成本与管理会计亨格瑞第13版英文版CA01

亨格瑞 成本与管理会计

亨格瑞成本与管理会计

亨格瑞(Hengrui)是一家知名的成本与管理会计公司。

他们专注于提供成本管理、绩效管理和策略管理等方面的解决方案和咨询服务。

成本管理是指通过对企业资源和活动的成本进行测算、分析和控制,来提高企业效益和降低成本的管理方法。

亨格瑞通过帮助企业建立

成本计划和预算、制定成本控制策略、优化成本结构等手段,帮助

企业降低成本、提高利润。

绩效管理是指通过设定绩效目标、制定绩效评价体系、实施绩效测

算和分析,来提高企业绩效和激励员工的管理方法。

亨格瑞通过设

计和实施绩效管理制度、开展绩效评估和考核、提供培训和改进方

案等手段,帮助企业优化绩效,实现战略目标。

策略管理是指通过对企业内外环境的分析和评估,制定和执行战略

计划,来提高企业竞争力和市场地位的管理方法。

亨格瑞通过帮助

企业制定战略目标、开展战略规划和执行、提供战略改善建议等手段,帮助企业提升竞争力,实现可持续发展。

亨格瑞拥有一支专业的团队,拥有丰富的成本与管理会计经验,能

够根据企业的实际情况,提供量身定制的解决方案,帮助企业提高

运营效率和盈利能力。

财务管理英文第十三版

Corporate Capital Gains / Losses

Currently, capital gains are taxed at ordinary income tax rates for corporations, or a maximum 35%.

The Capital Budgeting Process

Generate investment proposals consistent with the firm’s strategic objectives.

Estimate after-tax incremental operating cash flows for the investment projects.

c) - (+) Taxes (tax savings) due to asset sale or disposal of “new” assets

d) + (-) Decreased (increased) level of “net” working capital

e) = Terminal year incremental net cash flow

Depreciation and the MACRS Method

Everything else equal, the greater the depreciation charges, the lower the taxes paid by the firm.

成本与管理会计-亨格瑞-第13版-英文版-CA04

Batch-production operations

Costs cannot be directly traced to each unit of product.

Used for production of small, identical, low cost items.

The indirect costs of a cost object are costs that cannot be traced to the cost object in a cost-effective manner and are allocated to the cost object.

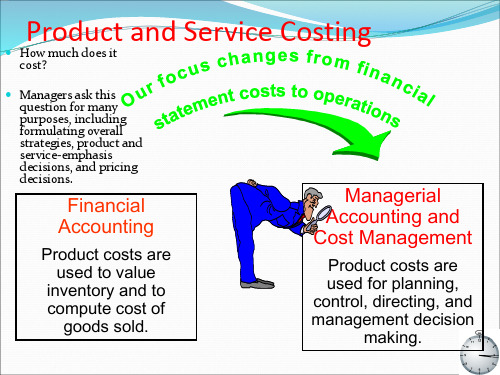

Financial Accounting

Product costs are used to value

inventory and to compute cost of

goods sold.

2019/10/16

Managerial Accounting and Cost Management

Product costs are used for planning, control, directing, and management decision

A job-costing system, or a job-order system, is used by a company that makes a distinct product or service called a job.

The product or service is often a single unit. The job is frequently the cost object. Costs are accumulated separately for each job or service.

《成本与管理会计》教师手册 costacctg13_im_02

An Introduction To Cost TermsAnd PurposesTRANSITION NOTESThis chapter has been rewritten to place more emphasis on the role of managerial decisions.Exhibits have been changed so the students can more easily follow the concepts. This chapter continues building on the framework begun in Chapter 1, emphasizing (1) calculating the cost of products or other cost objects, (2) obtaining information for planning and control as well as performance evaluation, and (3) identifying relevant information for decision making. It introduces concepts essential to topics covered in later chapters.PROBLEM MATERIALCORRELATION CHART13th Edition 12thEdition13thEdition12thEdition16 16 29 2817 New 30 2918 18 31 3019 19 32 3120 20 33 3221 Revised 34 3322 22 35 3423 New 36 New24 New 37 3625 Revised 38 3726 Revised 39 New27 New 40 3928 27I. LEARNING OBJECTIVES1.Define and illustrate a cost object2.Distinguish between direct costs and indirect costs3.Explain variable costs and fixed costs4.Interpret unit costs cautiously5.Distinguish among manufacturing companies, merchandising companies, andservice-sector companies6.Describe the three categories of inventories commonly found in manufacturingcompanies27.Distinguish inventoriable costs from period costs8.Explain why product costs are computed in different ways for different purposes9.Describe a framework for cost accounting and cost managementII. CHAPTER SYNOPSISChapter 2 defines and explains important cost accounting terms and concepts that will be discussed in the following chapters. Understanding the concepts and terms discussed inthis chapter is a prerequisite to successfully completing the remaining chapters of the text.One guiding principle is that the term cost is a relative term, dependent both on the “costobject” chosen and the purpose for which cost is being calculated and reported.Costs are a critical element in most business decisions. Students also need to recognizethat companies pay particular attention to costs because every dollar in cost reduction isone more dollar of operating income, whereas one more dollar of sales does notnecessarily result in the same impact due to the additional costs that may be incurred ingenerating those sales.“Cost” is often actually “estimated cost” due to difficulties involved in cost tracing andallocation, relevant range issues, which cost method is used, and the cost-benefitapproach to measuring costs. Although there are certain standard costing and reportingmethods followed by all, companies calculate and report the same types of datadifferently depending on their industry and sector. Companies commonly operate in themerchandising, manufacturing, and service sectors.III. POINTS OF EMPHASIS1.Although terminology can be boring, it is important that the students grasp andunderstand the terms introduced in this chapter. They will have some familiaritywith some of the terms; however, remind them that these words may havemeanings that are different in a cost accounting context.2.The distinction between inventoriable (or product) cost and period cost is animportant one that students may have some trouble grasping, as they areaccustomed to treating items such as wages, rent, utilities, and the like asexpenses of the period. Likewise, the term conversion cost is one that should bemastered early on.IV. CHAPTER OUTLINETEACHING POINT. The terminology in this chapter is importantfor the student to gain an understanding early in the course. Incovering the chapter, it is very beneficial to repeatedly askquestions such as: (1) What is the cost object in the situation? (2)What costs can be traced? and (3) Which costs are allocated?1Define and illustrate a cost object. . . examples of cost objects are products,services, activities, processes, and customers1.1Cost is a resource sacrificed or forgone to achieve a specific objective.1.2Actual cost is the historical amount, or cost incurred, as distinguished frombudgeted cost, which is the planned (or future) amount of cost.1.3Cost object is the purpose for which costs are being measured. Stated anotherway, the cost object is anything for which a measurement of costs is desired. For example, this can be a product, an assembly line, a product line, or a department.TEACHING POINT. Discuss with the students the concept ofcost object. Use different examples of cost objects. Help themrelate the concept to their own lives. The cost of taking a tripduring spring break, the cost of a date, the cost of a collegeeducation, and the cost of a single class—all make goodtalking points.(Exhibit 2-1 illustrates examples of cost objects at BMW.)1.4Cost Accumulation describes the process of accumulating costs in someorganized manner through the accounting system. Following accumulation, costs are assigned to the chosen cost object.1.5The process of cost assignment involves tracing and allocating costs,depending on the type of cost involved.Refer to Quiz Question 12Distinguish between direct costs and indirect costs. . . costs that are traced directly to the cost objectand indirect costs. . . costs that are allocated to the cost object2.1 Direct costs of a cost object are costs that are related to the cost object and canbe traced to it in an economically feasible manner. Many costs may be able to betraced to the cost object, but it is not always practical to do so from a cost-benefitperspective.2.2 Direct cost categories include direct materials and direct manufacturing labor.Direct materials are materials that go into the production of the product. Directlabor is the wages paid to workers who spend time working on the product.2.3 Indirect costs of a cost object are related to the cost object but cannot be tracedin an economically feasible manner. These costs are frequently referred to asfactory overhead, manufacturing overhead, or some similar term. These costsinclude supervisor salaries, supplies, or other costs incurred in the factory that arenot direct materials or direct labor.TEACHING POINT. Make the observation that the same costmay be direct or indirect depending on the cost object. Usesome illustrations. For example, a line supervisor in a factorycould be a direct cost if the cost object were the particularassembly line, but would be indirect if the finished product isthe cost object.2.4 There are several factors that affect the classification of costs as direct or indirect.Three of these factors include:•Materiality of the cost. The smaller the amount of the cost, the lesslikely that it is economically feasible to trace that cost to a particular costobject.•Ease of gathering the information. For example bar-code technologyhas made it possible to trace just about any material used in themanufacturing process.•Design of operations. A cost used exclusively for a specific cost objectcan be readily traced.(Exhibit 2-2 illustrates the assignment of direct and indirectcosts at BMW.)TEACHING POINT. Use an object in the classroom, such as astool or chair. Place it on a desk or somewhere the students caneasily see it. Ask: “W hat are the materials used in manufacturingthe object?” Once a list of materials is compiled, then have thestudents determine which are direct material costs and whichare indirect costs.Refer to Quiz Question 2 Exercise 2-17only ID as Direct or IndirectExplain variable costs and fixed costs. . . the two basic ways in which costs behave3.1 In order to adequately predict costs, their behavior must be understood. From abehavioral view, costs are classified as fixed or variable.3.2 A variable cost changes in proportion with changes in the activity level. Forexample, if the number of units produced doubles, direct materials (a variablecost) would double in total. Note, however, that the variable cost per unit staysthe same.3.3 Fixed costs do not change due to changes in the activity level. If units produceddoubles, fixed costs remain the same in total. However, when expressed on a per-unit basis, fixed costs would decline with an increase in activity.(Exhibit 2-3 displays the cost behavior of variable and fixedcosts in total.)3.4 Costs are not inherently fixed or variable; it depends on the defined cost object.They may be variable with respect to level of activity and fixed for another.3.5 A cost driver is what causes a cost to be incurred. Stated another way there is acause-and-effect relationship between the level of activity of the cost driver andthe cost incurred.TEACHING POINT. Use several examples that will help thestudents grasp this concept. For example, their cost ofgasoline is determined largely by the number of miles driven.This can also be used to illustrate that most costs, in realityhave multiple drivers. Gas cost is also affected by type ofdriving, the horsepower of the engine, and other factors.3.6 Relevant range is the range of activity within which costs behave as predicted.Outside this level of activity, costs behave differently. This is not a concept thatcan be determined from a textbook; observation of the actual costs must be donein order to determine this range.(Exhibit 2-4 illustrates the relevant range of fixed costs atThomas Transport Company.)3.7 In dealing with costs, it is important to distinguish between behaviors of costswhen expressed as unit costs and when dealing with total costs. Generally,decision makers should think in terms of total cost. However, in many decisionanalysis situations, calculating unit costs is essential.Refer to Quiz Question 3 Exercises 2-17 (fixed and variable) and 2-23Interpret unit costs cautiously. . . for many decisions, managers should use totalcosts, not unit costs4.1 Unit costs (also called average costs) are normally used in making decisions suchas product mix and pricing. However, managers should usually think in terms oftotal costs for most decisions.4.2 Fixed costs, when expressed on a unit basis can be misleading. For example, iffixed costs are $25,000 and you manufacture 5.000 units, fixed costs are $5 perunit. When production increases to 6,250 units, total fixed costs remain at$25,000, but the unit cost declines to $4. Avoid using the higher unit cost whenproduction level changes.Refer to Quiz Question 4 Exercise 2-275Distinguish among manufacturing companies,merchandising companies, and service-sectorcompanies. . . different types of companies face differentaccounting issues5.1 Manufacturing-sector companies purchase materials and components andconvert them into finished products.5.2 Merchandising-sector companies purchase and sell tangible products withoutchanging their basis form. These companies are known as retailers.5.3 Service-sector companies provide services (intangibles). However, there isfrequently a tangible aspect to the service.TEACHING POINT. Have the students name companies thatare representative of each sector. Likely, they will correctlyidentify the proper sector for each company. Point out,however, that a service company may have a tangible aspect,such as the tax return as the end product of a tax preparationservice. Conversely, a merchandising company mayemphasize the intangibles. As the saying goes, “sell the sizzle,not the steak.”Refer to Quiz Question 56Describe the three categories of inventoriescommonly found in manufacturing companies. . . the categories are direct materials, work inprocess, and finished goods6.1 The accounting system of a manufacturing company is more complex than for amerchandising or service company. The main reason for this complexity is in theinventories held by a manufacturer. These companies will have three types ofinventory.•Direct Materials Inventory, or simply Materials Inventory, consists of materials being held by the company, ready to begin the conversionprocess into a finished product.•Work-in-Process Inventory represents product partially worked on but not yet completed. WIP is a representation of what is on the factory floor.•Finished Goods Inventory is product that has been completed and has not yet been sold.6.2 Merchandising companies purchase products in their completed form and do notmake changes in their basic form. An inventory account for a merchandisingcompany is called Merchandise Inventory, or simply Inventory.6.3 The Work-in-Process account will have three debits, representing the three typesof manufacturing costs.•Direct material costs are the costs of materials that become part of the cost object and can be traced to the cost object in an economicallyfeasible manner.•Direct manufacturing labor costs include compensation ofmanufacturing labor that can be traced to the cost object in aneconomically feasible manner. This includes labor of workers who workdirectly on the product.•Indirect manufacturing costs are all manufacturing costs that are not direct materials or direct labor. These costs are allocated rather thantraced. Other terms for this category include manufacturing overhead orfactory overhead costs.Refer to Quiz Question 67Differentiate inventoriable costs. . . assets when incurred, then cost of goods soldfrom period costs. . . expenses of the period when incurred7.1 Inventoriable costs are all costs of a product that are considered assets on thebalance sheet. These costs are direct materials, direct labor, and factory overhead.They become a part of the cost of the product and are assets until sold, when they become cost of goods sold. These are also known as product costs.7.2 Period costs are all costs on the income statement other than cost of goods sold.Period costs are treated as expenses of the period in which they are incurred.7.3 Prime cost is a term used to describe all direct costs or direct materials plusdirect labor.7.4 Conversion cost is direct materials plus factory overhead. It is the cost ofconverting the materials into a finished product.TEACHING POINT. Many companies with highly automatedmanufacturing operations have little or no direct labor. Thesecompanies often only use two categories of manufacturingcosts—direct materials and conversion cost.7.5 Costs can be measured in different ways. The management accountant shoulddefine and understand the ways costs are measured in a particular company orsituation.TEACHING POINT. Labor costs can include only the wagepaid to the workers or it can be broadened to include the costof that labor to the employer—the wage rate plus the cost ofbenefits the employee receives. Overtime premium can betreated as direct labor or as overhead.(Exhibit 2-6 illustrates examples of period costs in a bank.)(Exhibit 2-7 shows the flow of costs through the three differenttypes of manufacturing inventory.)(Exhibit 2-8 uses a sample Cost of Goods Manufacturedschedule and a sample Income Statement to illustrate thecalculation and reporting of Cost of Goods Sold.)7.6 Two issues in cost measurement that require special attention are idle time andovertime premium. Idle time is wage paid for unproductive time caused by lackof orders, machine breakdowns, or other reasons. Overtime premium is the wagerate paid to workers in excess of their regular straight-time wage rate. Both ofthese are considered as overhead rather than direct labor costs.Refer to Quiz Questions 7 and 8 Assign Exercises 2-26 and 2-288Explain why product costs are computed indifferent ways for different purposes. . . examples are pricing and product-mixdecisions, government contracts, and financialstatements8.1 Product cost is a term with an ambiguous meaning because there are differentdefinitions of product cost depending on the purpose for measuring that cost.8.2 Pricing and product decisions require an emphasis on the total profitability ofdifferent products and would assign costs incurred in all business functions to theproduct.8.3 Contracting with government agenc ies is frequently done on the “product cost”plus a specified mark up. This is known as cost plus pricing. Governmentagencies frequently have detailed specifications about what costs can be includedin the cost base.8.4 Reporting product cost for financial statement purposes requires adherence toGAAP guidelines for costing.(Exhibit 2-11 illustrates how product costs can vary dependingon the purpose for which product cost is being calculated.)(Exhibit 2-12 lists alternative classifications of costs.)Refer to Quiz Question 99Describe a framework for cost accounting and costmanagement. . . three features that help managers makedecisions9.1 This chapter deals with a number of cost terms and purposes. These concepts canbe expressed in three features of cost accounting that have a wide range of usesin business applications.•Calculating the cost of products, services, and other cost objects.Managers use this information in a variety of ways to formulate strategyand make various decisions.•Obtaining information for planning and control and forperformance evaluation. Budgeting is the most commonly used tool forplanning and control and forces managers to:o Look aheado Translate strategy into planso Coordinate and communicate within the organizationo Provide a benchmark for evaluating performance•Analyzing the relevant information for making decisions. Managers must understand which revenues to consider and which to ignore in thedecision-making process. Management accounting can assist managers indetermining which costs are relevant.Refer to Quiz Question 10V. OTHER RESOURCESPlease visit the textbook companion website at . To download these and other resources, visit the Instructor’s Resource Center or access them on the Instructor’s Resource DVD (IR-DVD).The following exhibits were mentioned in this chapter of the Instructor’s Manual, and havebeen included in the PowerPoint Lecture presentation created specifically for this chapter.You may use the PowerPoint Lecture presentations “as is”, or modify them to suit yourindividual needs.Exhibit 2-1 illustrates examples of cost objects at BMW.Exhibit 2-2 illustrates the assignment of direct and indirect costs at BMW.Exhibit 2-3 displays the cost behavior of variable and fixed costs in total.Exhibit 2-4 illustrates the relevant range of fixed costs at Thomas Transport CompanyExhibit 2-6 illustrates examples of period costs in a bank.Exhibit 2-7 shows the flow of costs through the three different types of manufacturinginventory.Exhibit 2-8 uses a sample Cost of Goods Manufactured schedule and a sample IncomeStatement to illustrate the calculation and reporting of Cost of Goods Sold.Exhibit 2-11 illustrates how product costs can vary depending on the purpose for whichproduct cost is being calculated.Exhibit 2-12 lists alternative classifications of costs.Download pdf images of textbook illustrations and exhibits from the Image Library oraccess them via your IR-DVD.Solutions to Select End-of-Chapter Problems mentioned in this chapter, which have been fully worked out in PowerPoint, are available for download and included on the IR-DVD.CHAPTER 2 QUIZ1.Tanner Co. management desires cost information regarding their Rawhide brand. TheRawhide brand is a(n)a.cost object.b.cost driver.c.cost assignment.d.actual cost.2.The cost of replacement light bulbs on campus would be a direct cost to a college butwould need to be allocated as an indirect cost toa.departments.b.buildings.c.schools.d.individual student instruction.3.What is the total fixed cost of the shipping department of EZ-Mail Clothing Co. if it hasthe following information for 2002?Salaries $800,000 75% of employees on guaranteed contractsPackaging $400,000 depending on size of item(s) shippedPostage $500,000 depending on weight of item(s) shippedRent of warehouse space $250,000 annual leasea. $850,000b. $900,000c. $1,050,000d. $1,950,0004.Morton Graphics successfully bid on a job printing standard notebook covers during theyear using last year’s price of $0.27 per cover. This amount was calculated from prioryear costs, noting that no changes in any costs had occurred from the past year to thecurrent year. At the end of the year, the company manager was shocked to discover that the company had suffered a loss. “How could this be?” she exclaimed. “We had noincreases in cost and our price was the same as last year. Last year we had a healthyincome.” What could explain the company’s loss in income this current year?a.Their costs were all variable costs and the amount produced and sold increased.b.Their costs were mostly fixed costs and the amount produced this year was lessthan last year.c.They used a different cost object this year than the previous year.d.Their costs last year were actual costs but they used budgeted costs to make theirbids.5.Which type of company converts materials into finished products?a.Not-for-profitb.Servicec.Merchandisingd.Manufacturing6.The three categories of inventories commonly found in many manufacturing companiesare:a.Direct materials, direct labor, and indirect manufacturing costs.b.Purchased goods, period costs, and cost of goods sold.c.Direct materials, work in process, and finished goods.d.LIFO, FIFO, and weighted average.7.Inventoriable costs area.only purchased goods for resale.b. a category of costs used only for manufacturing companies.c.recorded as expenses when incurred and later reclassified as assets.d.recorded as assets when incurred.8.Period costs area.all costs in the income statement other than cost of goods sold.b.defined as manufacturing costs incurred this period on the schedule of cost ofgoods manufactured.c.always recorded as assets when first incurred.d.those costs that benefit future periods.9.The cost of a product can be measured as any of the following except as costa.gathered from all areas of the value chain.b.identified as period cost.c.designated as manufacturing cost only.d.explicitly defined by contract.10.The primary focus of cost management is toa.help managers make different decisions.b.calculate product costs.c.aid managers in budgeting.d.distinguish between relevant and irrelevant information.CHAPTER 2 QUIZ SOLUTIONS1. a2. d3. a4. b5. c6. c7. d8. a9. b10. aQuiz Question Calculations3. Fixed costs = (800,000) 75% + 250,000 = $850,000。

成本与管理会计亨格瑞第13版英文版CA

The development of management accounting emerged in the 1920s, when the focus shifted from mere cost measurement to cost analysis and control, emphasizing the role of accounting in decision-making and management control.

It involves the identification, measurement, and allocation of costs, as well as the preparation of cost reports and other management information to assist management in making decisions about product pricing, production, and resource allocation.

Direct and indirect costs

Activity Identification

The first step in the activity-based costing method involves identifying the various activities that take place within the organization.

Cost allocation and collection

Cost Allocation

Allocating costs to specific departments, projects, or products is essential for accurate financial reporting and decision-making.

成本与管理会计-亨格瑞-第13版-英文版-CA07共75页文档

2020/6/8

10

Static Budget

What was the actual operating profit?

Revenues (10,000 × $125) $1,250,000

Less Expenses:

Variable (10,000 × $95.01)

950,100

Fixed

285,000

TOTAL VARIABLE COST

VARIABLE COST PER JACKET

$60 16 12

$88

BUDGETED FIXED COSTS FOR PRODUCTION(0-12 000UNITS) BUGETED SELLING PRICE BUDGETED PRODUCTION AND SALES ACTUAL PRODUCTION AND SALES

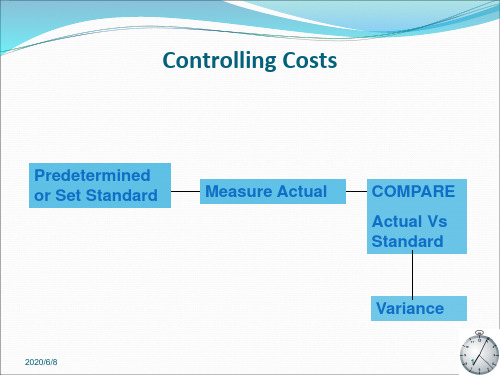

Purpose of variance

➢ Management by exception ➢ Performance evaluation ➢ Motivate managers ➢ Prompt strategy change

2020/6/8

2

Basic Concepts

Management by Exception – the practice of focusing attention on areas not operating as expected (budgeted)

2020/6/8

$276 000 $120/JACKET 12 000JACKETS 10 000JACKETS

6

2020/6/8

7

Static Budget

es and sells jackets.

成本与管理会计-亨格瑞-第13版-英文版-CA08_图文_图文

15

Variable overhead spending variance

=($29/machine hour-$30 /machine hour) ×4 500 machine-hours =(-1machine hour) ×4 500 machine-hours =$4 500F

=1 728 000/57 600=30/hour

Budgeted variable overhead cost rate per output unit

5

=0.4hour/unit×30=12/jacket

Variable overhead cost variances(P208 )

6

Flexible-budget analysis

The variable overhead efficiency variance measures the efficiency with which the costallocation base is used.

11

Variable Overhead Variances

Actual Variable Overhead Incurred

Step 3:

Identify the variable overhead costs associated with each costallocation base.

Step 4:

Compute the rate per unit of each cost-allocation base used to allocate variable overhead costs to output produced.

成本与管理会计-亨格瑞-第13版-英文版-CA08

Flexible Budget for Variable Overhead at Actual Hours

AH × SVR

Flexible Budget for Variable Overhead at

Standard Hours

SH × SVR

Spending Variance

Efficiency Variance

Workers were less skilled than expected in using machines?

Webb spend more on variable overhead costs , such as maintenance?

8

2019/10/7

Variable Overhead Variances

=$15 000U

14

2019/10/7

4500 HOURS VS 4000 HOURS

Possible causes for exceeding budget

Workers were less skilled than expected in using machines

Production scheduler inefficiently scheduled jobs ,resulting in more machinehours used than budgeted

overhead cost

Efficiency

cost-alocation base alocation based alowed

per unit of

Variance

used for actual output for actual output

成本与管理会计-亨格瑞-第13版-英文版-CA04共76页PPT资料

Learning objective 1 Learning objective 1

Basic Costing Terminology,conts.

Cost Assignment

Direct Costs

Indirect Costs

Cost Object

Cost Allocation

overhead

including responsibility

The direct costs of a cost object are costs that are related to the cost object and can be traced to the cost object in an economically feasible manner.

centers, departments,

customers, products, etc.

Basic Costing Terminology ,conts.

Cost assignment is a general term that includes cost tracing and cost allocation.

Costing

•Adjusting the Systems •Job costing vs

Over/Underappl

Process costing

ied Situations

Structure

•Journal Entries for the flow of

亨格瑞成本与管理会计

亨格瑞成本与管理会计

亨格瑞成本与管理会计(Hengry Cost and Management Accounting)是一种用于管理决策和成本控制的会计方法。

它提供了详细的成本信息,以帮助管理者做出准确的决策,并监控和控制企业的成本。

亨格瑞成本与管理会计主要包括以下几个方面:

1. 成本分类与分析:亨格瑞成本与管理会计通过对成本进

行分类和分析,帮助企业了解各项成本的性质和构成,并

将其与企业的经营活动相对应。

常见的成本分类包括直接

成本和间接成本、可变成本和固定成本等。

2. 成本核算与计算:亨格瑞成本与管理会计通过成本核算

和计算,确定各个产品或服务的成本,并将其分配到相应

的产品或服务上。

这有助于企业了解不同产品或服务的盈

利能力,并进行定价和销售策略的制定。

3. 成本控制与预算:亨格瑞成本与管理会计通过成本控制

和预算,帮助企业控制和管理成本,并制定合理的预算计划。

通过对实际成本与预算成本的比较,企业可以及时发

现和纠正成本偏差,并采取相应的措施进行成本控制。

4. 决策支持与绩效评估:亨格瑞成本与管理会计提供了决

策支持和绩效评估的信息。

通过对不同决策方案的成本效

益分析,帮助企业做出合理的决策,并评估和监控企业的

绩效。

总之,亨格瑞成本与管理会计是一种重要的管理工具,通过提供详细的成本信息和决策支持,帮助企业进行成本控制和管理,并提高企业的绩效和竞争力。

成本和管理会计亨格瑞第13版英文版CA01

reports financial and nonfinancial information to help managers make decisions to fulfill organizational goals. Managerial accounting need not be GAAP compliant.

8

Past-oriented

GAAP compliant; CPA audited Historical monthly, quarterly reports Indirect effects on employee behavior

1.

LEARNING OBJECTIVE 1

Describe how cost accounting supports

management accounting and financial accounting

2018/11/21

3

Accounting Discipline Overview

Financial Accounting – focus on reporting to

external users including investors, creditors, and governmental agencies. Financial statements must be based on GAAP.

Amounts and kinds of material used

Changes in plant processes Changes in product designs

管理会计第十三版英文影印版教学设计

Managerial Accounting 13th Edition English PhotocopyTeaching DesignIntroductionManagerial accounting is a critical component of any business operation as it ds in decision-making, provides financial informationfor internal use, and helps management in controlling costs andfinancial risks. As such, it is essential that students of accounting and business have a clear understanding of managerial accounting and its practical applications.The 13th edition of Managerial Accounting, an English photocopy version, provides in-depth coverage of the subject matter and helps students develop a strong foundation of knowledge for their future careers. The purpose of this teaching design is to provide an outline of the topics and teaching methods for the 13th edition of Managerial Accounting.Course OverviewCourse TitleManagerial AccountingCourse DescriptionThe course is designed for students who have a basic knowledge of financial accounting and wish to gn a deeper understanding of managerial accounting concepts. The course covers topics such as cost behavior,cost-volume-profit analysis, budgeting, responsibility accounting, and capital budgeting.Course GoalsThe primary goal of the course is to enable students to understand the fundamental principles of managerial accounting and how they can be applied in real-world situations. Specifically, the course ms to: •Develop students’ understanding of cost behavior and how to use it to make business decisions•Provide students with the skills to analyze and interpret financial information for internal use•Help students understand the various types of budgets and how they are used in managerial accounting•Develop students’ understanding of responsibility accounting and how it can be used to monitor performance•Help students understand the process of capital budgeting and how to evaluate investment projectsCourse Requirements•Attend lectures and participate in class discussions•Complete assigned readings and homework•Take quizzes and examsTeaching MethodologyLecturesThe course will be delivered through a series of lectures. In these lectures, the instructor will use a combination of PowerPointpresentations, case studies, and group discussions to illustrate key concepts and reinforce understanding. Lectures are designed to provide students with a comprehensive understanding of each topic covered in the course.Case StudiesCase studies are an important element of the course as they help students apply what they have learned in real-world situations. Students will be assigned case studies that require them to analyze financial data, interpret budgets, and make business decisions based on the information provided.Group DiscussionsGroup discussions will enable students to share their experiencesand perspectives on various managerial accounting concepts. They will be encouraged to provide insight on how the concepts can be applied intheir future careers and to generate ideas for resolving business issues.Quizzes and ExamsQuizzes and exams are designed to evaluate stude nts’ comprehensionof the course materials. Students will be tested on their understanding of key managerial accounting concepts and their ability to analyze financial data, interpret budgets, and make business decisions based on the information provided.AssessmentAssessment of student learning will be based on the following: •Quizzes (25%)•Midterm Exam (35%)•Final Exam (40%)ConclusionThe 13th edition of Managerial Accounting provides students with a comprehensive understanding of managerial accounting concepts and their practical applications. Through the use of lectures, case studies, and group discussions, students will be able to apply what they have learned in real-world situations and develop a strong foundation of knowledge that will serve them well in their future careers.。

成本与管理会计 亨格瑞 第13版 英文版 CA02

管理分析的方法与指标

添加 标题

财务比率分析:通过计算各种财务比率,如 流动比率、速动比率、存货周转率等,来评 估企业的偿债能力、营运能力和盈利能力。

添加 标题

结构分析:通过分析财务报表中各项目的构 成比例,了解企业各项业务的比重和结构特 点。

添加 标题

因素分析:通过分析影响企业财务状况的各 种因素,如市场环境、政策变化等,预测未 来的发展趋势。

间接成本法

定义:间接成本法是一种将间接成本分配到产品或服务中的成本计算方法

特点:将间接成本与直接成本一起分配到产品或服务中,以计算产品的总成本

适用范围:适用于生产过程中存在大量间接成本的情况

计算方法:根据不同的分配标准,如人工小时、机器工时等,将间接成本分配到产品或 服务中

作业成本法

定义:作业成本法是一种基于作业的成本核算方法,通过对作业进行成本分配,计算出产品或服 务的成本。

提供支持

现代管理会计: 进入21世纪,管 理会计更加注重 战略决策、风险 管理、绩效评价 等方面,成为企 业核心竞争力的

重要组成部分

管理会计的未来 发展:随着科技 的不断进步和全 球化的趋势,管 理会计将更加注 重数据分析和预 测,为企业提供 更加全面、精准

的支持

管理会计的基本原则和概念

管理会计的定义和目的 管理会计的基本原则 管理会计的概念框架 管理会计与财务会计的区别和联系

添加标题

成本会计的基本内容:成本会计主要包括成本核算、成本分析、成本控制等方面。其中,成本核算是对企业 生产经营过程中的各种成本进行分类、归集和分配的过程;成本分析是对企业成本进行比较、分析和评价的 过程;成本控制则是通过制定一系列措施,对企业生产经营过程中的成本进行监督和控制的过程。

成本与管理会计 亨格瑞 第 英文版

2020/4/17

3

LEARNING OBJECTIVE 1

Explain how broad averaging undercosts and overcosts products or services

P110

entree

dessert

drinks

total

emma

11

0

4

15

james

20

8

14

42

jessica

15

4

8

27

matthew

14

4

6

24

total

60

16

32

108

average

15

4

8

27

2020/4/17

6

Broad Averaging and Cross-subsidization,conts.

based management Compare activity-based costing systems and department costing

systems Evaluate the costs and benefits of implementing activity-based

costing systems

Present three guidelines for refining a costing system Distinguish between simple and activity-based costing systems Describe a four-part cost hierarchy Cost products or services using activity-based costing Explain how activity-based costing systems are used in activity-

成本与管理会计亨格瑞第13版英文版CA07

➢ Management by exception ➢ Performance evaluation ➢ Motivate managers ➢ Prompt strategy change

2021/1/13

3

3

Basic Concepts

Management by Exception – the practice of focusing attention on areas not operating as expected (budgeted)

Key difference is the use of the actual output level in the flexible budget.

2021/1/13

6

6

COST CATEGORY

DIRECT MATERIAL COST DIRECT MANUFACTURING LABOR COST VARIABLE MANUFACTURING OVERHEAD COSTS

Direct Material

Standard

Type of Product Cost

5

2021/1/13

5

Static and Flexible Budgets

Static budget

➢ Prepared for only one level of activity. ➢ It is based on the level of output planned at the start of

成本与管理会计亨 格瑞第13版英文版

CA07

Controlling Costs

Predetermined or Set Standard

《成本与管理会计》教师手册 costacctg13_im_04

Job CostingTRANSITION NOTESThe five-step decision process continues to be utilized in this chapter. This model is used in decision-making situations involving job costing, such as whether to bid on a job and the amount to bid. This process is illustrated by means of a decision-making example early in the chapter. The authors retain the seven step approach to job costing, which is the process the company undergoes to develop the job costing system. In line with the increased managerial emphasis, the use of materials, direct labor, work-in-process, and other subsidiary records is given additional emphasis. Many new problems have been introduced at the end of thechapter, and others have been revised.PROBLEM MATERIALCORRELATION CHART13th Edition 12thEdition13thEdition12thEdition161630 New17 Revised17 31 30181832 3119 Revised19 33 32202034 33212135 34222236 New23 Revised23 37 36242438 3725 New39 New262640 New272741 40282842 New29 NewI. LEARNING OBJECTIVES1.Describe the building-block concepts of costing systems2.Distinguish job costing from process costing3.Outline the seven-step approach to job costing4.Distinguish actual costing from normal costing5.Track the flow of costs in a job-costing system6.Dispose of underallocated or overallocated manufacturing overhead costs at theend of the fiscal year using alternative methods7.Apply variations from normal costing4II. CHAPTER SYNOPSISChapter 4 outlines the basics of costing systems by illustrating the accounting for costs ina typical job-costing system. Two new key terms related to costing systems areintroduced in this chapter; they are: cost pool and cost-allocation base.The chapter distinguishes job-costing systems from process-costing systems. Job-costing systems track costs to distinct jobs, whereas process-costing systems apply the averagecost to each unit of a large batch of identical or similar products. The seven-step process to job-costing is outlined, and normal-costing systems using standard costs are compared to actual-costing systems that use actual costs. The total of actual indirect costs oftendiffers from the total of indirect costs applied in standard-costing systems and the chapter illustrates how to account for any underallocation or overallocation of indirect costs at the end of the fiscal period.III. POINTS OF EMPHASIS1.If students have not grasped the terminology of cost accounting before beginningthis chapter, they are likely to remain in a “catch-up” mode for the rest of theclass. Make sure they understand the terminology before proceeding.2.Walking the students through the documents associated with job costing will helpthem understand the flow involved in a job-costing system. Relate thesedocuments to the seven steps in a job-costing system. Then tie the seven steps tothe journal entries and the flow of costs.3.Be sure the students grasp the definitions of actual and normal costing.4.Students should be able to calculate and understand the reasons for apredetermined overhead rate.IV. CHAPTER OUTLINE1Describe the building-block concepts of costingsystems. . . the building blocks are cost object, direct costs,indirect costs, cost pools, and cost-allocation basesBecause of the complexity of most manufacturing operations, companies need toestablish a system to track costs so they can properly determine product costs. Beforemoving into the details of these systems, the student should have a grasp of costaccounting terminology. From Chapter 2:1.1 A cost object is anything for which a measurement of costs is desired.1.2The direct costs of a cost object are costs that are related to the cost object andcan be traced to the cost object in an economically feasible manner.1.3The indirect costs of a cost object are costs that cannot be traced to the costobject in a cost-effective manner and are allocated to the cost object.1.4Cost assignment is a general term that includes cost tracing and cost allocation.1.5Two new terms related to costing systems are introduced in this chapter; they arecost pool, and cost-allocation base.• A cost pool is a grouping of individual indirect cost items.• A cost-allocation base is the driver or activity that is used to allocateindirect costs from the cost pool to the cost object.TEACHING POINT. These terms are the building blocks ofcosting systems. Take time at this point to reinforce theimportance and meaning of these terms. Go beyond having thestudents know the definitions; use illustrations to help themunderstand the terms operationally.Refer to Quiz Question 12Distinguish job costing. . . job costing is used to cost a distinct productfrom process costing. . . process costing is used to cost masses ofidentical or similar units2.1 Management uses two basic types of costing systems to assign costs to productsor services.•A job-costing system, or a job-order system, is used by a company thatmakes a distinct product or service called a job. The product or service isoften a single unit. The job is frequently the cost object. Costs areaccumulated separately for each job or service.•A process-costing system is used by a company that makes a largenumber of identical products. Costs are accumulated by department anddivided by the number of units produced to determine the cost per unit. Itis an average cost of all units produced during the period. The cost objectis masses of similar units of a product or service.TEACHING POINT. Give examples of products or services thatwould be accounted for under each system. A mechanic’sinvoice from a car repair shop is a good illustration of job-ordercosting, as it has direct materials, direct labor, and overheadsections. Point out that each repair job is different; the repairshop does not perform the same activities on each vehiclebrought in for repairs, therefore, it is accounted for under a job-costing system.As an example of a process system, you can use aninexpensive pen that some students will be using. Point outthat the manufacturer makes millions of these. Although theydiffer in ink color and point size (medium, fine, etc.) theprocess is the same—the company just uses black instead ofblue, fine instead of medium, and the pens are manufacturedby the same process at the same cost for each pen.2.2 The documents associated with a job-costing system are at the heart of job-ordercosting.•The job-cost record, also called a job-cost sheet, records all costsincurred on a particular job. Note that there are sections for directmaterial, direct labor, and overhead. Emphasize that the job-cost recordserves as a subsidiary ledger for work-in-process, then finished goods,and for the amount of cost of goods sold.•The materials-requisition record is completed to obtain materials for aparticular job from the materials storeroom. It must be properlycompleted and signed and forms the basis for the materials entry into thejob-cost record.•The labor-time record is completed by the employee to indicate whatjobs were worked on. This forms the basis for the direct labor entry intothe job-cost record. Note that this is a separate document from the clockcard; the clock card indicates how many hours the employee worked.The labor-time record indicates what work the employee performed.(Exhibit 4-1 offers examples of job costing and process costingin different sectors.)(Exhibits 4-2 and 4-3 display sample job-cost records.)Refer to Quiz Question 2 Exercise 4-163Outline the seven-step approach to job costing. . . the seven-step approach is used to computedirect and indirect costs of a job3.1 Actual costing is a costing system that traces direct costs to a cost object byusing actual direct-cost rates times the actual quantities of the direct-cost inputs.It allocates indirect costs based on the actual indirect-cost rate times the actualquantities of the cost-allocation bases.3.2 A seven-step approach is used to assign costs to an individual job. This approachis used by manufacturers, merchandisers, and companies in the service sector.Step 1:Identify the Job That Is the Chosen Cost Object. The sourcedocuments such as the job-cost sheet, the material-requisitionrecord, and the labor-time record assist managers in gatheringinformation about the costs incurred on a job.Step 2:Identify the Direct Costs of the Job. Most manufacturingoperations have two direct cost categories—direct materials anddirect manufacturing labor.Direct materials are ordered by means of a materials requisition.Quantities needed are based upon engineering specifications. Aspreviously indicated, the labor-time record indicates the amountof time an employee spends on a particular job.Step 3:Select the Cost-Allocation Bases to Use for AllocatingIndirect Costs to the Job. Since these costs cannot be traced tothe job, they must be allocated in a systematic manner.Step 4:Identify the Indirect Costs Associated with Each Cost-Allocation Base. Hopefully, a cause-and-effect relationship canbe established between the costs incurred and the cost-allocationbase (or cost driver).Step 5:Compute the Rate per Unit of Each Cost-Allocation BaseUsed to Allocate Indirect Costs to the Job.Actual manufacturing overhead rate = Actual manufacturingoverhead costs/Actual total quantity of cost allocation base.Step 6:Compute the Indirect Costs Allocated to the Job. Multiply theactual quantity of each different allocation base by the indirectcost rate for each allocation base.Step 7:Compute the Total Cost of the Job by Adding All Direct andIndirect Costs Assigned to the Job.(Exhibit 4-4 displays an overview of a typical job-costingsystem.)3.3 With modern technology, managers have much more timely and accurate productcost information, making it easier to manage and control jobs. Electronic DataInterchange (EDI), bar coding, electronic materials-requisition records, andelectronic labor-time records are just a few of the innovations that have enhancedjob-order cost systems.3.4 Normally, indirect cost rates are computed on an annual basis. There are tworeasons for using annual rates:•The numerator reason (indirect cost pool) avoids seasonal fluctuationsby incorporating a full year’s business cycle into the equation.•The denominator reason (quantity of the cost-allocation base) spreadsfixed costs over the course of a year, rather than using fluctuatingquantities each month.Refer to Quiz Question 34Distinguish actual costing. . . actual costing uses actual indirect-cost ratesfrom normal costing. . . normal costing uses budgeted indirect-costrates4.1 Normal costing is a costing system that:•traces direct costs to a cost object by using actual direct-cost rates timesthe actual quantities of the direct-cost inputs, and•allocates indirect costs based on the budgeted indirect-cost rates timethe actual quantities of the cost-allocation bases.4.2 Normal costing is frequently used to enable managers to overcome the problemsassociated with actual overhead rates encountered in actual costing.TEACHING POINT. Students frequently do not immediatelygrasp the difference in actual and normal costing. Emphasizethat the only difference in the two is in overhead. Actual costinguses actual overhead whereas normal costing usespredetermined (or budgeted) overhead rates.(Exhibit 4-5 differentiates actual and normal costing.)Refer to Quiz Question 4 Exercises 4-17 and 4-18Track the flow of costs in a job-costing system. . . from purchase of materials to sale of finishedgoods5.1 The flow of costs in a job-costing system can best be observed by tracing thejournal entries associated with such a system.5.2 Recall that manufacturing costs are product costs and that a manufacturer willhave three inventory accounts—materials, work-in-process, and finished goods.5.3 Illustrate the flow of costs by using journal entries and T-accounts.TEACHING POINT. Get the students engaged in the flow ofcosts with journal entries, T-accounts, and flow charts drawn onthe board. An understanding at this point will go a long waytoward helping the student transition to a manufacturing mindset.Exercise 4-24 is a good one to walk through to illustrate this.5.4 The manufacturing overhead accounts need some explanation here.Manufacturing overhead control represents actual manufacturing overheadincurred. These amounts would be expense in a non-manufacturing setting.Manufacturing overhead applied represents the amount of overhead allocatedto jobs. Some companies use only a single Manufacturing Overhead account.5.5 Materials, Work-in-Process, Finished Goods, and Manufacturing OverheadControl all are accounts having subsidiary ledgers explaining the balance in thegeneral ledger account.5.6 Note the importance of the job-cost sheet. It is the subsidiary ledger for Work-In-Process and becomes the subsidiary ledger for Finished Goods. When the productis sold, it is the basis for the amount of the journal entry to record COGS.TEACHING POINT. Recalling that companies use differentcosts for different purposes, a company could include directmarketing costs and customer-service costs to jobs, asappropriate.(Exhibits 4-6 through 4-8 display the flow of costs in a job-costing system.)Refer to Quiz Questions 5-7 Exercises 4-24 through 4-26Dispose of underallocated or overallocatedmanufacturing overhead costs at the end of thefiscal year using alternative methods. . . for example, writing off this amount to the Costof Goods Sold account6.1 Under normal costing there will be a difference in the balances of theManufacturing Overhead Control and the Manufacturing Overhead Appliedaccounts. This balance needs to be disposed of at the end of the year.6.2 If the Control account balance exceeds the Applied account balance, overheadhas been underapplied.6.3 If the Applied account balance exceeds the Control account balance, overheadhas been overapplied.TEACHING POINT. An illustration of a glass of water helps thestudents visualize this concept. Actual overhead is the waterpoured into the glass until it is full. When overhead is applied,water is removed from the glass. If any water remains, actualoverhead exceeds applied and overhead is underapplied. Ifthere is not enough water, applied overhead exceeds actualand overhead is overapplied.6.4 There are three approaches to dealing with the under- or overapplied overhead—the adjusted allocation rate-approach, the proration approach or the write off tocost of goods sold approach.•The adjusted allocation-rate approach restates all overhead entries in the general and subsidiary ledgers using actual rates rather than budgetedrates. With computerized systems, this approach has become easier toimplement. The approach gives the timeliness and convenience ofnormal costing during the year and the actual amounts at year end forplanning purposes.•The proration approach spreads the underallocated or overallocated overhead to Work-in-Process, Finished Goods, and Cost of Goods sold inproportion to the ending balances in these accounts.TEACHING POINT. Students will want to include the materialsaccount in this proration. Point out that overhead is beingprorated to those accounts that have overhead amounts inthem so materials should not receive an allocation.•The write-off to cost-of-goods-sold approach is the simplest. Under this approach the underallocated or overallocated overhead is simplywritten off to cost of goods sold. This method is acceptable if the amountis immaterial.TEACHING POINT. In a normal operating situation, the bulk ofthe adjustment would go to cost of goods sold under theproration approach. Therefore, the total amount of theadjustment must be very large before the amount becomessignificant enough to avoid usage of the write-off approach.Illustrate the three methods.Refer to Quiz Questions 8 and 9 Problem 4-347Apply variations from normal costing. . . variations from normal costing use budgeteddirect-cost rates7.1Job costing can also be utilized in service industries with a great deal of success.However, it is most useful when a variation of normal costing is applied.7.2 Under a variation from normal costing, direct labor costs are assigned to jobsbased on predetermined direct labor rates. The approach facilitates costing ofjobs as it is often difficult to determine the actual labor cost associated with aparticular job as it is completed.7.3 To implement this variation, calculate a budgeted direct labor rate by dividingbudgeted total direct labor costs by the budgeted total direct labor hours. This rate isthen applied to specific jobs based on the number of direct labor hours consumed bythe job.Refer to Quiz Question 10 Problem 4-29V. OTHER RESOURCESPlease visit the textbook companion website at . To download these and other resources, visit the Instructor’s Resource Center or access them on the Instructor’s Resource DVD (IR-DVD).The following exhibits were mentioned in this chapter of the Instructor’s Manual, andhave been included in the PowerPoint Lecture presentation created specifically for this chapter. You may use the PowerPoint Lecture presentations “as is”, or modify them tosuit your individual needs.Exhibit 4-1 offers examples of job costing and process costing in different sectors.Exhibits 4-2 and 4-3 display sample job-cost records.Exhibit 4-4 displays an overview of a typical job-costing system.Exhibit 4-5 differentiates actual and normal costing.Exhibits 4-6 through 4-8 display the flow of costs in a job-costing system.Download pdf images of textbook illustrations and exhibits from the Image Library oraccess them via your IR-DVD.Solutions to Select End-of-Chapter Problems mentioned in this chapter, which havebeen fully worked out in PowerPoint, are available for download and included on the IR-DVD.CHAPTER 4 QUIZ1. A cost-allocation base may be any of the following except aa.cost driver.b.cost pool.c.way to link indirect costs to a cost object.d.nonfinancial quantity.2. A company that manufactures dentures for use by local dentists would usea.process costing.b.personal costing.c.operations costing.d.job costing.3.The first step in the seven-step approach to job costing is toa.select the cost-allocation base to use in assigning indirect costs to the job.b.identify the direct costs of the job.c.identify the job that is the chosen cost object.d.identify the indirect-cost pools associated with the job.ing normal costing rather than actual costing requires that the allocating of indirectmanufacturing costs to work-in-process bea.done on a more timely basis, such as every two weeks rather than every month.b.journalized only at year end when adjusting entries are normally made.c.calculated by using the budgeted rate times actual quantity of allocation base.d.calculated by using the budgeted rate times the budgeted quantity of allocationbase.5.Manufacturing Overhead Controla.represents actual overhead costs incurred.b.has a normal debit balance.c.is a control account with a subsidiary ledger detailing the components ofmanufacturing overhead.d.All of the above6.Which of the following accounts is not classified as an asset?a.Manufacturing Overhead Controlb.Materials Controlc.Work-in-Process Controld.Finished Goods Control7.The costs incurred on jobs that are currently in production but are not yet complete wouldappear in thea.Materials Control account.b.Finished Goods Control account.c.Manufacturing Overhead Control account.d.Work-in-Process Control account.8.The Precision Widget Company had the following balances in their accounts at the end ofthe accounting period:Work-in-Process $ 5,000Finished Goods 20,000Cost of Goods Sold 200,000If their manufacturing overhead was overallocated by $8,000 and Precision Widgetadjusts their accounts using a proration based on total ending balances, the revised ending balance for Cost of Goods Sold would bea. $192,880.b. $200,00.c. $207,120.d. $208,000.9.Liberty Box Company calculated an indirect-cost rate of $12.50 per labor hour for fringebenefits for use in their normal costing system. At the end of the year, the actual cost offringe benefits was $980,000. The total of labor hours worked for the year was the sameamount as budgeted, 70,000 hours. If Job #640 required the use of 15 labor hours and the company used the adjusted allocation rate approach, by what amount would the cost ofJob #640 change?a.$560.00b.$281.25c.$22.50d.$20.5010.If each professional in a service company is paid on an annual salary basis, why mightthe firm want to use a predetermined or budgeted rate for direct or professional labor?a. A predetermined or budgeted rate is easier to justify to a client who mightquestion a billing rate.b.Professional staff persons do not keep accurate records of the jobs on which theywork.c.Professional staff incurs more client costs, such as travel, lodging, and out-of-town meals, while working on a job.d.Year-end bonuses paid to the professional staff are difficult to trace to individualjobs.CHAPTER 4 QUIZ SOLUTIONS1. b2. d3. c4. c5. d6. a7. d8. a9. c10. dQuiz Question Calculations8.Work in Process $5,000 / 225,000 2.2% ⨯ $8,000 = 176Finished Goods $20,000 /225,000 8.9% ⨯ $8,000 = 712Cost of Goods Sold $200,000 / 225,000 88.9% ⨯ $8,000 = 7,120 200,000 – 7,120 = $192,8809. 980.000/70,000 = $14.00 (actual rate)$14,000 – $12.50 = $1.50 excess of actual over budget1.50 ⨯ 15 hours – $22.50 additional cost。