bootstrapping

Bootstrapping算法

1、Bootstrapping方法简介

Bootstrapping算法又叫自扩展技术,它是一种被广泛用于知识获取的机器学习技术。

它是一种循序渐进的学习方法,只需要很小数量的种子,以此为基础,通过一次次的训练,把种子进行有效的扩充,最终达到需要的数据信息规模。

2、Bootstrapping算法的主要步骤

(1) 建立初始种子集;

(2) 根据种子集,在抽取一定窗口大小的上下文模式,建立候选模式

集;

(3) 利用模式匹配识别样例,构成候选实体名集合。

将步骤(2)所得的

模式分别与原模式进行匹配,识别出样例,构成候选集合。

(4) 利用一定的标准评价和选择模式和样例,分别计算和样例的信息

熵增益,然后进行排序,选择满足一定要求的模式加入最终可用模式集,选择满足一定条件的样例加入种子集。

(5) 重复步骤(2)-(4),直到满足一定的迭代次数或者不再有新的样例

被识别。

3 相关概念

(1)上下文模式

它是指文本中表达关系和事件信息的重复出现的特定语言表达形式,可以按照特定的规则通过模式匹配,触发抽取特定信息。

上下文模式是由项级成的有有序序列,每个项对应于一个词或者词组的集合。

(2)模式匹配

模式匹配是指系统将输入的句子同有效模式进行匹配,根据匹配成功的模式,得到相应的解释。

(3)样例

样例是在Bootstrapping迭代过程中,经过模式匹配后,抽取出来的词语。

Bootstrapping

Why bootstrapping works?

• If we want to ask a question of a population but you can't. So you take a sample and ask the question of it instead. Now, how confident you should be that the sample answer is close to the population answer obviously depends on the structure of population. One way you might learn about this is to take samples from the population again and again, ask them the question, and see how variable the sample answers tended to be. Since this isn't possible you can either make some assumptions about the shape of the population, or you can use the information in the sample you actually have to learn about it.

• NOTICE: Resampling is not done to provide an estimate of the population distribution--we take our sample itself as a model of the population.

稳健性检验方法

稳健性检验方法稳健性检验是指在统计学中用来检验模型的稳定性和鲁棒性的一种方法。

在实际应用中,由于数据的不确定性和复杂性,我们需要对模型进行稳健性检验,以确保模型的可靠性和有效性。

本文将介绍稳健性检验的基本原理、常用方法以及实际应用。

一、稳健性检验的基本原理。

稳健性检验的基本原理是通过对模型的参数进行一定的扰动,来检验模型对数据的变化和异常值的敏感程度。

在实际应用中,我们经常会遇到数据的异常值、缺失值等问题,这些问题可能会对模型的参数估计产生影响。

稳健性检验可以帮助我们评估模型对这些问题的鲁棒性,从而提高模型的可靠性和泛化能力。

二、稳健性检验的常用方法。

1. Bootstrapping(自助法)。

Bootstrapping是一种常用的稳健性检验方法,它通过对原始数据进行重抽样来估计参数的分布。

在每次重抽样中,我们可以得到一个新的参数估计值,通过对这些值的分布进行分析,可以评估模型对数据的变化和异常值的敏感程度。

2. Robust regression(鲁棒回归)。

Robust regression是一种通过对残差进行加权来减小异常值对参数估计的影响的方法。

它可以有效地降低异常值对模型的影响,提高模型的稳健性。

3. Sensitivity analysis(敏感性分析)。

敏感性分析是一种通过对模型参数进行一定范围内的变化来评估模型的稳健性的方法。

通过对参数进行逐步调整,我们可以了解模型对参数变化的敏感程度,从而评估模型的稳健性。

三、稳健性检验的实际应用。

稳健性检验在实际应用中具有重要的意义。

在金融领域,由于金融数据的复杂性和波动性,我们经常需要对模型进行稳健性检验,以确保模型对市场波动和异常事件的鲁棒性。

在医学领域,稳健性检验也被广泛应用于临床试验和流行病学研究中,以评估模型对异常数据和缺失数据的处理能力。

总之,稳健性检验是保证模型可靠性和有效性的重要手段。

通过对模型的稳健性进行评估,我们可以更好地理解模型对数据的敏感程度,从而提高模型的预测能力和泛化能力。

随机准备金-拔靴法bootstrapping方法

灰色区域的LDF是通过拔靴带法得到的一个拔靴带样本

14

© 2012 CPCR. All rights reserved.

针对LDF的拔靴带法举例

得到的未来赔款预测的一个拔靴带样本如下:

年度 1 2 3 4 1 1000 1200 1000 1200 2 1500 1600 1400 1680 3 终极 准备金 1600 1600 0 1700 1700 0 1493.333 1493.333 93.33333 1785 1785 585 Total: 678.3333

以上仅是一个拔靴带样本,我们需要重复m次,比如10 万次,得到总准备金的均值约是693,标准差约是88 本质上类似于针对LDF的随机链梯法

15

© 2012 CPCR. All rights reserved.

E&V提出的拔靴带法举例

已知的实际累积赔款三角形如下:

年度 1 2 3 4 1 1000 1200 1000 1200 2 1500 1600 1400 3 1600 1700 Ult 1600

重新构造一个增量三角形

年度 1 2 3 4 1 1,078.88 1,242.02 1,000.00 1,192.34 2 474.02 454.93 410.63 3 94.79 74.04 Ult -

重构增量三角形的算法为 ������‘ = ������ + ������ ∙ ������

3

© 2012 CPCR. All rights reserved.

拔靴带法的典故

术语“Bootstrap”来自短语“to pull oneself up by one's bootstraps” 源自西方神话故事“ The Adventures of Baron Munchausen”,男爵掉到了深湖底,没有工具,所以他 想到了拎着鞋带将自己提起来 计算机的引导程序boot也来源于此 意义:不靠外界力量,而靠自身提升自己的性能,翻译 为自助/自举

bootstrap 简单的评价打星

Bootstrap 简单的评价1. 介绍Bootstrap是一个流行的前端开发框架,旨在帮助开发人员快速构建响应式网站和Web应用程序。

它由Twitter开发,并于2011年首次发布。

Bootstrap提供了一系列的HTML、CSS和JavaScript组件,以及预定义的样式和布局,使开发人员能够轻松地创建专业且美观的网站。

2. 优点2.1 响应式设计Bootstrap的一个主要优点是其响应式设计。

响应式设计是指网站能够根据不同设备的屏幕尺寸和分辨率来自动调整布局和样式。

Bootstrap通过使用栅格系统和媒体查询来实现响应式设计。

开发人员可以轻松地根据需要定义不同屏幕大小的样式和布局,从而确保网站在各种设备上都能够良好地显示。

2.2 快速开发Bootstrap提供了大量预定义的样式和组件,使开发人员能够更快地构建网站和应用程序。

开发人员不再需要从头开始编写样式和布局,只需使用Bootstrap提供的类和组件,便可快速创建漂亮且一致的界面。

此外,Bootstrap还提供了一些实用的JavaScript插件,如轮播、模态框和下拉菜单等,以进一步简化开发过程。

2.3 浏览器兼容性Bootstrap经过广泛的测试,确保在所有主流浏览器中都能够良好地运行。

它能够适应不同浏览器的差异,确保在各种环境中的兼容性。

无需为不同浏览器编写特定的样式和脚本,开发人员只需专注于编写业务逻辑即可。

2.4 社区支持由于Bootstrap的广泛应用和开源性质,它拥有庞大的开发者社区。

社区成员分享各种教程、示例和插件,可以帮助开发人员解决各种问题。

此外,社区还提供了定期更新和改进,使Bootstrap始终保持最新且更加强大。

3. 缺点3.1 高度定制化的困难尽管Bootstrap提供了丰富的样式和组件,但它的定制化程度相对较低。

如果开发人员需要与众不同的界面风格或功能,可能需要花费更多时间和精力来修改和定制Bootstrap的样式和组件。

手机电视鉴权模块命令及文件

手机电视鉴权模块命令及文件1.命令AUTHENTICATE命令描述该命令被用于以下几种安全语境:GBA_U安全语境:当请求GBA引导过程时使用;MBMS安全语境:当请求MBMS安全过程时使用。

GBA_U安全语境支持两种模式:a) Bootstrapping模式:SD和BSF之间相互认证,并且在AKA认证过程中获取Ks。

b) NAF分散模式:通过Bootstrapping模式生成的密钥,获得MUK和MRK。

MBMS安全语境支持两种模式:a) MSK更新模式:更新MSK。

b) MTK生成模式:终端可获取MTK用于解密节目流。

AUTHENTICATE在2G环境下也扩展了对GBA语境的支持,以完成GBA引导过程。

GBA 安全语境(Bootstrapping模式)该命令用于手机电视用户鉴权,同时产生Ks。

3G Input:-RAND,CK、IK、SRES2G Input:- RAND,Kc、Ks_input、SRESOutput:- RES’、cnonceGBA安全语境(NAF分散模式)在网络侧推送业务密钥MSK时使用该命令,认证用户的合法性。

Input:- NAF_ID, IMPIOutput:- Ks_ext_NAFMBMS安全语境(MSK更新模式)UAM收到终端发来的MIKEY消息包后,验证消息后将业务密钥保存在卡内。

Input:- MIKEY message(HDR,EXT,TS,RAND,IDi,IDr,KEMAC)Output:- MIKEY message(HDR,TS,IDr,V)or-NoneMBMS 安全语境(MTK生成模式)UAM收到终端发来的MIKEY消息包后,验证密钥的有效性并输出节目流密钥(CW)。

Input:- MIKEY message(HDR,EXT,TS KEMAC)Output:- MTK and Salt (if available)命令参数和数据GBA安全语境(Bootstrapping 模式)GBA安全语境(Bootstrapping 模式)命令:3G状态下命令数据DATA描述:GBA安全语境 (NAF分散模式)GBA安全语境 (NAF分散模式)命令:MBMS安全语境 (适用于所有模式)MBMS安全语境数据域:返回状态条件UAM2.文件内容本章将详细说明UAM中与移动多媒体广播/手机电视业务相关的基本文件,定义基本文件的访问条件、数据项及编码方式。

操作系统的启动过程

操作系统的启动过程操作系统(Operating System,简称OS)是计算机系统中最基本的软件之一,它负责管理和控制计算机的硬件和软件资源,为用户和应用程序提供丰富的功能和良好的用户体验。

在计算机启动时,操作系统也需要经历一系列的启动过程,以确保系统能够正常运行。

下面将详细介绍操作系统的启动过程。

一、引导阶段(Bootstrapping Stage)在计算机加电启动后,首先会由计算机的固化ROM(Read-Only Memory)中的引导程序开始执行。

这个引导程序位于计算机的主板上,负责启动操作系统。

引导程序首先会检测计算机中是否有可引导的设备,比如硬盘、光盘、USB等。

一旦发现可引导设备,引导程序就会将该设备中特定的引导扇区(Boot Sector)加载到计算机的内存中。

二、引导扇区的执行当引导扇区被加载到内存后,计算机的控制权交给了引导扇区中的代码。

引导扇区中的代码被称为引导加载程序(Boot Loader),它是一段特殊的机器指令,负责进一步加载操作系统的核心部分。

三、操作系统核心加载引导加载程序会根据预先设定的规则和算法,搜索计算机硬件设备,找到存放操作系统的特定分区或文件。

然后,它将操作系统的核心部分一次性地加载到计算机的内存中。

操作系统核心通常被保存为一个或多个可执行文件,也被称为内核(Kernel)。

四、内核初始化当操作系统核心被加载到内存后,内核开始执行,并进入初始化阶段。

在这个阶段,内核会对计算机的硬件进行自检和初始化,包括对处理器、内存、设备等的初始化操作。

内核还会为各个子系统和模块分配和初始化资源,准备操作系统运行时所需要的环境。

五、用户空间初始化在内核初始化完成后,操作系统会创建一个或多个用户空间(User Space)。

用户空间是操作系统为应用程序和用户提供的执行环境。

操作系统会根据系统配置和用户需求,初始化用户空间中的各个组件,比如图形界面、网络服务、文件系统等。

bootstrapping method

bootstrapping methodBootstrapping is a statistical methodology that relies on resampling with replacement to estimate a population parameter. In bootstrapping, a sample of sizes equal to that of the population or dataset of interest is taken from the population with replacement. In other words, each sample is taken from the original population or dataset and added back to the population or dataset each time it is taken. This process is repeated until all of the samples from the original population or dataset have been re-sampled.The main technique used in bootstrapping is sampling with replacement. This means that each unit in the population is equally likely to be included in the sample, which ensures that each unit has an equal chance of being chosen. This ensures that bias is limited and the sample is representative of the population as a whole. Bootstrapping is useful for estimating population parameters when it is difficult or impossible to use traditional methods. For example, it can be used to estimate the likelihood of an event, calculate a confidence interval, or extrapolate from small samples.Bootstrapping can be used in a variety of applications, ranging from estimating the accuracy of a survey to the accuracy of a model. It is also used in machine learning applications, such as to find the best set of parameters for a model, and to assess the uncertainty in predictions. In addition, it can be used to assess the accuracy of a survey or the reproducibility of an experimental result.Overall, bootstrapping is a powerful technique for estimating population parameters when traditional methods or small sample sizes are not available. It is used in a variety of applications, from research to machine learning, and provides an effective way to measure accuracy and uncertainty.。

Bootstrapping

Bootstrapping转⾃:Bootstrapping从字⾯意思翻译是拔靴法,从其内容翻译⼜叫⾃助法,是⼀种再抽样的统计⽅法。

⾃助法的名称来源于英⽂短语“to pull oneself up by one’s bootstrap”,表⽰完成⼀件不能⾃然完成的事情。

1977年美国Standford⼤学统计学教授Efron提出了⼀种新的增⼴样本的统计⽅法,就是Bootstrap⽅法,为解决⼩⼦样试验评估问题提供了很好的思路。

Bootstrapping算法,指的就是利⽤有限的样本资料经由多次,重新建⽴起⾜以代表母体的新样本。

bootstrapping的运⽤基于很多统计学假设,因此假设的成⽴与否影响采样的准确性。

统计学中,bootstrapping可以指依赖于重置随机抽样的⼀切试验。

bootstrapping可以⽤于计算样本估计的准确性。

对于⼀个采样,我们只能计算出某个(例如)的⼀个取值,⽆法知道均值统计量的分布情况。

但是通过(⾃举法)我们可以模拟出均值统计量的近似分布。

有了分布很多事情就可以做了(⽐如说有你推出的结果来进⽽推测实际总体的情况)。

bootstrapping⽅法的实现很简单,假设抽取的样本⼤⼩为n:在原样本中有放回的抽样,抽取n次。

每抽⼀次形成⼀个新的样本,重复操作,形成很多新样本,通过这些样本就可以计算出样本的⼀个分布。

新样本的数量通常是1000-10000。

如果计算成本很⼩,或者对精度要求⽐较⾼,就增加新样本的数量。

优点:简单易于操作。

缺点:bootstrapping的运⽤基于很多统计学假设,因此假设的成⽴与否会影响采样的准确性。

1、⾃助法的基本思路:如果不知道总体分布,那么,对总体分布的最好猜测便是由数据提供的分布。

⾃助法的要点是:①假定观察值便是总体;②由这⼀假定的总体抽取样本,即再抽样。

由原始数据经过再抽样所获得的与原始数据集含量相等的样本称为再抽样样本(resamples)或⾃助样本(bootstrapsamples)。

Bootstrap方法的原理

Bootstrap方法的原理Bootstrap方法是一种统计学中常用的非参数统计方法,用于估计统计量的抽样分布。

它的原理是通过从原始样本中有放回地抽取大量的重复样本,然后利用这些重复样本进行统计推断。

Bootstrap方法的原理可以分为以下几个步骤:1. 抽样:从原始样本中有放回地抽取大量的重复样本。

这意味着每次抽样都是独立的,每个样本都有相同的概率被选中。

抽样的次数通常为几千次甚至更多,以确保得到足够多的样本。

2. 统计量计算:对于每个重复样本,计算所关心的统计量。

统计量可以是均值、中位数、方差等,具体根据问题的需求而定。

3. 统计量分布估计:将得到的统计量按照大小排序,然后根据排序结果计算置信区间或者计算假设检验的p值。

置信区间可以用来估计统计量的不确定性,p值可以用来判断统计量是否显著。

4. 结果解释:根据统计量的分布估计结果,对原始样本进行统计推断。

例如,可以利用置信区间判断总体均值的范围,或者利用p值判断两个样本的差异是否显著。

Bootstrap方法的原理基于自助法(bootstrapping)的思想,即通过从原始样本中有放回地抽取样本,模拟出多个类似于原始样本的重复样本。

这样做的好处是可以利用这些重复样本来估计统计量的抽样分布,而无需对总体分布做出任何假设。

Bootstrap方法的优点在于它不依赖于总体分布的假设,适用于各种类型的数据和统计量。

它可以提供更准确的估计和更可靠的推断结果,尤其在样本量较小或总体分布未知的情况下。

此外,Bootstrap方法还可以用于模型选择、参数估计和预测等统计问题。

总之,Bootstrap方法通过重复抽样和统计量计算来估计统计量的抽样分布,从而进行统计推断。

它的原理简单而直观,适用范围广泛,是统计学中常用的非参数统计方法之一。

第5章 整合创业资源

第5章整合创业资源第一部分本章概要1。

1重点概念1。

资源基础理论(Resource—based Theory):是把企业看作由一系列具有不同用途的资源相联结的集合,关注企业内部的资源对实现企业成长的重要性,以及企业在其成长战略中如何利用不同的资源。

2.步步为营(Bootstrapping):主要指在缺乏资源的情况下,创业者分多个阶段投入资源并且在每个阶段或决策点投入最少的资源.3。

拼凑(Bricolage):在已有元素基础上,不断替换其中的一些要素,形成新的认识。

4.信任:是涉及交易或交换关系的基础,是一种稳定的信念,维系着社会共享价值和稳定。

(来自“百度百科”)5.资源整合:指企业对不同来源、不同层次、不同结构、不同内容的资源进行识别与选择、汲取与配置、激活和有机融合,使其具有较强的柔性、条理性、系统性和价值性,并创造出新的资源的一个复杂的动态过程。

6。

利益相关者:组织外部环境中受组织决策和行动影响的任何相关者。

7。

双赢:双赢是成双的,对于客户与企业来说,应是客户先赢企业后赢;对于员工与企业之间来说,应是员工先赢企业后赢.双赢强调的是双方的利益兼顾,即所谓的“赢者不全赢,输者不全输"。

8。

博弈:在一定条件下,遵守一定的规则,一个或几个拥有绝对理性思维的人或团队,从各自允许选择的行为或策略进行选择并加以实施,并从中各自取得相应结果或收益的过程。

1。

2关键知识点1。

资源基础理论资源基础理论从企业的内部寻找企业成长的动因,用资源与能力来解释企业差异的原因.其基本假设是,企业具有不同的有形和无形的资源,这些资源可转变成独特的能力;资源在企业间是不可流动的且难以复制;企业内部能力、资源和知识的积累是企业获得超额利润和保持企业竞争优势的关键。

资源基础理论将企业描述成一组异质性资源的组合,创业因而可以看作整合异质性资源的过程,因此对资源的分类有助于理解资源整合的过程。

对创业资源的分类有很多种.结合多方面的研究成果,根据资源性质可将创业资源分为六种资源,即人力资源、社会资源、财务资源、物质资源、技术资源和组织资源.2. 创业者的可承受损失(1)时间。

自举法(Bootstrapping)

⾃举法(Bootstrapping)

⾃举法是在1个容量为n的原始样本中重复抽取⼀系列容量也是n的随机样本,并保证每次抽样中每⼀样本观察值被抽取的概率都是1/n(复置抽样)。

这种⽅法可⽤来检查样本统计数θ的基本性质,估计θ的标准误和确定⼀定置信系数下θ的置信区间。

⾃助法(Bootstrap Method)是Efron(1979)於Annals of Statistics所发表的⼀个办法,是近代统计发展上极重要的⼀个⾥程碑,⽽在执⾏上常需借助於现代快速的电脑。

举例来说,当⽤样本平均来估算母群体期望值时,为对此⼀估算的误差有所了解,我们常⽤信赖区间(confidence interval)的办法来做推估,此时得对样本平均的sampling distribution有所了解。

在基本统计教本上,当样本所来⾃的母群体,可⽤常态分配描述时,其sampling distribution可或为常态分配或为t分配。

但当样本所来⾃的母群体,不宜⽤常态分配描述时,我们或⽤电脑模拟或⽤渐进分析的办法加以克服。

当对母群体的了解不够深时,渐进分析的办法是较有效的⽅法,故中央极限定理(Central Limit Theorem),Edgeworth Expansion (small sample theory)等办法及其可⾏性及限制等於⽂献中⼴被探讨,⼈们虽不全然喜欢这些办法,但也找不出更理性的⽅法来取代渐进分析的办法。

⽽⾃助法确是⼀个相当具说服⼒的⽅法,更提供了统计⼯作者另⼀个寻找sampling distribution 的办法,故在近年来於⽂献中⼴被探讨。

[转载]Bootstrapping

![[转载]Bootstrapping](https://img.taocdn.com/s3/m/a914606b178884868762caaedd3383c4bb4cb471.png)

[转载]Bootstrapping关于Bootstrap的专门介绍,很全⾯。

如果能对Bias-corrected bootstrap给予更深⼊的分析对⽐就更好了。

原⽂地址:Bootstrapping作者:招展如桦BootstrappingBootstrapping is the practice of estimating properties of an estimator (such as its variance) by measuring those properties when sampling from an approximating distribution. One standard choice for an approximating distribution is the empirical distribution of the observed data. In the case where a set of observations can be assumed to be from an independent and identically distributed population, this can be implemented by constructing a number of resamples of the observed dataset (and of equal size to the observed dataset), each of which is obtained by random sampling with replacement from the original dataset.It may also be used for constructing hypothesis tests. It is often used as an alternative to inference based on parametric assumptions when those assumptions are in doubt, or where parametric inference is impossible or requires very complicated formulas for the calculation of standard errors.Informal descriptionThe basic idea of bootstrapping is that the sample we have collected is often the best guess we have as to the shape of the population from which the sample was taken. For instance, a sample of observations with two peaks in its histogram would not be well approximated by a Gaussian or normal bell curve, which has only one peak. Therefore, instead of assuming a mathematical shape (like the normal curve or some other) for the population, we instead use the shape of the sample.As an example, assume we are interested in the average (or mean) height of people worldwide. We cannot measure all the people in the global population, so instead we sample only a tiny part of it, and measure that. Assume the sample is of size N; that is, we measure the heights of N individuals. From that single sample, only one value of the mean can be obtained. In order to reason about the population, we need some sense of the variability of the mean that we have computed.To use the simplest bootstrap technique, we take our original data set of N heights, and, using a computer, make a new sample (called a bootstrap sample) that is also of size N. This new sample is taken from the original using sampling with replacement so it is not identical with the original "real" sample. We repeat this a lot (maybe 1000 or 10,000 times), and for each of these bootstrap samples we compute its mean (each of these are called bootstrap estimates). We now have a histogram of bootstrap means. This provides an estimate of the shape of the distribution of the mean from which we can answer questions about how much the mean varies. (The method here, described for the mean, can be applied to almost any other statistic or estimator.)The key principle of the bootstrap is to provide a way to simulate repeated observations from an unknown population using the obtained sample as a basis.Situations where bootstrapping is usefulAdèr et al.[4] recommend the bootstrap procedure for the following situations:When the theoretical distribution of a statistic of interest is complicated or unknown. Since the bootstrapping procedure is distribution-independent it provides an indirect method to assess the properties of the distributionunderlying the sample and the parameters of interest that are derived from this distribution.When the sample size is insufficient for straightforward statistical inference. If the underlying distribution is well-known, bootstrapping provides a way to account for the distortions caused by the specific sample that may not be fully representative of the population.When power calculations have to be performed, and a small pilot sample is available. Most power and sample size calculations are heavily dependent on the standard deviation of the statistic of interest. If the estimate used is[edit ][edit ][edit ][edit ]incorrect, the required sample size will also be wrong. One method to get an impression of the variation of the statistic is to use a small pilot sample and perform bootstrapping on it to get impression of the variance. DiscussionAdvantagesA great advantage of bootstrap is its simplicity. It is straightforward way to derive estimates of standard errors and confidence intervals for complex estimators of complex parameters of the distribution, such as percentile points, proportions, odds ratio,and correlation coefficients. Moreover, it is an appropriate way to control and check the stability of the results.Disadvantages Although bootstrapping is (under some conditions) asymptotically consistent, it does not provide general finite-sampleguarantees. Furthermore, it has a tendency to be overly optimistic.[citation needed ] The apparent simplicity may conceal the fact that important assumptions are being made when undertaking the bootstrap analysis (e.g. independence of samples) where these would be more formally stated in other approaches.Types of bootstrap scheme In univariate problems, it is usually acceptable to resample the individual observations with replacement ("case resampling" below). In small samples, a parametric bootstrap approach might be preferred. For other problems, a smooth bootstrap will likely be preferred.For regression problems, various other alternatives are available.[citation needed ]Case resampling Bootstrap is generally useful for estimating the distribution of a statistic (e.g. mean, variance) without using normal theory (e.g. z-statistic, t-statistic). Bootstrap comes in handy when there is no analytical form or normal theory to help estimate the distribution of the statistics of interest, since bootstrap method can apply to most random quantities, e.g., the ratio of variance and mean. There are at least two ways of performing case resampling.1. The Monte Carlo algorithm for case resampling is quite simple. First, we resample the data with replacement, and the size of the resample must be equal to the size of the original data set. Then the statistic of interest is computed from the resample from the first step. We repeat this routine many times to get a more precise estimate of the Bootstrapdistribution of the statistic.2. The 'exact' version for case resampling is similar, but we exhaustively enumerate every possible resample of the data set. This can be computationally expensive as there are a total of different resamples, where n is the size of the data set.Estimating the distribution of sample mean Consider a coin-flipping experiment. We flip the coin and record whether it lands heads or tails. (Assume for simplicity that there are only two outcomes) Let X = x 1, x 2, …, x 10 be 10 observations from the experiment. x i = 1 if the i th flip lands heads,and 0 otherwise. From normal theory, we can use t-statistic to estimate the distribution of the sample mean, .Instead, we use bootstrap, specifically case resampling, to derive the distribution of . We first resample the data to obtain a bootstrap resample . An example of the first resample might look like this X 1* = x 2, x 1, x 10, x 10, x 3, x 4, x 6, x 7, x 1, x 9. Note that there are some duplicates since a bootstrap resample comes from sampling with replacement from the data. Note also that the number of data points in a bootstrap resample is equal to the number of data points in our original observations. Then we compute the mean of this resample and obtain the first bootstrap mean : µ1*. We repeat this process to obtain the second resample X 2* and compute the second bootstrap mean µ2*. If we repeat this 100 times, then we have µ1*, µ2*, …, µ100*. This represents an empirical bootstrap distribution of sample mean. From this empirical distribution, one can derive a bootstrap confidence interval for the purpose of hypothesis testing.Regression In regression problems, case resampling refers to the simple scheme of resampling individual cases - often rows of a data set . For regression problems, so long as the data set is fairly large, this simple scheme is often acceptable. However, the method is open to criticism [citation needed ].In regression problems, the explanatory variables are often fixed, or at least observed with more control than the response[edit ][edit ][edit ][edit ][edit ][edit ][edit ][edit ]variable. Also, the range of the explanatory variables defines the information available from them. Therefore, to resample cases means that each bootstrap sample will lose some information. As such, alternative bootstrap procedures should be considered.Bayesian bootstrap Bootstrapping can be interpreted in a Bayesian framework using a scheme that creates new datasets through reweighting the initial data. Given a set of data points, the weighting assigned to data point in a new dataset is , where is a low-to-high ordered list of uniformly distributed random numbers on , preceded by 0 and succeeded by 1. The distributions of aparameter inferred from considering many such datasets are then interpretable as posterior distributions on that parameter.[5]Smooth bootstrapUnder this scheme, a small amount of (usually normally distributed) zero-centered random noise is added on to each resampled observation. This is equivalent to sampling from a kernel density estimate of the data.Parametric bootstrap In this case a parametric model is fitted to the data, often by maximum likelihood , and samples of random numbers are drawn from this fitted model. Usually the sample drawn has the same sample size as the original data. Then the quantity, or estimate, of interest is calculated from these data. This sampling process is repeated many times as for other bootstrapmethods. The use of a parametric model at the sampling stage of the bootstrap methodology leads to procedures which are different from those obtained by applying basic statistical theory to inference for the same model.Resampling residualsAnother approach to bootstrapping in regression problems is to resample residuals . The method proceeds as follows.1. Fit the model and retain the fitted values and the residuals .2. For each pair, (x i , y i ), in which x i is the (possibly multivariate) explanatory variable, add a randomly resampledresidual, , to the response variable y i . In other words create synthetic response variables where j is selectedrandomly from the list (1, …, n ) for every i .3. Refit the model using the fictitious response variables y*i , and retain the quantities of interest (often the parameters, ,estimated from the synthetic y*i ).4. Repeat steps 2 and 3 a statistically significant number of times.This scheme has the advantage that it retains the information in the explanatory variables. However, a question arises as to which residuals to resample. Raw residuals are one option; another is studentized residuals (in linear regression). Whilst there are arguments in favour of using studentized residuals; in practice, it often makes little difference and it is easy to run both schemes and compare the results against each other.Gaussian process regression bootstrap When data are temporally correlated, straightforward bootstrapping destroys the inherent correlations. This method uses Gaussian process regression to fit a probabilistic model from which replicates may then be drawn. Gaussian processes are methods from Bayesian non-parametric statistics but are here used to construct a parametric bootstrap approach, which implicitly allows the time-dependence of the data to be taken into account.Wild bootstrap Each residual is randomly multiplied by a random variable with mean 0 and variance 1. This method assumes that the 'true'residual distribution is symmetric and can offer advantages over simple residual sampling for smaller sample sizes.[6]Moving block bootstrap In the moving block bootstrap, n-b+1 overlapping blocks of length b will be created in the following way: Observation 1 to b will be block 1, observation 2 to b+1 will be block 2 etc. Then from these n-b+1 blocks, n/b blocks will be drawn at random with replacement. Then aligning these n/b blocks in the order they were picked, will give the bootstrap observations. This bootstrap works with dependent data, however, the bootstrapped observations will not be stationary anymore byconstruction. But, it was shown that varying the block length can avoid this problem.[7]Choice of statistic[edit ][edit ][edit ][edit ][edit ]The bootstrap distribution of a point estimator of a population parameter has been used to produce a bootstrapped confidence interval for the parameter's true value, if the parameter can be written as a function of the population's distribution .Population parameters are estimated with many point estimators . Popular families of point-estimators include mean-unbiased minimum-variance estimators , median-unbiased estimators , Bayesian estimators (for example, the posterior distribution 's mode , median , mean ), and maximum-likelihood estimators .A Bayesian point estimator and a maximum-likelihood estimator have good performance when the sample size is infinite,according to asymptotic theory . For practical problems with finite samples, other estimators may be preferable. Asymptotic theory suggests techniques that often improve the performance of bootstrapped estimators; the bootstrapping of a maximum-likelihood estimator may often be improved using transformations related to pivotal quantities .[8]Deriving confidence intervals from the bootstrap distribution The bootstrap distribution of a parameter-estimator has been used to calculate confidence intervals for its population-parameter.[citation needed ]Effect of bias and the lack of symmetry on bootstrap confidence intervalsBias : The bootstrap distribution and the sample may disagree systematically, in which case bias may occur.If the bootstrap distribution of an estimator is symmetric, then percentile confidence-interval are often used; such intervals are appropriate especially for median-unbiased estimators of minimum risk (with respect to an absolute loss function ). Bias in the bootstrap distribution will lead to bias in the confidence-interval.Otherwise, if the bootstrap distribution is non-symmetric, then percentile confidence-intervals are often inappropriate.Methods for bootstrap confidence intervalsThere are several methods for constructing confidence intervals from the bootstrap distribution of a real parameter:Percentile Bootstrap . It is derived by using the 2.5 and the 97.5 percentiles of the bootstrap distribution as the limits of the 95% confidence interval. This method can be applied to any statistic. It will work well in cases where the bootstrap distribution is symmetrical and centered on the observed statistic [9] and where the sample statistic is median-unbiased and has maximum concentration (or minimum risk with respect to an absolute value loss function). In other cases, the percentile bootstrap can be too narrow. When working with small sample sizes (i.e., less than 50), the percentile confidence intervals for (for example) the variance statistic will be too narrow. So that with a sample of 20 points, 90%confidence interval will include the true variance only 78% of the time, according to Schenker.[citation needed ]Bias-Corrected Bootstrap - adjusts for bias in the bootstrap distribution.Accelerated Bootstrap - The bootstrap bias-corrected and accelerated (BCa) bootstrap, by Efron (1987),[10] adjusts for both bias and skewness in the bootstrap distribution. This approach is accurate in a wide variety of settings, hasreasonable computation requirements, and produces reasonably narrow intervals.[citation needed ]Basic Bootstrap .Studentized Bootstrap .Example applicationsSmoothed bootstrap In 1878, Simon Newcomb took observations on the speed of light .[11] The data set contains two outliers , which greatly influence the sample mean . (Note that the sample mean need not be a consistent estimator for any population mean ,because no mean need exist for a heavy-tailed distributions .) A well-defined and robust statistic for central tendency is the sample median, which is consistent and median-unbiased for the population median.The bootstrap distribution for Newcomb's data appears below. A convolution-method of regularization reduces thediscreteness of the bootstrap distribution, by adding a small amount of N (0, σ2) random noise to each bootstrap sample. Aconventional choice is for sample size n .[citation needed ]Histograms of the bootstrap distribution and the smooth bootstrap distribution appear below[edit ][edit ][edit ]. The bootstrap distribution of the sample-median has only a small number of values. The smoothed bootstrap distribution has a richer support .In this example, the bootstrapped 95% (percentile) confidence-interval for the population median is (26, 28.5), which is close to the interval for (25.98, 28.46) for the smoothed bootstrap.Relation to other approaches to inference Relationship to other resampling methods The bootstrap is distinguished from :the jackknife procedure, used to estimate biases of sample statistics and to estimate variances, and cross-validation , in which the parameters (e.g., regression weights, factor loadings) that are estimated in one subsample are applied to another subsample.For more details see bootstrap resampling .Bootstrap aggregating (bagging) is a meta-algorithm based on averaging the results of multiple bootstrap samples.U-statisticsMain article: U-statistic In situations where an obvious statistic can be devised to measure a required characteristic using only a small number, r , of data items, a corresponding statistic based on the entire sample can be formulated. Given an r -sample statistic, one can create an n -sample statistic by something similar to bootstrapping (taking the average of the statistic over all subsamples of size r ). This procedure is known to have certain good properties and the result is a U-statistic . The sample mean and sample variance are of this form, for r =1 and r =2.。

Bootstrapping示例

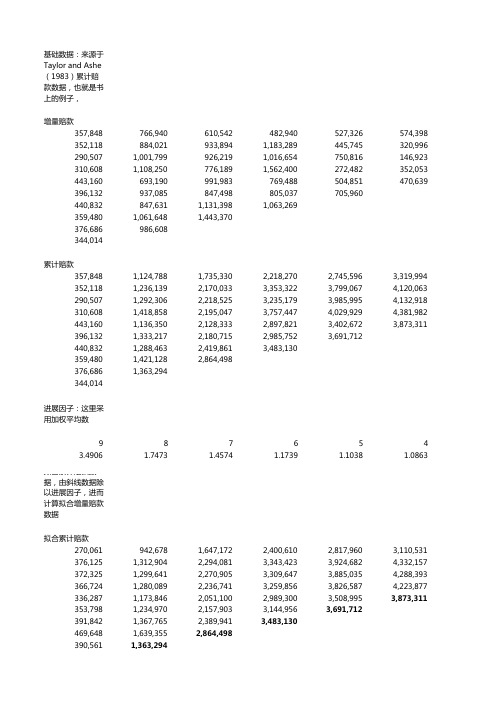

基础数据:来源于Taylor and Ashe(1983)累计赔款数据,也就是书上的例子,增量赔款357,848766,940610,542482,940527,326574,398 352,118884,021933,8941,183,289445,745320,996 290,5071,001,799926,2191,016,654750,816146,923 310,6081,108,250776,1891,562,400272,482352,053 443,160693,190991,983769,488504,851470,639 396,132937,085847,498805,037705,960440,832847,6311,131,3981,063,269359,4801,061,6481,443,370376,686986,608344,014累计赔款357,8481,124,7881,735,3302,218,2702,745,5963,319,994 352,1181,236,1392,170,0333,353,3223,799,0674,120,063 290,5071,292,3062,218,5253,235,1793,985,9954,132,918 310,6081,418,8582,195,0473,757,4474,029,9294,381,982 443,1601,136,3502,128,3332,897,8213,402,6723,873,311 396,1321,333,2172,180,7152,985,7523,691,712440,8321,288,4632,419,8613,483,130359,4801,421,1282,864,498376,6861,363,294344,014进展因子:这里采用加权平均数9876543.4906 1.7473 1.4574 1.1739 1.1038 1.0863拟合累计赔款数据,由斜线数据除以进展因子,进而计算拟合增量赔款数据拟合累计赔款270,061942,6781,647,1722,400,6102,817,9603,110,531 376,1251,312,9042,294,0813,343,4233,924,6824,332,157 372,3251,299,6412,270,9053,309,6473,885,0354,288,393 366,7241,280,0892,236,7413,259,8563,826,5874,223,877 336,2871,173,8462,051,1002,989,3003,508,9953,873,311 353,7981,234,9702,157,9033,144,9563,691,712391,8421,367,7652,389,9413,483,130469,6481,639,3552,864,498390,5611,363,294344,014拟合增量赔款270,061672,617704,494753,438417,350292,571 376,125936,779981,1761,049,342581,260407,474 372,325927,316971,2641,038,741575,388403,358 366,724913,365956,6521,023,114566,731397,290 336,287837,559877,254938,200519,695364,316 353,798881,172922,933987,053546,756391,842975,9231,022,1751,093,189469,6481,169,7071,225,143390,561972,733344,014计算残差:使用书中介绍的Pearson残差,r表示残差,C表示真实增量赔款,m表示拟合增量赔款(r=(C-m)/m^0.5)Pearson残差168.93115.01-111.94-311.63170.23521.04-39.14-54.51-47.73130.76-177.75-135.47-134.0977.35-45.71-21.67231.27-403.77-92.67203.92-184.51533.16-390.87-71.77184.29-157.75122.49-174.18-20.59176.1571.1759.56-78.52-183.21215.3178.26-129.87108.03-28.62-160.76-99.91197.16-22.2014.07-对Person残差有放回的抽样,第一步生成1到总数的随机数,第二步找到该随机数对应的行和列,第三步,找到对应的数NUM202146465051495523361295555492734541214463323324438483321492135253712341441474814395052ROW66101010101010781810101078105510878991086106879585910101941010COLUMN561156410281110104669241524823564674126452317357残差抽样-20.59176.15168.93168.93170.23521.04 -311.63-0.00203.9258.77--134.09-0.00-0.00-311.63-71.77-403.77-86.9159.56-183.21168.93231.27203.92-21.6725.11-54.51-111.94231.27176.15-311.63176.15207.21533.16-39.1459.56-403.77-183.21-177.75115.01-111.94-252.02108.03170.23-235.52用抽样所得残差与拟合赔款数据,得到抽样的增量赔款以及抽样的累计赔款。

bootstrapping中标准差计算

登录后才能查看或发表评论立即登录或者逛逛博客园首页

bootstrapping中 标 准 差 计 算

根据文献,我需要的bootstrapping标准差为

d(t)是我的原始叠加结果,b(t)是第i次bootstrapping的结果。 而Matlab中std函数提供的标准差:

所以直接采用std计算bootstrapping的标准差是不行的 所以写了一个bootstrapping的标准差的脚本:

t_e] = boot_error(b_data,d) %calculate standard error for bootstrapping data % b_data is a matrix, each sampling result is arranged in column. % b_data 是一个矩阵,每一个抽样结果按列排列。 % d is the observing data. boot_num=size(b_data,2); d_copy=repmat(d,[1,boot_num]); diff2=(d_copy-b_data).^2; Numerator_tmp=sum(diff2,2,'omitnan'); boot_num_real=sum(~isnan(b_data), 2); denominator=boot_num_real.*(boot_num_real-1); boot_e=sqrt(Numerator_tmp./denominator); end

matlabbootstrapping算法

matlabbootstrapping算法

Matlab蒙特卡罗(Bootstrap)算法介绍

1. 什么是Matlab蒙特卡罗(Bootstrap)算法?

Matlab蒙特卡罗(Bootstrap)算法是一种经典的机器学习方法,它可以通过模拟人们使用蒙特卡罗法的计算方式,来从输入数据中提取有用的参数。

这种方法通常被用于有限规模的机器学习问题,并且由于反复使用既有数据集和计算法则,因此

可以在相当小的计算和空间中获得很多信息。

2. Matlab蒙特卡罗(Bootstrap)算法的工作原理

Matlab蒙特卡罗(Bootstrap)算法的工作原理是很简单的,它的基本步骤是:首先,系统从输入数据中随机采样样本数据,注意,这里采样的是最大可能量;然后,按照用户指定的规则,利用采样出来的数据构建模型;最后,根据构建出来的模型,对新输入数据进行分析,从而获得输出数据。

3. Matlab蒙特卡罗(Bootstrap)算法的优势

4. Matlab蒙特卡罗(Bootstrap)算法的应用

Matlab蒙特卡罗(Bootstrap)算法可用于多种机器学习问题,例如文本分类、图像分类、语音识别、数据挖掘等。

这一算法的处理者应用,能够有效的解决复杂的机器学习问题,并减少大量的计算成本。

综上所述,Matlab蒙特卡罗(Bootstrap)算法是一种有效且简单易操作的机器学习方法,它能够有效地从输入数据中提取有用的参数并用于模型的构建,从而实现精准的分析结果,并有效的解决复杂的机器学习问题。

因此, Matlab蒙特卡罗(Bootstrap)算法在机器学习领域非常强大,具有广泛的应用前景。

拔靴法,自助法

拔靴法的基本原理及应用一、拔靴法的由来1977年美国斯坦福大学统计学教授Efron提出Bootstrapping 方法。

Bootstrapping的名字来源于英文短语“to pull oneself up by one’s bootstrap”中文翻译是“靠自己的力量振作起来”。

引用到中国后有两个中文名字,既叫“拔靴法”,又叫“自助法”。

二、拔靴法的基本原理及应用例:有一款研发的新药可以治疗某一种疾病。

我们想要知道这款新药对治疗疾病是否有效。

于是我们找来8个病人,让他们8个病人吃下这种新药,来测验这个新药是否对这种疾病有效。

数轴0点代表病人吃药后身体状态没好也没坏,跟不吃药没什么区别。

数轴负值表示病人吃药后身体状态变坏,数轴负值表示病人吃药后身体状态变好。

圆点代表8个病人吃药后的身体状态,其中有3个人吃药后身体变坏(-3.2,-2.8,-1.8),5个人吃药后身体变好(1.7,2,2.1,2.8,3.2)。

有的病人吃药后身体状态变好,有的病人吃药后身体状态变坏,那么这个新药到底对疾病有没有效果呢?我们可以计算一下8个病人吃药后身体状态的平均值M。

均值M=(-3.2-2.8-1.8+1.7+2.2.1+2.8+3.2)÷ 8=0.58个病人吃药后身体状态的均值为0.5。

我们由此可以得出新药物对疾病的效果就是0.5吗?当然不能!因为我们无法控制随机事件。

吃药后身体变好的5个病人,可能他们一开始身体就更健康,这是一个随机事件。

吃药后身体变坏的3个病人,可能他们的生活方式不健康,这又是一个随机事件。

单单通过这8个人的测验,我们无法确定是因为新药导致了他们身体的变化,还是因为随机事件导致了他们身体的变化。

如何解决这个问题呢?通常的做法就是进行费时费力费钱的多次重复测验。

我们做第1次测验时,8个病人身体状态的均值为0.5。

我们找另外8个病人重复第1次的测验,做第2次测验。

注意,样本抽样为不重复抽样,也就是说,我们第2次测验找的这8个病人,不能包含第1次测验的8个病人。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

A quick view of bootstrap (cont)

• It has minimum assumptions. It is merely based on the assumption that the sample is a good representation of the unknown population.

• Bootstrap distributions usually approximate the shape, spread, and bias of the actual sampling distribution.

• Bootstrap distributions are centered at the value of the statistic from the original data plus any bias, while the sampling distribution is centered at the value of the parameter in the population, plus any bias.

Cases where bootstrap does not apply

• Small data sets: the original sample is not a good approximation of the population • Dirty data: outliers add variability in our estimates. • Dependence structures (e.g., time series, spatial problems): Bootstrap is based on the assumption of independence.

How many bootstrap samples are needed?

Choice of B depends on • Computer availability • Type of the problem: standard errors, confidence intervals, …

• Complexity of the problem

Why resampling?

• Fewer assumptions

– Ex: resampling methods do not require that distributions be Normal or that sample sizes be large

• Greater accuracy: Permutation tests and come bootstrap methods are more accurate in practice than classical methods • Generality: Resampling methods are remarkably similar for a wide range of statistics and do not require new formulas for every statististic.

A quick view of bootstrapping

• Introduced by Bradley Efron in 1979 • Named from the phrase “to pull oneself up by one’s bootstraps”, which is widely believed to come from “the Adventures of Baron Munchausen”.

• Promote understanding: Boostrap procedures build intuition by providing concrete analogies to theoretical concepts.

Bootstrap distribution

• The bootstrap does not replace or add to the original data. • We use bootstrap distribution as a way to estimate the variation in a statistic based on the original data.

Bootstrapping

LING 572 Fei Xia 1/31/06

Outline

• Basic concepts • Case study

Motivation

• What’s the average price of house prices?

• From F, get a sample x=(x1, x2, …, xn), and calculate the average u.

Now we end up with bootstrap values

* * ˆ ˆ ˆ * (1 ,..., B )

• Use these values for calculating alll the quantities of interest (e.g., standard deviation, coຫໍສະໝຸດ fidence intervals)

An example

X1=(1.57,0.22,19.67, 0,0,2.2,3.12) Mean=4.13 X=(3.12, 0, 1.57, 19.67, 0.22, 2.20) Mean=4.46

X2=(0, 2.20, 2.20, 2.20, 19.67, 1.57) Mean=4.64 X3=(0.22, 3.12,1.57, 3.12, 2.20, 0.22) Mean=1.74

• In practice, it is computationally demanding, but the progress on computer speed makes it easily available in everyday practice.

• The population population distribution (unknown) • Original sample sampling distribution ? • Resamples bootstrap distribution

• Question: how reliable is u? What’s the standard error of u? what’s the confidence interval?

Solutions

• One possibility: get several samples from F. • Problem: it is impossible (or too expensive) to get multiple samples.

• Popularized in 1980s due to the introduction of computers in statistical practice.

• It has a strong mathematical background. • While it is a method for improving estimators, it is well known as a method for estimating standard errors, bias, and constructing confidence intervals for parameters.

Further reading

• SPlus: /splus

Case study

Additional slides

Resampling methods

• Boostrap • Permutation tests • Jackknife: we ignore one observation at each time • …

• Solution: bootstrapping

Procedure for bootstrapping

Let the original sample be x=(x1,x2,…,xn) • Repeat B times

– Generate a sample x* of size n from x by sampling with replacement. ˆ * for x*. – Compute