CFA Level 3 考点解析二

cfa3级 case study

CFA3级案例研究一、概述CFA3级考试是 Chartered Financial Analyst(注册金融分析师)资格认证考试的最高级别。

该考试是金融行业著名的专业人士认证考试之一,被认为是全球金融行业最具专业性和权威性的认证考试之一。

CFA3级考试的案例研究部分是考试的一个重要组成部分,通过对真实世界的金融案例进行分析和解决问题,考察考生在实际工作中处理复杂金融问题的能力,是考试的重点难点之一。

二、案例分析1. 案例背景本次案例研究的主题是关于某家上市公司的财务报表分析及估值分析。

这家公司是一家跨国企业,主要经营范围涉及多个行业,是全球知名的多元化企业。

在过去的几年中,该公司的业绩呈现出了一定的波动,市场对其未来的发展前景存在一定的分歧。

2. 案例问题本次案例研究主要围绕以下几个问题展开分析:(1)通过分析该公司的财务报表,对其财务状况做出评估,并指出存在的风险和挑战;(2)采用合适的方法对该公司进行估值分析,并提出自己的估值结论;(3)分析该公司所处行业的市场环境和竞争格局,评估其未来的发展潜力;(4)就公司的财务和经营情况,提出自己的投资建议。

3. 解决方法针对上述问题,考生需要运用所学的财务分析、公司估值、风险管理、投资组合管理等知识,结合行业动态和相关领域的最新研究成果,对该公司的财务状况和未来发展进行全面、深入的分析,并给出自己的见解和建议。

三、分析方法1. 财务报表分析需要对该公司的财务报表进行深入分析,包括利润表、资产负债表、现金流量表等,从中提取相关的财务指标,如利润率、资产负债率、经营现金流等,以此来评估该公司的财务状况。

2. 公司估值分析考生需要采用适当的估值模型对该公司进行估值,可以选择盈余折现模型(DCF)、市盈率法、市净率法等多种方法进行估值,综合考虑估值结果的优劣势,得出自己的估值结论。

3. 行业分析第三,需要对该公司所处行业的市场环境进行深入分析,包括行业生命周期阶段、市场增长率、供应链及竞争格局等,以便更好地了解该公司的发展潜力。

CFA三级中文精讲2PPT模板

0 5 2.5负债驱动型投资策略的风险 0 6 2.6债券指数及跟踪指数投资面临的

诸多问题

7固定收 益

2负债驱动的投资策略 和指数投资策略

2.7进行债券指 数投资的其他方

法

2.8选择参考 基准

2.9梯形债券 组合

7固定收 益

3收益率曲线投资策略

1

3.1收益率曲线及其变化

2

3.2久期和凸性

3

5

4.5国际信用组合

6

4.6结构性金融工具

04 8股权投资组合管理

8股权投资组合管 理

1股权投资组合概述 2资本市场的预期 3主动型权益投资策略 4主动投资:组合的构建

8股权投资 组合管理

1股权投资组合概述

01

1.1股权投 资在组合中

的角色

02

1.2股票市 场的划分方

法

03

1.3股权投 资组合的收

3

1.9宏观经济分析综述

4

1.10经济周期分析

5

1.11经济增长趋势

6

1.12外部冲击

5经济分析在组 合管理中的运用

1资本市场的预期

1.13国家 间的相互

影响

1.14经济 预测

1.16预测 汇率 ★★★

1.15运用 经济信息 预测收益

5经济分析在组 合管理中的运用

2股票市场估值

2.1股票市场估值:戈

2

3.2应税投资者的资产配置

3

3.3战略资产配置的修正

4

3.4资产配置的短期偏离

5

3.5资产配置中的行为偏差

6资产配 置

4外汇管理

1

4.1回顾外汇市场中的基本概念

2

cfa三级笔记

cfa三级笔记Monte Carlo simulation(专题)定义:Monte Carlo simulation allows asset manager to model the uncertainty of several key variables. Generates random outcomes according to assumed probability distribution for these key variables. It is flexible approach for exploring different market or investment scenario. 蒙特卡洛模拟是将变量(事先定义好分布)的值随机发射,生成了结果,可灵活的探索不同市场、投资环境下的状态。

较MVO的优势:1, Rebalancing and taxes, Monte carlo simulation allow to analyze different rebalancing policies and their cost over time(in multi-period situation). 蒙特卡洛模拟可以用于分析执行不同的再平衡策略、税收时的影响。

2, Path dependent. As there are cash out flow each year, terminal wealth(the portfolio’s value at a given point)will be path-dependent because of the interaction of cash flows and returns. 如果每年都有资金流出,指定时间的组合价值会受这些资金流出和收益的影响Cash flows in and out of a portfolio and the sequence of returns will have a material effect on terminal wealth, this is termed path-dependent.3, Monte Carlo can incorporate statistical properties outside the normal distribution, such as skewness and excess kurtosis.蒙特卡洛模拟可用于建模非正态分布。

CFA考试考点解答-CFA3级-金多多学员-2014-February

CFA3级到底考什么?CFA 考试难度大不大?对于已经通过了1级和2级的考生来说,通过3级是功德圆满,九九八十一难的最后的冲刺。

看一下金多多学员和金多多顶级老师的谈话,了解CFA3级的考点是如何分布的,CFA 协会又是如何出题的!2014年2月3日宋老师,您好。

我上一周在家过除夕期间,看完了R26-27的视频学习。

有以下一些问题请教:关于讲义R26:老师在slide26有说HF 是使用absolute measurement 来评价表现,而不是采取relative measurement (有benchmark )来评价的,但在slide27就有列出benchmarks ,这些HF indices 何用?不是用来做评价标准,就仅仅是用来供投资者构建HF portfolio 时参考吗?答:所谓HF 是absolute measurement, 是相对于其他传统的投资工具(比如共同基金)来讲的,因为HF 的策略和投资期限五花八门,有些甚至都没有系统性风险,很难在市场上找到现成的同样具有可比性的benchmark ,所以衡量HF 最直观的就是直接看它取得的alpha 的大小。

至于后面给出的一些benchmark ,都是一些机构自己统计出来的index ,但是我们后面也讲到了,这些指数存在很多的问题,所以仅供参考。

像HF ,PE (含VC )这类封闭性的投资工具,一些机构公布的指数都是仅供参考。

关于讲义R26:关于“look through leverage ”,意思就是我假定每家HF 借来的钱就是自己的,能够这么假定是因为杠杆率不影响ROA ,所以计算ROA 时直接看成没举债就行了。

但对于投资而言,更关注的还是ROE 吧?所以此时这种“look through leverage ”就没多大意义的?答:ROE 主要衡量的是上市公司。

对于封闭型的HF ,PE ,主要用IRR 和我们这里讲到的一些回报率来衡量。

2021cfa三级考点

2021cfa三级考点摘要:1.CFA三级考点的概述2.CFA三级考试的科目及重点3.备考CFA三级的方法和建议4.CFA三级考试的重要性正文:随着金融行业的不断发展,CFA(Chartered Financial Analyst)认证已经成为金融从业者追求的专业资格。

CFA三级考试是该认证体系中的最后一步,对于有志于成为一名合格的投资专业人士来说具有重要意义。

本文将概述CFA三级考点,并提供一些备考建议。

一、CFA三级考点的概述CFA三级考试分为两个部分,分别是上午的案例分析和下午的选择题。

上午的案例分析占总分值的50%,下午的选择题占总分值的50%。

通过三级考试后,考生需要完成一篇投资组合管理及财富规划的论文,方可获得CFA认证。

二、CFA三级考试的科目及重点1.投资工具:包括股票、债券、衍生品等金融产品的定价和分析方法。

2.资产配置:基于投资者的风险承受能力和投资目标,进行资产组合的设计和管理。

3.公司金融:重点关注财务报表分析、企业估值和资本结构决策等方面。

4.经济学:涉及宏观和微观经济学知识,为投资决策提供理论基础。

5.金融市场与金融机构:了解全球金融市场的运行机制和各类金融机构的职能。

6.伦理与职业道德:强调金融从业者的职业道德和行为规范。

三、备考CFA三级的方法和建议1.制定学习计划:根据自身情况,合理安排学习时间,确保各科目均衡掌握。

2.参加培训课程:可以选择线上或线下的培训课程,以提高学习效果。

3.做题巩固:通过模拟题和历年真题的练习,检验学习成果,查漏补缺。

4.积累实际经验:在实际工作中运用所学知识,提高投资决策能力。

5.注重伦理道德:在备考过程中,加强对伦理道德知识的学习,培养良好的职业道德素养。

四、CFA三级考试的重要性1.提升个人能力:通过CFA三级考试,可以系统地掌握金融投资领域的专业知识和技能。

2.提高职业竞争力:CFA认证是金融行业内的权威资格,有助于求职和晋升。

CFAlevel3notesCFA三级备考经验+原创学习笔记最新完整版

CFAlevel3notesCFA三级备考经验+原创学习笔记最新完整版CFA Level 3 NotesContentsBook 1 Ethical and Professional Standards and Behavioral Finance (1)Reading 1&2 Cod e and Standards and Guidance for Standards (3)Reading 3 Application of the Cod e and Standards (21)Reading 4 Asset Manager Cod e of Professional Conduct (22) Reading 5 The Behavioral Finance Perspective (25)Reading 6 The Behavioral Biases of Individuals (27)Reading 7 Behavioral Finance and Investment Processes (29) Book 2 Private Wealth Management and Institutional investors (32)Reading 8 Management Individual Investor Portfolios (32)Reading 9 Taxes and Private Wealth Management in a Gl obal Context (35)Reading 10 Estate Planning in a Gl obal Context (37)Reading 11 Concentrated Singl e-Asset Positions (39)Reading 12 Lifetime Financial Advice: Human Capital and Asset All ocation (44)Reading 13 Managing Institutional Investor Portfolios (46) Reading 14 Linking Pension Liabilities to Assets (53)Book 3 Economic Analysis, Asset All ocation and FI Portfolio Management (55)Reading 15 Capital Market Expectations (55)Reading 16 Equity Market Valuation (64)Reading 17 Asset All ocation (66)Reading 18 Currency Management: An Introduction (74)Reading 19 Market Ind exes and benchmarks (78)Reading 20 Fixed-Income Portfolio Management –Part Ⅰ (80)Reading 21 Relative-Value Methods for Gl obal Credit Portfolio Management .. 85 Reading 22 Fixed-Income Portfolio Management –Part Ⅱ (90)Book 4 Equity Portfolio Management, Alternatives, Risk, and Derivatives (95)Reading 23 Equity portfolio Management (95)Reading 24 Alternative Investments Portfolio Management (103)Reading 25 Risk Management (111)Reading 26 Risk Management Applications of Forward/Future Strategies (115)Reading 27 Risk Management Applications of Option Strategies (117)Reading 28 Risk Management Applications of Swap Strategies (119)Book 5 Trading, Monitoring, Rebalancing, Performance Evaluation, and GIPS (121)Reading 29 Execution of Portfolio Decisions (121)Reading 30 Monitoring and Rebalancing (126)Reading 31 Evaluating Portfolio Performance (129)Reading 32 Overview of the Gl obal Investment Performance Standards (135)CFA3级备考经验CFA3级考完,现在已经可以在名片上加那三个字母了。

2024年cfa三级考纲

2024年cfa三级考纲2024年CFA三级考纲是全球金融领域中备受瞩目的考试大纲,为CFA候选人提供了指导和准备的重要依据。

本文将对2024年CFA三级考纲进行全面解读,包括考试结构、考试科目和考试重点等方面的内容。

2024年CFA三级考试的结构与以往相似,分为两个考试,分别是上午的第一部分和下午的第二部分。

第一部分的考试时间为3小时,涵盖了宏观经济学、投资工具、资产估值、投资组合管理等方面的内容。

第二部分的考试时间为3小时,主要考察投资管理、财务报表分析、道德与职业标准等领域的知识。

2024年CFA三级考试的科目包括宏观经济学、投资工具、资产估值、投资组合管理、投资管理、财务报表分析和道德与职业标准。

这些科目涵盖了金融和投资管理的各个方面,考察了候选人的专业知识、技能和职业道德。

在宏观经济学科目中,考生需要了解宏观经济环境对投资决策的影响,包括经济周期、通货膨胀、利率等因素的分析和应用。

投资工具科目主要涉及各类投资工具的特点、风险和收益,包括股票、债券、期货、期权等,以及对这些投资工具进行选择和组合的技巧和策略。

资产估值科目考察了对金融资产和投资组合进行估值的方法和技巧,包括财务报表分析、DCF估值、市场多因素模型等。

投资组合管理科目重点是了解投资组合的构建和管理,包括资产分配、资产选择、风险管理等方面的知识和技能。

投资管理科目涵盖了投资管理的各个方面,包括投资决策、投资组织和投资绩效评估等内容。

财务报表分析科目要求考生掌握对财务报表进行分析和解读的技巧,包括利润表、资产负债表和现金流量表的分析方法和应用。

道德与职业标准科目是CFA考试中的重要部分,要求考生了解和遵守职业道德标准,包括投资决策的道德和法律准则、投资专业的职业行为等。

为了成功通过2024年CFA三级考试,考生需要有系统的学习计划和充分的准备。

首先,考生应该熟悉考试大纲,了解每个科目的重点和考点,制定相应的学习计划。

其次,考生需要进行大量的复习和练习,通过做题和模拟考试来提高自己的应试能力。

cfa二级课后题讲解

cfa二级课后题讲解

CFA二级课后题讲解的内容包括但不限于以下方面:

1. 财务分析:这部分主要考察考生对财务报表的解读能力,包括资产负债表、利润表和现金流量表等。

题目会要求考生分析公司的财务状况,评估其偿债能力、盈利能力、运营能力和发展能力。

2. 投资组合管理:这部分主要考察考生对投资组合管理的理解,包括资产配置、风险管理和业绩评估等。

题目会要求考生制定投资策略,评估投资组合的风险和回报,以及根据市场变化调整投资组合。

3. 经济学:这部分主要考察考生对宏观经济学的理解,包括国民收入、货币供应、财政政策和货币政策等。

题目会要求考生分析经济形势,评估经济政策的影响,以及预测经济未来的发展趋势。

4. 金融市场:这部分主要考察考生对金融市场的理解,包括股票市场、债券市场、期货市场和期权市场等。

题目会要求考生分析市场走势,评估市场风险,以及预测市场的未来变化。

5. 公司金融:这部分主要考察考生对公司金融的理解,包括资本预算、资本结构、股利政策和公司并购等。

题目会要求考生分析公司的财务决策,评估公司的价值,以及制定公司的财务策略。

以上是CFA二级课后题讲解的一些方面,希望对您有所帮助。

CFA通过Level 3的经验

CFA通过Level 3的经验我大体总结了一下:英语阅读量很大-------需要我们在被考试不断提高自身的阅读能力,以及抓重要信息的技巧!(有些信息都不需要读的)在这次上午的考试中,感觉更像是在做阅读理解题,计算得分数特别少,大部分是文字论述,所以说准确清晰的表达就显得格外重要,第一题考查的是个人(一个米兰城的职业足球明星)IPS制定问题,着个人的个人情况非常复杂,再算他的Required rate of reture时差不多要用到将近十个数据,所以建议大家先做分数少的题,做完一个对以下时间,这样你就知道下面做题的速度了,若一上来就做一个半小时的题目,一旦超时,后面再赶就相当困难了!还有一点就是,别一上来就闷头答题,按着题号在纸上狂写,后来发现答案写错了地方,一定要稳住情绪,在试卷要求的页面上写答案!三级考试的难点出现在Asset Valuation(占总分数的50%-60%)--原因很简单,这部分的内容相当的冗杂,有很多边边角角的东西,比如说在这次考试中,你不光可以见到模拟题中常出现的:1、Hedging your investments using derivatives,2、复合型期权的Pay-off关系,3、SWAP,4、credit derivatives,还可以发现有一些不被大家重视,也可以说是Notes中解释得不是很清晰的topics,例如:我们作投资决策当中用到的benchmark quality 如何衡量,不是notes中概括的SAMMURAI那么简单!还有一个关于Benchmark的题,现在想不清楚了!做这些提示,脑子一定要保持相当的清醒,到了下午大家也都感觉疲惫了,一定要克服困难,打足精神,可以这样说,没有一个选择题是可以看完接着就选出答案的送分题,出题人总是要考查大家题目背后的基础知识,经过一番逻辑推理才能得到可能的正确答案!Notes中没有afternoon session的历年真题,希望大家多做一些sample exam找找哪些知识点还需要温习!一般来说,这部分的Notes最少要看两遍!总体感觉,备考三级有一套Notes,已经足够!最后祝愿大家都能如愿通过考试!各位考生,2015年CFA备考已经开始,为了方便各位考生能更加系统地掌握考试大纲的重点知识,帮助大家充分备考,体验实战,高顿网校开通了全免费的CFA题库(包括精题真题和全真模考系统),题库里附有详细的答案解析,学员可以通过多种题型加强练习,通过针对性地训练与模考,对学习过程进行全面总结。

CFA三级考试12个考点全面解析

CFA三级考试12个考点全面解析(1)Ethics:在下午部分考察了两道题目。

这部分内容大部分和一级、二级相似,只是添加了AMC的一些考点。

两个Item Sets的12道题中有2道是关于AMC。

Duty to employer,Conflict of interest, Due Diligence相关的内容一直是重要的考点,这次的CFA考试三级中也考到了,不过相信已经进入三级考试的各位考生都已经十分熟悉。

(2)Behavior Finance:主要考查投资者行为偏差及其修正。

这些都是传统的重点,所以考生对这些概念肯定复习过,但在考试中更加注重结合案例的分析能力,必须在有限的时间内通过分析题干得到结论,对于考生对于该考点的熟练程度要求较高。

在考试中具体涉及到了mental accounting、anchoring等偏差,需要考生结合案例给出该投资者违法这两项规定的证据,并提出解决方案。

(3)Individual:是上午essay部分考试的重点,也是难点,这次有两道大题。

首先是计算题,计算投资组合的Liquidity needs以及给出退休后目标(FV)和期间现金流(PMT),要求计算投资组合Required return。

其次是分析题,主要包括:风险承受能力分析,如何使用期权(Put option)来处理concentrated equity asset,以及如何降低该期权策略成本等问题。

(4)Institution:也是上午essay部分考试的重点,这次也考了两道大题。

考察的重点在于结合具体案例,分析具体机构投资者的优缺点等。

第一道机构投资者IPS考察的是Pension,也是几乎每年必考的内容,通过一个公司收购另一家公司(less profitable)后一些基本面信息的改变(员工年龄变化,Sponsor 盈利能力的变化等)判断影响新的养老金Risk tolerance 的因素并分析原因。

第二题考察的是对比Endowment 和Insurance,根据基金经理的交易策略判断是否适用ALM(Asset liability management)还是AO(Asset only)进行管理,以及影响Risk tolerance的因素。

CFA备考指导:CFA考试Level 3备考心得

CFA考试Level 3备考心得CFA考试被称作金融第一考,考试分为Level1、Level2、Level3。

考试难度逐渐增加。

鹏生教育CFA考试培训频道一起来分享下一位学员备考CFA level3 的亲身经历。

一,关于考试本身:(1)L2难还是L3难?一定是L3。

即使不说考试内容,只考虑考生质量。

你想,2级本来就不简单,通过之后继续准备3级的人已经身经百战。

再能去参加考试坐在考桌前的人绝不会是空手而来。

其次对我们英语非母语的人来说挑战更大。

(2)看书还是notes?别纠结了,只看notes,书后题或许可以做。

官方的书肯定来不及看,专注于精简的notes是在有限的时间内取胜的基础。

(3)上午是不是比下午难?上午的比我当初想象的简单,下午比我想象的难很多(最后上午拿了7个A,下午只有3个A)。

二,关于准备过程:本人平时工作很忙且压力颇大,平均每天到家吃完饭从10点半开始看书至11点半至12点,即使这样的节奏一周也只能有2-3天,其他几天根本没时间再坐在书桌前。

每个周末能保持8-10小时看书时间,最后几周至12小时左右。

这种生活节奏给人最大的感觉就是忙完一天,头痛脑胀,恨不得吃晚饭躺下睡到第二天。

这时再想坐在书桌前静下心看书几乎不可能,因为大脑会自我保护,不允许过度运作。

最好的办法是去健身房运动半小时,回来洗个澡,立刻感觉神清气爽。

这多出来的精力又够你看1小时的书。

每人看书的速度和效率都不同。

在工作的考友们,强烈推荐你们提前开始看书,最好1月就可以开始了。

三级给人的感觉是:不看到第二遍基本摸不清考试脉络。

本人看书较慢,但至考试前一天,本人还硬是啃了3回书(第一轮2.5个月,第二轮1个月,第三轮2周)。

三,看书还是做题?和2级一样,做题在3级中也非常重要,重要性要超过2级很多。

这里有个小故事要分享。

在临考5周时,我看完第二轮书,但一题也没做。

当时觉得时间紧张,所以问了几个CFA同事(本人在万恶的美帝工作)下面5周什么战略最好。

CFA三级精要

Behavioral Heuristics – Check Anchor/OAR Availability– Conservatism, Anchoring,Overconfidence, Ambiguity aversion, Representativeness, Availability Traditional Finance – TF-RAR - Risk averse, Asset integration, Rational expectations Behavioral Finance – BF-LAB - Loss averse, Asset segregation, Biased expectationsType of Investors – CMIS - Cautious, Methodical, Individualistic, SpontaneousIPS Process – OCSAEEA, Old Cars Sell At Eastern European Auctions – Objectives,Constraints, Strategy, Allocation, Execution, Evaluation, AdjustmentsIPS Constraints – URLIT - Unique, Regulatory/legal, Liquidity, tIme, TaxTDA vs. TEA – Higher Enders Take TEA – Higher Ending Tax rate TEA betterResidence vs. Source – Pay Greater rate with Credit, Exempt Source Income, Deduct Paid Taxes If our Human Capital is Bond-like, we should invest more aggressively (equity) and our demand for life insurance increases.Type I & II Error – Type I, I did something (rejected H0) wrong; Type II, failed TO reject H0 Null = Manager adds no value; Reject & conclude that manager adds value when he actuallydoes not.DB Risk Toler/Objs. Factors– P.S. San Francisco Risked Everything With Certain Plan Features - Pension Surplus, Sponsor Finances, Risk Exposures, Workforce Characteristics, Same Prudent Man Rule : Foundation for all write stds. Of prudence apply in Legal/Reg.Prudent Expert : DB/DC planPrudent Investor : Endowment, Life InsurancePrudent Man Rule: the requirement that a trustee, investment manager of pension funds, treasurer of a city or county, or any fiduciary (a trusted agent) must only invest funds entrusted to him/her as would a person of prudence, i.e. with discretion, care and intelligence. Prudent Man Rule requires that each investment be judged on its own merits. Under the Prudent Man Rule, speculative or risky investments must be avoided. investments aren't viewed in a portfolio context.Prudent Expert Rule: Revised version of the prudent man rule required by ERISA to guide managers of pension and profit sharing portfolios. The main addition is that the manager must act as someone with familiarity with matters relating to the management of money, not just prudence.Prudent Investor rule: This is a modified version of Prudent Man Rule in that it views asset allocation from a portfolio context. An asset (like derivatives) may be too risky to invest if considered on astand-alone basis but can provide diversification benefits if viewed in a portfolio context.Life insurance companies' RETURN objective : APEG(Actuarial + Positive interest rate spread + Enhance Margin + Growth Surplus)An investor whose decisions are impacted by mental accounting will look at investments as separate, focusing on the risk of investments in isolation.According to behavioral finance, expert forecasters are overconfident in their forecasting ability due to cognitive dissonance.Cognitive dissonance states that individuals will avoid information (reflecting what has been actually experienced) that is in disagreement (dissonance) with the individual’s perceived ability of himself or herself. As a result, experts will have limited recollection of their failures.Frame dependence refers to investors' tendency to frame their tolerance on the current direction ofthe market or in the context of the information received rather than on its own merits.Anchoring refers to the inability to fully incorporate (adjust) the impact of new information on projections.Representativeness can cause investors’ perceptions to be based upon current or historical information rather than unbiased expectations resulting in overpriced “winners” underperforming and underpriced “losers” outperforming as prices retur n to their intrinsic values.If someone developed her investment style through trial and error, learning from her own mistakes. This is a sign of heuristic-driven bias.Behavioral finance assumes that:1.investors are loss averse, which means they prefer uncertain losses to certain losses.2.investors exhibit biased expectations, due to overconfidence in their ability to forecast the future.3.investors construct portfolios via asset segregation, meaning that they tend to focus on an asset’s individual investment features versus its impact on the overall portfolio positionBy admitting his mistake but reiterating other projections, one used the "single predictor" defense.Feeling that they should spread out their risk, but not knowing how leads to the 1/n diversification heuristic. Often times, participants will only have a rough understanding of the effects of correlation and diversification and will simply divide their assets equally over the investment options in the plan in an attempt diversify their portfolio.DC participants tend to hold excess stock of the company they work for due to familiarity and a perceived endorsement by management.The endorsement effect refers to the misconception that by offering an investment as an alternative, the sponsor is implicitly endorsing it as a good investment.Note that the status quo bias refers to a lack of action on the part of the participant. Also note that putting too much in company stock would be an example of an investor being “boundedly selfish” in that there does not seem to be a determination if the investment would be in the investor’s best interests.Trial and error and experimentation are heuristic learning processes. Heuristic learners pick up information simply, through their own efforts or from sources simple to access. They don't do research. When overconfident investors revise their forecasts based on new information, they tend to overestimate the impact. As an overconfident investor, one will be disappointed by the subsequent movements in Bison stock because of her initial overoptimism after the earnings announcement.Investors who use anchoring tend to underestimate the impact of new information because they are anchored in their old beliefs. One will be pleased by the subsequent movements in stock because hewill have initially underestimated the impact of the positive earnings announcement.Bank Security Portfolio Return Objs. – I Remember Living In CR – Interest Rate risk, Liquidity, Income, Credit RiskCME Form Process –Forming Expectations Needed Historically Provided Capital Managers Many Incentives & Gratifying Invitations Into Overlooking Market ExpectationsMade Rashly - Find Expectations Needed, Historical Performance, ChooseMethods/Models/Info, Get Info, Interpret Output, Make Expectations, Monitor &RefinePsych Traps –Overconfident Chief Executives Start Quietly Piling Risk– Overconfidence, Confirming Expectations, Status Quo, Prudence, RecallibilityBRIC-Size of BRIC economies could be >1/2 that of the G6 by 2025, and could surpass the G6 by 2040-India's growth is strongest at 5% for next 30-50 years-Global spending for BRICs - 4x as large as G6 by 2050-Real exchange rates for BRIC countries could strengthen by 300% by 2050-Slowest to open economy: India-Weaker tech progree: Brazil & India-Most rapidly aging: China & Russia-China's economy could overtake Germany in next 4 years, Japan by 2015, and US by 2039-India's economy could be larger than all but US & China in 30 years-BRIC per capita income will remain below G6 (except Russia)Factors that lead to growth-Technological progress-Growth in capital stock-Employment GrowthConditions for Sustained Economic Growth-Macroeconomic stability-institutional efficiencies-open trade-worker educationWhy Emerging Markets in a Portfolio?Increased growth in markets = increased demand for capital = stonger currency values = increased market caps which further justifies inclusion in a well diversified portfolioWhen evaluating a specific country, are the following good or bad signs?1. GDP=5% good if >4%, under may mean growing slower than population2. Defecit/GDP =10% bad >4% indicates substantial credit risk3. Foreign Debt/GDP = 75% bad >50%4. Debt /Current Acct Receipts =250% bad >200% considered high risk5. Reserves/Short Term Debt =200% good ≥200% safe, ≤100% very risky-BL is a top down approach-uses returns implied by the value weighted global market index-alter it slightly based on analyst opinions (like tactical asset allocation)-It will result in a well diversified portfolio, and will avoid the input bias from E(R)-Disadvantage is you must use historical volatility.-If you want to make your portfolio less risky (below average risk) but have no views, combine world portfolio with risk free asset. To make more risky (above average risk) you borrow at risk free rate and invest in the market portfolio.WACC with Pension Assets:βA,T=W O,T[βE,O1+D OE O]+ W P,T[W E,P∗βE,P]Note: For Operations: %Eq ↑→βO↓→βT↑→DE ↓ For Pension: %Eq ↑→βP ↑ →βT↓→DE↓Cyclical Bond:Increases in # of new issues associated with narrower spreads & stronger returns and vice versa,Liquidity Δs due to Economic ConditionsSecular Bond:Bond Structures are trending toward intermediate term bullet structures Implications: (1)Structures w/options embedded sell at premium due to scarcity value (2)Structures w/longerduration will sell at premium as percentage of long-term issues will decline - effective duration and aggregate interest rate risk sensitivity will also decline. (3) Credit-based derivatives use willincrease for return&/or diversification benefits; Liquidity increasing due to trading innovations &competition among managersLeverage, Portfolio Returns & DurationIf Return > cost of Debt → Return enhanced If Return < cost of Debt → Loss magni fied Leverage increases σ of R Port (Not R Investment), Investment Return increases σ of R PortDuration: D Port=(D I I−D B B)EI = B+ERisk Measurement Deficiencies:σ2&σ– Assumes NDistribution, requires [N*(N+1)]/2 estimated terms to estimateσPort2, Bond CharsΔw/time Shortfall Risk (risk of not achieving R= x) –Doesn’t account for magnitude of loss in $ terms Semi-σ2–Statistically accuracy<σ, difficult to compute on large port, may not be a good forecast VaR – does not indicate the magnitude of the very worst possible outcomesInt Rate Futures, Swaps, & Options - Lengthen - Long DD f >0, Shorten - Short DD f <0DD T = DD P + DD F; DD f=D f∗ΔIR(decimal)∗FaceValue∗(futures Price100)=DD CTDCTD Conv FactorNumber of Contracts to Hedge: #Contracts=DD T−DD PDD f =DD T−DD PDD CTDCTD Conv Factor⁄Hedge Ratio– relative sensitivity to Int Rate risk determines number of contracts required for an effective hedge -=DD PDD CTD ∗ConvFactr∗βYield=D H P HD CTD P CTD∗ConvFactr∗β=Factor Exposure(Bond to be ℎedged)Factor Exposure of futures contractβYield =E(relative Δ on Bond to be hedged & CTD Bond yield levels & spread)= α + b(Yield CTD) + εD Option(future)= ΔOption∗D U∗Leverage or [P UnderlyingP OptionInstrument]; If call → ΔOption & D U positiveCredit Options: (1)Credit Opt onU - Binary Credit Option –credit event trigger→buyer put gets X-V t(2)Credit Spread Opt – buyer gets (Spread Maturity–Spread Strike) * Notional Amt * Risk Factor Credit Forwards:ZeroSumGame(1 winner=1 loser)–buyer gets same payoff as Credit Spread OptCredit Swaps: CDS – buyer pays annual premium on notional amount & if a credit event creditevent occurs the buyer is compensated by seller for loss in investment valueInternational Bonds:Potential Sources of Excess Return on International Bond Portfolio:(1)Market Selection (2)Currency Selection (3)Duration Management (4)Sector Selection(5)Credit Anal (6)Markets outsideBenchmark–Indexes usually only sovereign might add CorpCou ntry/Yield β:ΔYield For=α+βCountry(ΔY Dom)+ε is regressed; βCountry=ρ(Y For,Y Dom)*σFor/σDomΔYield For=βCountry*ΔY Dom & ΔV ForB = -D ForB*ΔY For*100 ∴ΔV ForB=-D ForB*ΔY For Given ΔY D om*100 → Dur Contribution to Port Dom = Weight*D ForB*βCountryHedging Currency Risk: (1) Forward Hedge – manager enters contract to sell Currency For @ F0,M(2) Proxy Hedge – same but w/currency that is highly correlated w/Currency For bc Forward N/A(3) Cross Hedge –contract to sell Currency For for a 3rd currency–Δs risk exposure doesn’t removeReturns: R$ = R LC + R$ + R LC * R$ ; R$ ~ R LC + R$ ~ IntR$ + (R LC – IntR LC)→Best bond = Max(R LC-IntR LC) @same risk characteristics & ability to fully hedgeI f Receiving CurrX & believe CurrX will Appr/Depr More/Less vs. CurrDom than Prem/Disc→UnhedgedBreak Even Analysis: Gives manager an idea of Amt of risk associated with attempting toexploit Y advantage, by looking at Amt Y must widen to make Total Returns equal; Managermustassume a Set Time Horizon and measure Yield Δ in bond with Higher DurationBreak Even BP ΔY = Annual Yield AdvantageTime Horizon−Duration⁄Information Ratio= E(α)σα⁄= Active Return over Tracking Error (σα) measures tracking riskMBS securities exposed to "SIP Vodka Martinis":Sector risk Interest rate riskPrepayment riskVolatility risk Model RiskNon-MBS securities exposed to: "ISCOY":Interest rate riskSpread riskCredit riskOptionality riskYield curve riskTWO BOND HEDGEStep 1: Calculate the price of the MBS, 2-year, and 10-year securities assuming a level shift up ininterest rates (Level scenario)Step 1b: Do the same but for a equal level downward shiftStep 2: Do the same as Step1 and Step1b for an assumed steepening and flattening of the Yield curverespectively (Twist Scenario)Step3: Now you have two prices for each security for the "Level" shifts and two prices for eachsecurity for the "Twists" in the term structure... you now want to calculate the average price changefor each one.So if in Step1 you see that when the rates went up your MBS declined by $2.00 and when the rateswhen down your MBS increased by $2.00, you would take the average of the two to get $2.00average price change for the MBS (level). Do this for all the securities in both the Level and Twistscenarios.Step4: Once you have all the average price changes you can set up a system of equations to solve forthe optimal quantities of the 2-year and 10-year securities to invest in (Algebra 1)...They are:H2(AveChange in 2yr-Level) + H10(AveChange in 10yr-Level) = -AveChange in MBS-LevelH2(AveChange in 2yr-Twist) + H10(AveChange in 10yr-Twist) = -AveChange in MBS-TwistWhere:H2 = Number of 2year secuties needed per $1 of MBSH10 = Number of 10year secuties needed per $1 of MBSSolve for both H2 and H10... negative or positive will tell you if you should long or short them.By investing in these you will hedge your MBS against both level shifts and twists in the term structure.(or at least get pretty close)Reasons for NO T trading: Please Stop Bothering SusanPortfolio constraintsSeasonalityBuy and holdStory disagreementsThere are eight main reasons TO trade bonds - "really can cook, no salt you say?"really = relative value pick up (biggest reason)can = credit upsidecook = credit defenceno = new issue tradessalt = secot-rotation tradesyou = yield curve pickups say? = structure tradesSelling Disciplines:Opportunity Cost Sell Discipline – sell for better investment Deteriorating Fundamentals Sell Discipline – sell bc investment has worsened Down-from-Cost Sell Discipline – similar to a stop-loss Up-from-Cost Sell Discipline – similar to stop buy Valuation level Sell Discipline – sell if P/E or P/B rise above historical mean Target Price Sell Discipline – sell once reaches target priceFundamental Law of Active Management – Info Ratio ≈ IC ∗√IBIC=Investor Coefficient, the depth of knowledge about individual securities, measured bycomparing forecasts to actual outcomes; IB=Investor Breadth, the number of independentinvestment decisions, e.g. buying multiple stocks in a sector b/c investor believes sector willoutperform only 1 investment decisionPortfolio Active Risk – given a correlation of zero =√∑w α,i 2σα,i 2Utility = R a – λa 2σa 2 λa is level of risk aversion in terms of active returnTotal Active Return = true Ra + misfit Ra = activeR – normal Rport + normal Rport – benchmark RTotal Active Risk = = √∑w true 2+σmisfit 2True Info Ratio = true Ra / true riskPortable Alpha - example1: want European Equity Alpha but S&P 500 Beta: Buy S&P futures contract,Invest in Euro Equity manager, and Short Euro Equity index futures; thus getting Beta fromS&P and Alpha from Euro Equity; example2: buy S&P ETF and invest in small-cap long-short manager, receive Beta from S&P and Small-Cap AlphaMoral Hazard Problems (Corporate Governance):a) Insufficient Effort - refers to not hours in the office but managers allocation of work time;may avoid unpleasant or inconvenient activities at the shareholders expense (negotiating salaries,switching suppliers), may devote insufficient time to employee oversight (think Nick Leeson),may work on competing activities (political involvement, investments in other ventures) ratherthan managing the firm.b) Exravagant Projects - is when management continue to invest in high profile or pet projectseven though the return on the investments is not in the best interest of the company and itsshareholders. Empire Buildingc) Entrenchment Strategies -- when managers invest in bad projects but in projects where theyhave a strong understanding so that they become more valuable to the company, or manipulateperformance measures in their favor, take excessive or insufficient risk, resist hostile takeovers.d) Self-Dealing– when managers increase their private benefit from running the firmBoard of Directors (Corp Gov):-- Independent Chairman-- Majority should be independendent-- Audit, Compensation, Ethics, & Nominating committees should be majority independent-- Some board and/or committee meetings should be held without management present-- Should be able to seek outside advice at firm’s expense-- Should be required to hold minimum amount of equity-- Compensation should be equity-based-- Should have mandatory retirement age-- Self-evaluations of board should be doneEmerging Markets Finance -As markets move from segmented to integrated Equity P ↑ and E(R) ↓ bc in integrated marketCo-σ2is the only priced risk and it will be lower than the market’s stand-alone σ2Liberalization(dom) - characterized by privatization of firms & bank reformRisks/Issues: Contagion - crisis spreads to other countries. Contagion in Curr occurs for 1 of 5 reasons:(1)Country devalues Curr to keep exports competitive w/other country w/devalued Curr(2)Exports decline due to other countries in crisis (i.e. importers of their goods)(3)Intitial devalue wake-up-call to investors that other countries Curr.s have weaknesses(4)Crisis in country1 leads to credit crunch in another (ie country1 is their major creditor)(5)Initial crisis causes investors to liquidate their investments in other countriesNon-Normal Return Distribution– Fat tails & Negative skew(↑larger negative R frequency)CorpGov–traditionaly weak in EM,↑amt of insider ctrl&lowCEO turnover post-poor perform Liberalization:EqP↑, Volume↑,Liq↑,GDP↑,IPOs↑,Competition↑,CapitalFlows↑,FirmEfficiency↑Trade↑,E(R)↓,Cost of Capital↓,Cou ntryDebt↓,Infl↓,CurrencyVolatility↓If Home Country Bias exists cost of cap not as far ↓&EM Securities D less ↑Mean Variance: Optimizes a portfolio based on inputs of historical/expected returns and standard deviations. ie, given expected returns/deviations for 4 asset classes the Mean Variance method will calculate the optimal portfolio combination of the 4 assets to yield the best risk/return trade-off. Benefits - easy/cheap to implement and understand, only 1 output given.Negatives - requires a large amount of estimated input data, static approach (one iteration), canresult in concentrations due to the way the optimization works.Resampled Mean Variance: basically runs a bunch of Mean Variance optimizations based on different assumptions and averages the results to get an optimizes portfolio.Benefits - more optimizations result in better diversification and a more stable efficient frontier. Negatives - no mathematical rationale behind doing this method, still a static approach, relies on estimates.Black-Litterman: Starts with the market portfolio and backs out the expected returns, risk premiums, covariances, etc implied by market prices, assuming market equilibrium. From there a Mean-Variance optimization is run using those inputs to generate an efficient frontier.Benefits - high level of diversification, overcomes weakness of MV which is the variability of estimated returns.Negatives - static approach, difficult to estimate returns.Monte Carlo Simulation: Computer generated iterative process that incorporates different input variables (contributions/withdrawals, taxes, capital market factors, etc) to generate a range of possible outcomes.Benefits - multiple output = not a static approach, incorporates compounding and other relevant information, generates a distribution of returns instead of a single prediction.Negatives - complex and expensive to generate, still relies on the accuracy of input data. Microperformance Attribution:Pure Sector Allocation: (Wp - Wb)*(Rbj - Rb) - did the manager underweight underperforming sectors and overweight outperforming sectors. So you compare his weightings to the benchmarks and then compare the sector return in the benchmark to the overall return of the benchmark.Security Selection: Wb*(Rp - Rb) - Ignoring differences in weightings, did the manager do a better job at picking securities with each sector than if he replicated the sector securities from the benchmark. Allocation Selection: (Wp - Wb)*(Rp - Rb) - interaction of the prior two, did the manger overweightthe sectors where he was a better stock picker and underweight those where he wasn't.1. the question usually sets out a table showing the corner portfolios in order - usually starting from the highest risk/reward at the top - so it's easy to pick the right section (between 2 corners) that meets the return and risk objectives CORNER PORTFOLIOS2. when it comes to interpolating the point on the straight line between the 2 selected corners - the trick is in the exact wording of the targets in the IPS:- if the IPS sets a MINIMUM return goal (eg "at least 10%") and a fixed risk goal (eg "10% st.dev" or variance) then start with the stated RISK target and interpolate the portfolio return.- but if the IPS sets a single return goal (eg "10%") and a MAXIMUM risk goal (eg "no more than 10% st.dev") - then start with the stated RETURN target and interpolate the portfolio risk.3. only use lend/invest along the capital allocation line if the table has a risk-free asset in it, and there are other hints - eg if the IPS says that the investor considers the Sharpe ratio to be a primary measure. In that case - pick the portfolio with the higest sharpe, then lend (invest) at the RFR (which will be given) to move down to the target return or risk goal - then interpolate the risk and return in the total portfolio. This will be more efficient than any corner or straight section.Interest Rate Calls:In 40 days, a firm plans to borrow $5 million for 180 days.The borrowing rate is LIBOR plus 300 b.p.Current LIBOR is 5%.The firm buys a call that matures in 40 days with a NP of $5 million, 180 days in underlying (D = 180), and a strike rate of 4.5%. The call premium is $8,000.Calculate the effective annual rate on the loan if at expiration LIBOR = 5%Net loan amount= 5MM – 8M(1 + (0.08 * 40/360))= 4,991,929Call Payoff= 5MM(0.05 - 0.045) (180/360) = $12,500Dollar Cost of Loan=5MM * 0.08 * (180/360) – 12,500 = $187,500Effective Annual Rate= ($5,187,500 / $4,991,929)^(365/180) -1= 0.081043 or 8.1%Reading 48, question 5: Global Performance Attributiona) Calculate Local and Base (USD) portfolio returnsStep 1: Calculate the weight of each country component within the portfolio=(US Dollar value of each country as of 2006) / SUM(Total US Dollar value of portfolio as of 2006) Step 2: Calculate the portfolio returns in local currency for each country=(2007 portfolio value in local currency)/(2006 portfolio value in local currency)-1Step 3: Calculate the portfolio returns in USD for each countryFirst, convert the 2006 and 2007 Sterling and Euro portfolio values into USD using the 2006 and 2007 exchange rates. Then, apply the same concept as Step 3.=(2007 portfolio value in US Dollar)/(2006 portfolio value in US Dollar)-1Step 4: Calculate the total portfolio return in US Dollar and local currency=SUM(portfolio return in local currency * portfolio weight)and=SUM(portfolio return in US Dollar * portfolio weight)Are we good so far? Excellent, let's continue!b) Decompose the portfolio return into local currency capital gains and currency returnsThe objective here is to determine what portion of the portfolio's return came from capital gains in local currency and what portion of the portfolio's return came from currency returns.For example, you could buy a stock in Yen that drops in value, but the Yen itself could gain, which in theory could actually leave you with a gain depending on the difference between the loss on on the stock and gain on the Yen.We've actually already calculated the local currency capital gains in part A, step 2.Now, we have to calculate the currency returns for each country:=(local return - US Dollar return)***Note that this is where I begin to disagree with their mathematics. They are assuming that the local return and currency return can just be added together to get the US Dollar return, which isn't strictly true - ideally, you'd want to use this formula:(1 + local return) * (1 + currency return) - 1 = US Dollar returnbut their method is a reasonable (and simpler) approximation, although not entirely correct.End rant #1***Next, we need to calculate the total portfolio level currency return:=SUM(currency return * portfolio weight)c) Decompose the portfolio total return into the market, security selection and currency components. This is contribution. It is NOT relative to a benchmark, since it is decomposing the sources of the portfolio return.In this question, we're trying to explain the sources of the total return of the portfolio.***This is where it starts to get a bit murky due to the poor wording of the CFA material. I also think they're combining "contribution" (sources of TOTAL return) with "attribution" (sources of ACTIVE return) due to the inclusion of the selection component.End rant #2***So we need to find the following:Market ComponentSecurity Selection ComponentCurrency ComponentPortfolio Total Return = Market + Selection + CurrencyWe already found the Currency Component in part B.Market Component:=SUM(Index local return * portfolio weight)Security Selection Component:=SUM[(Portfolio local return - Index local return) * portfolio weight]。

cfa3级考纲

cfa3级考纲CFA Level 3考纲概述CFA(Chartered Financial Analyst)是全球金融领域最具权威的专业资格认证,分为三个级别。

CFA Level 3是CFA考试的第三阶段,也是取得 CFA 特许资格的最后一步。

这一级别的考试侧重于投资管理,要求考生具备扎实的理论基础和丰富的实践经验。

CFA Level 3考纲为考生提供了备考的指导方向。

考纲的主要内容CFA Level 3考纲涵盖了投资管理领域的核心知识,主要包括以下几个方面:1.资产估值:包括资产定价模型、企业金融、衍生工具、另类投资等方面的内容,要求考生熟练掌握各类资产的估值方法。

2.投资策略:涉及股票投资、债券投资、多元资产投资、绝对回报投资等策略,考生需要了解各种投资策略的特点和适用场景。

3.组合管理:这部分内容包括组合构建、风险管理、业绩评估等方面,考生需要具备组合管理的基本能力。

4.财富管理与合规:包括个人财富管理、机构投资者、合规与道德等方面,考生需要了解财富管理行业的相关法规和道德规范。

5.宏观经济与投资:涉及全球宏观经济分析、货币政策、地缘政治等因素对投资的影响,考生需要具备分析宏观经济环境的能力。

考纲的难度和重要性CFA Level 3考纲的难度较高,对考生的理论知识和实践经验都有较高的要求。

在备考过程中,考生需要花费大量时间和精力来学习和掌握考纲中的内容。

然而,通过C FA Level 3考试并取得CFA特许资格,将为考生在金融行业,尤其是投资管理领域带来巨大的职业发展机会。

因此,尽管考纲难度较大,但对于志在投资管理行业的专业人士来说,CFA Level 3考纲的重要性不言而喻。

总之,CFA Level 3考纲为考生提供了备考的指导方向,涵盖了投资管理领域的核心知识。

考生需要充分了解考纲的内容,并付出努力和时间来学习和掌握。

cfa三级必背知识点2023

cfa三级必背知识点2023【实用版】目录1.CFA 三级考试概述2.必背知识点分类3.权益投资4.固定收益投资5.衍生工具与另类投资6.投资组合管理与风险控制7.财务报表分析与企业估值8.2023 年 CFA 三级考试时间与备考建议正文【CFA 三级考试概述】CFA(Chartered Financial Analyst)是全球金融领域最具权威的专业资格认证,分为三个级别。

CFA 三级考试主要测试考生在投资管理方面的专业知识和应用能力。

通过三级考试,考生将获得 CFA 特许金融分析师的称号,具备在全球范围内从事投资管理、财务分析等职业的资格。

【必背知识点分类】CFA 三级考试涵盖了投资工具、公司金融、投资组合管理、财务报表分析等多个领域。

对于 2023 年的考生来说,以下几个方面的知识点是必须掌握的:1.权益投资:包括股票投资策略、股票估值方法等。

2.固定收益投资:包括债券投资策略、债券估值方法等。

3.衍生工具与另类投资:包括期货、期权、互换等衍生工具的投资策略,以及房地产、私募股权等另类投资的基本知识。

4.投资组合管理与风险控制:包括投资组合的构建、优化、风险衡量和控制等。

5.财务报表分析与企业估值:包括财务报表的解读、财务比率分析、企业价值评估等。

【权益投资】权益投资是 CFA 三级考试的重点之一,主要涉及股票投资策略和股票估值方法。

考生需要掌握的股票投资策略包括价值投资、成长投资、指数投资等;股票估值方法包括市盈率、市净率、股息贴现模型等。

【固定收益投资】固定收益投资是另一个重要领域,主要涉及债券投资策略和债券估值方法。

考生需要掌握的债券投资策略包括利率预测、信用评级、债券久期等;债券估值方法包括到期收益率、息票收益率、折扣率等。

【衍生工具与另类投资】衍生工具与另类投资是一个相对复杂的领域,主要涉及期货、期权、互换等衍生工具的投资策略,以及房地产、私募股权等另类投资的基本知识。

考生需要掌握衍生工具的基本原理、交易策略和风险管理;另类投资领域的基本知识,包括投资策略、风险控制等。

cfa三级课后题2023

cfa三级课后题2023CFA(Chartered Financial Analyst)是国际上最具权威性的金融分析师资格认证之一,分为三个级别,其中三级是最高级别。

CFA三级课后题是考生在备考过程中进行练习和巩固知识的重要环节。

本文将针对CFA三级课后题2023进行分析和解答,帮助考生更好地理解和掌握相关知识。

一、题目一题目描述:根据给定的财务数据,计算公司的净利润率、总资产周转率和权益乘数,并分析其财务状况。

解答:根据题目要求,我们需要计算公司的净利润率、总资产周转率和权益乘数,并对其财务状况进行分析。

1. 净利润率的计算公式为:净利润率 = 净利润 / 营业收入。

净利润率反映了公司每一单位销售收入所获得的净利润。

2. 总资产周转率的计算公式为:总资产周转率 = 营业收入 / 总资产。

总资产周转率反映了公司每一单位总资产所创造的销售收入。

3. 权益乘数的计算公式为:权益乘数 = 总资产 / 股东权益。

权益乘数反映了公司每一单位股东权益所支持的总资产规模。

通过计算得到的净利润率、总资产周转率和权益乘数,我们可以对公司的财务状况进行分析。

净利润率高表示公司每一单位销售收入所获得的净利润较多,说明公司的盈利能力较强;总资产周转率高表示公司每一单位总资产所创造的销售收入较多,说明公司的资产利用效率较高;权益乘数高表示公司每一单位股东权益所支持的总资产规模较大,说明公司的财务杠杆效应较强。

综上所述,通过计算和分析净利润率、总资产周转率和权益乘数,我们可以全面了解公司的财务状况,为投资决策提供参考依据。

二、题目二题目描述:根据给定的投资组合信息,计算组合的预期收益率、标准差和夏普比率,并分析其风险收益特征。

解答:根据题目要求,我们需要根据给定的投资组合信息,计算组合的预期收益率、标准差和夏普比率,并对其风险收益特征进行分析。

1. 预期收益率的计算公式为:预期收益率= ∑(投资比例 ×预期收益率)。

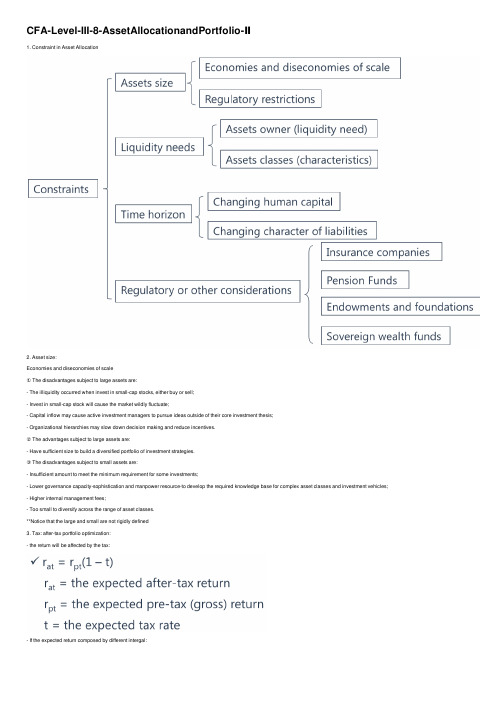

CFA-Level-III-8-AssetAllocationandPortfolio-Ⅱ

CFA-Level-III-8-AssetAllocationandPortfolio-Ⅱ1. Constraint in Asset Allocation2. Asset size:Economies and diseconomies of scale① The disadvantages subject to large assets are:- The illiquidity occurred when invest in small-cap stocks, either buy or sell;- Invest in small-cap stock will cause the market wildly fluctuate;- Capital inflow may cause active investment managers to pursue ideas outside of their core investment thesis;- Organizational hierarchies may slow down decision making and reduce incentives.② The advantages subject to large assets are:- Have sufficient size to build a diversified portfolio of investment strategies.③ The disadvantages subject to small assets are:- Insufficient amount to meet the minimum requirement for some investments;- Lower governance capacity-sophistication and manpower resource-to develop the required knowledge base for complex asset classes and investment vehicles; - Higher internal management fees;- Too small to diversify across the range of asset classes.**Notice that the large and small are not rigidly defined3. Tax: after-tax portfolio optimization:- the return will be affected by the tax:- If the expected return composed by different intergal:- As the tax and tax loss carry forward exist, the expected volatility of will be reduced as well.- As the expected return and after-tax standard deviation differ from the original data, the optimal portfolio would change as well- In another words, the rebalancing ranges for a taxable portfolio can be wider than those of a tax-exempt portfolio with a similar risk profile:* 由于税的存在使得range可以更宽,因为有税的影响在其中。

cfa三级原版书课后题讲解

cfa三级原版书课后题讲解(实用版)目录1.CFA 三级原版书概述2.CFA 三级原版书课后题的重要性3.如何高效利用课后题4.原版书课后题讲解的资源推荐正文CFA(Chartered Financial Analyst)是全球金融领域最具权威的专业资格认证,分为三个级别。

CFA 三级原版书是 CFA 三级考试的重要参考资料,其课后题对于考生掌握知识点、巩固理论体系和提高解题能力具有重要意义。

本文将介绍 CFA 三级原版书课后题的重要性,并提供一些建议和资源,帮助考生高效利用课后题。

首先,CFA 三级原版书课后题是对所学知识的巩固和拓展。

通过解答课后题,考生可以加深对知识点的理解,提高自己的分析能力和解决问题的能力。

同时,课后题涵盖了各个科目的重点内容,有助于考生梳理知识体系,发现自己的薄弱环节,进行有针对性的复习。

其次,CFA 三级原版书课后题可以提高考生的解题速度和准确率。

在实际考试中,时间有限,考生需要在规定时间内完成大量的题目。

课后题的练习可以让考生熟悉题型,掌握解题技巧,从而在考试中迅速找到解题思路,提高解题效率。

那么,如何高效利用课后题呢?1.结合教材和课堂笔记解答课后题。

在解答课后题时,考生可以回顾相关知识点,巩固课堂所学。

如果遇到不理解的地方,可以查阅教材或向老师请教。

2.制定学习计划,合理安排时间。

考生可以根据自己的学习进度,制定学习计划,每天解答一定数量的课后题。

这样既可以保证学习效果,又可以避免因为题目过多而产生挫败感。

3.分析错误,总结经验。

在解答课后题的过程中,考生可能会犯错误。

这时候,考生需要认真分析错误原因,总结经验教训,避免重复犯错。

4.参加学习小组或讨论组。

考生可以和其他考生一起讨论课后题,分享解题方法和经验,相互学习,共同进步。

最后,原版书课后题讲解的资源推荐如下:1.CFA 官方网站提供课后题答案解析,考生可以登录官方网站查看。

2.在线课程和培训机构也会提供课后题讲解,考生可以根据自己的需求选择合适的资源。

CFA三级行为金融学重难点解析

三级行为金融学重难点解析:个人行为偏差在行为金融学中,区分各类不同个人行为偏差是考试的重点,对于这些偏差的学习,要在理解的基础上,知道这些偏差对投资决策的影响以及弥补的办法。

在本文中,我们将逐个介绍各个行为偏差。

个人行为偏差可分为两类:1. 认知错误(cognitive errors):由于投资者在信息的接收、处理过程中出现的偏差.a)信任忠诚偏差(belief perseverance bias):信念忠诚是指人们一旦形成某一信念和判断以后,人们就会表现出对它的忠诚和信任,从而不再关注其他相关的信息,比如,一旦一个公司认为某个投资项目比其他项目利润丰厚这个信念之后,该信念就会在一定的时间内一定程度上左右着该公司的决策和判断,从而暂时屏蔽了其他有关该投资项目利润发展变化方面的信息.i. 保守偏差(conservation bias):。

投资者不能及时根据变化了的情况修正自己的预测模型,错误地对价格变化外推,导致股价过度反应(over—reaction).ii. 确认偏差(confirmation bias):投资者会过分地关注那些能支持自己结论的信息而忽视那些不支持自己结论的信息。

iii。

代表性偏差(Representativeness bias):人们会根据过去的传统和相似的情况,对事件分类,在判断概率时会根据经验判断事件的概率而忽略其他的因素。

其缺陷在于过分强调将事物划分的典型类别,而不关注潜在的其它可能证据。

例如,由于“代表性偏差"的存在使投资者对过去的输者组合表现出过度悲观,而对赢者组合过度乐观.iv. 控制错觉偏差(illusion of control bias):投资者认为他们能控制市场,而实际上不能。

v。

后市偏差(hindsight bias):在一件事情发生以后,人们往往会夸大自己的信念,这就是事后聪明偏差。

比如,某政治家当选以后,很多人会说这早就在他们的预料之中.事后聪明偏差的产生主要是由于人们对有关某事件发生与否的信息不充分.在该事件发生以后,当事人很简单地就将这些有限的信息与最终的结局相联系。

cfa三级框架

cfa三级框架CFA三级框架CFA(Chartered Financial Analyst)是国际上最具权威性和专业性的金融学考试之一,被广泛认可为全球金融从业人员的职业资格。

CFA三级考试是CFA考试中的最后一关,被认为是最具挑战性的一级。

本文将围绕CFA三级框架展开讨论,介绍其内容和考试要点。

一、CFA三级考试的框架CFA三级考试的框架包括三个主要部分,分别是资产估值和分析、投资工具和资金组合管理。

这三个部分涵盖了金融学的核心知识和实践技能,为考生提供了全面的金融投资知识体系。

1. 资产估值和分析资产估值和分析是CFA三级考试的第一部分,也是整个考试的基础。

在这一部分,考生需要掌握公司财务报表分析、财务报表分析和估值、估值模型和技术、资产定价模型以及公司综合估值等内容。

考生需要了解不同估值模型的特点和适用范围,能够运用这些模型对公司进行估值,为投资决策提供依据。

2. 投资工具投资工具是CFA三级考试的第二部分,主要介绍各种金融工具和投资策略。

考生需要了解各类金融工具的特点、优势和风险,并能够分析其适用性和投资组合构建方法。

此外,还需要掌握不同投资策略的原理和实施方法,以及如何评估和优化投资组合。

3. 资金组合管理资金组合管理是CFA三级考试的最后一部分,也是考生实践能力的体现。

在这一部分,考生需要学习资金组合理论、资产配置、绩效评估和风险管理等内容。

考生需要了解不同的资产配置方法和风险管理工具,能够根据投资目标和风险偏好制定合理的资产配置策略,并能够对投资组合进行绩效评估和风险控制。

二、CFA三级考试的要点1. 理解概念和原理CFA三级考试注重对金融学概念和原理的理解。

考生需要掌握各种金融工具的特点、原理和使用方法,理解投资组合理论和资产定价模型的基本原理,能够运用这些理论和模型解决实际问题。

2. 掌握分析和计算方法CFA三级考试中有很多与财务报表分析、估值和投资组合分析相关的计算题。

考生需要熟悉这些计算方法,掌握各种估值模型的计算步骤和公式,能够准确地进行计算和分析。

2021cfa三级考点

2021cfa三级考点摘要:I.前言- 介绍CFA 三级考试的重要性- 说明本文的主要内容II.2021 年CFA 三级考点的变化- 概述2021 年CFA 三级考试的主要变化- 分析变化的原因和影响III.2021 年CFA 三级考试的主要考点- 详细介绍2021 年CFA 三级考试的各个考点- 分析各考点的难度和重要性IV.如何应对2021 年CFA 三级考试的变化- 提供应对考试变化的策略和建议- 强调考生应该如何调整备考计划V.结论- 总结2021 年CFA 三级考试的主要考点和变化- 鼓励考生积极应对挑战,取得好成绩正文:CFA 三级考试是CFA 认证考试的最后一级,对于金融从业者来说具有重要意义。

本文将详细介绍2021 年CFA 三级考试的主要考点和变化,并提供应对策略和建议。

2021 年CFA 三级考试相较于往年发生了一些变化。

这些变化主要体现在考点的调整和考试内容的更新上。

为了适应行业的发展和需求,CFA 协会对三级考试的内容进行了相应的调整,以保证考生具备最新的知识和技能。

2021 年CFA 三级考试的主要考点包括:1.投资组合管理- 资产配置- 风险管理- 业绩评估2.财富管理- 客户需求分析- 投资建议- 财富传承3.合规与伦理- 法规遵循- 职业伦理- 内部控制4.风险管理- 市场风险- 信用风险- 操作风险5.衍生品与另类投资- 衍生品市场- 另类投资- 风险管理策略这些考点在三级考试中占据了较大的比重,考生需要重点关注。

为了应对2021 年CFA 三级考试的变化,考生应该:1.及时了解考试信息:关注CFA 协会官方网站,了解最新的考试动态和考点变化。

2.调整备考计划:针对新的考点,制定合适的备考计划,确保每个考点都得到充分的复习。

3.参加模拟考试:通过模拟考试,检验自己的备考进度和效果,及时调整学习方法。

4.加强实际操作能力:除了理论知识外,还要关注实际操作能力的培养,以提高自己在实际工作中的应用能力。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Reading 16: Linking Pension Liabilities to Assets The candidate should be able to: a. contrast the assumptions concerning pension liability risk in asset-only and liability-relative approaches to asset allocation; b. discuss the fundamental and economic exposures of pension liabilities and identify asset types that mimic these liability exposures; c. compare pension portfolios built from a traditional asset-only perspective to portfolios designed relative to liabilities and discuss why corporations may choose not to implement fully the liability mimicking portfolio. Reading 17: Allocating Shareholder Capital to Pension Plans The candidate should be able to: a. compare funding shortfall and asset/liability mismatch as sources of risk faced by pension plan sponsors; b. explain how the weighted average cost of capital for a corporation can be adjusted to incorporate pension risk and discuss the potential consequences of not making this adjustment; c. explain, in an expanded balance sheet framework, the effects of different pension asset allocations on total asset betas, the equity capital needed to maintain equity beta at a desired level, and the debt-to-equity ratio.

高顿财经:

高顿网校: |

CopyRight © 版权所有,如有疑问,请致电或访问网 站

1

பைடு நூலகம்