审计学一种整合的方法

审计学:一种整合方法(14)学习笔记

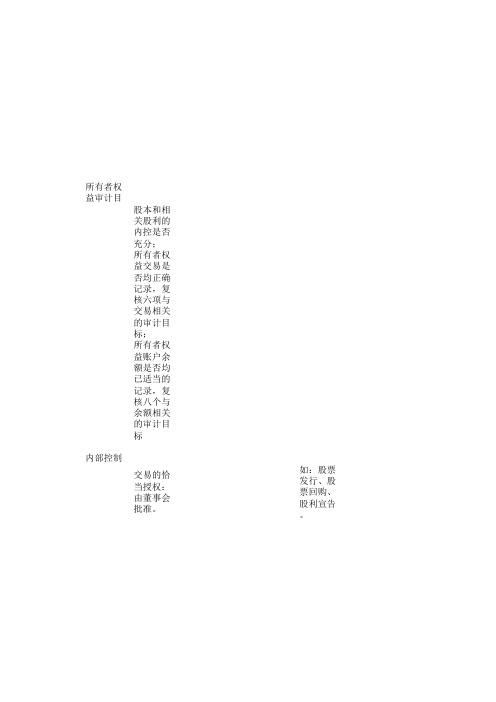

所有者权益审计目标股本和相关股利的内控是否充分;所有者权益交易是否均正确记录,复核六项与交易相关的审计目标;所有者权益账户余额是否均已适当的记录,复核八个与余额相关的审计目标内部控制交易的恰当授权:由董事会批准。

如:股票发行、股票回购、股利宣告。

正确的记录和职责分离:记录实际的股票持有着,以确保向其方法股利;股利支付支票由不股本审计所有发生的股本交易均已记录(完整):如果聘请了证券登记代理商、股票会议记录,特别是接近报表日的会议记录;审查股票登记簿;所有记录的都确实发生且记录准确(发生、准确):对所有的交易进行验证金收入日记账,确认会计记录是否正确;根据公司章程确定的股票面值的规定,确认股本溢股本记录准确:向股票过户代理机构函证确认资产负债表日发行在外的股份数;或审查股票记录股本已恰当地表达与披露股利审计:重点:交易审计;而非余额审计;如果有应付股利,则例外。

1、存在性审查董事会会议记录来确定每股股利和股利宣告的授权;关注已2、准确性每股股利与流通在外的股数的乘积计算已宣告鼓励的金额;如果如果自己制作股利并发放,通过重新计算和审阅现金支出记录来验证股利金额从股利支付中选取一个样本,将支票上的收款人姓名追查至股东记录,以确信收款人具有股计目标票回购、股利宣告。

其方法股利;股利支付支票由不负责股本记录的雇员填写;并对股东姓名和支票金额独立核对。

外的股份数;或审查股票记录和股权登记证明登记簿中所有流通在外的股票的会计记录;然后乘以面值来验证股本账户中记录授权;关注已宣告还未发放的股利;的金额;如果通过代理人发放,追查股利至向代理人支付现金的分录,同时进行函证;录来验证股利金额股东记录,以确信收款人具有股东资格;、股票过户代理机构,则向其函证股本交易是否发生、发生的交易记录是否准确;复核董事会;行验证:验证董事会会议记录,相关业务是否得到授权?向股票过户代理机构函证;追查至现的股票面值的规定,确认股本溢价金额是否正确。

审计学-一种整合的方法

Steps to Develop Audit Objectives

•4. Know general audit objectives for • classes of transactions and accounts.

•5. Know specific audit objectives for • classes of transactions and accounts.

➢ Actions when the auditor knows of an illegal act

Learning Objective 4

Classify transactions and account balances into financial statement cycles and identify benefits of a cycle approach to segmenting the audit.

Auditor’s Responsibilities for Discovering Illegal Acts

➢ Evidence accumulation and other actions • when there is reason to believe direct- or • indirect-effect illegal acts may exist

•The Sarbanes-Oxley Act provides for criminal •penalties for anyone who knowingly falsely •certifies the statements.

Learning Objective 3

Explain the auditor’s responsibility for discovering material misstatements.

阿伦斯 审计学:一种整合方法 课后习题答案

Chapter 1The Demand for Audit and Other Assurance Services Review Questions1-1The relationship among audit services, attestation services, and assurance services is reflected in Figure 1-3 on page 13 of the text. An assurance service is an independent professional service to improve the quality of information for decision makers. An attestation service is a form of assurance service in which the CPA firm issues a report about the reliability of an assertion that is the responsibility of another party. Audit services are a form of attestation service in which the auditor expresses a written conclusion about the degree of correspondence between information and established criteria.The most common form of audit service is an audit of historical financial statements, in which the auditor expresses a conclusion as to whether the financial statements are presented in conformity with generally accepted accounting principles. An example of an attestation service is a report on the effe ctiveness of an entity’s internal control over financial reporting. There are many possible forms of assurance services, including services related to business performance measurement, health care performance, and information system reliability.1-2 An independent audit is a means of satisfying the need for reliable information on the part of decision makers. Factors of a complex society which contribute to this need are:1.Remoteness of informationa.Owners (stockholders) divorced from managementb.Directors not involved in day-to-day operations ordecisionsc.Dispersion of the business among numerous geographiclocations and complex corporate structures2.Biases and motives of providerrmation will be biased in favor of the providerwhen his or her goals are inconsistent with thedecision maker's goals.3.Voluminous dataa.Possibly millions of transactions processed daily viasophisticated computerized systemsb.Multiple product linesc.Multiple transaction locationsplex exchange transactionsa.New and changing business relationships lead toinnovative accounting and reporting problemsb.Potential impact of transactions not quantifiable,leading to increased disclosures1-3 1. Risk-free interest rate This is approximately the rate the bank could earn by investing in U.S. treasury notes for thesame length of time as the business loan.2.Business risk for the customer This risk reflects thepossibility that the business will not be able to repay itsloan because of economic or business conditions such as arecession, poor management decisions, or unexpectedcompetition in the industry.rmation risk This risk reflects the possibility thatthe information upon which the business risk decision wasmade was inaccurate. A likely cause of the information riskis the possibility of inaccurate financial statements.Auditing has no effect on either the risk-free interest rate or business risk. However, auditing can significantly reduce information risk.1-4The four primary causes of information risk are remoteness of information, biases and motives of the provider, voluminous data, and the existence of complex exchange transactions.The three main ways to reduce information risk are:er verifies the information.er shares the information risk with management.3.Audited financial statements are provided.The advantages and disadvantages of each are as follows:1-5 To do an audit, there must be information in a verifiable form and some standards (criteria) by which the auditor can evaluate the information. Examples of established criteria include generally accepted accounting principles and the Internal Revenue Code. Determining the degree of correspondence between information and established criteria is determining whether a given set of information is in accordance with the established criteria. The information for Jones Company's tax return is the federal tax returns filed by the company. The established criteria are found in the Internal Revenue Code and all interpretations. For the audit of Jones Company's financial statements the information is the financial statements being audited and the established criteria are generally accepted accounting principles.1-6The primary evidence the internal revenue agent will use in the audit of the Jones Company's tax return include all available documentation and other information available in Jones' office or from other sources. For example, when the internal revenue agent audits taxable income, a major source of information will be bank statements, the cash receipts journal and deposit slips. The internal revenue agent is likely to emphasize unrecorded receipts and revenues. For expenses, major sources of evidence are likely to be cancelled checks, vendors' invoices and other supporting documentation.1-7This apparent paradox arises from the distinction between the function of auditing and the function of accounting. The accounting function is the recording, classifying and summarizing of economic events to provide relevant information to decision makers. The rules of accounting are the criteria used by the auditor for evaluating the presentation of economic events for financial statements and he or she must therefore have an understanding of generally accepted accounting principles (GAAP), as well as auditing standards. The accountant need not, and frequently does not, understand what auditors do, unless he or she is involved in doing audits, or has been trained as an auditor.1-81-9Five examples of specific operational audits that could be conducted by an internal auditor in a manufacturing company are:1.Examine employee time cards and personnel records todetermine if sufficient information is available to maximizethe effective use of personnel.2.Review the processing of sales invoices to determine if itcould be done more efficiently.3.Review the acquisitions of goods, including costs, todetermine if they are being purchased at the lowest possiblecost considering the quality needed.4.Review and evaluate the efficiency of the manufacturingprocess.5.Review the processing of cash receipts to determine if theyare deposited as quickly as possible.1-10 When using a strategic systems auditing approach in an audit of historical financial statements, an auditor must have a thorough understanding of the client and its environment. This knowledge should include the client’s regulatory and operating environment, business strategies and processes, and measurement indicators. The strategic systems approach is also useful in other assurance or consulting engagements. For example, an auditor who is performing an assurance service on information technology would need to understand the client’s business strategies and processes related to information technology, including such things as purchases and sales via the Internet. Similarly, a practitioner performing a consulting engagement to evaluate the efficiency and effectiveness of a cli ent’s manufacturing process would likely start with an analysis of various measurement indicators, including ratio analysis and benchmarking against key competitors.1-11 The major differences in the scope of audit responsibilities are:1.CPAs perform audits in accordance with auditing standards ofpublished financial statements prepared in accordance withgenerally accepted accounting principles.2.GAO auditors perform compliance or operational audits inorder to assure the Congress of the expenditure of publicfunds in accordance with its directives and the law.3.IRS agents perform compliance audits to enforce the federaltax laws as defined by Congress, interpreted by the courts,and regulated by the IRS.4.Internal auditors perform compliance or operational auditsin order to assure management or the board of directors thatcontrols and policies are properly and consistentlydeveloped, applied and evaluated.1-12 The four parts of the Uniform CPA Examination are: Auditing and Attestation, Financial Accounting and Reporting, Regulation, and Business Environment and Concepts.1-13 It is important for CPAs to be knowledgeable about e-commerce technologies because more of their clients are rapidly expanding their use of e-commerce. Examples of commonly used e-commerce technologiesinclude purchases and sales of goods through the Internet, automatic inventory reordering via direct connection to inventory suppliers, and online banking. CPAs who perform audits or provide other assurance services about information generated with these technologies need a basic knowledge and understanding of information technology and e-commerce in order to identify and respond to risks in the financial and other information generated by these technologies.Multiple Choice Questions From CPA Examinations1-14 a. (3) b. (2) c. (2) d. (3)1-15 a. (2) b. (3) c. (4) d. (3)Discussion Questions And Problems1-16 a. The relationship among audit services, attestation services and assurance services is reflected in Figure 1-3 on page 13of the text. Audit services are a form of attestationservice, and attestation services are a form of assuranceservice. In a diagram, audit services are located within theattestation service area, and attestation services arelocated within the assurance service area.b. 1. (1) Audit of historical financial statements2.(2) An attestation service other than an auditservice; or(3) An assurance service that is not an attestationservice (WebTrust developed from the AICPASpecial Committee on Assurance Services, but theservice meets the criteria for an attestationservice.)3.(2) An attestation service other than an auditservice4.(2) An attestation service other than an auditservice5.(2) An attestation service other than an auditservice6.(2) An attestation service that is not an auditservice (Review services are a form ofattestation, but are performed according toStatements on Standards for Accounting andReview Services.)7.(2) An attestation service other than an auditservice8.(2) An attestation service other than an auditservice9.(3) An assurance service that is not an attestationservice1-17 a. The interest rate for the loan that requires a review report is lower than the loan that did not require a review becauseof lower information risk. A review report provides moderateassurance to financial statement users, which lowersinformation risk. An audit report provides further assuranceand lower information risk. As a result of reducedinformation risk, the interest rate is lowest for the loanwith the audit report.b.Given these circumstances, Vial-tek should select the loanfrom City First Bank that requires an annual audit. In thissituation, the additional cost of the audit is less than thereduction in interest due to lower information risk. Thefollowing is the calculation of total costs for each loan:1-17 (continued)c. Vial-tek may desire to have an audit because of the manyother positive benefits that an audit provides. The auditwill provide Vial-tek’s management with assurance aboutannual financial information used for decision-makingpurposes. The audit may detect errors or fraud, and providemanagement with information about the effectiveness ofcontrols. In addition, the audit may result inrecommendations to management that will improve efficiencyor effectiveness.d. Under a strategic systems audit approach, the auditor musthave a thorough understanding of the client and itsenvironment, including the client’s e-commerce technologies,industry, regulatory and operating environment, suppliers,customers, creditors, and business strategies and processes.This thorough analysis helps the auditor identify risksassociated with the client’s strategies that may affectwhether the financial statements are fairly stated. Whenapplying the strategic systems audit approach, the auditoroften discovers ways to help the client improve businessoperations, thereby providing added value to the auditfunction.1-18 a. The services provided by Consumers Union are very similar to assurance services provided by CPA firms. The servicesprovided by Consumers Union and assurance services providedby CPA firms are designed to improve the quality ofinformation for decision makers. CPAs are valued for theirindependence, and the reports provided by Consumers Unionare valued because Consumers Union is independent of theproducts tested.b.The concepts of information risk for the buyer of anautomobile and for the user of financial statements areessentially the same. They are both concerned with theproblem of unreliable information being provided. In thecase of the auditor, the user is concerned about unreliableinformation being provided in the financial statements. Thebuyer of an automobile is likely to be concerned about themanufacturer or dealer providing unreliable information.c.The four causes of information risk are essentially the samefor a buyer of an automobile and a user of financialstatements:(1)Remoteness of information It is difficult for a userto obtain much information about either an automobilemanufacturer or the automobile itself withoutincurring considerable cost. The automobile buyer doeshave the advantage of possibly knowing other users who are satisfied or dissatisfied with a similar automobile.(2)Biases and motives of provider There is a conflictbetween the automobile buyer and the manufacturer. The buyer wants to buy a high quality product at minimum cost whereas the seller wants to maximize the selling price and quantity sold.(3)Voluminous data There is a large amount of availableinformation about automobiles that users might like to have in order to evaluate an automobile. Either that information is not available or too costly to obtain.1-18 (continued)(4)Complex exchange transactions The acquisition of anautomobile is expensive and certainly a complexdecision because of all the components that go intomaking a good automobile and choosing between a largenumber of alternatives.d.The three ways users of financial statements and buyers ofautomobiles reduce information risk are also similar:(1)User verifies information him or herself That can beobtained by driving different automobiles, examiningthe specifications of the automobiles, talking toother users and doing research in various magazines.(2)User shares information risk with management Themanufacturer of a product has a responsibility to meetits warranties and to provide a reasonable product.The buyer of an automobile can return the automobilefor correction of defects. In some cases a refund maybe obtained.(3)Examine the information prepared by Consumer ReportsThis is similar to an audit in the sense thatindependent information is provided by an independentparty. The information provided by Consumer Reports iscomparable to that provided by a CPA firm that auditedfinancial statements.1-19 a. The following parts of the definition of auditing are related to the narrative:(1)Virms is being asked to issue a report aboutqualitative and quantitative information for trucks.The trucks are therefore the information with whichthe auditor is concerned.(2)There are four established criteria which must beevaluated and reported by Virms: existence of thetrucks on the night of June 30, 2005, ownership ofeach truck by Regional Delivery Service, physicalcondition of each truck and fair market value of eachtruck.(3)Susan Virms will accumulate and evaluate four types ofevidence:(a)Count the trucks to determine their existence.(b)Use registrations documents held by Oatley forcomparison to the serial number on each truck todetermine ownership.(c)Examine the trucks to determine each truck'sphysical condition.(d)Examine the blue book to determine the fairmarket value of each truck.(4)Susan Virms, CPA, appears qualified, as a competent,independent person. She is a CPA, and she spends most of her time auditing used automobile and truck dealerships and has extensive specialized knowledge about used trucks that is consistent with the nature of the engagement.1-19(continued)(5)The report results are to include:(a)which of the 35 trucks are parked in Regional'sparking lot the night of June 30.(b)whether all of the trucks are owned by RegionalDelivery Service.(c)the condition of each truck, using establishedguidelines.(d)fair market value of each truck using thecurrent blue book for trucks.b.The only parts of the audit that will be difficult for Virmsare:(1)Evaluating the condition, using the guidelines of poor,good, and excellent. It is highly subjective to do so.If she uses a different criterion than the "bluebook," the fair market value will not be meaningful.Her experience will be essential in using thisguideline.(2)Determining the fair market value, unless it isclearly defined in the blue book for each condition.1-20 a. The major advantages and disadvantages of a career as an IRS agent, CPA, GAO auditor, or an internal auditor are:1-20 (continued)EMPLOYMENT ADVANTAGES DISADVANTAGESINTERNAL AUDITOR 1.Extensive exposure to allsegments of theenterprise with whichemployed.2.Constant exposure to oneindustry presentingopportunity for expertisein that industry.3.Likely to have exposureto compliance, financialand operational auditing.1.Little exposure totaxation and the auditthereof.2.Experience is limited toone enterprise, usuallywithin one or a limitednumber of industries.(b)Other auditing careers that are available are:Auditors within many of the branches of the federalgovernment ., Atomic Energy Commission)Auditors for many state and local government units .,state insurance or bank auditors)1-21 The most likely type of auditor and the type of audit for each of the examples are:EXAMPLE TYPE OF AUDITOR TYPE OF AUDIT1.2.3.4.5.6.7.8.9.10.11.12.IRSGAOInternal auditor or CPACPA or Internal auditorGAOCPAGAOIRSCPAInternal auditor or CPAInternal auditor or CPAGAOComplianceOperationalOperationalFinancial statementsOperationalFinancial statementsFinancial statementsComplianceFinancial statementsComplianceFinancial statementsCompliance1-22 a. The conglomerate should either engage the management advisory services division of a CPA firm or its own internalauditors to conduct the operational audit.b.The auditors will encounter problems in establishingcriteria for evaluating the actual quantitative events andin setting the scope to include all operations in whichsignificant inefficiencies might exist. In writing thereport, the auditors must choose proper wording to statethat no financial audit was performed, that the procedureswere limited in scope and that the results reported do notnecessarily include all the inefficiencies that might exist.1-23 a. The CPA firm for the Internet company described in this problem could address these customer concerns by performinga WebTrust attestation engagement. The WebTrust assuranceservice was created by the profession to respond to thegrowing need for assurance resulting from the growth ofbusiness transacted over the Internet.b.The appropriate WebTrust principle for each of the customerconcerns noted in the problem is as follows:1.Accuracy of product descriptions and adherence tostated return policies: (3) Processing Integrity.2.Credit card and other personal information: (1) OnlinePrivacy and (2) Security.3.Selling information to other companies: (1) OnlinePrivacy and (2) Security.4.System failure: (4) Availability.Internet Problem Solution: Assurance Services1-1 This problem requires students to work with the AICPA assurance services Web site.1.Considering the assurance needs of customers and thecapabilities of CPAs, the Special Committee on AssuranceServices developed business plans for six assurance services.Chapter 1 of the textbook discussed several of theseservices. Go to the service description for the assuranceservice that most interests you (any one of the six). Whatare the major aspects or sections of the associated businessplan ., does the plan address market potential, competition,etc.?)Answer: Each business plan provides background information,describes the service, assesses market potential, discussesissues such as competition and why CPAs should offer theservice, identifies practice tools available and steps thatCPAs must take to begin offering the services.2.The Special Committee's report on Assurance Servicesdiscusses competencies needed by assurance providers todayand in the coming decade. Briefly describe the 5 generalcompetencies needed in the next decade (Hint: See the“About Assurance Services” link. Then follow the“Assurance Services and Academia” link.)Answer:The Committee identified the following five majorimperatives regarding future competencies, each of whichimplies increasing emphasis on the competencies noted:1-1 (continued)Customer focus.Assurance service providers need tounderstand user decision processes and how informationshould enter into those processes. Increased emphasis isneeded on: understanding user needs, communication skills,relationship management, responsiveness and timeliness.Migration to higher value-added information activities. Toprovide more value to client/decision makers and others,assurance service providers need to focus less on activitiesinvolved in the conversion of business events intoinformation ., collecting, classifying, and summarizingactivities) and more on activities involved in thetransformation of information into knowledge ., analyzing,interpreting, and evaluating activities) that effectivelydrives decision processes. This will require: analyticalskills, business advisory skills, business knowledge, modelbuilding (including sensitivity analysis), understanding theclient’s business processes, measurement theory(development of operational definitions of concepts, designof appropriate measurement techniques, etc.).Information technology (IT).Assurance services deal ininformation. Hence, the profound changes occurring ininformation technology will shape virtually all aspects ofassurance services. As information specialists, assuranceservice providers need to embrace information technology inall of its complex dimensions. Embracing IT meansunderstanding how it is transforming all aspects of business.It also means learning how to effectively use newdevelopments in hardware, software, communications, memory,encryption, etc., in everything assurance service providersdo as information specialists, not only in dealing withclients, but also in dealing with each other as individuals,teams, firms, state societies, and national professionalorganizations.Pace of change and complexity. Assurance services will takeplace in an environment of rapid change and increasingcomplexity. Assurance service providers need to investheavily in life-long learning in order to maintain up-to-date knowledge and skills. They will require: intellectualcapability, learning and rejuvenation.Competition.Growth in new assurance services will dependless on franchise/regulation and more on market forces.Assurance service providers need to develop their marketingskills —the ability to see clients’ latent informationand assurance needs and rapidly design and deploy cost-effective services to meet those needs —in order toeffectively compete for market-driven assurance services.Required skills include: marketing and selling,understanding customer needs, designing and deployingeffective solutions.1-1 (continued)(Note: Internet problems address current issues using Internet sources. Because Internet sites are subject to change, Internet problems and solutions are subject to change. Current information on Internet problems is available at。

审计学 一种整合方法 Auditingand Assurance Services An integrated approach Test Bank chapter 9

Auditing and Assurance Services, 15e (Arens)Chapter 9 Materiality and RiskLearning Objective 9-11) If it is probable that the judgment of a reasonable person will be changed or influenced by the omission or misstatement of information, then that information is, by definition of FASB Statement No. 2:A) material.B) insignificant.C) significant.D) relevant.Answer: ATerms: FASB Statement No. 2; Probable judgment of a reasonable personDiff: EasyObjective: LO 9-1AACSB: Reflective thinking skills2) The scope paragraph of the standard unqualified auditor's report states that "… the standards require that we plan and perform the audit to obtain ________ assurance about whether the financial statements are free of material misstatement." What type of assurance is given?A) ImmediateB) LimitedC) ReasonableD) AbsoluteAnswer: CTerms: Type of assurance providedDiff: EasyObjective: LO 9-1AACSB: Reflective thinking skills3) Auditors are responsible for determining whether financial statements are materially misstated, so upon discovering a material misstatement they must bring it to the attention of:A) regulators.B) the audit firm's managing partner.C) the client shareholders.D) the client.Answer: DTerms: Discovery of a material misstatement must bring it to the attentionDiff: EasyObjective: LO 9-1AACSB: Reflective thinking skills4) Determining materiality requires professional judgment.Answer: TRUETerms: MaterialityDiff: EasyObjective: LO 9-1AACSB: Reflective thinking skillsLearning Objective 9-21) Audit standards require the auditor to consider materiality early in the audit. Which statement(s) regarding preliminary materiality are true?I. Preliminary materiality may change during the engagement.II. Preliminary materiality is the maximum amount by which the auditor believes the financials could be misstated and still not affect the decisions of reasonable users.A) I onlyB) II onlyC) both I and IID) neither are trueAnswer: CTerms: Preliminary materiality assessmentDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills2) Why do auditors establish a preliminary judgment about materiality?A) To determine the appropriate level of staff to assign to the auditB) So that the client can know what records to make available to the auditorC) To help plan the appropriate evidence to accumulateD) To finalize the control risk assessmentAnswer: CTerms: Purpose to establish preliminary judgment about materialityDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills3) If an auditor establishes a relatively high level for materiality, then the auditor will:A) accumulate more evidence than if a lower level had been set.B) accumulate less evidence than if a lower level had been set.C) accumulate approximately the same evidence as would be the case were materiality lower.D) accumulate an undetermined amount of evidence.Answer: BTerms: High level for materialityDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills4) The preliminary judgment about materiality and the amount of audit evidence accumulated are________ related.A) directlyB) indirectlyC) notD) inverselyAnswer: DTerms: Preliminary judgment about materiality and amount of evidence accumulatedDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills5) Which of the following is the primary basis used to decide materiality for a for-profit entity?A) Net salesB) Net assetsC) Net income before taxD) All of the aboveAnswer: CTerms: Primary basis to decide materiality for a for-profit entityDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills6) Auditing standards ________ that the basis used to determine the preliminary judgment about materiality be documented in the audit files.A) permitB) do not allowC) requireD) strongly encourageAnswer: CTerms: Auditing standards; Preliminary judgment about materiality documentedDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills7) Amounts involving fraud are usually considered ________ important than unintentional errors of equal dollar amounts.A) lessB) no lessC) no moreD) moreAnswer: DTerms: Amounts involving fraudDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills8) Qualitative factors can affect an auditor's assessment of materiality. Which of the following statements is true?I. Misstatements that are otherwise immaterial may be material if they affect earnings trends.II. Misstatements that are otherwise minor may be material if there are possible consequences arising from contractual obligations.A) I onlyB) II onlyC) I and IID) neither I nor IIAnswer: CTerms: Qualitative factors can affect auditor's assessment of materialityDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills9) The five steps in applying materiality are listed below in random order.1. Estimate the combined misstatement.2. Estimate the total misstatement in the segment.3. Set materiality for the financial statements as a whole.4. Determine performance materiality.5. Compare combined estimate with preliminary judgment about materiality.The first three steps in correct sequence would be:A) 1, 2, 5B) 3, 4, 2C) 2, 1, 5D) 3, 2, 4Answer: BTerms: Five steps in applying materialityDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skills10) Which of the following statements is not correct?A) Materiality is a relative rather than an absolute concept.B) The most important base used as the criterion for deciding materiality is total assets.C) Qualitative factors as well as quantitative factors affect materiality.D) Given equal dollar amounts, frauds are usually considered more important than errors. Answer: BTerms: MaterialityDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skills11) Certain types of misstatements are likely to be more important than other types to users, even if the dollar amounts are the same. Which of the following demonstrates this?Answer: ATerms: Certain types of misstatements are likely more important than other typesDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skills12) When setting a preliminary judgment about materiality:A) more evidence is required for a low dollar amount than for a high dollar amount.B) less evidence is required for a low dollar amount than for a high dollar amount.C) the same amount of evidence is required for either low or high dollar amounts.D) there is no relationship between it and the dollar amount of evidence needed.Answer: ATerms: Setting preliminary judgment about materialityDiff: ChallengingObjective: LO 9-2AACSB: Reflective thinking skills13) Lewis Corporation has a few large accounts receivable that total one million dollars whereasClark Corporation has many small accounts receivable that total one million dollars. Misstatement in any one account is more significant for Lewis corporation because of the concept of:A) materiality.B) audit risk.C) reasonable assurance.D) comparative analysis.Answer: ATerms: MisstatementsDiff: ChallengingObjective: LO 9-2AACSB: Reflective thinking skills14) Audit standards require the auditor to consider the combined amount of misstatement early in the audit. This is known as preliminary materiality judgment. List and discuss the three main factors that affect an auditor's preliminary judgment about materiality.Answer: The three main factors that affect an auditor's judgment about materiality are:•Materiality is a relative rather than an absolute concept. A misstatement of a given size might be material for a small company, whereas the same dollar misstatement could be immaterial for a larger one. •Benchmarks are needed for evaluating materiality. Because materiality is relative, it is necessary to have benchmarks for establishing whether misstatements are material. Net income before taxes is normally the most commonly used benchmark, but other possible benchmarks include current assets, total assets, current liabilities, and owners' equity.•Qualitative factors also affect materiality. Certain types of misstatements are likely to be more important to users than others, even if the dollar amounts are the same, such as misstatements involving frauds. Terms: Factors that affect auditor's preliminary judgmentDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skills15) Due to qualitative factors, certain types of misstatements are likely to be more important to users than others, even if the dollar amounts are the same. Identify two qualitative factors that might significantly affect an auditor's materiality judgment, and give an example of each.Answer: Qualitative factors that affect an auditor's materiality judgment include:•Amounts involving fraud. Amounts involving fraud are usually considered more important than unintentional errors of equal dollar amounts because fraud reflects on the honesty and reliability of the management or other personnel involved. For example, an intentional misstatement of inventory would be more important to users than a clerical error in inventory of the same amount.•Misstatements affecting contractual obligations. Misstatements that are otherwise minor may be material if there are possible consequences arising from contractual obligations. For example, if a misstatement causes a required minimum account balance to exceed the minimum, when the correct balance is less than the minimum, this misstatement likely would be important to users.•Amounts affecting a trend in earnings. Amounts that are otherwise immaterial may be material if they affect a trend in earnings. An example is if reported income has increased 3 percent annually for the past five years but income for the current year has declined 1 percent, that change may be material. Similarly, a misstatement that would cause a loss to be reported as a profit may be of concern.Terms: Qualitative factors that affect auditor's materiality judgmentDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skills16) The auditor's preliminary judgment about materiality is the maximum amount by which the auditor believes the financial statements could be misstated and still not affect the decisions of reasonable users. Answer: TRUETerms: Preliminary judgments about materialityDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills17) Preliminary judgments about materiality are often changed during the course of the engagement. Answer: TRUETerms: Preliminary judgments about materialityDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills18) Net assets are the most often used base for deciding materiality.Answer: FALSETerms: Base for deciding materialityDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills19) The lower the dollar amount of the preliminary judgment the more audit evidence is required. Answer: TRUETerms: Amount of preliminary judgment and audit evidence requiredDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills20) Amounts involving fraud are not usually considered qualitative factors affecting the preliminary materiality judgment.Answer: FALSETerms: Qualitative factors affecting preliminary materiality judgment; FraudDiff: EasyObjective: LO 9-2AACSB: Reflective thinking skills21) CPA firms can establish policy guidelines to help their auditors determine materiality.Answer: TRUETerms: Difficulty in applying concept of materialityDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skills22) Statements on Auditing Standards provide detailed, objective guidance on how auditors are to establish a preliminary materiality level, thus eliminating the need for subjective auditor judgment in this task.Answer: FALSETerms: Statements on Auditing Standards; Objective guidance on establishing preliminary materiality levelDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skills23) If the preliminary judgment of materiality increases, the amount of audit evidence required will decrease.Answer: TRUETerms: Preliminary judgment of materiality and audit evidenceDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skills24) Net income before tax is the normal base used to determine materiality in a not-for-profit company. Answer: FALSETerms: Base used to determine materialityDiff: ModerateObjective: LO 9-2AACSB: Reflective thinking skillsLearning Objective 9-31) When auditors allocate the preliminary judgment about materiality to account balances, the materiality allocated to any given account balance is referred to as:A) the materiality range.B) the error range.C) tolerable materiality.D) performance materiality.Answer: DTerms: Allocate preliminary judgment about materiality to account balancesDiff: EasyObjective: LO 9-3AACSB: Reflective thinking skills2) Auditors generally allocate the preliminary judgment about materiality to the:A) balance sheet only.B) income statement only.C) income statement and balance sheet.D) statement of cash flows.Answer: ATerms: Preliminary materiality allocationDiff: EasyObjective: LO 9-3AACSB: Reflective thinking skills3) Which of the following is an incorrect statement regarding the allocation of the preliminary judgment about materiality to balance sheet accounts?A) Auditors expect certain accounts to have more misstatements than others.B) The allocation has virtually no effect on audit costs because the auditor must collect sufficient appropriate audit evidence.C) Auditors expect to identify overstatements as well as understatements in the accounts.D) Relative audit costs affect the allocation.Answer: BTerms: Allocation of preliminary judgment about materialityDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills4) Which of the following statements is true concerning the allocation of preliminary materiality?A) It is necessary to allocate preliminary materiality to financial statements as a whole rather than by segments.B) Preliminary materiality should be allocated to income statement accounts only.C) Preliminary materiality is required by the SEC.D) The PCAOB term used when preliminary materiality is allocated to segments is tolerable misstatement.Answer: DTerms: Allocation of preliminary materialityDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills5) Which of the following statements is false?A) Either an overstatement of an asset account or an understatement of a liability account would have the same effect on the income statement.B) A misclassification in the balance sheet will have no effect on operating income.C) Either an overstatement of an asset account or an overstatement of a liability account would have the same effect on the income statement.D) Either an understatement of an asset account or an overstatement of a liability account would have the same effect on the income statement.Answer: CTerms: Effects of misstatementsDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills6) Which of the following are major difficulties auditors face when allocating materiality to balance sheet accounts?Answer: ATerms: Major difficulties auditors face when allocating materiality to balance sheet accountsDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills7) When allocating performance materiality:A) it is easy to predict in advance which accounts are mot likely to be misstated.B) only overstatements need to be considered.C) professional judgment is critical.D) the sum of all the performance materiality levels cannot exceed the preliminary judgment about materiality.Answer: CTerms: Major difficulties auditors face when allocating materiality to balance sheet accountsDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills8) When allocating materiality, most practitioners choose to allocate to:A) the income statement accounts because they are more important.B) the balance sheet accounts because most audits focus on the balance sheet.C) both balance sheet and income statement accounts because there could be errors on either.D) all of the financial statements because it is required by GAAS.Answer: BTerms: Allocating materialityDiff: ChallengingObjective: LO 9-3AACSB: Reflective thinking skills9) Which of the following is a correct statement regarding performance materiality?A) Determining performance materiality is necessary because auditors accumulate evidence by segments.B) The level of performance materiality does not affect the amount of evidence needed.C) Performance materiality cannot vary for different classes of transactions.D) Performance materiality is required for public companies, but not for private companies.Answer: ATerms: Tolerable misstatementsDiff: ChallengingObjective: LO 9-3AACSB: Reflective thinking skills10) Explain why it is necessary to allocate the preliminary judgment about materiality to individual accounts (segments) in the financial statements. Also explain why allocating to balance sheet accounts is more common than allocating to income statement accounts.Answer: Allocating the preliminary judgment about materiality to individual accounts (segments) is necessary because evidence is accumulated for accounts (segments) rather than for the financial statements as a whole. Allocating to accounts (segments) establishes a tolerable misstatement amount for each account, which helps the auditor decide the appropriate audit evidence to accumulate for each account. Most practitioners allocate materiality to balance sheet accounts rather than income statement accounts because most income statement misstatements have an equal effect on the balance sheet due to the nature of double-entry accounting. Because there are fewer balance sheet accounts than income statement accounts in most audits, and because most audit procedures focus on balance sheet accounts, materiality should be allocated only to balance sheet accounts.Terms: Allocation of the preliminary judgment about materialityDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills11) Auditor's allocate the preliminary judgment about materiality to financial statement segments rather than by financial statements as a whole. What is the term for the auditor's allocation of preliminary misstatement to account balances? What are three difficulties auditor's face when allocating materiality to balance sheet accounts?Answer: Performance materiality is the term for the auditor's allocation of the preliminary judgment of materiality to any given account balance. The three difficulties auditors face when allocating the preliminary materiality to account balances are:1. Auditors expect certain accounts to have more misstatement than others.2. Both overstatements and understatements must be considered.3. Audit costs can affect the allocation.Terms: Allocation of preliminary misstatement to account balances and difficulties that auditors face allocating preliminary materiality judgment to account balancesDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills12) Most practitioners allocate the preliminary judgment about materiality to both the balance sheet and income statement accounts.Answer: FALSETerms: Allocate preliminary judgment about materiality to balance sheet accountsDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills13) The primary purpose of allocating the preliminary judgment about materiality to financial statement accounts is to help the auditor decide the appropriate evidence to accumulate.Answer: TRUETerms: Primary purpose of allocating the preliminary judgment about materialityDiff: EasyObjective: LO 9-3AACSB: Reflective thinking skills14) Both overstatements and understatements must be considered when allocating materiality to balance sheet accounts.Answer: TRUETerms: Allocating materiality; Consideration of overstatements and understatementsDiff: EasyObjective: LO 9-3AACSB: Reflective thinking skills15) If an auditor assigns a tolerable misstatement of $1,000 to accounts payable, he or she would need to obtain more audit evidence for that account than if $100,000 had been assigned.Answer: TRUETerms: Tolerable misstatements and audit evidenceDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skills16) To maximize audit efficiency, the auditor should allocate less tolerable misstatement to accounts that can be verified by using low-cost audit procedures, such as analytical procedures, than to accounts that are more costly to audit.Answer: TRUETerms: Maximize audit efficiency, allocate less tolerable misstatementsDiff: ModerateObjective: LO 9-3AACSB: Reflective thinking skillsLearning Objective 9-41) Auditors are ________ to document the known and likely misstatements in the financial statements under audit.A) permittedB) requiredC) not allowedD) strongly encouragedAnswer: BTerms: Known and likely misstatements in the financial statementsDiff: EasyObjective: LO 9-4AACSB: Reflective thinking skills2) ________ misstatements are those where the auditor can determine the amount of the misstatement in the account.A) PotentialB) LikelyC) KnownD) ProjectedAnswer: CTerms: Misstatements where auditor can determine the amountDiff: ModerateObjective: LO 9-4AACSB: Reflective thinking skills3) Likely misstatements can result from:Answer: ATerms: Likely misstatements result fromDiff: ModerateObjective: LO 9-4AACSB: Reflective thinking skills4) When evaluating the audit findings, the auditor should be satisfied that the:A) amount of known misstatement is documented in the management representation letter.B) estimate of the total known and likely misstatements is less than a material amount.C) estimate of the total likely misstatement includes sample error.D) amount of known misstatement is acknowledged and recorded by the client. Answer: BTerms: Evaluating audit findings and materialityDiff: ChallengingObjective: LO 9-4AACSB: Reflective thinking skills5) Discuss each of the five steps in applying materiality in an audit, and identify the audit phase(s) in which each step is performed. List these steps in the order in which they occur.Answer: Step 1. Set preliminary judgment about materiality. This is the combined amount of misstatements in the financial statements that would be considered material. This decision is made in the planning stage of the audit.Step 2. Allocate preliminary judgment about materiality to segments. In this step, the auditor normally allocates the preliminary judgment about materiality to the balance sheet accounts. The amount of materiality allocated to an account is referred to as that account's performance materiality. This allocation is performed in the audit planning stage.Step 3. Estimate total misstatement in segment. In this step, the auditor projects the sample results to the population. An allowance for sampling risk is also calculated. This would be performed after the substantive tests for each account are completed.Step 4. Estimate the combined misstatement. In this step, the projected errors for each account are added, along with total sampling error, to calculate the combined misstatement. This would be performed after all substantive tests have been completed.Step 5. Compare combined estimated misstatement with preliminary or revised judgment about materiality. If the combined estimated misstatement is less than or equal to the judgment about materiality, then the auditor concludes the financial statements are fairly presented. This would be performed after all substantive tests have been completed, in the final review stage of the audit.Terms: Five steps in applying materiality in auditDiff: ChallengingObjective: LO 9-2, LO 9-3, and LO 9-4AACSB: Reflective thinking skills6) The preliminary judgment on materiality is compared to the total estimated misstatement amount to determine if an account balance is materially misstated.Answer: TRUETerms: Preliminary judgment on materiality; Estimated total misstatementsDiff: ModerateObjective: LO 9-4AACSB: Reflective thinking skills7) Total estimated misstatements include known misstatements and projected misstatements plus a sampling error.Answer: TRUETerms: Total estimated misstatements and sampling errorDiff: ModerateObjective: LO 9-4AACSB: Reflective thinking skills8) If the total misstatement of an account is known, a sampling error still needs to be determined. Answer: FALSETerms: Total estimated misstatements and sampling errorDiff: ModerateObjective: LO 9-4AACSB: Reflective thinking skills9) Sampling error represents the minimum misstatement amount that exists in all accounts subjected to sampling.Answer: FALSETerms: Total estimated misstatements and sampling errorDiff: ModerateObjective: LO 9-4AACSB: Reflective thinking skills10) If the auditor approaches the audit of the accounts in s sequential manner, the findings of the audit of accounts audited earlier can be used to revise the performance materiality established for accounts audited later.Answer: TRUETerms: Total estimated misstatements and sampling errorDiff: ModerateObjective: LO 9-4AACSB: Reflective thinking skillsLearning Objective 9-51) Which of the following audit risk components may be assessed in non-quantitative terms?Answer: ATerms: Audit risk components assessed in non-quantitative termsDiff: EasyObjective: LO 9-5AACSB: Reflective thinking skills2) Based on audit evidence gathered and evaluated, an auditor decides to increase the assessed level of control risk from that originally planned. To achieve an overall audit risk level that is substantially the same as the planned audit risk level, the auditor would:A) increase materiality levels.B) decrease detection risk.C) decrease substantive testing.D) increase inherent risk.Answer: BTerms: Control risk and planned audit risk modelDiff: ChallengingObjective: LO 9-5AACSB: Reflective thinking skills3) When dealing with audit risk:A) auditors accept some level of risk in performing the audit function.B) most risks that auditors encounter are relatively easy to measure.C) the audit risk model is only used for classes of transactions.D) most audit firms prefer to use a quantitative assessment for risk.Answer: ATerms: Audit riskDiff: ModerateObjective: LO 9-2 and LO 9-5AACSB: Reflective thinking skills4) Why do auditors use the audit risk model when planning an audit?Answer: The audit risk model is used primarily for planning purposes in deciding how much evidence to accumulate in each cycle. The auditor sets an acceptable level of audit risk, (AAR) assesses inherent risk (IR) and control risk (CR), and then uses the following audit risk model to determine an appropriate level of planned detection risk (PDR):PDR =Terms: Audit risk modelDiff: EasyObjective: LO 9-5AACSB: Reflective thinking skills5) The most important element of the audit risk model is control risk.Answer: FALSETerms: Audit risk model and control riskDiff: EasyObjective: LO 9-5AACSB: Reflective thinking skills。

阿伦斯 审计学:一种整合方法 课后习题答案ch01

Chapter 1The Demand for Audit and Other Assurance Services Review Questions1-1The relationship among audit services, attestation services, and assurance services is reflected in Figure 1-3 on page 13 of the text. An assurance service is an independent professional service to improve the quality of information for decision makers. An attestation service is a form of assurance service in which the CPA firm issues a report about the reliability of an assertion that is the responsibility of another party. Audit services are a form of attestation service in which the auditor expresses a written conclusion about the degree of correspondence between information and established criteria.The most common form of audit service is an audit of historical financial statements, in which the auditor expresses a conclusion as to whether the financial statements are presented in conformity with generally accepted accounting principles. An example of an attestation service is a report on the effe ctiveness of an entity’s internal control over financial reporting. There are many possible forms of assurance services, including services related to business performance measurement, health care performance, and information system reliability. 1-2 An independent audit is a means of satisfying the need for reliable information on the part of decision makers. Factors of a complex society which contribute to this need are:1.Remoteness of informationa.Owners (stockholders) divorced from managementb.Directors not involved in day-to-day operations ordecisionsc.Dispersion of the business among numerous geographiclocations and complex corporate structures2.Biases and motives of providerrmation will be biased in favor of the providerwhen his or her goals are inconsistent with thedecision maker's goals.3.Voluminous dataa.Possibly millions of transactions processed daily viasophisticated computerized systemsb.Multiple product linesc.Multiple transaction locationsplex exchange transactionsa.New and changing business relationships lead toinnovative accounting and reporting problemsb.Potential impact of transactions not quantifiable,leading to increased disclosures1-3 1. Risk-free interest rate This is approximately the rate the bank could earn by investing in U.S. treasury notes for thesame length of time as the business loan.2.Business risk for the customer This risk reflects thepossibility that the business will not be able to repay itsloan because of economic or business conditions such as arecession, poor management decisions, or unexpectedcompetition in the industry.rmation risk This risk reflects the possibility thatthe information upon which the business risk decision wasmade was inaccurate. A likely cause of the information riskis the possibility of inaccurate financial statements.Auditing has no effect on either the risk-free interest rate or business risk. However, auditing can significantly reduce information risk.1-4The four primary causes of information risk are remoteness of information, biases and motives of the provider, voluminous data, and the existence of complex exchange transactions.The three main ways to reduce information risk are:er verifies the information.er shares the information risk with management.3.Audited financial statements are provided.The advantages and disadvantages of each are as follows:1-5 To do an audit, there must be information in a verifiable form and some standards (criteria) by which the auditor can evaluate the information. Examples of established criteria include generally accepted accounting principles and the Internal Revenue Code. Determining the degree of correspondence between information and established criteria is determining whether a given set of information is in accordance with the established criteria. The information for Jones Company's tax return is the federal tax returns filed by the company. The established criteria are found in the Internal Revenue Code and all interpretations. For the audit of Jones Company's financial statements the information is the financial statements being audited and the established criteria are generally accepted accounting principles.1-6The primary evidence the internal revenue agent will use in the audit of the Jones Company's tax return include all available documentation and other information available in Jones' office or from other sources. For example, when the internal revenue agent audits taxable income, a major source of information will be bank statements, the cash receipts journal and deposit slips. The internal revenue agent is likely to emphasize unrecorded receipts and revenues. For expenses, major sources of evidence are likely to be cancelled checks, vendors' invoices and other supporting documentation.1-7This apparent paradox arises from the distinction between the function of auditing and the function of accounting. The accounting function is the recording, classifying and summarizing of economic events to provide relevant information to decision makers. The rules of accounting are the criteria used by the auditor for evaluating the presentation of economic events for financial statements and he or shemust therefore have an understanding of generally accepted accounting principles (GAAP), as well as auditing standards. The accountant need not, and frequently does not, understand what auditors do, unless he or she is involved in doing audits, or has been trained as an auditor.1-81-9Five examples of specific operational audits that could be conducted by an internal auditor in a manufacturing company are:1.Examine employee time cards and personnel records todetermine if sufficient information is available to maximizethe effective use of personnel.2.Review the processing of sales invoices to determine if itcould be done more efficiently.3.Review the acquisitions of goods, including costs, todetermine if they are being purchased at the lowest possiblecost considering the quality needed.4.Review and evaluate the efficiency of the manufacturingprocess.5.Review the processing of cash receipts to determine if theyare deposited as quickly as possible.1-10 When using a strategic systems auditing approach in an audit of historical financial statements, an auditor must have a thorough understanding of the client and its environment. This knowledge should include the client’s regulatory and operating environment, business strategies and processes, and measurement indicators. The strategicsystems approach is also useful in other assurance or consulting engagements. For example, an auditor who is performing an assurance service on information technology would need to understand the client’s business strategies and processes related to information technology, including such things as purchases and sales via the Internet. Similarly, a practitioner performing a consulting engagement to evaluate the efficiency and effectiveness of a cli ent’s manufacturing process would likely start with an analysis of various measurement indicators, including ratio analysis and benchmarking against key competitors.1-11 The major differences in the scope of audit responsibilities are:1.CPAs perform audits in accordance with auditing standards ofpublished financial statements prepared in accordance withgenerally accepted accounting principles.2.GAO auditors perform compliance or operational audits inorder to assure the Congress of the expenditure of publicfunds in accordance with its directives and the law.3.IRS agents perform compliance audits to enforce the federaltax laws as defined by Congress, interpreted by the courts,and regulated by the IRS.4.Internal auditors perform compliance or operational auditsin order to assure management or the board of directors thatcontrols and policies are properly and consistentlydeveloped, applied and evaluated.1-12 The four parts of the Uniform CPA Examination are: Auditing and Attestation, Financial Accounting and Reporting, Regulation, and Business Environment and Concepts.1-13 It is important for CPAs to be knowledgeable about e-commerce technologies because more of their clients are rapidly expanding their use of e-commerce. Examples of commonly used e-commerce technologies include purchases and sales of goods through the Internet, automatic inventory reordering via direct connection to inventory suppliers, and online banking. CPAs who perform audits or provide other assurance services about information generated with these technologies need a basic knowledge and understanding of information technology and e-commerce in order to identify and respond to risks in the financial and other information generated by these technologies.Multiple Choice Questions From CPA Examinations1-14 a. (3) b. (2) c. (2) d. (3)1-15 a. (2) b. (3) c. (4) d. (3)Discussion Questions And Problems1-16 a. The relationship among audit services, attestation services and assurance services is reflected in Figure 1-3 on page 13of the text. Audit services are a form of attestationservice, and attestation services are a form of assuranceservice. In a diagram, audit services are located within theattestation service area, and attestation services arelocated within the assurance service area.b. 1. (1) Audit of historical financial statements2.(2) An attestation service other than an auditservice; or(3) An assurance service that is not an attestationservice (WebTrust developed from the AICPASpecial Committee on Assurance Services, but theservice meets the criteria for an attestationservice.)3.(2) An attestation service other than an auditservice4.(2) An attestation service other than an auditservice5.(2) An attestation service other than an auditservice6.(2) An attestation service that is not an auditservice (Review services are a form ofattestation, but are performed according toStatements on Standards for Accounting andReview Services.)7.(2) An attestation service other than an auditservice8.(2) An attestation service other than an auditservice9.(3) An assurance service that is not an attestationservice1-17 a. The interest rate for the loan that requires a review report is lower than the loan that did not require a review becauseof lower information risk. A review report provides moderateassurance to financial statement users, which lowersinformation risk. An audit report provides further assuranceand lower information risk. As a result of reduced information risk, the interest rate is lowest for the loan with the audit report.b.Given these circumstances, Vial-tek should select the loanfrom City First Bank that requires an annual audit. In this situation, the additional cost of the audit is less than the reduction in interest due to lower information risk. The following is the calculation of total costs for each loan:1-17 (continued)c. Vial-tek may desire to have an audit because of the manyother positive benefits that an audit provides. The auditwill provide Vial-tek’s management with assurance aboutannual financial information used for decision-makingpurposes. The audit may detect errors or fraud, and providemanagement with information about the effectiveness ofcontrols. In addition, the audit may result inrecommendations to management that will improve efficiencyor effectiveness.d. Under a strategic systems audit approach, the auditor musthave a thorough understanding of the client and itsenvironment, including the client’s e-commerce technologies,industry, regulatory and operating environment, suppliers,customers, creditors, and business strategies and processes.This thorough analysis helps the auditor identify risksassociated with the client’s strategies that may affectwhether the financial statements are fairly stated. Whenapplying the strategic systems audit approach, the auditoroften discovers ways to help the client improve businessoperations, thereby providing added value to the auditfunction.1-18 a. The services provided by Consumers Union are very similar to assurance services provided by CPA firms. The servicesprovided by Consumers Union and assurance services providedby CPA firms are designed to improve the quality ofinformation for decision makers. CPAs are valued for theirindependence, and the reports provided by Consumers Union are valued because Consumers Union is independent of the products tested.b.The concepts of information risk for the buyer of anautomobile and for the user of financial statements are essentially the same. They are both concerned with the problem of unreliable information being provided. In the case of the auditor, the user is concerned about unreliable information being provided in the financial statements. The buyer of an automobile is likely to be concerned about the manufacturer or dealer providing unreliable information.c.The four causes of information risk are essentially the samefor a buyer of an automobile and a user of financial statements:(1)Remoteness of information It is difficult for a userto obtain much information about either an automobilemanufacturer or the automobile itself withoutincurring considerable cost. The automobile buyer doeshave the advantage of possibly knowing other users whoare satisfied or dissatisfied with a similarautomobile.(2)Biases and motives of provider There is a conflictbetween the automobile buyer and the manufacturer. Thebuyer wants to buy a high quality product at minimumcost whereas the seller wants to maximize the sellingprice and quantity sold.(3)Voluminous data There is a large amount of availableinformation about automobiles that users might like tohave in order to evaluate an automobile. Either that information is not available or too costly to obtain.1-18 (continued)(4)Complex exchange transactions The acquisition of anautomobile is expensive and certainly a complexdecision because of all the components that go intomaking a good automobile and choosing between a largenumber of alternatives.d.The three ways users of financial statements and buyers ofautomobiles reduce information risk are also similar:(1)User verifies information him or herself That can beobtained by driving different automobiles, examiningthe specifications of the automobiles, talking toother users and doing research in various magazines.(2)User shares information risk with management Themanufacturer of a product has a responsibility to meetits warranties and to provide a reasonable product.The buyer of an automobile can return the automobilefor correction of defects. In some cases a refund maybe obtained.(3)Examine the information prepared by Consumer ReportsThis is similar to an audit in the sense thatindependent information is provided by an independentparty. The information provided by Consumer Reports iscomparable to that provided by a CPA firm that auditedfinancial statements.1-19 a. The following parts of the definition of auditing are related to the narrative:(1)Virms is being asked to issue a report aboutqualitative and quantitative information for trucks.The trucks are therefore the information with which the auditor is concerned.(2)There are four established criteria which must beevaluated and reported by Virms: existence of the trucks on the night of June 30, 2005, ownership of each truck by Regional Delivery Service, physical condition of each truck and fair market value of each truck.(3)Susan Virms will accumulate and evaluate four types ofevidence:(a)Count the trucks to determine their existence.(b)Use registrations documents held by Oatley forcomparison to the serial number on each truck todetermine ownership.(c)Examine the trucks to determine each truck'sphysical condition.(d)Examine the blue book to determine the fairmarket value of each truck.(4)Susan Virms, CPA, appears qualified, as a competent,independent person. She is a CPA, and she spends most of her time auditing used automobile and truck dealerships and has extensive specialized knowledge about used trucks that is consistent with the nature of the engagement.1-19(continued)(5)The report results are to include:(a)which of the 35 trucks are parked in Regional'sparking lot the night of June 30.(b)whether all of the trucks are owned by RegionalDelivery Service.(c)the condition of each truck, using establishedguidelines.(d)fair market value of each truck using thecurrent blue book for trucks.b.The only parts of the audit that will be difficult for Virmsare:(1)Evaluating the condition, using the guidelines of poor,good, and excellent. It is highly subjective to do so.If she uses a different criterion than the "bluebook," the fair market value will not be meaningful.Her experience will be essential in using thisguideline.(2)Determining the fair market value, unless it isclearly defined in the blue book for each condition.1-20 a. The major advantages and disadvantages of a career as an IRS agent, CPA, GAO auditor, or an internal auditor are:1-20 (continued)EMPLOYMENT ADVANTAGES DISADVANTAGESINTERNAL AUDITOR 1.Extensive exposure to allsegments of theenterprise with whichemployed.2.Constant exposure to oneindustry presentingopportunity for expertisein that industry.3.Likely to have exposureto compliance, financialand operational auditing.1.Little exposure totaxation and the auditthereof.2.Experience is limited toone enterprise, usuallywithin one or a limitednumber of industries.(b)Other auditing careers that are available are:Auditors within many of the branches of the federalgovernment ., Atomic Energy Commission)Auditors for many state and local government units .,state insurance or bank auditors)1-21 The most likely type of auditor and the type of audit for each of the examples are:1-22 a. The conglomerate should either engage the management advisory services division of a CPA firm or its own internalauditors to conduct the operational audit.b.The auditors will encounter problems in establishingcriteria for evaluating the actual quantitative events andin setting the scope to include all operations in whichsignificant inefficiencies might exist. In writing thereport, the auditors must choose proper wording to state that no financial audit was performed, that the procedures were limited in scope and that the results reported do not necessarily include all the inefficiencies that might exist.1-23 a. The CPA firm for the Internet company described in this problem could address these customer concerns by performinga WebTrust attestation engagement. The WebTrust assuranceservice was created by the profession to respond to thegrowing need for assurance resulting from the growth ofbusiness transacted over the Internet.b.The appropriate WebTrust principle for each of the customerconcerns noted in the problem is as follows:1.Accuracy of product descriptions and adherence tostated return policies: (3) Processing Integrity.2.Credit card and other personal information: (1) OnlinePrivacy and (2) Security.3.Selling information to other companies: (1) OnlinePrivacy and (2) Security.4.System failure: (4) Availability.Internet Problem Solution: Assurance Services1-1 This problem requires students to work with the AICPA assurance services Web site.1.Considering the assurance needs of customers and thecapabilities of CPAs, the Special Committee on AssuranceServices developed business plans for six assurance services.Chapter 1 of the textbook discussed several of theseservices. Go to the service description for the assuranceservice that most interests you (any one of the six). Whatare the major aspects or sections of the associated businessplan ., does the plan address market potential, competition,etc.)Answer: Each business plan provides background information,describes the service, assesses market potential, discussesissues such as competition and why CPAs should offer theservice, identifies practice tools available and steps thatCPAs must take to begin offering the services.2.The Special Committee's report on Assurance Servicesdiscusses competencies needed by assurance providers todayand in the coming decade. Briefly describe the 5 generalcompetencies needed in the next decade (Hint: See the“About Assurance Services” link. Then follow the“Assurance Services and Academia” link.)Answer:The Committee identified the following five majorimperatives regarding future competencies, each of whichimplies increasing emphasis on the competencies noted:1-1 (continued)Customer focus.Assurance service providers need tounderstand user decision processes and how informationshould enter into those processes. Increased emphasis isneeded on: understanding user needs, communication skills,relationship management, responsiveness and timeliness.Migration to higher value-added information activities. To provide more value to client/decision makers and others, assurance service providers need to focus less on activities involved in the conversion of business events into information ., collecting, classifying, and summarizing activities) and more on activities involved in the transformation of information into knowledge ., analyzing, interpreting, and evaluating activities) that effectively drives decision processes. This will require: analytical skills, business advisory skills, business knowledge, model building (including sensitivity analysis), understanding the client’s business processes, measurement theory (development of operational definitions of concepts, design of appropriate measurement techniques, etc.).Information technology (IT).Assurance services deal in information. Hence, the profound changes occurring in information technology will shape virtually all aspects of assurance services. As information specialists, assurance service providers need to embrace information technology in all of its complex dimensions. Embracing IT means understanding how it is transforming all aspects of business. It also means learning how to effectively use new developments in hardware, software, communications, memory, encryption, etc., in everything assurance service providers do as information specialists, not only in dealing with clients, but also in dealing with each other as individuals,teams, firms, state societies, and national professionalorganizations.Pace of change and complexity. Assurance services will takeplace in an environment of rapid change and increasingcomplexity. Assurance service providers need to investheavily in life-long learning in order to maintain up-to-date knowledge and skills. They will require: intellectualcapability, learning and rejuvenation.Competition.Growth in new assurance services will dependless on franchise/regulation and more on market forces.Assurance service providers need to develop their marketingskills —the ability to see clients’ latent informationand assurance needs and rapidly design and deploy cost-effective services to meet those needs —in order toeffectively compete for market-driven assurance services.Required skills include: marketing and selling,understanding customer needs, designing and deployingeffective solutions.1-1 (continued)(Note: Internet problems address current issues using Internet sources. Because Internet sites are subject to change, Internet problems and solutions are subject to change. Current information on Internet problems is available at。

审计学-一种整合的方法43页PPT

1、 舟 遥 遥 以 轻飏, 风飘飘 而吹衣 。 2、 秋 菊 有 佳 色,裛 露掇其 英。 3、 日 月 掷 人 去,有 志不获 骋。 4、 未 言 心 相 醉,不 再接杯 酒。 5、 黄 发 垂 髫 ,并怡 然自乐 。

ห้องสมุดไป่ตู้

56、书不仅是生活,而且是现在、过 去和未 来文化 生活的 源泉。 ——库 法耶夫 57、生命不可能有两次,但许多人连一 次也不 善于度 过。— —吕凯 特 58、问渠哪得清如许,为有源头活水来 。—— 朱熹 59、我的努力求学没有得到别的好处, 只不过 是愈来 愈发觉 自己的 无知。 ——笛 卡儿

拉

60、生活的道路一旦选定,就要勇敢地 走到底 ,决不 回头。 ——左

阿伦斯-审计学:一种整合的方法-课后习题答案ch02