审计学一种整合方法Chapter19精品PPT课件

审计学一种整合方法 课件Chapter19

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 12

Related Documents and Reports

Processing and recording cash disbursements: Check Cash disbursements transaction file Cash disbursements journal or listing

19 - 2

Transactions in the Acquisition and Payment Cycle

1. Acquisitions of goods and services 2. Cash disbursements 3. Purchase returns and allowances and purchase discounts

Subsidiary accounts Supplies, Officers’ travel Legal fees Auditing fees, Taxes

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 19 - 5

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 16

Learning Objective 4

Understand internal control, and design and perform tests of controls and substantive tests of transactions for the acquisition and payment cycle.

审计学一种整合的方法1ppt课件

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

8-9

Understanding of the Client’s Business and Industry

Factors that have increased the importance of understanding the client’s business and industry:

Accept client and perform initial audit planning.

Understand the client’s business and industry.

Assess client business risk.

Perform preliminary analytical procedures.

8-7

Initial Audit Planning

➢ Client acceptance and continuance ➢ Identify client’s reasons for audit ➢ Obtain an understanding with the client ➢ Develop overall audit strategy

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

8-8

Learning Objective 3

Gain an understanding of the client’s business and industry.

审计学一种整合的方法课件

审计准则与审计标准

01 审计准则

审计准则是审计师在执行审计工作时必须遵循的 规范和原则,以确保审计质量和信誉。

02 审计标准

审计标准是衡量财务报表、内部控制和治理过程 可靠性的尺度,包括国际审计准则和国内审计准 则。

方法

采用生命周期评估方法, 从产品的设计、生产、使 用到废弃的整个过程进行 环境审计。

信息安全审计

定义

信息安全审计是一种对组织的信 息系统安全进行的审计,旨在评 估组织对信息安全的控制能力和

效果。

目的

确保组织的信息系统安全,防止信 息泄露、篡改或损坏,提高组织的 竞争力。

方法

采用风险评估方法,识别潜在的安 全风险,提出应对措施,并定期进 行安全审计。

国际化与本土化相结合

1 2 3

国际化趋势

随着经济全球化的不断发展,审计学逐渐走向国 际化,国际审计标准和准则逐渐成为各国审计的 基础。

本土化需求

各国在引进国际审计标准和准则的同时,也需要 根据本国实际情况进行适当的调整和修改,以适 应本土市场需求和发展。

国际化与本土化的平衡

各国在实现审计国际化的同时,要充分考虑本土 化需求,实现国际化和本土化的有机融合。

信息技术提高审计效率

随着信息技术的不断发展,审计学可以利用大数据、人工智能等 技术提高审计效率,减少人工操作,降低审计成本。

信息技术拓展审计范围

信息技术可以帮助审计学扩大数据来源和样本数量,从而更全面地 评估被审计单位的风险状况。

信息技术提高审计质量

通过信息技术,可以实现数据的实时监控和分析,及时发现潜在风 险,提高审计质量。

审计学:一种整合方法_第12版_英文版Chapter18-32页PPT资料

18 - 5

Accounts in the Payroll and Personnel Cycle

In most systems the accrued wages and salaries account is used only at the end of an accounting period.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

18 - 9

Timekeeping and Payroll Preparation

Time Card Job Time Ticket Payroll Transaction File Payroll Journal

Begins Ends

Hiring of personnel Payments

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

18 - 8

Personnel and Employment

Personnel records Deduction authorization form Rate authorization form

Accounts in the Payroll and Personnel Cycle

The overall objective in the audit of the payroll and personnel cycle is to evaluate whether the account balances affected by the cycle are fairly stated in accordance with generally accepted accounting principles.

审计学一种整合方法课件

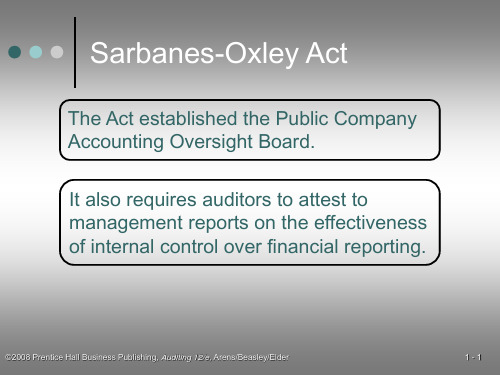

Sarbanes-Oxley Act

This Act requires the auditor of a public company to attest to management’s report on the effectiveness of internal control over financial reporting.

3. Auditor agrees with a departure from promulgated accounting principles

4. Emphasis of a matter

5. Reports involving other auditors

Substantial Doubt About Going Concern

Conditions for Standard Unqualified Audit Report

4. The financial statements are presented in accordance with generally accepted accounting principles.

Leare the five circumstances • when an unqualified report with • an explanatory paragraph or • modified wording is appropriate.

1. Significant recurring operating losses or working capital deficiencies.

2. Inability of the company to pay its obligations as they come due.

审计学一种整合的方法.pptx

statements and internal control

from the auditor’s responsibility

for verifying the financial

statements and effectiveness

of internal control.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-8

Learning Objective 3

Explain the auditor’s responsibility for discovering material misstatements.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-6

Management’s Responsibilities

Management is responsible for the financial statements and for internal control.

The Sarbanes-Oxley Act increases management’s responsibility for the financial statements.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-3

Steps to Develop Audit Objectives

1. Understand objectives and responsibilities for the audit.

审计学-一种整合的方法

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-3

Steps to Develop Audit Objectives

1. Understand objectives and responsibilities for the audit.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-5

Learning Objective 2

Distinguish management’s

responsibility for the financial

6-4Βιβλιοθήκη Steps to Develop Audit Objectives

4. Know general audit objectives for classes of transactions and accounts.

5. Know specific audit objectives for classes of transactions and accounts.

statements and internal control

from the auditor’s responsibility

for verifying the financial

statements and effectiveness

of internal control.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

审计学一种整合方法

审计学一种整合方法

审计学是一种整合方法,将不同的领域和技能相结合,提供全面的财务报告和披露服务。

审计学涵盖了财务审计、内部审计、社会审计和其他类型的审计,旨在确保企业、机构和个人的财务报告和披露符合法规要求。

在审计过程中,审计员需要整合多种技能和方法,包括财务分析、风险管理、信息系统审计、法律和合规等方面的知识。

他们需要将这些技能和方法应用于审计工作,以发现和纠正潜在的错误、欺诈和缺陷。

整合方法是审计学中的一个重要概念。

审计员需要将不同的技能和方法相结合,以提供全面的财务报告和披露服务。

例如,在财务分析方面,审计员需要使用会计数据、财务指标和统计分析方法,以评估企业财务状况的真实性和准确性。

在风险管理方面,审计员需要了解企业的风险模式和潜在风险,并评估可能的风险影响。

在信息系统审计方面,审计员需要了解企业信息系统的功能、结构和操作,以评估信息系统的性能和安全性。

除了整合技能和方法之外,审计学还需要适应不断变化的环境和法规要求。

因此,审计员需要不断更新他们的知识和技能,以适应不同的监管环境、技术和法规要求。

审计学的整合方法不仅可以提高审计员的专业水平和服务质量,还可以促进企业和社会诚信。

通过整合不同的技能和方法,审计员可以更准确地评估企业的财务报告和披露,提高企业和社会的信任度和透明度。

因此,审计学作为一种整合方法,具有重要的意义和应用价值。

审计学一种整合的方法4ppt课件

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

8-9

Understanding of the Client’s Business and Industry

Factors that have increased the importance of understanding the client’s business and industry:

Understand client’s business and industry

Industry and external environment

Business operations and processes

Management and governance

Objectives and strategies

➢ Information technology ➢ Global operations

➢ Human capital

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

8 - 10

Understanding of the Client’s Business and Industry

8-6

Learning Objective 2

Make client acceptance decisions and perform initial audit planning.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

审计学-一种整合的方法

It requires the CEO and the CFO of public companies to certify the quarterly and annual financial statements submitted to the SEC.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6 - 15

Transaction Flow Example

Transactions

Cash disbursements

Payroll services and disbursements

Journals Cash

disbursements journal

Payroll journal

Ledgers, Trial Balance, and Financial

statements and internal control

from the auditor’s responsibility

for verifying the financial

statements and effectiveness

of internal control.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

General ledger and subsidiary

records

General ledger trial balance

Acquisition of goods

and services

审计学-一种整合的方法-文档资料

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-6

Learning Objective 2

Distinguish management’s

responsibility for the financial

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-7

Management’s Responsibilities

Management is responsible for the financial statements and for internal control.

The Sarbanes-Oxley Act increases management’s responsibility for the financial statements.

➢ Actions when the auditor knows of an illegal act

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6 - 13

Learning Objective 4

Learning Objective 1

Explain the objective of conducting an audit of financial statements and an audit of internal controls.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

审计学-一种整合的方法

2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

5 - 16

Auditor's Deck of duty to perform Nonnegligent performance Contributory negligence Absence of causal connection

5 - 21

Learning Objective 6

Describe accountants' civil liability under the federal securities laws and related defenses.

2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

5 - 13

Four Major Sources of Auditors' Legal Liability

Liability to clients Liability to third parties Federal securities laws Criminal liability

2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

5-6

Business Failure, Audit Failure, and Audit Risk

审计学-一种整合的方法

statements and internal control

from the auditor’s responsibility

for verifying the financial

statements and effectiveness

of internal control.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6 - 14

Transaction Flow Example

Transactions Sales

Cash receipts

Journals Sales journal

Cash receipts journal

Ledgers, Trial Balance, and Financial

Statements

Actions when the auditor knows of an illegal act

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6 - 12

Learning Objective 4

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-2

Objective of Conducting an Audit of Financial Statements

The objective of the ordinary audit of financial statements is the expression of an opinion of the fairness with which they present fairly, in all respects, financial position, result of operations, and its cash flows in conformity with GAAP.

审计学:一种整合方法_第12版_英文版Chapter01-46页PPT资料

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1-1

Learning Objective 1

Describe auditing.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

1-2

Nature of Auditing

Auditing is the accumulation and evaluation of evidence about information to determine and report on the degree of correspondence between the information and established criteria.

1-7

Audit of a Tax Return Example

Competent, independent

person

Information

Federal tax returns filed by taxpayer

Internal Revenue

审计学-一种整合的方法-文档资料

6 - 16

Relationships Among Transaction Cycles

General cash

Capital acquisition and repayment cycle

Sales and collection

cycle

Acquisition and payment

cycle

Inventory and warehousing

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6-5

Learning Objective 2

Distinguish management’s

responsibility for the financial

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

6 - 11

Auditor’s Responsibilities for Discovering Illegal Acts

➢ Evidence accumulation and other actions when there is reason to believe direct- or indirect-effect illegal acts may exist

➢ Actions when the auditor knows of an illegal act

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

审计学-一种整合方法

审计学-一种整合方法审计学是一门综合性的学科,旨在通过评估和改善组织的财务信息,确保其准确、可靠、公正和合法。

它使用各种方法和技术来完成此任务,其中一种常见的方法是整合方法。

整合方法是将不同的审计方法和技术结合起来,以全面、系统地评估和改善组织的财务信息。

整合方法包括以下几个方面:1. 综合使用不同的审计方法:审计学使用了许多不同的方法,例如财务审计、内部审计、运营审计、合规审计等。

这些方法各具特点,在评估和改善财务信息方面起着不同的作用。

整合方法将这些不同的审计方法结合起来,以便综合评估和改善组织的财务信息。

2. 综合使用不同的审计技术:审计学使用了许多不同的技术,例如数据分析、风险评估、内部控制评价等。

这些技术可以帮助审计人员更好地理解组织的财务信息,发现潜在的问题和风险,并提出相应的改进建议。

整合方法将这些不同的审计技术整合在一起,以实现更全面、系统的审计。

3. 整合不同层次的审计:审计学涵盖了不同层次的审计,包括组织级审计、部门级审计和项目级审计等。

整合方法将这些不同层次的审计整合在一起,以充分发挥各级审计的作用,并确保评估和改善财务信息的全面性和准确性。

4. 整合不同领域的知识:审计学需要综合运用经济学、会计学、法律学和管理学等多个领域的知识。

整合方法将这些不同领域的知识整合在一起,以提高审计人员的综合素质和能力,更好地完成审计任务。

整合方法在实践中具有重要的意义和应用价值。

首先,整合方法可以帮助审计人员更全面、系统地评估和改善组织的财务信息,发现潜在的问题和风险,并提出相应的改进建议。

其次,整合方法可以提高审计的效率和质量,避免重复的工作和信息孤岛现象,提高工作的一致性和准确性。

再次,整合方法能够发挥多学科和多层次的优势,提供更全面、客观和可靠的审计意见和结论,满足各方对财务信息的需求和期望。

然而,整合方法也面临一些挑战和难题。

首先,整合不同的方法、技术和知识需要审计人员具备较高的综合素质和能力,这对人才培养和选拔提出了更高的要求。

审计学一种整合方式讲义

Learning Objective 2

Describe the fraud triangle and identify conditions for fraud.

The Fraud Triangle

Incentives/Pressures

Opportunities

Attitudes/Rationalization

A history of violations of laws is known

Management has a practice of making

overly aggressive or unrealistic forecasts

Examples of Risk Factors for Misappropriation of Assets

11

by directors

6

Ineffective or

10

nonexistent ethics or

8

compliance program

7

2003

1998

1994

Learning Objective 5

Develop responses to identified fraud risks.

Responding to the Risk of Fraud

11

11

Kickbacks

9

6

Financial reporting

7

fraud

3

2003

1998

Specific Fraud Risk Areas

Revenue and accounts receivable fraud risks Inventory fraud risks Purchases and accounts payable fraud risks Other areas of fraud risk

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Administrative Expense Control Account

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

Subsidiary accounts Supplies, Oees Auditing fees, Taxes

19 - 5

Learning Objective 2

Describe the business functions and the related documents and records in the acquisition and payment cycle.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 2

Transactions in the Acquisition and Payment Cycle

1. Acquisitions of goods and services 2. Cash disbursements 3. Purchase returns and allowances

➢ Recognizing the liability

➢ Processing and recording cash disbursements

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 4

Accounts in the Acquisition

and Payment Cycle

Manufacturing Expense Control Account

Subsidiary accounts Repair and maintenance Taxes, Supplies Freight in, Utilities

Accounts Payable

Acquisitions of goods and services

Selling Expense Control Account

Subsidiary accounts Commissions Travel, delivery expenses Repairs, Advertising

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 7

Classes of Transactions and Accounts

Cash disbursements: ➢ Cash in bank (from cash disbursements) ➢ Accounts payable ➢ Purchase discounts

Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable.

Chapter 19

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 1

Learning Objective 1

Identify the accounts and the classes of transactions in the acquisition and payment cycle.

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 8

Business Functions in the Cycle

➢ Processing purchase orders

➢ Receiving goods and services

and purchase discounts

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 3

Accounts in the Acquisition

and Payment Cycle

Cash in Bank

Property, Plant and Equipment

Purchase Discounts

Purchase discounts

Prepaid Expenses

©2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder

19 - 6

Classes of Transactions and Accounts

Acquisitions:

➢ Inventory ➢ Property, plant, and equipment ➢ Prepaid expenses ➢ Leasehold improvements ➢ Accounts payable ➢ Manufacturing expenses ➢ Selling and administrative expenses

Accounts Payable

Cash Acquisitions disbursements of goods and

services

Raw Material Purchases

Purchase Returns and Allowances

Purchase returns and allowances