《财务管理基础第13版》相关章节答案 ppt课件

财务管理基础工业出版社13版Chap006_PPT

1-24

Using Long-Term Financing for Part of Short-Term Needs

1-25

Short- Term Financing

1-9

Seasonal Sales Pattern in Target and Limited Brands

• Like publishers, retail companies do not stock inventory for more then a year • Fourth quarter is the biggest quarter for retailers • As per the figure, the Target is growing much faster than the Limited Brands • Even then, in the fourth quarter, peak earnings are almost equal for both the companies

1-16

Sales Forecasts, Cash Receipts, and Payments, and Cash Budget (cont’d)

• Table 6-3 is created to examine the buildup in accounts receivable and cash

– Lenders and financial managers need to plan inventory – Lack of correct inventory planning can lead to lost sales

财务管理基础工业出版社13版Chap019_PPT

Value of the Convertible Bond

• Must evaluate the conversion privileges • Other values to be considered include:

– Conversion value – Conversion premium – Pure bond value – Downside risks – Floor value

1-14

Diluted Earnings Per Share

• Assume 400,000 new shares will be created from potential conversion, while at the same time allowing for reduction in interest payments that would occur as a result of conversion of the debt to common stock • The before-tax interest payments are $450,000, the aftertax interest cost of $270,000 [$450,000 (1- .40) = $270,000] will be saved and can be added back to the income Diluted earnings = Adjusted earnings after taxes ; per share Shares outstanding + All convertible securities Reported Interest earnings savings = $1,500,000 + $270,000 = $1,770,000 = $1.26 1,000,000 + 400,000 1,400,000

《财务管理基础第13版》相关章节答案ppt课件

Chapter 1: The Role of Financial Management

ANSWERS TO QUESTIONS

1. With an objective of maximizing shareholder wealth, capital will tend to be allocated to the most productive investment opportunities on a risk-adjusted return basis. Other decisions will also be made to maximize efficiency. If all firms do this, productivity will be heightened and the economy will realize higher real growth. There will be a greater level of overall economic want satisfaction. Presumably people overall will benefit, but this depends in part on the redistribution of income and wealth via taxation and social programs. In other words, the economic pie will grow larger and everybody should be better off if there is no reslicing. With reslicing, it is possible some people will be worse off, but that is the result of a governmental change in redistribution. It is not due to the objective function of corporations. 2. Maximizing earnings is a nonfunctional objective for the following reasons: a. Earnings is a time vector. Unless one time vector of earnings clearly dominates all other time vectors, it is impossible to select the vector that will maximize earnings. b. Each time vector of earning possesses a risk characteristic. Maximizing expected earnings ignores the risk parameter. c. Earnings can be increased by selling stock and buying treasury bills. Earnings will continue to increase since stock does not require out-of-pocket costs. d. The impact of dividend policies is ignored. If all earnings are retained, future earnings are increased. However, stock prices may decrease as a result of adverse reaction to the absence of dividends. Maximizing wealth takes into account earnings, the timing and risk of these earnings, and the dividend policy of the firm. 3. Financial management is concerned with the acquisition, financing, and management of assets with some overall goal in mind. Thus, the function of financial management can be broken down into three major decision areas: the investment, financing, and asset management decisions. 4. Yes, zero accounting profit while the firm establishes market position is consistent with the maximization of wealth objective. Other investments where short-run profits are sacrificed for the long-run also are possible. 5. The goal of the firm gives the financial manager an objective function to maximize. He/she can judge the value (efficiency) of any financial decision by its impact on that goal. Without such a goal, the manager would be "at sea" in that he/she would have no objective criterion to guide his/her actions. 6. The financial manager is involved in the acquisition, financing, and management of assets. These three functional areas are all interrelated (e.g., a decision to acquire an asset necessitates the financing and management of that asset, whereas financing and management costs affect the decision to invest). 7. If managers have sizable stock positions in the company, they will have a greater understanding for the valuation of the company. Moreover, they may have a greater incentive to maximize shareholder wealth than they would in the absence of stock holdings. However, to the extent persons have not only human capital but also most of their financial

财务会计学(第13版)PPT第2章

打开阅读材料

打开例题

打开案例

Page 9

第一页 上一页

下一页 最后一页 结束

2.1 货币资金概述(introuction of 第一节 货ca币sh资,m金o(nceatsahr,ymroensoetuarrcyerse)sources)

2.1.2货币资金内部控制制度 2.货币资金内部控制制度的主要内容

贷:其他应付款—(×个人) 应支付给有关人员或单位的 营业外收入—现金溢余 无法查明原因的现金溢余,经批准

打开阅读材料

打开例题

打开案例

Page 22

第一页 上一页

下一页 最后一页 结束

2.2.2库存现金的收付与清查 2.库存现金清查 (4)库存现金溢余的处理原则 ①属于应支付给有关人员或单位的,应借记“待 处理财产损溢——待处理流动资产损溢”科目, 贷记“其他应付款——应付现金溢余(××个人)” 科目。 ②属于无法查明原因的现金溢余,经批准后,借记 “待处理财产损溢——待处理流动资产损溢”科 目,贷记“营业外收入——现金溢余”科目。

管理费用——现金短缺

无法查明的其他原因

贷:待处理财产损溢——待处理流动资产损溢

打开阅读材料

打开例题

打开案例

Page 21

第一页 上一页

下一页 最后一页 结束

2.2.2库存现金的收付与清查 2.库存现金清查 (3)库存现金长缺的处理原则 ①发生长款 借:库存现金

贷:待处理财产损溢—待处理流动资产损溢 ②长款处理 借:待处理财产损溢—待处理流动资产损溢

企业必须严格按规定的限额控制现金结余量。

打开阅读材料

打开例题

打开案例

Page 15

第一页 上一页

下一页 最ห้องสมุดไป่ตู้一页 结束

财务管理基础 13版 _pp13

• Potential Difficulties

• Capital Rationing

• Project Monitoring

• Post-Completion Audit

13.3 Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition. © Pearson Education Limited 2009. Created by Gregory Kuhlemeyer.

13.8

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition. © Pearson Education Limited 2009. Created by Gregory Kuhlemeyer.

Payback Solution (#2)

13.9

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition. © Pearson Education Limited 2009. Created by Gregory Kuhlemeyer.

PBP Acceptance Criterion

13.7 Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition. © Pearson Education Limited 2009. Created by Gregory Kuhlemeyer.

财务会计学(第13版)PPT第9章

1.应付职工薪酬(wages payable)定义:

是指职工为企业提供服务后,企业应当支

付给职工的各种形式的报酬或补偿。

指企业为获得职工提供的服务或解除劳

职 动关系而给予的各种形式的报酬或补偿。

工 薪 酬构

短期薪酬、离职后福利 辞退福利、其他长期职工福利

成 给职工配偶、子女、受赡养人、已

故员工遗属及其他受益人等的福利

例9-2

22

例9-2

23

例9-2

24

例9-2

25

9.2.3 短期借款的偿还

企业在短期借款到期偿还借款本金时 借:短期借款 贷:银行存款

26

承例9-1。北京宏达电子股份有限公司

2021年10月1日偿还短期借款80 000元,

编制会计分录如下:

例9-3 借:短期借款

80 000

贷:银行存款

80 000

6

2.按照偿付金额是否确定分类

按照偿付金额是否确定分类,可以分为金额 可以确定的流动负债和金额需要估计的流动负债。

(1)金额可以确定的流动负债

金额可以确定的流动负债是指有确切的债权人 和偿付日期并有确切的偿付金额的流动负债,主 要包括短期借款、应付票据、已经取得结算凭证 的应付账款、预收账款、应付职工薪酬、应付股 利、应付利息、应交税费和其他应付款等。

46

9.4.1 应付职工薪酬的核算内容

2.职工薪酬(wages payable)构成:

短期薪酬指企业在职工提供相关服务的年度报告 期间结束后十二个月内需要全部予以支付的职工薪酬。 短期薪酬具体包括:⑴职工工资、奖金、津贴和补贴, ⑵职工福利费,⑶医疗保险费、工伤保险费和生育保 险费等社会保险费,⑷住房公积金,⑸工会经费和⑹职 工教育经费,⑺短期带薪缺勤,⑻短期利润分享计划, ⑼非货币性福利以及⑽其他短期薪酬。

财务管理基础工业出版社13版Chap015_PPT

• Common during the issuance of additional shares

1-15

Dilution

• Problem associated with the issuance of additional securities:

15

Chapter

Investment Bankinw-Hill/Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Outline

1-5

Investment Banking Competitors

• There is intense competition in the market

– Being a leader in one sector helps a firm‟s overall reputation – It, however, does not ensure success in other areas

• Resulting from increase in shares outstanding

1-16

Market Stabilization

• An investment banker is responsible for stabilizing the offering during the distribution period:

• The underwriting spread represents the total compensation for all participating members

财务管理基础 financial management 清华大学出版社第13版ppt2

The Business, Tax, and Financial Environments

2.1

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition. © Pearson Education Limited 2009. Created by Gregory Kuhlemeyer.

The Business Environment

Corporation – A business form legally separate from its owners.

• •

An artificial entity that can own assets and incur liabilities. Business income is accounted for on the income tax form of the corporation.

Advantages

•

•

Disadvantages

• •

Limited liability

Easy transfer of ownership Unlimited life

Double taxation More difficult to establish More expensive to set up and maintain

• • •

The Business Environment

The Tax Environment

The Financial Environment

2.3

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition. © Pearson Education Limited 2009. Created by Gregory Kuhlemeyer.

《财务管理基础第13版》相关章节答案

. © Pearson Education Limited 2008

Chapter 1: The Role of Financial Management

ANSWERS TO QUESTIONS

1. With an objective of maximizing shareholder wealth, capital will tend to be allocated to the most productive investment opportunities on a risk-adjusted return basis. Other decisions will also be made to maximize efficiency. If all firms do this, productivity will be heightened and the economy will realize higher real growth. There will be a greater level of overall economic want satisfaction. Presumably people overall will benefit, but this depends in part on the redistribution of income and wealth via taxation and social programs. In other words, the economic pie will grow larger and everybody should be better off if there is no reslicing. With reslicing, it is possible some people will be worse off, but that is the result of a governmental change in redistribution. It is not due to the objective function of corporations.

财务管理基础工业出版社13版Chap020_PPT

Portfolio Effect

• The reduction or increase in risk may influence the P/E ratio as much as the change in the growth rate

– The initial price they are paid for their shares – The outlook for the acquiring firm

• Analysis is hence made mainly from the viewpoint of the firm

1-14

1-2

Largest Acquisitions Ever

1-3

Motives for Business Combinations

• Merger

– A combination of two or more companies in which ththe identity of the acquiring firm

• Eliminating overlapping functions in production and marketing • Meshing together various engineering capabilities

1-9

Motives of Selling Stockholders

– The assumption is that the firm has a 40% tax rate. The tax shield value of a carryforward to Firm A is equal to the loss involved times the tax rate ($220,000 X 40% = $88,000) – The company can reduce its total taxes from $120,000 to $32,000, and thus could pay $88,000 for the carryforward alone – The income available to stockholders also has increased by $88,000

财务管理基础工业出版社13版Chap013_PPT

1-9

Betas for Five-Year Period (Ending January 2006)

1-10

Risk and the Capital Budgeting Process

• Informed investors and managers need to decide between:

1-11

Risk-Adjusted Discount Rate

• Using different discount rates for proposals with different risk levels

– Investment with normal amount of risk may be discounted at the cost of capital – Investments carrying greater than normal risk will be discounted at a higher rate and so on

– Investments that produce ‘certain’ returns – Investments that produce an expected value of return, apart from having a high coefficient of variation

1-17

Capital Budgeting Analysis

1-18

Capital Budgeting Decision Adjusted for Risk

1-19

Simulation Models

• Help in dealing with uncertainties involved in forecasting the outcome of capital budgeting projects or other decisions

财务会计学(第13版)PPT第4章

4.2.1应收票据(notes receivable)

1.应收票据及其初始入账价值 (1)应收票据及其分类

•广 义

支票、银行本见票即付 无须将其列为

应 票及银行汇票

应收票据予以处

收

理

票 应收票据仅指企业持有的 据 未到期或未兑现的商业汇票

企业持有的未到期 或未兑现的各种票据

打开阅读材料

打开例题

打开案例

这两天中,只计算其中的一天。

打开阅读材料

打开例题

打开案例

Page 24

第一页 上一页

下一页 最后一页 结束

2.应收票据到期日的确定 ➢ 按月表示时,以到期月份中与出票日相同的

那一天为到期日;当签发承兑票据的日期为 某月月末时,统一以到期月份的最后一日为 到期日。 ➢ 按日表示时,从出票日起按实际经历的天数 计算,但出票日和到期日只能计算其中的一 天。

在实务中,票据的期限一般有按月表示和按日表示两 种。其中, 按月表示的汇票付款期限自出票日起按月计 算,按日表示的汇票付款期限自出票日起按日计算。

票据期限按月表示时,票据的期限不考虑各月份实 际天数多少,统一按次月对应日为整月计算。

票据期限按日表示时,票据的期限不考虑月数,统

一按票据的实际天数计算。在票据承兑日和票据到期日

Page 18

第一页 上一页

下一页 最后一页 结束

我国,商业汇票的期限一般不超过6个月

甲交付货物 乙 应收

持有期利息

公

公 票据 应收票据到期

司商业汇票 司 获取 前背书转让

贴现

应收票 据到期

bankacceptance

人 不 同

票 据 承 兑

商业承 承兑人是付款人 兑汇票

财务管理基础工业出版社13版Chap017_PPT

Poison Pills

• A rights offering made to existing shareholders of a company

– Used to avoid a takeover – Makes hostile takeovers very expensive and unattractive – Allows existing shareholders the right to buy additional shares of the stock at a very low price

• Holders of common stock must be given the first option to buy new shares

– Ensures that management cannot subvert the position of present stockholders

1-17

Advantages of ADRs for the U.S. Investor

• Annual reports and financial statements are presented in English according to GAAP • Dividends are paid in dollars and are more easily collected • Considered to be:

1-3

Preferred Stock

• Plays a secondary role in financing the corporate enterprise

– Represents a hybrid security by combining some of the features of debt and common stock – Stockholders do not have an ownership interest in the firm – Stockholders have a priority of claims to dividends superior to that of common stockholders

《财务管理基础》第13版课后答案3-16章

第三章货币的时间价值4.你在第十年年末需要50000美元。

为此,你决定在以后10年内,每年年末向银行存入一定的货币额。

若银行长期存款的年利率为8%,则你每年要存入多少钱才能在第十年年末获得50000美元。

(近似到整数)?【答】求贴现率8%,终值为50000美元的年金金额。

查表A3,(F/A,8%,10)=14.487。

所以,A=F/(F/A,8%,10)=50000/14.487=3451.37美元。

如果确定的年贴现率为14%,则该现金流的现值是多少?【答】求解现值,贴现率14%。

分开不同金额计算:1. P6-10=A×(P/A,14%,5)×(P/F,14%,5)=1400×3.433×0.519=2494.42;P5=1600×(P/F,14%,5)=1600×0.519=830.4;P4=1900×0.592=1124.8;P3=2400×0.675=1620;P2=2000×0.769=1538;P1=1200×0.877=1052.4;P1-10=2494.42+830.4+1124.8+1620+1538+1052.4=8660.02美元。

10.假设你将在第十年年末收到1000美元.如果你的机会成本利率(opportunity rate)是10%,那么在计息期分别是(1)每年计息一次,(2)每季计息一次,(3)永续计息时的现值各是多少?【答】(1)每年计息一次,P=F*(P/F,10%,10)=0.386*1000=386美元。

(2)每季度计息一次,P=F*(P/F,10%/4,10*4);美元查表A2 表不能直接查到,3%的现值=0.453*1000=453美元,2%的现值=0.307*1000=307美元,用插值法可得P=380美元。

(3)永续计息P=1000/2.718280(0.1*10)=367美元。

[管理学]公司财务管理基础13 PPT课件讲义_OK

![[管理学]公司财务管理基础13 PPT课件讲义_OK](https://img.taocdn.com/s3/m/1125b2c667ec102de3bd8968.png)

⑤记账

12

财会人员根据上述原始凭证编制记账凭证,根据记账凭证登记总账、明细帐。同 时仓库保管人员依据入库单登记保管账簿。 保持定期对账。

(3)具体Leabharlann 制要点①请购环节请购人员必须是获得授权的生产管理或采购部门人员,而且必须根据

采购预算或者实际需要开立申请,坚决杜绝无计划采购、不及时采购,确

保生产经营活动顺利进行。

内部控制规范就是以关键点为核心,制定员工操作 规范和业务操作指南,也是检查和监督的重点部位。

9

2.采购与付款控制

采购是公司开展业务活动的基本前提, 建立和完善采购与付款控制制度,是控 制业务过程的第一步,倘若发生任何差错和 舞弊,都将影响整个业务活动正常进行。因 此公司必须按照《企业内部控制应用指引第 7号-采购业务》规定,结合本单位实际制 定控制措施,并严格组织实施。

(1)设定该环节控制目标 (2)明确该环节的信息传递流程 (3)岗位分工与授权管理 (4)找出常见的内部控制缺陷 (5)设置控制关键点

4

(1)设定该环节控制目标

控制目标是实施内部控制的最终目的,也是评价内部控制 的主要标准和依据。因此,公司实施各业务环节控制时,首 先应确定控制目标,然后依据这个具体目标找出控制要素和关 键控制点,这样,才能保证控制达到理想程度。

案例2: 现在许多医疗公司在销售药品时,都会给医院采购人员和医生 销售佣金,

15

有时佣金高达40%,这样“重赏”之下,所导致的后果是,促使医生开 大药方,一场感冒就得上千元。这就加大了群众的就医成本,导致医患 关系极度紧张,有的医生因为开大处方每月获得的销售佣金比工资还多。

案例3: 某公司的采购员张某利用内部控制制度不健全,在自己一人与供货商谈判 的情况下,与供货方勾结,把采购价格每公斤提高了一元,然后供货方按 每公斤0.7元给其现金回扣,张某一次订货30吨,给公司造成损失3万元,张某 自己却中饱私囊2.1万元。结果公司成本增高,产品销售及其不利。 ③入库验收有漏洞,造成财产流失 验收人员不认真核对采购物资的数量和质量,或者对验收时发现的问题 没有及时报告,都会导致内部控制失灵,造成财产损失。其主要原因是验收 人员玩忽职守,不履行岗位职责,对内部控制制度认识不足,搞人情过关等, 这就容易诱发采购人员舞弊。 案例4: 某燃料公司从火车站往公司运煤炭,只追求运输速度,司机自装自运,回 来交货时,验收人员不进行计量重量,结果给司机有了作弊之机,每运一车就 在中途给亲属卸下几百公斤,到公司交货时又能顺利拿到验收单。运输半年, 途中偷盗煤炭几十吨,导致公司库存煤炭盘点短缺数额巨大。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

chapters have been written so that this can be done without any problem.

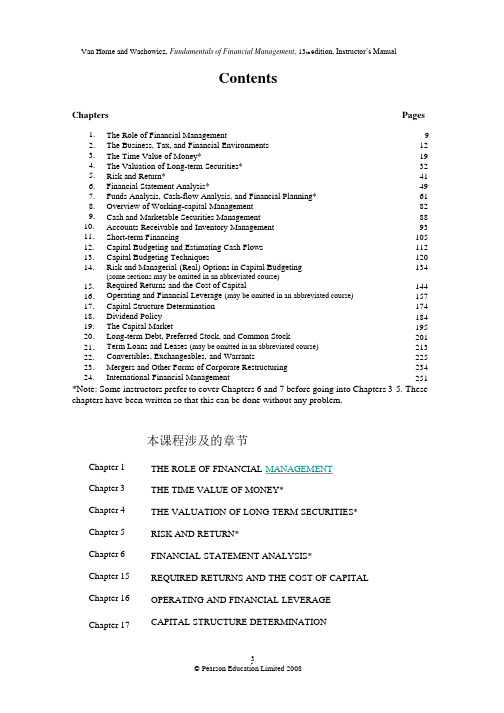

本课程涉及的章节

Chapter 1 Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 15 Chapter 16

1. With an objective of maximizing shareholder wealth, capital will tend to be allocated to the most productive investment opportunities on a risk-adjusted return basis. Other decisions will also be made to maximize efficiency. If all firms do this, productivity will be heightened and the economy will realize higher real growth. There will be a greater level of overall economic want satisfaction. Presumably people overall will benefit, but this depends in part on the redistribution of income and wealth via taxation and social programs. In other words, the economic pie will grow larger and everybody should be better off if there is no reslicing. With reslicing, it is possible some people will be worse off, but that is the result of a governmental change in redistribution. It is not due to the objective function of corporations.

9

2. The Business, Tax, and Financial Environments

12

3. The Time Value of Money*

19

4. The Valuation of Long-term Securities*

32

5. Risk and Return*

41

6. Financial Statement Analysis*

• 你所经历的课堂,是讲座式还是讨论式? • 教师的教鞭

• “不怕太阳晒,也不怕那风雨狂,只怕先生骂我 笨,没有学问无颜见爹娘 ……”

• “太阳当空照,花儿对我笑,小鸟说早早早……”

Chapter 1: The Role of Financial Management

ANSWERS TO QUESTIONS

Chapter 17

THE ROLE OF FINANCIAL MANAGEMENT THE TIME VALUE OF MONEY* THE VALUATION OF LONG-TERM SECURITIES* RISK AND RETURN* FINANCIAL STATEMENT ANALYSIS* REQUIRED RETURNS AND THE COST OF CAPITAL OPERATING AND FINANCIAL LEVERAGE CAPITAL STRUCTURE DETERMINATION

2020/12/12

3

1

© Pearson Education Limited 2008

The Role of Financial Management

Increasing shareholder value over time is the bottom line of every move we make.

120

14. Risk and Managerial (Real) Options in Capital Budgeting

134

(some sections may be omitted in an abbreviated course)

15. Required Returns and the Cost of Capital

144

16. Operating and Financial Leverage (may be omitted in an abbreviated course)

157

17. Capital Structure Determination

174

18. Dividend Policy

184

19. The Capital Market

49

7. Funds Analysis, Cash-flow Analysis, and Financial Planning*

61

8. Overview of Working-capital Management

82

9. Cash and Marketable Securities Management

195

20. Long-term Debt, Preferred Stock, and Common Stock

201

21. Term Loans and Leases (may be omitted in an abbreviated course)

213

22. Convertibles, Exchangeables, and Warrants

88

10. Accounts Receivable and Inventor Financing

105

12. Capital Budgeting and Estimating Cash Flows

112

13. Capital Budgeting Techniques

ROBERT GOIZUETA Former CEO, The Coca-Cola Company

9

2020/12/12

© Pearson Education Limited 2008

2

精品资料

• 你怎么称呼老师?

• 如果老师最后没有总结一节课的重点的难点,你 是否会认为老师的教学方法需要改进?

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

Contents

Chapters

Pages

1. The Role of Financial Management

225

23. Mergers and Other Forms of Corporate Restructuring

234

24. International Financial Management

251

*Note: Some instructors prefer to cover Chapters 6 and 7 before going into Chapters 3-5. These