eInvoice Monitoring

个体户开电子一票通的流程

个体户开电子一票通的流程英文回答:Opening an e-invoice account for a sole proprietorship involves several steps. Here is a detailed guide on how to go about it:1. Research and choose a suitable e-invoice provider: There are several e-invoice providers available in the market. It is important to research and choose a provider that suits your business needs. Look for factors such as cost, features, user-friendliness, and customer support.2. Gather the required documents: To open an e-invoice account, you will need to provide certain documents. These may include your business registration certificate, identification documents, bank account details, and any other relevant documents. Make sure you have all the necessary paperwork ready before proceeding.3. Contact the e-invoice provider: Reach out to the chosen e-invoice provider and express your interest in opening an account. They will guide you through the process and provide you with the necessary forms and instructions.4. Fill out the application form: Complete the application form provided by the e-invoice provider. This form will typically require information about your business, such as its name, address, contact details, and tax identification number. Fill in the required details accurately and double-check for any errors.5. Submit the application form and documents: Once you have filled out the application form, submit it along with the required documents to the e-invoice provider. This can usually be done through email or an online portal. Ensure that all the documents are properly scanned and legible.6. Verification and approval: The e-invoice providerwill verify the information provided and review your application. This process may take some time, so be patient. If any additional information or documents are required,they will inform you accordingly.7. Set up your e-invoice account: Once your application is approved, the e-invoice provider will provide you withthe necessary login credentials and instructions to set up your account. Follow the instructions carefully to create your account and customize it according to your preferences.8. Start issuing e-invoices: With your e-invoiceaccount set up, you can now start issuing e-invoices toyour customers. Familiarize yourself with the features and functionalities of the e-invoice system, such as invoice templates, tracking, and reporting.Remember to regularly update and maintain your e-invoice account to ensure smooth operations and compliance with any regulatory requirements.中文回答:个体户开通电子一票通需要经过几个步骤。

e-Freight Standard Operating Procedure BRU说明书

e-Freight Standard Operating Procedure BRU 0)IntroductionThis standard operating procedure is applicable for all export, import and transit shipments at Brussels Airport. No limitation is made in product types.1)Inventory of documents in the pouch2)Inventory minimum elements transmitted through e-MessagingFWB version 16 or higher. Mandatory & correct AWB & eAWB fields (include the rules from cargo IMP)FHL is not mandatory for eFreightFSU milestones⇨FSU FOH: Freight on hand / ready for check (goods were received at handlers warehouse where he takes liability for the goods but goods are not yet accepted for carriage) o GHA: is capable to send FOHo Not mandatory for eFreight, but will be required by the FF⇨FSU RCS: Received from shipper / transfer of responsibility at acceptance time, when goods are delivered ‘ready for carriage’o In the Netherlands, a specific paper for acceptance of eFreight export goods needs to be submitted by the GHA to the FF.Suggest: not to make a specific template for it⇨FSU DEP: Departure confirmationo At later stage in scopeo Currently not every forwarder’s system is able to display DEP contento Departure confirmations are sent via e-mail3)Export shipments2.2. Day-to-day operations2.3. Exceptional case: no electronic shipment data in GH A’s system upon delivery2.4. Exceptional case: discrepancy between goods delivered and dataFollow procedure RfC4)Import shipments 1.1.Pre-conditions1.2.Daily operations1.3.Exceptional case 1: electronic shipment data not found in GH A’s system1.4.Exceptional case 2: request for a paper copy of the AWBIn case a particular party needs a paper version; Party itself provides paper version.5)Transit shipments (Transfer)6)Abbreviations & definitionsFF: Freight ForwarderseExport licence: is an advantage but not mandatory. E-Export exists for (non) AEO (Authorized Economic Operator) and it allows FF to present the AWB copy on a later moment then before departure of the goods. The list of the e-Export licensed FF can be found on the ACB website … . Single Process:。

西方财务会计第六章答案

chapter 6 Accounting for merchandising businessesClass Discussion Questions1. Mercha ndising businesses acquire merchandise for resale to customers. It is the selling ofmerchandise, instead of a service, that makes the activities of a merchandising business dif-ferent from the activities of a service business.2. Yes. Gross profit is the excess of (net) sales over cost of merchandise sold. A net loss ariseswhen operating expenses exceed gross profit. Therefore, a business can earn a gross profit but incur operating expenses in excess of this gross profit and end up with a net loss.3. a. Incr ease c. Decreaseb. Increase d. Decrease4. U nder the periodic method, the inventory records do not show the amount available for saleor the amount sold during the period. In contrast, under the perpetual method of accounting for merchandise inventory, each purchase and sale of merchandise is recorded in the invento-ry and the cost of merchandise sold accounts. As a result, the amount of merchandise availa-ble for sale and the amount sold are continuously (perpetually) disclosed in the inventory records.5. The multiple-step form of income statement contains conventional groupings for revenuesand expenses, with intermediate balances, before concluding with the net income balance. In the single-step form, the total of all expenses is deducted from the total of all revenues, with-out intermediate balances.6. The major advantages of the single-step form of income statement are its simplicity and itsemphasis on total revenues and total expenses as the determinants of net income. The major objection to the form is that such relationships as gross profit to sales and income from opera-tions to sales are not as readily determinable as when the multiple-step form is used.7. a. 2% discount allowed if paid within ten days of date of invoice; entire amount of invoicedue within 60 days of date of invoice.b. Payment due within 30 days of date of invoice.c. Payment due by the end of the month in which the sale was made.8. a. A credit memorandum issued by the seller of merchandise indicates the amount for whichthe buyer's account is to be credited (credit to Accounts Receivable) and the reason for the sales return or allowance.b. A debit memorandum issued by the buyer of merchandise indicates the amount for whichthe seller's account is to be debited (debit to Accounts Payable) and the reason for the purchases return or allowance.9. a. The buyerb. The seller10. E xamples of such accounts include the following: Sales, Sales Discounts, Sales Returns andAllowances, Cost of Merchandise Sold, Merchandise Inventory.Ex. 6–1a. $490,000 ($250,000 + $975,000 – $735,000)b.40% ($490,000 ÷ $1,225,000)c. No. If operating expenses are less than gross profit, there will be a net income. On the otherhand, if operating expenses exceed gross profit, there will be a net loss.Ex. 6–2 : $15,710 million ( $20,946 million – $5,236 million )Ex. 6–3a. Purchases discounts, purchases returns and allowancesb. Transportation in;c. Merchandise available for saled. Merchandise inventory (ending)Ex. 6–41. The schedule should begin with the January 1, not the December 31, merchandise inventory.2. Purchases returns and allowances and purchases discounts should be deducted from (notadded to) purchases.3. The result of subtracting purchases returns and allowances and purchases discounts frompur chases should be labeled ―net purchases.‖4. Transportation in should be added to net purchases to yield cost of merchandise purchased.5. The merchandise inventory at December 31 should be deducted from merchandise availablefor sale to yield cost of merchandise sold.A correct cost of merchandise sold section is as follows:Cost of merchandise sold:Merchandise inventory, January 1, 2006 ........ $132,000 Purchases ........................................................... $600,000Less: Purchases returns and allowances$14,000Purchases discounts .............................. 6,000 20,000 Net purchases ..................................................... $580,000Add transportation in ....................................... 7,500Cost of merchandise purchased ................. 587,500 Merchandise available for sale ......................... $719,500 Less merchandise inventory,December 31, 2006....................................... 120,000 Cost of merchandise sold .................................. $599,500 Ex. 6–5Net sales: $3,010,000 ( $3,570,000 – $320,000 – $240,000 )Gross profit: $868,000 ( $3,010,000 – $2,142,000 )Ex. 6–6THE MERIDEN COMPANYIncome StatementFor the Year Ended June 30, 2006Revenues:Net sales ................................................................................. $5,400,000Rent revenue ......................................................................... 30,000Total revenues................................................................... $5,430,000 Expenses:Cost of merchandise sold ..................................................... $3,240,000Selling expenses .................................................................... 480,000Administrative expenses ...................................................... 300,000Interest expense .................................................................... 47,500Total expenses ................................................................... 4,067,500Net income ..................................................................................... $1,362,500Ex. 6–71. Sales returns and allowances and sales discounts should be deducted from (not added to)sales.2. Sales returns and allowances and sales discounts should be deducted from sales to yield "netsales" (not gross sales).3. Deducting the cost of merchandise sold from net sales yields gross profit.4. Deducting the total operating expenses from gross profit would yield income from operations(or operating income).5. Interest revenue should be reported under the caption ―Other income‖ and should be addedto Income from operations to arrive at Net income.6. The final amount on the income statement should be labeled Net income, not Gross profit.A correct income statement would be as follows:THE PLAUTUS COMPANYIncome StatementFor the Year Ended October 31, 2006Revenue from sales:Sales .................................................................... $4,200,000Less: Sales returns and allowances ............... $81,200Sales discounts ....................................... 20,300 101,500Net sales ........................................................ $4,098,500 Cost of merchandise sold ........................................ 2,093,000 Gross profit .............................................................. $2,005,500 Operating expenses:Selling expenses ................................................. $ 203,000Transportation out ............................................ 7,500Administrative expenses ................................... 122,000Total operating expenses ............................ 332,500 Income from operations .......................................... $1,673,000 Other income:Interest revenue ................................................. 66,500Net income ................................................................ $1,739,500 Ex. 6–8a. $25,000 c. $477,000 e. $40,000 g. $757,500b. $210,000 d. $192,000 f. $520,000 h. $690,000Ex. 6–9a. Cash ......................................................................................... 6,900Sales ................................................................................... 6,900 Cost of Merchandise Sold ...................................................... 4,830Merchandise Inventory .................................................... 4,830b. Accounts Receivable ............................................................... 7,500Sales ................................................................................... 7,500 Cost of Merchandise Sold ...................................................... 5,625Merchandise Inventory .................................................... 5,625c. Cash ......................................................................................... 10,200Sales ................................................................................... 10,200 Cost of Merchandise Sold ...................................................... 6,630Merchandise Inventory .................................................... 6,630d. Accounts Receivable—American Express ........................... 7,200Sales ................................................................................... 7,200 Cost of Merchandise Sold ...................................................... 5,040Merchandise Inventory .................................................... 5,040e. Credit Card Expense (675)Cash (675)f. Cash ......................................................................................... 6,875Credit Card Expense (325)Accounts Receivable—American Express ..................... 7,200Ex. 6–10It was acceptable to debit Sales for the $235,750. However, using Sales Returns and Allow-ances assists management in monitoring the amount of returns so that quick action can be taken if returns become excessive.Accounts Receivable should also have been credited for $235,750. In addition, Cost of Mer-chandise Sold should only have been credited for the cost of the merchandise sold, not the selling price. Merchandise Inventory should also have been debited for the cost of the merchandise re-turned. The entries to correctly record the returns would have been as follows: Sales (or Sales Returns and Allowances) ............................. 235,750Accounts Receivable ......................................................... 235,750 Merchandise Inventory .......................................................... 141,450Cost of Merchandise Sold ................................................ 141,450Ex. 6–11a. $7,350 [$7,500 – $150 ($7,500 × 2%)]b. Sales Returns and Allowances .............................................. 7,500Sales Discounts (150)Cash ................................................................................... 7,350Merchandise Inventory .......................................................... 4,500Cost of Merchandise Sold ................................................ 4,500Ex. 6–12(1) Sold merchandise on account, $12,000.(2) Recorded the cost of the merchandise sold and reduced the merchandise inventory account,$7,800.(3) Accepted a return of merchandise and granted an allowance, $2,500.(4) Updated the merchandise inventory account for the cost of the merchandise returned,$1,625.(5) Received the balance due within the discount period, $9,405. [Sale of $12,000, less return of$2,500, less discount of $95 (1% × $9,500).]Ex. 6–13a. $18,000b. $18,375c. $540 (3% × $18,000)d. $17,835Ex. 6–14a. $7,546 [Purchase of $8,500, less return of $800, less discount of $154 ($7,700 × 2%)]b. Merchandise InventoryEx. 6–15Offer A is lower than offer B. Details are as follows:A BList price ............................................................................... $40,000 $40,300Less discount ......................................................................... 800 403$39,200 $39,897 Transportation (625)$39,825 $39,897Ex. 6–16(1) Purchased merchandise on account at a net cost of $8,000.(2) Paid transportation costs, $175.(3) An allowance or return of merchandise was granted by the creditor, $1,000.(4) Paid the balance due within the discount period: debited Accounts Payable, $7,000, and cre-dited Merchandise Inventory for the amount of the discount, $140, and Cash, $6,860.Ex. 6–17a. Merchandise Inventory .......................................................... 7,500Accounts Payable ............................................................. 7,500b. Accounts Payable ................................................................... 1,200Merchandise Inventory .................................................... 1,200c. Accounts Payable ................................................................... 6,300Cash ................................................................................... 6,174Merchandise Inventory (126)a. Merchandise Inventory .......................................................... 12,000Accounts Payable—Loew Co. ......................................... 12,000b. Accounts Payable—Loew Co. ............................................... 12,000Cash ................................................................................... 11,760Merchandise Inventory (240)c. Accounts Payable*—Loew Co. ............................................. 2,940Merchandise Inventory .................................................... 2,940d. Merchandise Inventory .......................................................... 2,000Accounts Payable—Loew Co. ......................................... 2,000e. Cash (940)Accounts Payable—Loew Co. (940)*Note: The debit of $2,940 to Accounts Payable in entry (c) is the amount of cash refund due from Loew Co. It is computed as the amount that was paid for the returned merchandise, $3,000, less the purchase discount of $60 ($3,000 × 2%). The credit to Accounts Payable of $2,000 in en-try (d) reduces the debit balance in the account to $940, which is the amount of the cash refund in entry (e). The alternative entries below yield the same final results.c. Accounts Receivable—Loew Co. .......................................... 2,940Merchandise Inventory .................................................... 2,940d. Merchandise Inventory .......................................................... 2,000Accounts Payable—Loew Co. ......................................... 2,000e. Cash (940)Accounts Payable—Loew Co. ............................................... 2,000Accounts Receivable—Loew Co. .................................... 2,940Ex. 6–19a. $10,500b. $4,160 [($4,500 – $500) ⨯ 0.99] + $200c. $4,900d. $3,960e. $834 [($1,500 – $700) ⨯ 0.98] + $50Ex. 6–20a. At the time of sale c. $4,280b. $4,000 d. Sales Tax PayableEx. 6–21a. Accounts Receivable ............................................................... 9,720Sales ................................................................................... 9,000Sales Tax Payable (720)Cost of Merchandise Sold ...................................................... 6,300Merchandise Inventory .................................................... 6,300b. Sales Tax Payable ................................................................... 9,175Cash ................................................................................... 9,175a. Accounts Receivable—Beta Co. ........................................... 11,500Sales ................................................................................... 11,500 Cost of Merchandise Sold ...................................................... 6,900Merchandise Inventory .................................................... 6,900b. Sales Returns and Allowances (900)Accounts Receivable—Beta Co. (900)Merchandise Inventory (540)Cost of Merchandise Sold (540)c. Cash ......................................................................................... 10,388Sales Discounts (212)Accounts Receivable—Beta Co. ...................................... 10,600Ex. 6–23a. Merchandise Inventory .......................................................... 11,500Accounts Payable—Superior Co. ................................... 11,500b. Accounts Payable—Superior Co. (900)Merchandise Inventory (900)c. Accounts Payable—Superior Co. ......................................... 10,600Cash ................................................................................... 10,388Merchandise Inventory (212)Ex. 6–24a. debit c. credit e. debitb. debit d. debit f. debitEx. 6–25(b) Cost of Merchandise Sold (d) Sales (e)Sales Discounts(f) Sales Returns and Allowances (g) Salaries Expense (j) Supplies ExpenseEx. 6–26a. 2003: 2.07 [$58,247,000,000 ÷ ($30,011,000,000 + $26,394,000,000)/2]2002: 2.24 [$53,553,000,000 ÷ ($26,394,000,000 + $21,385,000,000)/2]b.These analyses indicate a decrease in the effectiveness in the use of the assets to generateprofits. This decrease is probably due to the slowdown in the U.S. economy during 2002–2003. However, a comparison with similar companies or industry averages would be helpful in making a more definitive statement on the effectiveness of the use of the assets.Ex. 6–27a. 4.13 [$12,334,353,000 ÷ ($2,937,578,000 + $3,041,670,000)/2]b. Although Winn-Dixie and Zales are both retail stores, Zales sells jewelry at a much slowervelocity than Winn-Dixie sells groceries. Thus, Winn-Dixie is able to generate $4.13 of sales for every dollar of assets. Zales, however, is only able to generate $1.53 in sales per dollar of assets. This makes sense when one considers the sales rate for jewelry and the relative cost of holding jewelry inventory, relative to groceries. Fortunately, Zales is able to counter its slow sales velocity, relative to groceries, with higher gross profits, relative to groceries. Appendix 1—Ex. 6–28a. and c.SALES JOURNALCost of MerchandiseSold Dr.Invoice Post.Accts. Rec. Dr. MerchandiseDate No. Account Debited Ref.Sales Cr. Inventory Cr.2006Aug. 3 80 Adrienne Richt ................... ✓12,000 4,0008 81 K. Smith .............................. ✓10,000 5,50019 82 L. Lao .................................. ✓9,000 4,00026 83 Cheryl Pugh ........................ ✓14,000 6,50045,000 20,000b. andc.PURCHASES JOURNALAccounts Merchandise OtherPost Payable Inventory Accounts Post.Date Account Credited Ref.Cr. Dr. Dr. Ref. Amount2006Aug. 10 Draco Rug Importers ................. ✓8,000 8,00012 Draco Rug Importers ................. ✓3,500 3,50021 Draco Rug Importers ................. ✓19,500 19,50031,000 31,000d.Merchandise inventory, August 1 ............................................... $ 19,000Plus: August purchases ................................................................ 31,000Less: Cost of merchandise sold ................................................... (20,000)Merchandise inventory, August 31 ............................................. $ 30,000ORQuantity Rug Style Cost2 10 by 6 Chinese* $ 7,5001 8 by 10 Persian 5,5001 8 by 10 Indian 4,0002 10 by 12 Persian 13,000$ 30,000*($4,000 + $3,500)。

外贸发票的分类

在国际贸易中,不同的用途使用不同的发票,不同的发票名称表示不同的发票种类,缮制时应严格按信用证的规定。

常见的发票种类及缮制方法如下:(1)商业发票:若L/C规定为INVOICE(发票)、COMMERCIAL INVOICE(商业发票)、SHIPPING INVOICE(装运发票)、TRADE INVOICE(贸易发票),一律可按商业发票掌握,一般只需将发票名称印为“INVOICE”字样。

(2)详细发票:若L/C规定“DETAILED INVOICE”,则如果发票内印有“INVOICE”字样,前面须加“DETAILED”,发票内容应将货物名称、规格、数量、单价、价格条件、总值等详细列出。

(3)证实发票:证实发票是证明所载内容真实、正确的一种发票,证实的内容视进口商的要求而定,如:发票内容真实无误、货物的真实产地、商品品质与合同相符、价格正确等等。

如果L/C规定“CERTIFIED INVOICE”,发票名称应照打,同时划去发票下通常印就的“E. &. O. E.”字样,通常在发票内注明“WE HEREBY CERTIFY THAT THE CONTENTS OF INVOICE HEREIN ARE TRUE &CORRECT”。

有些国家对证实发票规定有一定的格式,作为货物进口清关课以较低关税或免税证明。

有些地区的进口商凭证实发票代替海关发票办理清关或取得关税优惠。

有些进口商凭证实发票证明佣金未包括在货价内,借以索取价外报酬。

如果L/C规定“VISAED INVOIE”(签证发票),并指定签证人,则需由签证人在发票上盖章签字作签证,并加注证明文句,若证中未指定签证人,则以出口国商会作为签证人,其余与证实发票同。

(4)收妥发票,或称钱货两讫发票:若L/C规定需“RECEIPT INVOICE”,则照打名称,并在发票结文签字处加注货款已收讫条款:VALUE/PAYMENT RECEIVED UNDER CREDIT NO.××× ISSUED BY ××× BANK。

发票管理制度英文翻译范文

发票管理制度英文翻译范文Invoice Management System1. IntroductionIn order to effectively manage the company's financial transactions and ensure accurate record-keeping, it is essential to establish a systematic Invoice Management System. This system will outline the various processes involved in generating, issuing, receiving, recording, and archiving invoices. Adhering to this system will not only streamline the company's financial operations but also enable smooth auditing processes.2. ObjectivesThe primary objectives of the Invoice Management System are as follows:2.1. To ensure accurate and timely invoicing for goods and services provided by the company.2.2. To maintain appropriate control over invoice generation, approval, and delivery processes.2.3. To enable efficient tracking and monitoring of invoice payments.2.4. To facilitate proper recording and archiving of invoices for future reference and audits.2.5. To mitigate the risk of errors and fraud in the invoicing process.3. Responsibilities3.1. The Finance Department:3.1.1. Design and implement the Invoice Management System. 3.1.2. Generate invoices promptly and accurately.3.1.3. Verify the accuracy and completeness of invoices before issuing.3.1.4. Oversee the approval process for invoices.3.1.5. Maintain records of all issued and received invoices.3.1.6. Coordinate with other departments to resolve any invoicing discrepancies.3.1.7. Monitor the timely payment of invoices.3.1.8. Archive invoices in accordance with the company's recordkeeping policy.3.1.9. Provide necessary training and support to employees involved in the invoicing process.3.2. Business Units and Departments:3.2.1. Provide accurate and timely information to the Finance Department for invoice generation.3.2.2. Review and approve invoices within the allocated time frame.3.2.3. Communicate any discrepancies or concerns regarding invoices to the Finance Department promptly.3.2.4. Ensure timely payment of invoices within the agreed terms.4. Invoice Generation4.1. Invoices shall be generated promptly after the completion of a transaction for goods or services.4.2. The invoice should clearly state the following information: 4.2.1. Name and address of the company providing the goods or services.4.2.2. Name and address of the customer.4.2.3. Invoice number and date.4.2.4. Description of the goods or services provided.4.2.5. Quantity and unit price of the goods or services provided. 4.2.6. Total amount payable.4.2.7. Payment terms and due date.4.2.8. Any applicable taxes or fees.4.2.9. Payment instructions.5. Invoice Approval5.1. Invoices shall be approved by the relevant authority within each department or business unit.5.2. The approving authority shall verify the accuracy and completeness of the invoice before granting approval.5.3. Invoices exceeding a predefined threshold shall require additional approvals from higher-level authorities.5.4. Any discrepancies or concerns identified during the approval process shall be addressed and resolved before approving the invoice.6. Invoice Delivery6.1. Invoices shall be delivered to customers through the preferred communication channel, such as email or post.6.2. The delivery method shall ensure that invoices are received by the customer in a timely manner.6.3. The Finance Department shall maintain a record of all delivered invoices.7. Invoice Receipt and Recording7.1. Upon receiving an invoice from a supplier, the relevant department or business unit shall verify its accuracy and completeness.7.2. Any discrepancies or concerns identified shall be promptlycommunicated to the Finance Department.7.3. The Finance Department shall record the receipt of the invoice and update the accounts payable ledger accordingly.7.4. The received invoices shall be retained for future reference and audit purposes.8. Invoice Payment8.1. Invoices shall be paid within the agreed payment terms.8.2. The Finance Department shall monitor the payment status of invoices and follow up on any delays or outstanding payments. 8.3. Any disputes or concerns regarding invoices shall be resolved through mutually agreed-upon processes between the company and the supplier.9. Invoice Archiving9.1. Invoices shall be archived systematically in accordance with the company's recordkeeping policy.9.2. The Finance Department shall ensure that archived invoices are easily retrievable for future audits or reference purposes.9.3. Archived invoices shall be stored in a secure and controlled environment to prevent loss, damage, or unauthorized access. 10. Training and Compliance10.1. The Finance Department shall provide necessary training to employees involved in the invoicing process, ensuring their understanding of the Invoice Management System.10.2. Regular audits shall be conducted to ensure compliance with the established processes and procedures outlined in the Invoice Management System.10.3. Any non-compliance or deviation from the InvoiceManagement System shall be reported and addressed promptly. 11. ConclusionAn efficient and systematic Invoice Management System is crucial for the smooth financial operations of the company. By adhering to the outlined processes and procedures, the company can ensure accurate invoicing, timely payments, proper recordkeeping, and compliance with auditing requirements. The Invoice Management System requires collaboration between the Finance Department and other business units to achieve its objectives successfully.。

数电发票的开票流程

数电发票的开票流程English Answer:Electronic invoices (e-invoices) are digital invoices that are issued, received, and processed electronically. They offer a number of advantages over traditional paper invoices, such as reduced costs, improved efficiency, and increased security.Step 1: Invoice Creation.The e-invoice creation process begins with the generation of an invoice in an accounting software program. The invoice should include all of the necessary information, such as the invoice number, date, customer name and address, product or service description, quantity, unit price, total amount, and payment terms.Step 2: Invoice Validation.Once the invoice is created, it should be validated to ensure that all of the information is correct and complete. This can be done manually or using an automated validation tool.Step 3: Invoice Transmission.Once the invoice is validated, it can be transmitted to the customer electronically. This can be done via email, EDI, or a web portal.Step 4: Invoice Receipt.The customer receives the e-invoice electronically and can view it and process it using their own accounting software program.Step 5: Invoice Processing.The customer processes the e-invoice by paying the invoice amount and recording the transaction in their accounting system.Benefits of E-Invoicing.Reduced costs: E-invoicing eliminates the need for printing, mailing, and postage costs.Improved efficiency: E-invoicing automates the invoice process, which can save time and effort.Increased security: E-invoices are more secure than paper invoices, as they are less likely to be lost, stolen, or altered.Environmental benefits: E-invoicing reduces the use of paper and other resources, which can benefit the environment.Chinese Answer:电子发票的开票流程。

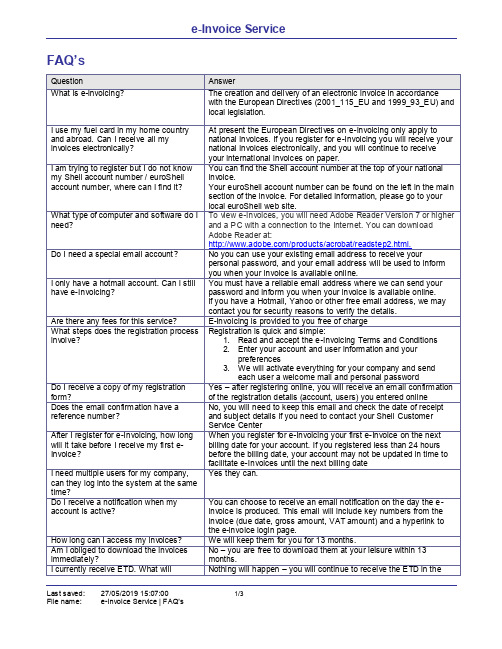

e-InvoiceService

Do I need a sonly have a hotmail account. Can I still have e-Invoicing?

Are there any fees for this service? What steps does the registration process in vol ve ?

e-Invoice Service

FAQ’S

Question What is e-Invoicing?

Answer

The creation and delivery of an electronic invoice in accordance with the European Directives (2001_115_EU and 1999_93_E U) and local legislation.

same way.

This service (called „EID‟ – electronic invoice data) will be available in the course of 2008.

Yes – The watermark on the invoice will show that the signature no longer is valid, indicating that the content of the file has been changed. You can print the PDF -invoice many times, but only the electronic PDF-file with certificate is the original legal invoice. The fiscal legislation requests that you store e-invoic es in electronic format. Storing a paper print and deleting the P DF invoice, is against regulations. No – the Shell e-invoicing service is fully compliant with local tax legislation. Yes – as soon as you are registered, you will receive a Welcome email from Atos with a system generat ed password. At first login, you will have to change this password into your own password, which can be the same as your euroS hell Online password. No – the invoice will be stored in your personal e-invoice web archive for 13 mont hs. At the moment of registration, you can choose to receive an email notification as soon as a new invoice is available in your web archi ve. The invoices that are normally bundled in one envelope, will now arrive at the same time in your personal web archive. You can download multiple invoice in one go, by simply selection them all, and choosing „Download‟. The invoices that are normally consolidated onto one invoice will still remain consolidated int o one invoice and will appear as one single invoice in your personal web archive. You need Adobe Reader version 7 or higher to view the e-invoic es and a P C with connection to the int ernet.

INVOICE STATEMENT发票声明书

1)收件人: Consignee: 地址: Address: 公司名称: Company Name: 城市/地区号: Town/Area Code: 电话 / 传真: Phone / Fax: 州名/国家: State/County:

2)运单号: Airway Bill No: 订单号(如果有): PO NO.(if have):

Total:

11)本人认为以上提供的资料属实和正确,货物原产地是:

I declare that the above information is true and correct to the best of my knowledge and that the goods are ATEMENT

10)报关总价 Total Value (USD$)

mation is true and correct to the best of my knowledge and

origin

Sample 签名: Signature: 公章: Stamp:

Reason for Export:

13)发件人 Consignor: 地址: Address: 州名/国家 State/County:

公司名称: Company Name: 城市/地区号: Town/Area Code: 电话/传真/电子邮件: Phone/Fax/E-mail:

3)详细的商品名称 4)海关商品编码 Full Description of Harmonised Goods code(if have) 5)生产厂商 Manufacturer 6)重量 Weight 9)单价 7)体积 8)数量 Unit Value Dimensions No.of Items (US$)

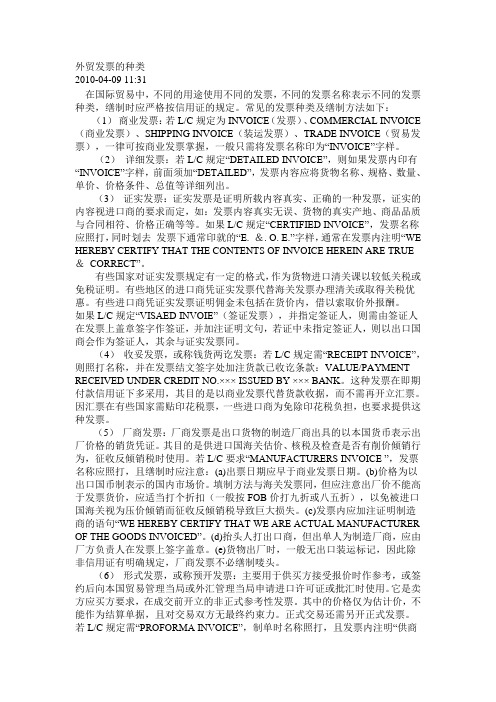

外贸发票的种类

外贸发票的种类2010-04-09 11:31在国际贸易中,不同的用途使用不同的发票,不同的发票名称表示不同的发票种类,缮制时应严格按信用证的规定。

常见的发票种类及缮制方法如下:(1)商业发票:若L/C规定为INVOICE(发票)、COMMERCIAL INVOICE (商业发票)、SHIPPING INVOICE(装运发票)、TRADE INVOICE(贸易发票),一律可按商业发票掌握,一般只需将发票名称印为“INVOICE”字样。

(2)详细发票:若L/C规定“DETAILED INVOICE”,则如果发票内印有“INVOICE”字样,前面须加“DETAILED”,发票内容应将货物名称、规格、数量、单价、价格条件、总值等详细列出。

(3)证实发票:证实发票是证明所载内容真实、正确的一种发票,证实的内容视进口商的要求而定,如:发票内容真实无误、货物的真实产地、商品品质与合同相符、价格正确等等。

如果L/C规定“CERTIFIED INVOICE”,发票名称应照打,同时划去发票下通常印就的“E. &. O. E.”字样,通常在发票内注明“WE HEREBY CERTIFY THAT THE CONTENTS OF INVOICE HEREIN ARE TRUE &CORRECT”。

有些国家对证实发票规定有一定的格式,作为货物进口清关课以较低关税或免税证明。

有些地区的进口商凭证实发票代替海关发票办理清关或取得关税优惠。

有些进口商凭证实发票证明佣金未包括在货价内,借以索取价外报酬。

如果L/C规定“VISAED INVOIE”(签证发票),并指定签证人,则需由签证人在发票上盖章签字作签证,并加注证明文句,若证中未指定签证人,则以出口国商会作为签证人,其余与证实发票同。

(4)收妥发票,或称钱货两讫发票:若L/C规定需“RECEIPT INVOICE”,则照打名称,并在发票结文签字处加注货款已收讫条款:VALUE/PAYMENT RECEIVED UNDER CREDIT NO.××× ISSUED BY ××× BANK。

DB33∕T 1136-2017 建筑地基基础设计规范

5

地基计算 ....................................................................................................................... 14 5.1 承载力计算......................................................................................................... 14 5.2 变形计算 ............................................................................................................ 17 5.3 稳定性计算......................................................................................................... 21

主要起草人: 施祖元 刘兴旺 潘秋元 陈云敏 王立忠 李冰河 (以下按姓氏拼音排列) 蔡袁强 陈青佳 陈仁朋 陈威文 陈 舟 樊良本 胡凌华 胡敏云 蒋建良 李建宏 王华俊 刘世明 楼元仓 陆伟国 倪士坎 单玉川 申屠团兵 陶 琨 叶 军 徐和财 许国平 杨 桦 杨学林 袁 静 主要审查人: 益德清 龚晓南 顾国荣 钱力航 黄茂松 朱炳寅 朱兆晴 赵竹占 姜天鹤 赵宇宏 童建国浙江大学 参编单位: (排名不分先后) 浙江工业大学 温州大学 华东勘测设计研究院有限公司 浙江大学建筑设计研究院有限公司 杭州市建筑设计研究院有限公司 浙江省建筑科学设计研究院 汉嘉设计集团股份有限公司 杭州市勘测设计研究院 宁波市建筑设计研究院有限公司 温州市建筑设计研究院 温州市勘察测绘院 中国联合工程公司 浙江省电力设计院 浙江省省直建筑设计院 浙江省水利水电勘测设计院 浙江省工程勘察院 大象建筑设计有限公司 浙江东南建筑设计有限公司 湖州市城市规划设计研究院 浙江省工业设计研究院 浙江工业大学工程设计集团有限公司 中国美术学院风景建筑设计研究院 华汇工程设计集团股份有限公司

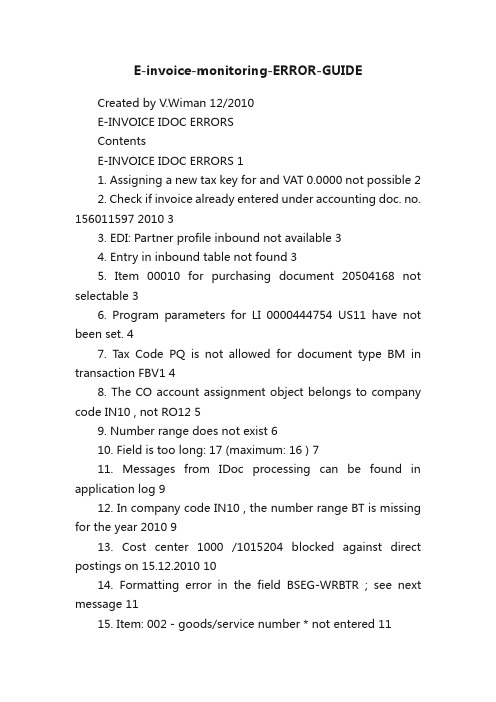

E-invoice-monitoring-ERROR-GUIDE

E-invoice-monitoring-ERROR-GUIDECreated by V.Wiman 12/2010E-INVOICE IDOC ERRORSContentsE-INVOICE IDOC ERRORS 11. Assigning a new tax key for and VAT 0.0000 not possible 22. Check if invoice already entered under accounting doc. no. 156011597 2010 33. EDI: Partner profile inbound not available 34. Entry in inbound table not found 35. Item 00010 for purchasing document 20504168 not selectable 36. Program parameters for LI 0000444754 US11 have not been set. 47. Tax Code PQ is not allowed for document type BM in transaction FBV1 48. The CO account assignment object belongs to company code IN10 , not RO12 59. Number range does not exist 610. Field is too long: 17 (maximum: 16 ) 711. Messages from IDoc processing can be found in application log 912. In company code IN10 , the number range BT is missing for the year 2010 913. Cost center 1000 /1015204 blocked against direct postings on 15.12.2010 1014. Formatting error in the field BSEG-WRBTR ; see next message 1115. Item: 002 - goods/service number * not entered 1116. PO item EP772946 /10 for vendor has GR-based IV activated but GR was not found 1117. Tax code K7 in procedure is invalid 1118. Tax data is missing at item level 1219. No (active) partner profile: sender LI 0000323023 , message type INVOIC 1320. ISO country key LAND1 is not assigned (header) 1321. Condition 4300 is only defined for customers 1422. Evaluated receipt settlement is active for purchase order 20921626 00010 1523. "User WF-BATCH already processing Purchasing doc. item 20943908 00010" 16 GENERIC VENDOR 1624. Unknown vendor. 1625. TAX ID found from Idoc. 171.Assigning a new tax key for and VAT 0.0000 not possibleRelates ALWAYS to missing OBCD table entry.Combinations of error message:a) Assigning a new tax key for ’and VAT 0.0000 not possibleOBCD entry for TAX type “VAT” is missing:SOLUTION:UPDATE OBCD table with:LI 465391 VAT 0.0000 FI P0(Tax type “VAT” is default value in idoc, if oth er Tax types are not identified.)b) Assigning a new tax key for F1S and VAT 0.0000 not possibleOBCD entry for TAX type “F1S” is missing.SOLUTION:UPDATE OBCD table with:LI 465391 F1S 0.0000 FI P0SAS needs to ask table update via ITSM ticket. (Only decimal related updates are preapproved in MS list, those can be done without ITSM ticket if needed. Example 13.00 rate exists, but idoc requires 13.000 (three decimals)).Notice:CTY (country) needs to be correct in OBCD table.Normal invoices, check the company code E1EDKA1 RE –LAND1.Freight cases:OBCD should be updated based on LAND1 field= SHIP TO COUNTRY: EIEDPA1 WE2.Check if invoice already entered under accounting doc. no. 156011597 2010→SAS needs to be check if this invoice is duplicate.Same invoice reference already used with document 156011597.3.EDI: Partner profile inbound not availableE-invoicing configuration missing for vendor. Error 56 is from partner profile, check: transaction WE20.→Request for SAS: Please raise ITSM ticket IT S AP FinancialSupport to add einvoicing configuration to vendor with selected companycode. SAS is required to add e-invocingconfiguration excel file to ticket. SAS needs to request also Idoc restarting after configurationsare in place.4.Entry in inbound table not foundE-invoicing configuration missing for vendor. Error 56 is from partnerprofile check: table WE20.→Request for SAS: Please raise ITSM ticket IT SAP Financial Support to add einvoicing configuration to vendor with selected companycode. SAS is required to add e-invocingconfiguration excel file to ticket. SAS needs to request also Idoc restarting after configurationsare in place5.Item 00010 for purchasing document 20504168 not selectablePO item is locked or deleted.To check the PO, use transaction ME23N – purchase order –other purch. Order→SOLUTION:SAS needs to contact to buyer to remove the lock.(they can switch invoice to wf or reprocessidoc after lock is removed.)6.Program parameters for LI 0000444754 US11 have not been set.Partner profile ok, but OBCE table configuration for this company code is missing.NOTE: In this error normally also other E-invoice configuration are missing for US11!!→Request for SAS: Please raise ITSM ticket IT SAP Financial Support to add e-invoicing configuration to vendor with selected company code. SAS is required to add e-invoicingconfiguration excel file to ticket.7.Tax Code PQ is not allowed for document type BM in transaction FBV1This combination is not allowed according to the validation rules.BM document type (Freight Appr WF)is coming from OBCE table,Taxcode PQ (Accruals, purchases 0% (Expenditure)) is coming from OBCD table.→SAS should change the coding either in OBCE or OBCD table for vendor. Or they can switch invoice to scanning work flow.To check OBCE:To check OBCD:8.The CO account assignment object belongs to company code IN10 , not RO12Invoice company code doesn’t match to delivery/purchase order mentioned in idoc.SOLUTION:SAS: switch inv. to scanning workflow. P2P freight invoices requires manual CC change.More information: This problem is normal in plant-to-plant cases, where freight invoices logic doesn’t work.(comment from SAS: logistics process problem, requires delivery term change.)Accountant needs to manually change the cost center to sender plant “inbound” costcenter (in this case RO12).Example:Invoice received for RO12Idoc field E1EDKA1 RE – Y3EDKPAR.PO and delivery can be found from E1EDP01 – E1EDP08 field.<- Purchase order<- Delivery To view PO: ME23NTo view Delivery: VL03NSAS needs to switch the invoice to scanning workflow andpost invoice to companycode IN10.9.Number range does not existCheck the error analysis by double clicking the error:Check if MM number range (logistics invoice verification) is not opened.-> YCA_GRID, NRIV, Subobject value :*company code*, Number range number: 01SOLUTION: SAS to request number range opening from MM team, or switch invoice to SWF and change the document type.10.Field is too long: 17 (maximum: 16 )Check detailed data from “logging” field<- Idoc segment<- Field nameIDOC view:Idoc field contains too many characters.SAS needs to switch invoice to scanning workflow. SAS could also communicate the problem with vendor if several errors exist.11.Messages from IDoc processing can be found in application logCheck more info from application log:Correct error can be found from “Message text”12.In company code IN10 , the number range BT is missing for the year 2010Check YCA_GRID, NRIV, Object name: RF_BELEG / Sub object value: IN10 / Number range number: BT/ year: 2010E-invoicing program has picked the document type either from OBCE table, or from YMM_EIN_DOCTYPE table.SAS to request number range opening for companycode via ITSM ticket.13.Cost center 1000 /1015204 blocked against direct postings on 15.12.2010One of the items in invoice is linked to blocked cost center.SAS needs to switch the invoice to scanning workflow and change the cost center manually.More information: To check the cost center, user KS03 and check interleaf “Control”14.Formatting error in the field BSEG-WRBTR ; see next messageProgramming error, relates to freight invoice invoice splitting.Issue VWS4VC7 created, will be solved after SAP upgrade freeze.→SAS nee ds to switch the invoice to scanning workflow.15.Item: 002 - goods/service number * not enteredOBCB entries missing from vendor.→SAS needs to request e-invoicing configuration for OBCB table via ITSM ticket.16.PO item EP772946 /10 for vendor has GR-based IV activated but GR wasnot foundGoods receipt missing from PO.→SAS needs to wait until the GR is done.Then they are able to reprocess the Idoc in workflow.→SAS can consider to increase “WAIT” time, if that is too short, example 0 hours.(Table: Y3FIT_VEN2WAIT)17.Tax code K7 in procedure is invalidCompany code FI11 doesn’t have active taxc ode called K7.Check FTXP:→Proposed solution:OBCD table to be checked by SAS:AND for further processing, SAS needs to send the invoice to scanning workflow and change the tax code.18.Tax data is missing at item level→Remember to check ALL errors for this vendor:Idoc error solving should be started from the first possible error, which is located in the bottom of the list! In this case “Program parameters for LI….”, which means that e-invoice configuration is missing for this companycode and SAS needs to create ITSM ticket to IT with configuration excel.19.No (active) partner profile: sender LI 0000323023 , message type INVOICPartnerprofile (WE20) has been marked to be “inactive”.Please activate it from “Classification” sheet.20.ISO country key LAND1 is not assigned (header)Idocs country is not defined according to ISO standards, which is the rule of SAP.SAS to switch invoice to SWF, and contact to vendor and inform correct country code to them.To check what field Idoc cannot understand, open the errorFrom “Logging” sheet, you can find usefull information to help to find the corre ct segment:(Sometimes segment is not exactly correct.)Check field E1EDPA1 – LAND1 from Idoc:21.Condition 4300 is only defined for customersIn this case the only value in Idoc, which relates to 4300 is payment term in idoc segment 16: (Idocs own diagnosis leads to segment 19 is misleading.)Check payment term OBB8,And you can find that this payment term is defined only for customers.SAS needs to switch the invoice to scanning workflow.And double check, if invoice should be posted with 4300 payment term -> requires paymentterm modification, or if it should be posted with other payment term.22.Evaluated receipt settlement is active for purchase order 20921626 00010Purchasing document has “ERS” tick on item level.Check PO with ME23N.→SAS needs to switch invoice to SWF, and check with buyer if invoice is ERS process relevant (invoiced separately via ERS process), or if ERS tick needs to be removed from PO.23."User WF-BATCH already processing Purchasing doc. item 2094390800010"PO is reserved by other background job or other user.→SAS to reprocess the Idoc in workflow.GENERIC VENDORIDOC STATUS 53VENDOR 513314REQUIRES ALWAYS CHECKING, WHY INVOICE HAS BEEN PARKED TO GENERIC VENDOR AND NOT TO CORRECT VENDOR.*************************************************************** *********************24.Unknown vendor.Idoc field: E1EDKA1 RSIdoc field: Y3EDKPARREASON: Service provider “OCR” couldn’t recognize vendor from the invoice.Process known and defined by SAS.SAS needs to switch invoice to scanning workflow.25.TAX ID found from Idoc.Two possibilities:- No VAT ID maintained in vendor master- Two or more vendors having same VAT ID in vendor masterINVESTIGATION:Check Idoc TAX ID from idoc field:E1EDKA RS – Y3EDKPAR - TAXIDCompare tax id to WAS (PWF) table: YBC_EINV_LFA1 (to view the table, use SE16)Search tax id from data.IF not found:→SAS to update vendor master for selected vendor.(WAS table YBC_EINV_LFA1 is automatically updated via background job on daily basis if vendor master is changed.) If found:→SAS should update “exclude” table, which excludes not used vendors away from WAS table YBC_EINV_LFA1.Exclude table YEFIT_EXC, updated with transaction YEINV_EXCL.。

IFS系统介绍

IFS 应用系统介绍................................................................................................................................................9

ifs系统介绍ifs系统win8系统功能介绍微信广告系统介绍系统介绍ppt系统介绍系统介绍ppt模板图书管理系统介绍linux系统介绍小米v6系统介绍

IFS 应用系统

功能方案

广州万迅电脑软件有限公司

广州万迅电脑软件有限公司 Tel:020-83283115 Fax:020-83283054

IFS 应用系统功能概要......................................................................................................................................10 IFS 应用系统 ......................................................................................................................................................10

开电子发票的操作流程

开电子发票的操作流程英文回答:Step 1: Registration and Application.Register for an electronic invoice (e-invoice) account with the tax authority or an authorized e-invoice platform.Complete the registration process and submit the necessary documents, such as business license and tax registration certificate.Step 2: Obtain Digital Certificate.Apply for a digital certificate from a certified authority to verify the authenticity and integrity of e-invoices.Install the digital certificate on the computer or device used for e-invoicing.Step 3: Software Installation.Install e-invoicing software provided by the tax authority or an authorized e-invoice platform.Configure the software according to the specific requirements of the business.Step 4: Issuing E-Invoices.Create e-invoices in the software using the prescribed format and data structure.Include mandatory fields such as invoice number, invoice date, seller and buyer details, goods or services, unit price, quantity, total amount, and tax details.Validate the e-invoices before submitting them to the tax authority or e-invoice platform.Step 5: Submission and Approval.Submit the validated e-invoices to the tax authority or e-invoice platform through the designated channel.The tax authority or e-invoice platform will review and approve the e-invoices, if they meet the validation criteria.Step 6: Issuance and Delivery.Once approved, the tax authority or e-invoice platform will issue the e-invoices with a unique invoice reference number (IRN).The e-invoices can be delivered to the buyers via email, SMS, or other electronic means.Step 7: Verification and Payment.Buyers can verify the authenticity of the e-invoices using the IRN and digital signature.Payments can be made electronically through designated payment channels.Step 8: Reporting and Reconciliation.Businesses are required to maintain records of e-invoices issued and received.They can generate reports from the e-invoicing software for compliance and reconciliation purposes.中文回答:第一步,注册和申请。

数电票季度申报流程

数电票季度申报流程英文回答:Electronic C-Invoicing Quarterly Reporting Process.Step 1: Preparation.Prepare all relevant e-invoice data for the quarter.Ensure that all invoices have been issued and received through the authorized platform.Obtain the necessary information, such as invoice numbers, amounts, and tax details.Step 2: Data Collection.Collect the e-invoice data from the platform or designated system.Verify the completeness and accuracy of the data.Organize the data into the required format for submission.Step 3: Submission.Access the e-invoice reporting portal.Upload the prepared e-invoice data files.Submit the data for validation and processing.Step 4: Validation and Processing.The platform will validate the data against the prescribed standards and requirements.Any errors or discrepancies will be identified and reported.The processed data will be used to generate thequarterly e-invoice report.Step 5: Review and Approval.Review the generated report for accuracy and completeness.Make any necessary corrections or adjustments.Approve the report for final submission.Step 6: Final Submission.Submit the approved report to the designated authority.The authority will process and store the report for compliance purposes.中文回答:电子发票季度申报流程。

简述发票作废的流程

简述发票作废的流程英文回答:Invoice Voiding Procedure.Step 1: Determine the Reason for Voiding.Error in invoice information (e.g., incorrect date, amount, customer details)。

Duplicate invoice issued.Customer request to cancel the invoice.Invoice has been paid and a credit memo needs to be issued.Step 2: Notify the Customer.Inform the customer about the reason for voiding theinvoice.Provide evidence of the error or cancellation request.Request the customer to acknowledge the void invoice.Step 3: Prepare a Void Invoice.Create a new invoice with a negative sign (-) or "Void" watermark.Include the original invoice number and date.Clearly state the reason for voiding the invoice.Step 4: Issue the Void Invoice.Send the void invoice to the customer.Keep a copy of the void invoice for your records.Step 5: Update Accounting Records.Record the void invoice in your accounting software.Adjust the outstanding balance for the customer.Reverse any revenue or expense entries related to the original invoice.Step 6: Document the Process.Maintain a record of all invoices voided, including the reason for voiding.Keep a copy of the void invoice and customer acknowledgment.中文回答:发票作废流程。

海运费用英语

海运费用英语海运费ocean freight集卡运费、短驳费Drayage订舱费booking charge报关费customs clearance fee操作劳务费labour fee or handling charge 商检换单费exchange fee for CIP换单费D/O fee拆箱费De-vanning charge港杂费port sur-charge电放费B/L surrender fee冲关费emergent declearation change海关查验费customs inspection fee待时费waiting charge仓储费storage fee改单费amendment charge拼箱服务费LCL service charge动、植检疫费animal & plant quarantine fee 移动式其重机费mobile crane charge进出库费warehouse in/out charge提箱费container stuffing charge滞期费demurrage charge滞箱费container detention charge卡车运费cartage fee商检费commodity inspection fee转运费transportation charge污箱费container dirtyness change坏箱费用container damage charge清洁箱费container clearance charge分拨费dispatch charge车上交货FOT ( free on track )电汇手续费T/T fee转境费/过境费I/E bonded charge空运方面的专用术语空运费air freight机场费air terminal charge空运提单费airway bill feeFSC (燃油附加费) fuel surchargeSCC(安全附加费)security sur-charge抽单费D/O fee上海港常用术语内装箱费container loading charge(including inland drayage) 疏港费port congestion charge他港常用术语场站费CFS charge文件费document charge海运maritime transportation海运保险单freight policy; marine insurance policy海运标号shipping designator海运材制材厂tide-water mill海运法Merchant Marine Act (美)海运法令ordinance regulating carriage of goods by sea海运费ocean freight海运费率ocean freight rate; sea freight海运和贮存的集装箱shipping and storage container海运货物floating cargo海运货物保险cargo marine insurance; marine cargo insurance 海运货物法例Carriage of Goods by Sea Act海运留置权maritime lien海运码头sea terminal海运事业shipping interest海运提货单marine bill of lading; ocean waybill; sea waybill海运统计maritime transport statistics; ocean transport statistics 海运信件sea mail海运业marine海运终点站 marine terminal海运费用简称(史上最全)TOP。

IBM Sterling e-Invoicing VAT 税收解决方案简介说明书

Upcoming legislation reinforces IBM Sterling e-Invoicing solutions sales opportunityValue-added tax (VAT) PrimerIn the European Union (EU) countries, VAT is an invoice-based tax. It is calculated per transaction. All business transactions require an invoice, these invoices become critical legal documents that must be processed and stored for 8 to 11 years in most jurisdictions. These stored invoices will be viewed by the tax auditor, and if the amount of tax on the invoice is not the same as the amount the company has paid, the company pays the difference. There are also potential fines for non-compliance with regulations and incomplete/missing evidence as well as the possibility of criminal prosecution for fraud.To avoid paying fines and having legal issues, companies must seek to ensure they are VAT compliant. There are two key methods of providing evidence that VAT has been paid : the EDI Compliance approach and the Digital Signature approach. These are at the opposite ends of the spectrum.The EDI Compliance approach relies on documented processes and puts a company in a historian or detective role when trying to prove compliance to regulations. Companies have to keep a lot of audit trails and process documentation, and then have to be able to follow the trail of the invoice, how it was created, and how it was processed electronically. They need to do this for potentially hundreds or thousands of invoices, which is a huge effort.The digital signature approach relies on technology to demonstrate compliance. It can be used to easily prove data integrity and authenticity – that’s specifically what it was created for. It is a much cleaner, simpler approach to compliance.When these two approaches are set against the risk, cost and complexity of long term auditability and management, digital signatures come out ahead. This is the approach IBM Sterling recommends to achieve VAT compliance, but we also work with customers who have chosen EDI compliance.Invoicing legislation continues to evolve to make the process easierThe EU electronic invoicing directives 2001/115/EC and 2006/112/EC set about reducing the burden of manual process across Europe. According to these directives, electronic invoices gain legal equivalence with paper and multiple options for compliance are defined such as digital signature and EDI as discussed earlier.(It is also important to note that there are global and local differences in companies’ approaches to invoicing. The extent of the compliance requirements in counties like the UK are less than in countries like Germany.)EU directive 2010/45, submitted In March of last year (2010), amends the original directive and removes some of the barriers to uptake of electronic invoicing. It ensures paper and electronic invoices can be treated equally.The new regulations come into effect in 2013, and companies can now use “business controls” to create a reliable audit trail rather than relying on technical solutions. However the basic guidelines about integrity and authenticity remain. Freedom of choice is not the same as all choices being equal. Companies still need to determine the optimum compliance option for their business.Invoicing options – from paper to digitalPaper95 % of all invoices are still paper. The data needs to be manually entered into an accounts payable system which is time consuming, costly, and error prone and the original invoice must be archived. The tax authorities use these archived invoices to prove compliance.ProcessThis model is useful for tax authorities that accept proof from companies who have robust, well documented processes in place. In situations where this model is in place, electronic invoicing has often been well established. Paper is still required in case of discrepancy.EDIEDI with contractual security processes is popular in specific regions/industries like France and Retail. This is strictly defined as per a 1994/820/EC recommendation which defines EDI as a security measure. This is not consistent with many modern EDI implementations.Digital signatureThis model eliminates the need for paper and process documentation by allowing signed electronic documents (like PDF, XML and EDI) as proof of compliance.ConclusionIn the end, this is not about a “one-size fits all” solution. Companies need to be able to match VAT compliance options with those of their partners. To do this, companies need to look for a solution that offers flexibility and a range of compliance options. Things to consider in this search include: – Support for all electronic options▪Digital Signature– Comprehensive signature support and industry best practices▪EDI / B2B– All document formats – EDI, XML, PDF, Web forms etc– All communication protocols – B2B protocols, email etc– Tight integration▪With your back end systems▪Automate A/P and A/R processes– Comprehensive archive / audit solution– Flexibility to interoperate with other e-Invoicing solutions and provide “on-behalf-of”services for those withoutFor more information:/software/xl/portal/content?synKey=P990396P78214T93Contact: Chris Hayes, Senior Product Marketing Manager, IBM Sterling B2B Integrator/IBM Sterling e-Invoicing, +44 208 867 8313, ******************.com。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Instructions to SAS – Process in Background

- Click on invoice in SAS User Workflow - click on Process in background

Instruction to SAS – switch to Scanning workflow

– Daily – To be done for the previous day

Incoming eInvoices monitoring in WAS

• Check the monitor:

– SE38, program: YFI9G_E3_MSG_MONITOR – Check all the invoices that are in status red.

-If content issue, the SAS user can select: ”send to scanning workflow” - it will then be posted manually based on the info given in the layout (as we do now with the PDF in scanning WF)

– For instance referring to a blocked cost center or a non-existing document (MM document), » SAS teams will switch the invoice to scanning workflow and park manually.

Incoming eInvoices monitoring in SAP

• Red: in error

– Status 56: ” EDI: Paቤተ መጻሕፍቲ ባይዱtner profile not available “ or “Entry in inbound table not found” or other » Issue is that the vendor is not configured yet. » The configuration details are given by SAS (Direct Purchase or Indirect purchase team) or Heikki Juvonen (GCO) can help. » The configuration should follow these templates: One vendor: mass upload:

Incoming eInvoices monitoring in SAP

• • Red: in error

– Status 51:

If related to Tax determination, need to add the correct line in OBCD for this vendor. Message is of type “Assigning a new tax key xxxx for yyyy and VAT xx.xx not possible”. After that, inform SAS to “process the idoc in background” If error message is ”Item: 003 - goods/service number * not entered” or ” Program parameters for LI 0000404199 FI11 have not been set”

Microsoft Office Excel 97-2003 Worksheet Microsoft Office Excel 97-2003 Worksheet

» After, the idoc needs to be reprocessed (not in WF yet). » SE38: RC1_IDOC_SET_STATUS, set status to 64 » Then: SE38: RBDAPP01 to process to status 62

Incoming eInvoices monitoring in SAP

• Yellow: not processed yet

– status 64: inbound messages have not been processed yet: » Program is RBDAPP01 » check if background job FI: EINVOICE INB.INVOICE IDOC is scheduled. – Status 62: » Check if there is a delay set in SM30 for this vendor, table: Y3FIT_VEN2WAIT. » If no delay, then the message is in error. » To check the error, look in SM58 (requires Firefighter, FSP emergency user) if there are some ARFC in error (user: WF-BATCH) or check in ST22 (Abap dumps) » If errors in SM58, choose Execute LUW to reprocess the line

• Possible errors:

– DUPC: Duplicated scanning reference, invoice was already processed. No action necessary but reply to the mailing list informing the vendor’s name if the case is not clear (invoice sent twice same day). – Company code not determined: check if value in E1EDKA1 –RE, field PARTN is present in table YBC_EINV_PCOMP (tc SE16) for this vendor.

eInvoice Monitoring To be done by Duty Officer

Draft Emmanuel Courbin – 05.02.10

Incoming eInvoices monitoring

• To be done in Production by the Duty Officer,

– error is that entry is missing in OBCB. Check the complete vendor config and ask the user to reprocess the idoc.

•

•

If error message is content related:

• Basic type • Enhancement • Logical message INVOIC02 Y3FIEINV INVOIC

– Status:

• Green: Status 53: all ok.

– Only case when it is needed to check the configuration is if the invoice arrive in SAP with the generic vendor (and not a valid vendor). Generic vendor in Q10: 513314, in P10: 513314 » If generic vendor is used, inform Heikki Juvonen (Current GCO for einvoicing) and answer the mailing list, and check if vendor master table has a TAXID defined for this vendor (table LFA1, field STCEG or STCD1 or straight FK03) and if the message contains a TAX ID in E1EDKA1 RE/ Y3EDKPAR TAXID » Request to add this to Master data is done by service team, then updated daily to WAS by program YBC_MAINTAIN_EINV_LIFNR, updating YBC_EINV_LFA1 » Messages received with the generic vendor will be changed manually, but this will fix the next ones. » If the generic vendor is used, can also be that there are duplicates for this VAT ID in YBC_EINV_LFA1

• NAIP Support contact: ext-support integrationplatforms (RES/Espoo)

– ext-support.integrationplatforms@

• If specific issue is signalled, check Application log, TC: SLG1

– Restrict to object Y3FI (einvoicing) and problem class: important.

Incoming eInvoices monitoring in SAP