corporate goverance syllbus

德国公司治理原则

German Panel on Corporate GovernanceCorporate Governance RulesforQuoted German CompaniesJanuary 2000German Panel on Corporate Governance *Code of Best PracticeforGerman Corporate GovernanceI.General questions of Corporate GovernanceThe purpose of Corporate Governance is to achieve a responsible, value-ori-ented management and control of companies. Corporate Governance Rules promote and reinforce the confidence of current and future shareholders, lend-ers, employees, business partners and the general public in national and inter-national markets. The Supervisory Board, Management Board and Executive Staff of the Company identify themselves with these Rules and are contractually bound by them. They are part of the general obligation to observe other inter-ests related to the corporate activity.The Rules of the Code serve as general guidelines for Corporate Governance for quoted German companies. Quoted companies are all enterprises whose shares are officially listed on a German stock exchange or traded over-the-counter. The Rules, their acceptance, implementation and respective adjust-ments to the specifics of the individual Company shall be communicated in the Annual Report.Due to the various legal systems, institutional parameters and traditions, there is presently no internationally accepted universal model for Corporate Govern-ance. The parameters for the Code are provided by codified law and leading cases, generally accepted national and international codes of good conduct and market practice. They include the directly relevant provisions of company and group law, in particular, the law governing stock corporations, financial ac-counting, banking supervision and the capital market as well as the Company's Memorandum and Articles of Association. From these derive the provisions, some of them detailed, with regard to the responsibilities and duties of the gov-erning bodies: Supervisory Board (§§ 95-116 German Stock Corporation Act), Management Board (§§ 76-94 German Stock Corporation Act) and General Meeting (§§ 118-147 German Stock Corporation Act) as well as the code of conduct of the members of the governing bodies.The essential points of the OECD Principles for Corporate Governance of May 1999 are covered as follows:Protection of Shareholders' rights: Following the introduction of the German Act on Corporate Control and Transparency (KonTraG) in 1998, there are adequate provisions safeguarding the rights of shareholders through the comprehensive mandatory rules under the German Stock Corporation Act. In particular, the fol-lowing OECD points are covered by mandatory law (§ 23 German Stock Corpo-ration Act):____________________________* Members:Prof. Dr. Theodor Baums, Prof. Dr. Dieter Feddersen, Ulrich Hartmann,Robert Koehler, Ulrich Hocker, Prof Dr. Rolf Nonnenmacher,- 2 -•full voting right for each ordinary share (§ 12 German Stock Corporation Act)•no impediments with regard to ownership or registration (§ 67 German Stock Corporation Act)•transferability of shares at any time (§ 68 German Stock Corporation Act)•participation, proxy and exercise of voting rights at General Meetings (§134 German Stock Corporation Act)•election of members of the Supervisory Board (§ 101 German Stock Corpo-ration Act)•participation in company profits (§ 58 German Stock Corporation Act).These points are mandatorily covered by German Law (§ 23 German Stock Corporation Act).An authorization to increase the share capital with exclusion of shareholder participation rights in order to pursue either an acquisition or a share placement near the prevailing market price will only be exercised by the Management Board if the share capital increase does not exceed 10 % of the then existing share capital. In this calculation the re-utilization of any repurchased shares will be included.Equal treatment of shareholders: The 'Equal treatment of shareholders' stipu-lated by the OECD is also in place for German companies. The precautionary measures against insider trading, self-dealing and disclosure of any personal interests in transactions or matters are extended beyond the legal requirements by the subsequent points 'II. Management Board' and 'III. Supervisory Board'. Until the enactment of the German Takeover Law, the voluntary Takeover Code of the Capital Markets Expert Commission of the German Ministry of Finance applies. This Code is accepted by the Company.In the case of repurchase of own shares according to § 71, subparagraph 1, No. 8 German Stock Corporation Act, the Company shall observe the principle of equal treatment of all shareholders.Disclosure and transparency: The point 'Disclosure and transparency' of the OECD Principles is generally covered by law for German companies through the corresponding provisions on the obligation to provide and enclose informa-tion (§§ 20 - 22, 160, 328 German Stock Corporation Act; §§ 15, 25 German Securities Trading Act; §§ 285, 325 ff German Commercial Code; §§ 35, 39 German Antitrust Act; § 24 German Banking Act). In addition, the Management Board shall regularly and with due regard to equal treatment of all shareholders ('Fair Disclosure') report on all Company matters through Annual and Interim Reports, 'ad hoc' communications, analyst and press conferences. The OECD information requirements are covered by these publicity undertakings.The Company shall adopt an accounting standard that is suitable for interna-tional comparison purposes..../3- 3 -As the Management Board and Supervisory Board of German companies have the decisive functions for Corporate Governance, the relevant points are dealt with in detail below:BoardI I.Management1.)Responsibilities and dutiesa) In the management of the Company, the Management Board is boundby Corporate interest, Company policy and the Group's guidelines aswell as the basic principles of proper management (§ 76 German StockCorporation Act).b) The Management Board develops, in consultation with the SupervisoryBoard, the strategy for the Group and is responsible for its implementa-tion.c) The Management Board is responsible for ensuring compliance withlegal provisions within the Group and to ensure their observation byGroup companies.2.)Information and disclosure requirementsa) The Management Board will publish without delay any new facts arisingin the sphere of the Company's activities which are not yet publiclyknown and, due to their impact on their financial position of the Com-pany or its general course of business, are likely to impact significantlyon the price of the Company's listed securities (§ 15 German SecuritiesTrading Act).As part of its regular communication efforts, the dates of major regularpublications (such as annual and quarterly reports, General Meetings)shall be published in a 'Financial Calendar' (at least one year) in ad-vance.The information published by the company shall also be available in the'Internet'. This is to include the invitation to General Meetings, theiragenda as well as shareholder initiatives and management commentshereto as well as voting results of such meetings. If possible, all publi-cations are provided in the English language.b) The company shall pursue the principle of equal treatment of all share-holders in the matter of information dissemination.c) The regular financial reporting (annual and quarterly reports) will betimely. The quarterly reports contain segment reporting as well as re-sults per share.d) The Management Board shall inform the Supervisory Board on a regu-lar basis, in good time and comprehensively about all relevant mattersregarding business development, risk exposure and risk managementof the company and major group subsidiaries.e) Should the business trend or risk exposure of the Group change sig-nificantly against plan, the Management Board must immediately in-f) The Management Board shall list in the Notes to the Company Ac-counts the corporations in which the Company holds a minimum of10% of the share capital. Exempt from this are participations that are ofimmaterial importance for the Company's asset, financial and profitsituation.Equally, any existing mutual shareholdings and any shareholdings inthe Company which have been notified by third parties as well as theowner(s) of such shareholdings must be reported in the Notes to theAccounts.g) As soon as the Company is notified (§ 25 German Securities TradingAct), or becomes otherwise aware that another party has obtained, ex-ceeds or no longer holds 5, 10, 25, 50 or 75% of the voting rights in theCompany, this will immediately be published by the ManagementBoard.h) In the Notes to the Company Accounts details with regard to the Man-agement Board's interest in shares of the Company (including any ex-isting option rights) and their changes in relation to the previous yearhave to be published.3.)Remunerationa) The remuneration of the Management Board and the Executive Staffshall include sufficient motivation to ensure long-term corporate valuecreation. This includes share option programmes and performance-re-lated incentives related to the share price development and the con-tinuing success of the company. In connection with the granting ofshare options and similar rights to members of the Management Boardand the executive staff the following points shall be observed:The initial exercise of the rights arising from share option programmesshall not be possible before two years since the grant. To document theincentive character as well as to balance the surrender of the subscrip-tion right by the shareholders, the exercise shall depend on achievingor exceeding relevant and transparent benchmarks (e.g. the develop-ment of an industry index).The structure, total amount, exercise prices and exercise periods aswell as the allocations of share options and similar rights in the report-ing period shall be published in the Notes to the Company Accounts,separately by members of the Management Board and Executive Staff.To ensure compliance with insider laws, suitable precautions likeclosed periods of time are implemented.b) The fixed and variable remuneration elements of the ManagementBoard shall be detailed in the Annual Report.4.)Rules governing conflicts of interest and own-account transactionsa) In the running of the management of the company, the ManagementBoard members must not pursue any own interest that could be in con-flict with the interest of the Company.b) Members of the Management Board must disclose to the SupervisoryBoard material personal interests in transactions of the Company and Group companies as well as other conflicts of interest. They must also inform their Management Board colleagues.c) All transactions between the Company or any Group company andManagement Board members as well as associated persons or com-panies must comply with normal industry standards. The transactions and the terms and conditions thereof must be approved in advance by the Supervisory Board. They may not run counter to the interests of the Company or any Group company. The granting of loans to Manage-ment Board members must be approved by the Supervisory Board with advance notice to the Management Board. In all such transactions, the Company shall be represented by the Supervisory Board.d) Management Board members and senior Group executives may notexploit business opportunities available to the Company or Group com-panies for themselves or for the benefit of associated persons or com-panies.e) Management Board members and senior Group executives are alsoprohibited from conducting transactions, conflicting with the interests of the Company or any Group company, for themselves or for associated persons. This prohibition also extends beyond their business duties.Management Board members must disclose to the whole Management Board transactions (except daily life transactions) among themselves or with Supervisory Board members or senior Group executives. The transactions require the approval of the Supervisory Board.f) Management Board members and senior Group executives are duringtheir employment subject to a comprehensive prohibition of competition (Members of the Management Board: § 88 German Stock Corporation Act).g) Any other activities of Management Board members, in particular theacceptance of Supervisory Board appointments, require the approval of the Supervisory Board. Any other activities of senior Group executives require the approval of the Management Board.h) The purchase and sale of Company shares, options or other share de-rivatives by members of the Management Board and senior Group ex-ecutives are subject to special rules. It is generally welcomed that the Management Board and senior Group executives document their iden-tification with the Company through a shareholder status.However, they should refrain from frequent transactions and counter transactions which aim to achieve very short term gains (speculative deals). Appropriate measures such as closed periods for the purchase or sale of shares should ensure the observation of the provisions of the insider laws. The Management Board shall ensure the compliance through a Compliance Officer that shall report to the Supervisory Board at least once a year.i) Management Board members and Group employees may in connec-tion with their activity neither request nor receive gifts or other advan-tages for themselves or third parties, if this could jeopardize the inter-ests of the Group or the interests of customers.I I I.Supervisory Board1.)Compositiona) The proposals for election of Supervisory Board members to the Gen-eral Meeting shall ensure that the proposed candidates have both therequired knowledge and skills as well as the relevant professional ex-perience. To ensure efficiency, regard will be given to size and compo-sition of the Supervisory Board. Board Members must make sufficienttime available to exercise their activity in a diligent manner.b) The Supervisory Board shall ensure independent advice and monitor-ing of the Management Board through a sufficient number of independ-ent persons who have no current or former business association withthe Group. This shall also be taken into consideration for the composi-tion of the Supervisory Board committees. The proposal for election tothe Supervisory Board shall not include as a matter of course the elec-tion of retiring Management Board members.c) If a member of the Supervisory Board does not participate personally inmore than half of the Board Meetings of any given fiscal year, this hasto be notified in the Annual Report.d) The remuneration of the Supervisory Board shall appropriately reflectthe responsibility, the work performed and the increase in the corporatevalue. The total remuneration shall be listed in the Notes to the Com-pany Accounts.e) The Notes to the Company Accounts shall contain details of the share-ownership (including existing option rights) of the Supervisory Boardmembers and their changes in relation to the previous year.2.)Responsibilities and dutiesa) The Supervisory Board advises the Management Board on a regularbasis regarding the management of the Company and the Group andmonitors the achievement of the long term corporate goals (monitoring:§ 111 German Stock Corporation Act). The Supervisory Board appointsthe members of the Management Board and ensures an orderly long-term succession planning (§ 84 German Stock Corporation Act).b) The Supervisory Board can subject certain transactions to its approval(§111 German Stock Corporation Act). This refers in particular to in-vestment projects, loans, the establishment of subsidiaries as well asthe acquisition or disposal of shareholdings above a certain size.c) The members are bound to confidentiality with regard to all specific in-formation and company secrets.d) The Supervisory Board issues its own Standing Rules and stipulatesthe information and reporting duties of the Management Board.e) The Supervisory Board mandates the Auditors to audit the Companyand the Group annual accounts (§111 German Stock Corporation Act).Particular regard shall be given to:•that the mandated Auditor has not achieved during the last five years with the Audit and advice of the Company (or with corpora-tions where the Company is a shareholder with more than 20%)more than 30% of his total revenue. This should also not be ex-pected for the current fiscal year,•that no auditor is employed in the Audit that has issued the audi-tors' confirmation for the Annual Accounts or Group Accounts inmore than 6 instances in the 10 years preceding the audit,•that no conflicts of interest exist for the Auditor.All members of the Supervisory Board shall receive the Audit Reportsin good time before the pertinent Supervisory Board meetings (§ 170German Stock Corporation Act). Audit related meetings shall be held inthe presence of the Auditors (§ 171 German Stock Corporation Act).f) Contracts, in particular consulting contracts of the company with mem-bers of Supervisory Board require the approval of Supervisory Board(except every day transactions).g) The Supervisory Board shall receive regularly (at least annually) a re-port by the Management Board with regard to donations exceeding anamount determined by the Supervisory Board.3.)Establishment of CommitteesThe Supervisory Board shall establish in line with its Standing Rules vari-ous committees to deal with complex business matters. With regard to the composition of such committees, the Supervisory Board shall ensure the requisite professional experience. Incorporation and duties of committees are subject to the specific circumstances and the size of the Company. The following committees could be instituted:•General Committee: The General Committee shall advise the Man-agement Board and prepare the decisions to be taken by the Super-visory Board. The General Committee deals with general policy mattersfor the Group. It discusses the strategy and planning for the Group andits business segments submitted by the Management Board on the ba-sis of different scenarios and their feasibility. The General Committeeassesses the internal state of the Group with regard to its operatingstrength, efficiency and potential to achieve the formulated targets. Itreviews the Corporate Governance Rules and their compliance on aregular basis (generally once a year).•Accounts and Audit Committee: The Accounts and Audit Committee is responsible for matters pertaining to the accounting and auditing for the Company and the Group. The Committee evaluates the Auditor's reports and reports to the Supervisory Board on its assessment of the comments in the audit report, particularly with regard to the future de-velopment of the Group. It verifies the Management Board's assump-tions on the budget figures for the Group and its business segments.Important other documents issued to shareholders shall be presented before publication to the Committee.The tasks of the Accounts and Audit Committee regularly comprise:- the preparation of the selection of the Auditor, the determination of major auditing issues, even if exceeding the legally required pointsand content of the Audit, as well as the determination of the Audi-tors' fee,- the preparation of the audit of the Annual and Group Accounts by the Supervisory Board, including the relevant business reports onthe basis of the results of the audit and additional points raised bythe Auditor,- the preparation of a report by the Management Board with regard to corporate donations exceeding an amount determined by theSupervisory Board,and, if applicable,- the discussion of partial auditing results during the year (e.g. of the internal control system),- the discussion of Interim Accounts and the results of any audits performed therefor.•Personnel Committee: The Personnel Committee deals with the per-sonnel issues of the Management Board (including its succession planning). The Personnel Committee shall recommend with regard to the content of the employment contracts of the Management Board in-cluding their remuneration. In addition, the Committee is responsible for the approval of paid for outside company work by members of the Man-agement Board. The granting of loans to members of the Management Board and the Supervisory Board shall also be dealt with by the Com-mittee.•Nomination Committee: The Nomination Committee is in charge of the composition, size and balance of the Supervisory Board and the proposals for election to the General Meeting.•Market- and Credit Risk Committee: This Committee supervises the handling of market risks and credit matters of the Group. It handles loans and other transactions requiring its approval and is informed of loans requiring its notification. For urgent matters, decisions can be delegated to nominated Committee members.- 9 -•Mediation Committee: German Stock companies that are subject to codetermination by law, are legally required to establish a MediationCommittee (§ 27 subpara 3 Co Determination Act of 1976). This Com-mittee delivers proposals for the appointment of Management Boardmembers if the required two thirds majority for the appointment or ter-mination of Management Board members has not been achieved.4.)Rules governing conflicts of interest and own-account transactionsa) The Supervisory Board members must disclose any conflicts of interestto the Chairman of the Supervisory Board or his deputy unless they re-tire for cause. In the event of conflicts of interests, the Chairman of theSupervisory Board or his deputy shall decide to whom the informationshould be forwarded and whether the member of the SupervisoryBoard in question shall participate in meetings.b) In their decisions Supervisory Board members must not pursue theirown interests or those of associated persons or companies, which arein conflict with the interests of the Company or any Group company.They may not pursue for their own benefit business available to theCompany or its Group companies. In the event of possible conflicts ofinterest, the interests of the Company and its Group companies musttake priority and the Supervisory Board members concerned must ab-stain from voting.c) All transactions between the Company, any Group company and Su-pervisory Board members as well as associated persons or companiesmust comply with normal industry standards. The transactions (except:daily life transactions) and their terms must be approved in advance bythe Supervisory Board. They may not run counter to the interests of theCompany or any Group company.d) The granting of loans to Supervisory Board members by the Companyor Group companies require the agreement of the Management Boardand the Supervisory Board.e) Supervisory Board members may, in conjunction with their activity,neither request nor receive gifts or other advantages for themselves orthird parties, if this could jeopardize the interests of the Group or cus-tomers.Frankfurt, January 2000。

管理学常用英文单词-含音标

管理学常用词汇A 11access discrimination ['æksɛs] [dɪ,skrɪmɪ'neʃən]进入歧视action research ['ækʃən] ['risɝtʃ] 动作研究;行为研究adjourning [ə'dʒɝnɪŋ] 解散期;解散阶段;中止阶段adhocracy [æd'hɔkrəsi] 无固定结构的管理方式或组织;临时委员会组织;administrative principle [əd'mɪnɪstretɪv] ['prɪnsəpl] 管理原则advanced negotiation[əd'vænst] [nɪ,ɡoʃɪ'eʃən]高级谈判alignment[ə'laɪnmənt] 结盟artifacts ['a:rtifækts]人工环境artificial intelligence [,ɑrtɪ'fɪʃl] [ɪn'tɛlɪdʒəns] 人工智能、巧匠avoiding learning [ə'vɔɪdɪŋ] ['lɜːnɪŋ]规避性学习ambidextrous approach [,æmbɪ'dekstrəs] [ə'prɔtʃ]双管齐下策略B 9balance sheet ['bæləns] [ʃit]资产负债表bias['baɪəs] 偏见BCG matrix( BCG:Boston Consulting Group['bɔstən] [kən'sʌltɪŋ] [gru ːp]) ['metrɪks] 波士顿矩阵,波士顿咨询集团矩阵bona fide occupation qualifications [,bəunə'faidi] [,ɑkju'peʃən] [,kw ɑləfə'keʃən] 善意职业资格审查bounded rationality ['baʊndɪd] [,ræʃən'æləti]有限理性bounded rationality perspective ['baʊndɪd] [,ræʃən'æləti] [pə'spekt ɪv]有限理性方法bureaucracy [bjʊ'rɑkrəsi]官僚机构benchmarking ['bentʃ,mɑ:kiŋ] 标杆管理;标记;确定基准点boundary-spanning roles ['baʊndri] ['spæniŋ] [rolz] 跨超边界作用C 42capturing value through pricing['kæptʃɚrɪŋ] ['vælju] [θru] ['praɪsɪŋ] 通过定价获取价值change agent [tʃendʒ] ['edʒənt] 变革推动者,促变者challenge ['tʃælɪndʒ]挑战chaos theory ['keɑs] ['θiəri] 混沌理论charismatic leaders [,kærɪz'mætɪk] ['lidɚz]魅力型领导者charity principle ['tʃærəti] ['prɪnsəpl] 博爱原则closing bell['klozɪŋ] [bɛl]收盘corporate social responsibility ['kɔrpərət] ['soʃl] [rɪ,spɑnsə'bɪləti]企业的社会责任competitive strategy[kəm'pɛtətɪv] ['strætədʒi]竞争战略;竞争策略confrontation [,kɑnfrənfrʌn'teʃən] 对话, 对抗;面对;对质confrontation meeting [,kɑnfrən'teʃən] ['mitɪŋ] 碰头会consortia [kən'sɔ:tɪə] 企业联合、联盟、合作coercive power [kəʊ'ɜːsɪv] ['paʊə] 强制权,强制力cohesiveness [ko'hisɪvnɪs] 凝聚力collaborative management [kə'læbəretɪv] ['mænɪdʒmənt]合作型管理comparable worth ['kɑmpərəbl] [wɝθ]可比价值;同值同酬competitive benchmarking [kəm'petɪtɪv] ['bentʃ,mɑ:kiŋ]竞争性基准competitive strategy[kəm'pɛtətɪv] ['strætədʒi]竞争策略constancy of purpose ['kɑnstənsi] [əv] ['pɜːpəs] 永久性目标contingency approach [kən'tɪndʒənsi] [ə'protʃ] 权变理论;权变方法;随机应变法corporate governance['kɔrpərət] ['gʌvɚnəns]企业管治corporate social performance ['kɔrpərət] ['səʊʃ(ə)l] [pə'fɔːm(ə)ns]企业社会绩效;公司社会表现corporate social responsibility ['kɔrpərət] ['səʊʃ(ə)l] [rɪ,spɑnsə'bɪləti]公司社会责任corporate social responsiveness ['kɔrpərət] ['səʊʃ(ə)l] [rɪ'spɑnsɪvnɪs]公司社会反应critical incident ['krɪtɪkl] ['ɪnsɪdənt] 危机事故;关键事件current assets ['kʌr(ə)nt] ['æset s] 流动资产current liabilities ['kʌr(ə)nt] [,laɪə'bɪləti]流动负债; 经常性贷款culture strength ['kʌltʃə] [streŋθ]文化强度; 文化力creative department [krɪ'etɪv] [dɪ'pɑrtmənt] 创造性部门creation of value[krɪ'eʃən] [əv] ['vælju]价值创造craft technology [kræft] [tɛk'nɑlədʒi]工艺技术、技艺性技术contextual dimension [kən'tɛkstʃuəl] [daɪ'mɛnʃən]关联性维度continuous process production [kən'tɪnjʊəs] ['prɑsɛs] [prə'dʌkʃən]连续加工生产collectivity stage [,kɑlɛk'tɪvəti] [stedʒ] 集体化阶段clan control [klæn] [kən'trol] 小团体控制clan culture [klæn] ['kʌltʃɚ] 小团体文化coalition [,koə'lɪʃən] 联合;结合,合并;联合团体collaborative [kə'læbəretɪv] 协作网络centrality [sɛn'træləti] 中心;中央;向心性;集中性centralization [,sɛntrəlɪ'zeʃən]集权化;中央集权管理charismatic authority [,kærɪz'mætɪk] [ə'θɔrəti] 魅力型权威、竭尽忠诚的权力customer insight['kʌstəmɚ] ['ɪn'saɪt]消费者洞察力;客户需求D 18decentralization [dɪ'sɛntrəlaɪ'zeʃən]分权;非集权化decision premise [dɪ'sɪʒn] ['premɪs]决策前提democracy management [də'mɑkrəsi] ['mænɪdʒmənt] 民主管理departmentalization [di:pɑ:t,mentəlai'zeiʃən]部门化; 部门划分designing effective organization[dɪ'zaɪnɪŋ] [ɪ'fɛktɪv] [,ɔrɡənə'zeʃən]设计有效的组织development structure[dɪ'vɛləpmənt] ['strʌktʃɚ]发展结构dialectical inquiry methods [,daɪə'lɛktɪkl] ['ɪŋkwaɪri] ['mɛθədz]辩证探求法differentiation strategy [,dɪfərenʃɪ'eɪʃn] ['strætədʒi] 差别化战略;差异化竞争战略differential rate system ['dɪfə'rɛnʃəl] [ret] ['sɪstəm] 差别报酬系统direct interlock [də'rɛkt] ['ɪntɚlɑk] 直接交叉divisional form [də'vɪʒənl] [fɔrm] 事业部模式division of labor [də'vɪʒən] [əv] ['lebɚ] 劳动(力)分工downward mobility ['daʊnwɚd] [mo'bɪləti] 降职流动、社会地位的下降dynamic engagement [daɪ'næmɪk] [ɪn'ɡedʒmənt]动态融合dynamic network [daɪ'næmɪk] ['nɛtwɝk] 动态网络domain [do'men] 领域;;域名;产业;地产dual-core approach ['dʊəl] [kɔr] [ə'protʃ] 二元核心模式dynamics of synergy[daɪ'næmɪks] [əv] ['sɪnɚdʒi]协力优势E 28effective decision making[ɪ'fɛktɪv] [dɪ'sɪʒn] ['mekɪŋ]有效决策制定effective leadership[ɪ'fɛktɪv] ['lidɚʃɪp]有效领导effective conflict resolution[ɪ'fɛktɪv] ['kɑnflɪkt] [rezə'luːʃ(ə)n]高效冲突管理electronic data-processing(EDP) [ɪ,lɛk'trɑnɪk] ['detə] ['prɑsɛsɪŋ]]电子数据处理employee-oriented style [ɪm'plɔɪi] ['orɪɛntɪd] [staɪl] 员工导向型风格empowerment [ɪm'paʊɚmənt] 许可,授权encoding [ɪn'kodɪŋ] 解码; 编码end-user computing ['end,ju:zə] [kəm'pjʊtɪŋ]终端用户计算系统enter ['ɛntɚ]进入;参加enterprise ['ɛntɚ,praɪz]企业entrepreneurship [,ɑntrəprə'nɝʃɪp] 企业家精神equity ['ɛkwəti]平等;相等equity theory ['ɛkwəti] ['θiəri] 公平理论espoused value [ɪ'spaʊzid] ['vælju]信仰价值ethics['eθɪks] 伦理学;伦理观;道德标准ethnocentric manager [,ɛθno'sɛntrɪk] ['mænɪdʒɚ] 种族主义的管理者expectancy theory [ɪk'spɛktənsi] ['θiəri] 期望理论expense budget [ɪk'spɛns] ['bʌdʒɪt] 费用预算;支出预算expense center [ɪk'spɛns] ['sɛntɚ]费用中心external audit [ɪk'stɝnl] ['ɔdɪt] 外部审计; 独立审计external stakeholders [ɪk'stɝnl] ['stekholdɚ] 外部利益相关者extreme circumstances[ɪk'strim] ['sɝkəmstæns iz]极端情况extrinsic rewards [ɛks'trɪnsɪk] [rɪ'wɔrdz] 外部奖励;外部报酬ethic ombudsperson ['ɛθɪk] [,ɔmbudz'pɝsn] 伦理巡视官external adaption [ɪk'stɝnl] [ə'dæpʃən] 外部适应性elaboration stage [ɪ,læbə'reʃən] [stedʒ] 精细阶段entrepreneurial stage [,ɑntrəprə'njʊrɪəl] [stedʒ] 创业阶段escalating commitment ['ɛskəletɪŋ] [kə'mɪtmənt] 顽固认同F 14family group ['fæməli] [gruːp] 家族集团;家族企业financing growth[fɪ'nænsɪŋ] [ɡroθ]财务增长financial management [faɪ'nænʃl] ['mænɪdʒmənt] 财务管理;金融管理financial statement [faɪ'nænʃl] ['stetmənt] 财务报表flat hierarchies [flæt] ['haɪə,rɑrkiz] 扁平型结构flexible budget ['flɛksəbl] ['bʌdʒɪt] 弹性预算force-field theory [fɔrs] [fild] ['θiəri] 场力理论formal authority ['fɔrml] [ə'θɔrəti] 正式授权;正式权限;合法权力formal systematic appraisal ['fɔrml] ['sɪstə'mætɪk] [ə'prezl] 正式的系统评估franchise ['fræntʃaɪz] 特许经营权formalization stage [,fɔməlɪ'zeʃən] [stedʒ] 规范化阶段functional grouping ['fʌŋkʃənl] ['ɡrupɪŋ] 职能组合formal channel of communication ['fɔrml] ['tʃænl] [əv] [kə,mjunɪ'keʃən] 正式沟通渠道fundamentals [,fʌndə'mɛntl] 基本面;基本原理G 16game theory [geɪm] ['θiəri] 博弈论general financial condition ['dʒɛnrəl] [faɪ'nænʃl] [kən'dɪʃən] 一般财务状况geocentric manager [,dʒio'sɛntrɪk] ['mænɪdʒɚ] 全球化管理者geographic and cultural boundaries[,dʒiə'ɡræfɪk] [ənd] ['kʌltʃərəl] ['baʊndri]地理和文化界限global brand['ɡlobl] [brænd]全球品牌global enterprise['ɡlobl] ['ɛntɚ'praɪz]全球化企业global market ['ɡlobl] ['mɑrkɪt]全球市场;国际市场globalization [,ɡləubəlai'zeiʃən] 全球化gossip chain ['ɡɑsɪp] [tʃen] 传言链grapevine ['ɡrepvaɪn] 小道消息;秘密情报网;传言网global strategic partnership ['ɡlobl] [strə'tidʒɪk] ['pɑrtnɚʃɪp] 全球战略伙伴关系general environment ['dʒɛnrəl] [ɪn'vaɪrənmənt] 一般环境;总体环境generalist ['dʒɛnrəlɪst] 通才;多面手;全面战略geographic grouping [,dʒiə'ɡræfɪk] ['ɡrupɪŋ] 区域组合global company ['ɡlobl] ['kʌmpəni] 跨国公司;全球公司global geographic structure ['ɡlobl] [,dʒiə'ɡræfɪk] ['strʌktʃɚ]全球区域结构H 11Hawthorne effect [hɔθən] [ɪ'fɛkt] 霍桑效应heuristic principles [hjʊ'rɪstɪk] ['prɪnsəpl] 启发性原理hierarchy ['haɪərɑrki] 科层制度high ambition[haɪ] [æm'bɪʃən]更高志向、雄心壮志high commitment[haɪ] [kə'mɪtmənt]高承诺high performance[haɪ] [pɚ'fɔrməns]高效能hiring specification ['haiəriŋ] ['spɛsəfə'keʃən] 招聘细则horizontal linkage model ['hɔrə'zɑntl] ['lɪŋkɪdʒ] ['mɑdl] 横向联系模型hybrid structure ['haɪbrɪd] ['strʌktʃɚ] 混合结构high-velocity environments [haɪ] [və'lɑsəti] [ɪn'vaɪrənmənts] 高速环境human resources['hjumən] [ri'zɔ:siz]人力资源I 23impoverished management [ɪm'pɑvərɪʃt] ['mænɪdʒmənt] 放任式管理 I income statement ['ɪnkʌm] ['stetmənt] 损益表information transformation ['ɪnfɚ'meʃən] [,trænsfɚ'meʃən] 信息转换infrastructure ['ɪnfrə'strʌktʃɚ] 基础设施integrative process ['ɪntɪɡretiv] ['prɑsɛs] 整合过程intelligent enterprises [ɪn'tɛlɪdʒənt] ['ɛntɚ,praɪz]智能企业;智慧型企业internal audit [ɪn'tɝnl] ['ɔdɪt] 内部审计internal stakeholder [ɪn'tɝnl] ['stekholdɚ] 内部相关者internship ['ɪntɝnʃɪp]实习intrapreneurship [,ɪntrəprɛ'nɝʃɪp]内部企业家精神intrinsic reward [ɪn'trɪnsɪk] [rɪ'wɔrd]内在报酬; 内在奖励inventory ['ɪnvəntɔri] 库存, 存货internal integration [ɪn'tɝnl] ['ɪntə'greʃən] 内部整合interorganization relationship [,ɪntɚ'ɔrɡənə'zeʃən l [rɪ'leʃən'ʃɪp] 组织间的关系intergroup conflict ['ɪntɚ'grʊp] ['kɑnflɪkt] 团体间冲突intergroup dynamics ['ɪntɚ'grʊp] [daɪ'næmɪks] 组间动力interlocking directorate [,intə'lɔkiŋ] [də'rɛktərət] 交叉董事会institutional perspective [,ɪnstɪ'tuʃənl] [pɚ'spɛktɪv] 制度视角;机构的观点intuitive decision making [ɪn'tuɪtɪv] [dɪ'sɪʒn] ['mekɪŋ]直觉决策idea champion [aɪ'diə] ['tʃæmpɪən] 构思倡导者incremental change [ɪnkrə'məntl] [tʃendʒ] 渐进式变革; 递增量informal organizational structure [ɪn'fɔrml] [,ɔɡənɪ'zeʃənəl] ['strʌkt ʃɚ]非正式组织结构informal performance appraisal [ɪn'fɔrml] [pɚ'fɔrməns] [ə'prezl]非正式业绩评价J 6job description [dʒɒb] [dɪ'skrɪpʃən]工作说明;职务描述job design[dʒɒb] [dɪ'zaɪn] 工作设计,职务设计job enlargement [dʒɒb] [ɪn'lɑrdʒmənt] 职务扩大化job enrichment [dʒɒb] [ɪn'rɪtʃmənt] 职务丰富化job rotation [dʒɒb] [ro'teʃən] 职务轮换job specialization [dʒɒb] [,spɛʃəlɪ'zeʃən]职务专业化K 2key performance areas [kiː] [pɚ'fɔrməns] ['ɛrɪəz]关键业务区key result areas [kiː] [rɪ'zʌlt] ['ɛrɪəz]关键绩效区L 18labor productivity index ['lebɚ] [,prodʌk'tɪvəti] ['ɪndɛks] 劳动生产力指数laissez management [lei'sei'] ['mænɪdʒmənt]自由化管理large batch production [lɑrdʒ] [bætʃ] [prə'dʌkʃən]大批量生产lateral communication ['lætərəl] [kə,mjunɪ'keʃən] 横向沟通leadership decision ['lidɚʃɪp] [dɪ'sɪʒn]领导决策leadership style ['lidɚʃɪp] [staɪl] 领导风格leadership in teams ['lidɚʃɪp] [ɪn] [timz]团队管理;团队领导力leading a turnaround['lidɪŋ] ['tɝnəraʊnd] 领导转变;管理转变least preferred co-worker(LPC) [list] [prɪ'fɝd] [,kəu'wə:kə] 最不喜欢的同事legitimate power [lɪ'dʒɪtɪmət] ['paʊɚ]合法权力liability ['laɪə'bɪləti] 债务;负债liaison [lɪ'ezɑn] 联络者line authority [laɪn] [ə'θɔrəti] 直线职权liquidity [lɪ'kwɪdəti] 流动性liaison role [lɪ'ezɑn] [rol] 联络员角色long-linked technology [lɔŋ] ['lɪŋkt] technology 纵向关联技术losses from conflict [lɔsiz] [frɒm] ['kɑnflɪkt]冲突带来的损失low-cost leadership [ləʊ] [kɔst] ['lidɚʃɪp] 低成本领先M 21management by objective ['mænidʒmənt] [baɪ] [əb'dʒɛktɪv]目标管理Managerial Grid [,mænə'dʒɪrɪəl] [ɡrɪd] 管理方格matrix bosses ['metrɪks] [bɔsiz] 矩阵主管management champion ['mænɪdʒmənt] ['tʃæmpɪən] 管理倡导者materials-requirements planning(MRP) [mə'tiəriəlz] [ri'kwaiəmənts] ['plænɪŋ]物料需求计划Maslow’s hierarchy of needs ['mæzləu] ['haɪərɑrki] [əv] [nid] 马斯洛需求层次论marketing argument ['mɑrkɪtɪŋ] ['ɑrɡjumənt] 管理文化多元化营销观market segmentation['mɑrkɪt][,sɛɡmɛn'teʃən]市场划分;市场细分multiculturalism [,mʌltɪ'kʌltʃərəlɪzm] 文化多元主义multi-divisional firm ['mʌlti] [də'vɪʒənl] [fɝm] 多部门公司moral rules ['mɔrəl] [rulz]道德准则management by walking around(MBWA) ['mænɪdʒmənt] [baɪ] ['wɔkɪŋ] [ə'raʊnd]走动式管理matrix structure ['metrɪks] ['strʌktʃɚ]矩阵结构multinational enterprise(MNE) [,mʌltɪ'næʃnəl] ['ɛntɚ'praɪz]跨国公司moral relativism ['mɔrəl] ['rɛlətɪvɪzəm] 道德相对主义mechanistic system [,mɛkə'nɪstɪk] ['sɪstəm] 机械式组织middle-of-the-road management ['mɪdl] [əv] [ðə] [rod] ['mænɪdʒmənt]中庸式管理meso theory ['mɛso] ['θiəri] 常态理论multi-domestic strategy ['mʌlti] [də'mɛstɪk] ['strætədʒi] 多国化战略mediating technology ['miːdɪeɪtɪŋ] [tɛk'nɑlədʒi] 调停技术motivation[,motə'veʃən] 动机;积极性;推动N 9naïve relativism [naɪ'iv] ['rɛlətɪvɪzəm] 朴素相对主义need-achievement [nid] [ə'tʃivmənt] 成就需要net asset [nɛt] ['æsɛt]净资产norming ['nɔ:miŋ] 规范化norms [nɔ:ms] 规范non-programmed decisions [nɑn 'proɡrəmd] [dɪ'sɪʒnz]非程序化决策non-substitutability [nɑn,səbstə,tjutə'biləti]非替代性non-routine technology [nɑn rʊ'tin] [tɛk'nɑlədʒi] 非例行技术niche [nitʃ] 领地; 壁龛;合适的职业;小众O 14off-the-job training ['ɔfðə'dʒɔb ] ['trenɪŋ ] 脱产培训on-the-job training ['ɑnðə'dʒɔb ] ['trenɪŋ ] 在职培训operation[,ɑpə'reʃən]运营operational budget ['ɑpə'reʃənl] ['bʌdʒɪt] 运营预算order backlog ['ɔrdɚ] ['bæklɔɡ] 订单储备organic system [ɔr'gænɪk] ['sɪstəm] 有机系统organizational development(OD) [,ɔɡənɪ'zeʃənəl] [dɪ'vɛləpmənt]组织发展organizational hierarchies [,ɔɡənɪ'zeʃənəl] ['haɪə,rɑrki] 组织层级;组织架构organizing for innovation['ɔrgə,naɪz ɪŋ] [fɔː] [,ɪnə'veʃən]组织创新orientation [orɪɛn'teʃən] 定位outcome interdependence ['aʊt'kʌm] [,ɪntɚdɪ'pɛndəns]结果的相互依赖性outplacement services ['aʊtplesmənt] ['sə:visis] 外延服务overconfidence['ovɚ'kɑnfɪdəns] 过分相信;自负organization ecosystem [,ɔ:ɡənai'zeiʃən] ['ɛko,sɪstəm] 组织生态系统P 27paradox of authority ['pærədɑks] [əv] [ə'θɔrəti]权威的矛盾paradox of creativity ['pærədɑks] [əv] [,krie'tɪvəti] 创造力的矛盾paradox of disclosure ['pærədɑks] [əv] [dɪs'kloʒɚ] 开放的矛盾paradox of identify ['pærədɑks] [əv], [aɪ'dɛntɪfaɪ] 身份的矛盾paradox of individuality ['pærədɑks] [əv] [,ɪndɪ,vɪdʒu'æləti] 个性的矛盾paradox of regression ['pærədɑks] [əv] [rɪ'ɡrɛʃən] 回归的矛盾partial productivity ['pɑrʃəl] [,prodʌk'tɪvəti] 部分生产率participative management [pɑ:'tisipə,tiv] ['mænɪdʒmənt] 参与式管理path-goal model [pæθ] [ɡol] ['mɑdl] 路径目标模型peer recruiter [pɪr] [rɪ'krʊtɚ] 同级招聘political action committees(PACs) [pə'lɪtɪkl] ['ækʃən] [kə'mitiz]政治活动委员会polycentric manager [pɑlɪ'sɛntrɪk] ['mænɪdʒɚ]多中心管理者portfolio framework [pɔrt'folɪo] ['fremwɝk] 业务组合框架portfolio investment [pɔrt'folɪo] [ɪn'vɛstmənt] 资产组合投资positive reinforcement ['pɑzətɪv] [,riɪn'fɔrsmənt] 正强化production flexibility [prə'dʌkʃən] [,flɛksə'bɪləti] 生产柔性profitability [,prɑfɪtə'bɪləti] 收益率; 赢利能力;利益率programmed decisions ['proɡr æ md] [dɪ'sɪʒən]程序化决策psychoanalytic view ['saɪko,ænl'ɪtɪk] [vju]精神分析法paradigm ['pærə'daɪm] 范式; 典范personal ratios ['pɝsənl] ['reʃoz]人员比例pooled dependence [puld] [dɪ'pɛndəns]集合性依存professional bureaucracy [prə'feʃənəl] [bjʊ'rɑkrəsi]专业官僚机构problem identification ['prɑbləm] [aɪ'dɛntəfə'keʃən]问题识别problemistic search ['prɔbləmistik] [sɝtʃ]问题搜寻population ecology model [,pɔpju'leiʃən] [ɪ'kɑlədʒi] ['mɑdl]种群生态模型public financing['pʌblɪk] [fɪ'nænsɪŋ]公共融资Q 4quality ['kwɑləti]质量quality circle ['kwɑləti] ['sɝkl] 质量圈question mark ['kwɛstʃən] [mɑːk] 问题类市场quid pro quo ['kwidprəu'kwəu] 交换物; 补偿物;相等物;交换条件;让步条件R 11rational approach ['ræʃnəl] [ə'protʃ] 理性方法rational model ['ræʃnəl] ['mɑdl] 理性模型rational-legal authority ['ræʃnəl] ['ligl] [ə'θɔrəti]理性—合法权威rational model of decision making ['ræʃnəl] ['mɑdl] [əv] [dɪ'sɪʒn] ['mek ɪŋ]理性决策模式realistic job preview(RJP) [,riə'lɪstɪk] [dʒɒb] ['pri'vjʊ]实际工作预览; 述评;reciprocal interdependence [rɪ'sɪprəkl] [,ɪntɚdɪ'pɛndəns] 相互依存性resource dependence ['risɔrs] [dɪ'pɛndəns] 资源依赖理论retention [rɪ'tɛnʃən] 保留reward system[rɪ'wɔrd] ['sɪstəm]薪酬体系routine technology [rʊ'tin] [tɛk'nɑlədʒi] 例行技术rules [rulz] 规则;条例S 39semivariable cost [,sɛmaɪ'vɛərɪəbl] [kɔst] 准可变成本sense of potency [sɛns] [əv] ['potnsi]力量感sensitivity training ['sɛnsə'tɪvəti] ['trenɪŋ]敏感性训练sexual harassment ['sɛʃʊəl] [hə'ræsmənt] 性骚扰short-run capacity changes ['ʃɔ:t'rʌn] [kə'pæsəti] [tʃendʒ] 短期生产能力变化single-strand chain ['sɪŋɡl] [strænd] [tʃen] 单向传言链situational approach [sɪtʃʊ'eʃənəl] [ə'protʃ] 情境方法situational force [sɪtʃʊ'eʃənəl] [fɔrs] 情境力量; 情境压力situational leadership theory [sɪtʃʊ'eʃənəl] ['lidɚʃɪp] ['θiəri] 情境领导理论sliding-scale budget ['slaɪdɪŋ] [skel] ['bʌdʒɪt] 移动规模预算small-batch production [smɔl] [bætʃ] [prə'dʌkʃən] 小规模生产sociotechnical approaches ['soʃiə 'tɛknɪkl] [ə'protʃiz]社会科技方法span of management [spæn] [əv] ['mænɪdʒmənt]管理幅度staff authority [stæf] [ə'θɔrəti] 参谋职权; 辅助权限standing plan ['stændɪŋ] [plæn]长设计划step budget [stɛp] ['bʌdʒɪt] 分步预算stewardship principle ['stuɚdʃɪp] ['prɪnsəpl] 管家原则stimulus ['stɪmjələs] 刺激storming ['stɔrmɪŋ] 激荡期;调整阶段strategic acquisitions[strə'tidʒɪk] [,ækwɪ'zɪʃən]战略并购strategic human resources[strə'tidʒɪk] ['hjumən] [ri'zɔ:siz]战略人力资源strategic maketing [strə'tidʒɪk] ['mɑrkɪtɪŋ]战略市场营销strategic management [strə'tidʒɪk] ['mænɪdʒmənt] 战略管理strategic partnering [strə'tidʒɪk] ['pɑrtnɚɪŋ]战略伙伴关系strategy formulation ['strætədʒi] [,fɔrmjə'leʃən] 战略制定strategy implementation ['strætədʒi] [,ɪmpləmɛn'teʃən] 战略实施strategic control [strə'tidʒɪk] [kən'trol] 战略控制strategic contingencies [strə'tidʒɪk] [kən'tɪndʒənsiz] 战略权变satisficing ['sætisfaisiŋ] 满意;满意法;满意度subsystems [sʌb 'sɪstəmz]子系统subunits [sʌb'junɪt] 子单位synergy ['sɪnɚdʒi]协同system boundary ['sɪstəm] ['baʊndri]系统边界structure dimension ['strʌktʃɚ] [daɪ'mɛnʃən] 结构性维度sequential interdependence [sɪ'kwɛnʃl] [,ɪntɚdɪ'pɛndəns]序列性依存; 相互依存self-directed team[,self di'rektid] [tim]自我管理型团队specialist ['spɛʃəlɪst] 专家;专门战略strategy and structure changes ['strætədʒi] [ənd] ['strʌktʃɚ] [tʃendʒz]战略与结构变革symptoms of structural deficiency ['sɪmptəm] [əv] ['strʌktʃərəl] [dɪ'f ɪʃənsi]结构无效的特征T 17tall hierarchies [tɔl] ['haɪə,rɑrki] 高长型科层结构task force or project team [tæsk] [fɔrs] [əv] ['prɒdʒekt] [tim] 任务小组或项目团队task independence [tæsk] [,ɪndɪ'pɛndəns]任务的内部依赖性task management [tæsk]['mænɪdʒmənt] 任务型管理task-oriented style [tæsk] ['orɪɛntɪd] [staɪl] 任务导向型管理风格team process [tim] ['prɑsɛs] 团队进程;团队合作total productivity ['totl] [,prodʌk'tɪvəti] 总生产率total quality management ['totl] ['kwɑləti] ['mænɪdʒmənt]全面质量管理trade agreement [treid] [ə'grimənt] 贸易协定;雇用合同;劳资协议training positions ['trenɪŋ] [pə'zɪʃənz]挂职培训training program ['trenɪŋ] ['proɡræm]培训程序transactional leaders [trænz'ækʃənl] ['lidɚz]交易型领导transformational leaders [,trænzfə'meʃənəl] ['lidɚz]变革型领导treatment discrimination ['tritmənt] [dɪ,skrɪmɪ'neʃən] 歧视待遇two-factory theory [tu] ['fæktri]['θiəri] 双因素理论two-boss employees [tu] [bɔs] [,ɛmplɔɪ'iz]双重主管员工technical or product champion ['tɛknɪkl] [ɔr] ['prɑdʌkt] ['tʃæmpɪən] 技术或产品的倡导者U 2unfreezing [ʌn'friz] 解冻unit production ['junɪt] [prə'dʌkʃən]单位产品V 11variation [,vɛrɪ'eʃən]变化;[生物] 变异,变种variety [və'raɪəti]变量valence ['veləns] 效价variable costs ['vɛrɪəbl] [kɔsts] 可变成本vertical communication ['vɝtɪkl] [kə,mjunɪ'keʃən] 纵向沟通vertical integration ['vɝtɪkl] ['ɪntə'greʃən] 纵向一体化vestibule training ['vɛstɪbjul] ['trenɪŋ] 仿真培训volume flexibility ['vɑljum] [,flɛksə'bɪləti] 产量的可伸缩性vertical linkage ['vɝtɪkl] ['lɪŋkɪdʒ]纵向连接venture team ['vɛntʃɚ] [tim] 风险团队value based leadership ['vælju] [best] ['lidɚʃɪp] 基于价值的领导W 7win-lose situation [wɪn] [luz] [,sɪtʃu'eʃən] 输赢情境win-win situation ['wɪn'wɪn] [,sɪtʃu'eʃən] 双赢情境workforce literacy ['wɝkfɔrs] ['lɪtərəsi]员工的读写能力work in progress [wɝk] [ɪn] ['prɑɡrɛs]在制品work flow redesign [wɝk] [flo] [,ridɪ'zaɪn] 工作流程再造成work flow automation [wɝk] [flo] [,ɔtə'meʃən]工作流程自动化whistle blowing ['wɪsl] ['bloɪŋ]揭发;举报Z 2zero-sum ['ziro'sʌm]零和;零和博弈zone of indifference(area of acceptance) [zon] [əv] [ɪn'dɪfrəns](['ɛr ɪə] [əv] [ək'sɛptəns])无差异区域(可接受区域)。

工商管理专业外文翻译--企业公民的阶段

外文原文Stages of Corporate CitizenshipBusiness leaders throughout the world are making corporate citizenship a key priority for their companies.1 Some are updating policies and revising programs; others are forming citizenship steering committees, measuring their environmental and social performance, and issuing public reports. Select firms are striving to align staff functions responsible for citizenship and move responsibility—and accountability—into lines of business. Vanguard companies are trying to create a broader market for citizenship and offer products and services that aim explicitly to both make money and make a better world.Amid the flurry of activity, many executives wonder what’s going on and worry whether or not their myriad citizenship initiatives make sense. Is their company prepared to take appropriate and effective actions on transparency, governance, community economic development, work-family balance, environmental sustainability, human rights protection, and ethical investor relationships?Is there any connection between, say, efforts in risk management, corporate branding, stakeholder engagement, supplier certification, cause related marketing, and employee diversity? Should there be? Studies conducted by the Center for Corporate Citizenship at Boston College suggest that the balance between confusion and coherence depends very much on what stage a company is in its development of corporate citizenship.Comparative neophytes, for instance, often lack understanding of these many aspects of corporate citizenship and have neither the expertise nor the machinery to respond to so many diverse interests and demands. Their chief challenges are to put citizenship firmly on the corporate agenda, get better informed about stakeholders’ concerns, and take some sensible initial steps.At the other extreme are companies that have already made a full-blown foray into citizenship. Their CEO is typically leading the firm’s position on social and environmental issues, and their Board is fully informed about company practices. Should these firms want to move forward, they might next try to connect citizenship to corporate branding and everyday employees through a “live the brand” campaign like those at IBM and Novo Nordisk or establish citizenship objectives for line managers, as DuPont and UBS have done.When it comes to making sense of corporate citizenship, much depends on what acompany has accomplished to date and how far it wants (and has to) go. The Center’s surveys of a random sample of American businesses find that roughly ten percent of company leaders don’t understand what corporate citizenship is all about. On the other end of the spectrum, not quite as many firms have integrated programs and are setting new standards of performance. In the vast majority in between, there is a wide range of companies in transition whose knowledge, attitudes, structures, and practices represent different degrees of understanding of and sophistication about corporate citizenship.Knowing at what stage a company is, and what challenges it faces in advancing citizenship, can clear up an executive’s confusion about where things stand, frame strategic choices about where to go, aid in setting benchmarks and goals, and perhaps speed movement forward.Stages of DevelopmentWhat does it mean that a company is at a “stage” of corporate citizenship?The general idea—found in the study of children, groups, and systems of all types, including business organizations—is that there are distinct patterns of activity at different points of development. Typically, these activities become more complex and sophisticated as development progresses and therefore capacities to respond to environmental challenges increase in kind. Piaget’s developmental theory, for example, has children progress through stages that entail more complex thinking and finer judgments about how to negotiate the social world outside of themselves. Similarly, groups mature along a developmental path as they confront emotional and task challenges that require more socially sensitive interaction and sophisticated problem solving.Greiner, in his groundbreaking study of organizational growth, found that companies also develop more complex ways of doing things at different stages of growth. They must, over time, find more direction after their creative start-up phase, develop an infrastructure and systems to take on more responsibilities, and then “work through” the challenges of over-control and red-tape through coordination and later collaboration across work units and levels.Development of CitizenshipThere are a number of models of “stages” of corporate citizenship. On a macro scale, for example, scholars have tracked changing conceptions of the role of business in society as advanced by business leaders, governments, academics, and multi-sectorassociations. They document how increasingly elaborate and inclusive definitions of social responsibility, environmental protection, and corporate ethics and governance have developed over recent decades that enlarge the role of business in society. Others have looked into the spread of these ideas into industry and society in the form of social and professional movements.At the level of the firm, Post and Altman have shown how environmental policies progressively broaden and deepen as companies encounter more demanding expectations and build their capability to meet them. In turn, Zadek’s case study of Nike’s response to challenges in its supply chain highlights stages in the development of attitudes about social responsibilities in companies and in corporate responsiveness to social issues. Both of these studies emphasize the role of organizational learning as conceptions of company responsibilities become more complex at successive stages of development, action requirements are more demanding, and the organizational structures, processes, and systems used to manage citizenship are more elaborate and comprehensive.What such firm-level frameworks have not fully addressed are the generative logic and mechanisms that drive the development of citizenship within organizations. Here we consider the development of citizenship as a stage-by-stage process where a combination of internal capabilities applied to environmental challenges propels development forward in a m ore or less “normal” or normative logic.Greiner’s model of organizational growth illustrates this normative trajectory. In his terms, the development of an organization is punctuated by a series of predictable crises that trigger responses that move the organization forward. What are the triggering mechanisms? They are tensions between current practices and the problems they produce that demand a new response from a firm. For instance, creativity, the entrepreneurial fire in companies in their first stage, also generates confusion and a loss of focus that can stall growth. This poses a “crisis of leadership” that is resolved—and a stage of orderly growth results—once the firm gains direction, often under new leadership and with more formal structures. A later tension between delegation and its consequences, sub-optimization and inter-group conflict, triggers a “crisis of control” and moves toward coordination. In development language, companies in effect “master” these challenges by devising progressively more effective and elaborate responses to them.The model presented here is also normative in that it posits a series of stages in thedevelopment of corporate citizenship. The triggers for movement are challenges that call for a fresh response. These challenges center initially on a firm’s credibility as a corporate citizen, then its capacities to meet expectations, the coherence of its many subsequent efforts, and, finally, its commitment to institutionalize citizenship in its business strategies and culture.Movement along a single development path is not fixed nor is attaining a penultimate “end state” a logical conclusion. This means that the arc of citizenship within any particular firm is shaped by the socio-economic, environmental, and institutional forces impinging on the enterprise. This effect is well documented by Vogel’s analysis of the “market for virtue” where he finds considerable variability in the business case for citizenship across firms and industries and thus limits to its marketp lace rewards. Notwithstanding, a company’s response to these market forces also varies based on the attitudes and outlooks of its leaders, the design and management of its citizenship agenda, and firmspecific learning. Thus, there are “companies with a conscience” that have a more expansive citizenship profile and firms that create a market for their good works.Dimensions of CitizenshipTo track the developmental path of citizenship in companies, we focus on seven dimensions of citizenship that vary at each stage:Citizenship Concept: How is citizenship defined? How comprehensive is it? Definitions of corporate citizenship are many and varied. The Center’s concept of citizenship considers the total actions of a corporation (commercial and philanthropic). Bettignies makes the point that terms such as citizenship and sustainability incorporate notions of ethics, philanthropy, stakeholder management, and social and environmental responsibilities into an integrative framework that guides corporate action.Strategic Intent: What is the purpose of citizenship in a company? What it is trying to achieve through citizenship? Smith observes that few companies embrace a strictly moral commitment to citizenship; instead most consider specific reputational risks and benefits in the market and society and thereby establish a business case for their efforts. Rochlin and Googins, in turn,see increasing interest in an “inside-out” framing where a value proposition for citizenship guides actions and investments. Leadership: Do top leaders support citizenship? Do they lead the effort? Visible, active, top level leadership appears on every survey as the number one factor drivingcitizenship in a corporation. How well informed are top leaders are about citizenship, how much leadership do they exercise, and to what extent do they “walk the talk”? Structure: How are responsibilities for citizenship managed? A three-year indepth study of eight companies in the Center’s Executive Forum on Corporate Citizenship found that many progressed from managing citizenship from functional “islands” to cross-functional committees and that a few had begun to achieve more formal integration through a combination of structures, processes, and systems.Issues Management: How does a company deal with citizenship issues that arise? Scholars have mapped the evolution of the public affairs office in corporations and stages in the management of public issues. How responsive a company is in terms of citizenship policies, programs, and performance?Stakeholder Relationships: How does a company engage its stakeholders? A wide range of trends—from increased social activism by shareholders to an increase in the number of non-governmental organizations (NGOs) around the world—has driven major changes in the ways companies communicate with and engage their stakeholders.Transparency: How “open” is a company about its financial, social, and environmental performance? The web sites of upwards of 80% of Fortune 500 companies address social and environmental issues and roughly half of the companies today issue a public report on their activities.Citizenship at Each StageThe model in Figure 1 presents the stages in the development of corporate citizenship along these seven dimensions. We illustrate each stage with selected examples of corporate practice. (Note, however, that we are not implying that these companies currently operate at that stage; rather, at the times noted, they were illustrative of citizenship at that development stage.) A close inspection of these companies reveals instances where they had a leading-edge practice in some dimensions but were less developed in others. This should come as no surprise. For example, the pace of a child’s physical, mental, and emotional development is seldom uniform. One facet typically develops faster than another. In the same way, the development of group and organizational capabilities is uneven. Firm-specific forces in society, industry dynamics, and other environmental influences feature in how citizenship develops within a firm.Stage 1. ElementaryAt this base stage, citizenship activity in a company is episodic and its programs are undeveloped. The reasons are straightforward: scant awareness of what corporate citizenship is all about, uninterested or indifferent top management, and limited or one-way interactions with external stakeholders, particularly in the social and environmental sectors. The mindset in these companies, and associated policies and practices, often centers on simple compliance with laws and industry standards.Responsibilities for handling matters of compliance in these firms are usually assigned to the functional heads of human resources, the legal department, investor relations, public relations, and community affairs. The job of these functional managers is to make sure that the company obeys the law and to keep problems that might arise from harming the firm’s reputation. In many cases, they take a defensive stance toward outside pressures—e.g., Nike’s dealings with labor activists in the early 1990s.Some corporate leaders, for example, have espoused economist Milton Friedman’s notion that their company’s obligations to society are solely to“make a profit, pay taxes, and provide jobs.”20 Others, particularly those heading smaller and mid-size businesses, comply willingly with employment and health, safety, and environmental regulations but have neither the resources nor the wherewithal to do much more for their employees, communities, or society.Former General Electric CEO Jack Welch is an exemplar of this principled big-business view. “A CEO’s primary social responsibility is to assure the financial success of the company,” he says. “Only a healthy, winning company has the resources and capability to do the right thing.”21GE’s financial success over the past two decades is unquestioned. However, the company’s reputation suffered toward the end of Welch’s tenure when it was revealed that that one of its business units had discharged tons of the toxic chemical PCB into the Hudson River. When challenged, Welch was defensive and pointed out that GE had fully complied with then existing environmental protection laws.This illustrates one of the triggers that move a company forward into a new stage of citizenship. Welch’s sta nce was plainly out of touch with changing expectations of corporate responsibilities and the contradiction between GE’s success at wealth creation and loss of reputation was palpable. Welch’s successor,Jeffrey Immelt, reversed this course, accepted at least partial financial responsibility for the clean up, and thereafter reprioritized citizenship on the company’s agenda.中文译文企业公民的阶段全世界的商界领袖都认为企业公民是他们公司的一个优先环节。

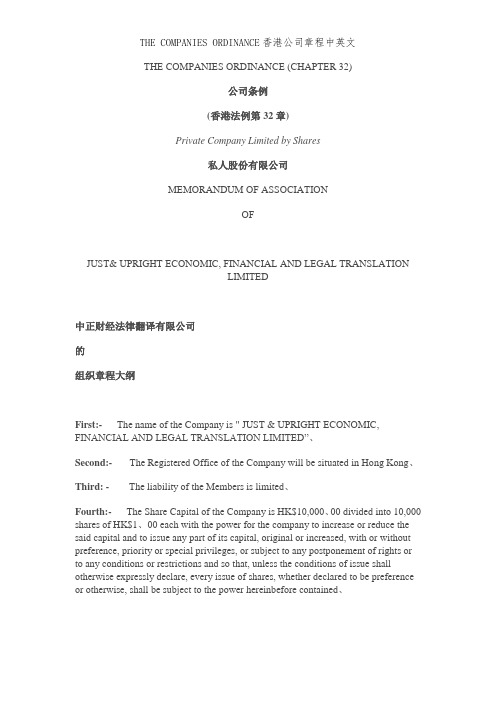

THE COMPANIES ORDINANCE香港公司章程中英文

THE COMPANIES ORDINANCE (CHAPTER 32)公司条例(香港法例第32章)Private Company Limited by Shares私人股份有限公司MEMORANDUM OF ASSOCIATIONOFJUST& UPRIGHT ECONOMIC, FINANCIAL AND LEGAL TRANSLATIONLIMITED中正财经法律翻译有限公司的组织章程大纲First:- The name of the Company is " JUST & UPRIGHT ECONOMIC, FINANCIAL AND LEGAL TRANSLATION LIMITED”、Second:- The Registered Office of the Company will be situated in Hong Kong、Third: -The liability of the Members is limited、Fourth:- The Share Capital of the Company is HK$10,000、00 divided into 10,000 shares of HK$1、00 each with the power for the company to increase or reduce the said capital and to issue any part of its capital, original or increased, with or without preference, priority or special privileges, or subject to any postponement of rights or to any conditions or restrictions and so that, unless the conditions of issue shall otherwise expressly declare, every issue of shares, whether declared to be preference or otherwise, shall be subject to the power hereinbefore contained、第一:公司名称为“中正财经法律翻译有限公司”。

公司理财(罗斯)第1章(英文

03 Valuation Basis

The concept and significance of valuation

要点一

Definition

Valuation is the process of estimating the worth of an asset or a company, typically through the use of financial metrics and analysis.

The Time Value of Money

ACCA P1 第一部分 scope of corporate governance 背书笔记