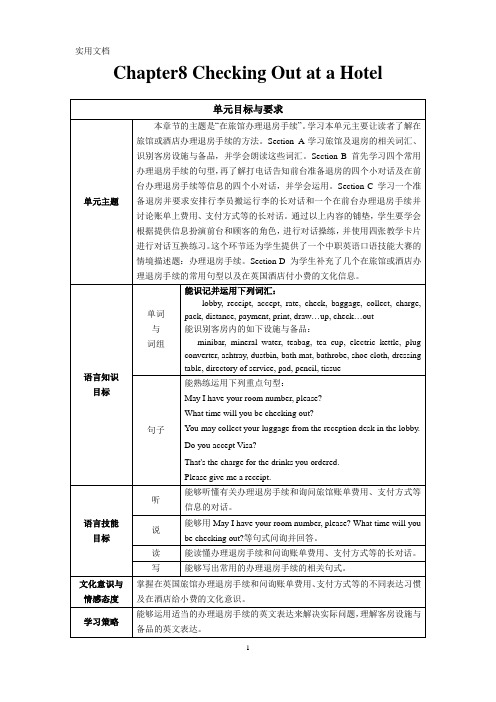

chapter8-全

英语实用口语Chapter-8-Checking-Out-at-a-Hotel--教学设计

Chapter8 Checking Out at a Hotel备注:本次教学设计打破以往的step by step的师生对话式的设计。

我们的设计提供多种选择性的活动设计,最大限度地提供给不同的教师、不同的学生选择性使用适合于你自己教学方式和学生的那种活动。

教学目的:这部分的教学目的是学习与主题相关的词汇。

通过单元词汇客房内设施与备品名称导入与学习,为整个单元的学习活动作必要的语言积累和准备。

使学生初步了解办理退房手续的常用词汇及相关客房设施与备品的英文名称,同时也为完成本单元的任务做了词汇上的准备。

Section A课时分配建议:1个课时。

Warming Up1A Match and say. 根据所给的图片和单词,配对并说出相应的名称。

【教学建议】教师与学生Free talk:Look! Where is Li Ming? 教师通过李明在Princess Hotel的照片,让学生猜猜图片中的李明在哪里,打算做什么。

当学生提到check out时,教师可随即表述:Li Ming is leaving for a new scenic spot. Now he is going to check out, too. 将话题引导到在旅馆办理退房手续的话题。

Step1: Individual activity. Students go through the pictures and know the meaning of each picture.【教学建议】教师提问:“What’s this?”或“What can you see in the picture / video?”,学生说出每张图片中涉及的办理退房手续时有关物品的英文名称,教师选择几组进行检查并给出反馈。

Step2: Individual activity. Students read the words (lobby, room number, receipt, reception desk), and match the words with pictures.【说明】本活动的目的是提供办理退房手续相关词汇,导入话题。

8-国民经济账户体系

Chapter 8 国民经济账户体系

28

SNA的账户设置

序号 国民经济总体

机构部门 国外(V)

0 货物和服务账户 ——

I

生产账户

货物和服务账户

II

收入分配和使用账户

初始收入和经常 转移账户

III

积累账户

积累账户

IV

资产负债表

资产负债表

Chapter 8 国民经济账户体系

29

I. 生产账户

I.1

生产账户

21.Earn from

67 18.Payoff to

22.borrowing

56 19.lending

total

663 total

credit 499 95 69 663

❖ 以上构成一个小型的国民经济账户体系。

❖ 国民经济账户不仅具备收付式平衡表的一般特点, 还具有下面的优点:表内总计平衡,表外借贷对 应,数据相互验证,便于观察分析。

18

(二)账户中的平衡项

❖ 交易账户的平衡项大多出现在左边; ❖ 资产负债账户,平衡项是净值,出现在账户右边; ❖ 积累账户中的非交易账户,平衡项为净值的变化,

出现在账户右边。

Chapter 8 国民经济账户体系

19

(二)账户中的平衡项

❖ 平衡项在账户形式上的作用 ▪ 使单个账户得以平衡 ▪ 使相邻账户得以连接

16

账户两方的术语

❖对于增加一个部门之经济价值的交易,SNA 采用 来源(resources)这样的术语。例如,工资与薪金 是其接受单位或部门的来源。按照惯例,来源放在 经常账户的右方。

❖ 账户的左方被称为使用(uses),使用是指减少一个 部门之经济价值的交易。仍以工资与薪金为例,对 于支付的单位或部门而言,它们是使用。

chapter-8高速CMOS逻辑电路设计---副本剖析

内部寄生电容

8.3 逻辑努力

反相器延时的计算

S(>1)倍对称反相器的延迟时间

R Rref S

Cin SCref

C p SC p ,ref

绝对延时

d abs kR(C p Cout ) kRref C p ,ref

相对延时

(h p)

d abs

加前级门的负载电容,导致恶性循环。必须采用

特别的电路设计来解决这个问题。

问题:

如何使反相

器链的总延

时最小?

8.2 驱动大电容

负载优化条件

第一级是标准尺寸反相器,输入电容为C1,FET 电阻为

R1,FET互导为β1,各级单调放大,即有

1 2 3 N 1 N

j R j C j 1

N

N 1

j 1

j 1

N级反相器链的总延时 d j R j C j 1 RN C L

N级反相器链的负载电容 C L C N 1 S N C1

代入尺寸放大关系

R1

j

•

S

C1

R j C j 1 S j 1

N

N

j 1

CGn (2 r )

1 r

g NAND 2

C

ref

Cin CGn (n r )

nr

一倍对称NANDn

CGn (n r )

1 r

g NAND 2

C

ref

n个输入

NOR

每个nFET的尺寸

1个pFET的尺寸

Cin CGn (1 2r )

跨文化商务交际Chapter_8_Intercultural_Management

What is intercultural management?

跨文化管理真正作为一门科学,是在20世纪70年代后 期的美国逐步形成和发展起来的。它研究的是在跨文化 条件下如何克服异质文化的冲突,进行卓有成效的管理, 其目的在于如何在不同形态的文化氛围中设计出切实可 行的组织结构和管理机制,最合理地配置企业资源,特 别是最大限度地挖掘和利用企业人力资源的潜力和价值, 从而最大化地提高企业的综合效益。 兴起这一研究的直接原因是二战后美国跨国公司进行 跨国经营时的屡屡受挫。

企业文化中一些典型的可观察到的要素

典礼和仪式 典故 象征物

语言

Some tips about Corporate culture

A company’s culture is greatly influenced b team as they set the policies and practices for the organization. Many articles and books have been written in recent years about culture in organizations, usually referred to as “corporate culture”. Every organization has its own unique culture or value set. To be specific, corporate culture can be looked as a system. Often the people who see an organization’s culture more clearly are those from the outside, the new comers, or the consultants.

Chapter 8 科技英语隐含的因果关系

8.3 包含定语从句的主从复合句表示因果关系

1 To make a bomb, we have to use uranium 235, in which all the atoms are available for fission. 制作原子弹,必须使用铀235,因为它的所有原子 都可以裂变。 2 We cannot live on Mars, where there is no air and water. 我们不能在火星上生存,因为那里没有空气,也 没有水。

8.1 形容词短语、分词短语、分词独立结构说 明原因(或条件)

1 Cold and drought tolerant, the new variety is adaptable to north China. 这种新品种耐寒耐旱,适合于在中国北方生长。 2 Free from the attack of moisture, a piece of iron does not rust as fast as we would expect. 如不受潮,铁块锈蚀的速度就不会像我们想象的那样快。 3 Neutrons, having no charge, are repelled neither by the electron cloud surrounding the nucleus nor by the nucleus itself. 中子(由于)不带电,所以既不受原子核周围的电子云也不受原子核本身的排 斥。 4 The moon having no atmosphere, there can be no wind nor, of course, can there be any noise, for sound is carried by the air. 因为月球上没有大气层,又没有风,当然也没有什么声响,因为声音是靠空气 传播的。 5 Some alloying elements ( such as chromium and tungsten) make the grain of steel finer, thus increasing the hardness and strength of steel. 有些合金元素(如铬和钨)能细化钢的晶粒,从而增加钢的硬度和强度。 6 A fusion reaction is going on in the sun to produce almost limitless energy. 太阳内部正在进行着核聚变反应,因而产生几乎无穷无尽的能量。

(完整版)财务管理CHAPTER8

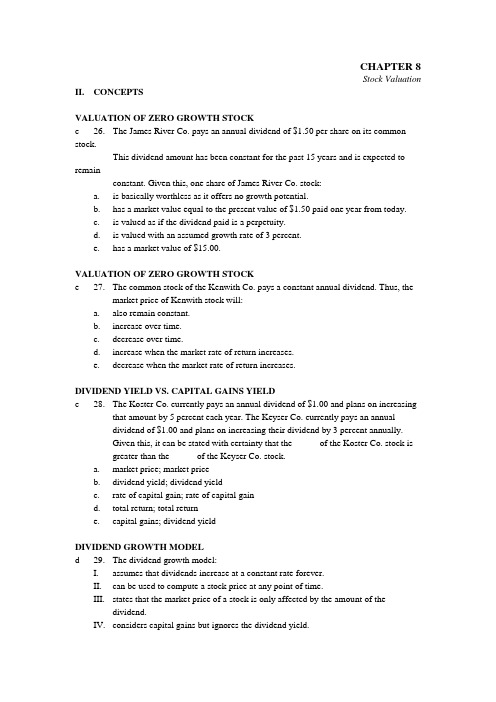

CHAPTER 8Stock Valuation II. CONCEPTSVALUATION OF ZERO GROWTH STOCKc 26. The James River Co. pays an annual dividend of $1.50 per share on its common stock.This dividend amount has been constant for the past 15 years and is expected to remainconstant. Given this, one share of James River Co. stock:a. is basically worthless as it offers no growth potential.b. has a market value equal to the present value of $1.50 paid one year from today.c. is valued as if the dividend paid is a perpetuity.d. is valued with an assumed growth rate of 3 percent.e. has a market value of $15.00.VALUATION OF ZERO GROWTH STOCKe 27. The common stock of the Kenwith Co. pays a constant annual dividend. Thus, themarket price of Kenwith stock will:a. also remain constant.b. increase over time.c. decrease over time.d. increase when the market rate of return increases.e. decrease when the market rate of return increases.DIVIDEND YIELD VS. CAPITAL GAINS YIELDc 28. The Koster Co. currently pays an annual dividend of $1.00 and plans on increasingthat amount by 5 percent each year. The Keyser Co. currently pays an annualdividend of $1.00 and plans on increasing their dividend by 3 percent annually.Given this, it can be stated with certainty that the _____ of the Koster Co. stock isgreater than the _____ of the Keyser Co. stock.a. market price; market priceb. dividend yield; dividend yieldc. rate of capital gain; rate of capital gaind. total return; total returne. capital gains; dividend yieldDIVIDEND GROWTH MODELd 29. The dividend growth model:I. assumes that dividends increase at a constant rate forever.II. can be used to compute a stock price at any point of time.III. states that the market price of a stock is only affected by the amount of the dividend.IV. considers capital gains but ignores the dividend yield.a. I onlyb. II onlyc. IIIand IV onlyd. I and II onlye. I, II, and III onlyDIVIDEND GROWTH MODELb 30. The underlying assumption of the dividend growth model is that a stock is worth:a. the same amount to every investor regardless of their desired rate of return.b. the present value of the future income which the stock generates.c. an amount computed as the next annual dividend divided by the market rate ofreturn.d. the same amount as any other stock that pays the same current dividend and has thesame required rate of return.e. an amount computed as the next annual dividend divided by the required rate ofreturn.DIVIDEND GROWTH MODELc 31. Assume that you are using the dividend growth model to value stocks. If you expectthe market rate of return to increase across the board on all equity securities, thenyou should also expect the:a. market values of all stocks to increase, all else constant.b. market values of all stocks to remain constant as the dividend growth will offset theincrease in the market rate.c. market values of all stocks to decrease, all else constant.d. stocks that do not pay dividends to decrease in price while the dividend-payingstocks maintain a constant price.e. dividend growth rates to increase to offset this change.NONCONSTANT GROWTHc 32. Latcher’s Inc. is a relatively new firm that is still in a period of rapid development. Thecompany plans on retaining all of its earnings for the next six years. Seven years fromnow, the company projects paying an annual dividend of $.25 a share and thenincreasing that amount by 3 percent annually thereafter. To value this stock as oftoday, you would most likely determine the value of the stock _____ years fromtoday before determining today’s value.a. 4b. 5c. 6d. 7e. 8NONCONSTANT GROWTHd 33. The Robert Phillips Co. currently pays no dividend. The company is anticipatingdividends of $0, $0, $0, $.10, $.20, and $.30 over the next 6 years, respectively. Afterthat, the company anticipates increasing the dividend by 4 percent annually. The firststep in computing the value of this stock today, is to compute the value of the stock inyear:a. 3.b. 4.c. 5.d. 6.e. 7.SUPERNORMAL GROWTHb 34. Supernormal growth refers to a firm that increases its dividend by:a. three or more percent per year.b. a rate which is most likely not sustainable over an extended period of time.c. a constant rate of 2 or more percent per year.d. $.10 or more per year.e. an amount in excess of $.10 a year.DIVIDEND YIELD AND CAPITAL GAINSe 35. The total rate of return earned on a stock is comprised of which two of thefollowing?I. current yieldII. yield to maturityIII. dividend yieldIV. capital gains yielda. I and II onlyb. I and IV onlyc. II and III onlyd. II and IV onlye. IIIand IV onlyDIVIDEND YIELDc 36. The total rate of return on a stock can be positive even when the price of the stockdepreciates because of the:a. capital appreciation.b. interest yield.c. dividend yield.d. supernormal growth.e. real rate of return.DIVIDEND YIELD AND CAPITAL GAINSc 37. Fred Flintlock wants to earn a total of 10 percent on his investments. He recentlypurchased shares of ABC stock at a price of $20 a share. The stock pays a $1 a yeardividend. The price of ABC stock needs to _____ if Fred is to achieve his 10percent rate of return.a. remain constantb. decrease by 5 percentc. increase by 5 percentd. increase by 10 percente. increase by 15 percentDIVIDEND GROWTH MODELd 38. Which one of the following correctly defines the dividend growth model?a. P0 = D0 (R-g)b. D = P0⨯ (R-g)c. R = (P0÷ D0) + gd. R = (D1÷ P0) + ge. P0 = (D1÷ R) + gSHAREHOLDER RIGHTSa 39. Shareholders generally have the right to:I. elect the corporate directors.II. select the senior management of the firm.III. elect the chief executive officer (CEO).IV. elect the chief operating officer (COO).a. I onlyb. I and III onlyc. II onlyd. I and II onlye. IIIand IV onlyCUMULATIVE VOTINGc 40. Jack owns 35 shares of stock in Beta, Inc. and wants to exercise as much control aspossible over the company. Beta, Inc. has a total of 100 shares of stock outstanding.Each share receives one vote. Presently, the company is voting to elect two newdirectors. Which one of the following statements must be true given thisinformation?a. If straight voting applies, Jack is assured one seat on the board.b. If straight voting applies, Jack can control both open seats.c. If cumulative voting applies, Jack is assured one seat on the board.d. If cumulative voting applies, Jack can control both open seats.e. Regardless of the type of voting employed, Jack does not own enough shares tocontrol any of the seats.STRAIGHT VOTINGa 41. ABC Co. is owned by a group of shareholders who all vote independently and whoall want personal control over the firm. If straight voting is utilized, a shareholder:a. must either own enough shares to totally control the elections or else he/she has nocontrol whatsoever.b. will be able to elect at least one director as long as there are at least three openpositions and the shareholder owns at least 25 percent plus one of the outstandingshares.c. must own at least two-thirds of the shares, plus one, to exercise control over theelections.d. is only permitted to elect one director, regardless of the number of shares owned.e. who owns more shares than anyone else, regardless of the number of shares owned,will control the elections.PROXY VOTINGe 42. The Zilo Corp. has 1,000 shareholders and is preparing to elect three new boardmembers. You do not own enough shares to control the elections but aredetermined to oust the current leadership. The most likely result of this situation isa:a. negotiated settlement where you are granted control over one of the three openpositions.b. legal battle for control of the firm based on your discontent as an individualshareholder.c. arbitrated settlement whereby you are granted control over one of the three openpositions.d. total loss of power for you since you are a minority shareholder.e. proxy fight for control of the firm.SHAREHOLDER RIGHTSe 43. Common stock shareholders are generally granted rights which include the right to:I. share in company profits.II. vote for company directors.III. vote on proposed mergers.IV. residual assets in a liquidation.a. I and II onlyb. II and III onlyc. I and IV onlyd. I, II, and IV onlye. I, II, III, and IVDIVIDENDSe 44. The Scott Co. has a general dividend policy whereby they pay a constant annualdividend of $1 per share of common stock. The firm has 1,000 shares of stockoutstanding. The company:a. must always show a current liability of $1,000 for dividends payable.b. is obligated to continue paying $1 per share per year.c. will be declared in default and can face bankruptcy if they do not pay $1 per year toeach shareholder on a timely basis.d. has a liability which must be paid at a later date should the company miss paying anannual dividend payment.e. must still declare each dividend before it becomes an actual company liability.DIVIDENDSb 45. The dividends paid by a corporation:I. to an individual become taxable income of that individual.II. reduce the taxable income of the corporation.III. are declared by the chief financial officer of the corporation.IV. to another corporation may or may not represent taxable income to the recipient.a. I onlyb. I and IV onlyc. II and III onlyd. I, II, and IV onlye. I, III, and IV onlyPREFERRED STOCKa 46. The owner of preferred stock:a. is entitled to a distribution of income prior to the common shareholders.b. has the right to veto the outcome of an election held by the common shareholders.c. has the right to declare the company bankrupt whenever there are insufficient funds topay dividends to the common shareholders.d. receives tax-free dividends if they are an individual and own more than 20 percent ofthe outstanding preferred shares.e. has the right to collect payment on any unpaid dividends as long as the stock isnoncumulative preferred.PREFERRED STOCKb 47. A 6 percent preferred stock pays _____ a year in dividends per share.a. $3b. $6c. $12d. $30e. $60PREFERRED STOCKe 48. Which one of the following statements concerning preferred stock is correct?a. Unpaid preferred dividends are a liability of the firm.b. Preferred dividends must be paid quarterly provided the firm has net income thatexceeds the amount of the quarterly dividend.c. Preferred dividends must be paid timely each quarter or the unpaid dividends startaccruing interest.d. All unpaid dividends on preferred stock, regardless of the type of preferred, must bepaid before any income can be distributed to common shareholders.e. Preferred shareholders may be granted voting rights and seats on the board ifpreferred dividend payments remain unpaid.PREFERRED STOCKe 49. In a liquidation, each share of 5 percent preferred stock is generally entitled to aliquidation payment of _____ as long as there are sufficient funds available.a. $1b. $5c. $10d. $50e. $100QUARTERLY INCOME PREFERRED SECURITIESb 50. Quarterly income preferred securities distribute payments to investors which are:I. taxed like interest income for tax purposes if the income recipient is an individual.II. excluded from the taxable income of any individual recipient.III. distributed from the after-tax income of the corporation.IV. tax deductible to the corporation.a. I and III onlyb. I and IV onlyc. II and III onlyd. II and IV onlye. II onlyPRIMARY MARKETd 51. Which one of the following transactions occurs in the primary market?a. the sale of ABC stock by Fred Jones to Mary Smithb. the tax-free gift of DEF stock to Heather by Jenniferc. the repurchase of GHI stock from Tim by GHId. the initial sale of JKL stock by JKL to Jamiee. the transfer of MNO stock from Tom to his son, JonDEALERS AND BROKERSd 52. Which one of the following statements concerning dealers and brokers is correct?a. A dealer in market securities arranges sales between buyers and sellers for a fee.b. A dealer in market securities pays the asked price when purchasing securities.c. A broker in market securities earns income in the form of a bid-ask spread.d. A broker does not take ownership of the securities being traded.e. A broker deals solely in the primary market.NEW YORK STOCK EXHANGEa 53. Technically, the actual owners of the New York Stock Exchange are its:a. members.b. specialists.c. dealers.d. floor brokers.e. commission brokers.FLOOR BROKERSd 54. Which one of the following players on the floor of the New York Stock Exchange canbe likened to part-time help in that they are called to duty only when others are fullyemployed?a. floor traderb. specialistc. dealerd. floor brokere. commission brokerSPECIALIST’S POSTb 55. The post is a stationary position on the floor of the New York Stock Exchangewhere a _____ is assigned to work.a. floor traderb. specialistc. dealerd. floor brokere. commission brokerSTOCK MARKET REPORTINGd 56. The closing price of a stock is quoted at 22.87, with a P/E of 26 and a net change of1.42. Based on this information, which one of the following statements is correct?a. The closing price on the previous day was $1.42 higher than today’s closing price.b. A dealer will buy the stock at $22.87 and sell it at $26 a share.c. The stock increased in value between yesterday’s close and today’s close by$.0142.d. The earnings per share are equal to 1/26th of $22.87.e. The earnings per share have increased by $1.42 this year.STOCK QUOTEb 57. A stock listing contains the following information: P/E 17.5, closing price 33.10,dividend .80, YTD % chg 3.4, and a net chg of -.50. Which of the following statementsare correct given this information?I. The stock price has increased by 3.4 percent during the current year.II. The closing price on the previous trading day was $32.60.III. The earnings per share are approximately $1.89.IV. The current yield is 17.5 percent.a. I and II onlyb. I and III onlyc. II and III onlyd. IIIand IV onlye. I, III, and IV onlyIII. PROBLEMSSTOCK VALUEd 58. Michael’s, Inc. just paid $1.40 to their shareholders as the annual dividend.Simultaneously, the company announced that future dividends will be increasing by4.5 percent. If you require an 8 percent rate of return, how much are you willing topay to purchase one share of Michael’s stock?a. $31.11b. $32.51c. $40.00d. $41.80e. $43.68STOCK VALUEe 59. Angelina’s made two announcements concerning their common stock today. First, thecompany announced that their next annual dividend has been set at $2.16 a share.Secondly, the company announced that all future dividends will increase by 4 percentannually. What is the maximum amount you should pay to purchase a share ofAngelina’s stock if your goal is to earn a 10 percent rate of return?a. $21.60b. $22.46c. $27.44d. $34.62e. $36.00STOCK VALUEd 60. How much are you willing to pay for one share of stock if the company just paid an$.80 annual dividend, the dividends increase by 4 percent annually and you require an8 percent rate of return?a. $19.23b. $20.00c. $20.40d. $20.80e. $21.63STOCK VALUEd 61. Lee Hong Imports paid a $1.00 per share annual dividend last week. Dividends areexpected to increase by 5 percent annually. What is one share of this stock worth toyou today if the appropriate discount rate is 14 percent?a. $7.14b. $7.50c. $11.11d. $11.67e. $12.25STOCK VALUEc 62. Majestic Homes stock traditionally provides an 8 percent rate of return. The companyjust paid a $2 a year dividend which is expected to increase by 5 percent per year. Ifyou are planning on buying 1,000 shares of this stock next year, how much should youexpect to pay per share if the market rate of return for this type of security is 9 percentat the time of your purchase?a. $48.60b. $52.50c. $55.13d. $57.89e. $70.00STOCK VALUEc 63. Leslie’s Unique Clothing Stores offers a common stock that pays an annual dividendof $2.00 a share. The company has promised to maintain a constant dividend. Howmuch are you willing to pay for one share of this stock if you want to earn 12 percentreturn on your equity investments?a. $10.00b. $13.33c. $16.67d. $18.88e. $20.00STOCK VALUEb 64. Martin’s Yachts has paid annual dividends of $1.40, $1.75, and $2.00 a share over thepast three years, respectively. The company now predicts that it will maintain aconstant dividend since its business has leveled off and sales are expected to remainrelatively constant. Given the lack of future growth, you will only buy this stock if youcan earn at least a 15 percent rate of return. What is the maximum amount you arewilling to pay to buy one share of this stock today?a. $10.00b. $13.33c. $16.67d. $18.88e. $20.00REQUIRED RETURNc 65. The common stock of Eddie’s Engines, Inc. sells for $25.71 a share. The stock isexpected to pay $1.80 per share next month when the annual dividend is distributed.Eddie’s has established a pattern of incr easing their dividends by 4 percent annuallyand expects to continue doing so. What is the market rate of return on this stock?a. 7 percentb. 9 percentc. 11 percentd. 13 percente. 15 percentREQUIRED RETURNa 66. The current yield on Alpha’s common stock is 4.8 percent. The company just paid a$2.10 dividend. The rumor is that the dividend will be $2.205 next year. The dividendgrowth rate is expected to remain constant at the current level. What is the requiredrate of return on Alpha’s stock?a. 10.04 percentb. 16.07 percentc. 21.88 percentd. 43.75 percente. 45.94 percentREQUIRED RETURNe 67. Martha’s Vineyardrecently paid a $3.60 annual dividend on their common stock. Thisdividend increases at an average rate of 3.5 percent per year. The stock is currentlyselling for $62.10 a share. What is the market rate of return?a. 2.5 percentb. 3.5 percentc. 5.5 percentd. 6.0 percente. 9.5 percentREQUIRED RETURNd 68. Bet’R Bilt Bikes just announced that their annua l dividend for this coming year will be$2.42 a share and that all future dividends are expected to increase by 2.5 percent annually. What is the market rate of return if this stock is currently selling for $22 ashare?a. 9.5 percentb. 11.0 percentc. 12.5 percentd. 13.5 percente. 15.0 percentDIVIDEND YIELD VS. CAPITAL GAINS YIELDb 69. Shares of common stock of the Samson Co. offer an expected total return of 12percent. The dividend is increasing at a constant 8 percent per year. The dividendyield must be:a. - 4 percent.b. 4 percent.c. 8 percent.d. 12 percent.e. 20 percent.CAPITAL GAINc 70. The common stock of Grady Co. returned an 11.25 percent rate of return last year.The dividend amount was $.70 a share which equated to a dividend yield of 1.5percent. What was the rate of price appreciation on the stock?a. 1.50 percentb. 8.00 percentc. 9.75 percentd. 11.25 percente. 12.75 percentDIVIDEND AMOUNTb 71. Weisbro and Sons common stock sells for $21 a share and pays an annual dividendthat increases by 5 percent annually. The market rate of return on this stock is 9 percent. What is the amount of the last dividend paid by Weisbro and Sons?a. $.77b. $.80c. $.84d. $.87e. $.88DIVIDEND AMOUNTd 72. The common stock of Energizer’s pays an annual dividend that is expected to increaseby 10 percent annually. The stock commands a market rate of return of 12 percent andsells for $60.50 a share. What is the expected amount of the next dividend to be paidon Energizer’s common stock?a. $.90b. $1.00c. $1.10d. $1.21e. $1.33d 73. The Reading Co. has adopted a policy of increasing the annual dividend on theircommon stock at a constant rate of 3 percent annually. The last dividend they paidwas $0.90 a share. What will their dividend be in six years?a. $.90b. $.93c. $1.04d. $1.07e. $1.11e 74. A stock pays a constant annual dividend and sells for $31.11 a share. If the rate ofreturn on this stock is 9 percent, what is the dividend amount?a. $1.40b. $1.80c. $2.20d. $2.40e. $2.80CONSTANT DIVIDENDb 75. You have decided that you would like to own some shares of GH Corp. but need anexpected 12 percent rate of return to compensate for the perceived risk of suchownership. What is the maximum you are willing to spend per share to buy GHstock if the company pays a constant $3.50 annual dividend per share?a. $26.04b. $29.17c. $32.67d. $34.29e. $36.59GROWTH DIVIDENDe 76. Turnips and Parsley common stock sells for $39.86 a share at a market rate of return of9.5 percent. The company just paid their annual dividend of $1.20. What is the rate ofgrowth of their dividend?a. 5.2 percentb. 5.5 percentc. 5.9 percentd. 6.0 percente. 6.3 percentGROWTH DIVIDENDc 77. B&K Enterprises will pay an annual dividend of $2.08 a share on their common stocknext week. Last year, the company paid a dividend of $2.00 a share. The companyadheres to a constant rate of growth dividend policy. What will one share of B&Kcommon stock be worth ten years from now if the applicable discount rate is 8percent?a. $71.16b. $74.01c. $76.97d. $80.05e. $83.25GROWTH DIVIDENDd 78. Wilbert’s Clothing Stores just paid a $1.20 annual dividend. The company has a policywhereby the dividend increases by 2.5 percent annually. You would like to purchase100 shares of stock in this firm but realize that you will not have the funds to do so foranother three years. If you desire a 10 percent rate of return, how much should youexpect to pay for 100 shares when you can afford to buy this stock? Ignore tradingcosts.a. $1,640b. $1,681c. $1,723d. $1,766e. $1,810GROWTH DIVIDENDb 79. The Merriweather Co. just announced that they are increasing their annual dividend to$1.60 and establishing a policy whereby the dividend will increase by 3.5 percentannually thereafter. How much will one share of this stock be worth five years fromnow if the required rate of return is 12 percent?a. $21.60b. $22.36c. $23.14d. $23.95e. $24.79GROWTH DIVIDENDb 80. Shares of the Katydid Co. common stock are currently selling for $27.73. The lastdividend paid was $1.60 per share. The market rate of return is 10 percent. At whatrate is the dividend growing?a. 2.50 percentb. 4.00 percentc. 5.98 percentd. 13.05 percente. 14.91 percentSUPERNORMAL GROWTHc 81. The Bell Weather Co. is a new firm in a rapidly growing industry. The company isplanning on increasing its annual dividend by 20 percent a year for the next four yearsand then decreasing the growth rate to 5 percent per year. The company just paid itsannual dividend in the amount of $1.00 per share. What is the current value of oneshare of this stock if the required rate of return is 9.25 percent?a. $35.63b. $38.19c. $41.05d. $43.19e. $45.81SUPERNORMAL GROWTHc 82. The Extreme Reaches Corp. last paid a $1.50 per share annual dividend. Thecompany is planning on paying $3.00, $5.00, $7.50, and $10.00 a share over the nextfour years, respectively. After that the dividend will be a constant $2.50 per share peryear. What is the market price of this stock if the market rate of return is 15 percent?a. $17.04b. $22.39c. $26.57d. $29.08e. $33.71SUPERNORMAL GROWTHd 83. Can’t Hold Me Back, Inc. is preparing to pay their first dividends. They aregoing to pay $1.00, $2.50, and $5.00 a share over the next three years, respectively.After that, the company has stated that the annual dividend will be $1.25 per shareindefinitely. What is this stock worth to you per share if you demand a 7 percentrate of return?a. $7.20b. $14.48c. $18.88d. $21.78e. $25.06NONCONSTANT DIVIDENDSc 84. NU YU announced today that they will begin paying annual dividends. The firstdividend will be paid next year in the amount of $.25 a share. The following dividendswill be $.40, $.60, and $.75 a share annually for the following three years, respectively.After that, dividends are projected to increase by 3.5 percent per year. How much areyou willing to pay to buy one share of this stock if your desired rate of return is 12 percent?a. $1.45b. $5.80c. $7.25d. $9.06e. $10.58NONCONSTANT DIVIDENDSb 85. Now or Later, Inc. recently paid $1.10 as an annual dividend. Future dividends areprojected at $1.14, $1.18, $1.22, and $1.25 over the next four years, respectively.Beginning five years from now, the dividend is expected to increase by 2 percentannually. What is one share of this stock worth to you if you require an 8 percent rateof return on similar investments?a. $15.62b. $19.57c. $21.21d. $23.33e. $25.98NONCONSTANT DIVIDENDSb 86. The Red Bud Co. pays a constant dividend of $1.20 a share. The company announcedtoday that they will continue to do this for another 3 years after which time they willdiscontinue paying dividends permanently. What is one share of this stock worth todayif the required rate of return is 7 percent?a. $2.94b. $3.15c. $3.23d. $3.44e. $3.60NONCONSTANT DIVIDENDSb 87. Bill Bailey and Sons pays no dividend at the present time. The company plans to startpaying an annual dividend in the amount of $.30 a share for two years commencingtwo years from today. After that time, the company plans on paying a constant $1 ashare dividend indefinitely. How much are you willing to pay to buy a share of thisstock if your required return is 14 percent?a. $4.82b. $5.25c. $5.39d. $5.46e. $5.58NONCONSTANT DIVIDENDSa 88. The Lighthouse Co. is in a downsizing mode. The company paid a $2.50 annualdividend last year. The company has announced plans to lower the dividend by $.50 ayear. Once the dividend amount becomes zero, the company will cease all dividendspermanently. You place a required rate of return of 16 percent on this particular stockgiven the company’s situation. What is one share of this stock worth to you today?a. $3.76b. $4.08c. $4.87d. $5.13e. $5.39NONCONSTANT DIVIDENDS。

Chapter8-厦门大学-林子雨-大数据技术原理与应用-第八章-流计算

《大数据技术原理与应用》

厦门大学计算机科学系

林子雨

ziyulin@

8.1.3 流计算概念

• 流计算:实时获取来自不同数据源的海量数据,经过实时 分析处理,获得有价值的信息

数据采集

实时分析处理

结果反馈

《大数据技术原理与应用》

流计算示意图

厦门大学计算机科学系

林子雨

ziyulin@

《大数据技术原理与应用》

厦门大学计算机科学系

林子雨

ziyulin@

8.1.1 静态数据和流数据

• 近年来,在Web应用、网络监控、传感监测等领域,兴起了一种新 的数据密集型应用——流数据,即数据以大量、快速、时变的流形式 持续到达

• 流数据具有如下特征: – 数据快速持续到达,潜在大小也许是无穷无尽的 – 数据来源众多,格式复杂 – 数据量大,但是不十分关注存储,一旦经过处理,要么被丢弃, 要么被归档存储 – 注重数据的整体价值,不过分关注个别数据 – 数据顺序颠倒,或者不完整,系统无法控制将要处理据,包括用户的 搜索内容、用户的浏览记录等数据。采用流计算进行实时数据分析, 可以了解每个时刻的流量变化情况,甚至可以分析用户的实时浏览轨 迹,从而进行实时个性化内容推荐

• 但是,并不是每个应用场景都需要用到流计算的。流计算适合于需要 处理持续到达的流数据、对数据处理有较高实时性要求的场景

传统的数据处理流程示意图

• 传统的数据处理流程隐含了两个前提:

– 存储的数据是旧的。存储的静态数据是过去某一时刻的快照,这 些数据在查询时可能已不具备时效性了

– 需要用户主动发出查询来获取结果

《大数据技术原理与应用》

厦门大学计算机科学系

林子雨

ziyulin@

英语词汇学课件chapter-8-Meaning-and-Context

1) a sheet of paper (thin flat sheets of substance for writing, printing, decorating walls, etc.)

2) a white paper (government document)

3) a term paper (essay written at the end of the term)

(1) The fish is ready to eat. (2) I like Mary better than Jean.

8.2.2 Indication of Referents

English has a large number of deictic(指示的) words such as now/then, here/there, I/you, this/that, which are often used to refer directly to the personal, temporal or locational characteristics of the situation. Without clear context, the reference can be very confusing, e.g. now.

4) today’s paper (newspaper)

5) examination paper (a set of questions used as an examination)

2) Grammatical Context

In some cases, the meanings of a polysemant may be influenced by the structure in which it occurs. This is what we call grammatical context. Let us consider the verb become for example.

有机化学Chapter8(立体化学)

(Ⅰ) 旋转90º 后得(Ⅱ), (Ⅱ)作镜象得(Ⅲ), (Ⅲ)等于(Ⅰ) 有4重交替对称轴的分子

相同,但在空间的排列方式不同。

构象异构 顺反异构

CH3 H C C CH3 H

CH3 H C C H CH3

C异构:本章学习

8.1 手性和对映体 生活中的对映体 (1)-镜象

沙漠胡杨

生活中的 对映体(2) -镜象

左右手互为镜象

桂林风情

镜象与手性Chirality的概念

同分异构现象

碳链异构(如:丁烷/异丁烷) 构造异构 官能团异构(如:醚/醇) constitutional 位臵异构(如:辛醇/仲辛醇)

同分异构 isomerism

立体异构 Stereo-

构型异构 configurational 对映非对映异构 构象异构 conformational

顺反,Z、E异构

[α]λ =

t

α ρ l· B

式中t表示温度,λ表示所用光的波长。 若所测的旋光物质为纯液体,只要把ρB换成液体的密

度ρ即可。

比旋光度只决定于物质的结构。

各种化合物的比旋光度是它们各自特有的物理常数.

乳酸

CH3CHCOOH OH

*

右旋体

α ° [ ] 20 D = + 3.8

α ° ] 20 左旋体 [ D = - 3.8

构造异构,分子中原子互相联接的方式和次序

不同而产生的异构现象。

武理工《运输管理》教案第8章 全球运输

第8章全球运输Chapter8GlobalTransportation一、学习目标本章节主要介绍全球运输的有关情况,让学生对全球物流业的发展有大致的了解,为以后的学习和工作储备一定的知识,开阔眼界。

二、背景介绍本土主要介绍提供全球物流集成时物流经营要面临的困难和挑战。

目前全球物流业已经发展到了一个全新的高度,而国内综合物流水平难以与其匹配。

国内综合物流面想参与国际物流竞争,面临更加复杂活动需要更大的投入。

三、关键词全球运输模式、全球中介、四、具体内容知识点一:全球运输模式全球运输被定义为出口和进口产品或运输服务超出了国家的界限。

货物在美国、欧洲、南美、亚洲和太平洋地区海洋之间移动。

航空、管道、水路、铁路、公路运输均可被使用。

运输需要一定的基础设施如管道,公路,铁路,港口和机场。

全球海运海运承运人提供高密度、低价的产品。

水路运输大宗商品价格相对较低。

例如,运往美国东部大部分的铝土矿(铝矿石)是来自来澳大利亚,而不是从美国西部,虽然美国西部存在铝土矿。

海陆运输IOOOO英里铝土矿运费少于2。

英里铁路运输。

海运货物可以被分为四个不同的类别:干散货,液体散货、集装箱和杂件货。

干散货货物包括煤、谷物、铁矿石、糖、肥料、氧化铝、铝土矿。

液体散装货物包括石油、化工、和肥料。

海洋航空公司经营班轮或非定期船运输。

有效的使用组合或托盘化运输,统一化操作,加速装卸能够降低了运输成本。

世界各地的很多货运是在班轮公会的控制下运转。

这些公会限定船东航行特定的贸易路线,确定成员。

班轮公会是开放的,只要符合和遵守会议规则就能申请加入。

全球空运对于大多数国家,航空运输是海运之外的又一选择。

空运的运量少于水运的是。

空运适合高价值产品的运输。

全球空运由于巨大的运费差异是不可能明显削弱海洋货运市场份额。

全球多式联运海洋货物运输通常涉及联合运输如航空运输。

因为各种运输模式各有利弊,根据货物的性质相互补充,不能完全被任何其他方式替代。

多式联运被定义为两个或两个以上的运输方式结合运输。

Chapter-8

⇒ c2 = 0

WL 3 W 4 WL3 ∴ EIy = x − x − x 12 24 24

Max occurs @ x = L /2 Max.

EIymax ∆ max

5WL4 =− 384 5WL4 = 384 EI

Example

y

x

P x

L P M= x 2 2 2 d y P L EI 2 = x f 0< x< for dx 2 2 dy P x 2 = + c1 EI Integrating g g d dx 2 2 L dy Since the beam is symmetric @ x= =0 2 dx 2 ⎛L⎞ ⎜ PL2 L P ⎝2⎠ c1 = − EI (0 ) = @ x= + c1 ⇒ 16 2 2 2 for 0 < x <

y x PL P L

Examples

x P

M = − PL + Px

d2y EI 2 = − PL + Px @ x dx x2 dy EI = − PLx + P + c1 Integrating once dx 2 2 ( dy 0) = 0 ⇒ EI (0 ) = − PL(0) + P + c1 ⇒ c1 = 0 @ x = 0 dx 2 2 3 PL PLx x Integrating twice EIy = − + P + c2 2 6 3 ( PL 2 0) @ x = 0 y = 0 ⇒ EI (0 ) = − (0) + P + c2 ⇒ c2 = 0 2 6

P 3 PL2 ∴ EIy = x − x 12 16

Max occurs @ x = L /2 Max.

Chapter 8 - Emotions and Moods

• Intensity – people give different responses to identical emotionprovoking stimuli • Sometimes personality is responsible, other times, it is the result of job requirements • People vary in their ability to express emotional intensity. • Jobs make different demands on our emotions.

Aspects of Emotions

• Biology – all emotions originate in the brain’s limbic system near the brain stem. • People tend to be happy or the happiest when the limbic system is inactive • When the limbic system is activated, negative emotions dominate • Not everyone’s limbic system is the same. Depressed people have more active limbic systems • Women tend to have more active limbic systems than men

• Affect – a broad range of feelings that people experience • Emotions – intense feelings that are directed at something or someone • Mood – feelings that tend to be less intense than emotions that often lasts longer than emotions

商务英语第二版 王关富 课文翻译-Chapter8

财富:如何改变苹果乔布斯的十年北京时间11月5日《财富》文章指出,专横但又极富才华的乔布斯是如何改变苹果的呢?这是一段扣人心弦的创业故事:年轻的乔布斯在上个世纪八十年代一手创立了苹果,九十年代回归,在随后的十年里,他在鬼门关前转了两圈,也曾陷入违反证券法的丑闻,但是他领导苹果开发的一系列产品一直到今天还很畅销,他经常作出的一些令人不愉快的行为成为四个不同行业的主流个性,数次荣登亿万富豪榜,长期担任硅谷最有价值公司的掌门人.这听起来是不是有点象天方夜谭? 也许吧.但是这却是史蒂夫乔布斯的真实经历,他对他接触到的任何事物都产生了巨大的影响.商业界过去的十年是属于乔布斯的.就在一年之前,任何关于他的生平介绍的文章似乎都带着一丝告别的意味. 但是时至今日,乔布斯又回来了.他经常签的“再多一件事(one more thing)”放在他自己的身上也同样合适.经过上半年长达6个月的病休之后,他又精神抖擞地出现在3.4万苹果员工的面前.他在离开的期间接受了肝脏移植手术.在乔布斯年轻的时候,他的身边就聚集了一大批富有才干的追随者.现在乔布斯已经到了54岁,仅仅是简单地列出他的辉煌成就就足以解释他为什么能够当选财富杂志的“十年CEO”.仅在过去的十年里,他就从根本上改变了音乐、电影和手机等三大市场的格局.而他对最初起家的电脑行业的影响力也是有增无减.他是一位少见的全球知名的生意人.即便是从未看过苹果年报或者商业杂志的消费者也能滔滔不绝地谈论乔布斯的设计品位、优雅的零售店以及他不拘一格的广告创意.他经常被比喻为演员、天生的推销员、魔法师以及专横的完美主义者.这些评价当然十分准确,同时它们也给乔布斯增添了不少的传奇色彩.他经常与撰稿人、工业设计师和音乐家们混在一起,虽然他的着装不太正统和讲究,但是别搞错了,他可是天生的企业家.他或许不太注意对客户进行研究,但是他会非常勤奋地工作以生产出客户愿意购买的产品.他是一个极富幻想的人,但是他也不脱离现实,他密切注意着苹果的各种运营和营销活动.他的好友、甲骨文首席执行官拉里埃利森说,乔布斯是一个不为金钱所动的人. 他的勤奋显然是处于内心对苹果的热爱,通过苹果这个媒介,他既是冷酷的裁决者,又是改变世界的执行者.不管对于苹果还是乔布斯来说,每个季度的财报都是令人大吃一惊的.苹果在2000年时的市值大约为50亿美元,不久之后乔布斯第一次披露了苹果的数字生活方式战略,当时几乎没有评论家们能理解他的战略意图. 如今,苹果的市值达到了1700亿美元,略微超过谷歌.当时苹果在个人电脑市场的份额大幅下滑,现金外流非常严重,公司几乎到了破产的边缘. 现在苹果手中的现金和现金等价物的总价值达到340亿美元,超过了竞争对手戴尔的总市值. Mac电脑在美国个人电脑市场上的份额达到了9%,而且还在继续增长.苹果在9个国家开设了275家零售店,在美国MP3播放器市场占有73%的份额,自从推出iPhone之后,它又无可争议地确立了它在创新上的领袖地位.迪斯尼在2006年斥资75亿美元收购了乔布斯创立和控制的皮克斯动画制片厂.乔布斯顺理成章地成为迪斯尼董事和大股东. 仅仅计算他所持有的苹果和迪斯尼股票的价值,他的净资产就达到了50亿美元.一些其他企业的高管也有人能够辉煌十年,但是无人能够与乔布斯相比.乔布斯的十年实际上始于1997年,当时的乔布斯在离开了公司12年之后刚刚回归.乔布斯重掌公司大权后的第二年,他就完成了新的领导班子的组建. 那些优秀的人才正是十年以来乔布斯智囊团的核心人物.随后,苹果推出了乔布斯回归之后的首款Mac电脑iMac,那款具有突破性意义的产品预示着苹果将恢复健康.iMac推出之后大获成功,加上乔布斯坚决果断地大幅削减成本,为苹果今后的发展积累了充足的现金. 他改善了苹果的资产负债表,为未来的大投资做好了准备.在一切看起来都还正处于最黑暗的时候,乔布斯就开始为苹果日后的飞跃式发展打基础.苹果在2000年9月份发布的财报未能达到预期目标,股价在随后的几个月里持续下跌,一直跌到相当于如今的7美元的水平上. 然而乔布斯到现在仍然记得苹果东山再起的关键因素.2001年,当全球市场下滑,全球都陷入衰退的时候,苹果在那一年的1月份发布了iTunes,在3月份发布了Mac OS X操作系统,在5月份开设了首家苹果零售店,在11月份推出了首款iPod.市场当时并未迅速发现那些事件的重要性.iTunes当时还只是内建在Mac电脑中的音乐播放软件,当时也没有销售音乐的网络商店. 但是新的操作系统带来了一款极具吸引力、强大而且精美的产品,那就是iPod.当苹果的股价一蹶不振的时候,市场不时会传出苹果即将被收购的传闻.鲜为人知的是,乔布斯当时确实慎重考虑过在收购集团银湖的帮助下将苹果私有化的方案. 收购苹果可能会成为整个世纪最大的交易,但是据知情人士称,乔布斯最终放弃了那个想法.那其实是苹果第二次面临可能被收购的命运.早在1997年的时候,乔布斯的好友埃利森就曾联合了一些财团,准备收购苹果.埃利森在最近一次接受采访时说,乔布斯不喜欢事后被人批评,搞得好象他纯粹是为了赚钱才重新出山的一样.他向我解释说,他认为他可以更轻松和更体面地作出决定.对那些在乔布斯重返苹果后开始关注苹果的人来说,首席执行官的任务就是确定公司今后的发展方向.他在2002年初曾对媒体说过:“我宁愿与索尼竞争,也不愿意在另一个产品领域与微软竞争.我们都是同时拥有硬件、软件和操作系统的完整产品厂商.我们可以为用户完全负责.我们可以做到其他人做不到的事情.”乔布斯相信,只要他可以与公众直接对话,公众会转到苹果这边来的.他所说的公众并不是指Mac电脑的忠实用户,而是普通的消费者.开设自己的零售店的战略在当时还遭到了普遍的嘲笑,许多人认为那样做可能会让苹果的现金外流.前苹果高管、现在担任Intuit董事长和苹果董事的Bill Campbell说:“当时董事会都很紧张,但是他还是那么做了.他知道客户们想要什么.”现在回头来看,当时的苹果零售店能够出售的产品是多么少啊.乔布斯知道,他应该拿出更多的产品.乔布斯将彻底了解苹果当作自己的任务.曾经与苹果断断续续地合作了几年的前Chiat/Day创意总监Ken Segall说:“乔布斯参与了许多非常细致的工作,你是绝对不会认为一家公司的首席执行官应该参与那些细致的工作的.” Segall说,每当苹果将要推出新产品之前,乔布斯都会发起了著名的“换个思路”活动.他甚至将这个活动推广到了广告团队.他说:“乔布斯会说'第四段的第三个单词不恰当,你也许可以考虑用那个单词.'这样的话.”同时兼顾细节管理和大局观是乔布斯的特色标志.在刚刚回到苹果的时候,他便意识到产品的精美设计是苹果区别于当时由戴尔、微软和英特尔等厂商引领的计算机行业的因素之一.产品设计顾问公司Ideo的首席执行官Tim Brown在他的新作《通过设计去改变》中写道:“我根本数不清到底有多少客户会冲进苹果零售店然后说'给我下一款iPod'.那可能跟那些小声地说'给我下一个乔布斯'的设计师的数量很接近.”乔布斯还非常善于把握时机.在苹果推出iTunes之前,音乐界一直都没能开发出自己的数字音乐销售网站.之后苹果便开始为把iTunes变成一个购买音乐的商店作准备.当iTunes还只能在Mac电脑上使用的时候,苹果就巧妙地同各大唱片公司签订了协议.在iTunes兼容Windows系统之前,苹果的地位非常低,这在当时或许是苹果的一项优势. 这也使得iTunes更象是一块试验田,而不是破坏性的转型之举.滚石乐队的Steve Knopper在其新作《自我破坏的欲望》中写道,环球音乐的高管Doug Morris曾经说过:“我不明白苹果怎么可能只用一年的时间就在Mac电脑上毁灭了唱片行业.”Knopper写道:“我们为什么不能尝试一下呢?乔布斯重返苹果的时候,他已经是孤注一掷了.只是他很聪明,知道该怎么做.他做得很辛苦,但是再怎么辛苦也比不上最近几十年以来唱片公司的任何一位律师在艺人合同中进行的谈判那么艰难.”乔布斯抓住了一项重要的工具,那就是他对信息的熟练控制.他仿佛演练他和其他高管将要对外公布的每一句话.苹果只授权极少数高管可以公开就特定话题发表意见.乔布斯会非常认真地推敲他和其他高管能够对外发布的每一句话以及不能对外公布的信息. 哈佛大学教授David Yoffie估计,在2007年宣布推出和开始销售首款iPhone之间的几个月里,苹果未作任何公开声明就已经接到了价值4亿美元的免费广告,因此刺激的媒体都陷入了疯狂.乔布斯本人也非常小心,极其注意不过多透露消息,只有苹果要推销产品的时候,他才会出来说几句.他在2004年接受了癌症手术,但是直到手术完成之后,他才在致员工的电子邮件形式的公开信中发布了那个消息.后来,他同样是通过另一封致员工的公开信解释了他离开公司的情况,而且没有提到他或苹果其他高管的其他消息.2。

国际财务管理课后习题答案chapter 8

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS ANDPROBLEMSQUESTIONS1. How would you define transaction exposure? How is it different from economic exposure?Answer: Transaction exposure is the sensitivity of realized domestic currency values of the firm’s contractual cash flows denominated in foreign currencies to unexpected changes in exchange rates. Unlike economic exposure, transaction exposure is well-defined and short-term.2. Discuss and compare hedging transaction exposure using the forward contract vs. money market instruments. When do the alternative hedging approaches produce the same result?Answer: Hedging transaction exposure by a forward contract is achieved by selling or buying foreign currency receivables or payables forward. On the other hand, money market hedge is achieved by borrowing or lending the present value of foreign currency receivables or payables, thereby creating offsetting foreign currency positions. If the interest rate parity is holding, the two hedging methods are equivalent.3. Discuss and compare the costs of hedging via the forward contract and the options contract.Answer: There is no up-front cost of hedging by forward contracts. In the case of options hedging, however, hedgers should pay the premiums for the contracts up-front. The cost of forward hedging, however, may be realized ex post when the hedger regrets his/her hedging decision.4. What are the advantages of a currency options contract as a hedging tool compared with the forward contract?Answer: The main advantage of using options contracts for hedging is that the hedger can decide whether to exercise options upon observing the realized future exchange rate. Options thus provide a hedge against ex post regret that forward hedger might have to suffer. Hedgers can only eliminate the downside risk while retaining the upside potential.5. Suppose your company has purchased a put option on the German mark to manage exchange exposure associated with an account receivable denominated in that currency. In this case, your company can be said to have an ‘insurance’ policy on its receivable. Explain in what sense this is so.Answer: Your company in this case knows in advance that it will receive a certain minimum dollar amount no matter what might happen to the $/€exchange rate. Furthermore, if the German mark appreciates, your company will benefit from the rising euro.6. Recent surveys of corporate exchange risk management practices indicate that many U.S. firms simply do not hedge. How would you explain this result?Answer: There can be many possible reasons for this. First, many firms may feel that they are not really exposed to exchange risk due to product diversification, diversified markets for their products, etc. Second, firms may be using self-insurance against exchange risk. Third, firms may feel that shareholders can diversify exchange risk themselves, rendering corporate risk management unnecessary.7. Should a firm hedge? Why or why not?Answer: In a perfect capital market, firms may not need to hedge exchange risk. But firms can add to their value by hedging if markets are imperfect. First, if management knows about the firm’s exposure better than shareholders, the firm, not its shareholders, should hedge. Second, firms may be able to hedge at a lower cost. Third, if default costs are significant, corporate hedging can be justifiable because it reduces the probability of default. Fourth, if the firm faces progressive taxes, it can reduce tax obligations by hedging which stabilizes corporate earnings.8. Using an example, discuss the possible effect of hedging on a firm’s tax obligations.Answer: One can use an example similar to the one presented in the chapter.9. Explain contingent exposure and discuss the advantages of using currency options to manage this type of currency exposure.Answer: Companies may encounter a situation where they may or may not face currency exposure. In this situation, companies need options, not obligations, to buy or sell a given amount of foreign exchange they may or may not receive or have to pay. If companies either hedge using forward contracts or do not hedge at all, they may face definite currency exposure.10. Explain cross-hedging and discuss the factors determining its effectiveness.Answer: Cross-hedging involves hedging a position in one asset by taking a position in another asset. The effectiveness of cross-hedging would depend on the strength and stability of the relationship between the two assets.PROBLEMS1. Cray Research sold a super computer to the Max Planck Institute in Germany on credit and invoiced €10 million payable in six months. Currently, the six-month forward exchange rate is $1.10/€ and the foreign exchange advisor for Cray Research predicts that the spot rate is likely to be $1.05/€ in six months.(a) What is the expected gain/loss from the forward hedging?(b) If you were the financial manager of Cray Research, would you recommend hedging this euro receivable? Why or why not?(c) Suppose the foreign exchange advisor predicts that the future spot rate will be the same as the forward exchange rate quoted today. Would you recommend hedging in this case? Why or why not?Solution: (a) Expected gain($) = 10,000,000(1.10 – 1.05)= 10,000,000(.05)= $500,000.(b) I would recommend hedging because Cray Research can increase the expected dollar receipt by $500,000 and also eliminate the exchange risk.(c) Since I eliminate risk without sacrificing dollar receipt, I still would recommend hedging.2. IBM purchased computer chips from NEC, a Japanese electronics concern, and was billed ¥250 million payable in three months. Currently, the spot exchange rate is ¥105/$ and the three-month forward rate is ¥100/$. The three-month money market interest rate is 8 percent per annum in the U.S. and 7 percent per annum in Japan. The management of IBM decided to use the money market hedge to deal with this yen account payable.(a) Explain the process of a money market hedge and compute the dollar cost of meeting the yen obligation.(b) Conduct the cash flow analysis of the money market hedge.Solution: (a). Let’s first compute the PV of ¥250 million, i.e.,250m/1.0175 = ¥245,700,245.7So if the above yen amount is invested today at the Japanese interest rate for three months, the maturity value will be exactly equal to ¥25 million which is the amount of payable.To buy the above yen amount today, it will cost:$2,340,002.34 = ¥250,000,000/105.The dollar cost of meeting this yen obligation is $2,340,002.34 as of today.(b)___________________________________________________________________Transaction CF0 CF1____________________________________________________________________1. Buy yens spot -$2,340,002.34with dollars ¥245,700,245.702. Invest in Japan - ¥245,700,245.70 ¥250,000,0003. Pay yens - ¥250,000,000Net cash flow - $2,340,002.34____________________________________________________________________3. You plan to visit Geneva, Switzerland in three months to attend an international business conference. You expect to incur the total cost of SF 5,000 for lodging, meals and transportation during your stay. As of today, the spot exchange rate is $0.60/SF and the three-month forward rate is $0.63/SF. You can buy the three-month call option on SF with the exercise rate of $0.64/SF for the premium of $0.05 per SF. Assume that your expected future spot exchange rate is the same as the forward rate. The three-month interest rate is 6 percent per annum in the United States and 4 percent per annum in Switzerland.(a) Calculate your expected dollar cost of buying SF5,000 if you choose to hedge via call option on SF.(b) Calculate the future dollar cost of meeting this SF obligation if you decide to hedge using a forward contract.(c) At what future spot exchange rate will you be indifferent between the forward and option market hedges?(d) Illustrate the future dollar costs of meeting the SF payable against the future spot exchange rate under both the options and forward market hedges.Solution: (a) Total option premium = (.05)(5000) = $250. In three months, $250 is worth $253.75 = $250(1.015). At the expected future spot rate of $0.63/SF, which is less than the exercise price, you don’t expect to exercise options. Rather, you expect to buy Swiss franc at $0.63/SF. Since you are going to buy SF5,000, you expect to spend $3,150 (=.63x5,000). Thus, the total expected cost of buying SF5,000 will be the sum of $3,150 and $253.75, i.e., $3,403.75.(b) $3,150 = (.63)(5,000).(c) $3,150 = 5,000x + 253.75, where x represents the break-even future spot rate. Solving for x, we obtain x = $0.57925/SF. Note that at the break-even future spot rate, options will not be exercised.(d) If the Swiss franc appreciates beyond $0.64/SF, which is the exercise price of call option, you will exercise the option and buy SF5,000 for $3,200. The total cost of buying SF5,000 will be $3,453.75 = $3,200 + $253.75.This is the maximum you will pay.4. Boeing just signed a contract to sell a Boeing 737 aircraft to Air France. Air France will be billed €20 million which is payable in one year. The current spot exchange rate is $1.05/€ and the one -year forward rate is $1.10/€. The annual interest rate is 6.0% in the U.S. and5.0% in France. Boeing is concerned with the volatile exchange rate between the dollar and the euro and would like to hedge exchange exposure. (a) It is considering two hedging alternatives: sell the euro proceeds from the sale forward or borrow euros from the Credit Lyonnaise against the euro receivable. Which alternative would you recommend? Why?(b) Other things being equal, at what forward exchange rate would Boeing be indifferent between the two hedging methods?Solution: (a) In the case of forward hedge, the future dollar proceeds will be (20,000,000)(1.10) = $22,000,000. In the case of money market hedge (MMH), the firm has to first borrow the PV of its euro receivable, i.e., 20,000,000/1.05 =€19,047,619. Then the firm should exchange this euro amount into dollars at the current spot rate to receive: (€19,047,619)($1.05/€) = $20,000,000, which can be invested at the dollar interest rate for one year to yield:$20,000,000(1.06) = $21,200,000.Clearly, the firm can receive $800,000 more by using forward hedging.(b) According to IRP, F = S(1+i $)/(1+i F ). Thus the “indifferent” forward rate will be:F = 1.05(1.06)/1.05 = $1.06/€. $ Cost Options hedge Forward hedge $3,453.75 $3,150 0 0.579 0.64 (strike price) $/SF$253.755. Suppose that Baltimore Machinery sold a drilling machine to a Swiss firm and gave the Swiss client a choice of paying either $10,000 or SF 15,000 in three months.(a) In the above example, Baltimore Machinery effectively gave the Swiss client a free option to buy up to $10,000 dollars using Swiss franc. What is the ‘implied’ exercise exchange rate?(b) If the spot exchange rate turns out to be $0.62/SF, which currency do you think the Swiss client will choose to use for payment? What is the value of this free option for the Swiss client?(c) What is the best way for Baltimore Machinery to deal with the exchange exposure?Solution: (a) The implied exercise (price) rate is: 10,000/15,000 = $0.6667/SF.(b) If the Swiss client chooses to pay $10,000, it will cost SF16,129 (=10,000/.62). Since the Swiss client has an option to pay SF15,000, it will choose to do so. The value of this option is obviously SF1,129 (=SF16,129-SF15,000).(c) Baltimore Machinery faces a contingent exposure in the sense that it may or may not receive SF15,000 in the future. The firm thus can hedge this exposure by buying a put option on SF15,000.6. Princess Cruise Company (PCC) purchased a ship from Mitsubishi Heavy Industry. PCC owes Mitsubishi Heavy Industry 500 million yen in one year. The current spot rate is 124 yen per dollar and the one-year forward rate is 110 yen per dollar. The annual interest rate is 5% in Japan and 8% in the U.S. PCC can also buy a one-year call option on yen at the strike price of $.0081 per yen for a premium of .014 cents per yen.(a) Compute the future dollar costs of meeting this obligation using the money market hedge and the forward hedges.(b) Assuming that the forward exchange rate is the best predictor of the future spot rate, compute the expected future dollar cost of meeting this obligation when the option hedge is used.(c) At what future spot rate do you think PCC may be indifferent between the option and forward hedge?Solution: (a) In the case of forward hedge, the dollar cost will be 500,000,000/110 = $4,545,455. In the case of money market hedge, the future dollar cost will be: 500,000,000(1.08)/(1.05)(124)= $4,147,465.(b) The option premium is: (.014/100)(500,000,000) = $70,000. Its future value will be $70,000(1.08) = $75,600.At the expected future spot rate of $.0091(=1/110), which is higher than the exercise of $.0081, PCC will exercise its call option and buy ¥500,000,000 for $4,050,000 (=500,000,000x.0081).The total expected cost will thus be $4,125,600, which is the sum of $75,600 and $4,050,000.(c) When the option hedge is used, PCC will spend “at most” $4,125,000. On the other hand, when the forward hedging is used, PCC will have to spend $4,545,455 regardless of the future spot rate. This means that the options hedge dominates the forward hedge. At no future spot rate, PCC will be indifferent between forward and options hedges.7. Airbus sold an aircraft, A400, to Delta Airlines, a U.S. company, and billed $30 million payable in six months. Airbus is concerned with the euro proceeds from international sales and would like to control exchange risk. The current spot exchang e rate is $1.05/€ and six-month forward exchange rate is $1.10/€ at the moment. Airbus can buy a six-month put option on U.S. dollars with a strike price of €0.95/$ for a premium of €0.02 per U.S. dollar. Currently, six-month interest rate is 2.5% in the euro zone and 3.0% in the U.S.pute the guaranteed euro proceeds from the American sale if Airbus decides to hedge using aforward contract.b.If Airbus decides to hedge using money market instruments, what action does Airbus need to take?What would be the guaranteed euro proceeds from the American sale in this case?c.If Airbus decides to hedge using put options on U.S. dollars, what would be the ‘expected’ europroceeds from the American sale? Assume that Airbus regards the current forward exchange rate as an unbiased predictor of the future spot exchange rate.d.At what future spot exchange rate do you think Airbus will be indifferent between the option andmoney market hedge?Solution:a. Airbus will sell $30 million forward for €27,272,727 = ($30,000,000) / ($1.10/€).b. Airbus will borrow the present value of the dollar receivable, i.e., $29,126,214 = $30,000,000/1.03, and then sell the dollar proceeds spot for euros: €27,739,251. This is the euro amount that Airbus is going to keep.c. Since th e expected future spot rate is less than the strike price of the put option, i.e., €0.9091< €0.95, Airbus expects to exercise the option and receive €28,500,000 = ($30,000,000)(€0.95/$). This is gross proceeds. Airbus spent €600,000 (=0.02x30,000,000) upfr ont for the option and its future cost is equal to €615,000 = €600,000 x 1.025. Thus the net euro proceeds from the American sale is €27,885,000, which is the difference between the gross proceeds and the option costs.d. At the indifferent future spot rate, the following will hold:€28,432,732 = S T (30,000,000) - €615,000.Solving for S T, we obtain the “indifference” future spot exchange rate, i.e., €0.9683/$, or $1.0327/€.Note that €28,432,732 is the future value of the proceeds under money market hed ging:€28,432,732 = (€27,739,251) (1.025).Suggested solution for Mini Case: Chase Options, Inc.[See Chapter 13 for the case text]Chase Options, Inc.Hedging Foreign Currency Exposure Through Currency OptionsHarvey A. PoniachekI. Case SummaryThis case reviews the foreign exchange options market and hedging. It presents various international transactions that require currency options hedging strategies by the corporations involved. Seven transactions under a variety of circumstances are introduced that require hedging by currency options. The transactions involve hedging of dividend remittances, portfolio investment exposure, and strategic economic competitiveness. Market quotations are provided for options (and options hedging ratios), forwards, and interest rates for various maturities.II. Case Objective.The case introduces the student to the principles of currency options market and hedging strategies. The transactions are of various types that often confront companies that are involved in extensive international business or multinational corporations. The case induces students to acquire hands-on experience in addressing specific exposure and hedging concerns, including how to apply various market quotations, which hedging strategy is most suitable, and how to address exposure in foreign currency through cross hedging policies.III. Proposed Assignment Solution1. The company expects DM100 million in repatriated profits, and does not want the DM/$ exchange rate at which they convert those profits to rise above 1.70. They can hedge this exposure using DM put options with a strike price of 1.70. If the spot rate rises above 1.70, they can exercise the option, while ifthat rate falls they can enjoy additional profits from favorable exchange rate movements.To purchase the options would require an up-front premium of:DM 100,000,000 x 0.0164 = DM 1,640,000.With a strike price of 1.70 DM/$, this would assure the U.S. company of receiving at least:DM 100,000,000 – DM 1,640,000 x (1 + 0.085106 x 272/360)= DM 98,254,544/1.70 DM/$ = $57,796,791by exercising the option if the DM depreciated. Note that the proceeds from the repatriated profits are reduced by the premium paid, which is further adjusted by the interest foregone on this amount.However, if the DM were to appreciate relative to the dollar, the company would allow the option to expire, and enjoy greater dollar proceeds from this increase.Should forward contracts be used to hedge this exposure, the proceeds received would be:DM100,000,000/1.6725 DM/$ = $59,790,732,regardless of the movement of the DM/$ exchange rate. While this amount is almost $2 million more than that realized using option hedges above, there is no flexibility regarding the exercise date; if this date differs from that at which the repatriate profits are available, the company may be exposed to additional further current exposure. Further, there is no opportunity to enjoy any appreciation in the DM.If the company were to buy DM puts as above, and sell an equivalent amount in calls with strike price 1.647, the premium paid would be exactly offset by the premium received. This would assure that the exchange rate realized would fall between 1.647 and 1.700. If the rate rises above 1.700, the company will exercise its put option, and if it fell below 1.647, the other party would use its call; for any rate in between, both options would expire worthless. The proceeds realized would then fall between:DM 100,00,000/1.647 DM/$ = $60,716,454andDM 100,000,000/1.700 DM/$ = $58,823,529.This would allow the company some upside potential, while guaranteeing proceeds at least $1 million greater than the minimum for simply buying a put as above.Buy/Sell OptionsDM/$Spot Put Payoff “Put”Profits Call Payoff“Call”Profits Net Profit1.60 (1,742,846) 0 1,742,846 60,716,454 60,716,454 1.61 (1,742,846) 0 1,742,846 60,716,454 60,716,454 1.62 (1,742,846) 0 1,742,846 60,716,454 60,716,454 1.63 (1,742,846) 0 1,742,846 60,716,454 60,716,454 1.64 (1,742,846) 0 1,742,846 60,716,454 60,716,454 1.65 (1,742,846) 60,606,061 1,742,846 0 60,606,061 1.66 (1,742,846) 60,240,964 1,742,846 0 60,240,964 1.67 (1,742,846) 59,880,240 1,742,846 0 59,880,240 1.68 (1,742,846) 59,523,810 1,742,846 0 59,523,810 1.69 (1,742,846) 59,171,598 1,742,846 0 59,171,598 1.70 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.71 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.72 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.73 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.74 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.75 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.76 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.77 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.78 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.79 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.80 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.81 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.82 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.83 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.84 (1,742,846) 58,823,529 1,742,846 0 58,823,529 1.85 (1,742,846) 58,823,529 1,742,846 0 58,823,529Since the firm believes that there is a good chance that the pound sterling will weaken, locking them into a forward contract would not be appropriate, because they would lose the opportunity to profit from this weakening. Their hedge strategy should follow for an upside potential to match their viewpoint. Therefore, they should purchase sterling call options, paying a premium of:5,000,000 STG x 0.0176 = 88,000 STG.If the dollar strengthens against the pound, the firm allows the option to expire, and buys sterling in the spot market at a cheaper price than they would have paid for a forward contract; otherwise, the sterling calls protect against unfavorable depreciation of the dollar.Because the fund manager is uncertain when he will sell the bonds, he requires a hedge which will allow flexibility as to the exercise date. Thus, options are the best instrument for him to use. He can buy A$ puts to lock in a floor of 0.72 A$/$. Since he is willing to forego any further currency appreciation, he can sell A$ calls with a strike price of 0.8025 A$/$ to defray the cost of his hedge (in fact he earns a net premium of A$ 100,000,000 x (0.007234 –0.007211) = A$ 2,300), while knowing that he can’t receive less than 0.72 A$/$ when redeeming his investment, and can benefit from a small appreciation of the A$.Example #3:Problem: Hedge principal denominated in A$ into US$. Forgo upside potential to buy floor protection.I. Hedge by writing calls and buying puts1) Write calls for $/A$ @ 0.8025Buy puts for $/A$ @ 0.72# contracts needed = Principal in A$/Contract size100,000,000A$/100,000 A$ = 1002) Revenue from sale of calls = (# contracts)(size of contract)(premium)$75,573 = (100)(100,000 A$)(.007234 $/A$)(1 + .0825 195/360)3) Total cost of puts = (# contracts)(size of contract)(premium)$75,332 = (100)(100,000 A$)(.007211 $/A$)(1 + .0825 195/360)4) Put payoffIf spot falls below 0.72, fund manager will exercise putIf spot rises above 0.72, fund manager will let put expire5) Call payoffIf spot rises above .8025, call will be exercised If spot falls below .8025, call will expire6) Net payoffSee following Table for net payoff Australian Dollar Bond HedgeStrikePrice Put Payoff “Put”Principal Call Payoff“Call”Principal Net Profit0.60 (75,332) 72,000,000 75,573 0 72,000,2410.61 (75,332) 72,000,000 75,573 0 72,000,2410.62 (75,332) 72,000,000 75,573 0 72,000,2410.63 (75,332) 72,000,000 75,573 0 72,000,2410.64 (75,332) 72,000,000 75,573 0 72,000,2410.65 (75,332) 72,000,000 75,573 0 72,000,2410.66 (75,332) 72,000,000 75,573 0 72,000,2410.67 (75,332) 72,000,000 75,573 0 72,000,2410.68 (75,332) 72,000,000 75,573 0 72,000,2410.69 (75,332) 72,000,000 75,573 0 72,000,2410.70 (75,332) 72,000,000 75,573 0 72,000,2410.71 (75,332) 72,000,000 75,573 0 72,000,2410.72 (75,332) 72,000,000 75,573 0 72,000,2410.73 (75,332) 73,000,000 75,573 0 73,000,2410.74 (75,332) 74,000,000 75,573 0 74,000,2410.75 (75,332) 75,000,000 75,573 0 75,000,2410.76 (75,332) 76,000,000 75,573 0 76,000,2410.77 (75,332) 77,000,000 75,573 0 77,000,2410.78 (75,332) 78,000,000 75,573 0 78,000,2410.79 (75,332) 79,000,000 75,573 0 79,000,2410.80 (75,332) 80,000,000 75,573 0 80,000,2410.81 (75,332) 0 75,573 80,250,000 80,250,2410.82 (75,332) 0 75,573 80,250,000 80,250,2410.83 (75,332) 0 75,573 80,250,000 80,250,2410.84 (75,332) 0 75,573 80,250,000 80,250,2410.85 (75,332) 0 75,573 80,250,000 80,250,2414. The German company is bidding on a contract which they cannot be certain of winning. Thus, the need to execute a currency transaction is similarly uncertain, and using a forward or futures as a hedge is inappropriate, because it would force them to perform even if they do not win the contract.Using a sterling put option as a hedge for this transaction makes the most sense. For a premium of:12 million STG x 0.0161 = 193,200 STG,they can assure themselves that adverse movements in the pound sterling exchange rate will not diminish the profitability of the project (and hence the feasibility of their bid), while at the same time allowing the potential for gains from sterling appreciation.5. Since AMC in concerned about the adverse effects that a strengthening of the dollar would have on its business, we need to create a situation in which it will profit from such an appreciation. Purchasing a yen put or a dollar call will achieve this objective. The data in Exhibit 1, row 7 represent a 10 percent appreciation of the dollar (128.15 strike vs. 116.5 forward rate) and can be used to hedge against a similar appreciation of the dollar.For every million yen of hedging, the cost would be:Yen 100,000,000 x 0.000127 = 127 Yen.To determine the breakeven point, we need to compute the value of this option if the dollar appreciated 10 percent (spot rose to 128.15), and subtract from it the premium we paid. This profit would be compared with the profit earned on five to 10 percent of AMC’s sales (which would be lost as a result of the dollar appreciation). The number of options to be purchased which would equalize these two quantities would represent the breakeven point.Example #5:Hedge the economic cost of the depreciating Yen to AMC.If we assume that AMC sales fall in direct proportion to depreciation in the yen (i.e., a 10 percent decline in yen and 10 percent decline in sales), then we can hedge the full value of AMC’s sales. I have assumed $100 million in sales.1) Buy yen puts# contracts needed = Expected Sales *Current ¥/$ Rate / Contract size9600 = ($100,000,000)(120¥/$) / ¥1,250,0002) Total Cost = (# contracts)(contract size)(premium)$1,524,000 = (9600)( ¥1,250,000)($0.0001275/¥)3) Floor rate = Exercise – Premium128.1499¥/$ = 128.15¥/$ - $1,524,000/12,000,000,000¥4) The payoff changes depending on the level of the ¥/$ rate. The following table summarizes thepayoffs. An equilibrium is reached when the spot rate equals the floor rate.AMC ProfitabilityYen/$ Spot Put Payoff Sales Net Profit 120 (1,524,990) 100,000,000 98,475,010 121 (1,524,990) 99,173,664 97,648,564 122 (1,524,990) 98,360,656 96,835,666 123 (1,524,990) 97,560,976 86,035,986 124 (1,524,990) 96,774,194 95,249,204 125 (1,524,990) 96,000,000 94,475,010 126 (1,524,990) 95,238,095 93,713,105 127 (847,829) 94,488,189 93,640,360 128 (109,640) 93,750,000 93,640,360 129 617,104 93,023,256 93,640,360 130 1,332,668 92,307,692 93,640,360 131 2,037,307 91,603,053 93,640,360 132 2,731,269 90,909,091 93,640,360 133 3,414,796 90,225,664 93,640,360 134 4,088,122 89,552,239 93,640,360 135 4,751,431 88,888,889 93,640,360 136 5,405,066 88,235,294 93,640,360 137 6,049,118 87,591,241 93,640,360 138 6,683,839 86,966,522 93,640,360 139 7,308,425 86,330,936 93,640,360 140 7,926,075 85,714,286 93,640,360 141 8,533,977 85,106,383 93,640,360 142 9,133,318 84,507,042 93,640,360 143 9,724,276 83,916,084 93,640,360 144 10,307,027 83,333,333 93,640,360 145 10,881,740 82,758,621 93,640,360 146 11,448,579 82,191,781 93,640,360 147 12,007,707 81,632,653 93,640,360 148 12,569,279 81,081,081 93,640,360 149 13,103,448 80,536,913 93,640,360 150 13,640,360 80,000,000 93,640,360。

线性系统理论Chapter8

MFD的特性

给定G(s)的右MFD,规定:MFD的次数degdetD(s), 给定G(s)的左MFD,规定:MFD的次数degdetDL(s); 给定G(s),其右MFD和左MFD都不是唯一的。并且, 不同的MFD,常可能有不同的次数;

3

N(s)D-1(s)为G(s)的一个右MFD,W(s)是非奇异多项 式矩阵,定义 N ( s ) = N ( s)W ( s ), D ( s) = D( s )W ( s ) 则N ( s ) D −1 ( s)也必是G(s)的右MFD,且成立

Q( s ) = Q ( s ), R( s ) = R ( s )

严格真有理分式矩阵 证明唯一性

D(s)为列既约时,由严真性判据,可证明结论。

结论8.15 若DL-1(s)NL(s)为非真,则必唯一地存在QL(s) 和RL(s),使成立 DL-1(s)NL(s) = QL(s) + DL-1(s)RL(s) 其中,DL-1(s)RL(s)是严格真的。如果DL(s)是行既约的, 那么 δriDL(s) > δriRL(s), i = 1,…,q

因为δ ci N cL ( s ) ≤ δ ci DcL ( s ) < δ ci S c ( s )

s →∞ − − lim N cL ( s) S c 1 ( s) = 0, lim DcL ( s ) S c 1 ( s ) = 0 s →∞

−1 lim G ( s ) = N hc Dhc = G0 (非零常阵)

12 返回

其中Nr(s)和Nl(s)为常阵,Qr(s)和Ql(s)分别可求出

8.4 不可简约矩阵分式描述

右互质MFD和左互质MFD

称一个矩阵分式描述G(s) = N(s)D-1(s)为右互质MFD, 如果N(s)和D(s)是右互质的。 称一个矩阵分式描述G(s) = DL-1(s)NL(s)为左互质MFD, 如果DL(s)和NL(s)是左互质的。

牛津英语九年级Chapter8Twogeniuses全

Einstein's special and general theories of relativity reinterpreted gravity as a curvature of spacetime and explained the equivalence of mass and energy.

Formulation of calculus

Newton developed calculus, a branch of mathematics that deals with continuous change, independently of Gottfried Wilhelm Leibniz.

Greatest scientist of the 20th century

Einstein's theories of relativity and quantum mechanics reshaped our understanding of the universe, introducing concepts like curved spacetime and quantum entanglement.

Scientific revolution

The works of Newton and Darwin helped initiate the scientific revolution, which transformed the way humans view the natural world.

03

Newton's Main Achievements

The law of universal gravitation

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

CF 3CHO > CH 2ClCHO > CH 3CHO O2N CHO > CHO > CH3 CHO

HCHO > RCHO >CH 3COCH3 >RCOCH 3 > RCOR' >RCOPh >PhCOPh

羰基碳的正电性愈强、所连基团空间位阻愈小、 亲核反应愈易进行。

COONa CH-OH + Cu(OH)2 CH-OH COOK

COONa CH-O Cu + 2 H2O CH-O COOK (Fehling试剂)

O R C H + 2 Cu(OH)2

酒石酸钾钠

O RC OH + Cu2O + 2 H2O

可鉴别脂肪醛与 酮,也可区别芳 醛与脂肪醛

Benedict试剂: CuSO4, Na2CO3, 柠檬酸钠 (Cu2+) 作用原理同Fehling试剂,用于区别脂肪醛与芳香醛。 2. 与希夫(Schiff)试剂反应

第8章 醛、酮、醌 (Aldehyde, Ketone and Quinone) 目的要求

1.掌握醛、酮的命名。 2.掌握醛、酮、醌的结构及性质。 亲核加成反应 羰基的还原反应 α-氢的反应 醛的特殊反应 作业:P210 1(1,3,5,7,9);5(1,2,4,6,8);6;13;14(2,3)

. AgNO3 + 3 NH3 H2O

Ag(NH3)2OH + NH4NO3 + 2 H2O

(Tollens试剂)

O (Ar)R C H + 2 [Ag(NH3)2]OH

(Ar)RCOONH4 +2Ag

△

银镜反应区 别醛与酮

+ 3 NH3 + H2O

与Fehling试剂作用 Fehling:CuSO4和 酒石酸钾钠的NaOH 溶液两部分,用时等体积混合。

4-甲氧基-3-环己烯酮

CH3 O 4-甲基-3-戊烯-2-酮 CH3C CHC CH3Βιβλιοθήκη OO2,4-己二酮

CH3CH2 C CH2 C CH3

O

柠檬醛(俗名) H

3,7-二甲基-2,6-辛二烯醛

1.命名下列化合物

O Cl NO2

6-硝基-4-氯-2,4-环己二烯酮

CH3 O CH3CCH2 C CH2CH CH3 CH2CH3 Cl

羰基平面 C=O极性较大,醛、酮是强极性分子(μ=2.3~2.8D).

8.1.2 分类

脂肪醛、酮

O O CH3 CH CH3CCH2CH3

CHO

O CCH3

芳香醛、酮

O

多元醛、酮

O

O O CH3C CH2C CH3

HCCH2CH2CH

8.1.3 命名

1.普通命名法 HCHO 甲醛 CH3CHO 乙醛

O (H) R C H 醛

酮 醌

共同特点:都含有羰基

O R C R'

O

O

O O

C Carbonyl group

O

8.1 结构、分类和命名

8.1.1 醛、酮的结构 O

121.7o 121pm

C

116.6o

比较

109o

143pm

H

H

平面分子

CH3

羰基碳为sp2杂化,碳原子的3 个sp2杂化轨道分别与氧及其它2 个原子形成 3个σ 键,这 3个σ 键 处于一个平面,羰基碳余下的1 个未杂化的 p 轨道与氧的 2p 轨 道彼此平行重叠,形成π键。

-HOH

负碳离子

H

OR CH C R'(H)

负烯醇离子

1. 卤代反应与碘仿反应

在酸或碱的催化下, - H被卤素代替的反应。

O RCH 2C-H(R') +

例

O

H+ X2 - RCHC-H(R') or: OH

O + Br 2

C H3C O O H

X

O Br

卤仿反应:

O CH3 C R I2

NaOH

将SO2通入品红水溶液中所得无色溶液即为Schiff试剂。

HSO2HN

2

CH SO3H

NH3Cl

+ 2RCHO

HO R H

C

SO2NH

2

CH SO3H

N+H3Cl

-H2SO4

HO R H

C

SO2NH

2

C 紫红色络合物

NH2ClH

H2SO4

甲醛产物颜色不变,其它醛产物颜色褪去 应用:区别醛和酮;区别甲醛和其它醛。

O CHO+H2N-NH-C-NH2

O CH=N-NH-C-NH2

苯甲醛缩氨脲

加成反应小结

与HCN加成可以增长碳链。

与NaHSO3加成可以分离和精制醛。

缩醛常用于在反应中保护醛基。

醛、酮与氨的衍生物(即羰基试剂)的反应 产物常用于醛、酮的分离和精制,其中2, 4-二硝基苯腙为黄色沉淀,常用于羰基化 合物的鉴别。

O + NH2OH

Hydroxylamine Cyclohexanone

N-OH + H2O

Cyclohexanone oxime (mp 90℃) 环己酮肟(白色结晶 mp90℃)

NO 2 CH3 CH3 C O + H2NNH NO2

NO 2 CH3 C NNH CH3 NO2 + H2O

2,4-Dinitrophenylhydrazine (yellow or light orange mp126℃) 丙酮 2,4-二硝基苯腙(黄色结晶 crystals) Propanone 2,4-dinitrophenylhydrazone

1. 与含碳亲核试剂的加成

(1)与HCN加成

O R C H(CH3) + HCN R OH C H(CH3) CN

OH

H3O

α-羟腈

R

C COOH H(CH3)

α-羟基酸

醛、脂肪族甲基酮 和小于8个碳的环酮 能发生该反应。

HCN

H+ + CNO O C CN + NC C

+ :CNR

slow

H R' C OMgX R

R R' C OMgX R

H3O+

H R' C OH H

伯醇

R'MgX EtOEt

H3O+

H R' C OH R 仲醇

R R' C OH R

R'MgX EtOEt

H3O+

叔醇

OH

如何由苯制备:

C CH2CH3 CH3

O C CH3

+

CH3COCl

无水AlCl3

CH3CH2Br+Mg

水合氯乙醛

水合茚三酮

4. 与氨的衍生物的加成

H C O + H N G

OH H C N G

-H2O

C O

+

H2N

G

-H2O

C N G

产物都有一定 的晶形和熔点

H2N—R H2N—OH R’ R—C=O+ R—C=O H2N—NH2 H2N—NH

R R'

O H2N—NH-C-NH2 R’ R-C=N-NH-CO-NH2(缩氨脲)

-H2O OH 50℃

OH CHCH2CHO

CH

CHCHO

O

O

KO H / H O 2 加热

CH 3C(CH 2)4CCH 3

CH 3

85% (请思考反应过程)

COCH3

8.2.3 醛的特殊反应

1. 与弱氧化剂反应

Tollens、Fehling、Benedict试剂

与Tollens试剂作用--银镜反应

8.2.2 α-H的反应

与官能团相连 的碳原子称αC

O C C H

α-H变为质子的倾 向增加

羰基使α-H变得活泼,易成为质子离去。这一离去倾向也因 sp 超共轭效应而加强。α-H离解后, 醛、酮可通过形成负碳离 子或负烯醇离子将负电荷离域到 O 和α-C 上而趋于稳定。

O - O OH R C C R'(H) R CH C R'(H)

O C CH3

+

无水乙醚

CH3CH2MgBr

无水乙醚

CH3CH2MgBr

H 3O

2. 与含硫亲核试剂NaHSO3反应

O HO (H)R C H(CH3) + O S ONa OH (H)R C H(CH3) SO3Na

例如:

O + NaHSO3

OH SO3Na

醛、脂肪族甲基酮 和小于8个碳的环酮 能发生该反应。

6,6-二甲基-2-氯-4-辛酮

8.2 醛、酮的化学性质

O C H

δ δ

羰基亲核加成

(H)

醛的特殊反应

C

α —H的反应

8.2.1 亲核加成反应(Nucleophilic addition)

R δ C R' + - δ+ δ O + δ Nu A

R R' C

O-

R A+ R'

OA C Nu

Nu

电性效应

C N

R’ R—C = N-R Schiff base R’ R—C = N-OH oxime (肟) R’ R—C=N-NH2 hydrazone(腙) R’ R-C=N-NH-C6H5 phenylhydrozone

G

由于上述N-取代亚胺容易通过结晶进行纯化, 并且又可经酸水解得到原来的醛或酮,所以这些 羰基试剂也用于醛、酮的分离及精制。