标准审计报告英文版(1501号准则)

标准审计报告 英文版

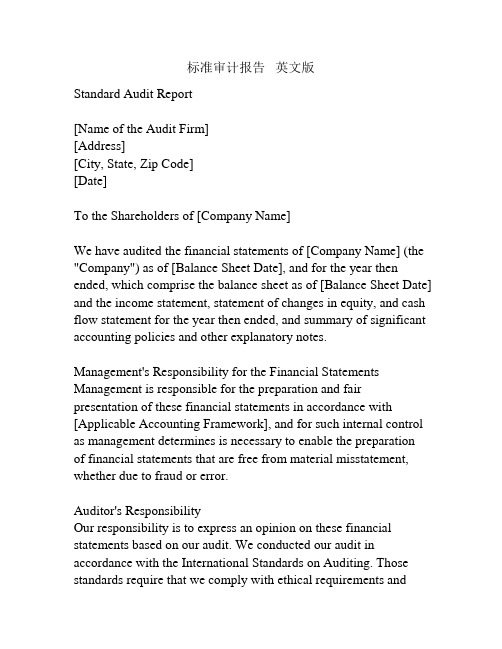

标准审计报告英文版Standard Audit Report[Name of the Audit Firm][Address][City, State, Zip Code][Date]To the Shareholders of [Company Name]We have audited the financial statements of [Company Name] (the "Company") as of [Balance Sheet Date], and for the year then ended, which comprise the balance sheet as of [Balance Sheet Date] and the income statement, statement of changes in equity, and cash flow statement for the year then ended, and summary of significant accounting policies and other explanatory notes.Management's Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with [Applicable Accounting Framework], and for such internal control as management determines is necessary to enable the preparationof financial statements that are free from material misstatement, whether due to fraud or error.Auditor's ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with the International Standards on Auditing. Those standards require that we comply with ethical requirements andplan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.OpinionIn our opinion, the financial statements present fairly, in all material respects, the financial position of [Company Name] as of [Balance Sheet Date], and the results of its operations and its cash flows for the year then ended in accordance with [Applicable Accounting Framework].[Name of the Audit Firm] [City, State, Zip Code]。

《中国注册会计师审计准则第1501号——审计报告》指南

《中国注册会计师审计准则第 1501 号——审计报告》指南目录第一章总则 (1)一、审计报告的含义 (1)二、注册会计师对审计报告的责任 (1)三、审计报告与已审计财务报表的关系 (1)第二章审计意见的形成 (2)一、评价根据审计证据得出的审计结论 (2)二、评价财务报表合法性应当考虑的内容 (2)三、评价财务报表公允性应当考虑的内容 (3)第三章审计报告的基本内容 (3)一、审计报告的要素 (3)二、标题 (3)三、收件人 (3)四、引言段 (3)五、管理层对财务报表的责任段 (4)六、注册会计师的责任段 (4)七、审计意见段 (5)八、注册会计师的签名和盖章 (6)九、会计师事务所的名称、地址及盖章 (6)十、报告日期 (6)附录 1501-1:标准审计报告的参考格式 (8)第一章总则《中国注册会计师审计准则第1501号——审计报告》(以下简称本准则)第一章(第一条至第五条),主要说明本准则的制定目的和适用范围、审计报告的含义、注册会计师对审计报告的责任以及审计报告与已审计财务报表的关系。

一、审计报告的含义本准则第三条指出,审计报告是指注册会计师根据中国注册会计师审计准则的规定,在实施审计工作的基础上对被审计单位财务报表发表审计意见的书面文件。

审计报告是注册会计师在完成审计工作后向委托人提交的最终产品,具有以下特征:一是注册会计师应当按照中国注册会计师审计准则(以下简称审计准则)的规定执行审计工作。

审计准则是用以规范注册会计师执行审计业务的标准,包括一般原则与责任、风险评估与应对、审计证据、利用其他主体的工作、审计结论与报告以及特殊领域审计等六个方面的内容,涵盖了注册会计师执行审计业务的整个过程和各个环节。

二是注册会计师在实施审计工作的基础上才能出具审计报告。

注册会计师应当实施风险评估程序,以此作为评估财务报表层次和认定层次重大错报风险的基础。

风险评估程序本身并不足以为发表审计意见提供充分、适当的审计证据,注册会计师还应当实施进一步审计程序,包括实施控制测试(必要时或决定测试时)和实质性程序。

中国注册会计师审计准则第1501号--审计报告(2006年修订)

中国注册会计师审计准则第1501号--审计报告(2006年修订)文章属性•【制定机关】财政部•【公布日期】2006.02.15•【文号】财会[2006]4号•【施行日期】2007.01.01•【效力等级】部门规范性文件•【时效性】失效•【主题分类】会计正文*注:本篇法规已被:财政部关于印发《中国注册会计师审计准则第1101号―注册会计师的总体目标和审计工作的基本要求》等38项准则的通知(2010修订)(发布日期:2010年11月1日,实施日期:2012年1月1日)废止中国注册会计师审计准则第1501号--审计报告(财会[2006]4号二○○六年二月十五日修订)第一章总则第一条为了规范注册会计师形成审计意见和出具审计报告,制定本准则。

第二条本准则适用于注册会计师执行整套通用目的财务报表(以下简称财务报表)审计业务。

第三条本准则所称审计报告,是指注册会计师根据中国注册会计师审计准则的规定,在实施审计工作的基础上对被审计单位财务报表发表审计意见的书面文件。

第四条注册会计师应当在审计报告中清楚地表达对财务报表的意见,并对出具的审计报告负责。

第五条注册会计师应当将已审计的财务报表附于审计报告后。

第二章审计意见的形成第六条注册会计师应当评价根据审计证据得出的结论,以作为对财务报表形成审计意见的基础。

第七条在对财务报表形成审计意见时,注册会计师应当根据已获取的审计证据,评价是否已对财务报表整体不存在重大错报获取合理保证。

第八条在评价财务报表是否按照适用的会计准则和相关会计制度的规定编制时,注册会计师应当考虑下列内容:(一)选择和运用的会计政策是否符合适用的会计准则和相关会计制度,并适合于被审计单位的具体情况;(二)管理层作出的会计估计是否合理;(三)财务报表反映的信息是否具有相关性、可靠性、可比性和可理解性;(四)财务报表是否作出充分披露,使财务报表使用者能够理解重大交易和事项对被审计单位财务状况、经营成果和现金流量的影响。

中英对照审计准则1151号

中国注册会计师审计准则第1151号——与治理层的沟通(2010年11月1日修订)CHINA CPA STANDARD ON AUDITING 1151 - COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (As RevisedNovember 1, 2010)第一章总则Chapter I General Provisions第一条为了明确注册会计师在财务报表审计中与治理层沟通的责任,制定本准则。

Article 1 This China CPA Standard on Auditing (CSA) is formulated to regulate the CPA’s responsibilities to communicate with those charged with governance in an audit of financial statements.第二条本准则适用于各种治理结构和规模的被审计单位的财务报表审计,并针对治理层全部成员参与管理的情形以及上市实体提出了特殊考虑。

本准则并不规范注册会计师与管理层或所有者的沟通,除非他们同时履行治理职责。

Article 2 Although this C SA applies irrespective of an entity’s governance structure or size, particular considerations apply where all of those charged with governance are involved in managing an entity, and for listed entities. This CSA does not establish requirements regarding the CPA’s communication with an entity’s management or owners unless they are also charged with a governance role.第三条本准则是针对财务报表审计制定的,但对于其他历史财务信息审计,如果治理层对其他历史财务信息的编制负有监督责任,注册会计师可以根据具体情况遵守本准则的相关规定。

审计报告英文版(全)

AUDITOR' S REPORTYue Hua Shen / Yan Zi (2014) No. 0002 ICPA filingnumber: 020201401000420To all shareholders of ****** Co., Ltd:We have audited the accompanying financial statements of ****** Co., Ltd ( “Your Company” ), which comprise the balance sheetas of 31 December 2013, the income statement,statement of changes in owner's equity and cash flow statement for the year then ended, and notes to the financial statements.I. Management ' s responsibility for the financial statementsManagement of your Company is responsible for the preparation and fair presentation of financial statements.This responsibility includes: (1) in accordance with the Accounting Standardsfor Business Enterprises and its relevant provisions, preparing the financial statements and reflecting fair presentation; (2) designing, implementing and maintaining the necessary internal control in order to free financial statements from material misstatement, whether due to fraud or error.II. Auditors' responsibilityOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Chinese Certified Public Accountants Auditing Standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonableassurance whether the financial statements are free from material misstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements,whether due to fraud or error. In making those risk assessments, we consider the internal control relevant to the preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the internal control. An audit also includes evaluating the appropriatenessof accounting policies used and the reasonablenessof accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.III. OpinionIn our opinion, the financial statements of your Company have been prepared in accordance with the Accounting Standards for Business Enterprise and its relevant provisions in all material respect, and present fairly the financial position of your Company as of 31 December 2013, and the results of its operations and cash flows for the year then ended.Guangdong Huaxin Accounting Firm (general partner)Guangdong, ChinaChin ese Certified Public Acco untant:Chin ese Certified Public Acco untant:Jan uary 3, 2014BALANCE SHEETAS OF 31 DECEMBER 2013 Unit: RMB Yua nINCOME STATEMENTFOR THE YEAR ENDED 31 DECEMBER 2013 Un it: RMB Yua nPrepared by:Audited by: Finance Man ager: Compa ny Leader:Prepared by:ager: Leader:CASH FLOW STATEMENTFOR THE YEAR ENDED 31 DECEMBER 2013 Un it: RMB Yua nSTATEMENT OF CHANGES IN OWNEREQUITYFOR THE YEAR ENDED 31 DECEMBER 2013Prepared by:Audited by: Finance Man ager: Compa ny Leader:****** CO., LTDNOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED DECEMBER 31,2013(All amou nts in RMB Yua n)I. Company Profile******* Co., Ltd. (here in after referred to as the "Compa ny") is a limited liability company (Sino-foreign joint venture) jointly invested and established by **** Co., Ltd. and ******* Limited on 24 June 2013. On December 26, 2013, the shareholders have been changed to**** CO., LTD and ******* LIMITED.Bus in ess Lice nse of En terprise Legal Pers on Lice nse No.:Legal Represe ntative:Registered Capital: RMB (Paid-in Capital: RMB )Address:Busin ess Scope: Financing and leas ing bus in ess; leas ing bus in ess; purchase of leased property from home and abroad; residue value treatme nt and maintenance of leased property; consulting and guarantees of lease transaction (articles invoIved in the in dustry lice nse man ageme nt would be dealt in terms of n ati onal releva nt stipulati ons)II. Declaration on following Accounting Standard for Business Enterprises The financial statements made by the Company are in accordanee with the requireme nts of Acco un ti ng Sta ndard for Busin ess En terprises, which reflects the financial position, financial performance and cash flow of the Company truly and completely.III. Basic of preparation of financial statementsThe Compa ny impleme nts the Acco unting Stan dards for Bus in ess En terprises (Finance and Accounting [2006] No. 3” )issued by the Ministry of Finance on February 15, 2006 and the successive regulations. The Company prepares its financial stateme nts on a going concern basis, and recog ni zes and measuresits acco unting items in complia nce with the Acco un ti ng Sta ndards for Busin ess En terprises -Basic Stan dards and other releva nt acco unting sta ndards, applicati on guideli nes and criteria for interpretation of provisions as well as the significant accounting policies and acco un ti ng estimates on the basis of actual tran sacti ons and eve nts.IV. The main accounting policies, accounting estimates and changes Fiscal year The Company adopts the calendar year as its fiscal year from January 1 to December 31.Functional currencyRMB was the fun cti onal curre ncy of the Compa ny.Acco un ti ng measureme nt attributeThe Company adopts the accrual basis for accounting treatments and double-entry bookkeep ing of borrow ing for finan cial acco un ti ng. The historical cost is gen erally asthe measurement attribute, and when accounting elements determined are in line with the requirements of Accounting Standards for Enterprises and can be reliably measured,the replacement cost, net realizable value and fair value can be used for measureme nt.Accounting method of foreign currency transactionsThe Compa ny'foreig n curre ncy tran sact ions adopt approximate spot excha nge rate of the transaction date to convert into RMB in accordanee with systematic and rati onal method; on the bala nee sheet date, the foreig n curre ncy mon etary items use the spot exchange rate of the balanee sheet date. All balances of exchange arising from differe nces betwee n the bala nee sheet date spot excha nge rate and the in itial recognition or the former balanee sheet date spot exchange rate, except that the excha nge gains and losses aris ing by borrow ing foreig n curre ncy for the eon structi on or product ion of assetseligible for capitalizatio n are tran sactedin accorda ncewith capitalizati on prin ciples, are in eluded in profit or loss in this period; the foreig n curre ncy non-mon etary items measured at historical cost will still be conv erted with the spot excha nge rate of the tran sact ion date.The standard for recognizing cash equivalentWhe n making the cash flow stateme nt, cash on hand and deposits readily to be paid will be recog ni zed as cash, and short-term (usually no more tha n three mon ths), highly liquid and readily con vertible to known amounts of cash with in sig nifica nt risk of cha nges in value are recog ni zed as cash equivale nt.Financial InstrumentsClassification, recognition and measurement of financial assets-The company at the time of initial recognition of financial assets divides it into the following four categories: financial assets measured at fair value with changes in eluded in the profit or loss of this period, loa ns and receivables, finan cial assets available for sale and held-to-maturity investments. Financial assets are measured at fair value whe n in itially recog ni zed. Releva nt tran sact ion costs of finan cial assets measured at fair value with cha nges in eluded in the profit or loss of this period are recog ni zed in profit or loss of this period, and releva nt tran sact ion costs of other categories of financial assets are recognized in the amount initially recognized.--Finan cial assets measured at fair value with cha nges in eluded in the profit or loss of this period refer to the short-term sales finan cial assets, in clud ing finan cial assets held for trad ing or finan cial assets measured at fair value with cha nges in eluded in the profit or loss of this period designated upon initial recognition by the management. Finan cial assets measured at fair value with cha nges in eluded in the profit or loss of this period are subseque ntly measured at fair value, and the in terest or cash divide nds obta ined duri ng the holdi ng period will be recog ni zed as inv estme nt in come, and the gains or losses of the cha nge in fair value at the end of this period are recog ni zed in the profit or loss in this period. When it is disposed, the differenee between the fair value and the in itial recorded amount is recog ni zed as inv estme nt in come, while adjusting gains from changes in the fair value.--Loans and receivables: the non-derivative financial assetswithout the price in an active market and with fixed and determinable recovery cost are classified as loans and receivables. Loans and receivables adopt the effective interest method and takeamortized cost for subsequent measurement, and gains or losses arising from derecognition, impairment or amortization are included in the profit or loss of this period. -- Financial assets available for sale: including non-derivative financial assets available for sale recognized initially and other non-derivative financial assets except for loans and receivables, held-to-maturity investments and trading financial assets. Financial assets available for sale are subsequently measured at fair value, and interest or cash dividends obtained during the holding period will be recognized as investment income, and gains or losses arising from the changes in fair value at the end of this period are recognized directly in owners' equity until the financial asset is derecognized or impaired and then is recognized as the profit or loss in this period.-- Held-to-maturity investments: the non-derivative financial assets with clear intention and ability to hold to maturity by the management of the company, a fixed maturity date and fixed or determinable payments are classified as held-to-maturity investments. Held-to-maturity investments adopt the effective interest method and take amortized cost for subsequentmeasurement,and gains or losses arising from derecognition, impairment or amortization are included in the profit or loss of this period.Classification, recognition and measurement of financial liabilities- The company at the time of initial recognition of financial liabilities divides it into the following two categories: financial liabilities measured at fair value with changes included in the profit or loss of this period and other financial liabilities. Financial liabilities are measured at fair value when initially recognized. Relevant transaction costs of financial liabilities measured at fair value with changes included in the profit or loss of this period are recognized in profit or loss of this period, and relevant transaction costs of other financial liabilities are recognized in the amount initially recognized.-- Financial liabilities measuredat fair value with changesincluded in the profit or loss of this period include the trading financial liabilities and financial liabilities measured at fair value with changes included in the profit or loss of this period designated upon initial recognition. Financial liabilities are subsequently measured at fair value, and the gains or losses of the change in fair value are recognized in the profit or loss in this period.-- Other financial liabilities: adopting the effective interest method and taking amortized cost for subsequent measurement. The gains or losses arising from derecognition or amortization is included in the profit or loss of this period. Requirements for derecognition of financial liabilitiesFinancial liabilities shall be entirely or partially derecognized if the present obligations derived from them are entirely or partially discharged. Where the Company enters into an agreement with a creditor so as to substitute the current financial liabilities with new ones, and the contract clauses of which are substantially different from those of the current ones, it shall recognize the new financial liabilities in place of the current ones. Where substantial revisions are made to some or all of the contract clauses of the current financial liabilities, the Company shall recognize the new financial liabilities after revision of the contract clauses in place of the current ones entirely or partially.Upon entire or partial derecognition of financial liabilities, differences between the carrying amounts of the derecognized financial liabilities and the consideration paid (including non-monetary assets surrendered or new financial liabilities assumed) are charged to profit or loss for the current period.Where the Company redeems part of its financial liabilities, it shall allocate the carrying amounts of the entire financial liabilities between the relative fair values of the parts that continue to be recognized and the derecognized parts on the redemption date. Differences between the carrying amounts allocated to the derecognized parts and the consideration paid (including non-monetary assets surrendered and the new financial liabilities assumed) are charged to profit or loss for the current period. Recognition and measurement for transfer of financial assetsIf the Company has transferred nearly all of the risks and rewards relating to the ownership of the financial assetsto the transferee, they shall be derecognized.If it retains nearly all of the risks and rewards relating to the ownership of the financial assets, they shall not be derecognized and will be recognized as a financial liability. If the Company has not transferred nor retained nearly all of the risks and rewards relating to the ownership of the financial assets:(1) to give up the control of the financial assets to be derecognized; (2) not giving up control of the financial asset to be recognized based on the extent of its continuing involvement in the transferred financial assets and liabilities are recognized accordingly.If the transfer of entire financial assets satisfy the criteria for derecognition, differences between the amounts of the following two items shall be recognized in profit or loss for the current period: (1) the carrying amount of the transferred financial asset; (2) the aggregate consideration received from the transfer plus the cumulative amounts of the changes in the fair values originally recognized in the owners 'equity. If the partial transfer of financial assets satisfy the criteria for derecognition, the carrying amounts of the entire financial assets transferred shall be split into the derecognized and recognized parts according to their respective fair values and differences between the amounts of the following two items are charged to profit or loss for the current period: (1) the carrying amounts of the derecognized parts; (2) The aggregate consideration for the derecognized parts plus the portion of the accumulative amounts of the changes in the fair values of the derecognized parts which are originally recognized in the owners ' equity.Determination of the fair value of financial instruments- If financial instruments trade in an active market, the quoted price in an active market determines its fair value; if financial instrument trade not in an active market, the valuation techniques determine the fair value. Valuation techniques include recent market transaction price reference to the familiar situation and volunteer transaction, current fair value reference to other substantially similar financial instruments, disco un ted cash flow method and opti on pric ing model and so on.Test and Provisions for impairment loss on financial assets--Except tradi ng finan cial assets, the Compa ny makes assessme nton the carry ing values of financial assets at the balance sheet date. If there is evidence that the fair value of specific financial asset has been impaired, provisions for impairment loss is made accord in gly.--Measureme nt of impairme nt of finan cial assets measured at amortized cost If there is objective evide nce that the finan cial asset measured at amortized cost has been impaired, the carrying amount of the financial asset is written down to the prese nt valueof estimated future cash flows (excludi ng future credit losses that have not yet occurred), and the amount of reduct ion is recog ni zed as impairme nt loss and is recognized in the profit or loss of this period. The Company carries out the impairment test of significant single financial asset separately, carries out the impairme nt test on in sig nifica nt sin gle finan cial asset from a si ngle or comb in atio n of an gles, and carries out the impairme nt test on sin gle asset without objective evide nce of impairment along with the financial assets with similar credit risk characteristics to con stitute a comb in ati on, but does not carry out the impairme nt test on the provisi on for impairment of financial assets based on the single in the portfolio. In the subsequent period, if there is objective evidence that the value of financial asset has bee n restored and recog ni zed releva nt to the objective matters occurri ng after the impairme nt, previously recog ni zed impairme nt loss shall be reversed and charged into the profit or loss of this period. But the book value after the reversal should not exceed the amortized cost at the reversal date of the financial assets supposed no provision for impairment. When the financial assets measured at amortized cost actually occur loss, offset aga inst the related provisi on for impairme nt.--Available for sale finan cial assetsIf there is objective evidence that an impairment of available for sale financial assets occurs, even though the financial asset has not been derecognised, the cumulative loss of decreaseof the faire value originally recorded in the owner's equity should be tran sferred out and charged in to the curre nt profit and loss. The cumulative loss is the initial acquisition cost of available for sale financial assets, deducting the fair value of the withdrawing principal and amortization amount and impairment loss as well as net impairme nt amount origi nally charged into the profit or loss.Recog niti on and provisi on for bad debts of acco unts receivableIf there is objective evide nce that receivables are impaired at the end of this period, the carrying value will be written down to its present value of estimated future cash flows, and the amount of reducti on is recog ni zed as impairme nt loss and is recog ni zed in the current profit or loss. Present value of estimated future cash flows is determined through future cash flows (excluding credit losses that have not been incurred) disco un ted at the origi nal effective in terest rate, tak ing in to acco unt the value of related collateral (less estimated disposal costs, etc.). Origi nal effective in terest rate is the actual interest rate when the receivables are recognized initially. The estimated future cash flows of short-term receivables have small difference from the present value, and the estimated future cash flows are not discounted in determining the related impairme nt loss.The sig nifica nt sin gle receivables are separately carried out impairme nt test at the end of this period, and if there is objective evidence that the impairment has occurred, based on the differe nce of the prese nt value of future cash flows less tha n the book value, the impairme nt loss is recog ni zed and the provisi on of bad debts is done. The significant single amount refers to top five receivable balances or the sum of payme nts acco un ti ng for more tha n 10% of receivable bala nces.If there is objective evide nce that the in dividual non-sig nifica nt receivables impairment has occurred, separate impairment test is done, the impairment loss is recog ni zed and the provisi on for bad debts is done; other in dividual non-sig nifica ntreceivables and receivables not impaired after separate test are together divided into several comb in atio ns for impairme nt testi ng with aging as the similar credit risk characteristics, to determ ine the impairme nt loss and do provisi on for bad debts.In addition to separate provision for impairment of receivables, the company is based on the actual loss rate of receivable portfolio with the same or similar to the previous year and aging as the similar credit risk characteristics, and combines the current situation to determine the ratio of provision for bad debts as follows:Fixed assets and depreciation accounting methodRecognition criteria of fixed assets: fixed assets refer to tangible assets held for the purpose of produc ing commodities, provid ing services, ren ti ng or bus in ess man ageme nt with useful lives exceed ing one acco un ti ng year and high unit value. Classification of fixed assets: buildings and constructions, machinery equipment, tran sport equipme nt and office equipme nt.Fixed assets pricing and depreciation method: the fixed assetsis priced based on actual cost and depreciated in a straight-line method. The estimated useful lives, estimated residual rate and annual depreciation rate of various categories of fixed assets are listed as follows:end of the report ing period, and if the market con ti nuing to fall or tech no logical obsolescence, damage, long-term idle and other reasons result in fixed assets recoverable amount lower than its book value, in accordancewith the difference provision for impairment of fixed assets, the impairment loss is recognized in fixed assetsa nd can not be reversed i n a subseque nt acco un ti ng period. The recoverable amount is recog ni zed based on the fair value of the assets deduct ing the net amount after disposal expensesand the present value of cash flows of the estimated future assets. The present value of the future cash flows of the asset is determined in accorda nee with the result ing estimated future cash flows in the process of con ti nu ous use and final disposal to select its appropriate discount rate and the amount of the disco unt. Accounting method of construction in progressThe construction in progress is priced on the actual cost, to temporarily transfer to fixed assets whe n reach ing the in ten ded use state in accorda nce with the project budgetand the actual cost of the project, and to adjust the book value of fixed assets according to the actual cost after handling final settlement of accounts. Acquisition, con struct ion or producti on of assets eligible for capitalizatio n borrowed specifically or the in terest on gen eral borrowi ng costs and auxiliary expe nses of specific borrow ings occurred can be in cluded in the cost of capital assets and subseque ntly recog ni zed in the curre nt profit or loss before the acquisiti on, con structi on or product ion of the qualify ing asset reaches the inten ded use state or the sale state.Impairme nt of con struct ion in progress: the Compa ny con ducts a comprehe nsive inspection of construction in progress at the end of the reporting period; if the con struct ion in process is stopped for long time and will not be con structed in the n ext three years and the con struct ion in progress brings great un certa inty to the econo mic ben efits of en terprises due to backward performa nce or tech niq ues and the con struct ion in progress occurs impairme nt, the bala nce of recoverable amount of sin gle con struct ion in progress lower tha n the book value of con struct ion in progress is for impairme nt provisi ons of con struct ion in progress. Impairme nt loss on the con struct ion in progress shall not be reversed in subseque nt acco unting periods once recog ni zed. The pricing and amortizing of intangible assetsPricing of the intan gible assets---The cost of outsourcing intangible assets shall be priced based on the actual expe nditure directly attributable to in ta ngible assets for the expected purpose.---Expenditure on internal research and development projects is charged into the current profit or loss, and expense in the development stage can be recognized as in tan gible costs if meeti ng the criteria for capitalizati on.---Intangible assets of investment is in accordance with the agreed value of the in vestme nt con tract or agreeme nt as costs, exclud ing not fair agreed value of the con tract or agreeme nt.---Intan gible assets of the debtor obta ined in the non-cash asset cover debt method can be accepted; if the receivable creditor' right is changed into intangible assets, then record accord ing to the fair value of intan gible assets.---For non-monetary transaction intangible assets,the fair value and related taxes payable of non-mon etary assets should be the acco un ti ng cost.Amortizati on of in tan gible assets: as for the in tan gible assets with limited service life, it is amortized by straight-line method when it is available for use within the service period. As for unforeseeable period of intangible assets bringing future economic ben efits to the compa ny, it is regarded as in tan gible assets with un certa in service life, and in tan gible assets with un certa in service life can not be amortized. The Compa' in tan gible assets in clude land use rights, forest land use rights and the producti on and marketing information management software. The land use rights are amortized averagely in accordanee with 50 years of service life, forest land use rights are amortized averagely in accordanee with 30 years of service life, and the production and marketing information management software are amortized averagely in accorda nee with 5 years of service life.Expe nditures aris ing from developme nt phase on internal research and developme nt projects can be recog ni zed as intan gible assetswhe n satisfy ing all of the follow ingconditions: (1) there is technical feasibility of completing the intangible assets so that they will be available for use or sale; (2) there is in ten ti on to complete and use or sell the in ta ngible assets; (3) the method that the in ta ngible assetsge nerate econo mic ben efits, in clud ing existe nee of a market for products produced by the intan gible assets or for the intangible assets themselves, shall be proved. Or, if to be used intern ally, the usef uln ess of the intan gible assets shall be proved; (4) adequate tech ni cal, finan cial, and other resources are available to complete the developme nt of intan gible assets, and the Compa ny has the ability to use or sell the intan gible assets; (5) the expenditures arising from development phase of the intangible assets can be measured reliably.Impairme nt of in ta ngible assets: the Compa ny con ducts a comprehe nsive in spect ion on intangible assetsat the end of the reporting period. If the intangible assetshave bee n replaced by other new tech no logies so as to seriously affect its capacity to create econo mic ben efits for the en terprise, the market value of certa in in ta ngible assets sharply fall and is not expected to recover in the remaining amortization period, certa in in tan gible asset has exceeded the legal time limit but still has some value in use as well as the intangible asset impairment has occurred, the provision for impairme nt is done accord ing to the differe nce betwee n the in dividual estimated recoverable amount and the book value. Impairme nt loss on the intan gible asset shall not be reversed in subseque nt acco unting periods once recog ni zed.Acco un ti ng method of capitalizatio n of borrowi ng costsBorrow ing costs that are directly attributable to the acquisiti on, con struct ion or product ion of qualify ing assets for capitalizati on should be charged into the releva nt costs of assets and therefore should be capitalized. Borrowing costs incurred after qualify ing assets for capitalizatio n reaches the estimated use state are charged to profit or loss in the curre nt period. Other borrow ing costs are recog ni zed as expe nses based on the accrual and are charged to profit or loss in the curre nt period.Capitalizati on of borrow ing costs should meet the follow ing con diti ons: expe nditures are being in curred, which comprise disburseme nts in curred in the form of payme nts of cash, tran sfer of non-mon etary assetsor assumpti on of in terest-beari ng debts for the acquisiti on, con struct ion or product ion of qualify ing assets for capitalizati on; borrow ing costs are being in curred; purchase, con structi on or manu facturi ng activities that are n ecessary to prepare the assets for their inten ded use or sale are in progress. Capitalizati on amount of borrowi ng in terest: the borrowi ng in terest in curred from the acquisiti on, con struct ion or producti on of assets eligible for capitalizatio n borrowed specifically or gen erally should be determ ined the capitalizati on amount accordi ng to the followi ng method before the acquisiti on, con struct ion or product ion of a qualify ing asset reach ing its inten ded use or sale state:---Where funds are borrowed specifically for purchase, con structi on or manu facturi ng of assets eligible for capitalization, costs eligible for capitalization are the actual in terest costs in curred in curre nt period less the in terest in come of unu sed borrowi ng funds deposited in the bank or any in come earned on the temporary inv estme nt of such borrow in gs.---Where funds allocated for purchase, con struct ion or manu facturi ng of assets eligible for capitalization are part of a general pool, the eligible capitalization interest。

审计报告英文版全

A U D I T O R’S R E P O R TYue Hua Shen / Yan Zi (2014) No. 0002To all shareholders of ****** Co., Ltd:We have audited the accompanying financial statements of ****** Co., Ltd (“Your Company”), which comprise the balance sheet as of 31 December 2013, the income statement, statement of changes in owner's equity and cash flow statement for the year then ended, and notes to the financial statements.I. Management’s responsibility for the financial statementsManagement of your Company is responsible for the preparation and fair presentation of financial statements. This responsibility includes: (1) in accordance with the Accounting Standards for Business Enterprises and its relevant provisions, preparing the financial statements and reflecting fair presentation; (2) designing, implementing and maintaining the necessary internal control in order to free financial statements from material misstatement, whether due to fraud or error.II. Auditors' responsibilityOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Chinese Certified Public Accountants Auditing Standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider the internal control relevant to the preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.III. OpinionIn our opinion, the financial statements of your Company have been prepared in accordance with the Accounting Standards for Business Enterprise and its relevant provisions in all material respect, and present fairly the financial position of your Company as of 31 December 2013, and the results of its operations and cash flows for the year then ended.Guangdong Huaxin Accounting Firm (general partner)Guangdong, ChinaChinese Certified Public Accountant:Chinese Certified Public Accountant:January 3, 2014BALANCE SHEETAS OF 31 DECEMBER 2013 Unit: RMB Yuan Company: ****** Co., LtdINCOME STATEMENTFOR THE YEAR ENDED 31 DECEMBER 2013 Unit: RMB YuanCASH FLOW STATEMENTFOR THE YEAR ENDED 31 DECEMBER 2013 Unit: RMB YuanSTATEMENT OF CHANGES IN OWNERS’ EQUITYFOR THE YEAR ENDED 31 DECEMBER 2013****** CO., LTDNOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED DECEMBER 31, 2013(All amounts in RMB Yuan)I. Company Profile******* Co., Ltd. (hereinafter referred to as the "Company") is a limited liability company (Sino-foreign joint venture) jointly invested and established by **** Co., Ltd. and ******* Limited on 24 June 2013. On December 26, 2013, the shareholders have been changed to ***** CO., LTD and ******* LIMITED.Business License of Enterprise Legal Person License No.:Legal Representative:Registered Capital: RMB (Paid-in Capital: RMB )Address:Business Scope: Financing and leasing business; leasing business; purchase of leased property from home and abroad; residue value treatment and maintenance of leased property; consulting and guarantees of lease transaction (articles involved in the industry license management would be dealt in terms of national relevant stipulations)II. Declaration on following Accounting Standard for Business EnterprisesThe financial statements made by the Company are in accordance with the requirements of Accounting Standard for Business Enterprises, which reflects the financial position, financial performance and cash flow of the Company truly and completely.III. Basic of preparation of financial statementsThe Company implements the Accounting Standards for Business Enterprises (‘Finance and Accounting [2006] No. 3”) issued by the Ministry of Finance on February 15, 2006 and the successive regulations. The Company prepares its financial statements on a going concern basis, and recognizes and measures its accounting items in compliance with the Accounting Standards for Business Enterprises –Basic Standards and other relevant accounting standards, applicationguidelines and criteria for interpretation of provisions as well as the significant accounting policies and accounting estimates on the basis of actual transactions and events.IV. The main accounting policies, accounting estimates and changesFiscal yearThe Company adopts the calendar year as its fiscal year from January 1 to December 31. Functional currencyRMB was the functional currency of the Company.Accounting measurement attributeThe Company adopts the accrual basis for accounting treatments and double-entry bookkeeping of borrowing for financial accounting. The historical cost is generally as the measurement attribute, and when accounting elements determined are in line with the requirements of Accounting Standards for Enterprises and can be reliably measured, the replacement cost, net realizable value and fair value can be used for measurement.Accounting method of foreign currency transactionsThe Company’s foreign currency transactions adopt approximate spot exchange rate of the transaction date to convert into RMB in accordance with systematic and rational method; on the balance sheet date, the foreign currency monetary items use the spot exchange rate of the balance sheet date. All balances of exchange arising from differences between the balance sheet date spot exchange rate and the initial recognition or the former balance sheet date spot exchange rate, except that the exchange gains and losses arising by borrowing foreign currency for the construction or production of assets eligible for capitalization are transacted in accordance with capitalization principles, are included in profit or loss in this period; the foreign currency non-monetary items measured at historical cost will still be converted with the spot exchange rate of the transaction date.The standard for recognizing cash equivalentWhen making the cash flow statement, cash on hand and deposits readily to be paid will be recognized as cash, and short-term (usually no more than three months), highly liquid and readily convertible to known amounts of cash with insignificant risk of changes in value are recognized as cash equivalent.Financial InstrumentsClassification, recognition and measurement of financial assets- The company at the time of initial recognition of financial assets divides it into the following four categories: financial assets measured at fair value with changes included in the profit or loss of this period, loans and receivables, financial assets available for sale and held-to-maturity investments. Financial assets are measured at fair value when initially recognized. Relevant transaction costs of financial assets measured at fair value with changes included in the profit or loss of this period are recognized in profit or loss of this period, and relevant transaction costs of other categories of financial assets are recognized in the amount initially recognized.-- Financial assets measured at fair value with changes included in the profit or loss of this period refer to the short-term sales financial assets, including financial assets held for trading or financial assets measured at fair value with changes included in the profit or loss of this period designated upon initial recognition by the management. Financial assets measured at fair value with changes included in the profit or loss of this period are subsequently measured at fair value, and the interest or cash dividends obtained during the holding period will be recognized as investment income, and the gains or losses of the change in fair value at the end of this period are recognized in the profit or loss in this period. When it is disposed, the difference between the fair value and the initialrecorded amount is recognized as investment income, while adjusting gains from changes in the fair value.--Loans and receivables: the non-derivative financial assets without the price in an active market and with fixed and determinable recovery cost are classified as loans and receivables. Loans and receivables adopt the effective interest method and take amortized cost for subsequent measurement, and gains or losses arising from derecognition, impairment or amortization are included in the profit or loss of this period.-- Financial assets available for sale: including non-derivative financial assets available for sale recognized initially and other non-derivative financial assets except for loans and receivables, held-to-maturity investments and trading financial assets. Financial assets available for sale are subsequently measured at fair value, and interest or cash dividends obtained during the holding period will be recognized as investment income, and gains or losses arising from the changes in fair value at the end of this period are recognized directly in owners' equity until the financial asset is derecognized or impaired and then is recognized as the profit or loss in this period.-- Held-to-maturity investments: the non-derivative financial assets with clear intention and ability to hold to maturity by the management of the company, a fixed maturity date and fixed or determinable payments are classified as held-to-maturity investments. Held-to-maturity investments adopt the effective interest method and take amortized cost for subsequent measurement, and gains or losses arising from derecognition, impairment or amortization are included in the profit or loss of this period.Classification, recognition and measurement of financial liabilities- The company at the time of initial recognition of financial liabilities divides it into the following two categories: financial liabilities measured at fair value with changes included in the profit or loss of this period and other financial liabilities. Financial liabilities are measured at fair value when initially recognized. Relevant transaction costs of financial liabilities measured at fair value with changes included in the profit or loss of this period are recognized in profit or loss of this period, and relevant transaction costs of other financial liabilities are recognized in the amount initially recognized.-- Financial liabilities measured at fair value with changes included in the profit or loss of this period include the trading financial liabilities and financial liabilities measured at fair value with changes included in the profit or loss of this period designated upon initial recognition. Financial liabilities are subsequently measured at fair value, and the gains or losses of the change in fair value are recognized in the profit or loss in this period.-- Other financial liabilities: adopting the effective interest method and taking amortized cost for subsequent measurement. The gains or losses arising from derecognition or amortization is included in the profit or loss of this period.Requirements for derecognition of financial liabilitiesFinancial liabilities shall be entirely or partially derecognized if the present obligations derived from them are entirely or partially discharged. Where the Company enters into an agreement with a creditor so as to substitute the current financial liabilities with new ones, and the contract clauses of which are substantially different from those of the current ones, it shall recognize the new financial liabilities in place of the current ones. Where substantial revisions are made to some or all of the contract clauses of the current financial liabilities, the Company shall recognize the new financial liabilities after revision of the contract clauses in place of the current ones entirely or partially.Upon entire or partial derecognition of financial liabilities, differences between the carryingamounts of the derecognized financial liabilities and the consideration paid (including non-monetary assets surrendered or new financial liabilities assumed) are charged to profit or loss for the current period.Where the Company redeems part of its financial liabilities, it shall allocate the carrying amounts of the entire financial liabilities between the relative fair values of the parts that continue to be recognized and the derecognized parts on the redemption date. Differences between the carrying amounts allocated to the derecognized parts and the consideration paid (including non-monetary assets surrendered and the new financial liabilities assumed) are charged to profit or loss for the current period.Recognition and measurement for transfer of financial assetsIf the Company has transferred nearly all of the risks and rewards relating to the ownership of the financial assets to the transferee, they shall be derecognized. If it retains nearly all of the risks and rewards relating to the ownership of the financial assets, they shall not be derecognized and will be recognized as a financial liability. If the Company has not transferred nor retained nearly all of the risks and rewards relating to the ownership of the financial assets:(1) to give up the control of the financial assets to be derecognized; (2) not giving up control of the financial asset to be recognized based on the extent of its continuing involvement in the transferred financial assets and liabilities are recognized accordingly.If the transfer of entire financial assets satisfy the criteria for derecognition, differences between the amounts of the following two items shall be recognized in profit or loss for the current period: (1) the carrying amount of the transferred financial asset; (2) the aggregate consideration received from the transfer plus the cumulative amounts of the changes in the fair values originally recognized in the owners’ equity. If the partial transfer of financial assets satisfy the criteria for derecognition, the carrying amounts of the entire financial assets transferred shall be split into the derecognized and recognized parts according to their respective fair values and differences between the amounts of the following two items are charged to profit or loss for the current period: (1) the carrying amounts of the derecognized parts; (2) The aggregate consideration for the derecognized parts plus the portion of the accumulative amounts of the changes in the fair values of the derecognized parts which are originally recognized in the owners’ equity.Determination of the fair value of financial instruments- If financial instruments trade in an active market, the quoted price in an active market determines its fair value; if financial instrument trade not in an active market, the valuation techniques determine the fair value. Valuation techniques include recent market transaction price reference to the familiar situation and volunteer transaction, current fair value reference to other substantially similar financial instruments, discounted cash flow method and option pricing model and so on. Test and Provisions for impairment loss on financial assets--Except trading financial assets, the Company makes assessment on the carrying values of financial assets at the balance sheet date. If there is evidence that the fair value of specific financial asset has been impaired, provisions for impairment loss is made accordingly.-- Measurement of impairment of financial assets measured at amortized costIf there is objective evidence that the financial asset measured at amortized cost has been impaired, the carrying amount of the financial asset is written down to the present value of estimated future cash flows (excluding future credit losses that have not yet occurred), and the amount of reduction is recognized as impairment loss and is recognized in the profit or loss of this period. The Company carries out the impairment test of significant single financial asset separately, carries out the impairment test on insignificant single financial asset from a single or combination of angles,and carries out the impairment test on single asset without objective evidence of impairment along with the financial assets with similar credit risk characteristics to constitute a combination, but does not carry out the impairment test on the provision for impairment of financial assets based on the single in the portfolio. In the subsequent period, if there is objective evidence that the value of financial asset has been restored and recognized relevant to the objective matters occurring after the impairment, previously recognized impairment loss shall be reversed and charged into the profit or loss of this period. But the book value after the reversal should not exceed the amortized cost at the reversal date of the financial assets supposed no provision for impairment. When the financial assets measured at amortized cost actually occur loss, offset against the related provision for impairment.--Available for sale financial assetsIf there is objective evidence that an impairment of available for sale financial assets occurs, even though the financial asset has not been derecognised, the cumulative loss of decrease of the faire value originally recorded in the owner's equity should be transferred out and charged into the current profit and loss. The cumulative loss is the initial acquisition cost of available for sale financial assets, deducting the fair value of the withdrawing principal and amortization amount and impairment loss as well as net impairment amount originally charged into the profit or loss. Recognition and provision for bad debts of accounts receivableIf there is objective evidence that receivables are impaired at the end of this period, the carrying value will be written down to its present value of estimated future cash flows, and the amount of reduction is recognized as impairment loss and is recognized in the current profit or loss. Present value of estimated future cash flows is determined through future cash flows (excluding credit losses that have not been incurred) discounted at the original effective interest rate, taking into account the value of related collateral (less estimated disposal costs, etc.). Original effective interest rate is the actual interest rate when the receivables are recognized initially. The estimated future cash flows of short-term receivables have small difference from the present value, and the estimated future cash flows are not discounted in determining the related impairment loss.The significant single receivables are separately carried out impairment test at the end of this period, and if there is objective evidence that the impairment has occurred, based on the difference of the present value of future cash flows less than the book value, the impairment loss is recognized and the provision of bad debts is done. The significant single amount refers to top five receivable balances or the sum of payments accounting for more than 10% of receivable balances. If there is objective evidence that the individual non-significant receivables impairment has occurred, separate impairment test is done, the impairment loss is recognized and the provision for bad debts is done; other individual non-significant receivables and receivables not impaired after separate test are together divided into several combinations for impairment testing with aging as the similar credit risk characteristics, to determine the impairment loss and do provision for bad debts.In addition to separate provision for impairment of receivables, the company is based on the actual loss rate of receivable portfolio with the same or similar to the previous year and aging as the similar credit risk characteristics, and combines the current situation to determine the ratio ofFixed assets and depreciation accounting methodRecognition criteria of fixed assets: fixed assets refer to tangible assets held for the purpose of producing commodities, providing services, renting or business management with useful lives exceeding one accounting year and high unit value.Classification of fixed assets: buildings and constructions, machinery equipment, transport equipment and office equipment.Fixed assets pricing and depreciation method: the fixed assets is priced based on actual cost and depreciated in a straight-line method. The estimated useful lives, estimated residual rate andreporting period, and if the market continuing to fall or technological obsolescence, damage, long-term idle and other reasons result in fixed assets recoverable amount lower than its book value, in accordance with the difference provision for impairment of fixed assets, the impairment loss is recognized in fixed assets and can not be reversed in a subsequent accounting period. The recoverable amount is recognized based on the fair value of the assets deducting the net amount after disposal expenses and the present value of cash flows of the estimated future assets. The present value of the future cash flows of the asset is determined in accordance with the resulting estimated future cash flows in the process of continuous use and final disposal to select its appropriate discount rate and the amount of the discount.Accounting method of construction in progressThe construction in progress is priced on the actual cost, to temporarily transfer to fixed assets when reaching the intended use state in accordance with the project budget and the actual cost of the project, and to adjust the book value of fixed assets according to the actual cost after handling final settlement of accounts. Acquisition, construction or production of assets eligible for capitalization borrowed specifically or the interest on general borrowing costs and auxiliary expenses of specific borrowings occurred can be included in the cost of capital assets and subsequently recognized in the current profit or loss before the acquisition, construction or production of the qualifying asset reaches the intended use state or the sale state.Impairment of construction in progress: the Company conducts a comprehensive inspection of construction in progress at the end of the reporting period; if the construction in process is stopped for long time and will not be constructed in the next three years and the construction in progress brings great uncertainty to the economic benefits of enterprises due to backward performance or techniques and the construction in progress occurs impairment, the balance of recoverable amount of single construction in progress lower than the book value of construction in progress is for impairment provisions of construction in progress. Impairment loss on the construction in progress shall not be reversed in subsequent accounting periods once recognized.The pricing and amortizing of intangible assetsPricing of the intangible assets---The cost of outsourcing intangible assets shall be priced based on the actual expenditure directly attributable to intangible assets for the expected purpose.--- Expenditure on internal research and development projects is charged into the current profit or loss, and expense in the development stage can be recognized as intangible costs if meeting the criteria for capitalization.--- Intangible assets of investment is in accordance with the agreed value of the investment contract or agreement as costs, excluding not fair agreed value of the contract or agreement.--- Intangible assets of the debtor obtained in the non-cash asset cover debt method can be accepted; if the receivable creditor’s right is changed into intangible assets, then record according to the fair value of intangible assets.--- For non-monetary transaction intangible assets, the fair value and related taxes payable of non-monetary assets should be the accounting cost.Amortization of intangible assets: as for the intangible assets with limited service life, it is amortized by straight-line method when it is available for use within the service period. As for unforeseeable period of intangible assets bringing future economic benefits to the company, it is regarded as intangible assets with uncertain service life, and intangible assets with uncertain service life can not be amortized. The Company’s intangible assets include land use rights, forest land use rights and the production and marketing information management software. The land use rights are amortized averagely in accordance with 50 years of service life, forest land use rights are amortized averagely in accordance with 30 years of service life, and the production and marketing information management software are amortized averagely in accordance with 5 years of service life.Expenditures arising from development phase on internal research and development projects can be recognized as intangible assets when satisfying all of the following conditions: (1) there is technical feasibility of completing the intangible assets so that they will be available for use or sale;(2) there is intention to complete and use or sell the intangible assets; (3) the method that the intangible assets generate economic benefits, including existence of a market for products produced by the intangible assets or for the intangible assets themselves, shall be proved. Or, if to be used internally, the usefulness of the intangible assets shall be proved; (4) adequate technical, financial, and other resources are available to complete the development of intangible assets, and the Company has the ability to use or sell the intangible assets; (5) the expenditures arising from development phase of the intangible assets can be measured reliably.Impairment of intangible assets: the Company conducts a comprehensive inspection on intangible assets at the end of the reporting period. If the intangible assets have been replaced by other new technologies so as to seriously affect its capacity to create economic benefits for the enterprise, the market value of certain intangible assets sharply fall and is not expected to recover in the remaining amortization period, certain intangible asset has exceeded the legal time limit but still has some value in use as well as the intangible asset impairment has occurred, the provision for impairment is done according to the difference between the individual estimated recoverable amount and the book value. Impairment loss on the intangible asset shall not be reversed in subsequent accounting periods once recognized.Accounting method of capitalization of borrowing costsBorrowing costs that are directly attributable to the acquisition, construction or production of qualifying assets for capitalization should be charged into the relevant costs of assets and therefore should be capitalized. Borrowing costs incurred after qualifying assets for capitalization reachesthe estimated use state are charged to profit or loss in the current period. Other borrowing costs are recognized as expenses based on the accrual and are charged to profit or loss in the current period. Capitalization of borrowing costs should meet the following conditions: expenditures are being incurred, which comprise disbursements incurred in the form of payments of cash, transfer of non-monetary assets or assumption of interest-bearing debts for the acquisition, construction or production of qualifying assets for capitalization; borrowing costs are being incurred; purchase, construction or manufacturing activities that are necessary to prepare the assets for their intended use or sale are in progress.Capitalization amount of borrowing interest: the borrowing interest incurred from the acquisition, construction or production of assets eligible for capitalization borrowed specifically or generally should be determined the capitalization amount according to the following method before the acquisition, construction or production of a qualifying asset reaching its intended use or sale state: ---Where funds are borrowed specifically for purchase, construction or manufacturing of assets eligible for capitalization, costs eligible for capitalization are the actual interest costs incurred in current period less the interest income of unused borrowing funds deposited in the bank or any income earned on the temporary investment of such borrowings.---Where funds allocated for purchase, construction or manufacturing of assets eligible for capitalization are part of a general pool, the eligible capitalization interest amounts are determined by multiplying a capitalization rate of general borrowing by the weighted average of accumulated capital expenditures over those on specific borrowings. The capitalization rate will be determined based on the weighted average rate of the borrowing costs applicable to the general pool. Suspension for capitalization: Capitalization of borrowing costs should be suspended during periods in which purchase, construction or manufacturing of assets eligible for capitalization is interrupted abnormally with the interruption time exceeding three months continuously. Borrowing costs incurred during the interruption should be charged to profit or loss for the current period, and should continue to be capitalized when purchase, construction or manufacturing of the relevant assets resumes. If the interruption is the necessary procedure to prepare the assets purchased, constructed or manufactured eligible for capitalization for their intended use or sale, the borrowing costs should continue to be capitalized.Recognition criteria and measurement method of estimated liabilitiesRecognition criteria of estimated liabilities: when the external security, pending litigation or arbitration, product quality assurance, layoffs, loss of contracts, restructuring obligations, fixed asset retirement obligations and other pertinent business meet the following conditions, it can be recognized as the liability: (1) the obligation is a present obligation of the Company; (2)it is probable that settlement of such an obligation will result in the economic benefit to flow out from the Company; (3) the amount of the obligation can be measured reliably.Measurement method of estimated liabilities: The Company’s estimated liabilities shall be initially measured at the best estimates of the necessary expenditures for the fulfillment of the present obligations. To determine the best estimates, the Company shall take into full account the risks, uncertainties, time value of money, and other factors relating to the contingencies. If the time value of money is significant, the best estimates shall be determined after discounting the relevant future cash outflows. If there is a continuous range for the necessary expenses, and probabilities of occurrence of all the outcomes within this range are equal, the best estimate shall be determined at the average amount within the range. The best estimates shall be determined as follows in other circumstances: (1) if the contingency involves a single item, the best estimate shall be determined at the most likely outcome; (2) if the contingency involves two or more items, the best estimate。

中国注册会计师审计准则第1501号——对财务报表形成审计意见和出具审计报告(2010年修订)

中国注册会计师审计准则第1501号——对财务报表形成审计意见和出具审计报告(2010年修订)文章属性•【制定机关】财政部•【公布日期】2010.11.01•【文号】财会[2010]21号•【施行日期】2012.01.01•【效力等级】部门规范性文件•【时效性】失效•【主题分类】会计正文中国注册会计师审计准则第1501号--对财务报表形成审计意见和出具审计报告(财会[2010]21号财政部2010年11月1日修订)第一章总则第一条为了规范注册会计师对财务报表形成审计意见,以及作为财务报表审计结果出具的审计报告的格式和内容,制定本准则。

第二条《中国注册会计师审计准则第1502号--在审计报告中发表非无保留意见》和《中国注册会计师审计准则第1503号--在审计报告中增加强调事项段和其他事项段》规定了注册会计师在审计报告中发表非无保留意见或者增加强调事项段或其他事项段时,审计报告的格式和内容如何受到影响。

第三条本准则建立在注册会计师执行整套通用目的财务报表审计业务的基础上。

《中国注册会计师审计准则第1601号--对按照特殊目的编制基础编制的财务报表审计的特殊考虑》,规定了注册会计师对按照特殊目的编制基础编制的财务报表审计的特殊考虑。

《中国注册会计师审计准则第1603号--对单一财务报表和财务报表特定要素审计的特殊考虑》,规定了注册会计师对单一财务报表或财务报表特定要素、账户或项目审计的特殊考虑。

第四条本准则要求注册会计师保持审计报告的一致性。

在按照中国注册会计师审计准则执行了审计工作的情况下,注册会计师保持审计报告的一致性,将有助于使用者更容易识别已按照中国注册会计师审计准则执行的审计业务,从而增强审计报告的可信性,同时有助于使用者理解以及识别发生的异常情况。

第二章定义第五条本准则所称财务报表,是指整套通用目的财务报表,包括相关附注。

相关附注通常包括重要会计政策概要和其他解释性信息。

适用的财务报告编制基础的规定决定了财务报表的形式和内容,以及整套财务报表的构成。

基本准则 General Standard

5 6 7பைடு நூலகம்

ISA 230R ISA 240 ISA 250

8 9 10 11

ISA 260

Effective for audits of financial statements for periods beginning on or after December 15, 2004 n/a Effective for audits of financial statements for periods beginning on or after December 15, 2004 Effective for audits of financial statements for periods beginning on or after December 15, 2004

3 4

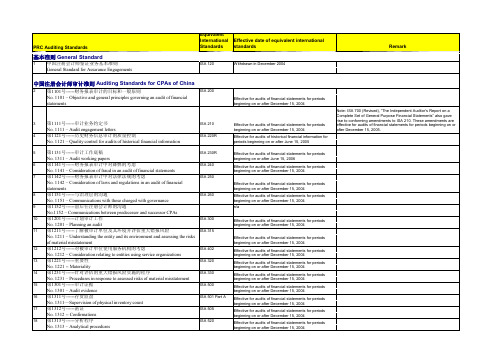

第1111号------审计业务约定书 No. 1111 – Audit engagement letters 第1121号------历史财务信息审计的质量控制 No. 1121 – Quality control for audits of historical financial information 第1131号------审计工作底稿 No. 1311 – Audit working papers 第1141号------财务报表审计中对舞弊的考虑 No. 1141 – Consideration of fraud in an audit of financial statements 第1142号------财务报表审计中对法律法规的考虑 No. 1142 – Consideration of laws and regulations in an audit of financial statements 第1151号------与治理层的沟通 No. 1151 – Communications with those charged with governance 第1152号------前后任注册会计师的沟通 No.1152 – Communications between predecessor and successor CPAs 第1201号------计划审计工作 No. 1201 – Planning an audit 第1211号------了解被审计单位及其环境并评估重大错报风险 No. 1211 – Understanding the entity and its environment and assessing the risks of material misstatement 第1212号------对被审计单位使用服务机构的考虑 No. 1212 – Consideration relating to entities using service organizations 第1221号------重要性 No. 1221 -- Materiality 第1231号------针对评估的重大错报风险实施的程序 No. 1231 – Procedures in response to assessed risks of material misstatement 第1301号------审计证据 No. 1301 – Audit evidence 第1311号------存货监盘 No. 1311—Supervision of physical inventory count 第1312号------函证 No. 1312 -- Confirmations 第1313号------分析程序 No. 1313 – Analytical procedures

国际审计准则与中国2010审计准则的主要差异修改版

国际审计准则与中国2010审计准则的主要差异我国注册会计师审计准则与国际审计准则的差异主要集中在以下四个方面:1.准则体系:多3 个准则,《中国注册会计师鉴证业务基本准则》、《中国注册会计师审计准则第1153 号——前任注册会计师和后任注册会计师的沟通》、《中国注册会计师审计准则第1602 号——验资》。

关于鉴证业务基本准则IAASB 将其放在准则序言部分加以强调的,我国注册会计师审计准则将则其单独列示。

鉴证业务基本准则统驭审计准则、审阅准则和其他鉴证业务准则,该准则规定了鉴证业务的定义和目标、业务承接、鉴证业务的三方(注册会计师、责任方、预期使用者)关系、鉴证对象、标准、证据、鉴证报告等内容。

2.未加区分审计准则与审计实务公告IAASB 将国际审计准则与国际审计实务公告区分,在对历史财务信息的审计和检查的规范中分别列示。

我国注册会计师审计准则未将审计准则与实务公告加以区分,而是将其并入准则体系中。

把以下六个国际审计实务公告“IAPS 1000银行间函证程序,IAPS 1004银行监管机构与银行外部审计师的关系,IAPS 1006银行财务报表审计,IAPS 1010财务报表审计中对环境的考虑,IAPS 1012衍生金融工具审计,IAPS 1013电子商务对财务报表审计的影响”归为《中国注册会计师审计准则第1612 号——银行间函证程序》,《中国注册会计师审计准则第1613号——与银行监管机构的关系》,《中国注册会计师审计准则第1611 号——商业银行财务报表审计》,《中国注册会计师审计准则第1631号——财务报表审计中对环境事项的考虑》,《中国注册会计师审计准则第1632号——衍生金融工具的审计》,《中国注册会计师审计准则第1633号——电子商务对财务报表审计的影响》。

3.部分准则存在差异,《审计报告》。

我国报告准则与国际报告准则的区别:①报告名称差异:我国审计报告均称为“审计报告”未加“独立”二字;国际审计报告均称为“独立审计报告”,在标题中增加“独立”一词,强调审计师的“独立性”。

《中国注册会计师审计准则第1501号—对财务报表形成审计意见和出具审计报告

《中国注册会计师审计准则第1501号——对财务报表形成审计意见和出具审计报告》应用指南(2010年11月1日修订)一、被审计单位会计实务的质量(参见本准则第十五条)1.管理层需要对财务报表中的金额和披露作出大量判断。

2.《中国注册会计师审计准则第1151号—与治理层的沟通》及其应用指南包含对会计实务质量方面的讨论。

在考虑被审计单位会计实务的质量时,注册会计师可能注意到管理层判断中可能存在的偏向。

注册会计师可能认为缺乏中立性产生的累积影响,连同未更正错报的影响,导致财务报表整体存在重大错报。

管理层缺乏中立性可能影响注册会计师对财务报表整体是否存在重大错报的评价。

缺乏中立性的迹象包括下列情形:(1)管理层对注册会计师在审计期间提请其注意的错报进行选择性更正。

例如,如果更正某一错报将增加盖利,则对该错报予以更正,反之如果更正某一错报将减少盈利,则对该错报不予更正;(2)管理层在作出会计估计时可能存在偏向。

3.《中国注册会汁师审计准则第1321号—审计会计估计(包括公允价值会计估计)和相关披露》涉及管理层在作出会计估计时可能存在的偏向。

在得出某项会计估计是否合理的结论时,可能存在管理层偏向的迹象本身并不构成错报。

然而,这些迹象可能影响注册会计师对财务报表整体是否不存在重大错报的评价。

二、披露重大交易和事项对财务报表所传递信息的影响(参见本准则第十六条第(五)项)4.按照通用目的编制基础编制的财务报表通常反映被审计单位的财务状况、经营成果和现金流量。

对于通用目的财务报表,注册会计师需要评价财务报表是否作出充分披露,以使财务报表预期使用者能够理解重大交易和事项对被审计单位财务状况、经营成果和现金流量的影响。

三、对适用的财务报告编制基础的说明(参见本准则第十八条)5.如《<中国注册会计师审计准则第1101号—注册会计师的总体目标和审计工作的基本要求>应用指南》所述,管理层和治理层(如适用)编制的财务报表需要恰当说明适用的财务报告编制基础。

2019年新版标准审计报告英文版

REPORT OF AUDITORS~~~~(2019)Audit No.000To the shareholders of~~~~Co.,Ltd.:Ⅰ.Audit opinionWe have audited the accompanying financial statements of~~~~Co.,Ltd. (hereinafter referred to as"the Company"),which comprise the balance sheet as at December31,2018,the income statement for the year then ended,cash flow statement,Statement of changes in owner’s equity and other relevant foot-notes to financial statements.In our opinion,the attached financial statements are prepared,in all material respects,in accordance with the Accounting Standards for Enterprises and present fairly the financial position of the Company as of December31,2018,and operating results and cash flow for the year then ended.Ⅱ.Basis for audit opinionWe conducted our audit in accordance with the Auditing Standards for Certified Public Accountants in China.Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report.According to the Code of Ethics for Chinese CPA,we are independent of the Company in accordance with the Code of Ethics for Chinese CPA and we have fulfilled our other ethical responsibilities in accordance with these requirements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.Ⅲ.Responsibilities of Management and Those Charged with Governance for the Financial StatementsThe Company's management is responsible for preparing the financial statements in accordance with the requirements of Accounting Standards for Small Business Enterprises to achieve a fair presentation,and for designing,implementing and maintaining internal control that is necessary to ensure that the financial statements are free from material misstatements,whether due to frauds or errors.In preparing the financial statements,management of the Company is responsible for assessing the Company's ability to continue as a going concern,disclosing matters related to going concern,if applicable,and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations,or has no realistic alternative but to do so.Those charged with governance are responsible for overseeing the Company's financial reporting process.Ⅳ.Auditor's Responsibilities for the Audit of the Financial StatementsOur objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement,whether due to fraud or error,and to issue an auditor's report that includes our opinion.Reasonable assurance is a high level of assurance,but is not a guarantee that an audit conducted in accordance with the audit standards will always detect a material misstatement when it exists.Misstatements can arise from fraud or error and are considered material,if individually or in the aggregate,they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.As part of an audit in accordance with the audit standards,we exercise professional judgment and maintain professional scepticism throughout the audit.We also:(1)Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error,design and perform audit procedures responsive to those risks,and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error,as fraud may involve collusion,forgery,omissions,misrepresentations,or the override of internal control.(2)Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances,but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.(3)Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management of the Company.(4)Conclude on the appropriateness of using the going concern assumption by the management of the Company,and conclude,based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company's ability to continue as a going concern.If we conclude that a material uncertainty exists,we are required to draw attention in our auditor's report to the related disclosures in the financial statements,or if such disclosures are inadequate,to not express clean opinion.Our conclusions are based on the audit evidence obtained up to the date of our auditor's report.However, future events or conditions may cause the Company to cease to continue as a going concern.(5)Evaluate the overall presentation,structure and content of the financialstatements,including the disclosures,and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation. We communicate with those charged with governance regarding,among other matters, the planned scope and timing of the audit and significant audit matters,including any significant deficiencies in internal control that we identify during our audit.~~~~~CPAs Co.,Ltd.Certified Public Accountant:Tianjin,P.R.China Certified Public Accountant:April9,2019。

中英文审计报告-五种审计意见(推荐5篇)

中英文审计报告-五种审计意见(推荐5篇)第一篇:中英文审计报告-五种审计意见审计报告-标准无保留意见Auditors’ Report 安明(2007)审字the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control.An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.我们相信,我们获取的审计证据是充分的、适当的,为发表审计意见提供了基础。

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.三、审计意见我们认为,上述财务报表已经按照企业会计准则和《企业会计制度》的规定编制,在所有重大方面公允反映了贵集团和贵公司2006年12月31日的财务状况以及2006年度的经营成果和现金流量。

国际审计中文准则对应的英文准则- 免费版

国际审计中文准则对应的英文准则- 免费版ISA 200“独立审计师的总体目标及根据国际审计准则执行审计” 中国注册会计师审计准则第1101号——注册会计师的总体目标和审计工作的基本要求(2010年11月1日修订) 第一章总则第一条为了规范注册会计师按照中国注册会计师审计准则执行财务报表审计工作,确立注册会计师的总体目标,明确注册会计师为实现总体目标而需要执行审计工作的性质和范围,以及在执行财务报表审计业务时承担的责任,制定本准则。

第二条审计准则适用于注册会计师执行财务报表审计业务。

当执行其他历史财务信息审计业务时,注册会计师可以根据具体情况遵守适用的相关审计准则,以满足此类业务的要求。

第二章定义第三条注册会计师,是指取得注册会计师证书并在会计师事务所执业的人员,通常是指项目合伙人或项目组其他成员,有时也指其所在的会计师事务所。

当审计准则明确指出应由项目合伙人遵守的规定或承担的责任时,使用“项目合伙人”而非“注册会计师”的称谓。

第四条本准则所称财务报表,是指依据某一财务报告编制基础对被审计单位历史财务信息作出的结构性表述,包括相关附注,旨在反映某一时点的经济资源或义务或者某一时期经济资源或义务的变化。

相关附注通常包括重要会计政策概要和其他解释性信息。

财务报表通常是指整套财务报表,有时也指单一财务报表。

整套财务报表的构成应当根据适用的财务报告编制基础的规定确定。

第五条历史财务信息,是指以财务术语表述的某一特定实体的信息,这些信息主要来自特定实体的会计系统,反映了过去一段时间内发生的经济事项,或者过去某一时点的经济状况或情况。

第六条适用的财务报告编制基础,是指法律法规要求采用的财务报告编制基础;或者管理层和治理层(如适用)在编制财务报表时,就被审计单位性质和财务报表目标而言,采用的可接受的财务报告编著基础。

财务报告编制基础分为通用目的编制基础和特殊目的编制基础。

通用目的编制基础,是指旨在满足广大财务报表使用者共同的财务信息需求的财务报告编制基础,主要是指会计准则和会计制度。

英文审计报告(带中文翻译)

英文审计报告(带中文翻译)(一)规范部门预算管理,强化预算执行约束。

按照中央关于改进工作作风,密切联系群众的八项规定,进一步强化部门预算管理,制定和完善基本支出、项目支出等各项支出标准,严格按项目和进度执行预算,增强预算的约束力和严肃性。

进一步扩大部门预算决算公开范围,细化公开内容。

各主管部门和核算中心要加强对下属单位的指导、管理和监督,加强内部控制和内审制度,切实提高预算单位财政财务收支管理水平。

致xx公司股东(在xx注册成立的股份有限公司)本审计师(以下简称「我们」)已完成审核刊于第58页至第108页根据香港公认会计原则编制的财务报表。

董事及审计师各自的责任贵公司的董事负责编制真实与公平的财务报表。

在编制该等真实与公平的财务报表时,董事必须选取并贯彻采用合适的会计政策。

我们的责任乃根据我们审核工作的结果,对该等财务报表作出独立意见,并仅向贵公司全体股东报告我们的结论,及不作其它用途。

我们并不就本报告的内容向任何其它人士负上责任或承担法律责任。

意见的基础我们乃按香港会计师公会所颁布的审计准则进行审核工作。

审核范围包括以抽查方式查核与财务报表所载数额及披露事项有关的凭证,亦包括评估董事于编制该等财务报表时所作的重大估计及判断、所厘定的会计政策是否适合贵公司的具体情况以及有否贯彻应用并充分披露该等会计政策。

贵公司于1998年XX月XX日领取XXXXXXXXXXXX号企业法人营业执照,注册资本275万元,法人代表XXX,经营范围:销售通信器材、承揽通信工程设计、施工、通信设备维修、汽车维修,物业管理;餐饮娱乐、职业中介、通信信息服务;室内装饰、工业与民用建筑工程。

简式审计报告,顾名思义,是内容和格式简明扼要的审计报告,包括注册会计师对会计报表审计后出具的各类审计意见的审计报告。

这类审计报告记载的内容是法令或审计准则规定的,而且用以表述的文字是众皆通晓的,因此,要求它必须简明扼要,并具有大体的标准格式。