金融机构风险管理练习题1

金融风险合理使用培训测试题及参考答案

金融风险合理使用培训测试题及参考答案

题目一

1. 金融风险是指什么?

金融风险是指金融活动中存在的可能造成经济损失的不确定性。

题目二

2. 请列举三种常见的金融风险类型。

- 市场风险:由于市场价格波动而导致的资产价值减少的风险。

- 信用风险:由于债务方无法按时履约而导致的损失风险。

- 操作风险:由于内部操作失误、技术故障或欺诈行为而导致

的损失风险。

题目三

3. 如何合理使用金融风险管理工具?

合理使用金融风险管理工具可以通过以下几个方面来实现:

- 定期评估和识别风险:对各种金融风险进行定期评估和识别,以便及时采取相应的防范和管理措施。

- 多样化投资组合:通过分散投资组合中的风险,减少单一投

资带来的潜在损失。

- 控制杠杆效应:控制杠杆比例,避免过度的借款或杠杆交易,以降低潜在损失的风险。

- 设定止损机制:设定合理的止损点,及时止损以减小风险。

题目四

4. 金融机构面临的主要风险是什么?

金融机构面临的主要风险包括市场风险、信用风险、流动性风险、操作风险和法律风险。

参考答案

1. 金融风险是指金融活动中存在的可能造成经济损失的不确定性。

2. 市场风险、信用风险、操作风险。

3. 合理使用金融风险管理工具可以通过定期评估和识别风险、多样化投资组合、控制杠杆效应、设定止损机制等方式来实现。

4. 金融机构面临的主要风险包括市场风险、信用风险、流动性风险、操作风险和法律风险。

证券金融基础知识(金融风险管理)习题及答案

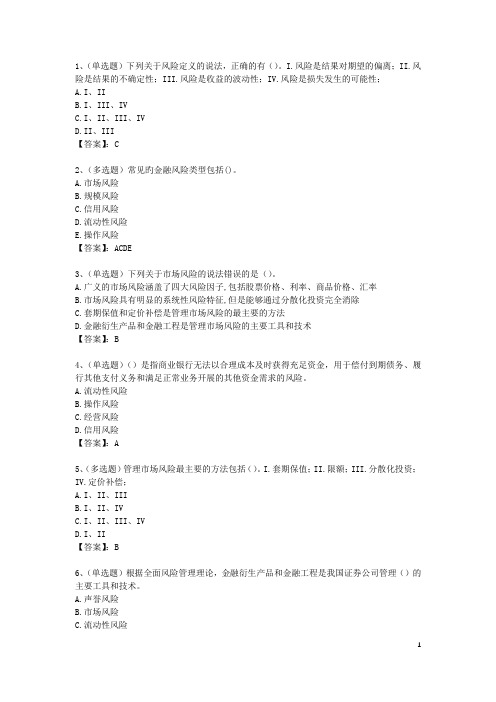

1、(单选题)下列关于风险定义的说法,正确的有()。

I.风险是结果对期望的偏离;II.风险是结果的不确定性;III.风险是收益的波动性;IV.风险是损失发生的可能性;A.I、IIB.I、III、IVC.I、II、III、IVD.II、III【答案】:C2、(多选题)常见旳金融风险类型包括()。

A.市场风险B.规模风险C.信用风险D.流动性风险E.操作风险【答案】:ACDE3、(单选题)下列关于市场风险的说法错误的是()。

A.广义的市场风险涵盖了四大风险因子,包括股票价格、利率、商品价格、汇率B.市场风险具有明显的系统性风险特征,但是能够通过分散化投资完全消除C.套期保值和定价补偿是管理市场风险的最主要的方法D.金融衍生产品和金融工程是管理市场风险的主要工具和技术【答案】:B4、(单选题)()是指商业银行无法以合理成本及时获得充足资金,用于偿付到期债务、履行其他支付义务和满足正常业务开展的其他资金需求的风险。

A.流动性风险B.操作风险C.经营风险D.信用风险【答案】:A5、(多选题)管理市场风险最主要的方法包括()。

I.套期保值;II.限额;III.分散化投资;IV.定价补偿;A.I、II、IIIB.I、II、IVC.I、II、III、IVD.I、II【答案】:B6、(单选题)根据全面风险管理理论,金融衍生产品和金融工程是我国证券公司管理()的主要工具和技术。

A.声誉风险B.市场风险C.流动性风险【答案】:B7、(单选题)下列关于风险与金融产品和投资的说法错误的是()。

A.任何金融产品都是风险和收益的组合B.风险是与收益相匹配的C.投资是以风险换收益D.以风险换收益也应无限制地承担风险【答案】:D8、(单选题)任何金融工具都可能出现因指数价格的不利变动而带来资产损失的可能性,这是()。

A.信用风险B.市场风险C.法律风险D.结算风险【答案】:B9、(单选题)()通常被定义为“公司融资类客户、交易对手或公司持有证券的发行人在无法履行合同义务的情况下,给公司造成损失的可能性,或者相关信用质量发生恶化情况下,给公司造成损失的可能性”。

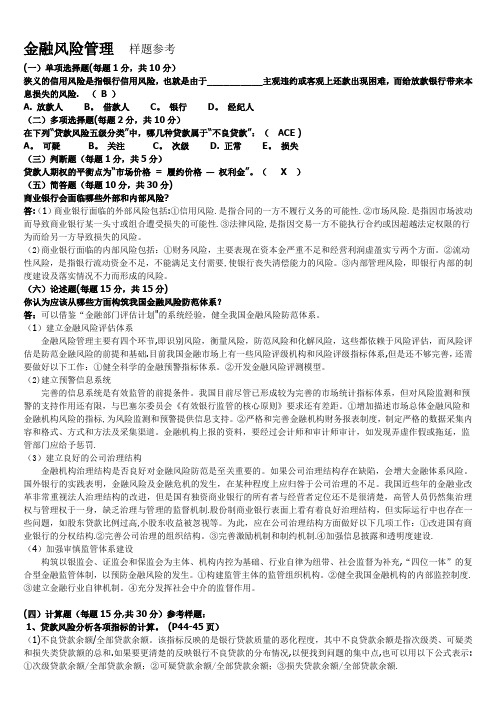

《金融风险管理》复习习题全集(包含答案)

金融风险管理样题参考(一)单项选择题(每题1分,共10分)狭义的信用风险是指银行信用风险,也就是由于__________主观违约或客观上还款出现困难,而给放款银行带来本息损失的风险. ( B )A. 放款人B。

借款人C。

银行D。

经纪人(二)多项选择题(每题2分,共10分)在下列“贷款风险五级分类”中,哪几种贷款属于“不良贷款”:(ACE )A。

可疑B。

关注C。

次级 D. 正常E。

损失(三)判断题(每题1分,共5分)贷款人期权的平衡点为“市场价格= 履约价格—权利金”。

(X )(五)简答题(每题10分,共30分)商业银行会面临哪些外部和内部风险?答:(1)商业银行面临的外部风险包括:①信用风险.是指合同的一方不履行义务的可能性.②市场风险.是指因市场波动而导致商业银行某一头寸或组合遭受损失的可能性.③法律风险,是指因交易一方不能执行合约或因超越法定权限的行为而给另一方导致损失的风险。

(2)商业银行面临的内部风险包括:①财务风险,主要表现在资本金严重不足和经营利润虚盈实亏两个方面。

②流动性风险,是指银行流动资金不足,不能满足支付需要,使银行丧失清偿能力的风险。

③内部管理风险,即银行内部的制度建设及落实情况不力而形成的风险。

(六)论述题(每题15分,共15分)你认为应该从哪些方面构筑我国金融风险防范体系?答:可以借鉴“金融部门评估计划"的系统经验,健全我国金融风险防范体系。

(1)建立金融风险评估体系金融风险管理主要有四个环节,即识别风险,衡量风险,防范风险和化解风险,这些都依赖于风险评估,而风险评估是防范金融风险的前提和基础.目前我国金融市场上有一些风险评级机构和风险评级指标体系,但是还不够完善,还需要做好以下工作:①健全科学的金融预警指标体系。

②开发金融风险评测模型。

(2)建立预警信息系统完善的信息系统是有效监管的前提条件。

我国目前尽管已形成较为完善的市场统计指标体系,但对风险监测和预警的支持作用还有限,与巴塞尔委员会《有效银行监管的核心原则》要求还有差距。

金融机构风险管理练习习题

【经典资料,WORD文档,可编辑修改】【经典考试资料,答案附后,看后必过,WORD文档,可修改】金融机构风险管理练习题第七章金融中介机构的风险练习1.描述下列金融机构在交易中遇到的风险敞口,请选出下面的一种或几种。

a利率风险b信用风险c表外风险d技术风险e汇率风险f国家风险(1)银行通过出售一年期CD为价值$2000万的五年期固定汇率的商业贷款融资。

(2)保险公司把保险费投在长期政府债券组合中。

(3)一家德国银行出售2年期、固定利率债券为波兰公司提供的2年期、固定利率贷款融资。

(4)英国银行收购澳大利亚银行减少结算操作的麻烦。

(5)使用远期或有合约对利率风险敝口进行了完全的套期保值。

(6)债券经纪人公司用自己的股本在LDC债券市场上购买巴西债务。

(7)银行出售一组抵押贷款作为抵押证券。

练习2公司特有信用风险与系统信用风险的区别是什么金融机构如何减少公司特有信用风险第八章:利率风险:重定价模型练习1:下面哪一项资产或负债符合一年期利率或重定价的敏感性条件天期美国国库券年期美国国库券年期美国国库券bank repurchases $100000 of common stockbank issues $2000000 of CDs and uses the proceeds for loans to home-owners.bank receives $500000 in deposits and invests them in T-bills.bank issued $800000 in common stock and lends it to help finance a new shopping mall.bank issued $1000000 in nonqualifying perpetual preferred stock and purchases general obligation municipal bonds.pay back $4000000 of mortgages, and the bank used the proceeds to build new ATMs.练习3:What is the bank’s capital adequacy level (unde r Basel I and Basel II)Off-balance-sheet items:Risk weight 100%:1.$80m in 2-year loan commitments to a large BB+ rated . corporation.2.$10m direct credit substitute standby letters of credit issued to a BBB rated . corporation.3.$50m in commercial letters of credit issued to a BBB- rated . corporation.Risk weight 50%:fixed-floating interest rate swap for 4 year with notional dollar value of $100m and replacement cost of $3m.two year Euro$ contract for $40m with a replacement cost of -$1m练习4:Third bank has following balance sheet (in millions) with the risk weights in parentheses.Assets Liabilities and EquityCash(0%)$20 Deposits$175OECD interbank deposits(20%)25Subordinated debt years)3Mortgage loans(50%)70cumulative preferred stock5。

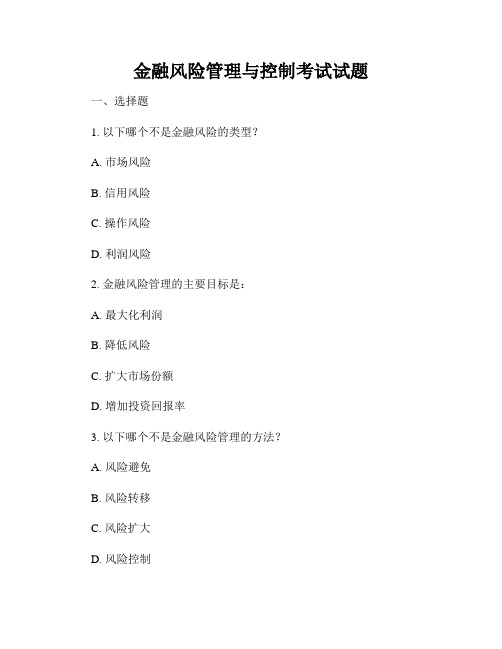

金融风险管理与控制考试试题

金融风险管理与控制考试试题一、选择题1. 以下哪个不是金融风险的类型?A. 市场风险B. 信用风险C. 操作风险D. 利润风险2. 金融风险管理的主要目标是:A. 最大化利润B. 降低风险C. 扩大市场份额D. 增加投资回报率3. 以下哪个不是金融风险管理的方法?A. 风险避免B. 风险转移C. 风险扩大D. 风险控制二、简答题1. 请简要介绍金融风险管理的目标和原则。

金融风险管理的目标是降低金融机构由于市场、信用、操作等因素造成的潜在损失,并确保金融活动的稳定和可持续发展。

其原则主要包括风险识别、风险评估、风险控制和风险监管。

通过全面了解和分析金融风险,制定相应的管理措施和策略,以保障金融安全和机构的可持续经营。

2. 请简述市场风险的特点和主要管理方法。

市场风险是金融机构面临的由市场价格波动和市场变化引起的风险。

其特点包括不可控性、不确定性和系统性。

对于市场风险的管理,主要方法包括风险避免、风险转移、风险分散和风险对冲。

通过合理分散投资组合、使用金融衍生品进行对冲交易等方式,降低市场风险对金融机构的影响。

三、案例分析某银行在进行信用风险管理时,发现一位借款人的信用评级发生了下降。

请问银行应该如何应对这种情况?针对这种情况,银行应该采取以下措施进行应对:1. 重新评估借款人的信用状况,了解其当前的还款能力和还款意愿。

2. 调整借款人的信用额度和利率,以反映其信用评级下降所带来的风险变化。

3. 提供额外的担保要求,如要求借款人提供抵押物或找到更可靠的第三方担保机构。

4. 定期监测借款人的还款情况,对于出现逾期或违约行为,采取相应的预警和追偿措施。

5. 考虑将债权出售给其他金融机构,以分散风险和回收资金。

通过以上措施,银行可以有效应对借款人信用评级下降所带来的信用风险,降低贷款违约的可能性,并保护自身的利益。

总结:金融风险管理与控制是金融机构必须重视和有效执行的重要工作。

通过对不同类型的风险进行准确的评估和监控,采取相应的管理方法和措施,可以降低金融机构面临的损失风险和经营风险,提高金融安全性和经济效益。

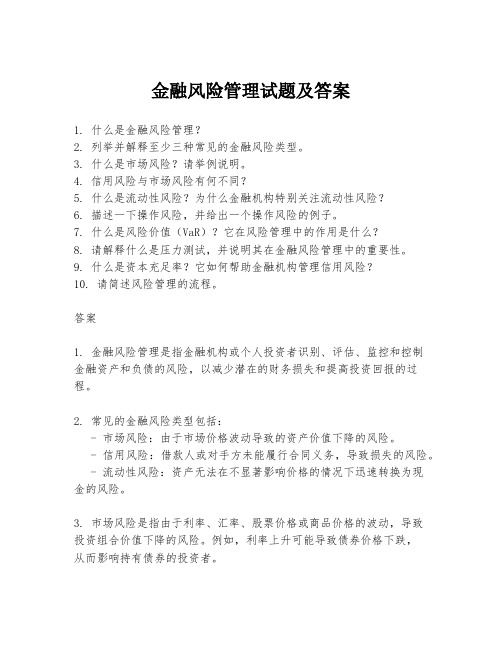

金融风险管理试题及答案

金融风险管理试题及答案1. 什么是金融风险管理?2. 列举并解释至少三种常见的金融风险类型。

3. 什么是市场风险?请举例说明。

4. 信用风险与市场风险有何不同?5. 什么是流动性风险?为什么金融机构特别关注流动性风险?6. 描述一下操作风险,并给出一个操作风险的例子。

7. 什么是风险价值(VaR)?它在风险管理中的作用是什么?8. 请解释什么是压力测试,并说明其在金融风险管理中的重要性。

9. 什么是资本充足率?它如何帮助金融机构管理信用风险?10. 请简述风险管理的流程。

答案1. 金融风险管理是指金融机构或个人投资者识别、评估、监控和控制金融资产和负债的风险,以减少潜在的财务损失和提高投资回报的过程。

2. 常见的金融风险类型包括:- 市场风险:由于市场价格波动导致的资产价值下降的风险。

- 信用风险:借款人或对手方未能履行合同义务,导致损失的风险。

- 流动性风险:资产无法在不显著影响价格的情况下迅速转换为现金的风险。

3. 市场风险是指由于利率、汇率、股票价格或商品价格的波动,导致投资组合价值下降的风险。

例如,利率上升可能导致债券价格下跌,从而影响持有债券的投资者。

4. 信用风险主要关注借款人或对手方的违约风险,而市场风险则关注市场因素对资产价值的影响。

市场风险通常可以通过对冲策略来管理,而信用风险则需要通过信用评估和信用衍生品等手段来控制。

5. 流动性风险是指在需要时无法以合理价格迅速出售资产的风险。

金融机构特别关注流动性风险,因为它可能导致资金链断裂,影响机构的正常运营。

6. 操作风险是指由于内部流程、人员、系统或外部事件的失败或不足导致的损失风险。

例如,一家银行的计算机系统遭受黑客攻击,导致客户数据泄露。

7. 风险价值(VaR)是一种衡量投资组合在一定置信水平下,预期在一定时间内可能遭受的最大损失的方法。

它帮助金融机构量化风险,制定风险限额。

8. 压力测试是一种评估金融机构在极端市场条件下的表现的方法。

金融风险管理练习试卷1(题后含答案及解析)

金融风险管理练习试卷1(题后含答案及解析) 题型有:1. 单项选择题 2. 多项选择题单项选择题共60题,每题1分。

每题的备选项中,只有l个最符合题意。

1.由于客户违约使银行债权得不到清偿而遭受损失的风险是( )。

A.信用风险B.操作风险C.法律风险D.声誉风险正确答案:A解析:由于客户违约使银行债权得不到清偿而遭受损失的风险是信用风险。

知识模块:金融风险管理2.银行在日常经营中因各种人为的失误、欺诈及自然灾害、意外事故引起的风险是( )。

A.操作风险B.市场风险C.利率风险D.国家风险正确答案:A解析:银行在日常经营中因各种人为的失误、欺诈及自然灾害、意外事故引起的风险是操作风险。

知识模块:金融风险管理3.银行无力满足客户提取存款和正常贷款需求而使银行收益和信誉蒙受损失的风险称为( )。

A.信誉风险B.存款和贷款风险C.流动性风险D.安全性风险正确答案:C解析:银行无力满足客户提取存款和正常贷款需求而使银行收益和信誉蒙受损失的风险称为流动性风险。

知识模块:金融风险管理4.巴塞尔银行监管委员会将银行业风险分为( )类型。

A.六种B.七种C.八种D.九种正确答案:C解析:巴塞尔银行监管委员会将银行业风险分为八种类型。

知识模块:金融风险管理5.由于客户违约使银行债权得不到清偿而遭受损失的风险是( )。

A.信用风险B.操作风险C.法律风险D.声誉风险正确答案:A解析:由于客户违约使银行债权得不到清偿而遭受损失的风险是信用风险。

知识模块:金融风险管理6.由于市场价格的变动而使银行遭受损失的风险称为( )。

A.流动性风险B.市场风险C.利率风险D.国家风险正确答案:B解析:由于市场价格的变动而使银行遭受损失的风险称为市场风险。

知识模块:金融风险管理7.银行在日常经营中因各种人为的失误、欺诈及自然灾害、意外事故引起的风险是( )。

A.操作风险B.市场风险C.利率风险D.国家风险正确答案:A解析:银行在日常经营中因各种人为的失误、欺诈及自然灾害、意外事故引起的风险是操作风险。

金融风险管理试卷

得分评卷人一、单项选择题(本大题共10小题,每小分,共10分)1.由于通货膨胀使货币贬值,证券公司实际收益下降,属于()风险。

A利率风险B政策性风险C购买力风险D信用风险2.()是金融机构流动性风险的内部来源。

A利率变动的影响B客户信用风险的影响C中央银行政策的影响D金融企业信誉的影响3.()称为短期远期利率风险。

A某种期限的短期利率在将来的系列利息期内面临的风险B某一期限的利率所面临的风险C某种期限的短期利率在将来的某个利息期内面临的风险D某一期限的利率在将来面临的外汇利率的风险4.下列描述正确的是()。

A预期市场利率走高,则将有效持续期缺口调整为正值B预期市场利率走高,则将有效持续期缺口调整为负值C预期市场利率走高,则将利率敏感性缺口调整为负值D预期市场利率走低,则将利率敏感性缺口调整为正值5.由于不完善或失灵的内部程序、人员和系统,或外部事件导致损失的风险称为()。

A操作风险B欺诈风险C政策风险D系统性风险6.增大金融交易成本属于金融风险的()效应。

A宏观经济效应B微观经济效应C政治效应D社会效应7.()不是金融风险的国际传递渠道。

A国际贸易渠道B国际金融渠道C人员流动渠道D相似传递渠道8.()是金融风险管理的内部组织形式。

A 股东大会B银行业协会C证券业协会D中央银行9.对面临暂时流动性困难的银行可以采取()危机处理的方式。

A接管B并购C破产D紧急救助10.商业银行风险产生的理论根源是()。

A商业银行存在大量不良贷款B金融监管的放松C商业银行的内在脆弱性D经济社会中存在泡沫现象得分评卷人二、多项选择题(本大题共5小题,每小题2分,共10分)11.按照金融风险的形态可以分为()。

A 信用风险B金融机构风险C流动性风险D利率风险 E 操作风险12.金融风险管理的程序包括()。

A 风险分类B风险识别C风险度量D 风险管理决策与实施E风险控制13.信用风险可以采用()管理策略。

A 预防策略B 规避策略C分散策略D 对冲策略E补偿策略14.()是金融监管的目标。

《金融风险管理》期末考试试卷附答案

《金融风险管理》期末考试试卷附答案一、单选题(本大题共20小题,每小题3分,共60分)1、促使或引起风险事件发生或风险事件发生时,致使损失增加、扩大的原因或条件是()A、风险因素B、风险事件C、风险成本D、风险损失2、由于个人的不诚实、不正直或不良企图导致风险事故的发生的因素是()A、心理风险因素B、有形风险因素C、道德风险因素D、实质风险因素3、在损失发生前,运用各种控制手段,力求消除各种隐患,减少风险诱因,降低损失的策略属于()A、风险融资B、风险控制C、风险转移D、风险补偿4、在金融风险管理活动中,明确风险的业务类别这项工作属于()A、金融风险的度量B、金融风险的监测C、风险报告D、金融风险的识别5、VaR方法最早用于度量()A、信用风险B、市场风险C、流动性风险D、操作风险6、通过多样化的投资来分散和降低风险的方法是()A、金融风险的分散B、金融风险的损失控制C、金融风险的转移D、金融风险的对冲7、经济主体根据一定原则,采取一定措施避开金融风险,以减少或避免由于风险引起的损失是()A、金融风险的规避B、金融风险的损失控制C、金融风险的预防D、金融风险的转移8、在信用风险分析常用的财务指标中,流动负债/有形净值属于()A、经营业绩指标B、偿债保障程度指标C、财务杠杆指标D、流动性指标9、下列方法中,属于现代信用风险度量方法的是()A、专家制度B、评级方法C、信用评分方法D、信用风险量化模型10、在现代信用风险度量方法中,以VaR为基础的是()A、信用风险量化模型B、信用监控模型C、信用风险计量模型D、信用风险组合模型11、在现代信用风险度量方法中,广泛使用信用等级转移分析和贷款集中度限制的是()A、信用风险计量模型B、信用风险量化模型C、信用监控模型D、信用风险组合模型12、在银行账户信用风险暴露分类中,个人住房抵押贷款属于()A、公司风险暴露B、股权风险暴露C、主权风险暴露D、零售风险暴露13、()指商业银行运用合格的抵质押品、净额结算、保证和信用衍生工具等方式转移或降低风险。

金融风险管理作业1答案

金融风险管理作业11、如何从微观和宏观两个方面理解金融风险?答:微观金融风险,是指微观金融机构在微观金融机构在从事金融经营活动和管理过程中,发生资产或收益损失的可能性。

宏观金融风险,是指整个金融体系面临的市场风险,当这种风险变为现实时,将会导致金融危机,不仅会对工商企业等经济组织产生深刻影响,对一国乃至全球金融及经济的稳定都会构成严重威胁。

2、金融风险与一般风险的区别是什么?答:风险(Risk)是指未来收益的不确定性。

金融风险(Financial Risk)是指金融变量的变动所引起的资产组合未来收益的不确定性。

3、金融风险有哪些特征?答:隐蔽性:如银行的金融风险往往只有通过资产结构、负债结构,以及它们彼此的比较才能发现,往往被日常的资产、负债的单方面活动所掩盖。

扩散性:因为银行之间的相互拆借。

加速性:因为客户的口口相传导致“挤兑”的现象。

可控性:通过分析资产负债可以提前发现问题,预先采取措施。

4、金融风险是如何分类的?答:对金融风险可以从形态和特征分类。

(1)按金融风险的形态划分信用风险。

信用风险又称违约风险,是指债务人无法还款或不愿还款而给债权造成损失的可能性。

流动性风险。

是指获取现金或现金等价物的能力出现了故障的风险。

利率风险。

是指由于利率变动导致经济主体收入减少或成本增加的风险。

汇率风险。

是指一个经济主体持有的意外的以外币计价的资产与负债等,因汇率的变动而发生损失的可能性。

操作风险。

是指由于企业或金融机构内部控制不健全或失效、操作失误等原因导致的风险。

政策风险。

是指国家政策变化给金融活动参与者带来的风险。

法律风险。

是指金融机构等因没有遵守法律条款,或法律条款不完善而引致的风险。

国家风险,是指由于国家政治、经济的重大变革导致的经济主体的风险。

(2)按金融风险其他特征分类按性质分类,系统性风险和非系统性风险。

前者靠分散投资无法避免。

按主体分类,金融机构、工商企业、居民、国家风险。

按层次分类,微观、宏观金融风险。

《金融风险管理》必考知识点期末考试题库1(含)答案解析

多选题

2. 市场风险包括以下哪些类型?( ACD )。

A、利率风险 B、负债风险 C、汇率风险

D、证券投资风险

【解析】:市场风险是由资产负债表内和表外的资产价值受到股票、利率、汇率的变动而发生反向

变化的风险,故市场风险只包括利率风险、汇率风险和证券投资风险。 判断题( :金融风险管理的主要类型之信用风险(P1 第七段最后一句)

2. 下列选项造成信用风险的因素有(ABD)。 A. 债务人的品质、能力 B. 经济恶化、公司倒闭 C. 利率波动 D. 产品滞销,公司经营不善

【解析】信用风险又称违约风险,是指交易对方信用状况和履约能力的变化导致债权人资产价值遭 损失的风险。而利率波动属于利率风险的范畴,利率风险属于市场风险的一种,因此不是造成信用 风险的因素。 【判断题】信用风险的存在情况 3. 信用风险是商业银行经营中最常见的一种风险,也是商业银行面临的最主要风险。(√) 【解析】信用风险主要存在于商业银行的贷款业务中,商业银行的许多非贷款业务同样存在信用风 险。公司经营状况恶化,易导致商业银行信用风险的频发。 单选题 以下关于利率风险的说法正确的有(B)

3.金融体系不稳定性理论认为金融风险的理论根源在于外在不稳定因素。(×)

【解析】:金融体系不稳定性理论认为,金融体系具有内在的不稳定性,这种不稳定性是金融风险 产生的理论根源。所以本题的外在不稳定因素错误。

单选题(4 分 1 题):

1.金融风险的预防是在( A ),经济主体采用的防范性措施。

A. 风险尚未导致损失之前

【解析】:C 金融市场和 E 中"整个经济"都是宏观层面的,因此 CE 属于宏观经济层面的功能,固 本题选 ABD。 判断题 结构风险也称为流动性风险,是由于流动性过度给经济主体造成损失的可能性。(×) 【解析】:该题目混淆内容,流动性风险是由于流动性过度给经济主体造成损失的可能性是正确的, 但是因为结构风险包含流动性风险与资本金结构风险。所以我们不能断定结构风险就是流动性风 险,固本题错误。

金融机构风险控制办法题库(题目+答案+解析)

金融机构风险控制办法题库(题目+答案+解析)金融机构风险控制办法题库(题目+答案+解析)题目1:金融机构风险控制的定义是什么?答案:金融机构风险控制是指金融机构通过风险识别、风险评估、风险防范和风险应对等一系列措施,对各类风险进行有效管理,以确保金融机构稳健经营和财务安全。

解析:金融机构风险控制是金融机构在经营过程中,为了保护自身资产和盈利能力,采取的一系列措施。

这些措施包括对风险的识别、评估和防范,以及应对风险的能力。

通过有效的风险控制,金融机构能够确保稳健经营和财务安全。

题目2:金融机构风险控制的主要目标是什么?答案:金融机构风险控制的主要目标是保持金融机构的稳健经营、维护股东权益、保障客户利益和遵守相关法规。

解析:金融机构风险控制的主要目标是确保金融机构能够持续稳健经营,同时保护股东和客户的利益。

此外,金融机构还需要遵守相关的法规要求,以保证合法合规经营。

题目3:金融机构风险控制的基本原则是什么?答案:金融机构风险控制的基本原则包括全面性、审慎性、及时性和有效性。

解析:金融机构在风险控制过程中应全面识别和评估各类风险,同时要审慎对待风险,及时采取相应的控制措施。

此外,风险控制措施应具备有效性,以确保金融机构能够有效地管理风险。

题目4:金融机构风险控制的流程主要包括哪些环节?答案:金融机构风险控制的流程主要包括风险识别、风险评估、风险防范和风险应对。

解析:风险识别是指识别金融机构在经营过程中可能面临的风险;风险评估是对识别出的风险进行分析和评估,确定风险的程度和可能性;风险防范是通过制定相应的政策和措施,预防风险的发生;风险应对是针对已发生的风险,采取相应的应对措施,减轻风险带来的影响。

题目5:如何提高金融机构风险控制的效率?答案:提高金融机构风险控制的效率,可以通过以下几个方面来实现:1. 建立完善的风险管理框架和制度;2. 加强风险管理人员的培训和专业素质;3. 采用先进的风险管理技术和工具;4. 建立健全内部监控和审计机制;5. 加强与其他部门的沟通与协作。

金融机构风险管理练习题

金融机构风险管理练习题1 2 3 4 5 6 7 8 9 10Chapter 6&7 testThe repricing gap model is a book value accounting based model.A positive repricing gap implies that a decrease in interest rates will cause interest expense to decrease more than the decrease in interest income. When a bank’s repricing gap is positive, net interest income is positively related to changes in interest rates.A bank with a negative repricing (or funding) gap faces reinvestment risk. The economic meaning of duration is the interest elasticity of a financial assets price.Duration considers the timing of all the cash flows of an asset by summing the product of the cash flows and the time of occurrence.Duration is equal to maturity when at least some of the cash flows are received upon maturity of the asset.Duration of a zero coupon bond is equal to the bond’s maturity. As interest rates rise, the duration of a consol bond decreases.For a given maturity fixed-income asset, duration decreases as the market yield increases.Multiple-Choice 1 The repricing gap approach calculates the gaps in each maturity bucket bysubtracting thea. current assets from the current liabilities.b. long term liabilities from the fixed assets.c. rate sensitive assets from the total assets.d. rate sensitive liabilities from the rate sensitive assets.e. current liabilities from tangible assets. 2 A positive gap implies that an increase in interest rates will cause _______ innet interest income.a. no changeb. a decreasec. an increased. an unpredictable changee. Either A or B. 3 If interest rates decrease 50 basis points for an FI that has a gap of +$5 million,the expected change in net interest income isa. + $2,500.b. + $25,000.c. + $250,000.d. - $250,000.e. - $25,000.4 The duration of a consol bond is a. less than its maturity.5678b. infinity.c. 30 years.d. more than its maturity.e. given by the formula D=1/1-R.An FI has financial assets of $800 and equity of $50. If the duration of assets is 1.21 years and the duration of all liabilities is 0.25 years, whatis the leverage-adjusted duration gap? a. 0.9000 years. b. 0.9600 years. c.0.9756 years. d. 0.8844 years.e. Cannot be determined.Calculate the duration of a two-year corporate bond paying 6 percentinterest annually, selling at par. Principal of $20,000,000 is due at the endof two years.a. 2 years.b. 1.91 years.c. 1.94 years.d. 1.49 years.e. 1.75 years.A $1,000 six-year Eurobond has an 8 percent coupon, is selling at par, and contracts to make annual payments of interest. The duration of this bond is4.99 years. What will be the new price using the duration model if interest rates increase to 8.5 percent? a. $23.10. b. $976.90. c. $977.23. d. $1,023.10.e. -$23.10.Calculating modified duration involvesa. dividing the value of duration by the change in the market interestrate. b. dividing the value of duration by 1 plus the interest rate.c. dividing the value of duration by discounted change in interest rates.d. multiplying the value of duration by discounted change in interest rates.e. dividing the value of duration by the curvature effect.Multiple Part QuestionsUse the following information to answer the next five (5) questions:The balance sheet of XYZ Bank. All figures in millions of US Dollars.Assets Liabilities 1 Short-term consumer loans (one-year maturity) 2 Long-term consumer loans 3 Three-month Treasury bills 4 Six-month Treasury notes 5 Three-year Treasury bond$ 150 1 Equity capital (fixed) 125 2 Demand deposits (two-year maturity)130 3 Passbook savings 135 4 Three-month CDs 170 5 Three-month bankers acceptances 120 6 Six-month commercial paper 140 7 One-year time deposits 8Two-year time deposits $970 $ 120 40 130 140 120 6 10-year, fixed-rate mortgages 7 30-year, floating-rate mortgages (rate adjusted every nine months) 1 2 3 4160 120 40 $970 Total one-year rate-sensitive assets is a. $540 million. b. $580 million. c. $555 million. d. $415 million. e. $720 million.Total one-year rate-sensitive liabilities is a. $540 million. b. $580million. c. $555 million. d. $415 million. e. $720 million.The cumulative one-year repricing gap (CGAP) for the bank is a. $25million. b. $-140 million. c. $15 million. d. $-150 million. e. $-15 million.The gap ratio is a. .015. b. -.015. c. .025. d. -.144. e. .154.5Suppose that interest rates rise by 2 percent on both RSAs and RSLs. The expected annual change in net interest income of the bank is a. -$300,000. b. $500,000. c. -$2,800,000. d. -$3,000,000. e. $300,000.Use the following information to answer the next three (2) questions:Consider a one-year maturity, $100,000 face value bond that pays a 6 percent fixed coupon annually. 6 What is the price of the bond if market interest rates are 7 percent? a. $99,050.15. b. $99,457.94. c. $99,249.62.d. $100,000.00.e. $99,065.42. 7 What is the price of the bond if market interest rates are 5 percent? a. $100,952.38. b. $101,238.10. c.$100,963.71. d. $100,000.00. e. $101,108.27.Use the following information to answer the next three (3) questions: Assets Par Rate Liabilities Par Rate Amount Amount 2-year commercial $400 million 10 % 1-year CDs, $450 7 % loans, annual fixed annual fixed million rate, at par rate, at par 1-year Treasury bills $100 million Net Worth $50 million 8 What is the duration of the commercial loans? a. 1.00 years. b.2.00 years. c. 1.73 years. d. 1.91 years. e. 1.50 years. 9 What is the FI's leverage-adjusted duration gap? a. 0.91 years. b. 0.83 years.10c. 0.73 years.d. 0.50 years.e. 0 years.What is the FI's interest rate risk exposure? a. Exposed to increasing rates. b. Exposed to decreasing rates. c. Perfectly balanced.d. Exposed to long-term rate changes.e. Insufficient information.Use the following information to answer the next three (2) questions:Consider a five-year, 8 percent annual coupon bond selling at par of$1,000. 11 12What is the duration of this bond? a. 5 years. b. 4.31 years. c. 3.96 years. d. 5.07 years.e. Not enough information to answer.If interest rates increase by 20 basis points, what is the approximate change in the market price using the duration approximation? a. -$7.98. b. -$7.94. c. -$3.99. d. +$3.99. e. -$7.94.感谢您的阅读,祝您生活愉快。

《金融风险管理》习题集

《金融风险管理》习题集《金融风险管理》习题集第一章、中国金融业概论一、名词解释1、“大一统”的银行体系2、双重银行体系3、政策性银行4、信用合作社5、汇率并轨二、单项选择1、在中国银行业的分类中,下列选项属于“国有银行”的是()A.商业银行B.农村商业银行C.政策性银行D.信用合作社2、2001年中国成立了第一家政策性保险公司,它是()A.中国人民保险公司B.太平洋保险公司C.平安保险公司D.中国进出口信用保险公司3、下列选项中不属于我国按照债券品种分类的市场是()A.银行间债券市场B.债券柜台交易市场C.交易所债券市场D.凭证式债券市场4、下列监管职能中,自2003年4月起不属于人民银行监管范围的有()A.不良贷款及银行的资本充足率B.银行间拆借市场C.银行间债券市场D.执行存款准备金的管理5、根据中国对世贸组织的承诺下列城市中,属于第一批开放的城市是()A.成都B.大连C.南京D.北京6、《境外金融机构投资入股中金融机构管理办法》中规定,境外金融投资机构中资机构入股比例的上限是()A.15%B.20%C.25%D.30%7、下列选项中,不属于中国银行业三个有待解决的问题是()A.使应该中国银行的资本充足率达到《巴塞尔协议Ⅱ》的要求B.改革四大国有银行C.改革农村信用合作社D.充足小型银行和困难银行8、保监会对设立中外合资寿险公司中外资参股比例的规定是()A.不得超过25%B.不得超过30%C.不得超过50%D.不得超过51%9、1995年《中国商业银行法》中第一次明确规定所有商业银行的资本充足率不得低于()A.2%B.4%C.6%D.8%10、下列选项中,不属于《巴塞尔协尔Ⅱ》的三大核心内容的是()A.信息披露B.资本充足率要求C.金融监管D.市场约束三、简答题1、请简要回答中国金融业的发展过程。

2、请简要回答中国银监会的主要职能与目标。

3、请简要回答外资银行进入中国的五个阶段。

4、请简要回答中国监管当局目前关于资本充足率的规定。

金融风险管理题库

一、单选题(以下各题给出的四个选项中,只有一项符合题目要求。

不选、错选均不得分。

)1. 风险是指( )。

DA 损失的大小B 损失的分布C 未来结果的不确定性D 收益的分布2.关于风险,下列说法错误的是()。

BA.风险和收益成正比B.风险是一个事后概念,损失是一个事前概念C.风险既是损失的来源,同时也是盈利的基础D.风险绝不等同于损失本身3.证券组合理论体现在以下哪个阶段?()CA.资产负债风险管理阶段B.负债风险管理阶段C.资产风险管理阶段D.全面风险管理阶段4.商业银行风险管理发展的4个阶段依次为()。

AA.资产风险管理阶段→负债风险管理阶段→资产负债风险管理阶段→全面风险管理阶段B负债风险管理阶段→资产风险管理阶段→资产负债风险管理阶段→全面风险管理阶段C.资产负债风险管理阶段→资产风险管理阶段→负债风险管理阶段→全面风险管理阶段D.资产风险管理阶段→资产负债风险管理阶段→负债风险管理阶段→全面风险管理阶段5.金融衍生产品、金融工程等一系列专业技术逐渐应用于商业银行的风险管理,这属于商业银行( )。

AA.资产风险管理阶段B.负债风险管理阶段C.资产负债风险管理阶段D.全面风险管理阶段6.下列属于按风险诱发原因分类的是()。

CA.资产风险和负债风险B.系统性风险和非系统性风险C.信用风险和市场风险D.纯粹风险和投机风险7.巴塞尔委员会以()方式把商业银行面临的风险分为八大类。

DA.损失结果B.风险事故C.风险发生的范围D.诱发风险的原因8.关于国家风险,下列说法错误的是( )。

AA.在同一个国家范围内的经济金融活动不存在国家风险B.国家风险分为政治风险、社会风险、经济风险C.国家风险是由债务人所在国家的行为引起的D.个人一般不会遭受国家风险9.由于形成的原因更加复杂和广泛,通常被视为一种综合风险的是()。

AA.市场风险B.信用风险C.流动性风险D.操作风险10.国家风险是由()引起的,超出了()的控制范围。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1.What is the process of asset transformation performed by a financial institution? Whydoes this process often lead to the creation of interest rate risk? What is interest rate risk?Asset transformation by an FI involves purchasing primary assets and issuing secondary assets as a source of funds. The primary securities purchased by the FI often have maturity and liquidity characteristics that are different from the secondary securities issued by the FI. For example, a bank buys medium- to long-term bonds and makes medium-term l oans with funds raised by issuing short-term deposits.Interest rate risk occurs because the prices and reinvestment income characteristics oflong-term assets react differently to changes in market interest rates than the prices and interest expense characteristics of short-term deposits. Interest rate risk is the risk incurred by an FI when the maturities of its assets and liabilities are mismatched.2.The sales literature of a mutual fund claims that the fund has no riskexposure since it invests exclusively in federal government securities that are free of default risk. Is this claim true? Explain why or why not. Although the fund's asset portfolio is comprised of securities with no default risk, the securities are exposed to interest rate risk. For example, if interest rates increase, the market value of the fund's Treasury security portfolio will decrease. Further, if interest rates decrease, the realized yield on these securities will be less than the expected rate of return because of reinvestment risk. In either case, investors who liquidate their positions in the fund may sell at a Net Asset Value (NAV) that is lower than the purchase price.3. What is market risk? How do the results of this risk surface in the operating performanceof financial institutions? What actions can be taken by FI management to minimize the effects of this risk?Market risk is the risk incurred from assets and liabilities in an FI’s trading book due to changes in interest rates, exchange rates, and other prices. Market risk affects any firm that trades assets and liabilities. The risk can surface because of changes in interest rates, exchange rates, or any other prices of financial assets that are traded rather than held on the balance sheet. Market risk can be minimized by using appropriate hedging techniques such as futures, options, and swaps, and by implementing controls that limit the amount of exposure taken by market makers.4. What is credit risk? Which types of FIs are more susceptibl e to this type of risk?Why?Credit risk is the risk that promised cash flows from loans and securities held by FIs may not be paid in full. FIs that lend money for long periods of time, whether as loans or by buying bonds, are more susceptible to this risk than those FIs that have short investment horizons. For example, life insurance companies and depository institutions generally must wait a longer time for returns to be realized than money market mutual funds and property-casualty insurance companies.5. What is foreign exchange risk? What does it mean for an FI to be net long in foreignassets? What d oes it mean for an FI to be net short in foreign assets? In each case, what must happen to the foreign exchange rate to cause the FI to suffer losses? Foreign e xchange risk is the risk that exchange rate changes can affect the value of an FI’s assets and liabilities denominated in non-domestic currencies. An FI is net long inforeign assets when the foreign currency-denominated assets exceed the foreigncurrency denominated liabilities. In this case, an FI will suffer potential losses if thedomestic currency strengthens relative to the foreign currency when repayment ofthe assets will occur in the foreign currency. An FI is net short in foreign assetswhen the foreign currency-denominated liabilities exceed the foreign currencydenominated assets. In this case, an FI will suffer potential losses if the domesticcurrency weakens relative to the foreign currency when repayment of the liabilitieswill occur in the domestic currency.6. What is the repricing gap? In using this model to evaluate interest rate risk, what is meantby rate sensitivity? On what financial performance variable does the repricing modelfocus? Explain.The repricing gap is a measure of the difference between the dollar value of assetsthat will reprice and the dollar value of liabilities that will reprice within a specifictime period, where reprice means the potential to receive a new interest rate. Rate sensitivity represents the time interval where repricing can occur. The modelfocuses on the potential changes in the net interest income variable. In effect, if interest rates change, interest income and interest expense will change as the various assets and liabilities are repriced, that is, receive new interest rates.e the following information about a hypothetical government security dealer named M.P. Jorgan. Marketyields are in parenthesis, and amounts are in millions. 8.11Assets Liabilities and EquityCash $10 Overnight Repos $1701 month T-bills (7.05%) 75 Subordinated debt3 month T-bills (7.25%) 75 7-year fixed rate (8.55% 1502 year T-notes (7.50%) 508 year T-notes (8.96%) 1005 year munis (floating rate)(8.20% reset every 6 months) 25 Equity 15Total Assets $335 Total Liabilities & Equity $335a. What is the funding or repricing gap if the planning period is 30 days? 91 days?2 years? Recall that cash is a noninterest-earning asset.Funding or repricing gap using a 30-day planning period = 75 - 170 = -$95million.Funding gap using a 91-day planning period = (75 + 75) - 170 = -$20 million.Funding gap using a two-year planning period = (75 + 75 + 50 + 25) - 170 =+$55 million.b. What is the impact over the next 30 days on net interest income if all interestrates rise 50 basis points? Decrease 75 basis points?Net interest income will decline by $475,000. ∆NII = FG(∆R) = -95(.005) = $0.475m.Net interest income will increase by $712,500. ∆NII = FG(∆R) = -95(.0075) = $0.7125m.c.The following one-year runoffs are expected: $10 million for two-yearT-notes, and $20 million for eight-year T-notes. What is the one-yearrepricing gap?Funding or repricing gap over the 1-year planning period = (75 + 75 + 10 + 20 +25) - 170 = +$35 million.d. If runoffs are considered, what is the effect on net interest income atyear-end if interest rates rise 50 basis points? Decrease 75 basis points?Net interest income will increase by $175,000. ∆NII = FG(∆R) = 35(0.005) = $0.175m.Net interest income will decrease by $262,500, ∆NII = FG(∆R) = 35(-0.0075) = -$0.2625m.8. Consumer Bank has $20 million in cash and a $180 million loan portfolio. Theassets are funded with demand deposits of $18 million, a $162 million CD and $20 million in equity. The loan portfolio has a maturity of 2 years, earnsinterest at the annual rate of 7 percent, and is amortized monthly. The bankpays 7 percent annual interest on the CD, but the interest will not be paid until the CD matures at the end of 2 years.a. What is the maturity gap for Consumer Bank?M A = [0*$20 + 2*$180]/$200 = 1.80 yearsM L = [0*$18 + 2*$162]/$180 = 1.80 yearsMGAP = 1.80 – 1.80 = 0 years.b. Is Consumer Bank immunized or protected against changes in interest rates?Why or why not?It is tempting to conclude that the bank is immunized because the maturity gap is zero. However, the cash flow stream for the loan and the cash flow stream for the CD are different because the loan amortizes monthly and the CD paysannual interest on the CD. Thus any change in interest rates will affect theearning power of the loan more than the interest cost of the CD.c. Does Consumer Bank face interest rate risk? That is, if market interestrates increase or decrease 1 percent, what happens to the value of the equity?The bank does face interest rate risk. If market rates increase 1 percent, thevalue of the cash and demand deposits does not change. However, the value ofthe loan will decrease to $178.19, and the value of the CD will fall to $159.01.Thus the value of the equity will be ($178.19 + $20 - $18 - $159.01) = $21.18.In this case the increase in interest rates causes the market value of equity toincrease because of the reinvestment opportunities on the loan payments.If market rates decrease 1 percent, the value of the loan increases to $181.84,and the value of the CD increases to $165.07. Thus the value of the equitydecreases to $18.77.d. How can a decrease in interest rates create interest rate risk?The amortized loan payments would be reinvested at lower rates. Thus eventhough interest rates have decreased, the different cash flow patterns of the loanand the CD have caused interest rate risk.9. You have discovered that the price of a bond rose from $975 to $995 when theYTM fell from 9.75 percent to 9.25 percent. What is the duration of the bond? We know years D years R R P P D 5.45.40975.1005.97520)1(=⇒-=-=+∆∆=- 10. If you use only duration to immunize your portfolio, what three factors affectchanges in the net worth of a financial institution when interest rates change?The change in net worth for a given change in interest rates is given by the followingequation:[]AL k where R R A k D D E L A =+∆--=∆1**Thus, three factors are important in determining ∆E.1) [D A - D L k ] or the leveraged adjusted duration gap. The larger this gap, the more exposed is the FI to changes in interest rates.2) A, or the size of the FI. The larger is A , the larger is the exposure to interest rate changes.3) ΔR /1 + R , or interest rate shocks. The larger is the shock, the larger is the interest rate risk exposure.11. What is meant by daily earnings at risk (DEAR )? What are the three measurablecomponents? What is the price volatility component?DEAR or Daily Earnings at Risk is defined as the estimated potential loss of a portfolio's value over a one-day unwind period as a result of adverse moves in market conditions, such as changes in interest rates, foreign exchange rates, and market volatility. DEAR is comprised of (a) the dollar value of the position, (b) the price sensitivity of the assets to changes in the risk factor, and (c) the adverse move in the yield. The product of the price sensitivity of the asset and the adverse move in the yield provides the price volatility component.12. Bank Two has a portfolio of bonds with a market value of $200 million. The bonds have anestimated price volatility of 0.95 percent. What are the DEAR and the 10-day VAR for these bonds?Daily earnings at risk (DEAR) =($ Value of position) x (Price volatility)= $200 million x .0095= $1.9million, or $1,900,000Value at risk (VAR) = DEAR x √N = $1,900,000 x √10= $1,900,000 x 3.1623 = $6,008,327.5513. The following are the foreign currency positions of an FI, expressed in dollars.15.5 Currency Assets Liabilities FX Bought FX Sold Swiss franc (SF) $125,000 $50,000 $10,000 $15,000British pound (£) 50,000 22,000 15,000 20,000Japanese yen (¥) 75,000 30,000 12,000 88,000a. W hat is the FI’s net exposure in Swiss francs?Net exposure in Swiss francs = $70,000.b. What is the FI’s net exposure in British pounds?Net exposure in British pounds = $23,000.c. What is the FI’s net exposure in Japanese yen?Net exposure in Japanese yen = -$31,000d. What is the expected loss or gain if the SF exchange rate appreciates by 1percent?If assets are greater than liabilities, then an appreciation of the foreign exchange rates will generate a gain = $70,000 x 0.01 = $7,000.e. What is the expected loss or gain if the £ exchange rate appreciates by 1percent?Gain = $23,000 x 0.01 = $230f. What is the expected loss or gain if the ¥ exchange rate appreciates by 2 percent?Loss = -$31,000 x 0.02 = -$6,200⏹练习1:⏹Calculate the repricing gap and the impact on net interest income of a 1 percent increasein interest rates for each of the following positions:⏹⏹Rate-sensitive assets = $200 million. Rate-sensitive liabilities = $100 million.Repricing gap = RSA RSL = $200 $100 million = +$100 million.NII = ($100 million)(.01) = +$1.0 million, or $1,000,000.⏹Rate-sensitive assets = $100 million. Rate-sensitive liabilities = $150 million.Repricing gap = RSA RSL = $100 $150 million = -$50 million.NII = (-$50 million)(.01) = -$0.5 million, or -$500,000.⏹Rate-sensitive assets = $150 million. Rate-sensitive liabilities = $140 million.Repricing gap = RSA RSL = $150 $140 million = +$10 million.NII = ($10 million)(.01) = +$0.1 million, or $100,000.⏹练习2:⏹Which of the following assets or liabilities fit the one-year rate or repricing sensitivitytest?⏹⏹91-day U.S. Treasury bills Yes⏹1-year U.S. Treasury notes Yes⏹20-year U.S. Treasury bonds No⏹20-year floating-rate corporate bonds with annual repricing Yes⏹30-year floating-rate mortgages with repricing every two years No⏹30-year floating-rate mortgages with repricing every six months Yes⏹Overnight fed funds Yes⏹9-month fixed rate CDs Yes⏹1-year fixed-rate CDs Yes⏹5-year floating-rate CDs with annual repricing Yes⏹Common stock No⏹练习3:Consider the following balance sheet for WatchoverU Savings, Inc. (in millions): Assets Liabilities and EquityFloating-rate mortgages Demand deposits(currently 10% annually) $50 (currently 6% annually) $70 30-year fixed-rate loans Time deposits(currently 7% annually) $50 (currently 6% annually $20Equity $10 Total Assets $100 Total Liabilities & Equity $100a. What is WatchoverU’s expected net interest income at year-end?Current expected interest income: $5m + $3.5m = $8.5m.Expected interest expense: $4.2m + $1.2m = $5.4m.Expected net interest income: $8.5m - $5.4m = $3.1m.b. What will be the net interest income at year-end if interest rates rise by 2 percent?After the 200 basis point interest rate increase, net interest income declines to:50(0.12) + 50(0.07) - 70(0.08) - 20(.06) = $9.5m - $6.8m = $2.7m, a decline of$0.4m.c. Using the cumulative repricing gap model, what is the expected net interestincome for a 2 percent increase in interest rates?Wachovia’s' repricing or funding gap is $50m - $70m = -$20m. The change innet interest income using the funding gap model is (-$20m)(0.02) = -$.4m.练习4:M A = [0*20 + 5*60 + 200*30]/320 = 19.69 years, and M L = [0*140 + 1*160]/300 = 0.533. Therefore the maturity gap = MGAP = 19.69 – 0.533 = 19.16 years. Nearby bank is exposed to an increase in interest rates. If rates rise, the value of assets will decrease much more than the value of liabilities.练习5M A = [0*20 + 15*160 + 30*300]/480 = 23.75 years.M L = [0*100 + 5*210 + 20*120]/430 = 8.02 years.MGAP = 23.75 – 8.02 = 15.73 years.Five-year BondPar value = $1,000 Coupon rate = 15% Annual paymentsR = 9% Maturity = 5 yearsTime Cash Flow PV of CF PV of CF x t1 $150 $137.62 $137.622 $150 $126.25 $252.503 $150 $115.83 $347.484 $150 $106.26 $425.065 $1,150 $747.42 $3,737.10$1,233.38 $4,899.76 Duration = $4899.76/1,233.38= 3.97 ≈ 4 years⏹ 练习The duration of the capital note is 1.8975 years.Two-year Capital Note (values in thousands of $s)Par value = $900 Coupon rate = 7.25% Semiannual paymentsR = 7.25% Maturity = 2 years Time Cash Flow PV of CF PV of CF x t0.5 $32.625 $31.48 $15.741 $32.625 $30.38 $30.381.5 $32.625 $29.32 $43.982 $932.625 $808.81 $1,617.63$900.00 $1,707.73 Duration = $1,707.73/$900.00 =1.8975The leverage-adjusted duration gap can be found as follows:[]years k D D gap duration adjusted Leverage L A 23.8000,000,1$000,900$8975.194.9=-=-=-⏹ Follow Bank has a $1 million position in a five-year, zero-coupon bond with a face valueof $1,402,552. The bond is trading at a yield to maturity of 7.00 percent. Thehistorical mean change in daily yields is 0.0 percent, and the standard deviation is 12basis points.⏹⏹ a. W hat is the modified duration of the bond?MD = 5 ÷ (1.07) = 4.6729 years⏹ b. W hat is the maximum adverse daily yield move given that we desire no more than a5 percent chance that yield changes will be greater than this maximum?Potential adverse move in yield at 5 percent = 1.65 = 1.65 x 0.0012 = .001980⏹ c. What is the price volatility of this bond?Price volatility = -MD x potential adverse move in yield= -4.6729 x .00198 = -0.009252 or -0.9252 percent⏹ d. W hat is the daily earnings at risk for this bond?DEAR = ($ value of position) x (price volatility)= $1,000,000 x 0.009252 = $9,252⏹The DEAR for a bank is $8,500. What is the VAR for a 10-day period? A 20-day period?Why is the VAR for a 20-day period not twice as much as that for a 10-day period?For the 10-day period: VAR = 8,500 x [10]½ = 8,500 x 3.1623 = $26,879.36For the 20-day period: VAR = 8,500 x [20]½= 8,500 x 4.4721 = $38,013.16The reason that VAR20 (2 x VAR10) is because *20+½ (2 x *10+½). The interpretation is that the daily effects of an adverse event become less as time moves farther away from the event.。