管理会计英语(英文版课件)1

管理会计 双语课件 Management accounting

01 会计信息的概念

Example

The following statements refer to qualities of good information:

(ⅰ) It should be communicated to the right person (ⅱ) It should always be completely accurate before it

关), Complete (完整 ), Accurate (准确 ), Clear (清楚), it should inspire confidence , it should be appropriately communicated , its volume should be manageable, it should be timely (及时 )and its cost (成本收

QUEห้องสมุดไป่ตู้TION

Accounting Information

C ONTENTS

1

信息的概念 The definition of

Information

2 信息的作用

The use of Information

3 案例

Case

01 会计信息的概念

Data and information

Data ( 数据 ) is the raw material for data processing.

01 会计信息的概念

Identify the users of TLC Daycare’s accounting information as internal(I) or external(E).

Lesson 6 Inventory management 英文管理会计课件 Management Accounting

Topic 1: Inventory management and EOQ

Inventory Management

➢ Inventory Management is planning, coordinating, and controlling activities related to the flow of inventory into, through, and out of an organization

14,000 12,000 10,000 8,000 6,000 4,000 2,000

-

Annual relevant ordering costs

Annual relevant carring costs

Annual relevant total costs

Order Quantity in units

2. To satisfy customer demand. 3. To avoid shutting down manufacturing

facilities because of machine failure, defective parts, unavailable parts, or late delivery of parts. 4. To buffer against unreliable production processes. 5. To take advantage of discounts. 6. To hedge against future price increases.

choose the inventory quantity per order to minimize costs

13

Topic 1: Inventory management and EOQ

管理会计课件 英文

1 - 11 1-11 - 11111111h11111ythtr

The Nature of Planning and Controlling

Management Process Internal Accounting System

Budgets, Special Reports

Other information systems

Mayfair Starbucks Store, March 31, 20X1

Sales Less: Ingredients Store labor Other labor Utilities, etc. Total expenses Operating income

Budget $50,000

22,000 12,000 6,000 4,500 $44,500 $ 5,500

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 1 - 14 1-11 - 14111111h11111ythtr

Budget: quantitative expression of a plan of action

Performance reports: compare actual results with budgeted amounts provide feedback by comparing results with plans highlight variances

Actual $50,000

24,500 11,600 6,050 4,500 $46,650 $ 3,350

Variance 0

$2,500 U 400 F 50 U 0 $2,150 U $2,150 U

《管理会计》课件全英文Acct_ch1_ManAcct_(Feb_25)

1. Externally focused 2. Must follow externally imposed rules 3. Objective financial information

1 -23

Types of Information

For management accounting, the The restrictions imposed on financial accounting tend to financial or nonfinancial produce objectivebe much more information may and verifiable financial information. subjective in nature.

Continued

1 -3

Objectives

5. Describe the role of management accountants in an organization. 6. Explain the importance of ethical behavior for managers and management accountants. 7. List three forms of certification available to management accountants.

1 -12

Management Process

The Management Process is defined by the following activities: Planning Controlling Decision Making

Decision making is the process of choosing among competing alternatives.

Lesson 4 Decision Making 英文管理会计课件 Management Accounting

between alternatives.

2020/6/17

The Concept of Relevant Cost Information

• Will you drive or fly to Florida for spring break?

2020/6/17

2: Different types of operating decisions

Learning objective • Using Incremental Analysis in different

operating decisions.

Required reading • Chapter 11, pages 301-318

decisions

Make or buy decisions

Joint product decisions

1: Relevant cost

Learning objective • Distinguish relevant from irrelevant

information in decisions situations.

decisions.

2020/6/17

Accepting Additional Business

The decision to accept additional business should be based on incremental costs and incremental revenues. Incremental amounts are those that occur if the company decides to accept the new business.

管理会计双语版总结PPT

第四页,共七十三页。

Chapter 3 :Determining Costs of Products

Job order costing

Direct material : trace Direct labor : trace Manufacturing overhead : allocate

Cost pool and allocation base Actual cost system vs. normal cost system Over-apply vs. under-apply

Three formulas (page 136)

Sensitivity analysis

8 第九页,共七十三页。

CVP Equations

Sales – Variable Costs – Fixed Costs = target profit

(SP/unit * units) – (VC/unit * units) – FC = target profit

Chapter 1: Introduction

Why management accounting? Origin and evolution of management

accounting Contrasting financial and management

accounting Ethical standards for management

Accounting rate of return

17

第十八页,共七十三页。

Chapter 9 : The Operating Budget

Different approaches to budgeting

管理会计英文课件

$ 0.026 $ 104 ???? $ 40 ???? ???? $ 25

12-9

Identifying Relevant Costs

Which costs and benefits are relevant in Cynthia’s decision? The cost of the car is a sunk cost and is not relevant to the current decision. The annual cost of insurance is not relevant. It will remain the same if she drives or takes the train.

12-3

Relevant Costs and Benefits

A relevant cost is a cost that differs between alternatives. A relevant benefit is a benefit that differs between alternatives.

Relaxing on the train is relevant even though it is difficult to assign a dollar value to the benefit.

The kennel cost is not relevant because Cynthia will incur the cost if she drives or takes the train.

However, the cost of gasoline is clearly relevant if she decides to drive. If she takes the train, the cost would not be incurred, so it varies depending on the decision.

管理会计英语英文版课件

Balance Sheet

As you know, the balance sheet reports assets, liabilities, and owners’ equity at a moment in time. The income statement summarizes revenue and expense transactions that occur during a period of time. Since revenue and expense transactions affect

Ex. assume that a machine has a cost of $4,900, an economic life of five years, and an estimated residual value of $400.

Annual depreciation expense=($4,900 - $400)/

There are several commonly used methods: straight-line, units-of-production , sum-of-theyears’ digits and declining-balance.

Methods of Calcine Method

The straight-line (SL) method allocates an equal

管理会计 双语课件 Management accounting

03 作业

High-Tech

Globalization

Economic Transition

03 作业 Need for innovation and relevant produces: – Activity-based management • ABC Improves accuracy of assigning costs

– Customer orientation

• Strategic positioning to maintain competitive advantage

• Value chain framework to focus on customer value

– Total quality management emphasized continuous improvement

1950-1980 1980-

Most of the product-costing and internal accounting procedures used in the last century were developed.

Emphasis of accounting information for internal management . Management accounting practices developed, including: Flexible budgeting, Standard costs, Variance analysis, transfer prices et al.

03 管理会计的定义

1 、国外会计学界的定义 1 )狭义管理会计 管理会计知识为企业内部管理者提供规划和控制所需信息的内部会计。 • 为企业管理当局的管理目标服务。

管理会计英语培训课程PPT课件(45张)

Short-term and Long-term Pricing Considerations

• The length of time a firm must commit its production capacity to fill that order is important because a long-term capacity commitment to a marginally profitable order may:

– Managers make decisions about establishing or accepting a price for their products

– Even when prices are set by the market and the firm has little or no influence on product prices, management still has to decide the best mix of products to manufacture and sell

– Such a firm is a price taker, and it chooses its product mix given the prices set in the marketplace for its products

Ability To Influence Prices

– Firms in an industry with relatively little competition, who enjoy large market shares and exercise industry leadership, must decide what prices to set for their products

lesson 8 Performance Management and Compensation 英文管理会计课件 Management Accounting

➢ Firms are increasingly presenting financial and nonfinancial performance measures for their subunits in a Balanced Scorecard, and it’s four perspectives:

14

Topic 3: Return on investment, residual income, and economic value added

Step 1: Choosing Among Different Performance Measures

➢ Four common measures of economic performance:

3. Choose a definition of the components in each Performance Measure

4. Choose a measurement alternative for each Performance Measure

5. Choose a target level of performance 6. Choose the timing of feedback

– Common costs

11

Topic 2: Responsibility centers and performance measures

Controllability Principle

➢The principle does not give the managers incentives to take actions that can affect the consequence of the uncontrollable event.

管理会计英文课件Chap008

8-2

Learning Objective 1

Understand why organizations budget and the processes they use to create budgets.

Profit Planning

Chapter 8

PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA

8-12

The Budget Committee

A standing committee responsible for

overall policy matters relating to the budget coordinating the preparation of the budget resolving disputes related to the budget approving the final budget

From the Sales Budget for April.

8-21

Expected Cash Collections

From the Sales Budget for May.

8-15

Learning Objective 2

Prepare a sales budget, including a schedule of expected cash collections.

管理会计英文课件

2. Allow the weakest link to set the tempo.

1. Identify the weakest link.

3. Focus on improving the weakest link. 4. Recognize that the weakest link is no longer so.

Maintain professional competence.

Competence

Provide accurate, clear, concise, and timely decision support information.

Follow applicable laws, regulations and standards.

Managerial Accounting and the Business Environment

Chapter 1

McGraw-Hill/Irwin

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

Customer Value Propositions

Board of Directors

Incentives and monitoring for

Top Management

To pursue objectives of

Stockholders

1-16

Enterprise Risk Management

Should I try to avoid the risk, share the risk, accept the risk, or reduce the risk?

管理会计英语课件01

A Brief History

• In 19th century America, textile mill owners kept detailed records of costs to direct efficiency improvement activities and to provide a basis for product pricing

Changing Focus

• Traditionally, management accounting information has been financial information – Denominated in a currency such as $ (dollars), £ (pound sterling), ¥ (yen), or € (euro) • Management accounting information has now expanded to encompass information that is operational or physical (nonfinancial) information: – Quality and process times – More subjective measurements, such as: • Customer satisfaction • Employee capabilities • New product performance

Management Accounting: Information That Creates Value

Chapter 1

Management Accounting Information

• The institute of Management Accountants has defined management accounting as:

成本管理会计课件(英文版)

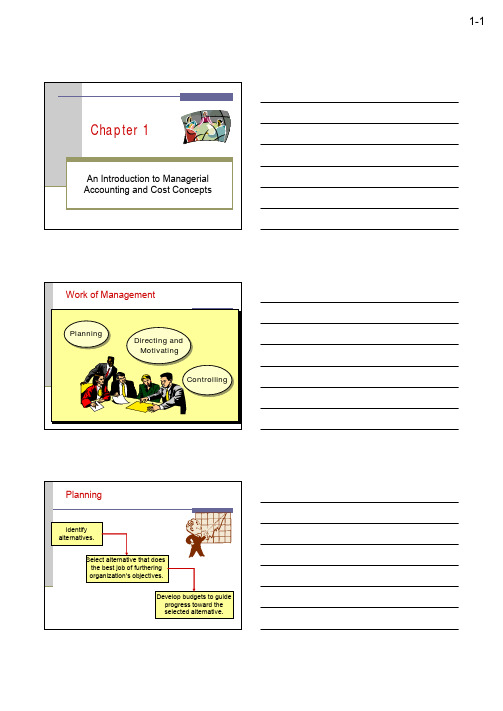

Chapter 1An Introduction to Managerial Accounting and Cost Concepts Work of ManagementPlanning Planning ControllingControlling Directing and MotivatingDirecting and Motivating PlanningIdentifyalternatives.Identify alternatives.Select alternative that does the best job of furthering organization’s objectives.Select alternative that does the best job of furthering organization’s objectives.Develop budgets to guide progress toward the selected alternative.Develop budgets to guide progress toward the selected alternative.Directing and MotivatingDirecting and motivating involves managing day-to-day activities to keep the organization running smoothly.n Employee work assignments.n Routine problem solving.n Conflict resolution.n Effective communications.ControllingThe control function ensuresthat plans are being followed.The control function ensures that plans are being followed. Feedback in the form of performance reports that compare actual results with the budget are an essential part of the control function.Feedback in the form of performance reports that compare actual results with the budget are an essential part of the control function.Planning and Control CycleDecision Making Formulating long-and short-termplans (Planning)Formulating long-and short-term plans (Planning)Measuringperformance(Controlling)Measuringperformance (Controlling)Implementing plans (Directingand Motivating)Implementing plans (Directing and Motivating)Comparing actual to planned performance(Controlling)Comparing actual to planned performance (Controlling)BeginComparison of Financial and Managerial AccountingFinancial Accounting Managerial Accounting1. Users External persons who Managers who plan formake financial decisions and control an organization2. Time focus Historical perspective Future emphasis3. Verifiability Emphasis on Emphasis on relevance versus relevance verifiability for planning and control4. Precision versus Emphasis on Emphasis on timeliness precision timeliness5. Subject Primary focus is on Focuses on segmentsthe whole organization of an organization6. GAAP Must follow GAAP Need not follow GAAPand prescribed formats or any prescribed format7. Requirement Mandatory for Notexternal reports MandatoryLearning Objective 1Identify and give examples ofeach of the three basicmanufacturing cost categories.The Product DirectMaterials Direct Materials Direct Labor Direct Labor Manufacturing OverheadManufacturing Overhead Manufacturing CostsDirect MaterialsRaw materials that become an integral part of the product and that can be conveniently traced directly to it.Example: A radio installed in an automobile Example: A radio installed in an automobile Direct LaborThose labor costs that can be easily traced to individual units of product.Example:Wages paid to automobile assembly workers Example:Wages paid to automobile assembly workers Manufacturing OverheadManufacturing costs cannot be traced directly to specific units produced.Examples:Indirect materials and indirect labor Examples:Indirect materials and indirect labor Wages paid to employees who are not directlyinvolved in productionwork.Examples:Maintenanceworkers, janitors andsecurity guards.Materials used to support the production process. Examples:Lubricants andcleaning supplies used in the automobile assembly plant.Classifications of Nonmanufacturing CostsSelling Costs Costs necessary to get the order and deliverthe product.AdministrativeCostsAll executive, organizational, and clerical costs.Learning Objective 2Distinguish betweenproduct costs and periodcosts and give examplesof each.Product Costs Versus Period CostsInventoryCost of Goods SoldBalance SheetIncomeStatement SaleProduct costs include direct materials, directlabor, andmanufacturingoverhead.Period costs are not included in product costs. They are expensed on the income statement.ExpenseIncomeStatementQuick Check üWhich of the following costs would beconsidered a period rather than a product cost in a manufacturing company?A. Manufacturing equipment depreciation.B. Property taxes on corporate headquarters.C. Direct materials costs.D. Electrical costs to light the production facility.E. Sales commissions.Which of the following costs would beconsidered a period rather than a product cost in a manufacturing company?A. Manufacturing equipment depreciation.B. Property taxes on corporate headquarters.C. Direct materials costs.D. Electrical costs to light the production facility.E. Sales commissions.Quick Check üPrime Cost and Conversion Cost Direct Material Direct Material Direct Labor Direct Labor Manufacturing OverheadManufacturing Overhead Prime Cost ConversionCost Manufacturing costs are oftenclassified as follows:Comparing Merchandising and Manufacturing ActivitiesMerchandisers . . .n Buy finished goods.n Sell finished goods.Manufacturers . . .n Buy raw materials.n Produce and sell finished goods.MegaLoMartBalance SheetMerchandiser Current Assets v Cash v Receivables v Prepaid Expenses v Merchandise Inventory Manufacturer Current Assets v Cashv Receivables v Prepaid Expenses v Inventories:1.Raw Materials2.Work in Process3.Finished GoodsMerchandiser Current Assets v Cash v Receivablesv Prepaid Expenses v Merchandise Inventory Manufacturer Current Assets v Cashv Receivables v Prepaid Expenses v Inventories:1.Raw Materials2.Work in Process3.Finished GoodsBalance SheetPartially complete products –some material, labor, oroverhead has been added. Completed productsawaiting sale. Materials waiting to be processed.Learning Objective 3Prepare an incomestatement includingcalculation of the cost ofgoods sold.The Income StatementCost of goods sold for manufacturers differs only slightly from cost of goodssold for merchandisers.Manufacturing Company Cost of goods sold: Beg. finished goods inv.14,200$ + Cost of goods manufactured 234,150 Goods available for sale 248,350$ - Endingfinished goods inventory (12,100)= Cost of goodssold 236,250$ Merchandising Company Cost of goods sold: Beg. merchandise inventory 14,200$ + Purchases 234,150 Goods available for sale 248,350$ - Ending merchandise inventory (12,100) = Cost of goodssold 236,250$ Inventory Flows Beginning balance Beginning balance Additions to inventory Additions to inventory +=Ending balance Endingbalance Withdrawals frominventory Withdrawalsfrom inventory +Quick Check üIf your inventory balance at the beginning of the month was $1,000, you bought $100 during the month, and sold $300 during the month, what would be the balance at the end of the month?A. $1,000.B. $ 800.C. $1,200.D. $ 200.If your inventory balance at the beginning of the month was $1,000, you bought $100 during the month, and sold $300 during the month, what would be the balance at the end of the month?A. $1,000.B. $ 800.C. $1,200.D. $ 200.Quick Check ü$1,000 + $100 = $1,100$1,100 -$300 = $800Learning Objective 4Prepare a schedule of cost of goods manufactured.Schedule of Cost of Goods Manufactured Calculates the cost of rawmaterial, direct labor andmanufacturing overheadused in production.Calculates the manufacturingcosts associated with goodsthat were finished during the period.ManufacturingWorkRaw Materials Costs In ProcessBeginning rawmaterials inventory +Raw materialspurchased =Raw materials available for usein production–Ending raw materialsinventory=Raw materials usedin productionAs items are removed from raw materials inventory and placed into the production process, they are called directmaterials.As items are removed from raw materials inventory and placed into the productionprocess, they are called direct materials.Schedule of Cost of Goods ManufacturedManufacturingWorkRaw Materials Costs In ProcessBeginning raw Direct materials materials inventory +Direct labor+Raw materials +Mfg. overhead purchased =Total manufacturing =Raw materials costs available for use in production –Ending raw materialsinventory=Raw materials used in production Conversion costs are costs incurred toconvert the direct material into a finishedproduct.Conversion costs are costs incurred to convert the direct material into a finished product.As items are removed from rawmaterials inventory and placed into the production process, they are called direct materials. As items are removed from raw materials inventory and placed into the production process, they are called direct materials. Schedule of Cost of Goods ManufacturedManufacturing WorkRaw Materials Costs In Process Beginning raw Direct materials Beginning work in materials inventory +Direct labor process inventory +Raw materials +Mfg. overhead +Total manufacturing purchased =Total manufacturing costs =Raw materials costs =Total work in available for use process for the in production period –Ending raw materials–Ending work in inventory process inventory=Raw materials used =Cost of goodsin production manufactured.All manufacturing costs incurred during the period are added to the beginning balance of work in process.All manufacturing costs incurred during the period are added to the beginning balance of work in process. Schedule of Cost of Goods Manufactured Manufacturing WorkRaw Materials Costs In Process Beginning raw Direct materials Beginning work in materials inventory +Direct labor process inventory +Raw materials +Mfg. overhead +Total manufacturing purchased =Total manufacturing costs =Raw materials costs =Total work in available for use process for the in production period –Ending raw materials –Ending work in inventory process inventory =Raw materials used =Cost of goods in production manufactured.Costs associated with the goods that are completed during the period are transferred to finished goods inventory.Costs associated with the goods that are completed during the period are transferred to finished goods inventory.Schedule of Cost of Goods ManufacturedWorkIn Process Finished GoodsBeginning work in Beginning finishedprocess inventory goods inventory+Manufacturing costs +Cost of goodsfor the period manufactured=Total work in process =Cost of goodsfor the period available for sale–Ending work in -Ending finishedprocess inventory goods inventory=Cost of goods Cost of goodsmanufactured sold Cost of Goods SoldManufacturing Cost FlowsSelling and Administrative Period Costs Finished Goods Cost ofGoodsSoldSelling and Administrative Manufacturing Overhead Work inProcessDirect Labor Balance Sheet Costs Inventories IncomeStatement Expenses Material Purchases Raw Materials Quick Check üBeginning raw materials inventory was $32,000. During the month, $276,000 of raw material was purchased. A count at the end of the month revealed that $28,000 of raw material was still present. What is the cost of direct material used?A.$276,000B.$272,000C.$280,000D.$ 2,000Beginning raw materials inventory was $32,000. During the month, $276,000 of raw material was purchased. A count at the end of the month revealed that $28,000 of raw material was still present. What is the cost of direct material used?A.$276,000B.$272,000C.$280,000D.$ 2,000Quick Check üBeg. raw materials 32,000$ +Raw materialspurchased 276,000=Raw materials availablefor use in production 308,000$ –Ending raw materialsinventory 28,000=Raw materials usedin production 280,000$Quick Check üDirect materials used in production totaled $280,000. Direct labor was $375,000 and factory overhead was $180,000. What were total manufacturing costs incurred for the month?A.$555,000B.$835,000C.$655,000D.Cannot be determined.Direct materials used in production totaled $280,000. Direct labor was $375,000 and factory overhead was $180,000. What were total manufacturing costs incurred for the month?A.$555,000B.$835,000C.$655,000D.Cannot be determined.Quick Check üDirect Materials 280,000$ +Direct Labor 375,000 +Mfg. Overhead 180,000=Mfg. Costs Incurredfor the Month 835,000$ Quick Check üBeginning work in process was $125,000. Manufacturing costs incurred for the month were $835,000. There were $200,000 of partially finished goods remaining in work in process inventory at the end of the month. What was the cost of goods manufactured during the month?A.$1,160,000B.$ 910,000C.$ 760,000D.Cannot be determined.Beginning work in process was $125,000. Manufacturing costs incurred for the month were $835,000. There were $200,000 of partially finished goods remaining in work in process inventory at the end of the month. What was the cost of goods manufactured during the month?A.$1,160,000B.$ 910,000C.$ 760,000D.Cannot be determined.Quick Check üBeginning work inprocess inventory 125,000$ +Mfg. costs incurredfor the period 835,000=Total work in processduring the period 960,000$ –Ending work inprocess inventory 200,000=Cost of goodsmanufactured 760,000$ Quick Check üBeginning finished goods inventory was $130,000. The cost of goods manufactured for the month was $760,000. The ending finished goods inventory was $150,000. What was the cost of goods sold for the month?A. $ 20,000.B. $740,000.C. $780,000.D. $760,000.Beginning finished goods inventory was$130,000. The cost of goods manufactured for the month was $760,000. The ending finished goods inventory was $150,000. What was the cost of goods sold for the month?A. $ 20,000.B. $740,000.C. $780,000.D. $760,000.Quick Check ü$130,000 + $760,000 = $890,000$890,000 -$150,000 = $740,000Learning Objective 5Define and giveexamples of variablecosts and fixed costs.Cost Classifications for Predicting Cost BehaviorHow a cost will react to changes in the level of business activity.v Total variable costschange when activitychanges.v Total fixed costs remainunchanged when activitychanges.How a cost will react to changes in the level of business activity.v Totalvariable costs change when activity changes.v Total fixed costs remain unchanged when activity changes.Total Variable Cost Your total long distance telephone bill is based on how many minutes you talk.Minutes Talked Tot a lL o n g D is t a n ceT elephon eBillVariable Cost Per UnitMinutes TalkedP e rM i n u te TelephoneC h argeThe cost per long distance minute talked is constant. For example, 10 cents per minute.Total Fixed CostYour monthly basic telephone bill probably does not change when youmake more local calls.Number of Local CallsM o n t h ly B a s icTelephoneB ill Fixed Cost Per Unit Number of Local Calls M o n t h l y B a s i c T e l e p h on eBillpe rLocalCa l lThe average fixed cost per local call decreases as more local calls are made.Cost Classifications for Predicting Cost BehaviorBehavior of Cost (within the relevant range)Cost In Total Per UnitVariable Total variable cost changes Variable cost per unit remains as activity level changes.the same over wide rangesof activity.Fixed Total fixed cost remains Average fixed cost per unit goes the same even when the down as activity level goes up.activity level changes.Quick Check üWhich of the following costs would be variable with respect to the number of cones sold at aBaskins & Robbins shop? (There may bemore than one correct answer.)A. The cost of lighting the store.B. The wages of the store manager.C. The cost of ice cream.D. The cost of napkins for customers.Quick Check üWhich of the following costs would be variable with respect to the number of cones sold at aBaskins & Robbins shop? (There may bemore than one correct answer.)A. The cost of lighting the store.B. The wages of the store manager.C. The cost of ice cream.D. The cost of napkins for customers.Learning Objective 6Define and giveexamples of direct andindirect costs. Assigning Costs to Cost ObjectsDirect costsn Costs that can beeasily and convenientlytraced to a unit ofproduct or other costobject.n Examples: Directmaterial and direct labor Indirect costsn Costs that cannot be easily and convenientlytraced to a unit ofproduct or other costobject.n Example: Manufacturing overheadLearning Objective 7Define and give examples ofcost classifications used inmaking decisions: differentialcosts, opportunity costs, andsunk costs.Cost Classifications for Decision MakingEvery decision involves a choicebetween at least two alternatives. Only those costs andbenefits that differbetween alternativesare relevant to thedecision. All othercosts and benefits canand should be ignored.Differential Costs and RevenuesCosts and revenues that differamong alternatives. Example:You have a job paying $1,500 per month in your hometown. You have a job offer in a neighboring city that pays $2,000 per month. The commuting cost to the city is $300 per month.Differential revenue is: $2,000 –$1,500 = $500Differential cost is:$300Net Differential Benefit is:$200Opportunity CostsThe potential benefit that is given up when one alternative is selectedover another.Example:If you werenot attending college,you could be earning$15,000 per year.Your opportunity costof attending college forone year is $15,000.Sunk CostsSunk costs cannot be changed by any decision. They are not differential costs and should be ignored when making decisions. Example:You bought an automobile that cost $10,000 two years ago. The $10,000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the $10,000 cost. Quick Check üSuppose you are trying to decide whether todrive or take the train to Portland to attend a concert. You have ample cash to do either, butyou don’t want to waste money needlessly. Isthe cost of the train ticket relevant in thisdecision? In other words, should the cost of thetrain ticket affect the decision of whether youdrive or take the train to Portland?A. Yes, the cost of the train ticket is relevant.B. No, the cost of the train ticket is notrelevant.Quick Check üSuppose you are trying to decide whether todrive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the cost of the train ticket relevant in this decision? In other words, should the cost of the train ticket affect the decision of whether you drive or take the train to Portland?A. Yes, the cost of the train ticket is relevant.B. No, the cost of the train ticket is notrelevant.Quick Check üSuppose you are trying to decide whether to drive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the annual cost of licensing your car relevant in this decision?A. Yes, the licensing cost is relevant.B. No, the licensing cost is not relevant.Quick Check üSuppose you are trying to decide whether to drive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the annual cost of licensing your car relevant in this decision?A. Yes, the licensing cost is relevant.B. No, the licensing cost is not relevant.Quick Check üSuppose that your car could be sold now for $5,000. Is this a sunk cost?A. Yes, it is a sunk cost.B. No, it is not a sunk cost.Suppose that your car could be sold now for $5,000. Is this a sunk cost?A. Yes, it is a sunk cost.B. No, it is not a sunk cost.Quick Check üSummary of the Types of Cost ClassificationsFinancial Reporting PredictingCost BehaviorAssigning Costs to Cost Objects Decision MakingEnd of Chapter 1。

管理会计第一章(英文版)

targets included in

system should be set at such a level that m an ag e r s and th e people who work for them are motivated to achieve them.

02

Describe and explain the essential requirements of a management accounting system

Chapter catalogue

Management Accounting Information

Collection and Measurement of Information 内容说明内容说明内容说明 Information for Strategic, Operational and Management 内容说明内容说明内容说明 Control

1.4 The Effect of Management Style and Structure

Style

Autocratic vs democratic 内容说明

Structure

内容说明 内容说明

02

An autocratic style, by contrast, means that decision 内容说明 making is exercised at a higher level and therefore the necessary information to enable the function to be carried out will similarly be provided at this level also.

财务管理会计案例培训课件英文版

Product-Level Activity

Organizationsustaining Activity

Customer-Level Activity

Identifying Activity to Include

Activity Cost Pool is a “bucket” in

Factory equipment depreciation

$300,000

Percent consumed by customer orders 20%

$ 60,000

Assigning Costs to Activity Cost Pools

Using the total costs and percentage consumption of overhead, costs are assigned to activity pools.

and then to products.

Departmental Overhead Rates

Indirect

Stage One:

Labor

Costs assigned

to pools

Cost pools

Department 1

Indirect Materials

Department 2

Other Overhead

Activity Based Costing

Departmental Overhead Rates

Plantwide Overhead

Rate

Overhead Allocation

Plantwide Overhead Rate

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Accounting-related Lenders Consultants Analysts Traders Managers Directors Underwriters Planners Appraisers

Financial Statements

Financial statements report on the financial performance and condition of an organization. There are four major financial statements Income Statement Balance Sheet Statement of Owner’s Equity Statement of Cash Flows

The system for recording debits and credits follows from the accounting equation: Assets = Liabilities + Owner’s Equity

Equity

Owner’s capital- Owner’s withdrawals+ RevenuesExpenses

Business Profit

Revenues: Amounts earned from selling products or services -Expenses: Costs incurred with revenues =Profit: Amounts earned from revenues less expenses incurred Loss occurs when expenses are more than revenues

The T-Account

The T-account is used as a simple tool for illustrating the balance in a given account . Account Title

(Left Side) Debit

(Right Side) Credit

Focus of Accounting

Identifying Economic Events Recording Economic Events Reporting and Analyzing Economic Events

Accounting and Technology

Reduces time, effort and cost of record-keeping Improves clerical accuracy Changes the way we store, process and summarize large masses of data

Normal Balances

The normal balance of each account refers to the debit or credit side where increases are recorded Assets= Liabilities + Owner’s Equity Debit Credit Debit Credit Debit Credit + + + Normal Normal Normal

Debits and Credits

Within every individual account, debits and credits have opposite effects.

Therefore, in an account where a debit is an increase, a credit is a decrease and vice versa.

Double-Entry Accounting

Double-entry accounting means every transaction affects and is recorded in at least two accounts. The total amount debited must equal the total amount credited for each transaction.

Accounting Equation

The accounting equation must remain in balance after each transaction.

Assets=Liabilities + Equity

The Account

The account is a detailed record of increases and decreases in specific assets, liabilities and equities. Asset Accounts Assets are resources controlled by an organization that have current and future benefits. cash, accounts receivable, notes receivable, office supplies, store supplies, prepaid insurance, equipment, buildings, land

ቤተ መጻሕፍቲ ባይዱ

A balance sheet reports on an organization’s financial position at a point in time The income statement , statement of owner’s equity and statement of cash flows report on performance over a period of time

Liabilities Accounts Liabilities are obligation to transfer assets or provide services to other entities. accounts payable, notes payable, unearned revenues, other liabilities Equity Accounts owner’s capital, owner’s withdrawal, revenues, expenses

Income Statement

Statement of Owner’s Equity

Balance Sheet

Fundamental Principles of Accounting Generally Accepted Accounting Principles (GAAP) 1.Business Entity Principle A business is accounted for separately from its owner or owners. 2. Objectivity Principle Financial statement information is supported by independent, unbiased evidence.

MODULE 1 UNDERSTANDING FINANCIAL STATEMENTS

Accounting Review

Power of Accounting

Accounting is a system that Identifies, Measures,Records, Communicates information that is Relevant, Reliable, Consistent, Comparable to help users make better decisions

Balance of an Account

An account balance is the difference between the increases and decreases in an account Total increases – Total decreases =Balance

Managerial accounting is the area of accounting aimed at serving the decisionmaking needs of internal users. It provides special purpose reports customize to meet the information needs of internal users. general accounting, cost accounting, budgeting,internal auditing, management consulting

Forms of Organization

Business :Sole Proprietorship , Partnership Corporation Non-business

Users of Accounting Information

Internal Users Managers ,Officers ,Internal Auditors Sales Managers ,Budget Officers Controller External Users Lenders ,Shareholders ,Government , Labour Unions ,External Auditors , Customers

Managerial General Accounting Cost Accounting Budgeting Internal Auditing Management -consulting services