安永-2007全球内审概述

雷曼事件中安永审计责任的分析与启示ppt课件

(二)会计师事务所的质量控制应当加强 从此次安永审计过失来看,如

果内部的项目质量复核以及同业复 核制度能有效运行,那么审计过程 中疏忽的问题很容易被发现,从而 避免审计失败的发生。

精品课件

结语

目前,美国法院对雷曼破产诉讼案的判 决正在进行中,安永并不是主要的责任方, 不太可能承担严重的法律责任,但是该案件 对所有的审计人员再次敲响了警钟,严格遵 照审计准则和职业道德规范有利于提高审计 人员的职业水平和审计质量。此外,会计审 计准则制定机构应当及时更新和完善,确保 企业会计核算有法可依,减少舞弊可能;监 管部门也要加大会计师事务所的建设力度, 确保审计市场的健康发展,保证审计工作的 价值和作用的发挥。

➢ 雷曼前高级副总裁马修·李曾对总额高达500亿美元 的回购“105”操作产生怀疑,并在2008年5月向安永 合伙人进行了报告,但是安永在随后与雷曼审计委员 会和内部审计人的多次会议中,也从未提及这一问题。

➢ 虽然安永接到举报是在2007年度财务报表的审计工作 完成以后,但作为审计人员,尤其是安永与雷曼存在 连续年度审计业务关系的情形下,不仅要考虑当年审 计的资产负债表的公允性,同时也应当评估其可能对 于2007年度报表的影响,考虑已经发表的审计意见是 否恰当,是否要进一步调查并出具补充说明。尤其是 当举报人是审计客户的关键人员和高层管理者,且该 人员在举报后即被雷曼辞退,安永更加应当将此事项 列为重点关注的对象。-

精品课件

三、安永应承担的审计责任

管理层的责任是保证公司的经 营效率效果、战略目标的实现并且按照 准则编制财务报告。而作为注册会计师, 安永会计师事务所的责任是严格遵守美 国审计准则的要求对财务报告发表审计 意见。

精品课件

(一)过失责任

安永会计师事务所全球审计指引

Appendix A: Primary Substantive Procedures (PSP) by Account [S11_Exhibit 1]As we are designing our audit procedures, consider the fact that we perform Primary Substantive Procedures (‘PSP’) on all audit engagements for all significant accoun ts, regardless of the combined risk assessments.The PSPs are applicable to all industries and financial reporting frameworks and are based on a standardized set of significant accounts, which includes a standard naming convention and the global working paper index (for example, C: Cash, including bank balances). Each PSP includes a title that describes the objective of the procedure. In addition, the most relevant assertions have been indicated for each of the respective procedures.PSPs describe the nature of the procedures to be performed. As part of the development of our audit procedures, we also include the timing and extent of the PSPs. However, the timing and extent of the primary procedures performed will be affected by our combined risk assessments. Some of the primary procedures may be performed as tests of controls as well as substantive procedures (known as dual-purpose tests).PSPs on their own will not necessarily provide all of the audit evidence we need on a particular assertion for a significant account. Therefore, our audit procedures also include other substantive procedures we believe are necessary to appropriately respond to our combined risk assessment. In addition, when developing our audit procedures we consider the applicability of any Illustrative Sector Specific Substantive Procedures that are available.* Balance Sheet and Profit Loss LegendBalance Sheet (B/S)E = ExistenceV = ValuationC = CompletenessR&O = Rights & ObligationsP&D = Presentation and DisclosureProfit Loss (P/L)O = OccurrenceM = MeasurementC = CompletenessP&D = Presentation and DisclosureRelated Topic:Illustrative Sector Substantive Procedures Directory System ID: 10114661Last Modified Date: 30 JUL 2007。

审计安永-第三组

安永公司的专业服务广告宣传

近年来, E&Y年销售额都保持了高速增长速度。这 与E&Y对专业服务广告宣传进行大刀阔斧的改革是分 不开的。

E&Y针对不同类型、不同规模的企业推出不同范围的 专业服务广告。通过广告宣传, E&Y获得了许多小 型公司和企业的信赖。尤其是规模较小的公司只需 付一定的会员费就能通过电子邮件向安永公司的咨 询顾问提出各自的问题。公司则依靠自己的专业知 识迅速提供给顾客可行的解决方案。

同时,Ernst & Yong Consulting还通过Ernie进行 一项 “Trend Watch”的调查,调查的对象是那些 人们最关心的问题。E&Y在咨询业的另一项创新是 Ernst & Young Enterpreneuria Consulting Group。在服务那些年利润高达1亿美元的大客户的 同时,Enterpreneuial Consulting Group着眼于 为小型客户提供服务。

安永的历程与启示

主 讲:王汉青 执 笔:刘彦龙 课件制作:申国瑞 搜集材料:卫培玺 马 讨论分析:吴 昭 王

腾王 斌王

博 王巧梅 斐王 馨

安永会计师事务所 (Ernst & Young, 台湾称为致远)是世界四大会计师事务所 之一。

安永会计师事务所主要提供审计、税 务及财务交易咨询等服务,至今已有一百 多年的历史。

安永的历程

1894年成立于美国纽约 ArthБайду номын сангаасr Young会计公司

1903年成立于美国 克利夫兰的Ernst & Ernst

1979年后合并为Ernst & Whinney

+

= 世界原八大会计师事务所之中的ArthurYoung 1989年兼并形成现在的Ernst& Young

国际注册内审师内部审计实务

国际注册内审师内部审计实务随着全球经济的日益发展,企业管理也变得更加复杂。

在这种情况下,内部审计(Internal Audit)作为一种在组织内部进行的独立、客观、系统性评估和咨询活动,成为了企业治理不可或缺的一部分。

国际注册内审师(Certified Internal Auditor,CIA)则是内部审计领域的专业人士,经过专业认证后,具备全面的内控知识和技能,能够有效地执行内部审计和提供咨询服务。

国际注册内审师内部审计实务则是CIA备考过程中一门非常重要的科目,下面我们就来了解一下。

一、内部审计的定义与作用内部审计是一种对组织内部各个职能部门进行独立、客观、系统性评估和咨询的活动,旨在提供价值和改进组织的运营和风险管理。

内部审计的作用包括:确保组织达成目标、促进风险管理、提高治理水平、支持决策制定、为内部控制提供保障、增强组织声誉等。

内部审计不仅仅是检查错误和制定建议,更重要的是与管理层进行沟通,以促进改进和持续的改进。

二、国际注册内审师的介绍国际注册内审师是全球公认的内部审计专业人士。

该职业从业者通常在企业组织任职,为管理层提供独立的咨询和建议,并评估企业的运营效率和内部控制。

它是一项对有希望提升其内部审计职业生涯的人员的要求。

持有CIA认证的人员必须满足各种教育、工作经验、注册和道德方面的要求,并参加通过考试才能得到此认证。

三、国际注册内审师内部审计实务国际注册内审师内部审计实务(Internal Audit Practice)是CIA考试的一门科目,它覆盖了国际内审实践和程序的广泛知识,重点关注内部审计的计划、執行和报告。

这门科目包括股东治理和监督、审核问题和风险评估、内部控制、内部审核流程、内部审计参考框架和托管等。

此外,该科目还关注了基于数据的分析方法及其应用、财务调查技术以及内部审核沟通。

四、国际注册内审师内部审计实务的重要性国际注册内审师内部审计实务是CIA考试的其中一门科目,具有重要的学习和应用价值。

安永-内部审计功能-概览培训

1

20

审计流程

制定年度内审计划 年度内审计 划 审计委员会 提出改善建议并上 报所发现的问题 审计报告 主席 / 首席执行官/ 审计委员会/ 被审计单位 报告阶段

1

计划阶段

设定审计项目大纲

工作范围

被审计单位

跟进审计工作

跟进审计报告

主席 / 首席执行官/ 审计委员会/ 被审计单位

3

设定审计项目详细 计划

3

内部审计运作概要

• • • • • • • 内部审计章程 内部审计结构 内部审计的工能描述 内审人员所需具备的技能 审计流程 制定审计计划 内审方法

– 测试种类 – 抽样方法 – 控制测试 – 记录文件

• 审计报告 • 内部审计项目种类 • 质量控制

4

内部审计章程

• 内部审计章程在任何内审部门都是最为重要的一个文件。 它需要经过董事会和审计委员会的批准。 • 章程能引起对内审功能及其在企业中所扮演角色的关注。 • 它是支持内审部门执行其工作职能的正式的权威性文件 (内部审计章程由董事会审批)。 • 通常而言,内部审计章程包括但不只限于以下内容:

6. 记录测试 结果。

35

内审方法 • 样本数量 – 例

抽查25 个样本

没有发现问题

结束,无异常

发现个别问题

额外抽查 25个样本

没有发现问题

发现问题

发现系统性问题

结束,发现问题

36

内审方法

• 样本数量 – 例

控制性质以及频率

人工控制,每日数次 人工控制,每日 人工控制,经常但非每日 人工控制,每周 人工控制,每月 人工控制,每季度 人工控制,每年

24

制定审计计划

• 审计项目计划范例

释放内部审计的战略价值--实现转型的三个步骤

、

内部 审计 的角色 演变

安永委托 福布斯观 察 ( obs nih ) 内部审计 不 Fre Is t 就 gs 断变化 的角色开展 了一 次全 球性调查 , 成功访 问57 , 4 人 其 中包括首 席执 行官 (0 ) 首席 财 务官 ( 7 4% 、 2 %)、 审计 委 员 会 主席 (7 ) 审计 委 员会 成员 (6 ) ; 1% 及 1% ② 他们 分 别 来 自于1个行 业 、11 9 0 家公 司。 些公 司的总部分别 设在 欧 这

洲 、中东及非 洲 ( 0 )、美洲 ( 9 和 亚太区 ( 2 ), 4% 3 %) 2%

在具备适 当能力 的时候 ,内部 审计部门可就业务流程与

控 制 在设 计 及运 营 有 效性 方 面 ,通 过识 别 不 足之 处 与 改 进机 会 ,直接协 助公 司实 现其业 务 目 。 标 内部 审计 部 门配合 公 司 的业 务 目标 的商业 价 值议 题

M o e Ac o n i g d m c u tn

审 计 广 角

释放内部审计的战略偷值

实现 转型 的三个 步骤

陈文贤 朱驿冰 王 莹

( 安永 [ 中国 ] 企业咨询有限公 司风险管理团队,上海 2 02 ) 0 10

本 文 从 首 席 执 行 官 、 首 席 财 务 官 、首 席 审计 官 和

动有关 的风险、操作风 险及构成公司重大风险的任何其

他 因 素 ;( )与 其他 风 险 职能 部 门相 协调 ,在 整 个 公 司 3 范 围 内为 风 险 和治 理 活 动提 供 高 效 的鉴 证 服务 ;( ) 4 在

的人认为需要在未来 1 2~ 2 个月内作出改进 ;只有 5 4 %

我们认 为 ,除 了检查 流程和控 制 ,内部审计 部 门还在 公 司 中扮 演重 要 的咨询角 色 。为实 现转型 ,内部审计 部 门 需要 : ( ) 1 确保 自身 的工作 配 合公 司 的关 键业 务 目标 ; ( 提高 审计 效 率 和效 果 ,简化 流程 ,促 进成 本 节约 ; 2) ( ) 盖 更广 范 围 的风 险 ,主 动 了解 当前 及 新 出现 的风 3 覆 险 ; ( 在 所有 业务 单位 实现 成本 效率 最大化 ; ( ) 4) 5 寻 找并 使 用适 当的 内外 部 人才 资源 ; ( ) 6 通过 持续 的业 务 改进 , 得竞 争优势 。内部审 计部 门将会 获得更 多机会 , 赢 快速实现 其竞争价 值 。 三、实现 内部 审计转 型 、提 升 其职能 的三个 步骤 ( ) 内部审计 与商 业价值 议题 挂钩 一 将 业 务 总 在不 断 演变 ,内部 审 计 部 门应 随着 公 司业 务 的改 变 而 不 断变 革 。 内部 审计 部 门 在公 司 内转 变 角 色 的 方 法 之 一 ,是 确 保 其 活 动 配 合 公 司 的 业 务 战 略 及 目标 。

安永_内部审计实务标准及演进

国际内部审计实务标准之“内部审计‖ 定义

第 12 页

《国际内部审计专业实务框架》培训资料

目 录

一、内部审计实务标准及演进 二、《内部审计实务标准》概览 三、 属性标准解析 四、 工作标准解析

第 13 页

《国际内部审计专业实务框架》培训资料

二、《内部审计实务标准》概览

1、内部审计的定义

►

内部审计是一种独立、客观的确认和咨询活动,旨在增加价值和改善组 织的运营。它通过应用系统的、规范的方法,评价并改善风险管理、控 制和治理过程的效果,帮助组织实现其目标 。(RB Page 1) Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization's operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes.

April 22, 2005

第8页

《国际内部审计专业实务框架》培训资料

一、内部审计实务标准及演进(续)

4、中国内部审计协会-内部审计基本准则

第9页

《国际内部审计专业实务框架》培训资料

一、内部审计实务标准及演进(续)

4、中国内部审计协会-中国内部审计实务指南(截至目前共2号)

cia 内部审计实务 内容点

cia 内部审计实务内容点摘要:一、前言二、CIA 内部审计的定义和作用三、CIA 内部审计的实务内容1.审计计划和程序2.审计证据的收集和分析3.审计报告的撰写和提交4.审计结果的跟踪和整改四、CIA 内部审计的挑战与应对策略五、总结正文:【前言】CIA,即国际注册内部审计师,是全球范围内公认的内部审计专业认证。

本文将重点介绍CIA 内部审计的实务内容,帮助大家更好地理解和运用内部审计知识。

【CIA 内部审计的定义和作用】CIA 内部审计是指企业内部对各项业务和管理活动进行独立、客观的评估和监督,以提高组织的运营效率、防范风险、促进管理创新的一种管理手段。

其作用主要体现在以下几个方面:1.保障组织内部控制制度的健全性和有效性;2.提高组织运营效率,降低成本;3.发现和预防潜在的风险,保障组织的安全和稳定;4.促进组织管理创新,提升竞争力。

【CIA 内部审计的实务内容】1.审计计划和程序审计计划是内部审计工作的起点,需要结合组织的发展战略、风险状况和管理需求,制定出一套科学合理的审计计划。

审计程序则是在审计计划的基础上,具体实施的步骤和方法,包括审计通知、现场审计、审计报告等环节。

2.审计证据的收集和分析审计证据是审计过程中最重要的成果之一,直接影响到审计报告的质量和可信度。

内部审计师需要运用各种审计方法,如检查、观察、询问、重新计算等,收集充分、可靠、有效的审计证据。

3.审计报告的撰写和提交审计报告是内部审计师对审计项目的总结和评价,需要明确指出审计目标、范围、发现和建议,以及相应的证据支持。

审计报告需提交给组织的高层管理人员和相关部门,以便他们采取相应的改进措施。

4.审计结果的跟踪和整改审计结果的跟踪和整改是内部审计工作的最后一环,也是确保审计成果得以实现的关键。

内部审计师需要对审计报告的整改情况进行持续跟踪,确保组织对审计发现和建议进行了有效整改。

【CIA 内部审计的挑战与应对策略】1.内部审计师的专业能力不足应对策略:加强内部审计师的专业培训,提高其审计技能和业务水平。

安永-寿险公司审计方法总结及一些问题的再思考

一年一度的审计工作即将接近尾声,此时此刻,我认为自己有必要再对这三年来 积累的算得上是经验的东西做一个总结。一方面使自己脑海中的记忆留在纸面上, 不至于明年忘记。另一方面,也是更为重要的,是为后来人迅速成为比较专业的 人寿保险审计师尽自己的微薄之力。既然自己已经走过不少弯路,那麽后来的人 完全可以在一条比较平坦的道路上走下去。让我们所有的客户都看到,我们安永 保险审计绝对是专业的,不容置疑的,让他们哪些鄙视的话语不会再出现。

感谢阅读,相信希望获得知识者均会从中获得其相应的知识。

张驰 2010-7-23

4

2007 年我曾经写了此文的第一版,之后总想每年更新一版,但每年忙季过后, 又总是以各种理由说服自己不更新。这次,是不得不做了,因为将不再有机会。 下面附上 3 年前此文的第一版前言。此版在第一版的基础上进行了大量的扩充和 延伸,也从侧面反映了自己 3 年来的成长。

在开始年度审计之前,需要上网填写一个叫GATC的东西,实际上就是在公司 系统中注册一下,可能便于公司领导层掌握吧。

1、了解客户业务(Under stand the Business),设定重要性水平(PM—Planning maturity),可容忍误差(TE—Tolerable Error),调整起点(SAD—Summary Audit difference),确定重大账户(Significant Account),预算的制作(Budget);

手册中汇尽量写明查阅相关信息的路径,方便后来人的使用。

孔子曰:“不患无位,患所以立;不患人之不己知,求为可知者”。

安永2007财年收入增15%达211亿美元

马威 ( P K MG) 日宣布 , 至 20 年 9 3 近 截 07 月 0日的会 计年 度 ,

制 的基 础 上 提高 风 险管理 的效 力 , 而 帮助 内 审部 门更好 继 地与公 司 日渐成熟 的风 险管理 能 力形 成 呼应 。 整个 亚太 地 区 的法 规 日 严格 , 求企 业改 进管 理体 益 要 系并增 加 财务 报告 的透 明度 。

地货 币计 算 , 增长 1 .% 。 则 27

法 国 审 计 法 院 庆 祝 成 立 2 0周 年 0

法 国审计法 院近 日举行 活 动庆 祝成 立 20 年 ,萨科 0周 齐 总统 到场 祝 贺并 承诺 将增 加 审计 法 院权力 , 加强 对公 共

财务 的监督 。

20 毕 马 威 所 有 三 个 核 心 部 门 的 营 收 均 非 常 强 07年

公 款 和舞 弊现 象损 害人 民对 政府 和公 务 员 的信 任 。 他承 诺 部位 于 美 国 的最 大 银行 审计 企 业 中 重新 夺得 第 一 的桂 冠 , 将 重点 打击 各种 舞 弊现 象 , 力推 行改 革 , 高预 算 资金 大 提 排 名标 准 为 审计 的银 行 资 产 份 额 以及 美 国会 计 事 务 所 审 的使用 效率 ,改善公 共 管 理 ,他 希望 审计 法 院在这 方 面发 计 客户人 数 。

( 自《 摘 财会信报》 京) 20 .1 1 .5 ( ,0 7 1 .9A )

该公 司成员机 构合并 营收增至 18 美元 , 中毕 马威所有 9亿 其 系列服务 均呈两位 增 长 , 上年 同期 则 为 19 美元 。 而 6亿 按美 元计 算 , 马威 合并 营 收增 长 了 1 .%, 按 当 毕 74 而

内部审计外包的经济学分析(1)

内部审计外包的经济学分析(1)内部审计俗称外包又称内部审计外部化(Outsourcing the Internal Audit Function),指企业将内部审计职能全部或部分地委托给会计师事务所或其他专业人员来实施。

内部审计外部化最先是由安达信、安永、毕马威等全球知名的咨询机构提出的。

上世纪90年代开始,内部审计外包既存引起了越来越多的关注,已经有为数不少的企业或事业单位实行内部审计外包。

据国外调查资料说明,在美国和加拿大,内部审计外包的企业比例分别从1996年的21.5%和31.5%上升到2005年的38.0%和34.8%,这些企业遍布于各行各业;而在尚未实施内部审计外包的企业中,分别还有3成和4成以上的企业打算未来进行内部审计外包。

内审外包主要采用以下四种形式:1.补充式外包,即将部分的内部审计政府职能赋予第三方。

例如,在一些关键性至关重要的内部审计项目中聘请外界专业人士提供帮助。

又如,在审计外地的分公司时,聘请懂提供贷款当地语言或熟悉当地习俗的审计人员提供帮助。

另外,在审计特殊领域(如电子数据处理系统)时,企业财务管理也可聘请这方面的专家参与会计。

2.审计管理咨询,主要是指请咨询机构帮助企业确定企业内部审计机构设置、人员数量及备有情况,并有可能促进构筑内部审计计划的形成和改进。

审计管理咨询服务还包括对内部审计招工人员的招聘工作,帮助管理层定义主要的审计风险核心领域等等。

3.内审职能全部外包。

在这种外包为形式下,企业不设内部审计部门,但是为了进行合理的经营性审计,就将内部审计职能全部外包给会计师事务所或咨询机构。

4.内外成员结合审计,亦可称合作内审。

这种外包形式下,内部审计工作由一个统一的项目和审计工作工作组来完成,成员包括内部审计师和外部审计师,但内部审计师和外部审计师对这种结合审计分别承担不同的责任。

以上各种以上内审外包形式独具特色,因企业规模及行业不同,在是否实行内部审计外包及实现全面实施的方式上可能都有所不同。

certified internal auditor介绍 -回复

certified internal auditor介绍-回复什么是Certified Internal Auditor(CIA)?Certified Internal Auditor(CIA)是由全球最大的专业内部审计组织——国际内部审计师协会(IIA)提供的认证。

CIA认证是内部审计领域的国际认可的标准,旨在衡量内部审计人员在专业知识、技能和职业素养方面的能力。

CIA认证证明了内部审计师的专业才能,对其事业发展具有重要影响。

为什么要考取CIA认证?1. 全球通用:CIA认证在全球范围内广受认可,获得CIA认证的内部审计师可以展示其在专业知识和技能上的优势。

无论是在国内还是国际,CIA 认证将为内部审计师提供更多就业机会和职业发展空间。

2. 提升专业声誉:CIA认证证明内部审计师具备高水平的专业素养,得到同行和雇主的认可。

这有助于提高他们在组织内的声誉和影响力,为未来的晋升和晋级创造更好的机会。

3. 扩展知识和技能:CIA认证要求内部审计师掌握一系列的核心知识领域,如内部审计专业实践、风险与控制、内部控制和信息技术审计等。

通过学习和准备CIA认证考试,内部审计师将提升自己的知识水平,并掌握更多的技能,为日后的工作提供更全面和深入的支持。

4. 职业发展机会:CIA认证为内部审计师提供了广泛的职业发展机会。

获得CIA认证后,内部审计师可以选择在各个行业和组织中寻求相关职位,如内部审计主管、内部审计经理和内部审计总监等。

同时,他们还可以通过不断提升自己的知识和技能,进一步拓展职业发展的道路。

怎么考CIA认证?1. 审核资格要求:获得CIA认证的考生需要具备一定的学历和工作经验。

研究生学历需要持续2年的内部审计或相关领域工作经验;本科学历需要持续7年的内部审计或相关领域工作经验。

此外,需要提供两位证明人的推荐信。

2. 报考CIA认证:考生需要在IIA官方网站注册并申请CIA考试。

考试分为三个部分,分别涵盖了内部审计的核心知识和技能。

IA Mgt Training-8-3-2007

2007年3月8日内部审计功能-管理层培训电器集团有限公司0法规的变化趋势和影响内部审计模型管理层的责任及角色设立内审部门的常见挑战大型跨国企业的内审功能实务分享什么是内部审计部门?§内审部门是一个为企业提供自我监督和内部咨询的团队*§内审部门在企业中是独立且客观的§内审部门是为企业增值并完善内部运作而设立的部门*国际内部审计师协会(IIA)在其制定并修改的《内部审计实务标准》及《职责说明》中认定:“内部审计是一种独立、客观的保证和咨询活动。

其目的是在于为组织增加价值和提高组织的运作效率。

它通过系统化和规范化的方法,评价和改进风险管理、监督内部控制的有效性,帮助组织实现其目标。

”23保险精算师风险管理委监策略风险流程改善评估督资金部行销部人力资源部法律顾问营运部税务主管企业发展员会董事会审计委员会风险管理监督监督日常风险管理监管外部审计师内部审计内部审计在风险管理框架里的角色生产部4合规检查内控业务流程风险管理内审重点内部审计角色的转变内审部门的工作汇报5内审部-培养管理人才的地方§公司的内审人员一般都:-了解公司整体架构和业务-对内控及管理方面有一定的认识-从独立的角度了解公司的问题和情况6内审部-培养管理人才的地方§内审人员日后有能力担当企业中的重要岗位。

以下是一些例子:-Frank Brod–区域副总裁, Microsoft Corp-Craig Omtvedt–高级副总裁& 财务总监,Fortune Brands Inc. -Mike Fawkes –高级副总裁,惠普公司(HP)7从三个不同的利益相关者角度来考虑内部审计的价值:§监管机构和投资者§董事会和审计委员会§管理层81)监管机构和投资者的角度§企业管治和风险管理框架里不可缺少的要素§监管要求-降低违规风险, 保障投资者权益§投资者-企业内在的自我监督和完善内控机制910n 反问: 公司的流程和控制有效吗?–没有问题暴露=有问题发生?n 建立制度只是规范管理的第一步,往往问题发生在日常操作过程中–专责部门监督执行–加强推行力度n协助董事会及审计委员会执行监察的职责2)董事会和审计委员会的角度3)管理层的角度§业务和风险不断变化,现有的流程和控制是否还合适?§业务单位能客观的对自身的内控程序有效性进行评价吗?1112内部审计所面对的利益相关者和提供的服务策略风险流程以下是内部审计部门所负责的不同种类的审计项目•财务审计–对企业目前财务状况的评估,以确定企业资产负债表、利润表及现金流量表是否合理公允。

2007CIA考试大纲:第二部分:实施内部审计业务

2007CIA考试大纲:第二部分:实施内部审计业务Part II - Conducting the Internal Audit Engagement第二部分–实施内部审计业务A. Conduct Engagements (25 - 35 percent) (Proficiency Level)实施审计业务(25 –35%) (要求熟练掌握)1. Research and apply appropriate standards:研究和采用适当的标准:a. IIA Professional Practices Framework (e.g., Code of Ethics, Standards, Practice Advisories)IIA 职业实务框架(如,《道德规范》、《标准》、《实务公告》);b. Other professional., legal, and regulatory standards其他职业的、法律的和法规的标准;2. Maintain awareness of potential for fraud when conducting an engagement在实施审计业务时,要保持防范潜在舞弊的意识:a. Notice indicators or symptoms of fraud注意舞弊的迹象和征兆;b. Design appropriate engagement steps to address significant risk of fraud设计适当的审计业务步骤以应对重大的舞弊风险;c. Employ audit tests to detect fraud采用审计测试以发现舞弊;d. Determine if any suspected fraud merits investigation确定是否应对任何可疑的舞弊进行调查3. Collect data.收集数据。

国外内部审计的发展轨迹

国外内部审计的发展轨迹内部审计并非诞生于20世纪初,它是企业发展规模逐渐扩大,为适应管理需求多样化、复杂化的产物。

随着世界经济繁荣和萧条的几番更替,无论在发达国家还是在发展中国家,也不论企业的规模大小、产业和类型,为何内部审计都受到广泛的重视?内部审计在国外的发展历程如何?未来将呈现怎样的发展趋势?文章将作出详细解答。

在2001年11月的美国安然公司财务舞弊事件中,唯一获判无罪的高层管理人员就是安然的首席内审员。

2002年5月,世界通讯公司再度爆发财务丑闻,其虚构的近100亿美元利润创下了财务舞弊的世界记录。

与安然事件类似,世通的财务舞弊也是由三位内审人员在执行内审工作过程中发现的。

他们不计个人安危、忠于职守、排除种种困扰、承受巨大的压力,毅然将世通的舞弊行为昭示于天下。

在上述各案中,尽管内审人员都恪尽职守,但为何仍阻挡不了此类弊案的发生?是企业的外部环境发生了变化?是企业对绩效的追逐已超过对高层主管道德价值和企业良心的关注?还是影响企业有效运作的基础框架已年久失修、不堪重负呢?这对处于内审领先地位,向来对企业执行严格监管的美国及其相关监管单位,不啻于巨大的耻辱和一个当头棒喝;而全球企业也都开始重新思考内审在企业中所扮演的角色、应起到的作用,并且审视包含公司层面在内的内部控制制度是否完善,应如何完善。

《萨班斯-奥克斯法案》也在此背景下应运而生。

在此期间,内审和审计委员会,似乎被企业和多数企业利益相关团体视为维护企业道德文化的最后一道防线。

国外内审产生的背景19世纪末、20世纪初,托拉斯和康采恩等组织快速发展和扩张,逐渐在主要资本主义国家中占据了垄断地位。

例如,1901年,美国钢铁公司垄断了全国钢产量的65%。

这些经营规模庞大的企业,经营地点分散,经营业务复杂,高层管理人员无法像以前那样在所有的经营活动上亲历亲为,由此,分权管理和多级控制逐渐成为大型企业的管理方式之一。

然而这种营运模式要想运作有效,势必需要建立适当的制度和程序以规范员工在日常营运作业中的合规合理性。

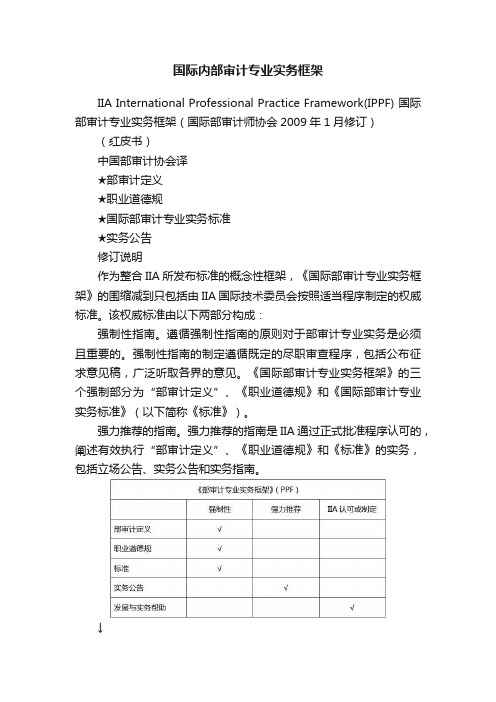

国际内部审计专业实务框架

国际内部审计专业实务框架IIA International Professional Practice Framework(IPPF) 国际部审计专业实务框架(国际部审计师协会2009年1月修订)(红皮书)中国部审计协会译★部审计定义★职业道德规★国际部审计专业实务标准★实务公告修订说明作为整合IIA所发布标准的概念性框架,《国际部审计专业实务框架》的围缩减到只包括由IIA国际技术委员会按照适当程序制定的权威标准。

该权威标准由以下两部分构成:强制性指南。

遵循强制性指南的原则对于部审计专业实务是必须且重要的。

强制性指南的制定遵循既定的尽职审查程序,包括公布征求意见稿,广泛听取各界的意见。

《国际部审计专业实务框架》的三个强制部分为“部审计定义”、《职业道德规》和《国际部审计专业实务标准》(以下简称《标准》)。

强力推荐的指南。

强力推荐的指南是IIA通过正式批准程序认可的,阐述有效执行“部审计定义”、《职业道德规》和《标准》的实务,包括立场公告、实务公告和实务指南。

↓新版IPPF所作的重大改变是:(1)程序改进。

加强了IPPF的各个部分,提高了透明度并确定了权威标准和修订周期。

标准的修订周期目前确定为三年,尽管并非每三年都需要进行修改,IIA 仍致力于确保对标准作全面的审核,并视需要进行修订。

(2)发展与实务帮助。

这一部分不再纳入柜架体系。

它曾经包含了部审计师在工作过程中可能会用到的所有资源(例如培训、出版物和研究报告等)。

由于新版IPPF 的围只包括上述的权威标准,这项容不再适合于新的框架。

(3)释义。

这是新增的对标准中的术语和短语作出的进一步阐释,置于需要加以解释的相关标准条款之下。

(4)实务公告。

这部分容在围上已经缩减为只包括用于实施“部审计定义”,《职业道德规》和《标准》的技术和方法。

原框架中涉及工具及技术方法的容已经移至实务指南部分。

(5)实务指南的立场公告。

这是IPPF新增的容,实务指南侧重于在工具和技术的具体运用方面提供指引,包括详细的流程、程序、方案和步骤(例如每一步所形成的结果的例)。

国际内部审计师

国际内部审计师国际内部审计师是一种专业角色,负责对企业的内部控制体系进行审计和评估,以确保企业运作的合法性、合规性和效率性。

国际内部审计师在全球范围内开展工作,为企业提供有关内部控制和风险管理方面的建议和指导。

本篇文章将从国际内部审计师的定义和职责、必备的知识和技能、以及成为一名优秀国际内部审计师的要素等方面进行探讨。

国际内部审计师的定义和职责国际内部审计师是一种专业角色,主要负责对企业的内部控制和风险管理等方面进行审计和评估。

他们通过收集和分析相关数据、进行调查和检查,评估企业的运营过程和控制措施是否合规、有效和适宜。

国际内部审计师的职责包括但不限于以下几个方面:1. 内部控制评估:国际内部审计师需要评估企业的内部控制体系,包括财务报告、风险管理、合规性和运营过程等方面。

他们会检查企业的流程和程序,了解是否存在潜在的风险和漏洞。

2. 风险管理:国际内部审计师需要帮助企业识别和评估风险,并提供相应的建议和解决方案。

他们会进行风险评估,制定应对策略,并监督和跟踪风险管理的执行情况。

3. 财务审计:国际内部审计师还需要对企业的财务报表进行审计,确保其准确性和可信度。

他们通过审查财务记录和交易,评估是否存在潜在的错误或违规行为,并提出相应的改进建议。

4. 内部审计报告:国际内部审计师会撰写内部审计报告,详细记录审计过程和发现的问题。

这些报告将向企业管理层和董事会提供重要的信息和建议,以促进内部控制的改进和发展。

必备的知识和技能要成为一名优秀的国际内部审计师,需要具备一定的知识和技能。

以下是一些必备的知识和技能:1. 会计和财务知识:国际内部审计师需要具备扎实的会计和财务知识,包括财务报表分析、成本管理、预算编制和财务控制等方面。

这些知识可以帮助他们理解企业的财务状况和运营情况,并识别潜在的风险和问题。

2. 内部控制和风险管理知识:国际内部审计师需要了解内部控制和风险管理的相关理论和实践。

他们需要掌握相关法规和规范,如《内部控制综合框架》和《风险管理指南》等。

影响内部审计职能有效发挥的因素

四、影响内部审计职能有效发挥的因素(一)与管理当局、外部审计师交流Gilmour(1998)认为,当高管层把内部审计看作是改善控制的资源,而且能够经常与审计师保持交流,并且在企业宣传内部控制是每个人的职责时,更有利于内部审计工作的开展.Raghunandan 等(2001)指出内部审计和高管层之间保持良好的关系,对于保证内部审计职能的有效性十分重要。

Twaijry 等(2003)在对沙特阿拉伯的内部审计部门经理进行问卷调查后发现,在存在内部审计的组织中,由于高管层和被审计单位不认可内部审计,使得内部审计部门得不到恰当的资源、缺乏合格人员,而且独立性较差。

可见,得到高管层的支持是保证内部审计部门实现自身价值的必备条件。

Campbell 等(2006)认为,在过去多数组织只关注内部审计对内部控制的有效性和公司财务健康状况进行独立评价的作用,但是萨班斯法案的颁布给内部审计提供了为组织创造更大价值的契机。

要为企业提供额外的价值,内部审计必须改变其在组织内部进行监督的“冷面孔”形象,成为管理部门的一个重要合作者,提供内部审计建议,帮助管理部门成功执行战略和创造更多公司价值。

一方面,内部审计提供有用的审计发现和建议,增加高管层对内部审计的兴趣;另一方面,高管层在资源使用上的支持和对内部审计意见的执行,可以保证内部审计工作的顺利开展和审计结果的权威性。

Sarens (2007)于2005 年11 月至2006 年3 月对比利时金融保险业、制造业和服务业公司的内部审计主管发放调查问卷,研究内部审计规模和控制环境之间的联系。

实证结果显示,高管层越支持,内部审计规模越大,风险防范越好。

(二)独立性李明辉(2009)指出,内部审计的独立性是内部审计活动所处的环境中不存在可能对内部审计人员的独立判断产生重大影响的事项,内部审计人员因而能够基于其自身的知识、经验和技能自由地开展审计工作,依照相关的职业准则搜集充分、适当的审计证据,并依据自己的专业判断作出客观公正、不偏不倚的结论。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

yq Global Internal Audit SurveyA current state analysis with insights intofuture trends and leading practicesGlobal Internal Audit Survey 2007About Ernst & YoungErnst & Young, a global leader in professional services, is committed to restoring the public’s trust in professional services firms and in the quality of financial reporting. Its 114,000 peoplein 140 countries pursue the highest levels of integrity, quality, and professionalism in providing a range of sophisticated services centered on our core competencies of auditing, accounting, tax, and transactions. Further information about Ernst & Young| and its approach to a variety of business issues can be found at /perspectives. Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited does not provide services to clients.Global Internal Audit Survey 2007The Shifting Internal Audit Landscapey 2Governancey 4Peopley 6Infrastructure and Operationsy 10Conclusiony 16Contents1The Shifting Internal Audit LandscapeThe Internal Audit landscape,recently dominatedby financial reportingcompliance-related efforts,is now being challenged bypressures on resources andgrowing demands to helpimprove overall businessperformance.2To help gauge these shifts in the global Internal Auditindustry, and to gain insight into future and leading trends,Ernst and Young recently conducted a survey of InternalAudit executives worldwide.In short, the survey reveals that Internal Audit is in the middleof an evolutionary transition, facing great challenges, as wellas new opportunities. There is a call for Internal Audit to domore to meet the needs of its stakeholders.The key findings are:Stakeholder expectations are increasing with greateryfocus on enterprise-wide risk assessment and businessand operational risk.In implementing enterprise-wide risk assessments, asywell as covering of key risk areas, there is an opportunityfor Internal Audit to improve coordination with other riskmanagement groups within the company.People are still the foremost challenge for InternalyAudit functions around the globe: recruiting, retooling,developing, and retaining the right skills.Industry, IT, fraud, and business and operational risk areythe specialized skills most difficult to recruit and retain.These are also among the areas which respondentsindicated pose greater risks to their companies.There is an opportunity for Internal Audit to betteryleverage technology and knowledge collection/sharingtools to improve effectiveness and efficiency significantly.Internal Audit functions around the world have the opportunityto expand their impact on – and improve their companies’performance in – enterprise-wide risk, particularly in areassuch as fraud, major capital programs (including IT),contracts, transactions and international expansion. Thepotential for increasing Internal Audit’s strategic relevance isgreat. Our survey shows that Internal Audit’s expanded rolein these areas is not only an objective, but is also expected.What had once been only desired is now anecessity.Complicating matters are Internal Audit’s efforts to reconcilethe sometimes-divergent objectives of the Audit Committeeand executive management. While the Audit Committee isinterested in keeping the company out of trouble, executivemanagement is also interested in Internal Audit’s point ofview on improving business performance.These new pressures, coupled with InternalAudit’s uniquely well-positioned role, makeunderstanding what is happening – and how torespond – a critical success factor.Stakeholders, including the Board of Directors, the AuditCommittee, employees, regulators and stockholders arewatching to see how Internal Audit functions will respond.In order to meet these expectations, and to become morestrategically relevant, Internal Audit leaders need to continueto think differently and react quickly.Ernst & YoungSetting The Scene For The SurveyStakeholders have long expected that Internal Audit functions keep their companies “out of trouble”. Now, there is an expectation that Internal Audit will also help to “make the business better” through improved performance thereby helping to improve the company’s return on investment.It is because Internal Audit is well-positioned to understand so many different aspects of the company that it finds itself in the middle of tremendous change and opportunity. About The SurveyThis report highlights the findings of our survey of Internal Audit executives representing 138 predominately public companies representing membership in the Global Business Week 1000, and the Standard & Poor’s Global 1200 from24 countries. Most of the participants’ companies were large multinational functions with revenues over US$ 4 billion.To help structure the survey results, we used Ernst and Young’s Internal Audit Framework, which has been usedby a number of leading companies to analyze their Internal Audit function. The 2007 Global Internal Audit Survey results therefore examine Internal Audit functions across three basic categories:Governancey – Focuses on the role and mandate ofthe Internal Audit function and its relationship with keystakeholdersPeopley – Focuses on the structure and processes torecognize, hire, retain and develop the competency ofthe Internal Audit staffInfrastructure and Operationsy – Focuses on themethodologies, technologies and quality programsthat support Internal Audit activities, and facilitate theachievement of Internal Audit objectives and mandate,as well as the practices used to execute audits andprovide service3After several years ofcompliance-relatedinvestment and increasedinternational competition,stakeholders are lookingto Internal Audit – with itsunique perspective thatspans the highest levelsof the company down tothe granular aspects ofdaily operations – to helpmanagement producefavorable returns.GOVERNANCEPEOPLEINFRASTRUCTURE& OPERATIONSPurpose& MandateResourcingCompetencyDevelopmentSustainingPeople ExcellenceTools &TechnologyOperationsQualityKnowledgeManagementMethodologyThe Ernst & Young Internal Audit FrameworkGlobal Internal Audit Survey 2007Ernst & Young4Compliance and Financial Reporting Efforts are Still SubstantialAt this stage of the global push for increased compliance, especially for SEC registrants, many might expect that Internal Audit functions would now be moving toward amore limited role, focusing more on the testing of higher risk and/or more complex areas. But our survey indicates that the number of companies where Internal Audit maintains the primary burden of testing internal control over financial reporting is still relatively high.Although the demands for compliance testing are declining for most Internal Audit functions, our survey showed that over 36% of the SEC-listed companies required to comply with SOX 404 responded that their Internal Audit function still has full responsibility for testing all SOX 404 controls.Increased Focus on Business and Operational RiskIn light of the changing demands, many Internal Auditfunctions are looking to better-align audit coverage with the company’s major business and operational initiatives and risk areas. Focus areas include major programs, contract management, international expansion, transactions, and major change initiatives.Nearly three-quarters of respondents indicated involvement in business process improvement. Fifty eight percent indicated involvement in contract auditing, and 57%involvement in the auditing of major programs. Nevertheless, the respondents recognized significant opportunities for Internal Audit to increase its effectiveness in these areas. In order to do so, Internal Audit must retool existing resources and add new resources/skills to these areas.Enterprise Risk Assessment Gaining MomentumBetter integration among all risk management functions within the organization, including Internal Audit, is a major factor in improving the effectiveness of the enterprise risk assessment process. In larger companies with multiple risk management functions, risk assessment and coverage activities need to be clearly defined, coordinated, and aligned with the company’s strategic objectives.Our research shows that many Internal Audit functions are involved in (and, in many cases, leading) an enterprise risk assessment process so those functions can refocus their efforts on the risk areas that have a significant impact on the business. Seventy-seven percent of companies surveyed perform an enterprise risk assessment. Manyfurther indicated deploying the leading practice of refreshing this assessment at key intervals throughout the annualaudit cycle. Respondents indicated that there are significant improvement opportunities in the scope and level of coverage across specific risk categories, especially operational, compliance, and strategic risk.GovernanceOur survey results indicate that the number ofcompanies where Internal Audit maintains the primary burden for full regulatory compliance and internal control over financialreporting and testing is stillrelatively high.The majority of companies surveyed have multiple risk management functions, in addition to Internal Audit, within their organization. Fifty percent of the companies surveyed have formal enterprise risk management functions. The growing perception that executive management has a relatively higher level of accountability than in the past creates an opportunity for Internal Audit to contribute to the formalization and integration of risk management within the company.However, only 29% of respondents indicated that Internal Audit has strong interaction and alignment with other risk management functions in the company, with proactive sharing of risk and control information. This suggests a significant opportunity for improved alignment, through the Internal Audit framework. There is a challenge for Internal Audit, together with people at all levels of the company, to build risk management into business management.Global Internal Audit Survey 20075Ernst & Young6“War for Talent” Is the Top Issue Facing Internal Audit FunctionsThe “war for talent” continues to be the greatest challenge for many Internal Audit functions. Although it appears that Internal Audit is able to secure an adequate budget, itstruggles to attract and retain “the right type of talent”. This leads to gaps in Internal Audit coverage and challenges in completing the Internal Audit plan. The survey found that:Forty-nine percent of respondents’ indicated an increasey in the size of the Internal Audit function during thepreceding 12 months, while 11% decreased, with the remaining 40% unchanged.Thirty-eight percent of respondents indicated they arey operating at less than 90% of budgeted headcount. Over one in five Internal Audit functions has an annualy staff turnover in excess of 20%. Thirty-six percent ofrespondents reported an estimated annual staff turnover rate of more than 15%.PeopleThe increase in demand for qualified personnel, especially those withspecialized skills, is creating a challenge for Internal Audit functions looking to fulfill theincreasing expectations.Global Internal Audit Survey 20077One of the greatest challenges manyrespondents cite is having too many Internal Auditors with financial reportingcompliance skills, but lacking Internal Auditors with the specialized skills to meet the needs of the company’s evolving risk profiles.Acquisition of Specialty Skills Is Particularly ChallengingAs a result, leading Internal Audit functions are transforming their people model in a variety of ways including: retooling existing resources, hiring new skills into the function, implementing rotational programs, and developing relationships with third-party service providers.Respondents are facing a number of hurdles in the drive to find and train “the right people”. The top skills that are among the most difficult for Internal Audit to recruit are, in order, IT auditing, industry experience, and fraud prevention/detection.To help illustrate this difficulty, the survey reveals that IT auditors represent only 10% of the Internal Audit headcount for over half of respondents’ Internal Audit functions. In today’s environment, leading Internal Audit functions have 25% of their staff focused on IT activities.Further, more than a third of respondents indicated that they do not have staff trained in fraud prevention/detection. Other significant skill gaps in key risk areas include transactions,tax, major programs, and contract auditing.Ernst & Young8Competency Development May Need Greater FocusMany Internal Audit functions need to invest more heavily incompetency models and training plans, upgrade training curriculums and increase the required hours for staff training each year.However, this appears to be a major challenge for many functions.Nearly half of the respondents (47%) require up to 40 hours of annual training for Internal Audit staff. Forty-three percent of the respondents do not have formal competency models/training requirements by level or by individual.As the chart below shows at least 52% of the respondents’ staff did not meet their training requirement standards in the last year.PeopleThere is a significant retooling effort required to expand Internal Audit skill sets from financial reporting compliance to business/operational risk competencies, as well as meet the expandingexpectations of stakeholdersto benefit the business.Global Internal Audit Survey 20079International Coverage Is A Major ChallengeThere are numerous challenges to the provision of effective Internal Audit coverage for international operations. These include:Differences in language and culture;y Knowledge of local laws, regulations and accountingy standards;A reluctance among Internal Audit staff to travel;y Adherence to quality standards; and y Increased costs.y Our survey found that a higher-than-expected (41%) percentage of Internal Audit functions are attempting toprovide international coverage from corporate headquarters, which provides limited ability to address the challenges noted above. Not surprisingly, only 34% of respondents are “highly satisfied” with Internal Audit coverage of their international operations.Multiple Factors in Retaining the Best TalentCompetitive compensation is only one of the many factors that impacts efforts to develop and sustain high-performing organizations. Other factors – such as training, mentoring, career opportunities, and new and challenging assignments – are equally important and, collectively, may be more important than compensation.Leading practice would dictate that addressing the challenge of creating adequate competency models would facilitate training plans, performance management systems, and the attraction of top talent to the Internal Audit function.Ernst & Young10Risk Assessment Trends and OpportunitiesIn a dynamic business environment, organizations face potential new risks or increased exposure from existing risks. This has resulted in many Internal Audit functionsrefreshing their annual risk assessment at least once a year – sometimes quarterly – in an effort to understand a changing risk profile, and to help make sure they have the tools in place to address these risks.We asked respondents how often their companies updated the risk assessment and Internal Audit plan during the year:Eighty-nine percent of respondents conduct a risky assessment to support the Internal Audit planningprocessForty-four percent of respondents update their risky assessment semi-annually, quarterly, or prior toconducting Internal AuditsOnly 44% of respondents provide standardizedy training to individuals responsible for conducting a riskassessmentOnly 43% of respondents present risks not covered by the Internal Audit plan to the Audit Committee. Institutional investors rate transparency as a key factor in making the decision to initiate an initial investment in a company. Ernst & Young’s 2007 Risk Management in Emerging MarketsSurvey also found that there is clear room for improvement in the documentation and, therefore, communication of the risk assessment process across a company.Completing the Internal Audit PlanThe difficulty in completing the Internal Audit plan during the audit cycle has been a consistent trend over in recent years. For some companies, efforts to comply with financial reporting compliance regulations continue to divert asignificant portion of the Internal Audit plan and resources away from other Internal Audit efforts.Again, this effort is being complicated by the challenge many Internal Audit functions have in finding and retaining the right talent to address areas of the Internal Audit plan requiring specialized skills.Only 21% of respondents were able to complete the y prior yearInternal Audit planOnly 24% completed up to 80% of the plany Our Risk Management in Emerging Markets Survey found that those individuals closest to the risk are often in the best position to assess the steps necessary to reduce their companies exposure to the risks. Internal Audit’s scope of responsibility is increasing beyong the level and/or skills base of its resources. An internal auditor from company headquarters is often not well placed to test a subsidiary’s risk. Internal Audit needs to be done locally by people with the appropriate knowledge. Respondents to Ernst & Young’s Companies on Risk Survey commented that they expect that greater alignment of Internal Audit with line management will lead to more effective decision making and communication across the business.Infrastructure and OperationsAudit Committees and executive management increasingly expect that Internal Audit shares not only the risks covered in the Internal Audit plan, but also risks that are not covered bythe Internal Audit plan.Global Internal Audit Survey 2007Interest in Continuous Internal Auditing Is IncreasingContinuous auditing has a significant impact on Internal Audit efficiency, especially as it migrates from manual to automated operations. Several elements need to be in place to fully leverage a continuous auditing program: a detailed plan of specific program objectives and resources/budget, the requisite skill sets to plan and implement the program, and executive management support for the initiative.More than half of the survey’s respondents (56%) have not implemented a continuous auditing program. Reasons for not doing so include perceived lack of value, lack of relevant skills, and budgetary constraints.Of the respondents who have not implemented continuous auditing, approximately half plan on doing so in the future. The 44% of respondents who have implementedcontinuous auditing list key activities including follow-up on recommendations, identifying control deficiencies, monitoring risks, and identifying potential fraud.1156%44%Does internal audit utilize continuous auditing?NoYesErnst & YoungUse of Data AnalyticsMany Internal Audit functions have limited capabilities to leverage data analytics effectively. As a result, data analytics are often relegated to relatively simple financial analysis and graphics support.Leading Internal Audit functions use data analytics for numerous activities, including risk assessment, planning, execution, and reporting. Additionally, data analysistechniques, such as predictive modeling, regression analysis, and data mining have been successfully used by Internal Audit functions for fraud detection, testing of controls, and root cause analysis.Ninety-three percent of respondents indicated that their Internal Audit functions use data analytics. However, only 42% of the respondents indicated that more than 60% of their staff is proficient in the use of data analytics.Tools and Technology UsageAnother area of potential improvement for Internal Audit includes enhancing specialized tools to facilitate work streams, collaborative efforts, knowledge exchange, and increased work mobility.Successful implementation of more sophisticated - and integrated - Internal Audit tools requires proper planning, resources, and budget. As a result, these short-term investments are likely to benefit the company.Tools and technologies implemented by Internal Audit typically support work papers (87%), audit planning (73%), reporting (71%), report writing (59%), tracking findings through remediation (52%), and knowledge sharing (51%).Specialized tools to support Internal Audit activities. The majority of respondents use Microsoft® applications (53%), followed by in-house systems (27%). Investments in other, more sophisticated tools is still limited but increasing.12Infrastructure and OperationsSuccessful implementation of more sophisticated - and integrated - Internal Audit tools requires proper planning, resources, and budget.Fraud Prevention and InvestigationRegulators around the world are requiring organizationsto become more vigilant regarding fraud. As such, leading Internal Audit functions are proactively investing morein fraud prevention, such as fraud risk assessment,data analytics for the early detection of fraud, and fraud awareness training.Nearly 65% of respondents indicated that fraud is a“very significant” or “somewhat significant” risk to their organization.Proactive fraud prevention, such as increasing awareness, identifying areas of vulnerability, and aiding in early detection of fraud, are less common among respondents than reactive activities. For example, providing fraud awareness training, conducting fraud risk assessments and utilizing modelingto identify potential frauds were far less frequently notedby respondents than the execution of Internal Audits and investigations.Fraud investigations have become more complex, especially with regard to privacy regulations. Organizations need to use subject matter specialists to conduct fraud investigations, obtain and maintain attorney-client “privilege”, exercise proper control over the chain of evidence which serves to limit the organization’s exposure/liabilities in the event of litigation.13Global Internal Audit Survey 2007Infrastructure and OperationsKnowledge ManagementIdeally, knowledge databases supporting the Internal Audit function should not only include leading practices from within the company, but also should extend to other leading companies as well.When asked how they expect their Internal Audit function will expand the use of leading practices and benchmarking data to support audit activities, only 47% of respondents indicated that they maintain a library of leading practices. Thirty-six percent indicated that they maintain industry-based business process models.Sources of knowledge for Internal Audit functions are varied, with the three main sources being the Institute of Internal Auditors, professional service firms, and industry trade associations.Measuring Internal Audit EffectivenessThe top two metrics used in measuring Internal Audit effectiveness include:Completed Internal Audits in comparison to the Internal yAudit plan (89%)The length of time for issuing Internal Audit reportsy(72%)Only 32% of respondents use length of time to resolve Internal Audit findings as a key metric, while 23% use support of key business initiatives.Surprisingly, the survey revealed that half of the respondents do not track the value their Internal Audit functions provideto the organization, while 13% measure value based upon actual cost savings.To reinforce their relevance to key stakeholders, Internal Audit needs to align Internal Audit plans and performance metrics to support key business initiatives. Value trackingis a mechanism which can reinforce relevance as well as help justify the Internal Audit investment. As Internal Audit’s involvement in certain business/operational risk areas increases – such as program auditing and contract auditing – tracking value will become more applicable.Knowledge of specificindustries, leading practices,and benchmark informationis a key component of aneffective and efficientInternal Audit function.This knowledge should beincluded in the training anddevelopment of new andexisting staff.Ernst & Young14Measuring Internal Audit Quality Array Array In an effort to better understand how companies enhancetheir Internal Audit functions to achieve continuousimprovement of service quality, and adherence to InternalAuditing standards, we asked what steps respondents aretaking to measure it:yEighty percent of respondents use the closing meeting,while 48% of respondents use a post-Internal AuditsurveyyFifty-two percent of respondents maintain moderateto strict compliance with Institute of Internal AuditorstandardsyForty-eight percent of respondents have had an externalquality assessment reviewLeading organizations combine a quality assessment reviewwith a functional performance assessment to conduct acurrent state/desired state Internal Audit gap analysis and tocreate an improvement plan for the function.Global Internal Audit Survey 200715Ernst & Young16While the survey provides strong insight into the efforts by Internal Audit functions around the world to strike a balance, it also raises questions for the future:Can Internal Audit functions successfully reconcile they sometimes-divergent goals of the Audit Committee, andexecutive management, finding a path that allows them to meet new expectations?How will Internal Audit functions continue to add valuey to their companies’ efforts to improve their business andoperational performance?Has the Internal Audit function identified and sharedy risks that are covered and not covered in their InternalAudit plan with the Audit Committee and executive management?Can Internal Audit functions continue to integrate theiry efforts with other risk management functions within theirrespective companies and gain better alignment to make risk management more effective and efficient?How will Internal Audit functions find and keep the righty people, and retool existing personnel, particularly inareas where needs are acute such as fraud, IT, and unique business and operational risks?Can Internal Audit functions leverage the benefit ofy technology tools and knowledge to help improve overallcoverage and relieve pressure on resources? Our 2007 Global Internal Audit Survey demonstrates a changing landscape and presents a significant opportunity. Those Internal Audit functions that are more able toanswer the questions above and take advantage of these opportunities will thrive in the future.ConclusionOur 2007 Global Internal Audit Survey reveals that Internal Audit functions around the world are being challenged in many ways. The challenges are numerous. But so are the opportunities ofgrowth, impact and influence.。