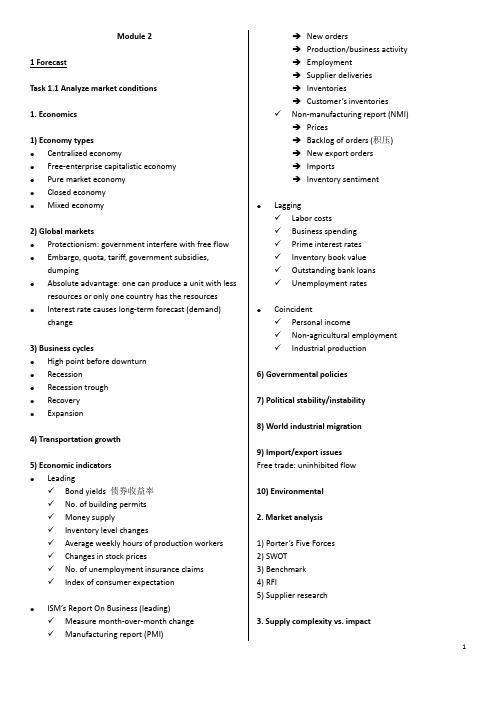

Study notes for Income tax_Ch. 19_part 1_SV

财务报表英文翻译

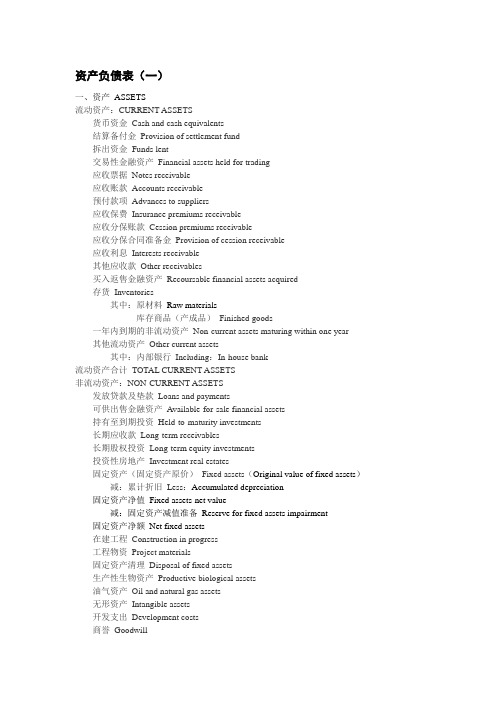

资产负债表(一)一、资产ASSETS流动资产:CURRENT ASSETS货币资金Cash and cash equivalents结算备付金Provision of settlement fund拆出资金Funds lent交易性金融资产Financial assets held for trading应收票据Notes receivable应收账款Accounts receivable预付款项Advances to suppliers应收保费Insurance premiums receivable应收分保账款Cession premiums receivable应收分保合同准备金Provision of cession receivable应收利息Interests receivable其他应收款Other receivables买入返售金融资产Recoursable financial assets acquired存货Inventories其中:原材料Raw materials库存商品(产成品)Finished goods一年内到期的非流动资产Non-current assets maturing within one year其他流动资产Other current assets其中:内部银行Including:In-house bank流动资产合计TOTAL CURRENT ASSETS非流动资产:NON-CURRENT ASSETS发放贷款及垫款Loans and payments可供出售金融资产Available-for-sale financial assets持有至到期投资Held-to-maturity investments长期应收款Long-term receivables长期股权投资Long-term equity investments投资性房地产Investment real estates固定资产(固定资产原价)Fixed assets(Original value of fixed assets)减:累计折旧Less:Accumulated depreciation固定资产净值Fixed assets-net value减:固定资产减值准备Reserve for fixed assets impairment 固定资产净额Net fixed assets在建工程Construction in progress工程物资Project materials固定资产清理Disposal of fixed assets生产性生物资产Productive biological assets油气资产Oil and natural gas assets无形资产Intangible assets开发支出Development costs商誉Goodwill长期待摊费用Long-term deferred expenses递延所得税资产Deferred income tax assets其他非流动资产Other non-current assets其中:特准储备物资Including:Physical assets reserve specifically authorized非流动资产合计TOTAL NON-CURRENT ASSETS资产总计TOTAL ASSETS二、负债LIABILITIES流动负债:CURRENT LIABILITIES短期借款Short-term borrowings向中央银行借款Borrowings from central bank吸收存款及同业存放Deposits from customers and interbank拆入资金Deposit funds交易性金融负债Financial assets held for liabilities应付票据Notes payable应付账款Accounts payable预收款项Payments received in advance卖出回购金融资产款Funds from sales of financial assets with repurchasement agreement 应付手续费及佣金Handling charges and commissions payable应付职工薪酬Employee benefits payable其中:应付工资Including:Wages payable应付福利费Welfare payable其中:职工奖励及福利基Including:Bonus and welfare fund for staff and workers应交税费Taxes and surcharges payable其中:应交税金Including:Taxes payable应付利息Interests payable应付股利Dividends payable其他应付款Other payables应付分保账款Cession insurance premiums payable保险合同准备金Provision for insurance contracts代理买卖证券款Funds received as agent of stock exchange代理承销证券款Funds received as stock underwrite一年内到期的非流动负债Non-current liabilities maturing within one year其他流动负债Other current liabilities其中:内部银行Including:In-house bank流动负债合计TOTAL CURRENT LIABILITIES非流动负债:NON-CURRENT LIABILITIES长期借款Long-term borrowings应付债券Debt securities issued长期应付款Long-term payables专项应付款Specific item payable预计负债Estimated Liabilities递延所得税负债Deferred tax liabilities其他非流动负债Other non-current liabilities其中:特准储备基金Including:Authorized reserve fund非流动负债合计TOTAL NON-CURRENT LIABILITIES负债合计TOTAL LIABILITIES三、所有者权益(或股东权益):OWNERS' EQUITY(or shareholders' equity)实收资本(或股本)Paid-up capital(or share capital)国家资本National capital集体资本Collective capital法人资本Legal person’s capital其中:国有法人资本State-owned legal person's capital集体法人资本Collective legal person's capital个人资本Personal capital外商资本Foreign capital减:已归还投资Less:Investment returned实收资本净额Net paid-up capital资本公积Capital reserves减:库存股Treasury stock专项储备Special reserves盈余公积Surplus reserves其中:法定公积金Statutory surplus reserve任意公积金Other surplus reserve储备基金Reserve fund企业发展基金Enterprise expansion fund利润归还投资Profits capitalized on return of investment一般风险准备Provision for normal risks未分配利润Retained earnings/Undistributed profits外币报表折算差额Exchange differences on translating foreign operations归属于母公司所有者权益合计Total equity attributable to the shareholders of parent companyTotal equity attributable to the shareholders of parent company少数股东权益Minority shareholders' equity (B/S)所有者权益合计TOTAL OWNERS' EQUITY负债和所有者权益总计TOTAL LIABILITIES AND OWNERS' EQUITY资产负债表(二)一、资产ASSETS流动资产: CURRENT ASSETS货币资金Cash and cash equivalents交易性金融资产Financial assets held for trading应收票据Notes receivable应收账款Accounts receivable减:坏帐准备Less:Provision for bad debts预付款项Advances to suppliers应收股利Dividends receivable其他应收款Other receivables存货Inventories其中:原材料Including:Raw materials库存成品及商品Inventory of finished goods低值易耗品Consumbles一年内到期的非流动资产Non-current assets maturing/due within one year 其他流动资产Other current assets流动资产合计TOTAL CURRENT ASSETS非流动资产:NON-CURRENT ASSETS可供出售金融资产Available-for-sale financial assets持有至到期投资Held-to-maturity investments长期应收款Long-term receivables长期股权投资long-term equity investments投资性房地产Investment real estate固定资产(固定资产原价)Fixed assets(Original value of fixed assets)减:累计折旧Less:Accumulated depreciation固定资产净值Fixed assets-net value减:固定资产减值准备Reserve for fixed assets impairment 固定资产净额Net fixed assets在建工程Construction in progress工程物资Project materials固定资产清理Disposal of fixed assets生产性生物资产Productive biological assets油气资产Oil and natural gas assets无形资产Intangible assets开发支出Development costs商誉Goodwill长期待摊费用Long-term deferred expenses递延所得税资产Deferred income tax assets其他非流动资产Other non-current assets非流动资产合计TOTAL NON-CURRENT ASSETS资产总计TOTAL ASSETS二、负债LIABILITIES流动负债:CURRENT LIABILITIES短期借款Short-term borrowings交易性金融负债Financial assets held for liabilities应付票据Notes payable应付账款Accounts payable预收款项Payments received in advance应付职工薪酬Employee benefits payable/Staff remuneration payables应交税费Taxes and surcharges payable应付股利Dividends payable其他应付款Other payables一年内到期的非流动负债Non-current liabilities maturing within one year其他流动负债Other current liabilities流动负债合计TOTAL CURRENT LIABILITIES非流动负债:NON-CURRENT LIABILITIES长期借款Long-term borrowings应付债券Debt securities issued长期应付款Long-term payables专项应付款Specific item payable预计负债Provisions for liabilities递延所得税负债Deferred income tax liabilities其他非流动负债Other non-current liabilities非流动负债合计TOTAL NON-CURRENT LIABILITIES负债合计TOTAL LIABILITIES三、所有者权益(或股东权益):OWNERS' EQUITY (or shareholders' equity)实收资本(或股本)Paid-up capital (or share capital)其中:国家资本National capital集体资本Collateral capital法人资本Legal person's capital个人资本Personal capital外商资本Foreign capital资本公积Capital reserves减:库存股Treasury stock盈余公积Surplus reserves未分配利润Retained earnings/Undistributed profit所有者权益(或股东权益)合计TOTAL OWNERS' EQUITY (OR SHAREHOLDERS' EQUITY)负债和所有者权益(或股东权益)总计TOTAL LIABILITIES AND OWNERS' EQUITY利润表一、营业总收入Overall sales/Overall income其中:营业收入Including: Sales/Income from operations/Income from operations 其中:主营业务收入Sales/Income from main business/Income from main business 其他业务收入Sales/Income from other business/Income from other business 利息收入Interests income已赚保费Insurance premiums earned手续费及佣金收入Handling charges and commissions income二、营业总成本Overall costs其中:营业成本Including: Costs of operations其中:主营业务成本Costs of main business其他业务成本Costs of other business利息支出Interests expenses手续费及佣金支出Handling charges and commissions expenses退保金Refund of insurance premiums赔付支出净额Net payments for insurance claims提取保险合同准备金净额Net provision for insurance contracts保单红利支出Commissions on insurance policies分保费用Cession charges营业税金及附加Taxes and surcharges on operations销售费用Selling and distribution expenses管理费用General and administrative expenses其中:业务招待费Entertainment expenses/Business entertainment研究与开发费Research and development costs财务费用Financial expenses其中:利息支出Interests expenses利息收入Interests income汇兑净损失Foreign exchange net loss资产减值损失Impairment loss on assets加:公允价值变动收益(损失以“-”号填列)Plus: Gain or loss from changes in fair values 投资收益(损失以“-”号填列)Investment income其中:对联营企业和合营企业的投资收益Including: Investment income from joint ventures and affiliates汇兑收益(损失以“-”号填列)Gain or loss on foreign exchange transactions三、营业利润(亏损以“-”号填列)Profit from operations加:营业外收入Plus: Non-operating profit其中:非流动资产处置利得Gain from disposal of non-current assets非货币性资产交换利得Gain from exchange of non-monetary assets政府补助Governmental subsidy债务重组利得Gain of debt restructuring减:营业外支出Less: Non-operating expenses其中:非流动资产处置损失Loss from disposal of non-current assets非货币性资产交换损失Loss from exchange of non-monetary assets债务重组损失Loss of debt restructuring四、利润总额(亏损总额以“-”号填列)Profit before tax加:应弥补亏损Loss to cover减:所得税费用Less: Income tax expenses五、净利润(净亏损以“-”号填列)Net profit其中:被合并方在合并前实现的净利润Among which: Net profit recognized before the merger归属于母公司所有者的净利润Net profit attributable to shareholders of parent company 少数股东损益Minority interest income六、每股收益:Earnings per share (EPS)基本每股收益Basic EPS稀释每股收益Diluted EPS七、其他综合收益Other comprehensive income八、综合收益总额Total comprehensive income归属于母公司所有者的综合收益总额Total comprehensive income attributable to shareholders of parent company归属于少数股东的综合收益总额Total comprehensive income attributable to minority shareholders现金流量表(都要校对一下)一、经营活动产生的现金流量Cash flows from operating activities销售商品、提供劳务收到的现金Cash received from the sales of goods and the rendering of services客户存款和同业存放款项净增加额Net increase in deposits from customers and placements from corporations in the same industry向中央银行借款净增加额Net increase in loan from central bank向其他金融机构拆入资金净增加额Net increase in funds borrowed from other financial institutions收到原保险合同保费取得的现金Cash premiums received on original insurance contracts收到再保险业务现金净额Cash received from re-insurance business保户储金及投资款净增加额Net increase in deposits and investments from insurers处置交易性金融资产净增加额Net increase in disposal of trading financial assets收取利息、手续费及佣金的现金Interest, handling charges and commissions received拆入资金净增加额Net increase in funds deposit回购业务资金净增加额Net increase in repurchasement business funds收到的税费返还Receipts of tax refunds收到其他与经营活动有关的现金Other cash received relating to operating activities 其中:企业内部银行收到的现金Including: Cash received by in-house bank经营活动现金流入小计Sub-total of cash inflows from operating activities购买商品、接受劳务支付的现金Cash payments for goods purchased and services received客户贷款及垫款净增加额Net increase in loans and payments on behalf存放中央银行和同业款项净增加额Net increase in deposits with centre bank and interbank支付原保险合同赔付款项的现金Payments of claims for original insurance contracts支付利息、手续费及佣金的现金Interests, handling charges and commissions paid支付保单红利的现金Commissions on insurance policies paid支付给职工以及为职工支付的现金Cash payments to and on behalf of employees支付的各项税费Payments of all types of taxes支付其他与经营活动有关的现金Other cash payments relating to operating activities经营活动现金流出小计Sub-total of cash outflows from operating activities经营活动产生的现金流量净额Net cash flows from operating activities二、投资活动产生的现金流量:Cash flows from investing activities收回投资收到的现金Cash received from disposals and withdraw on investment取得投资收益收到的现金Cash received from returns on investments处置固定资产、无形资产和其他长期资产收回的现金净额Net cash received from disposals of fixed assets, intangible assets and other long-term assets处置子公司及其他营业单位收到的现金净额Net cash received from disposals of subsidiariesand other business units收到其他与投资活动有关的现金Other cash received relating to investing activities投资活动现金流入小计Sub-total of cash inflows from investing activities购建固定资产、无形资产和其他长期资产支付的现金Cash payments to acquire and construct fixed assets, intangible assets and other long-term assets投资支付的现金Cash payments to acquire investments质押贷款净增加额Net increase in secured loans取得子公司及其他营业单位支付的现金净额Net cash payments for acquisitions of subsidiaries and other business units支付的其他与投资活动有关的现金Other cash payments relating to investing activities投资活动现金流出小计Sub-total of cash outflows from investing activities投资活动产生的现金流量净额Net cash flows from investing activities三、筹资活动产生的现金流量Cash flows from financing activities吸收投资所收到的现金Cash received from investors in making investment in the enterprise其中:子公司吸收少数股东投资收到的现金Including:Cash received from issuing shares of minority shareholders取得借款所收到的现金Cash received from borrowings发行债券收到的现金Proceeds from issuance of bonds收到的其他与筹资活动有关的现金Other cash received relating to financing activities筹资活动现金流入小计Sub-total of cash outflows from financing activities偿还债务所支付的现金Cash repayments of amounts borrowed分配股利、利润或偿付利息所支付的现金Cash payments for distribution of dividends or profits, or cash payments for interest expenses其中:子公司支付给少数股东的股利、利润Including: Subsidiary companies pay cash to minority shareholders for interest expenses and distribution of dividends or profit支付的其他与筹资活动有关的现金Other cash payments relating to financing activities筹资活动现金流出小计Sub-total of cash outflows from financing activities筹资活动产生的现金流量净额Net cash flows from financing activities四、汇率变动对现金及现金等价物的影响Effect of foreign exchange rate changes on cash and cash equivalents五、现金及现金等价物净增加额Net increase in cash and cash equivalents加:期初现金及现金等价物余额Plus:Cash and cash equivalents at beginning of period六、期末现金及现金等价物余额Cash and cash equivalents at end of period本月实际Actual for this month去年同期The corresponding period of last year本年累计Accumulative total for this year 行次Line金额Amount项目Item。

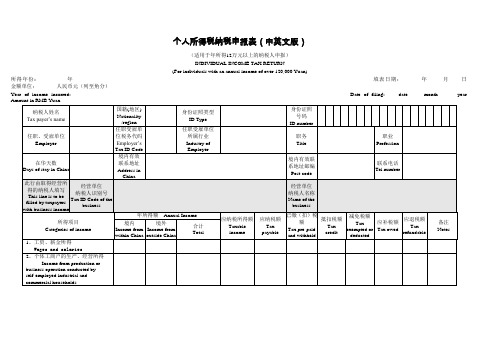

《个人所得税纳税申报表(中英文对照).》

个人所得税纳税申报表(中英文版)(适用于年所得12万元以上的纳税人申报)INDIVIDUAL INCOME TAX RETURN(For individuals with an annual income of over 120,000 Yuan)所得年份: 年填表日期:年月日金额单位:人民币元(列至角分)Year of income incurred: Date of filing: date month year Amount in RMB Yuan章):Signature of responsible tax officer : Filing date: Time: Year/Month/Date Responsible tax offic填表须知一、本表根据《中华人民共和国个人所得税法》及其实施条例和《个人所得税自行纳税申报办法(试行)》制定,适用于年所得12万元以上纳税人的年度自行申报。

二、负有纳税义务的个人,可以由本人或者委托他人于纳税年度终了后3个月以内向主管税务机关报送本表。

不能按照规定期限报送本表时,应当在规定的报送期限内提出申请,经当地税务机关批准,可以适当延期。

三、填写本表应当使用中文,也可以同时用中、外两种文字填写。

四、本表各栏的填写说明如下:(一)所得年份和填表日期:申报所得年份:填写纳税人实际取得所得的年度;填表日期,填写纳税人办理纳税申报的实际日期。

(二)身份证照类型:填写纳税人的有效身份证照(居民身份证、军人身份证件、护照、回乡证等)名称。

(三)身份证照号码:填写中国居民纳税人的有效身份证照上的号码。

(四)任职、受雇单位:填写纳税人的任职、受雇单位名称。

纳税人有多个任职、受雇单位时,填写受理申报的税务机关主管的任职、受雇单位。

(五)任职、受雇单位税务代码:填写受理申报的任职、受雇单位在税务机关办理税务登记或者扣缴登记的编码。

(六)任职、受雇单位所属行业:填写受理申报的任职、受雇单位所属的行业。

个人所得税英文参考文献

个人所得税英文参考文献个人所得税英语参考文献一:[1]José Félix Sanz-Sanz. The Laffer curve in schedular multi-rate income taxes with non-genuine allowances: An application to Spain[J]. Economic Modelling,2019,.[2]Craig Brett,John A. Weymark. Voting over selfishly optimal nonlinear income tax schedules[J]. Games and Economic Behavior,2019,.[3]Mónica Unda Gutiérrez. A Tale of Two Taxes: the Diverging Fates of the Federal Property and Income Tax Decrees in post-Revolutionary Mexico[J]. Investigaciones de Historia Económica - Economic History Research,2019,.[4]Sim Choon Ling,Abdullah Osman,Safizal Muhammad,Sin Kit Yeng,Lim Yi Jin. Goods and Services Tax (GST) Compliance among Malaysian Consumers: The Influence of Price, Government Subsidies and Income Inequality[J]. Procedia Economics and Finance,2019,35.[5]Martin Lopez-Daneri. NIT Picking: The Macroeconomic Effects of a Negative Income Tax[J]. Journal of Economic Dynamics and Control,2019,.[6]Tad Miller,Lindsay Miller,Jeffrey Tolin. Provision for income tax expense ASC 740: A teaching note[J]. Journal of Accounting Education,2019,35.[7]Petr David,Lucie Formanová。

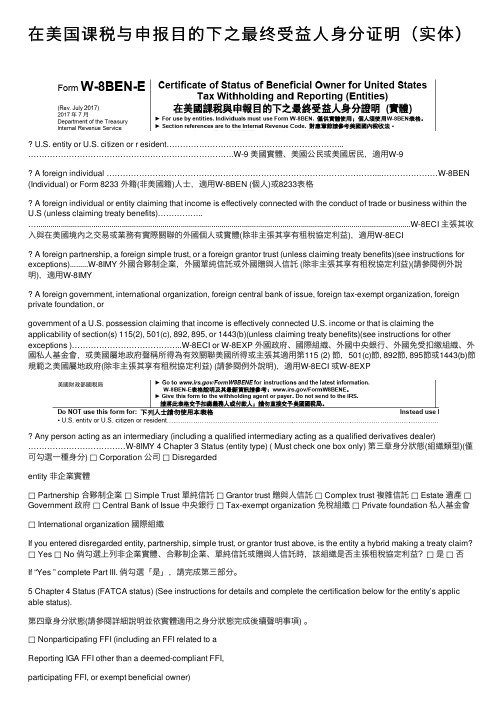

在美国课税与申报目的下之最终受益人身分证明(实体)

在美国课税与申报⽬的下之最终受益⼈⾝分证明(实体)U.S. entity or U.S. citizen or r esident………………………………………………………...………………………………………………………………….W-9 美國實體、美國公民或美國居民,適⽤W-9A foreign individual ………………………………………………………………………………………...…………………W-8BEN (Individual) or Form 8233 外籍(⾮美國籍)⼈⼠,適⽤W-8BEN (個⼈)或8233表格A foreign individual or entity claiming that income is effectively connected with the conduct of trade or business within the U.S (unless claiming treaty benefits)……………..…........................................................................................................................................................................................W-8ECI 主張其收⼊與在美國境內之交易或業務有實際關聯的外國個⼈或實體(除⾮主張其享有租稅協定利益),適⽤W-8ECIA foreign partnership, a foreign simple trust, or a foreign grantor trust (unless claiming treaty benefits)(see instructions for exceptions).........W-8IMY 外國合夥制企業,外國單純信託或外國贈與⼈信託 (除⾮主張其享有租稅協定利益)(請參閱例外說明),適⽤W-8IMYA foreign government, international organization, foreign central bank of issue, foreign tax-exempt organization, foreign private foundation, orgovernment of a U.S. possession claiming that income is effectively connected U.S. income or that is claiming the applicability of section(s) 115(2), 501(c), 892, 895, or 1443(b)(unless claiming treaty benefits)(see instructions for other exceptions )…………………………………..W-8ECI or W-8EXP 外國政府、國際組織、外國中央銀⾏、外國免受扣繳組織、外國私⼈基⾦會,或美國屬地政府聲稱所得為有效關聯美國所得或主張其適⽤第115 (2) 節,501(c)節, 892節, 895節或1443(b)節規範之美國屬地政府(除⾮主張其享有租稅協定利益) (請參閱例外說明),適⽤W-8ECI 或W-8EXPAny person acting as an intermediary (including a qualified intermediary acting as a qualified derivatives dealer)………………………………W-8IMY 4 Chapter 3 Status (entity type) ( Must check one box only) 第三章⾝分狀態(組織類型)(僅可勾選⼀種⾝分) □ Corporation 公司□ Disregardedentity ⾮企業實體□ Partnership 合夥制企業□ Simple Trust 單純信託□ Grantor trust 贈與⼈信託□ Complex trust 複雜信託□ Estate 遺產□Government 政府□ Central Bank of Issue 中央銀⾏□ Tax-exempt organization 免稅組織□ Private foundation 私⼈基⾦會□ International organization 國際組織If you entered disregarded entity, partnership, simple trust, or grantor trust above, is the entity a hybrid making a treaty claim?□ Yes □ No 倘勾選上列⾮企業實體、合夥制企業、單純信託或贈與⼈信託時,該組織是否主張租稅協定利益?□是□否If “Yes ” complete Part III. 倘勾選「是」,請完成第三部分。

OSHA现场作业手册说明书

DIRECTIVE NUMBER: CPL 02-00-150 EFFECTIVE DATE: April 22, 2011 SUBJECT: Field Operations Manual (FOM)ABSTRACTPurpose: This instruction cancels and replaces OSHA Instruction CPL 02-00-148,Field Operations Manual (FOM), issued November 9, 2009, whichreplaced the September 26, 1994 Instruction that implemented the FieldInspection Reference Manual (FIRM). The FOM is a revision of OSHA’senforcement policies and procedures manual that provides the field officesa reference document for identifying the responsibilities associated withthe majority of their inspection duties. This Instruction also cancels OSHAInstruction FAP 01-00-003 Federal Agency Safety and Health Programs,May 17, 1996 and Chapter 13 of OSHA Instruction CPL 02-00-045,Revised Field Operations Manual, June 15, 1989.Scope: OSHA-wide.References: Title 29 Code of Federal Regulations §1903.6, Advance Notice ofInspections; 29 Code of Federal Regulations §1903.14, Policy RegardingEmployee Rescue Activities; 29 Code of Federal Regulations §1903.19,Abatement Verification; 29 Code of Federal Regulations §1904.39,Reporting Fatalities and Multiple Hospitalizations to OSHA; and Housingfor Agricultural Workers: Final Rule, Federal Register, March 4, 1980 (45FR 14180).Cancellations: OSHA Instruction CPL 02-00-148, Field Operations Manual, November9, 2009.OSHA Instruction FAP 01-00-003, Federal Agency Safety and HealthPrograms, May 17, 1996.Chapter 13 of OSHA Instruction CPL 02-00-045, Revised FieldOperations Manual, June 15, 1989.State Impact: Notice of Intent and Adoption required. See paragraph VI.Action Offices: National, Regional, and Area OfficesOriginating Office: Directorate of Enforcement Programs Contact: Directorate of Enforcement ProgramsOffice of General Industry Enforcement200 Constitution Avenue, NW, N3 119Washington, DC 20210202-693-1850By and Under the Authority ofDavid Michaels, PhD, MPHAssistant SecretaryExecutive SummaryThis instruction cancels and replaces OSHA Instruction CPL 02-00-148, Field Operations Manual (FOM), issued November 9, 2009. The one remaining part of the prior Field Operations Manual, the chapter on Disclosure, will be added at a later date. This Instruction also cancels OSHA Instruction FAP 01-00-003 Federal Agency Safety and Health Programs, May 17, 1996 and Chapter 13 of OSHA Instruction CPL 02-00-045, Revised Field Operations Manual, June 15, 1989. This Instruction constitutes OSHA’s general enforcement policies and procedures manual for use by the field offices in conducting inspections, issuing citations and proposing penalties.Significant Changes∙A new Table of Contents for the entire FOM is added.∙ A new References section for the entire FOM is added∙ A new Cancellations section for the entire FOM is added.∙Adds a Maritime Industry Sector to Section III of Chapter 10, Industry Sectors.∙Revises sections referring to the Enhanced Enforcement Program (EEP) replacing the information with the Severe Violator Enforcement Program (SVEP).∙Adds Chapter 13, Federal Agency Field Activities.∙Cancels OSHA Instruction FAP 01-00-003, Federal Agency Safety and Health Programs, May 17, 1996.DisclaimerThis manual is intended to provide instruction regarding some of the internal operations of the Occupational Safety and Health Administration (OSHA), and is solely for the benefit of the Government. No duties, rights, or benefits, substantive or procedural, are created or implied by this manual. The contents of this manual are not enforceable by any person or entity against the Department of Labor or the United States. Statements which reflect current Occupational Safety and Health Review Commission or court precedents do not necessarily indicate acquiescence with those precedents.Table of ContentsCHAPTER 1INTRODUCTIONI.PURPOSE. ........................................................................................................... 1-1 II.SCOPE. ................................................................................................................ 1-1 III.REFERENCES .................................................................................................... 1-1 IV.CANCELLATIONS............................................................................................. 1-8 V. ACTION INFORMATION ................................................................................. 1-8A.R ESPONSIBLE O FFICE.......................................................................................................................................... 1-8B.A CTION O FFICES. .................................................................................................................... 1-8C. I NFORMATION O FFICES............................................................................................................ 1-8 VI. STATE IMPACT. ................................................................................................ 1-8 VII.SIGNIFICANT CHANGES. ............................................................................... 1-9 VIII.BACKGROUND. ................................................................................................. 1-9 IX. DEFINITIONS AND TERMINOLOGY. ........................................................ 1-10A.T HE A CT................................................................................................................................................................. 1-10B. C OMPLIANCE S AFETY AND H EALTH O FFICER (CSHO). ...........................................................1-10B.H E/S HE AND H IS/H ERS ..................................................................................................................................... 1-10C.P ROFESSIONAL J UDGMENT............................................................................................................................... 1-10E. W ORKPLACE AND W ORKSITE ......................................................................................................................... 1-10CHAPTER 2PROGRAM PLANNINGI.INTRODUCTION ............................................................................................... 2-1 II.AREA OFFICE RESPONSIBILITIES. .............................................................. 2-1A.P ROVIDING A SSISTANCE TO S MALL E MPLOYERS. ...................................................................................... 2-1B.A REA O FFICE O UTREACH P ROGRAM. ............................................................................................................. 2-1C. R ESPONDING TO R EQUESTS FOR A SSISTANCE. ............................................................................................ 2-2 III. OSHA COOPERATIVE PROGRAMS OVERVIEW. ...................................... 2-2A.V OLUNTARY P ROTECTION P ROGRAM (VPP). ........................................................................... 2-2B.O NSITE C ONSULTATION P ROGRAM. ................................................................................................................ 2-2C.S TRATEGIC P ARTNERSHIPS................................................................................................................................. 2-3D.A LLIANCE P ROGRAM ........................................................................................................................................... 2-3 IV. ENFORCEMENT PROGRAM SCHEDULING. ................................................ 2-4A.G ENERAL ................................................................................................................................................................. 2-4B.I NSPECTION P RIORITY C RITERIA. ..................................................................................................................... 2-4C.E FFECT OF C ONTEST ............................................................................................................................................ 2-5D.E NFORCEMENT E XEMPTIONS AND L IMITATIONS. ....................................................................................... 2-6E.P REEMPTION BY A NOTHER F EDERAL A GENCY ........................................................................................... 2-6F.U NITED S TATES P OSTAL S ERVICE. .................................................................................................................. 2-7G.H OME-B ASED W ORKSITES. ................................................................................................................................ 2-8H.I NSPECTION/I NVESTIGATION T YPES. ............................................................................................................... 2-8 V.UNPROGRAMMED ACTIVITY – HAZARD EVALUATION AND INSPECTION SCHEDULING ............................................................................ 2-9 VI.PROGRAMMED INSPECTIONS. ................................................................... 2-10A.S ITE-S PECIFIC T ARGETING (SST) P ROGRAM. ............................................................................................. 2-10B.S CHEDULING FOR C ONSTRUCTION I NSPECTIONS. ..................................................................................... 2-10C.S CHEDULING FOR M ARITIME I NSPECTIONS. ............................................................................. 2-11D.S PECIAL E MPHASIS P ROGRAMS (SEP S). ................................................................................... 2-12E.N ATIONAL E MPHASIS P ROGRAMS (NEP S) ............................................................................... 2-13F.L OCAL E MPHASIS P ROGRAMS (LEP S) AND R EGIONAL E MPHASIS P ROGRAMS (REP S) ............ 2-13G.O THER S PECIAL P ROGRAMS. ............................................................................................................................ 2-13H.I NSPECTION S CHEDULING AND I NTERFACE WITH C OOPERATIVE P ROGRAM P ARTICIPANTS ....... 2-13CHAPTER 3INSPECTION PROCEDURESI.INSPECTION PREPARATION. .......................................................................... 3-1 II.INSPECTION PLANNING. .................................................................................. 3-1A.R EVIEW OF I NSPECTION H ISTORY .................................................................................................................... 3-1B.R EVIEW OF C OOPERATIVE P ROGRAM P ARTICIPATION .............................................................................. 3-1C.OSHA D ATA I NITIATIVE (ODI) D ATA R EVIEW .......................................................................................... 3-2D.S AFETY AND H EALTH I SSUES R ELATING TO CSHO S.................................................................. 3-2E.A DVANCE N OTICE. ................................................................................................................................................ 3-3F.P RE-I NSPECTION C OMPULSORY P ROCESS ...................................................................................................... 3-5G.P ERSONAL S ECURITY C LEARANCE. ................................................................................................................. 3-5H.E XPERT A SSISTANCE. ........................................................................................................................................... 3-5 III. INSPECTION SCOPE. ......................................................................................... 3-6A.C OMPREHENSIVE ................................................................................................................................................... 3-6B.P ARTIAL. ................................................................................................................................................................... 3-6 IV. CONDUCT OF INSPECTION .............................................................................. 3-6A.T IME OF I NSPECTION............................................................................................................................................. 3-6B.P RESENTING C REDENTIALS. ............................................................................................................................... 3-6C.R EFUSAL TO P ERMIT I NSPECTION AND I NTERFERENCE ............................................................................. 3-7D.E MPLOYEE P ARTICIPATION. ............................................................................................................................... 3-9E.R ELEASE FOR E NTRY ............................................................................................................................................ 3-9F.B ANKRUPT OR O UT OF B USINESS. .................................................................................................................... 3-9G.E MPLOYEE R ESPONSIBILITIES. ................................................................................................. 3-10H.S TRIKE OR L ABOR D ISPUTE ............................................................................................................................. 3-10I. V ARIANCES. .......................................................................................................................................................... 3-11 V. OPENING CONFERENCE. ................................................................................ 3-11A.G ENERAL ................................................................................................................................................................ 3-11B.R EVIEW OF A PPROPRIATION A CT E XEMPTIONS AND L IMITATION. ..................................................... 3-13C.R EVIEW S CREENING FOR P ROCESS S AFETY M ANAGEMENT (PSM) C OVERAGE............................. 3-13D.R EVIEW OF V OLUNTARY C OMPLIANCE P ROGRAMS. ................................................................................ 3-14E.D ISRUPTIVE C ONDUCT. ...................................................................................................................................... 3-15F.C LASSIFIED A REAS ............................................................................................................................................. 3-16VI. REVIEW OF RECORDS. ................................................................................... 3-16A.I NJURY AND I LLNESS R ECORDS...................................................................................................................... 3-16B.R ECORDING C RITERIA. ...................................................................................................................................... 3-18C. R ECORDKEEPING D EFICIENCIES. .................................................................................................................. 3-18 VII. WALKAROUND INSPECTION. ....................................................................... 3-19A.W ALKAROUND R EPRESENTATIVES ............................................................................................................... 3-19B.E VALUATION OF S AFETY AND H EALTH M ANAGEMENT S YSTEM. ....................................................... 3-20C.R ECORD A LL F ACTS P ERTINENT TO A V IOLATION. ................................................................................. 3-20D.T ESTIFYING IN H EARINGS ................................................................................................................................ 3-21E.T RADE S ECRETS. ................................................................................................................................................. 3-21F.C OLLECTING S AMPLES. ..................................................................................................................................... 3-22G.P HOTOGRAPHS AND V IDEOTAPES.................................................................................................................. 3-22H.V IOLATIONS OF O THER L AWS. ....................................................................................................................... 3-23I.I NTERVIEWS OF N ON-M ANAGERIAL E MPLOYEES .................................................................................... 3-23J.M ULTI-E MPLOYER W ORKSITES ..................................................................................................................... 3-27 K.A DMINISTRATIVE S UBPOENA.......................................................................................................................... 3-27 L.E MPLOYER A BATEMENT A SSISTANCE. ........................................................................................................ 3-27 VIII. CLOSING CONFERENCE. .............................................................................. 3-28A.P ARTICIPANTS. ..................................................................................................................................................... 3-28B.D ISCUSSION I TEMS. ............................................................................................................................................ 3-28C.A DVICE TO A TTENDEES .................................................................................................................................... 3-29D.P ENALTIES............................................................................................................................................................. 3-30E.F EASIBLE A DMINISTRATIVE, W ORK P RACTICE AND E NGINEERING C ONTROLS. ............................ 3-30F.R EDUCING E MPLOYEE E XPOSURE. ................................................................................................................ 3-32G.A BATEMENT V ERIFICATION. ........................................................................................................................... 3-32H.E MPLOYEE D ISCRIMINATION .......................................................................................................................... 3-33 IX. SPECIAL INSPECTION PROCEDURES. ...................................................... 3-33A.F OLLOW-UP AND M ONITORING I NSPECTIONS............................................................................................ 3-33B.C ONSTRUCTION I NSPECTIONS ......................................................................................................................... 3-34C. F EDERAL A GENCY I NSPECTIONS. ................................................................................................................. 3-35CHAPTER 4VIOLATIONSI. BASIS OF VIOLATIONS ..................................................................................... 4-1A.S TANDARDS AND R EGULATIONS. .................................................................................................................... 4-1B.E MPLOYEE E XPOSURE. ........................................................................................................................................ 4-3C.R EGULATORY R EQUIREMENTS. ........................................................................................................................ 4-6D.H AZARD C OMMUNICATION. .............................................................................................................................. 4-6E. E MPLOYER/E MPLOYEE R ESPONSIBILITIES ................................................................................................... 4-6 II. SERIOUS VIOLATIONS. .................................................................................... 4-8A.S ECTION 17(K). ......................................................................................................................... 4-8B.E STABLISHING S ERIOUS V IOLATIONS ............................................................................................................ 4-8C. F OUR S TEPS TO BE D OCUMENTED. ................................................................................................................... 4-8 III. GENERAL DUTY REQUIREMENTS ............................................................. 4-14A.E VALUATION OF G ENERAL D UTY R EQUIREMENTS ................................................................................. 4-14B.E LEMENTS OF A G ENERAL D UTY R EQUIREMENT V IOLATION.............................................................. 4-14C. U SE OF THE G ENERAL D UTY C LAUSE ........................................................................................................ 4-23D.L IMITATIONS OF U SE OF THE G ENERAL D UTY C LAUSE. ..............................................................E.C LASSIFICATION OF V IOLATIONS C ITED U NDER THE G ENERAL D UTY C LAUSE. ..................F. P ROCEDURES FOR I MPLEMENTATION OF S ECTION 5(A)(1) E NFORCEMENT ............................ 4-25 4-27 4-27IV.OTHER-THAN-SERIOUS VIOLATIONS ............................................... 4-28 V.WILLFUL VIOLATIONS. ......................................................................... 4-28A.I NTENTIONAL D ISREGARD V IOLATIONS. ..........................................................................................4-28B.P LAIN I NDIFFERENCE V IOLATIONS. ...................................................................................................4-29 VI. CRIMINAL/WILLFUL VIOLATIONS. ................................................... 4-30A.A REA D IRECTOR C OORDINATION ....................................................................................................... 4-31B.C RITERIA FOR I NVESTIGATING P OSSIBLE C RIMINAL/W ILLFUL V IOLATIONS ........................ 4-31C. W ILLFUL V IOLATIONS R ELATED TO A F ATALITY .......................................................................... 4-32 VII. REPEATED VIOLATIONS. ...................................................................... 4-32A.F EDERAL AND S TATE P LAN V IOLATIONS. ........................................................................................4-32B.I DENTICAL S TANDARDS. .......................................................................................................................4-32C.D IFFERENT S TANDARDS. .......................................................................................................................4-33D.O BTAINING I NSPECTION H ISTORY. .....................................................................................................4-33E.T IME L IMITATIONS..................................................................................................................................4-34F.R EPEATED V. F AILURE TO A BATE....................................................................................................... 4-34G. A REA D IRECTOR R ESPONSIBILITIES. .............................................................................. 4-35 VIII. DE MINIMIS CONDITIONS. ................................................................... 4-36A.C RITERIA ................................................................................................................................................... 4-36B.P ROFESSIONAL J UDGMENT. ..................................................................................................................4-37C. A REA D IRECTOR R ESPONSIBILITIES. .............................................................................. 4-37 IX. CITING IN THE ALTERNATIVE ............................................................ 4-37 X. COMBINING AND GROUPING VIOLATIONS. ................................... 4-37A.C OMBINING. ..............................................................................................................................................4-37B.G ROUPING. ................................................................................................................................................4-38C. W HEN N OT TO G ROUP OR C OMBINE. ................................................................................................4-38 XI. HEALTH STANDARD VIOLATIONS ....................................................... 4-39A.C ITATION OF V ENTILATION S TANDARDS ......................................................................................... 4-39B.V IOLATIONS OF THE N OISE S TANDARD. ...........................................................................................4-40 XII. VIOLATIONS OF THE RESPIRATORY PROTECTION STANDARD(§1910.134). ....................................................................................................... XIII. VIOLATIONS OF AIR CONTAMINANT STANDARDS (§1910.1000) ... 4-43 4-43A.R EQUIREMENTS UNDER THE STANDARD: .................................................................................................. 4-43B.C LASSIFICATION OF V IOLATIONS OF A IR C ONTAMINANT S TANDARDS. ......................................... 4-43 XIV. CITING IMPROPER PERSONAL HYGIENE PRACTICES. ................... 4-45A.I NGESTION H AZARDS. .................................................................................................................................... 4-45B.A BSORPTION H AZARDS. ................................................................................................................................ 4-46C.W IPE S AMPLING. ............................................................................................................................................. 4-46D.C ITATION P OLICY ............................................................................................................................................ 4-46 XV. BIOLOGICAL MONITORING. ...................................................................... 4-47CHAPTER 5CASE FILE PREPARATION AND DOCUMENTATIONI.INTRODUCTION ............................................................................................... 5-1 II.INSPECTION CONDUCTED, CITATIONS BEING ISSUED. .................... 5-1A.OSHA-1 ................................................................................................................................... 5-1B.OSHA-1A. ............................................................................................................................... 5-1C. OSHA-1B. ................................................................................................................................ 5-2 III.INSPECTION CONDUCTED BUT NO CITATIONS ISSUED .................... 5-5 IV.NO INSPECTION ............................................................................................... 5-5 V. HEALTH INSPECTIONS. ................................................................................. 5-6A.D OCUMENT P OTENTIAL E XPOSURE. ............................................................................................................... 5-6B.E MPLOYER’S O CCUPATIONAL S AFETY AND H EALTH S YSTEM. ............................................................. 5-6 VI. AFFIRMATIVE DEFENSES............................................................................. 5-8A.B URDEN OF P ROOF. .............................................................................................................................................. 5-8B.E XPLANATIONS. ..................................................................................................................................................... 5-8 VII. INTERVIEW STATEMENTS. ........................................................................ 5-10A.G ENERALLY. ......................................................................................................................................................... 5-10B.CSHO S SHALL OBTAIN WRITTEN STATEMENTS WHEN: .......................................................................... 5-10C.L ANGUAGE AND W ORDING OF S TATEMENT. ............................................................................................. 5-11D.R EFUSAL TO S IGN S TATEMENT ...................................................................................................................... 5-11E.V IDEO AND A UDIOTAPED S TATEMENTS. ..................................................................................................... 5-11F.A DMINISTRATIVE D EPOSITIONS. .............................................................................................5-11 VIII. PAPERWORK AND WRITTEN PROGRAM REQUIREMENTS. .......... 5-12 IX.GUIDELINES FOR CASE FILE DOCUMENTATION FOR USE WITH VIDEOTAPES AND AUDIOTAPES .............................................................. 5-12 X.CASE FILE ACTIVITY DIARY SHEET. ..................................................... 5-12 XI. CITATIONS. ..................................................................................................... 5-12A.S TATUTE OF L IMITATIONS. .............................................................................................................................. 5-13B.I SSUING C ITATIONS. ........................................................................................................................................... 5-13C.A MENDING/W ITHDRAWING C ITATIONS AND N OTIFICATION OF P ENALTIES. .................................. 5-13D.P ROCEDURES FOR A MENDING OR W ITHDRAWING C ITATIONS ............................................................ 5-14 XII. INSPECTION RECORDS. ............................................................................... 5-15A.G ENERALLY. ......................................................................................................................................................... 5-15B.R ELEASE OF I NSPECTION I NFORMATION ..................................................................................................... 5-15C. C LASSIFIED AND T RADE S ECRET I NFORMATION ...................................................................................... 5-16。

个人所得税改革外文文献翻译2018-2019

个人所得税改革外文文献翻译2018-2019个人所得税改革外文翻译2018-2019英文Personal income tax reforms: A genetic algorithm approach Matteo Morini, Simone PellegrinoAbstractGiven a settled reduction in the present level of tax revenue, and by exploring a very large combinatorial space of tax structures, in this paper we employ a genetic algorithm in order to determine the ‘best’ structure of a real world personal income tax that allows for the maximisation of the redistributive effect of the tax, while preventing all taxpayers being worse off than with the present tax structure. We take Italy as a case study.Keywords:Genetic algorithms,Personal income taxation,Micro-simulation models,Reynolds–Smolensky index,Tax reforms Personal income tax (hereafter, PIT) is characterised around the world by several parameters that define its structure: marginal tax rates, upper limits of thresholds, allowances and deductions, as well as tax credits. Applied to the distribution of income observed in a specific country, the PIT structure of that country determines a given tax revenue and a given redistributive effect, as well as influences economic efficiency, first of all work incentives and tax compliance.The existing economic literature represents a fundamental tool forthe PIT design and for the need of balancing equity and efficiency, as well as social preferences for redistribution. This literature first focused on axioms that are required in order to equally apportion the burden of taxation among citizens (Mill,1848, Samuelson, 1947). However, starting with the seminal paper by Mirrlees (1971), the theoretical literature has mainly focused on the equity-efficiency trade-off in optimum taxation. This is a difficult task, since many empirical simulation studies have, in fact, shown that in the short-run it is almost impossible to find a tax reform, which does not decrease efficiency or equity and, at the same time, is still financially and politically feasible. Moreover, if applied to a real-world tax system, most of the results of the economic literature would imply considerable modifications of the present tax structure and would certainly affect the tax revenue, which is one of the most important concerns that policymakers have to face. In other words, governments are certainly interested in setting up a tax system by implementing the literature's results, at least in the long-run. In the short-run, they are undoubtedly subject to budget constraints and to the political feasibility of a reform.Despite these arguments, the PIT structure is subject to continuous evolution around the world. Peter, Buttrick and Duncan (2010) study and categorize the trends in the PIT structure over the period of 1981 to 2005 in 189 countries. They show that many governments substantially and/orfrequently change the PIT structure; according to their analysis, about 45 per cent of governments changed at least one parameter of the PIT every year. They also emphasize that ‘The high frequency of changes may also be due to the gradual enactment of tax reforms that get implemented over several years, fiscal policy responses to the business cycle, or continuous experimentation and search for the best tax structure.’This paper focus on these key issues by considering a recently proposed real-world tax cut; it evaluates a feasible taxreform by optimizing the government's target and, in the meantime, by exactly complying with the government's budget constraint. The solution for this problem can be obtained by employing a genetic algorithm (hereafter, GA): a search heuristic inspired by natural selection, well-suited to the identification of the most promising solution to the problem under consideration. To our knowledge, no previous attempts at employing GAs for PIT structure optimisation exist. The unique applications to tax systems deal with other and simpler aspects (Brooks, 2000, Chen and Lee, 1997).The tax cut, which we study, has recently been implemented by the Italian government. In order to increase the purchasing power of ‘poor’ PIT taxpayers, as well as taxpayers belonging to the ‘middle class’ (a proxy of the redistributive effect maximisation), the Italian government recently reduced the PIT revenue by 9.324 billion euros (about 6 per centof the PIT tax revenue) by introducing a cash transfer of 80 euros per month only for employees with a PIT gross income in the range of 8–26 thousand euros (about 10.9 million taxpayers).Considering this reform, two questions arise: is this tax cut allocation the best one the government could have considered? Or, given this settled amount of the tax cut, which is the best way to reform the whole PIT structure in order to achieve the highest redistributive effect, whilst leaving no taxpayers worse-off with respect to the present tax structure? The GA is an appropriate tool, and Italy is a perfect case study, since the Italian PIT is very complicated and its structure incorporates more than thirty parameters. Our results show that a more general, better, and more equity-oriented reform is possible; moreover, this methodology can be applied to any other specific target.The solution of the problem discussed here faces an equity-efficiency trade-off: in order for the redistributive effect to be its highest, the efficiency of the tax (i.e. the level of the effective marginal tax rates) can worsen. In this first paper we just focus on the equity side of the problem. This does not imply that we forget about efficiency; we suggest a few constraints to the allowable parameters of tax structure in order to not arrive at both trivial and inefficient solutions.Even if by employing the ‘best’ tax structure (almost) no taxpayer is worse-off, its actual applicability could face political resistance since allparameters of the tax change and, consequently, taxpayers could hardly believe that no one is worse-off. We do not discuss these political economy inconveniences. Finally, it has to be noted that we also do not consider taxpayers’ responses to the new parameters of the tax structure; it is a ‘short run’ solution that can help policy makers when they think of PIT reform. In order to consider taxpayers’ responses further research can be done regarding a long-run perspective: for example by modelling the equity-efficiency trade-off in a genetic algorithm framework or by employing agent-based models. This is the baseline of our further research.Given its progressive nature, the PIT is a globally fundamental tool through which the redistributive effect of the whole tax system of a country is achieved, even if a large variability, in terms of both tax revenue and redistributive effect, is observed around the world (Verbist and Figari, 2014, Wagstaff et al., 1999). The two key reasons for this variability deal with the role played by social preferences for redistribution (Lefranc, Pistolesi, & Trannoy, 2008) and the equity-efficiency trade-off oftaxation (Feldstein, 1976, Saez, 2001, Sandmo, 1981, Stern, 1976, Toumala, 2016).Starting from Mill's (1848) approach, economic theory has first elaborated precise axioms to equally apportion the burden of taxation among citizens. The principle of equal sacrifice can thus give normativeand positive contents to the ability-to-pay principle and justify the tax progressivity. The resulting degree of progressivity depends on the amount of tax revenue to be raised, as well as the social welfare function characterizing preferences of the society. Within this framework, Young (1990) proposed a theoretical strategy in order to test the possibility of stating that a country's lawmaker adopts a precise criterion of distributive justice and a particular social welfare function when he determines vertical equity and modifications in the PIT structure (e.g., Pellegrino, 2008 for an application to the Italian case). Young's (1990) framework does not consider efficiency and incentive effects, so his methodology favours high marginal tax rates on higher incomes. Berliant and Gouveia (1993) introduce incentive effects within Young's (1990) methodology, finding conditions for progressive taxation similar to the standard ones elaborated by Samuelson (1947).On the other hand, Mirrlees (1971) introduces the theory of optimal direct taxation, which also deals with the equity-efficiency trade-off. As the real-world PIT systems are very complex, empirical applications of the optimal income tax theory are based on stylised tax, which involve only a few tax parameters. Within this framework, the most effective estimation difficulties deal with the economic behaviour modelling since the labour supply responses (Aaberge and Colombino, 2013, Bargain et al.,2014, Blundell and Shephard, 2012) and the tax base responses to taxchanges have to be introduced and parameterised (Saez, 2001, Saez et al., 2012).On the contrary, governments have to face PIT structures composed by several parameters and, most importantly, the PIT structure observed in a country (in a given year) is indeed the result of several and partial adjustments that have occurred over the previous years. Focusing on those aspects, this paper differs from the existing literature for several reasons. First of all, it has a different the point of view from which the PIT reform is evaluated. Usually, the existing empirical literature evaluates the effects of a tax reform after the government introduces it. On the contrary, in this paper, we consider the government's point of view before such a reform is introduced.Let us consider a generic government. Every year, this government plans finance law, which sets the annual adjustments on the level of the overall value of public spending and tax revenue to be obtained by the current legislation, in order to achieve some specific goals (such as the level of the government deficit) set in the long-term budget. One possible adjustment is the level of the PIT revenue. Starting from the actual PIT structure, the government may then want to cut PIT revenue in order to increase the purchasing power of taxpayers; conversely, it may want to increase the redistributive effect of the tax leaving the tax revenue unchanged; or, it may want to increase tax revenue by letting the richesttaxpayers face the whole tax increase, or it may want to modify the PIT structure in order to reduce the inefficiencies of the tax. These are, of course, only some explanatory perspectives.Whatever the target, which parameters of the tax should be changed in order to optimize it? How much should they change? Or, more generally, how should the whole PIT structure change? Given this target, it is not the case that policy-makers consider these questions when thinking of such a PIT reform. In order to implement a reform, the government usually changes some parameters of the tax compatible with its revenue constraint. Whether such a tax structure change is aimed at achieving the best way to obtain the specific target is debatable. The perspective discussed here can therefore be useful in setting a short-run tax reform. Apart from exceptional cases, the tax cuts represent a small percentage of the overall revenue of the tax; on one hand, results of the economic literature can be only guidelines for the implementation of such a reduction; on the other hand, the government is primarily interested in correctly forecasting the tax reduction, given its balanced budget constraint.In this paper, we propose a new methodology to implement a personal income tax reform. In particular, given a settled tax cut decided upon by the government, (a similar strategy can be applied if the tax revenue increases), we show how a genetic algorithm can be employed, in order to find out the values of all parameters defining the structure of thepersonal income tax able to satisfy a specific target. Our methodology can be applied to any other specific target; as an example, in this work our target is the maximisation of the redistributive effect of the tax, while preventing all taxpayers being worse off with respect to the present tax structure. We apply this methodology to the Italian personal income taxation system for two reasons: the tax structure is quite complicated,and recently the government decided to reduce tax revenue by about 9.324 billion euro starting from 2015. The aim of this tax cut is to increase the purchasing power of ‘poor’ taxpayers and taxpayers belonging to the ‘middle class’, and the instrument is the introduction of a cash transfer (not related to the structure of the personal income tax) only for employees with gross incomes in the range 8–26 thousand euros (in order for the yearly gain to be about one thousand euros), whilst all other kinds of taxpayer are not affected by this money transfer. Here we show that a better and more equity-oriented reform is possible. This methodology allows a short run reform, and can help policy makers when they think of a tax reform.中文个人所得税改革:一种遗传算法摘要考虑到目前税收收入的逐渐减少,并且通过探索发现当前的税收结构有很大的改革空间,在本文中,我们采用遗传算法来确定现实世界个人所得税的“最佳”结构,该结构允许为了最大程度地提高税收的再分配效果,同时防止所有纳税人的状况比目前的税收结构更糟。

会计 英文版 十四单元 答案