ACCAF 知识点总结

ACCA-F7-知识点总结

ACCA考试F7知识点辅导I. The accounting problemBefore IAS37 provisions were recognized on the basis of prudence,little guidance was given on when a provision should be recognized and how it should be measured. This gave rise to inconsistencies,and also allowed profits to be manipulated.Some problems are noted below:(a) Provisions could be recognized on the basis of management intentions,rather than on any obligation to be entity;(b) Several items could be combined into one large provision. There were known as ‘big bath’ provisions;(c) A provision could be created for one purpose and then used for another;(d) Poor disclosure made it difficult to assess the effect of provisions on reported profits. In particular,provisions could be created when profits were high and released when profits were low in order to smooth profits.(1) DefinitionsIAS 37 views a provision as a liability.A provision is a liability of uncertainty timing or amount;A liability is an obligation of an enterprise to transfer economic benefits as a result of past transactions or events.Provision must be based on obligations,not management intentions.(2) Under IAS37, a provision should be recognized:a. When an enterprise has a present obligation;b. It is probable that a transfer of economic benefits will be required to settle it;c. A reliable estimate can be made of its amount; if a reasonable estimate cannot be made,then the nature of the provision and the uncertainties relating to the amount and timing of the cash flows should be disclosed.A provision is made for something which will probably happen. It should be recognizedwhen it is probable that a transfer of economic events will take place and when its amount can be estimated reliably.(3) Contingent liabilitiesDefinitionThe Standard defines a contingent liability as:(a) A possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the enterprise; or(b) A present obligation that arises from past events but is not recognized because:(i) It is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or(ii) The amount of the obligation cannot be measured with sufficient reliability.As a rule of thumb,probable means more than 50% likely. If an obligation is probable,it is not a contingent liability – instead,a provision is needed.Treatment of contingent liabilitiesContingent liabilities should not be recognized in financial statements but they should be disclosed. The required disclosures are:(a) A brief description of the nature of the contingent liability;(b) An estimate of its financial effect;(c) An indication of the uncertainties that exist;(d) The possibility of any reimbursement;(4) Contingent assetsDefinitionA possible asset that arises from the past events whose existence will be confirmed by the occurrence of one or more uncertain future events not wholly within the enterprise’s control.A contingent asset must not be recognized. Only when the realization of the relatedeconomic benefits is virtually certain should recognition take place. At that point,the asset is no longer a contingent asset.Disclosure:contingent assetsContingent assets must only be disclosed in the notes if they are probable. In that case a brief description of the contingent asset should be provided along with an estimate of its likely financial effect.II. Specific application1. Future operating lossesIn the past,provisions were recognized for future operating losses on the grounds of prudence. However these should not be provided for the following reasons.①They relate to future events;②There is no obligation to a third party. The loss-making business could be closed and the losses avoided.2. Onerous contractsAn onerous contract is a contract in which the unavoidable costs of meeting the contract exceed the economic benefits expected to be received under it.A common example of an onerous contract is a lease on a surplus factory. The leaseholder is legally obliged to carry on paying the rent on the factory,but they will not get any benefit from using the factory.The least net cost of an onerous contract should be recognized as a provision. The least net cost is the lower of the cost of fulfilling the contract or of terminating it and suffering any penalty payments.Some assets may have been bought specifically for the onerous contract. These should be reviewed for impairment before any separate provision is made for the contract itself.1DemoDroopers has recently bought all of the trade,assets and liabilities of Dolittle,an unincorporatd business. As part of the take-over all of the combined business’s activities have been relocated at Droopers main site. As a result Dolittle’s premises are now empty and surplus to requirements.However,just before the acquisition Dolittle had signed a three year lease for their premises at $6000 per calendar month. At 31 December 2003 this lease ad 32 months left to run and the landlord had refused to terminate the lease. A sub-tenant had taken over part of the premises for the rest of the lease at a rent of $2500 per calendar month.Required(a) Should Droopers recognized a provision for an onerous contract in respect of this lease?(b) Show how this information will be presented in the financial statements for 2003 and 2004. Ignore the time value of money.Solution:Droopers has a legal obligation to pay a further $192000 to the landlord,as a result of a lease signed before the year end. Therefore an onerous contract exists and must be provided for.There is also an amount recoverable form the sub-tenant of $80000(32×2500). This will be shown separately in the balance sheet as an asset.The $192000 payable and the $80000 recoverable can be netted off in the income statement.income statements20032004$$provision for onerous lease contract(net)112000 Dr.net rental payable on lease (72-30)-42000 Drrelease of provision42000 Cr112000 Dr.balance sheetsreceivalbesamounts recoverable from sub-tenants80000 Dr.50000 Drliabilitiesamounts payable on onerous contracts192000 Cr120000 Cr3. RestructuringA restructuring is a programme that is planned and controlled by management and has a material effect on:①The scope of a business undertaken by the reporting entity in terms of the products or services it provides; or②The manner in which a business undertaken by the reporting entity is conducted;Restructuring includes terminating a line of business,closure of business locations,changes in management structure,and refocusing a business’s operations.Restructuring provisions have always been quite common,and have often been misused. IAS37 restricts the recognition of restructuring provisions to situations where an entity has a constructive obligation to restructure.A constructive obligation will only arise if:①There is a detailed formal plan for restructuring. This must identify the businesses,locations and employees affected; and②Those affected have a valid expectation that the restructuring will be carried out. This can be by starting to implement the plan or by announcing it to those affected.The constructive obligation must exist at the year-end.(Any obligation arising after the year end may require disclosure under IAS10)A board decision alone will not create a constructive obligation unless:①The plan is already being implemented. For example,assets are being sold,redundancy negotiations have begun; or②The plan has been announced to those affected by it. The plan must have a strict timeframe without unreasonable delays; or③The Board itself contains representatives of employees or other groups affected by the decision.(This is common in mainland Europe.)An announcement to sell an operation will not create a constructive obligation. An obligation will only arise when a purchaser is found and there is a binding sale agreement.A restructuring provision should only include the direct costs of restructuring. These must be both:(a) Necessarily entailed by the restructuring; and(b) Not associated with the ongoing activities of the entity;The following costs must not be provided for because they relate to future events:(a) Retaining or relocating staff;(b) Marketing;(c) Investment in new systems and distribution networks;(d) Future operating losses (unless arising from an onerous contract)(e) Profits on disposal of assets.cca f7真题对于acca f7的考试的重要性我相信各位acca考生都心知肚明了,首先我们先看一下acca f7科目的考试内容ACCA F7科目介绍:F7《财务报告》是F3《财务会计》的后续课程或说是升级课程。

ACCA-F4知识要点汇总(精简版)

ACCA-F4知识要点汇总(精简版)1. 公司法律结构及管理公司的法律结构包括公司章程、股东协议、公司登记簿、董事会、股东大会、公司秘书等。

管理层需要遵守法律法规,同时也应该关注公司的社会责任和企业道德。

2. 公司财务及税务公司的财务部门需要负责编制财务报表、管理公司资金、进行预算和决策分析等。

税务部门需要负责申报税务、缴纳税款以及规划税务策略。

3. 合同法律框架合同是商业交易的基础,具有法律约束力。

合同的成立需要满足合同要素、合同内容的充分和明确、合同手续正确等条件。

合同的违约应该依法承担相应的法律责任。

4. 卖方和买方的权利与义务在商品的交易中,卖方需要履行交货、履行义务、提供货物信息等职责;买方需要履行付款、接收货物、检验货物、通知卖方等职责。

同时,卖方和买方也有权利保护自己的利益。

5. 银行融资银行融资是常见的企业融资方式,包括贷款、信用证、保函等。

企业在申请银行融资时需提供充分的资料和合理的担保措施,并在合同履行期内按期还款。

6. 国际贸易国际贸易的主体包括进出口商、代理商、货代、保险公司等。

在国际贸易中,涉及到的问题有贸易商信用、运输保险、海关手续等。

企业需要制定适应国际贸易的商业策略。

7. 合并与收购合并与收购是企业快速扩张的一种方式。

在进行合并与收购时,需要考虑战略目标、财务风险、员工合法权益等问题,并进行充分的财务、法律尽职调查。

8. 会计和审计会计和审计是公司财务管理的重要组成部分。

会计部门需要负责制定会计政策、编制财务报表等。

审计部门需要进行内部审核、外部审核等工作,并对财务报表的真实性和准确性进行评估。

ACCA F1 大题知识点

1.what are the porter`s value chain?(Porter grouped the various activities of an organization into a value chain.)The value chain describes those activities of the organization that add value to purchased inputs.The porter`s value chain comprise support activities, primary activities and margin. Primary activities are directly related to production, sales, marketing. Deliver and service. Support activities provide purchased inputs, human resources, technology and infrastructural functions to support the primary activities. The margin is the excess the customer is prepared to pay over the cost to the firm of obtaining resource inputs and providing value activities.2.What are the five competitive forces?The competitive environment is structures by five forces.Barriers to entry; substitute products; the bargaining power of customers; the bargaining power of suppliers; competitive rivalry (行业竞争对手)3.What are the differences between internal and external audit?a.Reason. Internal audit is an activity designed to add value and improve an organization`s operations. External audit is anexercise to enable auditors to express an opinion on the financial statements.b.Reporting to. Internal audit reports to the board of directors, or other charged with governance. The external auditors reportto the shareholders or members of a company on the stewardship of the directors.c.Relating to. Internal audit`s work relates to the financial statements. (Concerned with the financial records that underliethese.)d.Relationship. With the company. Internal auditors are very often employees of the organization. External auditors areindependent of the company and its management. (They are appointed by the shareholders.)4.Introduce the fiscal policy and monetary policyFiscal policy provides an method of managing aggregate demand in the economy. Fiscal policy includes government policy on taxation, public, borrowing and public spending. Monetary policy uses money supply. Interest rates or credit controls to influence aggregate demand. Monetary policy: government policy on the money supply, the monetary system, interest rates, exchange rates and the availability of credit.5.What the situations of budget surplus and budget deficit happen?When government`s income exceeds its expenditure and there is a negative PSNCR or Public sector debt repayment (PSDR), we say that the government is running a budget surplus. This may be a deliberate policy to reduce the size of the money supply by taking money out of the economy. When a government`s expenditure exceeds its income, we say that the government is runninga budget deficit.6.Why does organization exist? (In brief, organizations enable people to be more productive.)Organizations can achieve results which individuals cannot achieve by themselves.a.Overcome people`s individual limitations, whether physical or intellectual.b.Enable people to specialize in what they do best.c.Save time. Because people can work together or do two aspects of a different task at the same time.d.Accumulate and share knowledge.e.Enable synergy: by bring together two individuals their combined output will exceed their output if they continued workingseparately.7.What the different between private companies and public limited companies?In the UK, limited companies come in two types: private limited companies and public limited companies. They differ as follows.a.Member of shareholders, most private companies are owned by only a small number of shareholders. Public companiesgenerally are owned by a wide proportion of the investing public.b.Transferability of shares. Share in public companies van be offered ti the general public. In practice this means that they canbe traded on a stock exchange. Shares in private companies, on the other hand, are rarely transferable without the consent of the shareholders.c.Directors as shareholders. The directors of a private limited company are more likely to hold a substantial portion of thecompany`s shares than the directors of a public company.8.In mintzberg`s view, what are the five component parts of an organization.According to mintzberg`s view, the five component parts include strategic apex, operating core, middle line, techno structure and support staff.9.Introduce the components of the shamrock organization and the Anthony hierarchy.Shamrock organization includes self employed, contingent, professional and consumers. Robert Anthony classified managerialactivity as follows: strategic management, tactical management and operational management.10.What are the types of committee?Committee can be classified according to the power they exercise.a.Executive committees have the power to govern or administer.b.Standing committees are formed for a particular purpose on a permanent basis. Their role is to deal with routine businessdelegated to them at weekly or monthly meetings.c.AD hoc committees are formed to complete a particular task.d.Sub-committee may be formed to co-ordinate the activities of two or more committees.e.Management committees in many businesses contain executives at a number of levels not all the decisions in a firm need tobe taken by the board.11.What are the qualities of good information?The qualities of good information include accurate, complete, cost- beneficial, user-targeted, relevant, authoritative, timely, easy to use.12.Introduce Handy`s 4 types of culturea.Power culture is shaped by one individual.b.Role culture is a bureaucratic culture shaped by rationality, rules and procedures.c.Rask culture is shaped by a focus on outputs and results.d.Existential or person culture is shaped by the interests of individuals.13.List the potential benefits of the informal organization.The potential benefits of the informal organization include Employee commitment, knowledge sharing, speed, responsiveness, co-operation.P75,P70,P53,P18,P11。

ACCA F6知识要点汇总

F6知识点:第一章UK TAX SYSTEMTaxation function: encourage economic, social and environmental behaviour Structure: 税务由HMRC管理Human revenue and customs 英国税务及海关总署Source of law 立法Finance Act每年更新税率Tax year: April 6th to April 5thTax evasion is illegal 逃税非法 & Tax avoidance is legal 合理避税合法第二章Computation of taxable income and income tax liability1.Resident判定UK resident individuals UK & oversea income都交税Non‐UK resident individuals 仅UK income交税5 UK Ties:▲考试提供表格:Days inUK Previously resident Not previously resident < 16 Automatically not resident Automatically not resident 16 to 45 Resident if 4 UK ties(or more) Automatically not resident 46 to 90 Resident if 3 UK ties(or more) Resident if 3 UK ties(or more) 91 to 120 Resident if 2 UK ties(or more) Resident if 2 UK ties(or more) 121 to 182 Resident if 1 UK ties(or more) Resident if 1 UK ties(or more) 183 Automatically resident Automatically resident1. Types of incomeNon ‐saving income Trade incomeEmployment incomeProperty incomeSavings income Taxed income (20% tax 已扣)Bank interestBuilding society interest Interest received gross (未扣税)Government stocks (gilts 债券) interestNational saving & invest bank interest Dividend income 10% tax 已扣This tax credit is not refundable. Exempt income 免税收入,回答题目时必须注明时免税收入,不写没分Interest from Saving Certificates issued by National Savings and InvestmentBank(UK 国民储蓄和投资银行:储蓄账户免税,投资账户收税)国民储蓄券 Statutory redundancy money 裁员补偿Betting and gaming winnings 博彩奖金(收其他税,不收个税) Scholarships 奖学金Interest on damages for personal injuries 个人受伤赔偿,包括工资补贴等 in UK < 16Din UK < 46D, not resident in past 3 tax yearsFull time oversea work & in UK < 90Din UK >183D only home in UK Full time work in UK UK House in useSubstantive work in UK > 90D in either two past tax years more time in UK than oversea FamilyLocal authority grant 地方补助Income from investments made through new individual savings accounts (NISAs) NISA有3种, 每个Tax year overall subscription limit is 15,000。

accaf1知识点汇总

accaf1知识点汇总ACCA F1 Knowledge Points SummaryACCA F1 is the beginning course of the ACCA qualification. The syllabus includes management accounting, business organization and structure, financial accounting, and basic understanding of economics. Learning and mastering ACCA F1 knowledge points is important to successfully completing the rest of the qualification. In this article, we will summarize the key knowledge points of ACCA F1.1. The Business EntityThe business entity is the core of business studies. The different types of business entities determine the legal and financial responsibilities of the business. There are three main types of business entities: sole traders, partnerships, and companies. Understanding the differences between the three is important for analyzing and evaluating business operations.2. Costing and BudgetingCosting is the process of determining the cost of a product, service, or business operation. This is important for pricing decisions, operations analysis, and performance evaluation. Budgeting is the process of setting financial goals for a business and managing the resources to achieve these goals. Understanding the principles of costing and budgeting is essential to examine the financial performance of a business.3. Financial StatementsFinancial statements are the reports that summarize a business’s financial activity. The three primary financial statements are the balance sheet, income statement, and cash flow statement. The balance sheet shows the current financial situation of a business, the income statement analyzes the revenue and expenses, while the cash flow statement shows the flow of cash in and out of the business. The purpose of analyzing financial statements is to understand the financial health of a business and determine its profitability.4. Business StructuresBusiness structures refer to the different methods of organizing and operating a business. There are three main business structures:centralized, decentralized, and hybrid. A centralized structure has a single, central decision-making body, while a decentralized structure passes control to different sub-units. A hybrid structure combines elements of both centralized and decentralized structures. Understanding business structures is important for analyzing organizational effectiveness, as well as for making strategic decisionsin regards to organizational structure.5. Economic PrinciplesEconomic principles are basic rules that guide the study of economics. These principles include supply and demand, market equilibrium, opportunity cost, and comparative advantage. These concepts are important for understanding economic patterns, making strategic business decisions, and analyzing market behavior.6. Accounting ConceptsAccounting concepts refer to the basic principles of accounting that guide the reporting and interpretation of financial information. These concepts include the concept of double entry, accruals and prepayments, the accounting equation, and depreciation. Accounting concepts arecrucial for preparing and interpreting financial statements, as well as for making financial decisions based on a company’s financial data.In conclusion, ACCA F1 is a crucial course in the ACCA qualification. The syllabus teaches students a number of key concepts in business and finance, including costing and budgeting, financial statements, economics, business structures, and accounting. Understanding and mastering these concepts will lay a strong foundation for the rest of your studies and your future career in business and finance.。

ACCA F4知识点:Criminal law and Civil law

ACCA F4知识点:Criminal law and Civil law今天给大家来说一说ACCA F4中关于Criminal law和Civil law,即刑法和民法。

首先我们先来看一下它们的定义。

Civil law sets out the rights and duties of persons as between themselves. The person whose rights have been infringed can claim a remedy from the wrongdoer. 民法主要关注的是人的权利和责任以及对其的补偿。

Criminal law is concerned with the conduct that is considered so undesirable that the State punishes persons who transgress. 刑法主要关注的是一个违法的人对其的违法行为的惩罚。

关于Burden of proof,即举证责任,有相似的部分。

The necessity of proof normally lies with the person who lays charges, i.e. the claimant. 举证责任由原告承担。

这两者之间的区别主要体现在四个方面。

(1)Aim. Civil law is aimed to provide compensation for an injured party, whereas criminal law is to regulate society by the threat of punishment.(2)Parties. In a civil action, the claimant sues the defendant, while in a criminal action, the State prosecutes the defendant.(3)Standard of proof. In Civil law, if the claimant can prove the wrong on the balance of probabilities, his litigation is successful and the defendant is held liable. 民法中,要保持可能性的平衡。

超全ACCA FA(F3) 16-19章知识点总结(五)(干货精选)

超全ACCA FA(F3)16-19章知识点总结(五)(干货精选)ACCA F3是Financial Accounting (FA) 财务会计的简称,主要介绍了财务会计准则、相关会计科目账户建立以及准确财务信息的提供。

F3总体来说知识点细碎,考试范围广,要想掌握好F3的知识点,大量的练习是不可少的。

F3的整体难度为2颗星,建议留出一个月时间备考。

小盟君继续为大家分享ACCA F3知识点。

今天分享16-19章知识点,最后有公式详解呦。

1. 内部对账:自己家的帐和自己家的明细账对账。

2. 外部对账 :自己家的帐和外部的客户/供应商对账。

3.(内)balance c/d=total of listed balence:总账来自于日记账的加总做题时:control X →(adjust) adjustedMemo X →(adjust) adjusted4.总账&明细账:总账:control account ;general /nominal account明细账:memo account ;individual; list; ledger5.(外)两家公司进行对账:两家公司进行对账(期初一定能对的上)要对账的项目:Receivable<Dr> credit salesSales tax( if sale tax register)Interest on over due debtsDishonored chequeRefunds paid to credit customers<Cr> cash received from credit customersDiscount allowedReturn inwardsIrrecoverable debtsContra entry (对冲业务)Balance c/dPayable<Dr> cash paid to creditDiscount receivedReturn outwardsContra entryBalance c/d<Cr> credit salesSale tax(增值税的进项税)Refunds paid to credit suppliers6.refund:只要是refund都出现在增加的方向。

acca fm 知识点总结

acca fm 知识点总结作为ACCA考试的一部分, Financial Management(FM)是一个重要的科目。

该科目涵盖了许多财务管理的核心知识和技能。

准备FM考试需要对财务管理的理论和实践有深入的理解,并能够灵活运用这些知识解决实际问题。

在本文中,我们将对ACCA FM考试的知识点进行总结,希望对考生有所帮助。

1. 金融管理的基本概念金融管理是指企业如何有效地管理其财务资源以实现其目标。

这包括财务规划、财务决策、筹资、投资、风险管理等方面的内容。

2. 资本预算资本预算是指企业在购买固定资产、开发新产品、进行市场扩张等方面的投资决策。

在资本预算分析中,需要考虑投资的成本、收益、现金流等因素。

3. 资本结构资本结构是指企业通过债务和股权融资所形成的资本组合。

企业在确定资本结构时需要考虑成本、风险、灵活性等因素,并努力寻找最优的资本结构。

4. 企业估值企业估值是指对企业的价值进行评估,常用的方法包括财务比率分析、贴现现金流量法、市场比较法等。

企业估值对于收购、兼并、上市、融资等活动至关重要。

5. 资本成本资本成本是企业融资的成本,它影响了企业的投资决策、资本结构决策等。

资本成本的计算包括权益资本成本、债务资本成本和加权平均成本。

6. 资本市场资本市场是企业进行融资和投资的场所,包括股票市场、债券市场、外汇市场、衍生品市场等。

资本市场的运作对企业融资和投资具有重要影响。

7. 风险管理风险管理是企业管理和控制各种风险的过程,包括市场风险、信用风险、操作风险等。

企业需要使用各种金融工具来降低风险,例如期货、期权、互换等。

8. 财务分析财务分析是对企业财务状况和经营绩效进行评价,包括利润表、资产负债表、现金流量表等方面的分析。

通过财务分析,可以了解企业的盈利能力、偿债能力和经营风险。

9. 资金管理资金管理是指企业如何有效地管理其现金和流动资产,以满足日常经营和投资活动的需要。

资金管理涉及现金管理、流动资产投资、资金筹集等方面的内容。

ACCAF1知识点总结

ACCAF1知识点总结ACCA F1是《管理会计基础》(Fundamentals of Business Mathematics and Financial Accounting)的考试科目,也是ACCA资格认证的第一门科目。

以下是ACCA F1考试的知识点总结:1.经济和商业环境:-经济体系及其类型-供需关系-国际贸易-经济增长和就业-货币和货币政策-通货膨胀和利率2.成本与管理会计基础:-成本和费用的概念与分类-成本-收益分析-边际成本与边际收益-战略与战术成本-成本预测与变动成本-学习曲线3.管理会计制度和方法:-不同类型的管理会计信息-管理会计的目的和特点-管理会计条例与道德-成本-利润-利润关系-预算与预算控制-绩效评估和激励4.财务会计和财务报表:-财务会计的目的和特点-财务记录和凭证-会计方程式和会计周期-货币和计量概念-资产负债表和利润表的解读-现金流量表5.财务分析和财务比率:-财务分析的目的和方法-比率分析和比率计算-经营和财务风险-财务健康和稳定性分析-盈利能力和效率分析6.提供财务信息:-需要财务信息的利益相关者-可比性和一贯性原则-隐含与显性假设-外部财务报告-内部财务报告7.管理信息系统:-信息系统的组成和功能-数据的收集和处理-数据库和数据仓库-信息系统的设计和实施-信息系统的风险和控制8.管理与决策科学:-决策的类型和过程-优化和约束问题-边际分析和边际效益-敏感性分析和决策树-风险分析和决策9.商业伦理和社会责任:-伦理的定义和原理-伦理决策模型-商业伦理的重要性-伦理决策和社会责任-可持续发展和企业道德ACCAF1考试主要考察考生对管理会计和财务会计的基本概念和方法的理解与应用能力。

考生需要熟悉各种会计和管理会计方法,并能够解读和分析财务信息和财务报表。

此外,考生还需要了解企业的商业环境和相关的伦理和社会责任问题。

参加ACCAF1考试前,考生需要充分准备,并掌握上述知识点。

ACCA F5知识要点汇总(精简版)

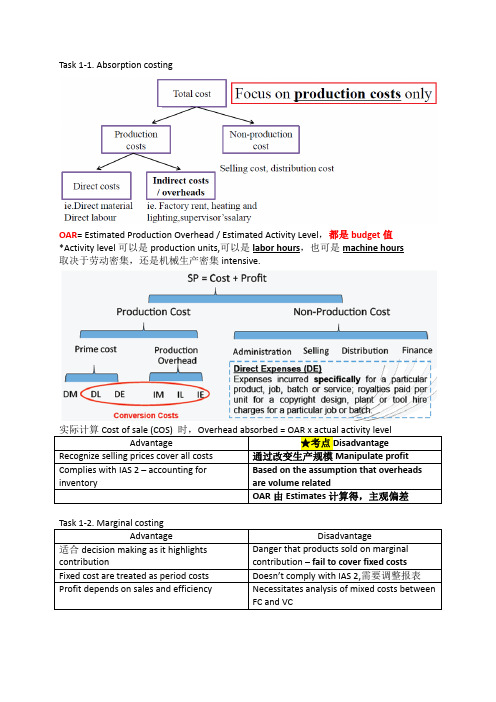

Task 1‐1. Absorption costingOAR= Estimated Production Overhead / Estimated Activity Level,都是budget值*Activity level可以是production units,可以是labor hours,也可是machine hours取决于劳动密集,还是机械生产密集intensive.实际计算Cost of sale (COS) 时,Overhead absorbed = OAR x actual activity levelAdvantage ★考点Disadvantage Recognize selling prices cover all costs 通过改变生产规模Manipulate profitComplies with IAS 2 – accounting for inventory Based on the assumption that overheads are volume relatedOAR由Estimates计算得,主观偏差Task 1‐2. Marginal costingAdvantage Disadvantage适合decision making as it highlights contribution Danger that products sold on marginal contribution – fail to cover fixed costsFixed cost are treated as period costs Doesn’t comply with IAS 2,需要调整报表 Profit depends on sales and efficiency Necessitates analysis of mixed costs betweenFC and VC☆技巧 AC = MC + (Closing Inventory – Opening Inventory) x OAR*The absorption costing requires subjective judgments.预算估计主观判断太多*There is often more than one way to allocate the overheads.制造成本分摊可操纵Task 2. Activity‐based costing★考点Traditional absorption costing适用于★考点Activity‐based costing适用于 One or a few simple and similar products Production has become more complex Overhead costs 占很小比例proportion Assess product profitability realistically资源consumption not driven by volumeLarger organizations & the service sector成本驱动drive:不同单位,不同OAR◆解题步骤:Cost Pool → Cost Drive → OAR → Absorbed → Full Cost★考点Advantage ★考点DisadvantageMore accurate cost/unit.适用绩效appraisal.Time consuming & expensiveControl OC by managing cost drivers Limited benefit当成本和volume related Profitability analysis to customers或生产线 Multiple cost drivers情况复杂,导致不精确Better understanding of what drives OC Arbitrary apportionment 任意分配★考点‐计算题(10.Dec.Q4) Problems when implementing ABC:‐ 耗时‐ 需要上层支持,因为缺乏信息‐ Project team运作,成员来自各个部门‐ IT部门支持‐ 了解成本结构‐ Cost‐benefit analysis★成本效益分析Target 3. Target costingCost plus pricing 传统成本法 Target costingFocus on internal Focus on external Steps of target costing 如何减少Cost gap✓ Product specifications ✓ Selling price ✓ Target profit: margin/ ROI ✓ Target cost ✓ Close the cost gap1) 购买便宜的材料(bulk buying 采购折扣或新供应商)2) 降低人工成本3) 提高生产能力,生产效率4) 以自动化替代人工automation 5) 减少无用环节 eliminate non value added activities6) 尽量减少部件数量,或尽可能使用多的标准件注:不能在质量上妥协compromise ,不得影响质量★考点Implications of target costing‐ Cost control: 目标成本体系中,价格是首要考量consideration ! 开发development过程中就要考虑成本,而不是后来产生时再考虑。

ACCA F阶段知识整理

ACCA F阶段知识整理ACCA考试科目一共有13门,其中F阶段考试科目一共占了9门课程,其中的重要性不言而喻,那么F阶段和P阶段有什么关联呢?P阶段应该如何选择呢?带着这些疑问一起和高顿ACCA来看看吧。

给大家整理了一套电子版ACCA备考资料,里面有很多ACCA考试资料可供大家选择。

而且在对于上班族来说,电子版的也很适合在地铁上查阅:电子版ACCA 备考资料F1 Accountant in Business这一门倾向于管理方面,课程难度不大,很多常识性的知识点,但是毕竟是ACCA第一门考试,所以刚开始大多数同学都会对很多专业词汇的英文表述不熟悉,加上F1中的知识点比较细碎,因此加大了学习的难度。

建议大家把每章的知识点自己做一个梳理总结,每一章节整理出大框架,可以很好地帮助本科的学习。

F2 Mangement Accounting这一门课是管理会计,课体总体难度不大,差异分析的部分可能有些难度,另外一些财务比率的计算需要掌握,为以后的学习打好基础。

F3 Financial Accounting这一门课是财务会计,属于基础会计学,其中会涉及到会计科目、会计分录、丁字账、试算平衡表等等一系列会计基础知识,对于没有会计基础的同学一开始会觉得一头雾水,但是入了门之后这门课程难度并不算大。

这一门课程是之后F7和P2的学习基础,一定要掌握知识点,同时积累英语专业词汇。

F4 Corporate and Business Law英美法系和大陆体系的不同在于他们使用的是判例法,因此F4中涉及到不同年代各种法律案例,并且有很多专业词汇。

以判例法为主考试难度感觉是在上升,但是通过率在上升F5 Performance Management这门课是管理会计的进阶,对于F2基础打得好的同学拿下这门课应该不在话下。

这门课程总体难度不大,重点在于掌握不同成本法及业绩评价方法的应用。

F6 Taxation这门课90%以上都是计算,是中国考生最拿手的地方。

ACCA F7知识要点汇总(精简版)

1)Probable ‐ Provision 的金额‐它自己可偿还的金额)

* Provision具体事项要以Provision Table的形式在

2)Possible ‐ CL ‐ disclose 3) Law suit ‐ 按照solicitor意见取最有可能的情况来判断,以此 Notes披露。

Policy转变:1)会改变报 告呈现形式;2)需要追 溯,改变过往报告保持

1) At R: HC= Price/production cost + Carrige inwards Production cost = DM,DL,depreciation,factory supervisors wage,storage(RM,WIP)... Based on normal capacity→normal/standard costing 2) After R: NRV(FV less cost to sell) 举例: Accounting Policy: 1) FIFO or AVCO; 2) Cost model or FV model Accounting estimate: 折旧年限从10年改为5年

*** 不能可靠计量成本的,则不能计提任何利润,COS按实际 70

数值,Revenue=COS,无PL。

Cash received=68→Dr Cash 68, Cr T/R 68

** 假设第一年盈利,第二年重复第一年的步骤;

** 假设第一年亏损,第二年不用再确认新的loss,CC直接转到

资金流向: Bank→Plant Plant→CC CC→GADFC GADFC+Profit→T/R T/R→Bank

△

2) Deduct the grand from the cost of the NCA that it finances

ACCA F1 重点词汇大全

ACCA F1 重点词汇大全1. Accountablity 责任2. Accounting 会计3. Activist 积极分子4. Ad hoc 临时5. Advocacy 辩护6. Agency theory 代理理论7. Aggregate demand 总需求8. Aggregate supply 总供给9. Apprisal 评估10. Artefact 人工11. Asset 资产12. Audit 审计13. Audit committee 审计委员会14. Audit trail 审计追踪15. Authority 权威16. Back-up 备份17. Balance of payment 国际收支平衡18. Bargaining power 讨价还价能力19. Belief 信仰20. Bonus scheme 奖金制度21. Boundaryless 无边界组织22. Budget 预算23. Business cycle 商业周期24. Business strategy 商业战略25. Capital 资本26. Capital expenditure 资本性支出27. Capital market 资本市场28. Centralization 集权29. Coach 教练30. Coercive 强迫31. Committee 委员会32. Competence 称职33. Compliance 遵守34. Confidentiality 保密性35. Conflict of interest 利益冲突36. Consensus 一致37. Consumer price index (CPI) 居民消费价格指数38. Consumer surplus 消费者剩余39. Contingency 权变40. Corporate 合作41. Corporate social responsibility (CSR) 企业社会责任42. Code of ethics 行为规范43. Cyclical unemployment 周期性失业44. Data 数据45. Decentralization 分权46. Delayering 简化管理结构47. Delegation 授权48. Demand 需求49. Demand curve 需求曲线50. Deontology 义务论51. Depression 萧条52. Direct discrimination 直接歧视53. Dismissal 辞退54. Diversity 多样性55. Dorming 调整期56. Double-entry bookkeeping 复式记账法57. Egoism 利己主义58. Elasticity 弹性59. Empowerment 授权60. Entrepreneurial 企业家61. Environmental footprint 环境脚印62. Equilibrium price 平衡价格63. Ethics 道德64. Exchange rate 汇率65. Executive director 执行董事66. External 外部67. Feedback 反馈68. Fiduciary responsibility 诚信义务69. Finance function 财务部70. Financial accounting 财务会计71. Financial statement 财务报表72. Firm 企业73. Fiscal policy 财政政策74. Flat organization 扁平结构75. Fraud 舞弊76. Frictional unemployment 摩擦性失业77. Generally Accepted Accounting Practice (GAAP) 美国通用会计准则78. Governance principle 治理原则79. Grievance 委屈80. Gross Domestic product 国内生产总值81. Gross National product 国民生产总值82. Group thinking 团队思维83. Hawthorne Study 霍桑实验84. Hollow organization 中空组织85. Honesty 诚实86. Hospitablity 热情87. Human Resourse Management (HRM) 人力资源管理88. Hygiene 保健89. Imperfect competition 不完全竞争90. Inbound logistic 向内运输91. Incentive 刺激92. Income 收入93. Induction 入职培训94. Inferior good 劣质产品95. Inflation 通货膨胀96. Inseparability 不可分割97. Intangibility 无形98. Integrity 诚实99. Intellectual 智商100. Interest rate 利率101. Internal audit 内审102. Internal control 内控103. International Accounting Standard Board (IASB) 国际会计准则理事会104. International Federation of Accountant (IFAC) 国际会计师联合会105. Interpersonal 人际106. Interview 面试107. Intimidation 恐吓108. Intrinsic 内部109. Job enlargement 工作扩大化110. Job enrichment 工作丰富化111. Job rotation 工作轮岗制112. Joint committee 联合委员会113. Judgement 判决114. Leadership 领导力115. Learning process 学习过程116. Liablity 负债117. Limited liability 有限责任118. Litigation 诉讼119. Lowballing 虚报低价120. Macroeconomic 宏观经济121. Management 管理122. Marginal utility 边际效益123. Market 市场124. Matrix 矩阵125. Mentor 导师126. Middle line 企业中层127. Microeconomic 微观经济128. Minimum wage 最低工资标准129. Module 模块130. Monetary policy 货币政策131. Money laundering 洗钱132. Monopolistic competition 垄断竞争133. Monopoly 垄断134. Morale 士气135. Motivation 激励136. Mourning 悲哀137. Multiplier effect 乘数效应138. Nomination committee 提名委员会139. Non-current asset 固定资产140. Non-governmental organization 非政府组织141. Norm 原则142. Objectivity 客观143. Offshore 离岸144. Oligopoly 寡头垄断145. Operational 运营146. Organization 组织147. Outbound logistic 向外运输148. Output 输出149. Oursource 外包150. Overhead 间接成本151. Ownership 所有权152. Partnership 合伙制153. Password 密码154. Payable 应付账款155. Payroll 工资156. Perception 感知157. Performance management 业绩管理158. Personality 性格159. Political 政治160. Price mechanism 定价机制161. Priortization 优先162. Privacy 隐私163. Probity 诚实164. Process 流程165. Procurement 采购166. Product life cycle 产品生命周期167. Professional 专业168. Profit 利润169. Project 项目170. Public sector 公共部门171. Purchasing 采购172. Quality control 质量控制173. Rate of unemployment 失业率174. Rational 理性175. Raw material 原材料176. Receivable 应收账款177. Recession 衰退178. Recovery 恢复179. Recruit 招聘180. Redundancy 裁员181. Relativism 相对主义182. Reputation 声誉183. Remuneration 薪酬184. Resignation 辞职185. Reward 奖励186. Retail Price Index (RPI) 居民消费价格指数187. Sarbanes-Oxley Act 萨班斯法案188. Scalar chain 层级链189. Selection 选拔190. Share capital 实收资本191. Shareholder 股东192. Social class 社会层级193. Sole trader 个体户194. Span of control 控制维度195. Spreadsheet 电子表格196. Stagflation 停滞性通货膨胀197. Stakeholder 企业利益相关者198. Strategy 战略199. Substitute 替代品200. Supervision 监督201. Supply 供给202. Synergy 协作203. Taxation 税务204. Team building 团队建设205. Teeming and lading 拆东墙补西墙206. Theorist 理论家207. Transparancy 透明208. Treasury 财政209. Uncertainty 不确定性210. Unemployment 失业211. Utilitarianism 功利主义212. Valence 效价213. Value chain 价值链214. Variable 变量215. Victimisation 受害216. Whistleblow 告密者217. Working capital 营运资本218. World Trade Organization (WTO) 世界贸易组织由东亚国际ACCA金牌讲师——孔令裔精心整理。

ACCA F1知识点:Stakeholder

ACCA F1知识点:StakeholderStakeholder是我们ACCA F1学的一个知识点几乎在我们所有学的科目中这就是一个basic的knowledge,甚至到了P3,P1,P5我们考试也会涉及到这个问题的分析。

Stakeholder利益相关者是哪些受到组织活动直接影响的个人或者群体。

首先看stakeholder的分类第一类是internal stakeholders,比如说组织中的员工,管理层员工。

他们关注组织的成长能不能持续经营,这关系到他们的岗位,愿景,利益,个人与组织一直的目标。

第二类是connected stakeholders,指那些与组织有商业关系的人,股东、银行、供应商、顾客等人。

股东在意股价会不会涨,能不能分到股利,银行在意借出的贷款能不能收回,供应商关注能不能收到货款,顾客关注能不能及时收货还有产品质量等等。

第三类external stakeholders.与组织没有商业关系,有政府,专业团体,还有一些pressure groups游说团体。

它们比较关注组织运行的合法性,是否遵守规章制度,污染,道德,权利。

能够影响组织,他们的意见一定要作为决策时需要考虑的因素。

但是,所有利益相关者不可能对所有问题保持一致意见,其中一些群体要比另一些群体的影响力更大,这是如何平衡各方利益成为战略制定考虑的关键问题。

这个问题就涉及到另一个Mendelow’s Matrix.企业在制定战略的时候要考虑到利益相关者,我们用两个维度衡量一个是利益相关者的权利大小,另外一个是利益水平。

权利底利益水平也低的人企业对他这类人做最少的努力。

如果权利水平低而利益水平高,企业要为这些人提供信息。

如果利益相关者的权力高但是利益水平低的话,企业要保证让这些人满意。

最最重要的如果这个人权力高利益水平也高,就是我们最主要的利益相关者,我们的战略要确保让他们接受。

关于利益相关者的问题我们就说到这里,这个点再很多科目考试答案中都可以出现,万金油一般,希望大家能掌握记住。

ACCAF7知识点总结

ACCA考试F7知识点辅导I. The accounting problemBefore IAS37 provisions were recognized on the basis of prudence,little guidance wasgiven on when a provision should be recognized and how it should be measured. This gave rise to inconsistencies,and also allowed profits to be manipulated.Some problems are noted below:(a) Provisions could be recognized on the basis of management intentions,rather than onany obligation to be entity;(b) Several items could be combined into one large provision. There were known as ‘big bath’ provisions;(c) A provision could be created for one purpose and then used for another;(d) Poor disclosure made it difficult to assess the effect of provisions on reported profits. Inparticular,provisions could be created when profits were high and released when profits werelow in order to smooth profits.(1) DefinitionsIAS 37 views a provision as a liability.A provision is a liability of uncertainty timing or amount;A liability is an obligation of an enterprise to transfer economic benefits as a result of pasttransactions or events.Provision must be based on obligations,not management intentions.(2) Under IAS37, a provision should be recognized:a. When an enterprise has a present obligation;b. It is probable that a transfer of economic benefits will be required to settle it;c. A reliable estimate can be made of its amount; if a reasonable estimate cannot be made,then the nature of the provision and the uncertainties relating to the amount and timing of thecash flows should be disclosed.A provision is made for something which will probably happen. It should be recognizedwhen it is probable that a transfer of economic events will take place and when its amount canbe estimated reliably.(3) Contingent liabilitiesDefinitionThe Standard defines a contingent liability as:(a) A possible obligation that arises from past events and whose existence will be confirmedonly by the occurrence or non-occurrence of one or more uncertain future events not whollywithin the control of the enterprise; or(b) A present obligation that arises from past events but is not recognized because:(i) It is not probable that an outflow of resources embodying economic benefits will berequired to settle the obligation; or(ii) The amount of the obligation cannot be measured with sufficient reliability.As a rule of thumb,probable means more than 50% likely. If an obligation is probable,it isnot a contingent liability – instead, a provision is needed.Treatment of contingent liabilitiesContingent liabilities should not be recognized in financial statements but they should bedisclosed. The required disclosures are:(a) A brief description of the nature of the contingent liability;(b) An estimate of its financial effect;(c) An indication of the uncertainties that exist;(d) The possibility of any reimbursement;(4) Contingent assetsDefinitionA possible asset that arises from the past events whose existence will be confirmed by theoccurrence of one or more uncertain future events not wholly within the enterprise’s controA contingent asset must not be recognized. Only when the realization of the relatedeconomic benefits is virtually certain should recognition take place. At that point,the asset is no longer a contingent asset.Disclosure:contingent assetsContingent assets must only be disclosed in the notes if they are probable. In that case abrief description of the contingent asset should be provided along with an estimate of its likely financial effect.II. Specific application1. Future operating lossesIn the past,provisions were recognized for future operating losses on the grounds of prudence. However these should not be provided for the following reasons.①They relate to future events;②There is no obligation to a third party. The loss-making business could be closed and the losses avoided.2. Onerous contractsAn onerous contract is a contract in which the unavoidable costs of meeting the contract exceed the economic benefits expected to be received under it.A common example of an onerous contract is a lease on a surplus factory. The leaseholder is legally obliged to carry on paying the rent on the factory,but they will not get any benefit from using the factory.The least net cost of an onerous contract should be recognized as a provision. The least net cost is the lower of the cost of fulfilling the contract or of terminating it and suffering any penalty payments.Some assets may have been bought specifically for the onerous contract. These should be reviewed for impairment before any separate provision is made for the contract itself.1DemoDroopers has recently bought all of the trade,assets and liabilities of Dolittle,anactivities have unincorporatd business. As part of the take-over all of the combined business’smises are now empty and surplus been relocated at Droopers main site. As a result Dolittle’s preto requirements.However,just before the acquisition Dolittle had signed a three year lease for their premises at $6000 per calendar month. At 31 December 2003 this lease ad 32 months left to runand the landlord had refused to terminate the lease. A sub-tenant had taken over part of the premises for the rest of the lease at a rent of $2500 per calendar month.Required(a) Should Droopers recognized a provision for an onerous contract in respect of this lease?(b) Show how this information will be presented in the financial statements for 2003 and2004. Ignore the time value of money.Solution:Droopers has a legal obligation to pay a further $192000 to the landlord,as a result of alease signed before the year end. Therefore an onerous contract exists and must be provided for.There is also an amount recoverable form the sub-tenant of $80000(32×2500). This will be shown separately in the balance sheet as an asset.The $192000 payable and the $80000 recoverable can be netted off in the income statement.income statements20032004$$provision for onerous lease contract(net)112000 Dr.net rental payable on lease (72-30)-42000 Drrelease of provision42000 Cr112000 Dr.balance sheetsreceivalbesamounts recoverable from sub-tenants80000 Dr.50000 Drliabilitiesamounts payable on onerous contracts192000 Cr120000 Cr3. RestructuringA restructuring is a programme that is planned and controlled by management and has a material effect on:①The scope of a business undertaken by the reporting entity in terms of the products or services it provides; or②The manner in which a business undertaken by the reporting entity is conducted;Restructuring includes terminating a line of business,closure of business locations,changes in management structure,and refocusing a business’s operations.Restructuring provisions have always been quite common,and have often been misused. IAS37 restricts the recognition of restructuring provisions to situations where an entity has a constructive obligation to restructure.A constructive obligation will only arise if:①There is a detailed formal plan for restructuring. This must identify the businesses,locations and employees affected; and②Those affected have a valid expectation that the restructuring will be carried out. This can be by starting to implement the plan or by announcing it to those affected.The constructive obligation must exist at the year-end.(Any obligation arising after the yearend may require disclosure under IAS10)A board decision alone will not create a constructive obligation unless:①The plan is already being implemented. For example,assets are being sold,redundancy negotiations have begun; or②The plan has been announced to those affected by it. The plan must have a strict timeframe without unreasonable delays; or③The Board itself contains representatives of employees or other groups affected by the decision.(This is common in mainland Europe.)An announcement to sell an operation will not create a constructive obligation. An obligation will only arise when a purchaser is found and there is a binding sale agreement.A restructuring provision should only include the direct costs of restructuring. These must be both:(a) Necessarily entailed by the restructuring; and(b) Not associated with the ongoing activities of the entity;The following costs must not be provided for because they relate to future events:(a) Retaining or relocating staff;(b) Marketing;(c) Investment in new systems and distribution networks;(d) Future operating losses (unless arising from an onerous contract)(e) Profits on disposal of assets.。

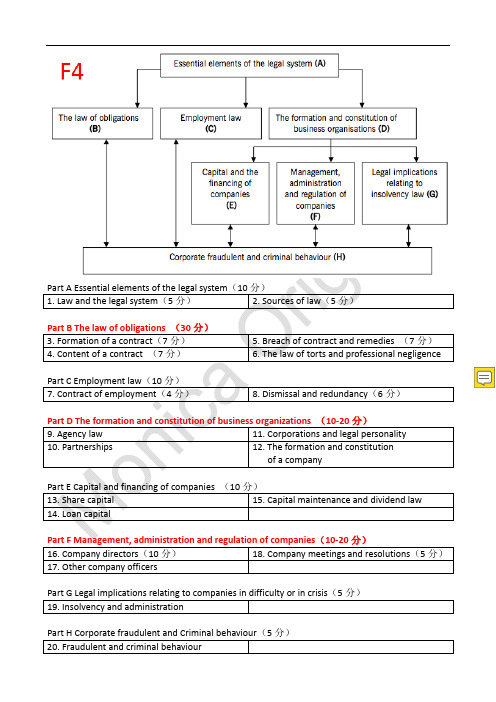

ACCA F4知识要点汇总(精简版)

1. Law and the legal system(5 分)

2. Sources of law(5 分)

Part B The law of obligations (30 分) 3. Formation of a contract(7 分) 4. Content of a contract (7 分)

European Court of Human Rights (ECtHR) 欧洲人权法院

The Privy Council 枢密院

d) In the Factortamecase(欧洲移民法和商船法): 欧洲法 EU law>欧盟成员国国内法律。 所以,最高法院的有效性受到 EU law 判决的约束。

Magistrates 治安官法院、Crown court

offences

偷盗、吸毒、对他人实施暴力 皇冠法院都可以审理

上述两种皆可能

刑事诉讼操作:

Magistrates 治安官法院

a) Summary offences without a jury 轻微罪行(没有陪审团) b) Commit defendants charged with an indictable offence to the Crown

平衡可能性,谁的证据更占优 排除合理怀疑,疑罪从无

Decision 判决结果

Remedies 法律救济 Distinct courts of instance court 初审法 院

Judge 法官:Liable/Not liable 有 责任/无责任 Damages(损害赔偿金) Magistrates 治安官法院、County court 郡法院

ACCA F4知识要点 第15章

第15章 Capital maintenance and dividend law资本的维持和分红1.Capital Maintenance 资本维护Creditor’s buffer: 公司盈利会留部分到一个储备账户,为了支付债权人的清偿,这个是留存的不能用于分红。

1.1 The single greatest advantage of trading through a company is the limited liability afforded to its members. In order to secure this companies face additional disclosure requirements, and have to follow the rules on capital maintenance, which prevent the members withdrawing their capital without restriction. 为了保证公司有额外的公开要求,公司必须遵守“资本维持”需求,来防止成员不受限制的撤回他们的资本。

The rules which dictate how a company is to manage and maintain its capital exist to maintain the delicate balance between the members’ enjoyment of limited liability and the creditors’ requirements that the company shall remain able to pay its debt.这个规则表明公司是如何保持成员享有有限责任和债权人的安全达到微妙的平衡。

1.2 The doctrine of capital maintenance operates through the maintenance of the creditors’buffer. In essence this is a collection of undistributable reserves that must be maintained by the company, thereby restricting the ability of a company to return capital to its members via dividends and share repurchases. 没有分配的利润保留,备在公司账户。

accaf阶段,p阶段

accaf阶段,p阶段ACCA F阶段-P阶段随着ACCA学习的不断深入,我们进入了ACCA F阶段的P阶段。

在这个阶段,我们将学习更加复杂和深入的会计知识和技能,为未来的职业发展打下坚实的基础。

本文将围绕P阶段展开,介绍其特点、学习内容和考试要点。

一、P阶段的特点P阶段是ACCA学习的重要阶段,也是整个F阶段的最后一个阶段。

相比于前面的三个阶段,P阶段的学习内容更加复杂和全面,要求学员具备扎实的会计基础知识和较高的学习能力。

P阶段的考试难度也相应增加,需要学员掌握的知识和技能更加全面和深入。

二、P阶段的学习内容在P阶段,我们将学习以下几个重要的会计知识点:1.高级财务报告与分析高级财务报告与分析是P阶段的核心内容之一。

在这门课程中,我们将学习如何分析和解读财务报表,评估公司的财务状况和业绩。

我们需要掌握各种财务指标和分析工具,以便能够准确地评估公司的财务状况和业绩。

2.风险管理与伦理风险管理与伦理是P阶段的另一个重点。

在这门课程中,我们将学习如何识别和评估企业面临的各种风险,并学习如何制定有效的风险管理策略。

同时,我们还将学习有关伦理和道德问题的知识,了解企业在经营活动中应该如何遵守道德规范和法律法规。

3.战略管理会计战略管理会计是P阶段的另一个重要课程。

在这门课程中,我们将学习如何将会计信息应用于战略决策和业务发展中。

我们需要掌握战略管理会计的基本概念和工具,以便能够为企业提供有效的战略决策支持。

4.高级审计与准则高级审计与准则是P阶段的最后一门课程。

在这门课程中,我们将学习如何进行高级审计工作,并熟悉国际审计准则。

我们需要了解审计的基本原理和方法,以及如何识别和解决审计中的各种问题。

三、P阶段的考试要点在P阶段的考试中,我们需要掌握以下几个重要的考试要点:1.理论与实践结合P阶段的考试注重理论与实践的结合。

我们需要了解各个知识点的理论基础,并能够将其应用于实际情况中。

在考试中,我们可能会遇到一些实际案例,需要根据所学知识进行分析和解决问题。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Chapter11. 民法(civil law)和刑法(criminal law )的划分Civil law: an form of private law , used by individuals to assert rights against other individualsCriminal law: an aspect of public law to regulate crimes and to punish offenders1. legislation(made by the Parliament)/secondarylegislation( in exercise of law-making powers delegatedby Parliament). [注:Necessity for delegatedlegislation/secondary legislation :more convenient ;can hand over the task of specifying the law in detail to experts] 2. 在case law 中:common law 普通法[created by judgesthrough the application of the principle of judicialprecedent. common law drew on customs/equity law 衡平法:to resolve disputes where damages are not asuitable remedy and to introduce fairness into the legal system.]2. 不同法院管辖事件的类型Chapter2 Chapter2 1. Doctrine of Precedence(遵循先例制度的一般规则): somedecisions made by a court are binding and similar subsequent legal cases should be decided on the basis of the law established in earlier cases.2. 可以创立判例法规则: Supreme Court/Court ofAppeal/High Court;不可以创立:Crown, Magistrates, County Courts cannot create precedent.3. Elements of judicial decision(影响法庭判决的因素):rationdecidendi 判决理由[the reason for the decision]/Obiter dicta 附带说明[statement made by the way, not binding, but merely of persuasive authority]4. 法官又可以因为那些理由拒绝先例(disregarding judicialprecedent): Overrule 取代[the procedure whereby a court higher in the legal hierarchy sets aside a legal ruling established in a previous case]/Reverse 推翻[a procedure whereby a court higher in the hierarchy reverses the decisionofalowercourtinthesamecase]/Distinguishing 法官的自由裁决[a precedent is avoided by a judge demonstrating that the material facts of two cases are not the same]5. Rules of Statutory Interpretation(法的解释):①the literalapproach :the literal rule[means that words in the Act should be given their literal and grammatical meaning rather than what the judge thinks they mean./the golden rule :this rule is applied in circumstances where the application of the literal rule is likely to result in an obviously absurd result. ②the purposive approach :the judge should ,where necessary ,look beyond the words of statute to find out the reason/purpose for its enactment,and that meaning should be interpreted in the light of the purpose[Mischief rule :purposive approach的具体表现形式/where a statute is designed to remedy a weakness in the law, the correct interpretation is the one which achieves it.]6.语言处理规则(法律没有追溯力a statute does not haveretrospective effect)Chapter3 合同法(IMP)1.合同的概念a legally binding agreement enforceable in law2.从要约到承诺是否达成agreement [invitations to treat要约邀请--offer要约--acceptance承诺----agreement]3.Termination of an offer:express rejection/counter off反要约/lapse of time/revocation of an off/death/if the off is suject toa condition,it will lapse on failure of that condition4.Privity of Contract合同相对性原则: the common law doctrinethat only those are party to the contract---have rights or liabilities under the contract/ have the right to enforce the contract,contracts cannot give rights or obligations to othersChapter41.分类标准Express and lmplied terms:某个条款是否经过双方当事人协商同意(agreed by the parties)Condition,warranties and innominate terms 核心,从属和无名条款:根据条款重要性2.免责条款(三观概念)Any clause that attempts to exempt , or limit, the liability of one party for breach of contract or negligence3 test: correctly incorporated into the contract形式正确/worded clearly to exclude the breach措辞清晰/reasonable per statute内容合理Chapter5 1.type of breach⏹Repudiatory breach根本性违约:refusal to perform拒绝履行/failure to perform an entire obligation不履行某项/incapacitation无力履行/breach ofcondition 违反核心条款/breach of an innominateterm违反无名条款⏹Anticipatory breach预期违约:未到合同履行时间,当事人提前说明无法履行;收到预期违约通知可立即追究违约责任,也可等到履行合同时间追究责任Lawful excuses for non-performance开脱责任:performance is impossible因不可预见的事情发生不可履行/尝试履行被拒绝/ the other party make it impossible for him to performance/contract is discharged through frustration情势变更/the party have been agreement permitted non-performance2.Remedies : when a breach occurs, the court has to decidewhat the appropriate remedy should be.3.Liquidated damage违约金:a genuine pre-estimate ofthe loss在订立合同前已经商定了,有利于解纠纷,如果违约金过高(远大于loss)判为惩罚性,则不可执行4.specific performance :the court directs a party tocomplete their contractual obligations以下几种情况法官不会让合同继续履行:courts cannot supervise法官无力监督履行/personal service/minors involvedChapter6 Tort侵权法A wrongful act against an individual which gives rise to a civil claim.1.过失侵权的4个证明环节(概念标准内容)Negligence:It arises when one person suffers damage or injury though the negligent act(or omission to act)of another person.①Duty of care注意义务(三步走原则)1.Reasonable foreseeability合理预见原则2.Proximity关联性原则3.Justness and fairness of imposing a duty of care公平合理地强加注意义务②A breach of that duty违反注意义务1.general rule:The test for establishing breach of duty is an objective one:a breach of duty occurs if the defendant:”...fails to do something which a reasonable man...would do.”2.Special factors to considera.The probability of injuryb.The seriousness of the risk造成伤害的严重性c.Cost and practicability成本可行性mon practice证明是行业误差范围内e.Skilled persons/professionalsf.Social benefit③The breach of duty caused harm to the claimant违反义务是导致损失的原因1.The but for test2.No break in the chain of causation切断因果关系链的要素a.A natural eventb.Act of a third party 原侵权人不承担责任c.Act of the claimant④The loss ware not too remote主张的赔偿合理Reasonable foresight只赔偿违法者可以合理预见的部分2.抗辩事由①Contributory negligence共同过失(一般只是减少赔偿额,个别情况全部免除)②Volenti non fit injuria同意不生违法(彻底免除)Chapter7 劳动法1.身份判别①Control test :The amount of control that one person had over the other②Integration test不会外包给他人的,不可或缺的③Multiple test/Economic reality testa. The regularity and method of payment报酬支付频率,支付方式b. The ownership of tools and equipment是否提供工具c. The regularity of hours of work工作时间d. The ability to delegate all the work/to provide substitute是否代理2.义务①Common Law Duties-Employers’ common law duties1)Duty of mutual trust and confidence2)To provide work for workers3)To pay wages/remuneration4)To indemnify employee against expenses and losses5)To provide for the care and safety of the employee6)No duty to provide reference when employees leave-Employees’ common law duties1) To obey reasonable and lawful orders2) To act faithfully/duty of faithful service/duty to account for all money and property3) To exercise reasonable skill and care in any activity in their role as an employee/reasonable competence to do his job4) Personal service亲自完成交付的责任②Statutory Duties1)Pay and equality不能低于国家平均2) Time off work3)Trade union officials工会组织罢工可以参加,还要给工资4) Every woman has a right to maternity leave and some are entitled to maternity pay5) Health and safety6)Working time:17week,not exceed 48 hours for each 7 days除非员工书面同意多工作7) Flexible workingChapter81.解雇通知时间的计算1m-2Y: not less than 1 week2y-12y:1 week for each year≥12y: not less than 12 week劳动者离职要提前一周通知,合同期满不续则每工作一年折合一个月工资2.自动正当参加非法集合罢工unofficial industrial action/对国家安全有威胁自动不正当怀孕pregnancy/员工参加工会活动/收购并购时的解雇dismissal on transfer of an undertaking/工作存在安全问题/最低工作标准/作息时间/员工在周天拒绝工作3.用人单位解雇不当Chapter9 代理法1.代理关系建立方式Express agreement between the agent and principal达成委托代理协议合同,口头书面皆可Implied agreement默认没有代理协议但默认存在关系Ratification追任代理人先履行合同,事后委托人建立合同关系Without consent of principal 没有征得委托人同意就建立关系necessity/Estoppel2.代理权限(3)Express authority明示代理权限Implied authority默认代理权限Apparent/ostensible authority看起来有代理权限,实际上并没有Chapter10 合伙企业法1.合伙企业(概念):the relationships that subsists betweenpersons carrying on a business in common with a view to profit. standard partnership is not s separate legal entity and its partners have full personal liability for the debts of partnership.2.Termination/dissolution合伙企业解散的债务处理:payingoff external debts/repaying to the partners any loans or advances/repaying the partner’s capital contribution/anything left over is then repaid to the partners in the profit sharing ratio .3.Termination/dissolution合伙企业解散的条件:expiry of afixed period stipulated in the partnership agreement/completion of the express purpose for which the partnership was formed/partner gives notice to leave/a new partner is admitted into the partnership/death or bankruptcy of partner/happeningof any event which makes company can’t carry on/on application by a partner the Court may decree a dissolution of the partnership4.Sole trade宏观特征:is not a separate legal entity, theperson and business are viewed as the same legal entity5.Authority合伙人的代理权限:express authority明示代理权限[from partnership agreement]/implied authority默示代理权限/apparent authority表面代理权限[已经退伙但其他人不知道]6. A partner’s liability usually extends to the period forwhich were actually a partner of a firm. 合伙人只对担任合伙人期间合伙企业产生的债务有清偿责任7.Limited Partnership(LP)特征:the partnership must beregister with the Company Registry/one or more of the partners must bear full,unlimited liability/partners with limited liability may not take part in management and cannot usually bind the business in contract/limited partner cannot withdraw their capital8.Limited Liability Partnership(LLP)特征:must be registeredwith the the Registrar of Companies, with formation documents signed by at least two members/has a legal personality separate/ the name of partnership must end with LLP/partners are known as members, of which there must be at least two/LLPs must file annual returns and accounts/all members are agents of LLP/all members’liability is limited/a designated member is responsible for administration and filing/LLP is not subject to corporation taxChapter121.设立pre-incorporation contacts谁来履行?Promoters发起人2.交什么文件①Memorandum of association公司章程(89年)②Application for registration注册申请书③A statement of capital and initial shareholdings关于公司资本坏人原始持有股份的状况说明④Statement of compliance遵从声明⑤A statement of company’s proposed officers拟任命谁为公司管理人员⑥A copy of any proposed articles of association自拟公司章程(06年)不是必须提交,没交使用默认模版3.2个证书的功能①Certificate of incorporation注册许可证Private company 只需要注册许可证,是形式审查②Trading certificate营业许可证Public company需要两个证,申领到注册许可证后一年内要申领到营业许可证,否则强制清算,是实质审查a.Allotted share capital is at least £50,000(允许股东分批缴纳)b.At least one quarter of the nominal value of the allotted share capital has been paid up(minimum £12,500)首次不低于票面的1/4,为确保一开始不会有资金困难c.Details of promoters’ expenses设立费用具体怎么产生d.A statement of compliance in respect of payment of nominal values and share premium4.章程修改的程序和内容-Contentsa. Directors’ powers and responsibilityb. Decisions making by directorsc. Appointment of directorsd. Organization and conduct of general meetingse. Issue and transference of sharesf. Payment of dividendsg. Exercise of members’ rights-Alteringa. Passing a special resolution通过股东会的特别决定,3/4以上同意批准b. Providing the alteration has been made “bona fide in the interest of the company as a whole”内容符合全体股东的意愿5.各个公司名称缩写代表含义-Ltd:Limited-plc:public limited companyChapter131.capital的分类2.普通股优先股的概念和差异3.Bonus issue红利股发行The capitalization of the reserves if a company by the issue if additional shares to existing shareholders, in proportion to their holdings. Such shares are normally fully paid-up with no cash called for from the shareholders4.Share premium概念shares may be issued at a price above their nominal value, the difference between the issue price and the nominal value is a share premium用途the issue of fully paid bonus share/writing off the preliminary expenses of company formation/writing off the discount on the issue of debentures/repurchase of debentures at a premiumChapter11 公司法The consequences of separate legal personality for the company are as follows:(1897年案例引出的规则)1: members' liability is limited.2: perpetual succession become possible as the company will need to be formally wounded-up.3: the company itself can own property.4 :the company can use, and be sued in its own name.Types of company (公司的分类)。