Income Tax 13

财务管理英文第十三版

Corporate Capital Gains / Losses

Currently, capital gains are taxed at ordinary income tax rates for corporations, or a maximum 35%.

The Capital Budgeting Process

Generate investment proposals consistent with the firm’s strategic objectives.

Estimate after-tax incremental operating cash flows for the investment projects.

c) - (+) Taxes (tax savings) due to asset sale or disposal of “new” assets

d) + (-) Decreased (increased) level of “net” working capital

e) = Terminal year incremental net cash flow

Depreciation and the MACRS Method

Everything else equal, the greater the depreciation charges, the lower the taxes paid by the firm.

财务报表分析与证券估值英文课件 (13)

Watch Deferred Revenue

Firms may defer revenue into a “cookie jar” and then dip into the cookie jar later

Microsoft, 2008-2010 (millions):

2010 Unearned revenue $29,374

A Growth Company? General Electric Corp.: 1993-2000

A Growth Company? General Electric Again.: 2001-2010

Is Nike a Growth Firm?

The Base for Growth: Sustainable Earnings

Operating Income = Core OI + Unusual items

2. Distinguish core income from sales from other core operating income:

Operating Income = Core OI from Sales + Core Other OI + Unusual items

Remember the Caveat: Beware of Paying Too Much for Growth

(Chapters 5, 6, and 7)

Firms can grow earnings, but not create value

üEarnings growth generated by investment

财务三大报表中英互译

资产负债表 Balance Sheet项目 ITEM货币资金 Cash短期投资 Short term investments应收票据 Notes receivable应收股利 Dividend receivable应收利息 Interest receivable应收帐款 Accounts receivable其他应收款 Other receivables预付帐款 Accounts prepaid期货保证金 Future guarantee应收补贴款 Allowance receivable应收出口退税 Export drawback receivable存货 Inventories其中:原材料 Including:Raw materials产成品(库存商品) Finished goods待摊费用 Prepaid and deferred expenses待处理流动资产净损失 Unsettled G/L on current assets一年内到期的长期债权投资 Long-term debenture investment falling due in a yaear 其他流动资产 Other current assets流动资产合计 Total current assets长期投资: Long-term investment:其中:长期股权投资 Including long term equity investment长期债权投资 Long term securities investment*合并价差 Incorporating price difference长期投资合计 Total long-term investment固定资产原价 Fixed assets-cost减:累计折旧 Less:Accumulated Dpreciation固定资产净值 Fixed assets-net value减:固定资产减值准备 Less:Impairment of fixed assets固定资产净额 Net value of fixed assets固定资产清理 Disposal of fixed assets工程物资 Project material在建工程 Construction in Progress待处理固定资产净损失 Unsettled G/L on fixed assets固定资产合计 Total tangible assets无形资产 Intangible assets其中:土地使用权 Including and use rights递延资产(长期待摊费用)Deferred assets其中:固定资产修理 Including:Fixed assets repair固定资产改良支出 Improvement expenditure of fixed assets其他长期资产 Other long term assets其中:特准储备物资 Among it:Specially approved reserving materials 无形及其他资产合计 Total intangible assets and other assets递延税款借项 Deferred assets debits资产总计 Total Assets资产负债表(续表) Balance Sheet项目 ITEM短期借款 Short-term loans应付票款 Notes payable应付帐款 Accounts payab1e预收帐款 Advances from customers应付工资 Accrued payro1l应付福利费 Welfare payable应付利润(股利) Profits payab1e应交税金 Taxes payable其他应交款 Other payable to government其他应付款 Other creditors预提费用 Provision for expenses预计负债 Accrued liabilities一年内到期的长期负债 Long term liabilities due within one year 其他流动负债 Other current liabilities流动负债合计 Total current liabilities长期借款 Long-term loans payable应付债券 Bonds payable长期应付款 long-term accounts payable专项应付款 Special accounts payable其他长期负债 Other long-term liabilities其中:特准储备资金 Including:Special reserve fund长期负债合计 Total long term liabilities递延税款贷项 Deferred taxation credit负债合计 Total liabilities* 少数股东权益 Minority interests实收资本(股本) Subscribed Capital国家资本 National capital集体资本 Collective capital法人资本 Legal person"s capital其中:国有法人资本 Including:State-owned legal person"s capital集体法人资本 Collective legal person"s capital个人资本 Personal capital外商资本 Foreign businessmen"s capital资本公积 Capital surplus盈余公积 surplus reserve其中:法定盈余公积 Including:statutory surplus reserve公益金 public welfare fund补充流动资本 Supplermentary current capital* 未确认的投资损失(以“-”号填列) Unaffirmed investment loss 未分配利润 Retained earnings外币报表折算差额 Converted difference in Foreign Currency Statements 所有者权益合计 Total shareholder"s equity负债及所有者权益总计 Total Liabilities & Equity利润表 INCOME STATEMENT项目 ITEMS产品销售收入Sales of products其中:出口产品销售收入 Including:Export sales减:销售折扣与折让 Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本 Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利 Gross profit on sales减:销售费用 Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益)Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years利润总额 Total profit减:所得税 Less:Income tax净利润 Net profit现金流量表Cash Flows StatementPrepared by:Period: Unit:Items1.Cash Flows from Operating Activities:01)Cash received from sales of goods or rendering of services02)Rental receivedValue added tax on sales received and refunds of value03)added tax paid04)Refund of other taxes and levy other than value added tax07)Other cash received relating to operating activities08)Sub-total of cash inflows09)Cash paid for goods and services10)Cash paid for operating leases11)Cash paid to and on behalf of employees12)Value added tax on purchases paid13)Income tax paid14)Taxes paid other than value added tax and income tax17)Other cash paid relating to operating activities18)Sub-total of cash outflows19)Net cash flows from operating activities2.Cash Flows from Investing Activities:20)Cash received from return of investments21)Cash received from distribution of dividends or profits22)Cash received from bond interest incomeNet cash received from disposal of fixed assets,intangible 23)assets and other long-term assets26)Other cash received relating to investing activities27)Sub-total of cash inflowsCash paid to acquire fixed assets,intangible assets28)and other long-term assets29)Cash paid to acquire equity investments30)Cash paid to acquire debt investments33)Other cash paid relating to investing activities34)Sub-total of cash outflows35)Net cash flows from investing activities3.Cash Flows from Financing Activities:36)Proceeds from issuing shares37)Proceeds from issuing bonds38)Proceeds from borrowings41)Other proceeds relating to financing activities42)Sub-total of cash inflows43)Cash repayments of amounts borrowed44)Cash payments of expenses on any financing activities45)Cash payments for distribution of dividends or profits46)Cash payments of interest expenses47)Cash payments for finance leases48)Cash payments for reduction of registered capital51)Other cash payments relating to financing activities52)Sub-total of cash outflows53)Net cash flows from financing activities4.Effect of Foreign Exchange Rate Changes on Cash Increase in Cash and Cash EquivalentsSupplemental Information1.Investing and Financing Activities that do not Involve in Cash Receipts and Payments56)Repayment of debts by the transfer of fixed assets57)Repayment of debts by the transfer of investments58)Investments in the form of fixed assets59)Repayments of debts by the transfer of investories 2.Reconciliation of Net Profit to Cash Flows from Operating Activities62)Net profit63)Add provision for bad debt or bad debt written off64)Depreciation of fixed assets65)Amortization of intangible assetsLosses on disposal of fixed assets,intangible assets66)and other long-term assets (or deduct:gains)67)Losses on scrapping of fixed assets68)Financial expenses69)Losses arising from investments (or deduct:gains)70)Defered tax credit (or deduct:debit)71)Decrease in inventories (or deduct:increase)72)Decrease in operating receivables (or deduct:increase)73)Increase in operating payables (or deduct:decrease)74)Net payment on value added tax (or deduct:net receipts75)Net cash flows from operating activities Increase in Cash and Cash Equivalents76)cash at the end of the period77)Less:cash at the beginning of the period78)Plus:cash equivalents at the end of the period79)Less:cash equivalents at the beginning of the period80)Net increase in cash and cash equivalents现金流量表的现金流量声明拟制人:时间:单位:项目1.cash流量从经营活动:01 )所收到的现金从销售货物或提供劳务02 )收到的租金增值税销售额收到退款的价值03 )增值税缴纳04 )退回的其他税收和征费以外的增值税07 )其他现金收到有关经营活动08 )分,总现金流入量09 )用现金支付的商品和服务10 )用现金支付经营租赁11 )用现金支付,并代表员工12 )增值税购货支付13 )所得税的缴纳14 )支付的税款以外的增值税和所得税17 )其他现金支付有关的经营活动18 )分,总的现金流出19 )净经营活动的现金流量2.cash流向与投资活动:20 )所收到的现金收回投资21 )所收到的现金从分配股利,利润22 )所收到的现金从国债利息收入现金净额收到的处置固定资产,无形资产23 )资产和其他长期资产26 )其他收到的现金与投资活动27 )小计的现金流入量用现金支付购建固定资产,无形资产28 )和其他长期资产29 )用现金支付,以获取股权投资30 )用现金支付收购债权投资33 )其他现金支付的有关投资活动34 )分,总的现金流出35 )的净现金流量,投资活动产生3.cash流量筹资活动:36 )的收益,从发行股票37 )的收益,由发行债券38 )的收益,由借款41 )其他收益有关的融资活动42 ),小计的现金流入量43 )的现金偿还债务所支付的44 )现金支付的费用,对任何融资活动45 )支付现金,分配股利或利润46 )以现金支付的利息费用47 )以现金支付,融资租赁48 )以现金支付,减少注册资本51 )其他现金收支有关的融资活动52 )分,总的现金流出53 )的净现金流量从融资活动4.effect的外汇汇率变动对现金增加现金和现金等价物补充资料1.investing活动和筹资活动,不参与现金收款和付款56 )偿还债务的转让固定资产57 )偿还债务的转移投资58 )投资在形成固定资产59 )偿还债务的转移库存量2.reconciliation净利润现金流量从经营活动62 )净利润63 )补充规定的坏帐或不良债务注销64 )固定资产折旧65 )无形资产摊销损失处置固定资产,无形资产66 )和其他长期资产(或减:收益)67 )损失固定资产报废68 )财务费用69 )引起的损失由投资管理(或减:收益)70 ) defered税收抵免(或减:借记卡)71 )减少存货(或减:增加)72 )减少经营性应收(或减:增加)73 )增加的经营应付账款(或减:减少)74 )净支付的增值税(或减:收益净额75 )净经营活动的现金流量增加现金和现金等价物76 )的现金,在此期限结束77 )减:现金期开始78 )加:现金等价物在此期限结束79 )减:现金等价物期开始80 ),净增加现金和现金等价物。

目前中国的19个税种

目前中国的19个税种1、增值税2、消费税3、营业税4、企业所得税5、个人所得税6、资源税7、城镇土地使用税8、土地增值税9、房产税 10、城市维护建设税 11、车辆购置税 12、车船税13、印花税 14、契税 15、耕地占用税 16、烟叶税 17、关税 18、船舶吨税 19、固定资产投资方向调节税(从2000年起暂停征收)增值税定义:增值税(value added tax)是对销售货物或者提供加工、修理修配劳务以及进口货物的单位和个人就其实现的增值额征收的一个税种。

从计税原理上说,增值税是以商品(含应税劳务)在流转过程中产生的增值额作为计税依据而征收的一种流转税。

实行价外税,也就是由消费者负担,有增值才征税没增值不征税,但在实际当中,商品新增价值或附加值在生产和流通过程中是很难准确计算的。

征收对象:在中华人民共和国境内销售货物或者提供加工、修理修配劳务以及进口货物的单位和个人,为增值税的纳税义务人。

但实际上,该税项将通过售价,转移给消费者。

征税内容:增值税征收范围包括:1、货物(有形动产,包括热力、电力、气体等);2、应税劳务(提供的加工修理修配劳务);3、进口货物。

适用税率:增值税税率分为四档:基本税率17%、低税率13%,征收率和零税率。

与国外的差异:增值税问世于法国。

早在1954年,法国即在原流转税的基础上建立了增值税,并逐步扩展到经济生活的各个领域。

目前法国是实行多档税率结构,包括标准税率(19.6%)、低税率(5.5%)、特别税率(2.0%)和零税率,与中国相类似。

而在美国,除了曾在密歇根州征收一种称为单一商业税(Single Business Tax)的增值税外,其他各州都没有征收增值税。

其原因主要在于两个方面:一是担心增值税的局限性会产生消极后果,如累退效应产生不公平,税负归宿不稳定,税负转嫁可能引起通货膨胀;更深层的原因是政治上的障碍,立法者担心增值税的引入会引起中央和地方在税收主权和利益方面的冲突。

个人所得税英文参考文献

个人所得税英文参考文献个人所得税英语参考文献一:[1]José Félix Sanz-Sanz. The Laffer curve in schedular multi-rate income taxes with non-genuine allowances: An application to Spain[J]. Economic Modelling,2019,.[2]Craig Brett,John A. Weymark. Voting over selfishly optimal nonlinear income tax schedules[J]. Games and Economic Behavior,2019,.[3]Mónica Unda Gutiérrez. A Tale of Two Taxes: the Diverging Fates of the Federal Property and Income Tax Decrees in post-Revolutionary Mexico[J]. Investigaciones de Historia Económica - Economic History Research,2019,.[4]Sim Choon Ling,Abdullah Osman,Safizal Muhammad,Sin Kit Yeng,Lim Yi Jin. Goods and Services Tax (GST) Compliance among Malaysian Consumers: The Influence of Price, Government Subsidies and Income Inequality[J]. Procedia Economics and Finance,2019,35.[5]Martin Lopez-Daneri. NIT Picking: The Macroeconomic Effects of a Negative Income Tax[J]. Journal of Economic Dynamics and Control,2019,.[6]Tad Miller,Lindsay Miller,Jeffrey Tolin. Provision for income tax expense ASC 740: A teaching note[J]. Journal of Accounting Education,2019,35.[7]Petr David,Lucie Formanová。

西方财务会计第六章答案

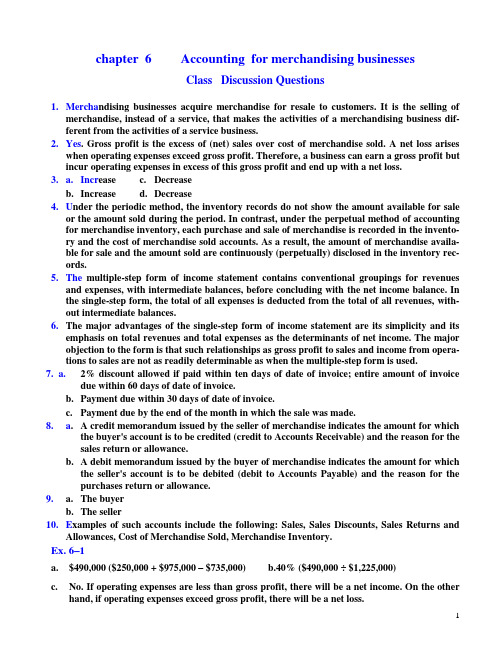

chapter 6 Accounting for merchandising businessesClass Discussion Questions1. Mercha ndising businesses acquire merchandise for resale to customers. It is the selling ofmerchandise, instead of a service, that makes the activities of a merchandising business dif-ferent from the activities of a service business.2. Yes. Gross profit is the excess of (net) sales over cost of merchandise sold. A net loss ariseswhen operating expenses exceed gross profit. Therefore, a business can earn a gross profit but incur operating expenses in excess of this gross profit and end up with a net loss.3. a. Incr ease c. Decreaseb. Increase d. Decrease4. U nder the periodic method, the inventory records do not show the amount available for saleor the amount sold during the period. In contrast, under the perpetual method of accounting for merchandise inventory, each purchase and sale of merchandise is recorded in the invento-ry and the cost of merchandise sold accounts. As a result, the amount of merchandise availa-ble for sale and the amount sold are continuously (perpetually) disclosed in the inventory records.5. The multiple-step form of income statement contains conventional groupings for revenuesand expenses, with intermediate balances, before concluding with the net income balance. In the single-step form, the total of all expenses is deducted from the total of all revenues, with-out intermediate balances.6. The major advantages of the single-step form of income statement are its simplicity and itsemphasis on total revenues and total expenses as the determinants of net income. The major objection to the form is that such relationships as gross profit to sales and income from opera-tions to sales are not as readily determinable as when the multiple-step form is used.7. a. 2% discount allowed if paid within ten days of date of invoice; entire amount of invoicedue within 60 days of date of invoice.b. Payment due within 30 days of date of invoice.c. Payment due by the end of the month in which the sale was made.8. a. A credit memorandum issued by the seller of merchandise indicates the amount for whichthe buyer's account is to be credited (credit to Accounts Receivable) and the reason for the sales return or allowance.b. A debit memorandum issued by the buyer of merchandise indicates the amount for whichthe seller's account is to be debited (debit to Accounts Payable) and the reason for the purchases return or allowance.9. a. The buyerb. The seller10. E xamples of such accounts include the following: Sales, Sales Discounts, Sales Returns andAllowances, Cost of Merchandise Sold, Merchandise Inventory.Ex. 6–1a. $490,000 ($250,000 + $975,000 – $735,000)b.40% ($490,000 ÷ $1,225,000)c. No. If operating expenses are less than gross profit, there will be a net income. On the otherhand, if operating expenses exceed gross profit, there will be a net loss.Ex. 6–2 : $15,710 million ( $20,946 million – $5,236 million )Ex. 6–3a. Purchases discounts, purchases returns and allowancesb. Transportation in;c. Merchandise available for saled. Merchandise inventory (ending)Ex. 6–41. The schedule should begin with the January 1, not the December 31, merchandise inventory.2. Purchases returns and allowances and purchases discounts should be deducted from (notadded to) purchases.3. The result of subtracting purchases returns and allowances and purchases discounts frompur chases should be labeled ―net purchases.‖4. Transportation in should be added to net purchases to yield cost of merchandise purchased.5. The merchandise inventory at December 31 should be deducted from merchandise availablefor sale to yield cost of merchandise sold.A correct cost of merchandise sold section is as follows:Cost of merchandise sold:Merchandise inventory, January 1, 2006 ........ $132,000 Purchases ........................................................... $600,000Less: Purchases returns and allowances$14,000Purchases discounts .............................. 6,000 20,000 Net purchases ..................................................... $580,000Add transportation in ....................................... 7,500Cost of merchandise purchased ................. 587,500 Merchandise available for sale ......................... $719,500 Less merchandise inventory,December 31, 2006....................................... 120,000 Cost of merchandise sold .................................. $599,500 Ex. 6–5Net sales: $3,010,000 ( $3,570,000 – $320,000 – $240,000 )Gross profit: $868,000 ( $3,010,000 – $2,142,000 )Ex. 6–6THE MERIDEN COMPANYIncome StatementFor the Year Ended June 30, 2006Revenues:Net sales ................................................................................. $5,400,000Rent revenue ......................................................................... 30,000Total revenues................................................................... $5,430,000 Expenses:Cost of merchandise sold ..................................................... $3,240,000Selling expenses .................................................................... 480,000Administrative expenses ...................................................... 300,000Interest expense .................................................................... 47,500Total expenses ................................................................... 4,067,500Net income ..................................................................................... $1,362,500Ex. 6–71. Sales returns and allowances and sales discounts should be deducted from (not added to)sales.2. Sales returns and allowances and sales discounts should be deducted from sales to yield "netsales" (not gross sales).3. Deducting the cost of merchandise sold from net sales yields gross profit.4. Deducting the total operating expenses from gross profit would yield income from operations(or operating income).5. Interest revenue should be reported under the caption ―Other income‖ and should be addedto Income from operations to arrive at Net income.6. The final amount on the income statement should be labeled Net income, not Gross profit.A correct income statement would be as follows:THE PLAUTUS COMPANYIncome StatementFor the Year Ended October 31, 2006Revenue from sales:Sales .................................................................... $4,200,000Less: Sales returns and allowances ............... $81,200Sales discounts ....................................... 20,300 101,500Net sales ........................................................ $4,098,500 Cost of merchandise sold ........................................ 2,093,000 Gross profit .............................................................. $2,005,500 Operating expenses:Selling expenses ................................................. $ 203,000Transportation out ............................................ 7,500Administrative expenses ................................... 122,000Total operating expenses ............................ 332,500 Income from operations .......................................... $1,673,000 Other income:Interest revenue ................................................. 66,500Net income ................................................................ $1,739,500 Ex. 6–8a. $25,000 c. $477,000 e. $40,000 g. $757,500b. $210,000 d. $192,000 f. $520,000 h. $690,000Ex. 6–9a. Cash ......................................................................................... 6,900Sales ................................................................................... 6,900 Cost of Merchandise Sold ...................................................... 4,830Merchandise Inventory .................................................... 4,830b. Accounts Receivable ............................................................... 7,500Sales ................................................................................... 7,500 Cost of Merchandise Sold ...................................................... 5,625Merchandise Inventory .................................................... 5,625c. Cash ......................................................................................... 10,200Sales ................................................................................... 10,200 Cost of Merchandise Sold ...................................................... 6,630Merchandise Inventory .................................................... 6,630d. Accounts Receivable—American Express ........................... 7,200Sales ................................................................................... 7,200 Cost of Merchandise Sold ...................................................... 5,040Merchandise Inventory .................................................... 5,040e. Credit Card Expense (675)Cash (675)f. Cash ......................................................................................... 6,875Credit Card Expense (325)Accounts Receivable—American Express ..................... 7,200Ex. 6–10It was acceptable to debit Sales for the $235,750. However, using Sales Returns and Allow-ances assists management in monitoring the amount of returns so that quick action can be taken if returns become excessive.Accounts Receivable should also have been credited for $235,750. In addition, Cost of Mer-chandise Sold should only have been credited for the cost of the merchandise sold, not the selling price. Merchandise Inventory should also have been debited for the cost of the merchandise re-turned. The entries to correctly record the returns would have been as follows: Sales (or Sales Returns and Allowances) ............................. 235,750Accounts Receivable ......................................................... 235,750 Merchandise Inventory .......................................................... 141,450Cost of Merchandise Sold ................................................ 141,450Ex. 6–11a. $7,350 [$7,500 – $150 ($7,500 × 2%)]b. Sales Returns and Allowances .............................................. 7,500Sales Discounts (150)Cash ................................................................................... 7,350Merchandise Inventory .......................................................... 4,500Cost of Merchandise Sold ................................................ 4,500Ex. 6–12(1) Sold merchandise on account, $12,000.(2) Recorded the cost of the merchandise sold and reduced the merchandise inventory account,$7,800.(3) Accepted a return of merchandise and granted an allowance, $2,500.(4) Updated the merchandise inventory account for the cost of the merchandise returned,$1,625.(5) Received the balance due within the discount period, $9,405. [Sale of $12,000, less return of$2,500, less discount of $95 (1% × $9,500).]Ex. 6–13a. $18,000b. $18,375c. $540 (3% × $18,000)d. $17,835Ex. 6–14a. $7,546 [Purchase of $8,500, less return of $800, less discount of $154 ($7,700 × 2%)]b. Merchandise InventoryEx. 6–15Offer A is lower than offer B. Details are as follows:A BList price ............................................................................... $40,000 $40,300Less discount ......................................................................... 800 403$39,200 $39,897 Transportation (625)$39,825 $39,897Ex. 6–16(1) Purchased merchandise on account at a net cost of $8,000.(2) Paid transportation costs, $175.(3) An allowance or return of merchandise was granted by the creditor, $1,000.(4) Paid the balance due within the discount period: debited Accounts Payable, $7,000, and cre-dited Merchandise Inventory for the amount of the discount, $140, and Cash, $6,860.Ex. 6–17a. Merchandise Inventory .......................................................... 7,500Accounts Payable ............................................................. 7,500b. Accounts Payable ................................................................... 1,200Merchandise Inventory .................................................... 1,200c. Accounts Payable ................................................................... 6,300Cash ................................................................................... 6,174Merchandise Inventory (126)a. Merchandise Inventory .......................................................... 12,000Accounts Payable—Loew Co. ......................................... 12,000b. Accounts Payable—Loew Co. ............................................... 12,000Cash ................................................................................... 11,760Merchandise Inventory (240)c. Accounts Payable*—Loew Co. ............................................. 2,940Merchandise Inventory .................................................... 2,940d. Merchandise Inventory .......................................................... 2,000Accounts Payable—Loew Co. ......................................... 2,000e. Cash (940)Accounts Payable—Loew Co. (940)*Note: The debit of $2,940 to Accounts Payable in entry (c) is the amount of cash refund due from Loew Co. It is computed as the amount that was paid for the returned merchandise, $3,000, less the purchase discount of $60 ($3,000 × 2%). The credit to Accounts Payable of $2,000 in en-try (d) reduces the debit balance in the account to $940, which is the amount of the cash refund in entry (e). The alternative entries below yield the same final results.c. Accounts Receivable—Loew Co. .......................................... 2,940Merchandise Inventory .................................................... 2,940d. Merchandise Inventory .......................................................... 2,000Accounts Payable—Loew Co. ......................................... 2,000e. Cash (940)Accounts Payable—Loew Co. ............................................... 2,000Accounts Receivable—Loew Co. .................................... 2,940Ex. 6–19a. $10,500b. $4,160 [($4,500 – $500) ⨯ 0.99] + $200c. $4,900d. $3,960e. $834 [($1,500 – $700) ⨯ 0.98] + $50Ex. 6–20a. At the time of sale c. $4,280b. $4,000 d. Sales Tax PayableEx. 6–21a. Accounts Receivable ............................................................... 9,720Sales ................................................................................... 9,000Sales Tax Payable (720)Cost of Merchandise Sold ...................................................... 6,300Merchandise Inventory .................................................... 6,300b. Sales Tax Payable ................................................................... 9,175Cash ................................................................................... 9,175a. Accounts Receivable—Beta Co. ........................................... 11,500Sales ................................................................................... 11,500 Cost of Merchandise Sold ...................................................... 6,900Merchandise Inventory .................................................... 6,900b. Sales Returns and Allowances (900)Accounts Receivable—Beta Co. (900)Merchandise Inventory (540)Cost of Merchandise Sold (540)c. Cash ......................................................................................... 10,388Sales Discounts (212)Accounts Receivable—Beta Co. ...................................... 10,600Ex. 6–23a. Merchandise Inventory .......................................................... 11,500Accounts Payable—Superior Co. ................................... 11,500b. Accounts Payable—Superior Co. (900)Merchandise Inventory (900)c. Accounts Payable—Superior Co. ......................................... 10,600Cash ................................................................................... 10,388Merchandise Inventory (212)Ex. 6–24a. debit c. credit e. debitb. debit d. debit f. debitEx. 6–25(b) Cost of Merchandise Sold (d) Sales (e)Sales Discounts(f) Sales Returns and Allowances (g) Salaries Expense (j) Supplies ExpenseEx. 6–26a. 2003: 2.07 [$58,247,000,000 ÷ ($30,011,000,000 + $26,394,000,000)/2]2002: 2.24 [$53,553,000,000 ÷ ($26,394,000,000 + $21,385,000,000)/2]b.These analyses indicate a decrease in the effectiveness in the use of the assets to generateprofits. This decrease is probably due to the slowdown in the U.S. economy during 2002–2003. However, a comparison with similar companies or industry averages would be helpful in making a more definitive statement on the effectiveness of the use of the assets.Ex. 6–27a. 4.13 [$12,334,353,000 ÷ ($2,937,578,000 + $3,041,670,000)/2]b. Although Winn-Dixie and Zales are both retail stores, Zales sells jewelry at a much slowervelocity than Winn-Dixie sells groceries. Thus, Winn-Dixie is able to generate $4.13 of sales for every dollar of assets. Zales, however, is only able to generate $1.53 in sales per dollar of assets. This makes sense when one considers the sales rate for jewelry and the relative cost of holding jewelry inventory, relative to groceries. Fortunately, Zales is able to counter its slow sales velocity, relative to groceries, with higher gross profits, relative to groceries. Appendix 1—Ex. 6–28a. and c.SALES JOURNALCost of MerchandiseSold Dr.Invoice Post.Accts. Rec. Dr. MerchandiseDate No. Account Debited Ref.Sales Cr. Inventory Cr.2006Aug. 3 80 Adrienne Richt ................... ✓12,000 4,0008 81 K. Smith .............................. ✓10,000 5,50019 82 L. Lao .................................. ✓9,000 4,00026 83 Cheryl Pugh ........................ ✓14,000 6,50045,000 20,000b. andc.PURCHASES JOURNALAccounts Merchandise OtherPost Payable Inventory Accounts Post.Date Account Credited Ref.Cr. Dr. Dr. Ref. Amount2006Aug. 10 Draco Rug Importers ................. ✓8,000 8,00012 Draco Rug Importers ................. ✓3,500 3,50021 Draco Rug Importers ................. ✓19,500 19,50031,000 31,000d.Merchandise inventory, August 1 ............................................... $ 19,000Plus: August purchases ................................................................ 31,000Less: Cost of merchandise sold ................................................... (20,000)Merchandise inventory, August 31 ............................................. $ 30,000ORQuantity Rug Style Cost2 10 by 6 Chinese* $ 7,5001 8 by 10 Persian 5,5001 8 by 10 Indian 4,0002 10 by 12 Persian 13,000$ 30,000*($4,000 + $3,500)。

注会考试-税法常用词汇

1 / 2税法常用英语词汇1. value added tax 增值税2. business tax 营业税3. consumption tax 消费税4. enterprise income tax 企业所得税5. customs tax 关税6. individual income tax 个人所得税7. resource tax 资源税8. urban and township land use tax 城镇土地使用税9. city maintenance and construction tax 城市维护扩建税10. farmland occupation tax 耕地占用税11. land appreciation tax 土地增值税12. stamp tax 印花税13. vehicle acquisition tax 车辆购置税14. deed tax 契税15. fuel tax 燃油税16. security transaction tax 证券交易税17. social security tax 社会保障税18. house property tax 房产税19. slaughter tax 屠宰税20. urban real estate tax 城市房地产税21. inheritance tax 遗产税22. banquet tax 筵席税23. vehicle and vessel usage tax 车船使用税24. vehicle and vessel license plate tax 车船使用牌照税25. vessel tonnage tax 船舶吨税26. agriculture tax 农业税27. animal husbandry tax 牧业税28. income tax on foreign enterprises and enterprises with foreign investment 外商投资及外国企业所得税29. fixed assets investment orientation regulation tax 固定资产投资方向调节税30. State Administration for Taxation 国家税务总局31. Local Taxation bureau 地方税务局32. tax filing 纳税申报/汇算清缴33. taxes payable 应交税金34. the assessable period for tax payment 纳税期限35. the timing of tax liability arising 纳税义务发生时间36. consolidate reporting 合并申报37. the local competent tax authority 当地主管税务机关38. the outbound business activity 外出经营活动39. Tax Inspection Report 纳税检查报告40. tax avoidance 避税41. tax evasion 逃税42. tax base 税基2 / 243. refund after collection 先征后退44. withhold and remit tax 代扣代缴45. collect and remit tax 代收代缴46. income from authors remuneration 稿酬所得47. income from remuneration for personal service 劳务报酬所得48. income from lease of property 财产租赁所得49. income from transfer of property 财产转让所得50. contingent income 偶然所得51. resident 居民52. non-resident 非居民53. tax year 纳税年度54. temporary trips out of the country 临时离境55. flat rate 比例税率56. withholding income tax 预提税57. withholding at source 源泉扣缴58. State Treasury 国库59. tax preference 税收优惠60. the first profit-making year 第一个获利年度61. refund of the income tax paid on the reinvested amount 再投资退税62. export-oriented enterprise 出口型企业63. new and hi-tech enterprise 高新技术企业64. Special Economic Zone 经济特区65. Arm's length transaction 独立交易66. Tax incentives 税收优惠67. Non- deductible expenses 不可抵扣的费用68. temporary differences 暂时性差异69. non-taxable income 非应税收入。

中级财务会计英文版.课后答案(chap2)

Exercise 2-4Requirement 1Sales price = 100 units x $600 = $60,000 x 70% = $42,000Requirement 2Exercise 7-4 (concluded)Requirement 3Requirement 1, using the net method:Requirement 2, using the net method:Exercise 2-7Requirement 1Estimated returns = 4% x $11,500,000 = $460,000Less: Actual returns (450,000)Remaining estimated returns $10,000Note: another series of journal entries that produce the same end result would be:Exercise 2-7 (continued)Requirement 2Beginning balance in allowance account $300,000 Add: Year-end estimate 460,000 Less: Actual returns (450,000) Ending balance in allowance account $310,000Exercise 2-8Requirement 1Bad debt expense = $67,500 (1.5% x $4,500,000)Requirement 2Allowance for uncollectible accountsBalance, beginning of year $42,000 Add: Bad debt expense for 2011 (1.5% x $4,500,000) 67,500 Less: End-of-year balance (40,000) Accounts receivable written off $69,500 Requirement 3$69,500 — the amount of accounts receivable written off.Exercise 2-9Requirement 1To record the write-off of receivables.To reinstate an account previously written off and to record the collection.Allowance for uncollectible accounts:Balance, beginning of year $32,000Deduct: Receivables written off (21,000) Add: Collection of receivable previously written off 1,200Balance, before adjusting entry for 2011 bad debts 12,200Required allowance: 10% x $625,000 (62,500) Bad debt expense $50,300 To record bad debt expense for the year.Requirement 2Current assets:Accounts receivable, net of $62,500 allowancefor uncollectible accounts $562,500Exercise 2-10Using the direct write-off method, bad debt expense is equal to actual write-offs. Collections of previously written-off receivables are recorded as revenue.Allowance for uncollectible accounts:Balance, beginning of year $17,280Deduct: Receivables written off (17,100)Add: Collection of receivables previously written off 2,200Less: End of year balance (22,410)Bad debt expense for the year 2011 $20,030 Exercise 2-11($ in millions)Allowance for uncollectible accounts:Balance, beginning of year $16Add: Bad debt expense 14Less: End of year balance (18)Write-offs during the year $ 12*Accounts receivable analysis:Balance, beginning of year ($1,084 + 16)$ 1,100Add: Credit sales 4,271Less: Write-offs* (12)Less: Balance end of year ($953 + 18) (971)Cash collections $4,388Exercise 2-12Requirement 1Requirement 22011 income before income taxes would be understated by $900 2012 income before income taxes would be overstated by $900.Exercise2-13Requirement 1Requirement 2$ 1,800 interest for 9 months÷ $28,200 sales price= 6.383% rate for 9 monthsx 12/9to annualize the rate_______= 8.511% effective interest rateExercise 2-14Requirement 1Book value of stock $16,000Plus gain on sale of stock 6,000= Note receivable $22,000Interest reported for the year $ 2,200= 10% rate Divided by value of note $ 22,000 Requirement 2To record sale of stock in exchange for note receivable.To accrue interest on note receivable for twelve months.Exercise 2-15Exercise 2-16Exercise 2-17Exercise 2-18Mountain High retains significant risks and rewards and therefore must treat the transfer as a secured borrowing. The accounts receivable stay on the balance sheet of Mountain High, and they must record a liability.Exercise 2-19Step 1: Accrue interest earned.Step 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 2-21Requirement 1Step 1: To accrue interest earned for two months on note receivableStep 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Exercise 7-21 (continued)Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 2-21 (concluded)Requirement 2To accrue interest earned on note receivable.。

月(季)度预缴纳税申报表 中英文

行次 (No)本期金额(Current amount)累计金额(accumulative amount)1234567891011121316---0.0017---0.001819 ———0.00200.000.0021 ——————220.000.0023240.000.002515-3技术先进型 technology advanced 实际已缴所得税额actual paid up income tax应补(退)的所得税额(11行-12行-16行)complement (return) income tax二、按照上一纳税年度应纳税所得额的平均额预缴tax prepaied in accordance with average payable amount of prior taxation year 本月(季)应纳所得税额(20行×21行)income tax payable amount of current month (quarter)三、按照税务机关确定的其他方法预缴tax prepaid in accordance with tax agent's confirmed addition way 上一纳税年度应纳税所得税额income tax payable amount of prior taxation year 本月(季)应纳税所得额(19行÷12或19行÷4)taxable amount of current month (quarter)税率(taxation rate)(25%)本月(季)确定预缴的所得税额certain prepaid tax of current month(quarter)总分机构纳税人(headquarters and branches taxer)中华人民共和国企业所得税月(季)度预缴纳税申报表(A类)People's Republic of China Enterpise income tax monthly(quaterly) prepayment tax return form税款所属期间: 年 月 日 至 年月 日Taxation period: (Y/M/D) to (Y/M/D)纳税人识别号(Taxer ID):纳税人名称: 金额单位:人民币元(列至角元)15-4其他 other1415一、据实预缴(Actual prepayment)15-1小型微利 small low-profit 15-2过渡期 transition period减:免税收入minus:tax exemption income 减:免税项目所得(农林牧渔业项目所得)minus:income of tax exemption project 减:弥补以前年度亏损minus: compensate prior year losss应纳所得税额(4行-5行-6行-7行-8行) Income tax payable amount14-2集成电路 Intergrated circuit14-3动漫软件企业 carton software enterprise 项目(Item)减:不征税收入minus:non-tax income 14-1软业 software Taxer Name: Monetary Unit: RMB 其中:高新技术企业including: Hi-tech enterprise 税率 (25%)应纳所得税额(9行×10行)Income tax payable amount 营业收入(operating Revenues)营业成本(operating cost)利润总额total profit减免所得税额Income tax reduction260.000.00270.000.00280.000.0029300.000.00代理申报中介机构公章:( Agent's company seal):经办人(Agent):经办人执业证件号码:(Agent registered ID No:代理申报日期Agent FilingDate: 年月 日(Y/M/D)谨声明:此纳税申报表是根据《中华人民共和国企业所得税法》、《中华人民共和国企业所得税法实施条例》和国家有关税收规定填报的,是真实的、可靠的、完整的。

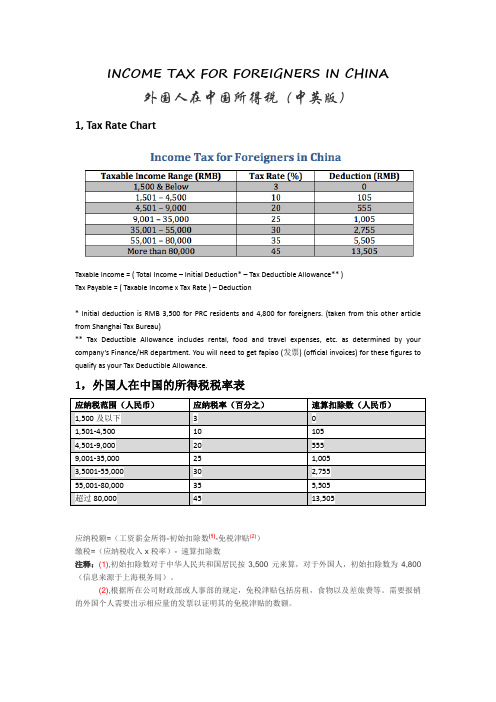

外国人税收方案INCOME TAX FOR FOREIGNERS IN CHINA

INCOME TAX FOR FOREIGNERS IN CHINA外国人在中国所得税(中英版)1, Tax Rate ChartTaxable Income = ( Total Income – Initial Deduction* – Tax Deductible Allowance** )Tax Payable = ( Taxable Income x Tax Rate ) – Deduction* Initial deduction is RMB 3,500 for PRC residents and 4,800 for foreigners. (taken from this other article from Shanghai Tax Bureau)** Tax Deductible Allowance includes rental, food and travel expenses, etc. as determined by your company’s Finance/HR department. You will need to get fapiao (发票) (official invoices) for these figures to qualify as your Tax Deductible Allowance.1,外国人在中国的所得税税率表应纳税范围(人民币)应纳税率(百分之)速算扣除数(人民币)1,500及以下 3 01,501-4,50010 1054,501-9,00020 5559,001-35,00025 1,0053,5001-55,00030 2,75555,001-80,00035 5,505超过80,00045 13,505应纳税额=(工资薪金所得-初始扣除数(1)-免税津贴(2))缴税=(应纳税收入x税率)- 速算扣除数注释:(1),初始扣除数对于中华人民共和国居民按3,500元来算,对于外国人,初始扣除数为4,800(信息来源于上海税务局)。

税务总局英语试题及答案

税务总局英语试题及答案一、选择题(每题2分,共20分)1. Which of the following is not a tax type?A. Income TaxB. Value-Added Tax (VAT)C. Property TaxD. Membership Fee2. The tax rate for individual income tax is:A. FixedB. ProgressiveC. RegressiveB. Proportional3. When is the deadline for filing annual tax returns?A. March 31stB. April 15thC. May 31stD. June 30th4. What is the primary purpose of a tax audit?A. To verify the accuracy of tax returnsB. To increase tax revenueC. To penalize taxpayersD. To provide tax advice5. Which of the following is a tax deduction?A. Charitable donationsB. Personal expensesC. Entertainment costsD. Travel expenses6. What does VAT stand for?A. Vehicle and Transportation TaxB. Value-Added TaxC. Voluntary Assistance TaxD. Vendor and Trader Tax7. Who is responsible for collecting VAT?A. ConsumersB. TaxpayersC. BusinessesD. Government agencies8. What is the tax implication of depreciation?A. It increases taxable incomeB. It reduces taxable incomeC. It has no impact on taxable incomeD. It is not applicable to tax calculations9. Which of the following is not considered a tax evasion?A. Underreporting incomeB. Overpaying taxesC. Falsifying recordsD. Concealing income10. What is the main difference between direct and indirect taxes?A. The way they are collectedB. The type of goods they apply toC. The frequency of paymentD. The method of calculation二、填空题(每空1分,共10分)11. The standard rate of VAT in many countries is ________.12. Tax evasion is a criminal offense and can result in________ and/or imprisonment.13. Taxpayers are required to keep financial records for at least ________ years for tax purposes.14. The term 'tax bracket' refers to the range of income that is taxed at a ________ rate.15. A ________ is a legal document issued by the taxauthority to collect taxes.三、简答题(每题5分,共20分)16. Explain the concept of 'tax avoidance' and how it differs from 'tax evasion'.17. Describe the process of filing a tax return for an individual.18. What are the consequences of not paying taxes on time?19. Discuss the role of tax incentives in promoting economic growth.四、论述题(每题15分,共30分)20. Discuss the impact of tax policy on business decisions and investment strategies.21. Analyze the ethical considerations involved in tax planning and compliance.五、案例分析题(共20分)22. A company reported a profit of $500,000 for the fiscal year. The corporate tax rate is 25%. However, due to various tax deductions, the taxable income was reduced to $400,000. Calculate the tax liability for the company and discuss the implications of tax deductions on corporate financial planning.答案:一、选择题1. D2. B3. B4. A5. A6. B7. C8. B9. B10. A二、填空题11. 20%12. Fines13. 614. Specific15. Tax Assessment三、简答题16. Tax avoidance is the legal use of tax laws to minimize tax liability, whereas tax evasion is the illegal act of not paying taxes through fraudulent means.17. The process involves gathering financial records, calculating taxable income, applying deductions and credits, and submitting the tax return to the tax authority by the deadline.18. Consequences include fines, penalties, interest on overdue taxes, and potential legal action.19. Tax incentives can encourage investment and business activities, leading to job creation and economic growth.四、论述题20. Tax policies can influence business decisions by affecting costs, profitability, and cash flow, which in turn can impact investment strategies.21. Ethical considerations include compliance with tax laws, fairness in tax contributions, and transparency in financial reporting.五、案例分析题22. The tax liability is $400,000 * 25% = $100,000. Tax deductions can reduce tax liability, improving cash flow and potentially increasing investment in business growth.。

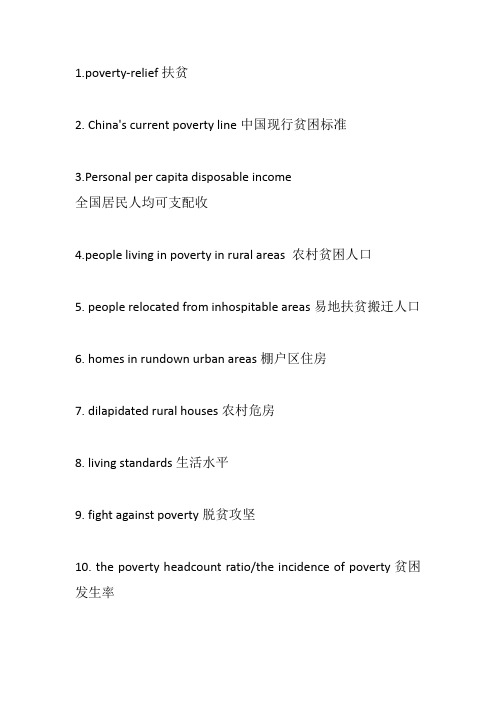

Unit 2 大学英语四六级段落翻译 poverty-relief主题词汇

1.poverty-relief扶贫2. China's current poverty line中国现行贫困标准3.Personal per capita disposable income全国居民人均可支配收4.people living in poverty in rural areas 农村贫困人口5. people relocated from inhospitable areas易地扶贫搬迁人口6. homes in rundown urban areas棚户区住房7. dilapidated rural houses农村危房8. living standards生活水平9. fight against poverty脱贫攻坚10. the poverty headcount ratio/the incidence of poverty贫困发生率11. The threshold for individual income tax个人所得税起征点12. special additional deduction专项附加扣除13.strengthen the economic foundation, enhance sustainability, and improve people’s lives 强基础、增后劲、惠民生14. people-centered development philosophy人民为中心15. international poverty line国际贫困标准16. working mechanism with central government responsible for overall planning, provincial-level governments assuming overall responsibility, and city and county governments responsible for program implementation.中央统筹、省负总责、市县抓落实的工作机制17. rural residents living in poverty农村贫困人口18. contiguous areas of extreme poverty集中连片特困地区19. the domestic and overseas export of labor劳务输出20. building the self-development capacity增强自我发展能力21. mechanisms for coordinating poverty reduction扶贫协作机制22. The system for ensuring responsibility is taken for poverty elimination脱贫攻坚责任制23. evaluations and assessment评估考核24. wellbeing of the people民生25. three-year renovation plan to address housing in rundown urban areas三年棚改攻坚计划26.public-rental housing units 公租房27. dilapidated houses built of such materials as beaten earth, and timber and bark破旧泥草房、土坯房、树皮房等危房28. eligible houseless first-time workers符合条件的新就业无房职工29. housing rental market住房租赁市场30. shared ownership housing共有产权住房31. the three critical battles三大攻坚战32. structural deleveraging结构性去杠杆33. shake off poverty脱贫34.manipulation of numbers in poverty elimination work 数字脱贫35. development-oriented poverty alleviation开发式扶贫36. guarantee their basic standards of living by improving various assurance programs完善各项保障制度来保障基本生活37. increase the supply of elderly care services增加养老服务供给38. raise the accessibility of medical services增强医疗服务的便利性39. far-flung areas边远地区40. the gap between the rich and the poor贫富差距41. Adequate food and clothing温饱42. absolute poverty standard 绝对贫困标准43.hamper overall economic development妨碍总体经济发展44.aggravate social contradictions加剧社会矛盾45.impoverished mountainous area贫困山区46. regional disparity地区差异47. illiteracy rate 文盲率48. low per capita income人均收入低49. The income gap further widens.收入差距进一步扩大50.targeted poverty reduction and alleviation精准扶贫精准脱贫51. strengthen rural compulsory education加强农村义务教育52. targeted poverty alleviation精准扶贫53. take advantage of local resources 利用本地资源54. step up infrastructure construction加强基础设施建设55. rural tourism乡村旅游56. new rural construction新农村建设。

美国投资指南[中英双语版]

![美国投资指南[中英双语版]](https://img.taocdn.com/s3/m/9ed3844bcf84b9d528ea7ace.png)

2.1 Registration and licensing...................................... 3 注册和许可

2.2 Price controls ........................................................ 3 价格控制

5.2 Taxable income and rates ..................................... 11 应税所得和税率 Taxable income defined .................................. 12 应税所得的定义 Deductions ..................................................... 13 费用扣除 Depreciation ................................................... 13 折旧 Losses ............................................................ 14 亏损

5.5 Foreign income and tax treaties ............................ 15 国外所得和税收协定 Witholding tax rates under US tax treaties ...... 15 美国税收协定中规定的预扣税率

5.6 Transactions between related parties .................... 18 关联方交易 Transfer pricing ............................................... 18 转让定价 Controlled foreign companies ......................... 18 受控外国公 Thin capitalization .......................................... 18 资本弱化 Consolidated returns ...................................... 19 合并纳税

2007年美国个人所得税申报表(中英对照)

2007年美国个人所得税申报表(中英对照)第一篇:2007年美国个人所得税申报表(中英对照)2007年美国个人所得税申报表(中英对照)(2008-06-01 22:25:12)FORM 1040 1040表格Department of the Treasury—Internal Revenue Service U.S.Individual Income Tax Return 财政部—国税局2007年美国个人所得税申报表IRS Use Only—Do not write or staple in this space.IRS专用—请勿书写或装订Label(See instructions on page 12.)标签行(请参阅说明)Use the IRS label.Otherwise,please print or type.请用国内税务署的专用标签,如果没有,请打印一份。

Presidential Election Campaign 总统竞选基金For the year Jan.1–Dec.31, 2007, or other tax year beginning , 2007, ending , 20 此报税表涵盖时间,从207年1月1日至12月31日,或含其它报税年度,起始日期,2007,到结束日期20 OMB No.1545-0074 OMB号 2545-0074Your social security number 您的社会安全号I f a joint return, spouse’s first name and initial 如为夫妇联报,配偶的名:You must enter your SSN(s)above 您必须得在上面填写您的社会安全号(SSN)City, town or post office, state, and ZIP code.If you have a foreign address, see page 12.城市名,城镇名或邮箱。

泰国个人所得税申报表

Name Surname ....................................................................................................................................,........

during tax year

la Additional Tax Payment

Declaration of intention to donate tax payment to political party

Political Party Identification Number

-----

---------

------

------

------

---- ---- ---- ---- ---- ---- ----

---- ---- ---- ---- ---- ---- ----

---- ---- ---- ---- ---- ---- ----

---- ---- ---- ---- ---- ---- ----

separately from taxpayer (4) Has no income

Reciept Book No..................................................No.................................................... Amount...................................................................Baht

ly No. Moo Lane/Soi ............................................................... ...............

个人所得税法英文版)

第15章个人所得税法Chapter 15 Individual Income Tax•Who are the individuals liable to Individual Income Tax?•What is the income from sources within China?•What is the income from sources outside China?•What income earned by an individual is subject to Individual Income Tax?•How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?•What does wage, salary income include specifically?•How are salaries and wages assessed for Individual Income Tax payable?•How is the “additional deduction for expenses”regulated for wages and salaries? •How to compute the income tax payable on the bonus income on the year-end in one payment?•How to compute the income tax payable on the income of welfare in kind?•How to compute the income tax payable on the income stock options of employees of enterprises?•How is severance pay taxed?•How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?•What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?•How to calculate the taxable income of individual Industrial and Commercial Households?•What are the rules concerning deductions for Individual Industrial and Commercial Households?•How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?•How do single proprietorship enterprises compute and pay income tax payable on their production and business income?•How to levy income tax payable by the investors of single proprietorship and partnership enterprises by mode of administrative assessment?•How do single proprietorship and partnership enterprises compute and pay income tax payable on their interest, dividend and bonus income as return from their investment?•How is income from contracted or leased operation of enterprises or institutions assessed for Individual Income Tax?•How is income from remuneration for personal service assessed for Individual Income Tax payable?•How to treat the receivables unrecoverable and the business losses incurred by Individual Industrial and Commercial Households?•What expenses are not allowed for deductions for Individual Industrial and Commercial Households?•What are the rules concerning the depreciation of the fixed assets of Individual Industrial and Commercial Households?•How to deduct the expenses concerning intangible assets used by Individual Industrial and Commercial Households?•How do Individual Industrial and Commercial Households compute their income tax payable?•How additional income tax is levied on remuneration income that is excessively high at one payment?•How is author’s remuneration income assessed for Individual Income Tax payable? •How is income from royalties assessed for Individual Income Tax payable?•How is income from lease of property assessed for Individual Income Tax payable? •How is income from transfer of property assessed for Individual Income Tax payable?•How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?•What do the interest, dividend, bonus, contingent income and/ or other income include specifically?•How are interests, dividends, bonuses, contingent income and/ or other income assessed for Individual Income Tax payable?•How to compute the income tax payable on income derived by two individuals or more together?•How is donation income assessed for Individual Income Tax payable?•How to compute the income tax payable in case that the employers bear the Individual Income Tax for the taxpayers?•How is income derived from sources outside China assessed for Individual Income Tax payable?•What are the main exemptions for Individual Income Tax?•What kind of bond interest income and earmarked saving deposit interest income are exempt from Individual Income Tax as ruled by the State?•What are the main reductions for Individual Income Tax?•What are the rules concerning the mode, time and places for Individual Income Tax payment?•How to report and pay income tax on wages and salaries income?•How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?•How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses?•How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?•How to report and pay income tax on income earned by taxpayers from sources outside China?纳税义务人判定标准征税对象范围1.居民纳税人(负无限纳税义务)(1)在中国境内有住所的个人(2)在中国境内无住所,而在中国境内居住满一年的个人。

Towa EX-300和Geller EX-300现金记账机操作及编程手册说明书

\

3.6 Programming the PLU Function...............................................................................19

Programming PLU Codes......................................................................................19

IL

i

I

1[

rh 'f'

lil

j I EX·S CONTENTS 97.10.91:17 PM ",",- '/3

rh

'f7

Contents

3.9 Setting the Exchange Rate .......................................................~ .................................29

Selecting a Taxation System ..................................................................................20

Setting the Tax Rate ................................................................................................21

2.3 Installing and Removing a Paper Roll......................................................................ll

个税申报 英语

个税申报英语个人所得税是每个纳税人必须缴纳的税种之一。

为了避免因语言障碍而影响申报工作的顺利进行,以下是有关个人所得税申报的英语表达。

1. 薪资所得:salary income2. 劳务报酬所得:remuneration income3. 个体工商户所得:individual business income4. 劳务派遣所得:dispatched labor income5. 物业租赁所得:property leasing income6. 手续费所得:commission income7. 著作权使用费所得:royalty income8. 利息、股息所得:interest and dividend income9. 资产转让所得:income from the transfer of assets10. 综合所得:comprehensive income11. 扣除:deduction12. 免税额:tax exemption13. 税前扣除:pre-tax deduction14. 税后扣除:post-tax deduction15. 抵扣:offset16. 纳税义务人:taxpayer17. 税务机关:tax authority18. 税务局:tax bureau19. 税收政策:tax policy20. 税率:tax rate21. 申报期限:filing deadline22. 纳税申报表:tax declaration form23. 税收征管:tax collection and management24. 税务登记:tax registration25. 税务咨询:tax consultation26. 税收优惠:tax incentives27. 税收逃漏:tax evasion以上是个人所得税申报中常用的英语表达。

希望这些词汇能帮助您更好地了解个人所得税申报的相关内容。

金融专业英语词汇大全13金融英语

金融专业英语词汇大全13金融英语1. state-owned enterprise bonus tax 国营企业奖金税2. state-owned enterprise income tax 国营企业所得税3. state-owned enterprise regulation tax 国营企业调节税4. state-owned enterprise wages regulation 国营企业工资调节税5. status inquiry 信用状况调查6. sticky deal 棘手交易7. stock index futures 股票指数期货8. stock index futures contract 股票指数期货合约9. stock indexes 股票指数10. stock wrap 股市行情11. stockpile financing 储存融资12. stop-gap fund 临时通融资金13. strike price 协定价格14. subaccount 公帐户15. sublease 转租,分租16. subrogated right 代位求偿17. subscription 认股书18. subsidy account 补助金帐户19. sum-of-the-years' digits method of depre年数总和折旧法20. sundry account 杂项帐户21. surrender of exchange 移存外汇22. surtax 附加税23. swap position 调期汇率头寸24. swap rate 掉期率25. swing 变动(幅度),摆动,涨落26. symmetry 对称27. syndicate leases 银团租赁28. synthetic financial futures position 综合金融期货头寸29. synthetic options 合成期权30. T/T (= Telegraphic Transfer) 电汇31. tariff 关税32. tax anticipation note (bill,bond) 预付税金票据,先期缴税债券33. tax avoidance 避免34. tax base 征税基础35. tax code 税法36. tax collection 税收制度37. tax concession 赋税优惠38. tax credit leases 减税租赁39. tax evasion 逃税40. tax grades 征税级距41. tax holiday 免税期42. tax on transport 运输税43. tax relief 税收减免44. tax statutes 税收法45. taxable 可征税的,应纳税的46. taxing power 税收能力,课税能力47. technology risk 技术风险48. telegraphic transfer (T/T) 电汇49. telephone transfers 电话转帐50. tell quel exchange rate 调整汇率51. teller's window (= teller' station) 出纳窗口52. temporary bridging finance 临时融资53. tender bond 投标保证金54. tender n. 货币,投、招标,提供,偿付55. terms of loan 放款条件56. the additional insured 附加被保险人57. the capacity of a tax 税收负担58. the Construction Bank of China 中国建设银行59. the Gilts 金边债券60. the International Trust and Investment C中国国际信托投资公司61. the open interest 未结清权益62. the People's Bank of China 中国人民银行63. the rate structure of the tax 税率结构64. thrift encouragement 储蓄鼓励65. tight market 旺市66. time lag 时滞67. time order 限时订单68. time-deposit accounts 定期存款帐户69. to be hedging 进行套做保值70. to defuse (attempted monopoly positions) 冲破(形成的市场垄断状况)71. total foreign exchange 外汇收支总额72. total FX portfolio 外汇投资总额73. total loss 全损74. total loss of part 部分全损75. total loss only 全损赔偿险76. trade claim 商业索赔77. trade risk 交易风险78. trading pit 交易场79. transaction exposure 交易风险80. transactions costs 交易费用81. transfer n. 转让,划拨,转帐82. transfer to reserve account 转到准备金帐户83. transferable money 可转帐货币84. translation exposure 转换风险85. transmitting bank 转证银行86. transnational leases 跨国租赁87. traveller's letter of credit 旅行信用证88. trust bank 信托银行89. trust fund 信托基金90. trust leases 信托租赁91. trust services 信托业务92. trustee bank 受托银行93. turnover of account receivable 应收帐款周转率94. turnover ratio of working capital 流动资本周转率95. two-tier exchange rate 双重汇率96. ultimate borrower 最终借款人97. ultra-cheap money policy 超低息政策98. unbalance finance 赤字财政99. uncovered interest arbitrage 未担保利率套利100. underinsurance 保险不足END。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Example

• In 2010/11 tax year, a company car was made available to Joe Soap before the start of this tax year with a list price of £14,500 plus delivery charges of £500. It was powered by petrol and had an official CO2 emissions figure of 167g/km.

Forms

P60 1. Summary of your pay and the tax that's been deducted from it in the tax year. 2. Your employer should give you a P60 to keep as a record at the end of every tax year (which runs from 6 April to 5 April the next year). If your employer doesn't give you a P60 at the end of the tax year, ask for it you're entitled to it by law if you are still working for the employer at 5 April. 3. You might need it: 1. to complete a Self Assessment tax return, if this applies to you 2. to claim back any tax you've overpaid 3. to apply for tax credits

Example

• Total car price = 15,000 • CO2 rate = 22% (Approved CO2 emissions figure rounded down to the next lowest 5g/km) • the car benefit for a full year = 3300 • fuel benefit Your employer uses a P11D to tell HMRC about the value of any 'benefits in kind' they've given you during the tax year. This means benefits or expenses that effectively increase your income, like: 1. a company car 2. private medical insurance 3. interest free loans

Review

Forms

P46 1. If you don’t have a P45 because, for example, you’re starting your first job or taking on a second job without giving up your other one, your new employer may give you a form P46 to complete. 2. It contains important information that affects the amount of tax you’ll pay, such as whether: 1. this is your first job 2. you've been claiming Jobseeker's Allowance or Employment and Support Allowance 3. you've got another job 4. you're paying off a student loan

Forms

P45 1. You get a P45 from your employer when you stop working for them. It's a record of your pay and the tax that's been deducted from it so far in the tax year. It shows: 1. your tax code and PAYE (Pay As You Earn) reference number 2. your National Insurance number 3. your leaving date 4. your earnings in the tax year 5. how much tax was deducted from your earnings