KKR 杠杆收购案例分析

经典LBO案例分析PPT课件(36页)

(百万US$) 资产

现金 应收帐款净值 存货 其他流动资产

固定资产净值

商誉和其他无形资产

已停止运营业务的净资产净值

其他资产

1986

827 1,675 2,620

273

5,343

4,603

716

644

15,766 4.40% 2,304

489 1,816

1,081 128

1,209 7.67%

3.13 -

1.14 36.42% 20.40

6.52 281.5 0.80

2.90 -7.35%

1.22 42.07% 24.30

8.38 283.2 0.70

4.11 41.72%

1.30

31.63% 28.80

1984年卖出 – Burmah Oil Company美国分部业务: 1976年购买, 1984年卖出

KKR 杠杆收购 RJR Nabisco ---- RJR Nabisco 公司1982-1987经营业绩概况

(百万US$) 业务状况

营业收入 年增长率

营业利润 利息费用 税前收益

持续经营业务净利润 非持续经营业务净利润

– 总购买价: US$170亿 – 比其股票市场价格US$55.875高出 34%

KKR 杠杆收购 RJR Nabisco ----KKR 于4天后宣布其LBO收购要约

• 时间: 1988年10月24日

– 在管理团队宣布其MBO要约的4天后

• 竞标者之二: Kohlberg, Kravis, Roberts & Co. (KKR)

经典LBO案例分析 KKR 杠杆购并 RJR NABISCO

KKR 杠杆收购 RJR Nabisco ----KKR和RJR Nabisco概况

KKR 公司收购案例分析 ppt课件

114 122 132 144 891 2 2 6 8

172 226 242 262 286 98342

折旧

449 475 475 475 475

资本性 支出 522 512 525 538 551

--

营运资

22

本变 0 7

动

3 5 200 225 250

• KRR为离开的雇员提供福利,而管理层在员工福 利的保障方面不到位,激怒了股东和员工

• 管理层没能通过重组证实它的证券的可靠性 • 管理层对公司业务比较熟悉,富有行业热情。而

KKR对公司业务不了解,缺乏行业热情。

KKR 公司收购所得税 税后利

润

198 199 199 199 199 90123

=75%x14.08%+25%x13.5%x(1-34%) =12.79% CV=FCFF/(WACC-g)=2536*(1+3%)/(12.79%-3%)=26681.1 折现后的CV=14616.75 百万美元

KKR 公司收购案例分析

• 公司总价值=前五年价值+增长期连续价值 =16058.21+ 14616.75 =30674.95 百万美元

• KKR本身提供20亿美元(其中15亿美元作 为股本),另外提供41亿美元作优先股, 18亿美元作可转债券。

• 接收RJR所欠的48亿美元外债

KKR 公司收购案例分析

• KKR 保持公司现有业务的完整性,保留所有的烟 草业务和绝大部分的食品业务。而管理层只保留 烟草业务,卖出食品业务

• KRR 给股东提供更多的股份,KRR提供25%,管 理层只给15%

减公司债务48亿美元 =权益价值=259亿美元 除以流通股本2.29亿股 = 每股内在价值=113元/股 比出价109元/股高4元/股

杠杆收购运作原理(一)

杠杆收购运作原理(一)概述在投资领域,杠杆收购可以被视为是一种获得资本收益的策略。

这种策略的核心在于使用借来的资本和公司现有的资本,来购买更多股票,最终实现收益。

那么,杠杆收购究竟是什么,它的原理是什么呢?下面来逐步解释。

什么是杠杆收购?杠杆收购是一种收购资产的策略。

这种策略中,投资者发行债券来借贷资本,用这些资本来购买目标企业的控股权。

另外,杠杆收购的过程中,收购方可以将目标公司的资产用作抵押品,以获得更多的融资。

同时,购买者通过削减目标公司的开支和优化资产组合以回报债券持有人。

在这种情况下,杠杆收购的原则在于,预期股票价格在收购之后上涨,从而为投资者带来更高的收益。

杠杆收购的原理是什么?使用借贷资本来购买更多股票的策略称为杠杆化。

投资者需要支付有利息的贷款,这些贷款使得股票价格上涨时将有更高的回报。

然而,如果股票价格下跌,那么投资者将不得不在一定时间内偿还这些贷款,否则会面临违约或破产的风险。

更深入地理解,以下是杠杆收购的原理和过程:1.公司发行债券来筹集资金。

2.使用这些资本来发起对一个或多个公司的收购。

3.通过目标公司的债权人抵押目标公司的资产,来筹集更多资金。

4.利用这些资金购买剩余的股份。

5.收购完成后,采取更高效管理策略,削减开支,并优化资产。

6.提高股票价格,以增加投资者的回报。

然而,杠杆收购风险较大,并不保证成功。

如果没有足够的资本回报债券持有人和利润,则会导致债务违约和破产。

结语总的来说,杠杆收购作为一种资本收益策略,需要投资者谨慎考虑其风险和回报。

在实际投资中,投资者需要充分了解目标公司的财务状况,以及杠杆收购的原理和规则,才能做出明智的投资决策。

杠杆收购的利弊在进行杠杆收购之前,需要充分了解其利弊。

以下是其主要利弊:利1.增加杠杆比率。

杠杆收购可以通过增加杠杆比率,来提升资本回报率。

投资组合杠杆比率越高,投资者的利润越高。

2.提高未来现金流量。

通过财务重组和资产优化,某些公司可以提高未来现金流量。

杠杆收购融资风险分析——基于KKR收购RJR NABISCO的实证分析

购 资本 结构 调整 模式 、杠杆 收购 控股公 司模 式和 策略 性杠杆 收购 模 式 。对 于财务 风险 来源 。戈俏梅 ( 0 2) 2 0 对杠杆 收购 高 负债 的 弊端进 行 了分析 。 指 出杠杆 收 购的成 功 与否取 决于企 业能 否有 还

19 9 0年到 1 9 年都 有一个 明显 的上 升 ,从 1 9 91 9 2年后 又趋 于平 稳 。这说 明收 购后 ,企业 在 1 9 、1 9 年 的经 营风 险很 大。企 0 1 9 9

内。

二是 财 务杠杆 ( F ) 析 。杠杆 收购 企 业的融 资风 险主 要 DL 分 体 现在 财务 杠 杆 ( F 上 。是指 每股 盈余 ( P 随息 税前 利 D L) E S)

润 ( BT)的变 动而 变动 的幅度 。 EI

D L ( P / P / △E I E I = B T E I I F = △E SE S) ( B T BT) E I / /( B T 】 —

把理 论和 实证 相结 合 。

额的 固定 利息 支出 时 ,企 业每股 盈余 下降 得更快 ,甚 至会 引起企

第一 ,财务 风 险分 析。

一

是经营杠杆分析。经营杠杆 ( OL) D 指息税前利润 ( BT) EI

变动率 相 当于 业务 量 【 S)变动率 的倍 数。

D = (△E I E I / △S S) T m ̄ BT OL B T B T) ( / = c / I / E

融 资财 式 、杠 杆收

营风 险越大 。 经计算 可得 ,收 购之 后 1 8 、 19 9 9 9 0年 的 D 分 别 为一 OL 2和

22 -,息税 前利 润在 1 9 9 0和 19 年分 别较 上一 年上 涨 1 .%和 91 29 1.% 。可 以看 出不 论 是 息 税 前利 润 的 变 化 幅 度还 是 D 70 OL 在

并购案例KKR收购RJR ppt课件

• 你所经历的课堂,是讲座式还是讨论式? • 教师的教鞭 • “不怕太阳晒,也不怕那风雨狂,只怕先生骂我

笨,没有学问无颜见爹娘 ……”

• “太阳当空照,花儿对我笑,小鸟说早早早……”

一、并购双方简介

KKR成立于

1976,是以收购、 重整企业为主营业

一、并购双方简介

——从其他行业引进管理者,其没有烟草业的从业经验

七、并购整合及并购中出现的问题

2.市场经营风险

1989年3月RJR停止了总理牌香烟的生产,随后公司进行了裁员,雇工人数减 少到2300人。在新管理人的领导下,公司改进了设备,提高了生产效率,同 时又大幅度削减了成本,使得公司烟草利润在1990年的上半年增加了46%。 但是其用烟草带来的现金清偿垃圾债券时,雷诺兹的竞争对手菲利普•莫里斯 却增加销售实力,降低了烟草价格。RJR的烟草市场在1989年萎缩了7%~ 8%。

七、并购整合及并购中出现的问题

3.财务风险

——KKR在1990春面临新的财务困境

(1)US$12亿的过桥贷款将于1991年2月到期; (2)US$70亿PIK债券必须于1991年4月28日前重新设定其固定利率。

——KKR采取行动进行债务重组(1990年7月16日)

1.增发普通股 2.PIK债券转股 3.以普通股或可转款优先股和少量现金交换PIK债券 4.申请US$22.5亿银行信贷额度以偿还US$12亿过桥贷款及US$10亿的浮息

RJR: 雷诺烟草公司,美国第二大烟草公司 Nabisco :美国第一大饼干公司 1985年,RJR 实行多元化经营, 购买 Nabisco (US$49亿) 后,

成立RJR Nabisco。

1988年成为LBO/MBO 的目标。

杠杆收购与管理层收购理论

杠杆收购与管理层收购理论杠杆收购是指以较低的现金投入,借助较高的债务负担,收购目标公司的一种并购方式。

而管理层收购是指公司的管理层将公司自有资金与第三方融资相结合,以购买公司的一部分股权,从而获得对公司的控制权。

本文将从理论角度探讨杠杆收购和管理层收购的概念、优势与风险,以及实施过程中的注意事项,旨在进一步了解并评价这两种并购方式的可行性和适用性。

首先,杠杆收购和管理层收购都是一种改变公司股权结构和所有权关系的方式。

在杠杆收购中,收购方不需要支付全部现金,而是以自有资金和债务的结合方式,支付一部分现金,向被收购方购买股权;而在管理层收购中,公司的管理层则通过自己的资金和第三方融资的方式,购买公司的一部分股权。

这两种方式都可以有效地改变公司的控制权和经营权,为收购方或管理层提供主导公司经营决策的机会。

其次,杠杆收购和管理层收购都具有一定的优势。

一方面,这两种收购方式可以降低收购方的资金压力,从而减轻其负债风险。

尤其是在杠杆收购中,收购方可以通过借入更多的债务资本来减少自有资金的使用,从而降低收购成本。

另一方面,这些收购方式还可以激励管理层更好地履行公司经营责任,提高公司的经营效率。

管理层收购可以帮助公司聚焦于长期价值创造,因为管理层作为股东,有更强的动力去追求公司的盈利和增长。

然而,杠杆收购和管理层收购也存在一定的风险和不确定性。

首先,高额的债务负担往往使公司的财务状况更加脆弱,一旦市场环境变化或者企业经营不善,可能会导致还款能力下降,进而影响公司的信誉和经营活动。

其次,管理层收购需要管理层具备较高的资金实力和专业知识,否则可能面临操纵、侵占公司资源的风险。

再次,两种收购方式都需要对公司进行改组和重组,可能引发人员流动、职位调整、组织变迁等问题,对公司员工产生一定的不利影响。

在实施杠杆收购和管理层收购的过程中,还需要注意以下几个问题。

首先,必须对目标公司进行充分的尽职调查,从而了解其财务状况、经营状况和市场前景,评估收购的风险和收益。

杠杆收购(LBO)

引言概述:杠杆收购(LBO)是一种常见的企业并购方式,它使用借入的资金来购买目标公司的股权。

通过利用借贷杠杆,LBO可以实现较少的投入资金,并通过使用目标公司的自身现金流来偿还债务。

本文将详细介绍杠杆收购的概念、原理以及在实际操作中的注意事项。

正文内容:一、杠杆收购的概念和原理1.1 定义:杠杆收购是指通过大量借入资金来购买目标公司的股权,并利用目标公司的现金流偿还债务的一种并购方式。

1.2 原理:杠杆收购利用了目标公司的现金流来偿还债务,将股权购买成本降低至最低,从而提高了收购方的回报率。

二、杠杆收购的优势和风险2.1 优势:2.1.1 资本投入较低:利用借入资金购买股权,减少自有资金的投入。

2.1.2 提高回报率:通过降低购买成本,增加收益和现金流,从而提高回报率。

2.1.3 管理层激励:杠杆收购可以激励目标公司的管理层,通过股权激励计划提高业绩。

2.2 风险:2.2.1 债务负担过重:大量的借入资金可能会增加目标公司的债务压力。

2.2.2 目标公司经营风险:如果目标公司的业绩下滑,可能无法按时偿还债务。

2.2.3 财务杠杆效应:杠杆收购将目标公司的财务风险扩大化,一旦经济环境不利,可能导致财务危机。

三、杠杆收购的操作步骤3.1 选择目标公司:评估目标公司的价值、发展潜力和现金流情况,选择适合进行杠杆收购的目标。

3.2 筹集资金:与银行、投资基金等金融机构商谈借款、融资等筹资方式。

3.3 财务尽职调查:对目标公司的财务状况、业绩、合同等进行详细调查,评估风险和潜在收益。

3.4 股权交易和合同签署:与目标公司进行股权转让交易,签署相关合同和协议。

3.5 资金结算和整合:支付购买股权的款项,整合目标公司和实现预期的财务目标。

四、杠杆收购的实施要点4.1 借款结构的优化:灵活选择债务和股权的结构,以降低借款成本和风险。

4.2 资产负债管理:合理管理目标公司的资产负债结构,确保现金流可以按时偿还债务。

杠杆收购:KKR杠杆收购雷诺.纳贝斯克公司 Microsoft Word 文档

杠杆收购:KKR杠杆收购雷诺·纳贝斯克公司1思路导航及其他2杠杆收购的前因后果3解析雷诺.纳贝斯克公司4解析KKR杠杆收购雷诺.纳贝斯克的方案5解构KKR杠杆收购雷诺.纳贝斯克的经济理由1.思路导航及其他杠杆收购是一种复杂的资本市场运作过程,被视为高难度的“金融外科手术技术”。

经典的杠杆收购,其中包括三个方面的经济含义。

①如何针对不同的杠杆收购对象的现金流的预测构造一个合理有效的金融方案以完成其杠杆收购。

杠杆收购不仅是多种金融工具的综合使用,例如,可转债、优先股等,还是一个金融创新的过程。

②如何选择一个恰当的杠杆收购对象。

并不是任何一个企业皆适合杠杆收购,适合杠杆收购的对象一般具备足够的、稳定的现金流,并且资本市场低估其价值,还需具备高昂的代理成本等。

③杠杆收购之后对公司进行有效的重组,包括资产结构的重组、财务结构的优化等。

何谓一个完美的杠杆收购案例呢?KKR收购雷诺·纳贝斯克公司是杠杆收购技术的完美体现,具备了杠杆收购的一切合理因素。

本节以此为样本,分析杠杆收购的来龙去脉、经济功能、经济条件、获利途径和杠杆收购的进程。

声明:①本案例的目的是用来说明杠杆收购的经济动因、条件等问题,并不是着重说明杠杆收购的细节问题。

②由于材料来源的局限性,材料之中可能存在引述、说明和数据不当的地方,但是这并不重要,需要读者格外关注的是背后的金融原理和逻辑。

③本案例并不是用来评论某个公司的经营、管理或其他,而是分析决策背后的经济逻辑。

④案例中的评论是基于学术目的,而不是对公司的经营、管理和其他进行判断和说明。

⑤本案例的素材来源于有关材料。

思路导航2.杠杆收购的前因后果1杠杆收购的前身:鞋带收购杠杆收购起源于“鞋带收购”。

所谓“鞋带收购”(Bootstraps)是投资者收购目标公司的股权,通常将其转变为私人公司,并在交易中尽可能减少买方的资本投入,尽量使用债务,收购金额一般在几十万美元和几百万美元之间。

最大规模的杠杆收购——收购纳贝斯科

案例提要79最大规模的杠杆收购—收购纳贝斯克公司案迄今为止规模最大的杠杆收购是1988年发生的价值246亿美元的纳贝斯克收购案。

这个食品和烟草公司在一场精彩的收购战役中被收购公司KKR公司据为己有。

纳贝斯克公司(RJR Nabisco)是一家拥有骆驼牌香烟、奥利奥饼干等著名产品的烟草及消费品会司。

1988年因烟草产品的业绩不好,又由于1987年10月股市崩盘的影响,公司的股价一路下滑,当时每股只有40美元。

公司大股东都认为公司的价值被严重低估,可一时又拿不出好的解决办法。

公司总裁提出以52美元~ ~58美元的价格回购股票2 000万股,获得董事会同意,随后以53. 50美元的价格完成了回购计划。

但是,股价很快又跌回到45美元,使公司投入的11亿美元打了水漂。

以后又考虑了许多收购或被收购的方案,包括与菲利普·莫里斯公司合并的方案,但没有成功。

在这种情况下公司总裁约翰逊(F. Ross·Johnson)开始对多家投资银行一再建议他的对公司进行管理层收购的建议进行了认真的思考和实际的计算,开始考虑如果进行管理层收购需要支付多少现金、公司的价值有多少、公司的各项资产如果出售的话价格是多少,以及公司的业务特别是公司的烟草业务带来的现金流有多少。

在投资银行希尔森公司的全力支持下,他向董事会提出以他为首的7位公司高管要收购公司,他的出价是每股75美元。

这看起来像管理层收购,但超过80%的股份归投资银行希尔森公司和为收购融资的投资者所有,所有的融资都是投资银行负责筹集,就连管理层购买他们自己的股票份额的钱也由投资银行负责为他们融资。

从这两点看,这是典型的以投资银行为主的杠杆收购。

但是,与一般的杠杆收购不同,公司总裁约翰逊要求控制收购后的董事会对收购后的公司运作与重组有否决权,而一般的杠杆收购主导权全在投资银行手中。

之所以形成这种局面是因为约翰逊牢牢地控制着公司,没有他的同意,杠杆收购是无法启动的,因为董事会不会考虑约翰逊不支持或竭力反对的事情。

收购教父:KKR公司

收购教父:KKR公司收购案例分析KKR公司成立于1976年。

创始人是亨利·克拉维斯和表兄乔治·罗伯茨以及他们的导师杰罗姆·科尔博格。

公司名称正源于这三人姓氏的首字母。

杰罗姆·科尔博格于1987年退出,但公司仍然沿用KKR的名称。

公司总部位于纽约。

在加州门罗帕克、伦敦、巴黎、东京和中国香港设有分支机构。

截至2006年9月30日,KKR投下去的270亿美元资本已经创造了大约700亿美元的价值。

一、KKR发展历程克拉维斯、罗伯茨表兄弟在1970年代初一起进入了贝尔斯登的企业金融部。

在那里他们遇到了科尔博格。

他们能够熟练的利用借贷资金收购一些经营状况良好或者拥有优良资产的公司,以杠杆收购闻名世界。

杠杆收购所聚集的资金,大约有60%来自原商业银行的贷款,仅有10%左右来自收购人。

而剩下的30%最初大多来自于保险公司。

但他们的资金承诺往往需要等待几个月。

1970年代初由于股市下滑的原因,许多公司大量出售分公司。

最初没有人知道KKR是什么公司,但是到了1981年他们迎来了6笔生意为他们带来了财富。

科尔博格领先华尔街其他投资公司率先认识到,如果管理层拥有公司的股票,他们将会更主动有效的管理好公司。

随着时间的流逝,科尔博格的步步为营法逐渐改变。

他最初的观念是他和合作伙伴一定要在项目中自己进行投资。

更重要的是,要同收购的管理层以及他们的投资者一同获利。

科尔博格的最终目的就是要实现共同致富,所有人一起挣钱的多赢局面。

KKR可以通过友好合作成为管理层的盟友。

公司可以收取相应的佣金,但这只是用来承担挑选适当收购候选人的成本以及帮助合作伙伴度过不能套现的非常时期。

随着收购规模的增大,收取的佣金也随之增加。

无论投资者如何,公司都能够盈利。

在1980年代早期,KKR公司的许多长期投资还未赢利,公司的资金十分紧张,新的竞争对手已经出现。

到了1985年,越来越多的华尔街公司开始考虑开设或者扩大自己的杠杆收购部门。

RJR案例分析(含答案)

RJR Nabisco----LBO caseKKR集团,(Kohlberg Kravis Roberts & Co. L.P.,简称KKR),即“科尔伯格-克拉维斯”,是以收购、重组企业为主营业务的股权投资公司,成立于1965,是美国著名的LBO基金,尤其擅长管理层收购(MBO)。

RJR Nabisco(R.J. Reynolds Tobacco Company),美国雷诺烟草控股公司,世界第三大私营卷烟生产企业,是一家成立于1875年的烟草公司,于1985年收购食品公司Nabisco,在1969年和1984年之间还进行了一系列其他行业公司的收购与退出,涉及运输、石油、餐饮等行业。

主营业务是烟草和饼干。

一、MBO及LBO要约及战略部署1988年10月20日,以Edward A. Horrigan为核心的RJR Nabisco经营管理团队首先向RJR发出MBO收购要约,每股US$75,比其股票市场价格US$55.875高出34%,总购买价US$170亿。

MBO团队认为RJR的烟草和食品业务的股票价值均被低估,提出收购后卖出食品业务,保留烟草业务,从上市公司转化为非上市公司,以期使公司价值得到市场正确评估。

管理层决定总体U$112每股,包括U$84现金,U$24的PIK优先股;U$4的可转换优先股;1988年10月24日,著名LBO基金KKR发起挑战,宣布以每股US$90,总价US$207亿对RJR公司进行LB0收购,比管理团队出价高出20%。

KKR团队则主张保留所有的烟草业务和大部分食品业务,以较为完整的原公司结构转化为非上市公司。

总体U$109每股,包括U$81现金,U$18的PIK优先股,U$10的可转换优先股。

二、收购原因首先是资本运营的潜在回报。

竞标人认为股票市场低估了RJR Nabisco企业价值。

RJR Nabisco的现金流很强且稳定,可以利用更优的资本结构(提高财务杠杆)来节约税收,提高企业价值。

(完整word版)杠杆收购融资结构及效应分析

杠杆收购融资结构及效应分析杠杆收购(Leveraged buyout,LBO)源于20世纪60年代美国,是80年代全球第四次并购浪潮中最具影响的一种特殊并购模式,目前已成为全球金融不可或缺的基本工具。

杠杆收购作为一种金融创新工具,通过对最小自有资本以小博大、高风险、高收益、高技巧的资本运作实现最快速的企业扩张.杠杆收购促使垃圾债券、过桥贷款、私募基金、风险资本等金融工具的涌现和盛行,并通过改善公司治理结构、降低代理成本、提高资本效率等方式创造特殊的股东价值。

1988年的美国KKR公司并购总金额达250亿美元RJR纳贝斯克公司,更是有史以来规模最大、最具神话特色的杠杆收购案。

近年来,我国陆续颁布《证券法》、《企业债券管理条例》、《商业银行并购贷款风险管理指引》、《上市公司收购管理办法》等一系列法律法规,以拓宽企业融资渠道、解决股权分置问题、完善资本市场,为杠杆收购在我国的发展和有效运用建立法律基础、提供制度保障.不断涌现的上市公司并购、跨境并购及外资并购案,使得越来越多的中国企业不得不与国际行业巨擘展开激烈竞争,了解和掌握杠杆收购融资运作模式,具有非常深远的意义。

一、杠杆收购原理杠杆收购是指收购者以较少的自有资金为基础,从投资银行或其他金融机构筹集大量的资金进行收购活动,继而以被收购企业的资产或现金流来支持偿还债务的并购方式。

[1]杠杆收购实质上就是举债收购,即以债务资本为主要融资工具,运用财务杠杆加大负债比例,以较少自有资金筹集主要资金进行收购、重组的一种资本运作方式。

杠杆收购目前主要有三种方式:目标公司管理层参与的杠杆收购(管理层收购MBO)、无目标公司管理层参与的杠杆收购LBO、目标公司雇员参与的杠杆收购(员工持股计划ESOP)。

区别于一般并购,杠杆收购主要的特征有(1)高负债率。

收购公司通常以权益和债权作为主要并购资金来源,债权/权益资金比率通常在6:1~12:1之间,权益资金(或自有资金)在收购总价款中一般只占10%~15%。

并购基金的杠杆收购(管理层收购)模式分析

并购基金的杠杆收购(管理层收购)模式分析利用自有资金开展股权投资业务,这是PE最基本的投资模式。

在金融规则与产品相对成熟的市场,股权投资机构往往会通过结构化设计,放大投资杠杆,获得更高收益率。

并购基金,是PE中侧重于关注控股式收购的资金,其对杠杆收购的设计与应用,最具代表意义,我们以此为例,介绍PE利用杠杆的通常模式。

为使对该问题的理解更为直观,我们引入两个案例,之后对其交易规则做简要梳理。

1、KKR的管理层收购+杠杆收购介绍KKR是克拉维斯(Henry Kravis)和表兄罗伯茨(George Roberts)以及他们的导师科尔博格(Jerome Kohlberg)三个人名字的缩写,1976年,三人共同创建了KKR公司。

KKR公司是以收购、重整企业为主营业务的股权投资公司,最擅长管理层收购。

在过去的30年当中,KKR累计完成了超过146项私募投资,交易总额超过了2630亿美元。

KKR在1988-1989年以310亿美元,杠杆收购RJR.Nabisco(当时美国的巨型公司之一,业务范围为烟草和食品),是世界金融史上最大的收购之一,该收购完成后,KKR的资产池有近590亿美元的资产组合;同期,只有4家美国公司——通用汽车、福特、埃克森、和IBM公司比它大。

KKR通常会选择符合下列标准的企业进行并购:1)、具有比较强且稳定的现金流产生能力;2)、企业经营管理层在企业经营管理岗位的工作年限较长(10年以上),经验丰富;3)、具有较大的成本下降、提高经营利润的潜力空间和能力;4)企业债务比例低。

除上述标准外,KKR还会特别强调收购方案必须被目标公司董事会与管理层接受,且必须说服管理层入股,以保证企业的核心竞争力,通过激励激发管理团队的创造力与战斗力。

KKR喜欢把自己的这种交易安排称为“管理层收购”,而不是“杠杆收购”;与“杠杆收购”相比,“管理层收购”除同样充分利用杠杆外,更重视目标公司管理层的作用。

选定目标企业后,KKR往往会通过以下方式解决资金问题:首先由公司的最高层管理人员和/或接管专家们领导的收购集团以少量资本组建执行收购的空壳公司。

杠杆收购经典案例KKR

杠杆收购经典案例/index.php 2007-11-23 14:26:26 《董事会》说到杠杆收购,就不能不提及20世纪80年代的一桩杠杆收购案——美国雷诺兹-纳贝斯克(RJR Nabisco)公司收购案。

这笔被称为“世纪大收购”的交易以250亿美元的收购价震惊世界,成为历史上规模最大的一笔杠杆收购,而使后来的各桩收购交易望尘莫及。

这场收购战役主要在RJR纳贝斯克公司的高级管理人员和著名的收购公司KKR (Kohlberg Kravis Roberts&Co.)公司之间展开,但由于它的规模巨大,其中不乏有像摩根士丹利、第一波士顿等这样的投资银行和金融机构的直接或间接参与。

“战役”的发起方是以罗斯·约翰逊为首的RJR纳贝斯克公司高层管理者,他们认为公司当时的股价被严重低估。

1988年10月,管理层向董事局提出管理层收购公司股权建议,收购价为每股75美元,总计170亿美元。

虽然约翰逊的出价高于当时公司股票53美元/股的市值,但公司股东对此却并不满意。

不久,华尔街的“收购之王”KKR公司加入这次争夺,经过6个星期的激战,最后KKR胜出,收购价是每股109美元,总金额250亿美元。

KKR本身动用的资金仅1500万美元,而其余99.94%的资金都是靠垃圾债券大王迈克尔.米尔肯(Michael Milken)发行垃圾债券筹得。

一、相关背景关于RJR纳贝斯克公司作为美国最大的食品和烟草生产商,雷诺兹-纳贝斯克公司是由美国老牌食品生产商Standard Brands公司、Nabisco公司与美国两大烟草商之一的RJR公司(Winston、Salem、骆驼牌香烟的生产厂家)合并而成。

在当时它是美国排名第十九的工业公司,雇员14万,拥有诸多名牌产品,包括奥利奥、乐芝饼干、温斯顿和塞勒姆香烟、Life Savers糖果,产品遍及美国每一个零售商店。

虽然RJR纳贝斯克公司的食品业务在两次合并后得到迅猛的扩张,但烟草业务的丰厚利润仍占主营业务的58%左右。

经典LBO案例分析-KKR-杠杆购并-RJR-NABISCO

• 1965 –1988 (13 年)

– 完成30例杠杆收购(LBO) – 购买价格总计超出US$300亿 – KKR自有资金仅US$22亿 – 复合年回报率达60%

RJR Nabisco?

• RJR: 雷诺烟草公司

• Nabisco: 中文名?

• 1985 -- RJR 实行多元化经营, 购买 Nabisco (US$49亿) 后, 成立RJR Nabisco

路漫漫其悠远

KKR 杠杆收购 RJR Nabisco ---- 特别委员会收到1988年11月18日投标结果

1988年11月18日

每股收购价

现金 PIK 优先股 可转换优先股 PIK 可转换债券 证券 股票权证

MBO团队 US$100

$90 $6 $4

KKR US$94

$75 $11

$8

可转换证券 条件:

$88 现金

$80 现金

$9 PIK 优先股

$17 PIK 优先股

(1)用优先股股票支付股息 (2)三年内重新设定其平价面值

(1)最初6年用优先股股票支付股息 (2)一定时期用浮动股息率 (3)浮动股息率时期后,按市场利率重新设定

其固定利率

$4 可转换优先股

$9 到期自动可转换债券

(1)13%累积股息率 (2)如全部转换成股票, 可占新公司

MBO团队通RJR Nabisco 特别委员会: 提出要提交一份新要约

路漫漫其悠远

KKR 杠杆收购 RJR Nabisco ---- 1988年11月29日5:00PM KKR与MBO团队标 的条件比较

1988年11月29日5:00PM

MBO团队 每股收购价 US$101

KKR 每股收购价 US$106

美国雷诺兹-纳贝斯克(rjrnabisco)公司收购案

杠杆收购的经典案例美国RJR Nabisco公司争夺战说到杠杆收购,就不能不提及20世纪80年代的一桩杠杆收购案——美国雷诺兹-纳贝斯克(RJR Nabisco)公司收购案。

这笔被称为“世纪大收购”的交易以250亿美元的收购价震动世界,成为历史上规模最大的一笔杠杆收购,而使后来的各桩收购交易望尘莫及。

这场收购战争主要在RJR纳贝斯克公司的高级治理人员和闻名的收购公司KKR (Kohlberg Kravis Roberts%26amp;Co.)公司之间展开,但由于它的规模巨大,其中不乏有像摩根士丹利、第一波士顿等这样的投资银行和金融机构的直接或间接参与。

“战争”的发起方是以罗斯·约翰逊为首的RJR纳贝斯克公司高层治理者,他们认为公司当时的股价被严重低估。

1988年10月,治理层向董事局提出治理层收购公司股权建议,收购价为每股75美元,总计170亿美元。

虽然约翰逊的出价高于当时公司股票53美元/股的市值,但公司股东对此却并不满足。

不久,华尔街的“收购之王”KKR公司加入这次争夺,经过6个星期的激战,最后KKR胜出,收购价是每股109美元,总金额250亿美元。

KKR本身动用的资金仅1500万美元,而其余99.94%的资金都是靠垃圾债券大王迈克尔.米尔肯(Michael Milken)发行垃圾债券筹得。

一、相关背景关于RJR纳贝斯克公司作为美国最大的食品和烟草生产商,雷诺兹-纳贝斯克公司是由美国老牌食品生产商Standard Brands公司、Nabisco公司与美国两大烟草商之一的RJR公司(Winston、Salem、骆驼牌香烟的生产厂家)合并而成。

在当时它是美国排名第十九的工业公司,雇员14万,拥有诸多名牌产品,包括奥利奥、乐芝饼干、温斯顿和塞勒姆香烟、Life Savers糖果,产品遍及美国每一个零售商店。

虽然RJR纳贝斯克公司的食品业务在两次合并后得到迅猛的扩张,但烟草业务的丰厚利润仍占主营业务的58%左右。

KKR的上市阳谋

据 知 悉 此 计 划 的投行 人 士 透 露 : 此 次 并购

领域 的资产 管理

,

此 外该 公 司 正 酝 酿建 立

一个58源自e l= O W O R L D 2 0 0 8 / 8 0

"

维普资讯

金 融前 瞻

F I N A N C E P E R S P EC T IV E 圈

。

门 财 经 畅销 书 《 口

,

的 财务 顾 问

今年 月

5

L

a z a r

d

的 能 源 与基 础

Ge

o r

将 的 野 蛮 人 》 此 并 购 案 收录 其 中

蛮人 就成 了 K K

”

此后

“

门口

。

的野

设 施 投 资 部 门负 责 人 兼 董 事 总 经 理

入职KKR

,

g e B il i c i c

R

。

必 向市 场 和 广 大 投 资 者 公 布 基 金 的 投 资

,

资本运 作颇

a

而非

35%

的企业 所 得税

、

鉴于 杠杆

策略

、

运 营状 况

、

财 务 状 况 和薪 酬 制 度

一

。

非主 流性

” 。

对此

,

C h in

Ve

n tu r e

分

收 购 的 规 模 日益 扩 大

贷款及 债券融资

缺 乏 透 明性 和 P E 的 高 利 润 正 是

,

实现在纽 约证 券

这段渊源

;

法 国律 师 事 务 所

。

d in P

ra

t

【金融】【并购】案例分析:KKR并购领袖

案例分析:KKR并购领袖通过将杠杆收购和管理层收购巧妙结合,KKR成为私募基金的并购领袖一手打造了“天价恶意收购”范例—雷诺兹·纳贝斯克收购案、“与企业管理层共谋”范例——劲霸电池收购案、“担任白武士”范例——西夫纬收购案等经典之作。

KKR坚守自己的收购原则,在多年的并购时间中创造出一套独特的获利方式。

Kohlberg Kravis Roberts & Co 1976年成立公司总部: 纽约管理规模: 270亿美元并购领域: 消费品、销售连锁、娱乐、IT服务、电信通讯、半导体芯片创始人:科尔伯格(Jerome Kohlberg)、罗伯茨(George Roberts)、克拉维斯(Henry Kravis)科尔伯格和罗伯茨是好朋友,而罗伯茨与克拉维斯是表兄弟。

科尔伯格在三人中资格最老,既是后两者的导师,也是KKR成立之初的主导者。

1976年,科尔伯格、罗伯茨和克拉维斯三人离开了贝尔公司,自己组建了KKR公司。

科尔伯格于1987年离开KKR。

克拉维斯则因为成就了KKR在华尔街杠杆收购中的大佬位置而被人们尊称为“亨利王”(亨利是克拉维斯的名)。

“LBO+ MBO”模式Kohlberg Kravis Roberts & Co(KKR)是私募股权基金之中最具有传奇色彩的公司。

在公司一系列令人眼花缭乱的收购战中,翻手为云、覆手为雨,专门用小钱并购那些经营不善的企业,然后通过与管理层合作,经过重组捞取令人咋舌的丰厚利润。

从某种意义上而言,KKR不仅将LBO发扬光大,更成为管理层收购(Management Buyout或MBO)的创始人。

在KKR成立后的前三年交易记录中,一共实现了六次收购。

KKR喜欢标榜这些交易是MBO,以此打响自己的“金字招牌”,使公司区别于其他精通LBO的同行。

不过,KKR的确十分在意目标公司的管理团队作用。

例如1977年4月收购的A.J.Industries是一家摇摇欲坠的联合型大企业,但它有一个非常突出的核心业务,更有一位精明执著的首席执行官雷蒙·欧可费(Raymond O'Keefe)。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Oct. 20, 1988

• Key PlayeБайду номын сангаасs: Management-led group

– F. Ross Johnson, CEO of RJR Nabisco – Shearson Lehman Hutton, Wall Street Investment Bank

• Proposal: $17 billion LBO at $75 per share

Nov. 3, 1988

Management-led group raised the price to $92 per share

Nov. 4, 1988

• Forstmann Little, another private equity firm, joined the battle with a higher bid • Shearson accused Forstmann of breach of promise

Nov. 19, 1988

• All potential buyers, KKR, First Boston, and management-led group, spent the day explaining their complex bids to RJR Nabisco’s directors • RJR Nabisco announced a new deadline, Nov. 29

Nov. 29, 1988

• Three competitors submitted the final bids:

– KKR: $24 billion, or $105.88 per share – Management-led group: $22.9 billion, or $101 per share – First Boston: $23.38 ~ $26.11 billion, or $102.14~ 115 per share

3. RJR Nabisco is cheap

• In Oct 19th, 1987, the stock price for RJR Nabisco is $55.875. All the competitors thought that the valuation for RJR Nabisco’s food business is dragged by the poor performance of its tobacco business. They considered the stock of RJR Nabisco as severely undervalued. • Low share price means that there is more room for a contest of acquiring the company. • Rewards from restructuring is very attractive to the barbarians at the gate.

2. RJR Nabisco is slow:

Actually, this could also be viewed as the result of being big. • In a much smaller company, the shareholders or the management team could use various strategy to resist an attack: poison pills, white knight, scorched earth… • But for a group as large as RJR Nabisco, none of these strategies would work out in a short period of time. • In a word, RJR Nabisco’s reaction is too slow, it could not spin off from an attack.

Nov. 18, 1988

• Just before the deadline, First Boston, another investment bank in Wall Street, joined this battle with a higher price • However, the financing for this offer is uncertain

1. RJR Nabisco is big:

The group was profitable (the tobacco business had a margin of 58% at that time) and had a steady cash flow. This could provide three reasons for an MBO or LBO: • Steady cash flow could make sure the interest is covered. • New debt will have a tax shield effect and the new management team could use a better capital structure to increase firm value. • No one could swallow such an elephant in a short time, that is why Ross Johnson expected no competitor at first when he proposed the offer. First Boston is a good example for this.

KKR’s LBO of RJR Nabisco

Demos GUO Stephen SUN

Outline

1. 2. 3. 4. Background The History of the RJR Nabisco Takeover Why RJR Nabisco? Why KKR?

1. Background

Oct. 28, 1988

RJR Nabisco agreed to give KKR confidential financial data about its operations

Nov. 1, 1988

• RJR Nabisco’s chairman, Charles E. Hugel, said it was highly likely that the company will be sold, the company’s stock rose to $85 a share • Some KKR’s investors balked at allowing KKR to use their cash in this buyout

Nov. 16, 1988

• Forstmann Little left, RJR Nabisco’s stock price tumbled to $84 • ITT, which held RJR Nabisco bonds, sued RJR Nabisco over the decline in the bonds’ value • RJR Nabisco announced a deadline for bid: Nov. 19

Who is RJR Nabisco?

• RJR Nabisco, Inc., was an American conglomerate headquartered in the New York City • RJR Nabisco was the 19th-largest industrial concern in U.S. • It formed in 1985 by the merger of Nabisco Brands and R.J. Reynolds Tobacco Company Nabisco R.J. Reynolds

Who is KKR?

• KKR & Co. L.P. is an American-based global private equity firm founded in 1976 • Co-founders: Jerome Kohlberg and cousins Henry Kravis and George Roberts, all of whom had previously worked at Bear Stearns • Jerome Kohlberg left KKR in 1987

• Stock price jumped to $90.875

Nov. 30, 1988

• KKR claimed victory for the staggering price of $24.88 billion, or $109 a share • Compared with the initial offer on Oct. 20 by management-led group: $17 billion, or $75 per share

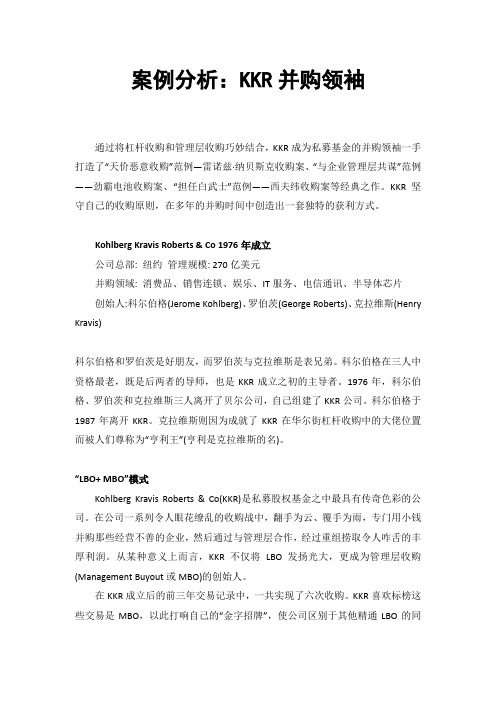

115 110 105 100 95 90 85 80 75

109

89 90 85 80 75 70

25-Oct 30-Oct

92 84

90.87

Offer Price Stock Price

4-Nov 9-Nov 14-Nov 19-Nov 24-Nov 29-Nov

70

20-Oct

3. Why RJR Nabisco?

Oct. 24, 1988

• Key Players: KKR

– Kohlberg, Kravis, Roberts & Company (KKR)