精品课程《财务管理基础》英文课件ch(8)PPT课件

合集下载

《财务管理基础》PPT课件

20.3

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition. © Pearson Education Limited 2009. Created by Gregory Kuhlemeyer.

Bonds and Their Features

4. Discuss the advantages and disadvantages of issuing/buying the three different types of long-term securities from the perspective of both the issuer and investor.

Bond – A long-term debt instrument with a final maturity generally being

10 years or more.

Basic Terms

Par Value

Coupon Rate

Maturity

Bond Ratings

20.4

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition. © Pearson Education Limited 2009. Created by Gregory Kuhlemeyer.

3. Explain the differences between various types of longterm securities in terms of claims on income and assets, maturities, security holders' rights, and the tax treatment of income from the securities.

财务管理英文课件

Early 20th century:

Concentrated on reporting to outsiders.

Early 21st century:

Insiders managing and controlling

the firm’s financial operations.

Copyright © 2003 Pearson Education Australia Pty Limited

• Interest in these topics grew and in turn spurred interest in security analysis, portfolio theory and caopyright © 2003 Pearson Education Australia Pty Limited

Slide: 1 - 7

Chief accountant is also called financial controller, whose responsibilities include financial reporting to outsiders as well as cost and managerial accounting and financial analysis on behalf of the firm’s managers.

Copyright © 2003 Pearson Education Australia Pty Limited

Slide: 1 - 5

• Capital budgeting became a major topic in finance.

• This led to an increased interest in related topics, most notably firm valuation.

财务专业英语ppt课件

E1-2 Divide into groups as instructed by your professor and discuss the following:

a. How does the description of accounting as the "language of business" relate to accounting as being useful for investors and creditors?

a. Information used to determine which products to produce. b. Information about economic resources, claims to those resources,

and changes in both resources and claims. c. Information that is useful in assessing the amount, timing, and

•Definition of Accounting: business language information system basis for decisions

•Types of Accounting Information: (1)Financial Accounting: •Internal users

篮球比赛是根据运动队在规定的比赛 时间里 得分多 少来决 定胜负 的,因 此,篮 球比赛 的计时 计分系 统是一 种得分 类型的 系统

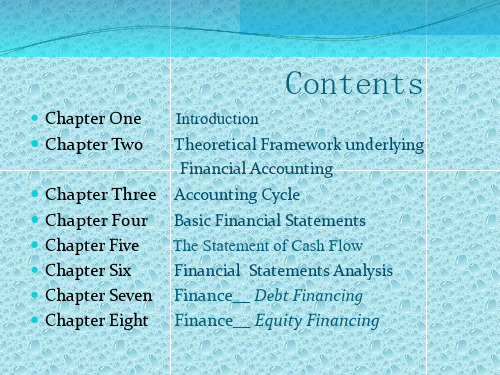

Contents

Chapter One

Chapter Two

Chapter Three Chapter Four

a. How does the description of accounting as the "language of business" relate to accounting as being useful for investors and creditors?

a. Information used to determine which products to produce. b. Information about economic resources, claims to those resources,

and changes in both resources and claims. c. Information that is useful in assessing the amount, timing, and

•Definition of Accounting: business language information system basis for decisions

•Types of Accounting Information: (1)Financial Accounting: •Internal users

篮球比赛是根据运动队在规定的比赛 时间里 得分多 少来决 定胜负 的,因 此,篮 球比赛 的计时 计分系 统是一 种得分 类型的 系统

Contents

Chapter One

Chapter Two

Chapter Three Chapter Four

财务管理英文课件

Copyright © 2003 Pearson Education Australia Pty Limited

Slide: 1 - 5

• Capital budgeting became a major topic in finance.

• This led to an increased interest in related topics, most notably firm valuation.

The more risk the firm is willing to assume, the higher the expected return from a given course of action.

Copyright © 2003 Pearson Education Australia Pty Limited

chapter 1 & 3 Scope and environment of

financial management

Copyright © 2003 Pearson Education Australia Pty Limited

Slide: 1 - 1

Development of Financial Management

Copyright © 2003 Pearson Education Australia Pty Limited

Slide: 1 - 10

Shareholder wealth maximisation?

Same as:

1. Maximising firm value 2. Maximising share values

Slide: 1 - 16

Risk and Returns

企业财务管理基础知识(ppt 19页)(英文版)

Dr. Chak-Tong Chau

Fulbright Guest Lecture Materials

4

Usefulness of Information

How do we know, a priori, that information is “useful”?

Consider the following payoff structure (known to all):

Y1

{S1}

Y2

{S2, S3}

Y3

{S4, S5, S6}

This new information system partitions the matrix as follows

Signal: Y1

Y2

Y3

S1

S2

S3

S4

S5

S6

e1=10 2

3

3

4

5

5

e2= 5 2

2

3

4

4

5

Question: Are the signals, Y1,,Y2 and Y3 useful?

Consider this new contingent contract (corresponding payoffs):

Prob. e1=0 e2= 5

e3= 6

S1 0.25

0 14,722 (20,000) 14,722 (20,000)

S2 0.25

0 14,722 (20,000) 20,544 (30,000)

S1

S2

S3

S4

Expected Expected

Prob. 0.25

0.25

0.25

财务管理专业英语PPT课件

2020/2/21

山东轻工业学院商学院

9

1)Account、Accounting & Accountant

Accountant:会计师、会计人员 Certified Public Accountant 注册会计师(CPA)

2020/2/21

山东轻工业学院商学院

10

2)Assets、Liabilities & Owner’s Equity

2020/2/21

山东轻工业学院商学院

16

Cash

$50,000 Current liabilities (4)

Accounts receivable 50,000 Long-term debt

(5)

Inventory

(1)

Shareholders’ equity (6)

Plant and equipment

10% Total assets turnover = 2 times Sales = $2 million Debt ratio = 50%

9. Capital Structure 资本结构

10. Dividend Policy 股利政策

11. Working Capital Management 营运资本管理

2020/2/21

山东轻工业学院商学院

5

一、Contents—内容

12. International Financial Management 国际财务管理

会计科目;账户

2020/2/21

山东轻工业学院商学院

8

1)Account、Accounting & Accountant

Accounting:会计、会计学 Financial Accounting and Managerial Accounting are two major specialized fields in Accounting. 财务会计和管理会计是会 计的两个主要的专门领域。 Accounting elements 会计要素

财务管理英文版166页PPT文档

Basket Wonders Statement of Earnings (in thousands) for Year Ending December 31, 2019a

Ⅰ.Primary Types of Financial Statements

Balance Sheet

A summary of a firm’s financial position on a given date that shows total assets = total liabilities + owners’ equity.

Examples of External Uses of Statement Analysis

Trade Creditors -- Focus on the liquidity of the firm. Bondholders -- Focus on the long-term cash flow of

Basket Wonders Balance Sheet (thousands) Dec. 31, 2019a

Cash and C.E.

$

a. How the firm stands on

90 Acct. Rec.c

a specific date.

394 Inventories

b. What BW owned.

16

Other Accrued Liab. d 100

Current Liab. e $ 500

Long-Term Debt f

530

Shareholders’ Equity

Com. Stock ($1 par) g

200

Add Pd in Capital g

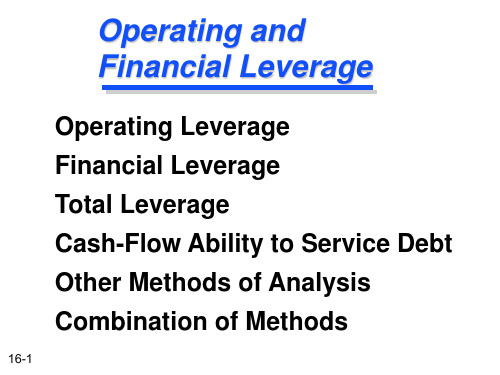

财务管理英文课件Operating-and-Financial-Leverage.ppt

16-4

Impact of Operating Leverage on Profits

(in thousands) Firm F Firm V Firm 2F

Sales

$15

Operating Costs

$16.5 $29.25

Fixed

7

Variable

3

Operating Profit $ 5

Break-Even (Quantity) Point

Break-Even Point -- The sales volume required so that total revenues and total costs are equal; may be in units or in sales dollars.

volume.

When studying operating leverage, profits refers to operating profits before taxes (i.e., EBIT) and excludes

debt interest and dividend payments.

16-1

Operating Leverage

Operating Leverage -- The use of fixed operating costs by the firm.

One potential effect caused by the presence of operating leverage is that a change in the volume of sales results in a more than proportional change in operating profit (or loss).

Impact of Operating Leverage on Profits

(in thousands) Firm F Firm V Firm 2F

Sales

$15

Operating Costs

$16.5 $29.25

Fixed

7

Variable

3

Operating Profit $ 5

Break-Even (Quantity) Point

Break-Even Point -- The sales volume required so that total revenues and total costs are equal; may be in units or in sales dollars.

volume.

When studying operating leverage, profits refers to operating profits before taxes (i.e., EBIT) and excludes

debt interest and dividend payments.

16-1

Operating Leverage

Operating Leverage -- The use of fixed operating costs by the firm.

One potential effect caused by the presence of operating leverage is that a change in the volume of sales results in a more than proportional change in operating profit (or loss).

财务管理学及财务知识分析(英文版)(PPT 31页)

= 7.0% + (6.0%)1.2 = 14.2%.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

10 - 17

What’s the DCF cost of common equity, ks? Given: D0 = $4.19; P0 = $50; g = 5%.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

10 - 14

Opportunity cost: The return stockholders could earn on alternative investments of equal risk.

Use this formula: kpD P p p$1 $1 1 .1 0 1 00.09 9 0 .0%.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

10 - 8

Picture of Preferred Stock

0

kp = ?

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

10 - 16

What’s the cost of common equity based on the CAPM?

kRF = 7%, RPM = 6%, b = 1.2.

ks = kRF + (kM – kRF )b.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

10 - 17

What’s the DCF cost of common equity, ks? Given: D0 = $4.19; P0 = $50; g = 5%.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

10 - 14

Opportunity cost: The return stockholders could earn on alternative investments of equal risk.

Use this formula: kpD P p p$1 $1 1 .1 0 1 00.09 9 0 .0%.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

10 - 8

Picture of Preferred Stock

0

kp = ?

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

10 - 16

What’s the cost of common equity based on the CAPM?

kRF = 7%, RPM = 6%, b = 1.2.

ks = kRF + (kM – kRF )b.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

财务管理英文课件

利润分配原则: 公平、公正、公 开

利润分配方式: 现金分红、股票 分红、实物分红 等

利润分配比例: 根据公司经营状 况、股东权益等 因素确定

利润分配时间: 根据公司财务状 况和股东需求确 定

财务预算

预算编制:根据公司战略和经营计划,制定财务预算 预算内容:包括收入、成本、费用、利润等各项财务指标 预算执行:按照预算执行,确保各项财务指标的实现 预算调整:根据实际情况,对预算进行调整,确保预算的准确性和可行性

社会环境:社会文化、价值观等 对企业财务管理的影响

添加标题

添加标题

添加标题

添加标题

法律环境:企业财务管理的法律 框架和规定

技术环境:新技术对企业财务管 理的影响,如云计算、大数据等

财务决策制定

投资决策

投资目标:确定 投资目标,如收 益最大化、风险 最小化等

投资策略:选择 合适的投资策略, 如分散投资、长 期投资等

财务分析

财务比率分析

流动比率:衡量企业短期偿债能力

权益乘数:衡量企业财务杠杆水平

速动比率:衡量企业立即偿债能力 资产负债率:衡量企业长期偿债能力

利息保障倍数:衡量企业偿付利息能 力

现金流量比率:衡量企业现金流量状 况

财务趋势分析

趋势分析的定义和目的 趋势分析的方法和工具 趋势分析的步骤和流程 趋势分析的应用和案例

财务管理基础知识

财务管理的概念

财务管理是组织 对资金、资产、 负债、收入、支 出等财务活动的 管理

财务管理的目标 是实现企业价值 最大化

财务管理的内容 包括财务计划、 财务控制、财务 决策、财务分析 等

财务管理的原则 包括成本效益原 则、风险控制原 则、信息透明原 则等

财务管理培训课程英文版23页PPT.pptx

10- 1

Topics Covered

Measuring Beta Portfolio Betas CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk

Irwin/McGraw-Hill

©The McGraw-Hill Companies, Inc.,2001

T u rb o R etu rn % + 0 .8 + 1 .8 - 0 .2 - 1 .8 + 0 .2 - 0 .8

Irwin/McGraw-Hill

©The McGraw-Hill Companies, Inc.,2001

10- 6

Measuring Market Risk

Example - continued

10- 12

Measuring Market Risk

Security Market Line - The graphic representation of the CAPM.

40

Expected Return (%) .

Rm 20

Rf 0 0

Irwin/McGraw-Hill

Security Market Line

When the market was down 1%, Turbo average % change was -0.8%

The average change of 1.6 % (-0.8 to 0.8) divided by the 2% (-1.0 to 1.0) change in the market produces a beta of 0.8.

Irwin/McGraw-Hill

Topics Covered

Measuring Beta Portfolio Betas CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk

Irwin/McGraw-Hill

©The McGraw-Hill Companies, Inc.,2001

T u rb o R etu rn % + 0 .8 + 1 .8 - 0 .2 - 1 .8 + 0 .2 - 0 .8

Irwin/McGraw-Hill

©The McGraw-Hill Companies, Inc.,2001

10- 6

Measuring Market Risk

Example - continued

10- 12

Measuring Market Risk

Security Market Line - The graphic representation of the CAPM.

40

Expected Return (%) .

Rm 20

Rf 0 0

Irwin/McGraw-Hill

Security Market Line

When the market was down 1%, Turbo average % change was -0.8%

The average change of 1.6 % (-0.8 to 0.8) divided by the 2% (-1.0 to 1.0) change in the market produces a beta of 0.8.

Irwin/McGraw-Hill

财务管理会计案例培训课件英文版

costs of the activity involved.

Product-Level Activity

Organizationsustaining Activity

Customer-Level Activity

Identifying Activity to Include

Activity Cost Pool is a “bucket” in

Factory equipment depreciation

$300,000

Percent consumed by customer orders 20%

$ 60,000

Assigning Costs to Activity Cost Pools

Using the total costs and percentage consumption of overhead, costs are assigned to activity pools.

and then to products.

Departmental Overhead Rates

Indirect

Stage One:

Labor

Costs assigned

to pools

Cost pools

Department 1

Indirect Materials

Department 2

Other Overhead

Activity Based Costing

Departmental Overhead Rates

Plantwide Overhead

Rate

Overhead Allocation

Plantwide Overhead Rate

Product-Level Activity

Organizationsustaining Activity

Customer-Level Activity

Identifying Activity to Include

Activity Cost Pool is a “bucket” in

Factory equipment depreciation

$300,000

Percent consumed by customer orders 20%

$ 60,000

Assigning Costs to Activity Cost Pools

Using the total costs and percentage consumption of overhead, costs are assigned to activity pools.

and then to products.

Departmental Overhead Rates

Indirect

Stage One:

Labor

Costs assigned

to pools

Cost pools

Department 1

Indirect Materials

Department 2

Other Overhead

Activity Based Costing

Departmental Overhead Rates

Plantwide Overhead

Rate

Overhead Allocation

Plantwide Overhead Rate

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2-8

Summary for Partnership

Advantages Can be simple Low setup cost, higher than sole proprietorship Relatively quick setup Limited liability for limited partners

Sole Proprietorships Partnerships (general and limited) Corporations Limited liability companies

2-4

The Business Environment

Sole Proprietorship -- A business form for which there is one owner. This single owner has unlimited liability for all debts of the firm.

Limited Partnership -- limited partners have liability limited to their capital contribution (investors only). At least one general partner is required and all general partners have unlimited liabil College, Waukesha, WI

After studying Chapter 2,

you should be able to:

1. Describe the four basic forms of business organization in the United States -- and the advantages and disadvantages of each.

financing offers a tax advantage over both common and preferred stock financing. 5. Describe the purpose and make up of financial markets. 6. Demonstrate an understanding of how letter ratings of the major rating agencies help you to judge a security’s default risk. 7. Understand what is meant by the term “term structure of interest rates” and relate it to a “yield curve.”

Oldest form of business organization. Business income is accounted for on your personal income tax form.

2-5

Summary for Sole Proprietorship

Advantages Simplicity Low setup cost Quick setup Single tax filing on individual form

Business income is accounted for on each partner’s personal income tax form.

2-7

Types of Partnerships

General Partnership -- all partners have unlimited liability and are liable for all obligations of the partnership.

Chapter 2

The Business, Tax, and Financial Environments

© Pearson Education Limited 2004

Fundamentals of Financial Management, 12/e

Created by: Gregory A. Kuhlemeyer, Ph.D.

2-6

Disadvantages

Unlimited liability

Hard to raise additional capital

Transfer of ownership difficulties

The Business Environment

Partnership -- A business form in which two or more individuals act as owners.

2-2

The Business, Tax, and Financial Environments

The Business Environment The Tax Environment The Financial Environment

2-3

The Business Environment

The U.S. has four basic forms of business organization:

2-9

Disadvantages

Unlimited liability for the general partner

2. Understand how to calculate a corporation's taxable income and how to determine the corporate tax rate - both average and marginal.

3. Understand various methods of depreciation. 4. Understand why acquiring assets through the use of debt

Summary for Partnership

Advantages Can be simple Low setup cost, higher than sole proprietorship Relatively quick setup Limited liability for limited partners

Sole Proprietorships Partnerships (general and limited) Corporations Limited liability companies

2-4

The Business Environment

Sole Proprietorship -- A business form for which there is one owner. This single owner has unlimited liability for all debts of the firm.

Limited Partnership -- limited partners have liability limited to their capital contribution (investors only). At least one general partner is required and all general partners have unlimited liabil College, Waukesha, WI

After studying Chapter 2,

you should be able to:

1. Describe the four basic forms of business organization in the United States -- and the advantages and disadvantages of each.

financing offers a tax advantage over both common and preferred stock financing. 5. Describe the purpose and make up of financial markets. 6. Demonstrate an understanding of how letter ratings of the major rating agencies help you to judge a security’s default risk. 7. Understand what is meant by the term “term structure of interest rates” and relate it to a “yield curve.”

Oldest form of business organization. Business income is accounted for on your personal income tax form.

2-5

Summary for Sole Proprietorship

Advantages Simplicity Low setup cost Quick setup Single tax filing on individual form

Business income is accounted for on each partner’s personal income tax form.

2-7

Types of Partnerships

General Partnership -- all partners have unlimited liability and are liable for all obligations of the partnership.

Chapter 2

The Business, Tax, and Financial Environments

© Pearson Education Limited 2004

Fundamentals of Financial Management, 12/e

Created by: Gregory A. Kuhlemeyer, Ph.D.

2-6

Disadvantages

Unlimited liability

Hard to raise additional capital

Transfer of ownership difficulties

The Business Environment

Partnership -- A business form in which two or more individuals act as owners.

2-2

The Business, Tax, and Financial Environments

The Business Environment The Tax Environment The Financial Environment

2-3

The Business Environment

The U.S. has four basic forms of business organization:

2-9

Disadvantages

Unlimited liability for the general partner

2. Understand how to calculate a corporation's taxable income and how to determine the corporate tax rate - both average and marginal.

3. Understand various methods of depreciation. 4. Understand why acquiring assets through the use of debt