Does guanxi help or hinder firm profitability关系帮助公司获利

国际财务管理课后习题答案chapter 8

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE SUGGESTED ANSWERS AND SOLUTIONS TO END—OF—CHAPTER QUESTIONS ANDPROBLEMSQUESTIONS1。

How would you define transaction exposure? How is it different from economic exposure? Answer:Transaction exposure is the sensitivity of realized domestic currency values of the firm’s contractual cash flows denominated in foreign currencies to unexpected changes in exchange rates。

Unlike economic exposure, transaction exposure is well-defined and short-term。

2。

Discuss and compare hedging transaction exposure using the forward contract vs。

money market instruments。

When do the alternative hedging approaches produce the same result?Answer: Hedging transaction exposure by a forward contract is achieved by selling or buying foreign currency receivables or payables forward。

On the other hand,money market hedge is achieved by borrowing or lending the present value of foreign currency receivables or payables, thereby creating offsetting foreign currency positions. If the interest rate parity is holding, the two hedging methods are equivalent。

罗斯公司理财第九版原版书课后习题Cha16

5. Business Risk versus Financial Risk Explain what is meant by business and financial risk.Suppose firm A has greater business risk than firm B. Is it true that firm A also has a higher cost of equity capital? Explain.6. MM Propositions How would you answer in the following debate?Q: Isn’t it true that the riskiness of a firm’s equity will rise if the firm increases its use of debt financing?A: Yes, that’s the essence of MM Proposition II.Q: And isn’t it true that, as a firm increases its use of borrowing, the likelihood of default increases, thereby increasing the risk of the firm’s debt?A: Yes.Q: In other words, increased borrowing increases the risk of the equity and the debt?A: That’s right.Q: Well, given that the firm uses only debt and equity financing, and given that the risks of both are increased by increased borrowing, does it not follow that increasing debtincreases the overall risk of the firm and therefore decreases the value of the firm?A: ??7. Optimal Capital Structure Is there an easily identifiable debt–equity ratio that will maximizethe value of a firm? Why or why not?8. Financial Leverage Why is the use of debt financing referred to as financial “leverage”?9. Homemade Leverage What is homemade leverage?10. Capital Structure Goal What is the basic goal of financial management with regard to capitalstructure?Questions and Problems connect™BASIC (Questions 1–16)1. EBIT and Leverage Money, Inc., has no debt outstanding and a total market value of$225,000. Earnings before interest and taxes, EBIT, are projected to be $19,000 if economic conditions are normal. If there is strong expansion in the economy, then EBIT will be 30 percent higher. If there is a recession, then EBIT will be 60 percent lower. Money is considering a $90,000 debt issue with an 8 percent interest rate. The proceeds will be used to repurchase shares of stock.There are currently 5,000 shares outstanding. Ignore taxes for this problem.1. Calculate earnings per share, EPS, under each of the three economic scenarios before anydebt is issued. Also calculate the percentage changes in EPS when the economy expands orenters a recession.2. Repeat part (a) assuming that Money goes through with recapitalization. What do youobserve?2. EBIT, Taxes, and Leverage Repeat parts (a) and (b) in Problem 1 assuming Money has a taxrate of 35 percent.3. ROE and Leverage Suppose the company in Problem 1 has a market-to-book ratio of 1.0.1. Calculate return on equity, ROE, under each of the three economic scenarios before anydebt is issued. Also calculate the percentage changes in ROE for economic expansion and recession, assuming no taxes.2. Repeat part (a) assuming the firm goes through with the proposed recapitalization.3. Repeat parts (a) and (b) of this problem assuming the firm has a tax rate of 35 percent.4. Break-Even EBIT Rolston Corporation is comparing two different capital structures, an all-equity plan (Plan I) and a levered plan (Plan II). Under Plan I, Rolston would have 240,000 shares of stock outstanding. Under Plan II, there would be 160,000 shares of stock outstanding and $3.1 million in debt outstanding. The interest rate on the debt is 10 percent and there are no taxes.1. If EBIT is $750,000, which plan will result in the higher EPS?2. If EBIT is $1,500,000, which plan will result in the higher EPS?3. What is the break-even EBIT?5. MM and Stock Value In Problem 4, use MM Proposition I to find the price per share of equityunder each of the two proposed plans. What is the value of the firm?6. Break-Even EBIT and Leverage Kolby Corp. is comparing two different capital structures.Plan I would result in 1,500 shares of stock and $20,000 in debt. Plan II would result in 1,100 shares of stock and $30,000 in debt. The interest rate on the debt is 10 percent.1. Ignoring taxes, compare both of these plans to an all-equity plan assuming that EBIT willbe $12,000. The all-equity plan would result in 2,300 shares of stock outstanding. Which of the three plans has the highest EPS? The lowest?2. In part (a) what are the break-even levels of EBIT for each plan as compared to that foran all-equity plan? Is one higher than the other? Why?3. Ignoring taxes, when will EPS be identical for Plans I and II?4. Repeat parts (a), (b), and (c) assuming that the corporate tax rate is 40 percent. Are thebreak-even levels of EBIT different from before? Why or why not?7. Leverage and Stock Value Ignoring taxes in Problem 6, what is the price per share of equityunder Plan I? Plan II? What principle is illustrated by your answers?8. Homemade Leverage Star, Inc., a prominent consumer products firm, is debating whether ornot to convert its all-equity capital structure to one that is 40 percent debt. Currently there are 5,000 shares outstanding and the price per share is $65. EBIT is expected to remain at $37,500 per year forever. The interest rate on new debt is 8 percent, and there are no taxes.1. Ms. Brown, a shareholder of the firm, owns 100 shares of stock. What is her cash flowunder the current capital structure, assuming the firm has a dividend payout rate of 100 percent?2. What will Ms. Brown’s cash flow be under the proposed capital structure of the firm?Assume that she keeps all 100 of her shares.3. Suppose Star does convert, but Ms. Brown prefers the current all-equity capital structure.Show how she could unlever her shares of stock to recreate the original capital structure.4. Using your answer to part (c), explain why Star’s choice of capital structure is irrelevant.9. Homemade Leverage and WACC ABC Co. and XYZ Co. are identical firms in all respectsexcept for their capital structure. ABC is all equity financed with $800,000 in stock. XYZ uses both stock and perpetual debt; its stock is worth $400,000 and the interest rate on its debt is 10 percent. Both firms expect EBIT to be $95,000. Ignore taxes.1. Richard owns $30,000 worth of XYZ’s stock. What rate of return is he expecting?2. Show how Richard could generate exactly the same cash flows and rate of return byinvesting in ABC and using homemade leverage.3. What is the cost of equity for ABC? What is it for XYZ?4. What is the WACC for ABC? For XYZ? What principle have you illustrated?10. MM Nina Corp. uses no debt. The weighted average cost of capital is 11 percent. If the currentmarket value of the equity is $43 million and there are no taxes, what is EBIT?11. MM and Taxes In the previous question, suppose the corporate tax rate is 35 percent. What isEBIT in this case? What is the WACC? Explain.12. Calculating WACC Weston Industries has a debt–equity ratio of 1.5. Its WACC is 12 percent,and its cost of debt is 9 percent. The corporate tax rate is 35 percent.1. What is Weston’s cost of equity capital?2. What is Weston’s unlevered cost of equity capital?3. What would the cost of equity be if the debt–equity ratio were 2? What if it were 1.0?What if it were zero?13. Calculating WACC Shadow Corp. has no debt but can borrow at 7 percent. The firm’s WACC iscurrently 11 percent, and the tax rate is 35 percent.1. What is Shadow’s cost of equity?2. If the firm converts to 25 percent debt, what will its cost of equity be?3. If the firm converts to 50 percent debt, what will its cost of equity be?4. What is Shadow’s WACC in part (b)? In part (c)?14. MM and Taxes Bruce & Co. expects its EBIT to be $140,000 every year forever. The firm canborrow at 9 percent. Bruce currently has no debt, and its cost of equity is 17 percent. If the tax rate is 35 percent, what is the value of the firm? What will the value be if Bruce borrows $135,000 and uses the proceeds to repurchase shares?15. MM and Taxes In Problem 14, what is the cost of equity after recapitalization? What is theWACC? What are the implications for the firm’s capital structure decision?16. MM Proposition I Levered, Inc., and Unlevered, Inc., are identical in every way except theircapital structures. Each company expects to earn $65 million before interest per year in perpetuity, with each company distributing all its earnings as dividends. Levered’s perpetual debt has a marketvalue of $185 million and costs 8 percent per year. Levered has 3.4 million shares outstanding, currently worth $100 per share. Unlevered has no debt and 7 million shares outstanding, currently worth $80 per share. Neither firm pays taxes. Is Levered’s stock a better buy than Unlevered’s stock?INTERMEDIATE (Questions 17–25)17. MM Tool Manufacturing has an expected EBIT of $42,000 in perpetuity and a tax rate of 35percent. The firm has $70,000 in outstanding debt at an interest rate of 8 percent, and its unlevered cost of capital is 15 percent. What is the value of the firm according to MM Proposition I with taxes? Should Tool change its debt–equity ratio if the goal is to maximize the value of the firm? Explain.18. Firm Value Old School Corporation expects an EBIT of $15,000 every year forever. Old Schoolcurrently has no debt, and its cost of equity is 17 percent. The firm can borrow at 10 percent. If the corporate tax rate is 35 percent, what is the value of the firm? What will the value be if Old School converts to 50 percent debt? To 100 percent debt?19. MM Proposition I with Taxes The Maxwell Company is financed entirely with equity. Thecompany is considering a loan of $1.4 million. The loan will be repaid in equal installments over the next two years, and it has an 8 percent interest rate. The company’s tax rate is 35 percent.According to MM Proposition I with taxes, what would be the increase in the value of the company after the loan?20. MM Proposition I without Taxes Alpha Corporation and Beta Corporation are identical inevery way except their capital structures. Alpha Corporation, an all-equity firm, has 10,000 shares of stock outstanding, currently worth $20 per share. Beta Corporation uses leverage in its capital structure. The market value of Beta’s debt is $50,000, and its cost of debt is 12 percent. Each firm is expected to have earnings before interest of $55,000 in perpetuity. Neither firm pays taxes.Assume that every investor can borrow at 12 percent per year.1. What is the value of Alpha Corporation?2. What is the value of Beta Corporation?3. What is the market value of Beta Corporation’s equity?4. How much will it cost to purchase 20 percent of each firm’s equity?5. Assuming each firm meets its earnings estimates, what will be the dollar return to eachposition in part (d) over the next year?6. Construct an investment strategy in which an investor purchases 20 percent of Alpha’sequity and replicates both the cost and dollar return of purchasing 20 percent of Beta’s equity.7. Is Alpha’s equity more or less risky than Beta’s equity? Explain.21. Cost of Capital Acetate, Inc., has equity with a market value of $35 million and debt with amarket value of $14 million. Treasury bills that mature in one year yield 6 percent per year, and the expected return on the market portfolio is 13 percent. The beta of Acetate’s equity is 1.15. The firm pays no taxes.1. What is Acetate’s debt–equity ratio?2. What is the firm’s weighted average cost of capital?3. What is the cost of capital for an otherwise identical all-equity firm?22. Homemade Leverage The Veblen Company and the Knight Company are identical in everyrespect except that Veblen is not levered. The market value of Knight Company’s 6 percent bonds is $1.2 million. Financial information for the two firms appears here. All earnings streams areperpetuities. Neither firm pays taxes. Both firms distribute all earnings available to common stockholders immediately.1. An investor who can borrow at 6 percent per year wishes to purchase 5 percent ofKnight’s equity. Can he increase his dollar return by purchasing 5 percent of Veblen’s equity if he borrows so that the initial net costs of the two strategies are the same?2. Given the two investment strategies in (a), which will investors choose? When will thisprocess cease?23. MM Propositions Locomotive Corporation is planning to repurchase part of its common stockby issuing corporate debt. As a result, the firm’s debt–equity ratio is expected to rise from 40 percent to 50 percent. The firm currently has $4.3 million worth of debt outstanding. The cost of this debt is 10 percent per year. Locomotive expects to have an EBIT of $1.68 million per year in perpetuity. Locomotive pays no taxes.1. What is the market value of Locomotive Corporation before and after the repurchaseannouncement?2. What is the expected return on the firm’s equity before the announcement of the stockrepurchase plan?3. What is the expected return on the equity of an otherwise identical all-equity firm?4. What is the expected return on the firm’s equity after the announcement of the stockrepurchase plan?24. Stock Value and Leverage Green Manufacturing, Inc., plans to announce that it will issue $3million of perpetual debt and use the proceeds to repurchase common stock. The bonds will sell at par with a 6 percent annual coupon rate. Green is currently an all-equity firm worth $9.5 million with 600,000 shares of common stock outstanding. After the sale of the bonds, Green will maintain the new capital structure indefinitely. Green currently generates annual pretax earnings of $1.8 million. This level of earnings is expected to remain constant in perpetuity. Green is subject to a corporate tax rate of 40 percent.1. What is the expected return on Green’s equity before the announcement of the debtissue?2. Construct Green’s market value balance sheet before the announcement of the debt issue.What is the price per share of the firm’s equity?3. Construct Green’s market value balance sheet immediately after the announcement of thedebt issue.4. What is Green’s stock price per share immediately after the repurchase announcement?5. How many shares will Green repurchase as a result of the debt issue? How many shares ofcommon stock will remain after the repurchase?6. Construct the market value balance sheet after the restructuring.7. What is the required return on Green’s equity after the restructuring?levered cost of equity. Now calculate the unlevered cost of equity, then the unlevered EBIT. What is the unlevered value of the company? What is the value of the interest tax shield and the value of the levered company?Mini Case: STEPHENSON REAL ESTATE RECAPITALIZATIONStephenson Real Estate Company was founded 25 years ago by the current CEO, Robert Stephenson. The company purchases real estate, including land and buildings, and rents the property to tenants. The company has shown a profit every year for the past 18 years, and the shareholders are satisfied with the company’s management. Prior to founding Stephenson Real Estate, Robert was the founder and CEO of a failed alpaca farming operation. The resulting bankruptcy made him extremely averse to debt financing. As a result, the company is entirely equity financed, with 20 million shares of common stock outstanding. The stock currently trades at $35.50 per share.Stephenson is evaluating a plan to purchase a huge tract of land in the southeastern United States for $60 million. The land will subsequently be leased to tenant farmers. This purchase is expected to increase Stephenson’s annual pretax earnings by $14 million in perpetuity. Kim Weyand, the company’s new CFO, has been put in charge of the project. Kim has determined that the company’s current cost of capital is 12.5 percent. She feels that the company would be more valuable if it included debt in its capital structure, so she is evaluating whether the company should issue debt to entirely finance the project. Based on some conversations with investment banks, she thinks that the company can issue bonds at par value with an 8 percent coupon rate. Based on her analysis, she also believes that a capital structure in the range of 70 percent equity/30 percent debt would be optimal. If the company goes beyond 30 percent debt, its bonds would carry a lower rating and a much higher coupon because the possibility of financial distress and the associated costs would rise sharply. Stephenson has a 40 percent corporate tax rate (state and federal).1. If Stephenson wishes to maximize its total market value, would you recommend that it issuedebt or equity to finance the land purchase? Explain.2. Construct Stephenson’s market value balance sheet before it announces the purchase.3. Suppose Stephenson decides to issue equity to finance the purchase.1. What is the net present value of the project?2. Construct Stephenson’s market value balance sheet after it announces that the firm willfinance the purchase using equity. What would be the new price per share of the firm’sstock? How many shares will Stephenson need to issue to finance the purchase?3. Construct Stephenson’s market value balance sheet after the equity issue but before thepurchase has been made. How many shares of common stock does Stephenson haveoutstanding? What is the price per share of the firm’s stock?4. Construct Stephenson’s market value balance sheet after the purchase has been made. 4. Suppose Stephenson decides to issue debt to finance the purchase.1. What will the market value of the Stephenson company be if the purchase is financed withdebt?2. Construct Stephenson’s market value balance sheet after both the debt issue and the landpurchase. What is the price per share of the firm’s stock?5. Which method of financing maximizes the per-share stock price of Stephenson’s equity?。

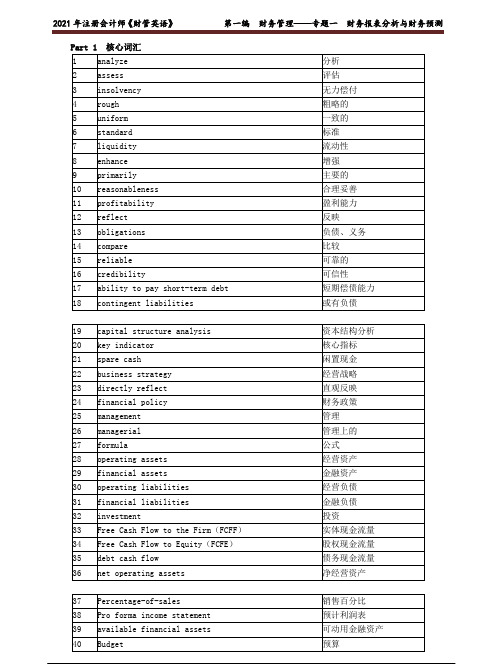

2021 年注册会计师《财管英语》各章节高频考点讲解及真题练习

Part 1 核心词汇Part 2 重难点讲解之一传统财务报表分析一、财务报表分析的目的与方法二、财务比率分析提示:提示:提示:提示:提示:【例题1 2016年考题】甲企业是一家医疗器械企业,现对公司财务状况和经营成果进行分析,以发现和主要竞争对手乙公司的差异。

(1)甲公司2015年主要财务数据如下所示:单位:万元(2)乙公司相关财务比率:要求:(1)使用因素分析法,按照营业净利率、总资产周转率、权益乘数的顺序,对2015年甲公司相对于乙公司权益净利率的差异进行定量分析;(2)说明营业净利率、总资产周转率、权益乘数三个指标各自经济含义及各评价企业哪方面能力,并指出甲、乙公司在经营战略和财务政策上的差别。

【答案】(1)甲公司:营业净利率=3600/30000×100%=12%总资产周转率=30000/24000=1.25(次)权益乘数=24000/12000=2Company Jia:Net Profit Margin=3600/30000×100%=12%Total assets turnover=30000/24000=1.25(times)Equity multiplier=24000/12000=2甲公司权益净利率=12%×1.25×2=30%乙公司权益净利率=24%×0.6×1.5=21.6%Rate of return on equity of Company Jia=12%×1.25×2=30%Rate of return on equity of Company Yi=24%×0.6×1.5=21.6%权益净利率差异=30%-21.6%=8.4%销售净利率差异造成的权益净利率差异=(12%-24%)×0.6×1.5=-10.8%Difference of rates of return on equity=30%-21.6%=8.4%Difference of rates of return on equity due to difference of net profit margins=(12%-24%)×0.6×1.5=-10.8%总资产周转率差异造成的权益净利率差异=12%×(1.25-0.6)×1.5=11.7%权益乘数差异造成的权益净利率差异=12%×1.25×(2-1.5)=7.5%Difference of rates of return on equity due to difference of total assets turnovers=12%×(1.25-0.6)×1.5=11.7%Difference of rates of return on equity due to difference of equity multipliers=12%×1.25×(2-1.5)=7.5%(2)营业净利率反映每1元销售收入取得的净利润,可以概括企业的全部经营成果,该比率越大,企业的盈利能力越强。

CFA考试二级模拟试题精选0401-20(附详解)

CFA考试二级模拟试题精选0401-20(附详解)1、The normalized earnings after tax for FAMCO is closest to:【单选题】A.$32,940,000.B.$34,260,000.C.$34,860,000.正确答案:C答案解析:C is correct. The new interest level is $2,000,000 instead of $1,000,000. SG&A expenses are reduced by $1,600,000 ( = $5,400,000 – $7,000,000) to $21,400,000 by salary expense savings. Other than a calculation of a revised provision for taxes, no other changes to the income statement results in normalized earnings before tax of $58,100,000 and normalized earnings after tax of $34,860,000.2、The hypothetical Orion trade generated an approximate:【单选题】A.loss of £117,000.B.gain of £117,000.C.gain of £234,000.正确答案:B答案解析:B is correct. The gain on the hypothetical Orion trade is £117,000, calculated as follows.3、What is the value per share of High Tech stock using the discounted cash flow approach if the terminal value of High Tech is based on using the cash flow multiple method to determine terminal value?【单选题】A.$35.22.B.$40.56.C.$41.57.正确答案:B答案解析:B is correct. The estimated stock price is $40.56.4、Dobson is wondering what the consequences would be if the duration of the first stage was assumed to be 11 years instead of 8, with all the other assumptions/estimates remaining the same. Considering this change, which of the following is true?【单选题】A.In the second approach, the proportion of the total value of the stock represented byB.The total value estimated using the third approach would increase.C.正确答案:B答案解析:B is correct. If the extraordinary growth rate of 14 percent is expected to continue for a longer duration, the stock’s value would increase. Choice A is false because given that the first stage is longer (11 years instead of 8), the terminal value is being calculated at a later point in time. So, its present value would be smaller. Moreover, the first stage has more years and contributes more to the total value. Overall, the proportion contributed by the second stage would be smaller. Choice C is false because the intrinsic value of the stock would be higher and the appropriate conclusion would be that the stock would be undervalued to a greater extent based on the first approach.5、When removing the multi-factor analysis from his research report, does Grohl violate any CFA Standards?【单选题】A.No.B.Yes, because he no longer has a reasonable basis for his recommendation.C.Yes, because he is required to make full and fair disclosure of all relevant正确答案:A答案解析:A is correct. Removing the multi-factor analysis from the research report does not constitute a violation. Grohl diligently prepared the internal document according to the firm’s traditional format with a complete fundamental analysis and recommendati on—indicating diligence and a reasonable basis for his recommendation. It would be wise for Grohl to retain records of the multi-factor analysis but he need not retain the analysis in the research report to comply with Standards V(A)–Diligence and Reasonable Basis or V(C)–Record Retention.6、The divestiture technique that Lee is recommending is most likely:【单选题】A.a spin-off.B.a split-off.C.an equity carve-out.正确答案:C答案解析:C is correct. An equity carve-out involves sale of equity in a new legal entity to outsiders, and would thus result in a cash inflow for Moonbase. A spin-off or a split-off does not generate a cash flow to the firm.7、Based on Note 16, after reclassifying pension components to reflect economic income or expense, the net adjustment to profit before taxation is:【单选题】A.–€205 million.B.–€94 million.C.+€129 million.正确答案:B答案解析:B is correct. Operating income is adjusted to include only the current service costs, the interest cost component is reclassified as interest expense, and the actual return on plan assets is added as investment income. Profit before taxation adjusted for actual rather than expected return on plan assets will decrease by €94 million (205 – 299).8、The value of Position 2 is closest to:【单选题】A.–¥149,925.B.–¥150,000.C.–¥150,075.正确答案:A答案解析:A is correct. The value of Troubadour’s euro/JGB forward position is calculated as9、【单选题】A.B.C.正确答案:C答案解析:The 7-year, 7.25% convertible bond has a market price of $947 (given) and, therefore, does not qualify (as it is below par).10、Which of the following statements regarding the consolidation of WMC's Ukrainian subsidiary for the next year is least likely correct? Compared to the temporal method, the Ukrainian subsidiary's translated:【单选题】 income before translation gains or losses would be higher using the current rate method.B.Debt-to-equity ratio would be higher using the current rate method.C.Gross profit margin would be lower using the current rate method.正确答案:C答案解析:Under both the current rate and temporal methods, the revenues for the Ukrainian subsidiary would be translated using the average rate. Cost of goods sold (COGS) would be translated using the historical rate for the temporal method and the average rate for the current rate method. When a currency is depreciating, the COGS based on historical cost (temporal method) will be higher than COGS translated at the average rate (current rate method) since the average rate will incorporate the historical exchange rate and the most recent (depreciated) exchange rate, decreasing the COGS. Since translated sales are the same under both methods, gross profit and the gross profit margin will be higher under the current rate method.。

罗斯《公司理财》英文习题答案DOCchap014

公司理财习题答案第十四章Chapter 14: Long-Term Financing: An Introduction14.1 a. C om m on Stock A ccountPar V alue$135,430$267,715 shares ==b. Net capital from the sale of shares = Common Stock + Capital SurplusNet capital = $135,430 + $203,145 = $338,575Therefore, the average price is $338,575 / 67,715 = $5 per shareAlternate solution:Average price = Par value + Average capital surplus= $2 + $203,145 / 67,715= $5 per sharec. Book value = Assets - Liabilities = Equity= Common stock + Capital surplus + Retained earnings= $2,708,600Therefore, book value per share is $2,708,600 / 67,715= $40.14.2 a. Common stock = (Shares outstanding ) x (Par value)= 500 x $1= $500Total = $150,500b.Common stock (1500 shares outstanding, $1 par) $1,500Capital surplus* 79,000Retained earnings 100,000Total $180,500* Capital Surplus = Old surplus + Surplus on sale= $50,000 + ($30 - $1) x 1,000=$79,00014.3 a. Shareholders’ equityCommon stock ($5 par value; authorized 500,000shares; issued and outstanding 325,000 shares)$1,625,000 Capital in excess of par* 195,000Retained earnings** 3,794,600Total $5,614,600*Capital surplus = 12% of Common Stock= (0.12) ($1,625,000)= $195,000**Retained earnings = Old retained earnings + Net income - Dividends= $3,545,000 + $260,000 - ($260,000)(0.04)= 3,794,600b. Shareholders’ equity$1,750,000Common stock ($5 par value; authorized 500,000shares; issued and outstanding 350,000 shares)Capital in excess of par* 170,000Retained earnings 3,794,600Total $5,714,600*Capital surplus is reduced by the below par sale, i.e. $195,000 - ($1)(25,000) =$170,00014.4 a. Under straight voting, one share equals one vote. Thus, to ensure the election of onedirector you must hold a majority of the shares. Since two million shares areoutstanding, you must hold more than 1,000,000 shares to have a majority of votes.b. Cumulative voting is often more easily understood through a story. Remember thatyour goal is to elect one board member of the seven who will be chosen today.Suppose the firm has 28 shares outstanding. You own 4 of the shares and one otherperson owns the remaining 24 shares. Under cumulative voting, the total number ofvotes equals the number of shares times the number of directors being elected,(28)(7) = 196. Therefore, you have 28 votes and the other stockholder has 168 votes.Also, suppose the other shareholder does not wish to have your favorite candidateon the board. If that is true, the best you can do to try to ensure electing onemember is to place all of your votes on your favorite candidate. To keep yourcandidate off the board, the other shareholder must have enough votes to elect allseven members who will be chosen. If the other shareholder splits her votes evenlyacross her seven favorite candidates, then eight people, your one favorite and herseven favorites, will all have the same number of votes. There will be a tie! If shedoes not split her votes evenly (for example 29 28 28 28 28 28 27) then yourcandidate will win a seat. To avoid a tie and assure your candidate of victory, youmust have 29 votes which means you must own more than 4 shares.Notice what happened. If seven board members will be elected and you want to becertain that one of your favorite candidates will win, you must have more than one-eighth of the shares. That is, the percentage of the shares you must have to win ismore than1.(The num ber of m em bers being elected The num ber you w ant to select)Also notice that the number of shares you need does not change if more than oneperson owns the remaining shares. If several people owned the remaining 168shares they could form a coalition and vote together.Thus, in the Unicorn election, you will need more than 1/(7+1) = 12.5% of theshares to elect one board member. You will need more than (2,000,000) (0.125) =250,000 shares.Cumulative voting can be viewed more rigorously. Use the facts from the Unicornelection. Under cumulative voting, the total number of votes equals the number of公司理财习题答案第十四章shares times the number of directors being elected, 2,000,000 x 7 = 14,000,000. Let x be the number of shares you need. The number of shares necessary is7x14,000,0007x7x250,000.>-==>> You will need more than 250,000 shares.14.5 She can be certain to have one of her candidate friends be elected under the cumulativevoting rule. The lowest percentage of shares she needs to own to elect at least one out of 6candidates is higher than 1/7 = 14.3%. Her current ownership of 17.3% is more thanenough to ensure one seat. If the voting rule is staggered as described in the question, shewould need to own more than 1/4=25% of the shares to elect one out of the three candidatesfor certain. In this case, she will not have enough shares.14.6 a. You currently own 120 shares or 28.57% of the outstanding shares. You need to control 1/3 of the votes, which requires 140 shares. You need just over 20 additionalshares to elect yourself to the board.b. You need just over 25% of the shares, which is 250,000 shares. At $5 a share it willcost you $2,500,000 to guarantee yourself a seat on the board.14.7 The differences between preferred stock and debt are:a. The dividends of preferred stock cannot be deducted as interest expenses whendetermining taxable corporate income. From the individual investor’s point of view,preferred dividends are ordinary income for tax purposes. From corporate investors,80% of the amount they receive as dividends from preferred stock are exempt fromincome taxes.b. In liquidation, the seniority of preferred stock follows that of the debt and leads thatof the common stock.c. There is no legal obligation for firms to pay out preferred dividends as opposed tothe obligated payment of interest on bonds. Therefore, firms cannot be forced intodefault if a preferred stock dividend is not paid in a given year. Preferred dividendscan be cumulative or non-cumulative, and they can also be deferred indefinitely.14.8 Some firms can benefit from issuing preferred stock. The reasons can be:a. Public utilities can pass the tax disadvantage of issuing preferred stock on to theircustomers, so there is substantial amount of straight preferred stock issued byutilities.b. Firms reporting losses to the IRS already don’t have positive income for taxdeduction, so they are not affected by the tax disadvantage of dividend vs. interestpayment. They may be willing to issue preferred stock.c. Firms that issue preferred stock can avoid the threat of bankruptcy that exists withdebt financing because preferred dividends are not legal obligation as interestpayment on corporate debt.14.9 a. The return on non-convertible preferred stock is lower than the return on corporatebond for two reasons:i. Corporate investors receive 80% tax deductibility on dividends if they hold thestock. Therefore, they are willing to pay more for the stock; that lowers its return.ii. Issuing corporations are willing and able to offer higher returns on debt since theinterest on the debt reduces their tax liabilities. Preferred dividends are paid outof net income, hence they provide no tax shield.b. Corporate investors are the primary holders of preferred stock since, unlikeindividual investors, they can deduct 80% of the dividend when computing their taxliability. Therefore, they are willing to accept the lower return which the stockgenerates.14.10 The following table summarizes the main difference between debt and equity.Debt EquityRepayment is an obligation of the firm Yes NoGrants ownership of the firm No YesProvides a tax shield Yes NoLiquidation will result if not paid Yes NoCompanies often issue hybrid securities because of the potential tax shield and thebankruptcy advantage. If the IRS accepts the security as debt, the firm can use it as a tax shield. If the security maintains the bankruptcy and ownership advantages of equity, the firm has the best of both worlds.14.11 The trends in long-term financing in the United States were presented in the text. If CableCompany follows the trends, it will probably use 80% internal financing, net income of the project plus depreciation less dividends, and 20% external financing, long term debt and equity.。

财务管理专业英语句子及单词翻译

财务管理专业英语句子及单词翻译Financial management is an integrated decision-making process concerned with acquiring, financing, and managing assets to accomplish some overall goal within a business entity.财务管理是为了实现一个公司总体目标而进行的涉及到获取、融资和资产管理的综合决策过程。

Decisions involving a firm’s short-term assets and liabilities refer to working capital management.决断涉及一个公司的短期的资产和负债提到营运资金管理The firm’s long-term financing decisions concern the right-hand side of the balance sheet.该公司的长期融资决断股份资产负债表的右边。

This is an important decision as the legal structure affects the financial risk faced by the owners of the company.这是一个重要的决定作为法律结构影响金融风险面对附近的的业主的公司。

The board includes some members of top management(executive directors), but should also include individuals from outside the company(non-executive directors).董事会包括有些隶属于高层管理人员(执行董事),但将也包括个体从外公司(非执行董事)。

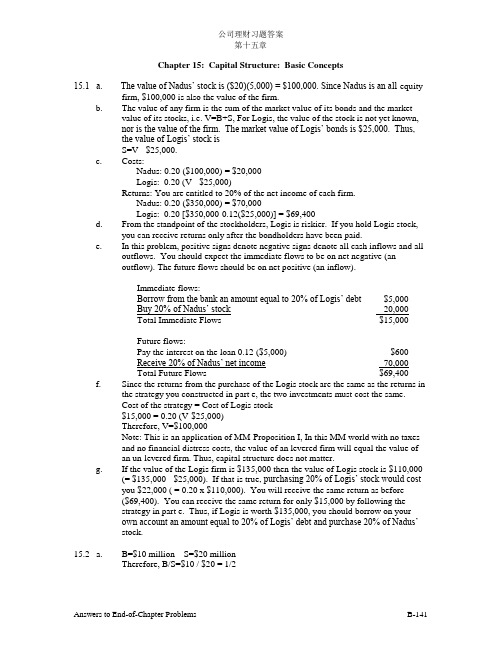

罗斯《公司理财》英文习题答案DOCchap015

公司理财习题答案第十五章Chapter 15: Capital Structure: Basic Concepts15.1 a. The value of Nadus’ stock is ($20)(5,000) = $100,000. Since Nadus is an all-equityfirm, $100,000 is also the value of the firm.b. The value of any firm is the sum of the market value of its bonds and the marketvalue of its stocks, i.e. V=B+S, For Logis, the value of the stock is not yet known,nor is the value of the firm. The market value of Logis’ bonds is $25,000. Thus,the value of Logis’ stock isS=V - $25,000.c. Costs:Nadus: 0.20 ($100,000) = $20,000Logis: 0.20 (V - $25,000)Returns: You are entitled to 20% of the net income of each firm.Nadus: 0.20 ($350,000) = $70,000Logis: 0.20 [$350,000-0.12($25,000)] = $69,400d. From the standpoint of the stockholders, Logis is riskier. If you hold Logis stock,you can receive returns only after the bondholders have been paid.e. In this problem, positive signs denote negative signs denote all cash inflows and alloutflows. You should expect the immediate flows to be on net negative (anoutflow). The future flows should be on net positive (an inflow).Immediate flows:Borrow from the bank an amount equal to 20% of Logis’ debt$5,000Buy 20% of Nadus’ stock -20,000Total Immediate Flows -$15,000Future flows:Pay the interest on the loan 0.12 ($5,000) -$600Receive 20% of Nadus’ net income 70,000Total Future Flows $69,400f. Since the returns from the purchase of the Logis stock are the same as the returns inthe strategy you constructed in part e, the two investments must cost the same.Cost of the strategy = Cost of Logis stock$15,000 = 0.20 (V-$25,000)Therefore, V=$100,000Note: This is an application of MM-Proposition I, In this MM world with no taxesand no financial distress costs, the value of an levered firm will equal the value ofan un-levered firm. Thus, capital structure does not matter.g. If the value of the Logis firm is $135,000 then the value of Logis stock is $110,000(= $135,000 - $25,000). If that is true, purchasing 20% of Logis’ stock would costyou $22,000 ( = 0.20 x $110,000). You will receive the same return as before($69,400). You can receive the same return for only $15,000 by following thestrategy in part e. Thus, if Logis is worth $135,000, you should borrow on yourown account an amount equal to 20% of Logis’ debt and purchase 20% of Nadus’stock.15.2 a. B=$10 million S=$20 millionTherefore, B/S=$10 / $20 = 1/2b. The required return is the firm’s after-tax overall cost of capital. In this no tax world,that is simplyrBVrSVr 0B S =+Use CAPM to find the required return on equity. Sr = 8% + (0.9)(10%) = 17%The cost of debt is 14%.Therefore,r$10 m illion$30 m illion0.14$20 m illion$30 m illion0.1716% 0=+=15.3 You expect to earn a 20% return on your investment of $25,000. Thus, you are earning$5,000 (=$25,000 x 0.20) per year. Since you borrowed $75,000, you will be makinginterest payments of $7,500 (=$75,000 x 0.10) per annum. Your share of the stock must earn $12,500 (= $5,000 + $7,500). The return without leverage is 0.125 (=$12,500 /$100,000).15.4 The firms are identical except for their capital structures. Thus, under MM-Proposition Itheir market values must be the same regardless of their capital structures. If they are not equal, the lower valued stock is a better purchase.Market values:Levered: V=$275 million + $100 x 4.5 million = $725 millionUnlevered: V= $80 x 10 million = $800 millionSince Levered’s market value is less than Unlevered’s market value, you should buyLevered’s stock. To understand why, construct the strategies that were presented in thetext. Suppose you want to own 5% of the equity of each firm.Strategy One: Buy 5% of Unlevered’s equityStrategy Two: Buy 5% of Levered’s equityStrategy Three: Create the dollar returns of Levered through borrowing an amount equal to 5% of Levered’s debt and purchasing 5% of Unlevered’s stock. If youfollow this strategy you will own what amounts to 5% of the equity ofLevered. The reason why is that the dollar returns will be identical topurchasing 5% of Levered outright.Dollar Investment Dollar Return Strategy One: -(0.05)($800) (0.05)($96)Strategy Two: -(0.05)($450) (0.05)[$96 - (0.08)($275)]Strategy Three:Borrow (0.05)($275) -[(0.05) ($275)] (0.08)Buy Unlevered -(0.05)($800) (0.05)($96)Net $ Flows -(0.05)($525) (0.05)[$96 - (0.08)($275)] Note: Dollar amounts are in millions.Note: Negative signs denote outflows and positive denotes inflows.Since the payoffs to strategies Two and Three are identical, their costs should be the same.Yet, strategy three is more expensive than strategy two ($26.25 million versus $22.5公司理财习题答案第十五章million). Thus, Levered’s stock is underpriced relative to Unlevered’s stock. You should purchase Levered’s s tock.15.5 a. In this MM world, the market value of Veblen must be the same as the market valueof Knight. If they are not equal, an investor can improve his net returns throughborrowing and buying Veblen stock. To understand the improvement, construct thestrategies discussed in the text. The investor already owns 0.0058343 (=$10,000 /$1,714,000) of the equity of Knight. Suppose he is willing to purchase the sameamount of Veblen’s equity.Strategy One (SI): Buy 0.58343% of Veblen’s equit y.Strategy Two (SII): Continue to hold the 0.58343% of Knight’s equity.Strategy Three (SIII): Create the dollar returns of Knight through borrowing anamount equal to 0.58343% of Knight’s debt and purchasing0.58343% of Veblen’s stock. If you follow this strategy youwill own what amounts to 0.58343% of the equity of Knight.The reason why is that the dollar returns will be identical topurchasing 0.58343% of Knight outright.Dollar Investment Dollar Return SI: -(0.0058343)($2.4) (0.0058343)($0.3)SII: -(0.0058343)($1.714) (0.0058343)($0.24)SIII:Borrow (0.0058343)($1) -[(0.0058343) ($1)] (0.06)Buy Veblen -(0.0058343)($2.4) (0.0058343)($0.3)Net $ Flows -(0.0058343)($1.4) (0.0058343)($0.24) Note: Dollar amounts are in millions.Note: Negative signs denote outflows and positive denotes inflows.Since strategies Two and Three have the same payoffs, they should cost the same.Strategy three is cheaper, thus, Knight stock is overpriced relative to Veblen stock.An investor can benefit by selling the Knight stock, borrowing an amount equal to0.0058343 of Knights debt and buying the same portion of Veblen stock. Theinvestor’s dollar returns will be identical to holding the Knight stock, but the costwill be less.b. Modigliani and Miller argue that everyone would attempt to construct the strategy.Investors would attempt to follow the strategy and the act of them doing so willlower the market value of Knight and raise the market value of Veblen until theyare equal.15.6 Each lady has purchased shares of the all-equity NLAW and borrowed or lent to create thenet dollar returns she desires. Once NLAW becomes levered, the return that the ladiesreceive for owning stock will be decreased by the interest payments. Thus, to continue to receive the same net dollar returns, each lady must rebalance her portfolio. The easiestapproach to this problem is to consider each lady individually. Determine the dollarreturns that the investor would receive from an all-equity NLAW. Determine what she will receive from the firm if it is levered. Then adjust her borrowing or lending position tocreate the returns she received from the all-equity firm.Before looking at the women’s positions, look at the firm value.All-equity: V=100,000 x $50 = $5,000,000Levered: V=$1,000,000 + 80,000 x $50 = $5,000,000Remember, the firm repurchased 20,000 shares.The income of the firm is unknown. Since we need it to compute the investor’s returns, we will denote it as Y. Assume that the income of the firm does not change due to the capital restructuring and that it is constant for the foreseeable future.Ms. A before rebalancing: Ms. A owns $10,000 worth of NLAW stock. That ownership represents ownership of 0.002 (=$10,000/$5,000,000) of the all-equity firm. That ownership entitles her to receive 0.002 of the firm’s income; i.e. her dollar return is 0.002Y. Also, Ms. A has borrowed $2,000. That loan will require her to make an interest payment of $400 ($2,000 x 0.20). Thus, the dollar investment and dollar return positions of Ms. A are:Dollar Investment Dollar Return NLAW Stock -$10,000 0.002YBorrowing 2,000 -$400Net -$8,000 0.002Y-$400Note: Negative signs denote outflows and positive denotes inflows.Ms. A after rebalancing: After rebalancing, Ms. A will want to receive net dollar returnsof 0.002Y-$400. The only way to receive the 0.002Y is to own 0.002 of NLAW’s stock. Examine the returns she will receive from the levered NLAW if she owns 0.002 of thef irm’s equity. She will receive (0.002) [Y - ($1,000,000)(0.20)] = 0.002Y - $400. This is exactly the dollar return she desires! Therefore, Ms. A should own 0.002 of the levered firm’s equity and neither lends nor borrow. Owning 0.002 of the firm’s equi ty means she has $8,000 (= 0.0002 x $4,000,000) invested in NLAW stock.Dollar Investment Dollar Return NLAW stock -$8,000 0.002Y - $400Ms. B before rebalancing: Ms. B owns $50,000 worth of NLAW stock. That ownership represents ownership of 0.01 (=$50,000/$5,000,000) of the all-equity firm. That ownership entitles her to receive 0.01 of the firm’s income; i.e. her dollar return is 0.01Y. Also, Ms. B has lent $6,000. That loan will generate interest income for her of the amount $1,200 (=$6,000 x 0.20). Thus, the dollar investment and dollar return positions of Ms. B are:Dollar Investment Dollar Return NLAW Stock -$50,000 0.01YLending -6,000 $1,200Net -$56,000 0.01Y + $1,200Ms. B after rebalancing: After rebalancing, Ms. B will want to receive net dollar returns of 0.01Y + $1,200. The only way to receive the 0.01Y is to own 0.01 of NLAW’s stock. Examine the returns she will receive from the levered NLAW if she owns 0.01 of the firm’s equity. She will receive (0.01) [Y - ($1,000,000) (0.20)] = 0.01Y - $2,000. This is not the return which Ms. B desires, so she must lend enough money to generate interest income of $3,200 (=$2,000 + $1,200). Since the interest rate is 20% she must lend公司理财习题答案第十五章$16,000 (= $3,200 / 0.20). The 0.01 equity interest of Ms. B means she will have $40,000 (=0.01 x $4,000,000) invested in NLAW.Dollar Investment Dollar ReturnNLAW Stock -$40,000 0.01Y - $2,000Lending -16,000 $3,200Net -$56,000 0.01Y + $1,200Ms. C before rebalancing: Ms. C owns $20,000 worth of NLAW stock. That ownershiprepresents ownership of 0.004 (=$20,000 / $5,000,000) of the all-equity firm. Thatownership entitles her to receive 0.004 of the firm’s income; i.e. her dollar return is 0.004Y.The dollar investment and dollar return positions of Ms. A are:Dollar Investment Dollar ReturnNLAW Stock -$20,000 0.004YMs. C after rebalancing: After rebalancing, Ms. C will want to receive net dollar returns of0.004Y. The only way to receive the 0.004Y is to ow n 0.004 of NLAW’s stock. Examinethe returns she will receive from the levered NLAW if she owns 0.004 of the firm’s equity.She will receive (0.004) [Y - ($1,000,000) (0.20)] = 0.004Y - $800. This is not the dollar return she desires. Therefore, Ms. C must lend enough money to offset the $800 she loses once the firm becomes levered. Since the interest rate is 20% she must lend $4,000 (=$800 / 0.20). The 0.004 equity interest of Ms. C means she will have $16,000 (0.004 x$4,000,000) invested in NLAW.Dollar Investment Dollar ReturnNLAW Stock -$16,000 0.004Y - $800Lending -4,000 $800Net -$20,000 0.004Y15.7 a. Since Rayburn is currently an all-equity firm, the value of the firm’s assets equalsthe value of its equity. Under MM-Proposition One, the value of a firm will notchange due to a capital structure change, and the overall cost of capital will remainunchanged. Therefore, Rayburn’s overall cost of capital is 18%.b. MM-Proposition Two states r r(B/S)(r r)=+-.S00BApplying this formula you can find the cost of equity.r = 18% + ($400,000 / $1,600,000) (18% - 10%) = 20%Sc. In accordance with Proposition Two, the expected return on Rayburn’s equity willrise with the amount of leverage. This rise occurs because of the risk which the debt adds.15.8 a.b.i. According to efficient markets, Strom’s stock price will rise immediately toreflect the NPV of the project.ii. The NPV of the facilities that Strom is buying isNPV= -$300,000 + ($120,000 / 0.15) = $500,000The sum of the old assets and the NPV of the new facilities is the new value ofthe firm ($5.5 million). Since new shares have not yet been sold, the price of theoutstanding shares must rise. The new price is $5,500,000 / 250,000 = $22.iii. Strom needed to raise $300,000 through the sale of stock that sells for $22.Thus, Strom sold 13,636.364 (=$300,000 / $22) shares.iv.v.vi. The returns available to the shareholders are the sum of the returns from each portion of the firm.Total earnings = $750,000 + $120,000 = $870,000Return = ($870,000 / $5,800,000) = 15%Note: The returns to the shareholder had to be the same since r0 was unchangedand the firm added no debt.c.i.Under efficient markets the price of the shares must rise to reflect the NPV of thenew facilities. The value will be the same as with all-equity financing because1. Strom purchased the same competitor and2. In this MM world debt is no better or no worse than equity.公司理财习题答案第十五章ii.iii. The cost of equity will be the earnings after interest and taxes divided by the market value of common. Since Strom pays no taxes, the cost of equity is simplythe earnings after interest (EAI) divided by the market value of common.EAI = $750,000 + $120,000 - $300,000 (0.10) = $840,000Cost of equity = $840,000 / $5,500,000 = 15.27%iv. The debt causes the equity of the firm to be riskier. Remember, stockholders are residual owners of the firm.v. MM-Proposition Two states,r r(B/S)(r r)15%($300,000/$5,500,000)(15%10%)15.27% =+-=+-=S00Bd. Examine the final balance sheet for the firm and you will see that the price is $22under each plan.15.9 a. The market value of the firm will be the present value of Gulf’s earning s after thenew plant is built. Since the firm is an all-equity firm, the overall required return isthe required return on equity.Annual earnings = Original plant + New Plant= $27 million + $3 million = $30 millionValue = $30 million / 0.1 = $300 millionb. Gulf Power is in an MM world (no taxes, no costs of financial distress). Therefore,the value of the firm is unchanged by a change in the capital structure.c. The overall required rate of return is also unchanged by the capital structurechange. Thus, according to MM-Proposition Two, r r(B/S)(r r)=+-. TheS00B firm is valued at $300 million of which $20 million is debt. The remaining $280million is the value of the stock.r S = 10% + ($20 million / $280 million) (10% - 8%) = 10.14%15.10 a. False. Leverage increases both the risks of the stock and its expected return. MMpoint out that these two effects exactly cancel out each other and leave the price ofthe stock and the value of the firm invariant to leverage. Since leverage is beingreduced in this firm, the risk of the shares is lower; however, the price of the stockremains the same in accordance with MM.b. False. If moderate borrowing does not affect the probability of financial distress,then the required return on equity is proportional to the debt-equity ratio [i.e.=+-]. Increasing the amount of debt will increase the return on r r(B/S)(r r)S00Bequity.15.11 a.i. Individuals can borrow at the same interest rate at which firms borrow.ii. There are no taxes.iii. There are no costs of financial distress.b.i. If firms are able to borrow at a rate that is lower than that at which individualsborrow, then it is possible to increase the firm’s value through borrowing. Asthe text discussed, since investors can purchase securities on margin, theindividuals’ effective rate is probably no higher than that of the firms.ii. In the presence of corporate taxes, the value of the firm is positively related to the level of debt. Since interest payments are deductible, increasing debtminimizes tax expenditure and thus maximizes the value of the firm for thestockholders. As will be shown in the next chapter, personal taxes offset thepositive effect of debt.iii. Because these costs are substantial and stockholders eventually bear them, they are incentives to lower the amount of debt. This implies that the capital structuremay matter. This topic will also be discussed more fully in the next chapter. 15.12 a and b.Total investment in the firm’s assets = $10 x 1million x 1% = $0.1 million3 choices of financing 20% debt 40% debt 60% debtTotal asset investment 0.1 0.1 0.1x ROA (15%) 0.015 0.015 0.015- Interest 0.2 x 0.1 x0.1 0.4 x 0.1 x 0.1 0.6 x 0.1 x 0.1Profit after interest 0.013 0.011 0.009/ Investment in equity 0.1 x 0.8 0.1 x 0.6 0.1 x 0.4ROE 16.25% 18.33% 22.5%Susan can expect to earn $0.013 million, $0.011 million, and $0.009 million,respectively, from the correspondent three scenarios of financing choices, i.e.borrowing 20%, 40%, or 60% of the total investment. The respective returns onequity are 16.25%, 18.33% and 22.5%.c. From part a and b, we can see that in an MM with no tax world, higher leveragebrings about higher return on equity. The high ROE is due to the increased risk ofequity while the WACC remains unchanged. See below.WACC for 20% debt = 16.25% x 0.8 + 10% x 0.2 = 15%WACC for 40% debt = 18.33% x 0.6 + 10% x 0.4 = 15%WACC for 60% debt = 22.5% x 0.4 + 10% x 0.6 = 15%This example is a case of homemade leverage, so the results are parallel to that of aleveraged firm.15.13 Suppose individuals can borrow at the same rate as the corporation, there is no needfor the firm to change its capital structure because of the different forecasts ofearnings growth rates, as investors can always duplicate the leverage by creatinghomemade leverage. Different expectation of earnings growth rates can affect theexpected return on assets. But this change is the result of the change in expectedoperating performance of the corporation and/or other macroeconomic factors. Theleverage ratio is irrelevant here since we are in an MM without tax world.公司理财习题答案第十五章15.14 a. current debt = 0.75 / 10% = $7.5 millioncurrent equity = 7.5 / 40% = $18.75 millionTotal firm value = 7.5 + 18.75 = $26.25 millionb. r s = earnings after interest/total equity value = $(3.75 - .75)/$18.75 = 16%r B =10%r 0 = (.4/1.4)(10%) + (1/1.4)(16%) = 14.29%r S after repurchase = 14.29% + (50%)(14.29% - 10%) = 16.44%So, the return on equity would increase from 16% to 16.44% with the completion of the planned stock repurchase.c. The stock price wouldn’t change because in an MM world, there’s no added value toa change in firm leverage. In other words, it’s a zero NPV transaction.15.15 a. Since V V T B L U C =+,V =V T B U L C -. L V = $1,700,000, B = $500,000 and C T =0.34. Therefore, the value of the unlevered firm isU V = $1,700,000 - (0.34)($500,000) = $1,530,000b. Equity holders earn 20% after-tax in an all-equity firm. That amount is $306,000(=$1,530,000 x 0.20). The yearly, after-tax interest expense in the levered firm is$33,000 [=$500,000 x 0.10 (1-0.34)]. Thus, the after-tax earnings of the equityholders in a levered firm are $273,000 (=$306,000 - $33,000). This amount is thefirm’s net income.15.16 The initial market value of the equity is given as $3,500,000. On a per share basis this is$20 (=$3,500,000 / 175,000). The firm buys back $1,000,000 worth of shares, or 50,000 (= $1,000,000 / $20) shares.In this MM world with taxes,V V T B L U C =+= $3,500,000 + (0.3) ($1,000,000) = $3,800,000Since V = B + S, the market value of the equity is $2,800,000 (= $3,800,000 - $1,000,000).15.17 a. Since Streiber is an all-equity firm,V = EBIT (1 - C T ) / 0r = $2,500,000 (1 - 0.34) / 0.20 = $8,250,000b. V V T B L U C =+= $8,250,000 + (0.34)($600,000) = $8,454,000c. The presence of debt creates a tax shield for the firm. That tax shield has value andaccounts for the increase in the value of the firm.d. You are making the MM assumptions:i. No personal taxesii. No costs of financial distressiii. Debt level of the firm is constant through time15.18 a. In this MM world with no financial distress costs, the value of the levered firm isgiven by V V T B L U C =+. The value of the unlevered firm is V = EBIT (1 - C T ) / r 0.The market value of the debt of Olbet is B = $200,000 / 0.08 = $2,500,000.Therefore, V = $1,200,000 (1 - 0.35) / 0.12 + ($2,500,000) (0.35) = $7,375,000b. Since debt adds to the value of the firm, it implies that the firm should be financedentirely with debt if it wishes to maximize its value.c. This conclusion is incorrect because it does not consider the costs of financialdistress or other agency costs that might offset the positive contribution of the debt. These costs will be discussed in further detail in the next chapter.15.19 a. Since Green is currently an all-equity firm, the value of the firm is the value of itsoutstanding equity, $10 million. The value of the firm must also equal the PV ofthe after-tax earnings, discounted at the overall required return. The after-taxearnings are simply ($1,500,000) (1 - 0.4) = $900,000. Thus, $10,000,000 =$900,000 / 0r0r = 0.09b. With 500,000 shares outstanding, the current price of a share is $20 (=$10,000,000 / 500,000). Green’s market value balance sheet isTherefore, at the announcement, the value of the firm will rise by the PV of the tax shield (PVTS). The PVTS is ($2,000,000) (0.4) = $800,000. Since the value of the firm has risen $800,000 and the debt has not yet been issued, the price of Green stock must rise to reflect the increase in firm value. Since the firm is worth $10,800,000 (=$10,000,000 + 800,000) and there are 500,000 shares outstanding,the price of a share rises to $21.60 (= $10,800,000 / 500,000). price of the stock rises to $21.60. Thus, Green will retire $2,000,000 / $21.60 = $92,592.59 shares. e. After the restructuring, the value of the firm will still be $10,800,000. Debt will be $2,000,000 and the 407,407.41 (=500,000 - 92,592.59) outstanding shares of stockwill sell for $21.60. )T -)(1r (B /S)(r r r C B 00S -+= = 0.09 + ($2,000,000 / $8,800,000) (0.09 - 0.06) (1 - 0.4) = 9.41%15.20 a.million $20.83$100.3515.0)65.0(4$B T r )T EBIT(1B T V V C 0C C U L =⨯+=+-=+= b.公司理财习题答案第十五章Answers to End-of-Chapter Problems B-15112.48%V )T EBIT(1r V S )T (1r V Br L C S L C B L WACC =-=+-= c. r r (B /S)(r r )(1-T S 00B C =+-)= 0.15 + [10 / (20.83 - 10)] (0.65) (0.15 - 0.10) = 18.01%15.21 a. r S = 0r + (B / S)( 0r – B r )(1 – C T )= 15% + (2.5)(15% – 11%)(1– 35%)= 21.50%b. If there is no debt, WACC r = r S = 15%c. S r = 15% + 0.75 (15% – 11%)(1 – 35%)= 16.95%B/S = 0.75, B = 0.75SB/(B+S) = 0.75S/(0.75S +S)= 0.75 /1.75S/(B+S) = 1– (0.75 /1.75) = (1/1.75)r WACC = (0.75/1.75)(0.11)(1– 0.35) + (1/1.75)(16.95%)= 12.75%S r = 15% + 1.5 (15% – 11%)(1 – 35%)= 18.90%B/S = 1.5, B = 1.5SB/(B+S) = 1.5S/(1.5S +S)= 1.5/2.5S /(B+S) = 1 – (1.5/2.5)WACC r = (1.5/2.5)(0.11)(1 – 0.35) + (1/2.5)(0.1890)= 11.85%15.22 Since this is an all-equity firm, the WACC = S r .$240,00025.0)4.01(000,100$r )T EBIT(1V S C U =-=-=If the firm borrows to repurchase its own shares, then the value of GT will be: L V = U V + C T B()$440,000000,500$4.025.0)6.0(000,100$=⨯+=。

国际财务管理课后习题答案chapter 5

CHAPTER 5 THE MARKET FOR FOREIGN EXCHANGESUGGESTED ANSWERS AND SOLUTIONS TO END-OF—CHAPTERQUESTIONS AND PROBLEMSQUESTIONS1。

Give a full definition of the market for foreign exchange。

Answer: Broadly defined, the foreign exchange (FX) market encompasses the conversion of purchasing power from one currency into another, bank deposits of foreign currency,the extension of credit denominated in a foreign currency, foreign trade financing, and trading in foreign currency options and futures contracts.2。

What is the difference between the retail or client market and the wholesale or interbank market for foreign exchange?Answer: The market for foreign exchange can be viewed as a two-tier market。

One tier is the wholesale or interbank market and the other tier is the retail or client market。

International banks provide the core of the FX market. They stand willing to buy or sell foreign currency for their own account。

高一英语经济学原理与金融知识单选题40题

高一英语经济学原理与金融知识单选题40题1. In a market economy, the price of a product is mainly determined by _____.A. the governmentB. producersC. the interaction of supply and demandD. consumers答案:C。

解析:在市场经济中,产品的价格主要由供求关系的相互作用决定。

选项A,在市场经济中政府不是主要决定产品价格的因素;选项B,生产者只能影响供应方面,单独生产者不能决定价格;选项D,消费者只能影响需求方面,单独消费者也不能决定价格。

本题考查“supply and demand(供求关系)”这个基本经济学概念的英语表达以及对市场经济中价格决定因素的理解。

2. Which of the following is a characteristic of a monopoly market?A. Many sellersB. Perfect competitionC. Only one sellerD. Easy entry for new firms答案:C。

解析:垄断市场的特征是只有一个卖家。

选项A,许多卖家是竞争市场的特征;选项B,完全竞争是另一种市场类型,和垄断市场特征不同;选项D,新企业容易进入是竞争市场的特点,而垄断市场通常有进入壁垒。

这里考查“monopoly((垄断)”这个概念对应的英语表达以及其特征的理解。

3. When the supply of a product increases while the demand remains the same, what will happen to the price?A. IncreaseB. Stay the sameC. Fluctuate randomlyD. Decrease答案:D。

财务管理专业英语复习题

《11级财务管理专业英语》复习资料考试题型:一、短语中英互译(20x1=20分)二、从下列选项中选出最佳答案(20x1=20分)三、计算题(25分)四、段落中英互译(35分)同学们:考试的时候请带上没有存储功能的计算器,试卷上只要是涉及到计算的题里面的数字可能与复习资料上的数字不完全一样,但是计算方法是完全一样的,所以大家要掌握计算方法,考试的时候要自己计算。

预祝同学们取得好成绩。

Part I terminology translation (1*20 points)Directions: interpret the following terminology in English or Chinese.(范围课后核心词汇)e.g.:1. financial management---译成汉语2.普通股----译成英语Part II Choice questions (1*20 points) (Please write your answer in the following table)1. Financial statement does not include ( )A. balance sheetB. income statementC. cash flow statementD. working sheet2. An increase in which one of the following will increase the operating cash flow?A.employee salariesB. office rentC. building maintenanceD. equipment depreciation3. The process of planning and managing a firm’s long-term investments is called:A. working capital management.B. financial depreciation.C. capital budgeting.D. capital structure.4. Cash equivalents include ( )A. time depositsB. inventoriesC. accounts receivableD. prepaid expenses5. The internal rate of return for a project will increase if:A. the initial cost of the project can be reduced.B. the total amount of the cash inflows is reduced.C. the required rate of return is reduced.D. the salvage value of the project is omitted from the analysis.6. Which of the following belongs to current liabilities?( )A. mortgages payableB. prepaid expensesC. notes payableD. bonds payable7. You spent $500 last week fixing the transmission in your car. Now, the brakes are acting up and you are trying to decide whether to fix them or trade the car in for a newer model. In analyzing the brake situation, the $500 you spent fixing the transmission is a(n) ___ cost.A. opportunityB. sunkC. incrementalD. fixed8. Which of the following statements are correct concerning diversifiable risks?I. Diversifiable risks can be essentially eliminated by investing in several securities.II. The market rewards investors for diversifiable risk by paying a risk premium.III. Diversifiable risks are generally associated with an individual firm or industry.IV. Beta measures diversifiable risk.A. I and III onlyB. II and IV onlyC. I and IV onlyD. II and III only9. Which of the following is a liability account?()A. prepaid insuranceB. additional paid-in capitalC. salaries payableD. accumulated depreciation10. Accountants employed by large corporations may work in the areas of the following except ( )A. product costing and pricingB. budgetingC. internal auditingD. product producing11. A corporation’s first sale of equity made available to the public is called a(n):()A. share repurchase program.B. private placement.C. initial public offering (IPO).D.seasoned equity offering (SEO).12. Standard deviation measures ____ risk.A. totalB. nondiversifiableC. unsystematicD. systematic13. ( ) is the value at some future time of a present amount of money, or a series of payments, evaluated at a given interest rate.A. future valueB. present valueC. intrinsic valueD. market value14. Ellesmere Corporation issues 1 million $1 par value bonds. The stated interest rate is 8% per year and the interest is paid twice a year. What is the real interest rate of the bond? ( )A. 6%B.4%C. 10%D. (1+8%/2)2-115. Your firm purchased a warehouse for $335,000 six years ago. Four years ago, repairs were made to the building which cost $60,000. The annual taxes on the property are $20,000. The warehouse has a current book value of $268,000 and a market value of $295,000. The warehouse is totally paid for and solely owned by your firm. If the company decides to assign this warehouse to a new project, what value, if any, should be included in the initial cash flow of the project for this building? ()A. $268,000B. $295,000C. $395,000D. $515,00016.Which one of the following will decrease the operating cycle?A. paying accounts payable fasterB. discontinuing the discount given for early payment of an accounts receivableC. decreasing the inventory turnover rateD. collecting accounts receivable faster17. Assume that dividends of a common stock will be maintained at D forever, and the required return of the stockholder is r, the par value of the stock is m, the value of the stock is ( )A. mB. m+DC. m+D/rD. D/r18. Which of the following items has the most risk? ( )A. treasury billB. corporate bondC. preferred stockD. common stock19. ( ) equals the gross profit divided by net sales of a firm.A. gross profit marginB. net profit marginC. return on investmentD. return on equity20. ( ) is the ratios that measure a firm’s ability to meet short-term obligationsA. liquidity ratiosB. leverage ratiosC. coverage ratiosD. activity ratios21.Sensitivity analysis helps you determine the:A. range of possible outcomes given possible ranges for every variable.B. degree to which the net present value reacts to changes in a single variable.C. net present value given the best and the worst possible situations.D. degree to which a project is reliant upon the fixed costs.22. According GAAP revenue is recognized as income when: ()A. a contract is signed to perform a service or deliver a good.B. the transaction is complete and the goods or services delivered.C. payment is received.D. income taxes are paid.E. all of the above.23. ( ) is the result of Net Profit Margin × total asset turnover × (total assets/shareholders’ equity)A. Return on equityB. return on investmentC. current ratioD. quick ratio24. Government tax law adjustment is ( ) to a firm.A. general economic riskB. inflation and deflation riskC. firm-specific risk25.Which of the following statements concerning the income statement is not true?A. It measures performance over a specific period of time.B. It determines after-tax income of the firm.C. It includes deferred taxes.D. It does not include depreciation.E. it treats interest as an expense.26.Which of the following is not a noncash deduction?A. Depreciation.B. Deferred taxes.C. Interest.D. Two of the aboveE. All of the above.27.Sasha Corp had an ROA of 10%. Sasha’s profit margin was 6% on sales of $180. What are total assets? ()A.$300B.$108C.$48. D$162.28. Calculate net income based on the following information ( )Sales = $200.00Cost of goods sold = $100.00Depreciation = $18.00Interest paid = $25.00Tax rate = 34%A. $16.50B. $37.62C. $34.60D. $4.6029.Which of the following is not true? ()A. Financial markets can be used to adjust consumption patterns over time.B. Corporate investment decisions have nothing to do with financial markets,C. Financial markets deal with cash flows over time.D. Investment decisions rely on the economic principles of financial markets.E. None of the above.30. ( ) is concerned with the acquisition, financing, and management of assets with some overall goal in mind.A. Financial managementB. Profit maximizationC. Agency theoryD. Social responsibility31. A major disadvantage of the corporate form of organization is the ( ).A. double taxation of dividendsB. inability of the firm to raise large sums of additional capitalC. limited liability of shareholdersD. limited life of the corporate form.32. Interest paid (earned) on both the original principal borrowed (lent) and previous interest earned is often referred to as ( ).A. present valueB. simple interestC. future valueD. compound interest33. If the intrinsic value of a share of common stock is less than its market value, which of the following is the most reasonable conclusion? ( )A. The stock has a low level of risk.B. The stock offers a high dividend payout ratio.C. The market is undervaluing the stock.D. The market is overvaluing the stock.34. A 250 face value share of preferred stock, pays a 20 annual dividend and investors require a 7% return on this investment. If the security is currently selling for 276, what is the difference (overvaluation) between its intrinsic and market value (rounded to the nearest whole dollar)?A. approximately 26B. approximately 10C. approximately 6D. approximately 135. Felton Farm Supplies, Inc., has an 8 percent return on total assets of 480,000 and a net profit margin of 6percent. What are its sales? ( )A. 3,750,000B.640,000C. 480,000D. 1,500,00036. A company can improve (lower) its debt-to-total asset ratio by doing which of the following?A. Borrow more.B. Shift short-term to long-term debt.C. Shift long-term to short-term debt.D. issue common stock.37. The DuPont Approach breaks down the earning power on shareholders' book value (ROE) as follows: ROE = ( ).A. Net profit margin × Total asset turnover × Equity multiplierB. Total asset turnover × Gross profit margin × Debt ratioC. Total asset turnover × Net profit marginD. Total asset turnover × Gross profit margin × Equity multiplier38. Which of the following items concerns financing decision? ( )A. sales forecastingB. bond issuingC. receivables collectionD. investment project selection39. Which of the following items is the function of a treasurer? ( )A. cost accountingB. internal controlC. capital budgetingD. general ledger40. For financial instruments, ( ) is judged in relation to the ability to sell a significant volume of securities ina short period of time without significant price concession.A. maturityB. marketabilityC. defaultD. inflation41. ( ) is the value at some future time of a present amount of money, or a series of payments, evaluated at a given interest rate.A. future valueB. present valueC. intrinsic valueD. market valuePart III: Calculation Questions ( 2*10 points)(注意:要写出计算公式和计算过程,否则不得分;需要用文字描述的问题回答内容要详细,语句正确、完整。

given to absolute profit index -回复

given to absolute profit index -回复"Given to Absolute Profit Index"Introduction:In the world of finance and investment, there are various ways to measure the performance and profitability of a company or investment strategy. One such measure is the Absolute Profit Index, which provides an indication of the absolute profitability of a business or investment, regardless of external factors. In this article, we will explore the concept of the Absolute Profit Index, its calculation, significance, and limitations.1. Understanding the Absolute Profit Index:The Absolute Profit Index is a financial metric that focuses on the absolute profitability of a company or investment in isolation, rather than relative to external factors such as industry benchmarks or market conditions. It provides insights into the true profitability of a business, devoid of external influences, and serves as a useful tool to assess the financial health and viability of an investment.2. Calculation of the Absolute Profit Index:To calculate the Absolute Profit Index, one needs to consider the total profit generated by the company or investment over a specific period, usually a financial year. This total profit figure is then compared to a predetermined benchmark or target profit, which is often set based on historical performance or industry standards. The result is a ratio or percentage that represents the absolute profitability of the investment.3. Significance of the Absolute Profit Index:The Absolute Profit Index offers several advantages in evaluating the profitability of a business or investment. By focusing solely on the absolute profit, it eliminates the influence of market conditions and industry comparisons, providing a clearer picture of the investment's intrinsic profitability. It enables investors and analysts to assess whether the company is generating profits on its own merits or relying on favorable external factors.4. Limitations of the Absolute Profit Index:While the Absolute Profit Index provides valuable insights into the standalone profitability of a company, it is important to acknowledge its limitations. As it disregards external factors, it may not reflect the true operational efficiency or competitiveadvantage of a business. Moreover, it may not account for potential risks and uncertainties that could impact future profitability. Therefore, the Absolute Profit Index should be considered alongside other financial metrics and qualitative factors for a comprehensive evaluation.5. Interpretation and Comparison:Interpretation of the Absolute Profit Index depends on the individual context and industry. A higher Absolute Profit Index suggests a more profitable investment, indicating that the company is consistently generating profits above the benchmark. Conversely, a lower index may indicate below-average profitability or challenges in achieving the set target. However, to make meaningful comparisons, industry benchmarks and historical data should be considered.6. Practical Applications:The Absolute Profit Index can be a useful tool for investors, financial analysts, and company management. Investors can utilize it to assess the profitability of potential investments, helping them make informed decisions. Financial analysts can include the Absolute Profit Index in their reports to provide a standaloneprofitability perspective to stakeholders. Company management can track the index over time to evaluate whether their strategies are enhancing absolute profitability.Conclusion:The Absolute Profit Index provides valuable insights into the absolute profitability of a business or investment. By focusing solely on the company's intrinsic profitability, it allows for a clearer evaluation of its financial health and viability. However, it is essential to recognize the limitations of this metric and consider it in conjunction with other financial indicators and qualitative factors for a comprehensive analysis. The Absolute Profit Index serves as a valuable tool in the world of finance, aiding investors, analysts, and management in making sound financial decisions.。

金融市场学双语-郭宁-思考题整理-ZUCC