. However, the transfer of an asset upon death is an exempt disposal. A person who inherits an asset takes it over at its value at the time of death.20 June 2012, and the land was inherited by his son, William. On that date the land wasThe transfer of th e land on Jorgeˇs death is an exempt disposal.All forms of property are chargeable assets unless exempted. The most important exempt assets as far as Paper F6 (UK)is concerned are:Certain chattels (see later)Motor carsUK Government securities (Gilts)In determining whether or not an individual is chargeable to CGT it is necessary to consider their residence status.Example 2 Explain when a person will be treated as resident or ordinarily resident in the UK for a particular tax year and state how a personˇs residence status establishes whether or not they are liable to CGT.A person will be resident in the UK during a tax year if they are present in the UK for 183 days or more.A person will also be treated as resident if they make substantial visits to the UK, with visits averaging 91 days or more over four consecutive tax years.Ordinary residence is not precisely defined, but a person will normally be ordinarily resident in the UK if this is where they habitually reside.A person is liable to CGT on the disposal of assets during any tax year in which they are either resident or ordinarily resident in the UK.Basic computation For individuals the basic CGT computation is quite straightforward.during March 2004. During May 2006 the roof of the factory was replaced at a cost ofCost164,000Enhancement expenditure 37,000Incidental costs (3,600 + 5,800)9,400_______ (210,400)________ Chargeable gain 109,600Annual exempt amount(10,600)_______Taxation gain99,000 _______The factory extension is enhancement expenditure as it has added to the value of the factory.The replacement of the roof is not enhancement expenditure, being in the nature of a repair.Note that the standardised term ˉchargeable gainˇ refers to the gain before deducting the annual exempt amount, while the term ˉtaxable gainˇ refers to the gain after deducting the annual exempt amount.Capital losses Capital losses are set off against any chargeable gains arising in the same tax year, even if this results in the annual exempt amount being wasted. Any unrelieved capital losses are carried forward, but in future years they are only set off to the extent that the annual exempt amount is not wasted.Example 4 FCapital losses brought forward(7,000)_______Chargeable gains10,600 Annual exempt amount (10,600)_______ Taxable gains Nil_______(10,600)so that chargeable gains are reduced to the amount of the annual exempt amount.()。

Taxation (税务)ACCA F6

4.1 ACCA F6课程全球考试成绩优异

年级/通过率 %

一次通过率 %

2001 65.5

2002 2003 2004 2005 2006 2007 2008

96

79.71 88.3 86.5

90.9 92.6% 尚未考

试

自2001年至今,我校F6的通过率始终保持在80%左右。F6 一共参加国际考试6次,其 中通过率四次在85%以上,马蕾同学以92的成绩分获得大陆第一。同时2006级的学生 的平均成绩67.77 分,2007级学生平均成绩70多分远远高于全球平均分。

accaf6西安交通大学管理学院一accaf6的发展与知识模块二accaf6的特色三主讲教师的学缘结构与队伍建设四教学效果五网络建设一accaf6课程发展与知识模块自20世纪30年代起acca资格考试在世界上160个国家推广到目前为止acca拥有30万学员设有340多个考点总部设在伦敦在美国洛杉矶加拿大多伦多澳大利亚悉尼中国香港设有分会在北京上海和广州以及都柏林新德里吉隆坡新加坡等70多个城市设有办事处

Taxation (税务)

ACCA F6

西安交通大学管理学院 张俊瑞、王静

1

大纲

一、ACCA F6的发展与知识模块 二、ACCA F6的特色 三、主讲教师的学缘结构与队伍建设 四、教学效果 五、网络建设

2

一、ACCA F6课程发展与知识模块

A本课程校内发展的主要历史沿革 B知识模块顺序及对应的学时 C课程的重点、难点及解决办法

12

c、实践教学活动的 设计思想与效果

实践教学活动设计的思想:以专业技能实践 为目标,设置与本科段专业学习相匹配的教 学实践课、模拟实践、社会实践三位一体的 教学实践模式。

2015年ACCA考试F6科目大解析

2015年ACCA考试F6科目大解析科目介绍:F6《税法》的大纲为学员介绍税法科目的核心知识点和主要的税法计算部分,它们影响着个人和商业活劢。

首先大纲介绍了英国的税法系统;其次介绍作为一名会计师必须详绅理解开掌握各种税收及其义务,例如个体所得税义务,公司所得税义务,应税利得,遗产税,国民保险制度,增值税和纳税人义务及其代理人。

除了掌握基础税法的核心部分,学员还应该能够计算应纳税义务,解释计算的依据,应用避税计划技巧为个体和公司避税,仍商业或者个人案例中识别各种税的合规问题。

近几年考试通过率趋势图:知识结构:科目关联性:F6课程是ACCA基础阶段唯一的一门税务科目,在整个ACCA课程体系中相对来说比较独立,和它直接相关的科目只有与业阶段的P6(高级税务)。

相关知识掌握:学习f6之前应该要有财务报表有基本的学习认知,因为在个人所得税和企业所得税的计算中需要懂得财务利润是怎么得来的,权责发生制和收付实现制的差别。

考试形式:今年f6暂时不做考题的变化。

F6的考试时长为3小时。

考试题共有五道全为必选题,以计算为主。

第一题主要是考察的是个人所得税和第事题主要考察的是公司税,这两道题一共55分,一题30分,另一题25分。

第三题主要考察的是个人戒者公司的应税利得,15分。

第四第五题考察的是大纲的其他部分,每题15分。

至少10分的内容会涉及增值税的考察,通常会包含在第一或第二题,但是增值税也有可能单独作为一题进行考察。

遗产税会出现在第三,第四或者第五题中考察,分值为5分至15分。

社会保险不会单独作为一题,一般在个人所得税戒公司税中考察。

集团的公司税可能会在第事题或第四,第五题中考察。

除了第三题之外,应税利得还可能会在其他题目中涉及一小部分。

关于税负最小化或者递延纳税义务的相关事项可能会在五道题目中任何一道出现。

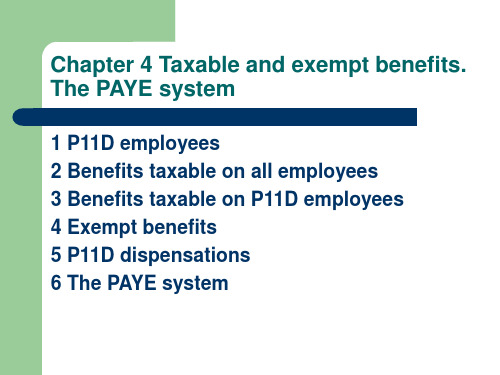

ACCA F6 四川大学工商管理学院 课件Chapter1

The threshold income level

Salary Benefits assessable on all employees Benefits assessable only on £8,500 (or more) earners Total earnings (for test purposes) £ × × × ×

1 P11D employees

Most employees are taxed on benefits under the benefits code. Employees involve excluded employees and P11D employees. ―Excluded employees‖ are only subject to part of the provisions of the code. Excluded employee: an employee in lower paid employment (general earnings for the tax year is less than £8,500) (a) not directors, or (b) director with no material interest (< 5%) in the company P11D employee: not excluded employees. A P11D employee is one who is an employee earning at least £8,500 per annum or a director of a company (in most cases).

Expenses related to living accommodation (reference to 2.3)

ACCAF6 (Chapter 1-16)-7

2015/7/23

2015/7/23

Premiums received on short term leases (≤50 years)

• A premium is a lump sum payment made by the tenant to the landlord on the initial granting a lease. • Landlord company: When a premium is received by the landlord, the premium is treated as property business income for the year of grant. The amount assessable is calculated as: P×(D1)*2% P=total premium; D=duration

2015/7/Biblioteka 3Furnished holiday letting rules

Besides, losses from FHL can only be offset against future profits from FHL. So, if someone has furnished holiday lettings and other lettings, draw up two profit and loss accounts as if they had two separate UK property businesses.

2015/7/23

Premiums received on short term leases (≤50 years)

• Tenant company Where a tenant company pays a premium for a short lease, it may deduct an amount from its trading profits in each year of the lease. The amount deductible each year = P×(D-1)*2%/D • Premium for granting subleases The sub-premium is treated in the normal way, but a relief is given for sub leaser. Relief = Taxable premium for head lease ×(sublease duration / head lease duration)

ACCA F6 知识点总结 2015年

Chapter 1 Introduction to the UK tax system1.HMRC:Her Majesty ’s Rvenue and Customs 英国税务海关总署2.factors affect tax policies:①econmic:whole;factors;behavior(donation,investment,saving,build own business,drink,fuel);②social:缩小贫富差距;③environment3.progressive taxation:income tax 随财富增加税率变高Regressive taxation:fuel duty 随财富减少税率变高Proportional taxation:财富增加比率不变,是固定数 Ad Valorem :增值税4.direct and indirect (VAT) taxes .5.treasure(财政局),chancellor of the exchequer,HMRC,Tribunal(first,upper),遵从欧盟规则6.避收两次税:避收两次;避免歧视;避免逃税漏税7.tax evasion(illegal) and tax avoidance(legal:abusive arrangement,tax mitigation)8.出现违反:告知;不改的话不予受理;报告单不能透露信息9.ISA :限额15000,存款投资股票免税(利息不用交个人所得,资产利得不用交税),亏损不能抵减。

Chapter 2 Introduction to Crporation Taxpany residence:place of incorporation 注册地:①UK;②Overseas(central management in UK)2.period of account(会计期,可长于/短于12个月) and chargeable accounting period(应税会计期,不能超过12个月,会计期大于12月时拆分)★3.financial year:FY 2014 01/04/2014-31/03/2015▲4.proforma of corporation tax computationFII:免税投资收入:①dividend(另一UK 公司,海外公司,unconected company(<50% share holding);②FII=dividends received from unconnected companies/90%★5.MR=standard fraction*(upper limit-augmented profit)*TTP/augmented profit6.大于12个月的拆分:①按期间:trading profit,property business income②按具体发生日期:interest income,chargeable gain,qualifying charitable donation,FIICapital allowance:计算每一个期间的capital allowance 后加总7.小于12个月:按比例:upper limit and lower limit 同样按比例减小8. associatied company:>50% share capital,>50% voting rights,>50% profit pr netAsset on winding up(结束).注意:Both UK and overseas,dormant companies excluded,一段时间为associated company 视为整个期间都是associated;Associated company dividend is not include FIIChapter 3 trading profit▲1.proforma for tax adjusted trading profits★2.decutible and non-decuctible(完全,唯一) 两个目的中有一个目的与金融无关,不可扣 ①fine 罚款(停车除外);②depreciation;③capital expenditure(性能有提升,不可扣),revenue expenditure(无提升,可扣)买破房,不翻新无法使用,CE;翻新前也可以使用RE,换烟囱,RE④lease car(租车):≤130g/km 全可扣,>130:15%不可扣⑤entertain and gift:employee deductible;customer(不可扣,除非:一年一人不超过50磅/不是实务研究代金券/gift 有给公司打广告⑥donation:可扣减三要素:trading purpose,local,给教育宗教文化慈善组织不满足三条件时,放在QCD 里面扣掉政治捐款不可扣,也不能放在QCD 里面扣★⑦legal fee:可扣:应收账款的催付,贷款用于经营,商标注册,短租续租,保护域名,起诉违约,会计审计费,版税不可扣:发行股票,被别人起诉,初次短期租约,与capital expenditure 相关的⑧debt:only 赊销未还可扣(即staff 不行),确认坏账又收到了算在other income 里⑨other:培训,商业会费,经营前7年内,裁员补偿,咨询服务3.Capital allowance:a businesstax relief for capital expenditure on qualifying asset.It coverd for expenditure on plant and machinery,and is given to the net cost of asset(original cost-disposal value)4.plant and machinery:land building and structures are not plant.so as walls,floors,ceilings,doors,gates,shutters,windows.①main pool:大多数资产,car with CO2 96g/km-130g/km②special rate pool :long life asset(≥25years,total cost of at least 100000 for 12 month),房间自带体系,cars with CO2>130g/km③short-life asset:预备8年内出售;购买资产的accounting period结束后两年内去税务局做认定(对unincorporate business,会计期结束后的1年内的1月31日之前);计算CA时单列,使用结束后计算balancing charge or balancing allowance;8年后仍在用转化为main pool;AIA5.WDA(writing down value.for still use,reducing balance basis余额递减法)Main pool-18% special pool-8% short life asset-18%(年折旧比率)6.AIA(annual investment allowance,for newly required) exception of motor carsProvide alloance of 100% for the first 500000 of expenditure(针对12个月)抵减顺序:SP→MP→SLA★7.motor car:针对于低排量(≤95g/km)汽车。

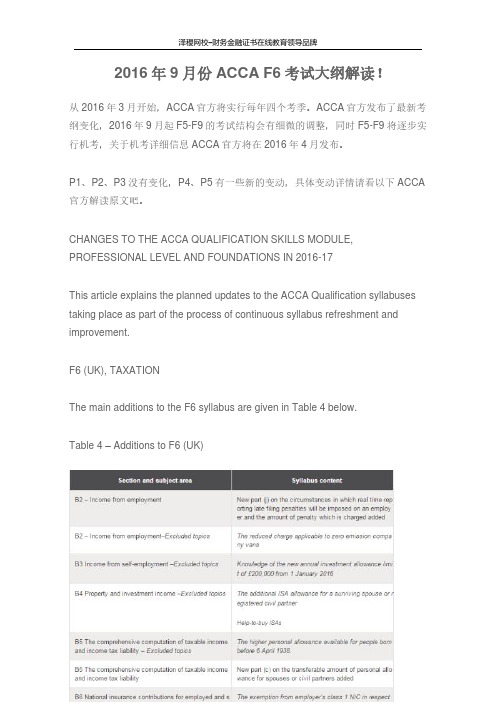

2016年9月份ACCA F6考试大纲解读

2016 年 9 月份 ACCA F6 考试大纲解读!

从 2016 年 3 月开始,ACCA 官方将实行每年四个考季。ACCA 官方发布了最新考 纲变化,2016 年 9 月起 F5-F9 的考试结构会有细微的调整,同时 F5-F9 将逐步实 行机考,关于机考详细信息 ACCA 官方将在 2016 年 4 月发布。

F6 (UK), TAXATION

The main additions to the F6 syllabus are given in Table 4 below.

Table 4 – Additions to F6 (UK)

泽稷网P2、P3 没有变化,P4、P5 有一些新的变动,具体变动详情请看以下 ACCA 官方解读原文吧。

CHANGES TO THE ACCA QUALIFICATION SKILLS MODULE, PROFESSIONAL LEVEL AND FOUNDATIONS IN 2016-17

This article explains the planned updates to the ACCA Qualification syllabuses taking place as part of the process of continuous syllabus refreshment and improvement.

ACCAF6 (Chapter 1-16)-4

Travel expenses • Employee‟s normal commuting costs (from home to permanent work place) are not deductible.

• Employees who do not have a permanent workplace, costs of journeys made from home to their temporary work place (less than 24 months) is deductible. • site based employees can deduct all the costs of the journeys made from home • Travels between different employers is not deductible.

Earnings are treated as received at the earlier of: The date that the amount is paid The date when the person becomes entitled to payment

2015/7/23

When earnings are received

2015/7/23

Allowable deduction

General rule Expenditures wholly exclusively and necessarily for the performance of duties of employment are deductible. Expenses giving private benefits are not deductible.

accaf阶段考试顺序

ACCA(特许公认会计师)考试的阶段包括三个主要的考试级别:基础阶段、应用阶段和专业阶段。

以下是一般情况下ACCA 考试阶段的顺序:1. 基础阶段(Fundamentals Level):- AB(F1)- Accountant in Business- MA(F2)- Management Accounting- FA(F3)- Financial Accounting- LW(F4)- Corporate and Business Law- PM(F5)- Performance Management- TX(F6)- Taxation- FR(F7)- Financial Reporting- AA(F8)- Audit and Assurance- FM(F9)- Financial Management2. 应用阶段(Applied Knowledge and Applied Skills):在完成基础阶段的所有九门考试后,您将获得ACCA 的知识模块证书(Knowledge Module Certificate)和技能模块证书(Skills Module Certificate)。

接下来,您可以选择应用阶段的考试顺序,选择适合自己的顺序考试。

- SBL(P1)- Strategic Business Leader- SBR(P2)- Strategic Business Reporting- APM(P3)- Advanced Performance Management- ATX(P6)- Advanced Taxation- AAA(P7)- Advanced Audit and Assurance3. 专业阶段(Strategic Professional):在完成应用阶段的所有考试后,您将获得ACCA 的技能模块证书(Skills Module Certificate)。

接下来是专业阶段的考试,其中包含两门必修考试和两门选修考试:- SBR(P2)- Strategic Business Reporting(如果在应用阶段未选择考试)- SBL(P4)- Strategic Business Leader(如果在应用阶段未选择考试)- Options Modules(从以下选项中选择两门考试):- AFM(P4)- Advanced Financial Management- APM(P5)- Advanced Performance Management- ATX(P6)- Advanced Taxation- AAA(P7)- Advanced Audit and Assurance请注意,考试的顺序并非固定的,您可以根据自己的需求和兴趣选择适合自己的考试顺序。

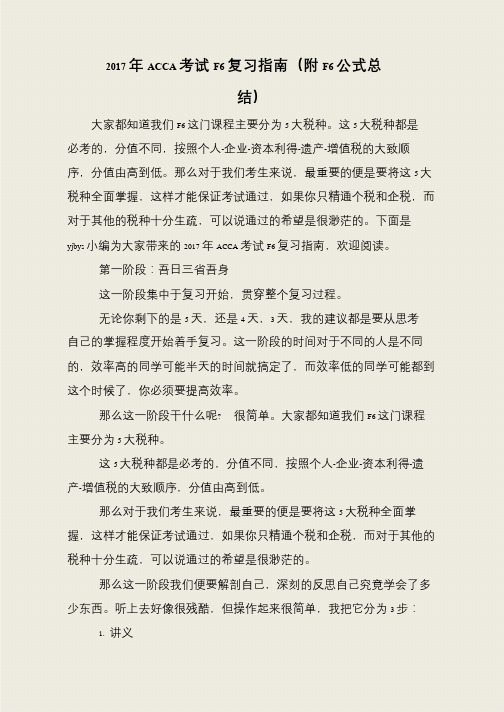

2017年ACCA考试F6复习指南(附F6公式总结)

2017 年ACCA 考试F6 复习指南(附F6 公式总

结)

大家都知道我们F6 这门课程主要分为5 大税种。

这5 大税种都是必考的,分值不同,按照个人-企业-资本利得-遗产-增值税的大致顺序,分值由高到低。

那么对于我们考生来说,最重要的便是要将这5 大税种全面掌握,这样才能保证考试通过,如果你只精通个税和企税,而对于其他的税种十分生疏,可以说通过的希望是很渺茫的。

下面是yjbys 小编为大家带来的2017 年ACCA 考试F6 复习指南,欢迎阅读。

第一阶段:吾日三省吾身

这一阶段集中于复习开始,贯穿整个复习过程。

无论你剩下的是5 天,还是4 天,3 天,我的建议都是要从思考自己的掌握程度开始着手复习。

这一阶段的时间对于不同的人是不同的,效率高的同学可能半天的时间就搞定了,而效率低的同学可能都到这个时候了,你必须要提高效率。

那么这一阶段干什么呢? 很简单。

大家都知道我们F6 这门课程主要分为5 大税种。

这5 大税种都是必考的,分值不同,按照个人-企业-资本利得-遗产-增值税的大致顺序,分值由高到低。

那么对于我们考生来说,最重要的便是要将这5 大税种全面掌握,这样才能保证考试通过,如果你只精通个税和企税,而对于其他的税种十分生疏,可以说通过的希望是很渺茫的。

那么这一阶段我们便要解剖自己,深刻的反思自己究竟学会了多少东西。

听上去好像很残酷,但操作起来很简单,我把它分为3 步:

1. 讲义。

ACCAF6 (Chapter 1-16)-5

2015/7/23

Interest-free or cheap loans

A benefit may arise when an employer lends money to an employee (or a close relative) with interest being charged at less than a commercial rate. The benefit is the difference between the interest calculated at the official rate and the interest actually paid. There are two methods to calculate the benefits. Normal (Average) method Alternative (Strict) method

(cost *- £75,000) * official interest rate

Tips:

1. If employer owned the property for the 6 years before first made available to employee, use market value when made available, instead of cost. 2. Official interest rate will be provided in the exam.

2015/7/23

f)

Sport and recreational facilities available generally for the staff. g) Outplacement counselling services to employees made redundant who have been employed full-time for at least two years. The services can include counselling to help adjust to the loss of the job and to help in finding other work. h) Workplace parking for bicycles plus a tax free cycling allowance of 20p per business mile. i) Weekly tax free allowance of £4 can be paid by employer to an employee who works from home.

ACCA考试技巧 F6税收(UK)

ACCA考试难不难解析ACCA考试技巧考试的目的是确保考生了解税收制度,和知识的所得税,国民保险税、资本利得税,遗产税,企业所得税和增值税。

教学大纲包括几乎所有FTX处理, 基金会在税收方面考试,以及一些新课题引入在F6级别。

考试提供了一个坚实的基础对于那些考生希望进步P6(英国), 先进的税收。

考试包括三个部分,每个部分内的所有问题是强制性的。

A部分部分A由15个目标测试问题值得每个2分。

的问题可以在任何区域的教学大纲,并将计算和叙述。

因为部分将包括客观试题的整体F6教学大纲,是非常重要的,确保考生时覆盖整个教学大纲修订F6的考试。

此外,重要的是,考生不花太多时间在任何一个问题。

重要的是要记住,每一个客观的测试问题只值两个标志。

B部分B部分由三个问题组成的五个客观测试项目价值两个标志; 因此每个问题值得总共十个标志。

每个问题将基于一个常见的场景“案例”,可以来自任何领域的教学大纲,并将计算和叙述。

类似于部分A,一些客观的测试项目可能需要更长的时间来回答这些问题,所以考生应该管理自己的时间在每一个“案例”问题,而不是试图分配时间每个客观的测验项目。

C部分部分C是由一个十的马克的问题和两个15的问题。

十的马克的问题可能来自任何领域的教学大纲。

15的两个问题将集中于所得税(教学大纲区B)和企业所得税(教学大纲区E)。

问题部分C将以计算为主,虽然每个问题可能包含写元素。

与部分A和B,auto-marked,部分C的问题仍将是手动标记,所以它是绝对重要的,所有的运作都是清晰显示。

最重要的教学大纲区域,你可以看到整个考试经常检查如下:所得税就业收入(尤其是应税收入,允许减免和福利)。

个体经营收入(尤其是评估的基础,是容许的支出,应税利润开始和停止,投资优惠和减免交易损失)。

房地产和投资收入(尤其是财产性收入、储蓄收入和股息收入)。

应纳税所得额的计算,所得税负债。

自我评估系统。

提交的信息的时间限制,索赔和支付的税收。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2015/7/23

Dividend income Dividends are received net of a 10% tax credit. So the net amount received for dividend must be grossed up by dividing 90%.

2015/7/23

The following interests received are not grossed up: 1. Interest from government stock (gilts) 2. Interest from investment account at National Savings and Investment Bank The following interests received are exempted: IAS savings certificates premium bonds

Employment income

Salary Bonus Commission / tips Add: Benefits in kind X X X X X Less:Allowable deductions (X) Employment income X

Monetary Earnings

Non-monetary Earnings

2015/7/23

(7,475)

X X X

(7,475)

X X

Deductible interest

• P25

2015/7/23

Savings income

Savings income are received net of 20% tax. So the net amount received for interest must be grossed up by dividing 80%. 1. Bank interest 2. Building society interest

X X X

X X X

Savings(×100/80)

Dividends(×100/90)

X

X

Xห้องสมุดไป่ตู้

X

Total income Less: Interest Paid

Net Income

X (X)

X

X

X

X (X)

X

X

X

Less: personal allowance

Taxable income Income Tax Liability

2015/7/23

Summary of tax rates

20%

20%

2,790 32,010

40%

150,000

45%

NSI

0

10%

20%

2,790 32,010

40%

150,000

45%

SI

0

DI

0

10%

2,790

10%

32,010

32.5%

37.5%

150,000

2015/7/23

Gift Aid

2015/7/23

Individual Savings Account This is subject to an overall annual investment limit of ₤11,520. investment of ₤5,760 can be cash Investments within an ISA are exempt from income tax and capital gains tax.

2015/7/23

Calculation pro-forma

Non-savings Income ₤ Savings income ₤ Dividend Income ₤ Total ₤

Trading profit Employment income Property business income

2015/7/23

child benefit

• when income tax charge arises • how to tax the benefit

2015/7/23

jointly hold property

• no claim • claim to make tax planning

2015/7/23

• The gift aid donation is paid net of 20%. • Additional tax relief is given by extending the donor‟s basic rate band and higher rate band by the gross amount of the donation. • adjusted net income

2015/7/23

Personal Allowance • All persons are entitled to a PA. It is deducted from Net Income. • PA for 2013/14 is ₤9,440 • If an individual‟s “adjusted net income” for 2013/134exceeds ₤100,000, the personal allowance is reduced by ₤1 for every ₤2 excess income. Once an individual‟s “adjusted net income” reaches ₤118,880 or over it will be reduced to nil. • “Adjusted net income” is after deducting trading losses, gross gift aid and gross personal pension contributions. • 60%

Chapter 2

The computation of taxable income and income tax liability

2015/7/23

Scope of income tax

• concerns whom will be taxed under the UK taxation law • p19

2015/7/23

Personal Allowance • PA for those aged 65-74 is ₤10,500 instead of ₤9,440. • PA for those aged 75 or over is ₤10,660 instead of ₤9,440. • If the individual‟s Net Income exceeds ₤26,100, the age allowance is reduced by ₤1 for each ₤2 Do not restrict allowance below the normal level of allowances (₤9,440) unless the adjusted net income exceed ₤100,000