会计英语新第一单元

1.会计英语第一章Accounting Environment

Ⅰ. Accounting: The Language of Business ( Ⅰ) Accounting is the information system that measures business activity, processes the information into reports, and communicates the results to decisions makers.

(Ⅲ) Corporation

A corporation is a business owned by stockholders, or shareholders. These are the people who own shares of ownership in the business. Corporation differ significantly from proprietorships and partnerships in another way. If a proprietorship or a partnership can not pay its debts, lenders can take the owners’ personal assets to satisfy the business’s obligation.

Management accounting focuses on information for internal decision makers, such as the company’s executives and the administrators of a hospital.

会计英语(第二版)第一章中英文互译

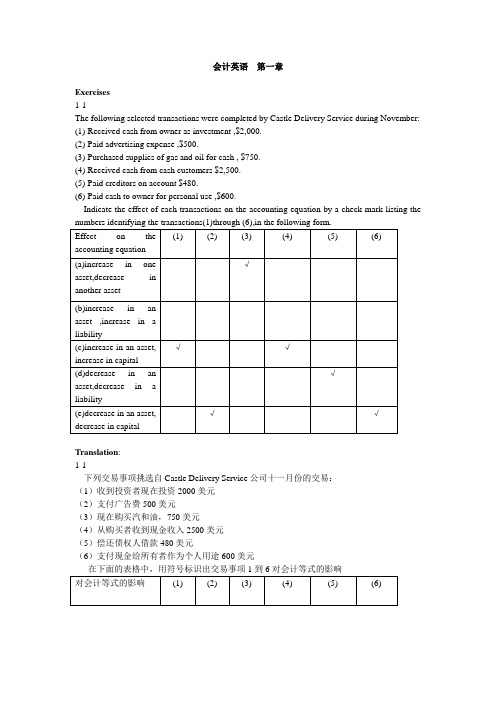

会计英语第一章Exercises1-1The following selected transactions were completed by Castle Delivery Service during November:(1)Received cash from owner as investment ,$2,000.(2)Paid advertising expense ,$500.(3)Purchased supplies of gas and oil for cash , $750.(4)Received cash from cash customers $2,500.(5)Paid creditors on account $480.(6)Paid cash to owner for personal use ,$600.Indicate the effect of each transactions on the accounting equation by a check mark listing theTranslation:1-1下列交易事项挑选自Castle Delivery Service公司十一月份的交易:(1)收到投资者现在投资2000美元(2)支付广告费500美元(3)现在购买汽和油,750美元(4)从购买者收到现金收入2500美元(5)偿还债权人借款480美元(6)支付现金给所有者作为个人用途600美元1-2Foreman Corporation, engaged in a service business , completed the following selected transactions during the period:1)Added additional investment, receiving cash2)Purchased supplies on account3)Returned defective supplies purchased on account and not yet paid for4)Received cash as a refund from the erroneous overpayment of an expense5)Charged customers for services sold on account6)Paid salary expense7)Paid a creditor on account8)Received cash on account from charge customer9)Paid cash for the owner’s personal use10)Determined the amount of supplies used during the monthTranslation :Foreman是一家从事服务行业的公司,以下是该公司在一段时间内的交易事项。

会计英语Unit 1

Exercises

Unit One

III. Decide whether the following statements are true or false. Write T for true and F for false.

( F ) 1. Accounting is another word for bookkeeping.

Unit One

4. A procedural element of accounting is _____.

A.planning B.control C√.bookkeeping D.auditing

5. Purposes of an accounting system include all of the following except _____.

按照一定的方法将相似商业交易的影响进行分类,并将其加 总或部分加总,以便提供给管理层和编制会计报告。

The development of corporation also created a new social need – the need for an independent audit to provide some assurance that management’s financial representations were reliable.

√D.all of the above

3. Accounting information is used by _____.

A.businesses

B. government regulation agencies

bor unions

√D.all of the above

会计英语(中英对照)

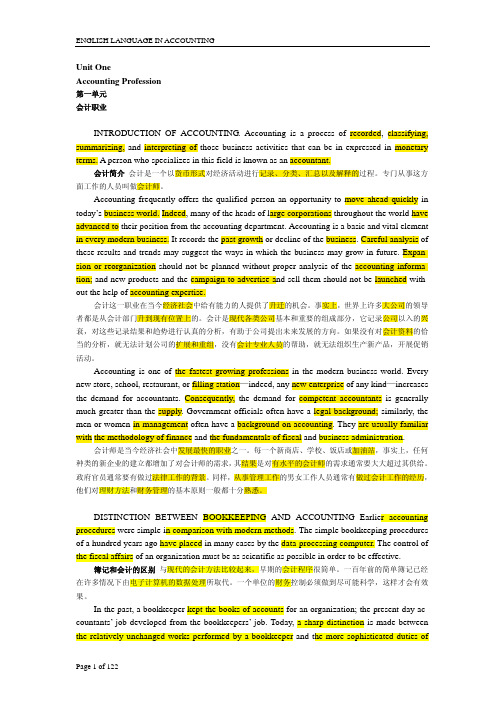

Unit OneAccounting Profession第一单元会计职业INTRODUCTION OF ACCOUNTING. Accounting is a process of recorded, classifying, summarizing, and interpreting of those business activities that can be in expressed in monetary terms. A person who specializes in this field is known as an accountant.会计简介会计是一个以货币形式对经济活动进行记录、分类、汇总以及解释的过程。

专门从事这方面工作的人员叫做会计师。

Accounting frequently offers the qualified person an opportunity to move ahead quickly in today’s business world. Indeed, many of the heads of large corporations throughout the world have advanced to their position from the accounting department. Accounting is a basic and vital element in every modern business. It records the past growth or decline of the business. Careful analysis of these results and trends may suggest the ways in which the business may grow in future. Expan-sion or reorganization should not be planned without proper analysis of the accounting informa-tion; and new products and the campaign to advertise and sell them should not be launched with-out the help of accounting expertise.会计这一职业在当今经济社会中给有能力的人提供了升迁的机会。

会计英语(0001)

会计英语第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

决策制定经济业务财务报告图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

会计英语第一章

会计英语第一课会计领域the field of accountingspecial termsaccountingcount n 计算、考虑、总计vt 计算、清点、数数儿,盘算内容极不同于calculate vt 计算、估计、推算calculator n 计算器compute v 计算,用计算机计算computer n 计算机,电脑count on 指望count out 边算便说出account n 计算、帐户(加前缀后的情况)vt vi 计算、说明accounting n 会计,会计学accountant n 会计师accountancy n 会计、会计工作on this account 由于这····on no account 决不····record n `record 记录,报告,档案,唱片发音时因动词、名词而不同。

v ri`cord 记录,表明,录音a 创纪录的classify v 分类,分等summarize v 概述,总结interpret v 解释,说明,口译还有:Business 事务,企业,实业界,经济业务等Monetary 货币的,金融的,财政的,财务的ManagementPolicy 方针、政策、策略Operation 开动、操纵、经营管理、起作用手术Carry out 从事某种工作Organization chartGraphic a 图解的,图示的Layout n 设计、布局Rank v 排列、次序、位置Cash flowReceipt n 收到,收条,收据Earning n 如同利润,net earnings 赚头,净赚Revenue n 如同收入,营业收入,毛收入Income n 如同收益如income statement 收益表Receive v 领,收,容纳Receivable a 应收的,应收款Expenditure n 支出,支付,现金支出(不见得一定是费用)Payout n 支付,支出的数额Disburse v 支付,开销Cost n v 花费,成本cost 与costing 区别Expensive a 花费多的,昂贵的Payroll n 支付的工资,工薪Expense n 花费,开支,损耗Expend v 用,消费Spend v 费,花费FiscalFinancial n 财政的,财务的,金融的(但不见得就是银行的,可银行的也能用这个词)Finanice n v 筹资,融资,贷款,财务,财政,金融,供给经费,筹措资金Financing n 筹资用资BookkeepingFinancial information 财务信息Bookkeeper 簿记员Financial transaction 财务交易Books of account 帐簿(注意与帐户之间的关系)Certified public accountantQualified opinion 保留意见Unqualified opinion 无保留意见Fair presentation 公允表达Chartered accountant 皇家特许会计师Audit(要注意这一词的广阔性)Auditing 审计,监测,审查Auditor 审计师,监测员Governmental and institutional accountingController/comptroller 主计长,总会计师Financial officer(official) CFO n 财务总监,财务经理Treasurer n 司库,财务(非会计)负责人Cost accountingAnalysis n 分析(读法)Analyze v 分析(读法)Catual unit value 实际单位价值AssetCash 现金Receivable 应收款Security 证券,此处指有价证券Property 财产Intangible 无形,此处为无形资产Goodwill 商誉Sale n 卖,销售Sell v 卖,卖出(sold sold)Purchase n 采购Buy v 买进(bought bought)Financial statement 财务报表,会计报表Managerial accountingFiscal report 财务报告Operating policy 经营方针,经营策略The purposes of accounting--recording financial information for legal and other reasons;--summarising financial information for users so that it is understandable and analysing financial information periodically so that it is useful;--communicating information for internal and external use i.e. to managers and other staff members (internal) and to users outside the business ((e)exter`nal) ;--analysis of performance to see whether performance is satisfactory;--planning and decision-making i.e. planning future activities and making business decision.The field of accounting第1段:Industry n 工业,产业,行业,也指企业(注意读法)Industrial a 工业的,产业的第2段:Business 在这里是指企业,同义词还有Corporation 公司,多指股份公司Enterprise 企业,泛指所有企业Manufactory 制造业工厂Plant 工厂,尤其是较大的工厂Factory 小工厂,作坊式厂Firm 商号,(会计师事务所)Mill 工厂,如纺织厂、粮食加工厂Shop 商店Store 商场,商城Company 泛指的公司Concern 企业Expansion 扩张Reorganization 重组Campaign 活动,指较大、有组织的系列活动,如选举,策划某一产品Movement 运动,如打打球,作体操Activity 小的活动,如记帐,生产Advertise v 注意读法(只有一个读法)Advertisement n 广告(两种读法,大概都行)第3段:第4段:Accounting procedure 会计程序Bookkeeping procedure 簿记程序Data processing 数据处理Fiscal affairs 财务业务Effect n v效果Effectiveness n 效力,效果Efficiency n 效率Economy n 经济,节省会计的艺术论及其由来;与中国现实情况的区别。

会计英语第一章解析

1.1 Nature and Content of Accounting

1.1.3 Users and Accounting Information

All parties interested in the financial health(财务状况) of a company are called stakeholders.

8

1.1 Nature and Content of Accounting

1.1.3 Users and Accounting Information

Two major classifications of stakeholders Internal users, who make decisions directly affecting the External users, internal operations who make decisions concerning their of the enterprise. relationship to the enterprise.

2

Part 1 Accounting Principle 会计原理 Chapter 1 Accounting and Its Environments 会计与环境

3

Mini Case

P2

Identify

1.Safety without war 2.Market for hang gliders sales 3.Policy from government ws and customs 5.People with well-education 6.Capital market 7.Infrastructure (基础设施)

会计英语第一章

-------------- What is Accounting?

1.1

What is Accounting

1.2

1.3 1.4

The Role of Accounting

Accounting and Bookkeeping The Accounting Process

1.5

Accounting Today

Accounting is the basic for decision making. Its purpose is to provide useful information to a variety of users so they can make informed decisions.

会计是决策的基础。它的目的是向大量的 用户提供有用的信息,从而让他们做出正 确的决策。

The Difference Between Accounting and Bookkeeping Bookkeeping Bookkeeping is the clerical side of accounting——the recording of routine transactions and day-to-day record keeping. Today such tasks are performed primarily by computers and skilled clerical personnel, not by accountant.

Basic Function of an Accounting 1.1.2 An information system System:

(1) Interpret and record the effects of

会计英语Unit 1

‹#›

• This accounting equation shows that assets are aqual to equities .会计公式表明, 资产等于权益。 • Equities are divided into liabilities and owner's equity .When any two of the elements are known,the third can be calculated.权益可分为负债和所有者权益。 当三要素中的任何两项已知,第三项即可通 过计算得知。 Phrase:divide...into...把...分成...

‹#›

Summary

• The passage tells us what is accounting,it's purpose,it's users,and it's three elements.

‹#›

Answers of Exercises

• 1.Equities = Liabilities + owner's equity • 2.A

‹#›

• These users may include owners,managers,creditors,government agencies,customers,labor unions,and competitors.这些使用者包括:所有者,经理, 债权人,政府机构,顾客,工会,以及竞争 对手。 • There are three basic accounting elements on the balance sheet:assets,liabilities,and owner's equity.They exists in every business entity.

会计英语第四版课件单元1

1.11 Owners’ Equity (Capital)

• Expenses include office rent, salaries, and utility payments etc.

1.7 The Statement of Changes in Equity

•

ABC Company

• Statement of Changes in Equity

•

For the Period Ended 2012

Beginning Contributed Capital

Plus: Capital Acquisition

Ending Contributed Capital

Beginning Retained Earnings Plus: Net Income Less: Distribution

1.9 Assets

• Asset refers to any item of economic value owned by an individual or corporation.

• Assets are divided into the following categories: current ,long-term, prepaid and deferred ,and intangible assets

• Owners’ equity refers to ownership interest in a corporation in the form of common stock or preferred stock. It also refers to total assets minus total liabilities, in which case it is also referred to as shareholders’ equity or net worth or book value.

会计专业英语新

Unit 1Finan cial in formati on about a bus in ess is n eeded by many outsiders .These outsiders in elude own ers, ban kers, other creditors, pote ntial in vestors, labor unions, gover nment age ncies ,and the public ,because all these groups have supplied money to the bus in ess or have some other in terest in the bus in ess that will be served by in formati on about its finan cial positi on and operati ng results. 许多企业外部的人士需要有关企业的财务信息,这些外部人员包括所有者、银行家、其他债权人、潜在投资者、工会、政府机构和公众,因为这些群体对企业投入了资金,或享有某些利益,所以必须得到企业财务状况和经营成果信息。

Unit 2Each proprietorship, partnership, and corporation is a separate entity.每一独资企业、合伙企业和股份公司都是一个单独的主体。

In accrual acco un ti ng, the impact of eve nts on assets and equities is recog ni zed on the acco unting records in the time periods whe n services are ren dered or utilized in stead of whe n cash is received or disbursed. That is revenue is recog ni zed as it is earn ed, and expe nses are recog ni zed as they are in curred - not when cash cha nges hands .if the cash basis acco un ti ng were used in stead of the accrual basis, revenue and expense recognition would depend solely on the timing of various cash receipts and disbursements.Unit 3During each acco un ti ng year ,a seque nee of acco un ti ng procedures called the acco unting cycle is completed.在每一会计年度内,要依次完成被称为会计循环的会计程序。

会计英语第一章练习题

会计英语第一章练习题第一题:Foreign Currency Translation外币翻译Foreign currency translation refers to the process of converting financial statements denominated in one currency into another currency. This is necessary when a company has subsidiaries or operations in different countries, or when it engages in international trade. The purpose of foreign currency translation is to present the financial information accurately and consistently to the users of the financial statements. In this article, we will discuss the key concepts and methods used in foreign currency translation.基于以下这个个案研究,回答以下问题(You may choose a specific case study related to foreign currency translation to answer the following questions.)Case Study:假设一家中国公司,有一个子公司在美国运营。

该子公司的财务报表是以美元计价的。

中国公司打算将其子公司的财务报表翻译成人民币,以便用于总公司的决策和分析。

以下是该子公司的财务报表:Income Statement销售收入:$1,000,000成本和费用:$800,000利润:$200,000Balance Sheet现金:$100,000应收账款:$300,000存货:$200,000固定资产:$500,000负债:$400,000所有者权益:$800,000Question 1:问题一:Based on the case study, explain the reasons why foreign currency translation is important for the Chinese company.根据个案研究,解释外币翻译对中国公司的重要性。

会计专业英语讲稿unit1

会计专业英语讲稿unit1Introduction (may be written last)Capture your listeners’ attention: Begin with a question, a funny story, a startling comment, or anything that will make them think.State your purpose; for example:‘I’m going to talk about...’‘This morning I want to explain…’Present an outline of your talk; for example:‘I will concentrate on the following points: First of all…Then…This will lead to… And finally…’The BodyPresent your main points one by one in logical order.Pause at the end of each point (give people time to take notes, or time to think about what you are saying).Make it absolutely clear when you move to another point. For example: ‘The next point is that ...’‘OK, now I am going to talk about ...’‘Right. Now I'd like to explain ... ’‘Of course, we must not forget that ...’‘However, it's important to realise that...’Use clear examples to illustrate your points.Use visual aids to make your presentation more interesting.The ConclusionIt is very important to leave your audience with a clear summary of everything you have covered.It is also important not to let the talk just fizzle out. Make it obvious that you have reached the end of the presentation.Summarise the main points again, using phrases like:‘To sum up...’‘So, in conclusion...’‘OK, to recap the main points…’Restate the purpose of your talk, and say that you have achieved your aim:‘I think you can now see that...’‘My intention was ..., and it should now be clear that ...’Thank the audience, and invite questions:‘Thank you. Are there any questions?’Unit One What is accounting ?Chapter ObjectivesUnderstand the definition of accountingUnderstand the function of accountingUnderstand the methods of accountingUnderstand the object of accounting.Understand the accounting elements Chapter Organisation1.1a What is the definition of accounting?1.1b What is the function of accounting ?1.1c What are the method of accounting ?1.1d What is the accounting object ?1.1e What is the accounting elements ?1.2 Core accounting terms1.3 Extended wordsCore terms reminderAccountingUnit of measurementAccountDocumentAccounting statementCostingAssetLiabilityOwner’s interestProfitIncomeExpenseCore accounting termsAccount [?‘ka?nt] n. 账户,户头Account book 账簿Accounting [?‘ka?nt??] n. 会计学,会计核算?Accounting element 会计要素Accounting object 会计对象Accounting statement 会计报表Accuracy [‘?kj?r?s?] n. 准确Asset [‘?set] n.资产Auditing['??d?t?? ] n. 审计Component[k?m‘p??n?nt] n. 成分;组成部分Costing[‘k?st??]n. 成本核算Decision-making 决策Document[‘d?kj?m(?)nt] n. 文件,单证,凭证?Double-entry bookkeeping 复式簿记Entity['ent?t?] n. 实体Expense[?k‘spens] n.费用Integrity[?n‘tegr?t?]n. 完整Legality[li?‘g?l?t?]n.合法Liability[la??‘b?l?t?]n.责任,负债Movement of fund 资金运动Owner’s interest 所有者权益Profit[‘pr?f?t]n.利润Trueness[‘tr?n?s]n.真实Parties concerned 有关各方Unit of measurement 计量单位Income[‘?nk?m]n.收入1.3 Extended wordsAnalyze [‘?n?la?z]n. 分析Calculate[‘k?lkj?le?t]vt.计算Compile [k?m‘pa?l] vt.编辑,编写Confirmation[k?nf?‘me??(?)n]n.确认Constitute [‘k?nst?tju?t]vt.构成Controlling[k?n‘tr??l??]n. 控制Currency[‘k?r(?)ns?]n.货币Ensure[?n‘]vt.确保Financial [fa?‘n?n?(?)l]adj. 财政的,财务的?Given [‘g?v(?)n]adj.特定的,指定的Inspection[?n‘spek?n]n.检查,视察Monitor [‘m?n?t?]vt.监督Orientation[,??r??n‘te??(?)n]n.定位Participate[pɑ?‘t?s?pe?t]vt.参与Process[‘pr??ses]n.过程,程序Property[‘pr?p?t?]n.财产Persue[ p??sju: ]vt.追求,从事Optimal[‘?pt?m(?)l]adj.最佳的,最理想的Providing a basis for 为……提供依据Recording[r?‘k??d??]n.记录Reflect[r?‘f lekt]vt.反映Represent[?repr?‘zent]vt.代表,表示Specific[sp?‘s?f?k]adj.特定的,具体的Vary with因……而变化Verify[‘ver?fa?]vt.核实With a view to 目的是1.1a DefinitionAccounting,①with a specific currency as its major unit of measurement,以货币作为主要计量单位②is the task of recording, calculatin g, controlling, analyzing andreporting the economic activities of a given entity/organization, 对特定实体/组织进行记录、计算、控制、分析、报告③with a view to providing financial and management information.以提供财务和管理信息的工作1.1b Functionreflect and control the process of economic activities.反映和控制经济活动过程ensure the legality, trueness, accuracy and integrity of accounting information.保证会计信息的合法、真实、准确和完整provide necessary financial data for economic management.为管理经济提供必要的财务资料participate in decision-making and pursue optimal benefit. 参与决策并谋求最佳的经济效益1.1c Methodssetting up the account and account book 设置账户和账簿filling in and auditing the accounting document 填写与审计会计凭证?double-entry bookkeeping 复式簿记costing 成本核算property inspection 财产检查compiling accounting statement 编制会计报表reviewing, checking and analyzing accounting data, etc.审阅、检查和分析会计数据等1.1d Accounting ObjectThe content that is verified and monitored within the work scope of accounting.会计工作所要核算和监督的内容Specifically, movements of fund represented in the routine operational activities of a business organization.具体来说,是指业务单位在日常经营活动中所表现出的资金运动。

会计英语 unit 1 Accounting

1.5 Professional ethics in accounting

1.1 Accounting: an information system

Accounting is an information system necessitated by the great complexity of modern business. In developing information about the activities of a business, every accounting system performs the following basic functions: ⑴ Interpret and record the effects of business transactions. ⑵ Classify the effects of similar transactions in a manner that permits determination of the various totals and subtotals useful to management and used in accounting reports. ⑶ Summarize and communicate the information contained in the system to decision-makers.

Unit One

会计,会计学 会计师,会计从业人员 簿记 企业 商业,企业 制定决策 交易,经济业务 投资者 债权人 资产

Vocabulary

liability owner’s equity / capital revenue expense income double-entry system American Institute of Certified Public Accountants (AICPA) Chinese Institute of Certified Public Accountants (CICPA)

会计英语Unit1

会计英语Unit1

‹#›

• Accoding to the American FASB,the objectives of financial reporting are to provide information that is:(1) useful to present the potential investors,creditors and other users information in making rational investment,credit,and similar decisions.财务报告的目标是向美国财务会计准则 委员会(American FASB)提供的信息,提供的信 息是:(1)在制定合理的投资、信贷和类似的决策时, 向潜在的投资者、债权人和其他用户提供信息。

A.Getting Started

• Key words

• information system信息系统 • business economic activities商业经济活动 • monetary 货币 • nonprofit organization非营利性组织 • Assurance service保证服务

‹#›

• The primary service offered by CPA firms covers assurance service and non-assurance service.Assurance service mainly includes review and auditing.注册会计师事务所提供的主要服务包括保证服 务和非保证服务。保证服务主要包括检查和审核。

会计英语第1章

◦ A unit which has independence or relative independence in management or economy.

◦ Also an economic unit stands on its own interest.

Four major accounting assumptions

◦ Business entity ◦ Going-concern ◦ Monetary unit ◦ Time period

1.2.1 Business Entity

A business entity should be accounted separately from other business entities, including its owner.

◦ Supervision function

to examine the authenticity, legality, and rationality of economic businesses of a specific accounting subject when the accounting personnel carry out the calculation function. Just as calculation function, it is one of the basic functions of accounting, and is also an important component of Chinese economic supervision system.

会计英语

Chapter 1 Overview of Accounting

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

4) income is taxed on their individual tax returns.

3 Types of business:

(1)manufacturing businesses (2)merchandising businesses

(3)service businesses

2 Organization of business

They are commonly organized as: (1)proprietorship : owned by one individual

(2)partnership : owned by two or more

(3)corporation : owners or stockholders a separate legal taxable entity. The ownership of a corporation is divided into shares of stock.

Internal users: managers 1 research and development managers 2 Purchasing managers 3 Human resource managers 4 Production managers 5 Distribution managers 6 Marketing managers 7 Service managers

4 fields of accounting:

(1) public (CPA, AICPA)

(2) private (CIA, CMA) (3) governme of accounting :

(1) (FA) financial accounting: external

一 What is accounting? ------“language of business”

Information system: business activities (monetary terms) 1 identify 2 record 3 communicate 4 report Accounting is an information system that provides reports to stakeholders about the economic activities and condition of a business.

(2) (MA) management (managerial) accounting: internal

四 Information users

external

users: 1 investors 2 creditors 3 governments agencies 4 employees and labor unions 5 customers: (decision-making life) 6 employees 7 suppliers 8 voters 9 contributors 10 the press

Questions:

Do you use accounting?

Is accounting important to you?

Exercises:

In what respect is a CPA similar to a doctor or a lawyer? Answer: CPAs offer their services to the public on an individual consultant basis for which they receive a fee. CPAs maybe self-employed or partners in a firm; or they may be employed by an accounting firm. CPAs enjoy professional status similar to that of doctors or lawyers.

二 Distinction between bookkeeping and accounting

Bookkeeping: enter data into financial record books (keep the books of accounts , unchanged work)

Accounting: analyze and interpret business transactions and events. (sophisticated; “art”)

三 Nature of a business

1 Business --------- organization which make the use of basic resources (input) to provide goods or services (outputs) to customers. Objective :maximize profits.

(4) limited liability corporation:

1) combines attributes of a partnership and a corporation in that it is organized as a corporation. 2) but it taxed as a partnership. 3) its owners liability is limited to their investment.

Unit One

Introduction

Objectives:

1

Describe the nature of business and the role of accounting in business.

Grasp the definition of accounting.

2

3

Kwon about the information users of accounting.