四大审计报告英文缩写

审计 英语词汇

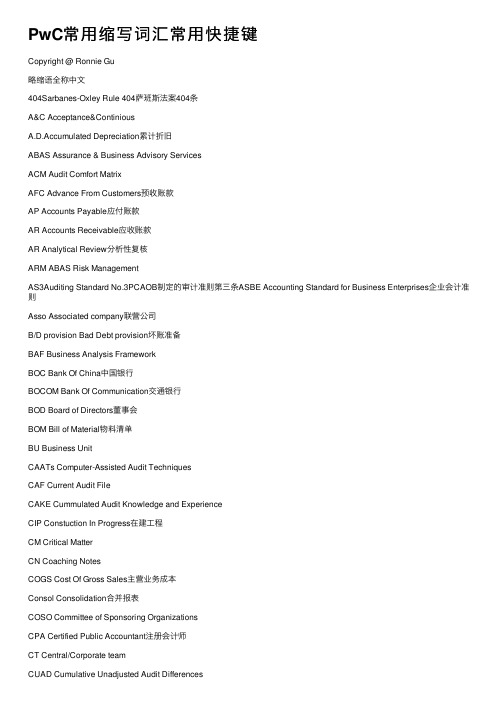

审计英语词汇审计法Audit Law, Audit Act审计法实施条例the Implementary Rules of the Audit law审计标准audit criteria,audit standard审计准则auditing standard审计原则auditing principles审计手册audit manual公认审计准则Generally Accepted Auditing Standards审计法律规范audit laws and regulations审计体制audit system审计权限audit purview;audit jurisdiction;audit mandate 审计职责audit responsibility审计监督audit supervision;supervision through auditing 审计管辖权audit jurisdiction审计执法implementation of audit laws and regulations审计处理audit sanction审计处罚audit penalty依法审计conduct auditing in accordance with laws审计意见audit opinion审计决定audit decision审计建议audit suggestion, audit recommendation复核意见conclusion of audit review审计复议audit appeal审计听证audit hearing审计复核audit review审计战略audit strategy审计计划audit plan审计方案auditing program 审计目标auditing objective 审计范围audit scope审计内容audit coverage审计结论audit conclusion审计任务audit assignments 审计结果audit finding审计报告audit report审计方法audit method审计过程auditing process审计证据audit evidence审计测试audit test审计风险audit risk审计抽样audit sampling审计软件audit software审计程序auditing procedures 审计调查audit investigation审计小组audit team审计线索audit trail工作底稿working paper绕过计算机审计auditing around the computer通过计算机审计auditing through the computer计算机辅助审计computer-assited audit信息技术审计IT audit合法性审计compliance audit, regularity audit合规性审计compliance audit综合审计comprehensive audit效益审计value for money audit (VFM audit)绩效审计performance audit财务审计financial audit财务报表审计financial statement audit财务收支审计audit of financial revenues and expenditures 决算审计final account audit经济责任审计accountability audit任中经济责任审计middle term accountability audit离任经济责任审计term-end accountability audit管理审计management audit项目审计project audit外部审计external audit内部审计internal audit政府审计government audit联合审计joint audit实地审计field audit期末审计final audit期中审计interim audit定期审计periodic audit初次审计initial audit初步审计preliminary audit事后审计post-audit事前审计pre-audit事中审计concurrent audit专项审计special audit法定审计statutory audit后续审计successive audit跟踪审计follow up audit全过程审计whole process auditing 突击审计surprise audit审计报告audit report标准报告standard report长式报告long-form report短式报告short-form report审计工作报告audit working report审计结果公告Announcement of Audit Findings审计长Auditor General副审计长Deputy Auditor General审计主任chief auditor资深审计师senior auditor审计师(员)auditor注册内部审计师certified internal auditor(CIA)注册信息系统审计师certified information systems auditor(CISA)注册公共会计师certified public accountant(CPA)特许会计师chartered accountant(CA)审计经费audit funds审计业务费audit operating expense审计专项经费special funds for auditing无保留意见:unqualified opinion保留意见qualified opinion无法表示意见: disclaimer of opinion否定意见:adverse opinion招生简章:物流师| 国际货代| 报关员| 报检员| 采购师| 学历教育用户帮助:关于我们| 联系我们| 用户手册| 在线报名| 支付方式| 论坛•首页•智丰培训•智丰人才•智丰就业•智丰咨询•智丰知识库•智丰俱乐部•会员专区•视频专区2008年暑期班生简章站内搜索: google提供|管理文章|资料下载|培训课件|管理文章分类大学生就业合同管理供应链管理绩效考核CRM专栏产品管理人力资源企业家动态国际管理成本管理战略管理流程管理生产管理知识管理管理方法管理杂谈管理理论自我成长营销管理财务税汇质量管理顾客管理领导力管理信息企业管理物流管理项目管理制度大全表格大全实用审计英语词汇(1)作者:admin发表时间:2008-3-5 11:31:27浏览117次发表/转载文章可换积分实用审计英语词汇(一)1 ability to perform the work能力履行工作2 acceptance procedures承兑程序过程3accountability 经管责任,问责性4accounting estimate会计估计5accounts receivable listing应收帐款挂牌6 accounts receivable应收账款7accruals listing 应计项目挂牌8accruals应计项目9accuracy准确性10adverse opinion否定意见11aged analysis年老的分析(法,学)研究12agents代理人13agreed-upon procedures 约定审查业务14analysis of errors错误的分析(法,学)研究15anomalous error反常的错误16appointment ethics任命伦理学17appointment 任命18associated firms联合的坚挺19association of chartered certified accounts(ACCA)特计的证(经执业的结社(ACCA)20assurance engagement保证债务21assurance保证22audit 审计,审核,核数23audit acceptance审计承兑24audit approach审计靠近25audit committee审计委员会,审计小组26ahudit engagement 审计业务约定书27audit evaluation审计评价28audit evidence审计证据29audit plan审计计划30audit program审计程序31 audit report as a means of communication审计报告如一个通讯方法32audit report审计报告33audit risk 审计风险34audit sampling审计抽样35audit staffing审计工作人员36audit timing 审计定时37audit trail审计线索38 auditing standards审计准则39auditors duty of care 审计(查帐)员的抚养责任40auditors report审计报告41authority attached to ISAs代理权附上到国际砂糖协定42automated working papers自动化了工作文件43 bad debts坏账44bank银行45 bank reconciliation银行对账单,余额调节表46beneficial interests受益权47best value最好的价值48business risk经营风险49cadbury committee cadbury委员会50cash count现金盘点51cash system兑现系统52changes in nature of engagement改变债务的性质上53charges and commitments费用和评论54charities 宽大55tom walls tom墙壁56 chronology of an audit一审计的年代表57CIS application controls CIS申请控制58CIS environments stand-alone microcomputers CIS环境单机微型计算器59client screening委托人甄别60closely connected接近地连接61clubs俱乐部62communications between auditors and management通讯在审计(查帐)员和经营之间63communications on internal control 内部控制上的通讯64companies act公司法65comparative financial statements比较财务报表66 comparatives比较的67competence能力68compilation engagement编辑债务69 completeness完整性70completion of the audit 审计的结束71compliance with accounting regulations 符合~的作法会计规则72computers assisted audit techniques (CAA Ts)计算器援助的审计技术(CAATs)73 confidence信任74confidentiality保密性75confirmation of accounts receivable应收帐款的查证76conflict of interest利益冲突77constructive obligation建设的待付款78contingent asset或有资产79contingent liability或有负债80control environment控制环境81control procedures控制程序82control risk控制风险83controversy论战84corporate governance 公司治理,公司管制85corresponding figures相应的计算86cost of conversion转换成本,加工成本87cost 成本88courtesy优待89 creditors债权人90current audit files本期审计档案91database management system(DBMS)数据库管理制度(数据管理系统)92date of report 报告的日期93depreciation折旧,贬值94design of the sample样品的设计95 detection risk检查风险96direct verification approach 直接核查法97directional testing方向的抽查98directors emoluments董事酬金99directors serve contracts董事服务合约100disagreement with management与经营的不一致101disclaimer of opinion拒绝表示意见102distributions分销,分派103documentation of understanding and assessment of control risk 控制风险的协商和评定的文件编集104documenting the audit process证明审计程序105due care应有关注106due skill and care到期的技能和谨慎107 economy经济108education教育109effectiveness效用,效果110efficiency效益,效率111eligibility/ineligibility合格/无被选资格112emphasis of matter物质的强调113engagement economics债务经济学114 engagement letter业务约定书115error差错116evaluating of results of audit procedures审计手序的结果评估117examinations检查118existence存在性119expectations期望差距120expected error预期的错误121experience经验122 expert专家123external audit独立审计124external review reports外部的评论报告125 fair公正126fee negotiation费谈判127final assessment of control risk控制风险的确定评定128final audit期末审计129financial statement assertions财政报告宣称130financial财务131finished goods产成品132flowcharts流程图133fraud and error舞弊134 fraud欺诈135fundamental principles基本原理136general CIS controls一般的CIS控制137 general reports to mangement对(牛犬等的)疥癣的一般报告138going concern assumption持续经营假设101 disclaimer of opinion 拒绝表示意见102 distributions 分销,分派103 documentation of understanding and assessment of control risk控制风险的协商和评定的文件编集104 documenting the audit process 证明审计程序105 due care 应有关注106 due skill and care 到期的技能和谨慎107 economy 经济108 education 教育109 effectiveness 效用,效果110 efficiency 效益,效率111 eligibility / ineligibility 合格/ 无被选资格112 emphasis of matter 物质的强调113 engagement economics 债务经济学114 engagement letter 业务约定书115 error 差错116 evaluating of results of audit procedures 审计手序的结果评估117 examinations 检查118 existence 存在性119 expectations 期望差距120 expected error 预期的错误121 experience 经验122 expert 专家123 external audit 独立审计124 external review reports 外部的评论报告125 fair 公正126 fee negotiation 费谈判127 final assessment of control risk 控制风险的确定评定128 final audit 期末审计129 financial statement assertions 财政报告宣称130 financial 财务131 finished goods 产成品132 flowcharts 流程图133 fraud and error 舞弊134 fraud 欺诈135 fundamental principles 基本原理136 general CIS controls 一般的CIS 控制137 general reports to mangement 对(牛犬等的)疥癣的一般报告138 going concern assumption 持续经营假设139 going concern 持续经营140 goods on sale or return 货物准许退货买卖141 goodwill 商誉142 governance 统治143 greenbury committee greenbury 委员会144 guidance for internal auditors 指导为内部审计员145 hampel committee hampel 委员会146 haphazard selection 随意选择147 hospitality 款待148 human resources 人力资源149 IAPS 1000 inter-bank confirmation proceduresIAPS 1000 在中间- 银行查证程序过程150 IAPS 1001 CIS environments-stand-alone microcomputersIAPS 1001 CIS 环境-单机微型计算器151 IAPS 1002 CIS environments-on-line computer systemsIAPS 1002 CIS 环境-(与主机)联机计算器系统152 IAPS 1003 CIS environments-database systemsIAPS 1003 CIS 环境- 数据库系统153 IAPS 1005 the special considerations in the audit of small entities 在小的个体审计中的IAPS 1005 特别的考虑154 IAS 2 inventories 信息家电2 库存155 IAS 10 events after the balance sheet date在平衡sheeet 日期後面的信息家电10 事件156 IFACs code of ethics for professional accountantsIFACs 道德准则为职业会计师157 income tax 所得税158 incoming auditors 收入审计(查帐)员159 independent estimate 独立的估计160 ineligible for appointment 无被选资格的为任命161 information technology 信息技术162 inherent risk 固有风险163 initial communication 签署通讯164 insurance 保险165 intangibles 无形166 integrity 完整性167 interim audit 中期审计168 internal auditing 内部审计169 internal auditors 内部审计师170 internal control evaluation questionnaires (ICEQs)内部控制评价调查表171 internal control questionnaires (ICQs)内部控制调查表172 internal control system 内部控制系统173 internal review assignment 内部的评论转让174 international audit and assurance standards board (IAASB)国际的审计和保证标准登船(IAASB)175 international auditing practice statements (IAPSs)国际的审计实务声明(IAPSs)176 international federation of accountants (IFAC)国际会计师联合会(IFAC)177 inventory system 盘存制度178 inventory valuation 存货估价179 ISA 230 documentation 文件编制180 ISA 240 fraud and error 国际砂糖协定240 欺诈和错误注会审计英语词汇表作者:- 文章来源:转载点击数:809 更新时间:2008-5-26 Auditing 审计1.Assurance engagements and external audit鉴证业务和外部审计Materiality,true and fair presentation,reasonable assurance重要性,真实、公允反映,合理保证Appointment,removal and resignation of auditors注册会计师的聘用,解聘和辞职Types of opinion:unmodified opinion,modified opinion,adverse opinion,disclaimer of opinion审计意见类型:无保留意见,保留意见,否定意见,无法表示意见Professional ethics:independence,objectivity,integrity,professional competence,due care,confidentiality,professional behavior职业道德:独立、客观和公正,专业胜任能力,应有的关注,保密性,职业行为Engagement letter审计业务约定书2.Planning and risk assessment审计计划和风险评估General principles一般原则Plan and perform audits with an attitude of professional skepticism计划和执行审计业务应保持应有的职业怀疑态度Audit risks = inherent risk ×control risk ×detection risk审计风险=固有风险×控制风险×检查风险Risk-based approach风险导向型审计Understanding the entity and knowledge of the business了解被审单位Assessing the risks of material misstatement and fraud估计重大错报或舞弊的风险Materiality (level),tolerable error重要性水平,可容忍误差Analytical procedures分析性复核程序Planning an audit制定审计计划Audit documentation:working papers审计记录:工作底稿The work of others利用其他人的工作Rely on the work of experts利用专家工作Rely on the work of internal audit利用内部审计人员的工作3.Internal control内部控制The evaluation of internal control systems内部控制系统评价Tests of control控制测试Substantive procedures (time,nature,extent)实质性程序(时间,性质,范围)Transaction cycles:revenue,purchases,inventory,etc.4.Audit evidence审计证据Obtain sufficient,appropriate audit evidence获取充分、适当的审计证据Assertions contained in the financial statements:completeness,occurrence,existence,measurement,presentation and disclosure,rights and obligations财务报表所包含的认定:完整性,发生,存在,计价,表达和披露,权利和义务The audit of specific items具体项目的审计Receivables:confirmation应收账款:函证Inventory:counting,cut-off,confirmation of inventory held by third parties存货:盘点,截止测试,对第三方持有存货进行函证Payables:supplier statement reconciliation,confirmation应付账款:供应商对帐,函证Bank and cash:bank confirmation货币资金:银行函证Auditing sampling审计抽样复核Subsequent events期后事项Going concern持续经营Management representations管理层声明Audit finalization and the final review:unadjusted differences终结审计和最后复核:未调整差异审计报告Appendix帐目名词一、资产类Assets流动资产Current assets货币资金Cash and cash equivalents现金Cash银行存款Cash in bank其他货币资金Other cash and cash equivalents外埠存款Other city Cash in bank银行本票Cashier''s cheque银行汇票Bank draft信用卡Credit card信用证保证金L/C Guarantee deposits存出投资款Refundable deposits短期投资Short-term investments股票Short-term investments - stock债券Short-term investments - corporate bonds基金Short-term investments - corporate funds其他Short-term investments - other短期投资跌价准备Short-term investments falling price reserves 应收款Account receivable应收票据Note receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable其他应收款Other notes receivable坏账准备Bad debt reserves预付账款Advance money应收补贴款Cover deficit by state subsidies of receivable库存资产Inventories物资采购Supplies purchasing原材料Raw materials包装物Wrappage低值易耗品Low-value consumption goods材料成本差异Materials cost variance自制半成品Semi-Finished goods库存商品Finished goods商品进销差价Differences between purchasing and selling price委托加工物资Work in process - outsourced委托代销商品Trust to and sell the goods on a commission basis受托代销商品Commissioned and sell the goods on a commission basis 存货跌价准备Inventory falling price reserves分期收款发出商品Collect money and send out the goods by stages待摊费用Deferred and prepaid expenses长期投资Long-term investment长期股权投资Long-term investment on stocks股票投资Investment on stocks其他股权投资Other investment on stocks长期债权投资Long-term investment on bonds债券投资Investment on bonds其他债权投资Other investment on bonds长期投资减值准备Long-term investments depreciation reserves股权投资减值准备Stock rights investment depreciation reserves债权投资减值准备Bcreditor''s rights investment depreciation reserves委托贷款Entrust loans本金Principal利息Interest减值准备Depreciation reserves固定资产Fixed assets房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement累计折旧Accumulated depreciation固定资产减值准备Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves机器设备减值准备Machinery equipment depreciation reserves工程物资Project goods and material专用材料Special-purpose material专用设备Special-purpose equipment预付大型设备款Prepayments for equipment为生产准备的工具及器具Preparative instruments and implement for fabricate 在建工程Construction-in-process安装工程Erection works在安装设备Erecting equipment-in-process技术改造工程Technical innovation project大修理工程General overhaul project在建工程减值准备Construction-in-process depreciation reserves固定资产清理Liquidation of fixed assets无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks, Trade names著作权Copyrights土地使用权Tenure商誉Goodwill无形资产减值准备Intangible Assets depreciation reserves专利权减值准备Patent rights depreciation reserves商标权减值准备trademark rights depreciation reserves未确认融资费用Unacknowledged financial charges待处理财产损溢Wait deal assets loss or income待处理财产损溢Wait deal assets loss or income待处理流动资产损溢Wait deal intangible assets loss or income待处理固定资产损溢Wait deal fixed assets loss or income2007-09-02accountant genaral 会计主任account balancde 结平的帐户account bill 帐单account books 帐account classification 帐户分类account current 往来帐account form of balance sheet 帐户式资产负债表account form of profit and loss statement 帐户式损益表account payable 应付帐款account receivable 应收帐款account of payments 支出表account of receipts 收入表account title 帐户名称,会计科目accounting year 或financial year 会计年度accounts payable ledger 应付款分类帐Accounting period(会计期间)are related to specifictime periods ,typically one year(通常是一年)资产负债表:balance sheet 可以不大写b利润表:income statements (or statements of income)利润分配表:retained earnings现金流量表:cash flows二、负债类Liability短期负债Current liability短期借款Short-term borrowing应付票据Notes payable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应付账款Account payable预收账款Deposit received代销商品款Proxy sale goods revenue应付工资Accrued wages应付福利费Accrued welfarism应付股利Dividends payable应交税金Tax payable应交增值税value added tax payable进项税额Withholdings on VAT已交税金Paying tax转出未交增值税Unpaid V AT changeover减免税款Tax deduction销项税额Substituted money on V AT出口退税Tax reimbursement for export进项税额转出Changeover withnoldings on V AT出口抵减内销产品应纳税额Export deduct domestic sales goods tax 转出多交增值税Overpaid V AT changeover未交增值税Unpaid V AT应交营业税Business tax payable应交消费税Consumption tax payable应交资源税Resources tax payable应交所得税Income tax payable应交土地增值税Increment tax on land value payable应交城市维护建设税Tax for maintaining and building citiespayable应交房产税Housing property tax payable应交土地使用税Tenure tax payable应交车船使用税V ehicle and vessel usage license platetax(VVULPT) payable应交个人所得税Personal income tax payable其他应交款Other fund in conformity with paying其他应付款Other payables预提费用Drawing expense in advance其他负债Other liabilities待转资产价值Pending changerover assets value预计负债Anticipation liabilities长期负债Long-term Liabilities长期借款Long-term loans一年内到期的长期借款Long-term loans due within one year一年后到期的长期借款Long-term loans due over one year应付债券Bonds payable债券面值Face value, Par value债券溢价Premium on bonds债券折价Discount on bonds应计利息Accrued interest长期应付款Long-term account payable应付融资租赁款Accrued financial lease outlay一年内到期的长期应付Long-term account payable due within one year 一年后到期的长期应付Long-term account payable over one year专项应付款Special payable一年内到期的专项应付Long-term special payable due within one year 一年后到期的专项应付Long-term special payable over one year递延税款Deferral taxes所有者权益类OWNERS'' EQUITY资本Capita实收资本(或股本) Paid-up capital(or stock)实收资本Paicl-up capital实收股本Paid-up stock已归还投资Investment Returned公积资本公积Capital reserve资本(或股本)溢价Cpital(or Stock) premium接受捐赠非现金资产准备Receive non-cash donate reserve股权投资准备Stock right investment reserves拨款转入Allocate sums changeover in外币资本折算差额Foreign currency capital其他资本公积Other capital reserve盈余公积Surplus reserves法定盈余公积Legal surplus任意盈余公积Free surplus reserves法定公益金Legal public welfare fund储备基金Reserve fund企业发展基金Enterprise expension fund利润归还投资Profits capitalizad on return of investment利润Profits本年利润Current year profits利润分配Profit distribution其他转入Other chengeover in提取法定盈余公积Withdrawal legal surplus提取法定公益金Withdrawal legal public welfare funds提取储备基金Withdrawal reserve fund提取企业发展基金Withdrawal reserve for business expansion提取职工奖励及福利基金Withdrawal staff and workers'' bonus andwelfare fund利润归还投资Profits capitalizad on return of investment应付优先股股利Preferred Stock dividends payable提取任意盈余公积Withdrawal other common accumulation fund应付普通股股利Common Stock dividends payable转作资本(或股本)的普通股股利Common Stock dividends change to assets(or stock)未分配利润Undistributed profit四、成本类Cost生产成本Cost of manufacture基本生产成本Base cost of manufacture辅助生产成本Auxiliary cost of manufacture制造费用Manufacturing overhead材料费Materials管理人员工资Executive Salaries奖金Wages退职金Retirement allowance补贴Bonus外保劳务费Outsourcing fee福利费Employee benefits/welfare会议费Coferemce加班餐费Special duties市内交通费Business traveling通讯费Correspondence电话费Correspondence水电取暖费Water and Steam税费Taxes and dues租赁费Rent管理费Maintenance车辆维护费V ehicles maintenance油料费Vehicles maintenance培训费Education and training接待费Entertainment图书、印刷费Books and printing运费Transpotation保险费Insurance premium支付手续费Commission杂费Sundry charges折旧费Depreciation expense机物料消耗Article of consumption劳动保护费Labor protection fees季节性停工损失Loss on seasonality cessation劳务成本Service costs2007-09-02五、损益类Profit and loss收入Income业务收入OPERA TING INCOME主营业务收入Prime operating revenue产品销售收入Sales revenue服务收入Service revenue其他业务收入Other operating revenue材料销售Sales materials代购代售包装物出租Wrappage lease出让资产使用权收入Remise right of assets revenue返还所得税Reimbursement of income tax其他收入Other revenue投资收益Investment income短期投资收益Current investment income长期投资收益Long-term investment income计提的委托贷款减值准备Withdrawal of entrust loans reserves 补贴收入Subsidize revenue国家扶持补贴收入Subsidize revenue from country其他补贴收入Other subsidize revenue营业外收入NON-OPERA TING INCOME非货币性交易收益Non-cash deal income现金溢余Cash overage处置固定资产净收益Net income on disposal of fixed assets出售无形资产收益Income on sales of intangible assets固定资产盘盈Fixed assets inventory profit罚款净收入Net amercement income支出Outlay业务支出Revenue charges主营业务成本Operating costs产品销售成本Cost of goods sold服务成本Cost of service主营业务税金及附加Tax and associate charge营业税Sales tax消费税Consumption tax城市维护建设税Tax for maintaining and building cities资源税Resources tax土地增值税Increment tax on land value5405 其他业务支出Other business expense销售其他材料成本Other cost of material sale其他劳务成本Other cost of service其他业务税金及附加费Other tax and associate charge费用Expenses营业费用Operating expenses代销手续费Consignment commission charge运杂费Transpotation保险费Insurance premium展览费Exhibition fees广告费Advertising fees管理费用Adminisstrative expenses职工工资Staff Salaries修理费Repair charge低值易耗摊销Article of consumption办公费Office allowance差旅费Travelling expense工会经费Labour union expenditure研究与开发费Research and development expense福利费Employee benefits/welfare职工教育经费Personnel education待业保险费Unemployment insurance劳动保险费Labour insurance医疗保险费Medical insurance会议费Coferemce聘请中介机构费Intermediary organs咨询费Consult fees诉讼费Legal cost业务招待费Business entertainment技术转让费Technology transfer fees矿产资源补偿费Mineral resources compensation fees排污费Pollution discharge fees房产税Housing property tax车船使用税V ehicle and vessel usage license plate tax(VVULPT) 土地使用税Tenure tax印花税Stamp tax财务费用Finance charge利息支出Interest exchange汇兑损失Foreign exchange loss各项手续费Charge for trouble各项专门借款费用Special-borrowing cost营业外支出Nonbusiness expenditure捐赠支出Donation outlay减值准备金Depreciation reserves非常损失Extraordinary loss处理固定资产净损失Net loss on disposal of fixed assets出售无形资产损失Loss on sales of intangible assets固定资产盘亏Fixed assets inventory loss债务重组损失Loss on arrangement罚款支出Amercement outlay所得税Income tax。

审计报告4种

审计报告4种常见类型及其作用在商业和金融领域,审计是一项非常重要的工作。

随着市场的发展和全球化的进程,审计的重要性也越来越凸显出来。

审计报告是审计过程中产生的一种文书,它对于公司和投资者来说具有重要的参考价值。

本文将介绍四种常见的审计报告类型并讨论它们的作用。

一、无保留意见审计报告(Unqualified Opinion)无保留意见审计报告是最理想的审计结果之一。

这种类型的审计报告表示审计师对财务报表进行了全面审计,并且未发现对财务状况、经营活动和现金流量的重大错误或虚假陈述。

这是对公司财务状况的一种积极认可,为投资者和股东提供了关于公司财务稳定性和可靠性的证明。

无保留意见审计报告的作用是确认财务报表的真实性和可靠性,有助于提高投资者和债权人对公司的信心。

它还能够增加公司的声誉和竞争力,为公司争取更好的融资条件。

二、保留意见审计报告(Qualified Opinion)保留意见审计报告是在审计过程中发现了一些限制或不足,但这些问题不是严重到使财务报表整体失真或不能可靠地表示公司的财务状况。

审计师在这种情况下会使用一种保留意见表达对财务报表的保留观点。

保留意见审计报告的作用是提醒读者注意报表中存在的问题和风险。

这种审计报告为投资者提供了有关公司财务可行性和可持续性的一些警示信号。

投资者需要更加仔细地分析和评估这些风险,以便作出正确的投资决策。

三、无法表示意见审计报告(Adverse Opinion)无法表示意见审计报告是最严重的审计结果之一。

这种情况发生在审计师确定财务报表中存在重大错误、虚假陈述或不合规的情况下。

审计师无法确认财务报表的可靠性,因此无法给出肯定的意见。

无法表示意见审计报告对公司的影响非常严重。

它可能导致投资者和债权人对公司产生质疑,并可能引起公司声誉和信任的损害。

此外,这种审计报告经常会导致相应的法律诉讼和调查。

四、无保留但有关注项审计报告(Disclaimer of Opinion)无保留但有关注项审计报告发生在审计师由于某种原因无法获得足够的审计证据,从而无法对财务报表的全部内容表达意见。

审计、财务常用英文词汇

审计类财会英语审计、财务常用英文词汇审计报告: Audit report资产负债表:Balance Sheet损益表:Income statement利润分配表:Profit distribution statement<中国注册会计师独立审计准则>:the Independent Auditing Standard for Chinese Certified Public Accountants会计报表:Financial statement在抽查的基础上:on a test basis主任会计师或授权副主任会计师:Chief Accountant or Authorized Assistant Chief Accountant中国注册会计师:Chinese Certified Public Accountant无钢印无效:shall not be valid without bearing the embossing seal年初数,年末数:Opening amounting\ closing amounting资产负债表:Balance sheet流动资产:Current assets货币资金:Cash短期、长期投资:Short-term、long-term investment应收票据:Notes receivable应收账款:Account receivable坏账准备:Less: provision for bad debt应收账款净额:Net value of account receivable预付账款:Advance to supplier应收出口退税:Receivable drawback for export应收补贴款: Receivable subsidy其他应收款:Other receivable存货:Inventories待转其他业务支出:Other business expense to be transferred 待摊费用:Prepaid expense待处理流动资产净损失:Net loss of current assets to be settled 一年内到期的长期债券投资:Long-term bonds investment due in 1 year其他流动资产:Other current assets流动资产合计:Total current assets固定资产:fixed assets固定资产原价:Original value of fixed assets累计折旧:accumulated depreciation固定资产净值:Net value of fixed assets固定资产清理:Disposal of fixed assets在建工程:Construction in process待处理固定资产净损失:Net loss of fixed assets to be settled固定资产合计:Total fixed assets无形资产及递延资产:Intangible assets & deferred assets递延税项目:Deferred tax负债及所有者权益:Liabilities & owner’s equity流动负债:current liabilities短期/长期借款:Short-term/long-term loan应付票据:Notes payable预收账款:Advance from clients其他应付款:Other payable应付工资:Accrued payroll应付福利费:Welfare payable应交税金/应付利润:Tax/ Profits payable其他应交款:Unpaid others预提费用:Accrued expense一年内到期的长期负债:Long-term liabilities due in 1 year应付债券:Bonds payable长期应付款:Long-term payable实收资本:Paid-in capital资本公积:Capital accumulation盈余公积:Surplus accumulation其中:公益金:Including; commonweal funds本年利润:Profits of current year未分配利润:Undistributed profits损益表/利润表:Income statement产品(商品)销售收入:Revenue of sales of products (commodities)出口产品销售收入:sales income of export products销售折扣与折让:Discount& transfer of sales产品销售净额;Net value of sales of products产品销售税金/成本:sales tax/cost of products出口产品销售成本:Sales cost of export products销售费用(经营费用):Sales expense (operation expense)产品销售利润:Sales profits of products加:其他业务利润:Add: other business profits营业/管理/财务费用;operation/overhead / finance expense利息支出(减利息收入):Interest expense (Less: interest income)汇兑损失(减汇兑收益):Exchange loss(exchange income)营业利润:Operation profits投资收益;Return on investment主营业务收入:Revenue of main business主营业务成本:cost of main business主营业务税金及附加:Tax & surtax of main business营业外收入/支出:Non-operation income /expense投资收益:return on business补贴收入:subsidy income以前年度损益调整:Adjustment for profits & loss of previous year所得税:income tax利润分配表:Profits Distribution Statement法定盈余公积:legal surplus accumulation法定公益金:Legal commonweal funds年初/末未分配利润: Undistributed profits of opening / closing year已弥补亏损:Loss being made up可供所有者分配的利润:Profits distributable to owner已分配股利:Distributed dividends其他转入:other transferred in提取法定公益金:Retained legal commonweal funds提取职工奖励及福利基金:Retained employee’s bonus & welfare funds提取储备基金:retained reversed funds提取企业发展基金:retained enterprise development funds利润归还投资:Retained profits into investor应付优先股/普通股股利:Dividends payable to preference / common stock提取任意盈余基金:Retained random surplus accumulation转作资本的普通股股利:Dividends of common stock transferred into capitall 附注:annotation to *《企业法人营业执照》:Business License for Legal Person经营期限:operation period投产:begin to produce采用的会计政策:Accounting policies implemented《企业会计准则》:Accounting Standard for Enterprises《工业企业会计制度》:Accounting System for Industrial Enterprise会计期间:Fiscal year记账原则和计价基础:Accounting principle and valuation basis 会计核算;Accounting records以权责发生制为原则;base on accrual-basis principle以历史成本为计价基础:be valued at one’s historical cost坏账:bad debt直接转销法:direct amortized method存货核算方法:Accounting method of inventories存货的够入与入库:inventories at purchasing and inventories to warehouse使用年限:service life固定资产折旧:Depreciation of fixed assets采用直线法平均计算:Be calculated using average service life method预计使用年限:anticipated service life预计净残值:anticipated net residual value使用年限:actual useful life专用生产设备:production machinery equipment收入实现条件:Recognition of revenue订单法:order method增值税:value added tax (VAT)现金:cash on hand银行存款:Bank deposit账龄:account-age期末余额:closing balance产成品:finished products实收资本: Paid-in capital本年实际:Actual amount of current year办公费; office expenses差旅费:traveling expenses电话费: telephone charge水电费:water and electricity charge金融机构手续费:Handling change of finance authority出资额:investment amount档案查询专用章:Special Seal for Archive Inquiry工商行政管理局:Administration for Industry and Commerce套印无效:Overprint shall be ineffective主管:authoritative organ原审批单位:the original examine and approve authority会计报表审计 Auditing Financial statements资本验证 Capital verification企业财务会计制度设计Setting up financial systems for enterprises exchange business代理记帐 Bookkeeping services外汇年检专项审计 Special audit and annual auditing of foreign exchange business企业合并、分立、清算审计Auditing transactions such as enterprises’ merger、split and liquidation投资可行性研究 Feasibility analysis for investment project百阳英语学院整理。

四大,IB和consulting是什么意思

四大,IB和consulting是什么意思四大,IB和consulting是什么意思四大就是国际四大会计师事务所,按照全球收入排名分别是PwC, Deloitte, EY和KPMGIB是投资银行Investment banking的简称,知名的投行如高盛和摩根斯丹利consulting指的是管理咨询公司,最富盛名的为Mckinsey,BCG 和Bainconsulting是什么意思consulting咨询双语对照词典结果:consulting[英][kən'sʌltɪŋ][美][kən'sʌltɪŋ]adj.商议的,顾问资格的,咨询的;v.商议,商量( consult的现在分词 ); 请教; 翻阅; 求教于;以上结果来自金山词霸例句:1.The most intense petition beeen consulting firms is for "whale" engagements.从事企业咨询的公司之间存在的最大竞争性因素是他们是否可以“全心全意”的投入工作。

咨询adj.商议的,顾问资格的,咨询的;v.商议,商量( consult的现在分词 ); 请教; 翻阅; 求教于; consulting firm是什么意思consulting firm咨询公司双语例句1An actuary at a consulting firm, Vicky needs to close a project tonight.Vicky是一家咨询公司的精算员,要在今晚把一个项目结束了。

2Architectural consulting firm little in Charlotte often gets hundreds of aspirantsfor entry-level positions.建筑咨询公司Little in Charlotte的初级岗位通常会有数百名追求者。

求一些会计常用指标的英文缩写

求一些会计常用指标的英文缩写求一些会计常用指标的英文缩写Process KPIs...Learning KPIs...Asset Utilization RatesAssets ($)Assets / employee ($)Budget VarianceBudget Variance: Cost versus BudgetBusiness MixCash FlowCash Flow per ShareCatastrophic LossesChannel Mix % (High cost manual channels vs low cost electronic channels)Combined RatioCommunity InvolvementCommunity Quality Statements (lists of examples on many fronts)Contribution to Overhead and ProfitCorporate CitizenshipCostCost RatiosCost Ratios: Administrative Cost per Customer, per Sale, per Transaction, per New Product, etc.Cost Ratios: Administrative Spending as % of SalesCost Ratios: per gallon, per pound, per transaction, per claim paid, per premium processedCost Reduction RatesCost versus Competitors'Cross SellingDays Cost of Sales in InventoryDeposit Service Cost (Change)Deposit Service Cost (per $ of Deposits)Earnings GrowthEarnings per ShareEnvironmental Concern: # of Pollution Emissions Violations Environmental Index: (key emissions levels, amount of hazardous waste hauled off, recycling rates)Environmental ResultsEnvironmental: % Chemical in the AirGross MarginGross Profit (vs potential)Gross Sales (vs petition)Indirect Expenses (% of sales)Investment (% of sales)求一些财务管理常用指标的英文缩写财务指标英文对照AAA 美国会计学会Abacus 《算盘》杂志abacus 算盘Abandonment 废弃,报废;委付abandonment value 废弃价值abatement ①减免②冲销ability to service debt 偿债能力abnormal cost 异常成本abnormal spoilage 异常损耗above par 超过票面价值above the line 线上项目absolute amount 绝对数,绝对金额absolute endorsement 绝对背书absolute insolvency 绝对无力偿付absolute priority 绝对优先求偿权absolute value 绝对值absorb 摊配,转并absorption aount 摊配账户,转并账户absorption costing 摊配成本计算法abstract 摘要表abuse 滥用职权abuse of tax shelter 滥用避税项目ACCA 特许公认会计师公会aelerated cost recovery system 加速成本收回制度aelerated depreciation method 加速折旧法,快速折旧法aeleration clause 加速偿付条款,提前偿付条款aeptance ①承兑②已承兑票据③验收aeptance bill 承兑票据aeptance register 承兑票据登记簿aeptance sampling 验收抽样aess time 存取时间acmodation 融通acmodation bill 融通票据acmodation endorsement 融通背书aount ①账户,会计科目②账簿,报表③账目,账项④记账aountability 经营责任,会计责任aountability unit 责任单位Aountancy 《会计》杂志aountancy 会计aountant 会计员,会计师aountant general 会计主任,总会计aounting in charge 主管会计师aountant,s legal liability 会计师的法律责任aountant,s report 会计师报告aountant,s responsibility 会计师职责aount form 账户式,账式aounting ①会计②会计学aounting assumption 会计假定,会计假设aounting basis 会计基准,会计基本方法aounting changes 会计变更aounting concept 会计概念aounting control 会计控制aounting convention 会计常规,会计惯例aounting corporation 会计公司aounting cycle 会计循环aounting data 会计数据aounting doctrine 会计信条aounting document 会计凭证aounting elements 会计要素aounting entity 会计主体,会计个体aounting entry 会计分录aounting equation 会计等式aounting event 会计事项aounting exposure 会计暴露,会计暴露风险aounting firm 会计事务所Aounting Hall of Fame 会计名人堂aounting harmonization 会计协调化aounting identity 会计恒等式aounting ine 会计收益aounting information 会计信息aounting information system 会计信息系统aounting internationalization 会计国际化aounting journals 会计杂志aounting legislation 会计法规aounting manual 会计手册aounting objective 会计目标aounting period 会计期aounting policies 会计政策aounting postulate 会计假设aounting practice 会计实务aounting principle 会计原则Aounting Principle Board 会计原则委员会aounting procedures 会计程序aounting profession 会计职业,会计专业aounting rate of return 会计收益率aounting records 会计记录,会计簿籍Aounting Review 《会计评论》aounting rules 会计规则Aounting Series Release 《会计公告文件》aounting service 会计服务aounting sofare 会计软件aounting standard 会计标准,会计准则aounting standardization 会计标准化Aounting Standards Board 会计准则委员会(英) Aounting Standards Committee 会计准则委员会(英) aounting system ①会计制度②会计系统aounting technique 会计技术aounting theory 会计理论aounting transaction 会计业务,会计账务Aounting Trend and Techniques 《会计趋势和会计技术》aounting unit 会计单位aounting valuation 会计计价aounting year 会计年度aounts 会计账簿,会计报表aount sales 承销清单,承销报告单aounts payable 应付账款aounts receivable 应收账款aounts receivable aging schedule 应收账款账龄分析表aounts receivable assigned 已转让应收账款aounts receivable collection period 应收账款收款期aounts receivable discounted 已贴现应收账款aounts receivable financing 应收账款筹资,应收账款融资aounts receivable management 应收账款管理aounts receivable turnover 应收账款周转率,应收账款周转次数aretion 增殖arual basis aounting 应计制会计,权责发生制会计arued asset 应计资产arued expense 应计费用arued liability 应计负债arued revenue 应计收入aumulated depreciation 累计折旧aumulated dividend 累计股利aumulated earnings tax 累积盈余税,累积收益税aumulation 累积,累计acid test ratio 酸性试验比率acquired pany 被盘购公司,被兼并公司acquisition 购置,盘购acquisition aounting 盘购会计acquisition cost 购置成本acquisition decision 购置决策acquisition excess 盘购超支acquisition surplus 盘购盈余across-the-board 全面调整ACT 预交公司税act 法案,法规action 起诉,诉讼active aount 活动账户active assets 活动资产activity 业务活动,作业activity aount 作业账户activity aounting 作业会计activity ratio 业务活动比率activity variance 业务活动量差异act of bankruptcy 破产法act of pany 公司法act of God 天灾,不可抗力actual capital 实际资本actual value 实际价值actual wage 实际工资added value 增值added value statement 增值表added value tax 增值税addition 增置,扩建additional depreciation 附加折旧,补提折旧additional paid-in capital 附加实缴资本additional tax 附加税adequate disclosure 充分披露adjunct aount 附加账户adjustable-rate bond 可调整利率债券adjusted gross ine 调整后收益总额,调整后所得总额adjusted trial balance 调整后试算表adjusting entry 调整分录adjustment 调整adjustment aount 调整账户adjustment bond 调整债券administrative aounting 行政管理会计administrative budget 行政管理预算administrative expense 行政管理费用ADR 资产折旧年限幅度ad valorem tax 从价税advance 预付款,垫付款advance corporation tax 预交公司税advances from customers 预收客户款advance to suppliers 预付货款adventure 投机经营,短期经营adverse opinion 反面意见,否定意见adverse variance 不利差异,逆差advisory services 咨询服务affiliated pany 联营公司affiliation 联营after closing trial balance 结账后试算表after cost 售后成本after date 出票后兑付after sight 见票后兑付after-tax 税后AGA *** 会计师联合会age 寿命,账龄,资产使用年限age allowance 年龄减免age *** ysis 账龄分析agency 代理,代理关系agency mission 代理佣金agency fund 代管基金agenda 议事日程,备忘录agent 代理商,代理人aggregate balance sheet 合并资产负债表aggregate ine statement 合并损益表AGI 调整后收益总额,调整后所得总额aging of aounts receivable 应收账款账龄分析aging schedule 账龄表agio 贴水,折价agiotage 汇兑业务,兑换业务AGM 年度股东大会agreement 协议agreement of partnership 合伙协议AICPA 美国注册公共会计师协会AIS 会计信息系统all capital earnings rate 资本总额收益率all-inclusive ine concept 总括收益概念allocation 分摊,分配allocation criteria 分配标准allotment ①分配,拨付②分配数,拨付数allowance ①备抵②折让③津贴allowance for bad debts 呆账备抵allowance for depreciation 折旧备抵账户allowance method 备抵法all-purpose financial statement 通用财务报表,通用会计报表alpha risk 阿尔法风险,第一种审计风险altered check 涂改支票alternative aounting methods 可选择性会计方法alternative proposals 替代方案,备选方案amalgamation 企业合并American Aounting Association 美国会计学会American depository receipts 美国银行证券存单,美国银行证券托存收据American Institute of Certified Public Aountants 美国注册会计师协会,美国注册公共会计师协会American option 美式期权American Stock Exchange 美国股票交易所amortization ①摊销②摊还amortized cost 摊余成本amount 金额,合计amount differ 金额不符amount due 到期金额amount of 1 dollar 1元的本利和*** ysis 分析*** yst 分析师*** ytical review 分析性检查annual audit 年度审计annual closing 年度结账annual general meeting 年度股东大会annualize 按年折算annualized present value 折算年度净现值annual report 年度报告annuity 年金annuity due 期初年金annuity in advance 预付年金annuity in arrears 迟付年金annuity method of depreciation 年金折旧法antedate 填早日期anticipation 预计,预列anti-dilution clause 防止稀释条款anti-pollution investment 消除污染投资anti-profiteering tax 反暴利税anti-tax avoidance 反避税anti-trust legislation 反拖拉斯立法A/P 应付账款APB 会计原则委员会APB Opinion 《会计原则委员会意见书》Application 申请,申请书applied overhead 已分配间接费用appraisal 估价appraisal capital 评估资本appraisal surplus 估价盈余appraiser 估价员,估价师appreciation 增值appropriated retained earnings 已拨定留存收益,已指定用途留存收益appropriation 拨款,指拨经费appropriation aount ①拨款账户②留存收益分配账户appropriation budget 拨款预算approval 核定,审批approved aount 核定账户approved bond 核定债券A/R 应收账款arbitrage 套利,套汇arbitrage transaction 套利业务,套汇业务arbitration 仲裁,公断arithmetical error 算术误差arm,s-length price 正常价格,公正价格arm,s-length transaction 一臂之隔交易,正常交易ARR 会计收益率arrears ①拖欠,欠款②迟付arrestment 财产扣押Authur Anderson & Co. 约瑟?安德森会计师事务所,安达信会计师事务所article 文件条文,合同条款articles of incorporation 公司章程articles of partnership 合伙契约articulate 环接articulated concept 环接观念artificial intelligence 人工智能ASB 审计准则委员会ASE 美国股票交易所Asian Development Bank 亚洲开发银行Asian dollar 亚洲美元asking price 索价,卖方报价assessed value 估定价值asses *** ent ①估定,查定②特别税捐,特别摊派税捐asset 资产asset cover 资产担保,资产保证asset depreciation range 资产折旧年限幅度asset-liability view 资产—负债观念asset quality 资产质量asset retirement 资产退役,资产报废asset revaluation 资产重估价asset stripping 资产剥离,资产拆卖asset structure 资产结构asset turnover 资产周转率asset valuation 资产计价assignment of aounts receivable 应收账款转让associated pany 联属公司,附属公司Association of Government Aounting *** 会计师协会assumed liability 承担债务,承付债务AT 税后at cost 按成本at par 按票面额,平价at sight 见票兑付,即期兑付attached aount 被查封账户attachment 扣押,查封attest 证明,验证attestation 证明书,鉴定书audit 审核,审计auditability 可审核性audit mittee 审计委员会audit coverage 审计范围audited financial statement 审定财务报表,审定会计报表audit evidence 审计证据,审计凭证Audit Guides 《审计指南》auditing ①审计②审计学auditing procedure 审计程序auditing process 审计过程auditing standard 审计标准,审计准则Auditing Standards Board 审计准则委员会Auditor 审计员,审计师auditor general 审计主任,总审计auditor,s legal liability 审计师法律责任auditor,s opinion 审计师意见书auditor,s report 审计师报告,查账报告财务指标英文对照AAA 美国会计学会Abacus 《算盘》杂志abacus 算盘 Abandonment 废弃,报废;委付 abandonment value 废弃价值abatement ①减免②冲销ability to service debt 偿债能力abnormal cost 异常成本 abnormal spoilage 异常损耗 above par 超过票面价值 above the line 线上项目 absolute amount 绝对数,绝对金额 absolute endorsement 绝对背书 absolute insolvency 绝对无力偿付absolute priority 绝对优先求偿权absolute value 绝对值absorb 摊配,转并 absorption aount 摊配账户,转并账户 absorption costing 摊配成本计算法 abstract 摘要表 abuse 滥用职权 abuse of tax shelter 滥用避税项目 ACCA 特许公认会计师公会 aelerated cost recovery system 加速成本收回制度aelerated depreciation method 加速折旧法,快速折旧法aeleration clause 加速偿付条款,提前偿付条款aeptance ①承兑②已承兑票据③验收 aeptance bill 承兑票据 aeptance register 承兑票据登记簿 aeptance sampling 验收抽样 aess time 存取时间 acmodation 融通 acmodation bill 融通票据acmodation endorsement 融通背书aount ①账户,会计科目②账簿,报表③账目,账项④记账 aountability 经营责任,会计责任 aountability unit 责任单位 Aountancy 《会计》杂志 aountancy 会计 aountant 会计员,会计师aountant general 会计主任,总会计aounting in charge 主管会计师aountant,s legal liability 会计师的法律责任aountant,s report 会计师报告 aountant,s responsibility 会计师职责aount form 账户式,账式aounting ①会计②会计学aounting assumption 会计假定,会计假设 aounting basis 会计基准,会计基本方法aounting changes 会计变更aounting concept 会计概念aounting control 会计控制aounting convention 会计常规,会计惯例aounting corporation 会计公司aounting cycle 会计循环aounting data 会计数据aounting doctrine 会计信条aounting document 会计凭证 aounting elements 会计要素 aounting entity 会计主体,会计个体 aounting entry 会计分录 aounting equation 会计等式 aounting event 会计事项 aounting exposure 会计暴露,会计暴露风险 aounting firm 会计事务所 Aounting Hall of Fame 会计名人堂 aounting harmonization 会计协调化 aounting identity 会计恒等式aounting ine 会计收益aounting information 会计信息aounting information s性趣指标的英文缩写你好!性趣指标Sexual interest indicators运算速度性能指标的英文缩写是MIPS?嗯。

标准的审计报告的类型包括

标准的审计报告的类型包括标准的审计报告主要包括以下几种类型:1. 无保留意见报告(Unqualified Opinion Report):这是最常见的审计报告类型,表示审计师认为财务报表按照相关会计准则进行编制,并且能够真实和公平地反映被审计实体财务状况、经营成果和现金流量。

2. 保留意见报告(Qualified Opinion Report):这种类型的审计报告表示审计师在财务报表的特定方面有保留意见,可能是由于被审计实体的财务记录不完整或信用评估受限。

然而,核心财务报表的大部分内容是准确和真实的。

3. 不无保留意见报告(Adverse Opinion Report):这是一种较为严重的审计报告类型,意味着审计师认为财务报表存在重大的错误、偏差或欺诈,使其无法真实和公平地反映被审计实体的财务状况、经营成果和现金流量。

4. 假设条件修改报告(Disclaimer of Opinion Report):这种类型的审计报告发生在审计师无法获得足够的审计证据的情况下,通常是由于被审计实体的财务记录不完整或可靠的证据不可获得。

因此,审计师无法对财务报表表达任何意见。

除了上述主要类型的审计报告外,还有其他特殊类型的审计报告,如:- 审计师附加报告:对于特定财务报表项目或事项,审计师可以提供附加报告,提供有关特定问题的说明和意见。

- 强调事项报告:审计师可以在审计报告中强调重要问题,如财务报告中存在的重要不确定性。

- 修正意见报告:当审计师在发出审计报告后发现错误时,可以发出修正意见报告,对先前发表的意见进行修正。

总之,审计报告的类型主要根据审计师对财务报表真实性和准确性的判断而定,从无保留意见到保留意见、不无保留意见和假设条件修改,反映了不同程度的审计问题和不确定性。

审核常用的英文缩写

审核常用的英文缩写1. ASAP:As Soon As Possible,意为“尽快”。

当我们在审核过程中需要加快进度时,可以使用这个缩写来提醒相关人员。

2. EOD:End Of Day,意为“当天结束”。

在审核截止日期临近时,我们可以使用这个缩写来提醒团队成员在当天完成审核工作。

3. KIV:Keep In View,意为“保留意见”。

当我们在审核过程中遇到一些需要进一步讨论或核实的问题时,可以使用这个缩写来表示暂时保留意见。

4. N/A:Not Applicable,意为“不适用”。

在填写审核表格或报告时,如果某个问题不适用于当前情况,可以使用这个缩写来表示。

5. RFI:Request For Information,意为“请求提供信息”。

在审核过程中,如果需要其他部门或同事提供相关资料,可以使用这个缩写来提出请求。

6. TBD:To Be Determined,意为“待定”。

在审核过程中,如果某个问题尚未确定,可以使用这个缩写来表示。

7. WFH:Work From Home,意为“在家办公”。

在疫情期间,很多公司采用了远程办公模式,我们可以使用这个缩写来表示员工在家办公。

9. WIP:Work In Progress,意为“进行中”。

在审核过程中,如果某个任务正在进行中,可以使用这个缩写来表示。

10. TBC:To Be Confirmed,意为“待确认”。

在审核过程中,如果某个问题需要进一步确认,可以使用这个缩写来表示。

掌握这些常见的英文缩写,有助于我们在审核过程中更加高效地沟通和协作。

同时,我们也要注意在合适的场合使用这些缩写,避免产生误解。

审核常用的英文缩写1. QA:Quality Assurance,意为“质量保证”。

在审核过程中,我们注重确保工作质量和符合标准,使用这个缩写来强调质量的重要性。

2. SOP:Standard Operating Procedure,意为“标准操作程序”。

审计英文词汇整理

审计英文词汇整理第一篇:审计英文词汇整理1.audit审计2.attestation鉴证3.credibility可信赖程度4.audit of financial statements 财务报表审计5.agreed-upon procedures 执行商定程序6.high levels of assurance 高水平保证pilation 编制8.reliability 可靠性9.relevance 相关性10.professional skepticism 职业谨慎11.objectivity 客观性12.professional competence 专业胜任能力13.Senior/CPA-in-charge 项目经理14.audit engagement letter 业务约定书15.recurring audit 连续审计16.the client 委托人17.change CPA 更换注册会计师18.the existing CPA 现任注册会计师19.the successor CPA 后任注册会计师20.the preceding CPA 前任注册会计师21.issue the audit report 出具审计报告22.expert 专家23.the board of directors 董事会24.knowledge of the entity‘ s business 了解被审计单位情况25.assess material misstatement risks评估重大错报风险26.detemine the nature,timing and extent of the audit procedures 确定审计程序的性质、时间和范围27.a general knowledge of初步了解―――的情况28.a more knowledge of 进一步了解的情况29.the prior year‘s working papers 以前年度工作底稿30.minutes of meeting 会议纪要31.business risks 经营风险32.appropriateness 适当性33.accounting estimate 会计估计34.management representations 管理层声明35.goingconcern assumption 持续经营假设36.audit plan 审计计划37.significant audit areas 重点审计领域38.error 错误39.fraud舞弊40.modified or additional procedures 修改或追加审计程序41.misappropriation of assets 侵占资产42.transactions without substance 虚假交易43.unusual pressures 异常压力44.the suspected noncompliance 涉嫌存在违法行为45.materialiy 重要性46.exceed the materiality level 超过重要性水平47.approach the materiality level 接近重要性水平48.an acceptably low level 可接受水平49.the overall financial statement level and in related account balances and transaction levels 财务报表层和相关账户、交易层50.misstatements or omissions 错报或漏报51.aggregate 总计52.subsequent events 期后事项53.adjust the financial statements 调整财务报表54.perform additional audit procedures 实施追加的审计程序55.audit risk 审计风险56.detection risk 检查风险57.inappropriate audit opinion 不适当的审计意见58.material misstatement 重大的错报59.tolerable misstatement 可容忍错报60.the acceptable level of detection risk 可接受的检查风险61.assessed level of material misstatement risk 重大错报风险的评估水平62.simall business 小规模企业63.accounting system 会计系统64.test of control 控制测试65.walk-through test 穿行测试munication沟通67.flowchart 流程图68.reperformance of internal control 重新执行69.auditevidence 审计证据70.substantive procedures 实质性程序71.assertions认定72.esistence存在73.occurrence发生pleteness完整性75.rightsand obligations 权利和义务76.valuationand allocation 计价和分摊77.cutoff截止78.accuracy准确性79.classification分类80.inspection检查81.supervision of counting 监盘82.observation观察83.confirmation函证putation计算85.analytical procedures 分析程序86.vouch核对87.trace追查88.audit sampling 审计抽样89.error误差90.expected error 预期误差91.population总体92.sampling risk 抽样风险93.non-sampling risk 非抽样风险94.sampling unit 抽样单位95.statistical sampling 统计抽样96.tolerable error 可容忍误差97.therisk of under reliance 信赖不足风险98.therisk of over reliance 信赖过度风险99.therisk of incorrect rejection 误拒风险100.the risk of incorrect acceptance 误受风险101.working trial balance 试算平衡表102.indexand cross-referencing 索引和交叉索引103.cashreceipt 现金收入104.cash disbursement 现金支出105.bank statement 银行对账单106.bank reconciliation 银行存款余额调节表107.balance sheet date 资产负债表日realizable value 可变现净值109.store room仓库110.sale invoice 销售发票111.price list 价目表112.positive confirmation request 积极式询证函113.negative confirmation request 消极式询证函114.purchase requisition 请购单115.receiving report 验收报告116.gross margin 毛利117.manufacturing overhead 制造费用118.material requisition 领料单119.inventory-taking存货盘点120.bond certificate 债券121.stock certificate 股票122.audit report 审计报告123.entity被审计单位124.addressee of the audit report 审计报告的收件人125.unqualified opinion 无保留意见126.qualified opinion 保留意见127.disclaimer of opinion 无法表示意见128.adverse opinion 否定意见审计词汇审计法 Audit Law, Audit Act审计法实施条例 the Implementary Rules of the Audit law 审计标准 audit criteria,audit standard 审计准则 auditing standard 审计原则 auditing principles 审计手册audit manual公认审计准则 Generally Accepted Auditing Standards审计法律规范audit laws and regulations 审计体制audit system审计权限 audit purview; audit jurisdiction;audit mandate 审计职责 audit responsibility审计监督 audit supervision; supervision through auditing 审计管辖权 audit jurisdiction审计执法 implementation of audit laws and regulations审计处理 audit sanction 审计处罚 audit penalty依法审计 conduct auditing in accordance with laws 审计意见audit opinion审计决定 audit decision审计建议audit suggestion, audit recommendation 复核意见conclusion of audit review 审计复议 audit appeal 审计听证 audit hearing 审计复核audit review 审计战略audit strategy 审计计划audit plan审计方案auditing program审计目标auditing objective 审计范围audit scope 审计内容audit coverage 审计结论audit conclusion 审计任务audit assignments 审计结果 audit finding 审计报告 audit report 审计方法audit method 审计过程auditing process 审计证据audit evidence 审计测试 audit test 审计风险 audit risk审计抽样 audit sampling审计软件 audit software审计程序 auditing procedures 审计调查 audit investigation 审计小组 audit team审计线索 audit trail 工作底稿 working paper绕过计算机审计auditing around the computer 通过计算机审计auditing through the computer 计算机辅助审计computer-assited audit 信息技术审计 IT audit合法性审计compliance audit, regularity audit 合规性审计compliance audit 综合审计 comprehensive audit效益审计value for money audit(VFM audit)绩效审计performance audit财务审计 financial audit财务报表审计 financial statement audit 财务收支审计 audit of financial revenues and expenditures决算审计 final account audit经济责任审计 accountability audit任中经济责任审计 middle term accountability audit 离任经济责任审计term-end accountability audit 管理审计management audit 项目审计project audit 外部审计external audit 内部审计internal audit 政府审计 government audit 联合审计 joint audit 实地审计 field audit 期末审计 final audit 期中审计 interim audit定期审计periodic audit初次审计 initial audit初步审计 preliminary audit 事后审计 post-audit 事前审计 pre-audit 事中审计concurrent audit 专项审计special audit 法定审计statutory audit 后续审计 successive audit 跟踪审计 follow up audit 全过程审计 whole process auditing 突击审计 surprise audit 审计报告 audit report 标准报告 standard report长式报告 long-form report 短式报告 short-form report审计工作报告 audit working report审计结果公告Announcement of Audit Findings审计长Auditor General副审计长 Deputy Auditor General 审计主任 chief auditor 资深审计师 senior auditor审计师(员)auditor注册内部审计师 certified internal auditor(CIA)注册信息系统审计师 certified information systems auditor(CISA)注册公共会计师certified public accountant(CPA)特许会计师 chartered accountant(CA)审计经费 audit funds审计业务费audit operating expense 审计专项经费special funds for auditing 无保留意见:unqualified opinion 保留意见qualified opinion 无法表示意见: disclaimer of opinion 否定意见:adverse opinion第二篇:审计常用英文词汇审计常用英文词汇1.Assurance engagements and external audit鉴证业务和外部审计Materiality,true and fair presentation,reasonable assurance重要性,真实、公允反映,合理保证Appointment,removal and resignation of auditors注册会计师的聘用,解聘和辞职Types of opinion: unmodified opinion,modified opinion,adverse opinion,disclaimer of opinion审计意见类型:无保留意见,保留意见,否定意见,无法表示意见Professional ethics: independence,objectivity,integrity,professional competence,due care,confidentiality,professional behavior职业道德:独立、客观和公正,专业胜任能力,应有的关注,保密性,职业行为Engagement letter审计业务约定书2.Planning and risk assessment审计计划和风险评估General principles一般原则Plan and perform audits with an attitude of professional skepticism计划和执行审计业务应保持应有的职业怀疑态度Audit risks = inherent risk ×control risk ×detec tion risk审计风险=固有风险×控制风险×检查风险Risk-based approach风险导向型审计Understanding the entity and knowledge of the business了解被审单位Assessing the risks of material misstatement and fraud估计重大错报或舞弊的风险Materiality(level),tolerable error重要性水平,可容忍误差Analytical procedures分析性复核程序Planning an audit制定审计计划Audit documentation: working papers审计记录:工作底稿The work of others利用其他人的工作Rely on the work of experts利用专家工作Rely on the work of internal audit利用内部审计人员的工作3.Internal control内部控制The evaluation of internal control systems内部控制系统评价T ests of control控制测试Substantive procedures(time,nature,extent)实质性程序(时间,性质,范围)Transaction cycles:revenue,purchases,inventory,etc.4.Audit evidence审计证据Obtain sufficient,appropriate audit evidence获取充分、适当的审计证据Assertions contained in the financial statements:completeness,occurrence,existence,measurement,presentation and disclosure,rights and obligations财务报表所包含的认定:完整性,发生,存在,计价,表达和披露,权利和义务The audit of specific items具体项目的审计Receivables: confirmation应收账款:函证Inventory:counting,cut-off,confirmation of inventory held by third parties存货:盘点,截止测试,对第三方持有存货进行函证Payables:supplier statement reconciliation,confirmation应付账款:供应商对账,函证Bank and cash: bank confirmation货币资金:银行函证Auditing sampling审计抽样5.Review复核Subsequent events期后事项Going concern持续经营Management representations管理层声明Audit finalization and the final review:unadjusted differences终结审计和最后复核:未调整差异第三篇:审计英文词汇1.audit审计2.attestation鉴证3.credibility可信赖程度4.audit of financial statements 财务报表审计5.agreed-upon procedures 执行商定程序6.high levels of assurance 高水平保证pilation 编制8.reliability 可靠性9.relevance 相关性10.professional skepticism 职业谨慎11.objectivity 客观性12.professional competence 专业胜任能力13.Senior/CPA-in-charge 项目经理14.audit engagement letter 业务约定书15.recurring audit 连续审计16.the client 委托人17.change CPA 更换注册会计师18.the existing CPA 现任注册会计师19.the successor CPA 后任注册会计师20.the preceding CPA 前任注册会计师21.issue the audit report 出具审计报告22.expert 专家23.the board of directors 董事会24.knowledge of the entity‘ s business 了解被审计单位情况25.assess material misstatement risks评估重大错报风险26.detemine the nature,timing and extent of the audit procedures 确定审计程序的性质、时间和范围27.a general knowledge of初步了解―――的情况28.a more knowledge of 进一步了解的情况29.the prior year‘s working papers 以前工作底稿30.minutes of meeting 会议纪要31.business risks 经营风险32.appropriateness 适当性33.accounting estimate 会计估计34.management representations 管理层声明35.going concern assumption 持续经营假设36.audit plan 审计计划37.significant audit areas 重点审计领域38.error 错误39.fraud 舞弊40.modified or additional procedures 修改或追加审计程序41.misappropriation of assets 侵占资产42.transactions without substance 虚假交易43.unusual pressures 异常压力44.the suspected noncompliance 涉嫌存在违法行为45.materialiy 重要性46.exceed the materiality level 超过重要性水平47.approach the materiality level 接近重要性水平48.an acceptably low level 可接受水平49.the overall financial statement level and in related account balances and transactionlevels 财务报表层和相关账户、交易层50.misstatements or omissions 错报或漏报51.aggregate 总计52.subsequent events 期后事项53.adjust the financial statements 调整财务报表54.perform additional audit procedures 实施追加的审计程序55.audit risk 审计风险56.detection risk 检查风险57.inappropriate audit opinion 不适当的审计意见58.material misstatement 重大的错报59.tolerable misstatement 可容忍错报60.the acceptable level of detection risk 可接受的检查风险61.assessed levelof material misstatement risk 重大错报风险的评估水平62.simallbusiness 小规模企业63.accountingsystem 会计系统64.testof control 控制测试65.walk-throughtest 穿行测试munication沟通67.flowchart 流程图68.reperformanceof internal control 重新执行69.auditevidence 审计证据70.substantiveprocedures 实质性程序71.assertions认定72.esistence存在73.occurrence发生pleteness完整性75.rightsand obligations 权利和义务76.valuationand allocation 计价和分摊77.cutoff截止78.accuracy准确性79.classification分类80.inspection检查81.supervisionof counting 监盘82.observation观察83.confirmation函证putation计算85.analyticalprocedures 分析程序86.vouch核对87.trace追查88.auditsampling 审计抽样89.error误差90.expectederror 预期误差91.population总体92.samplingrisk 抽样风险93.non-sampling risk 非抽样风险94.samplingunit 抽样单位95.statisticalsampling 统计抽样96.tolerableerror 可容忍误差97.therisk of under reliance 信赖不足风险98.therisk of over reliance 信赖过度风险99.therisk of incorrect rejection 误拒风险100.the risk of incorrect acceptance 误受风险101.workingtrial balance 试算平衡表102.indexand cross-referencing 索引和交叉索引103.cashreceipt 现金收入104.cashdisbursement 现金支出105.bankstatement 银行对账单106.bankreconciliation 银行存款余额调节表 107.balancesheet date 资产负债表日realizable value 可变现净值109.storeroom仓库110.saleinvoice 销售发票111.pricelist 价目表112.positiveconfirmation request 积极式询证函113.negativeconfirmation request 消极式询证函114.purchaserequisition 请购单115.receivingreport 验收报告116.grossmargin 毛利117.manufacturingoverhead 制造费用118.materialrequisition 领料单119.inventory-taking存货盘点120.bondcertificate 债券121.stockcertificate 股票122.auditreport 审计报告123.entity被审计单位124.addresseeof the audit report 审计报告的收件人125.unqualifiedopinion 无保留意见126.qualifiedopinion 保留意见127.disclaimerof opinion 无法表示意见128.adverseopinion 否定意见第四篇:英文工作经历词汇_范文英文工作经历词汇2008-01-28 15:58工作经历work experience 工作经历 occupational history 工作经历professional history 职业经历specific experience 具体经历responsibilities 职责 second job 第二职业achievements 工作成就,业绩 administer 管理assist 辅助 adapted to 适应于accomplish 完成(任务等)appointed 被认命的adept in 善于analyze 分析authorized 委任的;核准的 behave 表现break the record 打破纪录breakthrough 关键问题的解决control 控制 conduct 经营,处理cost 成本;费用 create 创造demonstrate 证明,示范 decrease 减少design 设计 develop 开发,发挥devise 设计,发明 direct 指导double 加倍,翻一番 earn 获得,赚取effect 效果,作用 eliminate 消除enlarge 扩大 enrich 使丰富exploit 开发(资源,产品)enliven 搞活establish 设立(公司等);使开业evaluation 估价,评价execute 实行,实施 expedite 加快;促进generate 产生 good at 擅长于guide 指导;*纵 improve 改进,提高initiate 创始,开创 innovate 改革,革新invest 投资 integrate 使结合;使一体化justified 经证明的;合法化的launch 开办(新企业)maintain 保持;维修 modernize 使现代化negotiate 谈判nominated 被提名;被认命的overcome 克服perfect 使完善;改善perFORM 执行,履行 profit 利润be promoted to 被提升为 be proposed as 被提名(推荐)为realize 实现(目标)获得(利润)reconstruct 重建recorded 记载的refine 精练,精制registered 已注册的 regenerate 更新,使再生replace 接替,替换 retrieve 挽回revenue 收益,收入 scientific 科学的,系统的self-dependence 自力更生 serve 服务,供职settle 解决(问题等)shorten 减低……效能simplify 简化,精简 spread 传播,扩大standard 标准,规格 supervises 监督,管理supply 供给,满足 systematize 使系统化test 试验,检验well-trained 训练有素的valuable 有价值的target 目标,指标working model 劳动模范 advanced worker 先进工作者个人资料name 姓名 in.英寸pen name 笔名 ft.英尺alias 别名 street 街Mr.先生 road 路Miss 小姐 district 区Ms(小姐或太太)house number 门牌Mrs.太太 lane 胡同,巷age 年龄 height 身高bloodtype 血型 weight 体重address 地址 born 生于permanent address 永久住址 birthday 生日province 省 birthdate 出生日期city 市 birthplace 出生地点county 县 home phone 住宅电话prefecture 专区 office phone 办公电话autonomous region 自治区 business phone 办公电话nationality 民族;国籍 current address 目前住址citizenship 国籍 date of birth 出生日期native place 籍贯 postal code 邮政编码duel citizenship 双重国籍 marital status 婚姻状况family status 家庭状况 married 已婚single 未婚 divorced 离异separated 分居 number of children 子女人数health condition 健康状况 health 健康状况excellent(身体)极佳 short-sighted近视far-sighted 远视 ID card 身份证date of availability 可到职时间 membership 会员、资格president 会长 vice-president 副会长director 理事 standing director 常务理事society 学会 association 协会secretary-general 秘书长 research society 研究会工作目标objective 目标 position desired 希望职位job objective 工作目标 employment objective 工作目标career objective 职业目标 position sought 谋求职位position wanted 希望职位 position applied for 申请职位离职原因for more specialized work 为更专门的工作for prospects of promotion 为晋升的前途for higher responsibility 为更高层次的工作责任for wider experience 为扩大工作经验due to close-down of company 由于公司倒闭 due to expiry of employment 由于雇用期满sought a better job 找到了更好的工作 to seek a better job 找一份更好的工作业余爱好hobbies 业余爱好 play the guitar 弹吉他reading 阅读 play chess 下棋play 话剧 long distance running 长跑play bridge 打桥牌 collecting stamps 集邮play tennis 打网球 jogging 慢跑sewing 缝纫 travelling 旅游listening to symphony 听交响乐 do some clay scultures 搞泥塑A Useful Glossary for Personal Resumesname 姓名 present address 目前住址alias 别名 permanent address 永久住址pen name 笔名 postal code 邮政编码date of birth 出生日期 home phone 住宅电话birthdate 出生日期 office phone 办公电话born 生于 business phone 办公电话birthplace 出生地点 Tel.电话birthday 生日 * 性别age 年龄 male 男native place 籍贯 female 女province 省 Mr.先生city 市 Miss 小姐autonomous region 自治区 Mrs.太太prefecture 专区 Ms 小姐或太太county 县 height 身高nationality 民族;国籍 cm.厘米citizenship 国籍 ft.英尺duel citizenship 双重国籍 in.英寸address 地址 weight 体重current address 目前住址 kg 公斤lbs 磅 very good 很好marital status 婚姻状况 good 好 family status 家庭状况 strong强壮married 已婚short-sighted近视single/unmarried 未婚far-sighted 远视divorced 离婚 color-blind 色盲separated 分居 ID card 身份证number of children 子女人数date of availability 可到职时间none 无 available 可到职street 街 membership 会员、资格lane 胡同,巷 president 会长road 路 vice-president 副会长district 区 director 理事house number 门牌 standing director 常务理事health 健康状况 secretary-general 秘书长health condition 健康状况 society 学会bloodtype 血型 association 协会excellent(身体)极佳 research society 研究会education 学历“Three Goods” student 三好学生educational background 教育程度 excellent League member 优秀团员educational history 学历 excellent leader 优秀干部curriculum 课程 student council 学生会major 主修 off-job training 脱产培训minor 副修 in-job training 在职培训educaitonal highlights 课程重点部分 educational system 学制curriculum included 课程包括 academic year 学年specialized courses 专门课程 semester 学期(美)courses taken 所学课程 term 学期(英)courses completed 所学课程 president 校长special taining 特别训练 vice-president 副校长social practice 社会实践 dean 院长part-time jobs 业余工作 assistant dean 副院长summer jobs 暑期工作 academic dean 教务员vacation jobs 假期工作 department chairman 系主任refresher course 进修课程 professor 教授extracurricular activities 课外活动 associate professor 副教授physical activities 体育活动 guest professor 客座教授recreational activities 娱乐活动 lecturer 讲师academic activities 学术活动 teaching assistant 助教social activities 社会活动 research fellow 研究员rewards 奖励 research assistant 助理研究员scholarship 奖学金 supervisor 论文导师principal 中学校长(美)Paty branch secretary 党支部书记headmaster 中小学校长(英)League branch secretary 团支部书记master 小学校长(美)commissary in charge of organization 组织委员dean of studies 教务长 commissary in charge of publicity 宣传委员dean of students 教导主任 degree 学位teacher 教师 post doctorate 博士后probation teacher 代课教师 doctor(Ph.D)博士tutor 家庭教师 master 硕士governess 女家庭教师 bachelor 学士intelligence quotient 智商 student 学生pass 及格 graduate student 研究生fail 不及格 abroad student 留学生marks 分数 returned student 回国留学生trades 分数 foreign student 外国学生scores 分数 undergraduate 尚未取得学位的大学生examination 考试 senior 大学四年级/高中三年级学生grade 年级 junior 大学三年级/高中二年级学生class 班级 sophomore 大学二年级/高中一年级学生monitor 班长 freshman 大学一年级学生vice-monitor 副班长 guest student 旁听生(英)commissary in charge of studies 学习委员 auditor 旁听生(美)commissary in charge of entertainment 文娱委员government-sponsored student 公费生 commissary in charge ofsports 体育委员 commoner 自费生commissary in charge of physical labour 劳动委员 extern 走读生day-student 走读生 old girl 女校毕业生(英)intern 实习生 half-timer 选读生prize fellow 奖学金生 evening student 夜校生boarder 寄宿生 frog-green 新生classmate 同班同学repeater 留级生schoolmate 同校同学alumnus 校友graduate 毕业生apprentice 学徒personal management 人事管理casual leave 例假;事假sick leave 病假office hours 办公时间eight-hour shift 8小时工作制shift *班morning session 上午班evening/night shift 小/大夜班day shift 日班attendance book 签到本late book 迟到本day off 休息日coffee break 上班中的休息时间work day 工作日work hour 工作时间working conditions 工作环境work permit 工作证work overtime 加班salary 薪水 wages 工资salary raise 加薪windfall 外快traveling allowance(for official trip)差旅费annual pension 年薪 year-end bonus 年终奖overtime pay 加班费punch the clock 打卡time recorder 打卡机sneak out 开溜on probation 试用 probation staff 试用人员agreement of employment 聘书evaluation of employee 考绩employee evaluation form 考绩表dock pay 扣薪unpaid leave 无薪假take-home pay(税后)净薪release pay 遣散费salary deduction 罚薪第五篇:建筑工程常用英文词汇Construction Site 建筑工地Apologize for any inconvenience caused during building operation 对施工期间带来的不便表示歉意。

审计报告的四大类型

审计报告的四大类型审计报告是审计师编制的一份专业文件,用于对被审计单位的财务状况、财务报表以及相关财务信息进行审计,并对审计结果进行表述和陈述。

审计报告通常被分为四大类型,包括无保留意见、保留意见、否定意见和无法表示意见。

下面将对这四大类型的审计报告进行详细介绍。

1. 无保留意见审计报告(Unqualified Opinion)无保留意见审计报告是最为常见和理想的审计报告类型,意味着审计师对财务报表的整体准确性、真实性和合规性没有发现任何重大错误或问题。

审计师相信财务报表公允地反映出被审计单位的真实财务状况,并且符合适用会计准则和法律法规的要求。

无保留意见审计报告在审计师对被审计单位的财务报表感到满意并认为其真实可信的情况下被发表。

2. 保留意见审计报告(Qualified Opinion)保留意见审计报告是指审计师在对被审计单位的财务报表进行审计时,发现了一些问题或限制了对一些重要信息的获取,但是对整体财务报表对负责毛病没有发现。

审计师在审计报告中详细描述了问题或限制,并明确指出这些问题可能对财务报表的真实性和准确性产生一定影响。

然而,这些影响并不足以使财务报表失去对负责毛病的合理保证。

3. 否定意见审计报告(Adverse Opinion)否定意见审计报告表示审计师认为被审计单位的财务报表不符合适用的会计准则和法律法规的要求,以及无法提供充分、准确的财务信息。

审计师发现了重大错误、重大违规行为、无法解决的差异或严重不一致,且这些问题对财务报表整体准确性和合规性产生了重大的影响。

否定意见审计报告会极大地影响被审计单位的财务状况和信用度,通常意味着被审计单位存在重大财务和合规问题。

4. 无法表示意见审计报告(Disclaimer of Opinion)无法表示意见审计报告是在审计师无法完全对财务报表进行充分、全面的审计,并对财务报表的真实性和合规性进行准确陈述的情况下发表的审计报告。

审计师可能无法获得所需的所有审计证据,或者被审计单位提供的财务记录或信息不完整、不可靠、不准确,导致审计师无法对财务报表做出充分的审计结论。

四大介绍

国际四大调查报告一发展历程国际四大会计师事务所简介“四大”(Big4)是国际四大会计师行的简称。

全球原有八大会计师行,经多次合并重组,形成著名的会计业五巨头,即安达信、普华永道、毕马威、德勤、安永。

2001年,安然事件导致安达信宣告破产,至此形成如今的“四大”格局。

“四大”以会计业起家,同时在金融、管理、信息系统等多个领域开展咨询业务。

具体介绍如下:一、KPMG(毕马威)(一)毕马威发展简史19世纪是会计业发展的黄金时期,尤其是苏格兰的注册会计师行业。

当时的工业革命为会计师提供广阔的发展空间,同时也吸引了越来越多的优秀人才投身于会计行业,威廉·巴克利·皮特(William Barclay Peat)就是其中的杰出代表。

皮特最初是一名苏格兰人开办的会计师事务所的低级职员,其后于1895年设立WB皮特公司(WBpeat &co.)。

1911年,皮特赴美国途中结识了詹姆斯·马威克(James Marwick)。

詹姆斯在纽约成功地经营着一家名为Marwick Mitchell的会计师事务所。

于是,1911年,William Barclay Peat&Co.和Marwick,Mitchell&Co.合并成为一家网络遍布全球的会计及专业咨询机构—Peat Marwick International(PMI),直到1987年PMI与KMG合并,在PM两侧增加了字母KG。

KMG是于1979年,Klynveld、Deutsche Treuhand-Gesellschaft 和跨国专业服务机构McLintock MainLafrentz进行合并组成的Klynveld Main Goerdeler(KMG)。

自1987年,PMI和KMG的成员机构进行合并后,它们在全球各地的所有成员机构均以毕马威的名义提供服务,或把毕马威之名纳入其机构名称内。

毕马威历史悠久,发展跨越三个世纪,KPMG的四个字母分别代表其主要创办人的英文名称缩写:K代表Klynveld—Piet Klynveld于1917年在阿姆斯特丹成立了Klynveld Kraayenhof&Co.。

审计师英语

审计师英语

审计师英语,通常指的是审计师在工作中所使用的专业英语。

由于审计师的工作涉及到大量的财务、会计和法律知识,因此审计师英语中会涉及到大量的专业术语和缩写。

以下是一些常见的审计师英语术语和缩写:

1. CPA (Certified Public Accountant):注册会计师

2. GAAP (Generally Accepted Accounting Principles):公认会计准则

3. IFRS (International Financial Reporting Standards):国际财务报告准则

4. ASME (American Society of Mechanical Engineers):美国机械工程师协会

5. SEC (Securities and Exchange Commission):美国证券交易委员会

6. EOQ (Economic Order Quantity):经济订货量

7. FIFO (First In, First Out):先进先出法

8. LIFO (Last In, First Out):后进先出法

9. EOAP (External Audit Procedure):外部审计程序

10. SSAE 18 (Statement on Standards for Attestation Engagements No. 18):鉴证业务准则公告第18号

以上是一些常见的审计师英语术语和缩写,但实际上还有很多其他的专业术语和缩写。

为了更好地掌握审计师英语,建议多阅读相关的专业文献、参加培训课程或与同行交流。

{财务管理内部审计}会计审计英语词汇大全