Chapter 9 A Survey of Utility-based Privacy-Preserving Data Transformation Methods

SOM Chapter 9

CHAPTER 9: STRATEGIC ALLIANCESTRUE/FALSE QUESTIONS1. Currently alliances account for 35% of the revenue of the largest 1,000 firms in theUnited States.TrueFalseAnswer: True Page: 278 Difficulty: Easy Chapter Objective: 12. A strategic alliance exists whenever three or more independent organizationscooperate in the development, manufacture, or sale of products or services.TrueFalseAnswer: False Page: 278 Difficulty: Easy Chapter Objective: 13. In a nonequity alliance firms create a legally independent firm in which they investand from which they share any profits that are created.TrueFalseAnswer: False Page: 278 Difficulty: Moderate Chapter Objective: 14. In an equity alliance cooperating firms supplement contracts with equity holdingsan alliance partners.TrueFalseAnswer: True Page: 278 Difficulty: Moderate Chapter Objective: 15. When a firm cannot realize the cost savings from economies of scale all by itself, itmay join in a strategic alliance with other firms so that together, both firms willhave sufficient volume to be able to gain the cost advantages of economies ofscale.TrueFalseAnswer: True Page: 280 Difficulty: Moderate Chapter Objective: 26. In general, due to the intangible nature of knowledge, firms are not able to usealliances to learn from their competitors.TrueFalseAnswer: False Page: 280 Difficulty: Moderate Chapter Objective: 27. When both parties to an alliance are seeking to learn something from that alliance,a learning race can evolve.TrueFalseAnswer: True Page: 281 Difficulty: Moderate Chapter Objective: 28. Network industries are characterized by decreasing returns to scale.TrueFalseAnswer: False Page: 281 Difficulty: Moderate Chapter Objective: 29. Firms with high levels of absorptive capacity will learn at higher rates than firmswith low levels of absorptive capacity, even if these two firms are trying to learn exactly the same things in an alliance.TrueFalseAnswer: True Page: 283 Difficulty: Moderate Chapter Objective: 210. Learning race dynamics are particularly common in relations among large, well-established firms.TrueFalseAnswer: False Page: 283 Difficulty: Moderate Chapter Objective: 211. In network industries with increasing returns to scale where standards areunimportant, strategic alliances can be used to create a more favorable competitive environment.TrueFalseAnswer: False Page: 283 Difficulty: Hard Chapter Objective: 212. Explicit collusion exists when firms directly communicate with each other tocoordinate their levels of production or their prices and is legal in most countries.TrueFalseAnswer: False Page: 285 Difficulty: Moderate Chapter Objective: 213. Tacit collusion exists when firms coordinate their pricing decisions not by directlycommunicating with each other, but by exchanging signals with other firms about their intent to cooperate.TrueFalseAnswer: True Page: 285 Difficulty: Moderate Chapter Objective: 214. Strategic alliances can help create the social setting within which tacit collusionmay develop.TrueFalseAnswer: True Page: 285 Difficulty: Moderate Chapter Objective: 215. Research shows that joint ventures between firms in the same industry may havecollusive implications and that these kinds of joint ventures are relatively common.TrueFalseAnswer: False Page: 286 Difficulty: Moderate Chapter Objective: 216. Alliances to facilitate entry into new industries are only valuable when the skillsneeded in these industries are complex and difficult to learn.TrueFalseAnswer: False Page: 286 Difficulty: Moderate Chapter Objective: 217. When information asymmetry exists between firms that currently own assets andfirms that may want to purchase these assets, the selling firm will often havedifficultly obtaining the full economic value of these assets.TrueFalseAnswer: True Page: 287 Difficulty: Moderate Chapter Objective: 218. In new and uncertain environments it is not unusual for firms to develop numerousstrategic alliances.TrueFalseAnswer: True Page: 288 Difficulty: Moderate Chapter Objective: 219. Research shows that as many as two-thirds of strategic alliances do not meet theexpectations of at least one alliance partner.TrueFalseAnswer: False Page: 288 Difficulty: Moderate Chapter Objective: 320. When potential cooperative partners misrepresent the skills, abilities, and otherresources that they will bring to an alliance, this is a form of cheating known asadverse selection.TrueFalseAnswer: True Page: 288 Difficulty: Moderate Chapter Objective: 321. In general, the less tangible the resources and capabilities that are to be brought to astrategic alliance, the less costly it will be to estimate their value before an alliance is created, and the more likely it is that adverse selection will occur.TrueFalseAnswer: False Page: 289 Difficulty: Moderate Chapter Objective: 322. Moral hazard occurs when partners in an alliance possess high-quality resourcesand capabilities of significant value in an alliance but fail to make those resources and capabilities available to alliance partners.TrueFalseAnswer: True Page: 289 Difficulty: Moderate Chapter Objective: 323. The existence of moral hazard in a strategic alliance proves that at least one of theparties is either malicious or dishonest.TrueFalseAnswer: False Page: 289 Difficulty: Moderate Chapter Objective: 324. In an alliance a holdup occurs when a firm that has not made significanttransaction-specific investments demands returns from an alliance that are higher than what the partners agreed to when they created the alliance.TrueFalseAnswer: True Page: 291 Difficulty: Moderate Chapter Objective: 325. Research on international joint ventures suggests that the existence of transaction-specific investments in their relationships makes these agreements relativelyimmune to holdup problems.TrueFalseAnswer: False Page: 291 Difficulty: Moderate Chapter Objective: 326. Although holdup is a form of cheating in strategic alliances, the threat of holdupcan also be a motivation for creating an alliance.TrueFalseAnswer: True Page: 292 Difficulty: Moderate Chapter Objective: 327. For a strategic alliance to be a source of sustained competitive advantage it must bevaluable in that it exploits an opportunity but avoids a threat and it must also berare and costly to imitate.TrueFalseAnswer: True Page: 292 Difficulty: Easy Chapter Objective: 428. The rarity of strategic alliances depends solely on the number of competing firmsthat have already implemented an alliance.TrueFalseAnswer: False Page: 292 Difficulty: Easy Chapter Objective: 429. In the short-run firms can gain some advantages by cheating their alliance partnersbut research suggests that cheating does not pay in the long run.TrueFalseAnswer: True Page: 293 Difficulty: Moderate Chapter Objective: 330. Successful strategic alliances are often based on socially complex relations amongalliance partners but virtually every firm in a given industry is likely to have the organizational and relationship-building skills required for alliance buildingmaking the possibility of direct duplication of strategic alliances very high.TrueFalseAnswer: False Page: 294 Difficulty: Moderate Chapter Objective: 431. In general, firms will prefer to go it alone rather than enter into a strategic alliancewhen the level of transaction-specific investment required to complete an exchange is low.TrueFalseAnswer: True Page: 295 Difficulty: Hard Chapter Objective: 532. Capabilities theory suggests that an alliance will be preferred over “going it alone”when an exchange partner possesses valuable, rare, and costly-to-imitate resources and capabilities.TrueFalseAnswer: True Page: 295 Difficulty: Moderate Chapter Objective: 533. When there is low uncertainty about the future value of an exchange, an alliancewill be preferred to going it alone.TrueFalseAnswer: False Page: 295 Difficulty: Moderate Chapter Objective: 534. Transaction cost economics suggests that going it alone is not a substitute forstrategic alliances since they are best chosen only when other alternatives are not viable.TrueFalseAnswer: True Page: 295 Difficulty: Moderate Chapter Objective: 535. An alliance will be preferred to an acquisition when there are legal constraints onacquisitions.TrueFalseAnswer: True Page: 296 Difficulty: Easy Chapter Objective: 536. The primary purpose of organizing a strategic alliance is to enable partners in thealliance to gain all the benefits associated with cooperation while minimizing the probability that cooperating firms will cheat on their cooperative agreements.TrueFalseAnswer: True Page: 297 Difficulty: Moderate Chapter Objective: 637. In general, contracts are sufficient to resolve all the problems associated withcheating in an alliance.TrueFalseAnswer: False Page: 298 Difficulty: Moderate Chapter Objective: 6 38. Sometimes the value of cheating in a joint venture is sufficiently large that a firmcheats even though doing so hurts the joint venture and forecloses futureopportunities.TrueFalseAnswer: True Page: 302 Difficulty: Moderate Chapter Objective: 639. While it is often the case that there will be important information asymmetriesbetween firms in an alliances these asymmetries are likely to be much less whenalliance partners come from different countries.TrueFalseAnswer: False Page: 303 Difficulty: Moderate Chapter Objective: 740. When firms begin to explore international operations they tend to do so first byengaging in alliances, then in market-based forms of exchange followed by equity investments and vertical integration if it makes economic sense to do so.TrueFalseAnswer: False Page: 304 Difficulty: Moderate Chapter Objective: 7 MULTIPLE CHOICE QUESTIONS41. Currently alliances account for _______ percent of the revenue of the largest 1,000firms in the United States.A. 15B. 25C. 35D. 45Answer: C Page: 278Difficulty: Moderate Chapter Objective: 142. A(n) _________ exists whenever two or more independent organizations cooperatein the development, manufacture, or sale of products or services.A. vertical marketB. strategic allianceC. initial public offeringD. market transactionAnswer: B Page: 278Difficulty: Moderate Chapter Objective: 143. A ________ is a form of nonequity alliance that exists when one firm allowsanother to use its brand name to sell its products.A. supply agreementB. distribution agreementC. licensing agreementD. joint ventureAnswer: C Page: 278Difficulty: Moderate Chapter Objective: 144. In a ___________ cooperating firms create a legally independent firm in whichthey invest and from which they share any profits that are created.A. licensing agreementB. supply agreementC. distribution agreementD. joint ventureAnswer: D Page: 279Difficulty: Moderate Chapter Objective: 145. Strategic alliances can create economic value through helping firms improve theircurrent operations byA. facilitating the development of technology standards.B. facilitating tacit collusion.C. exploiting economies of scale.D. managing uncertainty.Answer: C Page: 280Difficulty: Moderate Chapter Objective: 246. When both parties to an alliance are seeking to learn something from that alliance,a ________ can evolve.A. learning raceB. dynamic raceC. learning dynamicD. learning curveAnswer: A Page: 281Difficulty: Moderate Chapter Objective: 247. Network industries are characterized byA. increasing diseconomies of scale.B. increasing returns to scale.C. decreasing returns to scale.D. decreasing economies of scale.Answer: B Page: 281Difficulty: Moderate Chapter Objective: 248. A firm's ability to learn is known as itsA. competitive position.B. competitive advantage.C. distinctive competence.D. absorptive capacity.Answer: D Page: 283Difficulty: Moderate Chapter Objective: 249. In one study almost ______ percent of the managers in entrepreneurial firms feltunfairly exploited by their large-firm alliance partners.A. 80B. 20C. 50D. 10Answer: A Page: 283Difficulty: Hard Chapter Objective: 250. ________ exists when firms directly communicate with each other to coordinatetheir levels of production and/or their prices.A. Economies of scaleB. Explicit collusionC. A learning raceD. Tacit collusionAnswer: B Page: 285Difficulty: Moderate Chapter Objective: 251. _________ exists when firms coordinate their production and pricing decisions, notby directly communicating with each other, but by exchanging signals with other firms about their intent to cooperate.A. Economies of scaleB. Explicit collusionC. A learning raceD. Tacit collusionAnswer: D Page: 285Difficulty: Moderate Chapter Objective: 252. Strategic alliances are particularly valuable in facilitating market entry and exitwhen the value of market entry or exit isA. high.B. low.C. moderate.D. uncertain.Answer: D Page: 285Difficulty: Moderate Chapter Objective: 253. Although joint ventures between firms in the same industry _________ collusiveimplications, research has shown that these kinds of joint ventures are ________.A. may have; relatively rareB. are not likely to have; relatively rareC. may have; relatively commonD. are not likely to have; relatively commonAnswer: A Page: 286Difficulty: Hard Chapter Objective: 254. As long as the cost of _________ to enter a new industry less than the cost of_________, an alliance can be a valuable strategic opportunity.A. vertically integrating; learning new skills and capabilitiesB. learning new skills and capabilities; using an allianceC. using an alliance; learning new skills and capabilitiesD. learning new skills and capabilities; vertically integratingAnswer: C Page:286Difficulty: Moderate Chapter Objective: 2 55. Consistent with a real options perspective, firms in new and uncertainenvironments are likely toA. avoid using strategic alliances.B. develop numerous strategic alliances.C. develop few strategic alliances.D. engage in vertical integration.Answer: B Page: 288Difficulty: Moderate Chapter Objective: 256. Research shows that as many as ________ of all strategic alliances do not meet theexpectations of at least one alliance partner.A. one-thirdB. five-eighthsC. one-halfD. two-thirdsAnswer: A Page: 288Difficulty: Moderate Chapter Objective: 357. If TeleCo was to enter into a strategic alliance with a partner that promised it coulddeliver a high quality wireless infrastructure, when in fact the potential partner had neither the skills or abilities to provide this infrastructure, TeleCo could be said to be impacted byA. moral hazard.B. adverse selection.C. holdup.D. tacit collusion.Answer: B Page: 288Difficulty: Moderate Chapter Objective: 358. Adverse selection in a strategic alliance is likely only whenA. it is difficult or costly to observe the resources or capabilities that a partner bringsto an alliance.B. a potential partner can easily see the resources and capabilities that a firm isbringing to an alliance.C. it is difficult or costly to know how competitors will react to the strategic alliance.D. there are significant transaction-specific assets devoted to the alliance.Answer: A Page: 289Difficulty: Moderate Chapter Objective: 359. In general, the ________ tangible the resources and capabilities that are to bebrought to a strategy alliance, the ______ costly it will be to estimate their value before an alliance is created, and the ________ likely it is that adverse selectionwill occur.A. more; more; moreB. less; more; lessC. less; more; moreD. more; more; lessAnswer: C Page: 289Difficulty: Hard Chapter Objective: 360. _________ occurs when partners in an alliance possess high-quality resources andcapabilities of significant value in an alliance, but fail to make those resources and capabilities available to alliance partners.A. Moral hazardB. Adverse selectionC. HoldupD. Explicit collusionAnswer: A Page: 289Difficulty: Moderate Chapter Objective: 361. Often both parties in a failed alliance accuse each other ofA. adverse selection.B. tacit collusion.C. moral hazard.D. holdup.Answer: C Page: 289Difficulty: Moderate Chapter Objective: 362. When one firm makes more transaction-specific investments in a strategic alliancethan partner firms make, that firm may be subject to a form of cheating called_______ that occurs when a firm that has not made significant transaction-specific investments demands returns from an alliance that are higher than what the partners agreed to when they created the alliance.A. adverse selectionB. holdupC. moral hazardD. noncomplianceAnswer: B Page: 291Difficulty: Moderate Chapter Objective: 363. Research suggests that __________ are the type of alliance where existence oftransaction-specific investments often leads to holdup problemsA. licensing agreementsB. equity alliancesC. joint venturesD. distribution agreementsAnswer: C Page: 291Difficulty: Hard Chapter Objective: 364. The rarity of strategic alliancesA. depends solely on the number of competing firms that have already implementedan alliance.B. depends solely on whether or not the benefits that firms obtain from their alliancesare not common across firms in the industry.C. depend not only on the number of competing firms that have already implementedan alliance but also on whether or not the benefits that firms obtain from theiralliances are not common across competing firms in the industry.D. depends solely on the number of substitutes available for alliances.Answer: C Page: 292Difficulty: Moderate Chapter Objective: 465. One of the reasons why the benefits that accrue from a particular strategic alliancemay be rare is thatA. relatively few firms may have the complementary resources and abilities needed toform an alliance.B. there is a relatively large number of alliance partners available.C. relatively many firms may have the complementary resources and abilities neededto form an allianceD. there may be a relatively low amount of transaction-specific assets to enter intosimilar alliances.Answer: A Page: 294Difficulty: Moderate Chapter Objective: 466. Research indicates that the most common reason that alliances fail to meet theexpectations of partner firms isA. the lack of financial resources.B. the necessity of transaction-specific investments.C. the lack of transaction-specific investments.D. the partners’ inability to trust one another.Answer: D Page: 294Difficulty: Moderate Chapter Objective: 467. To the extent that a strategic alliance is based on ________ relations it will makethe alliances costly to imitate.A. socially complexB. tacit collusionC. explicit collusionD. moral hazardAnswer: A Page: 294Difficulty: Moderate Chapter Objective: 468. Two possible substitutes for strategic alliances includeA. going it alone and tacit collision.B. going it alone and acquisitions.C. acquisitions and explicit collusion.D. explicit collusion and tacit collusion.Answer: B Page: 294Difficulty: Moderate Chapter Objective: 569. Firms _________ when they attempt to develop all the resources and capabilitiesthey need to exploit market opportunities and neutralize market threats bythemselves.A. engage in tacit collusionB. form joint venturesC. go it aloneD. engage in explicit collusionAnswer: C Page: 295Difficulty: Moderate Chapter Objective: 570. Alliances will be preferred to going it alone whenA. the level of transaction-specific investments required to complete an exchange islow.B. there are no transaction-specific investments required to complete an exchange islow.C. when there is low uncertainty about the future value of an exchange.D. the level of transaction-specific investments required to complete an exchange ismoderate.Answer: D Page: 295Difficulty: Moderate Chapter Objective: 571. __________ theory suggests that under conditions of high uncertainty, firms maybe unwilling to commit to a particular course of action by engaging in an exchange with a firm and will choose, instead, the strategic flexibility associated withalliances.A. CapabilitiesB. Real optionsC. Transaction cost economicsD. Resource basedAnswer: B Page: 296Difficulty: Moderate Chapter Objective: 572. Alliances will be preferred to acquisitions whenA. alliances limit a firm's flexibility under conditions of high uncertainty.B. there is minimal unwanted organizational "baggage" in an acquired firm.C. there are legal constraints on acquisitions.D. the value of a firm's resources and capabilities does not depend on itsindependence.Answer: C Page: 296Difficulty: Moderate Chapter Objective: 573. An example of a contractual clause that deals with operating issues would be aA. noncompete clause.B. minority protection clause.C. put options clause.D. termination clause.Answer: A Page: 299Difficulty: Hard Chapter Objective: 674. All of the following are methods firms can use to reduce the threat of cheating instrategic alliances exceptA. contracts.B. equity investments.C. joint venturesD. tacit collusion.Answer: D Page: 300Difficulty: Moderate Chapter Objective: 675. Which of the following is a limitation of the reputational control of cheating in astrategic alliance?A. Subtle cheating in an alliance is likely to become public knowledge.B. Even if one firm is clearly cheating in an alliance, the other firm may not besufficiently tied into a network of firms to make this information public.C. The effect of a tarnished reputation forecloses future opportunities for a firm and ithelps reduce the current loses of the firm that was cheated.D. The reputation of the firm that was impacted by the cheating may be impacted assignificantly as the firm that committed the cheating.Answer: B Page: 301Difficulty: Moderate Chapter Objective: 676. When the probability of cheating in a cooperative relationship is greatest a(n)_________ is the preferred form of cooperation.A. equity agreementB. licensing agreementC. joint ventureD. distribution agreementAnswer: C Page: 301Difficulty: Moderate Chapter Objective: 677. ________ may enable partners to explore exchange opportunities that they couldnot explore if only legal and economic organizing mechanisms were in place.A. TrustB. Joint venturesC. Reputational effectsD. Equity investmentsAnswer: A Page: 302Difficulty: Moderate Chapter Objective: 678. While it is often the case that there will be important information asymmetriesbetween firms in an alliance, these asymmetries are likely to be ________ when alliances partners come from different countries.A. much lessB. about the same asC. much greaterD. marginally greaterAnswer: C Page: 303Difficulty: Moderate Chapter Objective: 779. As firms begin to explore international operations they generally begin to do so byA. using licensing agreements.B. importing or exporting.C. undertaking an equity investment.D. forming a joint venture.Answer: B Page: 304Difficulty: Moderate Chapter Objective: 780. The last step in exploiting international opportunities is oftenA. importing or exporting.B. forming a nonequity alliance.C. forming a joint venture.D. vertical integration in international operations.Answer: D Page: 304Difficulty: Moderate Chapter Objective: 7eBay the online auction company has an impressive portfolio of cooperative agreements. This portfolio includes an agreement with the U.S. Postal Service to facilitate the shipping of goods purchased through eBay auctions, an agreement to allow MBNA to use eBay's name on a credit card, an agreement in an online auction company in Korea that is supplemented with an investment by eBay in the Korean partner, and at one time eBay had formed an independent firm, called eBay Australia and New Zealand, with an Australian company known as ecorp.81. eBay's agreement with the U.S. Postal Service is most accurately classified as a(n)A. joint venture.B. equity agreement.C. licensing agreement.D. nonequity agreement.Answer: D Page: 278Difficulty: Moderate Chapter Objective: 182. eBay's agreement with MBNA is most accurately characterized as a(n)A. supply agreement.B. licensing agreement.C. equity alliance.D. joint venture.Answer: B Page: 278Difficulty: Moderate Chapter Objective: 183. eBay's agreement with the Korean online auction company is best characterized asa(n)A. licensing agreement.B. joint venture.C. equity alliance.D. distribution agreement.Answer: C Page: 278Difficulty: Moderate Chapter Objective: 184. eBay's former agreement with ecorp is best characterized as a(n)A. joint venture.B. equity alliance.C. licensing agreement.D. nonequity alliance.Answer: A Page: 279Difficulty: Moderate Chapter Objective: 185. If eBay's agreements with their Korean and Australian partners were intended toincrease the number of buyers and sellers and thereby increase the value of eBay's online auction services for every eBay user, this would imply that the onlineauction industry is an example of a _________ industry.A. decliningB. networkC. commodityD. matureAnswer: B Page: 281Difficulty: Moderate Chapter Objective: 286. If eBay entered the cooperative with its Australian partner for the purpose of testingthe attractiveness of the Australian and New Zealand auction industries prior tomaking a more significant investment in these industries, this would be an example ofA. transaction cost economics.B. tacit collusion.C. explicit collusion.D. real options.Answer: D Page: 287Difficulty: Hard Chapter Objective: 287. If, prior to entering the cooperative agreement with eBay, eBay's Korean partnerstated that it had the technological capabilities to facilitate eBay's Korean auction business when, in fact, the Korean company did not have these capabilities thiswould be an example ofA. adverse selection.B. explicit collusion.C. moral hazard.D. holdup.Answer: A Page: 288Difficulty: Moderate Chapter Objective: 388. If eBay's Australian partner agreed to provide marketing and technological skills tohelp eBay compete in the Australian and New Zealand auction industries butprovided skills that were significantly lower than promised this would be anexample ofA. holdup.B. moral hazard.C. averse selection.D. tacit collusion.Answer: B Page: 289Difficulty: Moderate Chapter Objective: 3。

APS专业单词汇总

设计design ,gestaltung,entwerfen设计管理designmanagement人机工程ergonomie设计项目designprojekt, designarbeit结构konstruktion界面interface轨迹spurdesigngeschichte设计史,designtheorie设计理论Kommmunikationsdesign视觉传达设计darstellung制图,vertiefung深入,mappe画夹,作品集zeichnen草图idee主意praesentation介绍演示Kunststoff 合成材料elementares gestalten 基础设计vom Happening zur Performance 展示设计Film/Video图象Fotografie图片Kunststoff综合材料Metallbildnerei金属雕塑die schoenen Kuenste 美术Bildhauerei雕塑Bildhauerkunst雕塑艺术StandBild(Statue)雕像die darstellenden Kuenste (Theater) 表演艺术die darstellende Kuenste (Malerei) 绘画艺术oeffentliche Einrichtungen 公共建筑物Architektur 建筑学der Zapfen 榫头der Duebel 木榫,木螺钉die Zarge (门窗)边框,框子Kontrast对比,反差Anatomie 解剖学,人体结构Typograph 书版印刷Strich 线条,笔法Schatten 阴影,影子Parallele 平行线V ertikale 垂直线Horizontale 水平线Kunstcharaktere美术字schriftart字体Form形式Meise手法Komposition构图Gedenkenverbindung联想V orstellungskraft 想象力V erpackung包装Logo标志Multimedium多媒体W ebseite网页Anzeige广告Tendenzdesign动态设计Tendenzbild动态画面Textur肌理Dessin图案Handelshaftlich商业性Auslese精华Kubisch立体Dreidimension立体Keramik陶瓷Bronze 青铜器Lakware漆器Skizze素描Literarisch速写Portrat人像Perspektiv透视Stillleben静物Proportion比例Abstraktion抽象konkret具象的Reinheit纯度Leichtigkeit明度Scherenschnitt剪纸Pinselsoitze毛笔1 摄影技术与实践: photograpic-Technik2. 大学英语: College Englisch3. 高等数学: Fortschrittliche Mathematik4. 工程制图基础Ingenieurwesenszeichnunggrundlagen5. 工业设计概Grundriss des Produktionsdesigns6. 绘画透视: perspektivische Zeichnungstechniken7. 政治理论: politische Theorie8. 体育: physische Ausbildung9. 大学物理:Collegephysik10.工程制图在设计上的应用Ingenieurwesenszeichnung für design11.基础素描:Zeichnensgrundlagen12.平面构成:Fläche Bildung13.色彩写生:Farbeskizze nach der Natur14.设计简史:Geschichte des Design15.速写:Skizze1 知识产权Intellectual Property2 著作权Copyright3 工业产权Industrial Property4 专利Patent5 发明专利Patent for Invention6 实用新型Utility Modle7 外观设计专利Registation of Design8 注册商标Registered Trade Mark9 广告法Advertising Law10 反不正当竞Repression of Untair Competition11 设计费Design Fee12 标准Standard13 德国工业标准Deutsche Industrie Normen1 工业工程学Industrial Engineering2 工业心理学Industrial Psychology3 科学管理法Scientific Management4 生产管理Production Control5 质量管理Quality Control6 系统工程System Engineering7 批量生产Mass Production8 流水作业Conveyer System9 互换式生产方式Interchangeable Produsction Method10 标准化Standardization11 自动化Automation12 市场调查Market Research13 商品化计划Merchandising14 产品开发Product Developement15 产品改型Model Change16 产品测试Product Testing17 产品成本Product Cost18 营销学Marketing德育Gemeinshaftskunde形势与政策Gesellschaftslage und Politik公益劳动Arbeit fuer GemeinW ohl平面构成Flaechebildung心理保健Psychische Pflege军训Militaerisches Training立体构成Raumbildung装饰基础Grundlage der Dekoration美学Aesthetik文字设计Entwurf des Zeichens马列主义原理Grundsaetzliche Theorien des Kommunismus und Lennismus人体工学Konstruktion gemaess des menschlichen Koerpers环境设施设计Entwurf der Umweltinfrastruktur 材料Material 模型Modell平面构成Zweidimensionale Bildung立体构成Dreidimensionale Bildung色彩构成Farbenbildung空间构成Raumbildung计算机辅助设计Konstruktion mit der Hilfe von Computer设计心理学Konstruktionspsychologie市场调查Marktuntersuchung产品改型Gestaltungsaenderung der Produkte产品形象Produktionsimage德国工业标准Maßstäbe der deutschen Industrie产品设计Produktionsentwurf人机工程Mensch-Maschine Ingenieurwissenschaft 设计草图Konstruktionsentwurf基础素描Zeichnensgrundlagen草图基础Darstellungsgrundlagen计算机辅助工业设计CAD computer aid design效果图darstellungstechnik视觉传达Visuelle Kommunikation行为艺术Performance Art美学概论Grundriss der Ästhetik平面构成Plankonstruktion法律基础Grundlage des Recchts中外美术史Geschichte der chinesischen und auslandischen bildenden Kunst字体设计与编排Design der Schriftart und Layout 色彩写生Fareskizze nach der Natur摄影基础Grundlage der Photographie色彩构成FabekonstruktionWEB网页设计基础Grundlage des W ebsitesdesign广告学W erbungstheorie立体构成Dreidimensionale Konstruktion平面广告设计W erbungsdesign包装设计V erpckungsdesign毕业采风Kunstpraxis插画Abbildungen装置艺术Installation Art1 设计Desgin2 现代设计Modern Desgign3 工艺美术设计Craft Design4 工业设计Industrial Design7 产品设计Product Design8 环境设计Environmental Design9 商业设计Comercial Design10 建筑设计Architectural11 一维设计One-dimension Design12 二维设计Tow-dimension Design13 三维设计Three-dimension Design14 四维设计Four-dimension Design16 家具设计Furniture Design17 玩具设计Toy Design18 室内设计Interior Design19 服装设计Costume Design20 包装设计ackaging Design21 展示设计Display Design23 生活环境Living Environment27 设计方法论Design Methodology28 设计语言Design Language29 设计条件Design Condition30 结构设计Structure Design31 形式设计Form Design32 设计过程Design Process50 功能Function51 独创性Originality52 创造力Creative Power54 创造性思维Creating Thinking55 广义工业设计Genealized Industrial Design56 狭义工业设计Narrow Industrial Design 57传播设计Communication Design58 建筑设计Architectural59装饰、装潢Decoration60 城市规划Urban Desgin61 生活环境Living Environment62 都市景观Townscape63 田园都市Gardon City64 办公室风致Office Landscape65 构思设计 Concept Design66 量产设计,工艺设计 Technological Design67 改型设计 Model Change68 设计调查Design Survey69 事前调查Prior Survey 70 动态调查Dynamic Survey71 超小型设计 Compact type72 袖珍型设计 Pocktable Type73 便携型设计 Protable type74 收纳型设计 Selfcontainning Design75 装配式设计 Knock Down Type76 集约化设计 Stacking Type77 成套化设计 Set (Design)78 家族化设计 Family (Design)79 系列化设计 Series (Design)80 组合式设计 Unit Design81 仿生设计 Bionics Design82 外装Facing83 创造性思维Creating Thinking84 等价变换思维Equivalent Transformationn Thought85 集体创造性思维法Brain Storming86设计决策(Design) Decision Making87 功能分化Functional Differentiation88 功能分析Functional Analysis89 生命周期Life Cycle90 照明设计 Illumination Design1 色Color2 光谱Spectrum3 物体色Object Color4 固有色Propor Color5 色料Coloring Material6 色觉三色学说Three-Component Theary7 心理纯色Unique Color8 拮抗色学说Opponent Color Theory9 色觉的阶段模型Stage Model of the Color Perception10 色彩混合Color Mixing11 基本感觉曲线Trisimulus V alus Curves12 牛顿色环Newton's Color Cycle13 色矢量Color V ector14 三原色Three Primary Colors15 色空间Color Space16 色三角形Color Triangle17 测色Colourimetry18 色度Chromaticity19 XYZ表色系XYZ Color System20 实色与虚色Real Color and Imaginary Color21 色等式Color Equation22 等色实验Color Matching Experiment23 色温Color T emperature24 色问轨迹Color T emperature Locus25 色彩三属性Three Attribtes and Color26 色相Hue27 色相环Color Cycle28 明度V alve29 彩度Chroma30 环境色Environmetal Color31 有彩色Chromatic Color32 无彩色Achromatic Colors33 明色Light Color34 暗色Dark Color35 中明色Middle Light Color36 清色Clear Color37 浊色Dull Color38 补色Complementary Color39 类似色Analogous Color40 一次色Primary Color41 二次色Secondary Color42 色立体Color Solid43 色票Color Sample44 孟塞尔表色系Munsell's Color System45 奥斯特瓦德表色系Ostwald's Color System46 日本色研色体系Practical Color Co-ordinate System47 色彩工程Color Engineering48 色彩管理Color Control49 色彩再现Color Reproduction50 等色操作Color Matching51 色彩的可视度Visibility Color52 色彩恒常性Color Constancy53 色彩的对比Color Contrast54 色彩的同化Color Assimilation55 色彩的共感性Color Synesthesia56 暖色与冷色W arm Color and Cold Color57 前进色与后退色Advancing Color Receding Color58 膨胀色与收缩色Expansive Color and Contractile Color59 重色与轻色Heavy Color and Light Color60 色价V aleur61 色调Color Tone 62 暗调Shade63 明调Tint64 中间调Halftone65 表面色Surface Color66 平面色Film Color67 色彩调和Color Harmony68 配色Color Combination69 孟塞尔色彩调和Munsell's Color Harmony70 奥斯特瓦德色彩调和Ostwald's Color Harmony1 传播Communication2 大众传播Mass Communication3 媒体Media4 大众传播媒体Mass Media5 视觉传播Visual Communication6 听觉传播Hearing Communication7 信息Information8 符号Sign9 视觉符号Visual Sign10 图形符号Graphic Symbol12 象征Symbol13 象征标志Symbol Mark14 音响设计Acoustic Design15 听觉设计Auditory Design16 听觉传播设计Auditory Communication Design17 图象设计Visual Communication Design18 视觉设计Visual Design19 视觉传播设计Visual Communication Design20 图形设计Graphic Desig21 编辑设计Editorial Design22 版面设计Layout23 字体设计Lettering25 宣传Propaganda26 广告Advertising38 招贴画海报Poster39 招牌Sign-board46 展示Display47 橱窗展示Window Display48 展示柜Cabinet49 博览会Exposition51 包装Packaging52 工业包装Industrial Packing56 动画Animation57 插图Illustration58 书法Calligraphy59 印刷Initial60 设计费design fee61 标准standard1 美Beauty2 现实美Acture Beauty3 自然美Natural Beauty4 社会美Social Beauty5 艺术美Artisitc Beauty6 内容与形式Content and Form7 形式美Formal Beauty8 形式原理Principles and Form9 技术美Beauty of T echnology10 机械美Beauty of Machine12 材料美Beauty of Material13 美学Aesthetics14 技术美学Technology Aesthetics15 设计美学Design Aesthetics16 生产美学PAroduction Aesthetics17 商品美学Commodity Aedthetics18 艺术Art19 造型艺术Plastic Arts20 表演艺术Performance Art21 语言艺术Linguistic Art22 综合艺术Synthetic Arts23 实用艺术Practical Art24 时间艺术Time Art25 空间艺术Spatial Art26 时空艺术Time and Spatial Art27 一维艺术One Dimantional28 二维艺术two Dimantional29 三维艺术Three Dimantional30 四维艺术Four Dimantional31 舞台艺术Stagecraft32 影视艺术Arts of Mmovie and Television33 环境艺术Environmental Art34 美术Fine Arts35 戏剧Drama36 文学Literature37 意匠Idea38 图案Pattern 39 构思Conception40 构图Composition41 造型Formation42 再现Representation43 表现Expression44 构成Composition45 平面构成Tow Dimentional Composition46 立体构成Three Dimentional Composition47 色彩构成Color Composition48 空间构成Composition of Space49 音响构成Composition and Sound50 多样与统一Unity of Multiplicity51 平衡Balance52 对称Symmetry53 调和、和声Harmony54 对比Contrast55 类似Similarity56 比例Proportion57 黄金分割Golden Section58 节奏Rhythm59 旋律Melody60 调子Tone61 变奏V ariation62 纹样Pattern63 形态Form64 有机形态Organic Form65 抽象形态Abstract Form66 简化形态Simptified Form67 变形Deformation68 图学Graphics69 透视画法Perspective80 平面视图Ground Plain82 设计素描Design Sketch83 预想图Rendering84 模型Model92 计算机图形学Computer Graphics95 计算机辅助设计COMPUTER AIDED DESIGN96 计算机辅助制造Computer Aided Manufacture97 计算机三维动画Computer Three Dimentional Animation98 计算机艺术Computer Arts100 计算机图象处理Computer Image Processing1 人类工程学Human Engineering2 人机工程学Man-Machine Engineering3 工效学Ergonomice4 人因工程学Human Factors Engineering5 人因要素Human Factors6 人机系统Man-Machine System7 人体工程学Human Engineering11 感觉Sensation12 知觉Perception15 视觉Visual Perception16 视觉通道Visual Pathway17 听觉Hearing Perception18 肤觉Skin Sensation19 视觉心理学Visual Psychology20 听觉心理学Hearing Psychology27 主观轮廓Subjictive Contour28 图形与背景Figure and Ground29 图形与背景逆转Reversible Figure36 空间知觉Space Perception37 立体视Stereopsis38 运动知觉Movement Perception39 视错觉Optical Illusion40 残像After Image41 似动Apparent Movement45 听觉刺激Auditory Stimulus46 声压Sound Pressure48 频谱Spectrum50 噪声Noise69 人体尺寸Humanlady Size70 作业空间W ork Space88 形态学Morphology89 仿生学Bionics90 人、环境系统Man-Environment System91 照明Hlumination92 振动Oscillate93 气候Climate设计师人名1-贝伦斯(Peter Behrens, 1868-1940)2-格罗披乌斯(W alter Gropius, 1883-1969)3-米斯(Ludwig Mies van der Rohe, 1886-1969)4-纳吉(Laszlo Moholy-Nagy, 1895-1946)5-布劳耶(Marcel Breuer, 1902-1981)6-华根菲尔德(Wilhelm W agenfeld, 1900-1990)7-布兰德(Marianne Brandt, 1893-1983)8-波尔舍(Ferdinand Alexander Porsche, 1875- 9-科拉尼(Luigi Colani, 1926- )10-拉姆斯(Dieter Rams, 1932- )11-艾斯林格(Hartmut Esslinger, 1944- )12-里特维尔德(Gerrit Rietveld, 1888-1964)13-提革(W alter Darwin T eaque,1883-1960)14-罗维(Raymond Loeway,1889~1986)15-德雷夫斯(Henry Dreyfess,1903-1972)16-沙里宁(Eero Saarinen,1910-1961)17-格雷夫斯(Michael Graves,1934 - )18-伊姆斯(Charles Eames,1907-1978)19-文丘里(Robert V enturi,1925- )20-赖特(Frank Lioyd Wright, 1869~1959)21-厄尔(Harley Earl,1893-1969)22-兰德(Paul Rand,1914-1996)23-贝聿铭(Pei Ieoh Ming ,1917-)24-盖里(Frank Gehry ,1947-)25-索特萨斯(Ettore Sottsass, 1917- )26-戈地(Antoni Gaudi, 1852-1926)27-庞蒂(Gio Ponti,1892-1979)28-塔特林(Vladimir Tatlin,1885-1953)29-康定斯基(W assily Kandinsky,1866-1944)30-柳宗理(1915-)31-五十岚威畅(Takenobu Igarashi,1944-)32-荣久庵宪司(Kenji Ekuan,1929-)33-福田繁雄(Shigeo Fukuda,1932-)34-乔治阿罗(Giorgio Giugiaro,1938-)35-罗西(Aldo Rossi,1931-1997)36-伊斯戈尼斯(Alec Issigonis,1906-1988)37-戴森(James Dyson,1947-)38-伊维(Jonathan Ive, 1967-)39-科伦波(Joe Colombo,1930-1971)40-尼佐里(Macello Nizzoli,1887-1969)41平尼法尼那(Pininfarina,1893-1966)42-威尔德(Henry V an de V elde,1863~1957)43-汉宁森(Poul Henningsen, 1894~1967)44-维纳(Hans W egner ,1914~ )45-沙逊(Sixten Sason,1912~1967)46-雅各布森(Arne Jacobsen, 1902~1971 )47-彦森(Jacob Jensen ,1926~ )48-潘顿(V erner Panton,1926-1998)49-阿尔托(Alvar Aalto,1898-1976)50-威卡拉(Tapio Wirkkala ,1915~1985)25 莫里斯Willian Morris (1834-1896E)26 奥斯特瓦德Wilhelm Friedrich Ostwald(1853-1932G)27 孟赛尔Albert F.Munsell (1858-1918A)28 凡.德.维尔德Henry V ande V elde (1863-1957)29 莱特Lloyd Wright (1867-1959A)30 贝伦斯Peter Behrens(1868-1940G)31 霍夫曼Joseph Hoffmann(1870-1956)32 皮克Frank Pick(1878-1941)33 维斯宁兄弟Alexander Leonid and Victor V esnin35 蒂格W alter Dorwin T eague36 利奇Bernard Leach37 勒.柯不西埃Le Corbusier(法)38 伊顿Johennes Itten40 庞蒂Gio Ponti41 拉塞尔Gordon Russel42 格迪斯Norman Bel Geddes43 洛伊Raymond Fermam44 里德Herbert Read45 莫荷利.纳吉Laszlo Moholy Nagy46 凡.多伦Harold V an Doren48 拜耶Herbert Bayer49 卡桑德拉 A.M.Cassandre50 佩夫斯纳Nikolans51 布劳耶尔Marcel Breuer52 佩里安Charlotte Perriand53 德雷夫斯Henry Dreyfuss54 迪奥Christian Dior55 鲍登Edward Bawden56 贾戈萨Dante Giacosa57 伊姆斯Charles Eames58冈特兰堡Gunter Ram bow59西摩·切瓦斯特Seymour Chwast60扎哈·哈迪德Zaha Hadid61三宅一生Issey Miyake62原研哉Kenyahara63川久保玲Rei Kawakubo64安藤忠雄Tadao Ando65包豪斯Bauhaus66菲力浦·斯达克phlllipe starck67路易斯·康福特·蒂法尼Louis Comfort Tiffany 1 学院派Academicism2 理性主义Rationalism3 非理性主义Irrationalism4 古典主义Classicism5 浪漫主义Romanticism6 现实主义Realism7 印象主义Impressionism8 后印象主义Postimpressionism9 新印象主义Neo-Impressionisme(法)10 那比派The Nabject11 表现主义Expressionism12 象征主义Symbolism13 野兽主义Fauvism14 立体主义Cubism15 未来主义Futurism16 奥弗斯主义Orphism17 达达主义Dadaisme(法)18 超现实主义Surrealism19 纯粹主义Purism20 抽象艺术Abstract Art21 绝对主义,至上主义Suprematism22 新造型主义Neo-plasticisme(法)23 风格派De Stiji24 青骑士Der Blaus Reiter25 抒情抽象主义L yric Abstractionism26 抽象表现主义Abstract Expressionism27 行动绘画Action Painting28 塔希主义Tachisme(法)29 视幻艺术Op Art30 活动艺术、机动艺术Kinetic Art31 极少主义Minimalism32 概念主义Conceptualism33 波普艺术Pop Art34 芬克艺术、恐怖艺术Funk Art35 超级写实主义Super Realism36 人体艺术Body Art37 芝加哥学派Chicago School38 艺术与手工艺运动The Arts & Crafts Movement39 新艺术运动Art Nouveau40 分离派Secession41 构成主义Constructivism42 现代主义Modernism43 包豪斯Bauhaus44 阿姆斯特丹学派Amsterdam School45 功能主义Functionalism46 装饰艺术风格Art Deco(法)47 国际风格International Style48 流线型风格Streamlined Forms49 雅典宪章Athens Charter50 马丘比丘宪章Charter of Machupicchu51 斯堪的纳维亚风格Scandinavia Style52 新巴洛克风格New Baroque53 后现代主义Postmodernism54 曼菲斯Memphis55 高技风格High Tech56 解构主义Deconstructivism57 手工艺复兴Crafts Revival58 准高技风格Trans High T ech59 建筑风格Architecture60 微建筑风格Micro-Architecture61 微电子风格Micro-Electronics62 晚期现代主义Late M材料与加工成型技术1 材料Material2 材料规划Material Planning3 材料评价Material Appraisal4 金属材料Metal Materials5 无机材料Inorganic Materials6 有机材料Organic Materials7 复合材料Composite Materials8 天然材料Natural Materials9 加工材料Processing Materials10 人造材料Artificial Materials11 黑色金属Ferrous Metal12 有色金属Nonferrous Metal13 轻金属材料Light Metal Materials20 陶瓷Ceramics21 水泥Cement22 搪瓷、珐琅Enamel23 玻璃Glass24 微晶玻璃Glass Ceramics25 钢化玻璃Tuflite Glass26 感光玻璃Photosensitive Glass27 纤维玻璃Glass Fiber28 耐热玻璃Hear Resisting Glass 29 塑料Plastics30 通用塑料Wide Plastics31 工程塑料Engineering Plastics34 橡胶Rubber35 粘接剂Adhesives36 涂料Paints37 树脂Resin59 ABS树脂Acrylonitrile Butadiene Styrene Redin60 感光树脂Photosensition Plastics61 纤维强化树脂Fiber Reinforced Plastic62 印刷油墨Printing Ink63 印刷用纸Printing Paper64 铜板纸Art Paper65 木材W ood66 竹材Bamboo67 树脂装饰板Decorative Sheet68 蜂窝机制板Honey Comb Core Panel69 胶合板V eneer70 曲木Bent W ood71 浸蜡纸W axed Paper72 青铜Bronge73 薄壳结构Shell Construction74 技术T echnic75 工具Tool76 金工Metal W ork77 铸造Casting78 切削加工Cutting79 压力加工Plastic W orking81 焊接W elding82 板金工Sheetmetal W oek83 马赛克Mosaic101 粘接与剥离Adhesion and Excoriation102 木材工艺W oodcraft103 竹材工艺Bamboo W ork104 表面技术Surface Technology105 镀饰Plating106 涂饰Coating107 电化铝Alumite108 烫金Hot Stamping112 金属模具Mold113 型板造型Modeling of T eplate114 染料Dyestuff115 颜料Artist Color1 维也纳工厂Wiener W erksttate2 德意志制造联盟Der Deutsche W erkbund3 克兰布鲁克学院The Cranbrook Academy4 国际现代建筑会议Congres Internationaux D'Architecture Moderne5 现代艺术馆Museum Of Modern Art6 芝加哥设计学院Chicago Institute of Design7 英国工业设计委员会Council of Industrial Design8 设计委员会The Desgin Council9 国际建筑师协会Union Internationale des Architects10 设计研究组织Design Research Unit11 日本工业设计师协会Japan Industrial Desginers Association12 日本设计学会Japanese Society for Science of Design13 乌尔姆造型学院Ulm Hochschule fur Gestallung14 国际设计协会联合会International Council of Societies Industrial Desgin15 国际工业设计会议International Design Congress ,ICSID Congress16 国际设计师联盟Allied International Designers17 国际室内设计师联合会International Federation of Interior Designers18 国际图形设计协会International Graphic Desgin Associations。

管理会计(英文版)课后习题答案(高等教育出版社)chapter 9

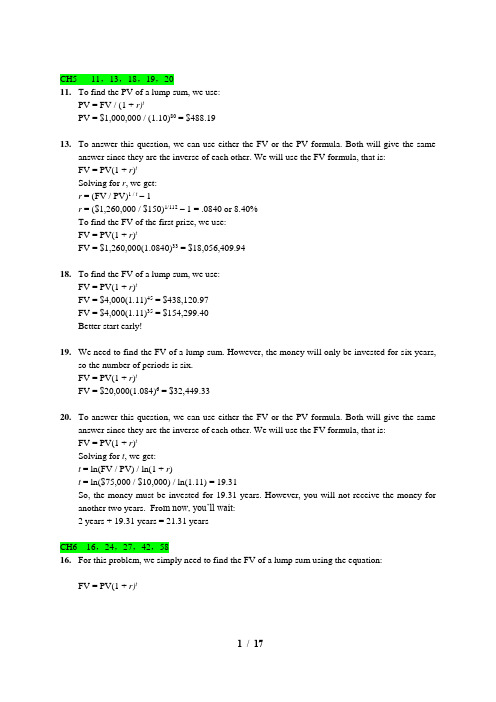

CHAPTER 9STANDARD COSTING:A MANAGERIAL CONTROL TOOL QUESTIONS FOR WRITING AND DISCUSSION1.Standard costs are essentially budgetedamounts on a per-unit basis. Unit standardsserve as inputs in building budgets.2.Unit standards are used to build flexiblebudgets. Unit standards for variable costsare the variable cost component of a flexiblebudgeting formula.3.The quantity decision is determining howmuch input should be used per unit of out-put. The pricing decision determines howmuch should be paid for the quantity of inputused.4.Historical experience is often a poor choicefor establishing standards because the his-torical amounts may include more inefficien-cy than is desired.5.Engineering studies can serve as importantinput to standard setting. Many feel that thisapproach by itself may produce standardsthat are too rigorous.6.Ideal standards are perfection standards,representing the best possible outcomes.Currently attainable standards are standardsthat are challenging but allow some waste.Currently attainable standards are oftenchosen because many feel they tend to mo-tivate rather than frustrate.7.Standard costing systems improve planningand control and facilitate product costing. 8.By identifying standards and assessing devi-ations from the standards, managers can lo-cate areas where change or corrective be-havior is needed.9.Actual costing assigns actual manufacturingcosts to products. Normal costing assignsactual prime costs and estimated overheadcosts to products. Standard costing assignsestimated manufacturing costs to products.10. A standard cost sheet presents the standardamount of and price for each input and usesthis information to calculate the unit standardcost. 11.Managers generally tend to have more con-trol over the quantity of an input used ratherthan the price paid per unit of input.12. A standard cost variance should be investi-gated if the variance is material and if thebenefit of investigating and correcting thedeviation is greater than the cost.13.Control limits indicate how large a variancemust be before it is judged to be materialand the process is out of control. Control lim-its are usually set by judgment although sta-tistical approaches are occasionally used. 14.The materials price variance is often com-puted at the point of purchase rather than is-suance because it provides control informa-tion sooner.15.Disagree. A materials usage variance canbe caused by factors beyond the control ofthe production manager, e.g., purchase of alower-quality material than normal.16.Disagree. Using higher-priced workers toperform lower-skilled tasks is an example ofan event that will create a rate variance thatis controllable.17.Some possible causes of an unfavorablelabor efficiency variance are inefficient labor,machine downtime, and poor quality mate-rials.18.Part of a variable overhead spending va-riance can be caused by inefficient use ofoverhead resources.19.Agree. This variance, assuming that variableoverhead costs increase as labor usage in-creases, is caused by the efficiency or ineffi-ciency of labor usage.20.Fixed overhead costs are either committedor discretionary. The committed costs willnot differ by their very nature. Discretionarycosts can vary, but the level the companywants to spend on these items is decided atthe beginning and usually will be met unlessthere is a conscious decision to change thepredetermined levels.21.The volume variance is caused by the actualvolume differing from the expected volumeused to compute the predetermined stan-dard fixed overhead rate. If the actual vo-lume is different from the expected, then thecompany has either lost or earned a contri-bution margin. The volume variance signalsthis outcome, and if the variance is large,then the loss or gain is large since the vo-lume variance understates the effect.22.The spending variance is more important.This variance is computed by comparing ac-tual expenditures with budgeted expendi-tures. The volume variance simply tellswhether the actual volume is different fromthe expected volume.EXERCISES 9–11. d2. e3. d4. c5. e6. a9–21. a. The operating personnel of each cost center should be involved in settingstandards. They are the primary source for quantity information. The mate-rials manager and purchasing manager are a source of information for ma-terial prices, and personnel are knowledgeable on wage information. The Accounting Department should be involved in overhead standards and should provide information about past prices and usage. Finally, if infor-mation about absolute efficiency is desired, industrial engineers can pro-vide important input.b. Standards should be attainable; they should include an allowance forwaste, breakdowns, etc. Market prices for materials as well as labor (un-ions) should be a consideration for setting standards. Labor prices should include fringe benefits, and material prices should include freight, taxes, etc.2. In principle, before formal responsibility is assigned, the causes of the va-riances must be known. To be responsible, a manager must have the ability to control or influence the variance. The following assignments of responsi-bility are general in nature and have exceptions:MPV: Purchasing managerMUV: Production managerLRV: Production managerLEV: Production managerOH variances: Departmental managers1. SH = 0.8 ⨯ 95,000 = 76,000 hours2. SQ = 5 ⨯ 95,000 = 475,000 components9–41. MPV = (AP – SP)AQ= ($0.03 – $0.032)6,420,000 = $12,840 FMUV = (AQ – SQ)SP= (6,420,000 – 6,400,000)$0.032 = $640 U2. LRV = (AR – SR)AH= ($12.50 – $12.00)2,000 = $1,000 UL EV = (AH – SH)SR= (2,000 – 1,850)$12.00 = $1,800 U9–51. Variable overhead analysis:Actual VOH Budgeted VOH Applied VOH2. Fixed overhead analysis:Actual FOH Budgeted FOH Applied FOH1. Materials: $60 ⨯ 20,000 = $1,200,000L abor: $21 ⨯ 20,000 = $420,0002. Budgeted Cost VarianceMaterials $1,215,120 $1,200,000 $ 15,120 U Labor 390,000 420,000 30,000 F *$122,000 ⨯ $9.96; 31,200 ⨯ $12.503. MPV = (AP – SP)AQ= ($9.96 – $10)122,000 = $4,880 FMUV = (AQ – SQ)SP= (122,000 – 120,000)$10 = $20,000 UAP ⨯ AQ SP ⨯ AQ SP ⨯ SQ4. LRV = (AR – SR)AH= ($12.50 – $14)31,200 = $46,800 FLEV = (AH – SH)SR= (31,200 – 30,000)$14 = $16,800 UAR ⨯ AH SR ⨯ AH SR ⨯ SH1. MPV = (AP – SP)AQ= ($8.35 – $8.25)114,000 = $11,400 UMUV = (AQ – SQ)SP= (112,500 – 115,200)$8.25 = $22,275 F(A three-pronged variance diagram is not shown because MPV is for mate-rials purchased and not materials used.)2. LRV = (AR – SR)AH= ($9.80 – $9.65)37,560 = $5,634 UNote: AR = $368,088/37,560LEV = (AH – SH)SR= (37,560 – 38,400)$9.65 = $8,106 FAR ⨯ AH SR ⨯ AH SR ⨯ SH3. Materials Inventory ................................... 940,500M PV ............................................................ 11,400Accounts Payable ............................... 951,900Work in Process ....................................... 950,400MUV ...................................................... 22,275Materials Inventory .............................. 928,125Work in Process ....................................... 370,560LRV ............................................................ 5,634LEV ....................................................... 8,106Accrued Payroll ................................... 368,0881. Fixed overhead rate = $0.55/(1/2 hr. per unit) = $1.10 per DLHSH = 1,180,000 ⨯ 1/2 = 590,000Applied FOH = $1.10 ⨯ 590,000 = $649,0002. Fixed overhead analysis:Actual FOH Budgeted FOH Applied FOH(600,000 expected hours = 1/2 hour ⨯ 1,200,000 units)3. Variable OH rate = ($1,350,000 – $660,000)/600,000= $1.15 per DLH4. Variable overhead analysis:Actual VOH Budgeted VOH Applied VOH1. Cases needing investigation:Week 2: Exceeds the 10% rule.Week 4: Exceeds the $8,000 rule and the 10% rule.Week 5: Exceeds the 10% rule.2. The purchasing agent. Corrective action would require a return to the pur-chase of the higher-quality material normally used.3. Production engineering is responsible. If the relationship is expected to pers-ist, then the new labor method should be adopted, and standards for mate-rials and labor need to be revised.9–101. Standard fixed overhead rate = $2,160,000/(120,000 ⨯ 6)= $3.00 per DLHStandard variable overhead rate = $1,440,000/720,000= $2.00 per DLH2. Fixed: 119,000 ⨯ 6 ⨯ $3.00 = $2,142,000Variable: 119,000 ⨯ 6 ⨯ $2.00 = $1,428,000Total FOH variance = $2,250,000 – $2,142,000= $108,000 UTotal VOH variance = $1,425,000 – $1,428,000= $3,000 F3. Fixed overhead analysis:Actual FOH Budgeted FOH Applied FOHThe spending variance is the difference between planned and actual costs.Each item’s variance should be analyzed to see if these costs can be r e-duced. The volume variance is the incorrect prediction of volume, or alterna-tively, it is a signal of the loss or gain that occurred because of producing at a level different from the expected level.4. Variable overhead analysis:Actual VOH Budgeted VOH Applied VOHThe variable overhead spending variance is the difference between the actual variable overhead costs and the budgeted costs for the actual hours used.The variable overhead efficiency variance is the savings or extra cost attri-butable to the efficiency of labor usage.9–111. MPV = (AP – SP)AQ= ($6.60 – $6.40)1,488,000= $297,600 UMUV = (AQ – SQ)SP= (1,480,000 – 1,400,000)$6.40= $512,000 UNote: There is no three-pronged analysis for materials because materials purchased is different from the materials used. (MPV uses materials pur-chased and MUV uses materials used.)2. LRV = (AR – SR)AH= ($18.10 – $18.00)580,000= $58,000 ULEV = (AH – SH)SR= (580,000 – 560,000)$18.00= $360,000 UAR ⨯ AH SR ⨯ AH SR ⨯ SH3. Fixed overhead analysis:Actual FOH Budgeted FOH Applied FOHNote: Practical volume in hours = 2 ⨯ 288,000 = 576,000 hours4. Variable overhead analysis:Actual VOH Budgeted VOH Applied VOH1. Materials Inventory ................................... 9,523,200MPV ............................................................ 297,600Accounts Payable ............................... 9,820,8002. Work in Process ....................................... 8,960,000MUV ............................................................ 512,000Materials Inventory .............................. 9,472,0003. Work in Process ....................................... 10,080,000LRV ............................................................ 58,000LEV ............................................................. 360,000Accrued Payroll ................................... 10,498,0004. Work in Process ....................................... 3,080,000Fixed Overhead Control...................... 2,240,000Variable Overhead Control ................. 840,0005. Materials and labor:Cost of Goods Sold .................................. 1,227,600MPV ...................................................... 297,600MUV ...................................................... 512,000LRV ....................................................... 58,000LEV ....................................................... 360,000 Overhead disposition:Cost of Goods Sold .................................. 160,000Fixed Overhead Control...................... 160,000Cost of Goods Sold .................................. 32,000Variable Overhead Control ................. 32,0001. Tom purchased the large quantity to obtain a lower price so that the pricestandard could be met. In all likelihood, given the reaction of Jackie Iverson, encouraging the use of quantity discounts was not an objective of setting price standards. Usually, material price standards are to encourage the pur-chasing agent to search for sources that will supply the quantity and quality of material desired at the lowest price.2. It sounds like the price standard may be out of date. Revising the price stan-dard and implementing a policy concerning quantity purchases would likely prevent this behavior from reoccurring.3. Tom apparently acted in his own self-interest when making the purchase. Hesurely must have known that the quantity approach was not the objective.Yet, the reward structure suggests that there is considerable emphasis placed on meeting standards. His behavior, in part, was induced by the re-ward system of the company. Probably, he should be retained with some ad-ditional training concerning the goals of the company and a change in em-phasis and policy to help encourage the desired behavior.9–14Materials:AP ⨯ AQ SP ⨯ AQ SP ⨯ SQLabor:AR ⨯ AH SR ⨯ AH SR ⨯ SH1. Materials Inventory ................................... 47,700MPV ...................................................... 5,700Accounts Payable ............................... 42,0002. Work in Process ....................................... 45,000MUV ............................................................ 2,700Materials Inventory .............................. 47,7003. Work in Process ....................................... 105,000LRV ....................................................... 2,300LEV (700)Accrued Payroll ................................... 102,0004. Cost of Goods Sold .................................. 2,700MUV ...................................................... 2,700MPV ............................................................ 5,700LRV ............................................................ 2,300LEV (700)Cost of Goods Sold ............................. 8,7001. VOH efficiency variance = (AH – SH)SVOR$8,000 = (1.2SH – SH)$2$8,000 = $0.4SHSH = 20,000AH = 1.2SH = 24,000 2. LEV = (AH – SH)SR$20,000 = (24,000 – 20,000)SR$20,000 = 4,000SRSR = $5LRV = (AR – SR)AH$6,000 = (AR – $5)24,000$0.25 = AR – $5AR = $5.253. SH = 4 ⨯ Units produced20,000 = 4 ⨯ Units produced Units produced = 5,000PROBLEMS9–171. Materials:AP ⨯ AQ SP ⨯ AQ SP ⨯ SQThe new process saves 0.25 ⨯ 4,000 ⨯ $3 = $3,000. Thus, the net savings attri-butable to the higher-quality material are ($6,000 –$3,000) –$2,300 = $700.Keep the higher-quality material!2. Labor for new process:AR ⨯ AH SR ⨯ AH SR ⨯ SHThe new process gains $3,000 in materials (see Requirement 1) but loses $6,000 from the labor effect, giving a net loss of $3,000. If this pattern is ex-pected to persist, then the new process should be abandoned.3. Labor for new process, one week later:AR ⨯ AH SR ⨯ AH SR ⨯ SHIf this is the pattern, then the new process should be continued. It will save $260,000 per year ($5,000 ⨯52 weeks). The weekly savings of $5,000 is the materials savings of $3,000 plus labor savings of $2,000.9–181. e2. h3. k4. n5. d6. g7. o8. b9. m10. l11. j12. c13. a14. i15. f9–191. Material quantity standards:1.25 feet per cutting board⨯ 67.50 feet for five good cutting boardsUnit standard for lumber = 7.50/5 = 1.50 feetUnit standard for foot pads = 4.0Material price standards:Lumber: $3.00 per footPads: $0.05 per padLabor quantity standards:Cutting: 0.2 hrs. ⨯ 6/5 = 0.24 hours per good unitAttachment: 0.25 hours per good unitUnit labor standard 0.49 hours per good unit Labor rate standard: $8.00 per hourStandard prime cost per unit:Lumber (1.50 ft. @ $3.00) $4.50Pads (4 @ $0.05) 0.20Labor (0.49 hr. @ $8.00) 3.92Unit cost $8.629–19 Concluded2. Standards allow managers to compare planned and actual performance. Thedifference can be broken down into price and efficiency variances to identify the cause of a variance. With this feedback, managers are able to improve productivity as they attempt to produce without cost overruns.3. a. The purchasing manager identifies suppliers and their respective pricesand quality of materials.b. The industrial engineer often conducts time and motion studies to deter-mine the standard direct labor time for a unit of product. They also can de-termine how much material is needed for the product.c. The cost accountant has historical information as well as current informa-tion from the purchasing agent, industrial engineers, and operating per-sonnel. He or she can compile this information to obtain an achievable standard.4. Lumber:MPV = (AP – SP)AQ= ($3.10 – $3.00)16,000 = $1,600 UMUV = (AQ – SQ)SP= (16,000 – 15,000)$3 = $3,000 URubber pads:MPV = (AP – SP)AQ= ($0.048 – $0.05)51,000 = $102 FMUV = (AQ – SQ)SP= (51,000 – 40,000)$0.05 = $550 ULabor:LRV = (AR – SR)AH= ($8.05 – $8.00)5,550 = $277.50 ULEV = (AH – SH)SR= (5,550 – 4,900)$8 = $5,200 U9–201. The cumulative average time per unit is an average. It includes the2.5 hoursper unit when 40 units are produced as well as the 1.024 hours per unit when 640 units are produced. As more units are produced, the cumulative average time per unit will decrease.2. The standard should be 0.768 hour per unit as this is the average time takenper unit once efficiency is achieved:[(1.024 ⨯ 640) – (1.28 ⨯ 320)]/(640 – 320)3. Std. Usage Std. CostDirect materials $ 4 25.000 $100.00 Direct labor 15 0.768 11.52 Variable overhead 8 0.768 6.14 Fixed overhead 12 0.768 9.22* Standard cost per unit $126.88* *Rounded4. There would be unfavorable efficiency variances for the first 320 units be-cause the standard hours are much lower than the actual hours at this level.Actual hours would be approximately 409.60 (320 ⨯ 1.28), and standard hours would be 245.76 (320 ⨯ 0.768).9–211. MPV = (AP – SP)AQ= ($4.70 – $5.00)260,000 = $78,000 FMUV = (AQ – SQ)SP= (320,000 – 300,000)$5 = $100,000 UThe materials usage variance is viewed as the most controllable because prices for materials are often market-driven and thus not controllable. Re-sponsibility for the variance in this case likely would be assigned to purchas-ing. The lower-quality materials are probably the cause of the extra usage.2. LRV = (AR – SR)AH= ($13 – $12)82,000 = $82,000 ULEV = (AH – SH)SR= (82,000 – 80,000)$12 = $24,000 UAR ⨯ AH SR ⨯ AH SR ⨯ SHProduction is usually responsible for labor efficiency. In this case, efficiency may have been affected by the lower-quality materials, and purchasing, thus, may have significant responsibility for the outcome. Other possible causes are less demand than expected, poor supervision, lack of proper training, and lack of experience.3. Variable overhead variances:Actual VOH Budgeted VOH Applied VOHFormula approach:VOH spending variance = Actual VOH – (SVOR ⨯ AH)= $860,000 – ($10 ⨯ 82,000)= $40,000 UVOH efficiency variance = (AH – SH)SVOR= (82,000 – 80,000)$10= $20,000 U4. Fixed overhead variances:Actual FOH Budgeted FOH Applied FOHThe volume variance is a measure of unused capacity. This cost is reduced as production increases. Thus, selling more goods is the key to reducing this variance (at least in the short run).5. Four variances are potentially affected by material quality:MPV $ 78,000 FMUV 100,000 ULEV 24,000 UVOH efficiency 20,000 U$ 66,000 UIf the variance outcomes are largely attributable to the lower-quality mate-rials, then the company should discontinue using this material.6. (Appendix required)Materials Inventory ................................... 1,300,000MPV ...................................................... 78,000Accounts Payable ............................... 1,222,000Work in Process ....................................... 1,500,000MUV ............................................................ 100,000Materials Inventory .............................. 1,600,0009–21 ConcludedWork in Process ....................................... 960,000LRV ............................................................ 82,000LEV ............................................................. 24,000Accrued Payroll ................................... 1,066,000Cost of Goods Sold .................................. 206,000MUV ...................................................... 100,000LRV ....................................................... 82,000LEV ....................................................... 24,000MPV ............................................................ 78,000Cost of Goods Sold ............................. 78,000VOH Control .............................................. 860,000Various Credits .................................... 860,000FOH Control .............................................. 556,000Various Credits .................................... 556,000Work in Process ....................................... 800,000VOH Control ......................................... 800,000Work in Process ....................................... 480,000FOH Control ......................................... 480,000Cost of Goods Sold .................................. 60,000VOH Control ......................................... 60,000Cost of Goods Sold .................................. 76,000FOH Control ......................................... 76,0009–221. Fixed overhead rate = $2,400,000/600,000 hours*= $4 per hour*Standard hours allowed = 2 ⨯ 300,000 units2. Little Rock plant:Actual FOH Budgeted FOH Applied FOHAthens plant:Actual FOH Budgeted FOH Applied FOHThe spending variance is almost certainly caused by supervisor’s salaries (for example, an unexpected midyear increase due to union pressures). It is unlikely that the lease payments or depreciation would be greater than bud-geted. Changing the terms on a 10-year lease in the first year would be un-usual (unless there is some sort of special clause permitting increased pay-ments for something like unexpected inflation). Also, the depreciation should be on target (unless more equipment was purchased or the depreciation budget was set before the price of the equipment was known with certainty).The volume variance is easy to explain. The Little Rock plant produced less than expected, and so there was an unused capacity cost: $4 ⨯ 120,000 hours = $480,000. The Athens plant had no unused capacity.9–22 Concluded3. It appears that the 120,000 hours of unused capacity (60,000 subassemblies)is permanent for the Little Rock plant. This plant has 10 supervisors, each making $50,000. Supervision is a step-cost driven by the number of produc-tion lines. Unused capacity of 120,000 hours means that two lines can be shut down, saving the salaries of two supervisors ($100,000 at the original salary level). The equipment for the two lines is owned. If it could be sold, then the money could be reinvested, and the depreciation charge would be reduced by20 percent (two lines shut down out of 10). There is no way to directly reducethe lease payments for the building. Perhaps the company could use the space to establish production lines for a different product. Or perhaps the space could be subleased. Another possibility is to keep the supervisors and equipment and try to fill the unused capacity with special orders orders for the subassembly below the regular selling price from a market not normally served. If the selling price is sufficient to cover the variable costs and cover at least the salaries and depreciation for the two lines, then the special order option may be a possibility. This option, however, is fraught with risks, e.g., the risk of finding enough orders to justify keeping the supervisors and equipment, the risk of alienating regular customers who pay full price, and the risk of violating price discrimination laws. Note:You may wish to point out the value of the resource usage model in answering this question (see Chapter 3).4. For each plant, the standard fixed overhead rate is $4 per direct labor hour.Since each subassembly should use two hours, the fixed overhead cost per unit is $8, regardless of where they are produced. Should they differ? Some may argue that the rate for the Little Rock plant needs to be recalculated. For example, one possibility is to use expected actual capacity, instead of prac-tical capacity. In this case, the Little Rock plant would have a fixed overhead rate of $2,400,000/480,000 hours = $5 per hour and a cost per subassembly of $10. The question is: Should the subassemblies be charged for the cost of the unused capacity? ABC suggests a negative response. Products should be charged for the resources they use, and the cost of unused capacity should be reported as a separate item—to draw management’s att ention to the need to manage this unused capacity.9–231. Normal Patient Day:Standard Standard StandardPrice Usage Cost Direct materials $10.00 8.00 lb. $ 80.00 Direct labor 16.00 2 hr. 32.00 Variable overhead 30.00 2 hr. 60.00 Fixed overhead 40.00 2 hr. 80.00 Unit cost $252.00 Cesarean Patient Day:Standard Standard StandardPrice Usage Cost Direct materials $10.00 20.00 lb. $200.00 Direct labor 16.00 4 hr. 64.00 Variable overhead 30.00 4 hr. 120.00 Fixed overhead 40.00 4 hr. 160.00 Unit cost $544.00 2. MPV = (AP – SP)AQ= ($9.50 – $10.00)172,000 = $86,000 FMUV = (AQ – SQ)SPMUV (Normal) = [30,000 – (8 ⨯ 3,500)]$10 = $20,000 UMUV (Cesarean) = [142,000 – (20 ⨯ 7,000)]$10 = $20,000 UMaterials .................................................... 1,720,000MPV ...................................................... 86,000Accounts Payable ............................... 1,634,000Work in Process ....................................... 1,680,000M UV ........................................................... 40,000Materials .............................................. 1,720,000MPV ............................................................ 86,000MUV ............................................................ 40,000Cost of Services Sold ......................... 126,0003. LRV = (AR – SR)AH= ($15.90 – $16.00)36,500 = $3,650 FLEV = (AH – SH)SRLEV (Normal) = [7,200 – (2 ⨯ 3,500)]$16 = $3,200 ULEV (Cesarean) = [29,300 – (4 ⨯ 7,000)]$16 = $20,800 UWork in Process ....................................... 560,000*LEV ............................................................. 24,000LRV ....................................................... 3,650Accrued Payroll ................................... 580,350 *[(2 ⨯ 3,500) + (4 ⨯ 7,000)] ⨯ $16 = $560,000Cost of Services Sold ............................... 20,350LRV ............................................................ 3,650LEV ....................................................... 24,0004. Variable overhead variances:Actual VOH Budgeted VOH Applied VOHFixed overhead variances:Actual FOH Budgeted FOH Applied FOHNote: SH = (2 ⨯ 3,500) + (4 ⨯ 7,000) = 35,000。

Cha10 罗斯公司理财第九版原版书课后习题

Company Stock One option in the 401(k) plan is stock in East Coast Yachts. The company is currently privately held. However, when you interviewed with the owner, Larissa Warren, she informed you the company was expected to go public in the next three to four years. Until then, a company stock price is simply set each year by the board of directors.Bledsoe S&P 500 Index Fund This mutual fund tracks the S&P 500. Stocks in the fund are weighted exactly the same as the S&P 500. This means the fund return is approximately the return on the S&P 500, minus expenses. Because an index fund purchases assets based on the composition of the index it is following, the fund manager is not required to research stocks and make investment decisions. The result is that the fund expenses are usually low. The Bledsoe S&P 500 Index Fund charges expenses of .15 percent of assets per year.Bledsoe Small-Cap Fund This fund primarily invests in small-capitalization stocks. As such, the returns of the fund are more volatile. The fund can also invest 10 percent of its assets in companies based outside the United States. This fund charges 1.70 percent in expenses.Bledsoe Large-Company Stock Fund This fund invests primarily in large-capitalization stocks of companies based in the United States. The fund is managed by Evan Bledsoe and has outperformed the market in six of the last eight years. The fund charges 1.50 percent in expenses.Bledsoe Bond Fund This fund invests in long-term corporate bonds issued by U.S.–domiciled companies. The fund is restricted to investments in bonds with an investment-grade credit rating. This fund charges 1.40 percent in expenses.Bledsoe Money Market Fund This fund invests in short-term, high–credit quality debt instruments, which include Treasury bills. As such, the return on the money market fund is only slightly higher than the return on Treasury bills. Because of the credit quality and short-term nature of the investments, there is only a very slight risk of negative return. The fund charges .60 percent in expenses.1. What advantages do the mutual funds offer compared to the company stock?2. Assume that you invest 5 percent of your salary and receive the full 5 percent match from EastCoast Yachts. What EAR do you earn from the match? What conclusions do you draw about matching plans?3. Assume you decide you should invest at least part of your money in large-capitalization stocksof companies based in the United States. What are the advantages and disadvantages of choosing the Bledsoe Large-Company Stock Fund compared to the Bledsoe S&P 500 Index Fund?4. The returns on the Bledsoe Small-Cap Fund are the most volatile of all the mutual funds offeredin the 401(k) plan. Why would you ever want to invest in this fund? When you examine the expenses of the mutual funds, you will notice that this fund also has the highest expenses. Does this affect your decision to invest in this fund?5. A measure of risk-adjusted performance that is often used is the Sharpe ratio. The Sharpe ratiois calculated as the risk premium of an asset divided by its standard deviation. The standard deviations and returns of the funds over the past 10 years are listed here. Calculate the Sharpe ratio for each of these funds. Assume that the expected return and standard deviation of the company stock will be 16 percent and 70 percent, respectively. Calculate the Sharpe ratio for the company stock. How appropriate is the Sharpe ratio for these assets? When would you use the Sharpe ratio?6. What portfolio allocation would you choose? Why? Explain your thinking carefully.。

学术英语词汇570

The Academic Word ListSublist 1 of the Academic Word List - Most frequent words in familiesThis sublist contains the most frequent words of the Academic Word List in the Academic Corpus. The most frequent members of the word families in Sublist 1 are listed below.analysis分析approach方法area地区领域assessment 评价assume假设authority权威available可提供的benefit好处,受益concept概念consistent一致的constitutional宪法的context 环境contract收缩合同create 创造data 数据definition 定义derived由来,派生distribution 分布economic 经济的environment 环境establish 建立estimate 估计evidence 证据export出口factors 因素financial 金融的formula公式function 功能identified确认的income 收入indicate 指出individual 个人的interpretation理解involved 涉及到issues 问题labour 劳动力legal 合法的legislation 立法major 主要的专业method 方法occur 出现percent 百分之period 时期policy 政策principle 原则procedure 步骤process 过程,处理required 必须的research 研究response 回应role 角色,作用section 部分sector 行业区域significant 重要的similar 相似的source 源头specific 具体的structure 结构theory 理论variables 变量Sublist 2 of the Academic Word List - Most frequent words in familiesThis sublist contains the second most frequent words in the Academic Word List from the Academic Corpus. The most frequent members of the word families in Sublist 2 are listed below.achieve获得acquisition收购获得administration管理affect影响appropriate合适的aspects 方面assistance 协助categories 种类chapter 章节commission委托community社区complex组成的,合成的computer电脑conclusion结论conduct做consequences 后果construction 建设consumer 顾客credit 信用cultural 文化的design 设计distinction 区别elements 元素equation等式evaluation 评价features 特点final 最后的focus 关注impact 影响injury 受伤institute 协会investment 投资items 项目条款journal期刊maintenance 维修normal 正常的obtained 获得participation 参与perceive 认识到positive 积极的potential 潜在的previous 之前的primary 主要的purchase 购买range 范围region 地区regulations 规则relevant 相关的resident 定居者resources 资源restricted 受限security 安全sought 寻找(过去式)select 挑选site 选址strategies 策略survey 调查text 文本1traditional 传统的transfer 转移Sublist 3 of the Academic Word List - Most frequent words in familiesThis sublist contains the third most frequent words of the Academic Word List in the Academic Corpus. The most frequent members of the word families in Sublist 3 are listed below.alternative 可供选择的circumstance 环境comments评论compensatio n 补偿components 组成部分consent同意considerable 大量的constant连续的constraints 限制contribution 贡献convention 准则coordination 协调core 核心的corporate大公司corresponding相应的criteria 标准deduction减除demonstrate证明document文件dominant 主导的emphasis重要性ensure确保excluded排除framework框架funds资金illustrated给…插图immigration移民implies 暗示initial 开始的instance例子interaction互动justification证明正确layer层link连接location地点maximum 最大minorities 少数negative 消极的outcomes 结果partnership合作philosophy 哲学physical 身体的proportion部分比例publish出版reaction 反应registered 登记reliance 依靠removed 移开scheme 计划方案sequence顺序sex 性shift 转换specified具体说明的sufficient足够的task 任务technical 技术的techniques 技术technology 技术validity合法性volume量Sublist 4 of the Academic Word List - Most frequent words in familiesThis sublist contains the fourth most frequent words of the Academic Word List in the Academic Corpus. The most frequent members of the word families in Sublist 4 are listed below.access获得adequate足够的annual年度的apparent明显的approximate近似attitudes 态度attributed 归因于civil国内的code代码commitment承诺communication交流concentration浓度conference会议contrast 对比cycle 循环debate 辩论despite尽管dimensions维度domestic 国内的emerge 出现error 错误ethnic 民族的goals 目标granted 授予hence 因此hypothesis 假说implementation 实施implications 含意暗示imposed 强加integration 结合internal 内部多investigation 调查job 工作2label 标签mechanism机制obvious 明显的occupational 职业的option选择output 产出overall 整体的parallel 平行parameters参数phase阶段predicted预测principal 主要的prior 先前的professional 专业的project项目promote促进regime政权resolution决心retained保留series 系列statistics统计status 地位stress 压力subsequent 紧随其后的sum 总量summary 总结undertaken 承担Sublist 5 of the Academic Word List - Most frequent words in familiesacademic学术的adjustment调整alter 改变amendment修订aware 注意到capacity 能力challenge挑战clause从句compounds混合物conflict 矛盾consultation 咨询contact接触decline 下降discretion谨慎draft 草稿enable 使…能energy能量enforcement 强制执行entities 实物equivalent相等的evolution 进化expansion扩张exposure 接触external 外部的facilitate协助fundamental 根本的generated产生generation 代image图像liberal 开明的licence 执照logic 逻辑marginal 边缘的medical 医学的mental 精神的modified 修改monitoring 监督network 网络notion 概念objective 客观的orientation定位perspective角度precise 精准的prime 主要的psychology 心理学pursue追逐ratio 比例rejected 拒绝revenue 税收stability稳定性styles 风格substitution 代替物sustainable 可持续的symbolic 象征的target 目标transition过度trend 潮流version 版本welfare 福祉whereas却Sublist 6 of the Academic Word List - Most frequent words in familiesabstract摘要accurate 准确的acknowledge承认aggregate 总计allocation分配assigned指派attached粘附author作者bond纽带brief简洁的capable有能力的cite引用cooperative合作的discrimination歧视display显示diversity多样性domain 领域edition版本enhanced提高estate地产exceed超过expert专家explicit明显的federal联邦的fees费用flexibility 灵活性furthermore而且gender 性别ignored忽视incentive 刺激incidence 发生incorporate纳入index 索引inhibition内抑感initiatives 主动性input输入instructions指示intelligence 智力interval间隔lecture 讲座migration 迁徙minimum 最小ministry 部motivation动机neutral 中立的nevertheless然而overseas 海外的precede先于presumption推测rational合理的recovery恢复revealed揭示scope范围subsidiary次要的tapes 带子trace追踪transformation蜕变transport交通underlying潜在的utility实用效用3Sublist 7 of the Academic Word List - Most frequent words in familiesadaptation适应adults成年人advocate支持aid 帮助channel渠道chemical 化学的classical经典的comprehensive全面的comprise由…组成confirmed确定contrary 相反的converted 转换couple 一对decade 十年definite明确的deny否认differentiation区分disposal丢弃dynamic动态的eliminate消除empirical经验主义的equipment设备extract 提取file 文件finite有限的foundation 基础global 全球的grade成绩guarantee保证hierarchical分等级的identical相似的ideology意识形态inferred推断innovation创新insert 嵌入intervention 干预isolate使孤立media媒体mode模式paradigm范例phenomenon 现象priority 优先权prohibited禁止publication 出版物quotation 引用release释放reverse倒退simulation 模仿solely独自的somewhat稍微submit提交successive连续的survive幸存thesis论文topic主题transmission传播ultimately最终地unique独特的visible可见的voluntary自愿的Sublist 8 of the Academic Word List - Most frequent words in familiesabandon放弃accompanied陪伴accumulation积累ambiguous模糊的appendix附录appreciation感激arbitrary武断的automatically自动的bias偏见chart图表clarity清楚conformity遵守commodity商品complement补充contemporary现代的contradiction矛盾crucial 重要的currency货币denote 指示detected察觉deviation偏离displacement位移dramatic戏剧的eventually最后的exhibit展示exploitation充分利用fluctuations波动guidelines指导highlighted强调implicit含蓄的induced引诱inevitably不可避免的infrastructure基础设施inspection检查intensity强度manipulation操控minimised最小化nuclear核offset抵消paragraph段落plus 加practitioners 从业者predominantly主导的prospect前景radical根本的random随意的reinforced加强restore储存revision修订schedule行程表tension紧张termination终结theme主题thereby因此uniform不变的vehicle工具轿车via通过virtually几乎widespread普遍的visual视觉的Sublist 9 of the Academic Word List - Most frequent words in familiesaccommodation住宿analogous类比的anticipated预料assurance确保attained获得behalf为了...的利益bulk 体积ceases停止coherence协调的coincide同时发生commenced开始4incompatible不兼容的concurrent同时发生的confined限制controversy争执conversely相反的device装置devoted投入diminished减少distorted/distortion 扭曲duration 持续erosion腐蚀ethical道德的format布局founded建立inherent内在的insights洞察力integral必需的intermediate中间的manual用手的mature成熟的mediation调停medium媒介military军事的minimal最小的mutual双方的norms惯例overlap重合passive消极的portion比例preliminary基础的protocol惯例qualitative质的refine提炼relaxed放松的restraints 限制revolution革命rigid严格的route线路scenario梗概sphere球面领域subordinate下级的supplementary补充道suspended暂停team团队temporary暂时的trigger 引起unified 统一的violation违背vision视力Sublist 10 of the Academic Word List - Most frequent words in familiesThis sublist contains the least frequent words of the Academic Word List in the Academic Corpus. The most frequent members of the word families in Sublist 10 are listed below.adjacent 比邻的albeit尽管assembly聚集到一起的人collapse倒塌colleagues同事compiled汇编conceived构思convinced使信服depression 萧条降低encountered 面临enormous 巨大的forthcoming 即将到来的inclination倾向integrity完整,诚实intrinsic内在的invoked引起产生levy 征收likewise同样nonetheless 尽管如此notwithstanding尽管odd 古怪的ongoing持续的panel 委员会,小组persistent 坚持不懈的posed形成构成reluctant不情愿的so-called所谓的straightforward 易懂的undergo经受whereby 借56。

美国大学审计学Auditing and Assurance Services习题解

5.