2009NBF基础班讲义(第2讲)

2009 B-2 Class Notes

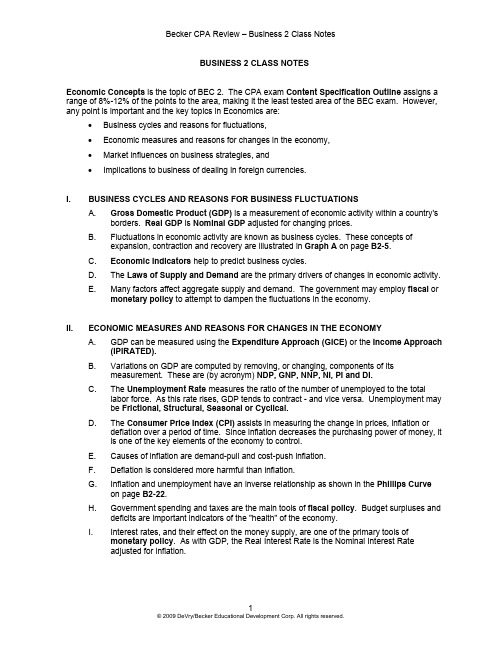

BUSINESS 2 CLASS NOTESEconomic Concepts is the topic of BEC 2. The CPA exam Content Specification Outline assigns a range of 8%-12% of the points to the area, making it the least tested area of the BEC exam. However, any point is important and the key topics in Economics are:•Business cycles and reasons for fluctuations,•Economic measures and reasons for changes in the economy,•Market influences on business strategies, and•Implications to business of dealing in foreign currencies.I. BUSINESS CYCLES AND REASONS FOR BUSINESS FLUCTUATIONSA. Gross Domestic Product (GDP) is a measurement of economic activity within a country'sborders. Real GDP is Nominal GDP adjusted for changing prices.B. Fluctuations in economic activity are known as business cycles. These concepts ofexpansion, contraction and recovery are illustrated in Graph A on page B2-5.C. Economic Indicators help to predict business cycles.Laws of Supply and Demand are the primary drivers of changes in economic activity.D. TheE. Many factors affect aggregate supply and demand. The government may employ fiscal ormonetary policy to attempt to dampen the fluctuations in the economy.II. ECONOMIC MEASURES AND REASONS FOR CHANGES IN THE ECONOMYA. GDP can be measured using the Expenditure Approach (GICE) or the Income Approach(IPIRATED).B. Variations on GDP are computed by removing, or changing, components of itsmeasurement. These are (by acronym) NDP, GNP, NNP, NI, PI and DI.Unemployment Rate measures the ratio of the number of unemployed to the totalC. Thelabor force. As this rate rises, GDP tends to contract - and vice versa. Unemployment maybe Frictional, Structural, Seasonal or Cyclical.Consumer Price Index (CPI) assists in measuring the change in prices, inflation orD. Thedeflation over a period of time. Since inflation decreases the purchasing power of money, itis one of the key elements of the economy to control.E. Causes of inflation are demand-pull and cost-push inflation.F. Deflation is considered more harmful than inflation.G. Inflation and unemployment have an inverse relationship as shown in the Phillips Curveon page B2-22.H. Government spending and taxes are the main tools of fiscal policy. Budget surpluses anddeficits are important indicators of the "health" of the economy.I. Interest rates, and their effect on the money supply, are one of the primary tools ofmonetary policy. As with GDP, the Real Interest Rate is the Nominal Interest Rateadjusted for inflation.J. In general, if the economy is in a decline, pumping money into the economy or making money "cheaper" will help to make the economy expand. Taking money out of theeconomy, or making it more expensive, will tend to slow down an economy that may berising too rapidly.ON BUSINESS STRATEGIESINFLUENCESIII. MARKETA. The ability of a firm to achieve success is a direct result of how well its strategic plan fitsthe market in which it operates and how well the firm carries out its plan.B. Strategic positioning involves defining the mission, identifying the strategy and criticalsuccess factors, and analyzing those factors by SWOT - Strengths, Weaknesses,Opportunities, and Threats.C. Once a strategic plan is implemented, it must be continually evaluated and revised whennecessary.fundamental law of demand holds that the price of a product and the quantityD. Thedemanded of that product are inversely related. Factors that will shift demand, other thanprice, are contained in the mnemonic WRITEN.fundamental law of supply holds that the price of a product and the quantity suppliedE. Theof that product are positively related. Factors, other than price, that will shift supply arecontained in the mnemonic ECOST.F. The interaction of supply and demand in an open market will determine the equilibriumprice of a product. If either the supply or demand curves shift, the equilibrium price willincrease or decrease.G. Demand for a product is said to be elastic if an increase in the price of the product willreduce total revenue; however, a price decrease will increase total revenue. If the price ofsuch a product increases, consumers will shift to substitute products.H. Demand for a product is said to be inelastic if an increase in the price of the product willincrease total revenue, and vice versa. If there are no available substitute products,consumers will have to pay the higher price for the product.I. Cross elasticity of demand measures the percentage change in the quantity demanded ofone good caused the by the price change of another. Positive cross elasticity =Substitute. Negative cross elasticity = Complementary.J. Income elasticity of demand measures the percentage change in quantity demanded for a product caused by a change in income. Positive income elasticity = Normal. Negativeincome elasticity = Inferior.K. To control an economy, a government may employ tools such as price ceilings, price floors, and subsidies.L. Explicit costs are "out-of-pocket," while implicit costs may include economic, or opportunity, costs. The difference between economic and accounting profits is similar innature.theshort run, costs are either fixed or variable. In the long run, all costs tend to be M. Invariable. Marginal cost is "the cost of producing one more unit."N. The four types of market structure are perfect competition, monopolies, monopolistic competition and oligopolies. The Market Structure Table on page B2-54 summarizes thedifferences.O. Economies are systems of markets that driven by factors of production: Capital, Entrepreneurial talent, Land and Labor (CELL).value chain analysis, a firm will analyze its flow of activities to assess how it creates P. Invalue in the marketplace.Q. The competitive strategy of a firm may focus on cost leadership or differentiation to a broad or narrow market. A firm may also aim to be a best cost provider.R. A firm may cooperate with others in its supply chain to more efficiently meet its market demand.IV. IMPLICATIONS OF DEALING IN FOREIGN CURRENCIESA. In addition to the political and economic risks of doing business in a foreign country, entitiesthat operate internationally face the risks of monetary exchange rate fluctuation. Theserisks are categorized as transaction, economic and translation.B. Exchange rates are influenced by trade-related and financial factors.C. Transaction exposure is the potential that an organization could suffer economic loss orexperience economic gain upon settlement of individual transactions as a result of changesin exchange rates.D. Economic exposure is the potential that the present value of an entity's cash flows couldincrease or decrease as the result of changes in the exchange rate.E. Translation exposure is the potential that the entity's financial statement components willchange as a result of exchange rate fluctuations and defines the effect of those changes inthe entity's earnings or other comprehensive income.F. Hedging techniques, such as future, forward and money market, will mitigate transactionrisks with receivables or payables.G. Valuation of transactions with foreign subsidiaries involves transfer pricing techniquesdesigned to minimize local taxation while remaining within local guidelines.For an approximate 10-point subject area, there is a lot of material to cover in BEC2. This outline is designed to highlight the important concepts that are covered in more detail in the text. Candidates are not expected to be Nobel Prize-winning economists; however, a good working knowledge of both macroeconomics and microeconomics is required. A basic understanding of the types of hedge instruments and their uses in business transactions is also necessary. The Appendices cover value chain analysis, supply chain management, and foreign currency dealings in more detail.。

2009-ob2态度

2.1.1 年龄 2.1.2 性别 2.1.3 婚姻 2.1.4 任职时间

传记特征:年龄

年龄 年龄 年龄

+ —

离职率 缺勤率 生产率

年龄 +

或U型

?

年龄 年龄

— +

可避免缺勤 不可避免缺勤

?

专业人士工作满意度 非专业人士工作满意度 先降低,至中年后升高

年龄

或U型

工作满意度

年龄

背景特征:性别

性別 性別 性別 性別 ? 女>男 ? ? 离职率 缺勤率 生产率 工作满意度

传记特征:婚姻

已婚〈 未婚

婚姻

已婚〈 未婚

离职率 缺勤率

?

婚姻 婚姻

已婚 〉 未婚

生产率 工作满意度

婚姻

传记特征:任职时间

_

任职时间

_

离职率 缺勤率

+

任职时间 任职时间

+

生产率 工作满意度

任职时间

2.2 能 力 (Ability) )

能力是从事各种活动、适应生存所必需且 影响活动效果的心理特征的总和。 对于一个管理者,重要的是应了解每个人 的能力差别与特长,使每个人的能力在工 作中得到最大发挥,于人、于组织均有利。

研究发现

购物单A 1听发酵粉 2块面包 1磅速溶咖啡 1.5磅碎牛肉 5磅土豆 一窜胡萝卜

购物单B 1听发酵粉 2块面包 1磅新鲜颗粒咖啡 1.5磅碎牛肉 5磅土豆 一窜胡萝卜

一个有经验的、 一个有经验的、 勤劳的、 勤劳的、慷慨 的讲究饮食的、 的讲究饮食的、 有家庭观念和 喜欢烹调的人

一个懒惰的、 一个懒惰的、吝啬 生活无计划的、 的、生活无计划的、 没有家庭观念的、 没有家庭观念的、 不称职的人

2009年二级建造师建设工程施工管理讲义91327

2022/2/3

二级建造师考前培训(péixùn) by CZZ

紧前工作 — 1 1 3 2 4,5 6 4,5 7,8

2022/2/3

二级建造师考前培训(péixùn) by

CZZ

第二十五页,共六十六页。

B

E

3

F G

6

A

1

2

5

CD4源自I78H

2022/2/3

二级建造师考前培训(péixùn) by

CZZ

第二十六页,共六十六页。

案例(àn lì)讨论—绘制网络图

内部装饰

粉刷完工

2 基础14 3 5

4 二6层地板 6 12

7 10

98

10

1-2-3-4-6-7-9-10 1-2-3-4-7-9-10 1-2-3-4-7-8-9-10 1-2-3-4-6-7-8-9-10 1-2-3-4-5-7-9-10 1-2-3-4-5-7-8-9-10 1-2-3-4-5-8-9-10 1-2-5-7-9-10 1-2-5-7-9-10

《建设(jiànshè)工程施工管理》又有区别于《建设工 程项目管理》的方面,后者着眼于全方位、全过 程介绍工程项目管理各方面知识,前者主要介绍 施工阶段的管理,因此,在二级建造师执业资格 考试中要重点掌握施工阶段的管理知识。

考虑到本课目只进行客观题考试,复习时,要严 格依据考试用书进行准备。在对考试用书进行多 遍疏理的基础上,适当做一些复习应考题是很有 必要的,这样可以检验知识的掌握程度,巩固所 学知识。

2009分析力学讲义

取如图所示X 为广义坐标

xx y 2 2 l x

2 2 2 2

A

y

T 1 m( x y ) 1 mx (1 2 x 2 ) 2 2 l x 2 2 ml x 2 2 2(l x )

B

x

V mg l x kx

2 2

杆作刚体一般运动

T2 T2c T ......(2)

' 2

质心动能

) 2 (a sin ) 2 V (a

2 c

1 ma2 2 1 ma2 sin 2 2 ......(3) T2c 2 2

相对质心运动为三维转动

1 ma2 I I 0 x cos Ix z y 3 y sin T ' 1 ( I 2 I 2 I 2 ) 2 x x y y z z 2 z 1 ma 2 ( 2 2 cos 2 )......( 4) 6 1 ma2 2 1 ma2 sin 2 2 1 ma2 2 T2c T1 2 2 2

p 2 2 H kl sin mgl cos 2 2ml

2

p 2 2 H kl sin mgl cos 2 2ml

2

H p p ml 2 H 2kl2 sin cos mgl sin p p 2 ml

L T V

1 ml 2 2 mgl cos 2

kl sin

2 2

L T V kl sin L mgl sin 2kl 2 sin cos d ( L ) ml 2 L ml 2 dt

2009-2-f6

金融危机历史、应对经验和对我国启示于泽刘凤良摘要:通过综述现有学者对于金融危机历史的研究,说明本次次贷危机引发的全球金融危机与之前的金融危机是类似的。

因此,我们可以从以往的政策和经济史中获得应对这次危机的经验。

现有研究发现,应对危机的各种短期政府政策并没有有效地降低危机的深度和加快危机复苏,这可能是因为在危机来临的时候,对于生产率提高起作用的是产业间资源调整和新产业发展。

政府的短期政策虽然能够帮助稳定一些信贷关系,但是因为没有对于外部重构的关注,所以作用不大。

因此,走出危机最重要的是进行产业结构调整,同时引入新行业。

从长期来看,新产业发展是最根本的解决道路。

所以,此次世界经济走出低谷也需要新产业的发展。

我们国家虽然没有金融危机,为了应对金融危机带来的衰退,需要在短期内稳定经济,中期调整产业结构,促进服务业等发展,长期发展新产业,对于新能源等行业有所为有所不为。

关键词:金融危机、生产率、新能源一、引言2007年以来,美国次贷危机引发了全球金融恐慌和经济衰退,我国也出台了各种政策积极应对。

而只有理解此次危机的根源,才能较为准确地判断世界经济走势,并制定我国相应的经济振兴策略。

关于此次金融和经济危机的原因,各国学者进行了大量研究。

早期的研究单纯认为危机来自于金融衍生品的滥用,并对金融家的贪婪和欺诈加以谴责。

Hellwig (2008)认为2000年以来,在美国低利率和股市并不繁荣的刺激下,投资者开始寻找可以提供高风险的资产,银行等金融机构寻找新的盈利点。

因此,可以同时满足二者的抵押贷款证券化高速发展。

抵押贷款证券化分散了来自于房地产投资的风险,但也产生了系统性风险。

特别投资主体(SIVs)的期限错配严重。

SIVs 投资的是长期资产,而其融资方式则是短期债务。

当融资出现问题时,就必须抛售资产。

而在利用市值计算的会计准则下,就会压低其他SIVs的资产,导致其他SIVs的抛售行为,压低整个市场的资产价格,并形成恐慌。

2009 F-1 Class Notes

FINANCIAL 1 CLASS NOTESWelcome to Financial Accounting & Reporting. This exam has a reputation as being demanding and the relative size of our four textbooks shows why. Most students find these topics to be the more challenging:●Consolidations and Investments [F-3]● Leases [F-5]●Bonds and Long-Term Liabilities [F-5]● Pensions [F-6]●Accounting for Income Taxes [F-6]●Governmental and Not-for-Profit [F-8 and F-9]The AICPA Content Specifications for FARE break down the exam into the following general areas and approximate percentages of exam points:1. Concepts and standards for financial statements (17%-23%)2. Typical items – recognition, measurement, valuation and presentation in financial statements(27%-33%)3. Specific types of transactions and events – recognition, measurement, valuation and presentationin conformity with GAAP (27%-33%)4. Accounting and reporting for governmental entities (8%-12%)not-for-profit entity accounting (8%-12%)5. NongovernmentalFinancial 1 includes the following:I. SOURCES OF GAAP AND BASIC FRAMEWORK AND CONCEPTSA. The hierarchy of sources is important, especially Category A (BOSSII).B. Terminology is key here - know the components of relevance and reliability (PFT andNRFV).II. REPORTING NET INCOMEA. Income Statement is an important topic.IDEA mnemonicthe1. Knowincome from continuing operations● I:●D: income from discontinued operations● E:extraordinary itemsaccounting principle change (to R/E)● A:III. DISCONTINUED OPERATIONSA. Accounting for discontinued operations can consist of gain or loss on current year'soperations, gain/loss on sale and impairment loss. Discontinued operations are shownnet of tax.1. Any of these must be reported as part of discontinued operations in the year incurred.If the operations are being "held for sale," they are treated as discontinued.IV. EXTRAORDINARY ITEMSA. Extraordinary items must be unusual and infrequent. "Unusual" requires the event beunrelated to the typical business activities of the firm. "Infrequent" means the event is notexpected to occur again in the foreseeable future. They are shown "net of tax."1. Unusual or infrequent items are reported within the "upper" (I) part of the incomestatement and before tax.V. ACCOUNTING CHANGESA. Accounting changes appear in three varieties: estimate, principle and entity.1.Changes in estimates, such as the useful life of a plant asset, are incorporated intothe accounting records for the current and future periods. No adjustment of priorfinancial statements is required. A change in depreciation method is a change inaccounting principle that is inseparable from a change in estimate, and is accountedfor as a change in estimate.2.Changes in principle (or method) involve switching from one acceptable method toanother. The cumulative effect is the change in retained earnings that results fromrestating prior years from the "old" method to the "new" method at the beginning ofthe earliest year presented. The cumulative effect is reported in the statement ofretained earnings, net of tax.a. Changes in principle - Exception:When it is impracticable to estimate the change in retained earnings thatwould result from restating the prior years financial statements, the change inmethod is applied prospectively [like changes in estimate]. In this case, norestatement of prior years occurs and there is no cumulative effect reported inthe statement of retained earnings: e.g., changing to LIFO from any otherinventory method.3.Change in entity requires restatement of prior year's financial statements to conformwith the new accounting entity when the prior financials are presented comparatively.VI. PRIOR PERIOD ADJUSTMENTS (CORRECTIONS OF ERRORS)A. Reported net of tax in the statement of retained earnings.VII. COMPREHENSIVE INCOMEA. Comprehensive Income includes all changes in owners' equity other than transactionswith owners. The formula shows that comprehensive income must include net incomeplus/minus other changes in owners' equity not resulting from transactions with owners.These other changes are known as "other comprehensive income" items.B. The mnemonic "PUFE" shows the four commonly tested sources of "other comprehensiveincome."●Pension funded status changes; covered in F6.●Unrealized gains and losses on AFS securities; covered in F3.●Foreign currency translation items; covered in F2.●Effective portion of cash flows hedges; covered in F7.C. Accumulated other comprehensive income is a cumulative sum of all of the individualcomponents of other comprehensive income. Accumulated other comprehensive income isan owners' equity item.D. There are three acceptable ways to present the statement of comprehensive income.VIII. BALANCE SHEET AND DISCLOSURES OVERVIEWA. Review the terminology and be able to recognize a classified balance sheet.B. The Summary of Significant Accounting Policies reflects the methods and policiesemployed by the firm.IX. INTERIM FINANCIAL REPORTINGA. Interim financial reporting uses the same GAAP as do annual financial reports. Timelinessis emphasized over reliability and income taxes are estimated each quarter based on theestimated average tax rate for the whole year.X. SEGMENT REPORTINGA. A reportable segment exists if it meets one of three tests:●10% of combined revenues to internal and external parties.●10% of reported profit or loss (as an absolute amount). You should be familiar withthe definition of operating profit: Segment revenues from sales to internal andexternal customers less directly traceable costs and also less reasonably allocatedcosts equals segment operating profit (loss).●10% of the combined assets of all operating segments.B. The "75% reporting sufficiency test" is a "catch all" requirement that may requireidentification of additional segments to attain the 75% level. This test requires thatreportable segments total at least 75% of revenue from external parties.C. The "90% single industry dominance test" means if one segment individually contains90% or more of the firm's revenues, profits and assets, then the segment reportingrequirement is waived for that firm.XI. DEVELOPMENT STAGE ENTERPRISESA. These firms have not yet started their primary operations or have generated insignificantrevenues to date.B. Development stage enterprises use "regular GAAP" with a couple of differences regardinglabeling and summation of cumulative reporting.XII. FAIR VALUE MEASUREMENTA. Fair value is the price to sell an asset or transfer a liability in an orderly transaction betweenmarket participants, measured in the principal, or most advantageous, market for the assetor liability.B. Entities can use the market approach, the cost approach, or the income approach, or acombination of these approaches, when measuring fair value.C. The fair value hierarchy prioritizes the inputs used in the market, cost & income valuationtechniques. Level I inputs have the highest priority and Level III inputs have the lowestpriority.。

lecture02

•

remote sensing system

– aircraft, satellite

NASA/JPL SIR-C Education Program NASA/JPL SIR-C Education Program Sean M. Buckley – sean.buckley@

– you may use something other than C or Fortran for homework and projects, e.g., Matlab

•

Polarization

– VV return will be stronger than HH return for vertically-oriented objects [Henderson and Lewis, p. 141]

γ

im aging plane squint angle

•

coherent

C = I + jQ = Ae jψ where A = I 2 + Q 2 and ψ = tan −1 ( Q I )

– mixing gives in-phase & quadrature

•

microwave/radio

pulse 1 sample N s -1 pulse 2 sample N s -1 pulse N p -1 sample N s -1 pulse N p sample N s -1

pulse 1 sample N s pulse 2 sample N s pulse N p -1 sample N s pulse N p sample N s

c02

Data and Expressions

• Let's explore some other fundamental programming concepts • Chapter 2 focuses on:

– – – – – – character strings primitive data the declaration and use of variables expressions and operator precedence data conversions accepting input from the user

Chapter 2: Data and Expressions

Java Software Solutions Foundations of Program Design Sixth Edition by Lewis & Loftus

Copyright © 2009 Pearson Education, Inc. Publishing as Pearson Addison-Wesley

Copyright © 2009 Pearson Education, Inc. Publishing as Pearson Addison-Wesley

2-8

Escape Sequences

• What if we wanted to print a the quote character? • The following line would confuse the compiler because it would interpret the second quote as the end of the string

System.out.println ("Whatever you are, be a good one.");

09年自考“英语(二)”完整讲义(92)

09年自考“英语(二)”完整讲义(92)3.人们寿命的长短取决于种种因素。

The length of life depends on various factors.Expectation of life is due to various factors.4.估计寿命是预计一个人能活得平均年数。

Expectation of life is the average numbers of years that a person is expected to live.The expectancy of life is the prediction of average years a person can live.5.长寿在改变我们的生活,改变我们的社会。

Long life is altering our life as well as our society.Long life is changing our lives,changing our society.四、历年考题1.Your account of what happened yesterday approximates _____ the real facts. (99.10)A. nearB. ofC. toD. upon答案:C.考点:此题考查词组approximate to 表示“与…接近”。

2.汉译英:正是由于出生率下降了,我们的社会才变得如此老龄。

(99.10)It is because the birthrate fell that our society had grown so old.3.Nations are _______ as “aged” when they have 7 percent or more of their people aged 65 or above.A. limitedB. classifiedC. originatedD. processed(00.4)答案:B.本题考查词组:classify as 表示把… 列为。

精选1基础工业工程第二讲bjf

工艺流程划分成工艺阶段毛坯—零件—部件—产品工艺阶段划分成工序毛坯——铸、锻、下料、焊接机加工——车、钻、铣、铇、磨工序再细分为工位

1.2.3 生产系统 (Production System)

生产系统的组织形式生产系统的组织是在生产过程中对设备、物料、人员进行综合配置,以实现生产过程的连续性、比例性、平行性和节奏性通常按生产设备的布置形式划分,有:产品(对象)布置原则、工艺布置原则或介于二者之间的成组(单元)布置原则及定位布置原则

创造产品和提供服务的行为

生产运作:

生产与运作是企业经营的基本职能之一

1.2.2 生产与运作管理(POM)

1.2.2 生产与运作管理(POM)

生产与运作管理是对提供公司主要产品或服务的生产运作系统进行设计、运行、评价和改进等管理活动的总称研究对象—— 生产与运作系统生产运作物质(实体)系统设计生产与运作过程的计划、组织与控制

资源要素关系

优化配置(处理四个关系)人——物物——物人——人生产系统——市场

研究的层次

1. 人与机器2. 局部与全局3. 人与人

企业基本活动

增值活动 占企业生产和经营活动 5%非增值活动 必要的活动: 60% 不必要的活动 : 35%

浪费: 1.不增值的活动 2.资源过量使用

动作的浪费两手空闲作业步行、弯腰、转身

加工的浪费多余的加工颠倒的程序。精度过高

库存的浪费不必要的搬运、存放、防护、寻找。资金占用、额外的管理费用。

制造过多/过早的浪费过多、过早、

管理的浪费事后管理。

八种浪费

最大的浪费

举例:库存掩盖了问题

库存之海

通过库存维持生产

2009text2 精读精讲

2009text2 精读精讲2009年《纽约时报》刊登了一篇名为《实用主义之危险》的文章,作者是学者斯坦利·菲什,他是哥伦比亚大学教授、知名实用主义者。

该文探讨了实用主义的崛起及其带来的潜在危险。

文章开头,菲什提到了实用主义在20世纪末至21世纪初兴起的趋势。

实用主义是一种哲学观点,注重实际行动和实效主义,在社会科学研究中有着广泛的应用。

实用主义者认为,知识的核心是其实用性,而不是理论的完备性。

然而,菲什指出,这种趋势可能会导致一种“实证至上”的态度,忽视了道德和伦理的考量。

接下来,菲什将实用主义和探索知识的目的做对比。

他指出,实用主义往往追求解决问题和应用知识,而探索知识的目的则是追求真理和了解世界的本质。

他担心实用主义的盛行可能导致人们只关注技术和应用,而忽视了理论和思考的重要性。

在文章的下一部分,菲什讨论了实用主义的政治含义。

他指出,实用主义者往往强调社会政策的实效性和解决方案的可行性,但忽视了道德和公正的考量。

他引用了一些案例,如布什政府的反恐政策和克林顿政府的医疗改革,来说明实用主义可能导致不公正和道德上的问题。

菲什还探讨了实用主义对教育的影响。

他指出,实用主义者倾向于将教育视为一种培养技能和解决问题的手段,而忽视了培养人的品德和思辨能力的重要性。

他认为,这种教育方法可能导致学生只关注应试技巧,而忽视了深入思考和综合能力的培养。

在文章的最后,菲什呼吁重新思考实用主义的影响。

尽管实用主义在解决问题和应用方面有其优点,但他警告说,我们不能忽视道德和伦理的考量。

实用主义应该与其他价值观相平衡,才能发挥其积极作用。

整个文章的结构清晰,逻辑严密。

菲什通过引用案例和论证来支持自己的观点,并提出了合理的解决方法。

他的写作风格简练明了,对实用主义的批评和警告直指问题的核心,引起人们对实用主义的思考。

总的来说,菲什的文章对实用主义提出了一些重要的批评和警告。

实用主义在解决问题和应用方面的优点不容忽视,但我们不能将其作为唯一的价值观。

09年技二基础研修-TBP基础课件-103页精品文档

Copyright 2006 TOYOTA INSTITUTE, Toyota Motor Corporation (Internal Use Only)

9

2.基本意识

5. 根据现场和事实进行判断

抛弃先入为主的观念,以客观的心态去 观察事物,不要混淆臆测与事实。

Copyright 2006 TOYOTA INSTITUTE, Toyota Motor Corporation (Internal Use Only)

具体行动 ・步骤 丰田工作方法

(丰田问题解决)

基本意识

丰田之路

TOYOTA WAY

Copyright 2006 TOYOTA INSTITUTE, Toyota Motor Corporation (Internal Use Only)

具体行动 ・步骤

1. 明确问题 2. 分解问题 P 3. 设定目标 4. 把握真因 5. 制定对策 D 6. 贯彻实施对策 7. 评价结果和过程

Copyright 2006 TOYOTA INSTITUTE, Toyota Motor Corporation (Internal Use Only)

3

1.何谓丰田工作方法(TBP)

有成效・高效率地解决问题的8个步骤 是建立在丰田价值观“TOYOTA WAY”基础之上的“丰田工作方法”的核心内

审视流程

31

Step 2. 分解问题

Process 1.将问题分层次,具体化

C

8. 巩固成果

A

基本意识

. 客户至上 . 经常自问自答“为什么” . 当事者意识 . 可视化 . 根据现场和事实进行判断 . 彻底地思考和执行 . 速度・时机 . 诚实・正直(实事求是) . 实现彻底的沟通 . 全员参与

2009融风暴下

❖ 媒體業→危險 ❖ 零售業→看漲 ❖ 觀光業→看漲 ❖ 幼教業→走下坡 ❖ 遊戲業→看漲 ❖ 成人進修業→微溫 ❖ 醫療業→微溫 ❖ 兩岸外交公務員→看漲

資料來源:Career雜誌四月號2009

20

未來職場新趨勢

2009年五大職場新興方向

資料來源:Career雜誌四月號2009

21

肆、如何增強職場競爭力

面臨裁員潮,為打贏「工作保衛戰」,增強職場 競爭力,需努力經營職場必備的「4個度」與建 立自我核心價值的「4項能力」。 4個度

專業度、配合度、貢獻度、能見度

4項能力

專業能力、組織力、執行力、應變力

資料來源:Career雜誌十二月號2019

22

「4個度」-強化「專業度」

❖語文能力(地方語言、英語、日語……等) ❖專業學科(主修、必修) ❖持續性的學習(進修、考照…) ❖人文素養(職場倫理、智慧財產權)

29

谢谢

12

次級房屋信貸危機 衍生CDO分攤風險

將這些貸款債權證券化, 變成CDO(抵押債權憑證)

房貸公司 風險變高

券商(投資銀行)

房貸機構業績大幅成長、 貸出去的錢變成了「債權」

13

銷售

買家

買家

次級房屋信貸危機 高槓桿操作錢滾錢

投資銀行幫 CDO投保,萬 一有風險,請 保險公司來賠。

保險公司

投資銀行 幫CDO投保

❖債券天王葛洛斯就指出,CDS的規模高達六十 二兆美元,等同於美國GDP(國內生產毛額) 的四倍。

15

次級房屋信貸危機 次貸引爆金融海嘯

❖因報酬率高、信用等級也高,這個基金廣受熱 愛,退休基金、教育基金、理財產品,甚至其 他國家的銀行也紛紛買入。

❖美國房地產開始走下坡後,房價下跌,優惠貸 款利率的兩年時限也到了,先是民眾無法償還 貸款,房屋價值也大幅跌落,房貸公司紛紛倒 閉。

数学建模 2009.2

经济数学模型

◆动态投入产出模型:针对若干时期,

研究再生产过程中各个生产部门之间的 相互联系问题;

静态投入产出模型与动态投入产出模型基本原理 相同。 本节以静态价值型投入产出模型为例,介绍投入 产出分析的基本原理。

经济数学模型

二、价值型投入产出模型

1、模型假设: (1)、将研究对象划分为n个部门,每个部门生产一

经济数学模型

设这三种产品的价格弹性矩阵为

1.2 0.1 0.1 E= ij 0.1 0.9 0.1 0.4 0.2 3

制订今年的生产计划,使销售总收入为最 大。假定政府规定价格升降幅度不得超过 10%。

经济数学模型

pi , qi ,(i 1, 2,3) 分别表示去年三种产品价格和产量

经济数学模型

4、完全消耗系数 第j部门在生产中除了要直接消耗第i个部 门的产品外,还要通过其它部门产品形成对第 i部门产品的间接消耗。部门之间的直接消耗 与部门之间的间接消耗之和称为完全消耗。 第j部门生产单位产品时对第i部门完全消耗的 产品数量,称为j部门对第i部门的完全消耗系 数。记作 bij .

下表是一个简化的价值型投入产出表,其 中

xij 表示第j部门消耗第i部门的产品数

量,也就是第i部门供给第j部门的数量。

价值型投入产出表

产出 投入

中

间

产品

最终产品 (合计)

n

部门 部门2 部门n 小计 1

总产品

物 质 消 耗

部门1 部门2 部门 n 折旧

x11 x21 xn1 D1

x12 x22 xn 2 D2

x

i 1

n

ij

D j Z j X j ( j 1, , ,n) 2

2009manmicro_L2

y , then y

x)

Problems with Rationality

I

Violations of Completeness

I

Obvious?

I

Violations of Transitivity

I I I

The just perceptible di¤erence problem The framing problem The Condorcet paradox (in violations group [not individual] rationality)

Rationality

I

% is rational if it’ s

I I

I

complete: 8x, y 2 X ,either x % y or y % x (the “or” here is an inclusive “or”) transitive: 8x, y , z 2 X ,if x % y and y % z, then x % z This is but one way to de…ne rationality. Re‡exivity (8x 2 X : x % x), as used in some text, is redundant.

I

% is rational =) u represents %?

I

% is rational =) u represents %?

I I

No. An example in Section 3.G (skipped for now) Homework Q4: Show that if X is …nite, then % is rational =) u represents %

2009text2 精读精讲

2009text2 精读精讲

摘要:

一、2007 年余杭区地下管线普查监理项目背景

二、地下管线普查监理项目的实施

三、项目成果与意义

四、项目流标与中标情况

正文:

一、2007 年余杭区地下管线普查监理项目背景

随着城市化进程的加快,城市地下管线的数量和复杂度不断增加,给城市规划、建设和管理带来了诸多挑战。

为了更好地掌握余杭区地下管线的情况,提高城市建设和管理的科学性和效率,2007 年,余杭区政府决定开展地下管线普查监理项目。

二、地下管线普查监理项目的实施

该项目主要包括对余杭区范围内的地下管线进行普查,以及对普查结果进行分析和整理,形成管线信息系统。

在项目实施过程中,相关部门积极组织专业力量,采用先进的技术设备和方法,确保普查数据的准确性和完整性。

此外,项目还引入了监理机制,对整个过程进行监督和管理,确保项目的顺利进行。

三、项目成果与意义

地下管线普查监理项目的完成,为余杭区城市规划、建设和管理提供了重要依据。

通过对地下管线的详细了解,可以优化城市规划设计,提高城市建设效率,降低管线事故发生的风险。

同时,管线信息系统的建立,为城市管理者提供了实时、准确的管线信息,极大地提高了城市管理水平。

四、项目流标与中标情况

根据提供的参考信息,2007 年余杭区地下管线普查监理项目在招标过程中出现了流标情况。

具体原因可能涉及招标文件的编制、投标单位的资质等方面的问题。

后来,经过重新招标,项目成功中标,由相关单位负责实施。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1.2 行为动词(也称实意动词)及其变体

英语语法规定,由行为动词充当谓语的句子,如果句子的时间参照点是“现在”和“过去”,谓语动词在形式上要做一些相应的变化。

其变化规则如下:

一,如果时间参照点为现在,当句子的主语是第一人称单复数、第二人称单复数、第三人称复数或名词复数时,充当谓语的行为动词必须用其现在体形式(由于行为动词的原形与现在体同形,故习惯上常不加以区分)。

例: We (I/You/They/The students) read newspapers every day.

二,如果时间参照点为现在,当句子的主语是第三人称单数或名词单数时,充当谓语的行为动词需做以下变化:

1)一般情况下,在动词原形后直接加 s ;如,walk ——walks; write ——writes

例

2)以 s, x, ch, sh 结尾的动词,后加 es ;如,toss ——tosses; tax ——taxes; punch ——punches; finish ——finishes 例

study ——studies; deny ——denies

4)以辅音字母加 o 结尾的动词,后加 es ;如,do---does; go---goes

例

三,如果时间参照点是过去,无论主语是第几人称,也无论主语是单数或复数,充当谓语用的行为动词一律用过去体形式(也称“过去式”)。

行为动词过去体的变化规则为:

1)一般情况下,直接在动词原形后加 ed ;如,walk ——walked; play ——played

例

2)以辅音字母加 y 结尾的动词原形,先将 y 变为 i ,然后再加 ed ;如,study ——studied; worry ——worried

但如果动词是以元音字母加 y 结尾,其变化则同(1)。

3)以一个元音字母加一个辅音字母结尾的动词,如果该动词的重音正好在尾音节,则要先双写结尾的那个辅音字母,然后再加 ed ;如,permit ——permitted; bit ——bitted

但如果动词是以两个元音字母加一个辅音字母结尾,或以一个元音字母加两个辅音字母结尾,尽管该音节为重读音

a. We walk to work every day. 这句话中的主语是第一人称复数,故谓语动词用 walk 这种形式。

b. He (She/The young man) walks to work every day. 这句话中的主语是第三人称单数,故谓语动词后需加s, 成为walks 这种形式 a. It (The grasshopper) tosses its head. b. He (The student) taxes his memory.

c. She (The angry woman) punches her husband on the nose.

d. Tom (The young man) finishes second in the contest. We (He/She/The young man) walked to work every Monday.

例 They (We/He/The students) studied Esperanto.

例 They (He) played football every other day.

例 He (The young man) admitted having broken the computer.

我们已经知道,行为动词的原形与现在体同形(只有当主语是第三人称单数时,动词词尾才以“-s ”或“-es ”的形式出现)。

现在体所表达的动作以“现在”(A 点)为时间参照,而过去体表达的动作则以“过去”(B 点)为时间参照。

且以行为动词study 为例:

Study

B A

(过去) (现在)

下列句子中,由于其谓语形式的不同,它们所表达的概念也就不一样。

a) We study English. 我们(现在)学习英语。

b) She studies English. 她(现在)学习英语。

c) We/She studied English. 我们/她(过去)学过英语。

a)、b)两句的谓语形式告诉我们:study 和 studies 所表示的动作都发生在“现在”(A 点);其中,studies 还告诉我们,这句话的主语是第三人称单数。

而 c) 句中的谓语动词是 studied ,它所表示的概念应是“过去”(B 点)。

我们注意到,行为动词在 B 点只有一种形式,这种形式已不再受主语人称与数变化的影响。

需要强调的是,在“现在”和“过去”两个时间点上,行为动词充当谓语的句子变为疑问句和否定句时须加时态助动词(Do )。

时态助动词 Do 虽无任何实际意义,但仍有原形、现在体、过去体三种不同形式:

(原形)

Do Do

Did Do/Does 其中,Does 用于主语 过去体 现在体 是第三人称单数时。

B A

(过去) (现在)

现在体表示的是“现在”(A 点)的概念,过去体表示的则是“过去”(B 点)的概念。

也就是说,在把表示 A 点的句子变为疑问句和否定句时,所选用的时态助动词应为 Do 或 Does ;而把表示 B 点的句子变为疑问句和否定句时,选用的时态助动词则只能是 Did 。

变疑问句时,将时态助动词 Do(Does/Did) 放到主语前面;变否定句时,将时态助动词放到主语后面,并在 do(does/did) 之后加上否定副词 not 。

英语语法还规定:在时态助动词 Do/Does/Did 之后,句子的谓语动词必须用原形。

因此,上述 a), b), c) 三句话在变疑问句和否定句时,应作如下调整:

陈 a)We study English. a) Do we study English? a) We do not study English. 述 b)She studies English. b) Does she study English? b) She does not study English. 句 c)We/She studied English.c) Did we/she study English?c) We/She did not study English.

不难看出,在表示“现在”和“过去”的动作行为时,英语句式的变换与句子的谓语动词有着密切的关系。

如果谓语由 Be 动词充当,变疑问句和否定句时,原句不须另加时态助动词(Do/Does/Did );但如果谓语由行为动词充当,变疑问句和否定句时,则要另加时态助动词(Do/Does/Did ),而原句的谓语动词也因此要改用原形。

值得提醒的是,时态助动词 Do 只限用于“现在”和“过去”两个时间点,即,在“现在”时间点上只能用Do (或Does),而在“过去”时间点上则只能用 Did 。

在表示其它时间点上的动作行为时,则另需选用相应的时态助动词。

除 Do/Does/Did 外,其它时态助动词还有:Will (Shall), Have 和 Be 。

以后学习中,我们将逐一介绍各种时态助动词的用法及其所表示的时态概念。

例。