UC Berkeley Haas 投资银行案例大赛 模板

《哈佛商业评论》案例大赛参赛文案

3

方案实施阶段

根据实际情况而定,一般需要3-6个月的时间。

预期效果

市场拓展

通过方案的实施,拓展市场份 额,提高品牌知名度和美誉度

。

销售增长

通过方案的实施,促进销售增 长,提高销售额和利润水平。

客户满意度提升

通过方案的实施,提高客户满 意度,增强客户忠诚度。

团队能力提升

通过方案的实施,提升团队的 市场分析能力、策划能力和执

政策调整风险

政府政策的调整可能对企业的经营产生重大影响,如税收 政策、环保政策等。企业应关注政策变化,及时调整经营 策略以适应政策变化。

竞争风险

竞争风险总结 竞争对手风险

替代品风险 潜在进入者风险

企业在市场竞争中面临来自竞争对手、替代品和潜在进入者的 压力。

竞争对手可能通过价格战、广告战、技术革新等方式抢占市场 份额。企业应不断提升自身竞争力,以应对竞争对手的挑战。

解决方案

03

详细阐述提出的解决方案,分析解决方案的可行性和有效性,

以及实施方案的具体步骤和措施。

对行业的展望

行业趋势

分析所在行业的未来发展趋势,包括技术、市场、竞争等方面的 变化。

行业挑战

探讨所在行业面临的挑战和难题,提出应对策略和解决方案。

行业机遇

发现所在行业的潜在机遇,提出抓住机遇的思路和措施。

关键流程

分析公司实现价值主张的关键流程,包括生产流程、销售流程等。

盈利模式

分析公司的盈利模式,包括收入来源、成本结构、盈利水平等,探 究公司如何实现盈利和可持续发展。

CHAPTER 03

案例解决方案

战略调整方案

01

02

03

04

总结词

投资银行跨国并购案例(范文)

投资银行跨国并购案例(范文)第一篇:投资银行跨国并购案例(范文)娃哈哈和达能集团的跨国并购案例达能并购失败的原因作为合资公司的大股东,并且在合资公司拥有娃哈哈商标权的前提下,达能集团对娃哈哈非合资部分的公司的强势并购为什么会失败呢?我认为原因有以下4点:1.在最初商标的转让的时候,两家公司实际上签订了“阴阳合同”,而国家商标局通过的《商标使用许可合同》中并不包括转让商标的条款,因此娃哈哈商标的转让实际上并没有通过国家商标局的批准。

2.由于非合资公司的总资产达56亿元,2006年利润达10.4亿元,因此如果收购完成的话,达能在中国的食品饮料行业将造成事实上的垄断,从而违反了相关法律的要求。

3.娃哈哈集团是由董事长宗庆后一手发展起来的,整个企业凝聚力强,因此在事态全面升级之后,娃哈哈集团员工代表、销售团队以及管理层几乎同时声援宗庆后,也给达能的并购造成了不小的难度。

4.娃哈哈作为民族企业的特殊性,不仅拥有广大的消费者基础,就是甚至连地方政府都声援娃哈哈,从而最终引起了国家领导人的关注。

而也正是通过两国国家领导人的协调,这次并购危机才得以化解。

思考与启示1.外资通过并购形成垄断,限制本土品牌的市场竞争近年来跨国公司通过系统性和大规模的并购,尤其是对行业龙头企业展开围剿和并购,在我国某些行业形成垄断,不能不引起我们的警觉。

法国达能集团并购娃哈哈如果获得成功的话,将会导致我国饮料行业外资控制市场的格局,从而形成对我国饮料市场的垄断,并限制其他中小企业的市场竞争,从而给我国果汁饮料市场竞争格局造成不利的影响。

2.外资并购与民族品牌的保护品牌是企业最重要的无形资产,也是企业市场竞争的利器,尤其是对于娃哈哈这种民族企业来说,品牌的保护显得尤为重要。

一旦民族品牌流失,对市场的控制力,创业者的信心,消费者的心理甚至国家的经济都会造成不小的影响。

因而,我国应该大力培育民族品牌,并对民族知名品牌提供必要的保护。

3.并购案例的警示就娃哈哈这个案例而言,此次跨国并购的教训之一在于我国企业在利用外资方面急于求成,弄巧成拙,同时对于合资和并购的有关法律法规缺乏专业了解,容易陷入外资并购陷阱和圈套。

投资银行业务的五大经典案例

投资银行业务的五大经典案例第一章:高盛与亚洲金融危机1997年,亚洲发生了一场金融危机,许多国家的货币贬值,债券市场崩盘。

当时,在亚洲的许多投资银行都陷入了困境。

而高盛却抓住了机会,成功地帮助客户进行了很多收购交易,挣得了大量的利润,成为当时亚洲金融危机中的一匹黑马。

第二章:JP摩根和华电国际2000年,中国华电集团在香港上市。

JP摩根是这次IPO的牵头保荐人之一,同时还参与了部分股权的购买。

在IPO过程中,JP摩根把卖方和买方的利益进行了很好的平衡,获得了客户的高度评价。

第三章:摩根士丹利和谷歌2004年,谷歌在纳斯达克上市。

摩根士丹利是这次IPO的独家保荐人,成功地完成了$19.6亿的融资。

由于该公司当时市值较低,摩根士丹利在为谷歌提供帮助的同时,也获得了很高的回报。

第四章:高盛和美国次贷危机2008年,美国爆发了次贷危机,许多投资银行都遭受了巨大的损失。

但高盛利用自身的风险管控能力,及时摆脱次贷危机的风险,还利用低价收购了许多财务稳健的机构。

这些举措最终帮助高盛度过了这一困难时期。

第五章:摩根士丹利和迪士尼2018年,迪士尼计划收购21世纪福克斯娱乐的部分资产。

摩根士丹利担任该交易的顾问,帮助迪士尼实现了这样一笔巨额的交易。

该交易的成功,也是摩根士丹利在娱乐产业领域的又一大成功案例。

结语以上五个经典案例,展示了投资银行业务的多种面貌,也充分证明了投资银行在当今商业世界中的重要性。

投资银行以其丰富的经验和技术优势,为客户提供多种服务,为客户创造价值。

在未来,投资银行业务将继续发展壮大,为各种交易提供专业服务,创造更多的商业价值。

英文投行案例分析报告

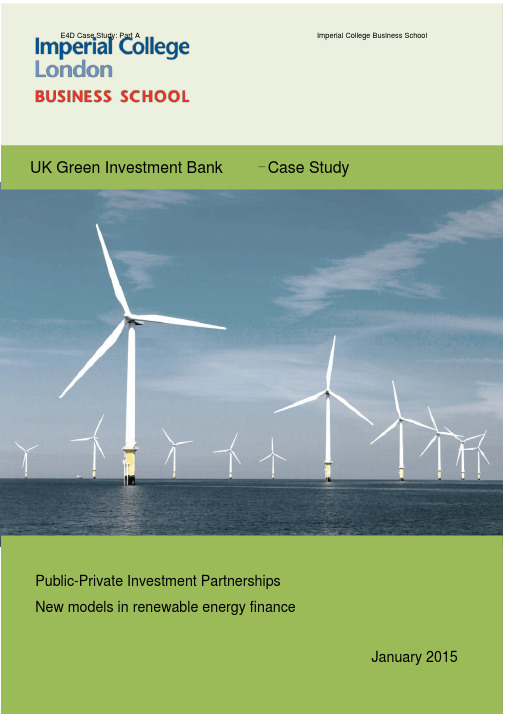

E4D Case Study: Part A Imperial College Business SchoolUK Green Investment Bank – Case StudyPublic-Private Investment PartnershipsNew models in renewable energy financeJanuary 2015UK Green Investment BankAbstractThe UK Green Investment Bank (UKGIB) became operational in October 2012, supported by £3 billion (approximately $5 billion) of government money. As part of a multifaceted climate change strategy enacted by the United Kingdom, the bank wasfounded with a m ission of “accelerating the UK’s transition to a more green economy,With anand creating an enduring institution, operating independently of government”. experienced, professional management team in place, the UKGIB's immediate taskate sector funding on new large-scale clean energy infrastructure.was to ‘crowd in’ privBut while the strategic mandate for the bank was clear, a series of tactical issues remained about how to select new investments and manage its growing investmentportfolio. For instance, how would the team be able to manage conflicting public andprivate interests? What specific type of investments would best counter market scepticism about the renewable energy projects? Most importantly, what investmentevaluation framework would enable them to deliver on their vision of being both ‘greenand profitable’?This case was prepared by Christopher Corbishley and Charles Donovan. The authors acknowledgethe support of the UK Green Investment Bank staff for their invaluable assistance in gathering thematerial for this case study.This case is for educational purposes and is not intended to illustrate either effective or ineffective management of an organisational situation. The situations and circumstancesdescribed may have been dramatized or modified for instructional purposes and may not accurately reflect actual events.This case study is provided free of charge under an Attribution-Non-commercial-No-DerivationsCreative Commons licence. You may download this work free of charge and share it freely. The casestudies may not, however, be changed in any way or used commercially.Motivations for a Green Investment BankFollowing the enactment of the Climate Change Act of 2008, the United Kingdommade a legal commitment to significantly reduce its carbon emissions by 2050 and togenerate up to 15% of energy from renewable sources by 2020. To meet these goals,a committee established by the UK House of Commons estimated that between £200billion and £1 trillion of new investment would be needed over the next two decades. Traditional sources of capital for green infrastructure were thought to be able to provide no more than £80 billion over this period.The analysis presented a serious investment shortfall, a situation exacerbated by theglobal financial crisis. New European guidelines would put large commercial banksunder immense pressure to reduce the size of their balance sheets. The perceivedrisks associated with renewable technologies meant investments into green energy infrastructure were falling dramatically (Figure 1).Figure 1: UK Renewable Energy Investment by segment (£bn)Source: UKGIB Annual Report 2013/14A series of influential reports subsequently observed a ‘market failure’ in the renewable energy sector, and hence advocated the creation of a state-backed infrastructure bank. Despite additional austerity measures sweeping across a number of government departments, after the 2010 general election the government budget contained the.first mention of a ‘green investment bank’By 2011, plans were set out for the activation of a Green Investment Bank in threephases (see Appendix 1): (i) Incubation within the department of Business, Innovation& Skills and the first direct financial investments by the UK government into the green economy; (ii) Establishment of the UKGIB as a stand-alone institution by 2012, and(iii) Commitment of full borrowing powers by 2015-16 "subject to public sector's net-debt falling as a percentage of GDP"."This is a big advance, the first investment bank in the world dedicated to greeningthe economy. It's a great achievement and an example of how the Government isworking together with the private sector to get big, long-term projects off the groundin a way that leaving it to the pure, free market can't do.”UK Business Secretary Vince CableOn 27 November 2012 the UK Green Investment Bank was established pending-approval from the European Union (EU) that its operations were not considered ‘anticompet itive’under state-aid regulations. Approval was granted soon after on the basis, which isthat the GIB’s lending and investment activities be “additional to the market”investors from the private sector, distortingto say the Bank must avoid “crowding out” existing markets or conferring any unfair advantage on certain market participants.Unique from most government initiatives, the GIB was required to work on aRather than providing grants,commercial basis, to be both ‘green and profitable’.regional assistance or one-off development loans, its purpose was to “crowd in” private. Thiscapital into renewable energy investments, as opposed to “crowding them out”occurs when public sector spending either replaces or drives down private sectorinvestment as a result of the government providing a good or a service (such asfinancing) that would otherwise be a business opportunity for the private sector. Aspart of this, the Bank was mandated to focus 80% of its activities on four priority sectors: Offshore wind,in which the market was perceived to have ‘failed’. These includedenergy efficiency, waste recycling and energy from waste.The UK’s Green Investment Bank model differs somewhat from its European counterparts, such as Germany’s much larger KfW bank, described as ‘the largest IFI and the European Investment Fund, which predominately providesin the world’ guarantees. It differs in its remit specifically to address a market failure in the ‘gre sector, as well as its obligation to be profitable. The GIB model has since become abeacon in other developed countries. In 2013 the New York Mayor, Andrew Cuomowith theannounced $210 million in initial capitalization for the ‘New York Green Bank’ aim eventually to hit a target $1 billion capitalization.Structured as a Public Limited Company (PLC) 100% owned by the UK Government,the GIB’sArticles of Association ensured it would maintain total operational independence, (see Appendix 2) representing a new form of public private partnership(PPP). Vested with £3 b illion of taxpayer capital, and the ability to structure greenenergy investment products across the capital structure, (from senior debt to equity),the bank was tasked with the execution of a critical government policy, one meant toensure the UK’s energy future needs were met.Renewables: The ‘Ugly Duckling’ of Infrastructure FinancingAs part of meeting its state aid mandate, the Bank was initially focussed on definingit was designed to address. Most assumed the failures were anthe ‘market failures’ inevitable cause of negative economic externalities, specifically the lack of a clearprice for carbon. This meant without intervention, the social costs of environmentalimpact were not borne by investors and the private sector, nor was the social benefitof more sustainable projects being captured or invested in.The global financial crisis had a profound impact on green infrastructure investment,as well as infrastructure financing more generally. Pressure from regulators, shareholders and governments to de-lever and de-risk made long-term financing aless attractive proposition for banks. The majority of risk came from what banks call. However, bank appetites to “maturity transformation” i.e. borrowing short to lend longhold long-term assets had diminished in favour of short-term financing due to the‘funding mismatch’ risk of financing longer-term project debt.Credit performance of infrastructure finance has previously been strong for the banks.Yet many commercial players were increasingly finding the cost of funding exceededthe margins on their books. This had become a particular problem in Europe, whichhistorically relied on a number of banks committed to long-term project financing. Inlobalcontrast to the ‘institutional’ structure of capital markets in North America, the gfinancial crisis had broken the European model of bank-led project financing, suggesting a new institutional structure was required for the UK.Tied to this was the fact that in a global economic environment of exceedingly lowlong-term interest rates, investment institutions needed to identify real (inflation protected) yields to match the quantum and maturity of their pension liabilities. Hencethe missing piece in this puzzle was the presence of new market infrastructure (i.e. the intermediaries and investment vehicles) that connected pools of capital with investment projects.Risks and uncertainties around clean technologiesInformation asymmetries and risk aversion have presented additional barriers to achieving higher levels of green infrastructure investment from private sector investors. As a relatively new industrial sector, there was not yet a historical trackrecord of financial performance upon which to evaluate risk and expected return. Inthe case of offshore wind there are countless risks both in terms of construction andoperations. Potential risks included adverse weather causing maintenance delays, themovement of foundations or array cable failures leading to construction delays, thelack of sufficient wind and technology risk associated with the corrosion of components. Such uncertainties were comparable to offshore oil and gas in the 1970sand 80s – a class of asset financing commercial banks has since become comfortablewith.Offshore wind plays a make or break role in the UK’s ability to hit its binding renewable energy targets. Forecasts of demand required to hit those targets demonstratepotential for generating sufficient electricity from renewables (Figure 2). However,supply from investor-backed developers willing to take on the construction risk suggested further encouragement was required to keep up with demand (Figure 3).Figure 2: Demand for Offshore Wind InfrastructureFigure 3: Supply Status of Offshore Wind Infrastructure ProjectsPolitical and regulatory hurdlesA number of regulatory hurdles exist in the broader European market where policy uncertainty and austerity measures have previously led to unplanned reductions in public-sector investments. For instance, retroactive changes in countries such as Greece and Spain have come close to destroying the market for green infrastructure investments. The withdrawal of support for wind energy in some countries contributedto heavy losses in the wind industry, casting doubt on the ability of suppliers to sustain themselves (Figure 4).Figure 4: Turbine Manufacturers’ Margins 2008 - 2012Source: Bloomberg New Energy Finance-It was originally conceived that the Green Investment Bank find its ‘additional, non distorting’ role through a market position in which it took “slightly too much of the ris for slightly too little of the return” on green infrastructure projects. This was envisagedin a world in which market failures - caused by information asymmetries and riskaversion - might cause the private sector to underestimate the potential returns ofgreen energy investments. Hence at first, it was proposed the bank should be agovernment-owned development bank that would own society’s “cost of capital”, thus making a real investment return, albeit a lesser return demanded by private sectorinvestors.A key question facing the newly established team of the Green Investment Bank wassubsequently how to accelerate a shift in perception about green energy investmentswhile earning a decent return for UK taxpayers.UKGIB’s Mission and Business ModelRather than acting as a “development agency”, such as the World Bank, the UKGIBteam saw its role in partnering with existing long-term investors and encouraging newones by being robustly commercial in its approach. Its mission of being “green and would ensure that investors could observe decent financial returns in theprofitable”renewable energy sector. Only in this way could the Bank change existing perceptionsand attract incremental capital into green infrastructure investments.The UKGIB’s ‘green impact’ is measured against five criteria:1. Reduce green-house gas emissions2. Improve efficiency in the use of natural resources3. Protect or enhance the natural environment4. Protect or enhance bio-diversity5. Promote environmental sustainabilityFigure 5: UKGIB’s Business ModelSource: UKGIB Annual Report 2013/14The Bank also has a financial bottom line, which is to say that it is unashamedly and. Financial returns are based on state aid rules, on unambiguously a “for profit” bankthe basis that they are always additional, but they are also based on sound financeand a commercial return. These principles are reflected in the expertise of theirbanking management team, who have been recruited from some of the world’s top institutions, as well as the Bank’s investment strategy and due diligence process. Inits articles of association, it is even determined ‘the GIB should plan to deliver a minimum of 3.5% annual nominal return on total investments after operating costs but (see Appendix 2).before tax’In order not to ‘crowd out’ private investments already taking place in the green economy, UKGIB’s priority sectors were selected on the basis that they were on thes to assist in the development ofcusp of being ‘mainstream investable’. Its mission waprivate sector markets in order that the bank’s role within them becomes redundant. For a project to be investable by the UKGIB it must fit all six criteria set out by the investment managers and signed off by the Chief Risk Officer through an internal review process:1. Fit within the state aid mandate in terms of specific ‘priority sectors’to every project. Developers must prove they cannot obtain2. Be ‘additional’funding elsewhere. Often the bank starts off as a cornerstone investor andcrowds in funding by articulating the investment story.3. Invest at market rate in order not to undercut competition. Funding must beprovided pari passu with other investors, or if the purpose is to feed stocksupply, it might involve taking equity in the project and then taking additionalrevenues on the basis it is signed off as conforming to ‘market economyinvestor principle’ (MEIP) rules.4. Conforms to the five green credentials outlined in its articles of association.5. Presents a suitable risk profile, which involves various models and forecasts,testing the assumptions for revenues, cost of delivery and cover ratio limits.6. Last but not least reputation is key, particularly the relationship with both theclient and the developer.To ensure the Bank would be profitable, it was made explicit that areas in which theUKGIB would not invest would include the provision of grants and regional assistance, subsidised debt or equity, high risk-lower reward, venture capital, development equityor lender of last resort. Instead four priority sectors to which 80% of the Bank’s investment capital would be dedicated would include offshore wind, waste/recycling,non-domestic energy efficiency and support to the Green Deal (Figure 5). The remaining 20% could then be committed to other green energy sectors, such as biomass, biofuels and transport, carbon capture, marine energy and renewable heat.Figure 5: Investment Strategy by Green Energy SectorSource: UKGIB Annual Report 2013/14 Creating the Investment FrameworkAn ongoing question for the Bank’s senior management was what level of return above 3.5% would legitimately reflect the opportunity cost of capital for investments in therenewable energy sector. The organization needed to adopt a financial framework forsetting project hurdle rates (i.e. the minimum internal rate of return (RRR) required tosanction a new investment).As a veteran in the investment banking community, Chief Risk Officer, Peter Knott wasfamiliar with the broad range of sophisticated analytical techniques for estimating project hurdle rates (see Appendix 3 for formulae provided by professional service firms). But to deliver on all aspects of the Bank’s m ission, he reasoned that the financial framework should adopt a relatively straightforward and transparent processfor setting discount rates. He knew that a good discount rate for a specific project should reflect two basic assumptions: the time value of money and an appropriate compensation for risk. But categorizing and quantifying investment risk for large renewable energy projects was proving to be challenging.Peter and his team wondered how they could quantify the risk factors involved in greeninfrastructure investments when making decisions based on a risk-adjusted rate ofreturn. On the one hand, they understood the attractiveness of infrastructure financingwas in its ‘dependability’ as an asset that delivers fixed returns, particularly debtfinancing which offered additional security in terms of repayment and less active management. On the other hand, risks to private participants were either demand riskin the case that consumption did not match expectations or political risk.Given that the UK government was legally committed to meeting 15% of energydemand from renewables by 2020, and that producer guarantees enjoyed cross-partysupport, are inflation-linked and typically run for 20 to 25 years, the investment risk foroperators was low. As an instrument of policy, the UKGIB carried little political risk.However, by coming in at the early stages of project investments, the team wasconcerned with construction risk and the potential for cost overruns, making developerdue diligence such an important part of the process.In order to calculate the hurdle rate for each project the team had to think carefullyabout how these risks would be quantified before they could proceed with theirinvestment decisions.Example ProjectsInvestment 1: Refinancing of a UK Offshore Wind Project – Rhyll FlatsRhyl Flats is a 90 MegaWatt wind farm located 8km off North Wales in which theUKGIB acquired a 24.95% direct equity stake from RWE AG for £57.7m. As one of thefirst investments, this represented a landmark step in supporting one of the Bank’core sectors (offshore wind). Its main aim was to develop a secondary market foroperating offshore wind assets, allowing the release of capital back to developers onthe basis that this could then be reinvested into other projects.Green Impact Financial Impact- Expected to provide enough clean, green electricity to power around 61,000 homes- Reduced reliance on imported gas - Helping to meet greenhouse gas emissions and renewable energy targets - Investment alongside Greencoat UK Wind Plc, first company to invest solelyin operating UK wind farms- GIB’s investment helped RWE meet its wish to sell a 49% holding- Investment will allow RWE to redeploy funding from the sale in further UK offshore wind developmentsInvestment 2: Wakefield Waste PFI ProjectDemonstrating the diversity of products it offers across the capital structure, the Bankalso provided £30.4m of senior debt funding to Shanks Group PLC to support a 250-year PFI waste contract with Wakefield Council. The loan was provided alongside three commercial banks to deliver essential funding to contribute towards recycling facilities, waste treatment and generating sustainable power. In terms of green impactit achieves annual landfill avoidance of 200,000 tonnes, helps to increase the localauthority diversion rate to 90%, increases its recycling rate to 52% and providespotential annual emissions saving of 33,300 tonnes of CO2e.Green ImpactFinancial Impact - Diversion of c.200,000 tonnes p.a. ofmunicipal solid waste from landfillhelping to increase local authority’s landfill diversion rate to 90% - Increase local authority ’s recycling rate to at least 52%, greater than UK ’s2020 target - Provide potential annual emissionssavings of approximately 34,300tonnes of CO 2e- GIB is providing senior debt and equity bridge facilities pari passu with three commercial lenders - GIB was invited to join banking club inmid-2012 providing necessary additionalliquidity to ensure achievement of financial close- Mobilised three times GIB investment Investment 3: Realm Energy Centres FundThe Bank has also committed £50m to the Aviva Investors REaLM Energy CentresFund, which provides long-term funding for public sector energy efficiency projects.The fund made its first investment of £36m (of which GIB contributed £18m) in anenergy centre project for Cambridge University Hospitals NHS Foundation Trust overa 25-year period. Technology includes a combined heat and power engine, biomassboilers, efficient dual fuel boilers and heat recovery from medical waste incineration.Green ImpactFinancial Impact - Expected CO 2e savings ofapproximately 8000 tonnes perannum - Reduce the Trust ’s overall energy bills by £20m over the 25 yearoperation of the project - Help the Trust achieve its 2020 carbon reduction goals- GIB ’s investment into the Fund has mobilised c £18m of private capital into the project from Aviva Investors REaLMInfrastructure Fund to support its first investment - GIB ’s full investment commitment of£50m will eventually mobilise a total of at least £50m private capital into the sector The Greencoat Fund - Achieving ‘additionality ’ at a fund levelWith experience providing both debt and equity in offshore wind projects, the UKGIBworked with Greencoat to raise an offshore wind fund in 2013. Together, they hadrecognised a high level of demand amongst pension funds, sovereign wealth fundsand institutional investors wishing to be exposed to the sector but lacking theconfidence and closeness to the industry to make substantial investments bythemselves. By helping to assess the fund's prospects for investment from theDepartment of Business Innovation & Skills and taking a 25% equity stake in RhylFlats, one of the fund's seed assets, the UKGIB helped to get the fund off the ground.This also involved negotiations with the EU Commission and the FCA to explore thepossibility of establishing a fund management business, which would help crowd-inown balance sheet to work but by usingprivate investment, not by putting the Bank’sits exper tise in investing its own funds to manage other people’s money, channelling investment into green infrastructure projects. Based on the success of the GIB’s fir fund of this kind (having achieved returns of between 8-9% in its first year), it plans tolaunch additional funds and financial products in future.Taking the Next StepsOver the last few months, Peter had been approached by a number of companiesseeking equity and/or debt investments in offshore wind projects currently under development in the United Kingdom. Having carried out due diligence on each of theprojects and the developers involved, he has boiled down the UKGIB’s options to threepotential investments. Before proceeding, he asked his investment team to carry outthe following task:Taking into account the key risk categories for an offshore wind project,determine the weighted average cost of capital (WACC) for the threeoffshore wind projects.The selection of a project-specific WACC should take into account an expected capitalstructure for each project, the cost of debt, and the expected return on equity.Summary data captured during the due diligence process is provided in a separatespreadsheet, providing both qualitative and quantitative insights on the relative risksassociated with each project.Generate a one page investment memorandum that justifies your WACCfor each project, taking into account the Bank’s strategic mandate as wellas comparable commercial returns in the sector.Identifying the risk categories and WACC associated with each project will be helpfulfor Peter in future to understand the minimum acceptable rate of return, given eachproject’srisk profile and the opportunity cost of other investments. The weightedaverage cost of capital across a variety of related sectors is included in Appendix 3 asa benchmark for his investment team.Appendix 1: UKGIB Timeline’sArticles of AssociationAppendix 3: WACC Benchmarks。

投资银行案例3

2020年4月6日

西南财经大学金融学院

26

二、企业收缩

企业收缩是指使企业规模及经营范围缩小的各 种行为,具体可分为分立和剥离两种形式。

(一)企业收缩的类型

8

3、收购(acquisitions):指一家企业通过某 种方式主动购买另一家企业的股权或资产的行 为。其目的是获得该企业的控制权。

4、合营企业(joint ventures):指相关公司 之间的小部分业务进行交叉合并的行为。通常 是有限的10—15年或更短的期限。

(二)企业扩张的动因

在不同的时期和不同的市场条件下,企业扩张 的动因是不同的。理论界从不同角度解释了企 业扩张的动因,其主要的理论有:

21

4、可转换债券方式

可转换债券是一种特殊的债券,它向其持有者提供了一种

选择权,即在某一给定的时间,按某一特定价格转换成公 司股票的权利,兼具了债券和股票的双重特征。

优点

缺点

收购公司 降低收购成本

股东权益可能被稀释

缓冲股本扩张压力 转债利率高于股息率

具有抵税效应

转股失败有财务压力

目标公司 拥有更多的选择权 无法转股套利收益较低

2020年4月6日

西南财经大学金融学院

10

2、财务协同效应理论

财务协同效应是指企业扩张后,由于税法、证 券市场投资理念和证券分析人士偏好等作用而 产生的一种好处。主要表现在:

(1)合理避税 (2)提高股票价格 (3)提高公司知名度

2020年4月6日

西南财经大学金融学院

11

财经案例分析大赛参赛作品

并在会计报表附注中作了披露。

•

案例一分析 ——对或有事项确认、计量、披露问

题的探讨

• 前言:在日益发展并日渐成熟的市场经济条件下,一个企 业在经营活动中势必将遇到各种挑战,或是面临诉讼、仲 裁、重组等具有较大不确定性的经济事项,或是为其他单 位提供债务担保,对消费者提供产品质量保证等。这些不 确定的事项都将对企业的财务状况和经营成果可能产生较 大影响。因此我国《企业会计准则第13号——或有事项》 对其确认、计量、披露问题进行了有关规范。

紫竹公司的这种做法会导致企业的负债减少,利润虚增,没有全面披露 经济事项和反映企业的财务状况,损害了证券市场的信息透明和公平竞 争,影响了广大投资者的利益。

在案例2中,紫竹公司未对商业承兑汇票贴现事项进是正确的

• 根据我国《企业会计准则第13条——或有事项》第十四条: 企业应当在附注中披露与或有事项有关的下列信息:(二) 或有负债(不包括极小可能导致经济利益流出企业的或有 负债)。

在案例3中,紫竹公司确认补偿金额是不正确的。

• 根据我国《企业会计准则第13 条——或有事项》第七条: 企业 清偿预计负债所需支出全部或 部分预期由第三方补偿的,补 偿金额只有在基本确定能够收 到时才能作为资产单独确认

• 所以紫竹公司将其为威伟公司偿付的贷 款本金确认为资产时,必须满足“基本 确定”这一确认条件。因此,紫竹公司 虽有权向威伟公司索取代为偿付的款项, 且威伟公司对紫竹公司代为偿付的款项 具有赔偿责任;但在2006年底,基于威 伟公司的财务状况,紫竹公司获得威伟 公司赔偿的可能性并未达到基本确定的 程度,不符合确认补偿的条件,因此不 能予以确认,紫竹公司确认补偿金额是 不正确的。

紫竹公司这样做会虚增资产,从而导致利润增加,不符合谨慎性原 则,没有公正的反映企业的财务状况和经营成果,同样影响了投资 者,债权人的利益。

金融案例大赛优秀案例范文

金融案例大赛优秀案例范文案例二:汇丰银行中高级管理人员的选拔培训汇丰银行全称“香港上海汇丰银行”(HSBC),是香港最大的英资银行,成立于18xx年,18xx年正式对外营业。

在当时的英国海外银行中,它是惟一将总部设于香港的银行。

由于经营上的自主权较大,它很快超过了众多的竞争对手,与港英政府建立了特殊关系并得到当地商业界的支持,多次挽救了香港的银行危机。

汇丰银行于开业当年的18xx年x月开始发钞,代理香港政府发行约85%的港币业务。

19xx 年后更作为港府指定的发钞银行与渣打银行和其后的中银集团共同享有港币发行业务。

汇丰一贯较多地参与制定和贯彻港府的金融决策。

汇丰的董事长一直是香港行政局的成员,是香港银行公会执行委员会的三名常设委员之一,并与渣打银行轮流担任正、副主席,还是香港外汇基金咨询委员会委员。

这些席位均使汇丰得以掌握政府在金融方面的政策并对其施加影响。

19xx年x月,汇丰银行宣布进行内部机构重组,成立一家在英国注册、总部设于香港的控股公司,并将汇丰在港的全部资产注入该公司,实现变相迁册。

19xx 年x月,汇丰宣布全面收购英国米特兰银行的计划,将汇丰总部迁往伦敦,完成最后迁册。

合并后的汇丰集团资产分布在亚太地区的份额从51%降到30%,欧洲地区的份额从20%上升到51%。

19xx年x月,香港金融管理局成立之后,运作卓有成效。

香港的宏观金融管理走上了健康发展的轨道。

汇丰银行作为一家牟利的私人银行,出于利益的考虑,一方面继续履行发钞银行的职能,另一方面积极拓展在香港和全球的业务,特别注重金融基础设施的投资(例如自己设计软件以配合新的银行业务)、全球化商业银行和投资银行业务的开拓及服务水平的提高。

19xx年,汇丰取得了总盈利近50亿美元的业绩。

汇丰银行在各项全球性评级活动中多次位居前列,①19xx年《远东经济评论》第五届亚洲公司200强年度排名,汇丰银行以5.89分连续第四届获第一名;②19xx 年x月份英国《欧洲货币》杂志刊出了按照资本金大小排列的19xx年世界前200家最大的银行,汇丰银行集团名列第三:⑧英国《银行家》杂志19xx年“世界1000家大银行新排名”,汇丰银行名列第五。

理财大赛预赛案例

理财大赛预赛案例第一篇:理财大赛预赛案例武汉分行理财经理大赛预赛案例案例一:高资产企业主投资移民规划1.家庭成员背景资料(未标明美元时均为人民币计价)张维和先生现年43岁,10年前与大学同学共同创立了一家模具制造有限责任公司,双方各占50%的股份。

2010年底公司净资产有8000万元,税前净利800万元,各股东都不领工资,税后利润全部分红。

太太现年42 岁,在家照顾孩子。

大儿子现年14 岁,读初一;女儿4 岁,在香港出生,目前读幼儿园。

全家月消费支出3万元,年学费支出子女各5万元。

不动产有三套,现住房市价350万元;度假别墅一套,市值1500万;大儿子名下有一套酒店式公寓,市值60万元,以上房产目前均无按揭。

家有汽车2台,市价200万元。

金融资产方面有人民币存款700万元,在香港存有50万美元,股票市值200万元,因太太投资经验很少,总体收益为负。

张先生夫妻未加入社保,全家仅有张先生由公司投保的意外险50万元。

2.理财目标与规划需求(1)企业转手规划:因模具制造业市场竞争激烈,近两年企业净利润几乎没有增长,张先生打算退出经营,另一股东仅愿意以账面价值出价4000万买下张先生股权继续经营。

张先生希望理财经理能够 1 对企业估值,希望可以说服另一股东提高收购价格。

(2)投资移民规划:张先生打算办理美国投资移民,按美国移民法要求投资100万美元并雇用当地人口,预估税后收益率为5%,1年后全家移民美国,届时全家年生活费为10万美元现值。

其中子女各1万美元,夫妻各4万美元。

两子女在美国求学直到取得硕士学位后的年学费支出各4万美元现值。

(3)移民换房规划:张先生打算出售度假别墅与酒店式公寓,保留现住房以便回国探亲时使用。

打算1年后在美国购买一套价值300万美元的别墅,不用贷款。

(4)财富传承规划:资产传承给子女,应如何规划来降低美国的遗产税或赠予税?另遗产中拟保留届时值人民币500万元在中国做公益事业,应该如何规划?3.基本假设(1)目前的宏观经济持续成长,经济成长率预估为9%,通货膨胀率预估为4%。

理财经理大赛案例编写

理财经理大赛案例编写案例名称:投资理财大赛背景:一家理财公司决定举办一场投资理财大赛,以挑选出最优秀的理财经理。

该公司的目标是寻找具有创新思维和良好投资能力的人才,以进一步提升公司在市场中的竞争力和业务发展。

案例描述:该大赛将由三个阶段组成:选拔赛、复赛和决赛。

参赛者需要参与各个阶段的测试和表现,最终经过综合评估选拔出胜出者。

选拔赛:在选拔赛阶段,参赛者将接受公司精心设计的理财知识测试。

测试内容包括理财基础知识、金融市场分析、投资组合管理等方面的考核。

参赛者需要通过这一阶段的测试,展示自己的理财知识储备和分析能力。

复赛:通过选拔赛晋级的参赛者将进入复赛阶段。

复赛的主要目的是考察参赛者在实际投资决策方面的能力。

参赛者将获得一定金额的虚拟资金,在限定的时间内制定并实施投资方案。

参赛者需要结合市场状况和不同投资品种的特点,制定高风险回报比的投资策略,并进行交易。

该阶段的评估将综合考虑参赛者的投资决策效果、风险控制能力和创新思维。

在复赛中表现出色的参赛者将晋级到决赛阶段。

决赛将是一场模拟实战演练的比拼。

参赛者将在真实市场环境下操作自己的投资组合,并根据市场动态进行调整。

决赛期间,参赛者还需要面对突发事件和市场波动,及时做出应对策略。

评委将以综合表现评估参赛者,包括投资回报率、风险控制、投资组合稳定性以及在压力下的应变能力等。

结果评选:根据三个阶段的综合表现,评委将评选出最优秀的理财经理。

评估标准将基于智慧投资策略、投资回报、风险控制水平、创新性思维、决策能力和团队合作能力等方面的成绩。

结语:通过该理财经理大赛,公司希望选拔到有潜力和能力的理财经理,为公司的业务发展注入新动力。

成功的参赛者将有机会加入该公司的团队,为客户提供专业的理财服务,并为公司实现长期稳定的增长做出贡献。

该大赛也将为投资理财行业培养更多优秀人才,提升行业整体水平。

成功的英文面试案例

成功的英文面试案例成功的英文面试案例Case Study-An Interview With Shell Oil panyThe Shell Oil pany is well known for its human resource assessment methodology, which has proven successful in the identification and selection of candidates for its global operations. Its approach and assessment criteria have been adopted by somegover____ent agencies for selecting scholars andpublic officials. While it is not a financial institution, the experience documented below is the first-hand real life experience of one of the authors that has applicability and relevance on interviewing with global financial institutions.Case study-The Shell Oil pany Interview Experience 壳牌石油公司以其人事评估方法著称,该方法成功地为其在全世界的机构选拔了大量优秀人才。

它的方法和评估标准已经被全世界很多政府机构采用,以选择奖学金得主和政府官员。

尽管它不属于金融机构,但以下案例是本书作者之一的亲身经历,相信对参加金融机构应聘的人士,也是有所裨益的。

案例分析^p 壳牌石油公司面试经历The second largest global oil giant and a Fortune 500 pany, Shell is known for its stringent selection criteria when it es to executive hiring. The interview process of this world-class pany is very thorough and demands a lot out of a candidate. The whole experience is exhausting (it lasts approximately 6 hoursincluding lunch) and one has to be very well prepared mentally to perform well.The setting is as such: The candidate, along with 5-6 other short-listed candidates, is invited to a local hotel/resort/country club for a day. The panel that will be interviewing you consists of senior managers from different divisions of the pany.One point to note for perspective: Through this thorough interview process, the pany seeks to employ candidates who can eventually progress to a General Management position in one of the pany’s numerousdivisions. The various stages of the long process include:作为全球第二大石油公司和财富500强企业,壳牌公司在挑选人才方面极为严格。

毕马威案例分析大赛全英文报告

employees (average of five giants); the companies in the industry need a world-wide management system. • Market barriers: Some giants in the industry like H&M and Inditex cause fierce competition.

√

3 Marketing Analysis

Branding Decision

• More than selling clothes but prompting a unique lifestyle.

Brand Diversification

Characteristic

Percentage of Sales(2011)

Rest of Europe 103.9(+10.7%)

Italy

1182.2(+2.2%)

Asia

432.6(+81.5%)

Americas

103.9(+6.6%) Rest of the world

16.9(+108.6%)

Market Targeting

Customer Targeting

Geographic Targeting

• Advertisements cause dispute. • Without a thorough understanding of the

2009年相约哈佛案例分析大赛——优秀文稿

3、多元化经营误区

盲目性:中国企业对内部经营单位的控制方式不严密、投资管理不规范、项目上马不理智。多元化表现出明显的“贪大求洋”特色,和一种明显的“大公司情结”,当原有产业和原有市场满足不了这种“非凡情结”的时候,就会迅速向其他产业和其他市场渗透,而不管这些产业与原产业之间的关联程度如何,结果业务跨度越大,业务之间的协同性、一致性越弱,甚至一些企业走到了为多元化而多元化的死胡同,“巨人集团”由软件起家,最后崩溃于房地产,就是这种盲目多元化的典型。为制造新的利润增长点进行的盲目扩张,使企业总部依据市场竞争前景确定业务取舍的能力减弱,在决策中,不确定性随着多元化的扩展而增多。这样,多元化企业最终就会完全丧失对其各层次业务的控制能力,而企业主要业务一旦失控,资金的流向根本就不能预测并及时回笼,企业必然走向毁灭。

充分利用资源、挖掘企业潜力增强内部的融资能力

随着企业的发展壮大,会逐渐在生产、技术、管理、销售等各个环节积累一定的资源或能力,通过多元化经营,能使一部分剩余能力得到充分的利用,使企业获取更大的收益。当出现产业衰退时可将其产生的大量闲置资金转移到其他产业上去保证企业其他产业有足够的实力参与市场竞争,最大限度地挖掘企业的潜力。目前,我国资产重组、兼并浪潮方兴未艾,企业之间的横向联系日益加强,这种态势下,多元化经营战略已成了许多企业在市场竞争中的必然战略选择。

1995——1999年成长阶段

以社会责任感的价值观,实现精细化工和日用化工攀升发展,管理开始精细化。

1995年3月,传化集团成立。

1997年,传化7万吨洗衣粉项目建成投产。

1998年,杭州传化华洋化工有限公司成立,重点开发荧光增白剂。

2016年贝恩杯案例分析大赛

Cosmetics Co. China Expansion Strategy for Cosmetics Co. April, 2016•Welcome to the 2016 Bain case competition!•Your team has been invited by the Strategy Director of Cosmetics Co. to participate in a pre-discussion on Cosmetics Co.’s expansion strategy in China for the next 5 years. The quality of your proposal and presentation will determine whether you can get a discussion with the CEO on a potential 3-month consulting project•Cosmetics Co. is one of the top South Korean/Japanese cosmetics manufacturers/ brand owners with multiple brands at different positioning and multiple categories of product offering•While Japan market is increasingly saturated and South Korea market growth is decelerating, China cosmetics market continues to grow rapidly. Cosmetics Co. views China as a critical market for its international growth and would like its China business to be a significant contributor to its revenue•The company has made some attempts in the past few years to penetrate China market. However it is not meaningful in market position yet, and lags behind major competitors. Management would like to revisit its plan for China expansion•The Strategy Director asked for your team’s help in thinking through the following key questions on key trends in China and its implications for Cosmetics Co.:-What are the most attractive product segments and demographics profiles of the target consumers? Which/what type of brand(s) should Cosmetics Co. prioritize in China?-What is the status quo of both offline and online channels for cosmetics sales in China? How should Cosmetics. Co think about their channel play?-What are the geographies that Cosmetics Co. should prioritize?-What is the best operating model (high-level) for Cosmetics Co.? Export, partnership, direct investment, etc.?•Your team may choose to focus on 2-3 questions that would make the most impact and would need to tell a compelling story supported by robust data and analyses•This proposal is due by end of day May 4th, and you may be asked to present these materials to Strategy Director in the following week•To ensure that your presentation hits the most important points and is “communicating-for-results”, you have agreed with the Strategy Director that-Maximum 15 slides for the presentation (not including agenda pages or additional data analyses in backup materials) –the objective is not be as comprehensive as possible, so please focus on what is most insightful and impactful-Minimum 26 font size for slide taglines; minimum 14 font size for main body text; maximum3 charts/graphs on a slide-All pages should be easy to read and understand for audience with a general background•To set a “Point of Departure”, your team can either choose an existing South Korean or Japanese cosmetics player similar to prior description as the hypothetical client, or assume a nonexistent player with similar characteristics•To help you quickly get up-to-speed, the Strategy Director has kindly shared some reference materials. Although some of these materials may be outdated, he/she believes that your team will be able to gather other interesting and powerful information from publicly available sources (e.g. company annual reports, analyst reports, business news) or primary research to support your analysis and recommendationGood luck!Reference Materials•Cosmetics overview•China shopper behavior key trendsSkin care and color cosmetics are two major subsets of beauty and personal carePRELIMINARYSource: EuromonitorChina is biggest driver of Asian skincare market growth; South Korea’s growth is deceleratingSource: Euromonitor; fixed 2013 exchange rates Skincare ForecastHistorical PRELIMINARYChina comprises ~40% of the Asia-Pacific color market (excl. Japan) and is growing at ~10% p.a.ColorPRELIMINARYForecastHistoricalNote: “Other” includes Afghanistan, American Samoa, Armenia, Azerbaijan, Bangladesh, Bhutan, Brunei, Cambodia, Fiji, French P olynesia, Guam, Kazakhstan, Kiribati, Kyrgyzstan, Laos, Macau, Malaysia, the Maldives, Mongolia, Myanmar, Nauru, Nepal< new Caledonia, North Korea, Pakistan, Papua New Guinea, the Philippines, Samoa, Singapore, Solomon Islands, Sri Lanka, Tajikistan, Tonga, Turkmenistan, Tuvalu, Uzbekistan, Vanuatu, and VietnamSource: Euromonitor; fixed 2013 exchange rates to US dollarChinese market more fragmented, accepting of multinationals; Korea, Japan dominated by regionalsNote: Shiseido categorized as regional/ ‘high potential’ brand by management but has multinational scope Source: Euromonitor; fixed 2013 exchange ratesPRELIMINARYCHINA (TOP 10 ARE 45% OF TOTAL)SOUTH KOREA (TOP 10 ARE 75% OF TOTAL)JAPAN(TOP 10 ARE 50% OF TOTAL)= Multinational = Non-multinational €15.9B total €3.3B total €12.2B total SkincareAverage selling price growth varies a lot across categories, from 13.5% to -1.8%2012-14 avg. inflation 2.5%Note: Price growth is calculated with RMB per KG/L data, except diaper is RMB per pack and toilet tissue is RMB per roll.RTD tea stands for Ready-To-Drink tea, CSD refers to carbonated soft drinkBeauty and baby products continue to dominate the e-commerce market, but other categories are catching up fastONLINEKey online categoriesForeign brands do well in China under personal care categoryCategory market share by foreign and Chinese brands (%, 2014)Traditional packaged food and beverageBeverage PackagedfoodCreated packagedfood and beverageBeverage Packagedfood Personal care Home careNonfood and beverageChinese (Mainland, Hong Kong, Macau and Taiwan)Foreign。

金融案例分析大赛作品

Annual Reate of Contribution Retun 9.09% $ 9.09% $ 9,900.00 9.09% $ 11,700.00 9.09% $ 1,141.00

$ $ $ $

Ending Balance 6,012.60 17,395.65 31,807.37 8,689.16

21-MIN 45,000.00 14,898.00 30,102.00 4,378.00 16,185.00 25,724.00 13,917.00

21-MAX $ 80,000.00 $ 29,936.00 $ 50,064.00 $ 7,282.00 $ 19,089.00 $ 42,782.00 $ 30,975.00

Reate of Retun 9.09% 9.09% 9.09% 9.09% 9.09% 9.09% 9.09% 9.09% 9.09% 9.09% 9.09% 9.09% 9.09% 9.09%

14%

42%

24%

9.09%

14%

6%

0%

10%

19%

29% 7.09%

10%

6%

27%

Gross Pay Total Deductions Net Take Home Income Total Expenses TotalRemaining Net Expenses Net Remaining

$ $ $ $ $ $ $

JOURNEYMAN JOURNEYMAN

Home Down Payment

Rising for Family

Children’s Education

Retirement

Assets

Cash

财务案例大赛样本案例分析3

4477%% 1133%%

23%

3366%%

266%%

18%

Class Notes General Books Sundries

Clothing

Computers

Software

5%

33%

6%

1122%%

8% 7%

23%

31%

338% 447% 55%

24%

4%

20055%%

10%

411%% --116%

16

Benchmarking - Competitive Strategy Level

Price

Price Trend

Low Decreasing Magnitude

Price Change

Amazon Ecampus

Fall,2003 -Fall,2004

-27.45%

-22.61%

Barnes &Noble

Potential for Expansion High Campus Contribution Strong Purchase Power

$1,400 $1,200 $1,000

$800 $600

$1,025 Average

$861

$1,026

25th

Median

$1,187

$1,338

75th Northlake

18

Benchmarking - Competitive Strategy Level

Service

• Faculty Overall Satisfaction • Customer Queuing Time

• % of Coursepacks Available First Day • % of Textbooks Available First Day

毕马威案例分析大赛作品

The mainstream position stategy

Capital cost

The mainstream position strategy

• With the advanced technology,

Disposable razors make a large part of the market because of the low price and convenience. Besides, threatening from shaving cream and depilatories should be taken into consideration either.

Niche or Mainstream?

Both!

Contents

1

Background

2

Question Rising

3

Case Analysis

4

Alternative Plans

5

Plan Implementation

6

Forecast

Background

Paramount is a global consumer products giant whose corporate divisions included Health, Cleaning, Beauty and Grooming. Paramount entered the nondisposable razor market in 1962 and quickly became a respected brand in the industry.

中文案例

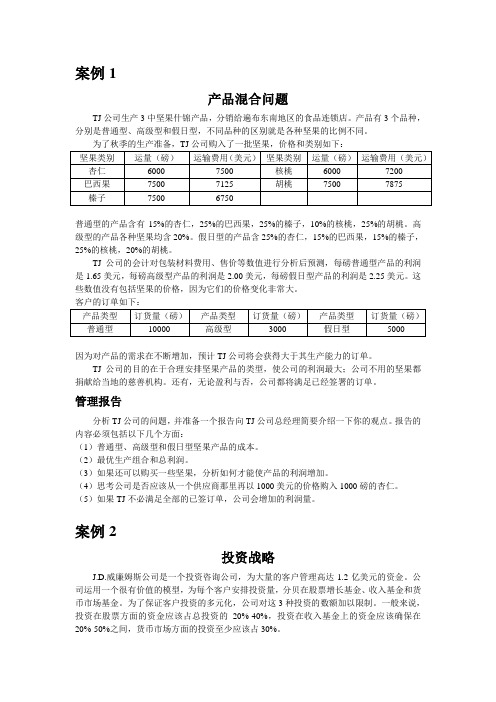

案例1产品混合问题TJ公司生产3中坚果什锦产品,分销给遍布东南地区的食品连锁店。

产品有3个品种,分别是普通型、高级型和假日型,不同品种的区别就是各种坚果的比例不同。

为了秋季的生产准备,TJ公司购入了一批坚果,价格和类别如下:坚果类别运量(磅)运输费用(美元)坚果类别运量(磅)运输费用(美元)杏仁6000 7500 核桃6000 7200 巴西果7500 7125 胡桃7500 7875榛子7500 6750普通型的产品含有15%的杏仁,25%的巴西果,25%的榛子,10%的核桃,25%的胡桃。

高级型的产品各种坚果均含20%。

假日型的产品含25%的杏仁,15%的巴西果,15%的榛子,25%的核桃,20%的胡桃。

TJ公司的会计对包装材料费用、售价等数值进行分析后预测,每磅普通型产品的利润是1.65美元,每磅高级型产品的利润是2.00美元,每磅假日型产品的利润是2.25美元。

这些数值没有包括坚果的价格,因为它们的价格变化非常大。

客户的订单如下:产品类型订货量(磅)产品类型订货量(磅)产品类型订货量(磅)普通型10000 高级型3000 假日型5000因为对产品的需求在不断增加,预计TJ公司将会获得大于其生产能力的订单。

TJ公司的目的在于合理安排坚果产品的类型,使公司的利润最大;公司不用的坚果都捐献给当地的慈善机构。

还有,无论盈利与否,公司都将满足已经签署的订单。

管理报告分析TJ公司的问题,并准备一个报告向TJ公司总经理简要介绍一下你的观点。

报告的内容必须包括以下几个方面:(1)普通型、高级型和假日型坚果产品的成本。

(2)最优生产组合和总利润。

(3)如果还可以购买一些坚果,分析如何才能使产品的利润增加。

(4)思考公司是否应该从一个供应商那里再以1000美元的价格购入1000磅的杏仁。

(5)如果TJ不必满足全部的已签订单,公司会增加的利润量。

案例2投资战略J.D.威廉姆斯公司是一个投资咨询公司,为大量的客户管理高达1.2亿美元的资金。

财务案例大赛样本案例分析1

Textbook sales for this fall had decreased from the prior fall sales

In September 2004 What to do

•Employ benchmarking analysis to figure out the reasons behind the poor performance

Northlake

41.49%

28.70%

GAP -12.79%

28.23%

20.70%

-7.53%

As a high-margin product line, used textbooks should be sold more.

12

Price gap between Northlake and Online Vendors

6.5% 6.40% $1,025

12.1% 5.6% 20.80% 14.4% $1,338 $313

Advantages

9

Financial perspective

Measures About Space Utilization

BMK (Average)

Northlake

GAP

Sales per sq.ft.of total space

Learning and growth

Cartons processed per employee hour Employee satisfaction Employee Turnover

5

The Analytical Hierarchical Process (AHP)

1=equal importance to both elements in the matrix 3=moderate importance of one element compared with another 5=strong importance of one element compared with another

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Investment Banking Case Competition

Presented by: Goldman, Sachs & Co.

Introduction

The Haas Investment Banking Case competition has been designed to provide interested students with an opportunity to demonstrate and to further develop their business skill set. While there will be a “winning team,” all participants will benefit from the experience. The case is ideal for those students considering a career in investment banking, venture capital, consulting, corporate finance or educational technology. The presentations by the finalists will also allow the panel of judges from 2U, Goldman Sachs, and the Haas School of Business to observe students’ presentation and analytical skills.

Teams

Students should form their own teams to participate in the competition. The recommended team size is four. However, a team may compete with a minimum of three individuals. There must be at least one team member who is not a Haas major. This rule is intended to replicate the work environments that graduates will experience in the field.

Submission Format and Due Date

Each team will present their conclusions through a written presentation (landscape format), similar to the discussion materials often used in investment banking, consulting and corporate board meetings (e.g. PowerPoint). Your presentation can be a maximum of 10 pages in length. You may have additional pages that include tables and exhibits (in addition to the 10 pages mentioned). The tables and exhibits will be a critical component of the final product as your conclusions will be based on this work. Your presentation should be converted to a PDF document and cannot exceed 5 MB in size. Email your PDF presentation file to casesubmission@ and include your team number in the subject line of your message. The email with your presentation attached is due by th Friday, October 10 by noon. No exceptions will be made for cases submitted after this time. We will also hold a conference call to answer any questions you may have regarding the case on October th 7 from 1:00-2:00PM PST. The dial in will be (212) 902-9977, participant code 4303359.

Data provided in this case is for educational purposes only and does not represent actual projections

1

Background

The Management team and Board of Directors of 2U have met several times this quarter to decide on the appropriate next steps for the Company. The Company filed its S-1 IPO registration document with the SEC in February 2014 (link to the filing: /Archives/edgar/data/1459417/000104746914001172/a2218267zs-1.htm). Although a relatively young Company, 2U has emerged as a leader within the developing online education space. The key decision makers of the Company are excited with the growth of the Company but want to continue to accelerate the business during favorable market conditions. Thus, the Company is exploring the prospect of an IPO but wants to make sure that the market will react favorably. Goldman Sachs has been invited by the Company and the Board to help them answer the following questions: 1) What is the value of 2U in the context of an IPO; 2) How will the markets and investors perceive a potential 2U IPO; 3) When is the most favorable time for 2U to pursue an IPO or any other alternative; 4) Is IPO the right choice?

Final Competition

The review committee comprised of Haas faculty, Goldman Sachs professionals, and a 2U management representative, will review the presentations and select three teams to participate in the th final round. The finalists will be notified on Monday, October 13 . The 2014 Haas Investment th Banking Case Competition Finals will be held Thursday, October 16 from 6-9:30PM in the Wells Fargo Room at the Haas School of Business. Each of the finalist groups will make a 10-minute presentation followed by 10 minutes of questions from a panel of judges. After a short recess, the winner will be announced, followed by the judges ’ critique of the presentations and a discussion of what actually occurred, with time allotted for questions from the audience. Attendance to the finals will be open to all and is encouraged for all who are interested.

Case Study

The case is based on an existing Company and attempts to simulate the strategic decisions that the Company and its advisors faced. While the facts cited in this case study are intended to re-create the general circumstances that existed, this case study has been adapted for the purpose of this competition and now provides a hypothetical situation – it does not intend to provide a complete or definitive recitation of facts or events. The financial information provided is for illustrative purposes only and does not represent current or historical projections from any of the companies cited in this case. Financial information not provided in this case will not be relevant for your analyses. Discussion with the management or any employee of the Company or any of the Company’s competitors is strictly prohibited and is cause for disqualification. Students also should not discuss the case with investment banking, consulting or finance-related professionals. Any activity of this sort will be obvious to the judges and is cause for disqualification. The case should be the original work of the team members alone. Students who have current or past experiences in banking, consulting, or finance should cite these experiences in their final deliverable.